Embed Size (px)

Citation preview

2 0 0 8 a n n u a l r e p o r t

S T A T E M E N T O F C O M P A N Y B U S I N E S SS T O C K H O L D E R S ’ I N F O R M A T I O N

Corporate OfficesPACCAR Building777 106th Avenue N.E.Bellevue, Washington98004

Mailing AddressP.O. Box 1518Bellevue, Washington98009

Telephone425.468.7400

Facsimile425.468.8216

Web sitewww.paccar.com

AeroCab, AERODYNE, Air Leaf, Braden, Carco, ComfortClass, DAF, Gearmatic, Kenmex, Kenworth, Kenworth Clean Power, Leyland, PACCAR, PACCAR MX, PACCAR PX, PacLease, PacTrac, Peterbilt, PX-6, PX-8, TRP, UltraCab and Unibilt are trademarks owned by PACCAR Inc and its subsidiaries.

Independent AuditorsErnst & Young LLPSeattle, Washington

SEC Form 10-KPACCAR’s annual report to the Securities and Exchange Commission will be furnished to stockholders on request to the Corporate Secretary, PACCAR Inc, P.O. Box 1518, Bellevue, Washington 98009. It is also available online at www.paccar.com/investors/investor_resources.asp, under SEC Filings.

Annual Stockholders’MeetingApril 28, 2009, 10:30 a.m. Meydenbauer Center11100 N.E. Sixth StreetBellevue, Washington98004

An Equal Opportunity Employer

This report was printed on recycled paper.

Stock Transfer and Dividend Dispersing AgentWells Fargo Bank Minnesota, N.A.Shareowner ServicesP.O. Box 64854St. Paul, Minnesota 55164-0854800.468.9716www.wellsfargo.com/shareownerservices

PACCAR’s transfer agent maintains the company’s shareholder records, issues stock certificates and distributes dividends and IRS Form 1099. Requests concerning these matters should be directed to Wells Fargo.

Online Delivery of Annual Report and Proxy StatementPACCAR’s 2008 Annual Report and the 2009 Proxy Statement are available on PACCAR’s Web site at www.paccar.com/2008annualmeeting/

Stockholders who hold PACCAR stock in street name may inquire of their bank or broker about the availability of electronic delivery of annual meeting documents.

Financial Highlights

Message to Shareholders

6 PACCAR Operations

Financial Charts

3 Stockholder Return Performance Graph

4 Management’s Discussion and Analysis

3 Consolidated Statements of Income

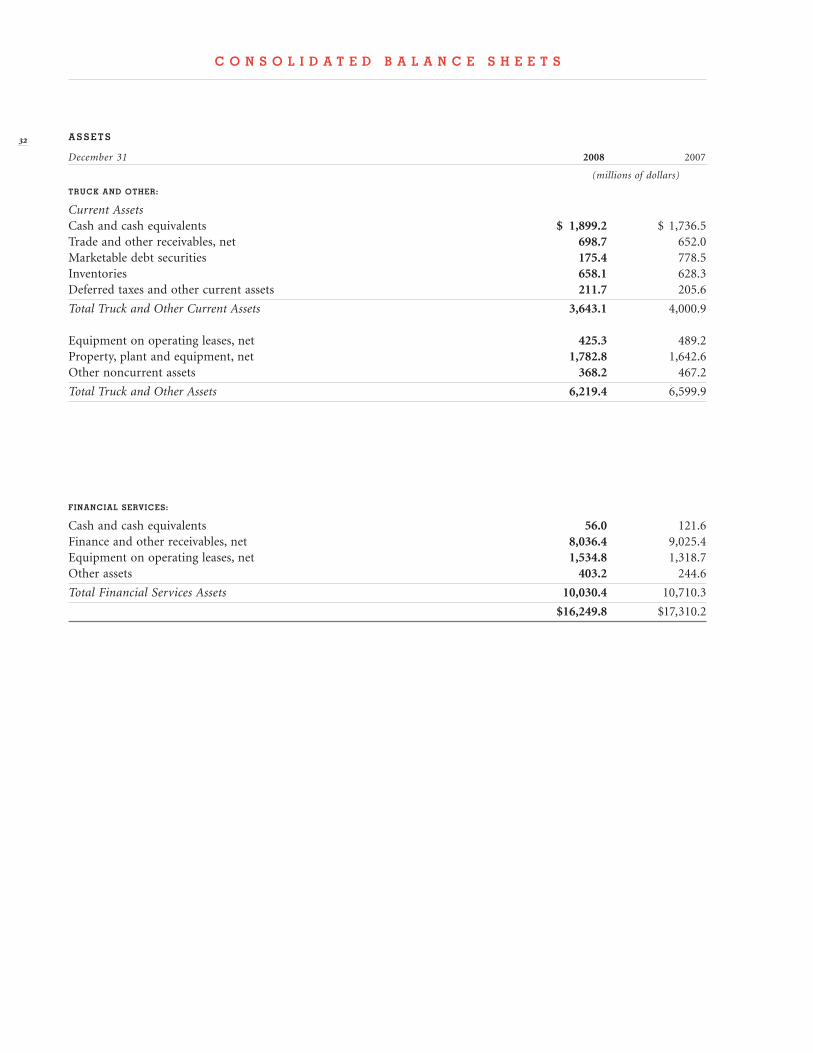

3 Consolidated Balance Sheets

34 Consolidated Statements of Cash Flows

35 Consolidated Statements

of Stockholders’ Equity

36 Consolidated Statements

of Comprehensive Income

36 Notes to Consolidated Financial Statements

50 Management’s Report on Internal Control

Over Financial Reporting

50 Report of Independent Registered Public

Accounting Firm on the Company’s

Consolidated Financial Statements

5 Report of Independent Registered Public

Accounting Firm on the Company’s

Internal Controls

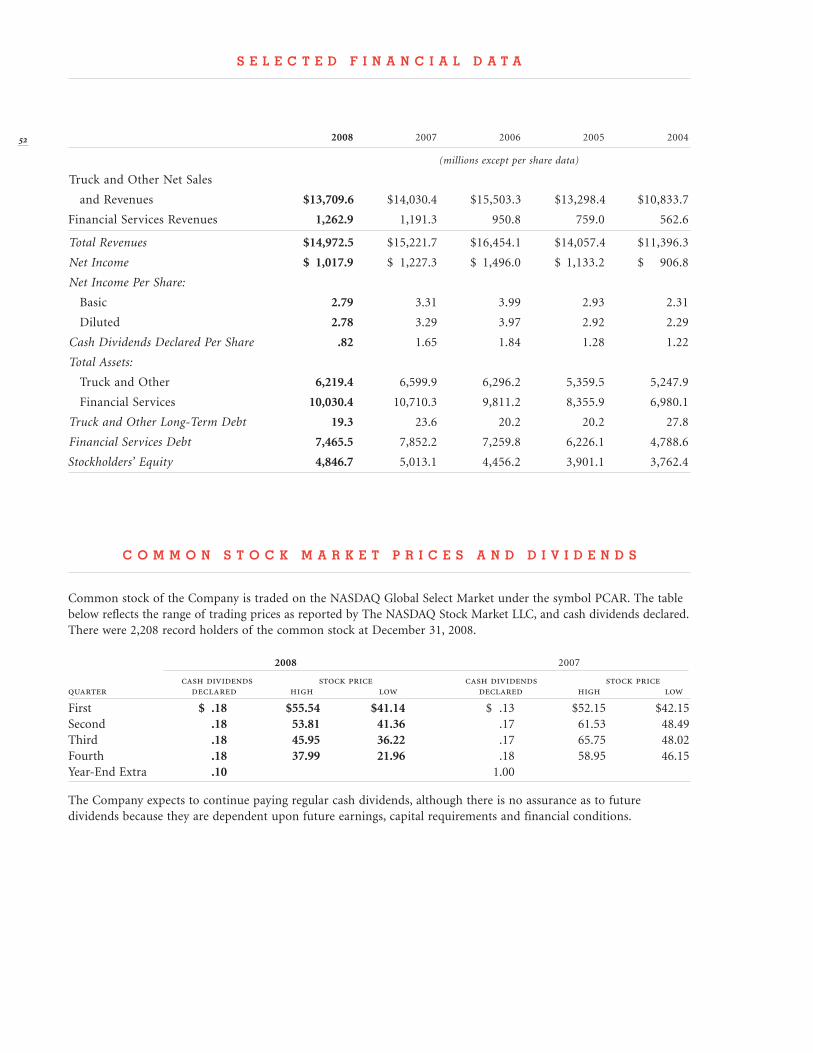

5 Selected Financial Data

5 Common Stock Market Prices and Dividends

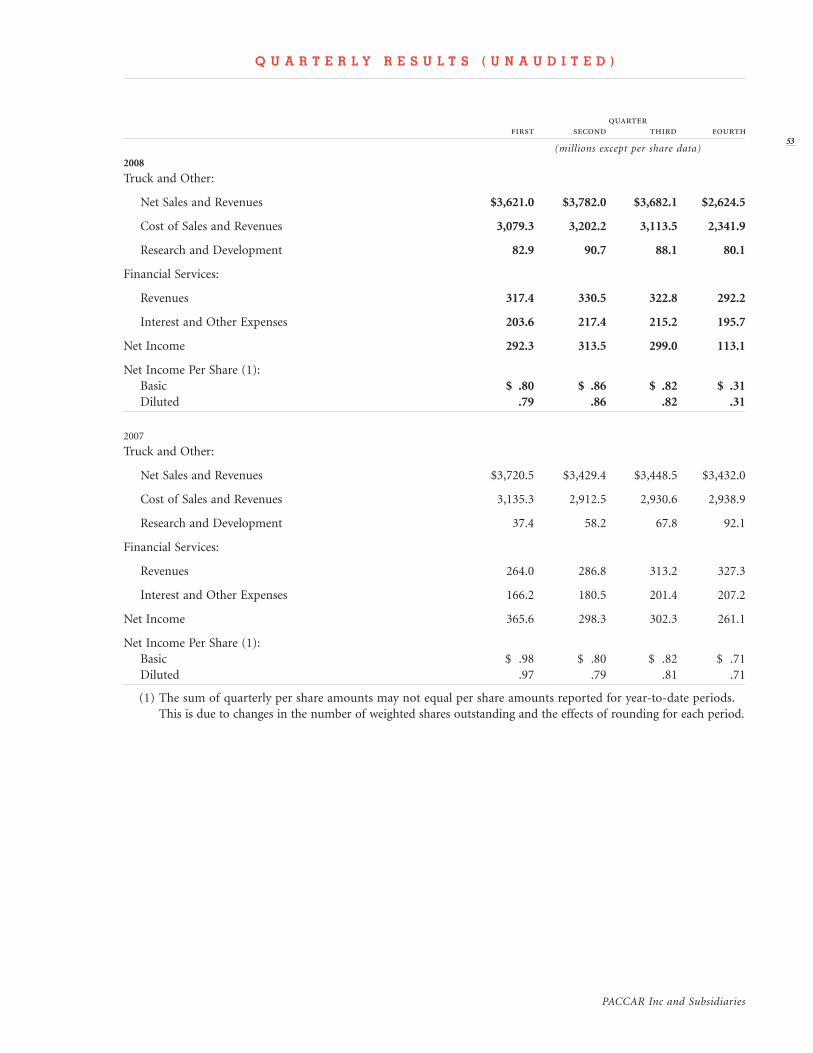

53 Quarterly Results

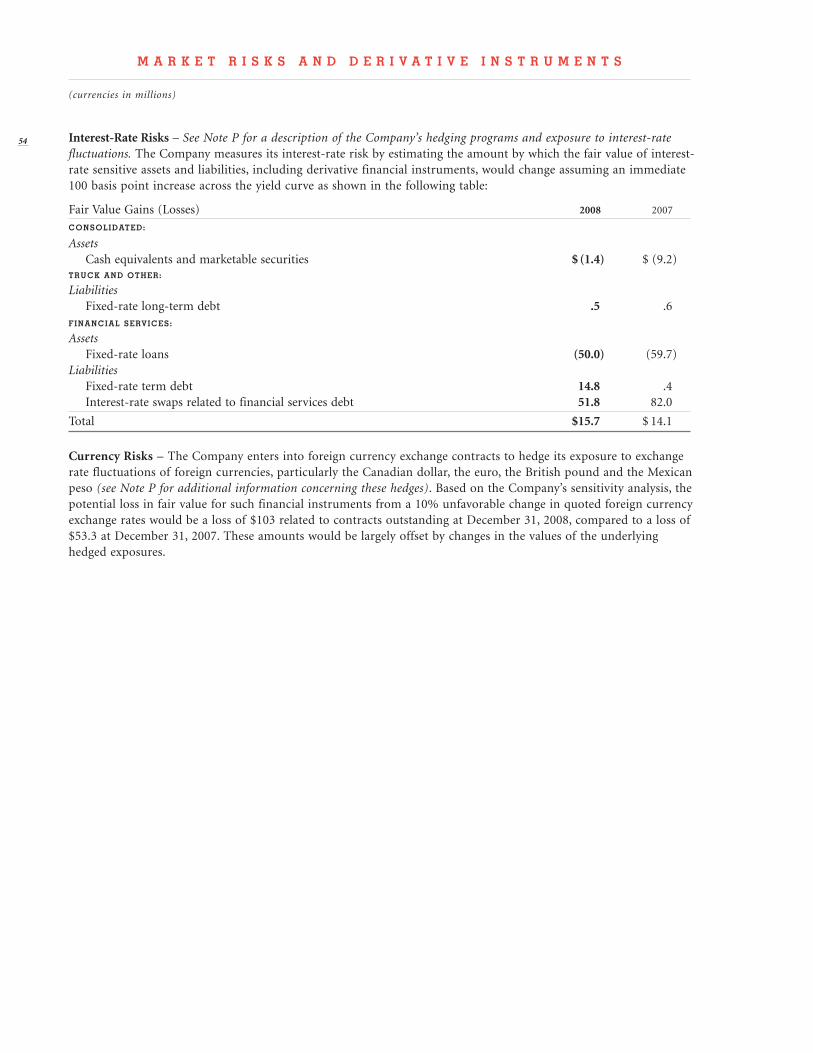

54 Market Risks and Derivative Instruments

55 Officers and Directors

56 Divisions and Subsidiaries

CONTENTS

PACCAR is a global technology company that manufactures Class 8 commercial

vehicles sold around the world under the Kenworth, Peterbilt and DAF nameplates.

