Embed Size (px)

Citation preview

-. Print CM

•

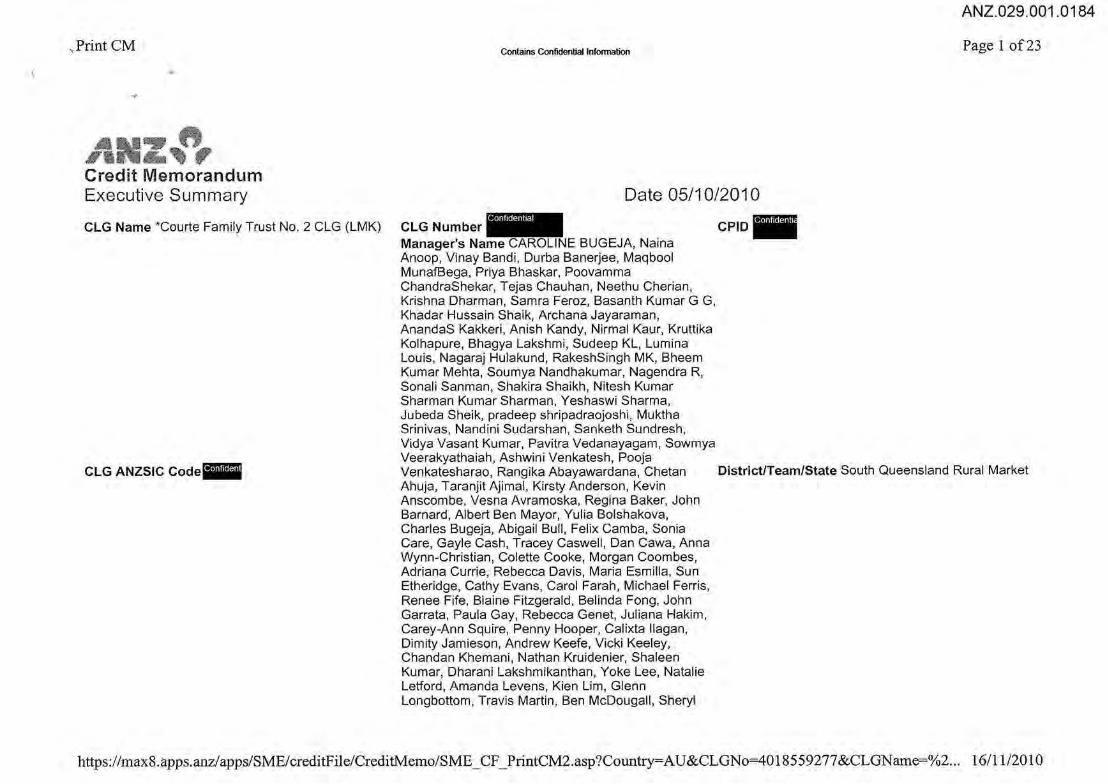

ANZ~8, Credit Memorandum Executive Summary

CLG Name *Courte Family Trust No. 2 CLG (LMK)

CLG ANZSIC Codelllll

Contains Confidential lnfOfTllation

Date 05/10/2010

CLG Number - CPID -Manager's Name CAROLINE BUGEJA, Naina Anoop, Vinay Sandi, Durba Banerjee, Maqbool MunafBega, Priya Bhaskar, Poovamma ChandraShekar, T ejas Chauhan, Neethu Cherian, Krishna Dharman, Samra Feroz, Basanth Kumar G G, Khadar Hussain Shaik, Archana Jayaraman, AnandaS Kakkeri, Anish Kandy, Nirmal Kaur, Kruttika Kolhapure, Bhagya Lakshmi, Sudeep KL, Lumina Louis, Nagaraj Hulakund, RakeshSingh MK, Bheem Kumar Mehta, Soumya Nandhakumar, Nagendra R, Sonali Sanman, Shakira Shaikh, Nitesh Kumar Sharman Kumar Sharman, Yeshaswi Sharma, Jubeda Sheik, pradeep shripadraojoshi, Muktha Srinivas, Nandini Sudarshan, Sanketh Sundresh, Vidya Vasant Kumar, Pavitra Vedanayagam, Sowmya Veerakyathaiah, Ashwini Venkatesh, Pooja

ANZ.029.001.0184

Page 1 of23

Venkatesharao, Rangika Abayawardana, Chetan District/Team/State South Queensland Rural Market Ahuja, Taranjit Ajimal, Kirsty Anderson, Kevin Anscombe, Vesna Avramoska, Regina Baker, John Barnard, Albert Ben Mayor, Yulia Bolshakova, Charles Bugeja, Abigail Bull, Felix Camba, Sonia Care, Gayle Cash, Tracey Caswell, Dan Cawa, Anna Wynn-Christian, Colette Cooke, Morgan Coombes, Adriana Currie, Rebecca Davis, Maria Esmilla, Sun Etheridge, Cathy Evans, Carol Farah, Michael Ferris, Renee Fife, Blaine Fitzgerald, Belinda Fong, John Garrata, Paula Gay, Rebecca Genet, Juliana Hakim, Carey-Ann Squire, Penny Hooper, Calixta Ilagan, Dimity Jamieson, Andrew Keefe, Vicki Keeley, Chandan Khemani, Nathan Kruidenier, Shaleen Kumar, Dharani Lakshmikanthan, Yoke Lee, Natalie Letford, Amanda Levens, Kien Lim, Glenn Longbottom, Travis Martin, Ben McDougall, Sheryl

