Embed Size (px)

Citation preview

Page 1 of 30

WTM/PS/46 /CFD/NOV/2014

BEFORE THE SECURITIES AND EXCHANGE BOARD OF INDIA

CORAM : PRASHANT SARAN, WHOLE TIME MEMBER

DECISION

On the Representation dated January 16, 2012 filed by Mr. Amit Bhagvatprasad Barot

Proceedings in compliance with the directions of the Hon'ble Securities Appellate

Tribunal made vide Order dated September 03, 2013 in the matter of Amit Bhagvatprasad

Barot vs. Securities and Exchange Board of India (Appeal No. 157 of 2012)

1. The instant proceeding is in compliance with the directions of the Hon'ble Securities

Appellate Tribunal (hereinafter referred to as "the Hon'ble SAT") made vide Order dated

September 03, 2013 in Appeal No. 157 of 2012 (Amit Bhagvatprasad Barot vs. Securities and Exchange

Board of India). Vide the Order, the Hon'ble SAT, inter alia observed and directed the Securities

and Exchange Board of India (hereinafter referred to as "the SEBI") as follows :

"……… We set aside impugned order dated 8th June, 2012 and direct SEBI to reconsider complaint of

appellant dated 16th January, 2012 afresh and pass appropriate orders as it deems fit. We make it clear that we

have not expressed any opinion on merits of the case………." {Emphasis supplied}

2. Background of the matter :

As the said application made by Mr. Amit Bhagvatprasad Barot is with respect to an open

offer made to acquire shares of the Target Company, Global Offshore Services Limited, it is

necessary to note the facts of the said open offer and the subsequent events before dealing with

the application :

(a) On November 6, 2007, India Star (Mauritius) Limited (hereinafter referred to as "the

Acquirer"), a public shareholder of Global Offshore Services Limited (previously known as

"Garware Offshore Services Limited") {hereinafter referred to a "Target Company"}, acquired

22,72,727 equity shares representing 9.54% of the paid up equity share capital of the Target

Company, through conversion of 25,00,000 Unsecured Optionally Convertible Debentures ("the

Page 2 of 30

OCDs"). This acquisition resulted in the increase in the shareholding of the Acquirer from

12.07% to 20.42% of the paid-up voting equity share capital of the Target Company triggering

regulation 10 of the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 1997

("the Takeover Regulations").

(b) Accordingly, the Acquirer, through HSBC Securities and Capital Markets Private

Limited ("the Merchant Banker") made an open offer vide Public Announcement dated

November 07, 2007 to acquire 20% of the share capital of the Target Company. The offer

opened on March 19, 2008 and closed on April 07, 2008. From the Post-offer Public

Announcement made on May 26, 2008, the following is inter alia noted :

Offer price per equity share `234.67/- including interest of `4.67/-

Shares acquired in the open offer 23,98,201 shares (10.06%)

Size of the offer (20% of voting capital) `56.28 crores

Post offer shareholding of the Acquirer 72,60,928 shares (30.48%)

(c) Complaint filed by Mr. Amit Bhagvatprasad Barot :

After almost 4 years, one Mr. Amit Bhagvatprasad Barot (hereinafter referred to as the

"applicant" or "complainant"), through M/s. Prism Partners, Advocates, filed a representation

dated January 16, 2012, inter alia stating the following :

(i) The applicant is a shareholder in the Target Company and has been holding 1,560 equity

shares, before, during and after the Open Offer made by the Acquirer. He did not tender the

equity shares in the Open Offer.

(ii) The applicant came across a press release dated August 16, 2011, in which it has been

stated that Sycamore Ventures and IFCI Limited, one of India's premier financial institutions,

have agreed to jointly launch the "IFCI-Sycamore Infrastructure Fund". On a review of the

information available, it has come to light for the first time that Sycamore Ventures is actually

the beneficial owner of the equity shares held in the Target Company through the Acquirer. A

copy of the press release dated August 16, 2011 was enclosed.

Page 3 of 30

(iii) The Acquirer and the Manager to the Open Offer did not make full disclosures as

required under the Takeover Regulations and on the contrary have withheld material

information, which resulted in projecting a clean image of the Acquirer because of which many

investors like the applicant took a decision not to tender their equity shares in the Open Offer.

Had the Acquirer and the Manager disclosed true and correct information, which were required

to be disclosed in the Letter of Offer ("the LOF"), the decision of the Acquirer would have been

different.

(iv) The applicant referred to the disclosures made in paragraphs 2.1 (a) i) {Background of the

offer}and also paragraph 3 (b) a) & b) of the LOF and contended as follows :

Contentions :

(1) The Acquirer and the Manager failed to make disclosure of the material information with

regard to the background of the Acquirer as required in the standard LOF format stipulated by

SEBI vide Circular dated March 08, 2004. In terms of paragraph 4 of the said SEBI Circular, it is

stated that in relation to the background of the acquirer, disclosures pertaining to the

identification of the promoters and or persons having control over such companies and the

group, if any, to which such companies belong to, should be disclosed. The relevant extract of the

said SEBI Circular was referred to :

" 4 Background of the Acquirer

….

4.1 If acquirer(s) (including PACs) is a company

…..

4.1.4 Brief history and major areas of operation

4.1.5 Identity of the promoters and or persons having control over such companies and the group if any, to which

such companies belong to."

(2) Sycamore Ventures, at the time of the Open Offer, was and continues to be in control of

the Acquirer as evidenced by the following facts :

(i) As per the date available on the website of "trademarkia.com", which is a search engine

for United States trademark, it is found that "indiaStar" is a mark owned and registered

Page 4 of 30

by Sycamore Management Corporation located in Princeton, New Jersey. Copy of the

above data was enclosed.

(ii) On a perusal of the information available on the website of Sycamore Ventures, it is

found that 'indiaStar Fund' is one of the funds of Sycamore Ventures and the Acquirer

was in fact controlled by Sycamore Ventures. Copy of the data was enclosed.

(3) However, the fact that Sycamore Ventures was controlling the Acquirer, was not

disclosed and the consequential disclosures pertaining to Sycamore Ventures including their track

record, litigations etc were also avoided.

(4) In the absence of the material information on beneficial owners and persons and the

group that is actually in control of the equity shares and voting rights of the Target Company, the

intentions of the Acquirer and the persons in control of the Acquirer, their investment

philosophy, intention to control the management and policy decisions and whether they support

the board of directors through their international experience or whether they are in joint control

with the promoters were not known. In the absence of this material information, there was an

intention to wilfully mislead the shareholders and hence an informed decision could not have

been taken on the impugned open offer made by the Acquirer.

(5) The correct background of one of the directors of the Acquirer i.e., Mr. Ravi Pratap

Singh, was deliberately withheld. As per the LOF, the experience of Mr. Ravi Pratap Singh is

disclosed as under :

"Ravi Singh is a partner with Sycamore Ventures. Over the course of his 25 year career, he has structured and led

numerous public and private financings, mergers and acquisitions and global investments. In the past he held

successive positions as a Manager with Coopers and Lybrand in New York (now Pricewaterhouse Coopers,

General Partner and Managing Director at Cowen & Company (now SG Cowen) ; Managing Director of

Forbes and Walker, a New York Merchant banking firm; Partner, Managing Director and Head of Technology

Investment Banking at Punk, Ziegel & Company and Founding Partner of Converge Partners LLC, a New

York based investment advisory firm."

However, according to the applicant, the following facts about Ravi Pratap Singh, who is in fact

responsible for the Acquirer (as per the information of Sycamore Ventures itself – refers to Exhibit 6 of the

application) have been deliberately withheld:

Page 5 of 30

(i) Mr. Singh's experience in Silverline Technology Limited ("Silverline") is disclosed

in other reports, whereas it has been withheld from the LOF with ulterior motives, as

his association with Silverline would raise the 'antennae' in the minds of the

shareholders and SEBI in view of the dubious track record of Silverline and its

association with the securities scam.

(ii) There were law suits for negligent misrepresentation, fraudulent misrepresentation

and securities laws violations by Sera Nova (a company taken over by Silverline) and the

promoters of Sera Nova including Mr. Ravi Pratap Singh.

(iii) Dahava Resources Limited of which Mr. Ravi Pratap Singh was the CEO had

violated securities laws and a "Cease Trade Order" was passed by the Canadian

regulators.

(6) The omission/withholding of the above information were deliberate and with ulterior

motives, as the LOF itself was signed by Ravi Pratap Singh as Managing Director of the

Acquirer.

