Embed Size (px)

Citation preview

PA RESOURCES

Annual Report 2015

PA RESOURCES ANNUAL REPORT 2015 2

CONTENT BOARD OF DIRECTORS´ REPORT 2015 3

Company development 3

The group´s business activities 3

Key events by region 5

Financial summary 6

Risks and uncertainties 9

Subsequent events 11

Board of Directors 12

Proposed distribution of earnings 12

FINANCIAL REPORTS 13

Group

5 year summary 13

Key ratio definition 13

Income statement 14

Statement of comprehensive income 14

Statement of financial position (Non-going concern) 15

Statement of financial position (Going concern) 16

Statement of changes in equity 17

Statement of cash flow statement 18

Parent company

Income statement 19

Statement of comprehensive income 19

Statement of financial position (Non-going concern) 20

Statement of financial position (Going concern) 21

Statement of changes in equity 22

Statement of cash flow statement 23

Group and Parent company

Notes 24

BOARD ASSURANCE 62

AUDITOR´S REPORT 63

PA RESOURCES ANNUAL REPORT 2015 3

BOARD OF DIRECTORS` REPORT 2015 PA Resources AB (publ), corporate identity number 556488-2180

COMPANY DEVELOPMENT

Following the failure of the Azurite field in the Republic of Congo to deliver the expected production

levels during 2011-2013 PA Resources has been burdened with an unsustainably high level of debt.

Subsequent capital raises and refinancing have been aimed towards reducing the debt burden and

supplying the necessary capital for the company to invest in its development portfolio for future

production and cash flows. In 2013 and 2014 the company entered into farm-out agreements for its

key development assets in order to raise cash and reduce its investment needs. The drop in oil price,

which commenced during the summer of 2014, together with Enquest’s reversal of the Tunisia farm-

out in January 2015 resulted in a situation where the company was unable to service its debts.

Between October 2014 and March 2015 PA Resources negotiated a potential refinancing plan

together with its major creditors and shareholders. Following lack of progress in the discussions the

company filed for corporate reorganisation on the 26 March 2015. The reorganisation process is

described in more detail below. In parallel with the reorganisation process the board of directors

initiated a strategic review process which was completed in November 2015 also described in more

detail below. Following the corporate reorganisation and the strategic review the company still

stands without long-term financing and has decided to sell its assets. As a result the board of

directors has concluded that the company’s financial statements can no longer be prepared under

the assumption of a going concern.

THE GROUP’S BUSINESS ACTIVITIES

Production and Sales

During the year, oil was produced from five fields of which three were located in Tunisia – where the

Didon field is the largest – and the Aseng and Diega fields in Equatorial Guinea. The fields in

Equatorial Guinea contributed to the production during the first quarter after which the ownership

was transferred to Gunvor and deconsolidated from PA Resources (see Enforcement of RBL-security).

Total production of oil amounted to 613,300 barrels (1,147,000) which is an average of 1,700 barrels

per day on a working interest basis (3,100). In total 640,500 barrels of oil (964,400) was sold during

2015 to an average price of USD 53 per barrel (96).

Loss of control subsidiary

On 7 April 2015 Gunvor exercised its security under the terms of the RBL-loan to take over the shares

in Osborne Resources Ltd. Osborne Resources Ltd held PA Resources interest in Block I in Equatorial

Guinea including the producing fields Aseng and Alen. Following the transaction PA Resources no

longer has any interests in Equatorial Guinea. The transaction resulted in a net capital gain of SEK 285

million. On the same day as Gunvor exercised its security, Gunvor also petitioned for bankruptcy in

PA Resources AB. Gunvor recalled the petition on 15 April 2015.

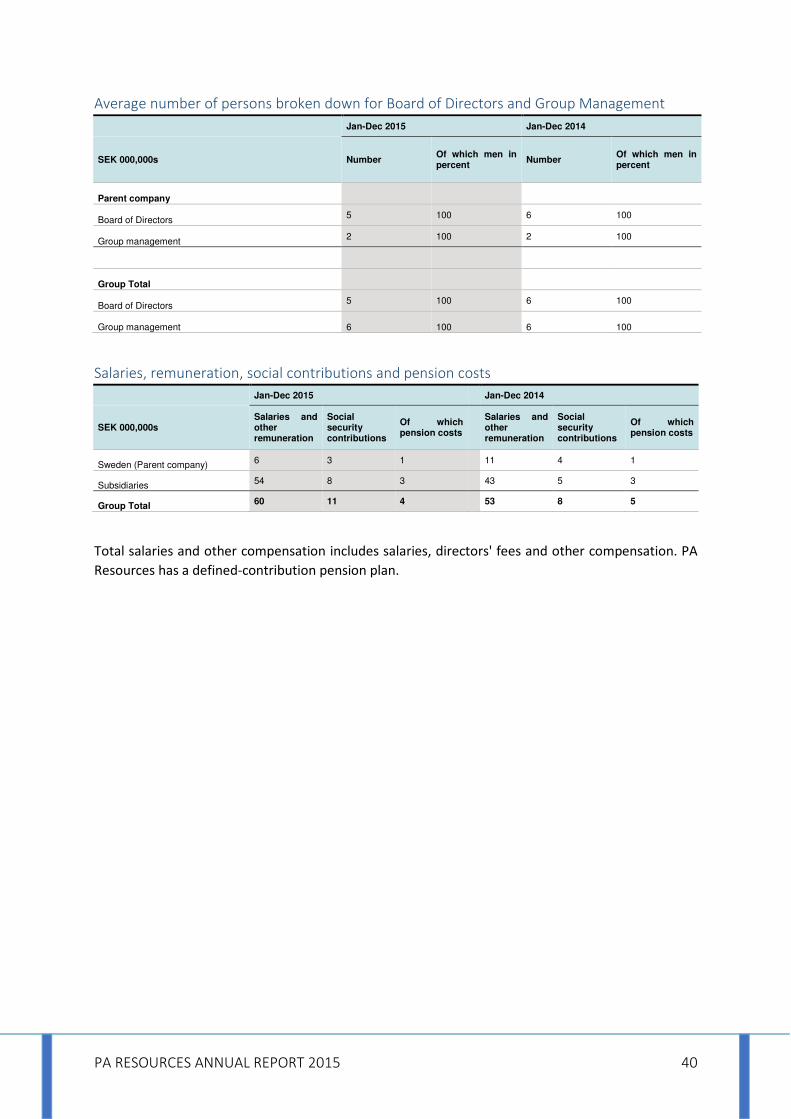

Employees

The average number of employees was 107 (121), of these 90 (99) were men and 17 (22) were

women. See more in Note 10, Employees, salaries and other remuneration.

Remuneration to group management

Remuneration of the CEO and other group management is comprised of fixed salary, variable

remuneration, other benefits and pensions as detailed in Note 11, Remuneration and other benefits;

PA RESOURCES ANNUAL REPORT 2015 4

Board of Directors and Group Management of the Parent Company. The guidelines for remuneration

of management were adopted by the 2015 Annual General Meeting.

Disputes

At the time of the annual report there are no material disputes between PA Resources and other

parties.

Delistings

PA Resources AB’s share has been listed on the Nasdaq Stockholm exchange since 2006. As part of

the agreements with the major creditors signed under the corporate reorganisation the company

agreed to seek a delisting when appropriate. On the 23 November 2015 the application for delisting

was filed and the last day for trading was 15 January 2016. As an event after the closing date PA

Resources delisted its SEK denominated bond also listed in the Nasdaq Stockholm exchange. Last day

of trading was 1 February 2016 and application to delist was submitted 25 January 2016. For more

information see Note 28, Significant events after the closing date.

Corporate Reorganisation

The 26 March 2015 PA Resources AB filed for corporate reorganisation at the Stockholm District

Court in accordance with the company reorganisation act (1996:764). The application was approved

the 27 march 2015. Lars Söderqvist, lawyer at Hökerberg & Söderqvist KB was appointed as

administrator of the reorganisation by the court. On 15 April 2015 a creditors meeting was held

following which the court allowed the reorganisation to continue until 29 June 2015. On 25 June

2015 PA Resources AB filed a petition to extend the corporate reorganisation. On 9 July the

Stockholm District approved the petition extending the corporate reorganisation by a further three

months until 28 September 2015. On 9 September 2015 PA Resources published the reorganisation

plan prepared by the company and the administrator. At the same time a request for composition

proceedings was handed in to the Stockholm District Court which subsequently set the date to the 2

October 2015. On the 29 September 2015 the holders of both the SEK- and NOK-denominated bonds

voted to adopt the proposed composition plan subject to subsequent approval by the court. On 2

October 2015 a qualified majority of creditors voted for the proposed composition plan which was

also adopted by the court. PA Resources also submitted a request for termination of the

reorganisation which was approved and as the composition became final and binding on the 24

October 2015 the corporate reorganisation was terminated.

The composition plan, approved by the creditors and adopted by the Stockholm District Court, split

the creditors into three groups. The first group are the individual creditors with claims below SEK

100,000 which are to receive full payment of their claims by the 26 March 2016. The second group;

creditors with claims exceeding SEK 100,000 and without agreements with the company, are entitled

to repayment of SEK 100,000 and 25% of their claim exceeding SEK 100,000 by the 26 March 2016.

The total amount due to these two groups of creditors amounts to approximately SEK 3 million. The

third group consists of a number of major creditors including the bondholders, Gunvor Group and

Murphy Oil Corporation. These creditors have, through bilateral agreements with the company,

agreed to receive repayment of their claims over a longer period of time from the company’s

available cash flow as defined by the composition plan. Any outstanding claims on the company still

not repaid by the 27 December 2017 and exceeding the book value of the company’s assets at that

time, will be converted to equity through an offset issue. The creditors with outstanding claims at

this time will, irrespective of the value of the claims, receive 95% of the company’s share capital after

the conversion.

PA RESOURCES ANNUAL REPORT 2015 5

Strategic Review Process

During the second quarter the board of directors initiated a review process to explore the company’s

strategic options going forward. The process included evaluating three main options, securing long

term funding of the group, exploring the possibility of a corporate transaction/M&A and as a third

option the divestment of business areas or individual assets. The review process was managed by an

internal project office which prepared the necessary marketing documents and materials. The review

was finalised in November 2015 concluding that a sale of the company’s assets was the only viable

alternative and the board instructed the management to proceed with a sale. See more under

Subsequent events.

Financial statements prepared as a non-going concern

The company has since the middle of 2014 been working to secure long-term financing for the

company’s operations and development projects. Following the corporate reorganisation and the

strategic review the company still stands without long-term financing and has decided to sell its

assets. As a result the board of directors has concluded that the company’s financial statements can

no longer be prepared under the assumption of a going concern. The consequences of the changes in

accounting principles are outlined in Note 2, Accounting principles etc.

KEY EVENTS BY REGION

West Africa

Block I, including PA Resources interest in the Aseng and Alen producing fields as well as the Diega

discovery, in Equatorial Guinea was deconsolidated as per 31 March 2015 following Gunvor Group’s

decision to enforce its security under the terms of the Reserve Based Lending (RBL) facility.