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME _CF _PrintCM2.asp?Country=AU&CLGNo=4018559277 &CLGName=%2... 16/1112010

Print CM

CLG ANZSIC Description Purpose of Advices: Customer since:

Date of Last Assessment/ Review

Current Risk Grade 6C

Proposal A brief description of this submission is:

Contains Confidential Information

Millar, Andrew Moore, Katrina Morgan, Rebecca Murray, Asha Narayan, Shelley Nauschutz, Stephanie Ng, Christine Nguyen, Mellisa Nolan, Dallas Padiachee, Anthony Palmer, Zoe Peers, Kristy Robertson, Jacki Chugg, Paula Ryan, Miranda Seakgosing, Sam Sem, Jane Shakespear-Druery, Ravi Sharma, Jeannie Shen, Patricia Shepherd, Peter Shone, David Simpson, Katie Simpson, Candice Smith, Peter Stephenson, Maureen Sugihartono, Li Sun, Justin The, Bunawat Thepabutra, Rita Thomas, Michael Tonkin, Lorena Torres, Jodie Townsend, Jen Tucker, Renu Vaishnav. Natalie Vrlic, Anne Walsh, Sandra Walsh, Katie Watts, Belinda Weir, John Whitehill, Malcolm White, Yoke Wong, Maggie Wynne, Esther Yong, Andrew Zemek

BEEF CATTLE FARMING Review and variation 03/2010

Date of Next Advices

Proposed Risk Grade 7C

Date of Next Full Review 31/03/2011

ANZ.029.001.0185

Page2 of23

Please refer to memo. diary note and emails with John Dallis in regards to this account. Facilities were substantially in arrears with Landmark at time of transfer to ANZ. The position has been well documented in previous advices.

Further discussions were held with clients 5 October and 20 October via phone calls and via email in regards to extra information that was sought and in regards to developments since last interview and as per diary note which is attached to this ACM. Outcomes are:

1. They have have emailed thro~R's for themselves but not their trusts; 2. The property listed for sale at--40 km north of Toowoomba, was initially believed to be mortgaged to CBA. The property is not in fact mortgaged to CBA but does have listed on it a mortgage to NAB. That was in regards to old lending clients had with NAB and it appears simply that the mortgage was never released. It should be able to be released wit~yable to NAB on this basis. 3. There has been some interest shown in th~ property but as yet no formal offers. Listed@ $180K. (No agents agreement provided yet) 4. There has been no interest as yet shownilrllerty a•'f® Listed @ $250K. (Copy of agents agreement held) 5. Clients .. have opted to list the property at ' '· · for sale through Ray White Rural at St George although it is at a very early stage and not yet active in

)https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME CF PrintCM2.asp?Country=A U&CLGNo=4018559277 &CLGName=%2... 16/11/2010

ANZ.029.001.0186

.,Print CM Contains Confidential Information Page 3 of23

listings. The agent has suggested a price somewhere between $1.3M and $1.6M for the property. 6. Clients are struggling now with all payments to all financiers although the extent of this is not clear.

It was put to clients that the bank would now be looking to bring all exiting ANZ debts into one with an initial term of 6 months with interest payable at the end of this term and with a review of their position to be done again at that time. Debt reductions would be required to some extent if they sell down eithe~or Casino during that 6 month period. Obviously with clients now listing- if they have any success with that, as mortgagee we would be ful~

Sale of rural property in that area is however slow so we would be surprised if there are any substantial developments in this regard in the short term.

Clients were receptive to the proposal. understanding that the whole plan was to give them some time to sell down assets in an orderly manner whilst not having their existing ANZ debts fall further into arrears. They understood the proposed time frame and that at the end of that 6 month period their position would be revisited and decisions beyond that time would be subject to further discussions. They were however, given their other lending is now also quite stressed, seeking to have flexibility on how much might be paid off their ANZ debt upon sale of any of the properties not held by us as security so that they could contain the overall position. No committment was given to our view on this aspect however we have built in a condition that clients come to the Bank if they arrange a sale and negotiate reductions to our debts from these sales. They will certainly need some cash to cover other debts so the request, when it involves unencumbered property, is not unreasonable.

We have had more cooperation from clients in the past week and discussions with Mrs Courte 20/10 do suggest they fully acknowledge the precarious nature of their position, but in saying that, also believe that they could act much quicker to look at liquidation of assets to clear/reduce debts. Whilst we do recommend that the proposed restructure go through, once the time period of 6 months has elapsed, if there are no reductions forthcoming by this time, migration to Lending Services would be prudent as they sale of assets will have to be actioned quickly to contain a blow out of debt due to accruing interest.

With this in mind, we propose to include stronger conditions into this approval now it very clear to clients of our expectations and requirements.

Privileged to make

We also propose to increase the pricing on the new facility to reflect an ever increasing risk with this credit, although we do not propose to levy any LAF in this case.

From an eCART perspective we have only been able to rate under the consumer model given lack of FS for the Trust which is the borrowing entity. It carries a recommended rating of a 7. Whilst valuations are dated for security held, it is considered that XV's are acceptable for this purpose and if a revaluation is required then we would recommend that valuations be sent to an external valuer with costs to be passed on to clients and through lack of other options, costs will need to be included in the final overall loan amount.

