Embed Size (px)

Citation preview

OVERVIEW OF THE OECD’S WORK ON COUNTERING INTERNATIONAL TAX EVASION

A Back Briefground Information

21 September 2009

For more information please contact:

Jeffrey Owens ([email protected]) or Pascal SaintAmans (pascal.saint[email protected])

of the OECD Centre for Tax Policy and Administration

Overview of the OECD’s Work on Countering International Tax Evasion

2 21 September 2009

Re rogr ss in implementing standards of transparency and exchange of information

1. The principles of transparency and exchange of information developed by the OECD’s Global Forum on Transparency and Exchange of Information have been accepted by countries around the world. In October 2008 the UN Committee of Experts on International Cooperation in Tax Matters incorporated these principles into its own model tax convention, clearly establishing the Global Forum standard as the internationally agreed standard for exchange of information and transparency in tax matters. On 2 April 2009 the OECD issued a Progress Report on the implementation of the internationally agreed tax standard for the 84 jurisdictions 1

cent p e

that participate in the Global Forum’s annual assessment of the legal and administrative framework for transparency and exchange of information. The Report shows that real progress has been made, both in terms of how widely the standards are accepted and the extent to which they have been implemented. Nonetheless, a great deal of work remains to make sure that all jurisdictions accept these principles, and to guarantee that jurisdictions that have made a commitment to implement the standard now follow through. The Global Forum will have to adapt to these new demands by providing a monitoring process that takes all relevant factors into account.

2. Since the beginning of 2009, international tax evasion and the implementation of the internationally agreed tax standard has been very high on the political agenda, reflecting recent scandals that have affected countries around the world, the spotlight that the global financial crisis has put on financial centres generally, and the recent G20 London Summit. In July 2008, the G8 Heads of State and Government urged “all countries that have not yet fully implemented the OECD standards of transparency and effective exchange of information in tax matters to do so without further delay, and encourage the OECD to strengthen its work on tax evasion and report back in 2010. 2 ” Similarly, the action plan issued by the G20 following its meeting in November 2008 recognised the importance of the OECD work in this area and urged that failures to implement the standards should be “vigorously addressed”. At its London Summit, the G20 followed up its Washington commitment by a strong call for action. This heightened political attention has led to a number of significant and positive developments among financial centres since the G20 met in November 2008:

• All OECD countries now accept Article 26 (Exchange of Information) of the OECD Model Tax Convention, as updated in 2005, following the withdrawal by Austria, Belgium, Luxembourg and Switzerland of their reservations to Article 26. These four countries are actively negotiating updates to their treaty networks. Belgium and Luxembourg have already signed at least 12 agreements that meet the standard and Switzerland has initialled 12 with OECD countries.

• Hong Kong (China), Macao (China) and Singapore – three jurisdictions that are amongs those surveyed by the Global Forum ‐ have each announced that they will put forward

e x rrelevant legislation in 2009 in order to comply with the internationally agr ed ta standa d.

• More than 90 tax information exchange agreements (TIEAs) have been signed or announced since last November, and over 130 TIEAs have been signed overall. In addition, scores more have already been initialled or are being negotiated.

1 The 84 jurisdictions consist of the OECD countries, the tax havens identified in 2000, countries that participate in the OECD’s Committee on Fiscal Affairs as Observers, and the financial centres identified in the

ing. outcomes of the Berlin 2004 Global Forum meet2 See Annex I for statements by the G7/G8/G20.

Overview of the OECD’s Work on Countering International Tax Evasion

21 September 2009 3

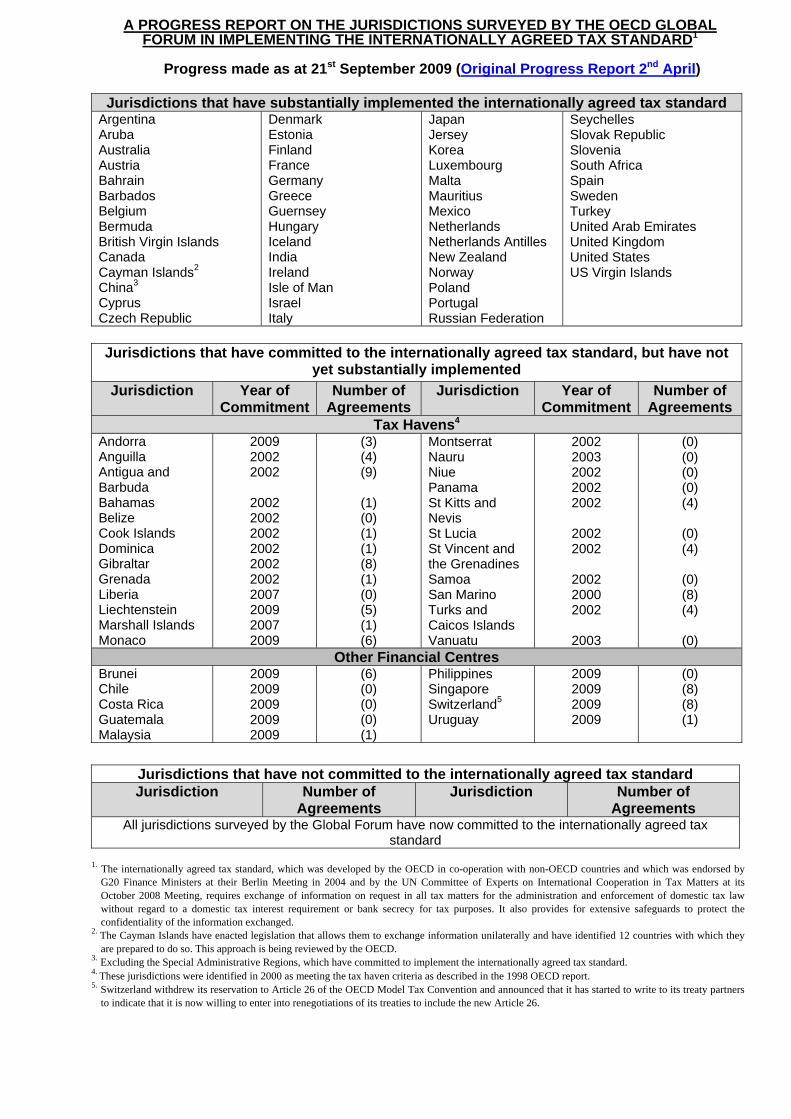

• Andorra, Liechtenstein and Monaco – identified by the OECD in 2002 as un‐cooperative tax havens – have endorsed the OECD standards and indicated their willingness to change their domestic legislation and to enter into agreements for the exchange of information. Each of

tthese jurisdictions has already signed i s first agreements.

• Since the issuance of the 2nd April Progress Report, 9 jurisdictions – Aruba, Austria, Belgium, Bermuda, British Virgin Islands, Bahrain, Cayman Islands, Luxembourg, Netherlands Antilles – have signed enough agreements so that they can now be considered

ntto have substantially impleme ed the internationally agreed tax standard.

• Prior to the issuance of the 2nd April Progress Report, Brunei and Guatemala wrote to the OECD to formally endorse the internationally agreed tax standard and identify the steps

or ttaken o be taken this year to implement the standard.

• Costa Rica, Malaysia, the Philippines and Uruguay, originally identified in the 2nd April Progress Report as not having endorsed the internationally agreed tax standard, have now done so and have identified concrete steps to be taken this year to implement it.

• With these endorsements, all countries surveyed by the Global Forum have now endorsed the standard.

