Embed Size (px)

Citation preview

Outlook for 2014

January 2014 Henry H. McVey

2

Important InformationThe views expressed in this presentation are the personal views of Henry McVey of Kohlberg Kravis Roberts & Co. L.P. (together with its affiliates, "KKR") and do not necessarily reflect the views of KKR itself. This presentation is not research and should not be treated as research. This presentation does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of KKR. This presentation is not intended to, and does not, relate specifically to any investment strategy or product that KKR offers. It is being provided merely to provide a framework to assist in the implementation of an investor’s own analysis and an investor’s own views on the topic discussed herein.

The views expressed reflect the current views of Mr. McVey as of the date hereof and neither Mr. McVey nor KKR undertakes to advise you of any changes in the views expressed herein. In addition, the views expressed do not necessarily reflect the opinions of any investment professional at KKR, and may not be reflected in the strategies and products that KKR offers, including strategies and products to which Mr. McVey provides investment advice on behalf of KKR. It should not be assumed that Mr. McVey will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein in managing client accounts. KKR and its affiliates may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this presentation.

This presentation has been prepared solely for informational purposes. The information contained herein is only as current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Charts and graphs provided herein are for illustrative purposes only. The information in this presentation has been developed internally and/or obtained from sources believed to be reliable; however, neither KKR nor Mr. McVey guarantees the accuracy, adequacy or completeness of such information. Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision.

There can be no assurance that an investment strategy will be successful. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. Target allocations contained herein are subject to change. There is no assurance that the target allocations will be achieved, and actual allocations may be significantly different than that shown here. This presentation should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy.

The information in this presentation may contain projections or other forward looking statements regarding future events, targets, forecasts or expectations regarding the strategies ‐described herein, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different from that shown here. The information in this presentation, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Performance of all cited indices is calculated on a total return basis with dividends reinvested. The indices do not include any expenses, fees or charges and are unmanaged and should not be considered investments.

The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Please note that changes in the rate of exchange of a currency may affect the value, price or income of an investment adversely.

Neither KKR nor Mr. McVey assumes any duty to, nor undertakes to update forward looking statements. No representation or warranty, express or implied, is made or given by or on behalf of KKR, Mr. McVey or any other person as to the accuracy and completeness or fairness of the information contained in this presentation, and no responsibility or liability is accepted for any such information. By accepting this presentation in its entirety, the recipient acknowledges its understanding and acceptance of the foregoing statement.

The MSCI sourced information in this presentation is the exclusive property of MSCI Inc. (MSCI). MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

I. Key Macro Conclusions & Economic Outlook

4

Outlook 2014: “Stay the Course” As a Global Recovery Unfolds

What Does “Stay the Course” Mean?

1. Retain key overweight positions in global equities and alternatives, including private credit, special situations and real assets.

2. To fund these risk buckets, we continue to target a massive underweight to government bonds and investment grade debt.

3. However, 2014 will not be a repeat of 2013. In particular, we believe 1) the “drag” from government austerity should decline in 2014; 2) equity trading multiples for stocks are now ahead of schedule.

5

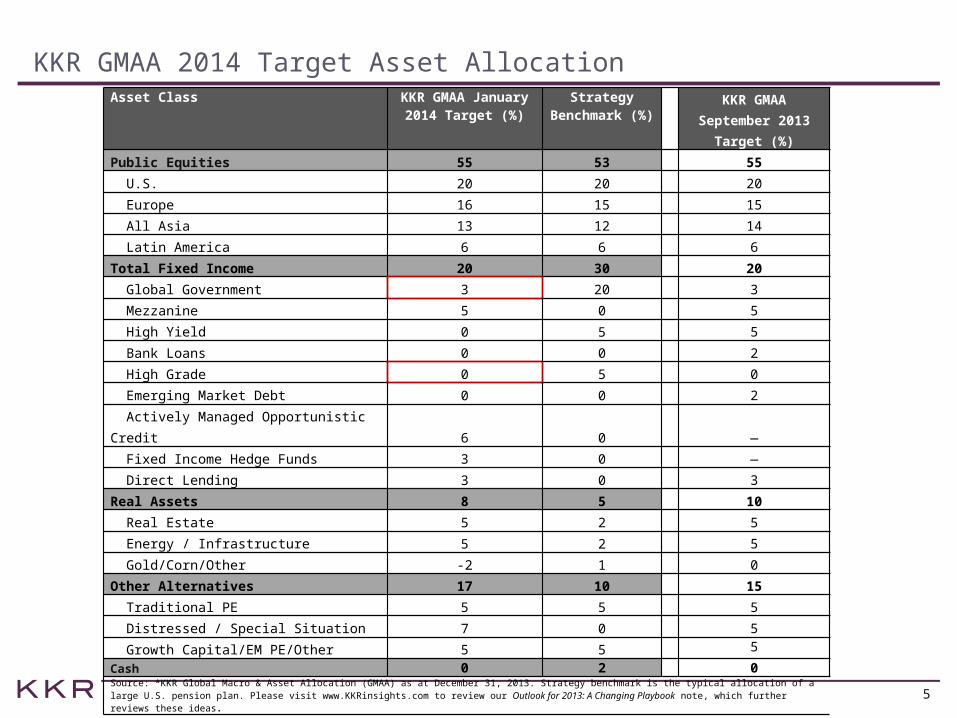

KKR GMAA 2014 Target Asset AllocationAsset Class KKR GMAA January

2014 Target (%)Strategy

Benchmark (%)

KKR GMAA September 2013

Target (%)

Public Equities 55 53 55

U.S. 20 20 20

Europe 16 15 15

All Asia 13 12 14

Latin America 6 6 6

Total Fixed Income 20 30 20

Global Government 3 20 3

Mezzanine 5 0 5

High Yield 0 5 5

Bank Loans 0 0 2

High Grade 0 5 0

Emerging Market Debt 0 0 2

Actively Managed Opportunistic Credit 6 0 ―

Fixed Income Hedge Funds 3 0 ―

Direct Lending 3 0 3

Real Assets 8 5 10

Real Estate 5 2 5

Energy / Infrastructure 5 2 5

Gold/Corn/Other -2 1 0

Other Alternatives 17 10 15

Traditional PE 5 5 5

Distressed / Special Situation 7 0 5

Growth Capital/EM PE/Other 5 5 5

Cash 0 2 0Source: *KKR Global Macro & Asset Allocation (GMAA) as at December 31, 2013. Strategy benchmark is the typical allocation of a large U.S. pension plan. Please visit www.KKRinsights.com to review our Outlook for 2013: A Changing Playbook note, which further reviews these ideas.

6

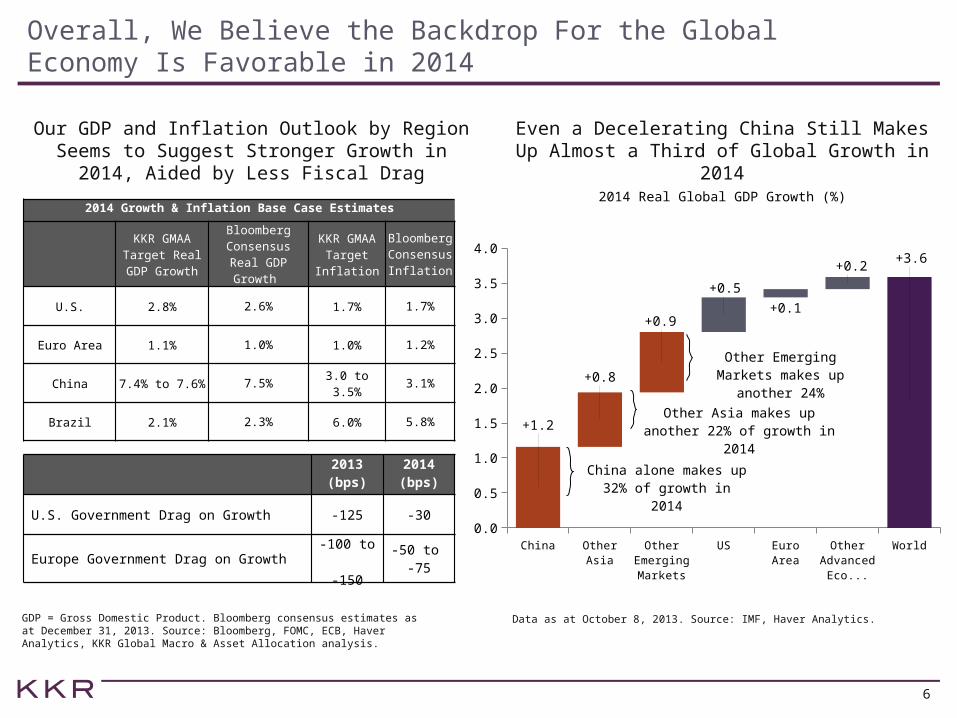

Overall, We Believe the Backdrop For the Global Economy Is Favorable in 2014

2014 Growth & Inflation Base Case Estimates

KKR GMAA Target Real GDP Growth

Bloomberg Consensus Real

GDP Growth

KKR GMAA Target

Inflation

Bloomberg Consensus

Inflation

U.S. 2.8% 2.6% 1.7% 1.7%

Euro Area 1.1% 1.0% 1.0% 1.2%

China 7.4% to 7.6% 7.5% 3.0 to 3.5% 3.1%

Brazil 2.1% 2.3% 6.0% 5.8%

Our GDP and Inflation Outlook by Region Seems to Suggest Stronger Growth in 2014,

Aided by Less Fiscal Drag

Even a Decelerating China Still Makes Up Almost a Third of Global Growth in 2014

China Other Asia

Other Emerging Markets

US Euro Area Other Ad-

vanced Economie

s

World0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

+1.2

+0.8

+0.9

+0.5

+0.1

+0.2+3.6

2014 Real Global GDP Growth (%)

China alone makes up 32% of growth in 2014

Other Asia makes up another 22% of growth in 2014

Other Emerging Markets makes up another 24%

GDP = Gross Domestic Product. Bloomberg consensus estimates as at December 31, 2013. Source: Bloomberg, FOMC, ECB, Haver Analytics, KKR Global Macro & Asset Allocation analysis.