Business Facilities Current Prooosed Variation(+/-)

Facilities or TBL ($) 862423 990000 127577 Security XTV ($) 900500 900500 0

Contingency Limit $0

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME_ CF _PrintCM2.asp?Country=AU&CLGNo=4018559277 &CLGNarne=%2... 16/11/2010

ANZ.029.001.0187

,Print CM

Credit Memorandum Streamlining Questions

CLG Name *Courte Family Trust No. 2 CLG Number CLG (LMK)

Industry Types Agribusiness

St I' . Q ream mmQ uestrons Generic Questions

Contains Confidential lnfoonation

Conf1dent1al

Calculated Risk Grade of 6C or below or downgrade by 2 or more since last assessment? Is Interest Cover Ratio from last financials <1.5 times?

Has the business been in operation for less than two years? Are current financial statements held outside current policy requirements?

Date 05/10/201 O

Are any taxation, GST or other statutory payments outstanding (other than normal arrangements)? Are there any accounts within the CLG experiencing delinquencies?

Has there been a change in ownership/control/legal structure since the last assessment? Has there been a change in key management since the last assessment?

Has there been a loss of any key supplier I customer I tenant that will have a significant impact on business results? Are there any Credit Risk Review comments outstanding? Has there been any material change in external borrowings (i.e. >10%) since the last review (as per the behaviour review)? Have there been any breaches in Covenants /Monitoring requirements since last assessment?

Has there been industry diversification since the last assessment? Are there other factors evident which may adversely affect the customer's future viability? Reducing Industry?

Agribusiness Questions Has gross farm income increased or decreased by more than 10%?

Have farm operating expenses increased or decreased by more than 10% Has net surplus cash position declined> 10% or increased >10%? Is the borrower's overall equity < 65%?

Are the historic figures different from the expected future performance?

Is farm production reliant on irrigation? Is farm performance and scale above or below district average?

ANZ.029.001.0188

Page 5 of23

Yes I No Yes Yes

No No Yes

Yes

No No Yes

No No No No Yes

No

Yes I No Yes Yes

Yes Yes

Yes No

No

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME _CF _PrintCM2.asp?Country=AU&CLGNo=4018559277 &CLGName=%2... 16/11/2010

ANZ.029.001.0189

, Print CM

Credit Memorandum Facilities Schedule

Contains Confidential lnfoonation

CLG Name .. Courte Family Trust No. 2 CLG Number CLG (LMK)

Borrower Facility Current Proposed Loan Purpose Type Limits Limits

ANZ Business Joseph Keith Francis Courte and Gail Louise Migration of Courte in their ABL - 809,398 0.00

Landmark Financial own capacities Variable Services Loan. and as trustees of To be repaid. the Courte Family Trust No 2 Joseph Keith Francis Courte and Gail Louise Migration of Courte in their ABL- 3,025 0.00

Landmark Financial own capacities Variable Services Loan. and as trustees of To be repaid. the Courte Family Trust No 2

Joseph Keith Francis Courte and Gail Louise Working capital. Courte in their Overdraft 50,000 0.00 Limit to be own capacities (revolving) cancelled. and as trustees of the Courte Family Trust No 2

Joseph Keith Francis Courte and Gail Louise

ANZ.029.001.0190

Page 7 of23

Date 05/10/2010

Facility Term Repayment Arrangement Pricing

Loan Loan Repayment Expiry Arrangement Amount Frequency Interest Fee Term Date Term

11 Years 3 24/11/2021 Interest Only 0.00 Quarterly Facility term BMI - 0.00 Months 0.22%

10 Years 11 27/07/2021 Interest Only 0.00 Quarterly Facility term BMI-

0.00 0.22% Months

N/A NR Interest Only 0.00 Monthly Facility term BMI + 0.00 3.18%

0 Years

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME _CF _PrintCM2.asp?Country=AU&CLGNo=4018559277 &CLGName=%2... 16/11/2010

