Embed Size (px)

Citation preview

OurNorco

Annual Report 2017100% FARMER OWNEDAN AUSTRALIAN FARMER OWNED DAIRY CO-OPERATIVE

www.norco.com.au

CONTENTS Corporate Profile 2

Facts at a Glance 3

Chairman’s Report 4

Norco Foods - Sales and Marketing 10

Norco Foods - Operations 12

Milk Supply 14

Norco Rural / Agribusiness 15

Financial Management 17

Norco People 18

Directors’ Report 20

Auditor’s Independence Declaration 27

Corporate Governance Statement 29

Financial Statements 34

Independent Auditor’s Report 58

Corporate and Branch Directories 64

Thank you to our Norco employees, Co-operative members, Norco Milk distributors and customers who feature in the annual report photography. Your time and participation is greatly appreciated.

1

Our Purpose

Our Values

Norco’s purpose is to build wealth, security and sustainability for our shareholders, business partners and employees.

We achieve this by:

• maintaining a diverse and strong range of businesses;

• being a competitive regional purchaser and supplier of milk; and

• creating integrated solutions for our partners.

Norco applies a common set of values to everything it does. These values include:

Respect

• We respect our shareholders, employees, business partners and customers.

• We respect a diversity of views and opinions.

• We encourage and support people to grow as individuals and contributors to our organisation.

• We respect our heritage and legacy.

• We respect our natural environment.

Responsible

• We are responsible for preserving the co-operative principles.

• We are responsible for our actions and our performance.

• We are responsible for providing a safe work environment.

Efficient

• We seek to add value in everything we do.

Innovation

• We seek to consistently improve through innovation.

Community

• We seek active involvement in our communities.

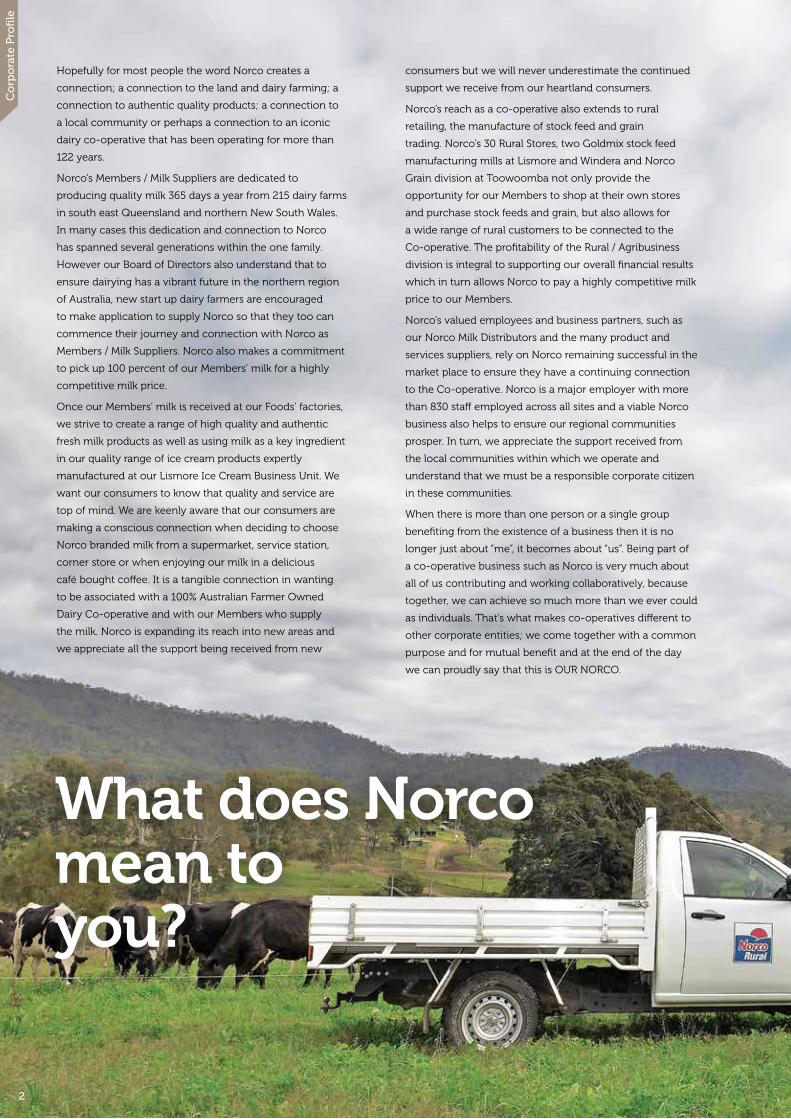

What does Norco mean toyou?

Hopefully for most people the word Norco creates a

connection; a connection to the land and dairy farming; a

connection to authentic quality products; a connection to

a local community or perhaps a connection to an iconic

dairy co-operative that has been operating for more than

122 years.

Norco’s Members / Milk Suppliers are dedicated to

producing quality milk 365 days a year from 215 dairy farms

in south east Queensland and northern New South Wales.

In many cases this dedication and connection to Norco

has spanned several generations within the one family.

However our Board of Directors also understand that to

ensure dairying has a vibrant future in the northern region

of Australia, new start up dairy farmers are encouraged

to make application to supply Norco so that they too can

commence their journey and connection with Norco as

Members / Milk Suppliers. Norco also makes a commitment

to pick up 100 percent of our Members’ milk for a highly

competitive milk price.

Once our Members’ milk is received at our Foods’ factories,

we strive to create a range of high quality and authentic

fresh milk products as well as using milk as a key ingredient

in our quality range of ice cream products expertly

manufactured at our Lismore Ice Cream Business Unit. We

want our consumers to know that quality and service are

top of mind. We are keenly aware that our consumers are

making a conscious connection when deciding to choose

Norco branded milk from a supermarket, service station,

corner store or when enjoying our milk in a delicious

café bought coffee. It is a tangible connection in wanting

to be associated with a 100% Australian Farmer Owned

Dairy Co-operative and with our Members who supply

the milk. Norco is expanding its reach into new areas and

we appreciate all the support being received from new

consumers but we will never underestimate the continued

support we receive from our heartland consumers.

Norco’s reach as a co-operative also extends to rural

retailing, the manufacture of stock feed and grain

trading. Norco’s 30 Rural Stores, two Goldmix stock feed

manufacturing mills at Lismore and Windera and Norco

Grain division at Toowoomba not only provide the

opportunity for our Members to shop at their own stores

and purchase stock feeds and grain, but also allows for

a wide range of rural customers to be connected to the

Co-operative. The profitability of the Rural / Agribusiness

division is integral to supporting our overall financial results

which in turn allows Norco to pay a highly competitive milk

price to our Members.

Norco’s valued employees and business partners, such as

our Norco Milk Distributors and the many product and

services suppliers, rely on Norco remaining successful in the

market place to ensure they have a continuing connection

to the Co-operative. Norco is a major employer with more

than 830 staff employed across all sites and a viable Norco

business also helps to ensure our regional communities

prosper. In turn, we appreciate the support received from

the local communities within which we operate and

understand that we must be a responsible corporate citizen

in these communities.

When there is more than one person or a single group

benefiting from the existence of a business then it is no

longer just about “me”, it becomes about “us”. Being part of

a co-operative business such as Norco is very much about

all of us contributing and working collaboratively, because

together, we can achieve so much more than we ever could

as individuals. That’s what makes co-operatives different to

other corporate entities; we come together with a common

purpose and for mutual benefit and at the end of the day

we can proudly say that this is OUR NORCO.

