Embed Size (px)

Citation preview

1

Organizational and Tax Issues in Managing Global Treasury

Global Cash Management Ltd. Grant Thornton International

Global Cash Management Ltd..Grant Thornton International 1

Demands of Managing a Global Treasury

?Managing Treasury on a global basis requires a tax driven focus in order to set up the most effective structure for managing liquidity and risk worldwide…..

2

Global Cash Management Ltd..Grant Thornton International 2

Objectives for Today

Today we will cover selected treasury issues and the related tax implications with a specific focus on:

• Structure

• Liquidity & Risk Management

Global Cash Management Ltd..Grant Thornton International 3

STRUCTURE

3

Global Cash Management Ltd..Grant Thornton International 4

Structure

• Operational Framework– Present situation => requirements

• Setting Up – key tax considerations – How, options & issues

• Centralized vs. Decentralized Treasury– Definitions, locations & activities

• Reporting – Tax & Treasury Issues

Global Cash Management Ltd..Grant Thornton International 5

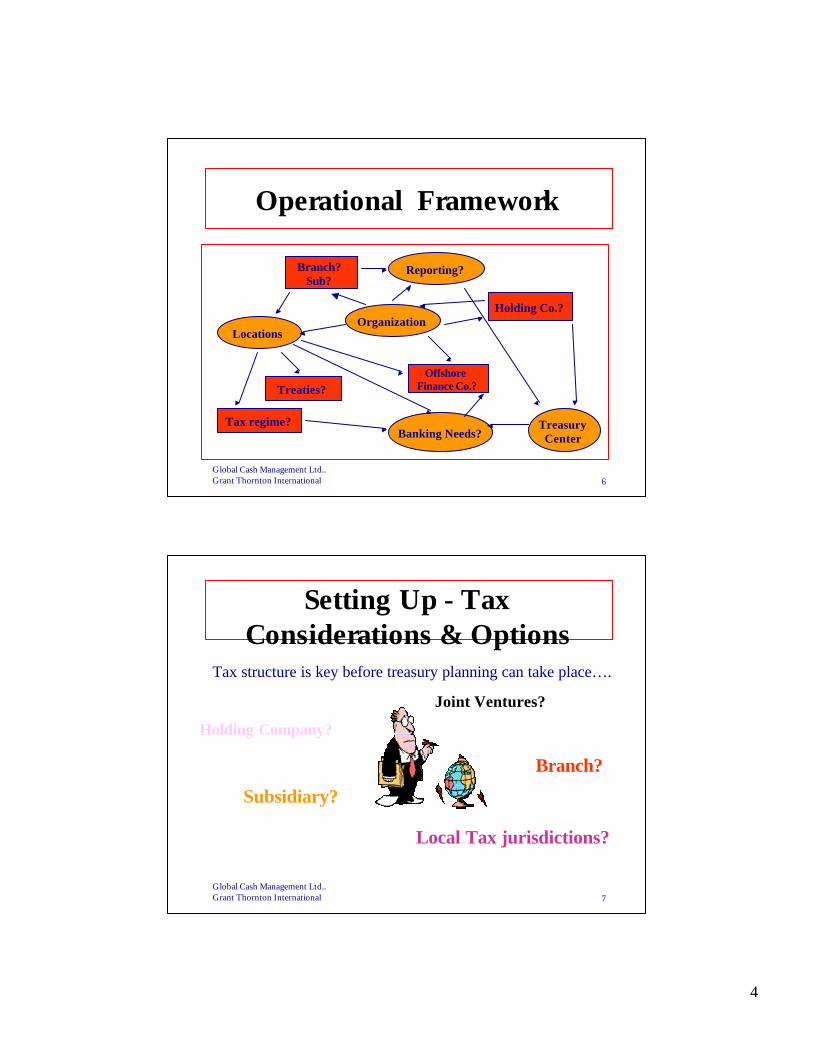

Operational Framework

• Numerous overseas operations– Sales offices– Manufacturing facilities– Warehousing & distribution centers– Joint ventures

• Requirements– Further centralize liquidity & risk management– Address reporting & information needs

4

Global Cash Management Ltd..Grant Thornton International 6

Operational Framework

LocationsOrganization

Banking Needs?Tax regime?

Treaties?

Holding Co.?

Offshore Finance Co.?

Branch?Sub?

Reporting?

TreasuryCenter

Global Cash Management Ltd..Grant Thornton International 7

Setting Up - Tax Considerations & Options

Tax structure is key before treasury planning can take place….

Subsidiary?

Branch?

Local Tax jurisdictions?

Holding Company?

Joint Ventures?

