Embed Size (px)

Citation preview

Overlaps in Indirect Taxes:

Complexities Beyond Control

Sunil B Gabhawalla

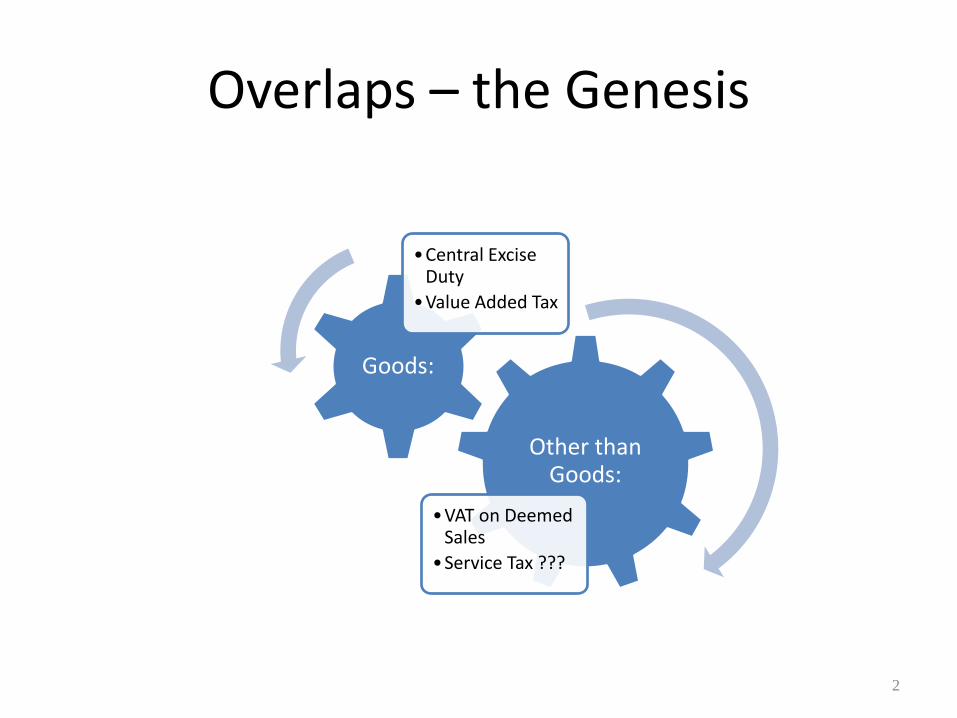

Overlaps – the Genesis

Other than Goods:

•VAT on Deemed Sales

•Service Tax ???

Goods:

•Central Excise Duty

•Value Added Tax

2

Overlaps – Constitutional Framework

• State Governments : – What is the point of delineation?

• Central Government : – Is there any ‘fetter’ on the residuary power to tax?

3

What shall we cover in this session?

