Embed Size (px)

Citation preview

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997)

Osman Karam usfa faLeading Indicators Approach for Business Cycle Forecasting and a Study

on Developing a Leading Economic Indicators Index for the Turkish EconomyAla M u ru tog lu

Chaos Theory, Non-Linear Behavior in Stock Returns,Thin Trading and Market Efficiency in Emerging Markets:

The Case of the Istanbul Stock Exchange A lpe r Ozuim

■

The ISE ReviewQuarterly Econom ics and Finance Review

On Behalf of the Istanbul Stock Exchange Publisher

ContributorsA d a le t P O L A T E rh a n E K E R

Chairman & CEOO s m a n B ÎR S E N

M u ra d K A Y A C A N G ü rse l K O N A

D r. M . K e m a l Y IL M A ZManaging Editor

D r. M era l VARIŞ TEZCANLI

Editor-in-ChiefS a a d e t Ö Z T U N A

S ed a t U Ğ U R G ö k h a n U G A N L e v e n t Ö Z E R A ltu ğ A K S O Y

G ö k h a n Ö N D E R O Ğ L U

Editorial BoardA n î S E R E N

S e z a i B E K G Ö Z H ik m e t T U R L İN

K u d re t V U R G U NA y d ın S E Y M A N Editorial Production & Printing

D r. M era l V A R IŞ T E Z C A N L I M a r t M a tb a a c ılıkR e c e p B İL D İK S a n a tla r ı T ie . L td . Ş ti.

A li K Ü Ç Ü K Ç O L A K H a lu k Ö Z D E M İR

T h e v iew s an d o p in io n s in th is J o u rn a l b e lo n g to th e au th o rs an d do n o t n e c e ssa r ily re f le c t th o se o f th e Is tan b u l S to c k E x c h a n g e m a n a g e m e n t a n d /o r its

T h is re v ie w p u b lish e d q u arte rly . D u e to its leg a l s ta tu s , th e Is tan b u l S to c k E x c h a n g e is e x e m p t fro m c o rp o ra te tax.

A d d ress : IM K B (IS E ), R e s e a rc h D e p a rtm e n t, 8 0 8 6 2 0 Is tin y e , Is ta n b u l/T U R K E Y P h o n e : (0 2 12 ) 2 98 21 0 0 F ax : (0 2 1 2 ) 298 25 0 0

In te rn e t w eb site : h ttp ://w w w .im k b .g o v .tr e -m a il: im k b -f@ im k b .g o v .tr e -m a il: a ra s tir@ im k b .g o v .tr

wd e p a rtm e n ts

Copyright © 1997 ISE All Rights Reserved

The ISE ReviewVolume 3_____ No. 9___________________January/February/March 1999

CONTENTS

ArticlesBasic Financial Characteristics in the Banking Sector: An Empirical

Analysis (1990-1997)Osman Karamustafa............................................................................... 1

Leading Indicators Approach for Business Cycle Forecasting and aStudy on Developing a Leading Economic Indicators Index for the Turkish EconomyAli Mürütoğlu....................................................................................... 21

Chaos Theory, Non-Linear Behavior in Stock Returns, Thin Trading and Market Efficiency in Emerging Markets: The Case of the Istanbul Stock ExchangeAlper Özün.............................................................................................41

Global Capital Markets.............................................................................. 75ISE Market Indicators.................................................................................87Book Reviews.................................................................................................91Emerging Markets: Research Strategies and Benchmarks

Michael Keppler and Martin Lechner “Financial Engineering”: A Complete Guide to Financial Innovation

John F. Marshall & Vipul K. Bansal Investment Intelligence from Insider Trading

H. Nejat SeyhunISE Publication List.....................................................................................97

The ISE Review Volume: 3 No: 9 January/February /March 1999 ISSN 1301-1642 © ISE 1997

BASIC FINANCIAL CHARACTERISTICS IN THE BANKING SECTOR: AN EMPIRICAL ANALYSIS

(1990-1997)

Osman KARAMUSTAFA*

AbstractT h is p a p e r a im s a t a n a ly s in g h o w f in a n c ia l c h a ra c te r is t ic s o f c o m m e r c ia l b a n k s o p e r a t in g in T u r k is h f in a n c ia l m a rk e ts d e v e lo p e d b e tw e e n 1 9 9 0 -1 9 9 7 . F in a n c ia l c h a ra c te r is t ic s a r e d e te rm in e d b y tr a n s f o rm in g d a ta o b ta in e d f ro m b a la n c e s h e e t a n d in c o m e s ta te m e n ts a n d c o l le c tin g th e s e ra tio s in c e r ta in g ro u p s th ro u g h th e u s e o f m u l t iv a r ia te s ta t i s t ic a l te c h n iq u e s , I t is fo u n d th a t f in a n c ia l s t ru c tu re o f b a n k s is th e m o s t im p o r ta n t v a r ia b le d e te rm in in g f in a n c ia l c h a ra c te r is t ic s , w h ic h u s u a l ly h a v e a s ta b le s t ru c tu re in th e p e r io d u n d e r c o n s id e ra t io n .

I. IntroductionIn the finance literature, the use of financial ratios as a data source to determine financial characteristics has usually been confined to firms operating outside the finance sector. Pinchel et aL (1973) were among the first who did research on the subject by studying 48 financial ratios of 221 companies between 1951-69. Similarly, O’Connor (1973) found 10 financial characteristics obtained from 33 financial ratios of 127 companies between 1950-66. He also examined the impact of these financial characteristics on returns on equities. In addition, Laurent (1979) suggested 10 financial characteristics by analysing 45 financial ratios of 63 companies. One of the recent studies on the subject was conducted by Martikainen (1993) who found 3 financial characteristics derived from 11 financial ratios of 28 companies between 1975-86.

These studies attempted to determine a specific number of financial ratios or factors on the basis of analysing a great number of ratios fwhich emphasise a specific financial dimension. Following this, the best ratios

* Faculty of Business Administration and Economics, Department of Management, Sakarya University, Esentepe, AdapazanE-mail: [email protected] Tel: 0264-3460334

Osman Karamustafa

are chosen by means of multivariate statistical techniques. Determining a smaller number of financial ratio groups enables both company management and outside interest groups such as customers, potential investors and researchers to have more valuable information in their decision-making activities. y

Financial ratios have a variety of applications through the use of multivariate statistical techniques. In the literature, correlation structures of ratios are analysed to establish ratio groups (Jackendoff, 1962). Ratios have, furthermore, been used as data sets to classify bonds (Horrigan, 1968; Pinches ve Mingo, 1973), predict company failures and bankruptcies (Beaver, 1966; Altman, 1968; Edmister, 1972; Goktan, 1981; Akta§, 1993) and analyse effects of shares on their returns (Martin, 1971). The use of financial ratios in the banking sector tends to concentrate on exam- lining financial structures of banks that have financial problems (Sinkey, ¡1975; Pettay and Sinkey, 1980) and evaluating their capital structure (Dince and Fortson, 1972). Moreover, in a study of 32 financial ratios of bankrupt banks, Meyer and Pifer (1970) found that bankruptcies could be predicted two years in advance.

All these studies vividly illustrate the significance of financial ratios for both banks and companies. This work makes an attempt to explain the structure of financial characteristics (derived from financial ratios) of commercial banks in Turkey in a certain period. The determination of whether financial characteristics have stable structures assists decision- making process of interest groups dealing with banks (Gombola and Ketz, 1983).

II. Thé Data and Research MethodThe research contains 18 financial ratios of private, public and foreign banks which operate in the Turkish financial system (see, table 2). These ratios are obtained from balance sheet and income statements of the banks between 1990-97. Data set used in the research is taken from 1997 Yearbook of Banks published by Turkish Union of Banks. Financial ratios in the below table have been analysed separately for each year in the period.

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997) 3

Table 2.1: Financial Ratios Used in the Research

(Equity Capital + Profit) / Total Assets (Equity Capital + Profit) / (Deposit+Non-Deposit Resources)

Net Working Capital / Total Assets (Equity Capital + Profit) /(Total Assets +Non-Cash Credit)

Net Profit for the Period / Average T.Assets Net Profit for the Period / Average Equity Capital

Net Profit for the Period / Average Paid-up Capital Liquid Assets / Total AssetsLiquid Assets/ (Deposif+Non-Deposit Resources) FC Liquid Assets / FC LiabilitiesOther Operating Income / Other Operating Expenses Total Income/ Total ExpensesTotal Credits / Total Assets Non-Performing Loans / Total

LoansLong Term Assets/ Total Assets FC Assets / FC Liabilitiesinterest Income on Non-Performing Loans/ Average Total Assets

Interest Income / Interest Expenses

Financial characteristics have been determined by “principal component factor analysis”. Factor analysis is a multivariate statistical method which shows whether correlations or covariances of an observable data set can be explained by a smaller number of unobservable potential factors or variables (Everit and Dunn, 1991). This paper endeavours to account for total variance of 18 financial ratios by reference to a smaller number of factors.

“A reliability test” has been conducted to see if variable groups determined by factor analysis are factors that affect financial characteristics of the banks. “Cronbach Alpha” value derived from this test indicates internal reliability of variables. If internal reliability of variables which make up a factor is below 0.50, these variables are sequentially excluded from the group. The analysis is, then, repeated to define factors in terms of variables which have greater internal reliability (Hair et al,, 1998). In this way, we can determine which variables impinge upon financial characteristics of the banks.

III. The ResultsThe results of the research are presented separately in tables for a seven year period, which contains standard data obtained from the statistical analysis.