(7) The Acquirer and its Managing Director Mr. Ravi Pratap Singh have committed a 'fraud'

in that, there has been a 'concealment of material fact in order that another person may act to his

detriment'; 'an active concealment of a fact by a person having knowledge or belief of the fact' ;

'deceptive behaviour by a person depriving another of informed consent or full participation' and

hence they have also violated the provisions of the SEBI (Prohibition of Fraudulent and Unfair

Trade Practices Relating to Securities Market) Regulations, 2003 ("the PFUTP Regulations") and

the Securities and Exchange Board of India Act, 1992 ("the SEBI Act").

Remedies sought by the applicant :

(i) As a shareholder, the applicant has a statutory right to true and adequate disclosure to

make an informed decision. This statutory right has been violated by the Acquirer with ulterior

motives and hence the applicant is entitled to a status quo ante vis-à-vis the Open Offer.

(ii) The withholding of the material information had a critical impact on the decisions of the

shareholders, as against the offer of 20% in the Open Offer, the Acquirer could garner only

10.06% of the equity shares, thus leaving the Open Offer under subscribed. Had true and

Page 6 of 30

adequate disclosures been made, the outcome could have been different, particularly the fact that

the Managing Director of the Acquirer, Mr. Ravi Pratap Singh was associated with Silverline

which was a so called "K-10 stocks" and was involved in the Ketan Parekh scam.

(iii) The Acquirer has employed and devised a scheme and artifice to defraud the

shareholders of the Target Company while dealing in its securities. It has also engaged itself in

an act and practice to defraud and deceive the shareholders of the Target Company. In

consideration of the facts and circumstances mentioned above, it is contended that the Acquirer

is in violation of regulation.

(iv) In view of facts and circumstances, the applicant requested SEBI to –

(i) Order the Acquirer to make another open offer and provide an opportunity to the

shareholders to take an informed decision whether to tender or not to tender their equity

shares.

(ii) Such offer be directed to be made by the Acquirer at the same price paid to the

shareholders in the impugned Open Offer plus interest from the due date of payment in

the impugned offer to the date of payment at the rate decided by SEBI.

(iii) Take punitive action against the Acquirer and its director including Mr. Ravi Pratap

Singh, the Managing Director.

(iv) Direct the Acquirer not to transfer, alienate or otherwise dispose of its shareholding in

the Target Company until the matter is reviewed by SEBI and orders are passed, as the

applicant apprehends that they may sell off their shareholding and avoid actions by SEBI,

which would be highly prejudicial to the interests of the applicant

(v) Pass such additional orders against the Acquirer and its directors, as SEBI may deem fit.

3. SEBI had also received several other complaints in the matter. The complaints were

examined and vide SEBI letter dated June 08, 2012, addressed to the complainants including the

applicant, SEBI inter alia replied that -

"….. it is disclosed at Para 3(g) of the Letter of Offer that the Acquirer is a privately held limited liability

company and is a wholly owned subsidiary of indiaSTAR Fund L.P., a limited partnership. Further, the

Page 7 of 30

fact regarding association of Mr. Ravi Pratap Singh, one of the directors of the board of directors of the target

company, with Sycamore Venture has been disclosed at Para 3(f) of the Letter of Offer.

3. In view of the above, there appears that the acquirer has not violated any of the provisions of SEBI (SAST)

Regulations, 1997 as alleged by the complainants. Hence, the question of SEBI giving any further directions

to the Acquirer does not arise."

4. The applicant filed an appeal before the Hon'ble Securities Appellate Tribunal in Appeal

No. 157 of 2012 challenging the aforesaid reply of SEBI, which was disposed off by the Hon'ble

SAT vide Order dated September 03, 2013, wherein the Hon'ble SAT had directed SEBI to

reconsider the applicant's representation and pass fresh orders. This Order of the Hon'ble SAT

has been mentioned in paragraph 1 above.

5. Thereafter, the applicant through his counsel, forwarded another letter dated September

12, 2013 inter alia stating the following :

(i) The allegations made and irregularities committed by the Acquirer i.e., India Star

(Mauritius) Limited are the ones which the applicant had noticed till the date of his complaint

dated January 16, 2012. However, in the reply (to the appeal of the applicant) filed by the

Acquirer, new disclosures were made, which proved the extent to which the Acquirer had

suppressed information from the shareholders of the target Company while making the open

offer.

(ii) The new disclosures which the Acquirer made in its Affidavit before the Hon'ble SAT are

as under :

(a) IndiaStar Fund LP ("ISLP"), the partnership firm which owns 100% of the

Acquirer is itself a 'pooling vehicle' and the Acquirer is a "special purpose vehicle".

(b) The actual owners of the funds for the purchase of the shares of the Target

Company were other investors of ISLP from various countries and such investors are the

'limited partners' of ISLP and the investment in the shares was made on their behalf and

they are the 'principal beneficiaries' thereof. However, even now, the identity of such

'limited partners' who are admitted to be the actual beneficiaries is still not disclosed.

(c) The funds contributed by the 'limited partners' have been invested by the 'general

partners' for the purchase of shares of the Target Company. However, even now, the

identity of such general partners is still not disclosed.

Page 8 of 30

(d) ISLP is administered, managed and supervised by the Sycamore Management

Corporation and pursuant to some agreement dated March 13, 2006.

(iii) Though the applicant asked for a copy of the agreement (pursuant to which ISPL is

administered, managed and supervised by Sycamore Management Corporation), the Acquirer

refused to disclose such agreement. The Acquirer continues to suppress this information.

(iv) None of the obviously relevant facts have been disclosed in the LOF. Even now the true

identity of the beneficial owners of the Acquirer and the investment in the Target Company has

not been disclosed and the identity of the 'persons having control over such companies' has not

been disclosed as required by clause 4.1.5 of SEBI's circular dated March 08, 2004. Ex-facie this is

a gross and wilful suppression.

(v) What is ex-facie evident from the aforesaid is the deep and pervasive control of Sycamore

group over the Acquirer and ISLP. As stated, the Acquirer, in its affidavit before the Hon'ble

SAT, has admitted that Sycamore Management Corporation is actually in management and

supervision of ISLP. ISLP 100% owns and controls the Acquirer. Sycamore Venture claims that

IndiaStar Fund is its investment and is within its portfolio. Sycamore Management Corporation

owns the name/trademark "IndiaStar Fund". The LOF does disclose that the Acquirer's director

Mr. John Whitman is a Managing Partner of "SMC" (now disclosed as Sycamore Management

Corporation) and that the director, Ravi Pratap Singh is a partner of Sycamore Ventures and that

director David Lichtenstein is the CFO of Sycamore Ventures. The Acquirer is beyond doubt a

part of the "Sycamore Group" but this was never disclosed in the LOF in violation of Clause

4.1.5 of the aforesaid SEBI Circular.

(vi) In its affidavit, the Acquirer while admitting that one Richard Chong was an employee of

Sycamore Management Corporation, and that he is being investigated by the authorities in the

USA for money laundering offences, it is stated that Sycamore Ventures/Sycamore Management

Corporation is not involved in the same. However, the report of the Permanent Sub-Committee

on Investigations of the United States Senate, which deals with the said money laundering

allegations does contain references to Sycamore Ventures and Mr. Chong's transfer of funds to

Sycamore Venture Capital LP, in which Mr. Chong was a partner.

Page 9 of 30

(vii) There was gross, wilful and fraudulent suppression in the LOF. The complete relevant

facts were not disclosed as required by the Takeover Regulations and the aforesaid SEBI

Circular. New additional highly relevant facts have been disclosed by the Acquirer only now.

(viii) In view of the above mentioned circumstances, SEBI should consider the new

disclosures now made by the Acquirer for the first time (which were not disclosed in the LOF),

while passing fresh orders.

(ix) The suppression of information by the Acquirer in the open offer had a critical impact on

the decisions of shareholders, whether to tender their shares in the Open Offer. Therefore, in the

interest of justice and equity, the applicant requested SEBI to direct the Acquirer to make a fresh

open offer and provide an opportunity to shareholders to take an informed decision whether to

tender its shares or not in the fresh open offer.

(x) It is also relevant for SEBI to note that as per the Economic Times Newspaper dated

May 13, 2013, it is noted that Germany's DVB Bank is in advanced talks with the Acquirer to

purchase 20% stake in Target Company(GOSL). It is therefore clear that Acquirer is making

efforts to exit its holding in GOSL and if such exit happens, the prayer made by the applicant

would become infructuous. SEBI may therefore pass appropriate orders against the Acquirer

restraining it from exiting GOSL.

6. Thereafter, vide letter dated October 14, 2013, the applicant through his counsel

requested SEBI to inform him regarding the status of his complaint and whether any steps were

taken to restrain the Acquirer from exiting the Target Company.