• Conceptual Similarities & Differences between various Indirect Taxes

• Illustrations of Overlapping Areas between VAT or Service Tax

• Way Forward

4

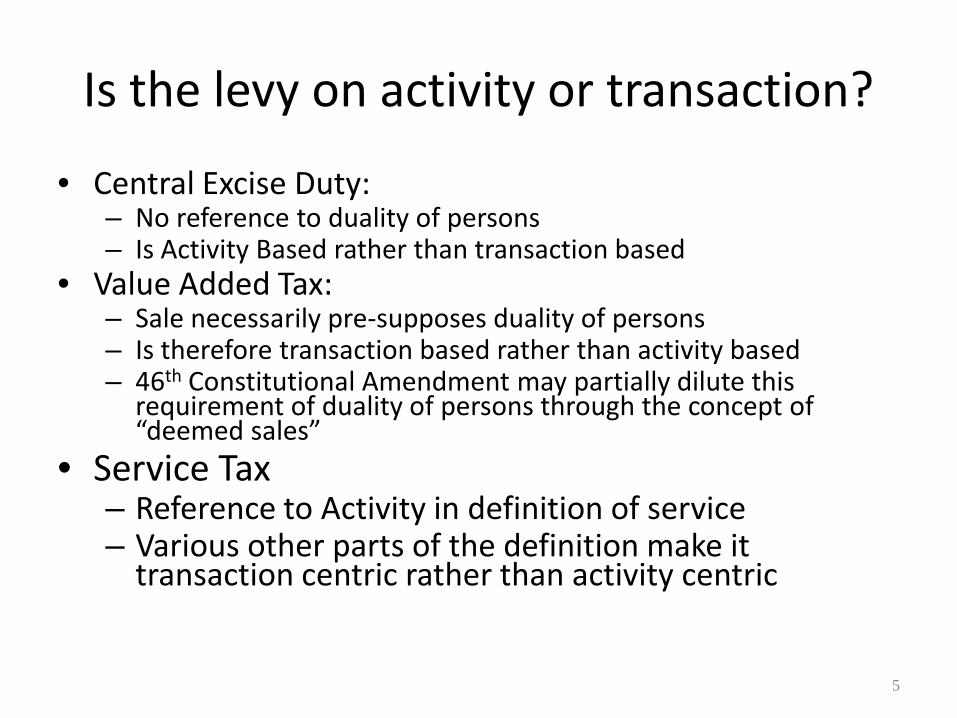

Is the levy on activity or transaction?

• Central Excise Duty: – No reference to duality of persons – Is Activity Based rather than transaction based

• Value Added Tax: – Sale necessarily pre-supposes duality of persons – Is therefore transaction based rather than activity based – 46th Constitutional Amendment may partially dilute this

requirement of duality of persons through the concept of “deemed sales”

• Service Tax – Reference to Activity in definition of service – Various other parts of the definition make it

transaction centric rather than activity centric

5

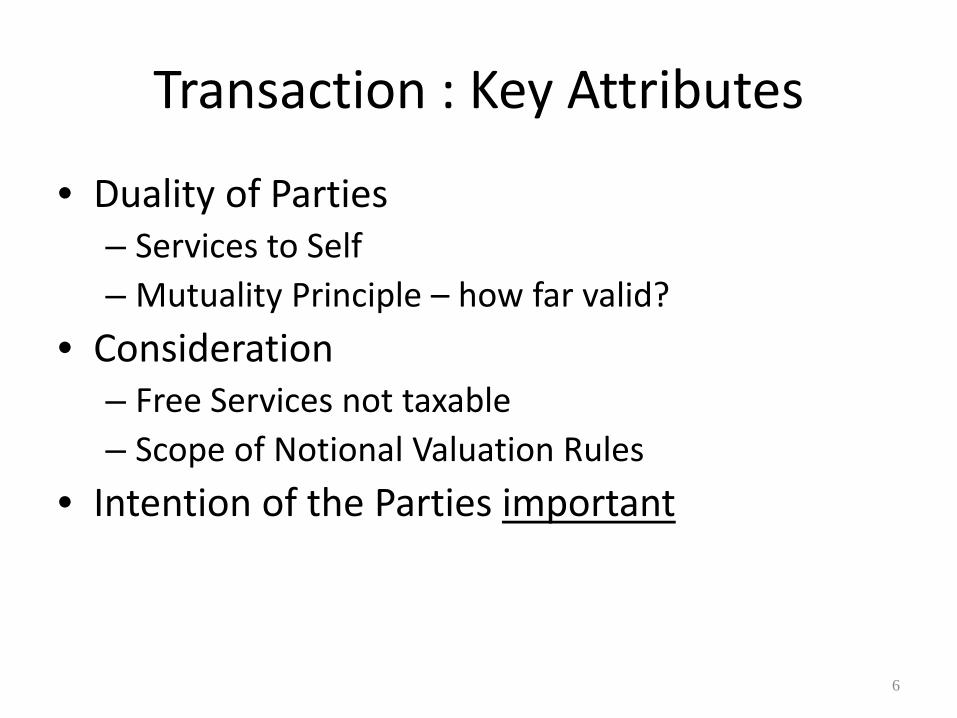

Transaction : Key Attributes

• Duality of Parties – Services to Self – Mutuality Principle – how far valid?