3. These policy changes represent a very significant step toward a level playing field as regards exchange of information for tax purposes. However, these must now be followed up with swift and consistent implementation, which the OECD will closely monitor. France and Germany organised a ministerial meeting on 21 October 2008 to discuss the issue of international tax evasion and the implementation of the OECD standards. A follow‐up meeting took place in June 2009 and issued a Communiqué endorsed by all 21 participating countries. On an individual basis, a number of countries have announced measures to combat tax evasion and encourage jurisdictions to implement the internationally agreed standards. For example, Canada, Italy and Australia have each recently adopted rules that link benefits or adverse consequences to the existence of full information exchange for tax purposes. Germany has passed legislation that would impose adverse tax consequences on transactions involving jurisdictions that do not exchange information in tax matters to the internationally agreed standards.

Th dards f Tr nsparency and Exchange of Information

4. OECD and non‐OECD countries working together in the OECD’s Global Forum on Transparency and Exchange of Information (see below) have developed standards of transparency and exchange of information that were adopted by the G20 Ministers of Finance at a meeting in Berlin (Germany) in 2004, Xianghe (China) in 2005 and by the UN Committee of Experts on International Cooperation in Tax Matters in October 2008. They serve as a model for the vast majority of the 3600 bilateral tax conventions entered into by OECD and non OECD countries and

y now ternational norm for tax cooperation.

e Stan o a

ma be considered as the in

5. standarThe ds require:

• Exchange of information on request where it is “foreseeably relevant” to the .administration and enforcement of the domestic laws of the treaty partner

• No restrictions on exchange caused by bank secrecy or domestic tax interest requirements.

Overview of the OECD’s Work on Countering International Tax Evasion

21 September 2009 4

• Availability of reliable information and powers to obtain it.

• Respect for taxpayers’ rights.

• Strict confidentiality of information exchanged.

Th ’s Harmful Tax Practices Project

6. The challenge of combating offshore tax evasion is not new, but it has grown more complex and more serious given the increased scope for illicit use of the international financial system in a globalised world . The OECD has been working on this issue since 1996, when the harmful tax practices project was launched. This initiative is carried out through the Forum on Harmful Tax Practices, a subsidiary body of the Committee on Fiscal Affairs (CFA) , and has consistently garnered the support of the international community. The standards developed by the OECD’s Global Forum in this area have been endorsed by the G 7/8, G20, the UN Committee of Experts on International

e OECD

Cooperation in Tax Matters, the EU and other international bodies.

7. The first major output of the Forum on Harmful Tax Practices was the 1998 Report, Harmful Tax Competition: An Emerging Global Issue 3 . The publication of this report initiated a period of intense dialogue aimed at eliminating preferential tax regimes within OECD member states, identifying “tax havens” and seeking their commitments to the principles of transparency and effective exchange of information and encouraging other non‐OECD economies to associate themselves with the harmful tax practices work.

Ha Tax Regimes

8. The project has been very successful. By 2004, all but one of the preferential tax regimes identified within the OECD had been abolished, amended or found not to be harmful. The only outstanding regime was the Luxembourg 1929 holding company regime. In December 2006 Luxembourg enacted legislation to abolish the regime by the end of 2010.

rmful Preferential

Tax n Work

9. In a report issued in 2000, the OECD identified a number of jurisdictions which it categorised as tax havens according to criteria it had established 4

Have

, 6 of them (Bermuda, Cayman Islands, Cyprus, Malta, San Marino, The Bahamas) made pre‐commitments to the standard and so were not included in the list. Between 2000 and 2002 the OECD worked with these jurisdictions to secure their commitment to implement the OECD’s standards of transparency and exchange of information. In all, 35 jurisdictions made formal commitments to implement these principles,

mbourg and Switzerland abstained in the approval o3 Luxe f the report.

4 See Harmful Tax Competition: An Emerging Global Issue (OECD, 1998), pp 21‐25.The four key factors are: No or nominal tax on the relevant income.; No effective exchange of information in respect of taxpayers benefiting from the low tax jurisdiction; Lack of transparency in the operation of the legislative, legal or administrative provisions; The absence of a requirement that the activity be substantial is important since it suggests that a jurisdiction may be attempting to attract investment or transactions that are purely tax driven. No or nominal tax is not sufficient in itself to classify a country as a tax haven.

Overview of the OECD’s Work on Countering International Tax Evasion

21 September 2009 5

including a number of jurisdictions that had already committed to these standards prior to the issuance of the report. 5

The al Forum on Transparency and Exchange of Information

10. The jurisdictions that have made commitments to transparency and effective exchange of information, both OECD and non‐OECD jurisdictions, have worked together in the Global Forum to develop the international standards for transparency and effective exchange of information in tax matters. A major achievement of this collaboration was the 2002 Model Agreement on Exchange of Information on Tax Matters. This model has been used as the basis for the negotiation of over 100

s 6 .

Glob

TIEA

11. The Global Forum met in Berlin in 2004 to discuss the fact that not all jurisdictions had shown the same willingness to implement the OECD standards and determine what was needed to promote the establishment of a global level playing field. The outcomes of that meeting outlined a series of steps involving individual, bilateral and collective actions which would be needed to both achieve and maintain the goal of a level playing field. These steps were further elaborated following the Global Forum meeting in Melbourne in 2005 7 . In addition, the Global Forum established the Sub‐

p onGrou Level Playing Field Issues to help carry this work further.

12. To help achieve a level playing field, jurisdictions were encouraged to fully implement the principles of transparency and exchange of information for tax purposes. Further, they were asked to review their policies in relation to six specific areas and report the outcome of their reviews at the next meeting of the Global Forum. Jurisdictions were also encouraged to negotiate agreements

allowing for the exchange of information in tax matters.

13. Since 2006, the Global Forum has published annual assessments of the legal and administrative framework for transparency and exchange of information in 84 countries. The last update was published in September 2009 as Tax Cooperation 2009: Towards a Level Playing Field – 2009 Assessment by the Global Forum on Transparency and Exchange of Information (www.oecd.org/ctp/htp/cooperation). The Sub‐Group on Level Playing Field Issues agreed that the 2009 assessment should highlight more clearly the distinction between those jurisdictions that are making progress and those that are not, by providing a simple, factual summary of the legal and administrative framework for transparency and exchange of information in place in a given country. This approach will make it easier to identify what strengths and weaknesses a jurisdiction has regarding its ability to exchange information for tax purposes. Furthermore, it was agreed that positive recognition would be provided for jurisdictions having concluded at this point in time at least 12 agreements that meet the internationally agreed standard.

5 See Towards Global Tax Cooperation: Progress in Identifying and Eliminating Harmful Tax Practices (2000) for a detailed history of the tax haven criteria and the development of these lists. 6 See Annex II for a list of TIEAs signed between OECD members and jurisdictions which have committed to the OECD’s standards of transparency and exchange of information. 7 For more information about the creation of the Sub‐Group and the Global Forum’s work on the establishment of a global level playing field see A Process for Achieving a Global Level Playing Field: Outcomes of the Berlin Global Forum Meeting (June 2004) and Progress Towards a Level Playing Field: Outcomes of the Melbourne Global Forum Meeting (15‐16 November 2005).

Overview of the OECD’s Work on Countering International Tax Evasion

21 September 2009 6

Imp g Compliance

15. The CFA also investigates how member governments can co‐operate to minimise the extent of tax evasion and avoidance. In this regard it has mandated a focus group to study the role that no

14. The Global Forum met in Mexico on September 1‐2 to discuss progress made in implementing the international standards, and how to respond to international calls to strengthen the work of the Global Forum. The main objectives for the meeting were to:

• Agree on restructuring the OECD Global Forum to expand its membership and ensure its members participate on an equal footing;

• Agree on how to establish an in‐depth peer review process to monitor and review progress made towards full and effective exchange of information; and

• Identify mechanisms to speed‐up the negotiation and conclusion of agreements to exchange information and to enable developing countries to benefit from the new more cooperative

tax environment.