Preparations were made for the drilling of the Baobab Marine-1 exploration well on the Mer

Profonde Sud licence in the Republic of Congo (Brazzaville). Drilling took place during the first quarter

of 2016.

North Africa

A cost cutting program was implemented on the Didon field reducing operating expenditure by over

20% compared to 2014.

A revised development plan for the Zarat field was submitted to La Direction de L’Energie (DGE) on

24 July 2015. The Development plan was the result of two years of work conducted by a joint PA

Resources and L’Enterprise Tunisienne d’Activites Petrolieres (ETAP) team.

The infrastructure upgrade program on the DST fields continued and included a well work over on

the Douleb field, the conversion of a producer to an injector well.

Force Majeur was declared on the Makhtar and Jelma exploration licenses in July 2015 as a result of

the adjacent mountain areas being declared a military zone.

The North Sea

On the 12/06 license in Denmark the drilling of the Lille John-2 appraisal well was completed with oil

encountered in the Miocene sandstone reservoir as expected. A drill stem test flowed at rates of up

to 1,400 barrels per day of 35○ API oil. The results of the well were evaluated and incorporated in an

updated development concept including both the Lille John and Border Tuck discoveries under the

name “Robin Hood”. The license partnership is targeting a 2016 declaration of commerciality in line

with license requirements.

PA RESOURCES ANNUAL REPORT 2015 6

FINANCIAL SUMMARY

One-off items

There have been a number of significant transactions affecting PA Resources in 2015, thus the 2015

year-end report include several non-recurring and non-cash, one-off items. These items are

described below and in Note 4, Segment information.

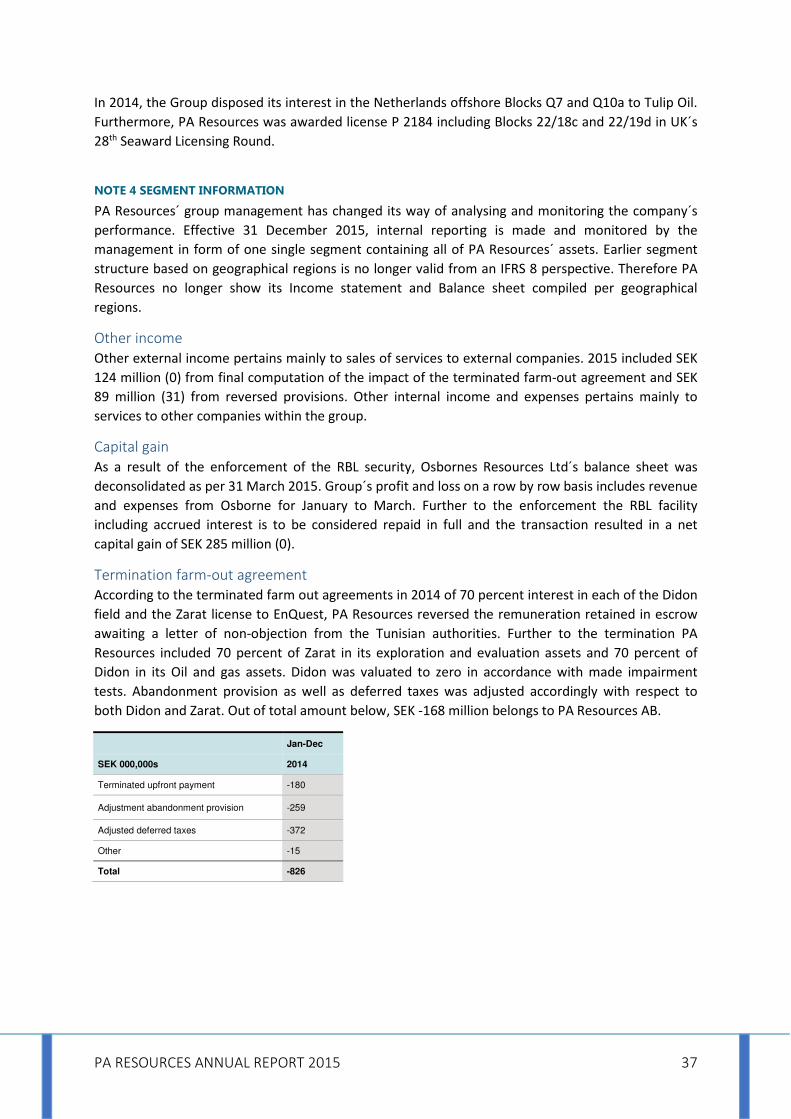

Jan-Dec

SEK 000,000s 2015 Accounted for in Income Statement

Profit for the period 779

Whereof one-off items

Final computation terminated farm out agreement 124 Other income

Reversed provisions 89 Other income

Enforcement of the RBL security 285 Capital gain

Market valuation E&E and O&G assets -1,969 Impairment losses

Exchange losses (net) -21 Other financial items (negative)

Expensed interest-bearing debt -42 Other financial items (negative)

Recognised fair value in connection with the composition plan 2,061 Other financial items (positive)

Revaluation tax provision 38 Income tax

Reversed deferred taxes in connection with market valuation of E&E and O&G assets

444 Income tax

Profit for the period excluding one-off items -230

Revenue and gross profit

Revenue amounted to SEK 242 million (603) and decreased as result of the deconsolidation of Aseng

and Alen, and lower sales price compared with the corresponding period a year ago. Revenue was

positively impacted by currency effects from the strengthened USD. Production costs including direct

production taxes of SEK -6 million (-10) amounted to SEK -184 million (-187) and decreased mainly as

a result of the RBL enforcement counteracted by the terminated farm-out agreement. Depletion of

oil and gas assets amounted to SEK -40 million (-195) and decreased mainly as a result of the book

values relating to the Didon field being impaired in the fourth quarter 2014 and of the RBL

enforcement. Gross profit amounted to SEK 17 million (222).

EBITDA and operating profit

EBITDA amounted to SEK 425 million (-481) and the EBITDA margin was 176 (-80) percent. EBITDA

was positively impacted by other income of SEK 222 million (46) mainly effects from provisions and

final computation of the impact of the terminated farm-out agreement. EBITDA was also positively

impacted by a capital gain of SEK 285 million (0) from enforcement of the RBL security by Gunvor

Group. Impairment losses amounted to SEK -1,969 million (-1,991) and is a result from assessed

market valuation of PA Resources exploration and evaluation assets and its oil and gas properties

including abandonment costs. For more information, see note 14, Exploration and evaluation assets

and Oil and gas properties. Operating profit amounted to SEK -1,590 million (-2,667).

PA RESOURCES ANNUAL REPORT 2015 7

Net financial items, tax and profit for the period

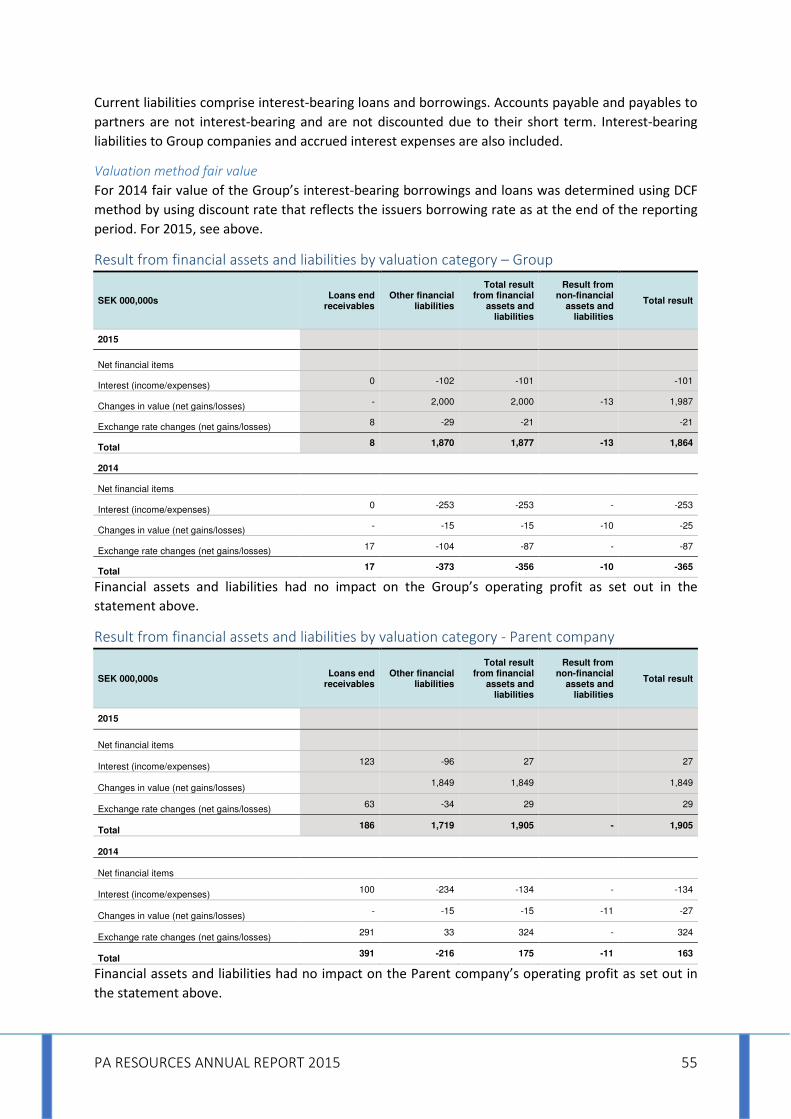

Net financial items for the Group amounted to SEK 1,864 million (-365) for the period. Interest

expense was SEK -102 million (-256). Other financial expenses amounted to SEK -74 million (-25) and

was negatively affected by expensed interest-bearing debt of SEK -42 million (0). Currency effects on

net financial items amounted to SEK -21 million (-87). Other financial income amounted to SEK 2,061

million (0) and is entirely attributable to the recognised fair value of interest-bearing loans and

borrowings and other liabilities in connection with the composition plan. Adjusted for currency

effects and other financial income, net financial items amounted to SEK -175 million (-278). Reported

tax amounted to SEK 504 million (74) and paid tax amounted to SEK -18 million (-165). Reported tax

including a reversal of deferred tax liabilities amounted to SEK 444 million in connection with market

valuation of Exploration and evaluation assets as well as Oil and gas assets. 2014 included SEK 137

million from reversal of deferred taxes with respect to impaired fixed assets. Profit for the period

amounted to SEK 779 million (-2,957).

Enforcement of RBL security

As per 7 April Gunvor Group, PA Resources´ largest creditor and shareholder demanded repayment

of amounts due under the RBL facility. PA Resources also received notice that Gunvor Group had

taken action to enforce its security under the RBL, shares in its wholly-owned subsidiary, Osborne

Resources Ltd. Osborne owns interests in Equatorial Guinea, the producing Aseng and Alen fields,

and the Block I exploration interest. The effect of this enforcement action is that Osborne is no

longer a subsidiary of PA Resources and has become a subsidiary of Gunvor Group.

As a result of the enforcement Osborne´s balance sheet was deconsolidated as per 31 March 2015.

