Embed Size (px)

Citation preview

Overcapacities in the steel industry

Paris, July 2, 2013

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

OECD Steel committee74th session

McKinsey & Company | 1

Disclaimer

While McKinsey & Company developed the outlooks and scenarios in

accordance with its professional standards, McKinsey&Company does not

warrant any results obtained or conclusions drawn from their use. The analyses

and conclusions contained in this document are based on various assumptions

that McKinsey&Company has developed regarding economic growth, and steel

demand, production and capacities which may or may not be correct, being

based upon factors and events subject to uncertainty. Future results or values

could be materially different from any forecast or estimates contained in the

analyses.

The analyses are partly based on information that has not been generated by

McKinsey&Company and has not, therefore, been entirely subject to our

independent verification. McKinsey believes such information to be reliable and

adequately comprehensive but does not represent that such information is in all

respects accurate or complete.

McKinsey & Company | 2

Contents

▪ Overcapacities in the steel industry – a challenge that will persist

▪ Industry restructuring – financial

situation of many steel companies will

require help from outside of the industry

McKinsey & Company | 3

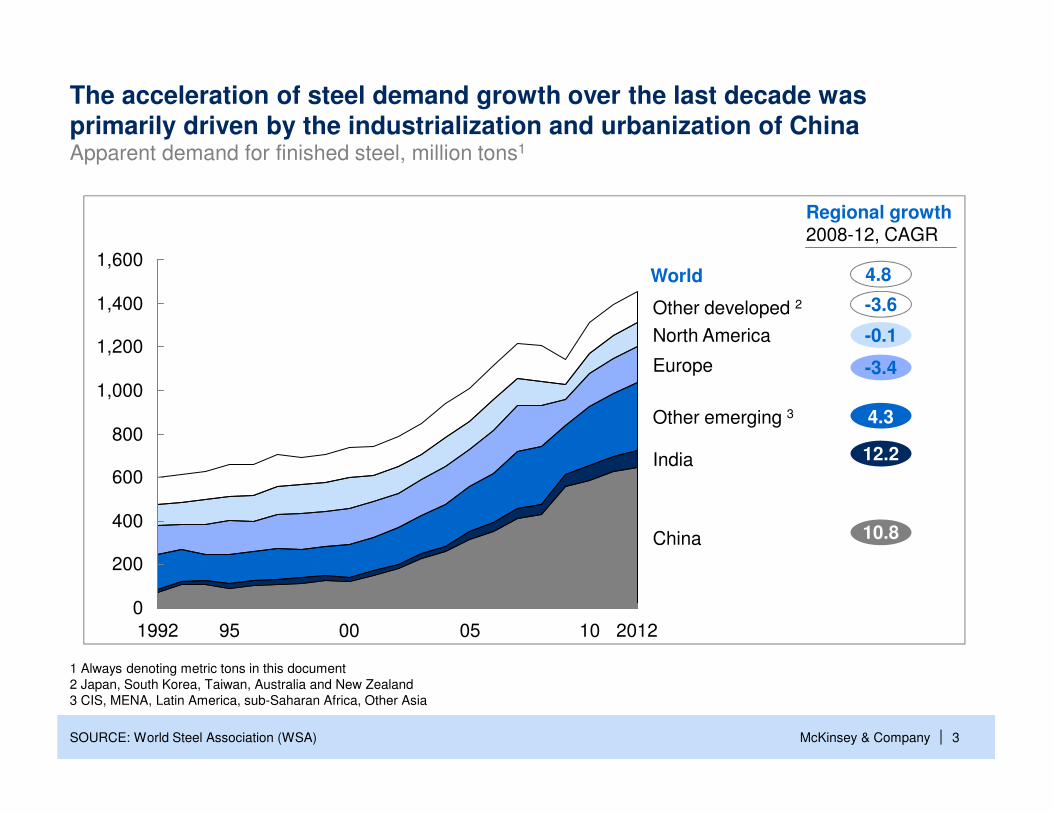

The acceleration of steel demand growth over the last decade was primarily driven by the industrialization and urbanization of ChinaApparent demand for finished steel, million tons1

SOURCE: World Steel Association (WSA)