Osman Karamustafa

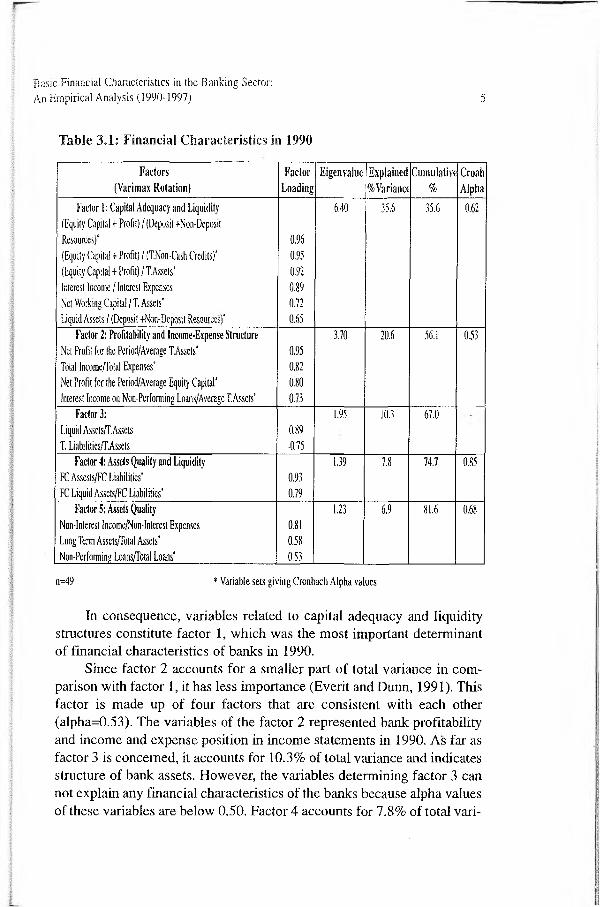

Table 3,1 shows that financial characteristics of commercial banks are grouped under five factors for the year 1990. In practice, variables explaining variance larger than variance of each variable are included in the model (Norusis, 1993), Thus, out of 18 principal components, only those with an eigenvalue greater than 1 are included in the model.

The first column in the table shows factors of the model and variables determining these factors. Factor loading defines to what extent variables affect factors and correlation coefficients between variables and factors. Hence, the most important variable determining factor 1 is the variable (Equity Capital+Profit)/ (Deposit+Non-Deposit Resources) which has the highest factor loading value. Eigenvalue column demonstrates to what degree factors account for total variance of 18 financial ratios. Thus, factor 1 explains 6.40 of the total variance. While factor 1 accounts for 35.6 % ([6.40/181*100) of total variance, factor 2 explains20.6 % of the rest. The first five factors included in the model account for81.6 percent of the variance. As the part of the factors explaining total variance decreases, they become less important in determining financial characteristics. Accordingly, factor 1, which has no relationship with the other factors accounting for the rest of the total variance, is the most crucial factor. “Cronbach Alpha” values in the table represent internal reliability of variables. As a result, six variables, which have the highest factor loading, determine factor 1. On the other hand, alpha reliability values of these six variables are below 0.50 (around 0.39). Although this outcome may indicate that six variables explain a financial characteristics, it also means that they randomly come together and there is an inconsistency among the variables. By leaving out each variable group consecutively, the reliability analysis is repeated to find out the variable causing low alpha value. For the factor 1, if we exclude “Interest Income/Interests Expenses)” variable, internal reliability among the other variables rises to an acceptable level (0.62). Hence, it is necessary to leave out this variable from the model. Variables with (*) sign denote variables producing acceptable alpha values.

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997) 5

Table 3.1: Financial Characteristics in 1990

Factors (Varimax Rotation}

FactorLoading

Eigenvalue Explained % Variance

Cumulative%

CroahAlpha

Factor I: Capital Adequacy and Liquidity(Equity Capita! + Profi!) / (Deposit +Non-Deposil Resources)'(Equity Capital + Profit) / (T.Non-Cash Credits)' {Equity Capital + Profit)/T. Assets' interest Income / Interest Expenses Ne! Working Capital / T. Assets*Liquid Assets / (Deposit +Non-Deposit Resources)*

0.960.950.920.890.720.65

6.40 35.6 35.6 0.62

Factor 2: Profitability and Income-Expense StructureNet Profit for the Period/Average TAssets*Total Income/Total Expenses*Net Profit for the Period/Average Equity Capital* interest Income on Non-Performing Loans/Average T.Assets*

0.950.820.800.73

3.70 20.6 56.1 0,53

Factor 3;Liquid Asseis/F. Assets T. Liabilides/LAssels

0.89-0.75

1.95 10.3 67.0

Factor 4: Assets Quality and LiquidityFC Assests/FC Liabilities*FC Liquid Assets/FC Liabilities’

0.930.79

1.39 7.8 111 0.85

Factor 5: Assets Quality Non-Interest income/Non-Interest Expenses Long Term Assets/Total Assets’ Non-Performing Loans/Total Loans*

0.810.580.53

1.23 6.9 81.6 0.68

n=49 * Variable sets giving Cronbach Alpha values

In consequence, variables related to capital adequacy and liquidity structures constitute factor 1, which was the most important determinant of financial characteristics of banks in 1990.

Since factor 2 accounts for a smaller part of total variance in comparison with factor 1, it has less importance (Everit and Dunn, 1991). This factor is made up of four factors that are consistent with each other (alpha=0.53). The variables of the factor 2 represented bank profitability and income and expense position in income statements in 1990. As far as factor 3 is concerned, it accounts for 10.3% of total variance and indicates structure of bank assets. However, the variables determining factor 3 can not explain any financial characteristics of the banks because alpha values of these variables are below 0.50. Factor 4 accounts for 7.8% of total vari

Osman Karamustafa

ance and is determined by two variables with alpha values above 0.50. These variables indicate the resources obtained from foreign currencies are invested as foreign currency deposited as liquid assets. Considering that alpha values of these variables are 0.85, we can argue that factor 4 explains a financial characteristics of the bank's. This factor can be named after the variables as “assets quality and liquidity”. Regarding factor 5, it explains about 7% of the total variance and is determined by three variables with factor loading above 0.50. Nonetheless, these variables have alpha values of 0.12. When reliability analysis is repeated by excluding “Non-Interest Income / Non-Interest Expenses” variable, alpha values rose to 0.68. As we define this factor in terms of the other two variables, it can be seen that this factor determines assets quality of the banks.

The table 3.2 illustrates financial characteristics for 1991. The most important factor explaining basic financial characteristics is determined by 7 variables and accounts for 44.1 percent of total variance. Reliability of the variables with each other is 0.58 but if we exclude “Interest Income/Interest Expenses” variable from the factor group, alpha value goes up to 0.65. Hence, it is necessary not to include this variable in the model. Upon a closer examination, it can be seen that variables showing the most important financial characteristics of the banks in 1991 were those financial ratios related to capital adequacy.

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997) 7

Table 3.2: Factor Analysis Results for 1991

Factors 1991 (Varimax Rotation)

FactorLoading

Eigenvaiue Explained % Variance

Cumulative%

CroahAlpha

Factor 1: Capital Adequacy (Equity Capital + Profit) / (Deposit+Non-Deposit Resources)*Interest Income / Interest Expenses (Equity Capital+Profit)/ (T. Assets+Non-casb Credits)* Liquid Assets / (Deposit* Non-Deposit Resources)* (Equity Capital + Profit) / T. Assets *Net Working Capital /T, Assets *Net Interest Income on Non-Performing Loans/Average T. Assets’

0.950.940.920.910.890.84

0.73

7.93 44.1 4.1 0.65

Factor 2; Profitability & Income-Expense StructureNet Profit for the Period / Average Equity Capital*Total Income / Total Expenses*Net Profit for the Period / Average T. Assets

0.910.730.69

3.36 18.7 62.8 0.65

Factor 3;Liquid Assets / T. Assets T. Loans/T. Assets FC Liquid Assets / FC Liabilities Non-Perfonning Loans /T . Loans

0.84-0.830.800.53

1.85 ■ 10.3 73.1

Factor 4:Non-Interest income / Non-Interest ExpensesNon-Performing Loans / T. LoansLong Term Assets / T. AssetsFactor 5: Equity Capital ProfitabilityNet Profit for the Period / Average Paid-up Capital

0.81'0.640.62

1.22

1.06

6.8

5.9

79.9

85.8

n=50 * Variable sets giving Cronbach Alpha values

Factor 2 accounts for 18.7 percent of total variance and factor loading consists of 3 variables, which have alpha values of 0.60. If “Net Profit for the Period / Average Total Assets” is left out, alpha increases to 0.65. Thus, if we define this factor on the basis of “Net Profit for the Period/Average Equity Capital and “Total Income/Total Expenses variables, factor 2 represents profitability and income-expense structure of the banks.

Since alpha values of variables constituting factor 3 and factor 4 are below 0.50, we can suggest that the variables are grouped within these factors randomly. Therefore, factor 3 and factor 4 do not demonstrate any

Osman Karamustafa

financial dimension of the banks. Regarding factor 5 in the table 3.2, it only accounts for 5.9% of the total variance.

The analysis reveals 6 main factors for 1992 (see table 3.3). Nevertheless, factor 2 has an alpha value of 0.24, which means that it does not explain any financial characteristics of the? banks. Hence, the remaining five factors indicate basic financial characteristics.

