Embed Size (px)

Citation preview

CORPORATE PRESENTATION

March 2018

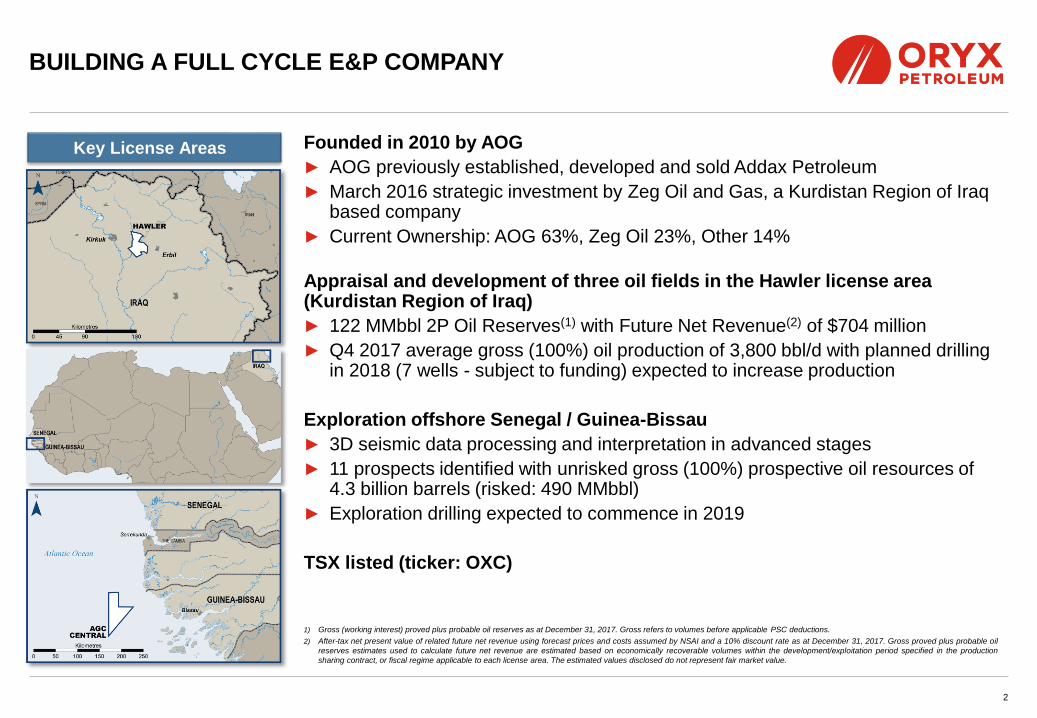

Founded in 2010 by AOG

► AOG previously established, developed and sold Addax Petroleum

► March 2016 strategic investment by Zeg Oil and Gas, a Kurdistan Region of Iraq based company

► Current Ownership: AOG 63%, Zeg Oil 23%, Other 14%

Appraisal and development of three oil fields in the Hawler license area (Kurdistan Region of Iraq)

► 122 MMbbl 2P Oil Reserves(1) with Future Net Revenue(2) of $704 million

► Q4 2017 average gross (100%) oil production of 3,800 bbl/d with planned drilling in 2018 (7 wells - subject to funding) expected to increase production

Exploration offshore Senegal / Guinea-Bissau

► 3D seismic data processing and interpretation in advanced stages

► 11 prospects identified with unrisked gross (100%) prospective oil resources of 4.3 billion barrels (risked: 490 MMbbl)

► Exploration drilling expected to commence in 2019

TSX listed (ticker: OXC)

2

BUILDING A FULL CYCLE E&P COMPANY

Key License Areas

1) Gross (working interest) proved plus probable oil reserves as at December 31, 2017. Gross refers to volumes before applicable PSC deductions.

2) After-tax net present value of related future net revenue using forecast prices and costs assumed by NSAI and a 10% discount rate as at December 31, 2017. Gross proved plus probable oil

reserves estimates used to calculate future net revenue are estimated based on economically recoverable volumes within the development/exploitation period specified in the production

sharing contract, or fiscal regime applicable to each license area. The estimated values disclosed do not represent fair market value.