ANZ.029.001 .0191

Print CM Contains Confidential lnfoonation

Page 8 of23

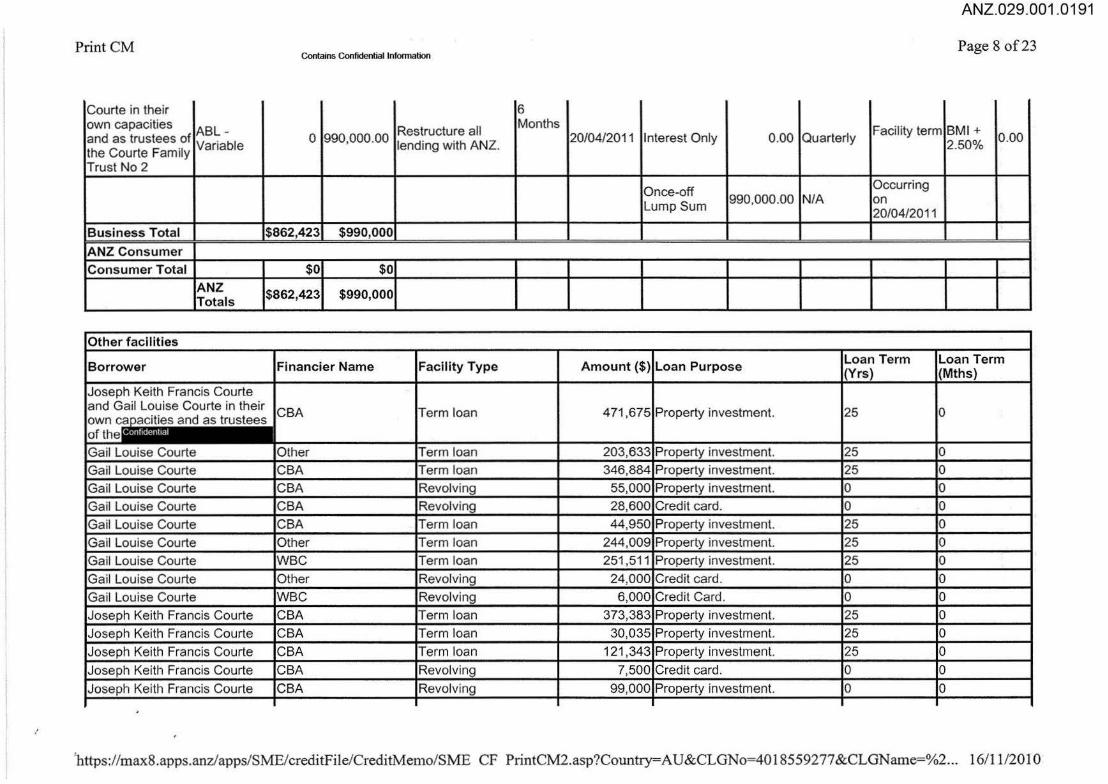

Courte in their 6 own capacities ABL- Restructure all Months Facility term BMI+ and as trustees of Variable 0 990,000.00

lending with ANZ. 20/04/2011 Interest Only 0.00 Quarterly 2.50%

0.00 the Courte Family Trust No 2

Once-off Occurring

Lump Sum 990,000.00 NIA on 20/04/2011

Business Total $862,423 $990,000

ANZ Consumer Consumer Total $0 $0

ANZ $862,423 $990,000 Totals

Iii ti

Borrower Financier Name Facility Type Amount($) Loan Purpose Loan Term Loan Term (Yrs) (Mths)

Joseph Keith Francis Courte and Gail Louise Courte in their CBA Term loan 471 ,675 Property investment. 25 0 own ca acities and as trustees of the

i 0 rt !her Term loan 203,633 Property investment. 25

-0 i rt 346,884 Property investment. 5 0 _ ui R I ing ,00 Prop ty i v s n. 0

a i c R ol in ,60 c di! card.

Gail Louise Courte CBA Te 0 ,9 0 - ro i t n. - 0

Gail Louise Courte Other Term loan 244,009 Properly investment. 25 0

Gail Louise Courte WBC Term loan 251,511 Property investment. 25 0

Gail Louise Courte Other Revolving 24,000 Credit card. 0 0

G ii L i Co c R volvin ,000 C edit C 0

Joseph Keith Francis Courte CBA Te ' 83 ro y i v st ent. 0 Joseph Keith Francis Courte CBA Term loan 30,035 Property investment. 0

Joseph Keith Francis Courte CBA Term loan 1, 4 roperly investment. 2 0

Joseph Keith Francis Courie CBA Revolving 7,500 Credit card. 0 0

s I h K it Ci t A R v ing 99,000 Property investment. 0 0

I

'https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME CF PrintCM2.asp?Country=AU&CLGNo=4018559277 &CLGName=%2... 16/11/2010

ANZ.029.001.0192

Print CM

Credit Memorandum Securities Schedule

CLG Name *Courte Family Trust No. 2 CLG Number CLG (LMK)

Schedule 1 Borrower

Contains Confidential lnfonnation

Conf1dent1al

ANZ.029.001.0193

Page 10 of23

Date 05/10/2010

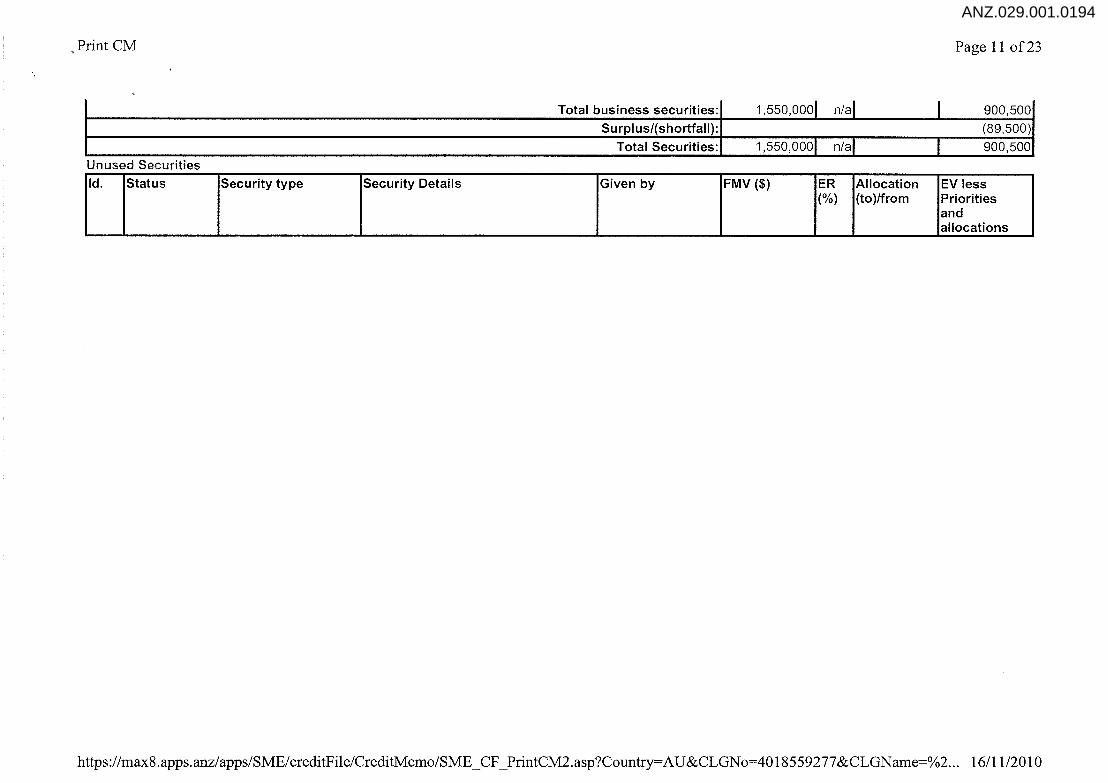

otal Business Facilities $ otal Consumer Facilities $ oseph Keith Francis Courte and Gail Louise Courte in their own capacities and as trustees of