Table 3.3: Factor Analysis Results for 1992

Factors {Varimax Rotation)

FactorLoading

Eigenvalue Explained%Varianct

Cumulative%

CroahAlpha

Factor 1: Capital Adequacy(Equity Capita! + Profit) / T. Assets*(Equity Capital+Profit)/(T. Assets +Non-Cash Credits)* Net Working Capital / T. Assets’(Equity Capital+Profit)/(Deposit+Non-Deposit Resources)

0.970.920.890.77

4.98 27.7 27.7 0.94

Factor 2:Total Income / Total ExpensesNet interest Income on Non-Performing loans/Average T. AssetsFC Assets / FC LiabilitiesLong Term Assets / T. AssetsInterest Income / Interest ExpenseNet Profit for the Period / Average T. Assets

0.77

0.67-0.60-0.600.570.55

3.20 17.8 45.5

Factor 3: Liquidity StructureFC Liquid Assets/ FC Liabilities T.Loans IT. Assets Liquid Assets/T. Assets*

0.91-0.810.78

2.37 13.2 58.7 0.70

Factor 4: Profitability of Equity Capital Net Profit for the Period / Average Equity Capital 0.84

1.50 8.4 67.1

Factor 5: Liquidity StructureLiquid Assets / (Dcposilf Non-Deposit Resources) 0.91

1.15 6.4 73.5

Factor 6: ProfitabilityNet Profit for the Period / Average Paid-up Capital 0.86

1.10 6.2 79.6

n—54 * Variable sets giving Cronbach Alpha values

Factor 1 is the most important principal component explaining 27.7% of total variance. Alpha values determining four variables of this factor are around 0.62. If “(Equity Capital+Profit)/(Deposits+Non-Deposit Resources)” variable is excluded, alpha values go up to 0.94. Taking all the remaining variables into consideration, this factor determines capital adequacy of the banks.

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997) 9

Factor 3 accounts for 13.2% of the total variance. If we do not include “Total Credits / Total Actives” variable in the model, alpha rises to 0.70. Hence, factor 3 is determined by “Liquid Assets/ Total Assets” and “FC Liquid Assets / FC Liabilities” and represents liquidity structure of the banks.

The last 3 factors for 1992 are affected by a variable. Thus, factor 4, factor 5 and factor 6 account for 8.4%, 6.4% and 6.2% of total variance and denote equity capital profitability, liquidity structure and bank profitability, respectively. We found four factors that explain 81 % of total variance for 1993 (see, table 3.4). Yet, since variables constituting factor 4 have low alpha values, they do not have any explanatory power.

Table 3.4: Factor Analysis Results for 1993

Factors (Varimax Rotation)

FactorLoading

Eigenvalue Explained%Variance

Cumulative%

CroahAlpha

Factor 1: Capital - Assets Quality (Equity Capital + Profit) / (T.Assets+Non-Cash Credits)* FC Assets / FC Liabilities'(Equity Capital + Profit) / TAssets*(Equity Capita 1+Pr ofit)/(Depos it+Non-Deposit Resources) FC Liquid Assets / FC Liabilities Interest Income / Interest Expenses Long Term Assets / T, Assets*

0.920.910.850.840.830,820.77

6.11 34.0 34.0 0.79

Factor 2; Profitability and Income- Expense Structure

Net Profit for the Period / Average Equity Capital* Net Profit for the Period / Avarage Paid-up Capital* Non-Interest Income / Non-interest Expense*Total Income / Total Expenses’Non-Performing Loans / T. Loans

0.810.80-0.750.68-0.60

5.07 28.2 62.2 0.85

Factor 3: Profitability and Income- Expense Structure

Net Working Capital / T. Assets Net Profit for the Period / Average T. Assets* Net interest Income on Non-Performing Loans/ Average T.Assets*

0.840.83

0.78

2.02 11.2 73.4 0.83

Factor 4:Total Loans / Total AssetsLiquid Assets / Total AssetsLiquid Assets / (Deposit+Non-Deposit Resources)

-0.830.810.57

1.32 7.4 80.8

n-55 * Variable sets giving Cronbach Alpha values

10 Osman Karamustafa

Factor 1 reveals the most important financial characteristics of banks as it accounts for a significant part of the total variance. Alpha values of the related variables are about 0.55. If “Interest Income / Interest Expenses” variable is left out, it increases to 0.79. Hence, variables related to capital adequacy and assets quality constitute the most important factor that explains basic financial characteristics of the banks in 1993. Factor 2 accounts for 28.2% of total variance. If “Non-Performing Loans/ Total Loans” variable is excluded, alpha value rises to 0.85. Factor 2 based on four variables in the above table denotes profitability of the banks. With regard to factor 3, if “Net Working Capital / Total Assets” variable is not included, alpha value goes up to 0.83. This factor accounts for 11.2 % percent of total variance and represents profitability of the banks.

For 1994, factor 3 and factor 5 are excluded from the analysis as alpha values of these factors are below 0.50. The remaining three factors determine financial characteristics of the banks (see table 3.5). Factor 1 describing profitability of banks and capital adequacy explains 40.7% of the total variance and is therefore the most important principle component.

Factor 2 accounts for 16.2% of the total variance. If we exclude “Liquid Assets / (Deposit+Non-Deposit Resources)” variable, alpha value increases to 0.53. As a result, this factor denotes profitability and income- expense structures of the banks. In addition, factor 4 defines liquidity structure of the banks and consists of (“Liquid Assets / Total Assets” and “FC Liquid Assets / FC Liabilities) variables with an alpha value of 0.76.

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997) 11

Table 3.5 : Factor Analysis Results for 1994Factors

(Varimax Rotation)Factor

LoadingEigenvalue Explained

^VarianceCumulative

%CroahAlpha

Factor 1: Profitability and Capital Adequacy Net Profit for the Period / Average Total Assets' Total Income / Total Expenses'Net Interest Income on Non-Performing Loans/ Average TAssets4Net Profit for the Period / Avarage Paid-up Capital Net Working Capital / T. Assets *(Equity Capital + Profit) / T. Assets*

0.920.83

0.830.800.670.61

7.32 40.7 40.7 0.72

Factor 2: Profitability&Income-Expense Structure(Equity Capital+Profit)/(Deposit+Non-Deposit Resources)* (Equity Capital + Profit)/(T. Assets+Non-Cash Credits)* Interest Income / interest Expenses*(Equity Capitai + Profit) / TAssets*Liquid Assets / (Deposit-i- Non-Deposit Resources)

0.810.780.730.690.53

2.91 16.2 56.9 0.53

Factor 3:Net Profit for the Period / Average Equity Capital Non-Performing Loans/T. Loans*Long Term Assets / T. Assets1

0.950.920.70

1.81 10.1 67.0

Factor 4: LiquidityLiquid Assets / Total Assets* Total Loans / Total Assets FC Liquid Assets/ FC Liabilities*

0.87-0.780.69

1.54 8.6 75.6 0.76

Factor 5:Non-Interest Income / Non-Interest Expense FC Assets/FC Liabilities (Equity Capital + Profit) / TAssets

0.900.83

1.44 8.0 83.6

n=55 * Variable -sets g iv in g Cronbach Alpha values

The tablé 3.6 illustrates that three factors determine financial characteristics of the banks for 1995. Alpha values of variables with (*) are around 0.93 and constitute factor 1. The high alpha value means that these variables are of considerable significance in defining this factor, which represents profitability and capital adequacy of the banks

Table 3.6: Factor Analysis Results for 1995

12 Osman Karamustafa

Factors (Varimax Rotation)

FactorLoading

Eigenvalue Explained % Variance

Cumulative%

CroahAlpha

Factor 1: Profitability and Capita! Adequacy Net Profit for the Period / Average Total Assets1 (Equity Capital + Profit) / (T.Assets+Non-Cash Credits)* (Equity Capital + Profit) / T,Assets*Net Profit for the Period / Avarage Paid-up Capital Net Working Capital / T. Assets*Net Interest Income on Non-Performing Loans/Average T. Assets*

0.850.840,760.760.75

0.68

7.12 39.6 39.6 0.93

Factor 2: Income-Expense Structure,Capital Adequacy and Liquidity

Interest Income / Interest Expense*(Equity Capital+Profit)/(Deposit+Non-Deposk Resources)* Liquid Assets / (Deposit+Non-Deposit Resources)’Total Income / Total Expenses*

0.930.860.700.63

2.93 16.3 55.9 0.53

Factor 3: Liquidity and Assets Quality Total Loans /Total Assets Liquid Assets / Total Assets*FC Liquid Assets / FC Liabilities* Non-Performing Loans /T. Loans’

-0.820.800.740.73

2.48 13.8 69.8 0.68

Factor 4:FC Assets / FC Liabilities Non-Interest Income / Non-Interest Expenses

0.880.75

1.25 7.0 76.7

FactorS:Net Profit for the Period / Average Equity Capital Long Term Assets j Total Assets

0.75-0.75

1.00 5.6 82.3

n=55 * Variable sets giving Cronbach Alpha values

Internal reliability of variables constituting factor 2 is 0.53. This factor explains 16.3% of total variance and defines capital adequacy and liquidity structure. “Liquid Assets/Total Liabilities” and “Non-Performing Loans / Total Loans” variables determine factor 3. It accounts for 13.8% of total variance and represents liquidity and assets structure of the banks. The first three factors in the table 3.7 represent basic financial characteristics of the banks in 1996. Factor 1 accounts for 33.6% of the total variance and is made up of capital adequacy and assets quality variables, which have an alpha value of 0.71.

