Embed Size (px)

DESCRIPTION

Overview of the reasons why there is a change in how transportation are financed. Chicago, May 14, 2007 Pedro A. Losada, Head of North American Project Finance. CINTRA –www.cintra.es. Transportation Infrastructure Developer Value creation through long term investments on toll roads - PowerPoint PPT Presentation

Citation preview

Overview of the reasons why there is a change in how transportation are

financed.

Chicago, May 14, 2007

Pedro A. Losada,

Head of North American Project Finance

6 October 2005

6 October 2005

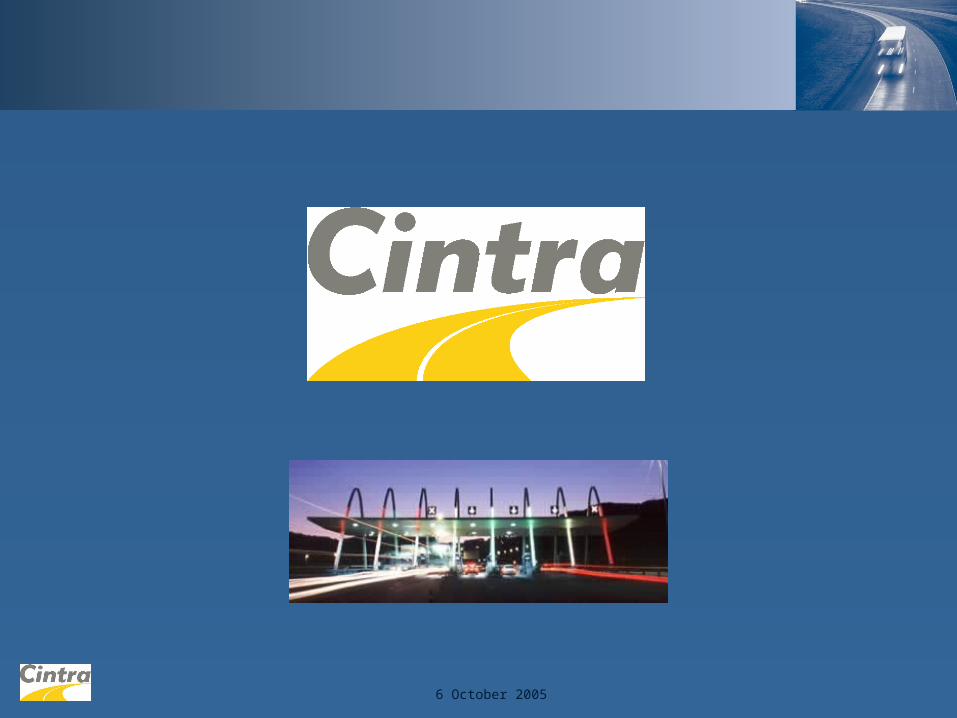

CINTRA – www.cintra.es

Transportation Infrastructure Developer Value creation through long term investments on toll roads

Since 1968 & for the long term – Bilbao Behobia

Listed in the Madrid (Spain) Stock Exchange Market cap $ 9 bn 62% of Cintra is held by Ferrovial (www.ferrovial.com)

20 road concessions in actual portfolio 2,500 miles Asset value $12 bn; equity investment $2.3 bn Canada, US, Spain, Chile, Ireland, Portugal and Greece 62% average controlling stake Remaining concession terms ranging from 11 to 99 years (weighted average 73 yrs)

Skilled project finance team $12 bn in non-recourse private debt structured since 1987 Wrapped and unwrapped bonds; bridge, mini-perm and long term bank loans