• Consideration – Free Services not taxable – Scope of Notional Valuation Rules

• Intention of the Parties important

6

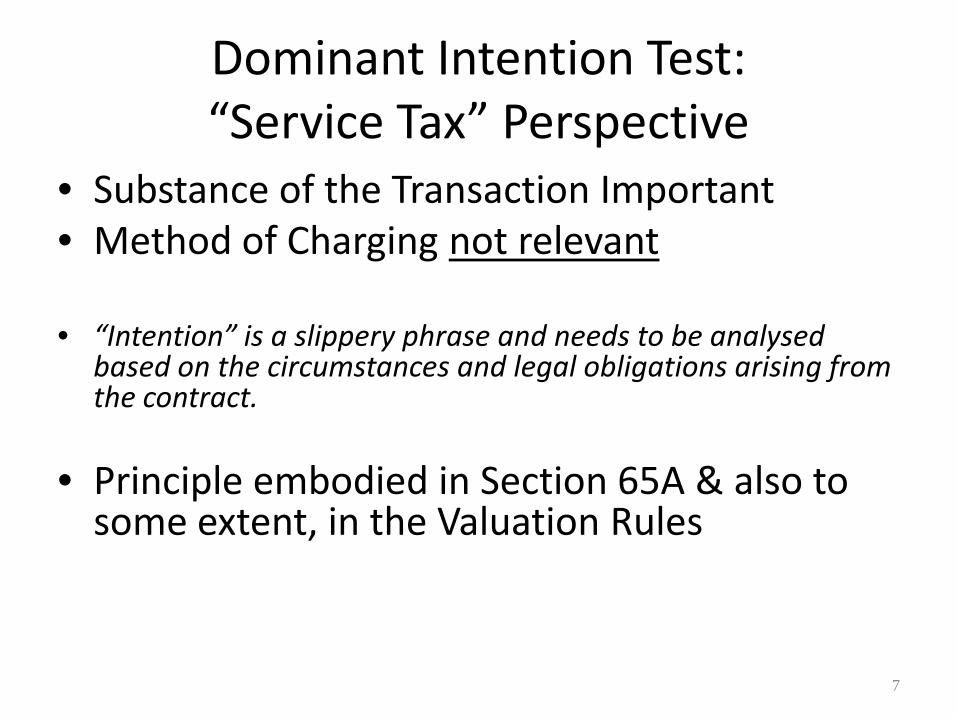

Dominant Intention Test: “Service Tax” Perspective

• Substance of the Transaction Important • Method of Charging not relevant

• “Intention” is a slippery phrase and needs to be analysed

based on the circumstances and legal obligations arising from the contract.

• Principle embodied in Section 65A & also to some extent, in the Valuation Rules

7

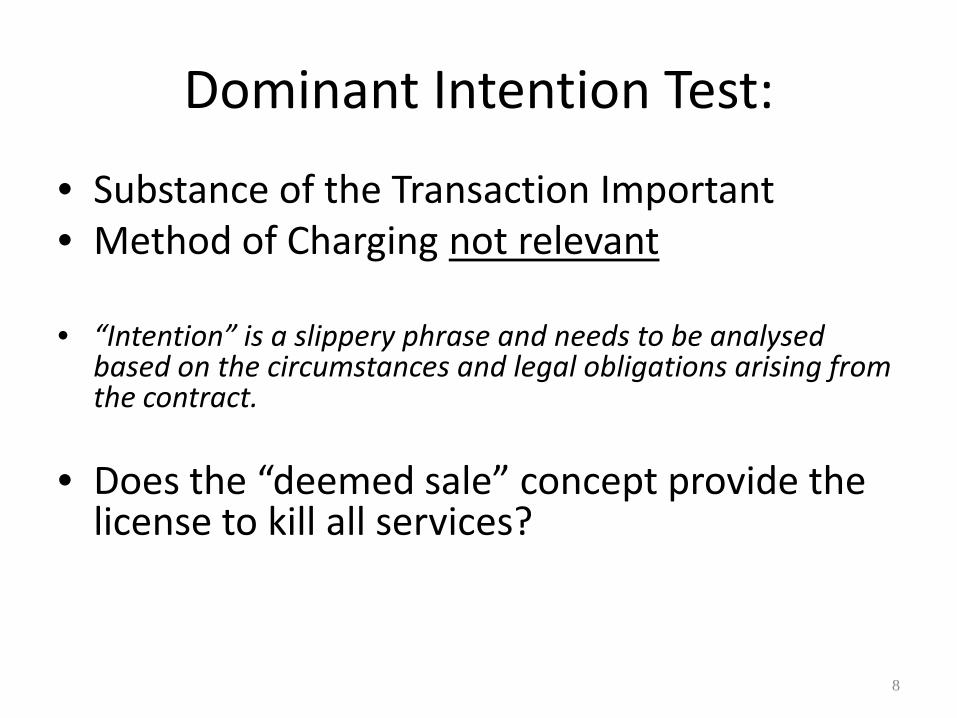

Dominant Intention Test:

• Substance of the Transaction Important • Method of Charging not relevant

• “Intention” is a slippery phrase and needs to be analysed

based on the circumstances and legal obligations arising from the contract.