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997) 13

Table 3.7: Factor Analysis Results for 1996Factors

(Varimax Rotation)Factor

LoadingEigenvalue Explained

%VarianaCumulative

%CroahAlpha

Factor 1: Capital Adequacy and Assets Quality (Equity Capital+Profit)/(Deposit+Non-Deposit Resources) (Equity Capital + Profit) / (T.Assets+Non-Cash Credits)* (Equity Capital + Profit) / T.Asscts'Interest Income / Interest Expenses Long Terra Assets / Total Assets*

0.940.900.890.860.73

6.04 33.6 33.6 0.71

Factor 2: Profitability&Income-Expense StructureNet Profit for the Period / Average Total Assets’Total Income / Total Expenses*Net Profit for the Period / Average Equity Capital*Net Working Capital / T. Assets

0.900.860.750.64

4.03 22.4 56.0 0.61

Factor 3: LiquidityLiquid Assets / Total Assets*Total Loans /Totai Assets FC Liquid Assets /F C Liabilities’Liquid Assets / (Deposit+Non-Deposit Resources)*

0.91-0.840.740.67

2.50 13.9 69.9 0.72

Factor 4:Non-Interest Income / Non-Interest Expenses FC Assets/FC Liabilities Net Interest Income on Non-Performing Loans/ Average T.Assets

0.930.79

-0.66

1.38 7.7 77.5

n=55 * Variable sets giving Cronbach Alpha values

Factor 2 is defined by four variables, which have factor loading above0.50. These variables explain a principal component provided that “Net Working Capital / Total Assets” variable is excluded from the model. Reliability coefficient of the other three variables is 0.61. Hence, factor 2 defines profitability and income-expense structure. Factor 3 represents Liquidity structure of the banks and explains 13.9 % of the total variance. It is determined by three variables with an alpha value of 0.72 (see, table 3.7).

Table 3.8 presents financial characteristics for 1997. Five principal independent components are determined on the basis of factor analysis. As a result of reliability test, the first three factors were found to determine basic financial characteristics of the banks in 1997. Alpha value of four variables constituting factor 1 is 0.67. This further demonstrates that these variables are consistent with each other. Compared to the other four

Osman Karamustafa.;

factors, this principal component accounts for the largest part of the total variance (33.5%) and is the most important financial characteristics of the banks. Considering factor loading, this factor can be called as “capital adequacy and assets quality” of banks.

Table 3.8: Factor Analysis Results for 1997

Factors (Varimax Rotation)

FactorLoading

Eigenvalue Explained%Variance

Cumulative%

CroahAlpha

Factor 1: Capital Adequacy and Assets Quality (Equity Capital+Profit)/(Deposit4-Non-Deposit Resources)’ (Equity Capital+Profit)/(T,Assets+Non-Cash Credits)* (Equity Capital + Profit/T,Assets’Long Term Assets / Total Assets’

0.930.920.910.73

6.03 33.5 33.5 0.67

Factor 2: Profitability, Capital Adequacy and Income-Expense Structure

Net Profit for the Period / Average Total Assets*Net Working Capital / T. Assets’Net Interest Income on Non-Performing Loans/ Average TAssets*Total Income / Total Expenses

0.860.82

0.640.60

3.66 20.4 53.9 0.84

Factor 3: LiquidityLiquid Assets / Total Assets*Total Loans/Total Assets FC Liquid Assets / FC Liabilities’

0.91-0.880.70

2.27 12.6 66.6 0.68

Factor 4:FC Assets / FC LiabilitiesNon-Interest Income/ Non-Interest ExpensesNet Profit for the Period / Avarage Paid-up Capital

0.920.91-0.61

1.92 10.7 77.2

Factor 5:Non-Performing Loans / Total Loans \ Net Profit for the Period / Average Equity Capital

-0.90 : o.73 :

1.35 ; 7.5 84.8 ;

n_55 * Variable sets giving Cronbach Alpha values

Since alpha value of the first three variables that constitute factor 2 is 0.84, these variables are important in defining this factor. Factor 2 accounts for 20.4 % of the total variance and defines profitability, capital adequacy and income-expense structure of the banks. Two variables (“Liquid Assets/Total Assets” and “FC Liquid Assets/FC Liabilities”) determine factor 3, which explains 10.7% of the total variance and describes liquidity structure of banks.

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997) 15

IV. Stability of Financial CharacteristicsWhether the ranking of the variables in terms of years are meaningful at the same significance level determines stability of financial characteristics of banks in a certain period. In this study, we determine whether the variables constituting the factors are in the same rank through the use of “Sperman Correlations”.

The table 4.1 shows if factor 1, which is the most significant financial characteristic, has a stable structure in the period of 1990-97. The variables determining factor 1 are in the same rank at a significance level of 0.05 or 0.01 except 1994. This reveals that the variables have a stable structure in the period under consideration except 1994. It can be argued that crisis in 1994 had negative effects on the stability of the financial characteristics of banks.

Table 4.1: Factor 1 Sperman Correlations

Factor 11991 ,8287**1992 ,7255** ,7007**1993 ,7957** ,5996** ,6429**1994 0,2755 ,5005* 0,4283 0,06091995 ,4716* ,6429** ,5542* 0,2074 ,8947**1996 ,9608** ,7792** ,7379** ,8473** 0,1827 0,37051997 ,8824** ,6842** ,6615** ,7317** 0,0361 0,2755 ,9422**

1990 1991 1992 1993 1994 1995 1996

* -Significance level,05 ** Significance level -,01 (2-tailed)

Factor 2 is composed of variables related to profitability and income- expense structures of banks. Variables associated with capital adequacy and liquidity structure have a considerable part in determining these factors in 1995 and 1997. The table 4.2 illustrates in which periods variables constituting factor 2 are stable at a statistically significant level.

Osman Karamustafa

Table 4.2: Factor 2 Sperman Correlations

Factor 21991 ,7709**1993 ,6140** ,6863**1994 -0,129 -0,16 -0,1331 ,y1995 0,257 0,2074 0,1558 ,8060**1996 ,7957** ,8885** ,6388** 0,063 0,44481997 ,7461** ,7069** ,5418* 0,2054 0,4365 ,8535**

1990 1991 1993 1994 1995 1996*- Significance level ,05 **- Significance level,01 (2-tailed)

In consequence, factors in 1994 and 1995 did not exhibit stability with the other factor variables. With the exception of these periods, all the factors are stable at a significance level of 0.05 or 0.01.

The table 4.3 presents whether variables of factor 3 have a stable structure in the periods under examination. The variables of this factor were stable at a signficance level of 0.05 in 1992, 1995 and 1996 and they were stable with each other at a significance level of 0.01 in 1995, 1996 and 1997.

Table 4.3: Factor 3 Sperman Correlations

Factor 31993 -0,3541995 ,5088* -0,15581996 ,4985* -0,1042 ,8906**1997 0,4303 0,1476 ,7461** ,8101**

1992 1993 1995 1996* - Significance level ,05 **- Significance level ,01 (2-tailed)

As can be seen in the table 4.4, factor 4 does not have a stable structure in the periods under consideration.

Table 4.4: Factor 4 Sperman Correlations

Factor <■1992 -0,34371994 0,3746 -0,1187

1990 1992 1994

* - Significance level i ,05 **- Significance level, 01 (2-tailed)

Basic Financial Characteristics in the Banking Sector:An Empirical Analysis (1990-1997) 17

Factor 5 only exhibits stability between 1990 and 1992 (see, table4.5)

Table 4.5: Factor 5 Sperman Correlations

Factor 51991 -0,12691992 -,7049** 0,1806

1990 1991 1992* - Significance level ,05 **- Significance level, 01 (2-tailed)

V. Concluding RemarksThis paper offers an analysis of how financial characteristics of commercial banks operating in Turkish financial system developed between 1990- 1997. The results of the study can be summarised as follows:

Variables describing the most important financial characteristics of the banks are generally those connected with capital adequacy of the banks. In addition, variables related to profitability determined factor 1 in 1994 and 1995. Considering that the system was in crisis in both years, it can be pointed out that periods in which capital adequacy is not the most important financial characteristic indicate a crisis in the banking system. Capital adequacy became the most crucial characteristics of the banks together with variables representing assets quality of the banks in 1996 and 1997.

The first three factors are the most significant factors determining financial characteristics because they account for a greater part of total variance. Variables related to capital adequacy exhibit stability year by year. This structure loses its stability relatively as the significance of the factors decreases. During the 1994 crisis, stable structures among the variables determining financial characteristics collapsed.

Although equity capital comprises a small part within total liabilities, its function as creating trust between depositors, other organizations and banks, reducing losses and being a fund resource for banks demonstrates the indispensability of capital adequacy for banks. Variables revealing capital structures of banks are more important than the other financial variables for interest groups in their decision-making process.

Osman Karamustafa

ReferencesA L T M A N , E d w a rd I ., “ F in a n c ia l R a tio s , D is c r im in a n t A n a ly s is o f th e P r e d ic t io n o f

C o rp o ra te B a n k ru p tc y ” , J o u rn a l o f F in a n c e , 2 3 , p p 5 8 9 -6 0 9 , S e p te m b e r 1 9 6 8 .A K T A Ş , R a m a z a n , “ E n d ü s tr i İ ş le tm e le r i iç in M a l i B a ş a r ıs ız l ık T a h m in i (Ç o k

B o y u tlu M o d e l U y g u la m a s ı) ” , T ü r k iy e İş B a n k a s ı K ü l tü r Y a y ın la r ı N o :3 2 3 , A n k a ra , 1 9 9 3 . .5

B A N K A L A R IM IZ 19 9 7 , T ü rk iy e B a n k a la r B ir l iğ i , M a y ıs 1998 .B E A V E R , W ill ia m H ., “ F in a n c ia l R a tio s a s P re d ic to r s o f F a i lu r e ” E m p ir ic a l R e s e a rc h

in A c c o u n t in g ” S e le c te d S tu d ie s , V o l.4 , p p 7 1 -1 1 1 , 1966 .D İ N C E , R .R ., C . F O R T S O N , “ T h e U s e o f D i s c i r im in a n t A n a ly s is to P r e d ic t th e

C a p i ta l A d e q u a c y o f C o m m e rc ia l B a n k s ” , J o u rn a l o f B a n k R e s e a rc h , p p 5 4 - 6 2 , S p r in g , 1 9 7 2 .