6 October 2005

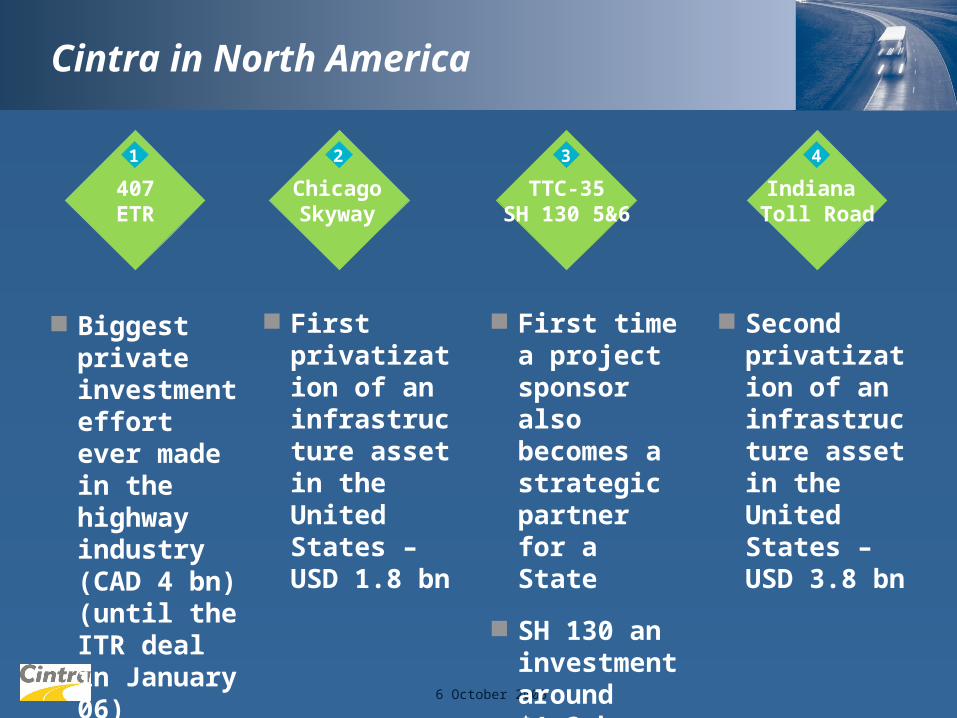

407 ETR

1

Chicago Skyway

2

TTC-35SH 130 5&6

3

Cintra in North America

First privatization of an infrastructure asset in the United States – USD 1.8 bn

First time a project sponsor also becomes a strategic partner for a State

SH 130 an investment around $1.3 bn

Indiana Toll Road

4

Second privatization of an infrastructure asset in the United States – USD 3.8 bn

Biggest private investment effort ever made in the highway industry (CAD 4 bn) (until the ITR deal in January 06)

6 October 2005

Options when financing PPPs

6 October 2005

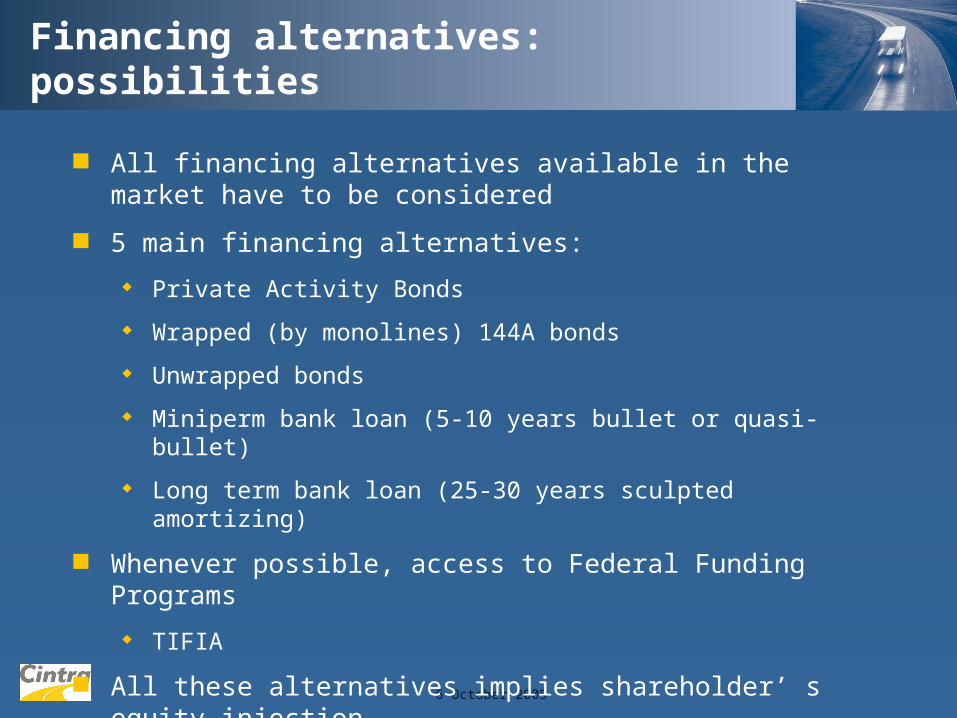

Financing alternatives: possibilities

All financing alternatives available in the market have to be considered

5 main financing alternatives:

Private Activity Bonds

Wrapped (by monolines) 144A bonds

Unwrapped bonds

Miniperm bank loan (5-10 years bullet or quasi-bullet)