7. The Merchant Banker, HSBC Securities and Capital Markets (India) Private Limited, vide

letter dated October 28, 2013 (this reply was in respect of the SEBI letter dated September 18, 2013

enclosing complaints received from certain shareholders (including the applicant) of the Target Company against the

Acquirer) inter alia stated the following :

A. Nature of the acquisition : (i) The stake of the Acquirer in the Target company was primarily in the nature of financial

investment and not held with the intent to control the management or policy decision of the

target company (as disclosed in paragraph 2.1(a) of the letter of offer) and accordingly the offer

was made under Regulation 10 of the Takeover Regulations and not under Regulation 12 even

Page 10 of 30

though the acquirer would be the single largest shareholder of the target company pursuant to

the open offer.

(ii) As disclosed in paragraphs 2.1(a) and 5(m) of the letter of offer, the acquirer did not have

any representation on the Board of the target company and did not intend to appoint its

representatives on the Board of Directors of the Target company in the future.

(iii) The acquirer shareholding of the Target Company is classified as public for the quarter

ended September 2013 as per disclosures made by the Target Company to the BSE.

B. Due Diligence (i) It has complied with the disclosure requirements and specifically the requirements

notified by SEBI to merchant bankers vide SEBI circular dated March 8, 2004. The

requirements imposed by SEBI inter alia require disclosure of the acquirer the brief history and

major areas of operation, identity of the promoters and the group to which the companies

belong. Para 3 of the letter of offer contains all necessary disclosure in this regard.

(ii) For the disclosures made in the letter of offer, it had relied on the information provided

by the acquirer in response to a request for such disclosure made by it.

(iii) As per the standard practice it obtained information and certificates from the acquirer in

relation to the information provided by the acquirer in the letter of offer. The last page of the

letter of offer conclusively establishes that the onus of correctness and accuracy of the

information provided to the manager to an open offer is on the acquirer.

(iv) As disclosed in the letter of offer (paragraph 3(b) the Acquirer was 100% owned by

IndiaSTAR Fund L.P. (ISLP or IndiaStar Fund), a limited liability partnership. ISLP is a fund

established to make equity and equity linked investments in growth companies with significant

interest in the Indian Subcontinent. This fund therefore an independent fund which has been

established to make investments in India. The Acquirer acts as an investment holding company

for IndiaSTAR Fund for all investments undertaken by the said fund. The ownership of the

trade mark (as alleged in the additional representation dated September 12, 2013) does not demonstrate

control by Sycamore. The practice in open offers does not mandate the disclosures of all

entities up the chain. Such disclosures of the holding companies are made typically when the

acquirer in question is being funded by such holding companies or is otherwise relying on the

Page 11 of 30

financial wherewithal of such holding company which was not the case with respect to this open

offer. Therefore, disclosures regarding the acquirer and immediate parent were considered

sufficient to meet the disclosure requirements under the Takeover Regulations.

(v) Further, as disclosed to SEBI vide letter dated January 30, 2008, it had provided the

following additional details on IndiaSTAR Fund.

"IndiaStar Fund L P is professionally managed broad based fund registering in the Cayman Islands as an

exempted limited partnership (the 'Fund" or the "Partnership"). The fund invests in growth companies with

potential for significant value appreciation utilizing a private equity discipline. IndiaStar Partner LP is registered

as the General Partner of the Partnership. In addition, the partnership has 38 limited partners, comprised of the

institutions, insurance companies, trusts and foundations and high net worth foreign individuals, principally based

in the US and Japan.

The Agreement of Limited Partnership between Indiastar Partners LP as the General Partner and 38 limited

partners of the Partnership states that "The limited partners shall take no part in the control or management of

the business or affairs of the Partnership nor shall the limited partners have any authority to act for or on behalf of

the Partnership or otherwise in respect of Partnership matters". Accordingly, Indiastar Partners LP, as the

General Partner of the Fund, has complete authority and responsibility for the management of Indiastar Partner

LP (should be read as 'IndiaStar Fund LP', as informed by the Merchant Banker). The sole general partner of

Indiastar Partner LP is Sycamore Management Corporation, 845 Alexander Road, Princeton, NJ 08540,

USA, a highly reputable professional investment management firm (SMC). Furthermore SMC has formed and

authorised an Investment Committee comprised of three members to manage all of the investment activities and

business matters of the fund".

(vi) In addition to the disclosures made by the acquirer, an independent due diligence was

conducted on the acquirer, its directors including Mr. Ravi Pratap Singh. The same was done for

ascertaining whether there is any adverse information which ought to be disclosed in the letter of

offer.

(vii) For carrying out such due diligence it utilised a system which involves carrying out a

search on an online database known as World Check. World Check creates and maintains a

database of heightened risk individuals and organisations. This database is used by organisations

around the world to help identify and manage financial, regulatory and reputational risks. Based

Page 12 of 30

on statistics, World Check provides practical intelligence for informed decision making, useful

for mergers and acquisitions, security of supply chain, cross border expansion and exploration

and production. It reports deliver a detail background check on any entity or individual no matter

where they are located in the world.

(viii) Like in all cases, HSBC Securities being the manager to the open offer in the present case

also conducted a background check on the acquirer and its directors. The search did not reveal

any adverse information against the acquirer and Mr. Ravi Pratap Singh. Even now if the search

is conducted on the said names, no adverse results are available.

(ix) It has therefore, taken such necessary steps within its control to ensure and prevent any

non disclosure in the letter of offer. Thus HSBC Securities is not and cannot be held liable for

the alleged non disclosures purportedly made in the letter of offer as alleged or at all.

(x) With respect to the non disclosure of pending litigation against acquirer and Mr. Ravi

Pratap Singh in the letter of offer, it stated that as disclosed in the paragraph 3 of the letter of

offer, the acquirer had confirmed that there are no pending litigations. It further reiterated that

the acquirer was not in control of the target company. Accordingly, the offer was not made

under Regulation 12 of the Takeover Regulations. Moreover the acquirer was a financial acquirer

and therefore could not control or decide the manner in which the target company was to be run.

This disclosure along with the Acquirer's investment objective has been clearly set out in the

letter of offer.

(xi) As regards the allegations that certain details regarding Mr. Ravi Pratap Singh, a director

on the Board of Directors of the acquirer, were not adequately disclosed in the letter of offer, it

was submitted that even if such association were to be true, Mr. Ravi Pratap Singh is just one of

the directors of the Board of Directors of the acquirers. The Board of Directors of the acquirer

consists of a number of distinguished personnel and the antecedents of one such member are in

no event reflective of the acquirer or the indiaSTAR Fund.

(xii) Even otherwise, the association of one of the directors of the acquirer with companies

that have faced lawsuits is to be seen in the context of the fact that the acquirer is not in control

of the management of the target company and is only a financial investor. Therefore, even if it

were to be assumed (though not admitted) that the allegations made by the applicant regarding

Mr. Ravi Pratap Singh are true, there is nothing to indicate such association could or has had any

Page 13 of 30

adverse impact on the target company, as the acquirer is not in control of the target company and

is only a shareholder.

(xiii) Further, SEBI does not warrant that any litigation against the directors of the acquirer be

disclosed for an open offer made in terms of Regulation 10 of the Takeover Regulations. In

terms of the SEBI circular, pending litigation matters of the acquirer is required to be disclosed

in the instances where the acquirer is a listed company.

8. The Acquirer, also made its response, through its Advocate, vide letter dated January 30,

2014 forwarded by the Merchant banker (HSBC Securities) through an email dated February 03,

2014. The following were inter alia its submissions :

(a) The Acquirer denied each of the allegations made by the applicant, as being erroneous in

law and fact.

(b) The "new disclosure" made in its affidavit in reply dated January 21, 2013 filed before the

Hon'ble SAT were made specifically to counter and refute the unsubstantiated allegation

made by the complainant in his appeal dated January 21, 2013. The new disclosure made

to refute those allegations, have no bearing or relevance whatsoever to the open offer

and were not required under the Takeover Regulations to be disclosed in the LOF.

(c) The Acquirer had provided and disclosed all relevant information in the LOF as required

by the Takeover Regulations. The Acquirer's transparency in responding to the

allegations made in the Appeal cannot remotely be interpreted, as is being sought by the

applicant, to be an admission by the Acquirer that the so called 'new disclosures' were

required to have been made in the LOF.