Co

rpo

rate

Pro

file

2

3

Facts at a Glan

ce

2015/16 2.0M 2014/15 3.1M

2013/14 0.5M 2012/13 0.4M

includes permanent, part-time and casual staff

norco foods 604

norco rural 173

norco agribusiness 38

corporate 22

2015/16 1,016 2014/15 968 2013/14 933 2012/13 947

FINANCIALYEAR

AVE BASE MILK PRICE

STEP UPS

AVE TOTAL MILK PAY

DIVIDEND SUPPLIERS’ PATRONAGE

TOTAL AVE MEMBER RETURNS

Total Member Returns Total Member Supply CENTS / L

2016/17 57.29 0.13 57.42 0.25* 0.51 58.182015/16 57.30 - 57.30 0.24 0.52 58.062014/15 56.48 - 56.48 0.22 0.52 57.222013/14 53.25 - 53.25 0.14 0.51 53.902012/13 51.50 0.24 51.74 - 0.45 52.19

Total Member Returns Northern Region five (5) yr contract price

2016/17 57.40 0.13 57.53 0.25* 0.51 58.292015/16 57.28 - 57.28 0.24 0.52 58.04

Total Member Returns Southern Region five (5) yr contract price

2016/17 56.34 0.13 56.47 0.25* 0.51 57.232015/16 57.52 - 57.52 0.24 0.52 58.28

*Dividend proposed for consideration at 2017 Annual General Meeting

1.1

837

1,03316/17 totalnet profit

as at 30 june 17

thousand litres16/17 averagemillion

staff

milk production

215farms16/17 member

2015/16 218 2014/15 218

2013/14 181 2012/13 159

222milk intake

million litres16/17 total members’

2015/16 222 2014/15 211 2013/14 163 2012/13 151

Our unique proposition in the market place continues to resonate with a growing consumer base

Business Overview 2016/17

The dairy industry has faced many challenges during

the 2016/17 financial year as well as there being a

significant amount of change in the market place

within which Norco operates. However, we have been

able to retain our total average farm gate milk price for

our Northern Region supply as well as maintain the

previously communicated position for our Southern

Region milk supply. Additionally, we have met all

required banking covenants, exceeded our collective

budgeted net profit and achieved all other financial

KPI’s. This is an excellent result taking into account the

volatile trading conditions in the market place. This

achievement is a reflection of our market positioning

as the true 100% Australian Farmer Owned Dairy Co-

operative producing quality, innovative products and

the hard work of all our people in the Co–operative. The

support shown by our valued customers for our Co-

operative and Member farms has ensured the continued

growth of the Norco brand.

The final result for 2016/17 has enabled us to continue

to build our brand in terms of market share and growing

a national footprint, as well as developing our brand

for export opportunities. The flow on effects from the

turmoil experienced in the southern regions of Australia

continue to challenge the dairy industry, however

Norco is absolutely focused on consistently showing

that a farmer owned co-operative model with solid

strategy, direction, management and performance can

continue to prosper. Our heritage as a 122 year old

100% Australian Farmer Owned Dairy Co-operative

has allowed us to strategically position our brand and

further enhance the point of difference and competitive

edge that we have compared to other processors. Our

diversified business model, geographical positioning,

quality of product and strong long term relationships

have again been significant drivers in achieving these

financial results.

We are the only true 100% Australian Farmer Owned

Dairy Co–operative competing in a market of

multinational owned processors.

We have collectively finished the 2016/17 financial year

4

Ch

airm

an’s

Rep

ort

We are the only true 100% Australian Farmer Owned Dairy Co–operative competing in a market of multinational owned processors

at an EBITDA (Earnings before Interest, Tax, Depreciation

and Amortisation) level of $8.859 million which is a net

profit result of $1.122 million. This is a good result taking

into account the volatile market due to issues in the

southern dairy regions of Australia. Our total core debt

as at 30 June 2017 reduced to $28.3 million due to $1.65

million being paid back to St George during the financial

year. We will continue to further invest in our plant

and equipment as well as our people as we grow our

business. Our collective sales for our Co-operative have

grown 2.7 percent to $555.6 million this year.

Our Norco Foods business division, consisting of the

Ice Cream Business Unit, Norco Milk and Milk Supply,

achieved an EBITDA (Earnings before Interest, Tax,

Depreciation and Amortisation) of $7.3 million. This is

a good result considering the ongoing market pricing

pressures being faced by Norco. Milk Supply improved

on last year, after taking into account the Retrospective

Milk Pay Step-Up payment paid to our Members, higher

milk component results achieved by our Members and

the large spring flush volume. Norco Milk’s sales were

up 8.9 percent on last year predominantly due to the

support shown by both Coles and Woolworths for Norco

branded milk, Route Trade business improvements

including Sydney and the continuous growth in branded

sales. The Norco branded sales volume increased 34.6

percent and the REAL volume increased 28.4 percent.

ICBU sales were down by 6.0 percent on last year’s

result which was driven by seasonality in terms of a late

summer and strong, ongoing discounting by branded

competitors.

Our Rural/Agri business division again had a strong

result in 2016/17 with a collective EBITDA result that

was up on last year by 24.4 percent after the Suppliers’

Patronage Scheme payments (Agri up by 18.7 percent /

Rural up 18.9 percent).This was driven by better trading

results achieved from our Rural Stores, our Lismore and

Windera Mills and also by the Grain Trading business.

The Rural Retail sales achieved a record level of $129.8

million. The Rural team continue to focus on operational

efficiencies, improved buying, customer service and

gross margins as well as ongoing planning of the

expansion of the Rural network over future years. The

Suppliers’ Patronage Scheme, being the rewards paid

5

6

out to our Members for shopping with Norco, totalled

$1.131 million versus the prior year’s $1.156 million.

The number of Member farms that purchased from the

business increased from 92 percent to 93 percent in

2016/17.

Corporate costs were under budget and as a percentage

of total sales finished the year at 0.9 percent of sales

versus the prior year’s 0.8 percent. This is an good result

considering the increased size of our overall business,

now with a collective turnover of more than $555

million. Corporate continues to manage and implement

tight cost and overheads control. This is reflected

in consistently being below the industry standard

spend level for a company of our turnover size. As we

consolidate our financial position and implement long

term opportunities we will continue to put further focus

on the development of our people, their skill sets and

succession planning.

Our Human Resources (HR) team continues to build

further training and development platforms for all our

teams in respect of best practices in Work Place Health

and Safety (WPHS) as well as individual professional

development programs. We again have seen great

improvement in all aspects of WPHS in the Co

operative’s business units.

Again this year there are a number of accomplishments

from all the teams at Norco. I have listed below some of

the key achievements from the 2016/17 financial year.

• Coles extended term contract for ten years signed.

• Improved Route Trade business sales up by 12.4

percent on previous year.

• Net profit of $1.122 million, budget exceeded.

• Collective Co-operative sales increase of 2.7 percent.

• Our total average milk price to our Members was

0.12 cents per litre (cpl) up on last year and achieved

57.42 cpl.

• The Rural/Agri business division achieved a net

profit improvement of 29.7 percent up on last year,

after patronage.

• Core debt reduction by $1.65 million to $28.3

million.

• Met all banking covenants and secured new banking

arrangements with Rabobank.

• Suppliers’ Patronage Scheme $1.131 million paid out.

• Norco Milk sales up 8.9 percent on last year. Norco

branded volume up 34.6 percent and REAL volume

up 28.4 percent.

• Cafe/Coffee project - two contracts signed with

Coffee brands.

• WPHS claims costs companywide improved by 30

percent on last year.

Our 2017/18 key points of focus are:

• Corporate:

- To continue to focus on cost controls and

efficiencies relating to all overheads.

- IT and systems development to meet business

growth requirements.

- People, professional development and succession

planning.

- To manage and meet all banking covenants.

• Rural/Agri Division:

- Continued focus on ongoing financial improvement

and market share growth of the Rural / Agri division.

- Explore further opportunities for expansion of the

Rural network.

- Improved Rural Stores buying, improve Rural Store

network sales, service and market share.

- Ongoing quality assurance.

- Increase volumes through Agribusiness mills.

- Further capital reinvestment as required in Stores

and Mills.

- Training and development of our sales people.

- Focus on training, reinvestment and upgrades in all

aspects of WPHS best practice at our sites.

• Foods’ Division:

- Capital upgrade at ICBU to take material costs out of

the business by 2019/20.

- Focus on Norco branded product market share and

point of difference.

- Quality assurance processes, systems and training

improvements.

- Ongoing development of strategic alliances with

Norco partners.

- Consistent milk volume pre-selling.