5

Global Cash Management Ltd..Grant Thornton International 8

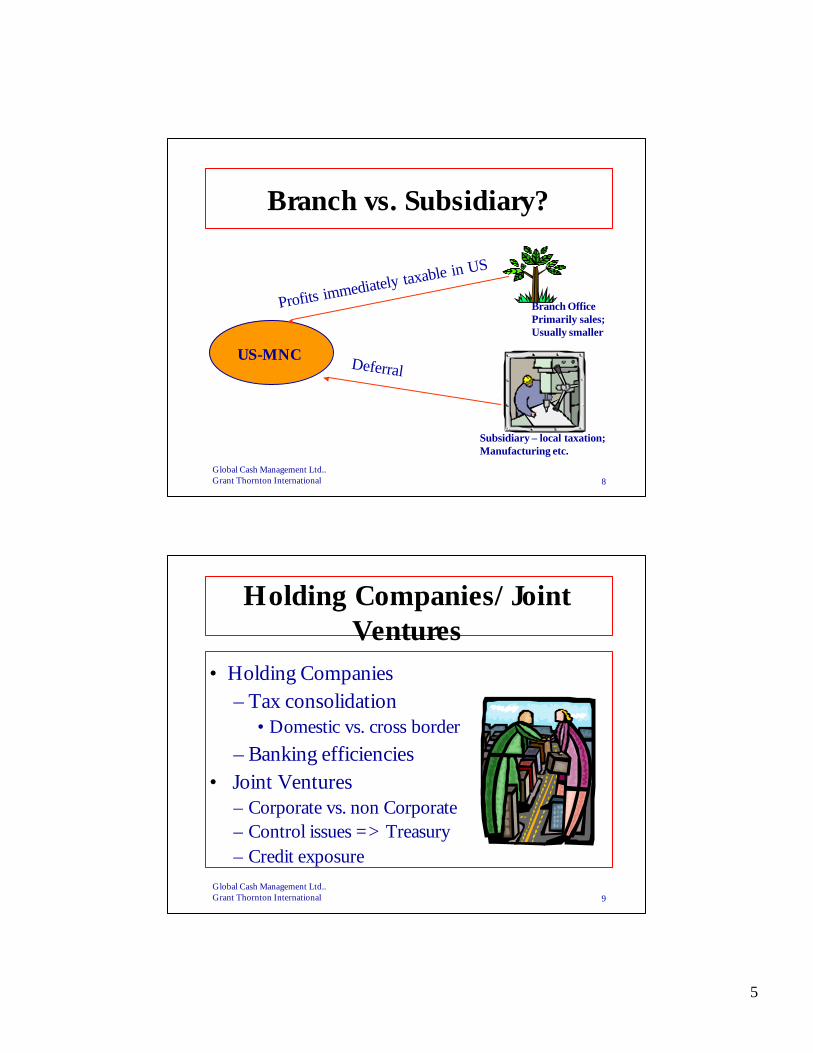

Branch vs. Subsidiary?

US-MNC

Profits immediately taxable in US

Branch OfficePrimarily sales; Usually smaller

Subsidiary – local taxation;Manufacturing etc.

Deferral

Global Cash Management Ltd..Grant Thornton International 9

Holding Companies/Joint Ventures

• Holding Companies– Tax consolidation

• Domestic vs. cross border– Banking efficiencies

• Joint Ventures– Corporate vs. non Corporate– Control issues => Treasury– Credit exposure