Data as at October 8, 2013. Source: IMF, Haver Analytics.

2013 (bps)

2014 (bps)

U.S. Government Drag on Growth -125 -30

Europe Government Drag on Growth -100 to -150

-50 to -75

7

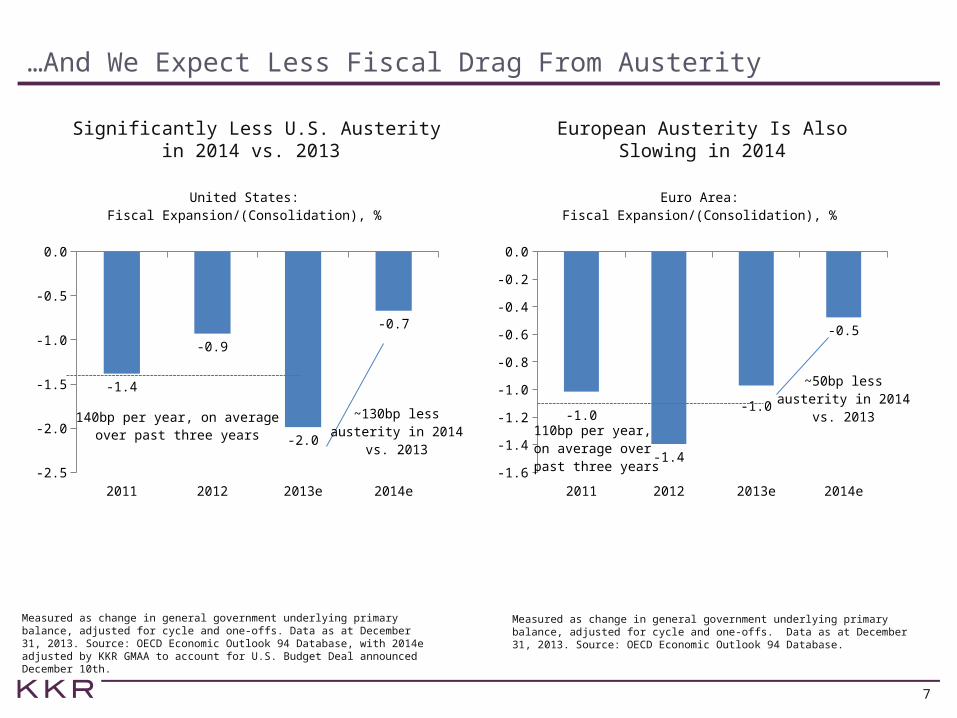

…And We Expect Less Fiscal Drag From Austerity

Significantly Less U.S. Austerity in 2014 vs. 2013

European Austerity Is Also Slowing in 2014

Measured as change in general government underlying primary balance, adjusted for cycle and one-offs. Data as at December 31, 2013. Source: OECD Economic Outlook 94 Database, with 2014e adjusted by KKR GMAA to account for U.S. Budget Deal announced December 10th.

Measured as change in general government underlying primary balance, adjusted for cycle and one-offs. Data as at December 31, 2013. Source: OECD Economic Outlook 94 Database.

2011 2012 2013e 2014e-2.5

-2.0

-1.5

-1.0

-0.5

0.0

-1.4

-0.9

-2.0

-0.7

United States:Fiscal Expansion/(Consolidation), %

~130bp lessausterity in 2014

vs. 2013

140bp per year, on averageover past three years

2011 2012 2013e 2014e-1.6

-1.4

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

-1.0

-1.4

-1.0

-0.5

Euro Area:Fiscal Expansion/(Consolidation), %

~50bp lessausterity in 2014

vs. 2013

110bp per year, on average over past three years

8

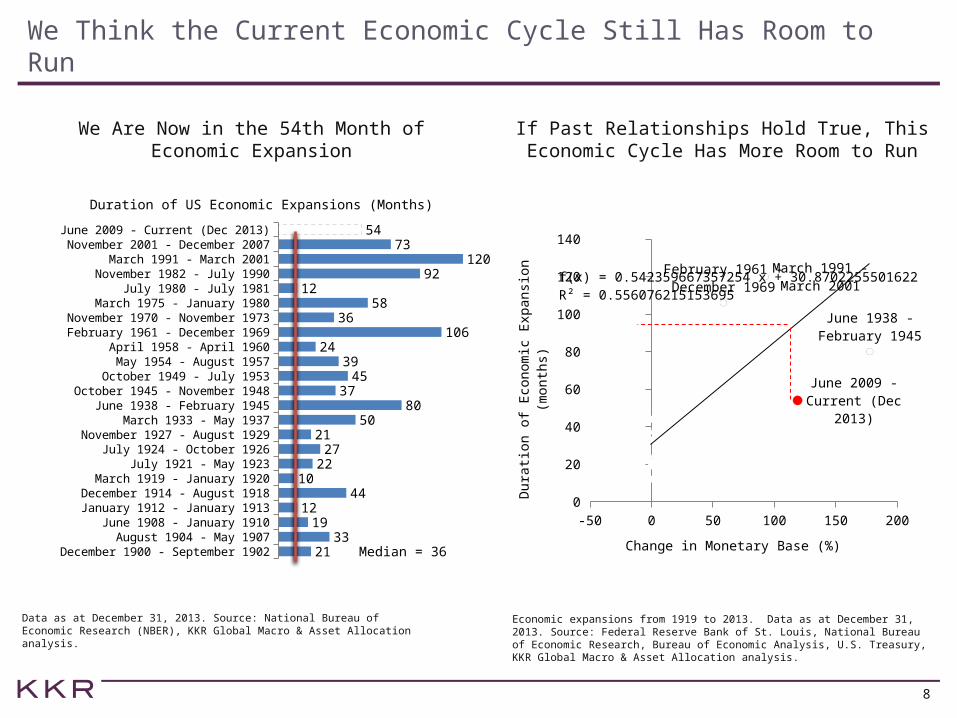

We Think the Current Economic Cycle Still Has Room to Run

We Are Now in the 54th Month of Economic Expansion

If Past Relationships Hold True, This Economic Cycle Has More Room to Run

Data as at December 31, 2013. Source: National Bureau of Economic Research (NBER), KKR Global Macro & Asset Allocation analysis.

Economic expansions from 1919 to 2013. Data as at December 31, 2013. Source: Federal Reserve Bank of St. Louis, National Bureau of Economic Research, Bureau of Economic Analysis, U.S. Treasury, KKR Global Macro & Asset Allocation analysis.

December 1900 - September 1902August 1904 - May 1907

June 1908 - January 1910January 1912 - January 1913

December 1914 - August 1918March 1919 - January 1920

July 1921 - May 1923July 1924 - October 1926

November 1927 - August 1929March 1933 - May 1937

June 1938 - February 1945October 1945 - November 1948

October 1949 - July 1953May 1954 - August 1957

April 1958 - April 1960February 1961 - December 1969

November 1970 - November 1973March 1975 - January 1980

July 1980 - July 1981November 1982 - July 1990

March 1991 - March 2001November 2001 - December 2007

June 2009 - Current (Dec 2013)

2133

1912

4410

2227

2150

8037

4539

24106

3658

1292

12073

54

Duration of US Economic Expansions (Months)

Median = 36

-50 0 50 100 150 2000

20

40

60

80

100

120

140

February 1961 - December 1969

March 1991 - March 2001

June 1938 - Feb-ruary 1945

June 2009 - Cur-rent (Dec 2013)

f(x) = 0.542359667357254 x + 30.8702255501622R² = 0.556076215153695

Change in Monetary Base (%)D

ura

tion o

f Eco

nom

ic E

xpansi

on (

month

s)

II. Macro Themes

10

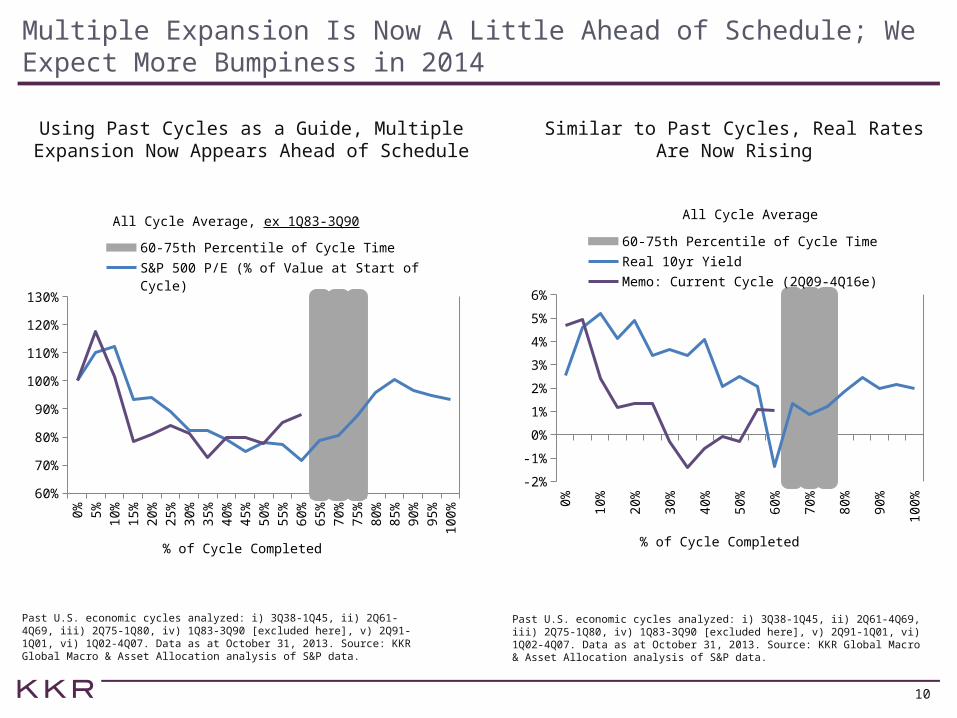

Multiple Expansion Is Now A Little Ahead of Schedule; We Expect More Bumpiness in 2014

Using Past Cycles as a Guide, Multiple Expansion Now Appears Ahead of Schedule

Similar to Past Cycles, Real Rates Are Now Rising

Past U.S. economic cycles analyzed: i) 3Q38-1Q45, ii) 2Q61-4Q69, iii) 2Q75-1Q80, iv) 1Q83-3Q90 [excluded here], v) 2Q91-1Q01, vi) 1Q02-4Q07. Data as at October 31, 2013. Source: KKR Global Macro & Asset Allocation analysis of S&P data.