3

HAWLER LICENSE (KURDISTAN REGION OF IRAQ)

Four discoveries with production from the Demir Dagh and Zey Gawra fields (3,800 bbl/d in Q4 2017)

Working Interests

► 65% Oryx Petroleum (Operator)

► 20% KEPCO (Kurdistan Regional Government)

► 15% KNOC (Korean National Oil Corporation)

► Unrisked 2C Gross (100%) contingent Oil Resources -

Development Pending of 83 MMbbl (Risked: 64 MMbbl)

► Appraisal / Exploration potential

• Unrisked Gross 2C (100%) contingent Oil Resources - Development

Unclarified of 145 MMbbl (Risked: 100 MMbbl)

• Unrisked Best Estimate Gross (100%) Prospective Oil Resources of

161 MMbbl (Risked: 6 MMbbl)

(1) The oil reserves, contingent resources and prospective resources data is based upon an evaluation by NSAI with effective date as at December 31, 2017. See material change report dated February 15, 2018 filed on SEDAR.

(2) Gross refers to volumes before applicable PSC deductions.(3) After-tax net present value of related future net revenue using forecast prices and costs assumed by NSAI and a 10% discount rate as at

December 31, 2017. The estimated values disclosed do not represent fair market value. See material change report dated February 15, 2018 filed on SEDAR.

Wells

Completed

Appraisal

Discovery

Planned Appraisal

Discovery: Oct 2013

Discovery: Dec 2013Currently producing

Discovery: Feb 2013Currently producing

Discovery: Mar 2014

Gross(2) Proved Plus Probable

Oil Reserves

Future Net

Revenue(3)

100% Working Interest

Field (MMbbl) (MMbbl) (US$MM)

Demir Dagh Cretaceous 86 56

Demir Dagh Jurassic 4 3

Zey Gawra Cretaceous 33 22

Banan East Cretaceous 36 23

Banan West Cretaceous 29 19

Total† 188 122 704

4

HAWLER LICENSE: FIELD DEVELOPMENT PLAN

Tertiary & Cretaceous

Reservoirs

Jurassic Reservoirs

Possible Triassic Reservoirs

Ain Al-Safra

220 km2

Zey Gawra

160 km2

Demir Dagh

197 km2

Relinquished Area

850 km2

AAS-1

BAN-2

BAN-1

ZAB-1

ZEG-1

DD-3&9

DD-10&11DD-2DD-5

DD-7

DD-8DD-4

AAS-2

Banan

211 km2

Demir Dagh (Cretaceous)► Three wells currently producing

► Medium grade crude (22º API average) with very

small quantities of gas and H2S

► Matrix and fracture porosity

► Further efforts to bring re-completed Demir

Dagh-8 well online in early 2018

► One short radius sidetrack planned in 2018

Gross (100%) 2P Oil Reserves:

86 MMbbl(1)

Demir Dagh (Jurassic)► One producing well for most of 2016 but shut-in

in December 2016

► Light crude with gas and H2S treatment required

► Fracture porosity only

Gross (100%) 2P Oil Reserves:

4 MMbbl(1)

Zey Gawra (Cretaceous)► Two wells drilled to date and producing with full

suite of test, logging, MDT data

► Light sweet crude (35º API)

► Matrix and fracture porosity

► ZEG-2 well drilled in Q1 2018 and expected to

be completed and in production in Q2 2018

► Additional well planned in 2H 2018

Gross (100%) 2P Oil Reserves:

33 MMbbl(1)

Demir Dagh and Zey Gawra producing from Cretaceous, with Banan (Cretaceous and Tertiary) expected to be evaluated in 2018

Banan (Cretaceous)► Two wells drilled to date with one DST

► Medium grade crude similar to Demir Dagh

Cretaceous (~20º API)

► Matrix and fracture porosity

► Further drilling planned in mid 2018

Gross (100%) 2P Oil Reserves:

64 MMbbl(1)

(1) As at December 31, 2017 per evaluation conducted by Netherland Sewell &

Associates, Inc. (‘NSAI’). See Material Change Report dated February 15, 2018

filed on SEDAR.

Banan (Tertiary)► No reserves booked

► Data collected during drilling of BAN-2

(suspended) suggested presence of sizable oil

column

► 3 wells planned in 2018

► ZEG-1 discovery in the Cretaceous in 2013

• 33 MMbbl Gross (100%) Proved Plus

Probable Oil Reserves(1)

• Light sweet crude (35º API)

• Matrix porosity similar to Demir Dagh

• Higher recovery rates than Demir Dagh

• Full suite of logging, MDT and test data for

ZEG-1, 2D seismic

► ZEG-1 ST and ZAB-1 ST successfully

completed as producers in Cretaceous

reservoir in late 2016 and mid-2017

respectively

► ZAB-1 re-entry in Tertiary reservoir

concluded in late 2016 but unable to be

completed as a producer

5

ZEY GAWRA DISCOVERY AND EARLY APPRAISAL

(1) As at December 31, 2017.