6

Global Cash Management Ltd..Grant Thornton International 10

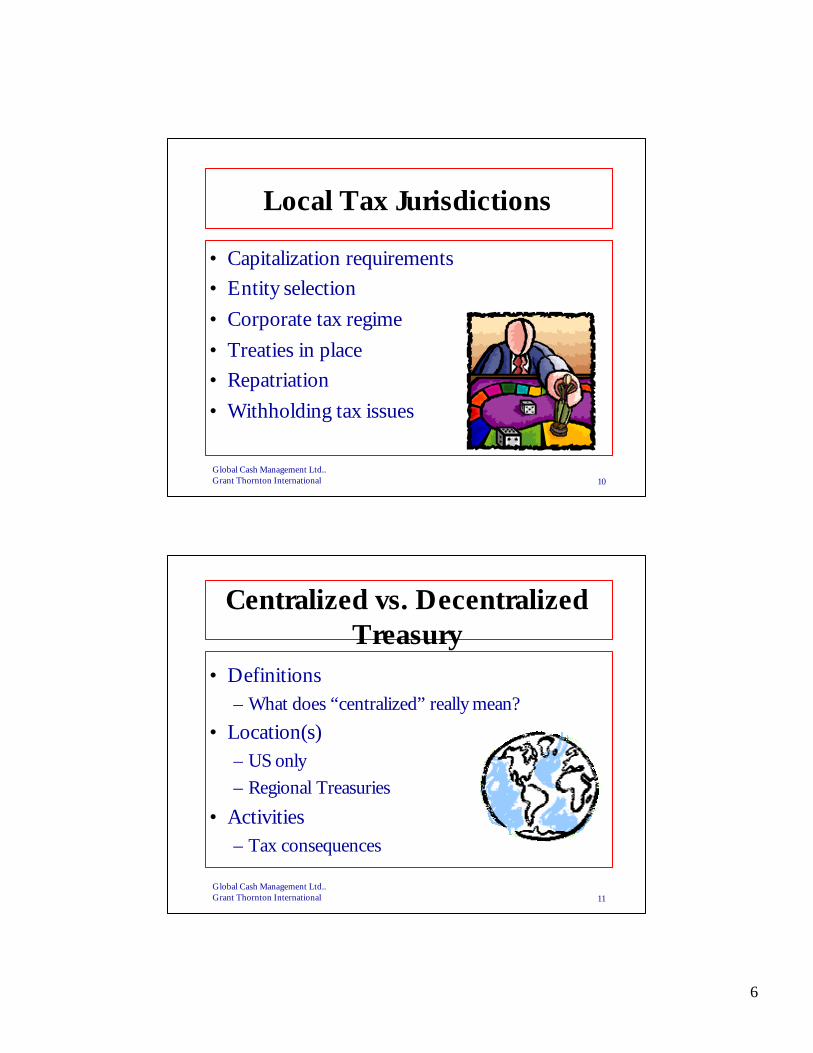

Local Tax Jurisdictions

• Capitalization requirements • Entity selection• Corporate tax regime• Treaties in place• Repatriation• Withholding tax issues

Global Cash Management Ltd..Grant Thornton International 11

Centralized vs. Decentralized Treasury

• Definitions– What does “centralized” really mean?

• Location(s) – US only– Regional Treasuries

• Activities– Tax consequences

7

Global Cash Management Ltd..Grant Thornton International 12

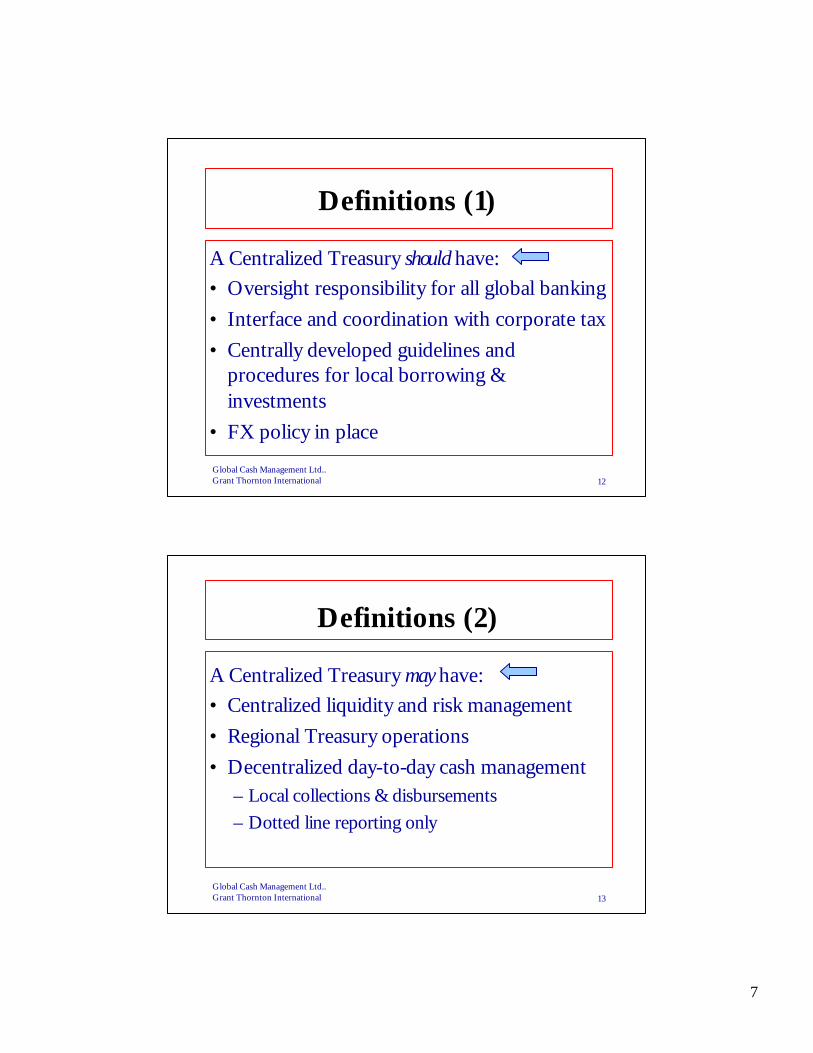

Definitions (1)

A Centralized Treasury should have:• Oversight responsibility for all global banking• Interface and coordination with corporate tax • Centrally developed guidelines and

procedures for local borrowing & investments

• FX policy in place

Global Cash Management Ltd..Grant Thornton International 13

Definitions (2)

A Centralized Treasury may have:• Centralized liquidity and risk management• Regional Treasury operations• Decentralized day-to-day cash management