1 Always denoting metric tons in this document

2 Japan, South Korea, Taiwan, Australia and New Zealand

3 CIS, MENA, Latin America, sub-Saharan Africa, Other Asia

400

200

0

China

India

Other emerging 3

Europe

North America

Other developed 2

20121005

1,600

00951992

1,400

1,200

1,000

800

600

Regional growth2008-12, CAGR

World

-3.6

-0.1

-3.4

4.3

12.2

10.8

4.8

McKinsey & Company | 4

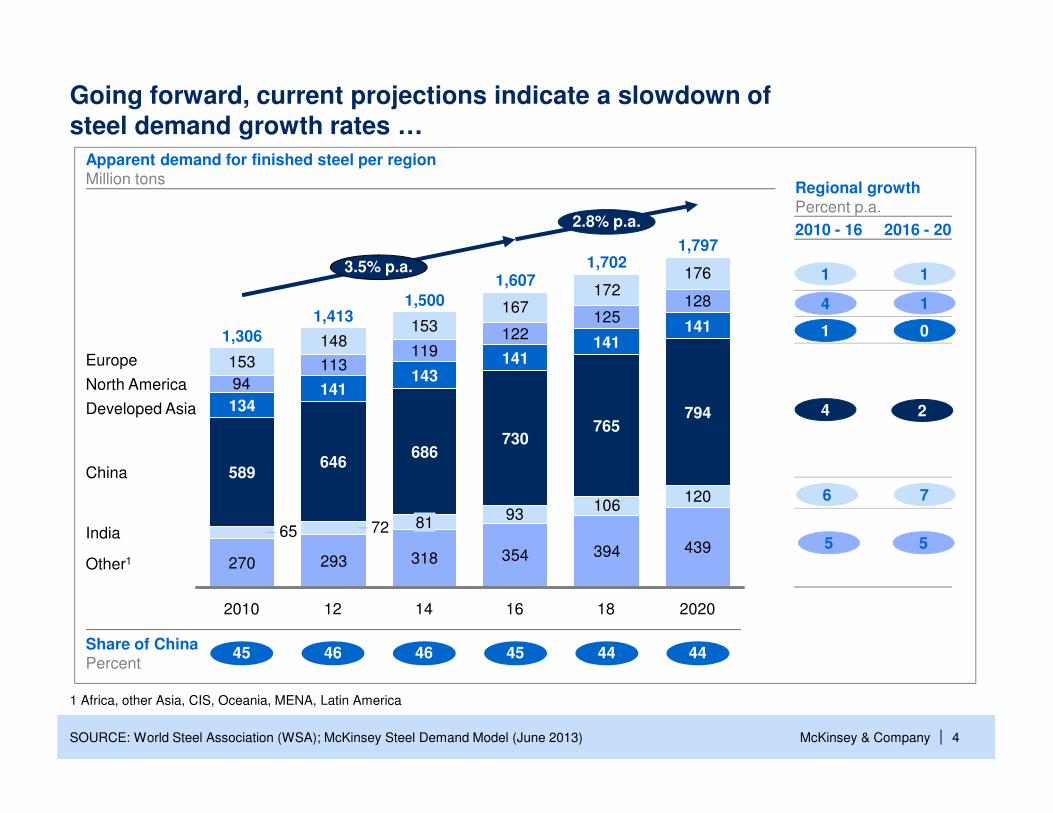

Going forward, current projections indicate a slowdown ofsteel demand growth rates …

270 293 318 354 394 439

93106

120

94113

119122

125128

153

148153

167172

176

7265

2.8% p.a.

3.5% p.a.

Other1

India

China

Developed Asia

North America

Europe

2020

1,797

794

141

18

1,702

765

16

1,607

730

141

14

1,500

81

686

143

12

1,413

646

141

2010

1,306

589

134

141

SOURCE: World Steel Association (WSA); McKinsey Steel Demand Model (June 2013)

Regional growthPercent p.a.

0

1

1

Share of ChinaPercent

45 46 45 4446 44

1

4

1

7

2

6

4

Apparent demand for finished steel per regionMillion tons

1 Africa, other Asia, CIS, Oceania, MENA, Latin America

5 5

2010 - 16 2016 - 20

McKinsey & Company | 5

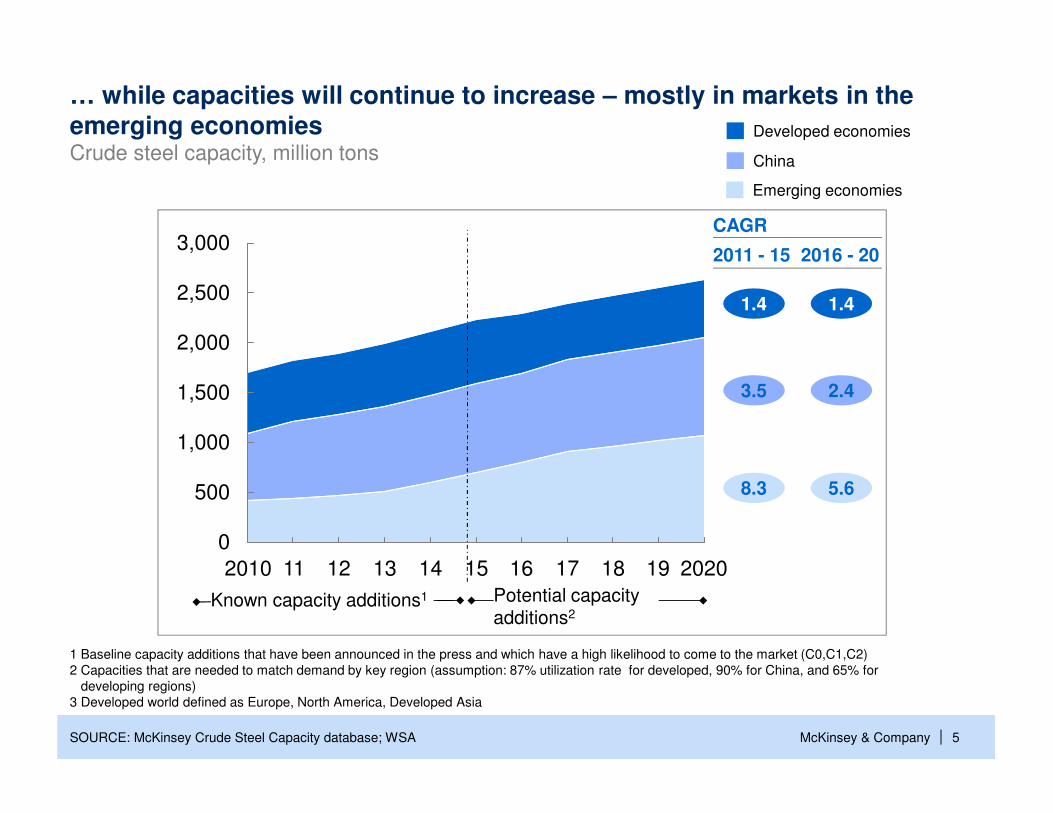

… while capacities will continue to increase – mostly in markets in the emerging economies

1 Baseline capacity additions that have been announced in the press and which have a high likelihood to come to the market (C0,C1,C2)

2 Capacities that are needed to match demand by key region (assumption: 87% utilization rate for developed, 90% for China, and 65% for

developing regions)