Long term bank loan (25-30 years sculpted amortizing)

Whenever possible, access to Federal Funding Programs

TIFIA

All these alternatives implies shareholder’ s equity injection

Detailed analysis required on a case by case basis

seeking optimal financing conditions tailored for each project

6 October 2005

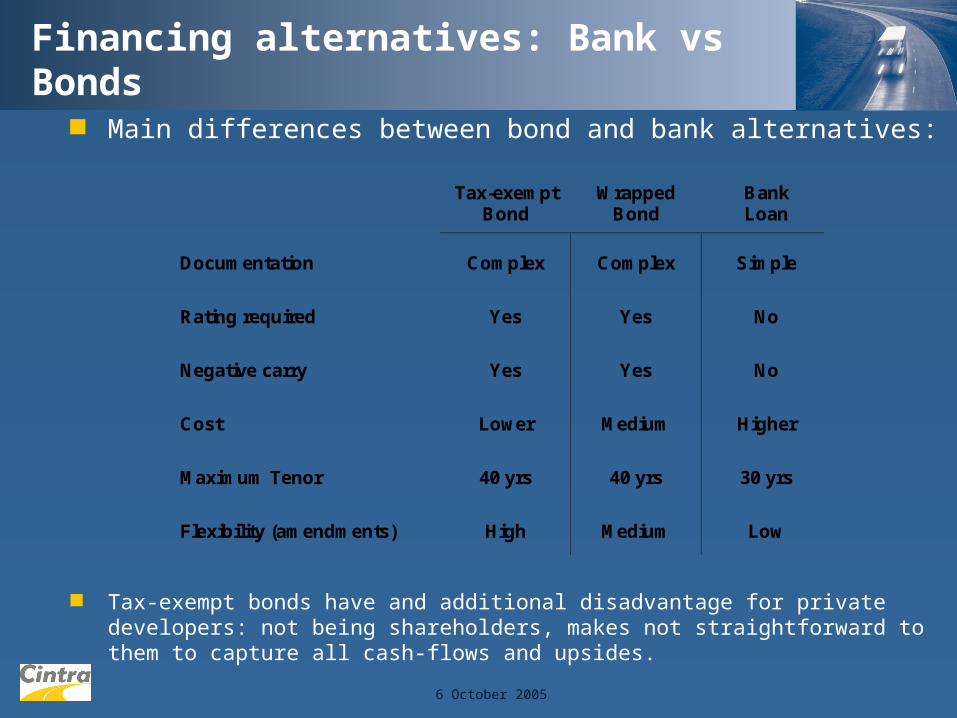

Financing alternatives: Bank vs Bonds

Main differences between bond and bank alternatives:

Tax-exempt bonds have and additional disadvantage for private developers: not being shareholders, makes not straightforward to them to capture all cash-flows and upsides.

Tax-exemptBond

WrappedBond

BankLoan

Documentation Complex Complex Simple

Rating required Yes Yes No

Negative carry Yes Yes No

Cost Lower Medium Higher

Maximum Tenor 40 yrs 40 yrs 30 yrs

Flexibility (amendments) High Medium Low

6 October 2005

Financing alternatives: Cintra’s experience

Wrapped bonds: Autopista del Maipo (US-144A & Chile); Talca-Chillán (Chile); Collipulli-Temuco (Chile); Euroscut Algarve (Portugal): Chicago Skyway (US).

Unwrapped bonds: 407-ETR (Canada)

Miniperm bank loan: Chicago Skyway (US); Radial 4 (Spain); Ocaña-La Roda (Spain); Ausol (Spain).

Long term bank loan: Eurolink (Ireland); Temuco-RioBueno (Chile); Norte Litoral (Portugal); M-45 (Spain).

In addition, Cintra team has experience in financing airports and car parks (among others: Sydney Airport, Bristol Airport, Belfast City Airport).