• Does the “deemed sale” concept provide the license to kill all services?

8

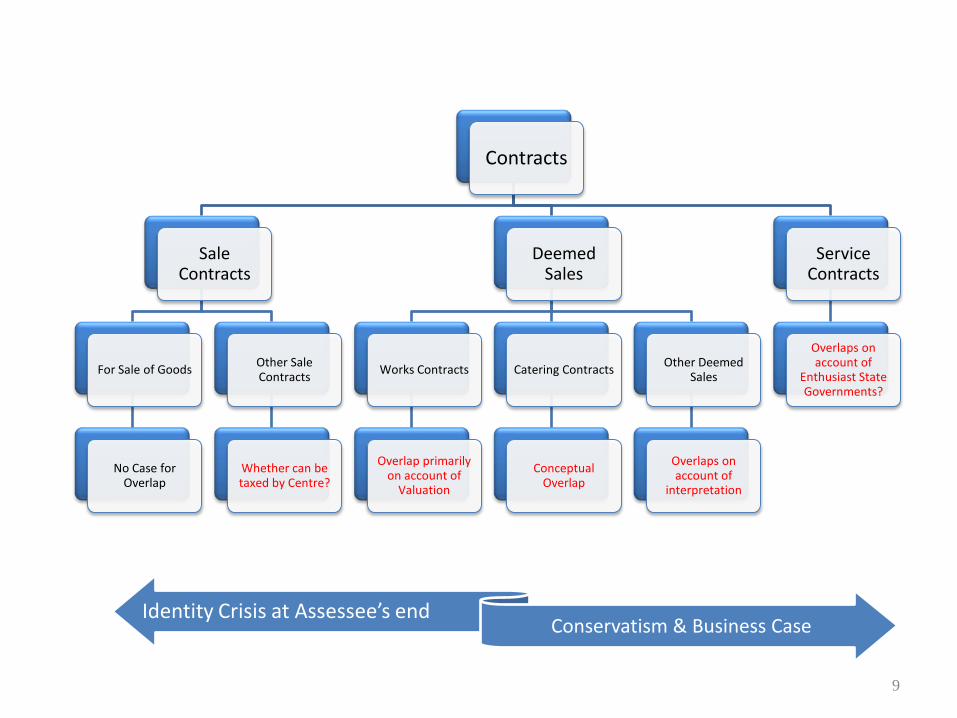

Contracts

Sale Contracts

For Sale of Goods

No Case for Overlap

Other Sale Contracts

Whether can be taxed by Centre?

Deemed Sales

Works Contracts

Overlap primarily on account of

Valuation

Catering Contracts

Conceptual Overlap

Other Deemed Sales

Overlaps on account of

interpretation

Service Contracts

Overlaps on account of

Enthusiast State Governments?

