Embed Size (px)

Citation preview

ORDINANCE OR LAW

All of the causes of loss forms contain an exclusion for the extra costs associated with the enforcement of any

ordinance or law regulating the construction, use or repair of any property or requiring the tearing down of any

property, including the cost of removing its debris.

B. Exclusions

1. We will not pay for loss or damage caused directly or indirectly by any of the following. Such

loss or damage is excluded regardless of any other cause or event that contributes concurrently or in any

sequence to the loss.

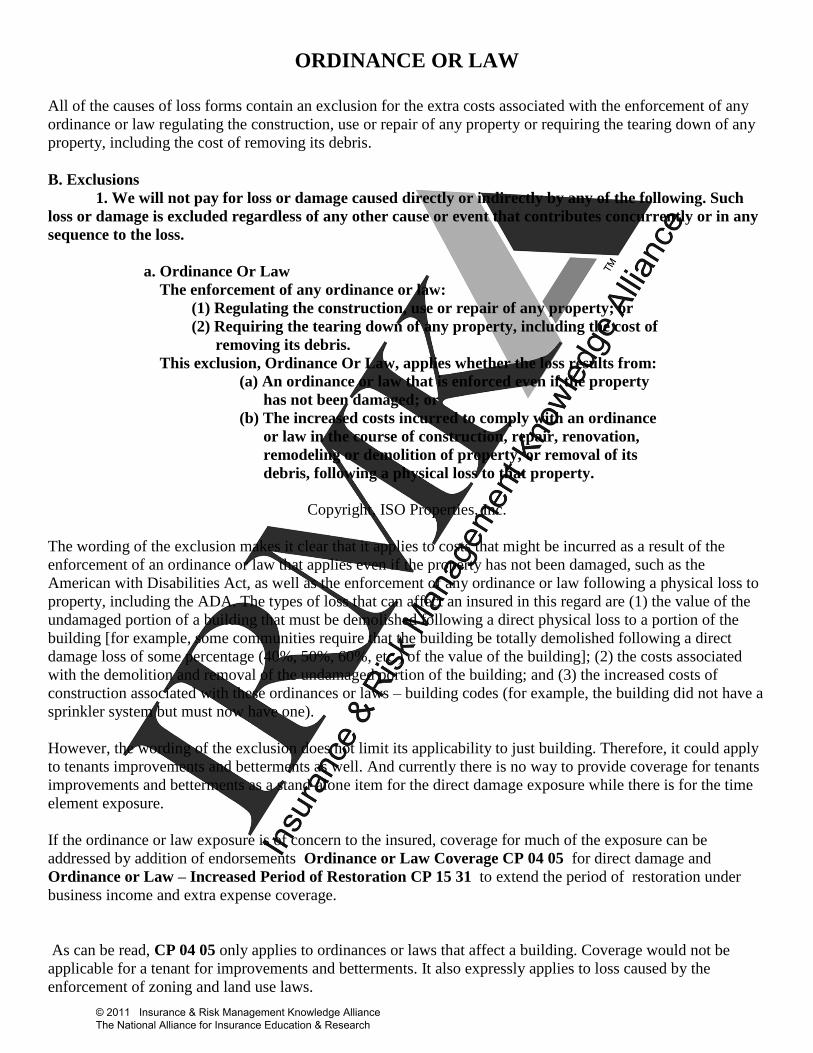

a. Ordinance Or Law

The enforcement of any ordinance or law:

(1) Regulating the construction, use or repair of any property; or

(2) Requiring the tearing down of any property, including the cost of

removing its debris.

This exclusion, Ordinance Or Law, applies whether the loss results from:

(a) An ordinance or law that is enforced even if the property

has not been damaged; or

(b) The increased costs incurred to comply with an ordinance

or law in the course of construction, repair, renovation,

remodeling or demolition of property, or removal of its

debris, following a physical loss to that property.

Copyright, ISO Properties, Inc.

The wording of the exclusion makes it clear that it applies to costs that might be incurred as a result of the

enforcement of an ordinance or law that applies even if the property has not been damaged, such as the

American with Disabilities Act, as well as the enforcement of any ordinance or law following a physical loss to

property, including the ADA. The types of loss that can affect an insured in this regard are (1) the value of the

undamaged portion of a building that must be demolished following a direct physical loss to a portion of the

building [for example, some communities require that the building be totally demolished following a direct

damage loss of some percentage (40%, 50%, 60%, etc.) of the value of the building]; (2) the costs associated

with the demolition and removal of the undamaged portion of the building; and (3) the increased costs of

construction associated with these ordinances or laws – building codes (for example, the building did not have a

sprinkler system but must now have one).