- Continued growth and development of our ice

cream business.

7

- Improvement of milk price at farm gate.

- Ongoing research and development of future export

opportunities.

- Continued market share growth and improvement

of profitability in the Route Trade.

- Continued development and growth in the Cafe/

Coffee market.

- Capital improvements on all Norco owned sites for

business development.

- Training and development of our teams.

• Human Resources:

- Focus on WPHS best practice across all business

units.

- Training and professional development

requirements for our teams.

- Succession planning.

- Improved communication processes and clear

strategic directional focus for all our business units.

• Focus of Senior Management Team:

- Improve core businesses’ profitability.

- Ongoing development of core strategic partnerships

across all business units.

- Continued improvement of asset values and

goodwill appreciation of the Co-operative.

- Competitive farm gate milk price and improved

shareholder return through ongoing profit

improvement across all divisions.

- Improve Member / Milk Supplier customer service,

support and communication.

- Achieve/exceed Key Performance Indicators and

budget.

- Strengthening positioning and ongoing

sustainability of the Co-operative.

- Ongoing focus on employee training, development,

mentoring and career/succession planning across

business units.

- Continued investment and improvement in all

aspects of WPHS.

- Focus on long term strategic plans.

- The continuation of the $0.0025 cpl Compulsory

Share Acquisition Scheme. The primary objective of

this scheme continues to be the timely repayment

of Dry Member capital and it is also pleasing to

report that we currently have an excess amount of

$435,000 contributed as at 30 June 2017 which can

be used for the secondary purpose of the scheme,

being to contribute to the funding of capital

projects.

Strategy

The Board continues to work with the management

team on growing our geographic footprint beyond

our traditional areas in the Norco Foods business. The

benefits of this strategy are far reaching; notably the

efficiencies created in our manufacturing facilities

and opportunities for our Members to grow their milk

supply under stable milk prices which in turn creates a

sustainable Co-operative and Member base. Our unique

proposition in the market place as a true Co-operative

owned by Australian farmers continues to resonate with

a growing consumer base.

However, provenance alone will not guarantee Norco’s

future sustainability and growth. The Co-operative

continues to maintain a strategy of having a diverse

business model that helps to safeguard both the overall

business profitability and also Member profitability.

In this regard, Rural Retail / Agri plays a key role in

supporting this strategy with its improved profit

contribution year on year over recent years. Rural /

Agri also values the support shown by the Member

farms when purchasing from this division through the

payment of loyalty rewards in the form of the Suppliers’

Patronage Scheme.

The Board is committed to pursuing a growth strategy

for the export of fresh milk and ice cream to Asia.

Progress is slow but we are committed to developing

relationships with customers that are long lasting.

Growth in the export portfolio has the potential to

reduce the Co-operative’s reliance on the Australian

retail market.

The crisis that has unfolded in Victoria over the last

18 months is a sombre reminder of the fragility of the

Australian dairy industry and although the picture is not

clear of what may occur into the future, it adds little to

speculate when our thoughts need to be with the dairy

farmers, employees, stakeholders and communities that

are reliant on a strong dairy industry in their region. As

a co-operative, what we can and must do is to learn

from these events, ensuring that our internal processes

are robust and that we communicate well and our

88

Members feel included. There is every reason to believe

that a well run and supportive co-operative can lead

the industry in milk pricing and contribute to the overall

future wellbeing of the dairy industry for all stakeholders

involved.

Board and management changes

As a result of the changes to Norco’s Rules which

became effective on 1 July 2014, the retiring Director for

the Northern Region, Mr AW (Tony) Wilson, whose dairy

farm interest is located in the Kyogle Local Government

Area of NSW, was no longer eligible to serve as a

Supplier Director for the Northern Region once his three

year term concluded and so could not offer himself for

re-election and accordingly retired at the 2016 Annual

General Meeting. Additionally, as reported last year, it

was determined that the casual vacancy created in the

Southern Region as a result of Mr PW Neal’s resignation

on 23 November 2015 would be filled as part of the 2016

ordinary election of Directors programme, as Mr Neal

was due to retire at the 2016 Annual General Meeting.

This allowed the opportunity for two new Directors

to be elected to the Board and after keenly contested

ballots, Mrs Elke Watson was elected as a supplier

Director in the Northern Region and Mr Greg Billing was

elected as a supplier Director in the Southern Region.

Mr Brett Kelly has resigned his role as Chief Executive

Officer (CEO) with effect from 29 September 2017. Brett

held the CEO position for more than nine years and

was instrumental in creating the Coles contract and

subsequent major capital projects that would allow

Norco to meet its contractual obligations to Coles. Brett

also drove the expansion of the Norco brand into China

which assisted in Norco’s brand growth domestically.

Brett doubled the size of the business in his time at

Norco and I would like to acknowledge and thank Brett

for his contribution.

Board and Member educational training

The Board continues to adhere to its established policy

9

requiring new Directors to undertake the Australian

Institute of Company Directors’ (AICD) Company

Directors’ Course within 12 months of commencing

their role. In this regard it is pleasing to report that both

Mr Greg Billing and Mrs Elke Watson completed the

Company Directors’ Course in June 2017. In addition,

all Directors are encouraged to participate in industry

events / workshops and educational programmes that

assist in Directors’ professional development.

Over the last 12 months the management team, in

consultation with the Board, conducted a media training

session for Members so that valuable skills could be

learnt in dealing with the media. Through the Member

Services Committee, the Board also continues to

support Members having the opportunity to participate

in international study tours. Our commitment to

educating our Members, employees and Directors is

absolutely critical to the future success of Norco as we

must expose ourselves to new and innovative ways of

doing business.

In conclusion, I would like to thank all Members / Milk

Suppliers, employees, stakeholders, customers and my

fellow Directors for your support, input and loyalty to

the Co-operative throughout the 2016/17 financial year.

I look forward to working with you all again to continue

to strengthen and improve the long term sustainability

of Norco in the 2017/18 financial year.

GREG McNAMARA

Chairman

Board of Directors

10

2016/17 proved to be another successful year for Norco Foods

across many facets of our sales and marketing activities as we

continue to build consumer support for Norco and our brands.

One of the many highlights for our team this year was winning

the 2017 Canstar Blue award for most satisfied customers.

Norco fresh milk achieved a 5 star rating for overall satisfaction,

the highest score possible, which is great recognition that our

consumers value high quality milk products. This quality was

further recognised with our REAL Iced Chocolate milk winning

the best flavoured milk in Australia at the Australian Grand Dairy

Awards for a second year in a row. We are extremely proud

that our Co-operative is being recognised as one of the best,

competing against all other dairy processors in the nation.

We may be a relatively small player in the national market,

however we have gained market share this year and we have

further growth aspirations. Our 100% Australian Farmer Owned

Dairy Co-operative point of difference provides a unique

proposition for existing and potential customers which is

assisting us greatly with our marketing message, our extended

geographic distribution reach, and with our award winning

products. As a result, the Norco branded milk volume grew 34.6

percent and the REAL volume 28.4 percent during 2016/17.

Our Board encouraged management to invest and strengthen

our marketing approach this year by employing Mr Ben Menzies

into the dedicated role of Norco Foods Marketing Manager.

Targeting consumers through a number of exciting strategies

including on-line marketing initiatives, Ben and his team have

developed a number of marketing activities that highlight our

Co-operative ethos, our dairy farmer Members, our quality

product offerings, the key selling story and our points of

difference, all of which make Norco uniquely stand out from the

rest of the industry.

Further incremental investment has been provided

during 2016/17 with the roll out of an external third party

merchandising team to service the grocery channel. This

investment allowed for each and every Coles and Woolworths

store that carries Norco branded products to receive a weekly

visit from a dedicated team member that assisted in ensuring

that we had our products available on shelf, in the right place

and that pricing and promotional tickets were on show.

This approach has resulted in additional sales by ensuring

compliance at each store level.