3 Developed world defined as Europe, North America, Developed Asia

Crude steel capacity, million tons

SOURCE: McKinsey Crude Steel Capacity database; WSA

3,000

2,500

2,000

1,500

1,000

500

0

20201918171615141312112010

Known capacity additions1 Potential capacity additions2

2011 - 15 2016 - 20

3.5

1.4

8.3

2.4

1.4

5.6

CAGR

Emerging economies

China

Developed economies

McKinsey & Company | 6

Global

Developed Asia

North America Europe

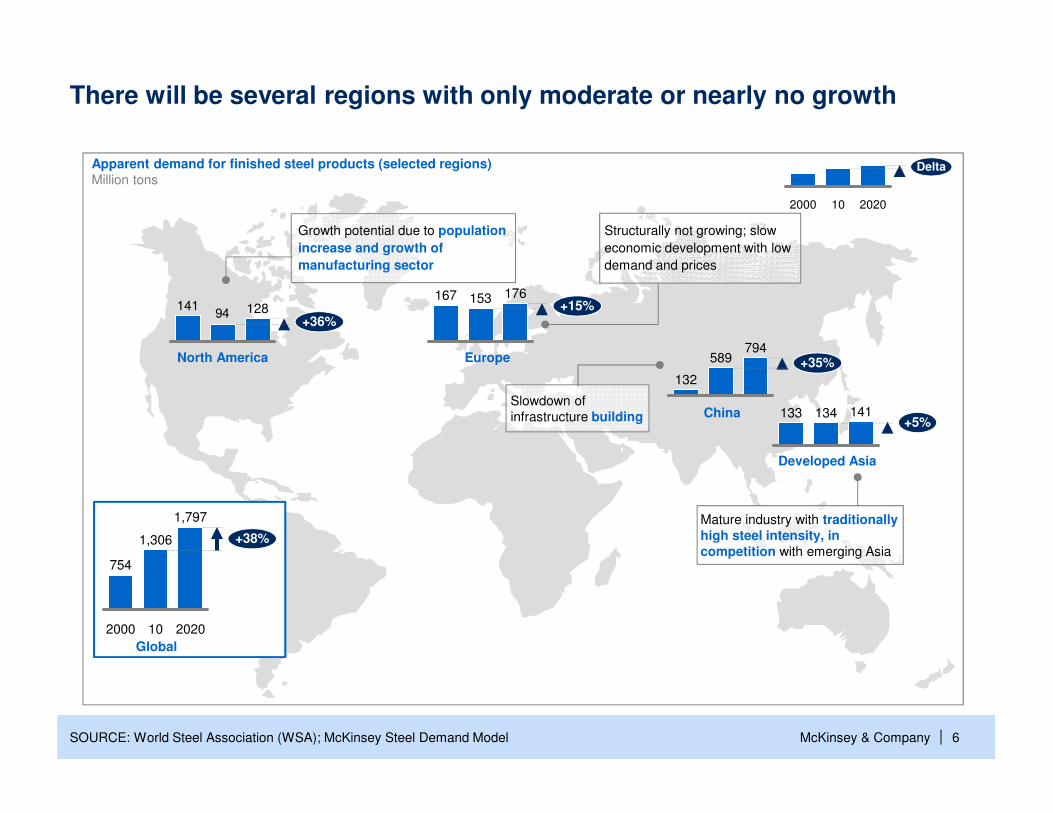

Growth potential due to population

increase and growth of

manufacturing sector

China

Apparent demand for finished steel products (selected regions)Million tons

There will be several regions with only moderate or nearly no growth

SOURCE: World Steel Association (WSA); McKinsey Steel Demand Model

Slowdown of

infrastructure building

1,797

+38%

202010

1,306

2000

754

Delta

2020102000

141+5%

134133

94 128+36%

141176

+15%153167

Structurally not growing; slow

economic development with low

demand and prices

794+35%589

132

Mature industry with traditionally high steel intensity, in competition with emerging Asia

Global

McKinsey & Company | 7

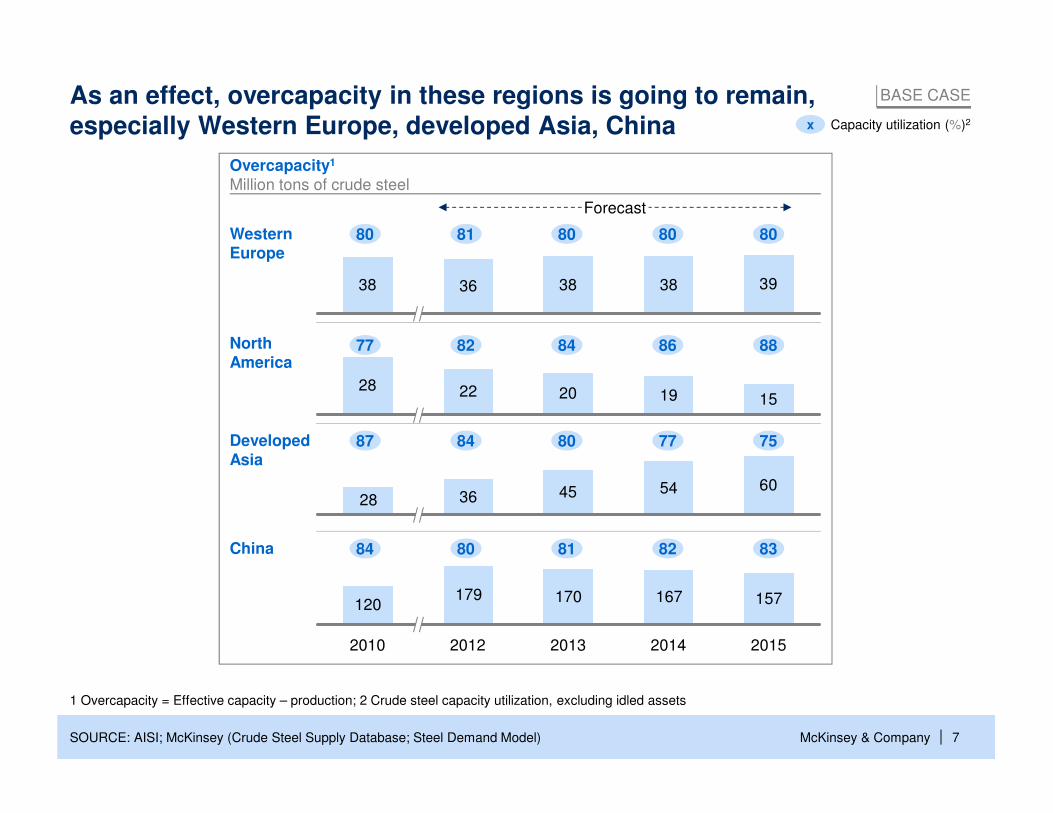

As an effect, overcapacity in these regions is going to remain,especially Western Europe, developed Asia, China