However, the wording of the exclusion does not limit its applicability to just building. Therefore, it could apply

to tenants improvements and betterments as well. And currently there is no way to provide coverage for tenants

improvements and betterments as a stand-alone item for the direct damage exposure while there is for the time

element exposure.

If the ordinance or law exposure is of concern to the insured, coverage for much of the exposure can be

addressed by addition of endorsements Ordinance or Law Coverage CP 04 05 for direct damage and

Ordinance or Law – Increased Period of Restoration CP 15 31 to extend the period of restoration under

business income and extra expense coverage.

As can be read, CP 04 05 only applies to ordinances or laws that affect a building. Coverage would not be

applicable for a tenant for improvements and betterments. It also expressly applies to loss caused by the

enforcement of zoning and land use laws.

© 2011 Insurance & Risk Management Knowledge Alliance The National Alliance for Insurance Education & Research

The coverage is only applicable to the ordinances and laws applicable to demolition, construction, repair,

zoning or land use that are in effect at the time of loss at the described premises. If one or more of these

changed as a result of the loss, but were not in effect at the time of loss, coverage would not apply. And, even

when coverage applies, it only applies to the minimum requirements.

The building must sustain direct physical loss or damage from a Covered Cause of Loss. However, it is possible

for coverage to apply if the building sustains direct physical loss or damage from a covered cause of loss as well

as from an uncovered cause of loss. (If this occurs, a proportionate loss payment will apply; example is shown

later in this article.) However, if the covered direct physical damage alone would have resulted in enforcement

of the ordinance or law, then the full amount of loss otherwise payable will be paid.

Excluded from coverage is the enforcement of any ordinance or law that results from pollution (as defined) or

fungus (as defined), wet or dry rot or bacteria as well as costs associated with testing for, monitoring, cleaning

up, removing, containing, treating, detoxifying or neutralizing, or in any way responding to or assessing the

effects of these.

The coverage specifically provided is for:

Loss to the Undamaged Portion of the Building

Demolition Cost

Increased Cost of Construction Coverage

Loss to the Undamaged Portion of the Building is included within the Limit of Insurance for the building. There

is no need to modify existing limits.

Demolition Cost Coverage will pay the cost to demolish and clear the site of undamaged parts of the same

building. Coinsurance does not apply to this coverage. A separate limit of insurance may apply.

Increased Cost of Construction will pay the increased cost to repair or reconstruct damaged portions of the

building in accordance with the minimum requirements of the ordinance or law as well as the increased cost to

reconstruct or remodel undamaged portions of the building whether or not demolition is required. But the

restored or remodeled property must be intended for similar occupancy as the current property (unless such

occupancy is not permitted by zoning or land use ordinance or law). And the increased cost of construction will

not be paid if the building is not repaired, reconstructed or remodeled. Coinsurance does not apply to this

coverage either. A separate limit of insurance may apply.

In addition, a single Limit of Insurance may apply to both Demolition Cost Coverage and Increased Cost of

Construction. If coverage is written in this manner, the Limit of Insurance may be used as needed for either of

these loss exposures.

Coverage is added for certain types of property that are normally considered Property NOT Covered:

Cost of excavations, grading, backfilling and filling

Foundation of the building

Pilings

Underground pipes, flues and drains

This means, for instance, that if there was a “law” that requires the building to be set back from the street 35

feet and, therefore, the foundation must be “moved”, coverage applies.