Our grocery channel sales continue to grow with the support

of the major retailers. Their support allows our core range of

products to be shipped to geographic regions outside of Norco’s

traditional territory, making our products available to new

customers who otherwise might not have the opportunity to

support Norco. The major retailers have also been supportive

Norco Foods -Sales and Marketing

Bu

sin

ess

Un

it R

epo

rts

11

34.6

Norco brandedmilk volume

%

28.4

and REAL volume

%

REAL Iced Chocolate milk

bestflavoured milk

in Australia

12

of our new and innovative product lines. Double digit

growth has been achieved in this segment this year.

Similarly, our Route Trade channel continues to grow

in strength and our reach continues to spread with

our network of dedicated Norco Milk Distributors. Our

focus on the Sydney market is working well for us.

We started supplying and gained distribution into the

Sydney based Harris Farm Markets network of stores, our

first major chain store relationship within the Sydney

basin. Additionally, we have signed up a number of new

distributors to support our growth in the Sydney region

which has primarily been back of house café sales to

date.

With the coffee market exploding in consumption and

milk making up 75 percent of the coffee cup, it’s an

important category that we have been focusing on by

establishing relationships and working alongside coffee

roasters to align their coffee beans with Norco milk. Our

heritage and provenance story works well in this segment

and the high quality profile of our milk provides the

perfect link with coffee roasters’ beans.

Our export business continues to be a sales strategy that

we are committed to and which will take time to build.

We are making grounds in this area and continue to field

inquiries for both milk and ice cream into China. We

have seen a number of clients come and go in this space

and although sales volumes have not been particularly

significant in the 2016/17 year, we do have some exciting

prospects that we are focusing on in the year ahead.

Ice cream is of particular interest given its long life and

Norco’s reputation for quality, and following on from a

successful sale of Norco ice cream through the on-line

Tmall business, we have certainly paved the way for

further sales opportunities.

Our ice cream business for the 2016/17 year was strong

yet faced challenging conditions. Price and supply

volatility in the commodity markets, in particular relating

to butter and cream, didn’t make it easy for us. In

addition, the activities of brand owners supporting half

price promotions meant the generic product market

into which we predominantly supply was affected by

softening sales. However on a more positive note, we

have won a major contract with one of the larger retailers

that will take us to new total production records in the

year ahead. There are certainly some exciting activities

to look forward to in the ice cream business unit during

2017/18.

ANDREW BURNS

General Manager Sales

and Marketing Norco Foods

I am pleased to report that Norco Foods Operations

has achieved significant progress in implementing our

business strategy during the 2016/17 financial year.

This strategy assisted us in achieving outstanding and

consistent results in safety, production efficiencies and

overall quality in all areas of our operations. By employing

this strategy, our Norco Foods Operations teams have

embraced the challenges that arise with continuous

growth at our manufacturing sites along with the need to

work through the logistics involved in an ever expanding

distribution network.

The commitment of our manufacturing teams to

continuous improvement and production line efficiencies

has resulted in increased production outputs while

ensuring quality product for our end users. First time

quality results for the year are the highest achieved to

date which is a credit to all staff given the increasing

production demands.

The Operations management team work closely with

the Sales and Marketing team to ensure the front end

Norco Foods - Operations

13

push into new sales markets is supported by cohesive

and responsive manufacturing and distribution functions

that consistently deliver solutions for the overall Norco

Foods business. Flexibility in factory operations, supply

chain management and a cross-functional focus were

all required to manage and respond to our changing

business needs during the 2016/17 year. Standout

achievements in manufacturing underpinned a year on

year volume growth of 4.5 percent in our milk plants.

At our Raleigh milk plant we increased our milk holding

capacity by installing two, 65,000 litre vats next to our

raw milk storage area. This extra holding capacity has

allowed the Raleigh team to smooth out production and

at the same time reduce tanker unloading down times.

Capital expenditure was approved to upgrade the waste

water plants at Labrador and Raleigh and both projects

are near the end of construction with an expected

completion date during September 2017.

While seeing a small reduction in volume at our Ice

Cream Business Unit (ICBU), our team still achieved an

outstanding result. This was driven by our strategy to

identify areas for improvement via the active involvement

of the manufacturing teams and through reporting

against set metrics and benchmarks. A large amount

of capital expenditure was spent at our ICBU focusing

on quality and process improvements and is expected

to provide a significant payback through improving

production and quality. Further significant amounts of

capital have also been committed to address the aging

plant and equipment and to put the business in a position

to be able to increase volume into the future.

It’s our people who ensure that Norco manufactured

products remain of the highest quality and meet our

customers’ requirements without fail. My appreciation

goes out to our highly skilled employees; it’s the people

that make our business.

As we embark on a new financial year, we look forward

to further strengthening the performance of the Norco

Foods Operations division.

ROBERT VANDERMAAT

General Manager Operations

Norco Foods

Norco Foods - Operations

4.5

MilkPlants

volume growth

%

65,000litre vats

installation of x2Raleigh Plant

14

Milk Supply

Any considered view on the Australian dairy industry for

2016/17 would largely reflect on the maelstrom that has

followed since some Victorian processors announced

retrospective farm gate price decreases in April 2016 in

the southern states.

The impacts have been wide ranging on farmers,

employees, rural communities, consumers, dairy industry

groups, government and regulatory authorities and dairy

processor operations whether large or small. The activity

and change that has followed within all these groups

has been a significant challenge for the dairy industry in

2016/17. Total Australian milk production fell 6.9 percent

or 700 million litres in 2016/17 as farmers reacted to

the management of the retrospective farm gate price

decreases and the negative outlook on price.

Norco was negatively impacted on a commercial basis

with significant market increases in external milk fat

pricing due to the availability of milk fat for our Ice Cream

Business Unit requirements. This issue was a result of the

reduced supply in Victoria and remains an industry wide

challenge. Norco’s positive relationships with customers

and suppliers ensured production continued throughout

the year.

In setting the Norco Milk Pay Rates for 2016/17, it was

important to take into account the need to balance

building in the Norco farm production increases of

2015/16 (+6.2 percent) whilst also reflecting a market

based farm gate milk price. Some difficult decisions were

made in regard to changing the volume capping of the

Collection Efficiency Bonus and, while continuing to

pay farm gate pricing over major competitors within

the region, a price decrease for the Southern Region

Members / Milk Suppliers was implemented. A Retrospect

Milk Pay Step Up payment was made for the first quarter

that reflected better than expected financial results from

an increase in Norco Branded milk sales and the higher

Rural / Agri division results.

The stability and growth of Norco within this

environment cannot be underestimated or ignored. The

level of resourcefulness, determination and resilience

of the Co-operative Members (through heat, flood and

increasing costs) and the employees to achieve success is

cause for quiet confidence for the future. A key and clear

milk supply strategy remains for Norco to manage the

overall supply position to maximise the financial return

for every litre of milk supplied for every Member of the

Co-operative.

Climate Conditions

2016/17 provided some very real and significant climatic

challenges for many, if not all, of Norco’s Members / Milk

Suppliers. After a dry spring / summer, all regions were

impacted by the very high temperatures and humidity

of late summer and finally the significant flood event in

the aftermath of Cyclone Debbie that devastated many

regions in March / April 2017. These testing events within

the year were the drivers of the lower farm production

growth which ended as a small increase of 0.9 percent

over the full year.

2016-17 Milk Supply summary

• Member supply was 221.8m litres for 2016/17 which was

steady compared to 2015/16 which saw a significant

volume growth from total supply.

• Total average farm gate milk price was 57.42 cents per

litre (cpl) versus 57.30 cpl for 2015/16.

• Northern Region average base farm gate price 57.53 cpl,

Southern Region average base farm gate price 56.47 cpl.

• Manufacturing litres were paid at base prices for the

third year in a row.

• For Member farms that supplied milk in both 2015/16

and 2016/17 there was an overall growth in volume of

+0.9 percent or 0.2 million litres versus the 2015/16 year.

• On this basis and by region, volume changes versus the

prior year were +1.0 percent for QLD, +3.2 percent for

North Coast NSW, -3.5 percent for Central North Coast

and +6.7 percent for the Southern Region.