Participants agreed that:

The Global Forum should be strengthened and restructured as

• All OECD, G20 and other jurisdictions covered by the 2009 Assessment should be invited to be members of the Global Forum

• The Global Forum will be the decision‐making body.

• In order to carry out an in‐depth monitoring and peer review of the implementation of the standards of transparency and exchange of information for tax purposes, the Global Forum agreed on the setting up of a Peer Review Group (PRG) to develop the methodology and detailed terms of reference for a robust, transparent and accelerated process.

• A report to the G20 on the outcomes from the meeting was agreed upon and will now be 2009 meetings. submitted to the G20 Finance Ministers and leaders for the September

• The first meeting of the Peer Review Group will take place in October.

For the full outcomes of the meeting, see www.oecd.org/tax/globalforum/loscabos

Acc Bank Information for Tax Purposes

14. In parallel with the work on harmful tax practices, the CFA is examining the extent to which OECD Member countries and observer countries have access to bank information for tax purposes. In 2000, Improving Access to Bank Information for Tax Purposes was published. The report set out an ideal standard of access to bank information, namely, that “all Member countries should permit access to bank information, directly or indirectly, for all tax purposes so that tax authorities can fully discharge their revenue raising responsibilities and engage in effective exchange of information with their treaty partners”. The CFA has been closely monitoring the progress made in implementing this standard and has issued two progress reports, in 2003 and 2007. With the recent announcements by Austria, Belgium, Luxembourg and Switzerland, all OECD countries now endorse this standard.

ess to

rovin

Overview of the OECD’s Work on Countering International Tax Evasion

21 September 2009 7

or nominal tax jurisdictions play in tax evasion. This work is intended to both identify particular challenges that these jurisdictions pose for tax administrations and to help administrations adopt best practices. The CFA is also examining the effectiveness of offshore compliance initiatives launched by OECD and non‐OECD countries.

16. Another important aspect of compliance work is carried out through the OECD’s Forum on Tax Administration (FTA), established by the CFA in 2002, which brings together tax commissioners from over 40 countries to promote cooperation between revenue bodies and to develop good tax administration practices. Over the last few years the FTA has examined a wide range of issues in the areas of compliance risk management, taxpayer services, and use of modern technology. At Seoul, Korea in September 2006, the FTA agreed to work together on ways to improve tax administration and to address the significant and growing problem of international non‐compliance with national tax requirements. The Seoul Declaration (www.oecd.org/ctp/ta/seouldeclaration) issued in conjunction with that meeting identified four areas in which the tax administration heads planned to intensify existing work or initiate new work under the auspices of the OECD, including:

• further developing a directory of aggressive tax planning schemes to assist member countries identify trends and measures to counter such schemes; and

• an examination of the role of tax intermediaries in relation to the promotion of unacceptable tax minimization arrangements;

17. At their subsequent meeting in January 2008 in Cape Town, South Africa ‐‐ the outcomes of which are set out in the Cape Town Communiqué ‐‐ the FTA Commissioners endorsed the conclusions and recommendations of the Study into the Role of Tax Intermediaries. The scope of this study was widened following the Seoul meeting to examine the tripartite relationship between large business taxpayers, revenue bodies and tax intermediaries on the basis that taxpayers represented the demand side of ‘’unacceptable tax minimisation arrangements’’. The Commissioners also noted the further progress with the development of the directory of aggressive tax planning schemes. In addition, responding to a recommendation of tax intermediaries' study, they commissioned further follow‐up studies involving the tax planning activities of high‐net‐worth individuals and banks. These studies were finalised and published in June 2009.

A PROGRESS REPORT ON THE JURISDICTIONS SURVEYED BY THE OECD GLOBAL FORUM IN IMPLEMENTING THE INTERNATIONALLY AGREED TAX STANDARD1

Progress made as at 21st September 2009 (Original Progress Report 2nd April)

Jurisdictions that have substantially implemented the internationally agreed tax standard

Argentina Aruba Australia Austria Bahrain Barbados Belgium Bermuda British Virgin Islands Canada Cayman Islands2 China3 Cyprus Czech Republic

Denmark Estonia Finland France Germany Greece Guernsey Hungary Iceland India Ireland Isle of Man Israel Italy

Japan Jersey Korea Luxembourg Malta Mauritius Mexico Netherlands Netherlands Antilles New Zealand Norway Poland Portugal Russian Federation

Seychelles Slovak Republic Slovenia South Africa Spain Sweden Turkey United Arab Emirates United Kingdom United States US Virgin Islands

Jurisdictions that have committed to the internationally agreed tax standard, but have not

yet substantially implemented Jurisdiction Year of

Commitment Number of

Agreements Jurisdiction Year of

Commitment Number of

Agreements Tax Havens4

Andorra Anguilla Antigua and Barbuda Bahamas Belize Cook Islands Dominica Gibraltar Grenada Liberia Liechtenstein Marshall Islands Monaco

2009 2002 2002

2002 2002 2002 2002 2002 2002 2007 2009 2007 2009

(3) (4) (9)

(1) (0) (1) (1) (8) (1) (0) (5) (1) (6)

Montserrat Nauru Niue Panama St Kitts and Nevis St Lucia St Vincent and the Grenadines Samoa San Marino Turks and Caicos Islands Vanuatu

2002 2003 2002 2002 2002

2002 2002

2002 2000 2002

2003

(0) (0) (0) (0) (4)

(0) (4)

(0) (8) (4)

(0)

Other Financial Centres Brunei Chile Costa Rica Guatemala Malaysia

2009 2009 2009 2009 2009

(6) (0) (0) (0) (1)

Philippines Singapore Switzerland5 Uruguay

2009 2009 2009 2009

(0) (8) (8) (1)

Jurisdictions that have not committed to the internationally agreed tax standard Jurisdiction Number of

Agreements Jurisdiction Number of

Agreements All jurisdictions surveyed by the Global Forum have now committed to the internationally agreed tax

standard

1. The internationally agreed tax standard, which was developed by the OECD in co-operation with non-OECD countries and which was endorsed by G20 Finance Ministers at their Berlin Meeting in 2004 and by the UN Committee of Experts on International Cooperation in Tax Matters at its October 2008 Meeting, requires exchange of information on request in all tax matters for the administration and enforcement of domestic tax law without regard to a domestic tax interest requirement or bank secrecy for tax purposes. It also provides for extensive safeguards to protect the confidentiality of the information exchanged.

2. The Cayman Islands have enacted legislation that allows them to exchange information unilaterally and have identified 12 countries with which they are prepared to do so. This approach is being reviewed by the OECD.

3. Excluding the Special Administrative Regions, which have committed to implement the internationally agreed tax standard. 4. These jurisdictions were identified in 2000 as meeting the tax haven criteria as described in the 1998 OECD report. 5. Switzerland withdrew its reservation to Article 26 of the OECD Model Tax Convention and announced that it has started to write to its treaty partners

to indicate that it is now willing to enter into renegotiations of its treaties to include the new Article 26.

COUNTERING OFFSHORE TAX EVASION

Some Questi the Projectons and Answers on

21 September 2009

For more information please contact:

Jeffrey Owens ([email protected]) or Pascal SaintAmans (pascal.saint[email protected])

of the OECD Centre for Tax Policy and Administration

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 10

The document was issued by the OECD Secretariat at the conclusion of the G20’s London Summit. It is a progress report on the implementation of the internationally agreed tax standard that identifies (i) jurisdictions that have substantially implemented the standard, (ii) other jurisdictions that have committed to but not yet implemented the standard and tax havens that have committed to but not yet implemented the standard, and (iii) jurisdictions

What is the status of the progress report issued on 2 April?

that have not committed to the standard.