– Local collections & disbursements– Dotted line reporting only

8

Global Cash Management Ltd..Grant Thornton International 14

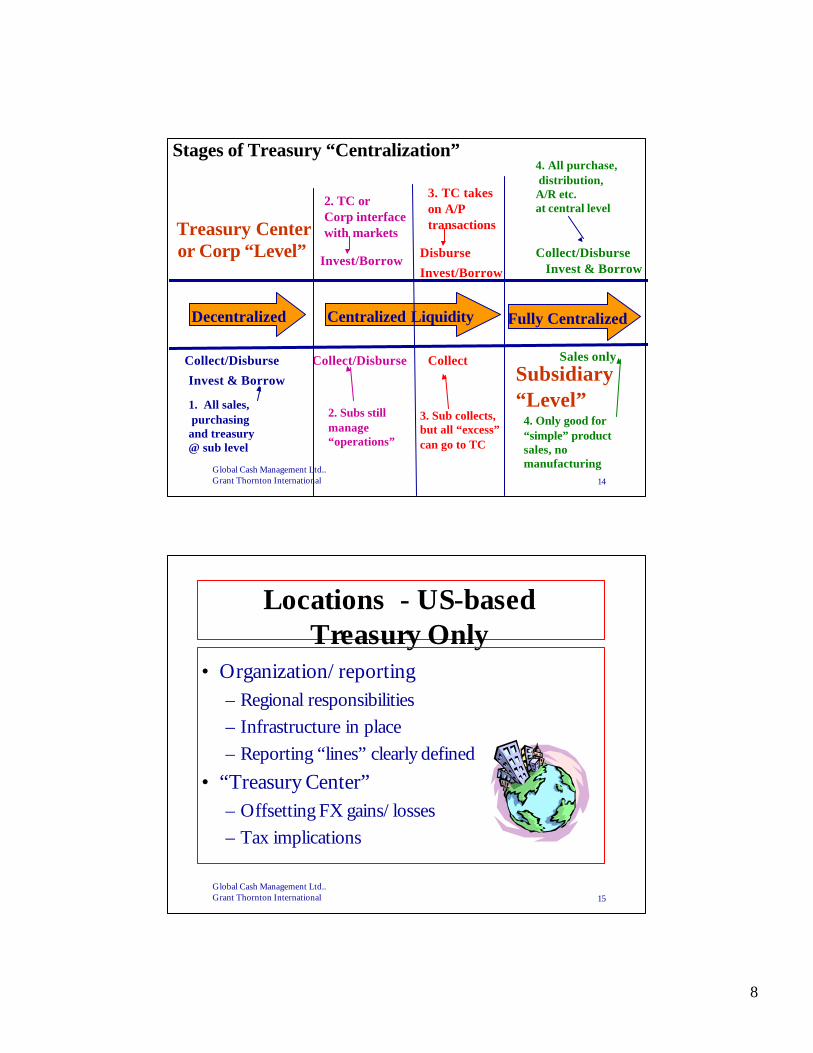

Stages of Treasury “Centralization”

Decentralized Fully CentralizedCentralized Liquidity

Collect/Disburse Collect/Disburse

Invest & Borrow

Invest/Borrow

Collect

Treasury Centeror Corp “Level”

Subsidiary “Level”

Disburse

Invest/Borrow Invest & BorrowCollect/Disburse

Sales only

1. All sales, purchasingand treasury @ sub level

4. All purchase,distribution,A/R etc.at central level2. TC or

Corp interfacewith markets

2. Subs stillmanage “operations”

3. TC takes on A/P transactions

3. Sub collects,but all “excess”can go to TC

4. Only good for“simple” productsales, no manufacturing

Global Cash Management Ltd..Grant Thornton International 15

Locations - US-based Treasury Only

• Organization/reporting– Regional responsibilities– Infrastructure in place– Reporting “lines” clearly defined

• “Treasury Center” – Offsetting FX gains/losses – Tax implications

9

Global Cash Management Ltd..Grant Thornton International 16

Locations – Regional Treasuries

• Existing overseas operation(s)– Major manufacturing location– Management/marketing center– Warehouse/distribution point– Finance Company or specific tax structure

• Tax jurisdiction/implications– Charging structure - restrictions– Substance – capitalization

Global Cash Management Ltd..Grant Thornton International 17

Activities

• Oversight/consulting• Intercompany netting• Liquidity management

– Financing– Investing

• FX trading• Tax implications

– Management fees?– Transfer pricing

10

Global Cash Management Ltd..Grant Thornton International 18

Reporting – Treasury Issues

• Treasury Issues– Direct vs. dotted line

• Rare to have direct reporting from foreign subsidiaries to Treasury

• “Political” considerations– Information requirements

• Frequency• Level of detail

Global Cash Management Ltd..Grant Thornton International 19

Reporting – Tax Issues

• Deferral vs. Consolidation• Functional currency• The reporting package – central vs. decentralized

access points• US GAAP vs. US tax GAAP vs. Foreign GAAP• Check the box options• Subpart F – anti-deferral issues• US earnings and profits issues

11

Global Cash Management Ltd..Grant Thornton International 20

Liquidity & Risk Management

Global Cash Management Ltd..Grant Thornton International 21

Liquidity & Risk Management

• Financing • Investing• Intercompany Cash Flows• Specialized Treasury Vehicles and

Arrangements• FX Risk Management

12

Global Cash Management Ltd..Grant Thornton International 22

Financing (1)

• Funding foreign operations– Debt vs. Equity financing – Thin capitalization issues

• Is interest deferred or lost under thin capitalization restriction?