The company competes in the North American Class 5-7 market with its medium-

duty models assembled in North America and sold under the Peterbilt and Kenworth

nameplates. The company also manufactures Class 4-7 trucks in the United

Kingdom for sale throughout Europe, the Middle East, Australia and Africa under

the DAF nameplate. PACCAR distributes aftermarket truck parts to its dealers

through a worldwide network of Parts Distribution Centers. Finance and leasing

subsidiaries facilitate the sale of PACCAR products in many countries worldwide.

Significant company assets are employed in financial services activities. PACCAR

manufactures and markets industrial winches under the Braden, Gearmatic and

Carco nameplates. PACCAR maintains exceptionally high standards of quality for

all of its products: they are well engineered, are highly customized for specific

applications and sell in the premium segments of their markets, where they have a

reputation for superior performance and pride of ownership.

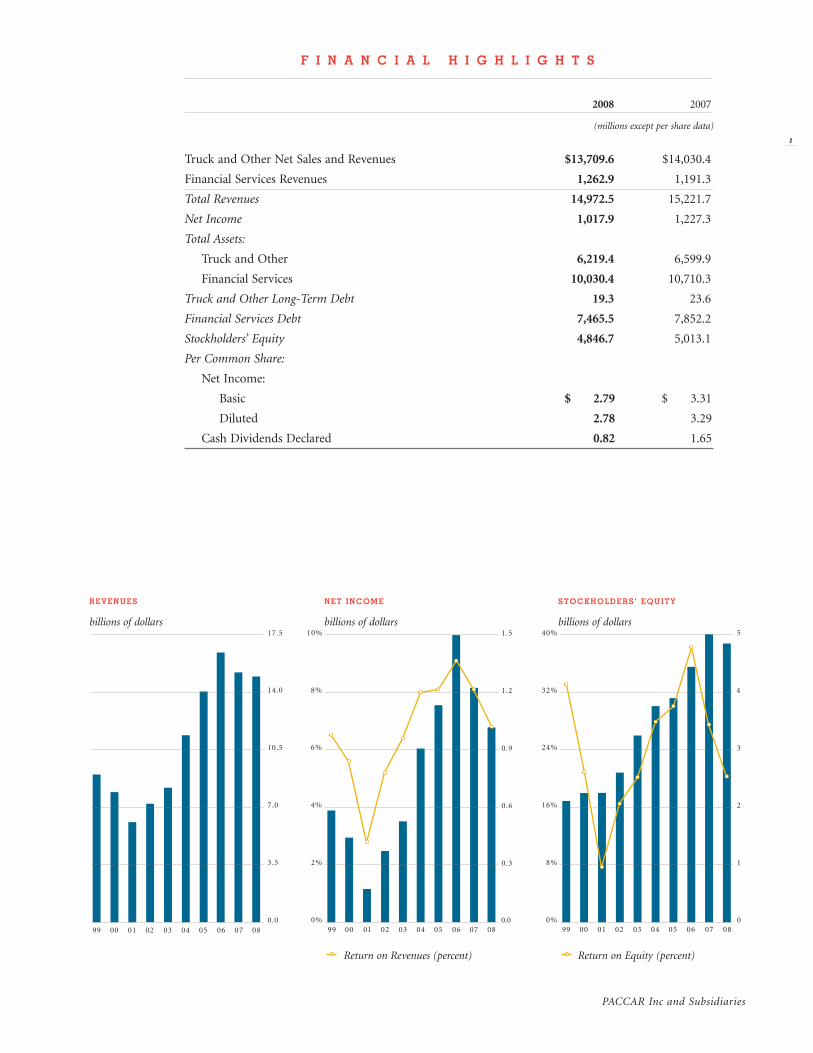

F i n a n c i a l h i g h l i g h t s

1

2008 2007

(millions except per share data)

Truck and Other Net Sales and Revenues $13,709.6 $14,030.4

Financial Services Revenues 1,262.9 1,191.3

Total Revenues 14,972.5 15,221.7

Net Income 1,017.9 1,227.3

Total Assets:

Truck and Other 6,219.4 6,599.9

Financial Services 10,030.4 10,710.3

Truck and Other Long-Term Debt 19.3 23.6

Financial Services Debt 7,465.5 7,852.2

Stockholders’ Equity 4,846.7 5,013.1

Per Common Share:

Net Income:

Basic $ 2.79 $ 3.31

Diluted 2.78 3.29

Cash Dividends Declared 0.82 1.65

PACCAR Inc and Subsidiaries

$

REVEnUEs

billions of dollars

stockholdERs’ EqUity

billions of dollars

nEt incomE

billions of dollars

Return on Equity (percent)

99 00 01 02 03 04 05 06 07 08

R E V E N U E S

billions of dollars17.5

14.0

10.5

7.0

3.5

0.099 00 01 02 03 04 05 06 07 08

N E T I N C O M E

billions o f do l lar s 1.5

1.2

0.9

0.6

0.3

0.0

4%

6%

8%

10%

2%

0%99 00 01 02 03 04 05 06 07 08

S T O C K H O L D E R S ’ E Q U I T Y

billions of dollars 5

4

3

216%

24%

32%

40%

8%

0%

1

0

Return on Revenues (percent)

2

Industry Class 8 truck sales in North America, including

Mexico, declined to 179,000 vehicles, compared to

207,000 the prior year. Over 3,000 fleets declared

bankruptcy due to lower freight volume, higher fuel

prices and the recessionary economy. The European

heavy truck market in 2008 was 334,000 vehicles,

compared to 337,000 in 2007, a strong performance that

declined abruptly in the fourth quarter 2008. Many of

our competitors are discounting their vehicles below

cost in the challenging market. There may be some

competitors exiting the business in the next few years

due to lack of profitability.

Even in this troubled market, PACCAR continued to

be one of the leaders in financial performance for

capital goods companies worldwide. After-tax return on

beginning shareholder equity (ROE) was 20.3 percent in

2008, compared to 27.5 percent in 2007. The company’s

2008 after-tax return on revenues was 6.8 percent.

PACCAR has distributed over $3.5 billion in dividends

and increased shareholder equity to $4.85 billion during

the last ten years. PACCAR’s average annual total

shareholder return was 17.6 percent over the last decade,

versus a negative 1.4 percent for the Standard & Poor’s

500 Index. The fragility of global financial institutions

provided a timely reminder of the merits of PACCAR’s

conservative business approach and quality product and

customer service focus.

t o o U R s h a R E h o l d E R s

PaccaR had a very good year in 2008, even as the global recession had an

increasingly negative impact on the company’s results throughout the year. PaccaR’s

success is due to its global diversification, superior product quality, technology-led

process efficiency and strong results from aftermarket parts and financial services.

the company has delivered an impressive 70 consecutive years of net income.

customers benefited from PaccaR’s record $805 million of capital investments and

research and development, which enhanced manufacturing capability, developed

innovative aftermarket support programs and accelerated new product introductions.

PaccaR delivered 126,000 trucks to its customers and sold $2.3 billion of aftermarket

parts. PaccaR had record truck deliveries in Europe, which were offset by a depressed

truck market in the U.s. and canada. PaccaR Financial services generated $3.4

billion of new loan and lease business.

net income of $1.02 billion on revenues of $15.0 billion was the fourth highest in

the company’s 103-year history. PaccaR declared cash dividends of $.82 per share,

including a special dividend of $.10 per share. Regular quarterly cash dividends have

increased over 500 percent in the last 10 years.

3

inVEsting FoR thE FUtURE — PACCAR’s solid

profits, excellent balance sheet and intense focus on

quality, technology and productivity enhancements have

allowed the company to invest $3.8 billion since 1999

in capital projects, products and processes. Yearly

productivity and efficiency improvement of 5-7 percent

and capacity improvement of over 100 percent in the last

five years have enhanced the capability of manufacturing

and parts facilities. PACCAR is recognized as one of the

leading applied-information technology companies in the

industry, and innovation continues to be a cornerstone

of its success.

Capital investments were a record $463 million in

2008. One exciting multi-year initiative is the

construction of PACCAR’s engine assembly plant in

Mississippi, which builds upon our legacy as a premier

engine manufacturer. Other major capital projects

during the year included the unveiling of an enhanced

engine research and development center in PACCAR’s

Technical Center (Mt. Vernon, Washington), opening of

a new parts distribution center (PDC) in Budapest,

Hungary, and a 20 percent capacity improvement at

Leyland’s manufacturing facility.

PACCAR continues to examine business opportunities

in Asia, with its primary focus on China and India.

PACCAR is increasing its purchases and component sales

in China through its Shanghai office. The business

opportunities in Asia have dampened, but still present

attractive long-term returns.

siX sigma — Six Sigma is integrated into all business

activities at PACCAR and has been adopted at 190 of the

company’s suppliers and many of the company’s dealers.

Its statistical methodology is critical in the development

of new product designs, customer services and

manufacturing processes. Since inception, Six Sigma has

delivered over $1.2 billion in cumulative savings across

the company. In addition, “High Impact Kaizen Events”

(HIKEs) leverage Six Sigma methods with production

flow improvement concepts. Almost 13,000 employees

have been trained in Six Sigma and 9,700 projects have

been implemented since its inception. Six Sigma, in

conjunction with Supplier Quality and Development,

has been vital to improving logistics performance and

component quality by the company’s suppliers.

inFoRmation tEchnology — PACCAR’s

Information Technology Division (ITD) and its 650

innovative employees are an important competitive

asset for the company. PACCAR’s use of information

technology is centered on developing and integrating

software and hardware that will enhance the quality and

efficiency of all products and operations throughout

the company, including the seamless integration of

suppliers, dealers and customers. In 2008, ITD provided

innovative advancements in new manufacturing software

and infrastructure capacity upgrades. Over 17,000 dealers,

customers, suppliers and employees have experienced

the company’s technology center highlighting surface

computing, tablet PCs, an electronic leasing and finance

office and an electronic service analyst.

tRUcks — U.S. and Canadian Class 8 industry retail

sales in 2008 were 153,000 units, and the Mexican market

totaled 26,000. The European Union (EU) industry

heavy truck sales were 334,000 units.

PACCAR’s Class 8 retail sales in the U.S. and Canada

achieved a market share of 26.0 percent in 2008

compared to 26.4 percent the prior year. DAF achieved

14.1 percent share in the 15+ tonne truck market in

Europe. Industry Class 6 and 7 truck registrations in the

U.S. and Canada were 60,000 units, a 31 percent decrease

from the previous year. In the EU, the 6- to 15-tonne

market was 80,000 units, down 5 percent from 2007.

PACCAR’s North American and European market shares

in the medium-duty truck segment were excellent, as the

company delivered 23,000 medium-duty trucks and

tractors in 2008.

A tremendous team effort by the company’s

purchasing, materials and production personnel

contributed to improved product quality and

manufacturing efficiency during challenging market

conditions. High commodity prices, which began to

abate during the year, were partially offset by PACCAR’s

excellent long-term supplier partnerships, which enabled

production and efficiency improvements.

PACCAR’s product quality continued to be recognized

as the industry leader in 2008. Kenworth dominated

customer satisfaction awards in the Class 8 markets and the

DAF CF was the 2008 Fleet Truck of the Year in the U.K.

Over 65 percent of PACCAR’s revenue was generated

outside the United States, and the company realized

4

excellent synergies globally in product development, sales

and finance activities, purchasing and manufacturing.

DAF Trucks achieved record truck production and sales

and excellent market share.

Leyland Trucks is the United Kingdom’s leading truck

manufacturer. Leyland expanded its innovative body-

building program that has delivered over 750 custom-

built-bodied vehicles to customers.

PACCAR Mexico (KENMEX) had a challenging year

as the Mexican economy slowed and truck fleets were

reduced. Their new manufacturing facility is delivering

improved efficiency and product quality.

PACCAR Australia achieved good results in 2008. The

introduction of new Kenworth models and expansion

of the DAF product range in Australia combined for a

24.5 percent heavy-duty market share in 2008. PACCAR

Parts Australian sales delivered another year of record

performance.

PACCAR International exports trucks and parts to

over 100 countries and had an excellent year due to strong

sales buoyed by natural resource exploration globally.

AFTERMARKET CUSTOMER SERVICES — PACCAR

Parts had an excellent year in 2008. With sales of

$2.3 billion, PACCAR Parts is the primary source for

aftermarket parts for PACCAR products, and supplies

parts for other truck brands to PACCAR’s dealer networks

around the world. Over five million heavy-duty trucks

are operating in North America and Europe, and the

average age of these vehicles is estimated to be over six

years. The large vehicle parc creates excellent demand

for parts and service and moderates the cyclicality of

truck sales.

PACCAR Parts added new distribution centers and

expanded current facilities to enhance logistics

performance to dealers and customers. PACCAR Parts

continues to lead the industry with technology that

offers competitive advantages at PACCAR dealerships.

Managed Dealer Inventory (MDI) is now installed at

1,050 PACCAR dealers worldwide. PACCAR Parts

enhanced its Connect program, a software solution for

customer fleet-maintenance management. The web-based

application provides fleets with the tools to reduce their

vehicle operating costs.