With the commitments of Costa Rica, Malaysia, the Philippines and Uruguay, all jurisdictions covered in the Global Forum’s assessments have now agreed

to implement the standard.

The progress report will be regularly updated as jurisdictions sign new eagre ments.

The internationally agreed tax standard on exchange of information, as developed by the OECD and endorsed by the UN and the G20, provides for full exchange of information on request in all tax matters without regard to a domestic tax interest requirement or bank secrecy for tax purposes. It also provides for extensive safeguards to protect the confidentiality of the

What is the internationally agreed tax standard?

information exchanged.

The countries covered by the Progress Report are those which have been surveyed by the OECD’s Global Forum on Taxation. The Global Forum survey covers the 30 OECD countries, countries that participate in the OECD’s Committee on Fiscal Affairs as “Observer” countries (Argentina, Chile, China, Russia, South Africa), jurisdictions that met the tax haven criteria and other

How were the jurisdictions covered by the Progress Report dentified? i

financial centres.

There can be no “hard and fast” line on how to measure progress in the implementation of the standard. The tables in the Progress Report represent an objective assessment of the situation in the countries surveyed by the Global Forum and has been guided by the work of the OECD’s Committee on Fiscal Affairs and the Global Forum. These experts have suggested a that at this point in time, a good indicator of progress is whether a jurisdiction has signed 12 agreements on exchange of information that meet the OECD standard. This threshold will be reviewed to take account of (i) the jurisdictions with which the agreements have been signed (a tax haven which has 12 agreements with other tax havens would not pass the threshold), (ii) the willingness of a jurisdiction to continue to sign agreements even after it has reached this threshold and (iii) the effectiveness of implementation.

What is the basis for distinguishing between those jurisdictions that have “substantially implemented” the internationally agreed tax standard and those that have not?

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 11

How will the OECD monitor implementation?

The Global Forum has until now prepared annual assessments, which form the factual basis for the progress report. In the current environment it is clear that more timely information will be needed to respond quickly to changing developments. Going forward the Global Forum will have to review its practice for updating the assessments. The Global Forum will be examining critically jurisdictions which, despite having made commitments before 2004, still have not signed a single agreement that meets the standard. The tables will be updated as new agreements meeting the internationally agreed tax standard are signed. Jurisdictions that have committed to the internationally agreed standard but have not yet substantially implemented it

How will the tables be updated?

will be identified as having substantially implemented it once they sign 12 agreements that meet the standard. No. An inherent element of the internationally agreed tax standard is the requirement to agree to the exchange of tax information with countries that require it in order to properly administer their own tax laws. A jurisdiction that refuses to agree to the exchange of information on the grounds that it has already “substantially implemented” the standard, cannot be seen to be fully ompliant with the standard.

If a jurisdiction has implemented the standard, does this mean they have no obligation to continue to negotiate information exchange agreements?

c

The Progress Report distinguishes between tax havens and the other financial centres. What is the difference?

Tax havens are jurisdictions that were identified by the OECD in June 2000 as meeting its tax haven criteria. The other financial centres were not identified as meeting these criteria. However, as the objective is to achieve a level playing field, these other jurisdictions were invited to participate in the Global Forum process.

How is a tax haven identified?

In 1998 the OECD set out a number of factors for identifying tax havens. The four key factors were:

1) No or nominal tax on the relevant income;

nge of information; 2) Lack of effective excha

3) Lack of transparency;

4) No substantial activities.

No or nominal tax is not sufficient in itself to classify a country as a tax haven. The fourth factor above “no substantial activities” was not considered when determining whether a jurisdiction was cooperative. Thus, in order to avoid being listed as an uncooperative tax haven, jurisdictions which met the criteria were asked only to make commitments to implement the principles of transparency and exchange of information for tax purposes.

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 12

Does the OECD have a list of tax havens?

Over 40 jurisdictions were identified as meeting the tax haven criteria in June 2000. By 2007, the vast majority of these have made commitments to implement transparency and effective exchange of information and are therefore not considered to be uncooperative jurisdictions by the OECD's Committee on Fiscal Affairs.

Until recently, three jurisdictions remained on the list of unco‐operative tax havens published by the OECD in 2002: Andorra, Monaco and Liechtenstein. In May, 2009, the OECD’s Committee on Fiscal Affairs removed these jurisdictions from the list in light of their March 2009 statements that they intend to rapidly implement international standards and the timetable set for such implementation. It is now considered that these jurisdictions have committed to the internationally agreed tax standard but not yet substantially implemented it, as shown in the Progress Report initially issued by the OECD Secretariat on 2 April.

The list of tax havens published in 2000 is comprised of those jurisdictions that meet the criteria described in the OECD’s 1998 Report Harmful Tax Competition: An Emerging Global Issue. There have been many positive changes in jurisdictions’ transparency and exchange of information practices since that time. The list of unco‐operative tax havens was comprised of tax havens identified by the OECD under criteria it established in 1998 and which have not made formal commitments to the OECD, after being requested to do so. Following the removal of Andorra, Liechtenstein and Monaco from the list,

What does the publication of the progress report mean for the other lists that the OECD has published?

no jurisdiction is currently listed as an unco‐operative tax haven by OECD.

While these lists are not replaced by the progress report, they should be seen in their historical context and the OECD will have to reassess their relevance in light of current developments.

Countering Offshore Tax Evasion: Some Questions and Answers

13 21 September 2009

Are Hong Kong, China and Macao, China tax havens?

No: they do not meet the definition of a tax haven as set out above.

Both have committed to the standards and have set out a timetable to implement them and are amongst the 84 jurisdictions surveyed by the Global Forum.

The key principles of transparency and exchange of information for tax

What is meant by high standards of transparency and exchange of information?

purposes can be summarised as follows:

• Exchange of information on request where it is “foreseeably relevant” to the administration and enforcement of the domestic laws of a treaty partner.

• No restrictions on exchange caused by bank secrecy or domestic tax interest requirements.

• Availability of reliable information, particularly accounting, bank and wers to obtain it. ownership information and po

• Respect for taxpayers’ rights.

f• Strict confidentiality o information exchanged.

Exchange of information on request occurs where one country’s competent authority asks for particular information from another competent authority. Typically, the information requested relates to an examination, inquiry or investigation of a taxpayer’s tax liability for specified tax years. The standard prohibits fishing expeditions. Before sending a request, the requesting country should use all means available in its own territory to obtain the information except where those would give rise to disproportionate difficulties. The request should be made in writing but in urgent cases an oral request may be accepted, where permitted under the applicable laws and procedures. Requests should be as detailed as possible and contain all the relevant facts, so that the competent authority that receives the request is well aware of the needs of the applicant contracting party and can deal with the request in an efficient manner. The OECD has developed guidance 8 on

How does exchange of information o n request work?

what could be included in a request.

Do the standards allow for the exchange of information on companies and trusts and their owners and beneficiaries?

Yes. The standards impose an obligation to exchange all types of information forseeably relevant to the administration and enforcement of the requesting country’s domestic tax laws. This could include information on companies and trusts and their owners and beneficiaries. Moreover, a state cannot decline to provide information in response to a request for exchange of information solely because it is held by a person acting in an agency or fiduciary capacity, such as a trustee.

The principles of transparency and effective information exchange have been articulated and refined through the work of the OECD’s Global Forum on Taxation consisting of OECD and non‐OECD countries and jurisdictions.

Who established the standards?