9

Identity Crisis at Assessee’s end Conservatism & Business Case

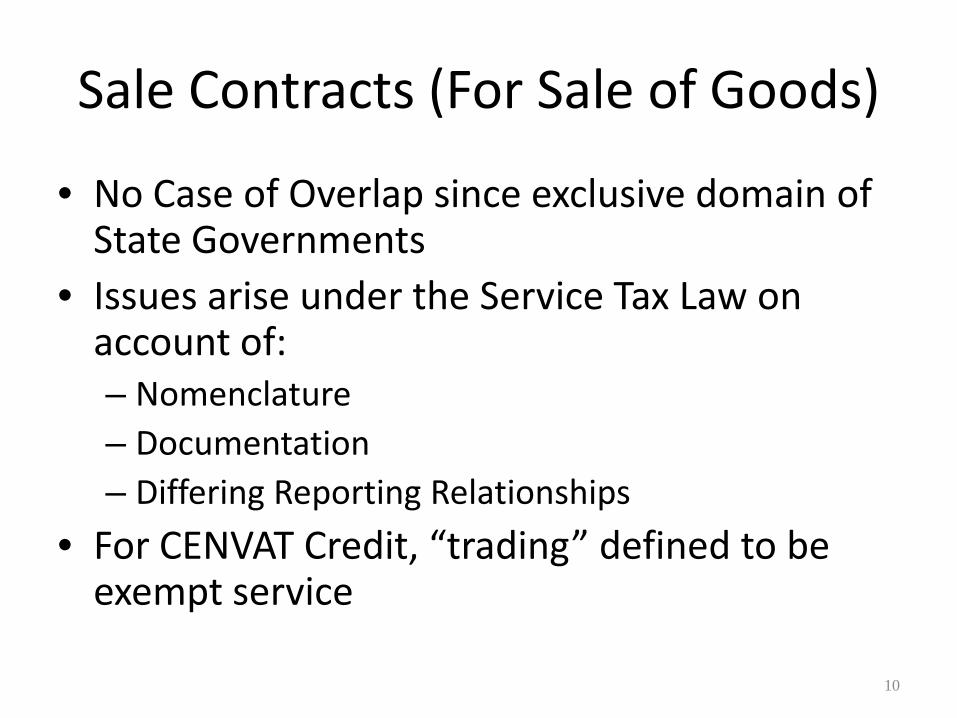

Sale Contracts (For Sale of Goods)

• No Case of Overlap since exclusive domain of State Governments

• Issues arise under the Service Tax Law on account of: – Nomenclature – Documentation – Differing Reporting Relationships

• For CENVAT Credit, “trading” defined to be exempt service

10

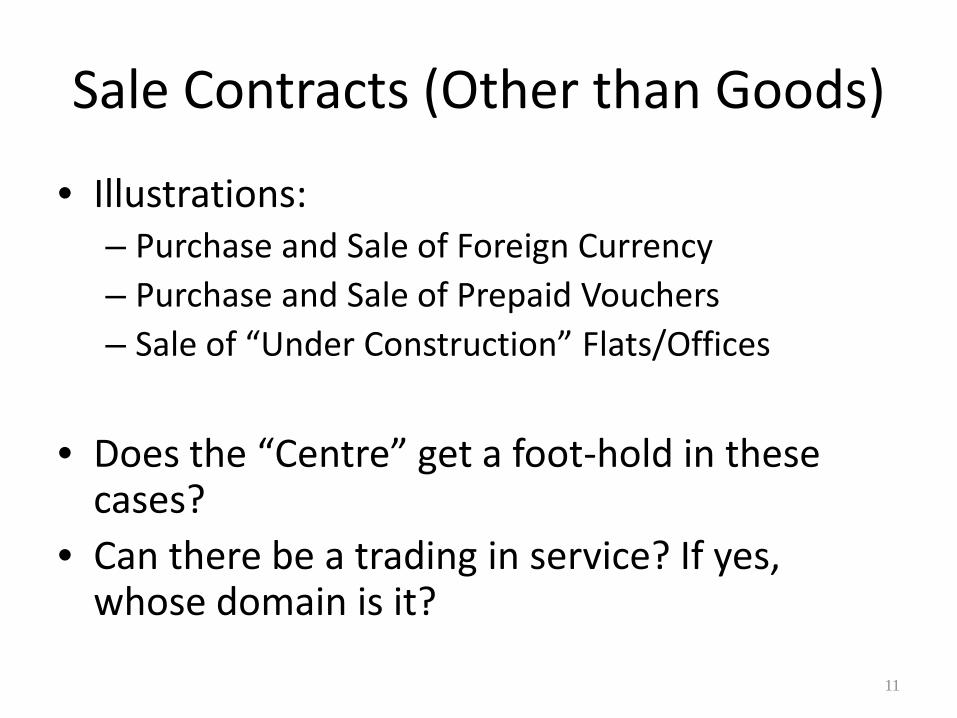

Sale Contracts (Other than Goods)

• Illustrations: – Purchase and Sale of Foreign Currency – Purchase and Sale of Prepaid Vouchers – Sale of “Under Construction” Flats/Offices

• Does the “Centre” get a foot-hold in these

cases? • Can there be a trading in service? If yes,

whose domain is it?