Milk Supply Services

Through a consultation process with Members / Milk

Suppliers with a more flat line milk production curve, the

Interest Free Extended Accounts system was amended

to allow Members / Milk Suppliers to better manage their

cash flow over the different seasons and cost structures.

Further, a program to encourage on-farm generator

purchases with 12 months interest free terms was

introduced. These programs reflect Norco’s commitment

to assist Members / Milk Suppliers outside of milk price

considerations.

Other services from our Milk Supply team included

increased activity for farm / business succession planning,

quality control, industry funding applications, practical

research and development projects (both internal and in

conjunction with dairy industry groups and educational

facilities) and preparation for the transfer of the Milk

Payment System to SAP from 1 July 2017. For a small

team, these are important improvements and activities

that will ultimately benefit both the Norco Members / Milk

Suppliers and the Dairy Industry as a whole.

ROB RANDALL

General Manager

Norco Milk Supply

57.42cents per litre

Total averagefarm gatemilk price

222million litres

Member supply

15

Norco Rural / Agribusiness

Norco’s long standing and ongoing strategy of supporting

a diversified business model has definitely paid dividends

this year. Within this broader corporate strategy, the Rural

/ Agribusiness (Agri) division also has business diversity

through a network of over 30 individual business units.

This diversity helped guide the business through localised

challenges whilst delivering a record Rural / Agri profit

result to the Co-operative.

The rural sector started 2016/17 with a continuation of

the previous year’s positive seasonal conditions, coupled

with ongoing strong commodity values across most

segments of the rural market that Norco Rural / Agri

services. The cattle market remained strong with record

high prices being maintained throughout the year.

The horticultural and small crop market continued to

experience strong demand and favourable commodity

values. Within this segment our avocado and macadamia

clients experienced a period of high demand and

continuing strength in prices. The blueberry market

within our region continued with significant expansion

and we experienced plantations being established

outside traditional coastal regions. The macadamia

industry remains strong and after a several year lull in

new plantings there is renewed interest and multiple

new orchards being established. Within the dairy industry

production and pricing throughout our region remained

relatively stable and we have largely avoided the market

conditions experienced in the southern production areas.

The grain cropping side of our business, which is

primarily based within the Inner Downs and Burnett

areas of Queensland, experienced a good winter crop

but these regions experienced a significant deterioration

in seasonal conditions in the second part of the year

culminating in the smallest summer crop in 25 years.

The dry conditions continued throughout these regions

and they largely missed the opportunity to plant a winter

crop. Grain commodity prices remained relatively stable

and on the soft side throughout the first half of the

financial year, but with the onset of the big dry on the

western side of the range and a failed summer crop that

then led into a significantly reduced winter crop, the

18.9

Ruralrecorded

an EBITDA increase of

%

18.7

and Agribusiness

%10Bundaberg

& Toowoomba

YE

AR

S

16

grain market reacted abruptly with a major increase in all

commodity values.

Seasonal conditions on the eastern side of the range

remained favourable throughout the year. However, there

were notable challenges with two major rainfall events

during March 2017 resulting in major flooding throughout

south east Queensland and northern New South Wales.

This had severe negative impacts on many agricultural

producers throughout these regions.

In the Rural division major projects for the year included

the 10 year anniversary of Norco’s entry into the

Bundaberg market. The anniversary coincided with the

business unit relocating to new and significantly larger

premises in May 2017. The Bundaberg business has grown

considerably during the last few years and now stands as

one of Rural’s largest retail operations. Also celebrating 10

years is our Toowoomba business unit. Norco purchased

the BEW business in 2007 and this business unit has also

moved into a brand new custom built facility. Our Coffs

Harbour operation moved nine years ago into a new site

and this business has now outgrown its current location

as well. An agreement has been signed for a new larger

site and this business unit will relocate in May 2018.

Operationally several upgrades have been implemented

to our IT system and we’re currently rolling out a Client

Relationship Management (CRM) system to our field and

technical sales personnel to assist them in their servicing

of our valued clientele. Additionally, a new appointment

of Operations Manager Sales was made to drive our focus

in the areas of client relationship and management. Peter

Harden joined the business in this role in September

2016.

There were two major changes to the Suppliers’

Patronage Scheme during 2016/17. The first was the

amendment to the calculation of rewards applicable

to transactions facilitated by Norco Rural for the goods

and services supplied by external parties. This change

was implemented in October 2016. The second change

approved in March 2017 for implementation in July

2017 was a change in the reward matrix. Historically the

reward matrix had five reward bands however effective

from July 2017 this will change to three and will result in

higher payments to Members.

In Agri, the Crest bird seed manufacturing facility in

Toowoomba was closed effective October 2016 and the

plant and equipment sold. At our feed mills, both facilities

took delivery of new Kenworth bulk delivery vehicles.

Work Health and Safety

Work Health and Safety continues to be a high focus

area within Rural / Agri. Multiple projects and intense

engagement with Norco’s Human Resources department

has delivered strong favourable outcomes with a 47.6

percent decline in the number of Workers’ Compensation

claims and a massive 87.8 percent reduction in claims

costs versus the year prior. This is a great outcome

achieved by the division.

Financial performance

The combined EBITDA result of the Norco Rural /

Agribusiness division after the Suppliers’ Patronage

Scheme was an increase over last year of 24.4 percent.

Rural recorded an 18.9 percent increase in EBITDA

and Agribusiness produced an 18.7 percent increase in

EBITDA. At the net profit level, the division delivered a

record net profit which was an increase on last year of

29.7 percent.

Sales through the Rural division tracked strongly and

ahead of last year consistently throughout the year.

Similar to last year, we experienced a strong run home,

with substantial sales activity across all segments and

product groups. The Rural division delivered a 5.6 percent

year on year increase in sales and the total year sales

number was a record for the division. Our average

transaction value increased by 2.6 percent and the

total number of transactions facilitated increased by 2.5

percent.

The Gross Profit margin was adverse to last year by 0.1

percent, but our commitment to supporting R&D brands

and recognised industry suppliers resulted in a 12.6

percent increase in Sundry Income. Rural’s net profit was

19.8 percent up on last year and the ROCE improved 7.3

percent versus the prior year.

Within the Agri division the headline sales number was

adverse 6.7 percent to last year. However, this decline is

largely a reflection of a poor summer crop, the resultant

reduced trading opportunities and also, on average,

lower per tonne commodity values to the corresponding

periods in the previous year. Notwithstanding this, our

feed mills recorded a 1.6 percent increase in volume

manufactured with total volume mix being favourable

towards non-bulk, higher value packaged products. In

addition, our Lismore mill recorded its highest overall

volume manufactured in 10 years and set a record for

production of packaged products. The Norco Grain

business unit set another record for volume traded with

volume up 10.8 percent year on year. With the increased

volume and a favourable product mix, the Agri division

recorded a 25.8 percent increase in net profit and a ROCE

improvement of 10.8% versus last year.

Suppliers’ Patronage Scheme

With the changes to the Suppliers’ Patronage Scheme

implemented in October 2016, the final year total spend

by Members with their Co-operative business was $1.131

million which was slightly below the previous year’s

$1.156 million. The number of Members transacting with

the Co-operative increased

from 92 percent to 93

percent.