8 Manual on the Implementation of Exchange of Information for Tax Purposes http://www.oecd.org/dataoecd/15/45/36647905.pdf

Countering Offshore Tax Evasion: Some Questions and Answers

14 21 September 2009

Currently the standards for exchange of information are set out in Article 26 of the OECD Model Convention 9 and the 2002 Model Agreement on Exchange of Information. 10 The Global Forum has also developed an availability and reliability standard for accounting records. These standards have been endorsed by the G20 and the UN Committee of Experts on International Cooperation in Tax Matters and now serve as a basis for most bilateral tax treaties as the internationally agreed standard for exchange of information.

The standard for exchange of information in both cases is the same: the information must be “forseeably relevant” to the administration or enforcement of the domestic tax laws of the country concerned or to the application of the treaty concerned but the form in which the exchange of information takes place can vary. Article 26 of the OECD Model Tax Convention provides “rules under which information may be exchanged to the widest possible extent” and includes exchange on request, automatic exchange and other forms of information exchange. Most OECD countries do engage in automatic exchange of information on a range of different types of income. In the context of the development of the 2002 Model Agreement on Exchange of Information in Tax Matters, it was agreed that for purposes of implementing the commitments made by jurisdictions identified as tax havens in 2000, exchange of information on request would be sufficient. Similarly, in the 2000 report, Improving Access to Bank Information for Tax Purposes, it was agreed to focus on exchange of information on request. In both cases, the decisions reflected the major step forward exchange on request would imply

Why exchange of information on request not automatic?

for the jurisdictions concerned.

Information exchanged for tax purposes must be treated as confidential. Bilateral tax treaties and TIEAs contain rules to ensure that information is used only for authorised purposes and thereby protect taxpayer privacy rights. Confidentiality rules also apply to information exchanged pursuant to other instruments. Typically unauthorised disclosure of tax related

What are the safeguards to protect confidentiality?

information received from another country is a criminal offence.

First, tax information received from another country can only be used for the purposes stated in the agreements. Second, a country is free to decline a request for information in a number of situations. One reason for declining to provide information relates to the concept of public policy/ordre public. “Public policy” generally refers to the vital interests of a country, for instance where information requested relates to a state secret. A case of “public policy” may also arise, for example, where a tax investigation in another country was

What if countries want to use tax information for other purposes?

motivated by racial or political persecution.

No. All countries have some form of bank secrecy. What is important is that it can be lifted in well defined circumstances to enable countries to enforce their own tax laws and to respond to requests for information pursuant to TIEAs or

at

Is bank secrecy incompatible with this standard?

tax treaties so th treaty partners can administer their own laws.

witzerland had What progress has Until recently, Austria, Belgium, Luxembourg and S

767_33614197_1_1_1_1,00.html9 See http://www.oecd.org/document/53/0,3343,en_2649_33 10 See http://www.oecd.org/dataoecd/15/43/2082215.pdf

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 15

been made in getting countries to endorse and enforce these standards?

reservations about key aspects of the Article 26 standard. Now all 30 Member countries have endorsed and agreed to implement the standard. In 2000 there were more than 40 offshore financial centres that did not accept these standards. Today there are none. Also, in 1998 other major financial centres such as Hong Kong and Singapore were not prepared to endorse the standards. Today they do and they have also identified steps they will take this year so as to be able to implement the standard. So over the last ten years the OECD has succeeded in getting these standards endorsed by all major financial centres.

Great progress has been made in improving access to bank information for tax purposes and ensuring the availability of ownership and accounting information. Progress in achieving exchange of information had been slower. Now all OECD countries accept the Article 26 standard. Hong Kong and Singapore have also stated that they will change their legislation this year so as to implement the standard. As regards the jurisdictions identified in 2000, there is now a network of over 130 Tax Information Exchange Agreements (TIEAs). Jurisdictions such as Aruba, Bahrain, Bermuda, British Virgin Islands, Cayman Islands, Jersey, Guernsey, the Isle of Man and the Netherlands Antilles have substantially implemented the exchange of information standard. Others such as Antigua and Barbuda, and Gibraltar have made good progress in signing agreements. The vast majority of these TIEAs have either only been recently ratified or are still awaiting ratification, so it is still too early to assess their effectiveness. One of the priorities of the OECD and the Global Forum will be to monitor implementation and to issue periodic report on the effectiveness of TIEAs, not just in terms of the number of agreements signed, but also in terms of the “quality “of the agreements (e.g. signed with which countries; how quickly do the agreements come into force: are they being effectively implemented). Annex II provides a summary of the situation as at

And has progress been made in implementing them?

21 September 2009.

While the vast majority of exchange agreements are entered into bilaterally through tax treaties or TIEAs, there are examples of multilateral instruments (such as the OECD/Council of Europe Convention on Mutual Administrative Assistance in Tax Matters) that are in operation. With the recent attention paid to this issue, and a large number of jurisdictions eager to achieve a high level of compliance quickly, the possibility of extending the multilateral instruments will be explored. Multilateral instruments could be of particular use to less developed countries eager to take advantage of increased transparency and exchange of information, but which lack the resources to negotiate a series of bilateral agreements. In addition a number of countries have enacted domestic legislation that allows for exchange of information on a unilateral basis. This approach is being examined by the OECD.

In addition to bilateral agreements, what other implementation options are available to countries?

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 16

What is the OECD’s current position as regards potential sanctions on countries who are ultimately not considered to have substantially implemented the standards?

The OECD does not have power to impose sanctions on countries that do not implement the standards. Individual countries whether OECD or non‐OECD will decide for themselves what actions they consider necessary to ensure the effective enforcement of their tax laws. The G20 has produced a list of potential measures based upon an analysis provided by the OECD. The OECD will continue to provide a forum where countries can discuss how to make these measures more effective.

For further information see “Overview of OECD’s Work on International Tax Evasion” www.oecd.org/tax/evasion or contact:

Jeffrey Owens ([email protected] or Pascal SaintAmans (pascal.saint[email protected]) of the OECD Centre for Tax Policy and Administration.

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 17

ANNEX I: STATEMENTS ON THE OECD’S WORK ON INTERNATIONAL TAX EVASION

BY THE G7/G8/G20

G8 Declaration: Meeting of Heads of Government L’Aquila, Italy 8 July 2009

mbFurther efforts in international tax and prudential cooperation and in co ating illicit financing 16. In this difficult time, the protection of our tax base and the efforts to combat tax fraud and tax evasion are all the more important, especially given the extraordinary fiscal measures adopted to stabilise the world economy and the need to ensure that economic activity is conducted in a fair and transparent manner. We are making progress in promoting tax information exchange and transparency across the globe, which is helping to widen the acceptance of internationally agreed standards on the exchange of tax information and increase the number of bilateral agreements signed by several jurisdictions. But there is no space for complacency: all jurisdictions must now uickly implement their commitments. We cannot continue to tolerate large amounts of capital qhidden to evade taxation. 7. Echoing the call of the G‐20, an appropriate follow up framework is needed to fully benefit from his ren ed em a t1t

ew ph sis on ax information exchange and transparency:

a. the OECD Global Forum on Transparency and Exchange of Information must implement a peer‐review process that assesses implementation of international

s d o j astandards by all juri dictions an pr vides an ob ective and credible b sis for further action;

b. since all countries monitored so far by the Global Forum have committed to implement international standards on exchange of tax information, efforts should

exchange and increasing the now concentrate on implementing actual information number, quality and relevance of the agreements that adhere to these standards;

c. participation to the Global Forum should be expanded; d. recognising the particularly damaging effects of tax evasion for developing countries,

concrete progress needs to be made towards enabling developing countries to benefit from the new co‐operative tax environment, including through enhanced participation in the Global Forum and the consideration of a multilateral approach for exchange of information;

e. criteria used to define jurisdictions which have not yet substantially implemented internationally agreed standards on tax information exchange and transparency should be revised as part of the peer review assessment process to ensure an effective implementation of international standards; and

f. a toolbox of effective countermeasures for countries to consider for use against countries that do not meet international standards in relation to tax transparency should be discussed and agreed.