– Is interest on cash or accrual on related party debt?

– Withholding tax issues

Global Cash Management Ltd..Grant Thornton International 23

Financing (2)

• Access to credit markets and costs• Use of overdraft lines

– Impact on centralized debt facilities and loan covenants

• Offset between surplus and deficit positions– Notional “pooling” vs. ZBAs– Tax implications

13

Global Cash Management Ltd..Grant Thornton International 24

Financing (3)

• Interest on related party debt • Parental guarantees

– Arm’s Length Requirement– 956 issue (deemed dividends)– 90 day grace period

Global Cash Management Ltd..Grant Thornton International 25

Investing

• Mechanics– Banking arrangements/costs

• Locations– Withholding tax/Reserve requirements

• Currencies and FX management • Interest

– Subpart F

– High tax kickout

14

Global Cash Management Ltd..Grant Thornton International 26

Intercompany Flows (1)

• Intercompany sales & payables– Terms – 90 day rule

• Opportunities for liquidity & risk management

– Opportunities for bilateral offset or multilateral netting?

• Transfer pricing - strategies– Pricing in relation to -

• Goods or services• Leases or licenses• Debt?

Global Cash Management Ltd..Grant Thornton International 27

Intercompany Flows (2)

• Dividends– Rate averaging between high/low rate countries– To the US– To intermediate foreign holding companies– Deductions of dividends vs. interest– Dividend imputation systems– Split rate systems and the dividend issue– Withholding tax – Subpart F implications

15

Global Cash Management Ltd..Grant Thornton International 28

Intercompany Flows (3)

• Foreign Tax Credits– Withholding taxes and the direct foreign tax

credit– Indirect foreign tax credit– The global foreign tax credit limitation

baskets– Required expense allocations and

apportionments– Excess foreign tax credit positions

Global Cash Management Ltd..Grant Thornton International 29

Intercompany Flows (4)

• Subpart F– Implications of intermediate dividend receiving

holding companies– Subpart F high tax kickout exception for

dividends– Subpart F same country exception for dividends– 956A in intercompany pooling/centralized