11

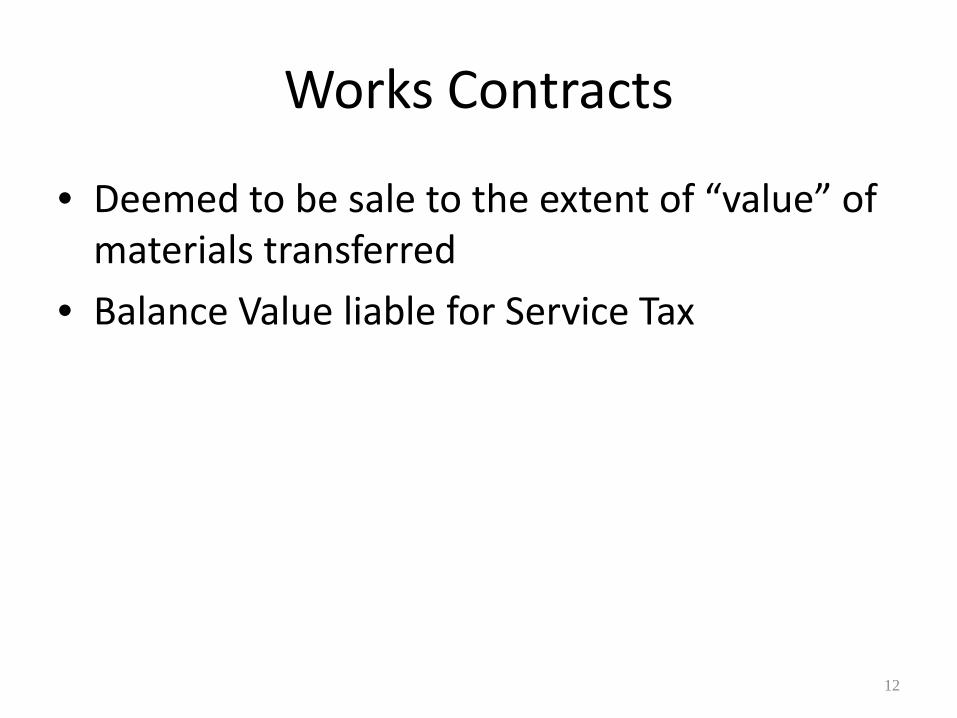

Works Contracts

• Deemed to be sale to the extent of “value” of materials transferred

• Balance Value liable for Service Tax

12

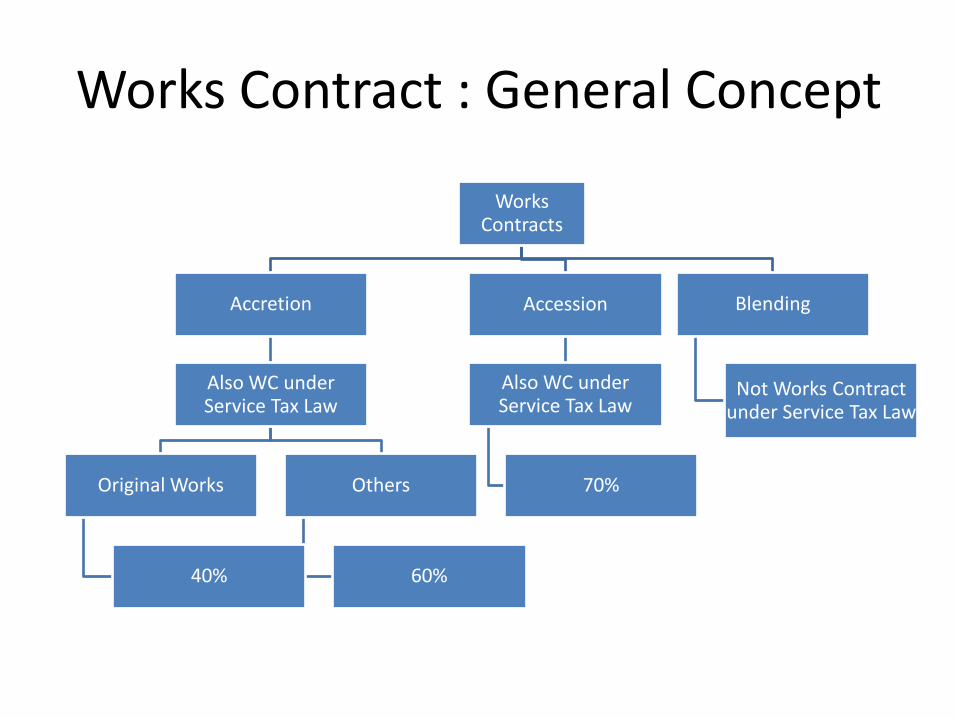

Works Contract : General Concept

Works Contracts

Accretion

Also WC under Service Tax Law

Original Works

40%

Others

60%

Accession

Also WC under Service Tax Law

70%

Blending

Not Works Contract under Service Tax Law

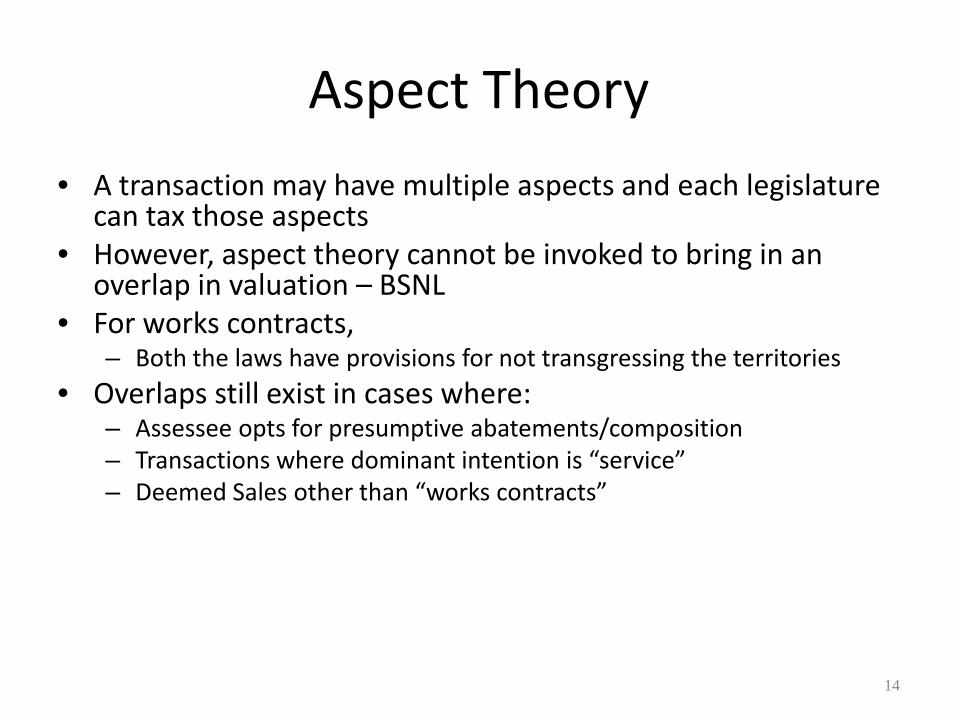

Aspect Theory

• A transaction may have multiple aspects and each legislature can tax those aspects

• However, aspect theory cannot be invoked to bring in an overlap in valuation – BSNL

• For works contracts, – Both the laws have provisions for not transgressing the territories

• Overlaps still exist in cases where: – Assessee opts for presumptive abatements/composition – Transactions where dominant intention is “service” – Deemed Sales other than “works contracts”