We ask the OECD to swiftly address these challenges, propose further steps and report by the time of the next G20 Finance Ministers’ meeting.

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 18

Statement of G8 Finance Ministers Lecce, Italy, 13 June, 2009 We welcome progress in negotiations of agreements on the exchange of information for tax purposes. We urge further progress in the implementation of the OECD standards and the involvement of the widest possible number of jurisdiction s, including developing countries. It is also essential to develop an effective peer‐review mechanism to assess compliance with the same standards. This could be delivered by an expanded Global Forum. We also look forward to an update on progress on the G20 agreement to tackle tax havens at the next OECD Ministerial meeting.

The Lecce Framework

The Lecce Framework recognizes that there is a wide range of instruments, both existing and under development, which have a common thread related to propriety, integrity and transparency and classifies them into five categories: corporate governance, market integrity, financial regulation and supervision, tax cooperation, and transparency of macroeconomic policy and data. Specific issues covered include, inter alia, executive compensation, regulation of systemically important institutions, credit rating agencies, accounting standards, the cross‐border exchange of information, bribery, tax havens, non‐cooperative jurisdictions, money laundering and the financing of terrorism, and the quality and dissemination o f economic and financial data.

G20 Communiqué: The Global Plan for Recovery and Reform London, U.K. 2 April 2009 15. To this end we are implementing the Action Plan agreed at our last meeting, as set out in the ttached progress report. We have today also issued a Declaration, Strengthening the Financial ystemaS

. In particular we agree:

to take action against non‐cooperative jurisdictions, including tax havens. We stand ready to deploy sanctions to protect our public finances and financial systems. The era of banking secrecy is over. We note that the OECD has today published a list of countries assessed by the Global Forum against the international standard for exchange of tax information;

GL20 Declaration: Strengthening the Financial System ondon, U.K. 2 April 2009 Tax havens and noncooperative jurisdictions It is essential to protect public finances and international standards against the risks posed by non‐cooperative jurisdictions. We call on all jurisdictions to adhere to the international standards in the prudential, tax, and AML/CFT areas. To this end, we call on the appropriate odies to conduct and strengthen objective peer reviews, based on existing processes, including bthrough the FSAP process. We call on countries to adopt the international standard for information exchange endorsed by the G20 in 2004 and reflected in the UN Model Tax Convention. We note that the OECD has today

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 19

published a list of countries assessed by the Global Forum against the international standard for xchange of information. We welcome the new commitments made by a number of jurisdictions eand encourage them to proceed swiftly with implementation. We stand ready to take agreed action against those jurisdictions which do not meet nternational standards in relation to tax transparency. To this end we have agreed to develop a oolboxit

of effective counter measures for countries to consider, such as:

• and financial institutions to increased disclosure requirements on the part of taxpayers

• report transactions involving non‐cooperative jurisdictions; withholding taxes in respect of a wide variety of payments;

• ect of expense payments to payees resident in a non‐denying deductions in respcooperative jurisdiction;

•

reviewing tax treaty policy;

• asking international institutions and regional development banks to review their investment policies; and,

giving extra weight to the principles of tax transparency and information exchange when •designing bilateral aid programs.

e also agreed that consideration should be given to further options relating to financial W

relations with these jurisdictions. We are committed to developing proposals, by end 2009, to make it easier for developing countries to secure the benefits of a new cooperative tax environment. G20 Working Group on Reinforcing International Cooperation and Promoting Integrity in Financial Markets (WG2), Final Report: 27 March 2009

Mediumterm actions:

Uncooperative and non‐transparent jurisdictions that pose risks of illicit financial activity (Action plan No. 32); Financial Action Task Force (FATF) (Action plan No. 33) and tax information exchange (Action plan No. 34)

39. We reaffirm our commitment to the high standards of transparency and exchange of information for tax purposes as reflected in the OECD’s Model Tax Information Exchange Agreement and Article 26 of the OECD Model Tax Convention. We urge all countries to fully implement the OECD standards. This model was also agreed by the UN.

40. We urge the international bodies responsible for prudential and regulatory standards, anti money laundering and terrorist financing, and tax matters ‐ the FSF, the FATF and the OECD ‐ to accelerate their work of identifying uncooperative jurisdictions and developing a toolbox of effective countermeasures against these jurisdictions; they should update G20 Finance Ministers and Central Bank Governors.

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 20

G20 Declaration of the Summit on Financial Markets and the World Economy Washington, D.C. 15 November 2008 Actions Taken and to Be Taken Promoting Integrity in Financial Markets: We commit to protect the integrity of the world's financial markets by bolstering investor and consumer protection, avoiding conflicts of interest, preventing illegal market manipulation, fraudulent activities and abuse, and protecting against illicit finance risks arising from non‐cooperative jurisdictions. We will also promote information sharing, including ith respect to jurisdictions that have yet to commit to international standards with respect to bank ecrecy and transparency. ws Action Plan to Implement Principles for Reform Promoting Integrity in Financial Markets Tax authorities, drawing upon the work of relevant bodies such as the Organization for Economic Cooperation and Development (OECD), should continue efforts to promote tax information xchange. Lack of transparency and a failure to exchange tax information should be vigorously ddressed. ea G8 Communiqué: Meeting of Heads of Government Hokkaido Japan 9 July 2008

Abuses of the Financial System 20. We urge all countries that have not yet fully implemented the OECD standards of transparency and effective exchange of information in tax matters to do so without further delay, and encourage the OECD to strengthen its work on tax evasion and report back in 2010. G8 Communiqué: Meeting of Finance Ministers Osaka Japan 14 June 2008

Abuses of the Financial System

In view of the recent developments, we urge all countries that have not yet fully implemented the OECD standards of transparency and effective exchange of information in tax matters to do so without further delay. We welcome the efforts of the OECD in this regard, and ask the OECD to strengthen its work on tax evasion.

G20 Communiqué: Meeting of Ministers and Governors in Melbourne 1819 November 2006 Further to our 2004 commitment to achieving high standards of transparency and exchange of information for tax purposes, we welcome the release of the Global Forum on Taxation 2006 assessment which shows that progress has been made in the implementation of those standards. Further progress is needed and we encourage continuing implementation efforts and call on those countries and territories that have not yet implemented high standards of transparency and exchange of information to do so.

Countering Offshore Tax Evasion: Some Questions and Answers

21 21 September 2009

G20 Communiqué: Meeting of Finance Ministers and Central Bank Governors Xianghe, Hebei, China, 1516 October 2005 9. We reaffirmed our commitments to the purposes of the “G‐20 Statement on Transparency and Exchange of Information for Tax Purposes” that was endorsed last year. In this context, we welcome the efforts of the OECD Global Forum on Taxation to promote high standards of transparency and effective exchange of information for tax purposes.

G8 Communiqué on Africa Gleneagles, UK 14 July 2005 Para. 14(i) In response to this African commitment, we will: … (i) Take concrete steps to protect financial markets from criminal abuse, including bribery and corruption, by pressing all financial centres to obtain and implement the highest international standards of transparency and exchange of information. We will continue to support Financial Stability Forums ongoing work to promote and review progress on the implementation of international standards, particularly the new process concerning offshore financial centres that was agreed in March 2005, and the OECD’s high standards in favour of transparency and exchange of information in all tax matters.

G20 Statement on Transparency and Exchange of Information for Tax Purposes Meeting of Finance Ministers and Central Bank Governors Berlin, Germany 20–21 November 2004 We, the Finance Ministers and Central Bank Governors of the G20, are committed to enhancing good governance and fighting illicit use of the financial system in all its forms. Consequently, we are committed to transparency and exchange of information for tax purposes. We regard this as vital to enhance fairness and equity in our societies and to promote economic development.