ZEG-1

Pila Spi – Avanah - Khurmala

Bakhtiari - Fars

Kolosh

Shiranish

Qamchuqa – Sarmord - Garagu

Najmah - Sargelu

AlanMus Adaiyah

Butmah

Triassic

ZAB-1 ZEG-1ZEG-2

ZAB-1-ST

ZEG-1-ST

NW SE

Reserves

Contingent Resources

6

ZEY GAWRA APPRAISAL AND EARLY PRODUCTION

Top Shiranish

ZAB-1 ZAB-1-ST ZEG-2 ZEG-1

ZEG-1-STSHIRANISH

KOMETAN

QAMCHUQA

SARMORD

ZAB-1

ZAB-1-ST

ZEG-2

ZEG-1

► Two wells planned in 2018• Increase production

• Better understand different free water level measurements at ZAB-1ST and ZEG-1ST

► ZEG-2 drilled in Q1 2018 and expected to be completed as a producer and online in Q2 2018

► Additional well to be drilled 2H 2018

Cretaceous map

DD-2

DD-7

DD-8

DD-3

DD-9DD-4

DD-6

DD-5

DD-10

DD-11

BAN-1

7

DEMIR DAGH FIELD APPRAISAL AND DEVELOPMENT

► Ten wells drilled to date• Two deep wells to evaluate all reservoirs (DD-2 & 3)

• Eight shallow wells appraising Cretaceous (DD-4, 5, 6, 7, 8, 9, 10 & 11)

• Vertical / deviated well designs

► Six wells completed for production with three wells currently producing• DD-2, 4, 6, 7 & 10 completed in Cretaceous

• DD-3 completed in Jurassic

• DD-2 and DD-3 shut-in due to high water production

• DD-7 shut-in due to marginal production levels

Potential Horizontal Well

► Efforts to bring re-completed DD-8 well in

Cretaceous online as a producer planned

in Q1 2018

► Short radius sidetrack of DD-5 planned in

1H 2018

• Successful completion high in the Cretaceous

reservoir could provide important validation of

a horizontal well development

DD-H

Cretaceous map

► Two wells drilled in 2014

• BAN-1 (DST)

• BAN-2 (suspended, no DST)

► Both wells confirmed oil in Cretaceous reservoir (Reserves)

• Medium grade crude similar to Demir DaghCretaceous (~20° API)

• Matrix and fracture porosity

► Data collected during drilling of BAN-2 indicated presence of sizeable oil column in Tertiary reservoir (Contingent Resources)

► Interpretation of data is that Banan is actually two fields separated by a fault (Banan West and Banan East)

► 2018 drilling activity planned in Banan West

• Re-entry of BAN-2 targeting Cretaceous

• Drilling of three wells targeting Tertiary

8

BANAN DISCOVERY AND EARLY APPRAISAL

BAN-2

BAN-1

Bakhtiari - Fars

Pila Spi – Gercus - Sinjar

Kolosh

Shiranish – Kometan – Qamchuqa

Sarmord - Garagu

Najmah

Mus - Adayiah - Butmah

Triassic

BAN-2S N

Reserves

Contingent Resources

Pilaspi map

9

HAWLER PRODUCTION FACILITIES

► Facilities with capacity of 40,000 bbl/d at Demir Dagh

• Two trains to accommodate both crude oil with and without H2S treatment requirements

► ~1km tie-in pipeline from production facilities to KRI-Turkey export pipeline

► 25,000 bbl of storage capacity and 12,000 bbl/d unloading capacity Truck Loading Station (TLS) at

Demir Dagh

► Initial leased processing facilities installed at Zey Gawra (~6,000 bbl/d) in Q4 2016 with trucking to

Demir Dagh for export pipeline entry

• A more permanent solution contemplates pipeline transport back to facilities at Demir Dagh for processing and

export

ITP

40” & 46” pipelines, 600 & 900 Mbbl/d capacity(1)

KRI - Turkey

24/36” oil pipeline, 700 Mbbl/d capacity

10

KURDISTAN REGION: SUPPLY DYNAMICS

Export Sales:

► Via Turkey by KRI - Turkey pipeline

► Recent KRI exports of oil ~300,000

bbl/d

► Payments from the KRG to oil

exporters largely current since

September 2015 and now based on

Production Sharing Contracts

► Realisation referenced to

international prices

Domestic Sales:

► Pre-payment for sales

► Realisations at discount to

international prices

► Limited demand

To Ceyhan

Oryx Petroleum is currently exporting all production by pipeline

(1) Iraq portion of ITP currently non-operational

Illustrative Netback ($/bbl)

Contractor Netback

Realised Price $50.00 $60.00 $70.00

Royalties 10% (5.00) (6.00) (7.00)

Net revenue 45.00 54.00 63.00

Cost oil 40% 18.00 21.60 25.20

Profit oil 27.00 32.40 37.80

Contractor share 28% 7.56 9.07 10.58

Government share 72% 19.44 23.33 27.22

Total Contractor (Cost + Profit oil) 25.56 30.67 34.27

Less: Opex(1) (7.50) (7.50) (7.50)

Contractor Netback 18.06 23.17 26.77

Oryx Petroleum Netback

Revenue 65% 32.50 39.00 45.50

Less: Royalties & Government share

of Profit oil65% (15.89) (19.07) (22.24)

Less: Capacity Payment(2) (0.74) (0.88) (1.03)

Less: Opex 85% (6.38) (6.38) (6.38)

Plus: Carry Recovery(3) 3.60 4.32 5.04

Oryx Petroleum After-tax Netback 13.09 16.99 20.89

► Realised Prices (Export via pipeline):

• Brent less $12/bbl with adjustment for API gravity

and sulphur content

► Contractor Profit oil and Oryx Petroleum capacity

building payment assumes R factor <1

► Normalised Opex to be achieved as production

increases

• $10.00/ bbl+ expected in near term

• ~$7.50/bbl assuming gross (100%) production of 7,000 –

8,000 bbl/d

► Opex and Capex carries

• Oryx Petroleum carries 20% KRG share

• Oryx Petroleum carries KRG capex up to $300

million

• Recoverable from KRG share of cost oil

11

HAWLER NEAR TERM NETBACKS

(1) Assumes gross (100%) production of 7,000 - 8,000 bbl/d

(2) 15% of Oryx Petroleum Share of Profit oil

(3) Government share of cost oil

12

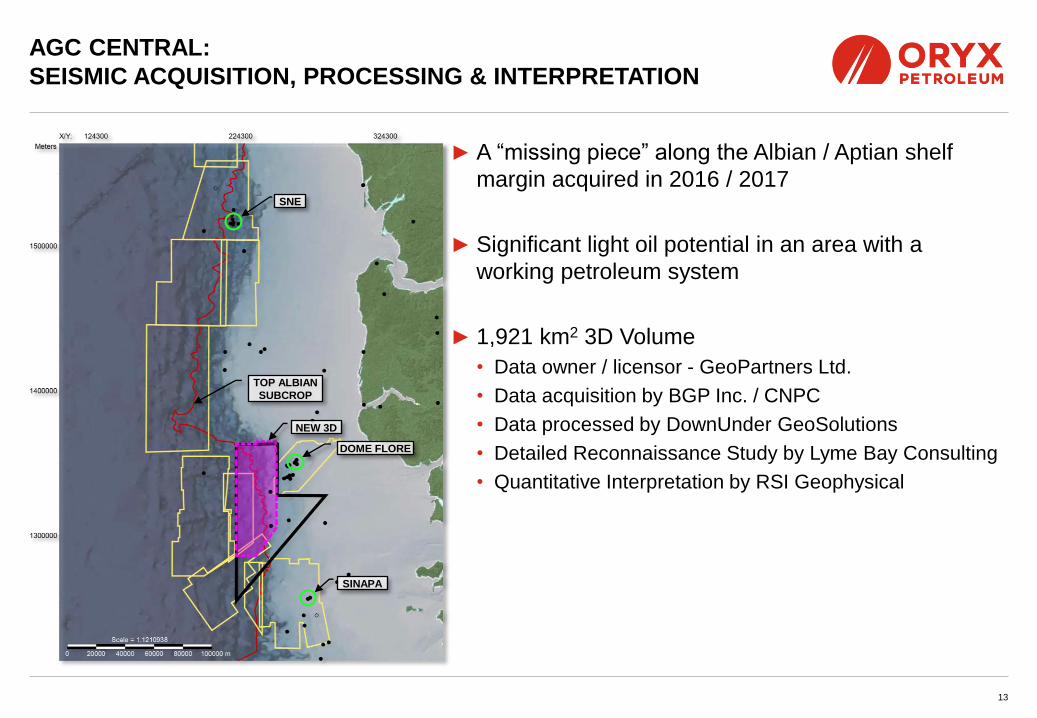

AGC CENTRAL (SENEGAL / GUINEA BISSAU)

