Embed Size (px)

Citation preview

OPTIONS FOR REDUCTION OF UPSTREAM EMISSIONS FROM OIL PRODUCTION:

SIGNIFICANCE, IMPLEMENTATION AND CONSEQUENCES

THEODORE GOUMASKONSTANTINA NTRENOGIANNI IOANNIS STEFANOU

VDBVerband der Deutschen Biokraftstoffindustrie e. V. Am Weidendamm 1AD -10117 Berlinwww.biokraftstoffverband.de

OVID Verband der ölsaatenverarbeitenden Industrie in Deutschland e. V.Am Weidendamm 1AD - 10117 Berlinwww.ovid-verband.de

MARCH 2016

THEODORE GOUMASKONSTANTINA NTRENOGIANNI IOANNIS STEFANOU

OPTIONS FOR REDUCTION OF UPSTREAM EMISSIONS FROM OIL PRODUCTION:

SIGNIFICANCE, IMPLEMENTATION AND CONSEQUENCES

CONTENTS

ABBREVIATIONS 6EXECUTIVE SUMMARY 8

1 INTRODUCTION TO THE PROJECT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2 OVERVIEW OF UPSTREAM EMISSION REDUCTION MEASURES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132.1 Overview of Upstream Emitting Activities 13

2.1.1 Significance of venting, flaring and fugitive emissions 142.1.2 Flaring emissions 172.1.3 Venting and Fugitive emissions 18

2.2 Upstream Emission Reduction Technologies 192.2.1 Overview of APG Utilisation Options 192.2.2 Technologies for APG utilisation 222.2.3 Abatement options for methane emissions 242.2.4 Assessment of UER Technologies 242.2.5 UER technologies based on renewable sources 26

2.3 Upstream Emission Reduction Incentives 262.3.1 Overview of EU crude oil supply 272.3.2 Geography of upstream emissions 282.3.3 Russia 302.3.4 Nigeria 352.3.5 Norway 382.3.6 Iraq 412.3.7 Iran 432.3.8 Canada 44

3 POTENTIAL AND INCENTIVES OF UPSTREAM EMISSION REDUCTION . . . . . . . . . . . . . . . . . . . . . . . . . 483.1 Introduction to the FQD 483.2 Incentives and policies for Upstream Emission Reduction 49

3.2.1 Cap-and Trade Systems 503.2.2 Emission (Carbon) Tax 513.2.3 Direct Regulations 523.2.4 Current practice 52

3.3 The EU legislative context 533.3.1 Emission Intensity Standards and the FQD 533.3.2 The Renewable Energy Directive 54

3.4 The case of California 553.5 The British Columbia case 563.6 Emission offset mechanisms 573.7 The European Emissions Trading Scheme 57