SOURCE: AISI; McKinsey (Crude Steel Supply Database; Steel Demand Model)

1 Overcapacity = Effective capacity – production; 2 Crude steel capacity utilization, excluding idled assets

BASE CASE

x Capacity utilization (%)2

38 36 38 38 39

Overcapacity1

Million tons of crude steel

80 81 80 80 80

Forecast

28 22 20 19 15

36 45 54 6028

120179 170 167 157

20152014201320122010

77 82 84 86 88

87 84 80 77 75

84 80 81 82 83

Western Europe

North America

Developed Asia

China

McKinsey & Company | 8

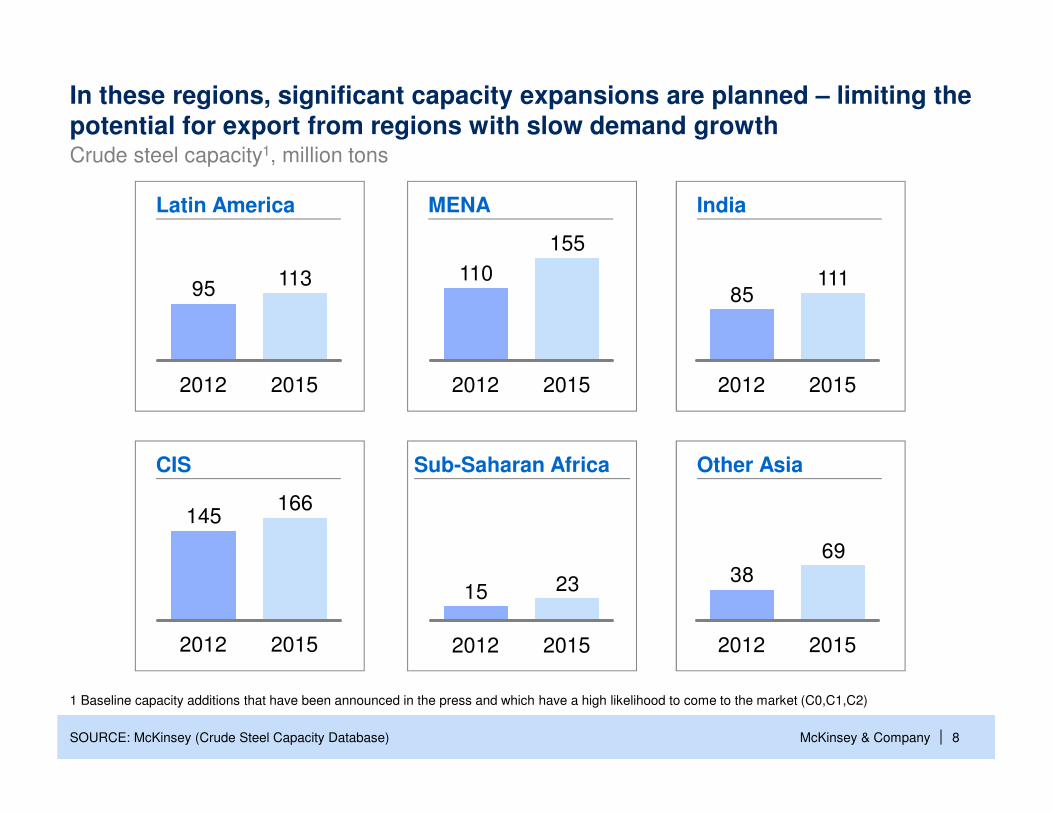

In these regions, significant capacity expansions are planned – limiting the potential for export from regions with slow demand growth Crude steel capacity1, million tons

SOURCE: McKinsey (Crude Steel Capacity Database)

95113

20152012

Latin America

2012

110

155

2015

MENA India

85

20152012

111

2315

2012 2015

Sub-Saharan Africa Other Asia

6938

201520122012 2015

145166

CIS

1 Baseline capacity additions that have been announced in the press and which have a high likelihood to come to the market (C0,C1,C2)

McKinsey & Company |SOURCE: McKinsey

Trends with significant impact on steel demand, varying by end user segment

ILLUSTRATIVE

Transport

Construction

Equipment

Metal goods

Shipbuilding

Oil & gas

180

672

356

91

60

155

Demand 2012 (Million tons)

Steel Intensity 2025(Indexed, 2012)

85-90

105

~100

100-105

95-100

~100

Overall industry trend

Urbanization drives a shift towards organized construction and higher buildings,

resulting in increased steel intensity

Increased mechanization (e.g., off-site cutting and bending of steel) to reduce wastage

Higher buildings and more prefabrications foster a product shift towards more structural steel

Demand and, partly, production shift to emerging countries is ongoing, which can

imply decreased intensities in Europe, but on overall, the sector will remain stable.

Mechanization will drive demand in emerging countries

Unconventional technologies (shale, CBM, etc.) and deep-water drilling is

increasing which is more steel intensive than conventional technologies

Shift in pipe materials, e.g., for flexible piping is ongoing

Demand and production shift implies an increased need for new distribution pipelines

Current large overcapacity will drive a decrease in orders in the coming years

Larger vessels can imply less total material and a decrease in steel intensities

Consumer appliances player experimenting with a lot of new material (e.g., glass) but

stainless steel likely to dominate the market

Growth of lightweight materials, mainly in cars, is ongoing, so far especially in

Europe (China to catch up by 2030)