E D M I S T E R , R o b e r t O ., “ A n E m p ir ic a l T e s t o f F in a n c ia l R a t io A n a ly s is fo r S m a ll B u s in e s s F a i lu re P re d ic t io n ” , J o u rn a l o f F in a n c ia l a n d Q u a n ti ta t iv e A n a ly s i s ” , p p 1 9 7 7 -9 3 , M a rc h 1972 .

E V E R 1 T T , B .S . a n d D U N N , G ., A p p l ie d M u l t iv a r ia te D a ta A n a ly s is , L o n d o n : E d w a r d A rn o ld , 1991 .

G O M B O L A , M ic h a e l J ., J. E d w a rd K E T Z , “ F in a n c ia l R a t io P a t te rn s in R e ta i l a n d M a n u f a c tu r in g O r g a n iz a t io n s ” ,F in a n c ia l M a n a g e m e n t , p p 4 5 -5 6 , S u m m e r , 1983 .

G Ö K T A N , E rk u t , “ M u h a s e b e O ra n la r ı Y a rd ım ıy la v e D is k r im in a n t A naliz ; T e k n iğ in i K u l la n a ra k E n d ü s tr i İ ş le tm e le r in in M a l i B a ş a r ıs ız l ığ ın ın T a h m in i Ü z e r in d e A m p ir ik B ir A r a ş t ı r m a ” , B a s ı lm a m ış D o ç e n t l ik T e z i, 1 9 8 1 .

H A IR , Jr. J o s e p h , R o lp h e E . A N D E R S O N , R o n a ld L . T A T H A M , W il l ia m C . B L A C K , “ M u ltiv a r ia te D a ta A n a ly s is W ith R e a d in g s ” , 5 .B a s k ı, P re n t ic e - H a ll , ın c , U S A , 1 9 9 8 .

H O R R IG A N , J a m e s O ., “ A S h o r t H is to ry o f F in a n n c İa l R a tio A n a ly s i s ” T h e A c c o u n t in g R e v ie w , 4 3 , p p 2 8 4 -2 9 4 . , 1 9 6 8 .

J A C K E N D O F F , N a th a n ia l , “ A S tu d y o f P u b li s h e d I n d u s t r y F in a n c ia l a n d O p e ra t in g R a t io s ” , S m a ll B u s in e s s M a n a g e m e n t R e s e a rc h R e p o r t , U S A , T e m p le U n i, , 196 2 .

L A U R E N T , C .R ., “ I m p ro v in g T h e E f f ic ie n c y a n d E f f e c t iv e n e s s o f F in a n c ia a l R a tio A n a ly s i s ” , J o u rn a l o f B u s in e s s F in a n c e & A c c o u n t in g , 6 ,3 , p p 4 0 1 -1 3 , 1 9 7 9 .

M A R T IK A IN E N , T e p p o , “ S to c k R e tu rn s a n d C la s s if ic a t io n P a t te rn o f F i r m - S p e c if ic F in a n c ia l V a ria b le s : E m p ir ic a l E v id e n c e W ith F in n is h D a ta ” , J o u rn a l o f B u s in e s s F in a n c e & A c c o u n t in g , 2 0 (4 ) , p p 5 3 7 - 5 5 7 , J u n e 1993 .

M A R T IN , A lv in , “ A n E m p ir ic a l T e s t o f th e R e le v a n c e o f A c c o u n t in g In f o rm a t io n fo r I n v e s tm e n t D e c i s io n s ” , J o u r n a l o f A c c o u n t i n g R e s e a r c h , p p 1 -3 1 , S u p p le m e n t , 197 1 .

M E Y E R , P a u l A ., H o w a rd W . P IF E R , “ P re d ic t io n o f B a n k F a i lu r e s ” , J o u rn a l o f F in a n c e , p p 8 5 3 -6 3 , S e p te m b e r , 1 9 7 0 .

N O R U S IS , M a r i ja J . , “ S P S S fo r W in d o w s P r o fe s s io n a l S ta t is t ic s - R e le a s e 6 .0 ” , S P S S In c , C h ic a g o , U S A , 1 9 9 3 .

P E T T W A Y , R .H ., J.F . S IN K E Y , “ E s ta b l i s h in g O n - S i te B a n k E x a m in a t io n P r io r i ty :A n E a r ly W a rn in g S y s te m U s in g A c c o u n t in g a n d M a r k e t I n f o rm a t io n ” , J o u rn a l o f F in a n c e , p p 1 3 7 -5 0 , M a r c h 1980 .

P IN C H E S , G e o rg e E „ K e n t A . M IN G O , J .K e n t, C A R U T H E R S , “ T h e S ta b i l i ty o f P a t te rn s in In d u s t r ia l O r g a n iz a t io n s ” , T h e J o u rn a l o f F in a n c e , Vo 1:28, N o :3 , p p 3 8 9 -9 6 , 1973 .

Basic Financial Characleristics in the Banking Seclor:An Empirical Analysis (1990-1997) 19

P IN C H E S , G e o rg e E ., K e n t A . M IN G O , “ A M u lt iv a r ia te A n a ly s is o f I n d u s t r ia l B o n d R a t in g s ” , J o u rn a l o f F in a n c e , 2 8 , p p 1 -1 8 , M a rc h 1973 .

S IN K E Y , J .F ., “ A M u l t iv a r ia te S ta t is t ic a l A n a ly s is o f th e C h a ra c te r is t ic s o f P ro b le m B a n k s ” , J o u r n a l o f F in a n c e , p p 2 1 -3 6 , M a rc h , 1975 .

O ’C O N N O R , M e lv in C . “ O n th e U s e fu ln e s s o f F in a n c ia l R a t io s to In v e s to r s in C o m m o n S to c k ” , T h e A c c o u n t in g R e v ie w , p p 3 3 9 -3 5 2 , A p r i l 197 3 .

The ISE Review Volume: 3 No: 9 January/February/March 1999 ISSN 1301-1642 © ISE 1997

LEADING INDICATORS APPROACH FOR BUSINESS CYCLE FORECASTING AND

A STUDY ON DEVELOPING A LEADING ECONOMIC INDICATORS INDEX FOR THE

TURKISH ECONOMY

Ali MÜRÜTOĞLU*

AbstractB u s in e s s c y c le s , o n e o f th e m a in c h a ra c te r is t ic s o f d e v e lo p e d c o u n t r i e s ’ e c o n o m ie s , h a v e b e g u n to p la y a n im p o r ta n t r o le fo r th e T u rk is h E c o n o m y . E s p e c ia l ly a f te r th e 1 9 9 4 c r is is (w h ic h w a s o n e o f th e m o s t s e v e re o n e s in c e th e f o u n d a tio n o f T u rk is h R e p u b l ic ) a n d th e c u r r e n t s lo w -d o w n o f th e e c o n o m y ( m a in ly b e c a u s e o f th e g lo b a l c r is is w h ic h s te m m e d f ro m th e s o u th -e a s t A s ia n c o u n tr ie s a n d R u s s ia ) , i t h a s b e c o m e v i ta l to fo r e s e e th e fu tu re o f th e e c o n o m y (i .e . w h ic h p h a s e th e e c o n o m y w il l b e in th e b u s in e s s c y c le in th e fu tu re ) fo r th e d e c is io n m a k e r s b o th in p u b l ic a n d p r iv a te s e c to rs . T h u s , i t c a n b e p o s s ib le to ta k e c o n t r a r y a c t io n s to r e d u c e th e h a r m f u l e f fe c ts o f r e c e s s io n s .

O n e m e th o d o f s h o r t - te r m fo r e c a s t in g o f e c o n o m ic c o n d i t io n is th e L e a d in g E c o n o m ic I n d ic a to r s A p p r o a c h w h ic h is th e s u b je c t o f th is s tu d y . In th is s tu d y , a f te r e x p la in in g b u s in e s s c y c le s a n d L e a d in g E c o n o m ic In d ic a to rs A p p r o a c h to fo r e c a s t th e b u s in e s s c y c le s , I a n a ly z e n e a r ly 5 0 e c o n o m ic t im e s e r ie s to f in d a L e a d in g E c o n o m ic In d ic a to r s In d e x fo r th e T u rk is h e c o n o m y .T h e r e s u l t in g in d e x is c o m p r is e d o f n in e e c o n o m ic s e r ie s w h ic h a r e s ta n d a r d iz e d a n d c o m p o s e d w i th e q u a l w e ig h t to fo r m “ T h e L e a d in g In d ic a to rs In d e x f o r th e T u rk is h E c o n o m y ” . T h e s e r ie s a re a s fo llo w s ; T o ta l I m p o r t o f I n v e s tm e n t G o o d s , T o ta l I m p o r t o f In te r m e d ia te G o o d s , C u rre n c y , M 2 , R e s e r v e M o n e y , D e p o s i t M o n e y B a n k s ’ C r e d i t s , N e t C r e d i t V o lu m e , C o n s o l id a te d B u d g e t M o n t h ly E x p e n d i tu r e s , T o ta l C a p i t a l o f N e w ly E s ta b l is h e d F irm s .

L introductionGenerally, two kinds of movements can be observed in the economies of the countries with free market economic system. These movements are

* Floor Specialist in the Bonds and Bills Department at the Istanbul Stock Exchange Address: IMKB Tahvil ve Bono Piyasası 80860 Istinye, Istanbul, Phone: 0-212-2982578, e-mail: amurut@lycoserriailcom)The view and opinions expressed here are those of the author and do not reflect those of îhe ISE.

22 Ali Miiriitoglu

the long-run growth (or decline) and short-run fluctuations. Long-run growth (or decline) can be defined as the trend observed in the general economic indicators (such as GNP, employment, industrial production, investment etc) in the long run. On the other hand, short-term fluctuations are the changes of the economic variables (0NP, industrial production, employment, interest rates etc) around this long-run trend. The fluctuations show a cyclical characteristic and are called business cycles.