FINANCIAL SERVICES — PACCAR Financial Services’

(PFS) conservative business approach, coupled with

PACCAR’s superb S&P credit rating of AA- and the

strength of the dealer network, enabled PFS to earn good

results in 2008 despite turbulent worldwide financial

markets. The PACCAR Financial Services group of

companies has operations covering three continents

and 20 countries. The global breadth of PFS and its

responsive credit application processes supported a

portfolio of 166,000 trucks and trailers, with total assets

of $10 billion and earned a pre-tax profit of $217 million.

PACCAR Financial Services is the preferred funding

source in North America for Peterbilt and Kenworth

trucks, financing 32 percent of dealer sales.

The unsettled financial markets and resulting “credit

crunch” presented a daily challenge that increased

funding costs for our customers and prompted a

contraction in our finance companies’ assets. Special

praise is merited for PACCAR’s treasury and finance

teams who diligently, creatively and positively managed

the company through a very challenging market in 2008.

PACCAR Financial Europe (PFE) completed its

seventh year of operations, with increased assets and

good profits as it served DAF dealers in 16 European

countries. PFE provides wholesale and retail financing

for DAF dealers and customers, and finances 21 percent

of DAF’s vehicle sales.

PACCAR Leasing (PacLease) earned its 15th

consecutive year of record operating profits and placed

4,900 new PACCAR vehicles in service in 2008. The

PacLease fleet grew to over 32,500 vehicles as 18 percent

of the North American Class 6-8 market selected full-

service leasing to satisfy their equipment needs. PacLease

substantially strengthened its market presence in 2008,

increasing its global network to 362 outlets, and

represents one of the largest full-service truck rental

and leasing operations in North America.

ENVIRONMENTAL LEADERSHIP — PACCAR is a global

environmental leader. A significant accomplishment

during the year was earning ISO 14001 environmental

certification at all PACCAR manufacturing facilities in

Europe and North America. PACCAR introduced

medium-duty hybrid-electric vehicles, which can achieve

up to a 30 percent fuel economy improvement. Several

of the manufacturing facilities achieved “Zero Waste to

Landfill” status during the year. PACCAR employees

are environmentally conscious and utilize van pools, car

pools and bus passes for 30 percent of their business

commuting.

A LOOK AHEAD — The dedicated efforts of PACCAR’s

18,000 employees enabled the company to distinguish

itself as a global leader in the technology, capital goods,

financial services and aftermarket parts businesses.

Superior product quality, technological innovation and

balanced global diversification are three key operating

characteristics that define PACCAR’s business philosophy.

In North America and Europe, the recession will have

a negative impact on the truck market in 2009. The

implementation of updated North American engine

emission standards in 2010 may encourage some

operators to slightly pull forward their truck purchases.

Current estimates for Class 8 trucks in North America

indicate that annual industry sales could be similar to

2001 and range from 130,000-170,000 units. This is one

of the lowest levels of sales in the last 10 years. Sales

for Class 6-7 trucks are expected to be between 50,000-

60,000 vehicles. The European heavy-duty truck market,

which had a strong year in 2008, could decline by 40

percent, with sales between 200,000-240,000 trucks,

while demand for medium trucks should range from

50,000-65,000 units.

Though PACCAR had a very good year in 2008, with

several operating divisions achieving record results, the

outlook for 2009 appears difficult due to tumultuous

economic conditions. The company has taken proactive

steps to adjust production rates as well as structurally

reduce costs throughout the organization. The benefits of

geographic diversification, dedicated employees, quality

products, modern facilities, innovative IT systems and a

strong balance sheet, working in tandem with the best

distribution network in the industry, are the fundamental

elements that make PACCAR a vibrant, dynamic

company. PACCAR is well positioned and committed to

maintaining the profitable results its shareholders expect,

by delivering global leading products and services.

PACCAR recognizes two significant retirements. Vice

Chairman Mike Tembreull retired upon completion of

over 38 years of exemplary service, in which he was

instrumental in the profitable growth of PACCAR

Financial and the integration of DAF into PACCAR.

Jim Pigott is retiring after 37 years on the Board of

Directors. Jim also worked for PACCAR for thirteen years

and was an inspirational leader on the Board, sharing his

wisdom, insight and global business knowledge. We

thank Jim and Mike for their dedication and wish both

a happy and healthy retirement.

PACCAR and its employees are firmly committed to

strong quality growth and are proud of the remarkable

achievement of 70 consecutive years of net profit.

PACCAR plans for the long-term, and our shareholders

have benefited from that approach. The embedded

principles of integrity, quality and consistency of

purpose continue to define the course in PACCAR’s

operations. The proven business strategy — delivering

technologically advanced, premium products and an

extensive array of tailored aftermarket customer services

— enables PACCAR to approach growth opportunities

pragmatically with a long-term focus. In a challenging

recession, PACCAR continues to enhance its stellar

reputation as a leading technology company in the

capital goods and financial service marketplace.

5

m A r K c . p i g O t t

Chairman and Chief Executive Officer

February 16, 2009

pAccAr Executive committee

Seated Left to Right: Jim Cardillo, Mike Tembreull, Mark Pigott,

Tom Plimpton; Standing Left to Right: Dave Anderson, Aad

Goudriaan, Ron Armstrong, Dan Sobic, Bob Christensen,

Michael Barkley

D A F T R U C K S

DAF Trucks N.V. celebrated its 80th anniversary in 2008 by achieving new sales and

production records. Truck deliveries exceeded 64,000 units as DAF strengthened its

reputation as one of Europe’s leading commercial vehicle manufacturers.

DAF Trucks increased its market share in both the light and heavy truck segments due to a class-leading

product range and a comprehensive dealer network throughout Europe. In the light truck segment, market share

grew from 8.3 percent in 2007 to 9.3 percent in the EU last year. In the over 15-tonne segment, DAF’s EU share

increased from 13.9 percent in 2007 to 14.1 percent in 2008.

The DAF CF85 won “Fleet Truck of the Year” for an unprecedented eighth time at the Motor Transport awards in

London. Organized by the leading British magazine Motor Transport, the judging panel consisted of 25 prominent

U.K. based fleet operators. The CF series also captured the “Technology and Innovation Award,” a distinction

awarded by the Australian trade journal Motoring Matters to truck and trailer manufacturers who have made

important contributions to the advancement of vehicle and driver safety.

DAF earned, for the second year, the award for “Best Bus

Engine Producer” and “Best Coach Engine Producer” at Bus

World Asia in Shanghai. The engines were honored due to the

reliability and durability of the PACCAR 9.2-liter and PACCAR

12.9-liter engines, combined with their excellent fuel efficiency.

In 2008, DAF Trucks was the world’s first truck

manufacturer to offer Enhanced Environmentally-friendly

Vehicles (EEV) in its entire product range. These EEV trucks feature particulate emissions 50 percent lower than

the stringent Euro 5 emission standards scheduled for October 2009.

DAF unveiled significant enhancements to its popular CF and XF105 models for 2009. The vehicles offer

attractive and contemporary new interior designs, an enhanced driveline and — as options — adaptive cruise

control and forward collision warning systems. In recognition of its 80th anniversary, DAF unveiled a limited

edition XF105. The special flagship model exhibits a striking distinctive exterior design with silver accents and

extensive premium interior features.

DAF introduced a sophisticated telematics package that offers a data communications system enabling

operators to optimize fuel management and their business processes.

The PACCAR Production System (PPS) integration enhanced DAF’s manufacturing efficiency and product

quality. The 50-PPM (Parts Per Million) Initiative, introduced in all manufacturing plants, sets a new standard

for supplier operational excellence.

DAF Trucks expanded its extensive distribution network with 25 new facilities opening in Central and Eastern

European markets.

7

DAF has earned a reputation, during the past 80 years, for developing, manufacturing and

servicing innovative, industry-leading transport equipment of the highest quality. DAF

marked its eighth decade with a special, limited edition of its flagship model XF105.

p e t e r b i l t m o t o r s c o m p a n y

peterbilt set a market share record in 2008, capturing more than 13 percent of class 8

truck sales in the U.s. peterbilt’s innovative fuel-conserving technology, leading-edge

aerodynamics and superior product quality reinforce peterbilt’s position as the “class”

of the industry.

Peterbilt Models 387 and 386 were recognized as fuel efficient and environmental vehicle leaders by the

Environmental Protection Agency’s (EPA) SmartWaySM program. These Peterbilt trucks utilize a proprietary

range of fuel-saving, low-emission equipment specifications for Class 8 long-haul tractors and trailers which

have established the industry performance standard.

In 2008, Peterbilt introduced the Class 6 Model 330 and Class 7 Model 335 hybrid vehicles that reduce

emissions and the vehicle’s carbon footprint, as well as delivering Peterbilt quality and performance. The

fuel savings achieved by these hybrid vehicles range up to

30 percent depending on the application.

Peterbilt introduced the Model 388 Low Profile truck,

designed specifically for the auto carrier industry. The lower

cab height allows the transport of larger vehicles and increases

by 10 percent the number of vehicles that may be hauled.

Peterbilt is developing hybrid Hydraulic Launch Assist

technology on its low-cab-forward Model 320 for vocational and refuse applications. Testing has shown a

significant improvement in fuel economy and potential brake maintenance reduction of 50 percent annually.

Peterbilt launched a proprietary front Air Leaf Suspension on Models 384, 386, 388 and 389, which offers a

20 percent improvement in ride and delivers excellent handling characteristics.

Peterbilt updated its conventional medium-duty product Model 335 with a new dash featuring improved

side-window defrost and new panel colors. The Peterbilt Navigation System incorporates a five-inch touch-

screen and an MP3 audio player.

Peterbilt continues to make significant investments in its manufacturing facilities to enhance efficiency and

product quality. The Denton, Texas, plant installed a chassis robotic paint system to increase capacity by 50

percent and enhance Peterbilt’s industry-leading quality. Peterbilt is the first North American truck

manufacturer to achieve this innovative milestone.

The Peterbilt Denton facility achieved an impressive environmental standard of “Zero Waste to Landfill” and

global ISO 14001 certification. The elimination of waste was accomplished through recycling programs, employee

involvement and partnering with strategic suppliers. Peterbilt Denton produced its 300,000th vehicle during the

year.

The Peterbilt dealer network expanded to a record 246 locations throughout the U.S. and Canada.

9

Peterbilt’s Model 384, offering a luxurious 63-inch Unibilt UltraCab sleeper, merges excellent

aerodynamics and fuel efficiency with a “classic” conventional profile. The durable, lightweight

chassis features exceptional maneuverability, visibility and ergonomic design.

f i n a n c i a l c h a r t s

k e n w o r t h t r u c k c o m p a n y

kenworth swept the vehicle segment awards in the 2008 J.D. power and associates

heavy Duty truck customer Satisfaction Study for the second consecutive year —

ranking highest in the over the road and Vocational categories.*

Kenworth introduced a new Driver Information Center for the T2000, which provides drivers with real-time

information to increase fuel economy and efficiency. The Driver Information Center offers an enhanced

multiplex instrumentation system featuring diagnostic information to optimize engine performance.

Kenworth delivered record Class 6-7 market share in the U.S. as more customers recognized the benefits of

Kenworth vehicle durability and ease of handling for city applications.

Kenworth’s new T270 and T370 medium duty diesel-electric hybrid trucks offer

fuel efficiency improvements up to 30 percent in delivery applications and up to

50 percent in utility applications.

Kenworth T800 liquefied natural gas (LNG) trucks were launched with excellent

results. Greenhouse gas emissions were reduced by 20 percent and this new model

has been embraced as a leading alternative fuel vehicle at West Coast ports, such as

the Ports of Los Angeles and Long Beach.

The environmentally friendly Kenworth Clean Power no-idle system is available

on all 72-inch AeroCab sleepers, including the T660, T800 and W900 models. Clean

Power is a proprietary thermal storage technology that maintains constant cab

temperature during non-driving hours. Savings from Clean Power can improve fuel

economy by up to eight percent for fleets with high idle time.

Kenworth Class 8 truck models introduced updated interior trim packages that

incorporated additional storage, ergonomic display panels and new dash refinements.

Kenworth introduced new proprietary suspensions to enhance the ride and handling performance in its

vehicles. The Kenworth AG130 front-axle air suspension is the first front air suspension designed for Kenworth

trucks and improves ride performance by over 15 percent. The new AG400L rear suspension is available in a

tandem axle configuration for Class 8 trucks and a single axle configuration for medium duty models.

Kenworth installed a second robotic paint line at its Chillicothe, Ohio, plant. This is the first PACCAR facility

to integrate four robots painting cabs, hoods and sleepers simultaneously. Kenworth plants in Chillicothe and

Renton, Washington, earned the International Organization for Standardization (ISO) 14001 certification for

superior environmental management systems.

The Kenworth Dealer Network increased to a record 301 dealer locations in the U.S. and Canada.

11

* Kenworth received the highest numerical score among Over the Road and Vocational Class 8 trucks in the proprietary J.D. Power and Associates 2008 Heavy-Duty Truck Customer Satisfaction StudySM. Study based on 2,692 U.S. responses and measures opinions of principal maintainers. Proprietary study results are based on experiences and perceptions of those surveyed in March-June 2008.

Kenworth is a leader in designing innovative, technology-driven products that meet the

challenges of today’s operating environment. The T660 AeroCab AERODYNE delivers fuel

optimizing aerodynamic design and long-haul luxury.

12

P A C C A R A u s t R A l i A

Kenworth dominated the Australian heavy-duty truck market in 2008, capturing

62 percent of the highest horsepower segment, and remained the number one

manufacturer of heavy commercial vehicles in the market.