Past U.S. economic cycles analyzed: i) 3Q38-1Q45, ii) 2Q61-4Q69, iii) 2Q75-1Q80, iv) 1Q83-3Q90 [excluded here], v) 2Q91-1Q01, vi) 1Q02-4Q07. Data as at October 31, 2013. Source: KKR Global Macro & Asset Allocation analysis of S&P data.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

60%

70%

80%

90%

100%

110%

120%

130%

60-75th Percentile of Cycle TimeS&P 500 P/E (% of Value at Start of Cycle)Memo: Current Cycle (2Q09-4Q16e)

% of Cycle Completed

All Cycle Average, ex 1Q83-3Q90

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

60-75th Percentile of Cycle Time

Real 10yr Yield

Memo: Current Cycle (2Q09-4Q16e)

% of Cycle Completed

All Cycle Average

11

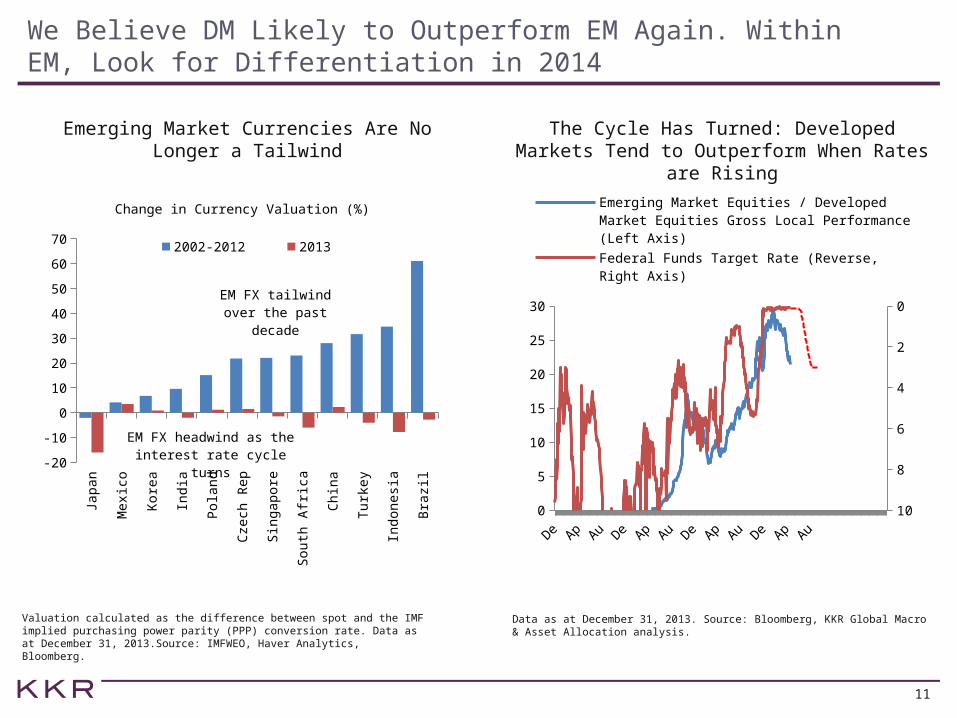

We Believe DM Likely to Outperform EM Again. Within EM, Look for Differentiation in 2014

Emerging Market Currencies Are No Longer a Tailwind

The Cycle Has Turned: Developed Markets Tend to Outperform When Rates are Rising

Valuation calculated as the difference between spot and the IMF implied purchasing power parity (PPP) conversion rate. Data as at December 31, 2013.Source: IMFWEO, Haver Analytics, Bloomberg.

Data as at December 31, 2013. Source: Bloomberg, KKR Global Macro & Asset Allocation analysis.

Japan

Mexic

o

Kore

a

India

Pola

nd

Cze

ch R

ep

Sin

gapore

South

Afr

ica

Chin

a

Turk

ey

Indonesi

a

Bra

zil

-20

-10

0

10

20

30

40

50

60

70

Change in Currency Valuation (%)

2002-2012 2013

EM FX tailwind over the past decade

EM FX headwind as the interest rate cycle turns

88 91 94 97 00 03 06 09 12 15 180

5

10

15

20

25

30 0

2

4

6

8

10

Emerging Market Equities / Developed Market Equities Gross Local Performance (Left Axis)

Federal Funds Target Rate (Reverse, Right Axis)

KKR Estimate (Reverse, Right Axis)

12

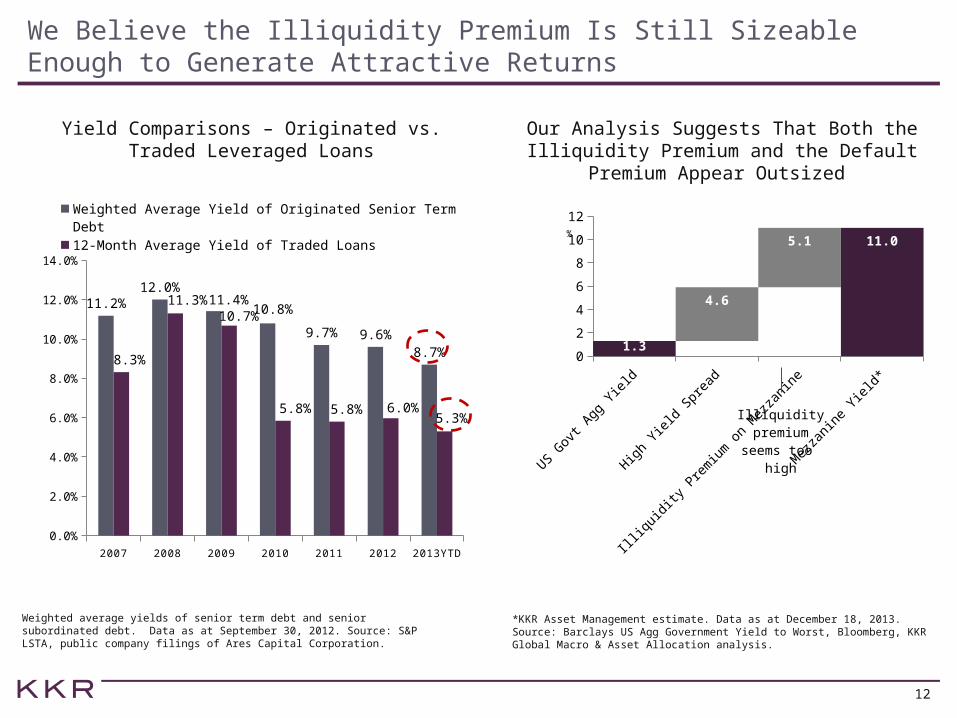

We Believe the Illiquidity Premium Is Still Sizeable Enough to Generate Attractive Returns

Yield Comparisons – Originated vs. Traded Leveraged Loans

Our Analysis Suggests That Both the Illiquidity Premium and the Default Premium

Appear Outsized

Weighted average yields of senior term debt and senior subordinated debt. Data as at September 30, 2012. Source: S&P LSTA, public company filings of Ares Capital Corporation.

*KKR Asset Management estimate. Data as at December 18, 2013. Source: Barclays US Agg Government Yield to Worst, Bloomberg, KKR Global Macro & Asset Allocation analysis.

2007 2008 2009 2010 2011 2012 2013YTD0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

11.2%12.0%

11.4%10.8%

9.7% 9.6%8.7%8.3%

11.3%10.7%

5.8% 5.8% 6.0%5.3%

Weighted Average Yield of Originated Senior Term Debt

12-Month Average Yield of Traded Loans

US Gov

t Agg

Yie

ld

High

Yiel

d Sp

read

Illiq

uidi

ty P

rem

ium

on

Mez

zani

ne

Mezza

nine

Yie

ld*

0

2

4

6

8

10

12

1.3

4.6

5.1 11.0%

Illiquidity premium

seems too high

13

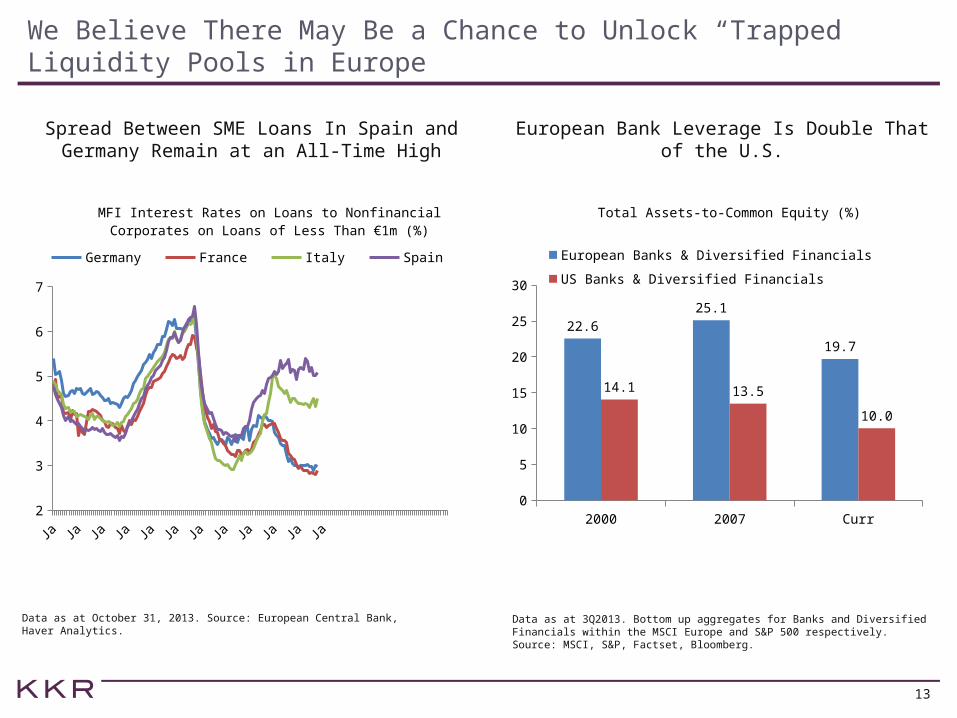

We Believe There May Be a Chance to Unlock “Trapped” Liquidity Pools in Europe

Spread Between SME Loans In Spain and Germany Remain at an All-Time High

European Bank Leverage Is Double That of the U.S.