6 October 2005

Main reasons of the change

High Market’s liquidity

Competitive financial covenants

Aggressive financial structures

Non breakage costs and no negative carry (Greenfields)

Quick transaction's execution

Reserves requirements

Refinancing risk

Access to new instruments available in the marketplace

Concession Term

Competitive process (Ag. Rating)

6 October 2005

Chicago Skyway case study

6 October 2005

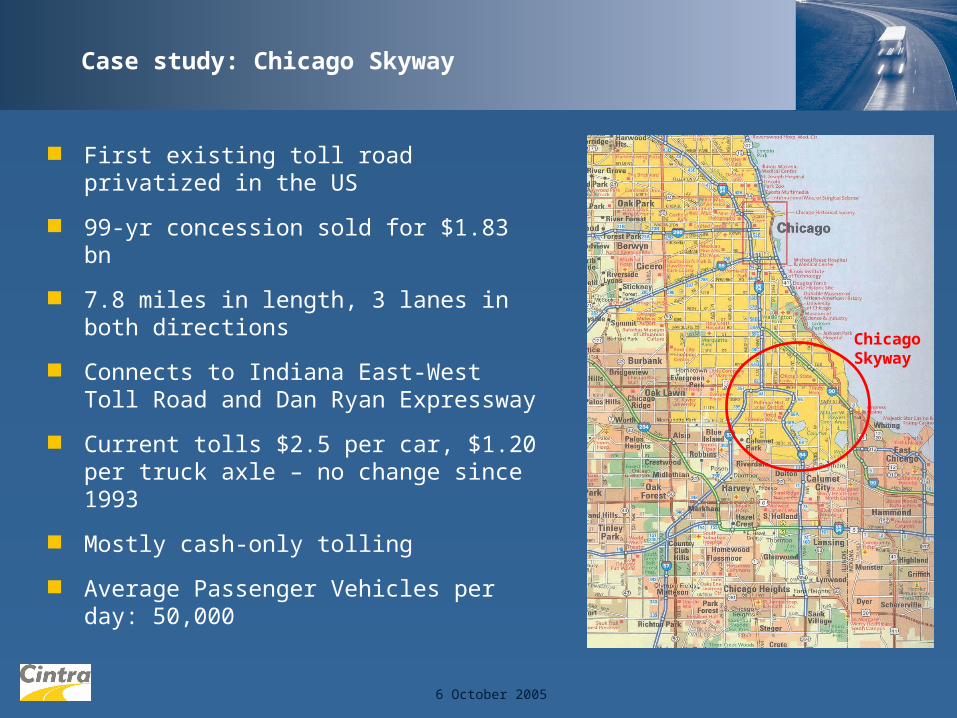

Case study: Chicago Skyway

ChicagoSkyway

First existing toll road privatized in the US

99-yr concession sold for $1.83 bn

7.8 miles in length, 3 lanes in both directions

Connects to Indiana East-West Toll Road and Dan Ryan Expressway

Current tolls $2.5 per car, $1.20 per truck axle – no change since 1993

Mostly cash-only tolling

Average Passenger Vehicles per day: 50,000

6 October 2005

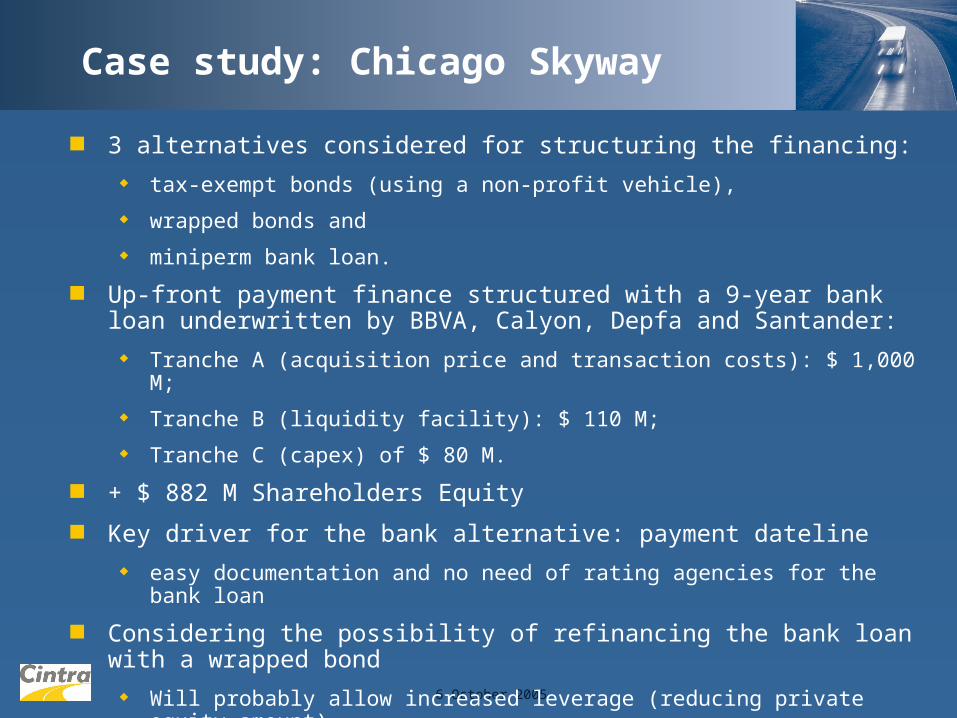

Case study: Chicago Skyway

3 alternatives considered for structuring the financing:

tax-exempt bonds (using a non-profit vehicle),

wrapped bonds and

miniperm bank loan.