Kenworth expanded its product offering in 2008 with the introduction of the Model T388. The new medium

duty conventional offers 430 horsepower and is directed at short haul and urban applications where excellent

visibility and tight turning circles are paramount. A new, larger cab option was added to Kenworth’s flagship

over-the-highway truck model, providing increased driver comfort and maximizing carrying capacity.

Kenworth became the first manufacturer in Australia to offer a factory installed liquefied natural gas (LNG)

engine option, providing substantial fuel savings and reducing greenhouse gas emissions by over 20 percent.

PACCAR Parts Australia achieved record sales and profitability with an expanded product range and dealer

network.

In 2008, PACCAR Australia’s Kenworth “Innovation Truck” showcased a broad spectrum of advanced vehicle

technology designed to improve environmental performance, productivity, efficiency and safety. The vehicle’s

innovative concepts include collision-avoidance systems, advanced lighting and wireless communications.

In Australia, Kenworth is the most revered nameplate in heavy duty trucking. An agile and versatile performer, this

T350 Agitator provides customers with a half tonne more payload than competitive trucks in a chassis design that’s as

maneuverable as a cabover.

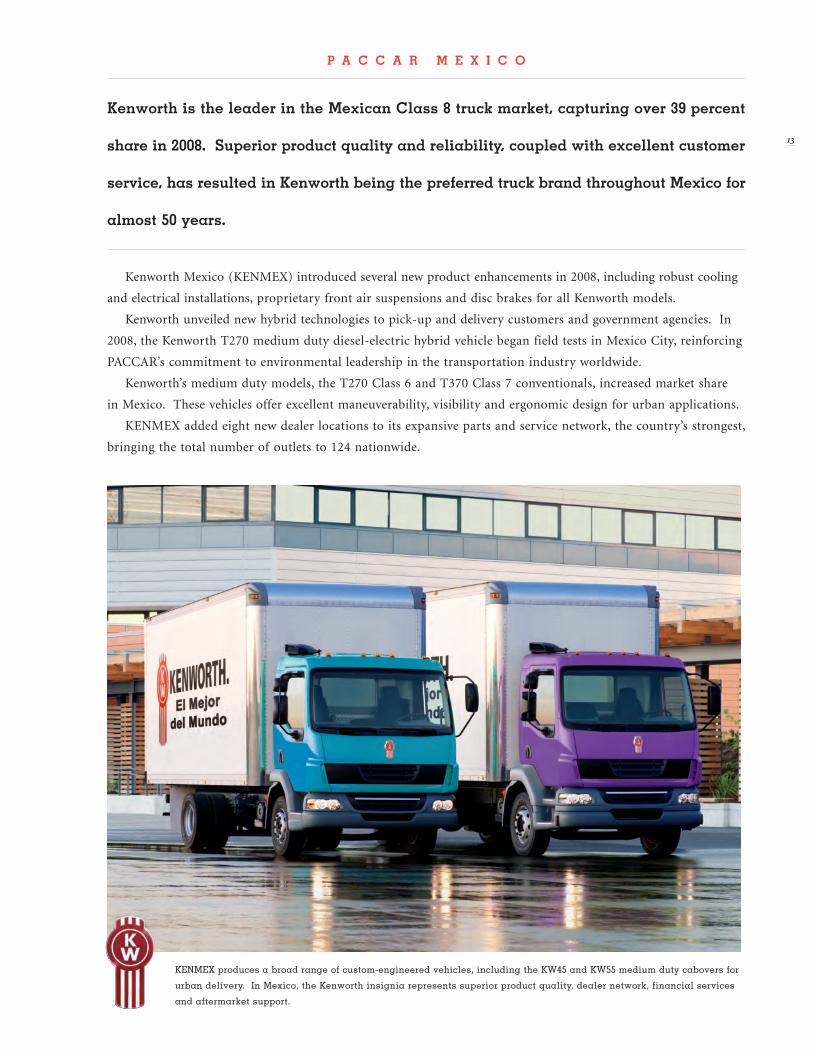

p a c c a r m e x i c o

Kenworth is the leader in the mexican class 8 truck market, capturing over 39 percent

share in 2008. Superior product quality and reliability, coupled with excellent customer

service, has resulted in Kenworth being the preferred truck brand throughout mexico for

almost 50 years.

Kenworth Mexico (KENMEX) introduced several new product enhancements in 2008, including robust cooling

and electrical installations, proprietary front air suspensions and disc brakes for all Kenworth models.

Kenworth unveiled new hybrid technologies to pick-up and delivery customers and government agencies. In

2008, the Kenworth T270 medium duty diesel-electric hybrid vehicle began field tests in Mexico City, reinforcing

PACCAR’s commitment to environmental leadership in the transportation industry worldwide.

Kenworth’s medium duty models, the T270 Class 6 and T370 Class 7 conventionals, increased market share

in Mexico. These vehicles offer excellent maneuverability, visibility and ergonomic design for urban applications.

KENMEX added eight new dealer locations to its expansive parts and service network, the country’s strongest,

bringing the total number of outlets to 124 nationwide.

13

KENMEX produces a broad range of custom-engineered vehicles, including the KW45 and KW55 medium duty cabovers for

urban delivery. In Mexico, the Kenworth insignia represents superior product quality, dealer network, financial services

and aftermarket support.

14

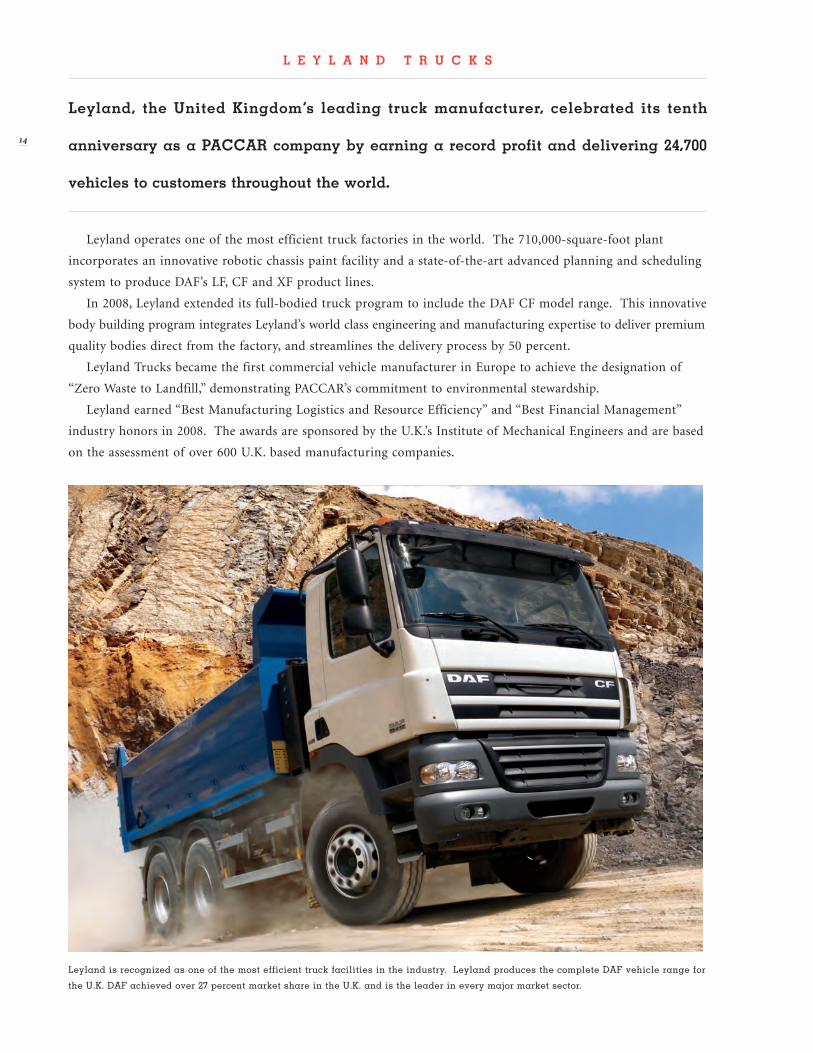

l e y l a n d t r u c K S

leyland, the united Kingdom’s leading truck manufacturer, celebrated its tenth

anniversary as a paccar company by earning a record profit and delivering 24,700

vehicles to customers throughout the world.

Leyland operates one of the most efficient truck factories in the world. The 710,000-square-foot plant

incorporates an innovative robotic chassis paint facility and a state-of-the-art advanced planning and scheduling

system to produce DAF’s LF, CF and XF product lines.

In 2008, Leyland extended its full-bodied truck program to include the DAF CF model range. This innovative

body building program integrates Leyland’s world class engineering and manufacturing expertise to deliver premium

quality bodies direct from the factory, and streamlines the delivery process by 50 percent.

Leyland Trucks became the first commercial vehicle manufacturer in Europe to achieve the designation of

“Zero Waste to Landfill,” demonstrating PACCAR’s commitment to environmental stewardship.

Leyland earned “Best Manufacturing Logistics and Resource Efficiency” and “Best Financial Management”

industry honors in 2008. The awards are sponsored by the U.K.’s Institute of Mechanical Engineers and are based

on the assessment of over 600 U.K. based manufacturing companies.

Leyland is recognized as one of the most efficient truck facilities in the industry. Leyland produces the complete DAF vehicle range for

the U.K. DAF achieved over 27 percent market share in the U.K. and is the leader in every major market sector.

15

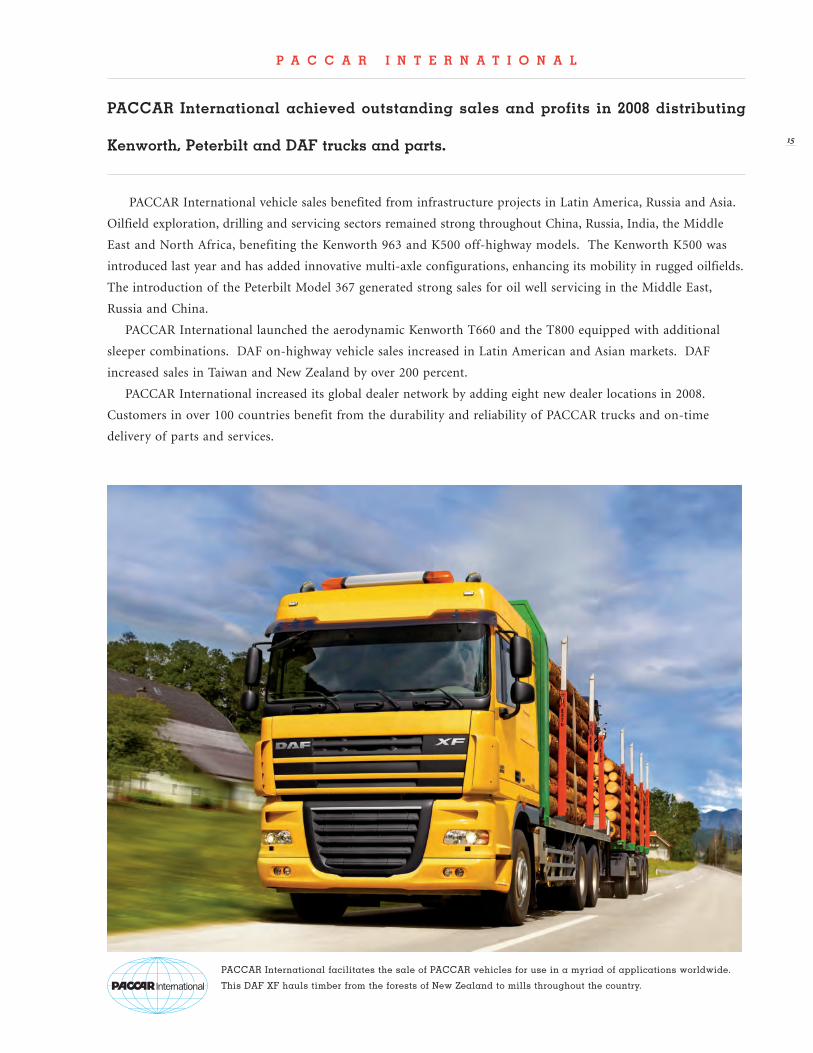

p a c c a r i n t e r n a t i o n a l

paccar international achieved outstanding sales and profits in 2008 distributing

Kenworth, peterbilt and DaF trucks and parts.

PACCAR International vehicle sales benefited from infrastructure projects in Latin America, Russia and Asia.

Oilfield exploration, drilling and servicing sectors remained strong throughout China, Russia, India, the Middle

East and North Africa, benefiting the Kenworth 963 and K500 off-highway models. The Kenworth K500 was

introduced last year and has added innovative multi-axle configurations, enhancing its mobility in rugged oilfields.

The introduction of the Peterbilt Model 367 generated strong sales for oil well servicing in the Middle East,

Russia and China.

PACCAR International launched the aerodynamic Kenworth T660 and the T800 equipped with additional

sleeper combinations. DAF on-highway vehicle sales increased in Latin American and Asian markets. DAF

increased sales in Taiwan and New Zealand by over 200 percent.

PACCAR International increased its global dealer network by adding eight new dealer locations in 2008.

Customers in over 100 countries benefit from the durability and reliability of PACCAR trucks and on-time

delivery of parts and services.

PACCAR International facilitates the sale of PACCAR vehicles for use in a myriad of applications worldwide.

This DAF XF hauls timber from the forests of New Zealand to mills throughout the country.

P A C C A R P A R t s

PACCAR Parts achieved excellent results in 2008 with strong sales and profit

performance — delivering 1.3 million parts shipments worldwide to 1,900 Kenworth,

Peterbilt and DAF dealer locations.