Financial systems must respect commercial confidentiality, but confidentiality should not be allowed to foster illicit activity. Lack of access to information in the tax field has significant adverse effects. It allows some to escape tax that is legally due and is unfair to citizens that comply with the tax laws. It distorts international investment decisions which should be based on legitimate commercial considerations rather than the circumvention of tax laws. The G20 therefore regards it as a mark of good international citizenship for countries to eliminate practices that restrict or frustrate the ability of another country to enforce its chosen system of taxation.

We are therefore committed to the high standards of transparency and exchange of information for tax purposes that have been reflected in the Model Agreement on Exchange of Information on Tax Matters as released by the OECD in April 2002. We call on all countries to adopt these standards.

High standards of transparency require that governmental authorities have access to bank information and other financial information held by financial intermediaries and to beneficial ownership information regarding the ownership of all types of entities. High standards of exchange of information require that such information be available for exchange with other countries in civil and criminal tax matters. Exchange of information in tax matters should not be limited by dual incrimination principles in criminal tax matters or by the lack of domestic tax interest in civil tax matters. There must be appropriate safeguards on the use and disclosure of any exchanged information. Exchange of information should therefore be implemented through legal mechanisms providing for the use of such information only for authorized tax purposes, thus ensuring the protection of taxpayers’ rights and the confidentiality of tax information.

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 22

We call on all countries with financial centres to adopt and implement the high standards articulated by the OECD so that we can move towards an international financial system that is free of distortions created through lack of transparency and lack of effective exchange of information in tax matters. It is important that countries which do meet these standards have confidence that they will not be disadvantaged and that financial centres in countries that choose not to meet these standards will not benefit from that choice.

The G20 therefore strongly support the efforts of the OECD Global Forum on Taxation to promote high standards of transparency and exchange of information for tax purposes and to provide a cooperative forum in which all countries can work towards the establishment of a level playing field based on these standards.

G7 Economic Communiqué: Making a success of globalization for the benefit of all Lyon, France 28 June 1996 16. Finally, globalization is creating new challenges in the field of tax policy. Tax schemes aimed at attracting financial and other geographically mobile activities can create harmful tax competition between States, carrying risks of distorting trade and investment and could lead to the erosion of national tax bases. We strongly urge the OECD to vigorously pursue its work in this field, aimed at establishing a multilateral approach under which countries could operate individually and collectively to limit the extent of these practices. We will follow closely the progress on work by the OECD, which is due to produce a report by 1998.