. he Courte Famil Trust No 2 990,000 0

Id. Status Security type

Business securities a To be taken

b To be taken

c To be taken

1st One Provision Mortgage

1st One Provision Mortgage

1st One Provision Mortgage

Security Details

In favour of: Joseph Keith Francis Courte and Gail Louise Courte in their own capacities and as trustees of the Court~d Rural~Miles 4415 Kylie Phipps 28/09/2009

In favour of: Joseph Keith Francis Courte and Gail Louise Courte in their own capacities and as trustees of the Cou · Rural llHebel 4486 Kylie Phipps ~09/2009

In favour of: Joseph Keith Francis Courte and Gail Louise Courte in their own capacities and as trustees of the Courte Fam~·1 Trust No 2 Standard Residential • · · Kylie Phipps 1

Given by

Joseph Keith Francis Courte and Gail Louise Courte in their own capacities and as trustees of the Courte Family Trust No2 Joseph Keith Francis Courte and Gail Louise Courte in their own capacities and as trustees of the Courte Family Trust No2

Joseph Keith Francis Courte and Gail Louise Courte in their own capacities and as trustees of the Courte Family Trust No 2

FMV ($)

360,000

950,000

240,000

ER (%)

55

55

75

Allocation (to)/from

0

0

0

EV less Priorities and allocations

198,000

522,500

180,000

1

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME CF PrintCM2.asp?Country=A U&CLGNo=4018559277 &CLGName=%2. .. 16/11/2010

ANZ.029.001.0194

Print CM

Credit Memorandum General Remarks

Conf1dent1al

CLG Name *Courte Family Trust No. 2 CLG Numbe CLG (LMK)

Key Ratios

E . J ntitv : hK"hF osep, e1t . c ranc1s ourte an dG "IL . C a1 ou1se

Interest cover ratio

Gross farm income ($)

Debt to gross farm income (%)

Operating expenses to gross farm income(%)

Farm operating surplus ($)

Farm debt ratio (%)

Total debt ratio(%)

ourte tn t

Contains Confidential lnfonnation

Date 05/10/2010

h" e1r own capacities an d f as trustees o the c ourte Family Trust No 2 30/06/2008 30/06/2009 Variation%

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

0.00 0.00 0.00 0.00 0.00 0 .00 0.00 0.00 0.00 0.00 0.00 0.00

Commentary : No ratio calculations possible given no actual FS held for borrowing entity.

ANZ.029.001.0195

Page 12 of23

Prospective

'https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME CF PrintCM2.asp?Country=AU&CLGNo=4018559277&CLGName=%2... 16/11/2010

Contains Confidential lnfonnation , Print CM

Credit Memorandum Risks and Mitigants

CLG Name *Courte Family Trust No. 2 CLG Number CLG (LMK)

Outstanding taxation or other statutory payments Awaiting information from accountant

Delinquent accounts

Conf1dent1al

I

Date 05/10/2010

ANZ loan seriously in arrears - appears loans with other financiers also under pressure. See general comments

Loss of key supplier/customer/tenant Lost the lessee of the property ·- so now looking to sell this property. Loss of rent has impacted cash flows

Other factors Excessive debt, too may commitments, lack of real income to service debt, poor prospects. Refer general comments

Historic figures differ from the expected future performance Past results have little bearing on clients current position - refer CTS and general comments.

General Comments

ANZ.029.001.0196

Page 13 of23

There are a number of aspects of this credit which are poor and for which there a few mitigants. Debt reduction via sale of assets is the only option available for clients. Ability to service debts is not evident from income streams. Loan to be strictly conditioned to enable monitoring and to protect enforceability of the banks security.

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME _CF_ PrintCM2.asp?Country=A U&CLGNo=4018559277 &CLGN ame=%2... 16/11/2010

Contains Confidential Information

Print CM

Credit Memorandum Capacity to Service Date 05/10/2010

CLG Name *Courte Family Trust No. 2 CLG Numbe CLG (LMK)

Conf1dent1al

Entity: Gail Louise Courte, Joseph Keith Francis Courte, Jo- and Gail Louise Courte in their own capacities and as trustees of the ' ' · · Joseph Keith Francis Courte and Gail Louise Courte in their own capacities and as trustees of the Courte Family Trust No 2

Taxable income Mr Courte

taxable income Mrs Courte Net profit before tax

Interest add backs Mr Courte Interest add backs Mrs Courte

Interest expenses

Depreciation Mr Courte Depreciation Mrs Courte

Depreciation expenses Extraordinary expenses

Actual available for debt servicing Credit costs for existing and new facilities Business taxation