► 3,150 km2 licence area in water depths of

100 - 1,500m

► Carbonate edge play type similar to

SNE-1 discovery identified from seismic

data

► 750 km2 of seismic obligation in initial 3-

year exploration phase

• 1,921 km2 3D Seismic survey and fast track

processing completed in early 2017

• Full processing / interpretation / mapping of

prospects expected to be completed in Q2

2018

• 11 prospects identified with gross unrisked

(100%) best estimate prospective resources

of 4.3 billion barrels (risked 490 MMbbl)(1)

► First renewal of initial exploration phase

expected in October 2018

• Two well work commitment with first

exploration drilling expected in 2019

Significant light oil potential in an area with a working petroleum system and recent discoveries in adjoining areas

► 80% Oryx Petroleum (Operator)

► 20% AGC

(1) As at December 31, 2017 per evaluation conducted by Netherland Sewel & Associates, Inc. (‘NSAI’). See Material Change Report dated February 15, 2018

► A “missing piece” along the Albian / Aptian shelf

margin acquired in 2016 / 2017

► Significant light oil potential in an area with a

working petroleum system

► 1,921 km2 3D Volume

• Data owner / licensor - GeoPartners Ltd.

• Data acquisition by BGP Inc. / CNPC

• Data processed by DownUnder GeoSolutions

• Detailed Reconnaissance Study by Lyme Bay Consulting

• Quantitative Interpretation by RSI Geophysical

13

AGC CENTRAL:

SEISMIC ACQUISITION, PROCESSING & INTERPRETATION

SNE

NEW 3D

TOP ALBIAN

SUBCROP

SINAPA

DOME FLORE

PLAY TYPES

1) Maastrichtian – clastic play

2) Santonian - clastic play

3) Albian / L. Cenomanian – clastic play (SNE analogue)

4) Albian / Aptian – carbonate / clastic play

14

AGC CENTRAL: PLAY TYPES

2

1

3

4

AGC Central 3D (2017)

15

AGC CENTRAL: INITIAL INTERPRETATION OF SEISMIC DATA

AGC Central Risk Assessment

Play Type Reservoir Trap Source Seal

Maastrichtian Clastics Low High Low (Albian) Medium

Santonian Clastics Medium Medium Low (Turonian) Medium

Albian / L. Cenomanian Clastics Medium Low Low (Turonian & Albian) Low

Albian / Aptian Carbonates Medium Low Low (Albian) Low

W E

LOWER SENONIAN

UNCONFORMITY

Zey Gawra Drilling

► Two new wells targeting Cretaceous

Banan Drilling

► Re-entry of BAN-2 well targeting Cretaceous

► Three new wells targeting Tertiary reservoir

Facilities

► Primarily related to Banan

► Flowlines and field infrastructure required to support new wells

Demir Dagh Drilling

► Short radius sidetrack of Demir Dagh-5 well

► Seismic acquisition and interpretation costs, drilling preparations, PSC costs

16

2018 CAPITAL EXPENDITURE FORECAST

Note:

1) The above table excludes license acquisition costs. Totals in rows and columns may not add-up due to rounding

2) Other is comprised primarily of facilities and license maintenance costs and technical support

Hawler

AGC Central

Location License / Field / Activity2018

Forecast

$ millions

Kurdistan Region Hawler

Zey Gawra-Drilling 9

Demir Dagh-Drilling 4

Demir Dagh-Facilities 2

Banan-Drilling 11

Banan-Facilities 6

Other(2) 3

Total Hawler 35

West Africa AGC Central--Drilling Prep 6

AGC Central--Other(2) 7

Capex Total(1) 48

AOG Credit Facility

► $77 million balance of principal plus accrued interest

► Interest payable in shares of OXC

► Currently scheduled to mature in July 2019

Contingent Consideration

► Payable to vendor of Hawler license area upon a second commercial discovery

► $71 million balance of principal plus accrued interest

• Remainder payable (contingent) in annual instalments on September 30 of 2018 - 2021 if second commercial discovery declared before September 30, 2018

Liquidity Outlook

► Cash on hand at December 31, 2017 ($38.6 million), expected net revenues from sales, and proceeds from sale of HMB interest expected to fund planned expenditures through the end of 2018