(d) The Complainant has, right from the outset, been seeking to abuse and manipulate SEBI

and the Hon'ble SAT to further his own unjust enrichment. The complainant has 'lied' on

record that he owned 1,560 equity shares in Target Company "before, during, and after

the open offer". An inspection of Target Company's shareholding records clearly

established that the Complainant held 4,200 equity shares as on the date of the Public

Announcement and held 1,560 equity shares throughout the period of open offer. The

data revealed that the complainant actually sold 2640 equity shares of Target Company

after the PA was made on November 07, 2007. Even subsequent to the open offer the

Complainant periodically traded in shares of Target Company on the stock exchange, and

his holding at a certain point went down to as low as 72 equity shares (on October 10,

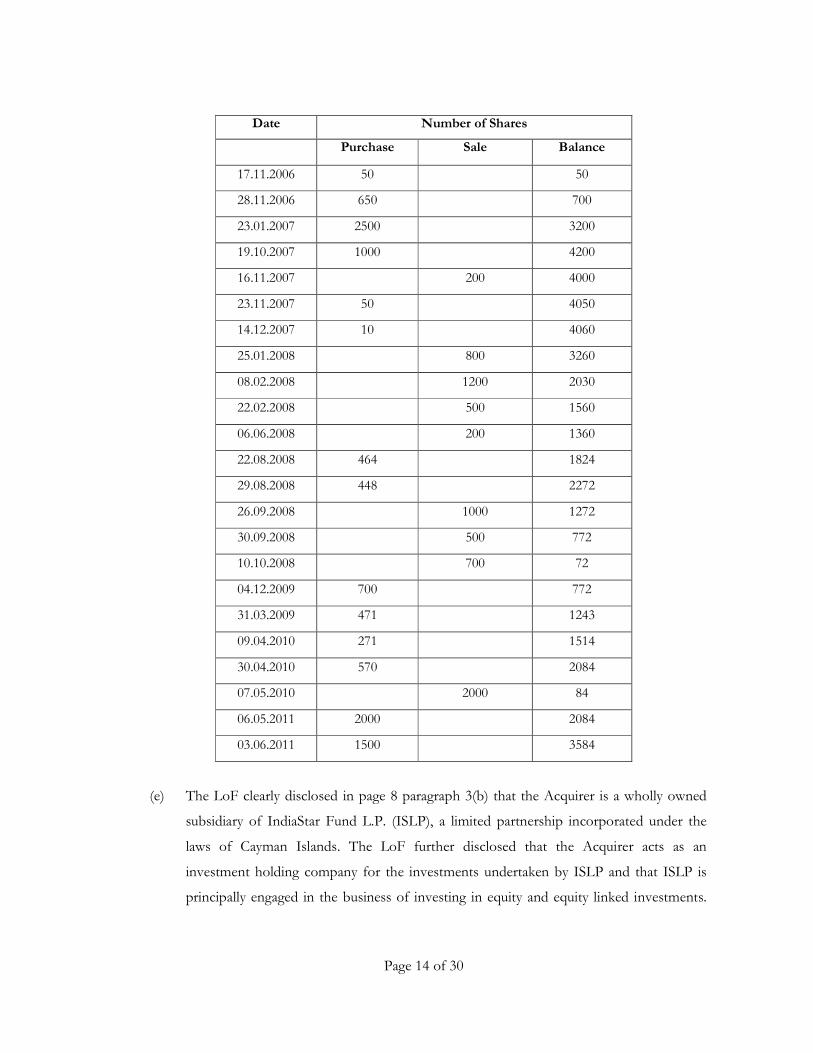

2008). Details of the transaction history of the Complainant is as follows –

Page 14 of 30

Date Number of Shares

Purchase Sale Balance

17.11.2006 50 50

28.11.2006 650 700

23.01.2007 2500 3200

19.10.2007 1000 4200

16.11.2007 200 4000

23.11.2007 50 4050

14.12.2007 10 4060

25.01.2008 800 3260

08.02.2008 1200 2030

22.02.2008 500 1560

06.06.2008 200 1360

22.08.2008 464 1824

29.08.2008 448 2272

26.09.2008 1000 1272

30.09.2008 500 772

10.10.2008 700 72

04.12.2009 700 772

31.03.2009 471 1243

09.04.2010 271 1514

30.04.2010 570 2084

07.05.2010 2000 84

06.05.2011 2000 2084

03.06.2011 1500 3584

(e) The LoF clearly disclosed in page 8 paragraph 3(b) that the Acquirer is a wholly owned

subsidiary of IndiaStar Fund L.P. (ISLP), a limited partnership incorporated under the

laws of Cayman Islands. The LoF further disclosed that the Acquirer acts as an

investment holding company for the investments undertaken by ISLP and that ISLP is

principally engaged in the business of investing in equity and equity linked investments.

Page 15 of 30

Hence, the disclosures in the LoF make it abundantly clear that ISLP is a limited

partnership which makes equity linked investments, which has several limited partners as

is customary in any fund or investment company.

(f) It is fairly common and customary structure for investment funds to be set up as limited

partnerships which receive investment from various investors who in turn are the limited

partners of the partnership. The funds invested by the limited partners into the limited

partnership are typically managed by professional fund management companies on behalf

of the limited partners. As disclosed in LoF, ISLP (the entity that owns 100% of the

share capital of the Acquirer) is a limited partnership and as such, is a broad based entity

which cannot be said to be controlled or owned by any particular person or group of

persons. Therefore, the identity of the partners of ISLP or the fact that ISLP's funds are

managed by a professional fund management company are irrelevant and immaterial for

the purposes of the Open offer and were not required to be disclosed under the

Takeover Regulations. Similarly, the Acquirer does not consider that details pertaining to

trademark licensing arrangement for the use of the "indiaStar" name were relevant or

required by the Takeover Regulations to be disclosed in the LoF.

(g) In the disclosure in page 9 paragraph 3(f) of the LoF, the complete details of the board of

directors of the Acquirer was disclosed as required by the Takeover Regulations. The said

disclosure of the board composition of the Acquirer had profiles of each of the directors

which made it very evident that 3 of the directors of Acquirer were associated with

Sycamore Ventures Group and Sycamore Management Corporation.

The Acquirer reiterated that the only reason why it provided the information in its reply filed

before the Hon'ble SAT was merely to address the unsubstantiated and wild allegations made by

the applicant in his appeal. The transparent disclosure by the Acquirer of all the information to

the Hon'ble SAT to defend the vexatious proceedings commenced by the applicant cannot be

construed as an admission by the Acquirer that any of these facts were necessary disclosures to

be made in the LOF as per the Takeover Regulations.

9. In addition to above, the following are the information disclosed in the reply submitted

to Hon'ble SAT by Merchant Banker and Mr. Ravi Pratap Singh :

Page 16 of 30

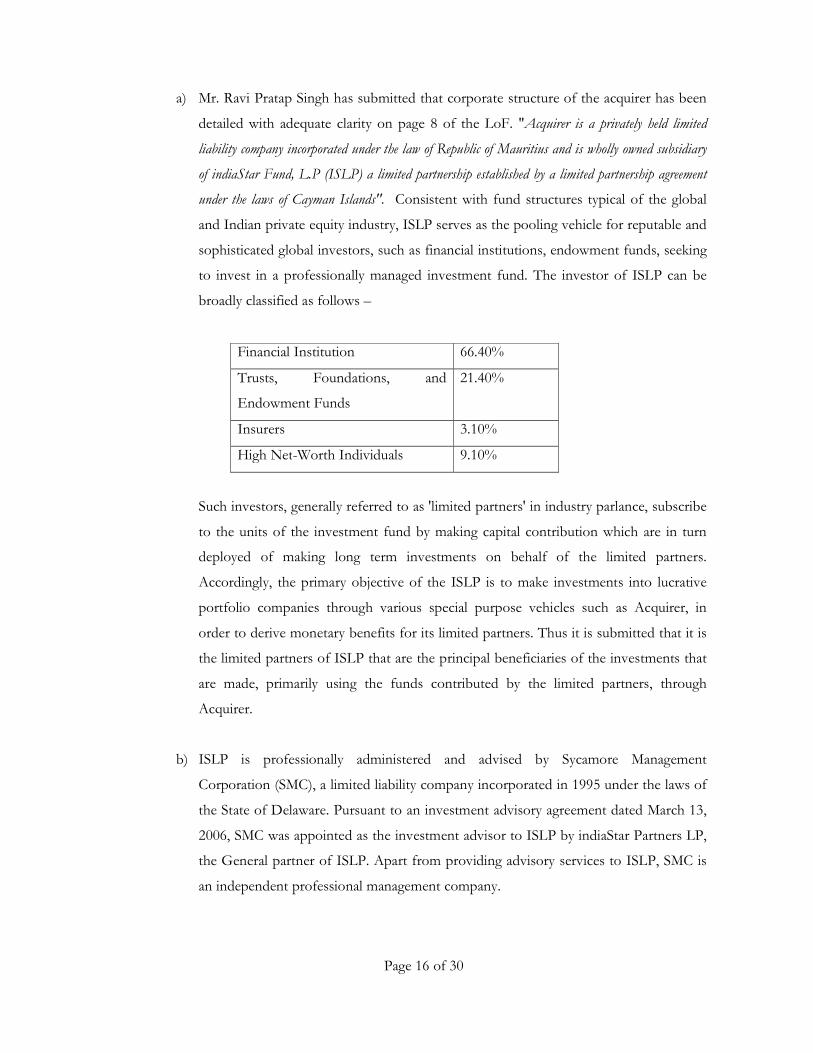

a) Mr. Ravi Pratap Singh has submitted that corporate structure of the acquirer has been