Data as at October 31, 2013. Source: European Central Bank, Haver Analytics.

Data as at 3Q2013. Bottom up aggregates for Banks and Diversified Financials within the MSCI Europe and S&P 500 respectively. Source: MSCI, S&P, Factset, Bloomberg.

03 04 05 06 07 08 09 10 11 12 13 142

3

4

5

6

7

MFI Interest Rates on Loans to Nonfinancial Corpo-rates on Loans of Less Than €1m (%)

Germany France Italy Spain

2000 2007 Curr0

5

10

15

20

25

30

22.625.1

19.7

14.1 13.5

10.0

Total Assets-to-Common Equity (%)

European Banks & Diversified Financials

US Banks & Diversified Financials

III. Equities

15

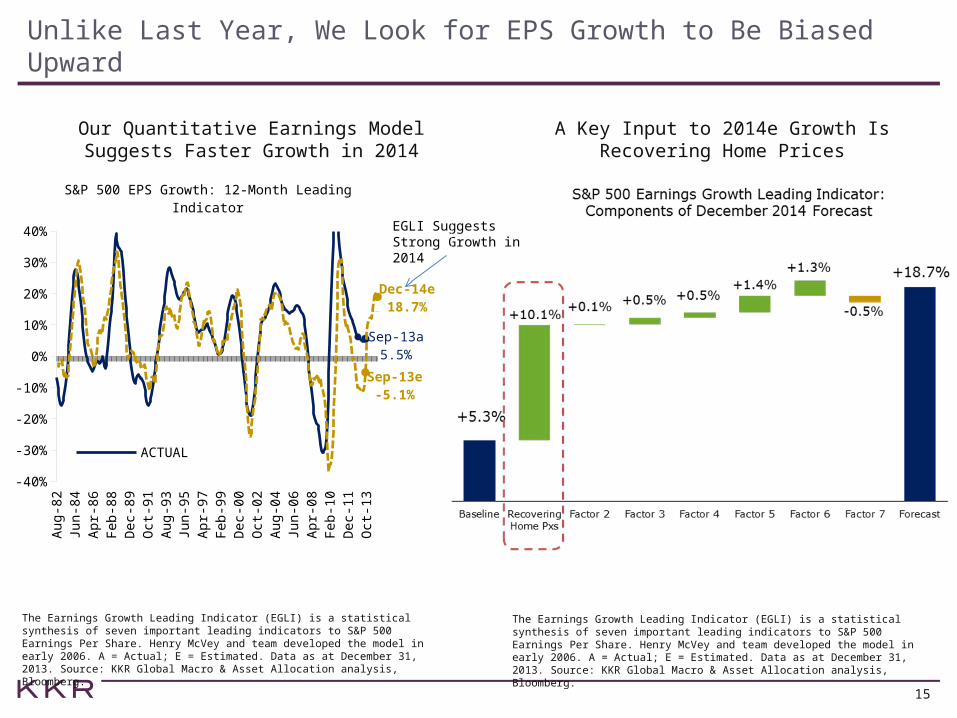

Unlike Last Year, We Look for EPS Growth to Be Biased Upward

Our Quantitative Earnings Model Suggests Faster Growth in 2014

A Key Input to 2014e Growth Is Recovering Home Prices

The Earnings Growth Leading Indicator (EGLI) is a statistical synthesis of seven important leading indicators to S&P 500 Earnings Per Share. Henry McVey and team developed the model in early 2006. A = Actual; E = Estimated. Data as at December 31, 2013. Source: KKR Global Macro & Asset Allocation analysis, Bloomberg.

The Earnings Growth Leading Indicator (EGLI) is a statistical synthesis of seven important leading indicators to S&P 500 Earnings Per Share. Henry McVey and team developed the model in early 2006. A = Actual; E = Estimated. Data as at December 31, 2013. Source: KKR Global Macro & Asset Allocation analysis, Bloomberg.

EGLI Suggests Strong Growth in 2014

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Sep-13a5.5%

Sep-13e-5.1%

Dec-14e18.7%

S&P 500 EPS Growth: 12-Month Leading Indicator

ACTUALPREDICTED (3mo MA)

16

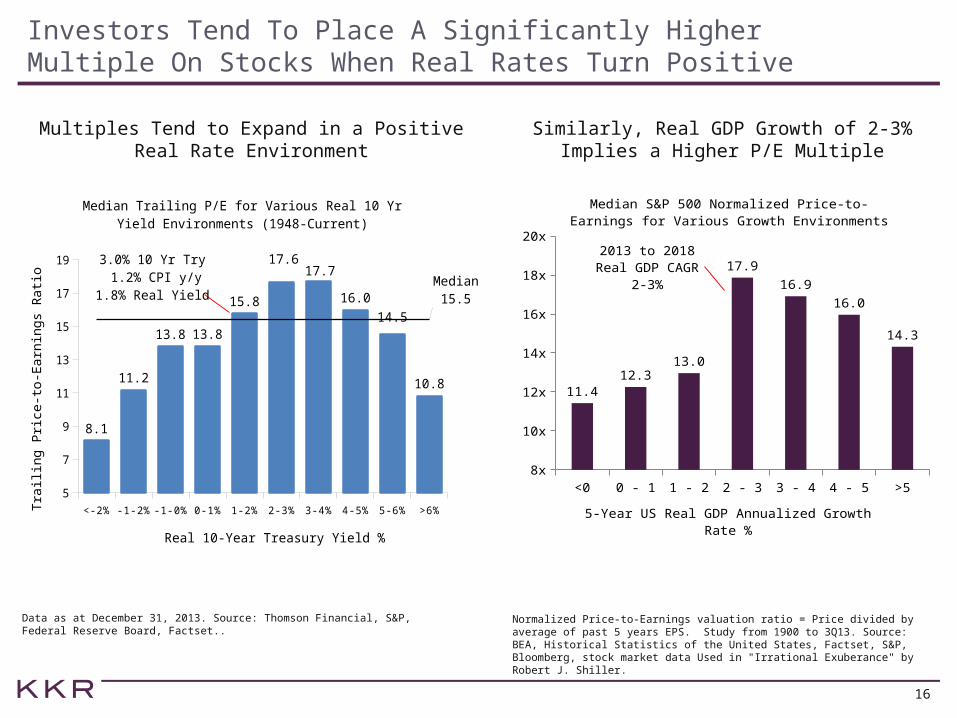

Investors Tend To Place A Significantly Higher Multiple On Stocks When Real Rates Turn Positive

Multiples Tend to Expand in a Positive Real Rate Environment

Similarly, Real GDP Growth of 2-3% Implies a Higher P/E Multiple

Data as at December 31, 2013. Source: Thomson Financial, S&P, Federal Reserve Board, Factset..

Normalized Price-to-Earnings valuation ratio = Price divided by average of past 5 years EPS. Study from 1900 to 3Q13. Source: BEA, Historical Statistics of the United States, Factset, S&P, Bloomberg, stock market data Used in "Irrational Exuberance" by Robert J. Shiller.

<-2% -1-2% -1-0% 0-1% 1-2% 2-3% 3-4% 4-5% 5-6% >6%5

7

9

11

13

15

17

19

8.1

11.2

13.8 13.8

15.8

17.617.7

16.0

14.5

10.8

Median15.5

Median Trailing P/E for Various Real 10 Yr Yield Envi-ronments (1948-Current)

Real 10-Year Treasury Yield %

Trai

ling

Pric

e-to

-Ear

ning

s R

atio

3.0% 10 Yr Try 1.2% CPI y/y

1.8% Real Yield

<0 0 - 1 1 - 2 2 - 3 3 - 4 4 - 5 >58x

10x

12x

14x

16x

18x

20x

11.412.3

13.0

17.9

16.9

16.0

14.3

Median S&P 500 Normalized Price-to-Earnings for Various Growth Environments

5-Year US Real GDP Annualized Growth Rate %

2013 to 2018 Real GDP CAGR 2-3%

17

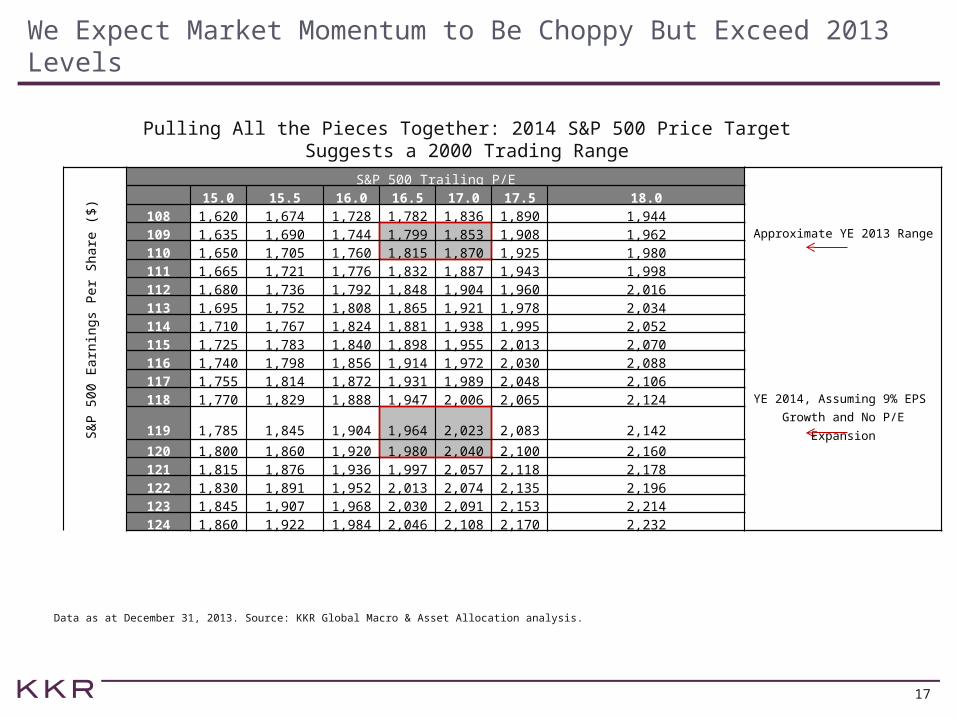

We Expect Market Momentum to Be Choppy But Exceed 2013 Levels

Pulling All the Pieces Together: 2014 S&P 500 Price Target Suggests a 2000 Trading Range

Data as at December 31, 2013. Source: KKR Global Macro & Asset Allocation analysis.