© 2011 Insurance & Risk Management Knowledge Alliance The National Alliance for Insurance Education & Research

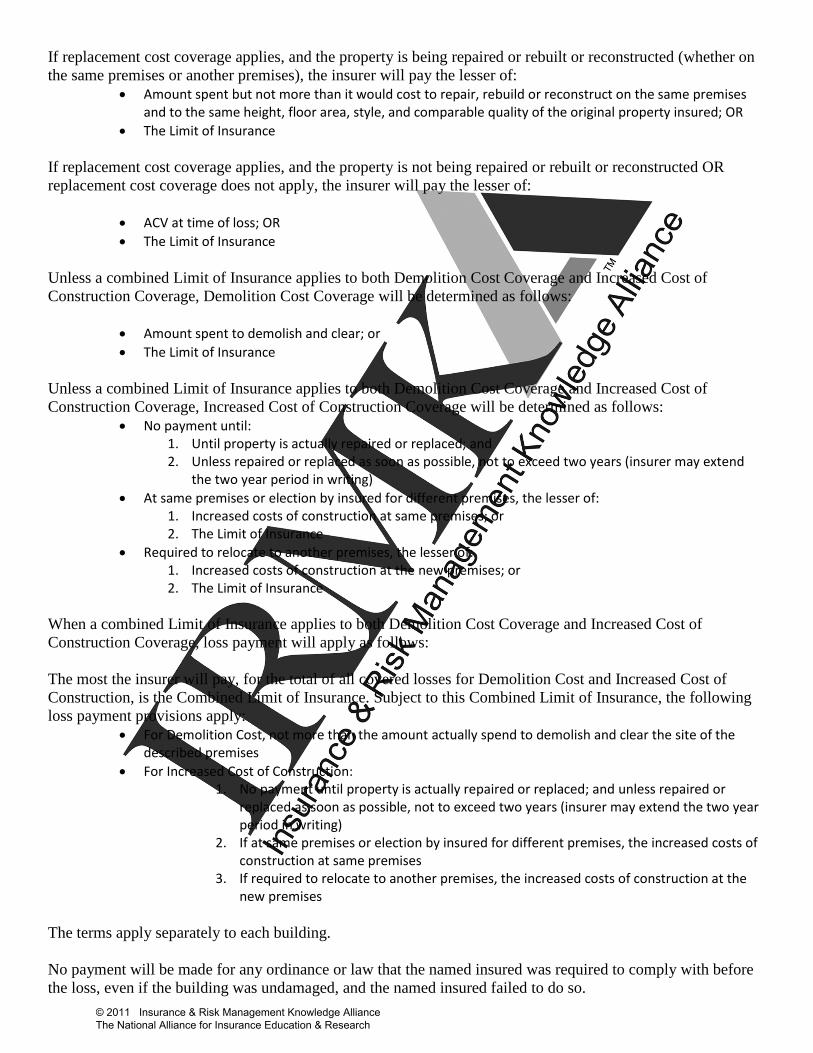

If replacement cost coverage applies, and the property is being repaired or rebuilt or reconstructed (whether on

the same premises or another premises), the insurer will pay the lesser of:

Amount spent but not more than it would cost to repair, rebuild or reconstruct on the same premises and to the same height, floor area, style, and comparable quality of the original property insured; OR

The Limit of Insurance

If replacement cost coverage applies, and the property is not being repaired or rebuilt or reconstructed OR

replacement cost coverage does not apply, the insurer will pay the lesser of:

ACV at time of loss; OR

The Limit of Insurance

Unless a combined Limit of Insurance applies to both Demolition Cost Coverage and Increased Cost of

Construction Coverage, Demolition Cost Coverage will be determined as follows:

Amount spent to demolish and clear; or

The Limit of Insurance

Unless a combined Limit of Insurance applies to both Demolition Cost Coverage and Increased Cost of

Construction Coverage, Increased Cost of Construction Coverage will be determined as follows:

No payment until: 1. Until property is actually repaired or replaced; and 2. Unless repaired or replaced as soon as possible, not to exceed two years (insurer may extend

the two year period in writing)

At same premises or election by insured for different premises, the lesser of: 1. Increased costs of construction at same premises; or 2. The Limit of Insurance

Required to relocate to another premises, the lesser of: 1. Increased costs of construction at the new premises; or 2. The Limit of Insurance

When a combined Limit of Insurance applies to both Demolition Cost Coverage and Increased Cost of

Construction Coverage, loss payment will apply as follows:

The most the insurer will pay, for the total of all covered losses for Demolition Cost and Increased Cost of

Construction, is the Combined Limit of Insurance. Subject to this Combined Limit of Insurance, the following

loss payment provisions apply:

For Demolition Cost, not more than the amount actually spend to demolish and clear the site of the described premises

For Increased Cost of Construction: 1. No payment until property is actually repaired or replaced; and unless repaired or

replaced as soon as possible, not to exceed two years (insurer may extend the two year period in writing)

2. If at same premises or election by insured for different premises, the increased costs of construction at same premises

3. If required to relocate to another premises, the increased costs of construction at the new premises

The terms apply separately to each building.