DAMON BAILEY

General Manager Norco

Rural / Agribusiness

17

Corporate - Financial Management

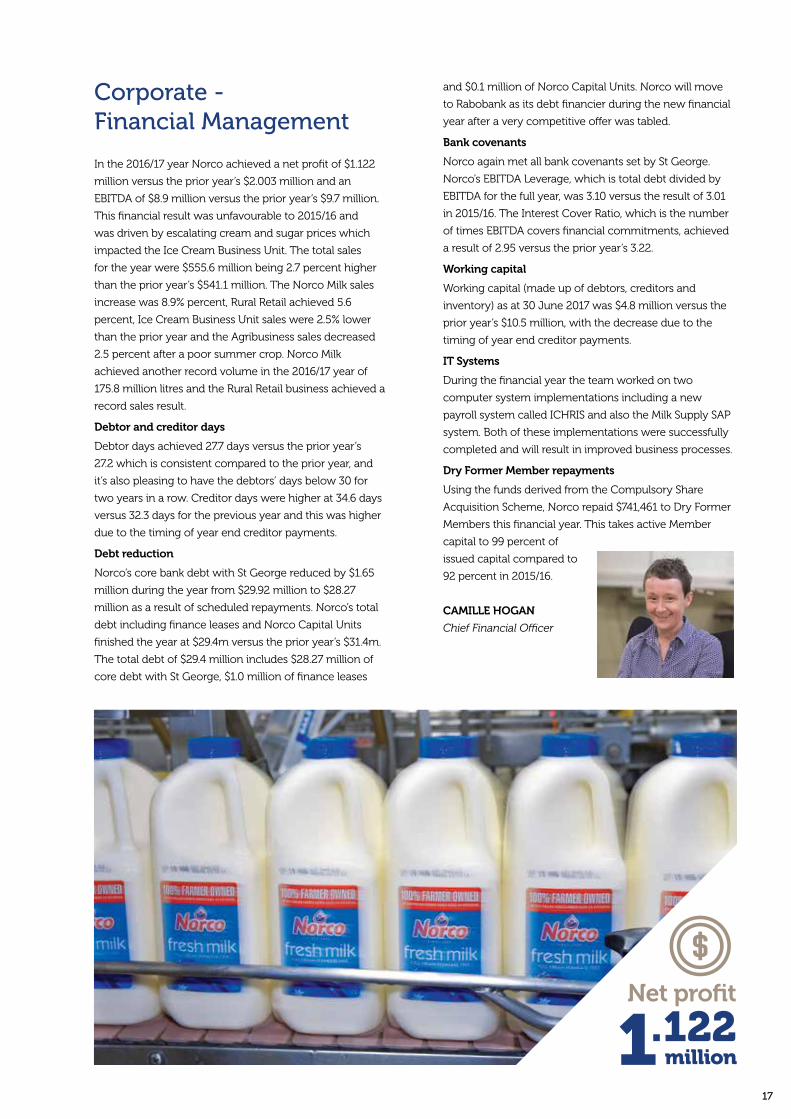

In the 2016/17 year Norco achieved a net profit of $1.122

million versus the prior year’s $2.003 million and an

EBITDA of $8.9 million versus the prior year’s $9.7 million.

This financial result was unfavourable to 2015/16 and

was driven by escalating cream and sugar prices which

impacted the Ice Cream Business Unit. The total sales

for the year were $555.6 million being 2.7 percent higher

than the prior year’s $541.1 million. The Norco Milk sales

increase was 8.9% percent, Rural Retail achieved 5.6

percent, Ice Cream Business Unit sales were 2.5% lower

than the prior year and the Agribusiness sales decreased

2.5 percent after a poor summer crop. Norco Milk

achieved another record volume in the 2016/17 year of

175.8 million litres and the Rural Retail business achieved a

record sales result.

Debtor and creditor days

Debtor days achieved 27.7 days versus the prior year’s

27.2 which is consistent compared to the prior year, and

it’s also pleasing to have the debtors’ days below 30 for

two years in a row. Creditor days were higher at 34.6 days

versus 32.3 days for the previous year and this was higher

due to the timing of year end creditor payments.

Debt reduction

Norco’s core bank debt with St George reduced by $1.65

million during the year from $29.92 million to $28.27

million as a result of scheduled repayments. Norco’s total

debt including finance leases and Norco Capital Units

finished the year at $29.4m versus the prior year’s $31.4m.

The total debt of $29.4 million includes $28.27 million of

core debt with St George, $1.0 million of finance leases

and $0.1 million of Norco Capital Units. Norco will move

to Rabobank as its debt financier during the new financial

year after a very competitive offer was tabled.

Bank covenants

Norco again met all bank covenants set by St George.

Norco’s EBITDA Leverage, which is total debt divided by

EBITDA for the full year, was 3.10 versus the result of 3.01

in 2015/16. The Interest Cover Ratio, which is the number

of times EBITDA covers financial commitments, achieved

a result of 2.95 versus the prior year’s 3.22.

Working capital

Working capital (made up of debtors, creditors and

inventory) as at 30 June 2017 was $4.8 million versus the

prior year’s $10.5 million, with the decrease due to the

timing of year end creditor payments.

IT Systems

During the financial year the team worked on two

computer system implementations including a new

payroll system called ICHRIS and also the Milk Supply SAP

system. Both of these implementations were successfully

completed and will result in improved business processes.

Dry Former Member repayments

Using the funds derived from the Compulsory Share

Acquisition Scheme, Norco repaid $741,461 to Dry Former

Members this financial year. This takes active Member

capital to 99 percent of

issued capital compared to

92 percent in 2015/16.

CAMILLE HOGAN

Chief Financial Officer

1.122Net profit

million

18

Staffemployed

604Norco Foods

173Norco Rural

38Norco

Agribusiness

22Corporate

19

Corporate - Norco People

Human Resources

Norco employs a range of strategic workforce initiatives

to recruit, retain, manage and train both its regular

employees and casuals. Having a committed and

competent workforce plays an instrumental role in

securing the future success of our diverse Co-operative.

During 2016/17, the Human Resources (HR) team

provided key support to the changing operating context

in Norco, while also managing substantial changes in its

own resources and structure. At the same time, HR has

focused on positioning Norco as an organisation where

talent is nurtured and where innovation and delivery of

results are promoted.

During 2016/17, HR dedicated significant time and effort

to the development and implementation of the new

ICHRIS HR and Payroll system which was implemented

across the organisation. The integrated system

allows enhanced talent management, streamlining of

processes and consistency, for both HR practitioners

and users company-wide. The new system will also

facilitate monitoring and reporting in real time on key

HR processes and metrics such as sick leave and hours

worked.

With the continued growth of Norco, HR is working with

line managers to promote an enhanced performance

culture, by increasing engagement, encouraging

managers to provide honest and constructive feedback,

as well as supporting employees in receiving it. This

strategic agenda includes several initiatives such as

effectively developing talent and enhancing leadership

capacity and addressing performance management

issues. This focus on an enhanced performance culture

will continue during the next year.

Work Health & Safety

It’s been a big year for safety at Norco with a continuous

improvement mentality resulting in a 10 percent

reduction in Workers’ Compensation claims compared

with the previous year. It is also pleasing to see that the

severity of injuries has also decreased as indicated by

the lower overall average cost per claim.

Through a series of external audits, Norco has

maintained the external third party accreditation of

our Work Health and Safety Management system. This

together with self generated internal safety audits has

resulted in the implementation of numerous physical

safety improvements across many of our sites as well as

improved Policies and Procedures.

Some of the continuous improvement actions that have

taken place over the past year which have contributed

to the positive result are:

• Continuation of the proactive guarding project

designed to reduce the risk of moving machinery, thus

reducing the risk to all employees who work around

plant and equipment.

• Instigation of a proactive working at heights project,

focusing on heights access and the tasks performed

at heights in order to determine and implement

engineering solutions to minimise the risk of this type

of work.

• The filming of a series of Norco specific WHS induction

videos for all employees with all employees being re-

inducted.

• Continued development and implementation of

a Human Resources Information System with a

focus on Work Health and Safety and Learning and

Development modules.

The WHS Information System will become an integral

part of the Norco Work Health and Safety Management

System. Implementation of the WHS database will

enable us to analyse, identify and monitor safety

improvement opportunities through capturing relevant

safety information resulting from Incident Reporting,

Hazard Analysis, Risk Assessments, Audits etc.

Going forward, we must challenge ourselves to move

further into the proactive space in terms of safety, with

the health, safety and wellbeing of our employees,

customers and contractors

paramount to all our

activities.

TOM McATEE

General Manager Human

Resources38

2020

The Directors present their report together with the financial reports for Norco Co-operative Limited (‘the Co-operative’)

for the year ended 30 June 2017 and the Auditors’ report thereon.

The Board of Directors currently comprises six supplier Directors (non executive) and no Independent Directors.