Group´s profit and loss on a row by row basis includes revenue and expenses from Osborne for

January to March. Further to the enforcement the RBL facility including accrued interest is to be

considered repaid in full and the transaction resulted in a net capital gain of SEK 285 million.

Cash Flow and investments

The Group’s operating cash flow for the period was SEK -86 million (-108). Cash flow from investing

activities for the period amounted to SEK -40 million (-101). Cash flow from financing activities

amounted to SEK 41 million (-55).

Financial Position

As per 31 December 2015 the book value of the Group’s net borrowings was SEK 32 million,

compared to SEK 2,468 million at year-end 2014. Net borrowings decreased mainly as a result of the

recognised fair value of the interest-bearing debt followed the agreed composition plan in the third

quarter. For more information, see note 19, Interest-bearing loans and borrowings. The decrease is

also a result of the enforced RBL security. The facility, including accrued interest, of approximately

SEK 762 (USD 88.4 million) was considered repaid in the first quarter 2015. PA Resources

shareholder´s equity amounted to SEK -12 million compared to SEK -810 million at year-end 2014 and

increased mainly from the recognised fair value of the existing interest-bearing debt followed the

agreed composition plan, negatively counteracted by asset market valuation. Equity also increased

from the capital gain as a result of the enforced RBL security. Cash and cash equivalents amounted to

SEK 67 million compared with SEK 148 million at year-end 2014.

PA RESOURCES ANNUAL REPORT 2015 8

Financing

PA Resources reached during the second quarter an agreement with its major creditors to provide

the company with funding. The funding which PA Resources secured during the reorganization

enables the Group to borrow money through the issue of Reorganisation Notes with a principal

amount up to 15 MUSD in aggregate. The reorganization Notes have a subscription price of 50% of

their face value, which means that the maximum amount of funds that can be received is 7,5 MUSD.

For more information, see note 19, Interest-bearing loans and borrowings.

Parent Company

Operating profit amounted to SEK -42 million (-199). Net financial items for the period amounted to

SEK 1,181 million (-2,459), and included a capital gain of SEK 427 million from the enforcement of the

RBL security. Net financial items was negatively affected by a net impairment charge of SEK 955

million (1,125) for receivables from subsidiaries and of SEK 195 million (1,730) for shares in

subsidiaries as a result of a market valuation in PA Resources´ Exploration- and evaluation assets as

well as Oil- and gas assets. The finance net was positively affected by the recognised fair value of

liabilities to an amount of SEK 1,909 million (0). Previous year included SEK 232 million from a

dividend received from affiliates.

Equity amounted to SEK 11 million compared to SEK -1,128 million at year-end 2014 and increased

mainly from the other financial income as a result of the recognised fair value of liabilities and the

gain from the enforced RBL security. The share capital as per 31 December 2015 was distributed

among 113,167,992 shares. In connection with the annual general meetings on 28 July 2015, the

decision was to reduce the share capital to SEK 11,316,799.20 for covering of losses. It was further

decided at the extraordinary general meeting on 27 October 2015, to reduce the share capital to SEK

800,000 for covering of losses. Both reductions were made without redemption of shares. New share

quota value is SEK 800,000 / 113,167,992.

Balance Sheet for Liquidation Purposes

Total shareholders’ equity in the parent company amounted to SEK -1,128 million at year-end 2014,

which was less than one-half of the registered share capital of SEK 1,415 million. As a consequence,

the company’s board of directors resolved to prepare a balance sheet for liquidation purposes. The

balance sheet showed, after adjustments, that shareholders’ equity was still less than one-half of the

registered share capital. At an Extraordinary General Meeting held on 27 February 2015 the

shareholders resolved, as recommended by the board, that PA Resources would not be liquidated,

but carry on its business. The Companies Act stipulates that a new general meeting of shareholders

shall be held within eight months at which the shareholders shall resolve on the issue of liquidation

once again. In conjunction with the new general meeting the board of directors shall prepare a new

balance sheet for liquidation purposes. If this new balance sheet does not show that the company’s

shareholder’s equity has been restored and amounts to at least the registered share capital then the

company is required to go into liquidation. At the Extra General Meeting held on the 27 October

2015, PA Resources´ board of directors presented a new balance sheet for liquidation purposes per

30 September 2015 in which the equity had been restored and as a result the meeting voted to

continue operations.

PA RESOURCES ANNUAL REPORT 2015 9

RISKS AND UNCERTAINTIES

Operational Risks

Varying production levels

PA Resources produces at a limited number of fields. This means that natural decline in production

and production disruptions at individual wells or facilities can have a negative impact on total

production levels and revenue. In conjunction with work on producing oil fields, production levels

may be subject temporarily to negative impact.

Fluctuations in the price of oil and gas

The world market price of oil and gas fluctuates from day to day and is influenced by a wealth of

factors outside of PA Resources’ control, including the global economic trend, government and

central bank measures, geopolitical unrest, weather, availability of oil, investment costs and access to

alternative energy sources. In the long term, demand for oil and gas can also be influenced by the

climate debate and the endeavour to reduce carbon emissions to the atmosphere. Major price

fluctuations are negative since lower revenues and increased uncertainty impact the size of

investments.

PA Resources was impacted by the effect of falling oil prices during 2015 as the Brent benchmark fell

by almost 30% from USD 51.8 per barrel in January to USD 36.5 at the end of December.

Natural disasters

PA Resources’ existing or future production facilities may be impacted by natural disasters. Should

such an event occur, existing oil production may be negatively affected or even cease. Natural

disasters can have a devastating effect on the activities of the company, wiping out large values. In

addition, natural disasters can mean a stop in production with accompanying major costs for

restoring production as well as a period with no or partial sales revenue.

Accidents, damage & delays

The Group may also suffer accidents and damage to facilities, environmental damage or personal

injuries. For example, fires, explosions, blowouts, accidental leaks and shipping accidents can occur.

Delays can arise due to bad weather, poorly performed work by external partners, changes in

government requirements and delayed deliveries of equipment.

Geological risks

All estimations of oil and gas reserves and resources involve a certain degree of uncertainty. The risk

exists that the estimated volumes will not accord with reality. The probability of discoveries of oil or

gas varies. If a well proves to be dry, there will be no return on the investment. Even if an oil

discovery is made, the qualities of the bedrock may prevent production.

Shared Ownership and partnership

PA Resources has shared ownership in several licences in partnership with other companies. In a

partnership, it may be difficult to influence how operations on the licence are conducted, especially

where PA Resources isn’t the operator. If a partner doesn’t meet its obligations, PA Resources may,

among other things, risk losing its rights or income, or be forced to take on obligations or costs to

cover that partner’s obligations.

PA Resources was financially impacted by Enquest’s decision to pull out of the farm-out deal in

Tunisia in January 2015.

PA RESOURCES ANNUAL REPORT 2015 10

Financial Risks

Financing and Liquidity Risks

PA Resources is in need of refinancing for maintenance, development and exploration of the Group’s

licences and discoveries. In addition, the Group needs a liquidity reserve for the management of

current payment obligations in operating activities, planned investments and amortisations.

Refinancing risk is defined as the risk that financing or refinancing is troublesome or costly to secure.

PA Resources’ business activities are capital intensive. Field exploration and development requires

access to financing as a supplement to cash flow from operations. The ability to make investments

may be impaired if the cash flow were to be insufficient or external sources of capital limited. If the

Group is unable to meet its amortisation or interest payments fall due and unable to renegotiate or

refinance the loans there is a risk of a new issue of shares. If a new issue of shares cannot be

performed the company could become subject to a reconstruction process or be placed into

receivership.

PA Resources´ strategy according to completed review process is to sale the company´s assets in

order to repay outstanding debt to its creditors in accordance with agreed composition plan. If the

transactions cannot be completed and thus PA Resources cannot repay debt to its creditors in

accordance with the composition plan there is a risk that the company is placed into receivership. For

more information, see Subsequent events.

Other Financial Risk

Through its operations, PA Resources is exposed to the majority of financial risks, including interest

risk, credit risk and currency risk as well as transaction risk and translation risk. Read more in Note

26, Financial risk.

Political Risks

Political and economic instability and corruption

PA Resources conducts business activities in countries where corruption exists and a substantial level

of risk exists in respect of political instability. The concept, political instability, comprises financial

vulnerability and vulnerability to unrest. Unrest, political and economic instability in society, can

hinder the company from conducting business, cause production interruptions, delays and pose a

threat to safety among other items.

Negative Changes to fiscal terms

PA Resources’ operations are affected by the applicable tax rules of each country in which the Group

operates. Tax often comprises various combinations of royalties, discounts on oil produced, income

tax, investment subsidies, stamp duty and capital gains tax. Oil producing developing countries have

had a tendency to raise these taxes in pace with rises in oil prices, which can negatively impact

earnings and cash flow.

PA RESOURCES ANNUAL REPORT 2015 11

SUBSEQUENT EVENTS

PA Resources delist its share

PA Resources share´s last day of trading at Nasdaq Stockholm was 15 January 2016. The decision

notified by Nasdaq was based on PA Resources application to delist submitted 20 November 2015.

PA Resources delist its SEK denominated bond

PA Resources SEK denominated bond´s last day of trading at Nasdaq Stockholm was 1 February 2016.

The decision notified by Nasdaq was based on PA Resources application to delist submitted 25

January 2016.

Drilling Results on Baobab Marine-1 Well at Mer Profonde Sud

During February 2016 final results came from the Baobab Marine-1 commitment well drilled in the

Mer Profonde Sud Block offshore the Republic of Congo. Although good quality sands were present,

no hydrocarbons were encountered, suggesting lack of communication with the known oil source.

PA Resources divests its North Sea portfolio

As per 5 February 2016 PA Resources signed an agreement with Petrogas E&P regarding the sale of

its affiliates PA Resources UK Ltd and PA Resources Denmark ApS including the Danish license 12/06

which holds the Broder Tuck and Lille John discoveries, as well as its exploration licences in the UK,

Germany and the Netherlands. PA Resources completed the transaction with Petrogas E&P

announced as per 24 March 2016 and payment for the transaction has been received. Included in the

transaction is also a highly uncertain and contingent consideration based on future oil price

development. The consideration is not included in the 2015 valuation of PA Resources' net assets.

PA Resources divests its North Africa portfolio

As per 9 May 2016 PA Resources AB announced that its wholly owned subsidiaries, PA Resources

Tunisia Limited, Hydrocarbures Tunisie Didon Limited, Hydrocarbures Didon Jersey Limited and

Hydrocarbures Tunisie Corporation, executed a sale and purchase agreement with ETAP, The

Tunisian national oil company, to sell their entire licence interests onshore and offshore Tunisia, to

ETAP. The transaction is expected to complete within the next month.

Use of proceeds from divested assets

Followed above divestments PA Resources will have no assets left. The proceeds from the sale will be

used to repay creditors in accordance with the reorganisation plan adopted in October 2015. As per

release date of this annual report category B** has been repaid in full while category A* has agreed

to delay part of payment until completion of the North Africa transaction, but is expected to

ultimately receive full payment. Category C *** are expected to receive a significantly lower

proportion than its nominal values. The liabilities are thus recognised at the values expected to be

paid. Given that the transaction in North Africa completes there will also be sufficient funds to

implement the solvent wind down, which given above is the Board´s intention to suggest for the

shareholders.