Tax est Mr Courte

Tax est Mr Courte

Tax Mr Courte Tax Mrs Courte

Personal taxation

Personal living expenses

Total Commitments

Actual surplus/defici t

Sensitised finance commitments

Sensitised surplus/deficit

30/06/2008

63,356 61 ,310

45,950 38,500

2,150 1,193

12,356 11,310

ANZ.029.001.0197

Page 14of23

30/06/2009

-13,493

57,693 124,666 44,200

58,259 53,183

84,450 111,442

1,588

995 3,343 2,583

212,459 158,225 1,362,993 1 ,362,993

12, 172 23,666 12,172

30,000 30,000 1,416,659 1,405, 165

(1 ,204,200) (1,246,940)

1,450,093 1 ,450,093

(1 ,291,300) (1,334,040)

Commentary: The data above comprises only information from the personal returns of Mr and Mrs Courte. We have not been provided with any taxation data for

'https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME CF PrintCM2.asp?Country=AU&CLGNo=4018559277 &CLGName=%2... 16111/2010

, Print CM

ANZ.029.001.0198 Contains Confldeotial lnfomiation

Page 15 of23

their 2 trusts at this time.

Historical data is of little use in this case because we are missing data and also clients personal situation has varied so much in that Mrs Courte is currently not full time at nursing because of the recent birth of another child and Mr Courte also ceased to operate his vehicle trading business. They have also lost the tenant to the property - nd the simple reality right now is that clients do not have sufficient income streams to service debts.

From what we have been provided, which is in essence a summary of their complex rental position and other incomes is that they have the following income streams: *Total weekly residential rentals of $5242 = $22715 pm= $272584 gross pa (No allowances made here for expenses such as rates, agents costs, R & M, rates etc. *Rental of[A ltit!tjiD block - $200 per week= $10,400 pa (Again no deductions allowed for) * Current part time nursing income Mrs Courte net after tax pfn - $858 = $22308 pa * We have no details for any farm related income but that would be nominal at best * We are not aware of any other inocme that Mr Courte may be generating

The total gross income on these figures is $305k approx. The loss of the income from the P'!T" property lease was worth some $71 K pa which is indeed substantial and Mrs Court's lower wages also has an impact. Not withstanding these items though, even through removing the $990K to be repaid to our ASL, which reduces actual commitments for the next 12 months to approx $373K, clients would not be able to service interest on all debts after other expenses on rental properties are brought to account and some amount allowed for in living costs - you will note we input $30K - clients do appear to live quite frugally.

Indeed they have not really been servicing any landmark/ANZ debts for quite some time - thus the overdrawn account we have in place now which has arisen purely due to the redirection of interest. Through restructuring the ANZ debts and effectively deferring interest for 6 months, this should at least take some pressure off clients to focus on servicing other debts and selling down assets for debt reduction.

It is far from ideal that we submit to allowing other financiers priority to be serviced ahead of us, however, due to the nature of the lending they have in place it is most doubtful that they would be able to do any restructures with the other financiers so it is prudent that we give them an opportunity to endeavour to meet those obligations whilst at the same time setting very clear expectations for what is required in regards to meeting ANZ payments.

Credit costs for existing and new facilities for the next twelve months ($)

Borrower Facility Repayment I Reduction Amount (L) Interest Duration (D) Term (T) Credit Costs Arrangement Rate (I)

Courte Family Trust No 2 ASL - Variable Interest Only 0 8.9 n/a n/a 0

Courte Family Trust No 2 ASL - Variable Interest Only 0 8.9 n/a n/a 0

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME_CF _PrintCM2.asp?Country=AU&CLGNo=4018559277&CLGName=%2 ... 16/11/2010

ANZ.029.001.0199 Contains Confidential Information

Print CM Page 16 of23

Courte Family Trust No 2 Overdraft (revolving) Interest Only 0 12.3 n/a n/a 0

Courte Family Trust No 2 ABL - Variable Interest Only 990,000 11.62 n/a n/a 115,038

Courte Family Trust No 2 ABL - Variable Once-off Lump Sum 990,000 11.62 n/a n/a 990,000 Conf 1dent1al

Term loan 471 ,675 6.66 n/a 300 months 38,785

Gail Louise Courte Term loan 203,633 7.25 n/a 300 months 17,662

Gail Louise Courte Term loan 346,884 6.86 n/a 300 months 29,050

Gail Louise Courte Revolving 55,000 6.96 n/a n/a 3,828

Gail Louise Courte Revolving 28,600 20.49 n/a n/a 5,860

Gail Louise Courte Term loan 44,950 6.86 n/a 300 months 3,764

Gail Louise Courte Term loan 244,009 6.7 n/a 300 months 20,138

Gail Louise Courte Term loan 251,511 7.16 n/a 300 months 21,641

Gail Louise Courte Revolving 24,000 20.74 n/a n/a 4,978

Gail Louise Courte Revolving 6,000 21 .24 n/a n/a 1,274

Joseph Keith Francis Term loan 373,383 6.76 n/a 300 months 30,985 Courte

Joseph Keith Francis Term loan 30,035 6.76 n/a 300 months 2,492 Courte

Joseph Keith Francis Term loan 121,343 6.85 n/a 300 months 10, 153 Courte

Joseph Keith Francis Revolving 7,500 20.99 n/a n/a 1,574 Courte

Joseph Keith Francis Revolving 99,000 6.61 n/a n/a 6,544 Courte

Joseph Keith Francis Term loan 388,845 7.25 n/a 300 months 33,727 Courte

Joseph Keith Francis Term loan 246,727 9.32 n/a 300 months 25.498

'https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME CF PrintCM2.asp?Country=A U&CLGNo=4018559277 &CLGN ame=%2... 1611 1/2010-