&P S&P 500 Trailing P/E 15.0 15.5 16.0 16.5 17.0 17.5 18.0

108 1,620 1,674 1,728 1,782 1,836 1,890 1,944 109 1,635 1,690 1,744 1,799 1,853 1,908 1,962 Approximate YE 2013 Range

110 1,650 1,705 1,760 1,815 1,870 1,925 1,980111 1,665 1,721 1,776 1,832 1,887 1,943 1,998 112 1,680 1,736 1,792 1,848 1,904 1,960 2,016 113 1,695 1,752 1,808 1,865 1,921 1,978 2,034 114 1,710 1,767 1,824 1,881 1,938 1,995 2,052 115 1,725 1,783 1,840 1,898 1,955 2,013 2,070 116 1,740 1,798 1,856 1,914 1,972 2,030 2,088 117 1,755 1,814 1,872 1,931 1,989 2,048 2,106 118 1,770 1,829 1,888 1,947 2,006 2,065 2,124 YE 2014, Assuming 9% EPS

119 1,785 1,845 1,904 1,964 2,023 2,083 2,142 Growth and No P/E Expansion

120 1,800 1,860 1,920 1,980 2,040 2,100 2,160121 1,815 1,876 1,936 1,997 2,057 2,118 2,178 122 1,830 1,891 1,952 2,013 2,074 2,135 2,196 123 1,845 1,907 1,968 2,030 2,091 2,153 2,214 124 1,860 1,922 1,984 2,046 2,108 2,170 2,232

S&

P 5

00

Earn

ing

s Pe

r S

hare

($

)

18

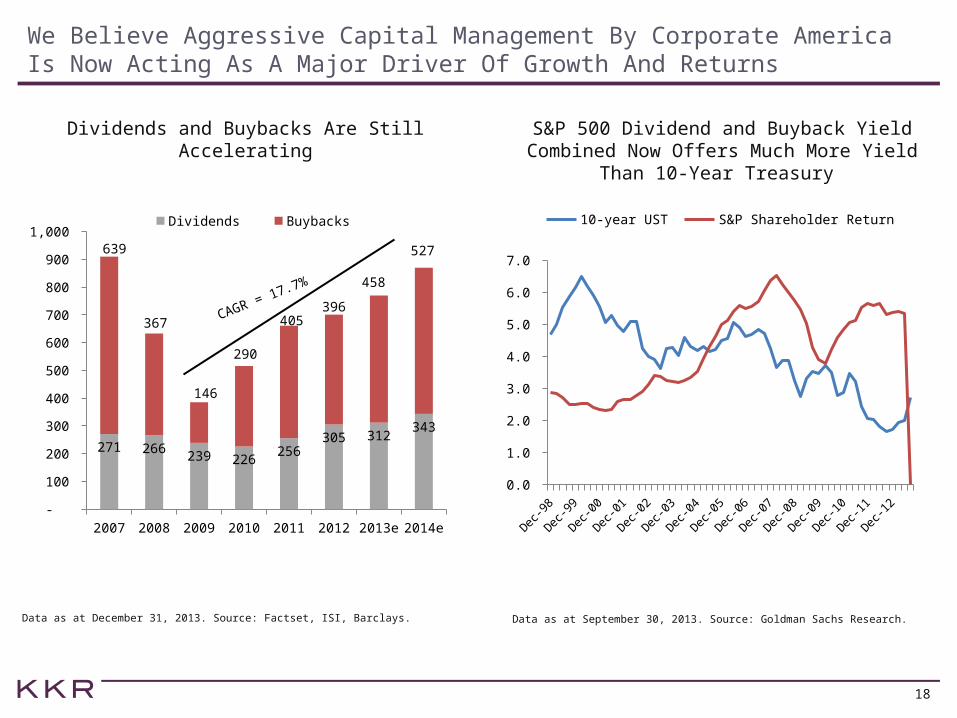

We Believe Aggressive Capital Management By Corporate America Is Now Acting As A Major Driver Of Growth And Returns

Dividends and Buybacks Are Still Accelerating S&P 500 Dividend and Buyback Yield Combined Now Offers Much More Yield Than

10-Year Treasury

Data as at December 31, 2013. Source: Factset, ISI, Barclays. Data as at September 30, 2013. Source: Goldman Sachs Research.

Dec-9

8

Dec-9

9

Dec-0

0

Dec-0

1

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Dec-1

3

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

10-year UST S&P Shareholder Return

2007 2008 2009 2010 2011 2012 2013e 2014e -

100

200

300

400

500

600

700

800

900

1,000

271 266 239 226 256

305 312 343

639

367

146

290

405 396

458

527

Dividends Buybacks

CAGR = 17.7%

IV. Fixed Income

20

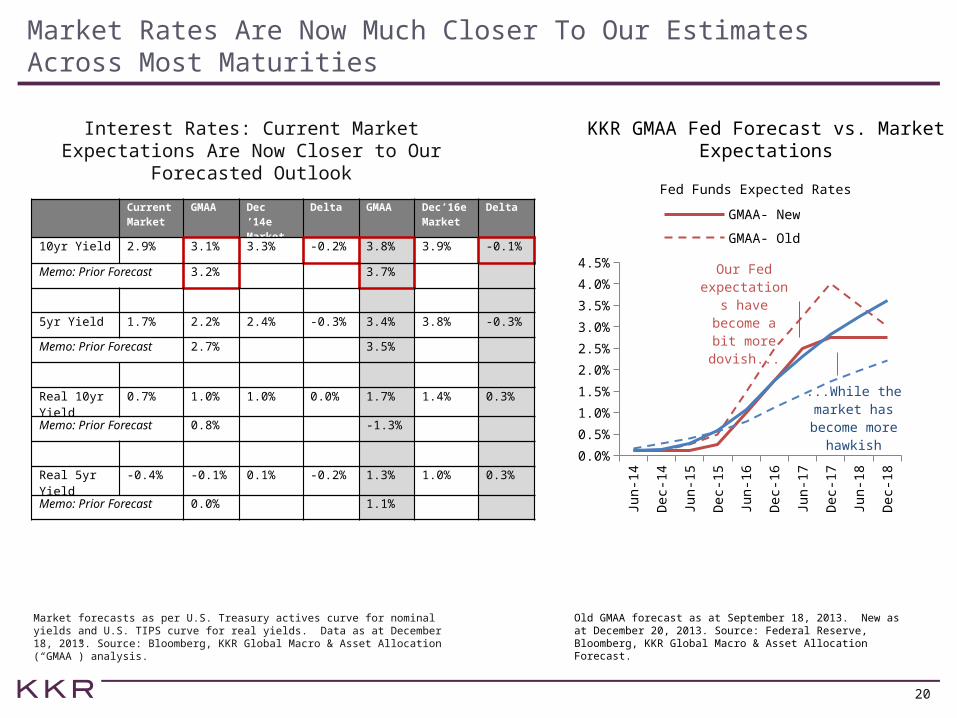

Market Rates Are Now Much Closer To Our Estimates Across Most Maturities

Interest Rates: Current Market Expectations Are Now Closer to Our Forecasted Outlook

Market forecasts as per U.S. Treasury actives curve for nominal yields and U.S. TIPS curve for real yields. Data as at December 18, 2013. Source: Bloomberg, KKR Global Macro & Asset Allocation (“GMAA”) analysis.

Current Market

GMAA Dec’14eMarket

Delta GMAA Dec’16eMarket

Delta

10yr Yield 2.9% 3.1% 3.3% -0.2% 3.8% 3.9% -0.1%

Memo: Prior Forecast 3.2% 3.7%

5yr Yield 1.7% 2.2% 2.4% -0.3% 3.4% 3.8% -0.3%

Memo: Prior Forecast 2.7% 3.5%

Real 10yr Yield

0.7% 1.0% 1.0% 0.0% 1.7% 1.4% 0.3%

Memo: Prior Forecast 0.8% -1.3%

Real 5yr Yield

-0.4% -0.1% 0.1% -0.2% 1.3% 1.0% 0.3%

Memo: Prior Forecast 0.0% 1.1%

KKR GMAA Fed Forecast vs. Market Expectations

Jun-1

4

Dec-

14

Jun-1

5

Dec-

15

Jun-1

6

Dec-

16

Jun-1

7

Dec-

17

Jun-1

8

Dec-

18

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

GMAA- New GMAA- Old

Market-Current Market - 12/31/12

Fed Funds Expected Rates

...While the market has be-

come more hawkish

Our Fed ex-pectations

have become a bit more dovish...