In recent years, business cycles have become important for Turkey in parallel with the efforts for transforming its economy from planned to free-market economy. As a result, forecasting business cycles has become a necessity for the Turkish economy.

Various kinds of methods have been used in the short-run forecasting of economic activity. These methods vary from the qualitative types, based mainly on the experience and knowledge of the forecaster, to the quantitative methods (e.g., econometric models which are very complicated and based on the cause and effect relationship in the economy). Leading Economic Indicators Approach, one of the types of these methods, is the topic of this paper.

In this study, after providing brief information about business cycles, leading indicators are considered in detail. After examining the leading indicators approach in the world and Turkey, a “Leading Economic Index for the Turkish Economy” is developed in the last section.

II. Business CyclesSeveral definitions of business cycles have been proposed in the literature so far. Among these, the definition proposed by Arthur F. Burns and Mitchell C. Wesley (1946) is the most comprehensive and widely accepted. According to this definition, business cycles are types of fluctuations found in the aggregate economic activity of nations that organize their work mainly in the business enterprise. A cycle consists of expansions occurring at about the same time in many economic activities, followed by similarly general recessions, contractions and revivals which merge into the expansion phase of the next cycle. This sequence of changes is recurrent but not periodic; the time span of business cycles vary from more than one year to ten or twelve years. They are not divisible into shorter cycle of , similar character with amplitudes approximately their own.

On the other hand, some authors claim business cycles of 50-60

Leading Indicators Approach for Business Cylcle Forecasting and a Study onDeveloping a Leading Economic Indicators Index for the Turkish Economy 23

years in length. Especially Kontradief and Schumpeter (1939) argue that business cycles cover 50-60 years period and do not only reflect economic changes but also social changes. However, this definition does not have many advocates.

Business cycles can be divided into two periods. The period that starts from the beginning trough to the end of the peak of the cycle is called the expansion period, from the peak to the ending trough is called the contraction period. Expansion period is further divided into two phases. From the beginning trough to the half of the expansion period is called the recovery phase, from the end of the recovery phase to the peak is called the prosperity phase. Also the contraction period is divided into two phases. The phase that starts from the peak and ends at the middle of the contraction period is called the crisis phase. In this phase, the economic activity declines sharply. The phase from the middle of the contraction period to the next trough is called the recession phase. If the recession phase is long and deep it is called the depression.

III. Leading Indicators ApproachLeading indicators approach assume that economic fluctuations are inevitable. In a certain business cycle, all economic time series do not

Ali Miiriitoglu

move with the general economic condition. Some of them move before, some of them move at the same time while some others follow the general economic condition with a lag. Economic series which move before the general economic condition are called leading series, series that move with the general economic condition are called coinciding series and series that follow the general economic condition with a lag are called the lagging series. Leading indicators approach is based on determining the leading series and using them to forecast the condition of the economy in the near future.

Most of the leading series reflect the future plans about economic activities, decisions about the future and contracts that are related to the future. Economic series like new orders for goods and services, new constructions, activities in the intermediate goods industry, prices of raw materials and intermediate goods, etc. have the potential to show the direction of the future economic activity.

Although the leading indicators approach is an easy and practical way for forecasting economy’s future, it has some drawbacks; firstly, there are limited numbers of economic series that reflect the economic condition regularly. Even the best leading indicator provides forecast correctly at 80-90 per cent of the time. Secondly, the lead time of leading indicators is not stable, it changes with time. Lastly, even if we suppose that the leading indicators forecast the economic condition correctly, both with respect to time and direction, they cannot show the magnitude of the change in economic activity.

IV. Leading Indicators Approach in USA and Europe

A. Leading Indicators Approach in USAIn USA, currently 112 economic indicators are monitored continuously. They are updated when necessary. From these indicators, 61 of them are classified as leading, 24 of them are classified as coinciding and 19 of them are classified as lagging indicators. Remaining 8 indicators can not be classified. These indicators represent 7 different sectors of the economy. These sectors are:

1. Labor and Unemployment,2. Production and Income,3. Consumption, Trade and Sales,4. Fixed Income Investments,

5. Stocks,6. Prices, Costs and Profit7. Money and Credit.

U.S. Department of Commerce, Bureau of Economic Analysis has done studies related to these kind of economic indicators. Findings are published in the monthly periodical Business Conditions Digest. Leading Indicator Index for the US economy is also published in this periodical. There are 11 leading, 4 coinciding and 7 lagging economic indicators stated in Business Conditions Digest. Components of Leading Economic Index of the US economy are follows:1. Average workweek, production workers, manufacturing2. Layoff rate, manufacturing3. Net orders for consumer goods and materials, 1972 dollars4. New building permits, private housing5. Vendor performance, percent of companies receiving slower delivery6. Performance in the sales and deliveries7. Changes in sales prices of important materials8. Consumer expectations index9. Money supply, M2, 1972 dollars10. Contracts and orders for plant and equipment, 1972 dollars11. Stock prices, 500 common stock

Currently in USA, there are some studies for dividing leading indicators into short leading and long leading indicators and changing some of the economic series. The main objective of these studies is to form a Leading Index that reflects the services sector and international economic developments.

B. Leading Indicators for OECD Countries:OECD has been carrying out various studies about leading indicators in the member country’s economy. The OECD indicator system use of Index of Total Industrial Production as the reference series. OECD has been monitoring approximately 190 economic series from 8 main sectors of the economies’ of member countries. Some of these series cannot be monitored for all member countries. The different subject areas from which the leading indicator series are chosen are set out in Table 1.

Leading Indicators Approach for Business Cyicle Forecasting and a Study onpeveloping a Leading Economic Indicators Index for the Turkish Economy 25

Ali Mürütoglu

Table 1: Leading Indicators Used in OECD System

COUNTRIES

I. PRODUCTION, STOCKS AND ORDERS1. Industrial Productions in Specific Branches2. Oalers3. Stocks- Materials- Finished Goods- Imported Products

4. Ratios, e.g. inventory/shipment

I 2 3 4 5 6 7 8 y ¡0 ¡1 12 13 14 15 16 17 18 Î9 20 21 22 23

11

1

1

1

1) 1

1

121

21

1 54

24I1

II. CONSTRUCTION, SALES AND TRADES1. Constructions Approvals2. Construction Starts3. Sales or Registrations of Motor Vehicles4. Retail sales

11

1 I 11111

1

1

1 1 1

1

11

11

3655

HI. LABOUR FORCE1. Ratio, New Employment/Employment2. Layoffs/Initial claims, Unemployment Insurance3. Vacancies4. Hours Worked 1

1

1

1I

1

12 1 2

IV. PRICES, COSTS AND PROFITS1. Wages and Salaries Per Unil of Output2. Price Indices3. Profits

11 1

i2 1 I

1

2

362

V. MONETARY AND FINANCIAL1. Forcing Exchange Holdings2. Deposits3. Credit4. Ratios, e.g. Loans/Deposits5. Money Supply6. Interest Rates7. Slock Prices8. Company Formation

1

1

1

!111

11!11

1

1

1 11I

11

2

1 131

111

I

I 111

11

1

13

1

111

111

1

11

1

2241171412I

VI. FOREIGN TRADE1. Export Aggregates2. Export Components3. Trade Bilance4. Terms of Trade

11 1 1

2

1 1 1 1

1

1

12 16

V II. BUSINESS SURVEYS1. General Situation2. Production3. Orders inflow/New Orders4. Ordersbook/Sales5. Stock of Raw Materials .6. Stock of Finished Goods7. Capacity Utilization8. Bottlenecks9. Employment10. Prices

11

!

1

1

1II

1

1

1

11

i

I

1

121

1

11

1

I

11

1

I11 1

1

1

1

1

I

111

1

I11 1

11

1

2

21

1111

1i

1

1

111

6151!113102231

V III. ECONOMIC ACTIVITY IN FOREIGN COUNTRIES 1 5 2 1 9INDICATORS 12 9 11 8 f) 7 9 1Ü u 9 2 9 9 7 11 it 6 7 12 7 10 4 189

Source: Nilsson, Ronny, “Leading Indicators for OECD, Centra! and Eastern European Countries” in is the Economic Cycle Still Alive; Theory, Evidence and Policy edited by Mario Baldassari and Paulo Annunziato, St. Martin Press Inc. New York, 1994.

COUNTRIES1. Canada 7. Denmark 13. Ireland 19. Sweden2. USA 8. Finland i4. Italy 20. Switzerland3. Japan 9. France 15. Netherlands 21.UK4. Australia 10. Germany 16. Norway 22. Yugoslavia5. Austria 11. Luxembourg 17. Portugal 23. All Countries6. Belgium 12. Greece 18. Spain

Leading Indicators Approach for Business Cylcle Forecasting and a Study onDeveloping a Leading Economic Indicators Index for the Turkish Economy 2.7

V, Studies on Leading Economic Indicators in TurkeyStudies on leading indicators in Turkey are still in its infancy. One reason for this is the argument that claim; Turkish economy is still at the beginning of the free market economy and business cycles which are characteristics of the capitalist economies are as not as important as they are for the developing countries. One other factor that prevent studies on leading indicators approach in Turkey is that until recent times, economic time series have not been published regularly so it is difficult to find reliable economic data in the past period.