Contains Confidential lnfOfTllation ANZ.029.001.0200

_Print CM Page 17 of23

I Courte

Total: 1,362,993 1

Sensitised finance commitments for the next twelve months ($)

Borrower Facility Amount (l ) Interest Duration (D) Term (T} Sensitised Rate (I) Costs

Courte Family Trust No 2 ABL - Variable 0 8.9 365 days 4045 days 0

Courte Family Trust No 2 ABL - Variable 0 8.9 365 days 3925 days 0

Courte Family Trust No 2 Overdraft (revolving) 0 12.3 n/a n/a 0

Courte Family Trust No 2 ABL - Variable 990,000 11.62 174 days 174 days 1,023,278 c onfldent1al II Term loan 471 ,675 13.72 n/a 300 months 66,924

Gail Louise Courte Term loan 203,633 13.72 n/a 300 months 28,893

Gail Louise Courte Term loan 346,884 13.72 n/a 300 months 49,218

Gail Louise Courte Revolving 55,000 13.72 n/a n/a 10, 111

Gail Louise Courte Revolving 28,600 13.72 n/a n/a 5,258

Gail Louise Courte Term loan 44,950 13.72 n/a 300 months 6,378

Gail Louise Courte Term loan 244,009 13.72 n/a 300 months 34,621

Gail Louise Courte Term loan 251,511 13.72 n/a 300 months 35,686

Gail Louise Courte Revolving 24,000 13.72 n/a n/a 4,412

Gail Louise Courte Revolving 6,000 13.72 n/a n/a 1,103

Joseph Keith Francis Courte Term loan 373,383 13.72 n/a 300 months 52,978

Joseph Keith Francis Courte Term loan 30,035 13.72 n/a 300 months 4,262

Joseph Keith Francis Courte Term loan 121 ,343 13.72 n/a 300 months 17,217

Joseph Keith Francis Courte Revolving 7,500 13.72 n/a n/a 1,379

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME _CF _PrintCM2.asp?Country=AU&CLGNo=4018559277 &CLGName=%2... 16/11/2010

ANZ.029.001.0201

Print CM

Credit Memorandum Corporate Information

CLG Name *Courte Family Trust No. 2 CLG Number CLG (LMK)

General corporate background

ANZ.029.001.0202 Contains Confidential lnfOfTllatioo

Page 19 of23

Date 05/10/2010 Conf1dent1al

Clients background was in nursing (Mrs Courte) and motor vehicle industry (Mr Courte) who bought cars, repaired and serviced and then re sold them. They began building their residential property portfolio over the past 10 years or so and from perusal of the LMK file, it appears they approached LMK for finance in June 2005 when they sought funds to buy a rural property at Goondiwindi. It was considered at that time that they may not have been viable as 100% finance was sought -$540K.

That request was superceeded in Sept 05 by a request for $900K to buy a different property for $1 .2M - some $300K was to be drawn from credit lines they had already - again there were issues of concern identified regarding overal CTS debts of some $2.4M at that stage.

It appears that clients property purchase options changed quite a bit over a 12 month period as properties they looked at were sold to other parties. They eventually settled on their existing home property at Miles in June 06 for which finance was approved and TBL $395K. Within 3/4 months of that purchase they then acquired · for $882K with TBL $1.3M approx.

Since that time they have sold assets and reduced debts but also increased borrowings due to a variety of reasons but it is clear that the opinion in 2008 was that clients were quite stretched. In late 2009 further lending was approved subject to a condition that the resiential property we hold now at Oakey be sold . Cleints resisted the condition because of CGT issues for Mrs Courte. In essence the last approval remains unactioned and due to non meeting of payments , and clients OD debt has blown out due to redirection of interest payments.

They are not active farmers as they have just $1 OK of cattle based on fresh SP held.

Management profile

It appears quite clear that clients have dealt through brokers to get loans for investment properties and have built their portfolio on the back of 1/0 lending and steadily increasing values. There is no doubt that the lower income of Mrs Courte now, the loss of rent on P'lf"and Mr Courte ceasing to trade motor vehicles has impacted their income streams severely and they now find themselves in their current predicament.

We believe that clients have endeavoured to give the perception that they can manage their affairs but based on the number of loans they have current across a variety of lenders and that they are all either stressed or close to it - or in our case severely in arrears, we consider management ability to be poor.

Their ability as actual farmers in operating a beef cattle business on their home farm is also considered poor as they do not appear to have a strong background in the industry and with just $1 OK in cattle held now, the future in that industry is not sustainable.

Corporate Tree

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME_CF _PrintCM2.asp?Country=AU&CLGNo=4018559277&CLGNarne=%2. .. 16/1 1/2010

ANZ.029.001.0203

Print CM

Credit Memorandum Manager approval

CLG Name *Courte Family Trust No. 2 CLG Numbe CLG (LMK)

Loss in event of default

Are securities cross-collateralised? Total Proposed ANZ Business Limits($)

Contains Confidential lnfonnation

Conf1dent1al

Does any business entity in the customer group have a security shortfall? The sum of all security shortfall for the business entities in the customer group ($) Security Cover(%)

Date 05/10/2010

Yes 990,000 Yes 89,500 91 c

ANZ.029.001.0204

Page 21 of23

Security Indicator Commentary : As noted in Exec summary, vals were done internally on the rural properties by ex employee Kylie Phipps. They appear

to be realistic on the surface but if a revaluation is needed on any or all security properties we would recommend they be outsourced given the precarious nature of the client group. Costs could eb included into the final restructured loan amount.