17

KEY BALANCE SHEET ITEMS (DECEMBER 31, 2017)

AND LIQUIDITY OUTLOOK

► Expected Production Ramp-up in the

Kurdistan Region of Iraq

• Q4 2017 Gross (100%) average oil production of

3,800 bbl/d

• Regular revenue payments for oil exports paid

through November 2017

• Seven wells planned in 2018

► Significant Potential Resource Upside in

AGC Central license area offshore Senegal

/ Guinea-Bissau

• Based on initial interpretation of 3D seismic 11 oil

prospects identified with gross unrisked (100%)

best estimate prospective resources of 4.3 billion

barrels (risked 490 MMbbl)(1)

• Exploration drilling expected to commence in 2019

► Available liquidity to fund current plans

through end of 2018

18

POSITIONED FOR GROWTH IN 2018 AND BEYOND

(1) As at December 31, 2017 per evaluation conducted by Netherland Sewel & Associates, Inc. (‘NSAI’). See Material Change

Report dated February 15, 2018

This document has been prepared by Oryx Petroleum Corporation Limited (“Oryx Petroleum” or the “Corporation”) for information purposes only. This document should be read in conjunction with the annual information form of Oryx Petroleum dated March 23, 2017 (the

“AIF”). Additional information about Oryx Petroleum is available on its website at www.oryxpetroleum.com and Oryx Petroleum’s profile at www.sedar.com.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Statements that are not reported financial results or other historical information are forward-looking information within the meaning of applicable Canadian securities laws and forward-looking statements within the meaning of applicable United States securities laws

(collectively, “forward-looking statements”). This presentation includes forward-looking statements regarding Oryx Petroleum and the industry in which it operates, including statements about, among other things, exploration and drilling activities, expectations, beliefs, plans,

future oil prices, business and acquisition strategies, opportunities, objectives, prospects, assumptions, including those related to trends, prospects, future events and performance. Sentences and phrases containing or modified by words such as “anticipate”, “plan”,

“continue”, “estimate”, “intend”, “expect”, “may”, “will”, “project”, “predict”, “potential”, “targets”, “projects”, “is designed to”, “strategy”, “should”, “believe” and similar expressions, and the negative of such expressions, are not historical facts and are intended to identify forward-

looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. Forward-looking statements should not be read as

guarantees of future events, future performance or results, and will not necessarily be accurate indicators of the times at, or by which, such events, performance or results will be achieved, if achieved at all. Forward-looking statements are based on information available at

the time and/or management’s expectations with respect to future events that involve a number of risks and uncertainties, any of which could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. The factors described

under the heading “Risk Factors” in the AIF provide examples of the risks, uncertainties and events that may cause Oryx Petroleum’s actual results to differ materially from the expectations it describes in its forward-looking statements. Readers should be aware that the

occurrence of the events described in such risk factors could have an adverse effect on, among other things, Oryx Petroleum’s business, prospects, operations, results of operations and financial condition.

Specific forward-looking statements contained in this presentation include, among others, statements, management’s beliefs, expectations or intentions regarding the following: the ability of each of the Corporation and its partners to fund ongoing exploration and meet their

respective financing and carry obligations with respect to the license areas of Oryx Petroleum; the performance characteristics and discovery potential of Oryx Petroleum’s properties; the Corporation’s expectations of current and future production levels; exploration work

plans, conceptual development and marketing plans; the reserve and resource potential of Oryx Petroleum’s license areas; the political, economic, regulatory and business stability of the jurisdictions in which Oryx Petroleum operates; export pipeline options and export

capacity; the Corporation’s re-forecasted capital expenditure program and the Corporation’s expectations regarding the use of existing capital, its ability to raise capital, develop reserves and resources and to add reserves and resources through exploration, acquisitions and

development; the amount, nature, timing and effects of the Corporation’s capital expenditures; the Corporation’s plans for drilling wells and chance of success; the Corporation’s plans for completion or acquisition of seismic data; market prices and supply and demand

fundamentals for oil and other commodities; timing and amount of the Corporation’s potential future production, forecasts of capital expenditures, net revenues, future development plans and the sources of financing thereof; the Corporation’s operating and other costs and

expenses; business strategies and plans of management; anticipated benefits and enhanced shareholder value resulting from prospect development and acquisitions; and oil reserves and resources quantities and the discounted present value of future net cash flows from

these reserves and resources.

Readers are cautioned that the foregoing list of forward-looking statements should not be construed as being exhaustive.