Up-front payment finance structured with a 9-year bank loan underwritten by BBVA, Calyon, Depfa and Santander:

Tranche A (acquisition price and transaction costs): $ 1,000 M;

Tranche B (liquidity facility): $ 110 M;

Tranche C (capex) of $ 80 M.

+ $ 882 M Shareholders Equity

Key driver for the bank alternative: payment dateline

easy documentation and no need of rating agencies for the bank loan

Considering the possibility of refinancing the bank loan with a wrapped bond

Will probably allow increased leverage (reducing private equity amount)

6 October 2005

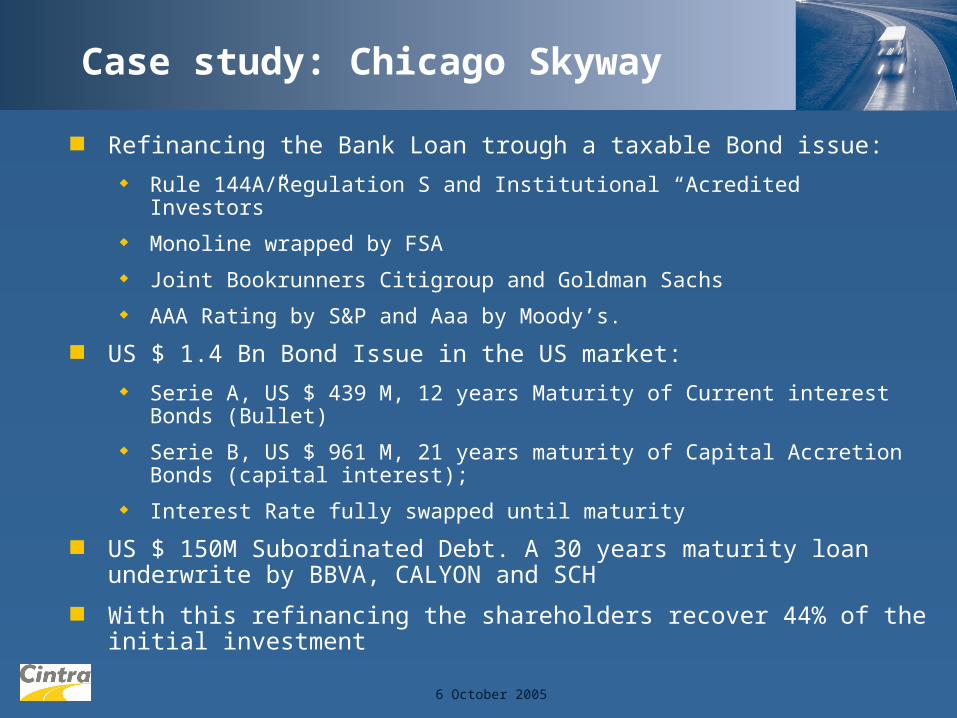

Case study: Chicago Skyway

Refinancing the Bank Loan trough a taxable Bond issue:

Rule 144A/Regulation S and Institutional “Acredited Investors”

Monoline wrapped by FSA

Joint Bookrunners Citigroup and Goldman Sachs

AAA Rating by S&P and Aaa by Moody’s.

US $ 1.4 Bn Bond Issue in the US market:

Serie A, US $ 439 M, 12 years Maturity of Current interest Bonds (Bullet)

Serie B, US $ 961 M, 21 years maturity of Capital Accretion Bonds (capital interest);

Interest Rate fully swapped until maturity

US $ 150M Subordinated Debt. A 30 years maturity loan underwrite by BBVA, CALYON and SCH

With this refinancing the shareholders recover 44% of the initial investment

6 October 2005

Questions…

Questions… … thank you!

www.cintra.es

![Martha’s Vineyard DRAFT Transportation Improvement Program …€¦ · June-July 2016 "The preparation of this report has been financed in part through grant[s] from the Federal](https://img.pdfslide.us/doc/110x75/5fc7fe16ebaeaf268c473757/marthaas-vineyard-draft-transportation-improvement-program-june-july-2016-the.jpg)