Intensified penetration of electrical vehicles which have lower steel intensity as

compared to conventional vehicle

Size of vehicles is shifting, depending on region

McKinsey & Company | 10

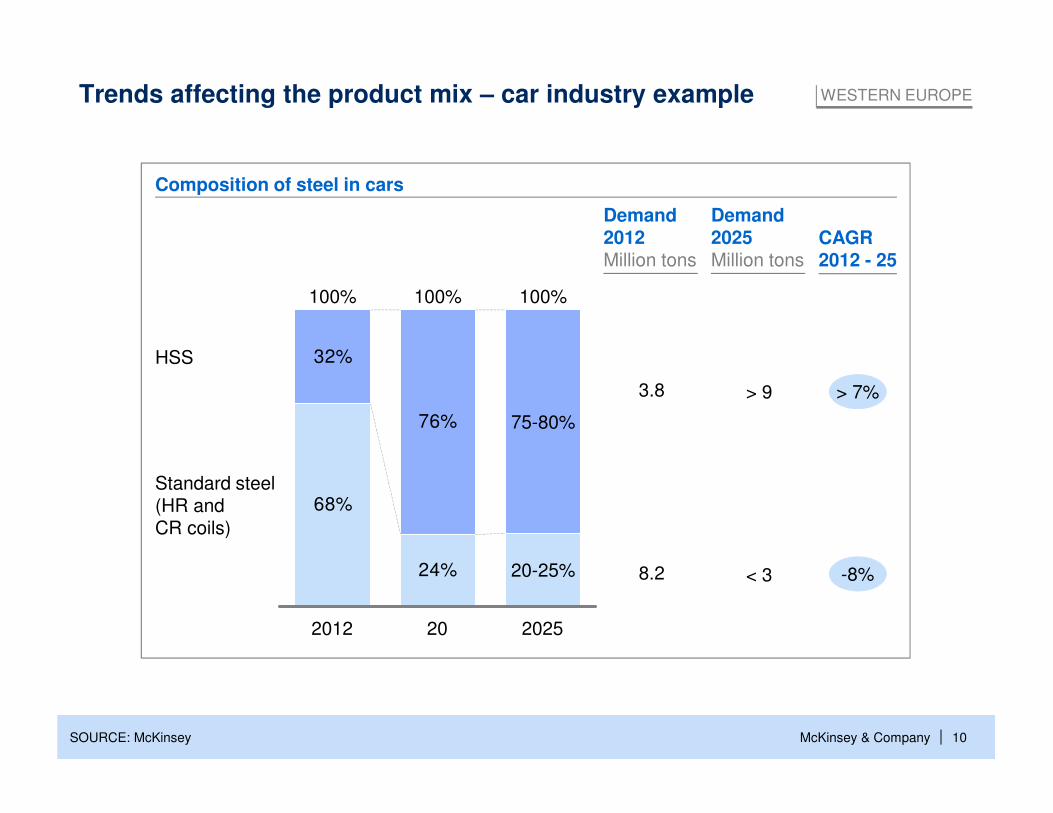

Trends affecting the product mix – car industry example

Demand2012Million tons

Demand2025Million tons

CAGR2012 - 25

68%

24%

32%

76%

Standard steel (HR and CR coils)

HSS

2025

100%

20-25%

75-80%

20

100%

2012

100%

3.8

8.2

> 7%

-8%

> 9

< 3

WESTERN EUROPE

SOURCE: McKinsey

Composition of steel in cars

McKinsey & Company | 11

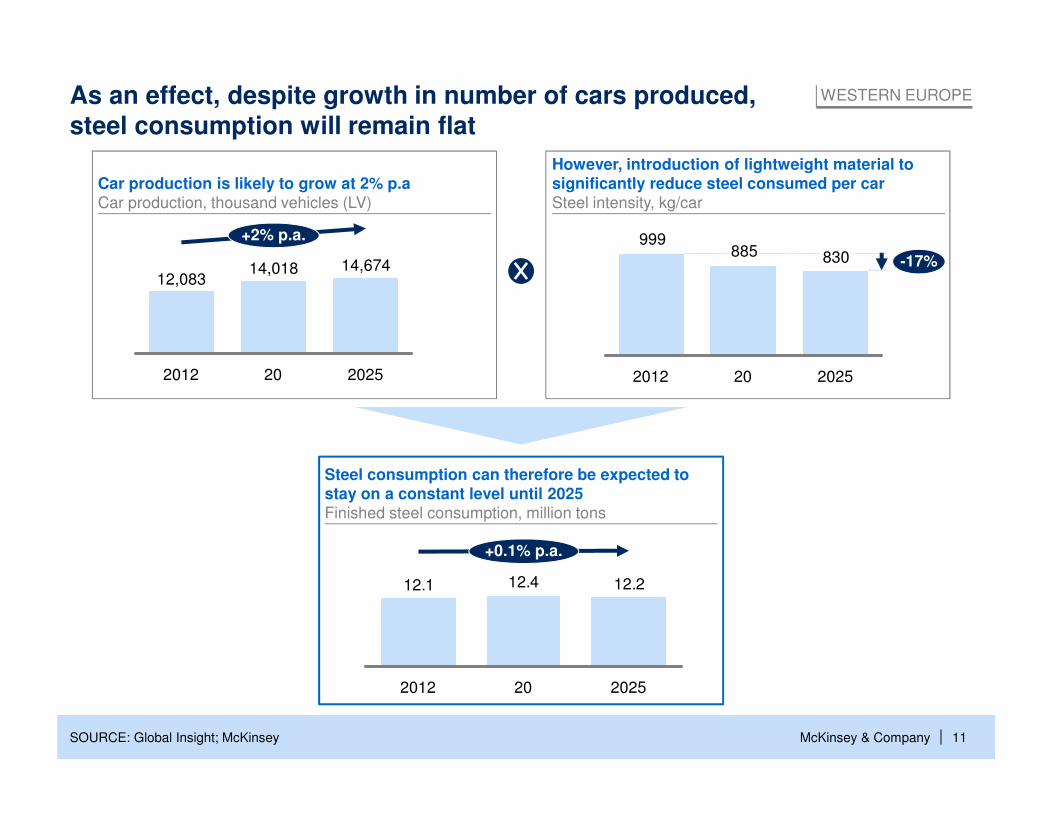

As an effect, despite growth in number of cars produced, steel consumption will remain flat

+2% p.a.

2025

14,674

20

14,018

2012

12,083

12.212.412.1

+0.1% p.a.