Old GMAA forecast as at September 18, 2013. New as at December 20, 2013. Source: Federal Reserve, Bloomberg, KKR Global Macro & Asset Allocation Forecast.

21

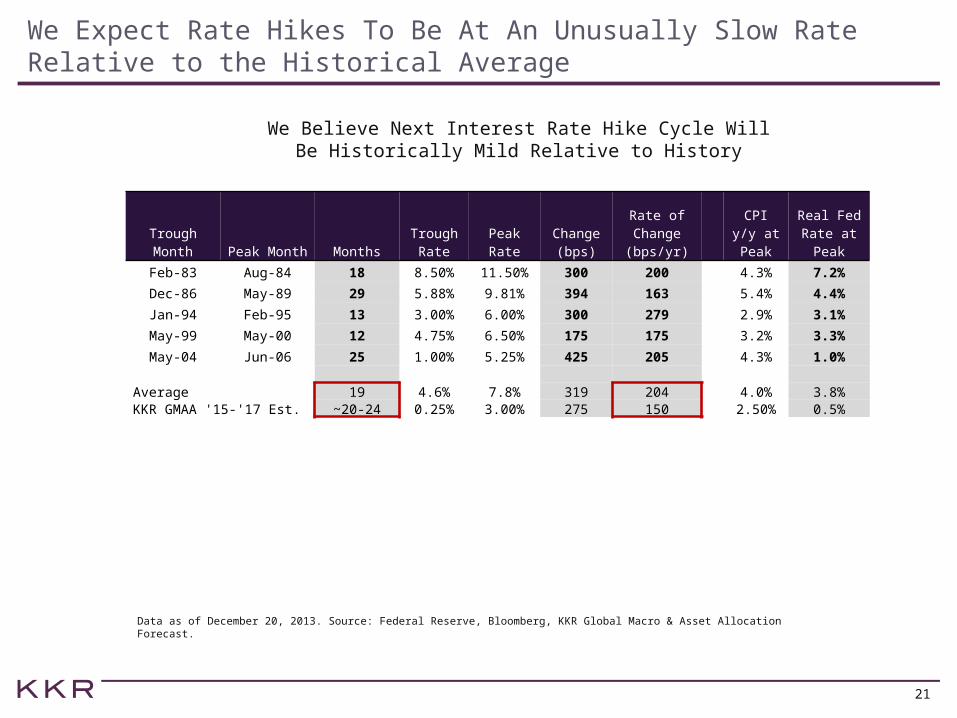

We Expect Rate Hikes To Be At An Unusually Slow Rate Relative to the Historical Average

We Believe Next Interest Rate Hike Cycle Will Be Historically Mild Relative to History

Data as of December 20, 2013. Source: Federal Reserve, Bloomberg, KKR Global Macro & Asset Allocation Forecast.

Trough Month Peak Month Months

Trough Rate

Peak Rate

Change (bps)

Rate of Change (bps/yr)

CPI y/y at Peak

Real Fed Rate at Peak

Feb-83 Aug-84 18 8.50% 11.50% 300 200 4.3% 7.2%

Dec-86 May-89 29 5.88% 9.81% 394 163 5.4% 4.4%

Jan-94 Feb-95 13 3.00% 6.00% 300 279 2.9% 3.1%

May-99 May-00 12 4.75% 6.50% 175 175 3.2% 3.3%

May-04 Jun-06 25 1.00% 5.25% 425 205 4.3% 1.0%

Average 19 4.6% 7.8% 319 204 4.0% 3.8%KKR GMAA '15-'17 Est. ~20-24 0.25% 3.00% 275 150 2.50% 0.5%

22

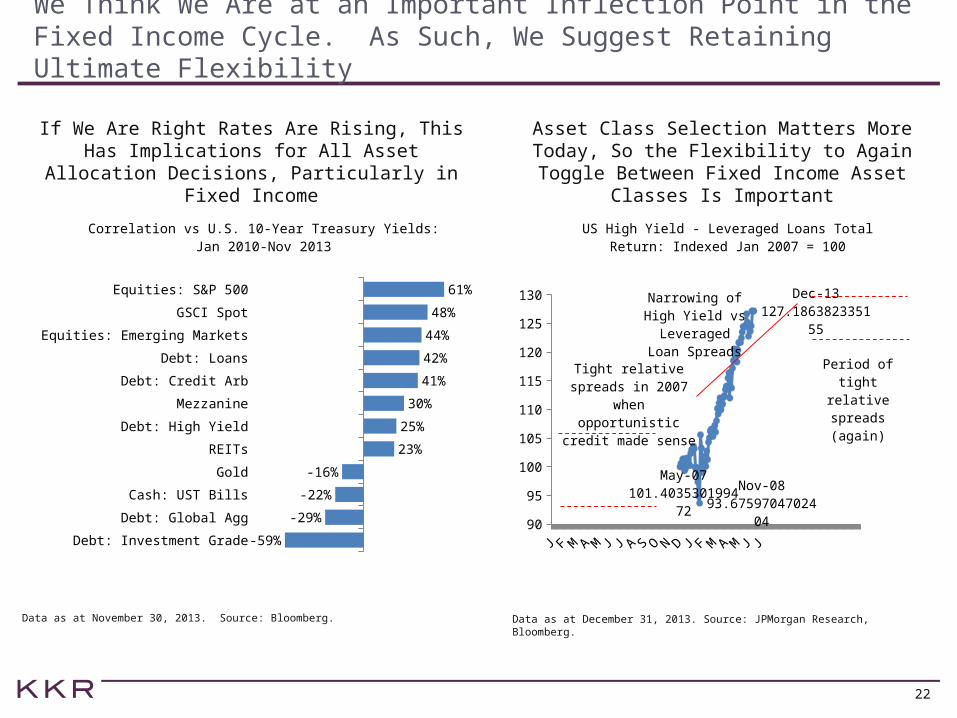

We Think We Are at an Important Inflection Point in the Fixed Income Cycle. As Such, We Suggest Retaining Ultimate Flexibility

If We Are Right Rates Are Rising, This Has Implications for All Asset Allocation Decisions,

Particularly in Fixed Income

Asset Class Selection Matters More Today, So the Flexibility to Again Toggle Between Fixed Income Asset Classes Is Important

Data as at November 30, 2013. Source: Bloomberg. Data as at December 31, 2013. Source: JPMorgan Research, Bloomberg.

Debt: Investment Grade

Debt: Global Agg

Cash: UST Bills

Gold

REITs

Debt: High Yield

Mezzanine

Debt: Credit Arb

Debt: Loans

Equities: Emerging Markets

GSCI Spot

Equities: S&P 500

-59%

-29%

-22%

-16%

23%

25%

30%

41%

42%

44%

48%

61%

Correlation vs U.S. 10-Year Treasury Yields: Jan 2010-Nov 2013

07 08 09 10 11 12 13 1490

95

100

105

110

115

120

125

130

07101.4035301994

7208

93.6759704702404

13127.1863823351

55

US High Yield - Leveraged Loans Total Return: Indexed Jan 2007 = 100

Tight relative spreads in 2007

when opportunistic credit made sense

Narrowing of High Yield vs

Leveraged Loan Spreads

Period of tight relative

spreads (again)

23

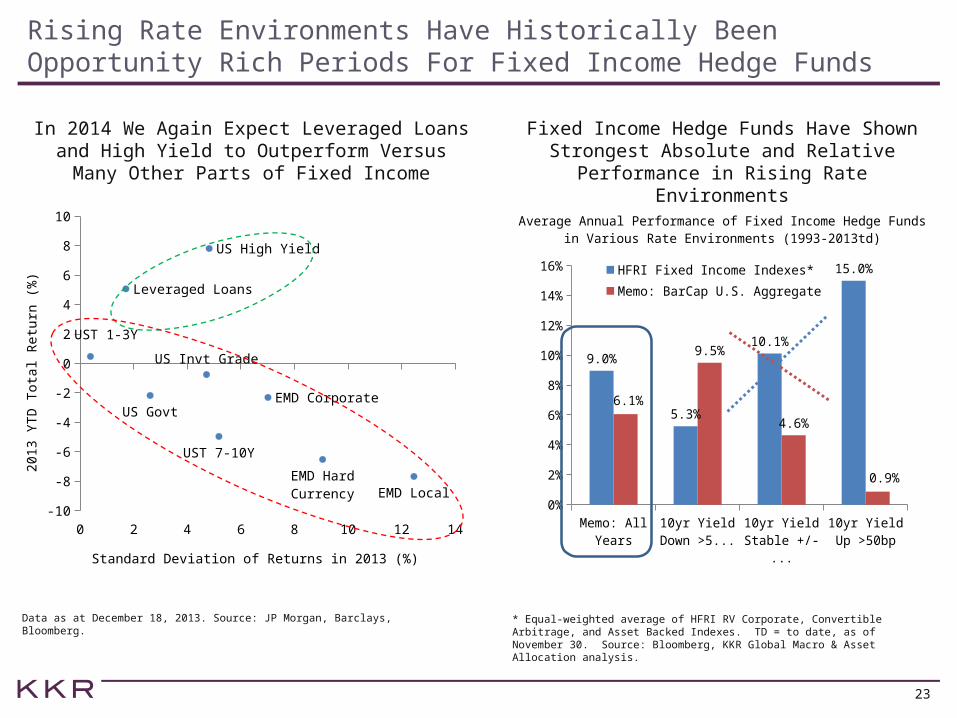

Rising Rate Environments Have Historically Been Opportunity Rich Periods For Fixed Income Hedge Funds

In 2014 We Again Expect Leveraged Loans and High Yield to Outperform Versus Many

Other Parts of Fixed Income

Fixed Income Hedge Funds Have Shown Strongest Absolute and Relative

Performance in Rising Rate Environments

Data as at December 18, 2013. Source: JP Morgan, Barclays, Bloomberg. * Equal-weighted average of HFRI RV Corporate, Convertible Arbitrage, and Asset Backed Indexes. TD = to date, as of November 30. Source: Bloomberg, KKR Global Macro & Asset Allocation analysis.