detailed with adequate clarity on page 8 of the LoF. "Acquirer is a privately held limited

liability company incorporated under the law of Republic of Mauritius and is wholly owned subsidiary

of indiaStar Fund, L.P (ISLP) a limited partnership established by a limited partnership agreement

under the laws of Cayman Islands". Consistent with fund structures typical of the global

and Indian private equity industry, ISLP serves as the pooling vehicle for reputable and

sophisticated global investors, such as financial institutions, endowment funds, seeking

to invest in a professionally managed investment fund. The investor of ISLP can be

broadly classified as follows –

Financial Institution 66.40%

Trusts, Foundations, and

Endowment Funds

21.40%

Insurers 3.10%

High Net-Worth Individuals 9.10%

Such investors, generally referred to as 'limited partners' in industry parlance, subscribe

to the units of the investment fund by making capital contribution which are in turn

deployed of making long term investments on behalf of the limited partners.

Accordingly, the primary objective of the ISLP is to make investments into lucrative

portfolio companies through various special purpose vehicles such as Acquirer, in

order to derive monetary benefits for its limited partners. Thus it is submitted that it is

the limited partners of ISLP that are the principal beneficiaries of the investments that

are made, primarily using the funds contributed by the limited partners, through

Acquirer.

b) ISLP is professionally administered and advised by Sycamore Management

Corporation (SMC), a limited liability company incorporated in 1995 under the laws of

the State of Delaware. Pursuant to an investment advisory agreement dated March 13,

2006, SMC was appointed as the investment advisor to ISLP by indiaStar Partners LP,

the General partner of ISLP. Apart from providing advisory services to ISLP, SMC is

an independent professional management company.

Page 17 of 30

c) As is typical in the case of a corporate entity, the management and control of the

Acquirer, including decisions on investments and disinvestments, finally vests in the

board of directors of the Acquirer (BoD). The BoD, independently and at its sole

discretion, decides on investments and disinvestments. The composition of BoD of

Acquirer was clearly disclosed in page 10 through para 13 of the LoF which also make

it amply clear that three of the directors of BoD (viz. John R Whitman (managing

partner of SMC), Ravi Pratap Singh (partner at Sycamore Ventures), and David S.

Lichtenstin (Chief financial officer at Sycamore Ventures)) are associated with

Sycamore Management Corporation and Sycamore Ventures.Mr. Ravi Pratap Singh has

denied the allegation of non-disclosure that some of Acquirer's key decision-makers

were also key decision-makers of some Sycamore entities, as baseless and completely

irrelevant for the purposes of the disclosure requirement under the Takeover

Regulations.

d) In the light of the above, Mr Ravi Pratap Singh has submitted that neither does

Sycamore Ventures have any, direct or indirect, shareholding in the Acquirer nor does

it exercise control over the Acquirer which would deem it to be promoter of the

Acquirer. He has also submitted that it would be incorrect, to classify the Acquirer or

ISLP as belonging to the Sycamore Ventuers group or any other group.

e) The statement that Sycamore Ventures is in control of the Acquirer merely on the

ground that the trademark 'indiaStar' is registered in the name of SMC, is untenable

and misleading. SMC, had in the course of its management and administrative services

has registered the trademark 'indiaStar' and has permitted ISLP and the Acquirer to use

such trademark. Such an arrangement does not give SMC control or ownership over

the Acquirer or ISLP as alleged by the applicant.

f) Submissions regarding alleged non-disclosure pertaining to Ravi Pratap Singh: All the

relevant and the material details regarding his academic and professional background

had been provided in page 10 of LoF and no material disclosures have been withheld.

The following submissions were made :

• He was the chief financial officer of SeraNova prior to its merger with Silverline

in 2001. In order to facilitate the integration of SeraNova into Silverline, he was

Page 18 of 30

requested to act as the co-CEO of Silverline for a limited period of

approximately 7 months (August 2001 to March 2002). The MB has stated that

Mr. Ravi Pratap Singh has confirmed that he has not been made party to any

legal proceeding or investigation by any regulatory authority in connection with

his holding the position of co-CEO in Silverline.

• In his capacity as a director of SeraNova, he was made a party to a lawsuit filed

by NSA Investment against SeraNova regarding certain disputed loan

obligation. Subsequently, NSA Investment and SeraNova arrived at an amicable

out of court settlement regarding the dispute and the said lawsuit was thereafter

withdrawn several years prior to the Open Offer. The said dispute therefore,

was not even in existence at the time of the Open offer.

• He was on the board of directors of Dahava Resources from June 2006 until his

resignation in June 2009. On February 7, 2008 a cease trade order was passed by

the British Columbia Securities Commission against Dahava Resources

restraining insider and persons in control of Dahava Resources due to a delay in

filing the comparative financial statement for the financial year ended September

30, 2007 and Form 52-102F1 (Management's Discussion and Analysis) from the

financial year ended September 20, 2007 and which cease trade order was

subsequently revoked upon submission of the necessary documents by Dahava.

10. Subsequently, the Merchant Banker vide email dated May 08, 2014 submitted that

Sycamore Management Corporation (“SMC”) is a professional services company, which, under

separate service contracts, provides investment management and other services to multiple and

unrelated series of private equity funds, one of which is indiaSTAR Fund L.P. (“ISLP”) – the

entity that owns 100% of the share capital of indiaSTAR (Mauritius) Limited (i.e., the Acquirer).

SMC also provides services to several other funds. The MB has also stated that “Sycamore

Ventures” is a brand name used by SMC and there is no entity in existence called “Sycamore

Ventures”, and as such, there can be no question of disclosing any alleged “Control” by

“Sycamore Ventures” of the Acquirer as the complainant seeks to suggest.

The following submissions were also made :

Page 19 of 30

(a) The funds that SMC operates under the “Sycamore Ventures” brand have very different

investment strategies and geographical focus from ISLP and the Acquirer. The MB has

stated that importantly, the investors in each of these funds are completely different from

one another, and accordingly, are completely different from the investors in

ISLP/Acquirer. Hence, ISLP and the Acquirer have no connection or commonality with

the other funds that SMC provides services to, let alone be controlled by the “Sycamore

Ventures” funds.

(b) The composition of the investment committee (committee that is charged with taking

investment and exit decisions of a private equity fund) of each of the funds or series of

funds that SMC provides services to is very different from the composition of the

investment committee of the indiaStar funds.

(c) Very importantly, the stock price of the Target Company has in recent times, experienced

a significant hike in value, going up to an all time high of `359.50/- per share, which is

significantly above the open offer price of around `235/- per share. Hence, without

prejudice to any of the points made above or in the Affidavit-in-response, the

complainant or any other person who may be similarly aggrieved, has had a very

reasonable window of opportunity in recent times to sell their shares of the Target

Company at a price that is substantially higher than the open offer price.

11. Consideration :

As the applicant has contended that the Acquirer failed to make proper and complete disclosures

in the LOF, I first proceed to consider the mandatory requirements to be made in the letter of

offer. SEBI vide Circular dated March 08, 2004 had specified formats for letter of offer under

the Takeover Regulations. Clause 4 of the "Format of the Standard Letter of Offer" requires

disclosures of the Background of the Acquirer(s) (including PACs, if any).

"4 BACKGROUND OF THE ACQUIRER (INCLUDING PACs, IF ANY)

(In case, the open offer is for the change in control of the Target Company or is an offer where the offer price is

payable in terms of exchange of securities, details under this heading shall be given as per Annexure I. In all other

cases, the following details shall be furnished)

4.1 If acquirer(s) (including PACs) is a company

4.1.1 Name, address (registered and corporate office) and phone no. of the company(ies).

Page 20 of 30

4.1.2 The relationship, if any, existing between them

4.1.3 Salient features of the agreement, if any, entered between them with regard to the offer/ acquisition of shares.

4.1.4 Brief History & Major areas of operations.

4.1.5 Identity of the promoters and /or persons having control over such companies and the group, if any, to which

such companies belong to.