In making the forward-looking statements in this presentation, the Corporation has made assumptions regarding: timing and results of exploration activities; the enforceability of the Corporation’s production sharing contracts and risk exploration contracts; treatment under the

fiscal terms of production sharing contracts, risk exploration contracts, governmental regulatory regimes and royalty laws; the timing and terms of government approvals and the timing and terms of any renewal or extension of any of the Corporation’s license areas; the cost

of expenditures to be made by Oryx Petroleum; future crude oil prices and prices realised by Oryx Petroleum on oil production sold; the amount of oil production sold domestically in the Kurdistan Region and the amount of oil production sold as export; oil from the Kurdistan

Region refining capacity in the local jurisdiction and access to local and international markets for crude oil production; the Corporation’s ability to obtain and retain qualified staff and equipment in a timely and cost-efficient manner; the political situation and stability in

jurisdictions in which Oryx Petroleum has licenses, including, without limitation, that the recent escalation in violence in Iraq relating to the incursion by the Islamic State in Iraq and Syria (ISIS) will not adversely disrupt the Corporation’s production and development activities

in the Kurdistan Region; the regulatory, legal and political framework governing the production sharing contracts, risk exploration contracts, royalties, taxes and environmental matters in the jurisdictions in which the Corporation conducts and will conduct its business and the

interpretations of applicable laws; the ability to renew its licenses on attractive terms; the Corporation’s current and future production levels and the timing and payment mechanism for export oil from the Kurdistan Region; the market for domestic oil sales in the Kurdistan

Region and the timing and payment mechanism for such domestic sales in the Kurdistan Region; the applicability of technologies for the recovery and production of the Corporation’s oil reserves and resources; ability to gain access to existing facilities or to build necessary

facilities to sell oil production; operating costs; availability of equipment and qualified contractors and personnel; future capital expenditures to be made by the Corporation; future sources of funding for the Corporation’s capital programs; the Corporation’s future debt levels;

geological and engineering estimates in respect of the Corporation’s reserves and resources; the geography of the areas in which the Corporation is conducting exploration and development activities; the impact of increasing competition on the Corporation; the ability of the

Corporation to obtain financing and, if obtained, to obtain acceptable terms; and government/state participation in the Corporation’s development activities through the exercise of back-in rights.

Forward-looking statements involve significant risks and uncertainties, should not be read as guarantees of future events, performance or results, and will not necessarily be accurate indicators of whether or not such events, performance or results will be achieved. Forward-

looking statements are based on information available at the time and/or management’s expectations with respect to future events that involve a number of risks and uncertainties. Any forward-looking statements concerning prospective results of operations, financial

position, production, expectations of cash flows and future cash flows that are based upon assumptions about future results, economic conditions and courses of action and are presented for the purpose of providing prospective purchasers with a more complete perspective

on Oryx Petroleum’s present and planned future operations and such information may not be appropriate for other purposes and actual results may differ materially from those anticipated in such forward-looking statements.

Actual results could differ materially from those anticipated in or implied by any forward-looking statements, including without limitation, as a result of the risk factors, which are described in detail under “Risk Factors” in the AIF. Readers should reference the factors

discussed under the heading “Risk Factors” in the AIF. The forward-looking statements included in this presentation are expressly qualified by this cautionary statement and readers are cautioned that any forward-looking statement speaks only as of the date of this

presentation. The Corporation does not undertake any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable securities laws. If the Corporation does update

one or more forward-looking statements, it is not obligated to, and no inference should be drawn that it will, make additional updates with respect thereto or with respect to other forward-looking statements.

19

DISCLAIMER

RESERVES AND RESOURCES ADVISORY

The reserves and resources and associated future net revenue information presented herein are estimates only. In general, estimates of oil reserves and resources and the future net revenue therefrom are based upon forward-looking statements and a number of variable

factors and assumptions, such as production rates, ultimate reserve recovery, timing and amount of capital expenditures, ability to transport production, marketability of oil, royalty rates, the assumed effects of regulation by governmental and other regulatory agencies and

future operating costs, all of which may vary materially from actual results, and for resources, additional variable factors and assumptions such as discovery and commerciality. For those reasons, estimates of the oil reserves and resources attributable to any particular group

of properties, as well as the classification of such reserves and resources (based on risk of recovery) and estimates of future net revenues associated with such reserves and resources prepared by different engineers (or by the same engineers at different times) may vary.

The actual reserves and resources of Oryx Petroleum may be greater or less than those estimated and such variation may be material.