0 2 4 6 8 10 12 14-10

-8

-6

-4

-2

0

2

4

6

8

10

US High Yield

Leveraged Loans

UST 1-3Y

US Invt Grade

US GovtEMD Corporate

UST 7-10Y

EMD Hard Cur-rency EMD Local

Standard Deviation of Returns in 2013 (%)

2013 Y

TD

Tota

l R

etu

rn (

%)

Memo: All Years

10yr Yield Down >50

bp

10yr Yield Stable +/-

50bp

10yr Yield Up >50bp

0%

2%

4%

6%

8%

10%

12%

14%

16%

9.0%

5.3%

10.1%

15.0%

6.1%

9.5%

4.6%

0.9%

HFRI Fixed Income Indexes*

Memo: BarCap U.S. Aggregate

Average Annual Performance of Fixed Income Hedge Fundsin Various Rate Environments (1993-2013td)

V. Real Assets

25

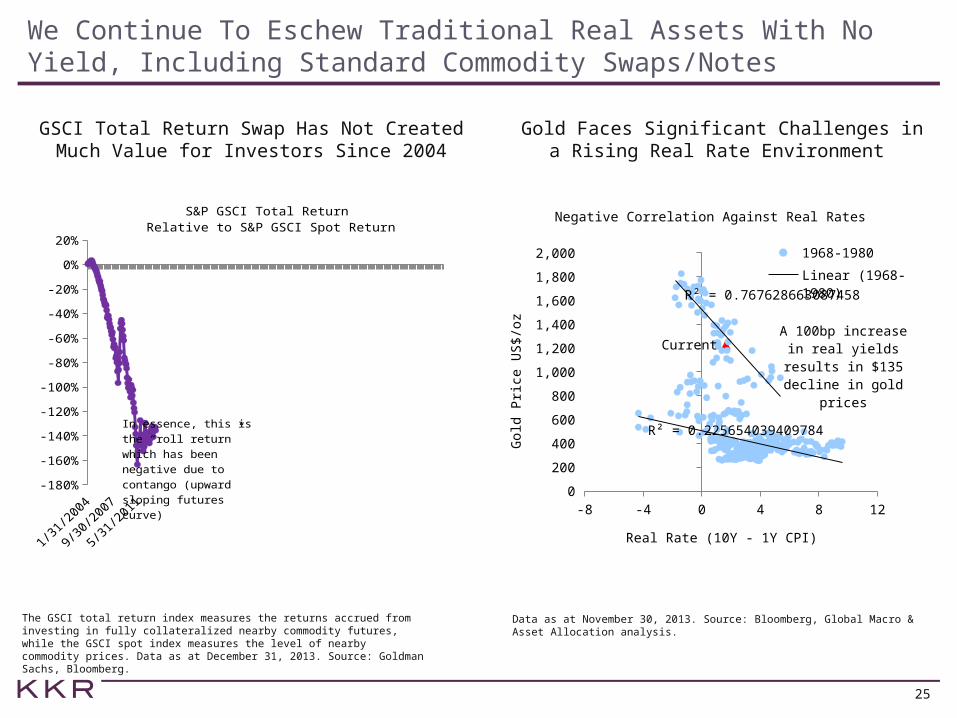

We Continue To Eschew Traditional Real Assets With No Yield, Including Standard Commodity Swaps/Notes

GSCI Total Return Swap Has Not Created Much Value for Investors Since 2004

Gold Faces Significant Challenges in a Rising Real Rate Environment

The GSCI total return index measures the returns accrued from investing in fully collateralized nearby commodity futures, while the GSCI spot index measures the level of nearby commodity prices. Data as at December 31, 2013. Source: Goldman Sachs, Bloomberg.

Data as at November 30, 2013. Source: Bloomberg, Global Macro & Asset Allocation analysis.

-8 -4 0 4 8 120

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Current

R² = 0.767628663087458

R² = 0.225654039409785

Negative Correlation Against Real Rates

1968-1980Linear (1968-1980)1980-2009

Real Rate (10Y - 1Y CPI)G

old

Pri

ce U

S$/o

z A 100bp increase in real yields results in $135 decline in

gold prices

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013-180%

-160%

-140%

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

S&P GSCI Total Return Relative to S&P GSCI Spot Return

In essence, this is the “roll return” which has been negative due to contango (upward slop-ing futures curve)

26

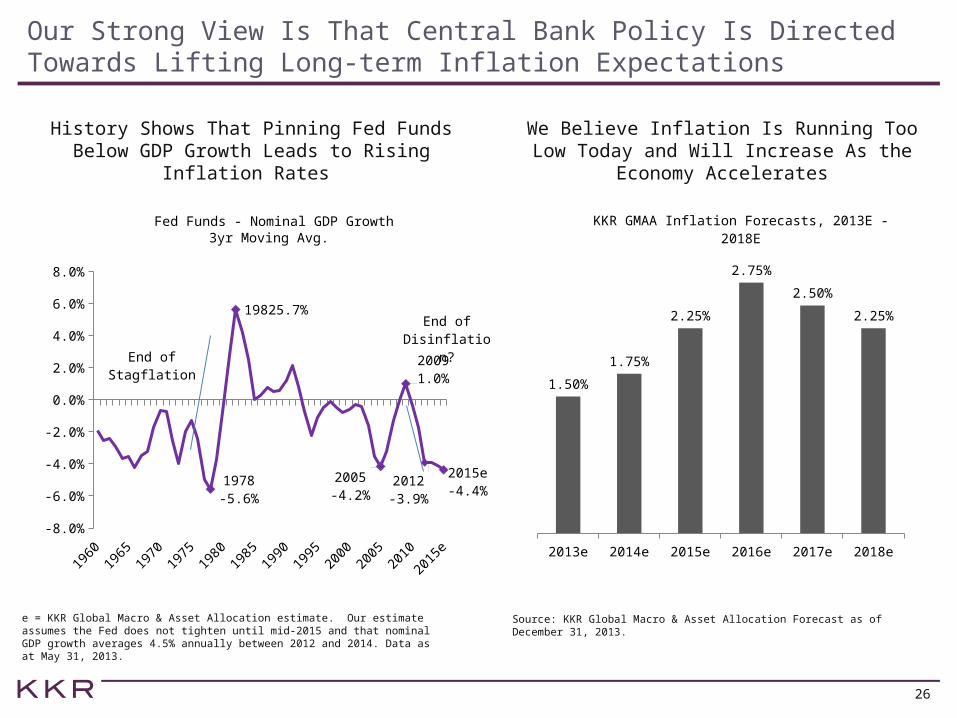

Our Strong View Is That Central Bank Policy Is Directed Towards Lifting Long-term Inflation Expectations

History Shows That Pinning Fed Funds Below GDP Growth Leads to Rising Inflation Rates

We Believe Inflation Is Running Too Low Today and Will Increase As the Economy

Accelerates

e = KKR Global Macro & Asset Allocation estimate. Our estimate assumes the Fed does not tighten until mid-2015 and that nominal GDP growth averages 4.5% annually between 2012 and 2014. Data as at May 31, 2013.

Source: KKR Global Macro & Asset Allocation Forecast as of December 31, 2013.

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

1978-5.6%

19825.7%

2005-4.2%

20091.0%

2012-3.9%

2015e-4.4%

3yr Moving Avg.Fed Funds - Nominal GDP Growth

End of Stagflation

End ofDisinflation?

2013e 2014e 2015e 2016e 2017e 2018e

1.50%

1.75%

2.25%

2.75%

2.50%

2.25%

KKR GMAA Inflation Forecasts, 2013E - 2018E

VI. Alternatives

28

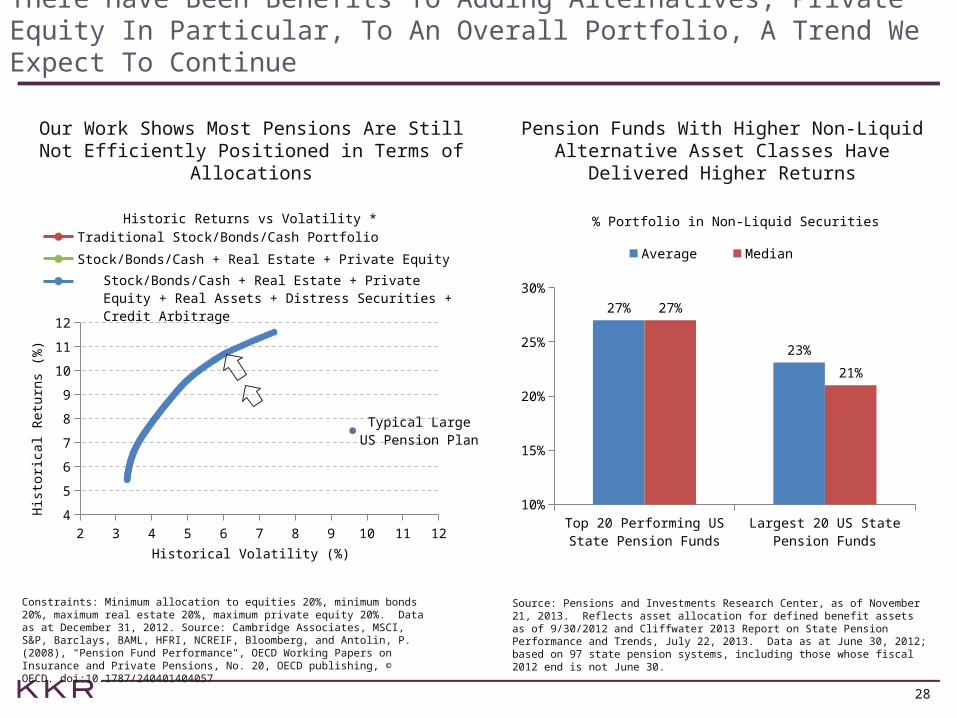

There Have Been Benefits To Adding Alternatives, Private Equity In Particular, To An Overall Portfolio, A Trend We Expect To Continue

Our Work Shows Most Pensions Are Still Not Efficiently Positioned in Terms of Allocations

Pension Funds With Higher Non-Liquid Alternative Asset Classes Have Delivered

Higher Returns

Constraints: Minimum allocation to equities 20%, minimum bonds 20%, maximum real estate 20%, maximum private equity 20%. Data as at December 31, 2012. Source: Cambridge Associates, MSCI, S&P, Barclays, BAML, HFRI, NCREIF, Bloomberg, and Antolin, P. (2008), "Pension Fund Performance", OECD Working Papers on Insurance and Private Pensions, No. 20, OECD publishing, © OECD. doi:10.1787/240401404057

Source: Pensions and Investments Research Center, as of November 21, 2013. Reflects asset allocation for defined benefit assets as of 9/30/2012 and Cliffwater 2013 Report on State Pension Performance and Trends, July 22, 2013. Data as at June 30, 2012; based on 97 state pension systems, including those whose fiscal 2012 end is not June 30.