* Category A (Reorganisation notes) is described in detail in section 8.4.3.1 and 6.7 of the Reorganisation Plan.

** Category B (Creditors with principal claims below 100 000 SEK as well as above 100 000 SEK without specific agreement) is described in

detail in sections 8.4.3.1, 8.2 and 8.3 of the Reorganisation Plan. Category B does not include bondholders as explained in section 6.4.

*** Category C (Creditors above 100 000 SEK with specific agreements) is described in detail in section 8.4 in the Reorganisation plan.

PA RESOURCES ANNUAL REPORT 2015 12

BOARD OF DIRECTORS

The Board of Directors in PA Resources AB as per signing of the Annual report:

Catharina Nystedt-Ringborg (Director as of 27 October 2015)

Mark McAllister

Paul Waern (Chairman as of 28 July 2015)

The Board of Directors in PA Resources AB during 2015/2016:

Garrett Soden (Director from 27 October 2015 until 2 February 2016)

Jérôme Schurink (Chairman and director until 11 April 2015)

Nils Björkman (Director until 28 July 2015)

Philippe Probst (Director until 28 July 2015)

Philippe R. Ziegler (Director until 28 July 2015)

Tomas Hedström (Director from 28 July until 27 October 2015)

PROPOSED DISTRIBUTION OF EARNINGS

The Board of Directors proposes that the Non-restricted equity of the Parent company of SEK

9,987,000 including the Profit for the year of SEK 1,139,271,000 to be carried forward.

PA RESOURCES ANNUAL REPORT 2015 13

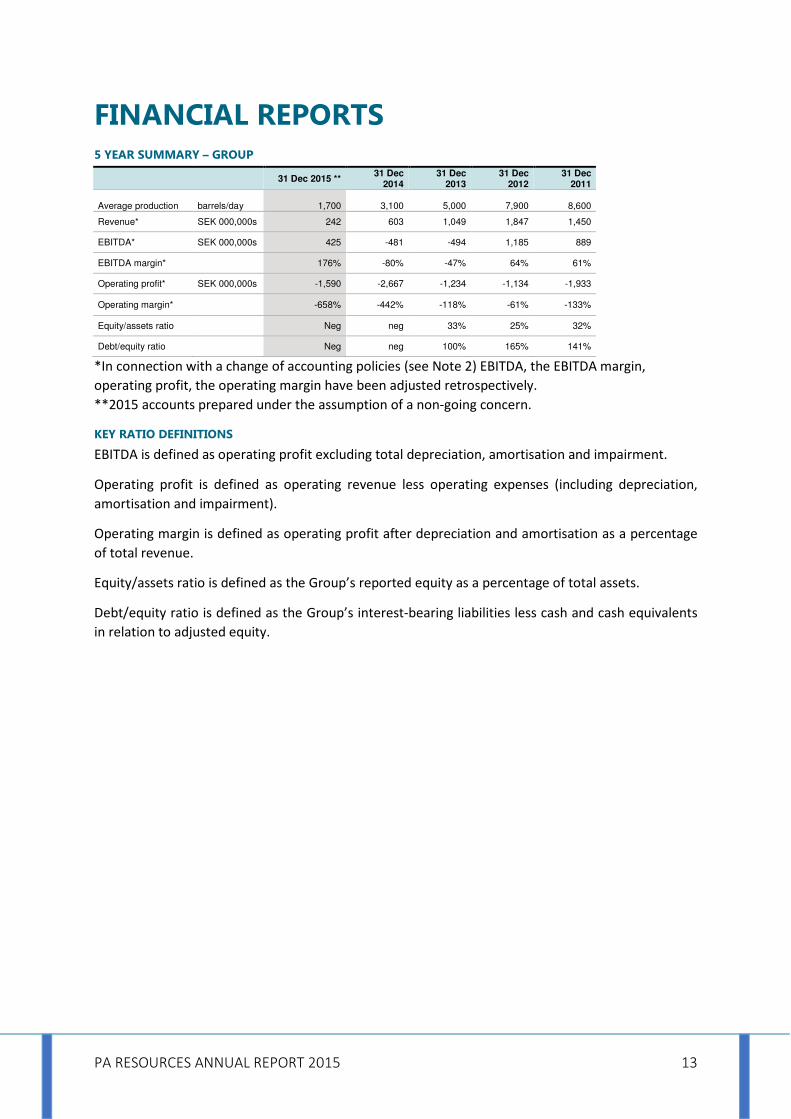

FINANCIAL REPORTS 5 YEAR SUMMARY – GROUP

31 Dec 2015 ** 31 Dec

2014 31 Dec

2013 31 Dec

2012 31 Dec

2011

Average production barrels/day 1,700 3,100 5,000 7,900 8,600

Revenue* SEK 000,000s 242 603 1,049 1,847 1,450

EBITDA* SEK 000,000s 425 -481 -494 1,185 889

EBITDA margin* 176% -80% -47% 64% 61%

Operating profit* SEK 000,000s -1,590 -2,667 -1,234 -1,134 -1,933

Operating margin* -658% -442% -118% -61% -133%

Equity/assets ratio Neg neg 33% 25% 32%

Debt/equity ratio Neg neg 100% 165% 141%

*In connection with a change of accounting policies (see Note 2) EBITDA, the EBITDA margin,

operating profit, the operating margin have been adjusted retrospectively.

**2015 accounts prepared under the assumption of a non-going concern.

KEY RATIO DEFINITIONS

EBITDA is defined as operating profit excluding total depreciation, amortisation and impairment.

Operating profit is defined as operating revenue less operating expenses (including depreciation,

amortisation and impairment).

Operating margin is defined as operating profit after depreciation and amortisation as a percentage

of total revenue.

Equity/assets ratio is defined as the Group’s reported equity as a percentage of total assets.

Debt/equity ratio is defined as the Group’s interest-bearing liabilities less cash and cash equivalents

in relation to adjusted equity.

PA RESOURCES ANNUAL REPORT 2015 14

INCOME STATEMENT – GROUP

SEK 000,000s Notes 2015 * 2014

Revenue 2 242 603

Production costs 2, 5 -184 -187

Depletion oil and gas properties 2, 14 -40 -195

Gross profit 2 17 222

Other income 4 222 46

Capital gain 4 285 -

Termination farm-out agreement 4 - -826

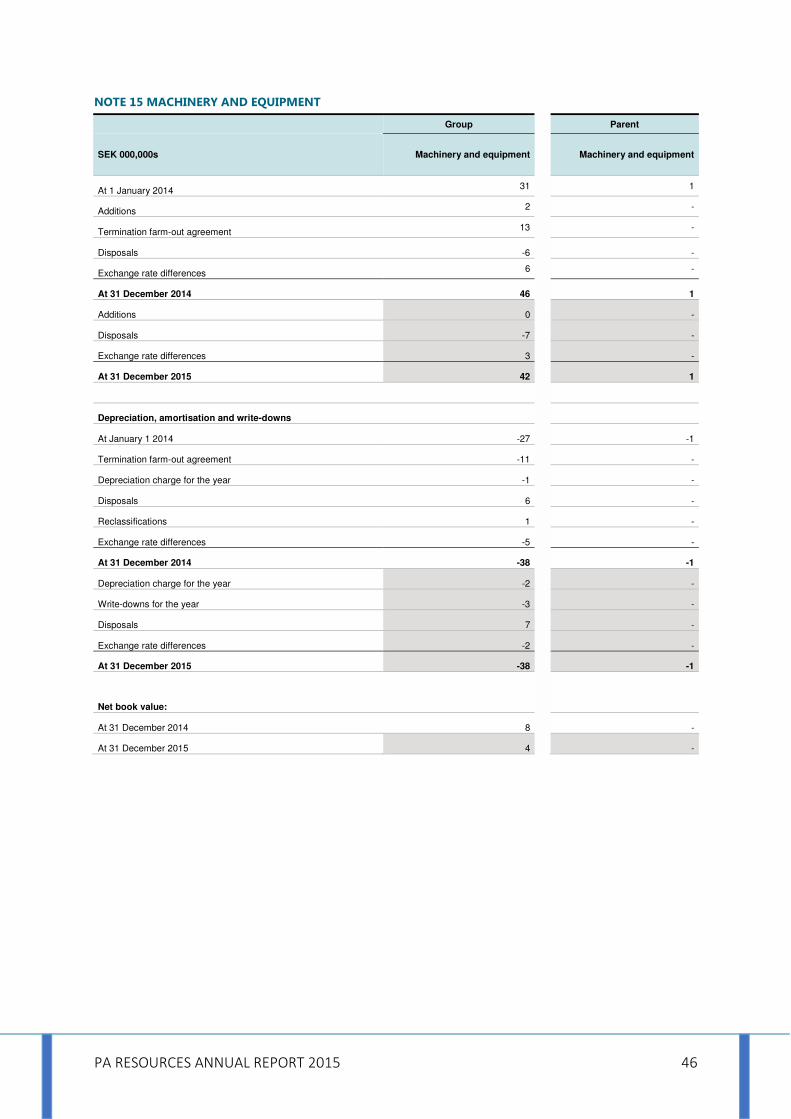

Impairment losses 14, 15, 16 -1,969 -1,991

General, administration and depreciation expenses 6, 7, 8, 9, 10, 11 -145 -118

Operating profit 2 -1,590 -2,667

Financial income 12 2,061 3

Financial expenses 12 -197 -368

Total financial items 1,864 -365

Profit before tax 275 -3,032

Income tax 2, 13 504 74

Profit for the period 779 -2,957

Profit for the year and earnings per share are attributable to owners of the parent.

STATEMENT OF COMPREHENSIVE INCOME – GROUP

Jan-Dec Jan-Dec

SEK 000,000s Notes 2015 * 2014

Profit for the year 779 -2,957

Other comprehensive income

Items that may be reclassified into profit or loss

Exchange differences during the period 101 353

Items reclassified into profit or loss

Accumulated exchange differences reclassified into profit and loss

-81 -

Other comprehensive income for the year 20 353

Total comprehensive income for the year 799 -2,605

Total comprehensive income is attributable to the owners of the parent.

*2015 accounts prepared under the assumption of a non-going concern.