PACCAR Parts expanded its worldwide parts distribution centers (PDC) to 13 to support the growing network

of dealers and customers. The 260,000-square-foot parts distribution center in Budapest, Hungary, began operation

in 2008 and serves DAF’s customers in Central and Eastern Europe. PACCAR Parts completed a 45,000-square-

foot addition of the San Luis Potosi, Mexico, PDC, enhancing service to its Kenworth Mexico dealers.

Introduction of the Peterbilt Preferred, Kenworth Privileges and the DAF “MAX” Loyalty Cards generated

significant retail sales in 2008. More than 75,000 customers worldwide are registered to utilize PACCAR Parts

monthly parts and service programs.

PACCAR Parts implemented a new Radio Frequency (RF) Shipping System in its North American distribution

centers. The system processes freight bills and customer order invoices and reduces transportation costs by

consolidating multiple shipments.

Four PACCAR Parts distribution centers in the U.S. achieved ISO14001 Environmental Certification.

16

PACCAR Parts employs state-of-the-art technologies — wireless voice recognition, integrated logistic systems and tablet PCs. These

innovative investments have contributed to PACCAR Parts’ sophisticated distribution centers leading the industry in aftermarket

customer support.

17

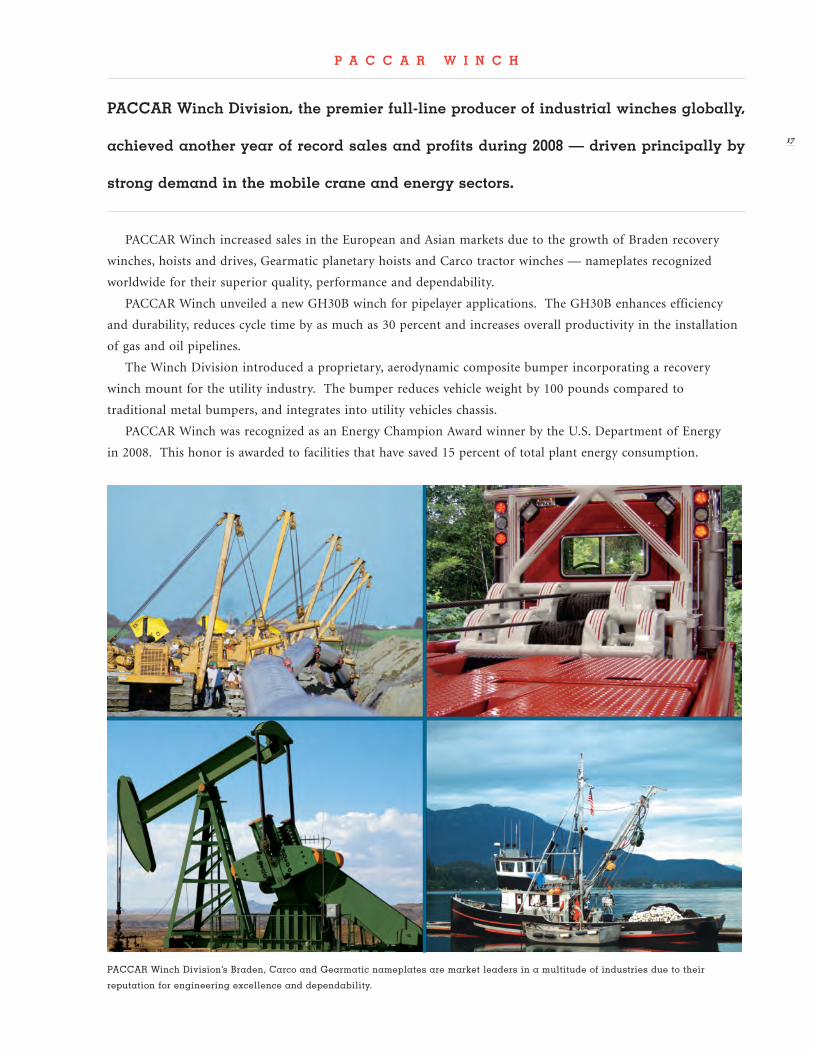

p a c c a r W i n c h

paccar Winch division, the premier full-line producer of industrial winches globally,

achieved another year of record sales and profits during 2008 — driven principally by

strong demand in the mobile crane and energy sectors.

PACCAR Winch increased sales in the European and Asian markets due to the growth of Braden recovery

winches, hoists and drives, Gearmatic planetary hoists and Carco tractor winches — nameplates recognized

worldwide for their superior quality, performance and dependability.

PACCAR Winch unveiled a new GH30B winch for pipelayer applications. The GH30B enhances efficiency

and durability, reduces cycle time by as much as 30 percent and increases overall productivity in the installation

of gas and oil pipelines.

The Winch Division introduced a proprietary, aerodynamic composite bumper incorporating a recovery

winch mount for the utility industry. The bumper reduces vehicle weight by 100 pounds compared to

traditional metal bumpers, and integrates into utility vehicles chassis.

PACCAR Winch was recognized as an Energy Champion Award winner by the U.S. Department of Energy

in 2008. This honor is awarded to facilities that have saved 15 percent of total plant energy consumption.

PACCAR Winch Division’s Braden, Carco and Gearmatic nameplates are market leaders in a multitude of industries due to their

reputation for engineering excellence and dependability.

18

p a c c a r f i n a n c i a l s e r v i c e s

paccar financial services companies (pfs), which support the sale of paccar trucks

worldwide, achieved good results, reporting pre-tax profits of $217 million. pfs

portfolios are comprised of 166,000 trucks and trailers, with total assets of $10 billion.

PACCAR’s excellent credit rating of AA- and conservative business model enables PACCAR Financial to

profitably support the sale of PACCAR trucks in 20 countries on three continents. In 2008, record high fuel

prices coupled with a weaker economy and the financial liquidity crisis challenged the global transport industry.

PACCAR Financial’s ability to access capital markets at competitive rates enabled PFS to provide customers with

attractive financing to meet daily operating requirements.

PFS achieved 28 percent market share and strengthened its position as the preferred source of financing for

Kenworth, Peterbilt and DAF vehicles worldwide through superior customer service and streamlined credit processing.

PFS launched a web-based customer portal that delivers online services, including electronic payments and

current account information 24 hours a day.

PACCAR Financial Europe (PFE) expanded its financial services to DAF dealers and customers in 16 Western

and Central European countries.

PACCAR Financial facilitates the sale of Kenworth, Peterbilt and DAF vehicles worldwide, offering a full

spectrum of creative, flexible financial products and value-added services — consistently supporting sales in

every phase of the business cycle.

19

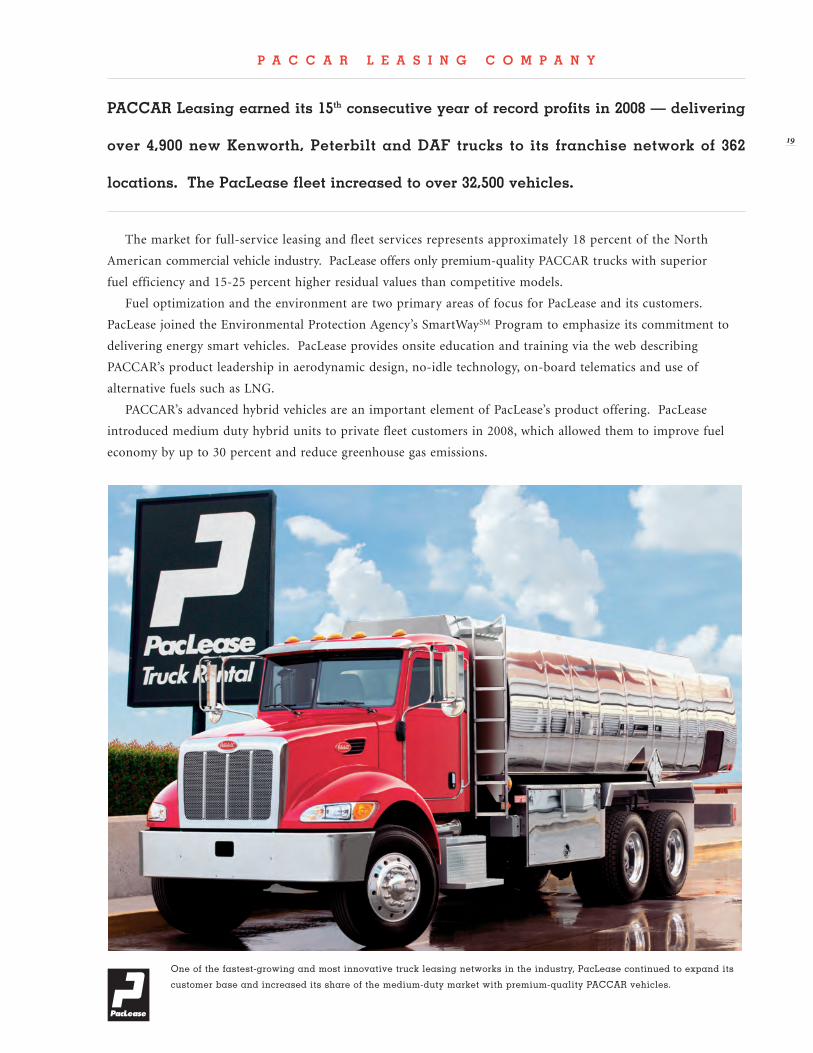

p a c c a r L e a s i n g c o m p a n y

paccar Leasing earned its 15th consecutive year of record profits in 2008 — delivering

over 4,900 new Kenworth, peterbilt and DaF trucks to its franchise network of 362

locations. The pacLease fleet increased to over 32,500 vehicles.

The market for full-service leasing and fleet services represents approximately 18 percent of the North

American commercial vehicle industry. PacLease offers only premium-quality PACCAR trucks with superior

fuel efficiency and 15-25 percent higher residual values than competitive models.

Fuel optimization and the environment are two primary areas of focus for PacLease and its customers.

PacLease joined the Environmental Protection Agency’s SmartWaySM Program to emphasize its commitment to

delivering energy smart vehicles. PacLease provides onsite education and training via the web describing

PACCAR’s product leadership in aerodynamic design, no-idle technology, on-board telematics and use of

alternative fuels such as LNG.

PACCAR’s advanced hybrid vehicles are an important element of PacLease’s product offering. PacLease

introduced medium duty hybrid units to private fleet customers in 2008, which allowed them to improve fuel

economy by up to 30 percent and reduce greenhouse gas emissions.

One of the fastest-growing and most innovative truck leasing networks in the industry, PacLease continued to expand its

customer base and increased its share of the medium-duty market with premium-quality PACCAR vehicles.

20

p a c c a r t e c h n i c a l c e n t e r S

paccar’s technical centers utilize world-class testing facilities and advanced

simulation technologies to accelerate product development and ensure that paccar

continues to provide the highest-quality products in the industry.

PACCAR’s world-class technical centers in Europe and North America are equipped with state-of-the-art

product test and validation capabilities and staffed with technical experts in powertrain and vehicle development.

Sophisticated computer simulations and advanced analysis of engine and vehicle control systems are used to

optimize vehicle efficiency while meeting strict emission regulations. Material laboratories, utilizing electron beam

microscope technology, support the investigation and selection of new materials to reduce vehicle weight while

increasing performance. Vehicle laboratories simulate truck durability testing of the equivalent of one million

miles in months, rather than years.

In 2008, a new 75,000-square-foot Engine Development Center opened at DAF Eindhoven. This sophisticated

facility with 20 advanced test cells leads the global development of PACCAR engines designed for use in Kenworth,

Peterbilt and DAF vehicles. The test cells are utilized to develop new technologies for engine cooling, electrical

systems and exhaust after-treatment.

PACCAR Technical Centers, located in Eindhoven, the Netherlands, and in Washington State, employ highly sophisticated engineering

analysis, simulation and rapid prototyping technologies to accelerate the development of world-class components and designs.

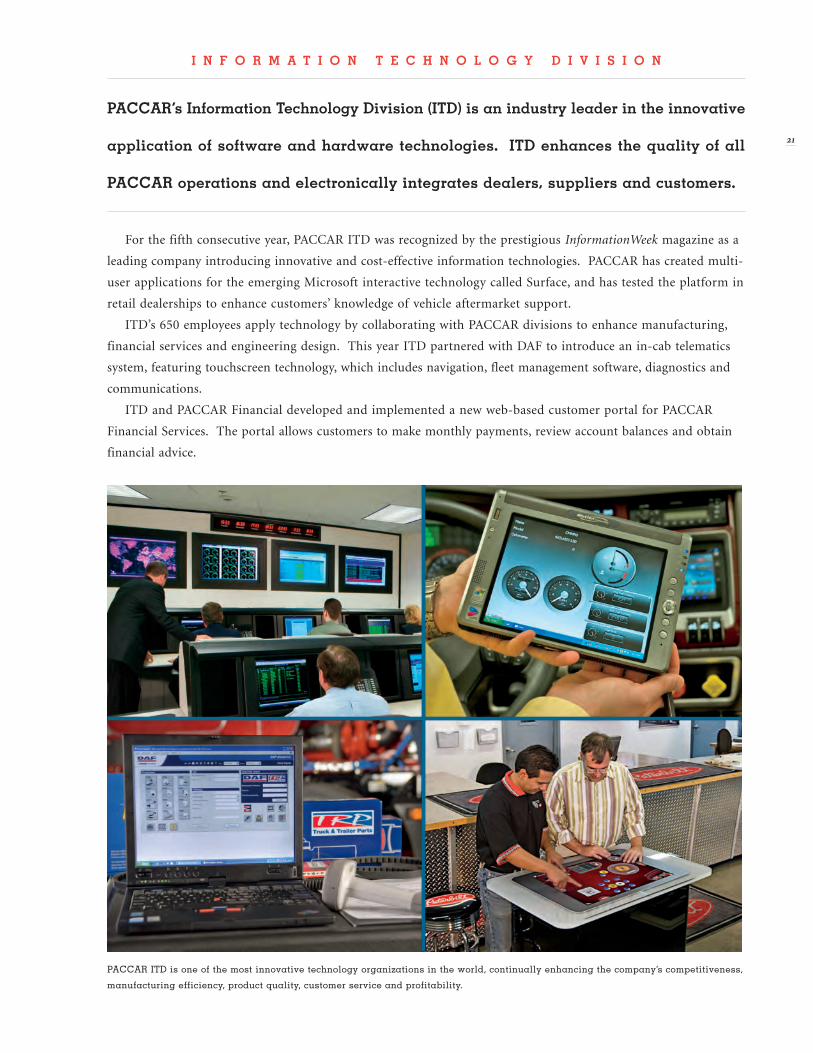

I N F O R M A T I O N T E C H N O L O G Y D I V I S I O N

PACCAR’s Information Technology Division (ITD) is an industry leader in the innovative

application of software and hardware technologies. ITD enhances the quality of all

PACCAR operations and electronically integrates dealers, suppliers and customers.