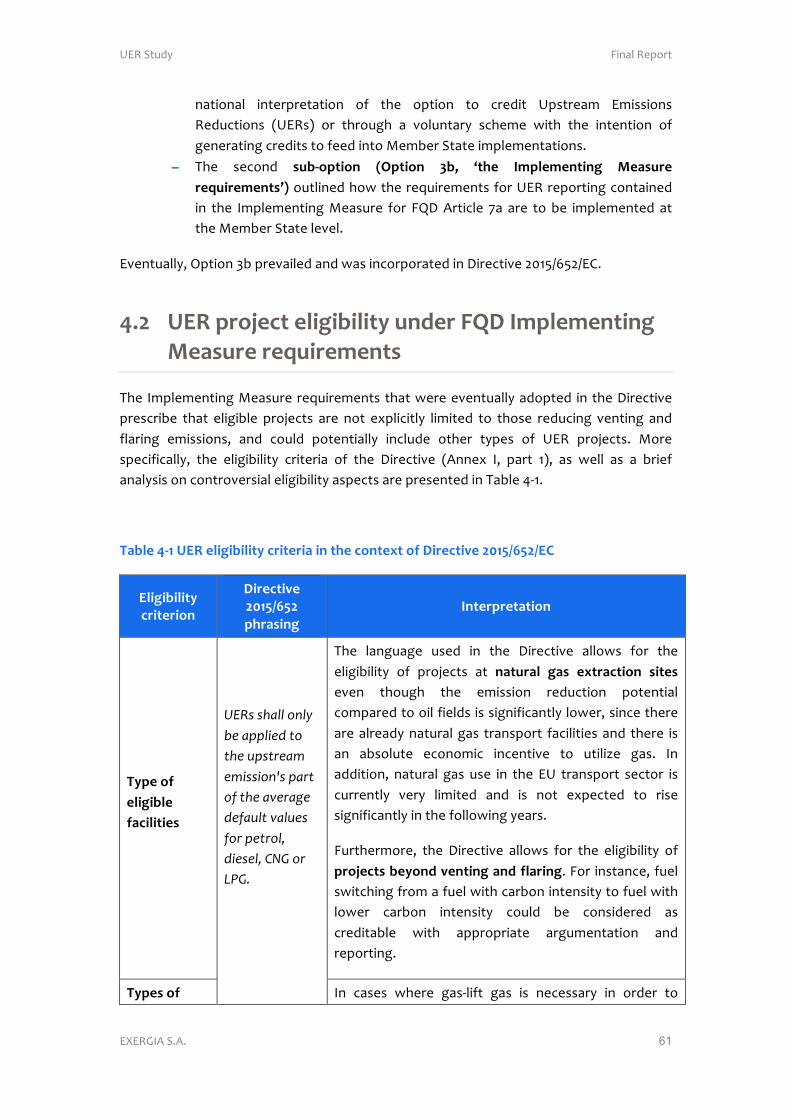

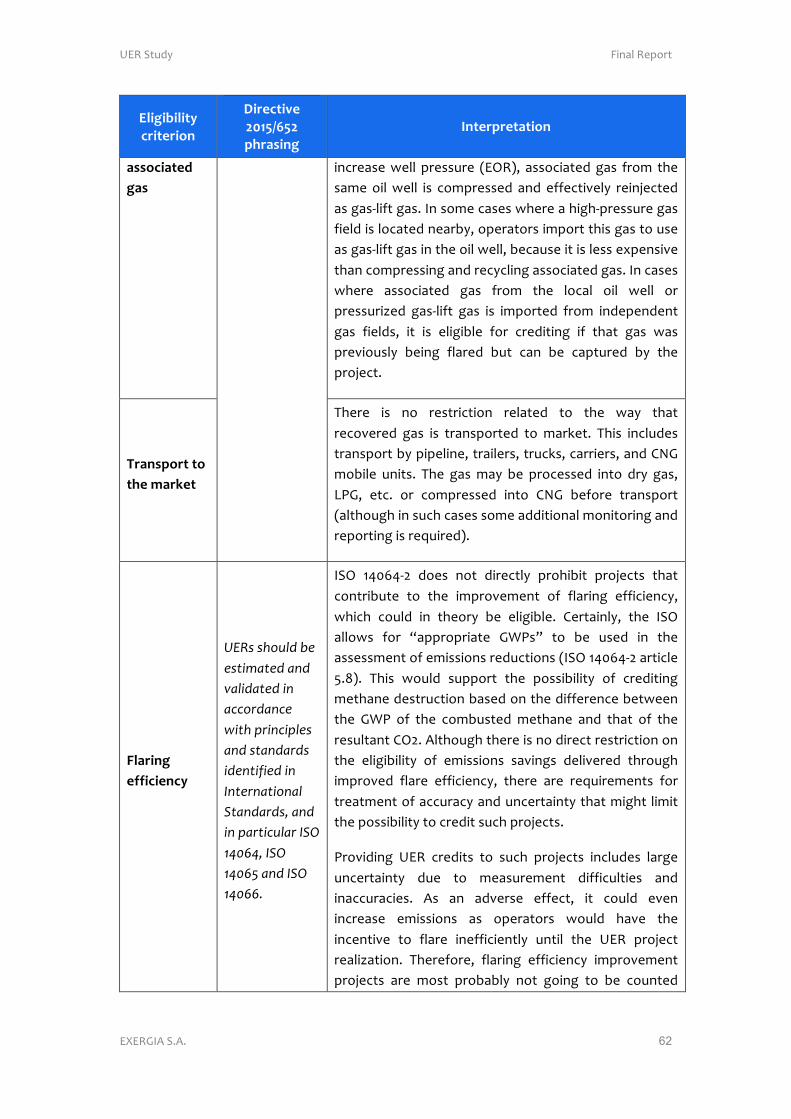