2025202012

830885999

-17%

2025202012

WESTERN EUROPE

SOURCE: Global Insight; McKinsey

However, introduction of lightweight material to significantly reduce steel consumed per carSteel intensity, kg/car

Car production is likely to grow at 2% p.aCar production, thousand vehicles (LV)

Steel consumption can therefore be expected to stay on a constant level until 2025Finished steel consumption, million tons

McKinsey & Company | 12

▪ Overcapacities in the steel

industry – a challenge that will persist

▪ Industry restructuring – financial situation of many steel companies will require help from outside of the industry

Contents

McKinsey & Company | 13

06

18.5

07

10.0

08

-2.7

09 10

-24.1

-16.2

11

-29.8

11.3

13E

0.6

12E 2014E04

24.8

05

18.820.9

03

9.3

02

1.3

01

-0.9

2000

0.9

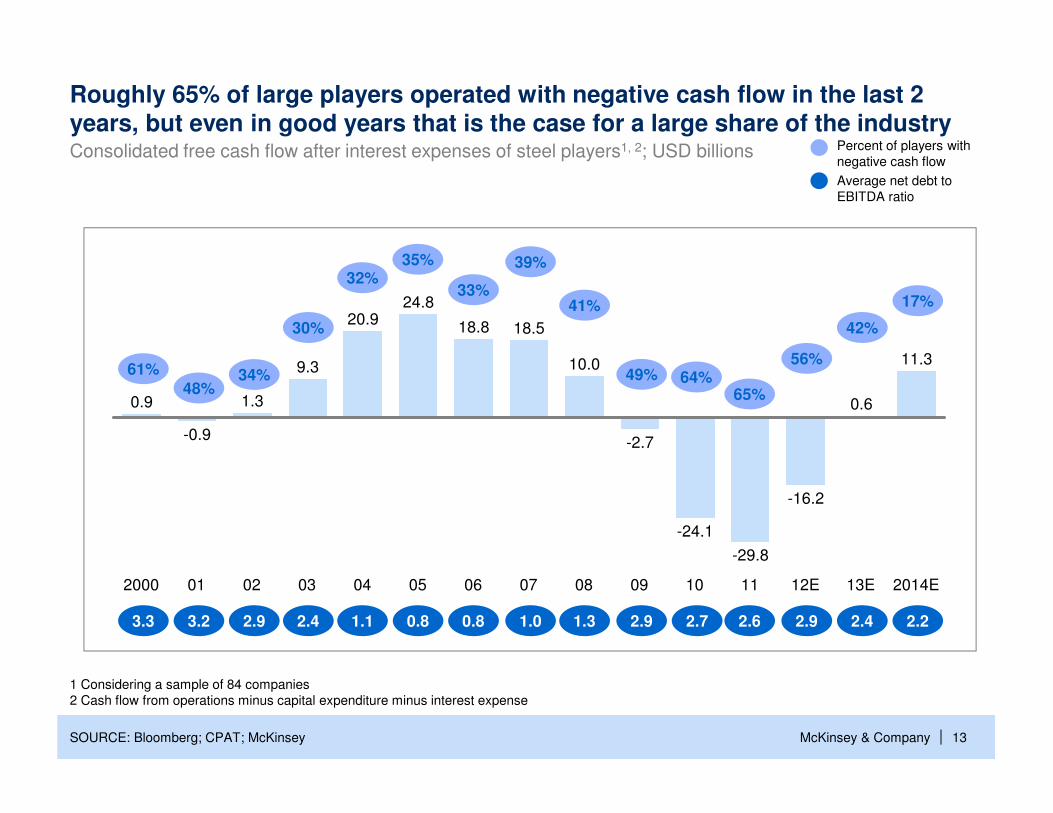

Roughly 65% of large players operated with negative cash flow in the last 2 years, but even in good years that is the case for a large share of the industry

SOURCE: Bloomberg; CPAT; McKinsey

Consolidated free cash flow after interest expenses of steel players1, 2; USD billions