offshore investing

16

Global Cash Management Ltd..Grant Thornton International 30

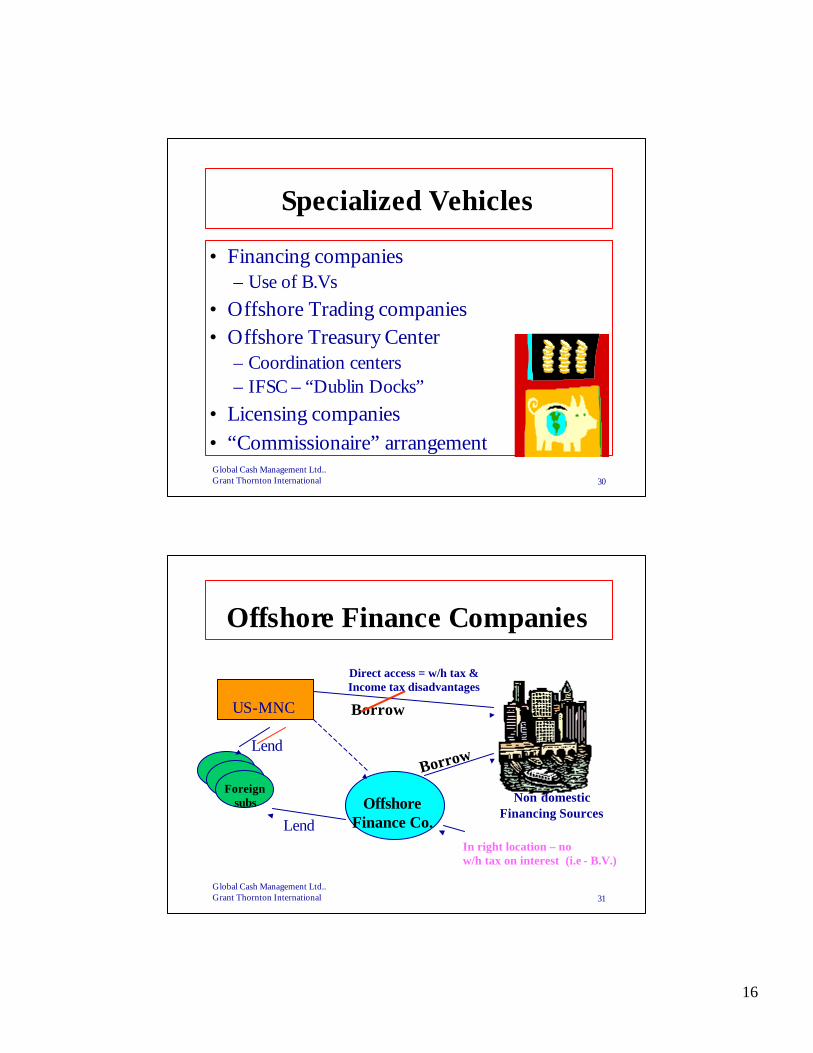

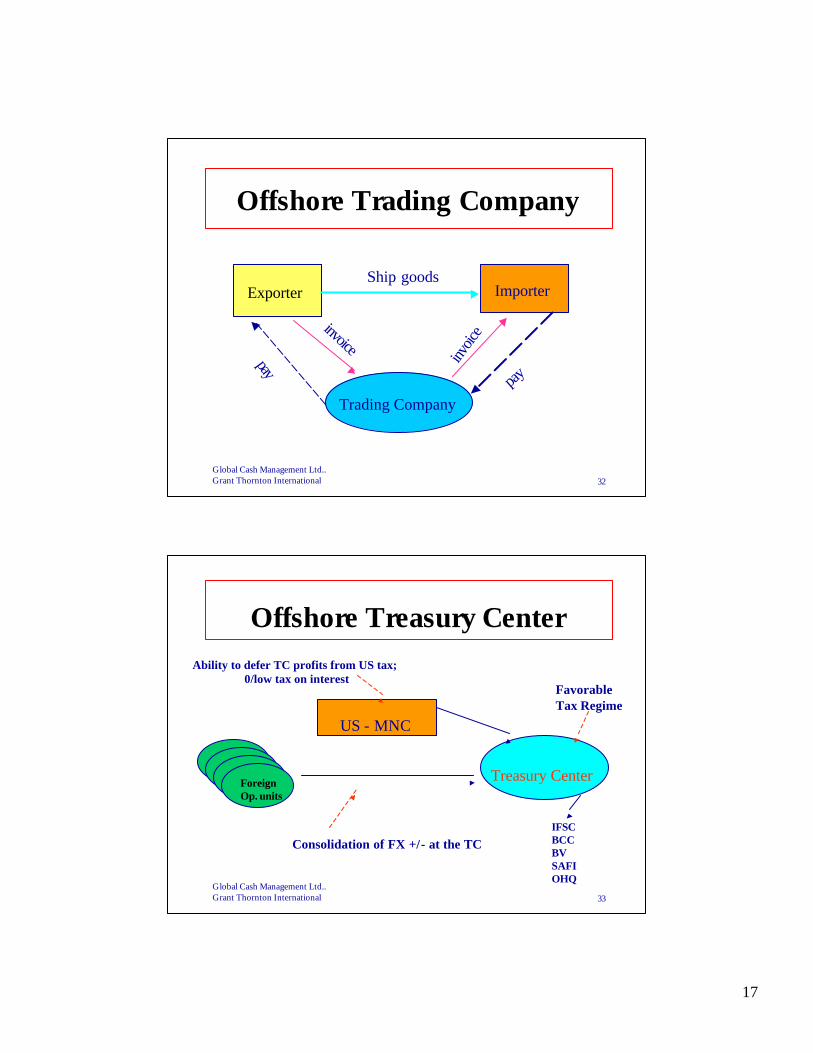

Specialized Vehicles

• Financing companies– Use of B.Vs

• Offshore Trading companies• Offshore Treasury Center

– Coordination centers– IFSC – “Dublin Docks”

• Licensing companies• “Commissionaire” arrangement

Global Cash Management Ltd..Grant Thornton International 31

Offshore Finance Companies

US-MNC

OffshoreFinance Co.

Non domesticFinancing Sources

Direct access = w/h tax &Income tax disadvantages

Borrow

Foreign subs

Borrow

LendIn right location – now/h tax on interest (i.e - B.V.)