In addition, Oryx Petroleum’s actual production, revenues, development, capital and operating expenditures, as applicable, with respect to its reserves and resources will vary from estimates thereof and such variations could be material. Any activities undertaken by Oryx

Petroleum to develop or permit the reclassification of its reserves and resources will be subject to the terms of the applicable contractual arrangement.

Statements relating to “net present value”, “future net revenues”, “reserves” and “resources” are deemed to be forward-looking statements, as they involve the implied assessment, based on certain estimates and assumptions (including, without limitation, pricing

assumptions), that the reserves and resources described exist in the quantities predicted or estimated, and can be profitably produced in the future. Readers should refer to the AIF for information regarding the assumptions related to the reserves and resources reported

herein. There is no assurance that forecast price and cost assumptions will be attained and variances could be material.

Proved oil reserves are those reserves which are most certain to be recovered. There is at least a 90% probability that the quantities actually recovered will equal or exceed the estimated proved oil reserves. Probable oil reserves are those additional reserves that are less

certain to be recovered than proved oil reserves. There is at least a 50% probability that the quantities actually recovered will equal or exceed the sum of the estimated proved plus probable oil reserves. Possible oil reserves are those additional reserves that are less certain

to be recovered than probable oil reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of estimated proved plus probable plus possible oil reserves.

Contingent oil resources are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations using established technology or technology under development, but which are not currently considered to be commercially

recoverable due to one or more contingencies. Contingencies may include factors such as economic, legal, environmental, political, and regulatory matters, or a lack of markets. Contingent oil resources are further subdivided in accordance with the level of certainty

associated with recoverable estimates assuming their discovery and development and may be sub classified based on project maturity. Contingent oil resources entail additional commercial risk than reserves. There is no certainty that it will be commercially viable to

produce any portion of the contingent oil resources. Moreover, the volumes of contingent oil resources reported herein are sensitive to economic assumptions, including capital and operating costs and commodity pricing.

Prospective oil resources are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from undiscovered accumulations by application of future development projects. Prospective oil resources have both an associated chance of discovery

and a chance of development. Prospective oil resources entail more commercial and exploration risks than those relating to oil reserves and contingent oil resources. The risked prospective oil resources reported in this presentation are risked resources that have been

risked for chance of discovery, for chance of development. If a discovery is made, there is no certainty that it will be developed or, if it is developed, there is no certainty as to the timing or cost of such development.

The reserves estimates and evaluation and resource estimates and evaluation contained herein are derived from the NSAI Report which was prepared with reference to NI 51-101 relying on the COGE Handbook definitions. Reserves and resources provided herein are as at

December 31, 2017 and are only valid as of such date.

The estimates of reserves and resources and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves and resources and future net revenue for all properties, due to the effects of aggregation. The estimated future net

revenues contained herein are valid only as at December 31, 2017 and do not necessarily represent the fair market value of Oryx Petroleum’s reserves and resources.

As used herein, unless otherwise indicated, “gross” means, in respect of reserves, resources, production, area, capital expenditures or operating expenses, the total reserves, resources, production, area, capital expenditures or operating expenses, as applicable, attributable

to either (i) 100% of the license area, field, prospect or lead; or, (ii) the Corporation’s working interest in the license area, field, prospect or lead, as indicated, prior to the deductions specified in the applicable production sharing contract, risk exploration contract or fiscal

regime for each license area.

In addition to the general advisory language above, the below notes qualify certain reserves and resources volumes and other oil and gas information disclosed in this document:

“†”: This volume is an arithmetic sum of multiple estimates of reserves or resources, as applicable, which statistical principles indicate may be misleading as to volumes that may actually be recovered. Readers should give attention to the estimates of individual classes of

reserves or resources, as applicable, and appreciate the differing probabilities of recovery associated with each class as explained above.

“‡”: All field fluid measurements will require laboratory analysis to confirm results and should be considered preliminary until such analysis has been done. The test results are not necessarily indicative of long-term performance or of ultimate recovery.

20

DISCLAIMER

![附 属 書 Ⅰ 附 属 書 Ⅱ 附 属 書 Ⅲ - METI...Oryx dammah シロオリックス [Sahara Oryx; Scimitar-horned Oryx] Oryx leucoryx アラビアオリックス [Arabian Oryx;](https://img.pdfslide.us/doc/110x75/610ed737b544d54b153db177/e-a-e-a-e-a-meti-oryx-dammah-ffff.jpg)