1 Considering a sample of 84 companies

2 Cash flow from operations minus capital expenditure minus interest expense

Percent of players with

negative cash flow

Average net debt to

EBITDA ratio

3.3 3.2 2.9 2.4 1.1 0.8 0.8 1.0 1.3 2.9 2.7 2.9 2.4 2.22.6

61%

48%34%

30%

32%33%

39%

41%

49%

65%

56%

42%

17%

64%

35%

McKinsey & Company | 14

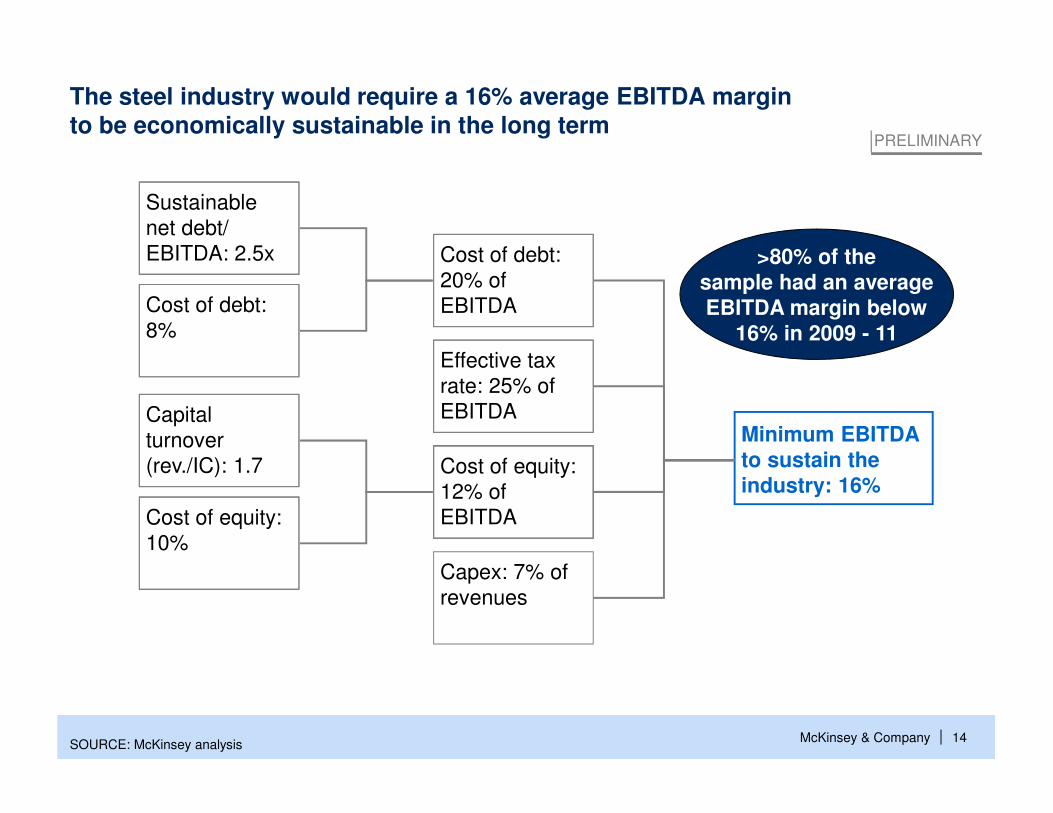

The steel industry would require a 16% average EBITDA margin to be economically sustainable in the long term

SOURCE: McKinsey analysis

Sustainable

net debt/

EBITDA: 2.5x

Cost of debt:

8%

Minimum EBITDA to sustain the industry: 16%

Capex: 7% of

revenues

Effective tax

rate: 25% of

EBITDA

Cost of debt:

20% of

EBITDA

Cost of equity:

12% of

EBITDA

Capital

turnover

(rev./IC): 1.7

Cost of equity:

10%

PRELIMINARY

>80% of thesample had an average EBITDA margin below

16% in 2009 - 11

McKinsey & Company | 15

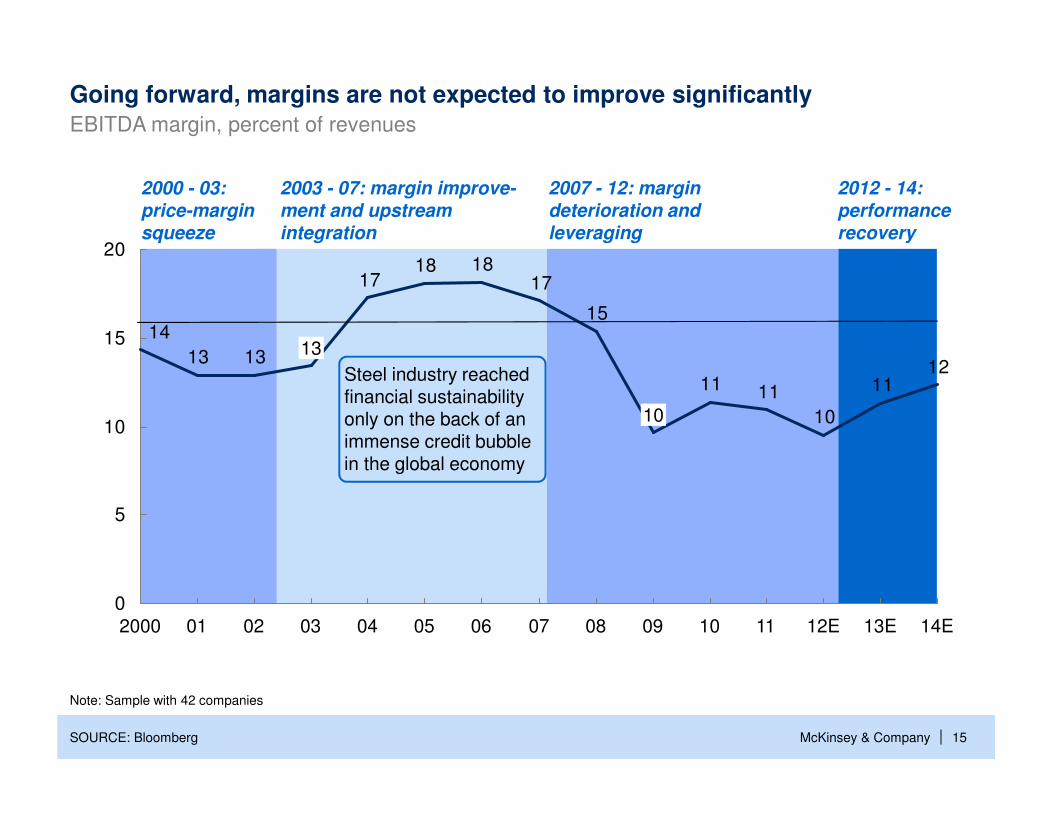

Going forward, margins are not expected to improve significantly

SOURCE: Bloomberg

EBITDA margin, percent of revenues

2000 - 03:

price-margin

squeeze

2003 - 07: margin improve-

ment and upstream

integration

2007 - 12: margin

deterioration and

leveraging

2012 - 14:

performance

recovery

1211

10

1111

15

171818

17

1313

14

0

5

10

15

20

10

14E13E12E11100908070605040302012000

13

Note: Sample with 42 companies

Steel industry reached financial sustainability only on the back of an immense credit bubble in the global economy