Lend

17

Global Cash Management Ltd..Grant Thornton International 32

Offshore Trading Company

Exporter Importer

Trading Company

Ship goods

invoice

invoic

e

pay

pay

Global Cash Management Ltd..Grant Thornton International 33

Offshore Treasury Center

US - MNC

Treasury CenterForeignOp. units

Consolidation of FX +/- at the TC

FavorableTax Regime

Ability to defer TC profits from US tax; 0/low tax on interest

IFSCBCCBV SAFIOHQ

18

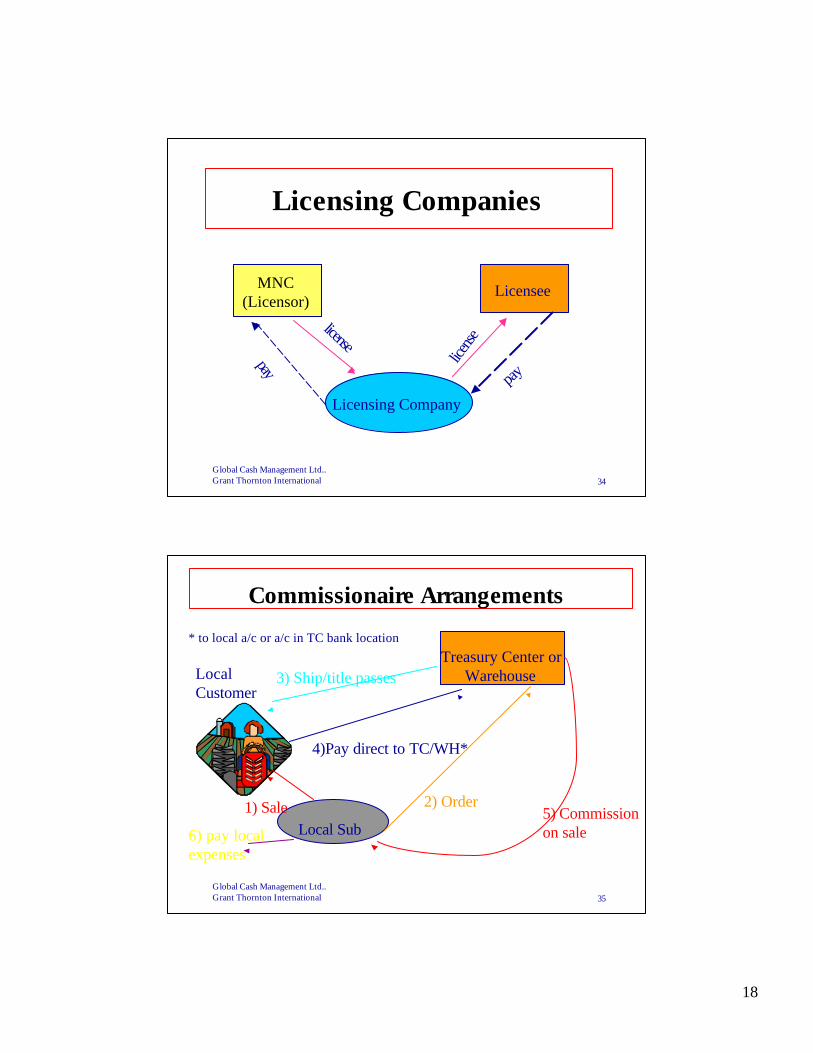

Global Cash Management Ltd..Grant Thornton International 34

Licensing Companies

MNC(Licensor)

Licensee

Licensing Company

license

licen

se

pay

pay

Global Cash Management Ltd..Grant Thornton International 35

* to local a/c or a/c in TC bank location

Treasury Center orWarehouse

Local Sub

3) Ship/title passes

1) Sale 2) Order

4)Pay direct to TC/WH*

5) Commission on sale

LocalCustomer

6) pay localexpenses

Commissionaire Arrangements

19

Global Cash Management Ltd..Grant Thornton International 36

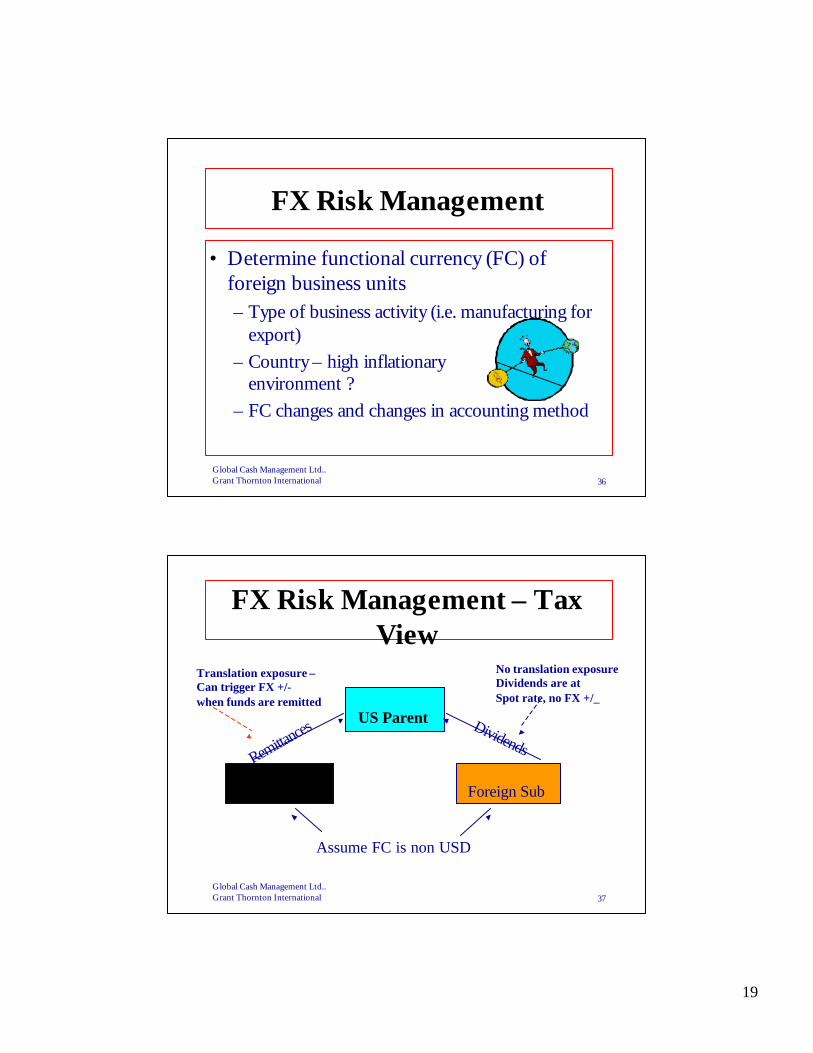

FX Risk Management

• Determine functional currency (FC) of foreign business units– Type of business activity (i.e. manufacturing for