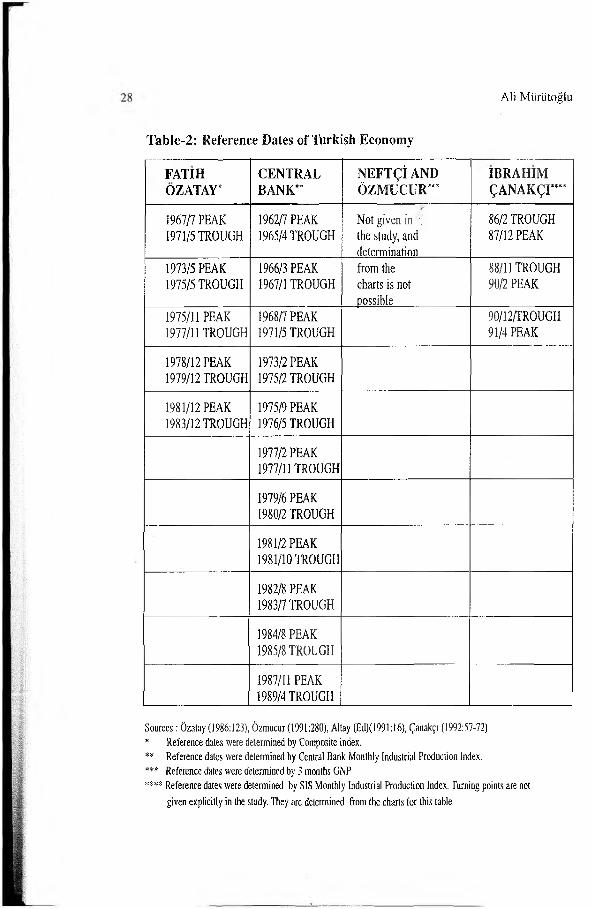

The first study on leading indicators in Turkey was made by Fatih Özatay. Özatay(1986), while searching business cycles in the Turkish economy, constructed a reference series and a leading economic indicators index for the Turkish economy. The second study on this subject was undertaken by Neftçi and Özmucur. In this study, Neftçi and Özmucur (1991) formed an Economic Condition Index (ECI) and a Leading Indicators Index (LII). They also calculated probabilities for the turning points of the cycle. Third study was made by a team within the Central Bank of the Republic of Türkiye (Altay et al., 1991). The last study about the issue was made by Çanakçı (1992). In this study, he analyzed 50 economic series from different sectors of the economy and showed that it is possible to find leading indicators for the Turkish economy. Reference dates (turning points of the cycles) of the Turkish Economy found by above studies are shown in Table-2.

Aîi Mürütoğiu

Table-2: Reference Dates of Turkish Economy

FATIHOZATAY*

CENTRALBANK**

NEFTÇİANDÖZMUCUR***

IBRAHIMÇANAKÇI”**

1967/7 PEAK 1971/5 TROUGH

1962/7 PEAK 1965/4 TROUGH

Not given in •; the study, and determination

86/2 TROUGH 87/12 PEAK

1973/5 PEAK 1975/5 TROUGH

1966/3 PEAK 1967/1 TROUGH

from the charts is not possible

88/11 TROUGH 90/2 PEAK

1975/11 PEAK 1977/11 TROUGH

1968/7 PEAK 1971/5 TROUGH

90/12/TROUGH 91/4 PEAK

1978/12 PEAK 1979/12 TROUGH

1973/2 PEAK 1975/2 TROUGH

1981/12 PEAK 1983/12 TROUGH

1975/9 PEAK 1976/5 TROUGH

1977/2 PEAK 1977/11 TROUGH

1979/6 PEAK 1980/2 TROUGH

1981/2 PEAK 1981/10 TROUGH

1982/8 PEAK 1983/7 TROUGH

1984/8 PEAK 1985/8 TROUGH

1987/11 PEAK 1989/4 TROUGH

Sources: Özatay (1986:123), Özmucur (1991:280), Allay (Ed)(1991:16), Çanakçı (1992:57-72)* Reference dates were deteimined by Composite index.** Reference dates were determined by Central Bank Monthly Industrial Production Index.*** Reference dates were determined by 3 months GNP**** Reference dates were determined by SIS Monthly Industrial Production Index. Turning points are not

given explicitly in the study. They are determined from the charts for this table

v Leading Indicators Approach for Business Cylcle Forecasting and a Study on ̂ Developing a Leading Economic Indicators Index for the Turkish Economy 29

VI. A Study on Developing a Leading Economic Indicators Index for the Turkish EconomyStudies on developing leading indicators indices for the Turkish economy and the results of these studies were mentioned above. Economic series used as leading indicators should always be monitored and updated if necessary. Especially for the countries like Turkey that experiences a rapid and continuous change in its economic structure, such updates become vital. Thinking from this point of view, new leading indicators index for the Turkish Economy is developed in this section. The methodology and findings of this study are explained below:

A. Period of the Study and Definition of the Business CycleIn this study, business cycles are defined as deviations from the long run trend of the economy. Data used in this study compromises a 116 months’ time period from January 1989 to August 1998.

B. Reference SeriesWhen developing a leading indicator index, the first step is to define the reference series (cycle) and find the turning points of this series. In this study SIS (State Institute of Statistics) Monthly Industrial Production Index is used as the reference series. This index is calculated using production data of 112 basic industrial goods which compromise nearly 60% of the total industrial production. It is also calculated separately for mining, manufacturing, electricity, gas and water subsectors of the industry.

The main reason for selecting the SIS Monthly Industrial Production Index as the reference series is the assumption that fluctuations in the Turkish economy mainly reflected in the industrial sector constitutes an important part of the economy. Furthermore, the results of macro economic policy can easily be seen in the industrial sector.

C. Candidate Series for Leading Indicators IndexNearly 50 economic series from different parts of the economy are analyzed in order to develop the Leading Indicators Index.

Regarding the increasing importance of the monetary aggregate figures for the Turkish economy after 1990, series related with money and credit side of the economy are analyzed extensively. Building activities are treated as an indicator of the economic revival and series relating to the building activities, both with respect to building and occupancy permits, are taken into consideration. The number as well as capital amount

30 Ali Miirlitoglu

of newly established companies are closely related with the expectation about the economy’s future. Imports of capital goods and raw materials, in particular, are important for reflecting the future production plans of the firms. Lastly, government expenditures can be cause for a recession or revival by affecting the economy as a whole. ?

D. Decomposition of Time SeriesA time series is composed of trend, seasonal fluctuations, cycle and irregular components. Trend (T) is the long-run increase or decrease persistent in the series. Most time series show an increasing trend in the long-run. Seasonal fluctuations can be defined as movements in the series due to seasonal effects such as changes in the climate, in customs related to the year or to holidays. Irregular component (I) is the random movement that can be seen in the series. Irregular components are caused by unusual events such as war, strike, extremely adverse weather conditions etc.

These components can be combined together using two different ways depending on the characteristic of the increase in values of the series. If the value of increase in the series in the course of time is constant, the additive form is used. Accordingly, in a given time (t), the series Y(t) is expressed as follows;

Y(t) = T(t) + S(t) + C(t) + I(t)

If the increase in series is not constant but it is in proportion with the value of the series in the course of time, in other words, if the increase in the value of the series depends on the series own value, then multiplicative form is used. Accordingly, in a given time (t), the series Y(t) is expressed as follows;

Y(t) = T(t) x S(t) x C(t) x I(t)

Since the increase in economic series in the course of time is related with the series own magnitude, the multiplicative form should be used in the economic series analysis.

After defining economic time series in multiplicative form, each cycle component of the series is determined. In order to do this, other components (trend, seasonal, irregular) of the series are determined and the series is clarified from these components.

In this study, centered moving average (or seasonal index) method is

Leading Indicators Approach for Business Cylcle Forecasting and a Study onDeveloping a Leading Economic Indicators Index for the Turkish Economy 31

used to eliminate the seasonal effects from the series. In this method, firstly, 12-month moving averages are calculated using the monthly data. Secondly, 2-months moving averages are calculated from these averages and seasonal indexes are found for each month. Finally, monthly values of original series are divided into seasonal indices for that particular month. The resulting new series is eliminated from the seasonal component and includes only trend, cycle and irregular factors.

The least square (regression) method is used for eliminating trend components from the series. Since proportional increases are important for most economic series, a semi-logarithmic trend equation is used in the regression analysis. This equation can be expressed as:

Ln Y(t) = a + b(t) + u

Here, Y(t) shows the trend component of the series, a is the constant, t is time and u is the error term. For each series, a and b coefficients are determined using the regression analysis. Subsequently, series without seasonal components is divided by series which is calculated using the above equation in order to find the series which is eliminated from seasonal and trend factors.

The new series is eliminated from the seasonal and trend factors and only includes cycle and irregular components. 3-month moving averages are calculated in order to eliminate the irregular components. After this, the resulting series only include the cycle component. The series is standardized by subtracting each month’s value from the average of the series and divided by its standard deviation. The reason for this standardization is to make possible to the comparison of two series with different units.

E. Determining the Turning Points of the SeriesTurning points in the reference series determined by using the above methods are given in Chart 2:

32 Ali Miiriitoglu

Chart 2: SIS Monthly Industrial Production Index (Standard Values)

In the time period between January 1989-August 1998, three completed and one incomplete cycles are determined. The average length of 3 cycles is calculated as 27.4 months. Dates of the turning point in the reference series are given in Table 3:

Table 3: Dates of Turning Points for the Turkish Economy

CYCLE BEGINNINGTROUGH

PEAK TERM INALTROUGH

I 06/89 10/90 07/91II 07/91 12/93 06/94III 06/94 07/95 03/96IV 03/96 07/97 ?

F. Determining the Leading IndicatorsIn order to find leading indicators, turning points and cross correlation analyses of all series with respect to reference series are completed. In the turning point analysis, the leading time (in months) of turning points of candidate series turning points with respect to turning points of reference series are calculated. The average leading time of candidate series throughout the whole cycle is also taken into account. In order to be used as a leading indicator, the leading time of economic series should not vary

Leading Indicators Approach for Business Cylcle Forecasting and a Study onDeveloping a Leading Economic Indicators Index for the Turkish Economy 33

significantly while the number of cycles (turning points) in the candidate series must be equal to the number of cycles in the reference series.