Countering Offshore Tax Evasion: Some Questions and Answers

23 21 September 2009

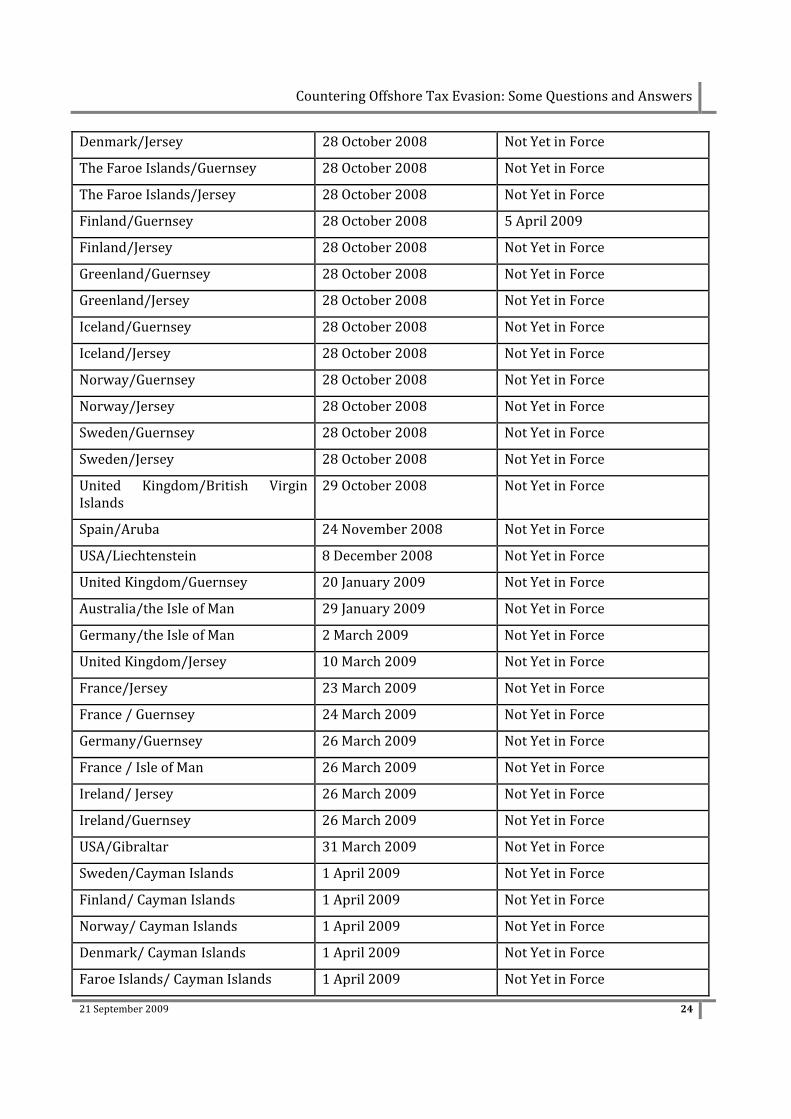

ANNEX II: TIEAS SIGNED BETWEEN OECD MEMBERS AND COMMITTED JURISDICTIONS SINCE 2000

SIGNATORIES DATE SIGNED DATE OF ENTRY INTO FORCE

USA/Antigua and Barbuda 6 December 2000 10 February 2003

USA/Cayman Islands 27 November 2001 10 March 2006

USA/Bahamas 25 January 2002 31 December 2003

USA/British Virgin Islands 3 April 2002 10 March 2006

USA/Netherlands Antilles 17 April 2002 22 March 2007

USA/Guernsey 19 September 2002 30 March 2006

USA/Isle of Man 3 October 2002 26 June 2006

USA/Jersey 4 November 2002 26 June 2006

USA/Aruba 21 November 2003 13 September 2004

The Netherlands/Isle of Man 12 October 2005 21 July 2006

Australia/Bermuda 10 November 2005 20 September 2007

Australia/Antigua and Barbuda 30 January 2007 Not yet in Force

Australia/Netherlands Antilles 1 March 2007 4 April 2008

New Zealand/Netherlands Antilles 1 March 2007 2 October 2008

The Netherlands/Jersey 20 June 2007 1 March 2008

Sweden/Isle of Man 30 October 2007 27 December 2008

Finland/Isle of Man 30 October 2007 19 June 2008

Norway/Isle of Man 30 October 2007 23 August 2008

Denmark/Isle of Man 30 October 2007 26 September 2008

Faroe Islands/Isle of Man 30 October 2007 3 August 2008

Greenland/Isle of Man 30 October 2007 11 April 2008

Iceland/Isle of Man 30 October 2007 Not yet in Force

United Kingdom/Bermuda 4 December 2007 10 November 2008

Ireland/Isle of Man 24 April 2008 31 December 2008

The Netherlands/Guernsey 25 April 2008 11 April 2009

Spain/Netherlands Antilles 10 June 2008 Not Yet in Force

Germany/Jersey 4 July 2008 Not Yet in Force

United Kingdom/Isle of Man 29 September 2008 2 April 2009

Australia/British Virgin Islands 27 October 2008 Not Yet in Force

Denmark/Guernsey 28 October 2008 7 May 2009

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 24

Denmark/Jersey 28 October 2008 Not Yet in Force

The Faroe Islands/Guernsey 28 October 2008 Not Yet in Force

The Faroe Islands/Jersey 28 October 2008 Not Yet in Force

Finland/Guernsey 28 October 2008 5 April 009 2

Finland/Jersey 28 October 2008 Not Yet in Force

Greenland/Guernsey 28 October 2008 Not Yet in Force

Greenland/Jersey 28 October 2008 Not Yet in Force

Iceland/Guernsey 28 October 2008 Not Yet in Force

Iceland/Jersey 28 October 2008 Not Yet in Force

Norway/Guernsey 28 October 2008 Not Yet in Force

Norway/Jersey 28 October 2008 Not Yet in Force

Sweden/Guernsey 28 October 2008 Not Yet in Force

Sweden/Jersey 28 October 2008 Not Yet in Force

United Kingdom/British Virgin Islands

29 October 2008 Not Yet in Force

Spain/Aruba 24 November 2008 Not Yet in Force

USA/Liechtenstein 8 December 2008 Not Yet in Force

United Kingdom/Guernsey 20 January 2009 Not Yet in Force

Australia/the Isle of Man 29 January 2009 Not Yet in Force

Germany/the Isle of Man 2 March 2009 Not Yet in Force

United Kingdom/Jersey 10 March 2009 Not Yet in Force

France/Jersey 23 March 2009 Not Yet in Force

France / Guernsey 24 March 2009 Not Yet in Force

Germany/Guernsey 26 March 2009 Not Yet in Force

France / Isle of Man 26 March 2009 Not Yet in Force

Ireland/ Jersey 26 March 2009 Not Yet in Force

Ireland/Guernsey 26 March 2009 Not Yet in Force

USA/Gibraltar 31 March 2009 Not Yet in Force

Sweden/Cayman Islands 1 April 2009 Not Yet in Force

Finland/ Cayman Islands 1 April 2009 Not Yet in Force

Norway/ Cayman Islands 1 April 2009 Not Yet in Force

Denmark/ Cayman Islands 1 April 2009 Not Yet in Force

Faroe Islands/ Cayman Islands 1 April 2009 Not Yet in Force

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 25

Greenland/ Cayman Islands 1 April 2009 Not Yet in Force

Iceland/ Cayman Islands 1 April 2009 Not Yet in Force

Denmark/Bermuda 17 April 2009 Not Yet in Force

Faroe Islands/Bermuda 17 April 2009 Not Yet in Force

Finland/Bermuda 17 April 2009 Not Yet in Force

Greenland/Bermuda 17 April 2009 Not Yet in Force

Iceland/Bermuda 17 April 2009 Not Yet in Force

New Zealand/Bermuda 17 April 2009 Not Yet in Force

Norway/Bermuda 17 April 2009 Not Yet in Force

Sweden/Bermuda 17 April 2009 Not Yet in Force

Denmark/British Virgin Islands 18 May 2009 Not Yet in Force

Faroe Islands/British Virgin Islands 18 May 2009 Not Yet in Force

Finland/British Virgin Islands 18 May 2009 Not Yet in Force

Greenland/British Virgin Islands 18 May 2009 Not Yet in Force

Iceland/British Virgin Islands 18 May 2009 Not Yet in Force

Norway/British Virgin Islands 18 May 2009 Not Yet in Force

Sweden/British Virgin Islands 18 May 2009 Not Yet in Force

Netherlands/Bermuda 8 June 2009 Not Yet in Force

Australia/Jersey 10 June 2009 Not Yet in Force

France/British Virgin Islands 17 June 2009 Not Yet in Force

Ireland/Cayman Islands 23 June 2009 Not Yet in Force

Ireland/Gibraltar 24 June 2009 Not Yet in Force

Germany/Bermuda 3 July 2009 Not Yet in Force

Netherlands/Cayman Islands 8 July 2009 Not Yet in Force

New Zealand/Cook Islands 9 July 2009 Not Yet in Force

Belgium/Monaco 15 July 2009 Not Yet in Force

United Kingdom/Anguilla 20 July 2009 Not Yet in Force

Ireland/Anguilla 22 July 2009 Not Yet in Force

Ireland/Turks and Caicos 22 July 2009 Not Yet in Force

Netherlands/Anguilla 22 July 2009 Not Yet in Force

Netherlands/Turks and Caicos 22 July 2009 Not Yet in Force

New Zealand/Guernsey 22 July 2009 Not Yet in Force

Countering Offshore Tax Evasion: Some Questions and Answers

21 September 2009 26

United Kingdom/Turks and Caicos 23 July 2009 Not Yet in Force

New Zealand/Isle of Man 27 July 2009 Not Yet in Force

New Zealand/Jersey 27 July 2009 Not Yet in Force

Ireland/Bermuda 28 July 2009 Not Yet in Force

Monaco/San Marino 29 July 2009 Not Yet in Force

United Kingdom/Liechtenstein 11 August 2009 Not Yet in Force

Germany/Gibraltar 13 August 2009 Not Yet in Force

New Zealand/Gibraltar 13 August 2009 Not Yet in Force

New Zealand /Cayman Islands 14 August 2009 Not Yet in Force

New Zealand/British Virgin Islands 14 August 2009 Not Yet in Force

Australia/Gibraltar 25 August 2009 Not Yet in Force

United Kingdom /Gibraltar 27 August 2009 Not Yet in Force

Canada/Netherlands Antilles 29 August 2009 Not Yet in Force

Netherlands/St Kitts and Nevis 1 September 2009 Not Yet in Force

Mexico/Netherlands Antilles 1 September 2009 Not Yet in Force

Denmark/St. Kitts and Nevis 1 September 2009 Not Yet in Force

Denmark/St. Vincent and the Grenadines

1 September 2009 Not Yet in Force

Netherlands/St. Vincent and the Grenadines

1 September 2009 Not Yet in Force

Germany/Liechtenstein 2 September 2009 Not Yet in Force

Denmark/Anguilla 2 September 2009 Not Yet in Force

Denmark/Gibraltar 2 September 2009 Not Yet in Force

Netherlands/Antigua and Barbuda 2 September 2009 Not Yet in Force

Denmark/Antigua and Barbuda 2 September 2009 Not Yet in Force

Denmark/Turks and Caicos Islands 7 September 2009 Not Yet in Force

United States/Monaco 8 September 2009 Not Yet in Force

Denmark/Aruba 10 September 2009 Not Yet in Force

Finland/Aruba 10 September 2009 Not Yet in Force

Iceland/Aruba 10 September 2009 Not Yet in Force

Norway/Aruba 10 September 2009 Not Yet in Force

Sweden/Aruba 10 September 2009 Not Yet in Force

Denmark/Netherlands Antilles 10 September 2009 Not Yet in Force

Countering Offshore Tax Evasion: Some Questions and Answers

Finland/Netherlands Antilles 10 September 2009 Not Yet in Force

Iceland/Netherlands Antilles 10 September 2009 Not Yet in Force

Sweden/Netherlands Antilles 10 September 2009 Not Yet in Force

Norway/Netherlands Antilles 10 September 2009 Not Yet in Force

Austria/St. Vincent and the Grenadines

14 September 2009 Not Yet in Force

Austria/Monaco 15 September 2009 Not Yet in Force

Austria/Andorra 17 September 2009 Not Yet in Force

Austria/Gibraltar 17 September 2009 Not Yet in Force

Liechtenstein/Andorra 18 September 2009 Not Yet in Force

San Marino/Andorra 21 September 2009 Not Yet in Force

21 September 2009 27

![Countering Terrorist Ideologies[1]](https://img.pdfslide.us/doc/110x75/55cf97d0550346d03393c601/countering-terrorist-ideologies1.jpg)