PA RESOURCES ANNUAL REPORT 2015 15

STATEMENT OF FINANCIAL POSITION – GROUP (NON-GOING CONCERN)

31 Dec

SEK 000,000s Notes 2015

ASSETS

Exploration and evaluation assets & Oil and gas properties 14, 16 140

Machinery and equipment 15 4

Financial assets 22 1

Deferred tax assets 13 9

Inventory 17 40

Accounts receivable and other receivables 18 50

Tax assets 13 13

Cash and cash equivalents 67

TOTAL CURRENT ASSETS 324

EQUITY

Equity attributable to owners of the parent

Share capital 1

Other capital contributions 6,464

Reserves -706

Retained earnings and profit for the year -5,770

TOTAL EQUITY -12

LIABILITIES

Provisions 20 98

Deferred tax liabilities 13 -

Tax liabilities 13 29

Interest-bearing loans and borrowings 19 99

Accounts payable and other liabilities 21 111

TOTAL CURRENT LIABILITIES 336

TOTAL EQUITY AND CURRENT LIABILITIES 324

PLEDGED ASSETS 24 46

CONTINGENT LIABILITIES 24 -

PA RESOURCES ANNUAL REPORT 2015 16

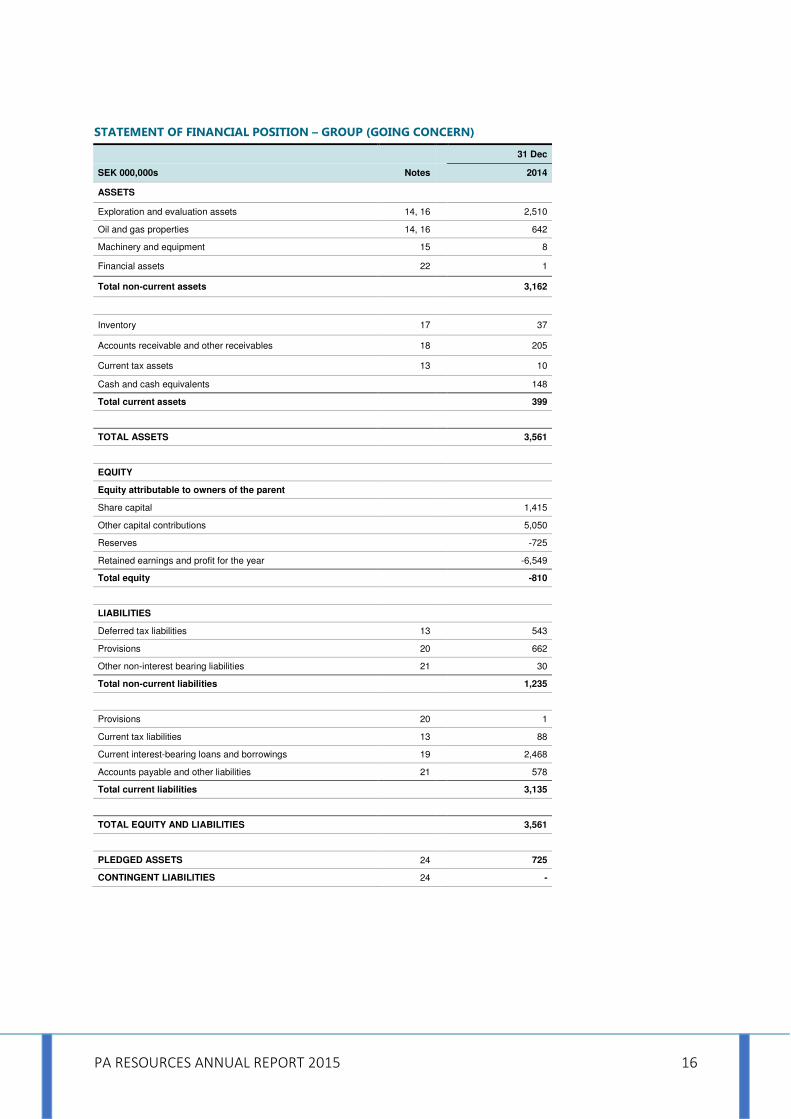

STATEMENT OF FINANCIAL POSITION – GROUP (GOING CONCERN)

31 Dec

SEK 000,000s Notes 2014

ASSETS

Exploration and evaluation assets 14, 16 2,510

Oil and gas properties 14, 16 642

Machinery and equipment 15 8

Financial assets 22 1

Total non-current assets 3,162

Inventory 17 37

Accounts receivable and other receivables 18 205

Current tax assets 13 10

Cash and cash equivalents 148

Total current assets 399

TOTAL ASSETS 3,561

EQUITY

Equity attributable to owners of the parent

Share capital 1,415

Other capital contributions 5,050

Reserves -725

Retained earnings and profit for the year -6,549

Total equity -810

LIABILITIES

Deferred tax liabilities 13 543

Provisions 20 662

Other non-interest bearing liabilities 21 30

Total non-current liabilities 1,235

Provisions 20 1

Current tax liabilities 13 88

Current interest-bearing loans and borrowings 19 2,468

Accounts payable and other liabilities 21 578

Total current liabilities 3,135

TOTAL EQUITY AND LIABILITIES 3,561

PLEDGED ASSETS 24 725

CONTINGENT LIABILITIES 24 -

PA RESOURCES ANNUAL REPORT 2015 17

STATEMENT OF CHANGES IN EQUITY – GROUP

Equity attributable to owners of the parent

SEK 000,000s Notes Share capital Other capital contribution Reserves

Retained earnings and profit for the

year Total

Balance at 1 January 2014 1,415 5,050 -1,078 -3,592 1,795

Total comprehensive income for the period

353 -2,957 -2,605

Closing balance at 31 december 2014 1,415 5,050 -725 -6,549 -810

Balance at 1 January 2015 1,415 5,050 -725 -6,549 -810

Total comprehensive income for the period 20 779 799

Transactions with shareholders

Reduction share capital -1,414 1,414 -

Closing balance at 31 december 2015 1 6,464 -706 -5,770 -12

The share capital as per 31 December 2015 was distributed among 113,167,992 shares. In connection

with the annual general meetings on 28 July 2015, the decision was to reduce the share capital to

SEK 11,316,799.20 for covering of losses. It was further decided at the extraordinary general meeting

on 27 October 2015, to reduce the share capital to SEK 800,000 for covering of losses. Both

reductions were made without redemption of shares. New share quota value is SEK 800,000 /

113,167,992. No dividend was decided on for the 2014 financial year or previous financial years. The

Board of Directors proposes to the Annual General Meeting that no dividend be paid for the 2015

financial year. Reserves pertain to effects from translation of operations in foreign currency.

PA RESOURCES ANNUAL REPORT 2015 18

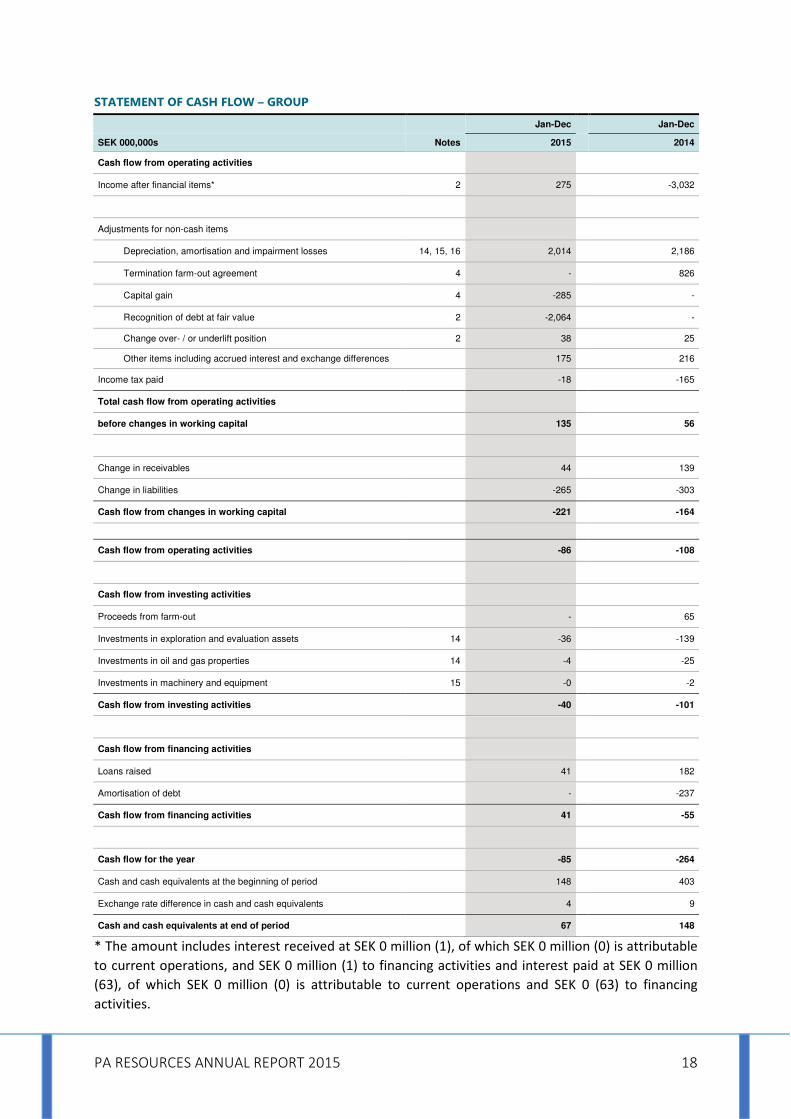

STATEMENT OF CASH FLOW – GROUP

Jan-Dec Jan-Dec

SEK 000,000s Notes 2015 2014

Cash flow from operating activities

Income after financial items* 2 275 -3,032

Adjustments for non-cash items

Depreciation, amortisation and impairment losses 14, 15, 16 2,014 2,186

Termination farm-out agreement 4 - 826

Capital gain 4 -285 -

Recognition of debt at fair value 2 -2,064 -

Change over- / or underlift position 2 38 25

Other items including accrued interest and exchange differences 175 216

Income tax paid -18 -165

Total cash flow from operating activities

before changes in working capital 135 56

Change in receivables 44 139

Change in liabilities -265 -303

Cash flow from changes in working capital -221 -164

Cash flow from operating activities -86 -108

Cash flow from investing activities

Proceeds from farm-out - 65

Investments in exploration and evaluation assets 14 -36 -139

Investments in oil and gas properties 14 -4 -25

Investments in machinery and equipment 15 -0 -2

Cash flow from investing activities -40 -101

Cash flow from financing activities

Loans raised 41 182

Amortisation of debt - -237

Cash flow from financing activities 41 -55

Cash flow for the year -85 -264

Cash and cash equivalents at the beginning of period 148 403

Exchange rate difference in cash and cash equivalents 4 9

Cash and cash equivalents at end of period 67 148

* The amount includes interest received at SEK 0 million (1), of which SEK 0 million (0) is attributable

to current operations, and SEK 0 million (1) to financing activities and interest paid at SEK 0 million

(63), of which SEK 0 million (0) is attributable to current operations and SEK 0 (63) to financing

activities.

PA RESOURCES ANNUAL REPORT 2015 19

INCOME STATEMENT – PARENT COMPANY

Jan-Dec Jan-Dec

SEK 000,000s Notes 2015 * 2014

Other income 4 42 15

Termination farm-out agreement 4 - -168

General, administration and depreciation expenses 6, 7, 8, 9, 10, 11 -84 -47

Operating profit -42 -199

Result from participations in Group companies 25 -723 -2,623

Financial income and similar 12 2,061 460

Financial expenses and similar 12 -157 -297

Total financial items 1,181 -2,459

Profit before tax 1,139 -2,659

Income tax 13 - 0

Profit for the year 1,139 -2,658

STATEMENT OF COMPREHENSIVE INCOME – PARENT COMPANY

Jan-Dec Jan-Dec

SEK 000,000s Notes 2015 2014

Profit for the year 1,139 -2,658

Other comprehensive income

Total items that may be reclassified into profit or loss - -

Total comprehensive income for the year 1,139 -2,658

*2015 accounts prepared under the assumption of a non-going concern.