2 3 4 5 6 7 8 9 10 11 124

5

6

7

8

9

10

11

12

Typical Large US Pension Plan

Historic Returns vs Volatility *

Traditional Stock/Bonds/Cash Portfolio

Stock/Bonds/Cash + Real Estate + Private Equity

Historical Volatility (%)

His

tori

cal R

etu

rns

(%)

Stock/Bonds/Cash + Real Estate + Private Equity + Real Assets + Distress Securities + Credit Arbitrage

Top 20 Performing US State Pension Funds

Largest 20 US State Pension Funds

10%

15%

20%

25%

30%

27%

23%

27%

21%

% Portfolio in Non-Liquid Securities

Average Median

29

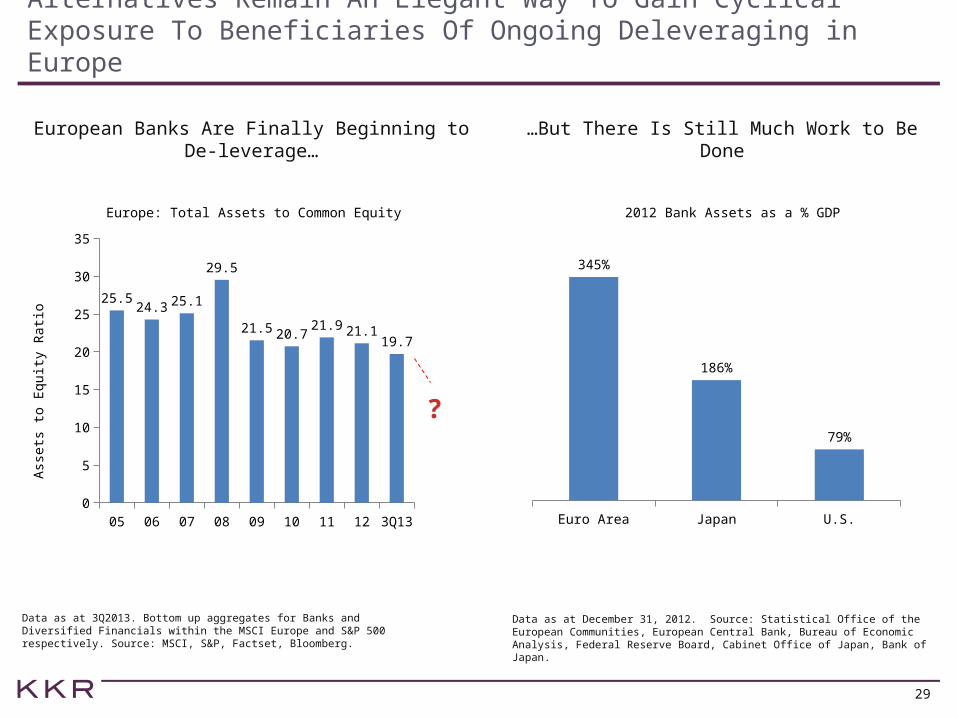

Alternatives Remain An Elegant Way To Gain Cyclical Exposure To Beneficiaries Of Ongoing Deleveraging in Europe

European Banks Are Finally Beginning to De-leverage…

…But There Is Still Much Work to Be Done

Data as at 3Q2013. Bottom up aggregates for Banks and Diversified Financials within the MSCI Europe and S&P 500 respectively. Source: MSCI, S&P, Factset, Bloomberg.

Data as at December 31, 2012. Source: Statistical Office of the European Communities, European Central Bank, Bureau of Economic Analysis, Federal Reserve Board, Cabinet Office of Japan, Bank of Japan.

05 06 07 08 09 10 11 12 3Q13

0

5

10

15

20

25

30

35

25.524.3 25.1

29.5

21.5 20.721.9 21.1

19.7

Europe: Total Assets to Common Equity

Ass

ets

to E

quit

y R

ati

o

?

Euro Area Japan U.S.

345%

186%

79%

2012 Bank Assets as a % GDP

VI. Currencies

31

In The Currency Arena, We Believe Pressure On Fiscal And Current Deficits Makes Currencies A Logical “Release Valve”

We Think a Dollar Bull Market Has Begun Within Latin America, We Think Mexico is More Attractive than Brazil

Data as at December 4, 2013. Source: Bloomberg. Data as at December 31, 2013. Source: Bloomberg.

01234567891011121314151617181920212223242526272829303132333435363738394041424344454647484950515253545556575859606162636465666768697071727374757677787980

100

110

120

130

140

150

160

US Trade Weighted Major Dollar: Trough to Peak: Indexed: Trough=100

10/31/1978 (77m)

4/30/1995 (82m)

8/31/2011 (28m to-date)

Jan-1

0

May-1

0

Sep-1

0

Jan-1

1

May-1

1

Sep-1

1

Jan-1

2

May-1

2

Sep-1

2

Jan-1

3

May-1

3

Sep-1

3

0.12

0.13

0.14

0.15

0.16

0.17

0.18

0.19

0.20

Mexican Peso/Brazilian Real

VII. Asset Allocation Summary/Q&A

33

Outlook 2014: “Stay the Course” As a Global Recovery Unfolds

What Does “Stay the Course” Mean?

1. Retain key overweight positions in global equities and alternatives, including private credit, special situations and real assets.

2. To fund these risk buckets, we continue to target a massive underweight to government bonds and investment grade debt.

3. However, 2014 will not be a repeat of 2013. In particular, we believe 1) the “drag” from government austerity should decline in 2014; 2) equity trading multiples for stocks are now ahead of schedule.

34

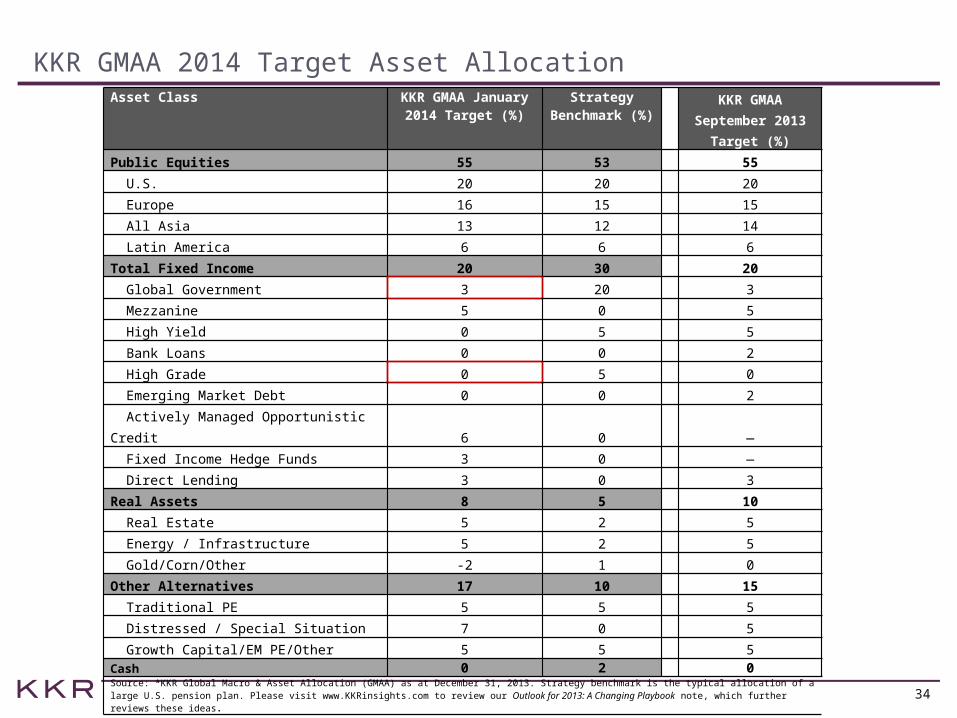

KKR GMAA 2014 Target Asset AllocationAsset Class KKR GMAA January

2014 Target (%)Strategy

Benchmark (%)

KKR GMAA September 2013

Target (%)

Public Equities 55 53 55

U.S. 20 20 20

Europe 16 15 15

All Asia 13 12 14

Latin America 6 6 6

Total Fixed Income 20 30 20

Global Government 3 20 3

Mezzanine 5 0 5

High Yield 0 5 5

Bank Loans 0 0 2

High Grade 0 5 0

Emerging Market Debt 0 0 2

Actively Managed Opportunistic Credit 6 0 ―

Fixed Income Hedge Funds 3 0 ―

Direct Lending 3 0 3

Real Assets 8 5 10

Real Estate 5 2 5

Energy / Infrastructure 5 2 5

Gold/Corn/Other -2 1 0

Other Alternatives 17 10 15

Traditional PE 5 5 5

Distressed / Special Situation 7 0 5

Growth Capital/EM PE/Other 5 5 5Cash 0 2 0Source: *KKR Global Macro & Asset Allocation (GMAA) as at December 31, 2013. Strategy benchmark is the typical allocation of a large U.S. pension plan. Please visit www.KKRinsights.com to review our Outlook for 2013: A Changing Playbook note, which further reviews these ideas.