The Directors bring a range of skills and experience to the Board room in addition to their core strength of having a detailed

understanding of the dairy industry. This includes having experience in wider agricultural sectors (in addition to dairying),

extensive experience in business planning and strategy and strong leadership. In coming together as a Board, the Directors

have a shared desire to ensure Norco’s strategic business objectives are met while at all times, acting in the best interests of

the Members as a whole.

For the full 2016/17 financial year, the Board continued to utilise the consultancy services of Ms Tanya Crowther, who

actively contributed to the overall performance of the Board and attended all monthly Board meetings during the year. Ms

Crowther continues to be contracted by the Board to provide her services.

The Directors also acknowledge that the market place within which Norco operates, on both a domestic and global

platform, is changing at a fast pace. Directors are constantly on a path of learning as the Co-operative has a diversified

business model which needs to move with the market. Continually improving the knowledge and skills base in the Board

room assists to ensure that the Directors are able to govern the Co-operative in the most effective manner possible, using all

relevant information, tools and resources available to them.

During the year, the Chairman asked members of the management team to provide in depth information regarding various

aspects of the business in the form of master classes. The Directors received master classes on merchandising, the Route

Trade and the budget process. The Directors also explored the potential use of solar power on farms, inviting Mr N d’Avoine

of CommPower to speak about this emerging opportunity. The opportunity also arose to visit the University of Queensland

Gatton Campus, with the dairy farm on site being a Member farm of the Co-operative. As a result of this visit, the two

organisations have forged a much closer bond in relation to potential research and development projects and also student

placements on Norco Member farms.

The Directors also continue to be committed to their ongoing professional development and during the year have had the

opportunity to attend, and represent Norco, at a range of industry conferences. All Directors are members of the Australian

Institute of Company Directors (AICD) and are encouraged to attend various AICD educational courses and functions.

It is pleasing to report that the two Directors elected to the Board on 9 November 2016, Mr GJ Billing and Mrs E Watson,

completed the AICD Company Directors’ Course during June 2017.

Strategic discussions play an important role at each and every Board meeting and time is always allocated to this important

aspect of the business, which allows the Directors and the management team to look forward and discuss emerging

opportunities and trends as well as future challenges. In addition, a yearly strategic workshop involving Directors and the

management team is held which underpins the Co-operative’s strategic plan.

In coming together as a Board, the Directors have a shared desire to ensure Norco’s strategic business objectives are met while at all times, acting in the best interests of the Members as a whole.

Dir

ecto

rs’ R

epo

rt

21

Gregory J McNamara – Chairman

Greg McNamara has been a Director of Norco Co-

operative Limited for 21 years and is from the Central

Region. In addition to his role as Chairman of the Board

of Directors, he is a member of the Member Services

Committee.

In partnership with his wife Sue and son Todd, Greg

runs a 300 head dairy herd at Goolmangar just

outside Lismore. He has extensive experience across

the agricultural sector, including dairy, beef, pigs,

horticulture and animal genetics.

A primary focus for Greg during 2016/17 in his role as

Chairman has been to ensure the successful integration

of two new Directors into the Norco business from

November 2016 while ensuring the business stayed on

track in achieving its overall strategic objectives which

include rewarding Members’ with a sustainable and

competitive milk price through having a diverse and

successful business model.

Greg is a member of the Australian Institute of Company

Directors and continues to be a keenly sought after

speaker for industry events and forums. During the

2016/17 year, Greg attended the Australian and New

Zealand Co-operative Leaders Forum in Auckland

New Zealand. Greg is also a Board member of the

New South Wales Business Chamber and Chairperson

of the Industry Advisory Group (IAG) within the

Farm Co-operatives and Collaboration Pilot Program

(FCCPP). More recently, Greg has accepted the role of

Chairperson of the Australian Organic Industry Working

Group which has been established to facilitate a

restructure of the organic industry in Australia.

Gregory J Billing - Director

Greg was elected to the Board of Directors on 9

November 2016 and is a supplier Director from Norco’s

Southern Region. Greg is a member of the Member

Services Committee.

Greg is a fourth generation dairy farmer and in

partnership with his wife Carmen, they have grown their

dairy herd from 44 cows to over 600 at the present time

on their Dorrigo property. The large dairy herd means

that Greg and Carmen have a team of employees to

assist with milking and herd management while Greg

concentrates on the pastures and heifer raising activities.

The governance programmes for potential new

Directors run by the Co-operative in recent years

provided the groundwork for Greg to gain a good

understanding of the Norco business and governance

issues before nominating for a position on the Board

of Directors. As a Norco Board member, Greg is

enthusiastic about the future for Norco and the dairy

industry and has a passion to see more young people

come into the industry, as the future of dairying lies

with the next generation. Greg is also a supporter of the

farmer owned co-operative model and is keen to see

strategies implemented that grow a stronger business

with a positive and aggressive vision for the future and

which in turn, builds wealth for Norco’s Members.

In addition to learning about the Norco business

in depth since becoming a Director, Greg has also

completed the AICD Company Directors’ Course

(residential) during June 2017.

DIRECTORS

22

Heath B J Hoffman - Director

Heath was elected to the Board of Directors on 12

November 2014 and is a supplier Director from the

Northern Region. He is a member of the Audit and Risk

Management Committee.

Heath is a member of a family partnership that owns

and operates a dairy farm near Warwick milking 300

Holstein cows on a full TMR (total mixed ration) system.

Having now almost completed a full three year term

as a Director, Heath has proven himself as both an

effective team member in the Board room and also as

an independent thinker in relation to Norco’s strategy

going forward. For Heath, a basic strategic goal is to

ensure there is a successful future for the northern

dairy industry. Heath is also equally comfortable

discussing the strategy for the Norco Foods’ business

as he is discussing the strategy for Rural / Agri and has

demonstrated a keen interest in understanding the

business operations.

Heath is a member of the Australian Institute of

Company Directors. During the year, Heath travelled

to Victoria with the General Manager Milk Supply to

investigate the use and application of vat temperature

probes for Norco’s Member farms as a way of potentially

saving Members from needing to dispose of milk that

has been compromised during the cooling process.

Michael C Jeffery - Director

Michael Jeffery was elected as a Director on 14

November 2012 and is from the Southern Region.

Michael is Chairman of the Audit and Risk Management

Committee.

Michael has been farming at Austral Eden near Kempsey

in a family partnership for 28 years and milks a herd

of 300 cows. He has extensive business, marketing

and dairy industry experience, including in overseas

countries and has held a number of positions including

directorships in dairy related export, consulting and

genetics businesses. In addition, Michael has been

a state delegate of both the NSW Dairy Farmers’

Association and Holstein Australia for five years. He had

been on LiveCorp’s China Live Export Industry Working

Group Committee for two years and as part of the

NorcoNet communication network, has been Chairman

of the Nambucca / Kempsey group for three years.

Michael also holds an Advanced Diploma in Agriculture.

More recently, Michael has been appointed as an

Alternate Delegate to the Dairy Connect Farm Group

Board and is the current Chairman of the Kempsey Dairy

Industry Group, a position he has held for five years.

Michael is a member of the Australian Institute of

Company Directors and has also previously completed

the AICD Finance for Directors course. During the year,

Michael attended the Australian and New Zealand Co-

operative Leaders Forum in Auckland, New Zealand with

the Chairman and earlier in the 2016/17 financial year

also represented Norco at the Industry Session of the

Regional Economic Opportunities Infrastructure Project

in Coffs Harbour.

23

Leigh Shearman - Director

Leigh was elected as a Director on 14 November 2012

and is from the Central Region. Leigh is Chairperson of

the Member Services Committee.

Leigh owns and operates a dairy farm at Goolmangar

just outside Lismore milking 180 cows. Leigh also has

experience across a broad agricultural base gained over

many years, including beef, horticulture and intensive

piggery farming. She has also owned and operated a

retail franchise and has worked in the banking industry

for 10 years. Leigh has a Diploma in Rural Business

Management, Diploma of Agriculture and Certificate

III Financial Services. Leigh is the vice chairperson of

the Far North Coast Dairy Industry Group Inc (DIG),

chairperson of the Goolmangar Water Users Association

and a member of the Steering Committee for the

Northern Rivers Resource Efficiency Focus Farm.