McKinsey & Company | 16

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

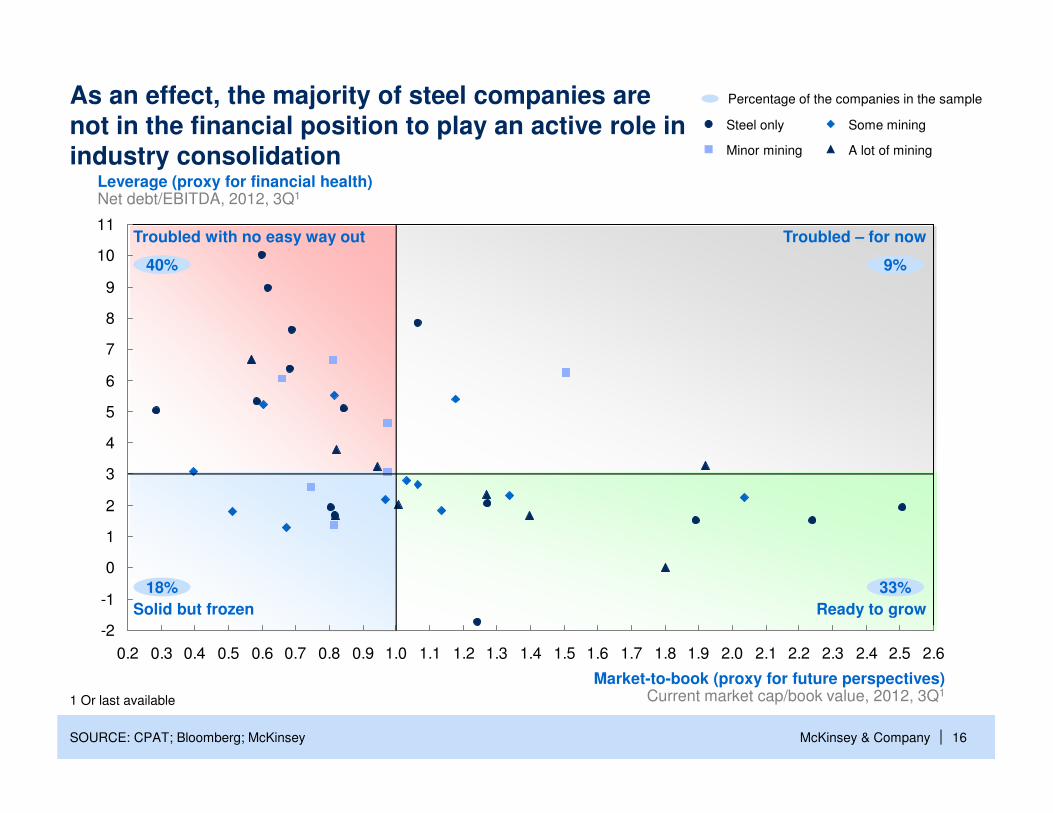

0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4 2.5 2.6

Leverage (proxy for financial health)Net debt/EBITDA, 2012, 3Q1

Market-to-book (proxy for future perspectives)Current market cap/book value, 2012, 3Q1

As an effect, the majority of steel companies are not in the financial position to play an active role in industry consolidation

SOURCE: CPAT; Bloomberg; McKinsey

Troubled with no easy way out Troubled – for now

Solid but frozen Ready to grow

Percentage of the companies in the sample

A lot of mining

Some mining

Minor mining

Steel only

9%

1 Or last available

40%

18% 33%

McKinsey & Company | 17

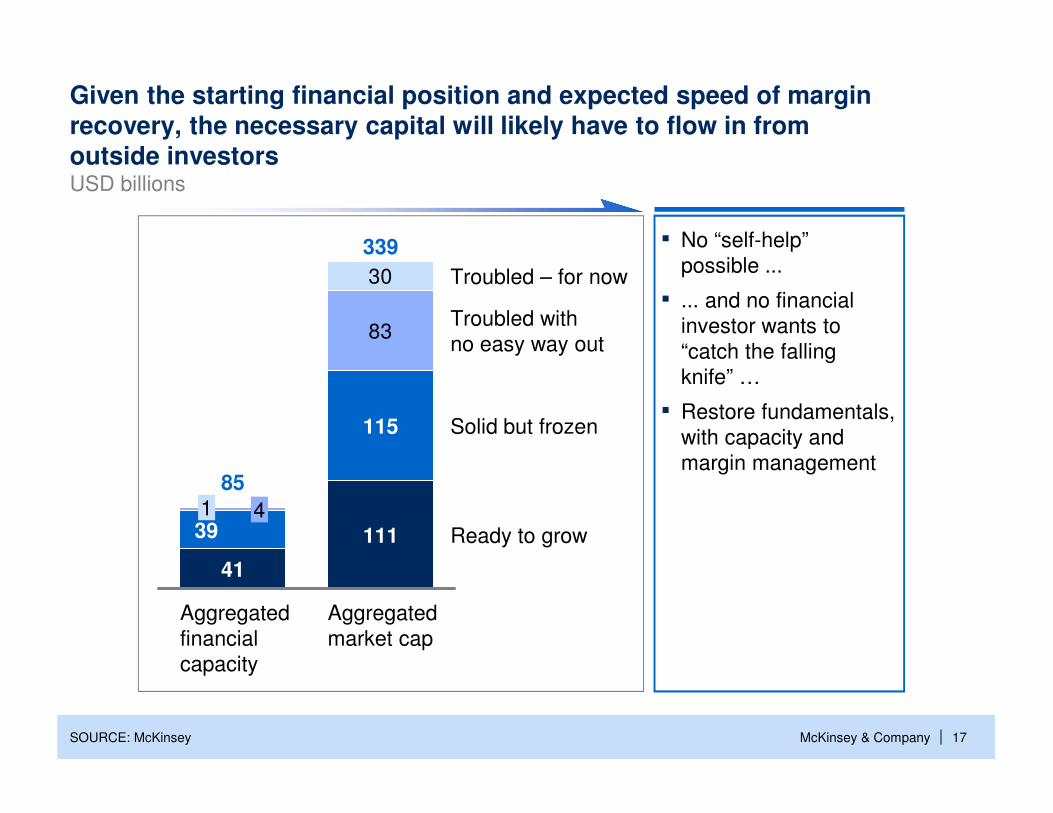

Given the starting financial position and expected speed of margin recovery, the necessary capital will likely have to flow in from outside investors

83

30

Ready to grow

Solid but frozen

Troubled with

no easy way out

Troubled – for now

Aggregated

market cap

339

111

115

Aggregated

financial

capacity

85

41

3941

SOURCE: McKinsey

USD billions

▪ No “self-help”

possible ...

▪ ... and no financial

investor wants to

“catch the falling

knife” …

▪ Restore fundamentals,

with capacity and

margin management