PA RESOURCES ANNUAL REPORT 2015 20

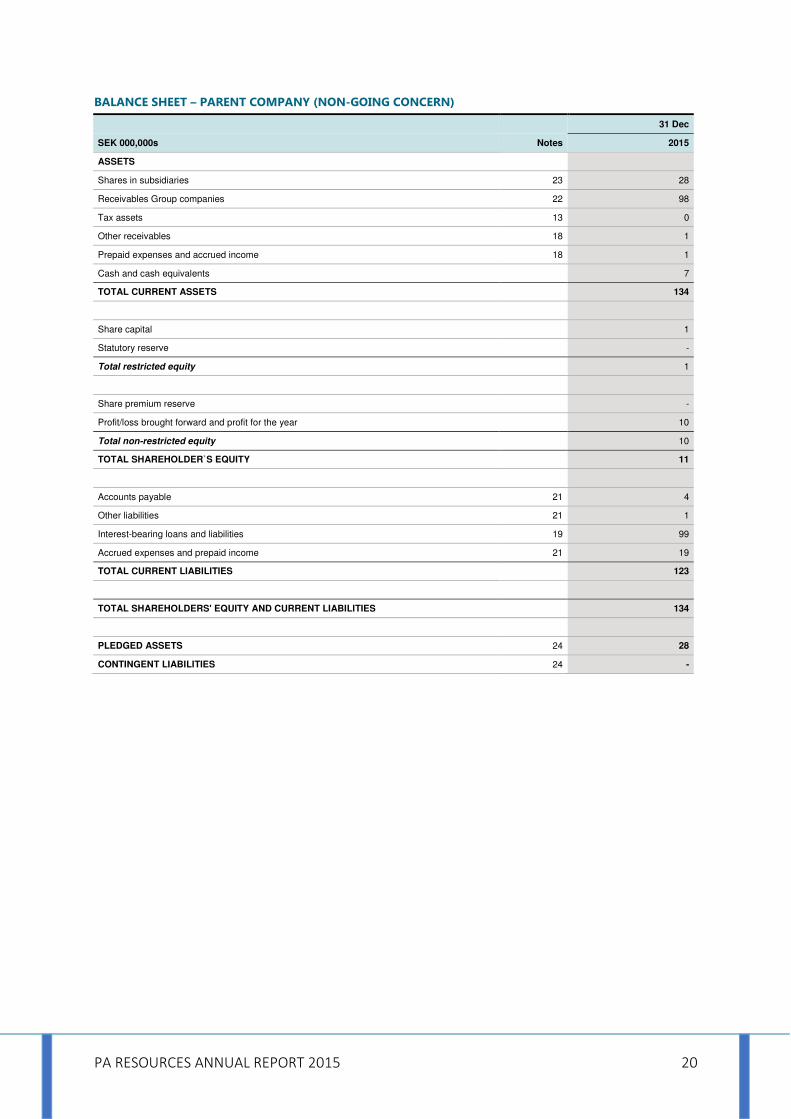

BALANCE SHEET – PARENT COMPANY (NON-GOING CONCERN)

31 Dec

SEK 000,000s Notes 2015

ASSETS

Shares in subsidiaries 23 28

Receivables Group companies 22 98

Tax assets 13 0

Other receivables 18 1

Prepaid expenses and accrued income 18 1

Cash and cash equivalents 7

TOTAL CURRENT ASSETS 134

Share capital 1

Statutory reserve -

Total restricted equity 1

Share premium reserve -

Profit/loss brought forward and profit for the year 10

Total non-restricted equity 10

TOTAL SHAREHOLDER`S EQUITY 11

Accounts payable 21 4

Other liabilities 21 1

Interest-bearing loans and liabilities 19 99

Accrued expenses and prepaid income 21 19

TOTAL CURRENT LIABILITIES 123

TOTAL SHAREHOLDERS' EQUITY AND CURRENT LIABILITIES 134

PLEDGED ASSETS 24 28

CONTINGENT LIABILITIES 24 -

PA RESOURCES ANNUAL REPORT 2015 21

BALANCE SHEET – PARENT COMPANY (GOING CONCERN)

31 Dec

SEK 000,000s Notes 2014

ASSETS

Shares in subsidiaries 23 241

Receivables Group companies 22 808

Total non-current assets 1,050

Current tax assets 13 0

Other receivables 18 2

Prepaid expenses and accrued income 18 1

Cash and cash equivalents 88

Total current assets 92

TOTAL ASSETS 1,141

SHAREHOLDERS' EQUITY

Share capital 1,415

Statutory reserve 115

Total restricted equity 1,530

Share premium reserve -

Profit/loss brought forward and profit for the year -2,658

Total non-restricted equity -2,658

Total shareholders' equity -1,128

LIABILITIES

Liabilities Group companies 22 22

Accounts payable 21 1

Other liabilities 21 0

Current interest-bearing loans and liabilities 19 2,191

Accrued expenses and prepaid income 21 56

Total current liabilities 2,270

TOTAL SHAREHOLDERS' EQUITY AND LIABILITIES 1,141

PLEDGED ASSETS 24 18

CONTINGENT LIABILITIES 24 -

PA RESOURCES ANNUAL REPORT 2015 22

STATEMENT OF CHANGES IN EQUITY – PARENT COMPANY

Restricted equity Non-restricted equity

SEK 000,000s Notes Share capital Statutory Reserve

Other capital contribution

Retained earnings

Profit for the year Total

Balance at 1 January 2014 1,415 985 2,888 -1,199 -2,559 1,530

Transfer of previous year´s result -870 -2,888 1,199 2,559 -

Total comprehensive income for the year -2,658 -2,658

Closing balance at 31 December 2014 1,415 115 - - -2,658 -1,128

Balance at 1 January 2015 1,415 115 - - -2,658 -1,128

Transfer of previous year´s result -115 -2,543 2,658 -0

Total comprehensive income for the period

1,139 1,139

Transactions with shareholders

Reduction share capital -1,414 1,414 -

Closing balance at 31 December 2015 1 - - -1,130 1,139 11

PA RESOURCES ANNUAL REPORT 2015 23

STATEMENT OF CASH FLOW – PARENT COMPANY

Jan-Dec Jan-Dec

SEK 000,000s Notes 2015 2014

Cash flow from operating activities

Income after financial items* 1,139 -2,659

Adjustments for non-cash items

Termination farm-out agreement 4 - 168

Impaiment losses participations in Group companies 25 195 1,730

Impaiment losses Intercompany receivables 25 955 1,125

Capital gain -427 -

Recognition of debt at fair value -1,912 -

Dividend recieved - -232

Other items including accrued interests and exchange gains and losses (net)

-79 -167

Income tax paid - -

Total cash flow from operating activities

before changes in working capital -129 -35

Change in receivables 9 -22

Change in liabilities 59 -40

Cash flow from changes in working capital 68 -62

Cash flow from operating activities -61 -97

Cash flow from investing activities

Loans given to subsidiaries -61 -123

Cash flow from investing activities -61 -123

Cash flow from financing activities

Loans raised 41 182

Amortisation of debt - -237

Cash flow from financing activities 41 -55

Cash flow for the year -81 -275

Cash and cash equivalents at the beginning of period 88 363

Cash and cash equivalents at end of the year 7 88

* The amount includes interest received at SEK 0 million (1), of which SEK 0 million (0) is attributable

to current operations, and SEK 0 million (1) to financing activities and interest paid at SEK 0 million

(49), of which SEK 0 million (0) is attributable to current operations and SEK 0 million (49) to financing

activities.

PA RESOURCES ANNUAL REPORT 2015 24

NOTES

1 Company information 25

2 Accounting principles etc 25

3 Acquisitions of operations and licence shares 36

4 Segment information 37

5 Production costs 38

6 Total general, administration and depreciation expenses 38

7 Other expenses 38

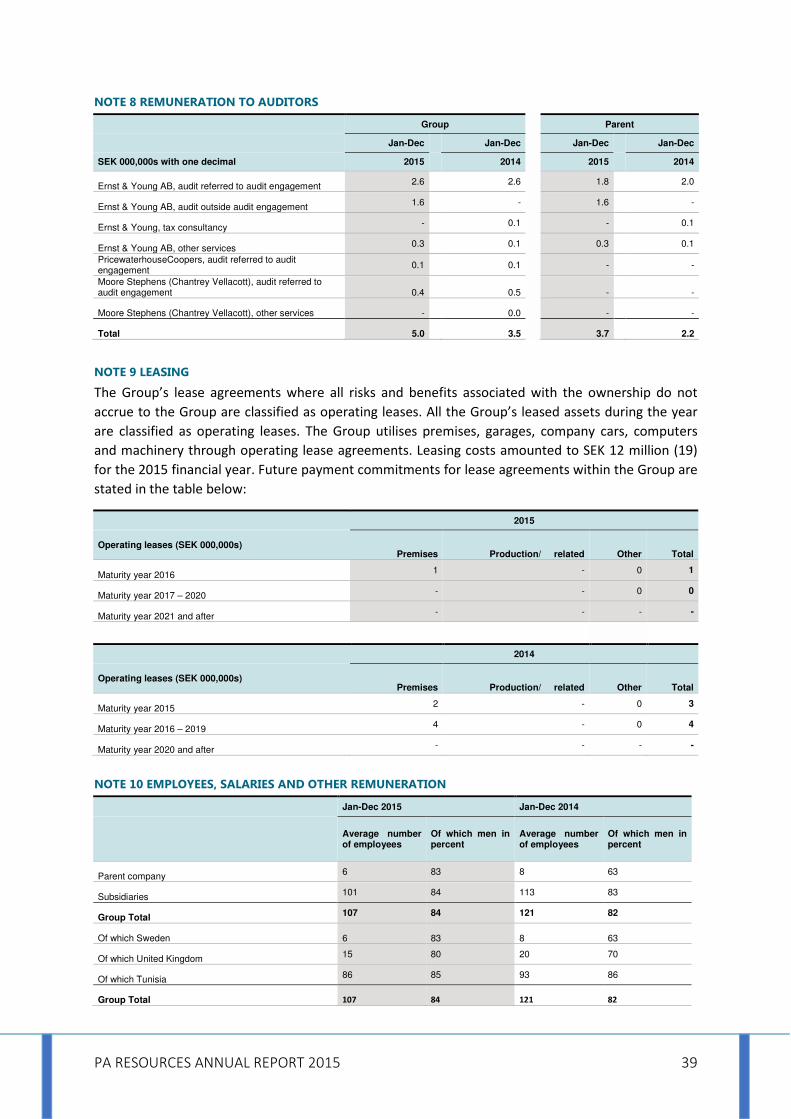

8 Remunerations to auditors 39

9 Leasing 39

10 Employees, salaries and remuneration 39

11 Remuneration and other benefits; Board of Directors and

senior executives of the Parent company 41

12 Financial income and expenses 42

13 Income tax 42

14 Exploration and evaluation assets and oil and gas properties 44

15 Machinery and equipment 46

16 Impairment testing exploration and evaluation assets and

oil and gas properties 47

17 Inventories 48

18 Accounts receivables and other receivables 49

19 Interest-bearing loans and borrowings 49

20 Provisions 51

21 Accounts payable and other liabilities 52

22 Financial instruments 52

23 Shares in subsidiaries 56

24 Pledged assets and contingent liabilities 57

25 Result from participations in Group companies 57

26 Financial risk 58

27 Related party disclosure 60

28 Significant events after the closing date 61

PA RESOURCES ANNUAL REPORT 2015 25

NOTE 1 COMPANY INFORMATION

The Parent company PA Resources AB (publ) is a Swedish limited company domiciled in Stockholm

(corporate identity number 556488-2180). The Group’s business consists of either that itself or in

collaboration with others pursue prospecting business, extract oil and gas and own and administer,

which includes buying and selling, concessions, stocks and shares in companies who pursue

prospecting- and extracting business and be engaged in other activities thereto. The Parent

company’s functional currency, and the currency in which the accounts are presented, is Swedish

kronor (SEK). This annual report and the consolidated accounts of PA Resources AB (publ) for the

year ending 31 December 2015 were approved for publication by the Board of Directors on 9 June

2016 and will be submitted for adoption at the Annual General Meeting on 30 June 2016.