4.1.6 Confirm and disclose as to whether the applicable provisions of chapter II of SEBI Takeover Regulations

has been complied with by acquirer/ PACs within the time specified in the Regulations. Delay or non-compliance

with these provisions if any, may be disclosed in the letter of offer. Further the extent of compliance by the

acquirers/ PACs with the applicable provisions of chapter II should be furnished under a separate annexure to

SEBI along with the draft letter of offer as per the format at Annexure III of the standard letter of offer.

4.1.7 Names and residential addresses of Board of directors of acquirer(s).

Confirm whether any of such director(s) is already on the Board of Directors of Target Company. If so, disclosures

in terms of Regulation 22(9).

4.1.8 Details of the experience, qualifications, date of appointment of the Board of Directors.

……….." In the LOF, the details regarding Background of the Acquirer in this case was presented as item

3 from page no. 8 onwards. The following were the disclosures :

"3. BACKGROUND OF THE ACQUIRER - M/s. IndiaSTAR (Mauritius) Limited

(“Acquirer”)

a) The Acquirer, indiaSTAR (Mauritius) Ltd., is a privately held limited liability company incorporated on

February 17, 2006 (Registration Number 61002) in the Republic of Mauritius under the (Mauritius)

Companies Act, 2001 with its registered office at Level 3, Alexander House, 35 Cyber city, Ebene, Mauritius.

Tel: +230 403 0800.The Acquirer does not have a separate corporate office.

b) The Acquirer is a wholly owned subsidiary of indiaSTAR Fund, L.P., a limited partnership established by a

Limited Partnership Agreement dated December 5, 2005 under the Limited Partnership laws of Cayman

Islands, having its registered office at c/o Trident Trust Company (Cayman) Ltd., P.O. Box 847 GT, One

Capital Place, George Town, Grand Cayman, Cayman Islands. Tel: +345 949 0800; Fax: +345 949 0881;

Email: [email protected]. indiaSTAR Fund, L.P. owns 3,70,50,001 (three crore, seventy lakhs

,fifty thousand and one) shares, as of limited review financial on September 28, 2007 representing 100% (one

hundred percent) of the issued and outstanding shares of the Acquirer. Further as of limited review financial dated

November 6, 2007 indiaSTAR Fund, L.P. owns 6,86,50,001 (six crore, eighty six lakhs ,fifty thousand and

one) shares, representing 100% (one hundred percent) of the issued and outstanding shares of the Acquirer. The

principal purpose of indiaSTAR Fund, L.P.is to invest in equity, equity linked and equity related investments in

Page 21 of 30

growth companies with significant interest in the Indian subcontinent. The Acquirer acts as an investment holding

company for indiaSTAR Fund L.P. for all investments undertaken by indiaSTAR Fund, L.P.

c) The Acquirer is an India-focused investment company that primarily provides growth capital to mid-market

companies in India. To date, the Acquirer has consummated investments in (i) Radha Madhav Corporation

Limited, (ii) Surana Industries Limited, (iii) IOL Chemicals and Pharmaceuticals Limited, and (iv) KEW

Industries Limited, in addition to its existing investment in the Target. The above-mentioned investments excepted,

the Acquirer has no other existing business in India. Further, the Acquirer has not promoted any company in

India. Outside of India, the Acquirer has established SV India I Ltd, a wholly owned subsidiary in Mauritius

(the “Subsidiary”). The Subsidiary is only intended to be an investment holding company and as on date of the

PA, the Subsidiary has not made any investments and has not conducted any business.

d) The Acquirer confirms that it has complied with the provisions of Chapter II of the SEBI (SAST)

Regulations within the time specified in the SEBI (SAST) Regulations.

e) Shareholding pattern of the Acquirer, as on the date of the PA, is as under:

Sl. No. Shareholder’s category No. and percentage of shares held

1. Promoters 68,650,001 ordinary Shares of face value USD 1, 100%

2. FII/Mutual Funds/FIs/Banks Nil

3. Public Nil

Total paid up capital 68,650,001 ordinary Shares of face value USD 1, 100%

…………

h) The Acquirer is a privately held limited liability company and is not listed on any stock exchange. The Acquirer is a wholly owned subsidiary of indiaSTAR Fund, L.P., a limited partnership. i) The Acquirer has a total of fully paid up 68,650,001 ordinary shares of face value USD 1 each amounting to a paid up share capital of USD 68,650,001 ……………….." The applicant has alleged that the Acquirer did not make complete disclosures as according to

him, 'Sycamore Ventures' controlling and continuing to control the Acquirer was not disclosed

by the Acquirer in the LOF. According to the applicant, the trademark "indiaStar" was owned

and registered by Sycamore Management Corporation ("SMC") and that IndiaStar Fund is one of

the funds of Sycamore Ventures. In the supplementary representation (applicant's letter dated

September 12, 2013 sent through his counsel), the applicant has mentioned of new disclosures which

were made by the Acquirer in his affidavit filed before the Hon'ble SAT. According to applicant,

the facts such as :

Page 22 of 30

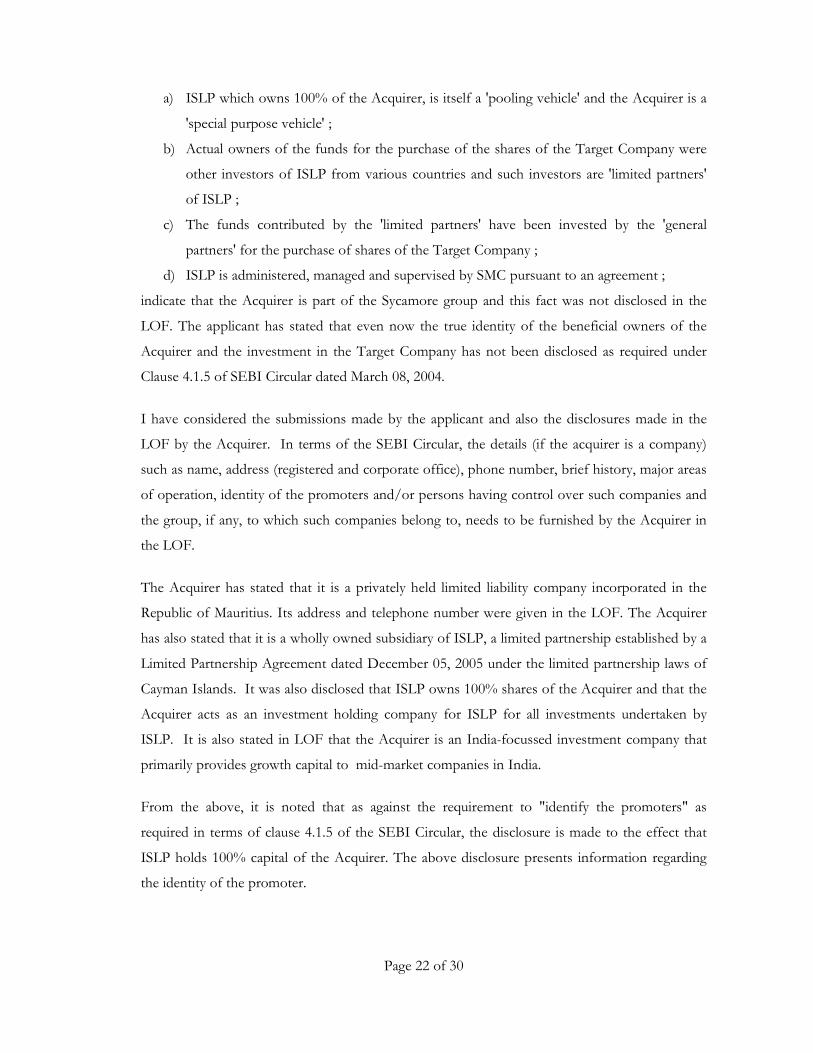

a) ISLP which owns 100% of the Acquirer, is itself a 'pooling vehicle' and the Acquirer is a

'special purpose vehicle' ;

b) Actual owners of the funds for the purchase of the shares of the Target Company were

other investors of ISLP from various countries and such investors are 'limited partners'

of ISLP ;

c) The funds contributed by the 'limited partners' have been invested by the 'general

partners' for the purchase of shares of the Target Company ;

d) ISLP is administered, managed and supervised by SMC pursuant to an agreement ;

indicate that the Acquirer is part of the Sycamore group and this fact was not disclosed in the

LOF. The applicant has stated that even now the true identity of the beneficial owners of the

Acquirer and the investment in the Target Company has not been disclosed as required under

Clause 4.1.5 of SEBI Circular dated March 08, 2004.