For cross correlation analysis, correlation coefficients between the reference series and one, two, three...ten months lagging values of the candidate series are calculated. When determining leading indicators, series whose two, three or more months lagging values have a high correlation coefficient between the reference cycle values are selected.

Following the above analyses, nine economic series are selected as leading indicators. These series are as follows:1. Total Import of Investment Goods, in million dollar2. Total Import of Intermediate Goods, in million dollar3. Currency (in 1987 prices), billion TL4. M2 (in 1987 prices), billion TL5. Reserve Money (in 1987 prices), billion TL6. Deposit Money Banks Credits (in 1987 prices), billion TL7. Net Credit Volume (in 1987 prices), billion TL8. Consolidated Budget Monthly Expenditures (in 1987 prices), billion TL9. Total Capital of Newly Established Firms (in 1987 prices), billion TL

Leading indicators found in this study are in harmony with the finding of the previous studies. Consolidated Budget Monthly Expenditures and M2 were also taken into consideration in the TUSIAD Leading Indicators Index. Imports Volume and Total Imports of Investment Goods are in accord with the study concluded by the Central Bank. Consolidated Budget Monthly Expenditures, Net Credit Volume, Total Import of Investment Goods and M2 were also determined as leading indicators by Çanakçı.

G. Constituting the Index:The Leading Indicators Index is obtained by giving equal weight to the standard values of the above leading indicator series and adding them. In the analyzed period three completed cycle are determined as shown in Table 4.

34 Ali Miirütoglu

Table 4: Turning Points of Leading Indicators Index

CYCLE BEGINNINGTROUGH

PEAK TERMINALTROUGH

I 06/89 07/90 05/91II 05/91 04/93 05/94III 05/94 04/96 10/96IV 10/96 7

Following the analysis of turning points it can be said that the leading indicators index led the reference series very successfully until June 1994, but after this point, the leading power of the index has decreased slightly. However, the turning point analysis by itself is not enough to judge about the power of the leading indicators index. The relationship between the reference series and the index throughout the whole period must be also taken into account. For this purpose, both the Industrial Production Index and the Leading Indicators Index are given in Chart 3.

Chart 3 : Monthly Industrial Production and Leading Indicators Index (Standard Values)

2,00 1,50 1,00 0,50

. 0,00 - 0,50 - 1,00 ••1,50 - 2,00 - 2,50 - 3,00 - 3,50

As it can be observed from the chart, the leading indicators index is(other than a few exceptions) successful in leading the reference series.

SiS MONHTHI.Y INDUSTRIAL PRODUCTION ------ LEADING INDICATOR INDEX

H. Using the Leading Indicators Index in ForecastingThe leading indicators index is now ready for short-term forecasting of the economic activity. There are various methods for using leading indicators index in the short-mn forecasting of economic activity.1 But none of these methods give the correct forecast all the time. In addition, these methods should be considered as completing rather than competing and more than one method must be used to make the forecast more reliable.

Lastly, it must be stated that the result of the forecast of the leading indicator index should be used carefully. When making the final decision, the results of other methods should also be considered. As a fact, all methods of forecasting are only decision tools and findings of these methods should be combined with the insights and experiences of the forecaster.

VII. Summary and ConclusionIn this study, monthly data of nearly 50 economic series from different sectors are analyzed in this study in the time period between January 1989- August 1998 and 9 economic series are determined as leading indicators for the Turkish economy. These series are used to develop a Leading Indicators Index for the Turkish economy which can be used for forecasting the turning points of industrial production. In the period of analysis, three complete and one incomplete cycles are determined in the Industrial Production Index. Accordingly, June 1989, Julyl991, Junel994 and March/1996 are determined as trough dates and October 1990, December 1993, July 1995 and July 1997 are determined as peak dates of these cycles.

The leading economic series that formed the Leading Indicators Index are as follows:I. Total Import of Investment Goods, in million dollar2. Total Import of Intermediate Goods, in million dollar3. Currency (in 1987 prices), billion TL4. M2 (in 1987 prices), billion TL5. Reserve Money (in 1987 prices), billion TL6. Deposit Money Banks Credits (in 1987 prices), billion TL7. Net Credit Volume (in 1987 prices), billion TL8. Consolidated Budget Monthly Expenditures (in 1987 prices), billion TL9. Total Capital of Newly Established'Firms (in 1987 prices), billion TL

Leading Indicators Approach for Business Cylcle Forecasting and a Study onDeveloping a Leading Economic Indicators Index for the Turkish Economy 35

1 Interested reader can find details of these methods from the books and articles slated in the Bibliography.

34 Ali Mürütoglu

Table 4: Turning Points of Leading Indicators Index

CYCLE BEGINNINGTROUGH

PEAK TERM INALTROUGH

I 06/89 07/90 05/91II 05/91 04/93 05/94III 05/94 04/96 10/96IV 10/96 ?

Following the analysis of turning points it can be said that the leading indicators index led the reference series very successfully until June 1994, but after this point, the leading power of the index has decreased slightly. However, the turning point analysis by itself is not enough to judge about the power of the leading indicators index. The relationship between the reference series and the index throughout the whole period must be also taken into account. For this purpose, both the Industrial Production Index and the Leading Indicators Index are given in Chart 3.

Chart 3 : Monthly Industrial Production and Leading Indicators Index (Standard Values)

As it can be observed from the chart, the leading indicators index is(other than a few exceptions) successful in leading the reference series.

Leading Indicators Approach for Business Cylcle Forecasting and a Study onDeveloping a Leading Economic Indicators Index for the Turkish Economy 35

H. Using the Leading Indicators Index in ForecastingThe leading indicators index is now ready for short-term forecasting of the economic activity. There are various methods for using leading indicators index in the short-run forecasting of economic activity.1 But none of these methods give the correct forecast all the time. In addition, these methods should be considered as completing rather than competing and more than one method must be used to make the forecast more reliable.

Lastly, it must be stated that the result of the forecast of the leading indicator index should be used carefully. When making the final decision, the results of other methods should also be considered. As a fact, all methods of forecasting are only decision tools and findings of these methods should be combined with the insights and experiences of the forecaster.

VII. Summary and ConclusionIn this study, monthly data of nearly 50 economic series from different sectors are analyzed in this study in the time period between January 1989- August 1998 and 9 economic series are determined as leading indicators for the Turkish economy. These series are used to develop a Leading Indicators Index for the Turkish economy which can be used for forecasting the turning points of industrial production. In the period of analysis, three complete and one incomplete cycles are determined in the Industrial Production Index. Accordingly, June 1989, July 1991, Junel994 and March/1996 are determined as trough dates and October 1990, December 1993, July 1995 and July 1997 are determined as peak dates of these cycles.

The leading economic series that formed the Leading Indicators Index are as follows:I. Total Import of Investment Goods, in million dollar2. Total Import of Intermediate Goods, in million dollar3. Currency (in 1987 prices), billion TL4. M2 (in 1987 prices), billion TL5. Reserve Money (in 1987 prices), billion TL6. Deposit Money Banks Credits (in 1987 prices), billion TL7. Net Credit Volume (in 1987 prices), billion TL8. Consolidated Budget Monthly Expenditures (in 1987 prices), billion TL9. Total Capital of Newly Established'Firms (in 1987 prices), billion TL

1 Interested reader can find details of these methods from the books and articles stated in the Bibliography,

36 Ali Miirütoğlu

This study shows that business cycles are found in the Turkish Economy as in other developed countries’ economies and more studies should be done in the area of business cycles and leading indicators approach.

In order to make the leading indicators’ forecast more reliable and useful, some arrangement should be made. Firstly, the current values of most economic series are announced with a long time of 3-4 months delay. This hinders the power of leading indicators in forecasting. Secondly, the scope of series, in particular, the real sector of the economy, should be watched continuously and updated if necessary. Lastly, the number of surveys which shows that expectations of economic actors (firms, households etc) must be increased.

The leading indicator index should be observed in certain time periods and must be updated when necessary. Some series may be omitted from and some others may be inserted in the index. Also the techniques that are used when developing an index must also be updated in the light of new developments.

BibliographyA lta y , S ., A r ık a n , A ., B a k ır , H . v e T a ta r A ., “ L e a d in g In d ic a to rs : T h e T u rk is h

E x p e r ie n c e ” , 20. C IRETKonferansı, B u d a p e ş te , 2 -5 E k im 3991 .A n n u z ia to , P a u lo v e B a ld a s s a r r i , M a r io , e d s . , Is the Business Cycle Still Alive:

Theory, Evidence and Policies, S ( t) . M a r t i n ’s P re s s In c .,N e w Y o rk , 1 9 9 4 . A re n , S a d u n , İstihdam Para ve iktisadi Politika, 10. B a s k ı , S a v a ş Y a y ın la r ı , A n k a ra ,

1 9 9 2 .B o s c h a n C . V e E b a n k s W ., "The Phase- Average Trend, a New Way o f Measuring

Economic Growth”, P ro c e e d in g s o f th e B u s in e s s a n d E c o n o m ic S ta t is t ic s S e c t io n , A m e r ic a n S ta t is t ic a l A s s o c ia t io n , 1 9 7 8 .

B ry G . V e B o s c h a n C ., “Cyclical Analysis o f Time Series : Selected Procedures and Computer Programs”, N B E R , T e c h n ic a l P a p e r , n .2 , 1 9 7 1 .

B u rn s , A .F ., V e M i tc h e l l W .C ., Measuring Business Cycles, N B E R S tu d ie s in B u s in e s s C y c le s N o . 2 , C o lo m b ia U n iv e r s i ty P re s s , N e w Y o rk , 1946 .