NOTE 2 ACCOUNTING PRINCIPLES ETC

Note 2.1 Description of significant accounting prinNote 2.1 Description of significant accounting prinNote 2.1 Description of significant accounting prinNote 2.1 Description of significant accounting principlesciplesciplesciples

The sections within this Annual Report which are classified as formal financial reports according to

IFRS are:

• the consolidated Income Statement, Statement of Comprehensive Income, Statement of Financial

Position, Statement of Changes in Equity and Statement of Cash Flows

• the Parent company’s Income Statement, Statement of Comprehensive Income, Balance Sheet,

Statement of Changes in Equity and Statement of Cash Flows

• the notes to the financial reports

Non-going concern

The company has since the middle of 2014 been working to secure long-term financing for the

company’s operations and development projects. Following the corporate reorganisation and the

strategic review the company still stands without long-term financing and has decided to sell its

assets. As a result the board of directors has concluded that the company’s financial statements,

effective 31 December 2015, can no longer be prepared under the assumption of a going concern.

Following the decision to prepare the accounts without the assumption of a going concern PA

Resources values its exploration and evaluation assets and its oil and gas properties including

abandonment costs at the lowest of either carrying value or fair value less cost to sell (FVLCS).

Market valuation of the assets are based on sales values net of transaction costs. Provision for

abandonment earlier accounted for as provision are, as a consequence of not applying going

concern, now included net in evaluation and exploration assets & oil and gas properties. Further,

according to the strategic review process described under Board of Director´s report, the conclusion

is to sale all of the company´s assets and in such case IFRS 5 is not applicable. PA Resources AB

accounts for its participations in group companies in accordance with what is expected to be

obtained through the sale, net.

As per 2 October, 2015 a qualified majority of the company’s creditors choose to support the

proposed composition plan put forward by PA Resources AB and the administrator at the

composition proceedings at the Stockholm District Court. Following the decision of the board to

prepare the Annual report in accordance with a non-going concern, PA Resources, effective 31

December, 2015 has derecognised its interest-bearing loans and borrowings accounted for at

amortised cost and thereafter recognised its interest-bearing loans and borrowings at fair value and

in accordance with the terms of the adopted composition plan.

PA RESOURCES ANNUAL REPORT 2015 26

The PA Resources group´s and parent company´s financial statements are as per December 31, 2015

prepared on a non-going concern basis, whereas all earlier periods are prepared under the

assumption of a going concern. As a result of the non-going concern assumption all non-current

assets and liabilities have been reclassified to current assets and liabilities in both the PA Resources

group´s and parent company´s statement of financial position ending 31 December 2015. The

changed assumption does not impact the net result or the cash flow statement in any of the previous

or current periods. No retrospective changes have been made.

Basis for preparation of the financial statements

Except for what is described above under “Non-going concern”, the consolidated financial

statements are based on historical acquisition costs except in the case of financial instruments, which

could be reported at fair value. Group´s outstanding under- / overlift positions of hydrocarbons are

valued at the balance sheet date and recognised as if the positions have been sold. Valuations are

performed either with Brent spot price at the balance sheet date taking eventual discount or

premium into consideration or with prevailing contract prices. Unless otherwise indicated, all

amounts are reported in thousands of Swedish kronor (SEK million).

Statement of conformity with regulations applied

The consolidated financial statements and the financial statements for the Parent company have

been prepared in accordance with International Financial Reporting Standards (IFRS) including

interpretation statements issued by the International Financial Reporting Interpretations Committee

(IFRIC ) and in accordance with Swedish laws. Since the Parent company is a company within the EU,

only IFRS adopted by the EU are applied. In addition, the Annual Accounts Act and the Swedish

Financial Reporting Board’s recommendation RFR 1, Supplementary Accounting Rules for the Group

have been applied. The financial statements for the Parent company have been prepared applying

recommendation RFR 2, Accounting for Legal Entities, statements from the Swedish Financial

Reporting Board and the Annual Accounts Act.

Consolidated financial statements

Basis of consolidation

The consolidated financial statements encompass the Parent company and its subsidiaries. The

financial reports for the Parent company and the subsidiaries included in the consolidated financial

statements cover the same period and have been prepared in accordance with the same accounting

principles as applied for the Group.

All intra-group transactions and accounts, as well as gains and losses on transactions between Group

companies are eliminated entirely.

A subsidiary or its assets and liabilities are included in the consolidated financial statements from the

acquisition date, which is the day a controlling influence in the subsidiary arises, and are included in

the consolidated financial statements until the day the controlling influence ceases. Controlling

influence means the right to formulate the subsidiary’s operational and financial strategies with a

view to obtaining financial benefits.

Acquisitions of operations are reported in the consolidated financial statements using the purchase

method of accounting. The purchase method of accounting means, among other things, that the

acquisition cost of the shares is distributed to the assets, commitments taken over and liabilities

acquired at the acquisition date based on their fair values at the time. If the acquisition cost exceeds

the fair value of the acquired company’s net assets, the excess value is first allocated to acquired oil

and gas properties and thereafter, any difference is recognised as goodwill. If the acquisition cost is

PA RESOURCES ANNUAL REPORT 2015 27

lower than the fair value of the acquired company’s net assets, the difference is reported directly in

the income statement.

Segment reporting

Followed that PA Resources´ share is delisted, the company is no longer obliged to apply IFRS 8.

Further PA Resources´ group management has changed its way of analysing and monitoring the

company´s performance, the internal reporting, effective 31 December 2015, is made and monitored

by the management in form of one single segment containing all of PA Resources´ assets. Earlier

segment structure based on geographical regions is no longer valid from an IFRS 8 perspective.

Therefore PA Resources no longer show its Income statement and Balance sheet compiled per

geographical regions.

Translation of foreign currency

Functional currency and reporting currency

The functional currency of each unit within the Group is determined by reference to the economic

environment in which the units carry on their respective operations. Monetary receivables and

liabilities in each subsidiary that are expressed in foreign currencies are translated into the functional

currency at the exchange rate in force on the balance sheet date. All translation differences are

reported in the income statement. The Group continuously analyses circumstances that could

indicate a change in the functional currency from local currency to USD in the Group’s subsidiaries.

Translation of foreign operations

The consolidated financial statements of PA Resources are presented in Swedish kronor (SEK), which

is the Parent company’s functional and reporting currency.

Assets and liabilities in other functional currencies are translated into SEK at the exchange rate

effective on the balance sheet date. Income statements are translated at the average exchange rate

for the year. Translation differences arising on the translation of foreign operations are reported

directly against equity in the statement of comprehensive income.

Exchange rates

The following exchange rates were used in the preparation of the financial statements:

Closing day rate 31 Dec 2015

Average rate Jan-Dec 2015

Closing day rate 31 Dec 2014

Average rate Jan-Dec 2014

1 EUR in SEK 9.14 9.36 9.52 9.10

1 USD in SEK 8.35 8.44 7.81 6.86

1 TND in SEK 4.15 4.30 4.19 4.04

1 NOK in SEK 0.96 1.05 1.05 1.09

1 GBP in SEK 12.38 12.90 12.14 11.29

1 DKK in SEK 1.22 1.25 1.28 1.22

New accounting policy – Exchange gains/losses

PA Resources decided in the first quarter 2015 to change accounting policy for exchange gains/losses

earlier presented in operating profit now in net financial items. The changed accounting policy does

not impact the net result in any of the previous and current periods. It did not either impact the split

between operating- and non-operating result. Even though the previously applied policy, as

presented in the income statement were in full compliance with IFRS, the assessment is now that the

new presentation and changed policy provide a better presentation and more relevant information

for the reader. PA Resources is doing this on a voluntary basis and there are no historical errors. PA

PA RESOURCES ANNUAL REPORT 2015 28

Resources has changed the accounting policies in accordance with IAS 8 - Accounting Policies,

Changes in Accounting Estimates and Errors.

Revenue recognition

Group revenue primarily refers to revenue from sales of oil. Revenue is based on sales which are

primarily managed by yearly contracts signed with a small number of major international oil and gas

companies in which oil sold is priced at the applicable world market price less any discounts and plus

any premiums due to the quality of the oil and gas equivalents. Pricing occurs during a

predetermined time period prior to and following the day on which physical delivery is made from

vendor to vendee. Interest income is recognized in accordance with the effective rate method and

primarily refers to interest income from cash and cash equivalents and receivables. The majority of

the Parent company’s revenue is made up of sales of services to other companies within the Group.

Production costs (Direct production taxes)

Current license terms for some producing oil fields require direct production taxes (royalties) to be

paid.

Remunerations to employees, Board of Directors and senior executives

Short-term remunerations

Salaries, other remuneration and benefits as well as social security contributions are reported as

personnel expenses in the income statement when they arise.

Post-employment remunerations

Pension costs for defined-contribution plans are reported as personnel expenses in the income

statement. The defined-contribution plans are the only pension schemes in place within PA

Resources. More information regarding the expenses during the financial year is provided in Note 10,

Employees, salaries and other remuneration.

Recognition of exploration and evaluation assets as well as oil and gas properties

Except for what is described above under Non-going concern, Expenditures for exploration and

evaluation of oil and gas properties are reported according to the Full Cost Method. All costs

attributable to exploration, drilling and evaluation of such interests are capitalised in full. The

expenditures are accumulated separately for each licence right and the capitalisation of exploration

and evaluation assets, or alternatively oil and gas properties depends on the development phase that

has been reached.

The balance sheet item exploration and evaluation assets refer to acquired licence/concession rights

and other capitalised exploration and evaluation expenditure.