I have considered the submissions made by the applicant and also the disclosures made in the

LOF by the Acquirer. In terms of the SEBI Circular, the details (if the acquirer is a company)

such as name, address (registered and corporate office), phone number, brief history, major areas

of operation, identity of the promoters and/or persons having control over such companies and

the group, if any, to which such companies belong to, needs to be furnished by the Acquirer in

the LOF.

The Acquirer has stated that it is a privately held limited liability company incorporated in the

Republic of Mauritius. Its address and telephone number were given in the LOF. The Acquirer

has also stated that it is a wholly owned subsidiary of ISLP, a limited partnership established by a

Limited Partnership Agreement dated December 05, 2005 under the limited partnership laws of

Cayman Islands. It was also disclosed that ISLP owns 100% shares of the Acquirer and that the

Acquirer acts as an investment holding company for ISLP for all investments undertaken by

ISLP. It is also stated in LOF that the Acquirer is an India-focussed investment company that

primarily provides growth capital to mid-market companies in India.

From the above, it is noted that as against the requirement to "identify the promoters" as

required in terms of clause 4.1.5 of the SEBI Circular, the disclosure is made to the effect that

ISLP holds 100% capital of the Acquirer. The above disclosure presents information regarding

the identity of the promoter.

Page 23 of 30

As regards the requirement to state that "persons having control over such companies and the

group, if any, to which such companies belong to" as also required in terms of clause 4.1.5 of the

SEBI Circular, I note the following :

The Merchant Banker and the Acquirer have stated that authority and responsibility over ISLP

was by IndiaStar Partners LP, a general partner. Further, SMC was a sole general partner of

IndiaStar Partners LP. The Merchant Banker has also stated that "The sole general partner of

Indiastar partners LP(general partner of indiaSTAR L.P.) is Sycamore Management

Corporation, 845 Alexander Road, Princeton, NJ 08540, USA, a highly reputable professional investment

management firm (“SMC”). Furthermore, SMC has formed and authorized an Investment Committee comprised

of three members to manage all of the investment activities and business matters of the Fund.”

The statements made by the Acquirer and the Merchant Banker with respect to the manner of

holding the Acquirer can be pictorially represented as follows :

Sycamore Management Corporation

(sole general partner of Indiastar partners LP)

Indiastar Partners LP

(general partner of indiaSTAR L.P.)

IndiaSTAR Fund, L.P. (Parent company of

India STAR (Mauritius) Ltd

IndiaSTAR (Mauritius) Ltd (Acquirer)

The above manner of control by SMC, as represented by the Acquirer and the Merchant Banker,

on the Acquirer has not been disclosed in the LOF. Instead, the Acquirer and the Merchant

Banker hurried their way to terminate the disclosures at the first possible stop. Therefore, the

disclosure made in the LOF does not present a true and a fair representation of the persons

having control over the Acquirer.

The Acquirer has a responsibility to disclose all relevant disclosures in satisfaction of the SEBI

guidelines made in this regard. Further, the Merchant Banker is also expected to have done its

SMC and IndiaStar

Partners LP are two

entities which have not

been disclosed in the

LOF.

These two entities

have been disclosed in

the LOF

Page 24 of 30

due diligence regarding the facts, statements and disclosures made in the LOF. It is for this very

purpose that merchant banker, who are SEBI registered intermediaries, are given the

responsibility to ensure that proper and adequate disclosures are made by an acquirer in a letter

of offer. The veracity and adequacy of such statements/disclosures should have been examined

by the Merchant Banker and in case any disclosure is not properly or adequately presented, it is

his responsibility to probe into the same so that investors who are the target in any open offer do

get all details which will enable them to make a reasoned decision on whether to off-load or hold

on to the shares whenever there is a substantial acquisition of shares or voting rights, or change

in control in a target company.

In this regard, I refer to the following observations made by the Hon'ble SAT in the matter of

Eider-E-Commerce Ltd. vs. SEBI (Order dated January 01, 2001) on the importance of SEBI

mandating disclosures in offer documents. Though the observations are made in respect of the

disclosures under the SEBI (Disclosure and Investor Protection) Guidelines, 2000, the same

would hold good for disclosures in LOF filed under the Takeover Regulations also :

".......The Issuer Company is required to maintain certain standards of disclosure relating to various matters

having a bearing on the investment decision of the investors. The Respondent has already prescribed the disclosure

requirements and an issuer company in its own interest is required to fulfil those requirements, lest the public issue

will not be through. The lead manager is also required to ensure that the information furnished in the offer

document is not in any way exaggerated or deficient and that the material facts are not suppressed to the

disadvantage of the subscribers."

On a consideration of the above observations and taking into account the importance of such

proper and adequate disclosures in offer documents, it could be concluded that the Acquirer and

the Merchant Banker have failed to reach the standards of disclosures expected by SEBI. For the

same, the Acquirer and the Merchant Banker are reprimanded and are advised to comply with

disclosure requirements mandated by SEBI in its regulations and circulars, in letter and spirit.

Allegation with respect to the disclosures of details of Mr. Ravi Pratap Singh.

As mentioned above, the SEBI Circular vide Clause 4.1.7 and 4.1.8, mandates that details such as

(1) Names and residential addresses of Board of directors of Acquirer ; and

(2) Details of the experience, qualifications, date of appointment of the Board of directors,

be disclosed in the LOF.

Page 25 of 30

In the LOF, the following details are given with respect to Mr. Ravi Singh :

"………

f) The Directors of indiaSTAR (Mauritius) Limited and their addresses are as listed below :

(only that of Mr. Ravi Singh is mentioned)

Name (Age)/Date of

Appointment

Educational Qualification

Experience Residential Address

Ravi Pratap Singh (49) Director since February 17, 2006

Ravi has an MBA in Finance & International Business from Columbia University, New York, and BS in Mechanical Engineering from University of Delhi, India.

Ravi Singh is a Partner with Sycamore Ventures. Over the course of his 25-year career, he has structured and led numerous public and private financings, mergers & acquisitions and global investments. In the past, he held successive positions as a Manager with Coopers & Lybrand in New York (now PriceWaterhouseCoopers); General Partner and Managing Director at Cowen & Company (now SG Cowen); Managing Director of Forbes & Walker, a New York merchant banking firm; Partner, Managing Director and Head of Technology Investment Banking at Punk, Ziegel & Company and Founding Partner of Converge Partners LLC, a New York based investment advisory firm.

701 Horseshoe Trail, Franklin Lakes, NJ 07417, USA

g) None of the Directors of the Acquirer is on the Board of Directors of the Target.

…….." From a reading of the above disclosures, it can be said that the Acquirer has complied with the

requirements of the aforesaid requirement of the SEBI Circular.

The applicant has stated that Mr. Singh's experience in Silverline ; law suits for negligent

misrepresentation and securities laws violations by Sera Nova and its promoters including Mr.

Singh ; and Dahava Resources of which Mr. Singh was the CEO had violated securities laws and

a cease trade order was passed by Canadian Regulators, were not disclosed in the LOF.

The Merchant Banker has contended that even if the allegations were true, there was nothing to

indicate that such association could or has had any adverse impact on the Target Company, as

the Acquirer is not in control of the Target Company and is only a shareholder. Further, it is

also contended that SEBI does not require disclosure of litigation against directors of the

Acquirer in an open offer made in terms of regulation 10 of the Takeover Regulations. Further,

Page 26 of 30

pending litigation matters of the Acquirer have to be disclosed in instances where the Acquirer is

a listed company.

In this regard, I note that Clause 4 of the SEBI Circular does not mandate disclosures of

litigations against directors of the Acquirer. Further, the Acquirer is not a listed company in

order to compel it to disclose litigation matters.

I also note that the aforesaid SEBI Circular does not also mandate the disclosure of information

with respect to investigations/proceedings against employees of the Acquirer. Therefore, the

allegation with respect to references being made of Sycamore Ventures and Mr. Chong

(employee of SMC) may also not stand.

In view of the above, the allegations made by the applicant in this regard does not have any

merit.

12. I also note that the complainant has been using the name "Sycamore Ventures” in his

representation. The same, as clarified by the Acquirer/Merchant Banker, is a brand name used

by SMC and there is no entity in existence with the name “Sycamore Ventures”. Accordingly,

there can be no question of disclosing any alleged “Control” by “Sycamore Ventures” of the

Acquirer.