14

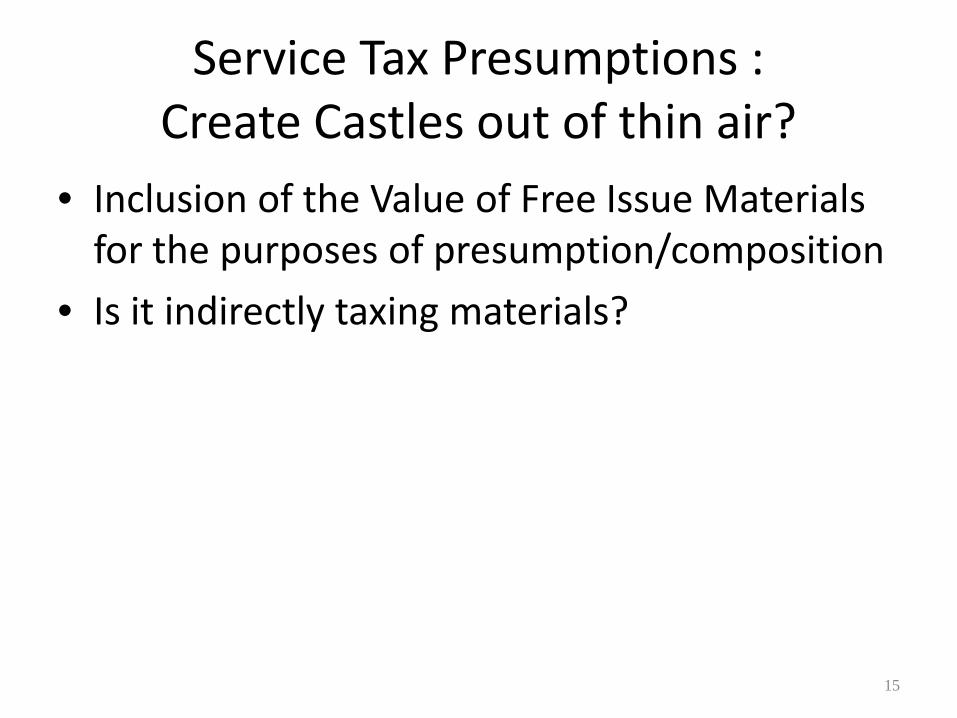

Service Tax Presumptions : Create Castles out of thin air?

• Inclusion of the Value of Free Issue Materials for the purposes of presumption/composition

• Is it indirectly taxing materials?

15

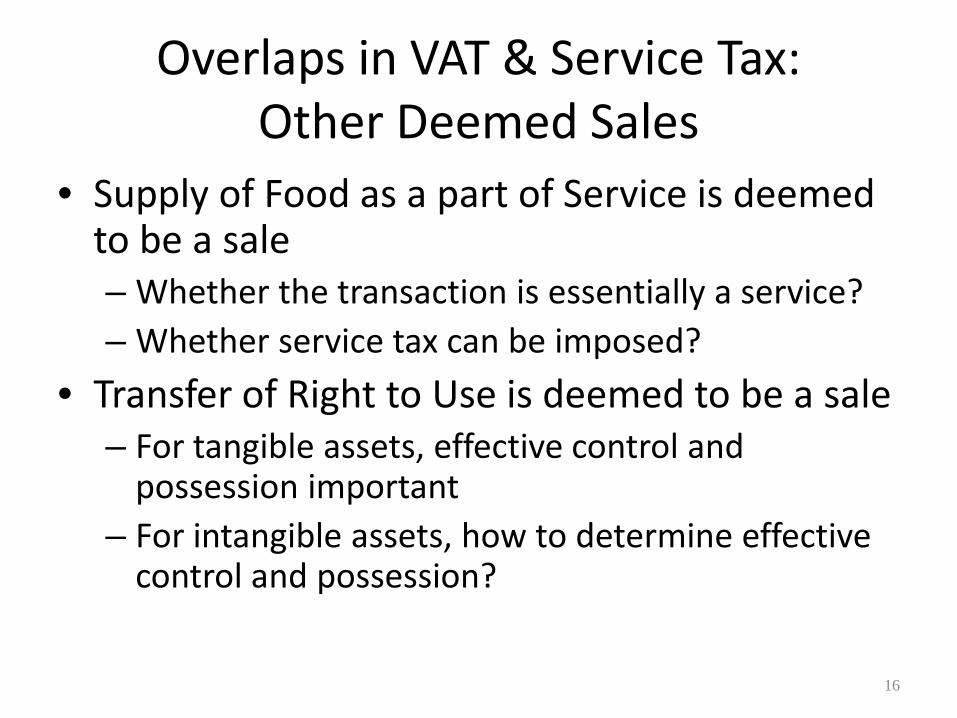

Overlaps in VAT & Service Tax: Other Deemed Sales

• Supply of Food as a part of Service is deemed to be a sale – Whether the transaction is essentially a service? – Whether service tax can be imposed?

• Transfer of Right to Use is deemed to be a sale – For tangible assets, effective control and

possession important – For intangible assets, how to determine effective

control and possession?

16

Service Contracts: Overdue Enthusiasm

• If the dominant intention is provision of service, VAT should not be applicable.

• Due respect needs to be given to the aspects of: – Goods

– Transfer

– Limited Scope for Vivisection

17

Classification of Contracts: Identity Crisis

• Loyalty Programs

• Facility Management Contracts

• Photography Contracts

• Maintenance Contracts

• BOT Contracts

• Software Transactions

18

Software: Inability to “MISS” it…

• Whether goods or services?

• Whether there is any distinction between packaged software and customised software?

• Whether the answers depend on the medium of delivery?

19

Causes of Overlaps : Summary

• Presumptive Schemes

• Deemed Sale of “Supply of Food as part of service” – no resolution so far

• Lack of factual clarity in case of lease transactions

• Error in identification &/or Non Acceptance of Principle of Dominant Intention

20

Any Questions??

Thank you for a patient hearing..