export)– Country – high inflationary

environment ?– FC changes and changes in accounting method

Global Cash Management Ltd..Grant Thornton International 37

FX Risk Management – Tax View

US Parent

Foreign Branch Foreign Sub

Translation exposure –Can trigger FX +/-when funds are remitted

No translation exposureDividends are at Spot rate, no FX +/_

Remittances Dividends

Assume FC is non USD

20

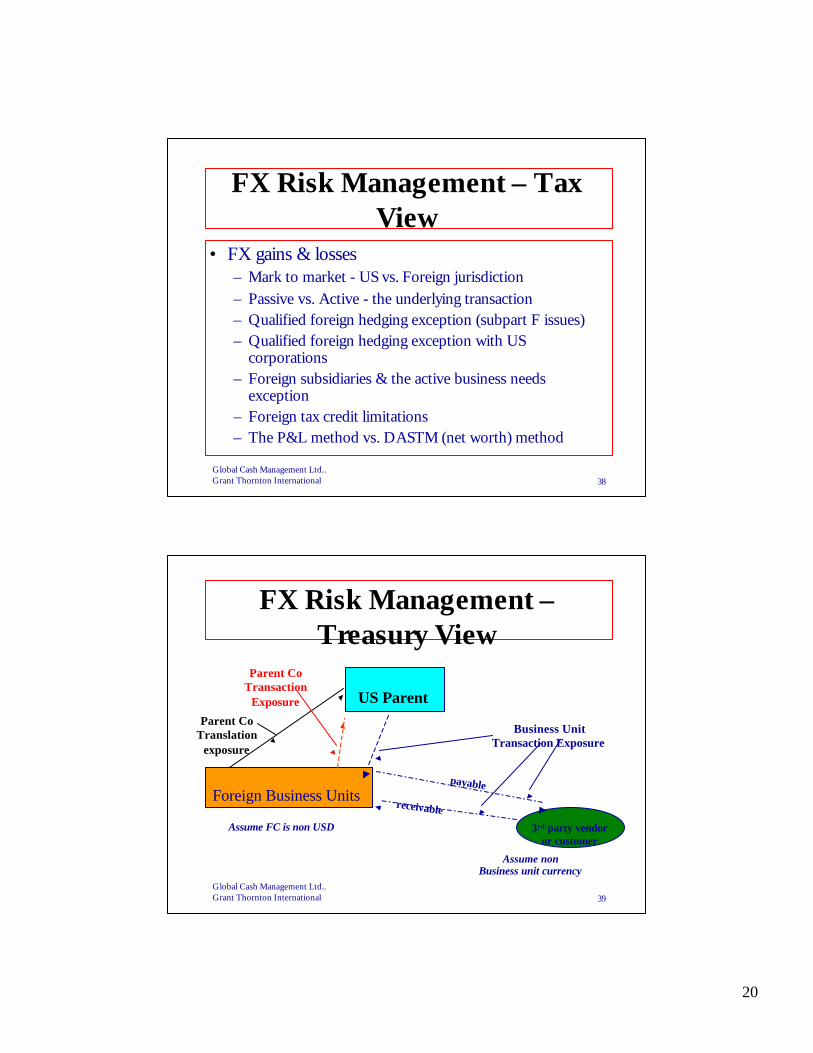

Global Cash Management Ltd..Grant Thornton International 38

FX Risk Management – Tax View

• FX gains & losses – Mark to market - US vs. Foreign jurisdiction– Passive vs. Active - the underlying transaction– Qualified foreign hedging exception (subpart F issues)– Qualified foreign hedging exception with US

corporations– Foreign subsidiaries & the active business needs

exception– Foreign tax credit limitations– The P&L method vs. DASTM (net worth) method

Global Cash Management Ltd..Grant Thornton International 39

FX Risk Management –Treasury View

US Parent

Foreign Business Units

Assume FC is non USD 3rd party vendoror customer

receivable

Parent CoTranslation

exposure

Parent CoTransaction

Exposure

Business UnitTransaction Exposure

payable

Assume nonBusiness unit currency

21

Global Cash Management Ltd..Grant Thornton International 40

FX Risk Management –Treasury View

• Protect profit/shareholder value• Natural offsets• Policy & Procedures

– Accountability• Hedging

– Objectives/philosophy• Centralizing risk

– Mechanics – Offset of FX +/-

Global Cash Management Ltd..Grant Thornton International 41

Summary

+

Treasury

Tax

22

Global Cash Management Ltd..Grant Thornton International 42

Summary

• Tax planning impacts how Treasury will– Manage cash flows– Structure financing & credit facilities– Interface with foreign operations

• Ongoing coordination with tax ensures– Logical set up of specialized vehicles– Tax effective solutions for liquidity management

challenges