Leigh is a strong believer in the benefits of being part

of a co-operative and is confident that this model will

ensure the long term sustainability of Norco’s Members

and other stakeholders associated with, and reliant on, a

strong and progressive Norco business.

Leigh is a member of the Australian Institute of

Company Directors. As Chairperson of the Member

Services Committee, Leigh is committed to encouraging

Members having the opportunity to improve their

skills and farming techniques to ensure the long term

sustainability of the Norco farm base. One way of

achieving this is through study tours. Over recent years

Norco, through the Member Services Committee, has

organised highly successful study tours to New Zealand

and recently an ambitious tour of Western Europe and

Ireland has been undertaken.

Elke Watson - Director

Elke was elected to the Board of Directors on 9

November 2016 and is a supplier Director from Norco’s

Northern Region. Elke is a member of the Audit and Risk

Management Committee.

Elke and her husband Peter farm at Conondale in

Queensland where they milk 250 - 300 cows. They

also have four young adult children with an interest in

the farm. Elke and Peter transferred their milk supply to

Norco in July 2014 from another processor and value

being part of a co-operative again.

Elke is in the process of studying a business

management degree on a part-time basis and has a

Diploma in Human Resource Management and has

extensive business experience outside of the farm

environment, including 25 years experience in financial

management. Elke is a past State Councillor of the

Queensland Dairyfarmers’ Organisation (QDO) and still

maintains membership in, and association with, this

organisation.

Elke enthusiastically participated in the governance

program for potential new Directors in 2016 before

nominating for a Board position. Now as a member of

the Norco Board of Directors, Elke is keen to work for

all Members of the Co-operative to ensure there is a

sustainable dairy industry in the subtropical region. In

addition to taking on the challenge of learning about

the Norco business in depth since becoming a Director,

Elke has also completed the AICD Company Directors’

Course (residential) during June 2017.

Note: At the Directors’ meeting held on 14 and 15 December 2016 it was determined that the operation of both the Milk

Supply Advisory Committee and Brand Management Advisory Committee would again be suspended for a further 12

months and that any items previously considered by these committees would be incorporated into the Directors’ meetings

until further notice.

24

DIRECTOR ELECTIONS – 2016/17

As reported last year, it was determined that the casual

vacancy created in the Southern Region as a result of Mr

PW Neal’s resignation on 23 November 2015 would be

filled as part of the 2016 ordinary election of Directors

programme, as Mr Neal was due to retire at the 2016

Annual General Meeting.

As a result of the changes to Norco’s Rules which

became effective on 1 July 2014, the retiring Director for

the Northern Region, Mr AW (Tony) Wilson, whose dairy

farm interest is located in the Kyogle Local Government

Area of NSW, was no longer eligible to serve as a

Supplier Director for the Northern Region and so could

not offer himself for re-election.

As a result of the Southern Region vacancy and Mr AW

Wilson being ineligible for re-election in the Northern

Region, Member nominations were called for both

regions. Northern Region Member nominations were

received from Mr MT Trace, Mr PJ Rough and Mrs E

Watson. Southern Region Member nominations were

received from Mrs SE McGinn, Mr CJ Brander and Mr

GJ Billing. Accordingly a postal ballot was held for both

regions resulting in Mrs E Watson (Northern Region)

and Mr GJ Billing (Southern Region) being elected for

three year terms effective from the 2016 Annual General

Meeting on 9 November 2016.

The positions of Chairman and Deputy Chairman are

voted on annually by the Directors following the Annual

General Meeting.

Directors’ Meetings

The number of Board meetings (and meetings of the

Audit and Risk Management Committee) and number of

meetings attended by each of the Directors of the Co-

operative during the financial year are:

During the course of the 2016/17 financial year there

were also seven Directors’ meetings and one Audit

and Risk Management Committee meeting held by

teleconference. Teleconferences are organised to

discuss and resolve specific issues that cannot be held

over until the next scheduled monthly meeting and

generally the duration of such teleconferences is one

hour or less. Teleconferences are a cost effective and

practical way for Directors to discuss specific issues in

a timely manner given that their residences are spread

over a large geographic area.

CORPORATE INFORMATION Corporate structure

Norco Co-operative Limited is a co-operative limited by

shares which is incorporated and domiciled in Australia.

Nature of operations and principal activities

The principal activities of the Co-operative during the

financial year were the processing, manufacture and

sale of dairy products, the manufacture and sale of

stockfeeds and rural retailing.

Employees

The Co-operative employed 540 full-time, 54 part-time

permanent and 243 casual employees at 30 June 2017

(2016: 510 full-time, 69 part-time permanent and 227

casual employees).

Results of operations

The net amount of the operating profit for the financial

year of the Co-operative after providing for income tax

was $893,000 (2016: $721,000 profit).

Derivatives and other financial instruments

The Co-operative’s activities expose it to changes in

interest rates, foreign exchange rates and commodity

prices. It is also exposed to credit, liquidity and cash flow

risks from its operations. During the year, the Board has

maintained policies and procedures in each of these

areas to manage these exposures. Management reports

to the Board on a monthly basis on the monitoring of

and compliance with the policies in place.

Dividends

Dividends paid during the 2016/17 financial year totalled

Directors’ Meetings

Audit and Risk

Management

Committee Meetings

A B A B

GJ McNamara 13 13 - -

GJ Billing 8 8 - -

HBJ Hoffman 13 13 9 9

MC Jeffery 13 13 9 9

L Shearman 13 13 - -

E Watson 8 8 6 6

AW Wilson 5 5 3 3

A Reflects the number of meetings held during the time the Director held office during the year

B Number of meetings attended

25

$550,000 (being a dividend rate of 6.0% [six percent] on

issued capital), declared and approved by Members at

the 2016 Annual General Meeting, which was held on 9

November 2016.

Operations review

The Directors’ have reviewed the Co-operative’s

operations during the financial year and the results of

those operations, which are discussed in the Chairman’s

Report for the financial year ended 30 June 2017 (see

page 4).

Events subsequent to balance date

On 1 September 2017 the Co-operative entered into a

three year term financing facility with Rabobank. This

new facility replaces the existing facility with St George

Bank as disclosed in Note 13.

Mr Brett Kelly resigned from his role as Chief Executive

Officer effective 29 September 2017. The Board is

currently recruiting to fill the vacancy.

Other than the matters listed above, during the interval

between the end of the financial year and the date of

this report, there has not arisen any item, transaction

or event of a material and unusual nature which, in the

opinion of the Directors, is likely to significantly affect

the operations of the Co-operative, the results of those

operations or the state of affairs of the Co-operative in

subsequent financial years.

Future developments

In the opinion of the Directors, disclosure of information

regarding the likely developments in the operations of

Norco in future financial years and the expected results

of those operations is likely to result in unreasonable

prejudice to the Co-operative. Accordingly, this

information has not been disclosed in this report.

Indemnification and insurance of Directors and

Officers

The Co-operative has entered into agreements to

indemnify all Directors named at the beginning of this

report, former Directors and current and former Officers

of the Co-operative against all liabilities to persons

(other than to the Co-operative or to a related body

corporate) which arise out of the performance of their

normal duties as a Director or Officer, unless the liability

relates to conduct involving a lack of good faith.

The Co-operative has agreed to indemnify the Directors

and Officers against all costs and expenses incurred in

defending an action that falls within the scope of the

indemnity and any resulting payments. The relevant

insurances cover legal liabilities and associated costs

arising from the performance of their duties as Directors

and Officers and compensation for loss or injury

sustained in the course of such duties.

Indemnification of Auditors

To the extent permitted by law, the Co-operative

has agreed to indemnify its Auditors, Ernst & Young

Australia, as part of the terms of its audit engagement

agreement against claims by third parties arising from

the audit (for an unspecified amount). No payment has

been made to indemnify Ernst & Young during or since

the financial year.

Options over unissued shares

Options over unissued shares have not been granted

to any person or Director since the end of the previous

financial year to date of this report.

Directors’ benefits

Since the end of the previous financial year, except as