For the fifth consecutive year, PACCAR ITD was recognized by the prestigious InformationWeek magazine as a

leading company introducing innovative and cost-effective information technologies. PACCAR has created multi-

user applications for the emerging Microsoft interactive technology called Surface, and has tested the platform in

retail dealerships to enhance customers’ knowledge of vehicle aftermarket support.

ITD’s 650 employees apply technology by collaborating with PACCAR divisions to enhance manufacturing,

financial services and engineering design. This year ITD partnered with DAF to introduce an in-cab telematics

system, featuring touchscreen technology, which includes navigation, fleet management software, diagnostics and

communications.

ITD and PACCAR Financial developed and implemented a new web-based customer portal for PACCAR

Financial Services. The portal allows customers to make monthly payments, review account balances and obtain

financial advice.

21

PACCAR ITD is one of the most innovative technology organizations in the world, continually enhancing the company’s competitiveness,

manufacturing efficiency, product quality, customer service and profitability.

f i n a n c i a l c h a r t s

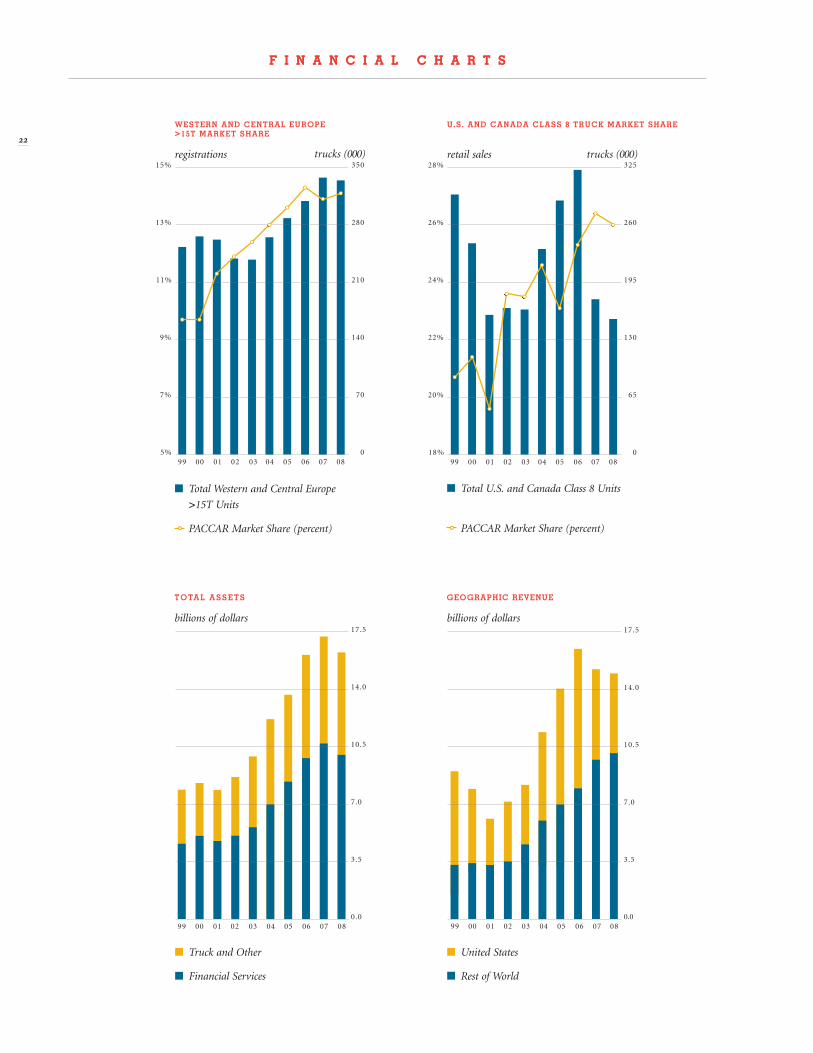

22

f i n a n c i a l c h a r t s

■ Total U.S. and Canada Class 8 Units

PACCAR Market Share (percent)

GEOGraPhic rEVEnUE

billions of dollars

t O ta l a s s E t s

billions of dollars

■ Total Western and Central Europe

>15T Units

PACCAR Market Share (percent)

■ Truck and Other

■ Financial Services

■ United States

■ Rest of World

U.s. and canada class 8 trUck markEt sharE

retail sales

WEstErn and cEntral EUrOPE >15t markEt sharE

registrations

99 00 01 02 03 04 05 06 07 08

17.5

14.0

10.5

3.5

7.0

0.0

GEOGRAPHIC REVENUE

billions of dollars

W E S T E R N A N D C E N T R A L E U R O P E > 1 5 T M A R K E T S H A R E

99 00 01 02 03 04 05 06 07 08

15%

13%

11%

9%

7%

5%

280

350

210

140

70

0

registrations

U . S . A N D C A N A D A C L A S S 8 T R U C K M A R K E T S H A R E

99 00 01 02 03 04 05 06 07 08

28%

26%

24%

22%

20%

18%

260

325

195

130

65

0

retail sales

99 00 01 02 03 04 05 06 07 08

17.5

14.0

10.5

3.5

7.0

0.0

T O TA L A S S E T S

b il lions o f do l lar s

trucks (000)

trucks (000)

PACCAR Inc and Subsidiaries

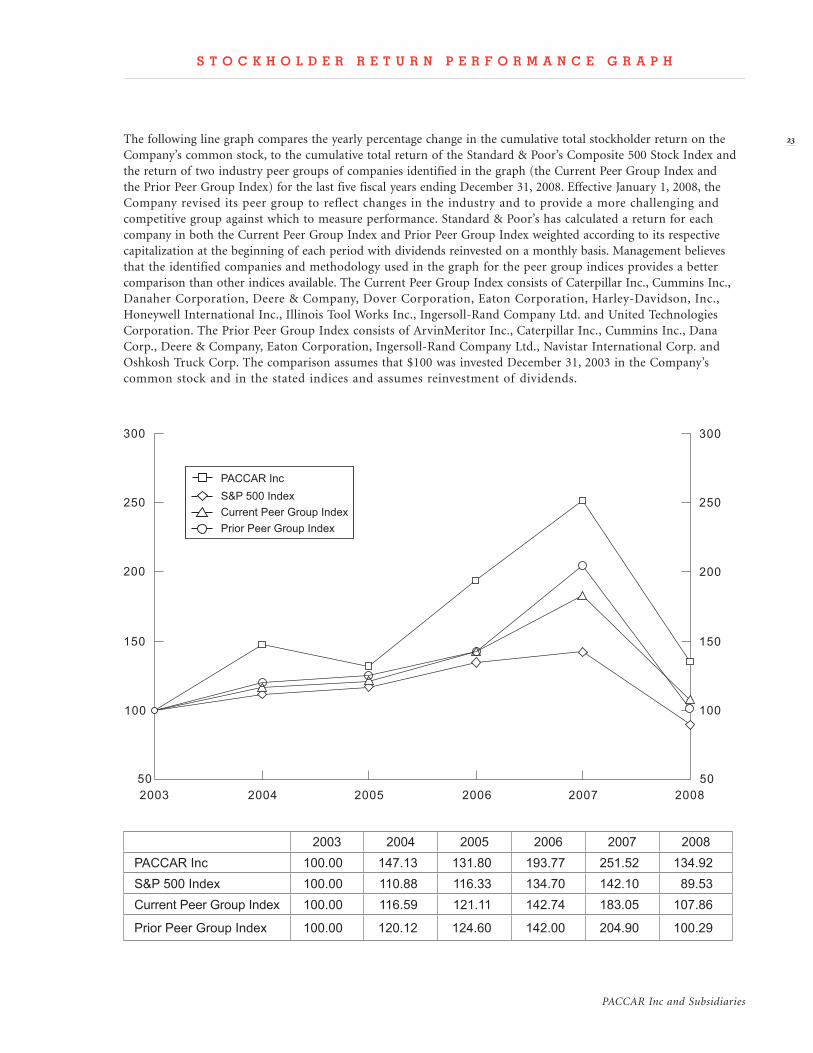

S T O C K H O L D E R R E T U R N P E R F O R M A N C E G R A P H

The following line graph compares the yearly percentage change in the cumulative total stockholder return on the Company’s common stock, to the cumulative total return of the Standard & Poor’s Composite 500 Stock Index and the return of two industry peer groups of companies identified in the graph (the Current Peer Group Index and the Prior Peer Group Index) for the last five fiscal years ending December 31, 2008. Effective January 1, 2008, the Company revised its peer group to reflect changes in the industry and to provide a more challenging and competitive group against which to measure performance. Standard & Poor’s has calculated a return for each company in both the Current Peer Group Index and Prior Peer Group Index weighted according to its respective capitalization at the beginning of each period with dividends reinvested on a monthly basis. Management believes that the identified companies and methodology used in the graph for the peer group indices provides a better comparison than other indices available. The Current Peer Group Index consists of Caterpillar Inc., Cummins Inc., Danaher Corporation, Deere & Company, Dover Corporation, Eaton Corporation, Harley-Davidson, Inc., Honeywell International Inc., Illinois Tool Works Inc., Ingersoll-Rand Company Ltd. and United Technologies Corporation. The Prior Peer Group Index consists of ArvinMeritor Inc., Caterpillar Inc., Cummins Inc., Dana Corp., Deere & Company, Eaton Corporation, Ingersoll-Rand Company Ltd., Navistar International Corp. and Oshkosh Truck Corp. The comparison assumes that $100 was invested December 31, 2003 in the Company’s common stock and in the stated indices and assumes reinvestment of dividends.

100

2003 2004 2005 2006 2007 2008

150

200

50 50

100

150

200

250

PACCAR Inc

S&P 500 Index

Current Peer Group Index

300300

Prior Peer Group Index

250

2003 2004 2005 2006 2007 2008PACCAR Inc 100.00 147.13 131.80 193.77 251.52 134.92S&P 500 Index 100.00 110.88 116.33 134.70 142.10 89.53Current Peer Group Index 100.00 116.59 121.11 142.74 183.05 107.86

Prior Peer Group Index 100.00 120.12 124.60 142.00 204.90 100.29

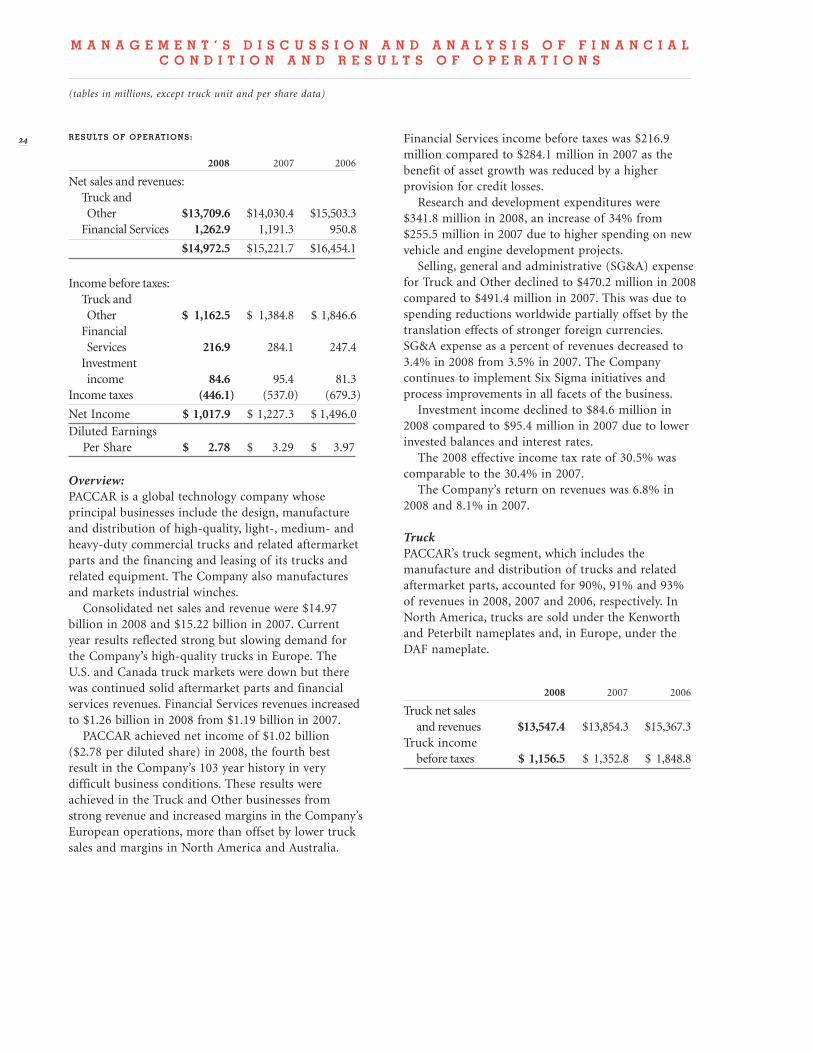

results of operations:

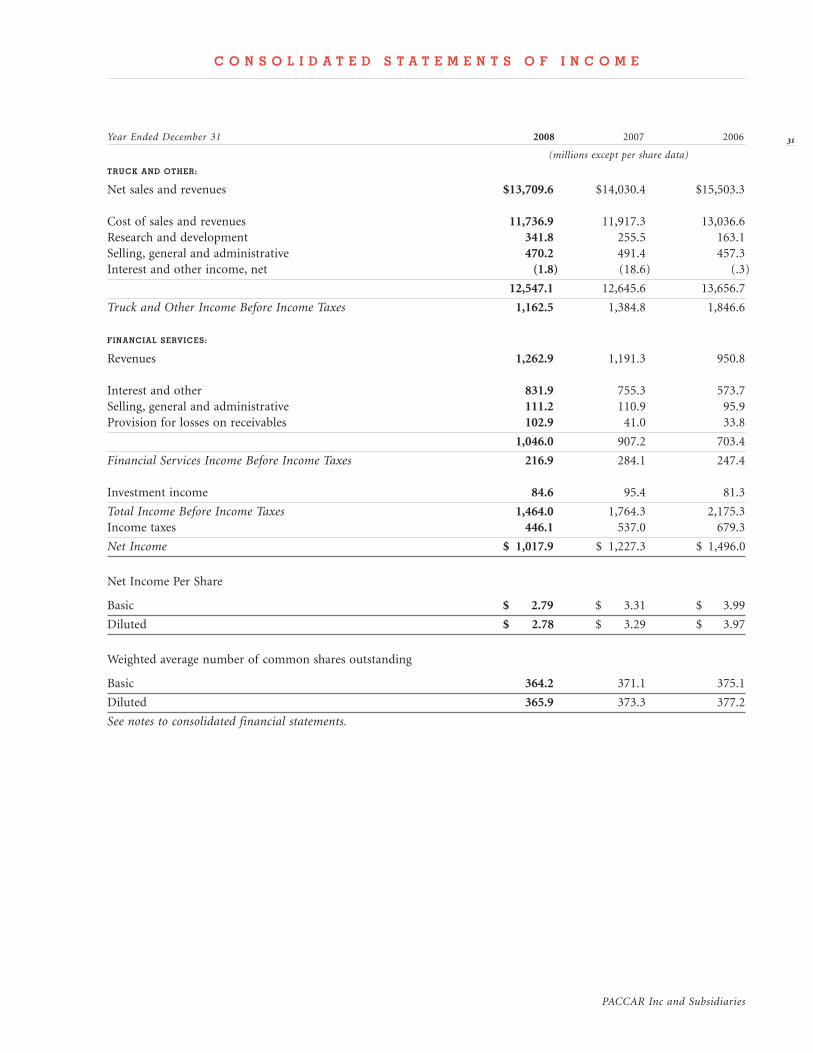

2008 2007 2006

Net sales and revenues: Truck and Other $13,709.6 $14,030.4 $15,503.3 Financial Services 1,262.9 1,191.3 950.8

$14,972.5 $15,221.7 $16,454.1

Income before taxes: Truck and Other $ 1,162.5 $ 1,384.8 $ 1,846.6 Financial Services 216.9 284.1 247.4 Investment income 84.6 95.4 81.3Income taxes (446.1) (537.0) (679.3)

Net Income $ 1,017.9 $ 1,227.3 $ 1,496.0

Diluted Earnings Per Share $ 2.78 $ 3.29 $ 3.97

Overview:PACCAR is a global technology company whose principal businesses include the design, manufacture and distribution of high-quality, light-, medium- and heavy-duty commercial trucks and related aftermarket parts and the financing and leasing of its trucks and related equipment. The Company also manufactures and markets industrial winches. Consolidated net sales and revenue were $14.97 billion in 2008 and $15.22 billion in 2007. Current year results reflected strong but slowing demand for the Company’s high-quality trucks in Europe. The U.S. and Canada truck markets were down but there was continued solid aftermarket parts and financial services revenues. Financial Services revenues increased to $1.26 billion in 2008 from $1.19 billion in 2007. PACCAR achieved net income of $1.02 billion ($2.78 per diluted share) in 2008, the fourth best result in the Company’s 103 year history in very difficult business conditions. These results were achieved in the Truck and Other businesses from strong revenue and increased margins in the Company’s European operations, more than offset by lower truck sales and margins in North America and Australia.

Financial Services income before taxes was $216.9 million compared to $284.1 million in 2007 as the benefit of asset growth was reduced by a higher provision for credit losses. Research and development expenditures were $341.8 million in 2008, an increase of 34% from $255.5 million in 2007 due to higher spending on new vehicle and engine development projects. Selling, general and administrative (SG&A) expense for Truck and Other declined to $470.2 million in 2008 compared to $491.4 million in 2007. This was due to spending reductions worldwide partially offset by the translation effects of stronger foreign currencies. SG&A expense as a percent of revenues decreased to 3.4% in 2008 from 3.5% in 2007. The Company continues to implement Six Sigma initiatives and process improvements in all facets of the business. Investment income declined to $84.6 million in 2008 compared to $95.4 million in 2007 due to lower invested balances and interest rates. The 2008 effective income tax rate of 30.5% was comparable to the 30.4% in 2007. The Company’s return on revenues was 6.8% in 2008 and 8.1% in 2007.

TruckPACCAR’s truck segment, which includes the manufacture and distribution of trucks and related aftermarket parts, accounted for 90%, 91% and 93% of revenues in 2008, 2007 and 2006, respectively. In North America, trucks are sold under the Kenworth and Peterbilt nameplates and, in Europe, under the DAF nameplate.

2008 2007 2006

Truck net sales and revenues $13,547.4 $13,854.3 $15,367.3Truck income before taxes $ 1,156.5 $ 1,352.8 $ 1,848.8

M a n a g e M e n t ’ s d i s c u s s i o n a n d a n a l y s i s o f f i n a n c i a l c o n d i t i o n a n d r e s u l t s o f o p e r a t i o n s

(tables in millions, except truck unit and per share data)

PACCAR Inc and Subsidiaries

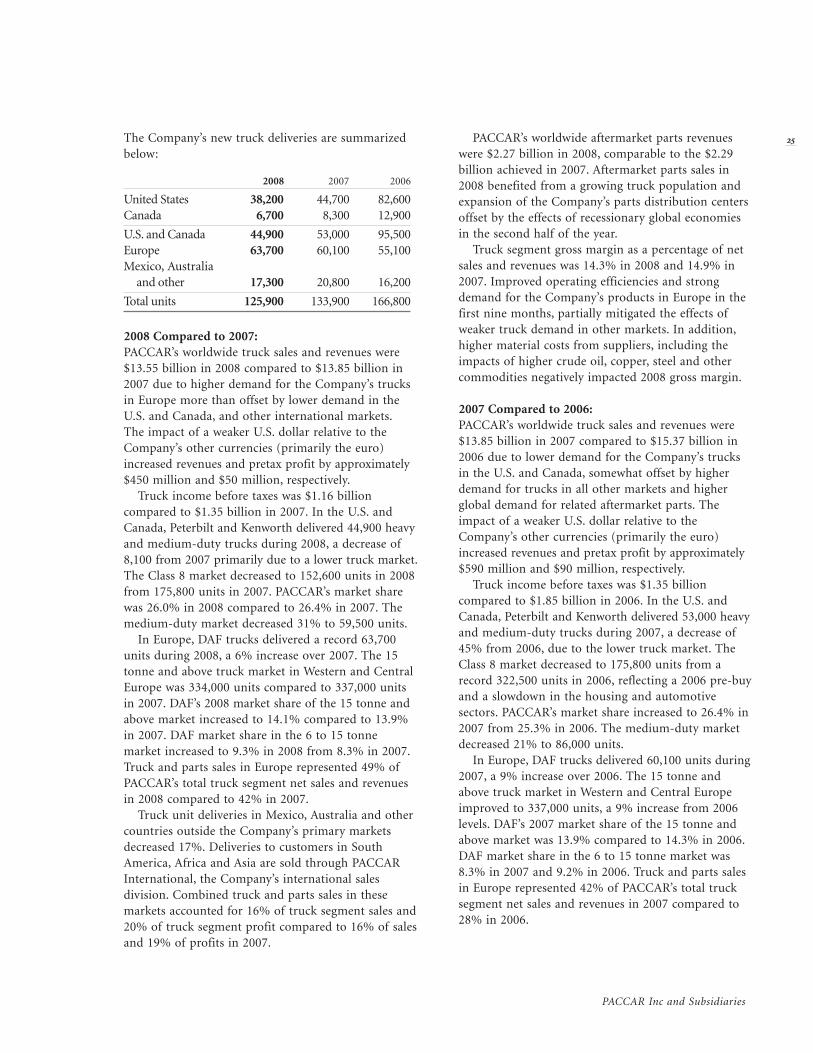

The Company’s new truck deliveries are summarized below:

2008 2007 2006

United States 38,200 44,700 82,600Canada 6,700 8,300 12,900

U.S. and Canada 44,900 53,000 95,500Europe 63,700 60,100 55,100Mexico, Australia and other 17,300 20,800 16,200

Total units 125,900 133,900 166,800

2008 Compared to 2007:PACCAR’s worldwide truck sales and revenues were $13.55 billion in 2008 compared to $13.85 billion in 2007 due to higher demand for the Company’s trucks in Europe more than offset by lower demand in the U.S. and Canada, and other international markets. The impact of a weaker U.S. dollar relative to the Company’s other currencies (primarily the euro) increased revenues and pretax profit by approximately $450 million and $50 million, respectively. Truck income before taxes was $1.16 billion compared to $1.35 billion in 2007. In the U.S. and Canada, Peterbilt and Kenworth delivered 44,900 heavy and medium-duty trucks during 2008, a decrease of 8,100 from 2007 primarily due to a lower truck market. The Class 8 market decreased to 152,600 units in 2008 from 175,800 units in 2007. PACCAR’s market share was 26.0% in 2008 compared to 26.4% in 2007. The medium-duty market decreased 31% to 59,500 units. In Europe, DAF trucks delivered a record 63,700 units during 2008, a 6% increase over 2007. The 15 tonne and above truck market in Western and Central Europe was 334,000 units compared to 337,000 units in 2007. DAF’s 2008 market share of the 15 tonne and above market increased to 14.1% compared to 13.9% in 2007. DAF market share in the 6 to 15 tonne market increased to 9.3% in 2008 from 8.3% in 2007. Truck and parts sales in Europe represented 49% of PACCAR’s total truck segment net sales and revenues in 2008 compared to 42% in 2007. Truck unit deliveries in Mexico, Australia and other countries outside the Company’s primary markets decreased 17%. Deliveries to customers in South America, Africa and Asia are sold through PACCAR International, the Company’s international sales division. Combined truck and parts sales in these markets accounted for 16% of truck segment sales and 20% of truck segment profit compared to 16% of sales and 19% of profits in 2007.

PACCAR’s worldwide aftermarket parts revenues were $2.27 billion in 2008, comparable to the $2.29 billion achieved in 2007. Aftermarket parts sales in 2008 benefited from a growing truck population and expansion of the Company’s parts distribution centers offset by the effects of recessionary global economies in the second half of the year. Truck segment gross margin as a percentage of net sales and revenues was 14.3% in 2008 and 14.9% in 2007. Improved operating efficiencies and strong demand for the Company’s products in Europe in the first nine months, partially mitigated the effects of weaker truck demand in other markets. In addition, higher material costs from suppliers, including the impacts of higher crude oil, copper, steel and other commodities negatively impacted 2008 gross margin.

2007 Compared to 2006:PACCAR’s worldwide truck sales and revenues were $13.85 billion in 2007 compared to $15.37 billion in 2006 due to lower demand for the Company’s trucks in the U.S. and Canada, somewhat offset by higher demand for trucks in all other markets and higher global demand for related aftermarket parts. The impact of a weaker U.S. dollar relative to the Company’s other currencies (primarily the euro) increased revenues and pretax profit by approximately $590 million and $90 million, respectively. Truck income before taxes was $1.35 billion compared to $1.85 billion in 2006. In the U.S. and Canada, Peterbilt and Kenworth delivered 53,000 heavy and medium-duty trucks during 2007, a decrease of 45% from 2006, due to the lower truck market. The Class 8 market decreased to 175,800 units from a record 322,500 units in 2006, reflecting a 2006 pre-buy and a slowdown in the housing and automotive sectors. PACCAR’s market share increased to 26.4% in 2007 from 25.3% in 2006. The medium-duty market decreased 21% to 86,000 units. In Europe, DAF trucks delivered 60,100 units during 2007, a 9% increase over 2006. The 15 tonne and above truck market in Western and Central Europe improved to 337,000 units, a 9% increase from 2006 levels. DAF’s 2007 market share of the 15 tonne and above market was 13.9% compared to 14.3% in 2006. DAF market share in the 6 to 15 tonne market was 8.3% in 2007 and 9.2% in 2006. Truck and parts sales in Europe represented 42% of PACCAR’s total truck segment net sales and revenues in 2007 compared to 28% in 2006.