When PA Resources appraises and assesses an exploration permit as profitable a plan for

development is applied for. On receiving the plan for development, the asset is reclassified under oil

and gas properties and, in conjunction with reclassification, the assets are tested for any possible

need for impairment, for the purpose of ascertaining their value. If the asset is relinquished to the

government authorities or is assessed as unprofitable, the asset is expensed by PA Resources

through recognition as an impairment loss in profit or loss.

The balance sheet item, oil and gas properties, refers both to reclassified exploration and evaluation

assets as well as capitalised development expenses. Depreciation commences for the actual asset in

conjunction with the start of production. Assets are regularly tested for any possible need for

PA RESOURCES ANNUAL REPORT 2015 29

impairment and where a need is identified, the asset is expensed through recognition as an

impairment loss in profit or loss.

Joint arrangements

PA Resources has interests in licences in the North Africa, West Africa and the North Sea and

recognises investments in joint operations (exploration and evaluation assets as well as oil and gas

properties) by reporting its share of related expenses, assets, liabilities and cash flows under the

respective items in the Group’s financial statements. For those licences that are not deemed to be a

joint arrangement under the definition in IFRS 11 because there is no joint control, PA Resources

recognises its share of related expenses, assets, liabilities and cash flows on a line-by-line-basis in the

financial statements in accordance with applicable IFRS.

Farm-out accounting

Farm-outs are accounted for in accordance with the principles of IFRS 6 with respect to exploration

and evaluation assets. PA Resources recognises cash payments received directly against the asset

and retains the recorded portion of the asset less any cash received. This entails that no revenue is

recognised in connection with the farm-out unless the cash received exceeds the book value of the

farmed out asset. No entries at the transaction date are made regarding any future payments. In

case where a farm-out pertains to PA Resources’ oil and gas assets, accounting is performed in

accordance with IAS 16. Accordingly, PA Resources derecognises the carrying amount of the asset

attributable to the proportion farmed out and recognises any future payments on the balance sheet.

After recording any cash received as part of the transaction, a gain or loss is recognised in the income

statement. After the completed transaction, PA Resources tests its cash generating units for

impairment. Impairment losses are charged to the income statement.

Depletion oil and gas properties

Depletion of oil and gas properties commences in conjunction with the start of production and are

calculated using the Unit of Production Method and are depleted in line with the year’s production in

relation to the estimated total proven and probable reserves of oil and gas. Technical installations

and equipment are linear depreciated over the assets’ expected useful life. The estimated useful life

is ten years for technical installations and five years for equipment.

Recognition of machinery and equipment

Machinery and equipment is valued at cost after a deduction for accumulated depreciation and any

impairment losses. Linear depreciation is applied over the assets’ expected useful life. The estimated

useful life for machinery and equipment is 3–5 years.

Impairment losses

Except for what is described above under Non-going concern, PA Resources regularly assesses its

exploration and evaluation assets as well as its oil and gas properties for any need for impairment.

This is performed in conjunction with each balance sheet date or if there are events or changes in

circumstances that indicate that carrying values of assets may not be recoverable.

Such indicators include changes in the Group’s business plans, relinquished licences, changes in raw

materials prices leading to lower revenues and, for oil and gas properties, downward revisions of

estimated reserve quantities.

Testing for impairment losses is performed for each cash generating unit, which corresponds to

licence right, production sharing agreement or equivalent owned by PA Resources. A cash generating

unit thus usually corresponds to each acquired asset in each country in which PA Resources carries

on exploration and development operations. Impairment testing means that the balance sheet item

PA RESOURCES ANNUAL REPORT 2015 30

amount for each cash generating unit is compared to the recoverable amount for the assets, which is

the higher of the fair value of the assets less sales expenses and the value in use. The value in use of

the assets is based on the present value of future cash flows discounted by weighted average cost of

capital (WACC ); see also Note 16 Impairment testing exploration and evaluation assets and oil and

gas properties. An impairment loss is recorded when an asset’s or a cash generating unit’s recorded

value exceeds the value in use. Impairment losses are charged to the income statement.

Reversal of impairment losses

At least once every year an assessment is made as to whether there are any indications that

impairment losses reported previously are no longer justified or have reduced in extent. If such

indications exist, a new calculation of the recoverable amount is made. A previously recognised

impairment loss is reversed only to the extent that the asset’s reported value after reversal does not

exceed the reported value the asset would have had if the impairment loss had never been

recognised.

If this is the case, the book value of the asset is increased to its recoverable amount. After a reversal

the depreciation charge is adjusted in future periods to distribute the asset’s revised book value over

its expected remaining useful life.

Inventory

Outstanding inventory consist of other supplies and materials and is valued at the lower of cost and

net realizable value. When assessing obsolescence of inventory items, consideration is given to the

age of the inventory, the material and the rate of turnover. Any impairment of the inventory affects

operating profit.

Under- or overlift positions of hydrocarbons

PA Resources’ under- or overlift position of hydrocarbons is reported as if they had been sold at the

balance sheet date. Valuation is performed either based on the Brent spot price at the respective

balance sheet date taking any discounts or premiums into consideration, or according to the

prevailing contract price. An underlift position is included in Accounts receivable and other

receivables, while an overlift position is included in Accounts payable and other liabilities. A change

in the under- or overlift position is reflected in the income statement as Revenue.

Financial instruments

PA Resources’ financial instrument assets comprise accounts receivable and other receivables, other

financial non-current assets and cash and cash equivalents.

The assets can, on occasion, also comprise derivatives for which hedging has been performed by the

Group with respect to matching the interest-bearing liability to the corresponding asset’s currency

risk. Financial instrument liabilities comprise interest-bearing loans and borrowings and the short-

term portion thereof, derivatives, for which hedging has been performed, as well as accounts

payable and other liabilities.

Recognition and derecognition in the balance sheet

PA Resources reports a financial asset or a financial liability in the balance sheet when the company

becomes a party to the instrument’s contractual terms. The company derecognises a financial

liability or part thereof when the obligation stated in the relevant contract is fulfilled or otherwise

terminated.

PA Resources currently reports all its financial instruments gross, but net reporting is possible where

there is a legal right of offset. Recognition and Derecognition in the balance sheet are reported on

PA RESOURCES ANNUAL REPORT 2015 31

the transaction date, which is the day on which PA Resources undertakes to acquire or sell the

financial instrument in question.

Classification by means of measurement

Initial measurement

PA Resources initially recognises its financial instruments at fair value plus a supplement for directly

attributable transaction expenses, usually the transaction price. This principle is applied to all

financial instruments apart from those in the category financial assets or liabilities carried at fair

value through profit or loss, which are recognised at fair value excluding transaction expenses.

Except for what is described above under Non-going concern, this category comprises only

derivatives.

PA Resources classifies its financial instruments in the following categories based on the purpose for

which the instrument was acquired. This classification generally forms a basis for how the financial

instrument is measured after it is first reported. On each closing date the company tests all its

financial assets for impairment, apart from those in the category financial assets or liabilities carried

at fair value through profit or loss.

In the Parent company the same measurement principles are applied, subject to the restrictions

contained in Chapter 4 § 14 of the Swedish Annual Accounts Act; at present these restrictions result

in no differences between the Parent company and the Group.

After initial recognition, the company’s financial instruments are reported as described below.

Subsequent measurement

Financial assets measured at fair value through profit or loss

In this category PA Resources classifies derivatives with a positive fair value as a separate

subcategory. These are continually measured at fair value with changes in value through profit or

loss. At present PA Resources has no hedging instruments that are identified as effective, and instead

reports all its positive derivatives in this subcategory. PA Resources held no assets or liabilities under

this category at year-end or at the end of the preceding year.

Loans and receivables

PA Resources classifies mainly receivables generated by the company in its operations in this

category, but acquired receivables can also be included. At present it contains deposits for leased

drilling equipment, accounts receivable, receivables from partners, accrued interest income, accrued

income from oil inventories and cash and cash equivalents. These are measured at amortised cost,

using the effective interest method established at the time of acquisition.

Where accounts receivable are concerned, provision for impairment is made if there is objective

evidence that the Group will not receive the amount due according to the original terms of the

receivables. Impairment of accounts receivable is reported in the operating result.

Available-for-sale financial assets

PA Resources sees this category as a residual category containing long-term assets not classified in

any other category. For the current year, as well as for the comparative period, there are no assets in

this category.

The assets are measured at fair value directly through other comprehensive income, except where

impairment is applied. No impairment was applied during the year and any change in value is

recognised in other comprehensive income.

PA RESOURCES ANNUAL REPORT 2015 32

Financial liabilities measured at fair value through profit or loss

In this category PA Resources classifies derivatives with a negative fair value as a separate

subcategory. These are continually measured at fair value with changes in value through profit or

loss. At present PA Resources has no hedging instruments that are identified as effective, and instead

reports all its negative derivatives in this subcategory. Except for what is described above under Non-

going concern, PA Resources held no assets or liabilities under this category at year-end or at the end

of the preceding year.

Other financial liabilities

Except for what is described above under Non-going concern, PA Resources includes in this category

Interest-bearing loans and borrowings, which are measured at amortised cost using the effective

interest method which is the category’s main assessment method. Within this category, secured

loans can be measured at fair value. However, at present there are no loans that are secured. The

company also places in this category accounts payable, the short-term portion of interest-bearing

loans and borrowings as well as other financial liabilities such as liabilities to partners as well as

accrued interest expenses and accrued exploitation and drilling expenses.

Compound financial instruments

A compound financial instrument contains both a liability component and an equity component,

which are each classified separately. PA Resources reports its convertible debentures in this way,

with the liability component reported under Interest-bearing loans and borrowings within the

category Other financial liabilities.

Measurement of fair value

PA Resources bases the fair value of financial instruments depending on available market data at

time of valuation. Data are categorised into three categories; Level 1: quoted prices in active

markets. Level 2: valuation based on observable market data. Level 3: valuation techniques incorpor-

ating information other than observable market data. The reported value – after any impairment – of

accounts receivable and accounts payable is assumed to equate to their fair value, since these entries

are short-term in nature.

Embedded derivatives

An embedded derivative is a contract with derivative-like properties, but which forms part of another

contract. An embedded derivative is to be distinguished from the host contract and recognised as a

separate derivative where the economic properties and risks are not closely related to those of the

host contract. PA Resources holds embedded derivatives in its bond loans, known as call options,

which means that the company can call for early redemption at a value in excess of the nominal

amount. However, these are considered to be closely related, and as a result they are not reported

separately.

Borrowing costs

Borrowing costs are capitalised when these refer to the purchase, construction or production of

assets which necessarily take considerable time to complete for their intended use or sale.

Capitalisation only takes place if it is assessed that this will involve probable economic advantage.

Interest on loans referring to the acquisition and development of oil and gas properties, for which

the borrowing costs can be included in the acquisition value, is capitalised during the period of time

necessary to finalise the work and complete the asset for its intended use. Capitalisation of interest

expenditures is begun when an acquisition is made and when investment and development costs

arise, either in the oil and gas properties where the Group is operator or as allocated through

PA RESOURCES ANNUAL REPORT 2015 33

invoices from operators of oil and gas properties in which the Group is a partner. The interest is