As it sits now however, despite a shortfall on margins, we are reasonably safe and do not envisage any real loss.

Conclusions and recommendations

Clearly this is a very distressed credit and the proposed restructure should be the bank's final measue of assistance. The restructure gives clients 6 months to proactively and voluntarily sell down assets and make debt reductions. Should there be none forthcoming in that time then the issue of asset sell down will have to be pushed, thus the proposed conditions shown herein.

If clients reject the proposed Letter Of Offer in regards to the conditions, which they have done so before, then we would recommend that the file be placed immediately into Lending Services for issue of demand letters based on arrears in place now.

Manager approval

Your decision is: Recommended

Conditions precedent

• ANZ obtaining a satisfactory credit report, in ANZ's absolute opinion, from any credit reporting agency used by ANZ.

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME _CF _PlintCM2.asp?Countiy=A U &CLGNo=40185 59277 &CLGName=%2. .. 16/11/2010

ANZ.029.001.0205 Contains Confidential lnfOfTllation

Print CM Page 22 of23

Other conditions

• You agree that if you enter into the loan or facility as a trustee, you will be liable under the loan or facility both personally and as trustee of the trust. You also assure ANZ that: (i) the loan or facility is for a proper purpose under the trust; (ii) you have the power and authority under the trust to enter into the contract; and (iii) You have the right to be indemnified fully out of the trust property, before the beneficiaries of the trust, for all liabilities you incur under the loan or facility.

• You agree that the following properties may be revalued for ANZ at least once eve 12 months at our cost while facilities continue to be provided by ANZ: 15 as described in title reference Hebel Qld 4486 as described

in tit e re erence Oakey as described in title reference Each valuation must be undertaken by a valuer acceptable to ANZ. In addition, reserves e ng o revalue at any time any property held as security at its cost.

• You execute or undertake to execute (or arrange for its execution) in favour of ANZ a first Water Rights Mortgage incorporating the ANZ's Standard Provisions for Water Mortgages registrable in or notifiable to the relevant water authority over any water rights held or to be held by you (or anyone on your behalf or associated with you), which, either now or later, are or may be used upon the mortgaged land, whether or not any of those water rights: (i) attach to or benefit the mortgaged land or any other land; (ii) remain unused; (iii) are transferable for the benefit of any other land or person or corporation; or (iv) are transferable by any other person or corporation to you . You also undertake: (i) to execute all other documents and securities as ANZ may require to enable ANZ to be fully secured in respect of those water rights; (ii) to direct the Water Authority to deliver to ANZ any document of title to the Water Rights; (iii) to deliver to ANZ the document of title to the Water Rights immediately, if it is issued to you; and (iv) not, without ANZ's prior consent, to deal with, lease or dispose of any Water Right or any interest or right relating to a Water Right, either temporarily or permanently.

• Customers agree not to raise any further outside borrowings without the Banks prior knowledge (and consent which would not be unreasonably withheld. • Clients undertake to provide the Bank with copies of agents agreements in respect to the property nd the

property known as ~Crows Nest Qld by 30 November 2010. Conf1dent1al

• Clients to advise th~ received for the following properties within 1 week of any s~e: lilHebel Qld as described in title reference P'I® I 1 Crows Nest Qld; 3.~ Dyrabb N W.

• Clients to advise the Bank within 1 week of any formal contract for sale bein si ned on any of the properties listed below: · · P 11f'Hebel Qld as described in title reference • · · Crows Nest Qld; 3. • • · · yrabba NSW. In the event of a sale eing arranged on the properties listed at 2 and 3 above, clients undertake to direct an amount offunds from final settlements to the bank in accordance with agreements made with the bank prior to final settlements. In the event of a sale being arranged on the property listed at 1 above, all ANZ debts are to be cleared from settlement funds.

• Clients acknowledge that failure to make reductions to ANZ debts at the end of the six month time frame for the ANZ Business Loan Variable Rate will require a full review of their position with further properties to be listed for sale to make reductions to all debts including ANZ.

• Clients agree and undertake to provide updated tenancy agreements of leased properties along with details of properties listed for sale and the progress of such by 15 February 2011

Financial reports

• Your financial statements within 30 days of request. For the purpose of this condition , financial statements includes any financial records, projections or statements.

Financial covenants

Nil

.. https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME CF PrintCM2.asp?Countiy=AU&CLGNo=4018559277&CLGName=%2... 1611112010

'

Print CM

Contains Confidential lnfcxmation

..

Signed by: Dimity Jamieson

Dated: 28/10/2010

Credit Memorandum Credit approval

CLG Name *Courte Family Trust No. 2 CLG Number CLG (LMK)

Credit approval

Your decision is: Approved

Departmental issues:

Conf1dent1al

CCR as per Non Agri 7 C AAA VU to confirm current valuations

Other matters:

ANZ.029.001.0206

Page 23 of23

Date 05/10/2010

Diary note to be completed on delivery of letter of offer, & respective conditions Clearly we are remedying defaults however LOF clearly states that should client fail to reduce debt further asset sales will be required. Proection of their equity requires early sales whilst it is acknowelded market may not assist, hence term & interest relief. Clients must be realistic to protect residual assets.

Decision by: Adrian Husking Date: 16/11/201012:30:13 PM

https://max8.apps.anz/apps/SME/creditFile/CreditMemo/SME _CF _PrintCM2.asp?Country=AU&CLGNo=4018559277 &CLGName=%2... 16/11/2010