Truck unit deliveries in Mexico, Australia and other countries outside the Company’s primary markets increased 28%. Combined truck and parts sales in these markets accounted for 16% of truck segment sales and 19% of truck segment profit, an increase from 10% of sales and 9% of profits in 2006. PACCAR’s worldwide aftermarket parts revenues were $2.29 billion in 2007, an increase of 18% compared to $1.94 billion in 2006. Aftermarket parts sales increased in all major markets from a growing truck population, expansion of parts distribution centers and focused sales efforts. Truck segment gross margin as a percentage of net sales and revenues was 14.9% in 2007 and 15.7% in 2006. Improved operating efficiencies and strong demand for the Company’s products outside the U.S. and Canada were dampened by a weak truck market in the U.S. and Canada. Higher material costs negatively impacted truck gross margins.

Truck OutlookWorldwide recessionary economic conditions are currently forecast to dampen demand for heavy-duty trucks for 2009. In North America, industry retail sales are expected to be 130,000–170,000 trucks. Western and Central European heavy-duty registrations for 2009 are projected to decline between 30% to 40% to 200,000–240,000 units. International markets are also expected to be weaker in 2009.

Financial ServicesThe Financial Services segment, which includes wholly owned subsidiaries in the U.S., Canada, Mexico, Europe and Australia, derives its earnings primarily from financing or leasing PACCAR products.

2008 2007 2006

Financial Services: Average earning assets $10,369.0 $10,158.0 $8,746.0 Revenues 1,262.9 1,191.3 950.8 Income before taxes 216.9 284.1 247.4

2008 Compared to 2007:PACCAR Financial Services (PFS) revenues increased 6% to $1.26 billion due to higher earning assets in all markets outside the U.S. and Canada and higher average finance yields. New business volume was $3.35 billion in 2008 compared to $3.94 billion in 2007. The

decrease in volume was due to fewer new trucks sold and a lower finance share of new truck sales. PFS provided loan and lease financing for 28% of PACCAR new trucks delivered in 2008 compared to 29% in 2007. Income before taxes was $216.9 million compared to $284.1 million in 2007 primarily due to a higher provision for losses on receivables. Net portfolio charge-offs were $104.8 million compared to $25.8 million in 2007 due to higher charge-offs related to recessionary conditions in the U.S. and Canada and to a lesser extent Europe. At December 31, 2008, the earning asset portfolio quality overall was solid with the percentage of accounts 30+ days past-due at 3.3%, although up from 2.0% at the end of 2007, primarily due to the difficult economy worldwide.

2007 Compared to 2006:PACCAR Financial Services (PFS) revenues increased 25% to $1.19 billion due to higher earning assets worldwide and higher interest rates. New business volume was $3.94 billion in 2007 compared to $4.24 billion in 2006. Income before taxes increased 15% to a record $284.1 million from $247.4 million in 2006. The improvement was primarily due to higher finance gross profit, partly offset by an increase in selling, general and administrative expenses to support business growth and a higher provision for losses on receivables. The increase in finance gross profit was due to higher asset levels and interest rates, offset partly by a higher cost of debt. Net portfolio charge-offs were $25.8 million compared to $13.9 million in 2006 due to higher charge-offs in the U.S. and Canada. At December 31, 2007, the percentage of accounts 30+ days past-due was 2.0%, up from 1.1% at the end of 2006, primarily due to higher past dues in the U.S. and Canada.

Financial Services OutlookFinancial Services segment results are principally dependent on the generation of loans and leases and the related spread between the yields on loans and leases and borrowing costs and the level of credit losses. A reduction in average earning assets is expected as lower PACCAR truck sales will likely result in lower new business volume in 2009.

PACCAR Inc and Subsidiaries

The segment continues to be exposed to the risk that economic weakness around the world may continue to exert pressure on the profit margins of truck operators and result in higher past-due accounts and repossessions.

Other BusinessIncluded in Truck and Other is the Company’s winch manufacturing business. Sales from this business represent approximately 1% of net sales for 2008, 2007 and 2006.

liquidity and capital resources:

December 31

2008 2007 2006

Cash and cash equivalents $1,955.2 $1,858.1 $1,852.5Marketable debt securities 175.4 778.5 821.7

$2,130.6 $2,636.6 $2,674.2

The Company’s total cash and marketable debt securities decreased $506.0 million in 2008. Cash provided by operations of $1,304.9 million was used primarily to pay dividends of $629.2 million, make capital investments totaling $462.8 million and repurchase PACCAR stock for $230.6 million. Cash required to originate new loans and leases was funded by repayments of existing loans and leases as well as Financial Services borrowings. The Company has line of credit arrangements of $3.51 billion. The unused portion of these credit arrangements was $3.26 billion at December 31, 2008.Included in these arrangements are $3.0 billion of bank facilities, of which $2.0 billion matures in June 2009 and $1.0 billion matures in 2012. PACCAR intends to replace these credit facilities as they expire with facilities of similar amounts. The bank facilities are primarily maintained to provide backup liquidity on commercial paper borrowings of the financial services companies. There were no borrowings outstanding under these facilities at December 31, 2008. In November 2008, PACCAR Inc filed a shelf registration under the Securities Act of 1933. In February 2009, the Company issued $750 million of fixed rate medium-term notes under this registration. The registration expires in 2011 and does not limit the principal amount of debt securities that may be issued during the period. The Company believes its strong liquidity position and AA- investment grade credit rating will continue to provide financial stability and access to capital markets at competitive interest rates.

In October 2007, PACCAR’s Board of Directors approved the repurchase of $300 million of the Company’s common stock. Through December 31, 2008, $292 million of shares have been repurchased. In July 2008, PACCAR’s Board of Directors approved the repurchase of an additional $300 million of the Company’s common stock. No shares have been repurchased pursuant to the July 2008 authorization.

Truck and OtherThe Company provides funding for working capital, capital expenditures, research and development, dividends, stock repurchases and other business initiatives and commitments primarily from cash provided by operations. Management expects this method of funding to continue in the future. Long-term debt totaled $19.3 million as of December 31, 2008. Expenditures for property, plant and equipment in 2008 totaled a record $462.8 million compared to $425.7 million in 2007. Major capital projects included the continuation of construction of an engine production facility in Mississippi and completion of construction of a new parts distribution center in Hungary. In addition, the Company made significant investments related to new product development and plant capacity. Over the last ten years, the Company’s combined investments in worldwide capital projects and research and development totaled $3.82 billion which have significantly increased capacity, efficiency and quality of the Company’s premier products. The Company has reduced its planned capital expenditures to reflect current economic conditions. As a result, capital spending in 2009 is expected to be approximately $150 to $200 million. Spending on research and development in 2009 is expected to be approximately $200 to $250 million. PACCAR will continue to focus on engine development, new product programs and manufacturing efficiency improvements.

Financial ServicesThe Company funds its financial services activities primarily from collections on existing finance receivables and borrowings in the capital markets. An additional source of funds is loans from other PACCAR companies. PACCAR’s strong cash position and credit ratings enabled PFS to meet its funding requirements despite a decline in liquidity in the debt and capital markets since the second half of 2007. The primary sources of borrowings in the capital markets are commercial paper and medium-term notes issued in the public markets and, to a lesser extent, bank loans. The majority of the medium-term notes are issued by PACCAR’s largest financial services subsidiary, PACCAR Financial Corp. (PFC). PFC filed a shelf registration under the Securities Act of 1933 in November 2006. The registration expires in November 2009 and does not limit the principal amount of debt securities that may be issued during the period. PFC participates in the Commercial Paper Funding Facility offered by the Federal Reserve Bank of New York. Under this funding facility, PFC may issue 90-day commercial paper through October 30, 2009. The total amount of commercial paper that PFC may have outstanding under this program is $1.46 billion, of which, $.74 billion was outstanding at December 31, 2008. In June 2008, PACCAR’s European finance subsidiary, PACCAR Financial Europe, renewed and increased the registration of a €1.5 billion medium-term note program with the London Stock Exchange. On December 31, 2008, €402 million remained available for issuance. This program is renewable annually through the filing of a new prospectus. In June 2008, PACCAR Mexico registered a 7.0 billion peso medium-term note program with the Comision Nacional Bancaria y de Valores. The registration expires in 2012 and at December 31, 2008, 6.1 billion pesos remained available for issuance. To reduce exposure to fluctuations in interest rates, the Financial Services companies pursue a policy of structuring borrowings with interest-rate characteristics similar to the assets being funded. As part of this policy, the companies use interest-rate contracts. The permitted types of interest-rate contracts and transaction limits have been established by the Company’s senior management, who receive periodic reports on the contract amounts outstanding and counterparty’s involved.

PACCAR believes its Financial Services companies will be able to continue funding receivables, servicing debt and paying dividends through internally generated funds, access to public and private debt markets and lines of credit.

Commitments The following summarizes the Company’s contractual cash commitments at December 31, 2008:

Maturity

Within More than One Year One Year Total

Borrowings $5,558.2 $1,909.1 $7,467.3Operating leases 25.2 41.2 66.4Purchase obligations 164.8 155.6 320.4Other obligations 5.8 29.4 35.2

Total $5,754.0 $2,135.3 $7,889.3

The Company had $7.89 billion of cash commitments, substantially all of which mature within three years. Of the total cash commitments for borrowings, $7.47 billion were related to the Financial Services segment. As described in Note J of the consolidated financial statements, borrowings consist primarily of term notes and commercial paper issued by the Financial Services segment. The Company expects to fund its maturing Financial Services debt obligations principally from funds provided by collections from customers on loans and lease contracts, as well as from the proceeds of commercial paper and medium-term note borrowings. Purchase obligations are the Company’s contractual commitment to acquire future production inventory and capital equipment. Other obligations include deferred cash compensation. The Company’s other commitments include the following at December 31, 2008:

Commitment Expiration

Within More than One Year One Year Total

Letters of credit $ 34.2 $ 1.5 $ 35.7Loan and lease commitments 105.1 105.1Equipment acquisition commitments 53.4 53.4Residual value guarantees 67.3 198.7 266.0

Total $206.6 $253.6 $460.2

PACCAR Inc and Subsidiaries

Loan and lease commitments are for funding new retail loan and lease contracts. Equipment acquisition commitments require the Company, under specified circumstances, to purchase equipment. Residual value guarantees represent the Company’s commitment to acquire trucks at a guaranteed value if the customer decides to return the truck at a specified date in the future.

impact of environmental matters:

The Company, its competitors and industry in general are subject to various domestic and foreign requirements relating to the environment. The Company believes its policies, practices and procedures are designed to prevent unreasonable risk of environmental damage and that its handling, use and disposal of hazardous or toxic substances have been in accordance with environmental laws and regulations enacted at the time such use and disposal occurred. Expenditures related to environmental activities in 2008, 2007 and 2006 were immaterial. The Company is involved in various stages of investi gations and cleanup actions in different countries related to environmental matters. In certain of these matters, the Company has been designated as a “potentially responsible party” by domestic and foreign environmental agencies. The Company has provided an accrual for the estimated costs to investigate and complete cleanup actions where it is probable that the Company will incur such costs in the future. Management expects that these matters will not have a significant effect on the Company’s consolidated cash flow, liquidity or financial condition.

critical accounting policies:

In the preparation of the Company’s financial statements, in accordance with U.S. generally accepted accounting principles, management uses estimates and makes judgments and assumptions that affect asset and liability values and the amounts reported as income and expense during the periods presented. The following are accounting policies which, in the opinion of management, are particularly sensitive and which, if actual results are different from estimates used by management, may have a material impact on the financial statements.

Operating LeasesThe accounting for trucks sold pursuant to agreements accounted for as operating leases is discussed in Notes A and G of the consolidated financial statements. In deter mining its estimate of the residual value of such vehicles, the Company considers the length of the lease term, the truck model, the expected usage of the truck and anticipated market demand. If the sales price of the trucks at the end of the term of the agreement differs from the Company’s estimate, a gain or loss will result. The Company believes its residual-setting policies are appropriate; however, future market conditions, changes in government regulations and other factors outside the Company’s control could impact the ultimate sales price of trucks returned under these contracts. Residual values are reviewed regularly and adjusted if market conditions warrant.

Allowance for Credit LossesThe Company determines the allowance for credit losses on financial services receivables based on a combination of historical information and current market conditions. This determination is dependent on estimates, including assumptions regarding the likelihood of collecting current and past-due accounts, repossession rates and the recovery rate on the underlying collateral based on used truck values and other pledged collateral or recourse. The Company believes its reserve-setting policies adequately take into account the known risks inherent in the financial services portfolio. If there are significant variations in the actual results from those estimates, the provision for credit losses and operating earnings may be materially impacted.

Product WarrantyThe expenses related to product warranty are estimated and recorded at the time products are sold based on historical and current data and reasonable expectations for the future regarding the frequency and cost of warranty claims. Management believes that the warranty reserve is appropriate and takes actions to minimize warranty costs through quality-improvement programs; however, actual claims incurred could materially differ from the estimated amounts and require adjustments to the reserve.

9

30 Pension and Other Postretirement BenefitsThe Company’s accounting for employee pension and other postretirement benefit costs and obligations is based on management assumptions about the future used by actuaries to estimate net costs and liabilities. These assumptions include discount rates, long-term rates of return on plan assets, health care cost trends, inflation rates, retirement rates, mortality rates and other factors. Management bases these assumptions on historical results, the current environment and reasonable estimates of future events. The discount rate for each plan is based on market interest rates of high-quality corporate bonds with a maturity profile that matches the timing of the projected benefit payments of the plans. Changes in the discount rate affect the valuation of the plan benefits obligation and funded status of the plans. The long-term rate of return on plan assets is based on projected returns for each asset class and relative weighting of those asset classes in the plans. Actual results that differ from these assumptions are accumulated and amortized into expense over future periods. While management believes the assumptions used are appropriate, significant differences in actual experience or significant changes in assumptions would affect pension and other postretirement benefit costs and obligations and the balance sheet funded status of the plans.