No payment will be made for any ordinance or law that the named insured was required to comply with before

the loss, even if the building was undamaged, and the named insured failed to do so.

© 2011 Insurance & Risk Management Knowledge Alliance The National Alliance for Insurance Education & Research

Example of Proportionate Loss Payment for Ordinance or Law Coverage Losses.

Assume:

Wind is a Covered Cause of Loss; Flood is an excluded Cause of Loss

The building has a value of $200,000

Total direct physical damage to building: $100,000

The ordinance or law in this jurisdiction is enforced when building damage equals or exceeds 50% of the building's value

Portion of direct physical damage that is covered (caused by wind): $30,000

Portion of direct physical damage that is not covered (caused by flood): $70,000

Loss under Ordinance or Law Coverage for Increased Cost of Construction: $60,000 Step 1:

Determine the proportion that the covered direct physical damage bears to the total direct physical damage.

$30,000 $100,000 = .30

Step 2:

Apply that proportion to the Ordinance or Law loss.

$60,000 x .30 = $18,000

In this example, the most that will be paid under this endorsement for the Increased Cost of Construction is

$18,000, subject to the applicable Limit of Insurance and any other applicable provisions.

Note: The same procedure applies to losses under Loss to the Undamaged Portion of the Building and

Demolition Cost Coverage.

When an ordinance or law affects the construction or repair of any property or requires the tearing down of

parts of any property not damaged by a Covered Cause of Loss and was in effect at the time of loss, the time

required for compliance will extend the period of restoration. However, the unendorsed business income and

extra coverage forms define “period of restoration” as:

3. "Period of restoration" means the period of time that:

a. Begins:

(1) 72 hours after the time of direct physical loss or damage for Business Income Coverage; or

(2) Immediately after the time of direct physical loss or damage for Extra Expense Coverage;

caused by or resulting from any Covered Cause of Loss at the described premises; and

b. Ends on the earlier of:

(1) The date when the property at the described premises should be repaired, rebuilt or replaced

with reasonable speed and similar quality; or

(2) The date when business is resumed at a new permanent location.

"Period of restoration" does not include any increased period required due to the enforcement of any

ordinance or law that:

(1) Regulates the construction, use or repair, or requires the tearing down, of any property; or

(2) Requires any insured or others to test for, monitor, clean up, remove, contain, treat, detoxify

or neutralize, or in any way respond to, or assess the effects of "pollutants".

The expiration date of this policy will not cut short the "period of restoration".

Copyright, ISO Properties, Inc.

CP 15 31 extends coverage to include the increased period of restoration due to the enforcement of any

ordinance or law that regulates the construction or repair, or requires the tearing down, of any property.

The coverage is only applicable to the ordinances and laws that are in effect at the time of loss at the described

premises. If one or more of these changed as a result of the loss, but were not in effect at the time of loss,

coverage would not apply. And, even when coverage applies, it only applies to the minimum requirements. © 2011 Insurance & Risk Management Knowledge Alliance The National Alliance for Insurance Education & Research

As with the direct damage coverage, this endorsement excludes from coverage the enforcement of any

ordinance or law that results from pollution (as defined) or fungus (as defined), wet or dry rot or bacteria as well

as costs associated with testing for, monitoring, cleaning up, removing, containing, treating, detoxifying or

neutralizing, or in any way responding to or assessing the effects of these.

Unlike CP 04 05, there is no specific language that addresses losses caused by enforcement of zoning and land

use requirements or loss caused by the enforcement of the Americans with Disabilities Act. This lack of

consistency could cause concern as to whether or not coverage is provided for losses caused by these types of

building ordinances. The Americans with Disabilities is a law that regulates the construction or repair of

property. If the zoning or land use requirements come within the parameters of coverage will depend upon if

they regulate the construction or repair of property or require the tearing down of parts of any property not

damaged by a Covered Cause of Loss.

If CP 04 05 is added to the direct damage “side” of coverage, CP 15 31 definitely should be added to the time

element “side”!

Edition 03/2011

© 2011 Insurance & Risk Management Knowledge Alliance The National Alliance for Insurance Education & Research