13. Relief sought by the Complainant : The Complainant in his complaint has requested

SEBI to direct the Acquirer to make another open offer and provide an opportunity to the

shareholders to take an informed decision whether to tender or not to tender their equity shares.

He has also requested that such offer be directed at the same price paid to the shareholders in the

impugned Open Offer plus interest from the due date of payment in the impugned offer to the

date of payment at the rate decided by SEBI.

I have considered the request. The Complainant needs to appreciate that the open offer in this

matter had closed on April 07, 2008. Shares which were tendered have been purchased and

consideration had moved from the Acquirer to those shareholders who had tendered shares in

the open offer in terms of the completion of the activity schedule of such open offer. The

Complainant has made his complaint on January 16, 2012, which is almost after 4 years of

completion of the open offer made by the Acquirer. Though there is no limitation period for

Page 27 of 30

such complaints or representations to be made to SEBI, in terms of the Takeover Regulations, a

period of 21 days is available for the shareholders to peruse the LOF and forward their

grievances/complaints, if any, in connection with the open offer to SEBI/Merchant

Banker/Acquirer. Even if a complaint is received after one day of closure and completion of

open offer formalities, the same would create a huge difficulty in undoing the process that are

already completed. Further, it could also be possible that third party rights are created in the

meantime. If representations and complaints are made after a considerable lapse of time seeking

for another fresh offer, the same could create uncertain ground for acquirers who have acquired

voting rights or gained control and also for the target companies.

The disclosures made under the Takeover Regulations to be made in the LOF is almost similar to

that of a notice, giving details of a proposed compromise or arrangement under sections 391/393

of the Companies Act, 1956 (now repealed), to a creditor or member of a company. The same is

done so that the concerned creditor or member may consider the proposal and file his objections

to such proposal. If such objections are not sufficient, the court may proceed and approve such

scheme. In this regard, the following observations made in the matter of Kusum Products Limited

[1999 98 CompCas 10 Cal], by the Hon'ble Calcutta High Court are worth noting :

"......65. It is well settled that if the statutory formalities have been complied with and the scheme is fair and

reasonable, there is no fraud involved, then the court would proceed to give effect to the majority decision of the

shareholders of the company. In other words, only if the court finds that the scheme is fraudulent or unreasonable,

the court would proceed not to sanction the scheme. Reference may be made in this connection to Palmer's Company

Law, 24th edition, para. 70.14. If the court is satisfied that all the statutory formalities have been complied with

and the scheme is fair and reasonable and there is no fraud involved in propounding the scheme, the petitioners are

taken to have discharged their onus and the scheme ought to be sanctioned by the court.

....... 66. The onus lies heavily on those who oppose the sanction of the scheme to show that the scheme is unfair,

unreasonable or fraudulent. In this connection, the following decisions may also be taken note of : (i) Hindustan

General Electric Corporation Ltd., In re ; (ii) Sussex Brick Co. Ltd. In re [1960] 30 Comp Cas 536 ; [1961]

1 Ch. 289, In the aforesaid decisions, it was held in No. (i) case that (head-note of AIR 1959 Cal) "the

functions and duties of the court in the matter of sanctioning of schemes are well known. Any scheme which is fair

and reasonable and made in good faith will be sanctioned if it could reasonably be supported by sensible people to

be for the benefit of each class of the members or creditors concerned. It is also the duty of the court to see that the

resolutions were passed by the statutory majority. The majority of the three-fourths value must be of persons who

were present and who took part in the voting. Mere presence would not be enough. The onus of proving

Page 28 of 30

unreasonableness or unfairness about the scheme or of want of good faith is on those who object to the sanction of

the scheme. This onus is not discharged by vague and general assertions devoid of any particulars."

67. In the aforesaid decision No. (ii) it was held that although it might be possible to find faults in a scheme that

would not be sufficient ground to reject it. It was further held that a scheme must be obviously unfair, patently

unfair, unfair to the meanest intelligence. It cannot be said that no scheme can be effective to bind a dissenting

shareholder unless it complies to the extent of 100 per cent. It is the consistent view of the courts that no scheme can

be said to be fool-proof and it is possible to find faults in a particular scheme but that by itself is not enough to

warrant a dismissal of the petition for sanction of the scheme. The courts have gone further to say that a scheme

must be held to be unfair to the meanest intelligence before it can be rejected. It must be affirmatively proved to the

satisfaction of the court that the scheme is unfair before the scheme can be rejected by the court. ......... "

In the present case, I note the allegation that adequate disclosures with respect to the persons in

control of the Acquirer was not made. However, it has not been shown that the shortfall in

disclosure would have changed the decision of the shareholders who had tendered shares in the

open offer. Further, for the inadequate disclosures, as discussed above, the Acquirer and the

Merchant Banker have been reprimanded. Repeated violations by either of them would be

viewed very seriously by SEBI.

There is another reason why I would not be agreeable to granting the relief as sought for by the

Complainant. The complainant has stated that he owned 1,560 equity shares in the target

Company "before, during, and after" the open offer. As per submissions made to SEBI, it has been

observed that claim of the complainant is not true. At the time of PA, the complainant held 4200

shares of Target Company. He sold 2640 equity shares of Target Company after the PA was

made on November 07, 2007. Even subsequent to the open offer, the Complainant periodically

traded in shares of Target Company on the stock exchange, and his holding at a certain point

went down to as low as 72 equity shares. Subsequently, before filing the complaint, he bought

shares of Target Company and as on the date of complaint he was holding 3,584 shares of the

Target Company. Moreover, the complainant has also purchased 700 shares during April 2013,

which is much after his complaint. It is surprising to note as to how the Complainant had

purchased shares when he has made such allegations in his complaints and has requested SEBI to

direct the Acquirer to make another open offer to the shareholders. In this regard, the Hon'ble

Supreme Court has held that a person approaching court for an equitable relief should come with

clean hands. Any suppression or concealment of relevant facts would make him ineligible for

such relief. In this regard, I note the following :

Page 29 of 30

(1) The Hon'ble Supreme Court in Mohammadia Co-op. Building Society Ltd. v. Lakshmi Srinivasa

Co-op. Building Society Ltd. [(2008) 7 SCC 310} had observed that "71. Grant of a decree for

specific performance of contract is a discretionary relief. There cannot be any doubt whatsoever that the

discretion has to be exercised judiciously and not arbitrarily. But for the said purpose, the conduct of the

plaintiff plays an important role. The courts ordinarily would not grant any relief in favour of the person

who approaches the court with a pair of dirty hands."

[Emphasis supplied]

(2) Further, the Hon'ble Supreme Court in G. Jayashree v. Bhagwandas S. Patel, [(2009) 3 SCC

141], has observed "..........A plaintiff is expected to approach the court with clean hands. His conduct

plays an important role in the matter of exercise of discretionary jurisdiction by a court of law...."

In view of the above observations, it may not be appropriate and reasonable to allow the relief as

sought for by the Complainant.

14. The Complainant has also referred to a news item and stated that a foreign bank was in

advanced talks with the Acquirer to acquire 20% stake in the Target Company and requested

SEBI to restrain the Acquirer from exiting its shareholding in the Target Company. In this

regard, I note that the said news item was on May 13, 2013, whereas the complainant has made

the said allegation belatedly in his additional complaint dated September 12, 2013. Further, I also

note from the shareholding pattern of the Company for the quarter ended June 2014, that the

Acquirer is shown as public shareholder of the Company holding 72,60,928 shares (29.36%). This

quantity of shares is the same as was its shareholding post the open offer made by it in the year

2008. The apprehension of the applicant that the Acquirer would exit the Company is therefore

not warranted.

15. Considering the facts and circumstances of this case and the observations made in this

decision, a direction in the nature of ordering the Acquirer to make another public offer is not

warranted. As discussed above, the Acquirer and the Merchant Banker should be reprimanded

for failing to reach the standards of disclosure expected under the SEBI regulations.

Page 30 of 30

Decision:

16. In view of the above reasons and observations, I hereby dispose of the application dated

January 16, 2012 and the supplementary representation dated September 12, 2013 filed by Mr.

Amit Bhagvatprasad Barot, without granting any relief.

17. I reprimand the Acquirer and the Merchant Banker for failing to reach the standards of

disclosures expected under the SEBI Circular dated March 08, 2004.

PRASHANT SARAN

WHOLE TIME MEMBER

SECURITIES AND EXCHANGE BOARD OF INDIA

Date : November 21st, 2014

Place : Mumbai