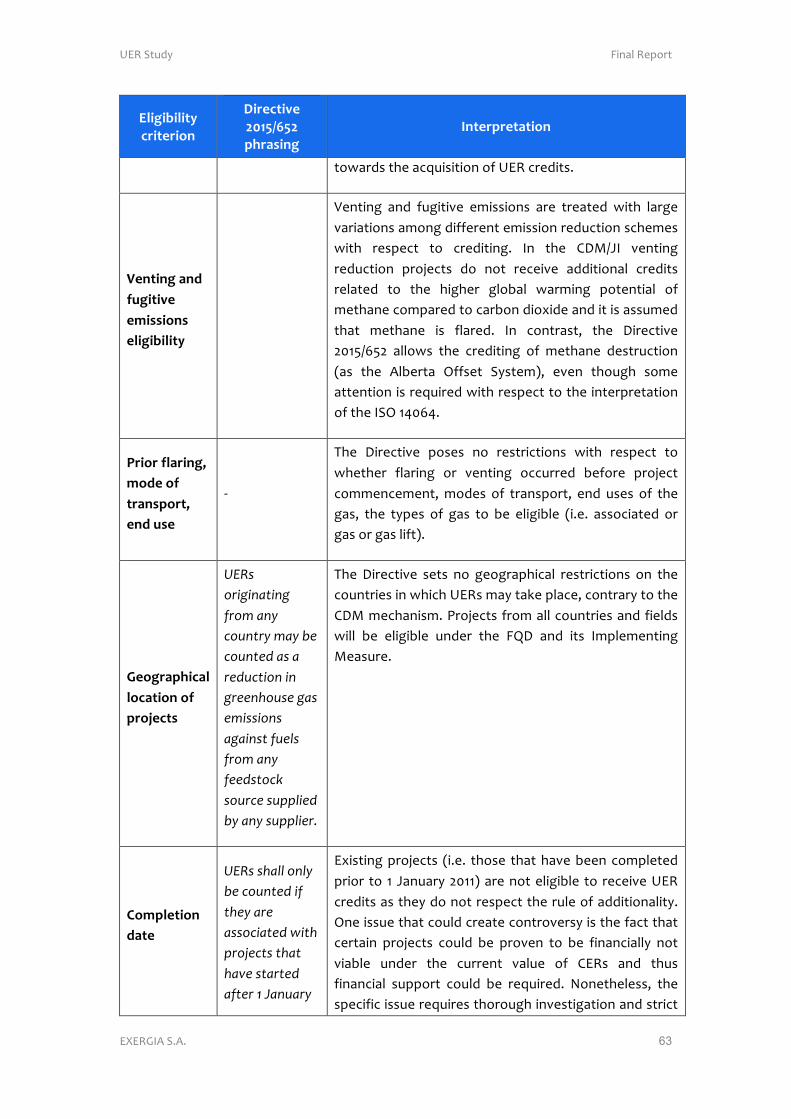

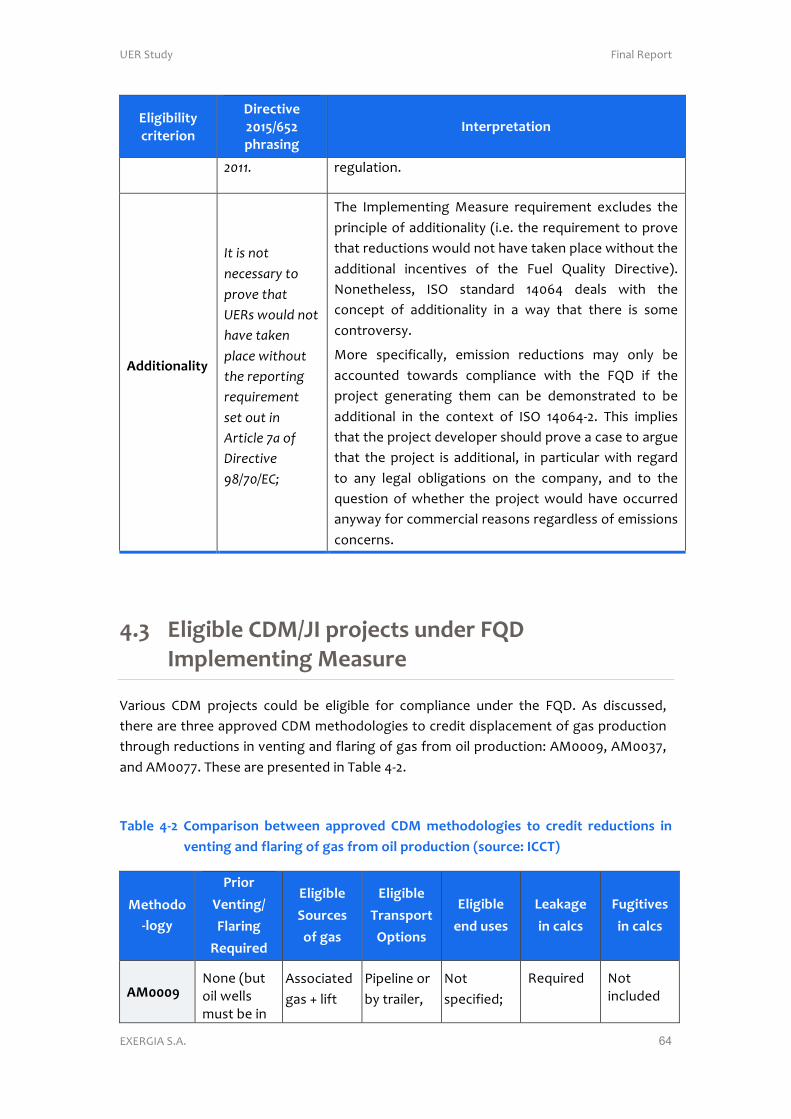

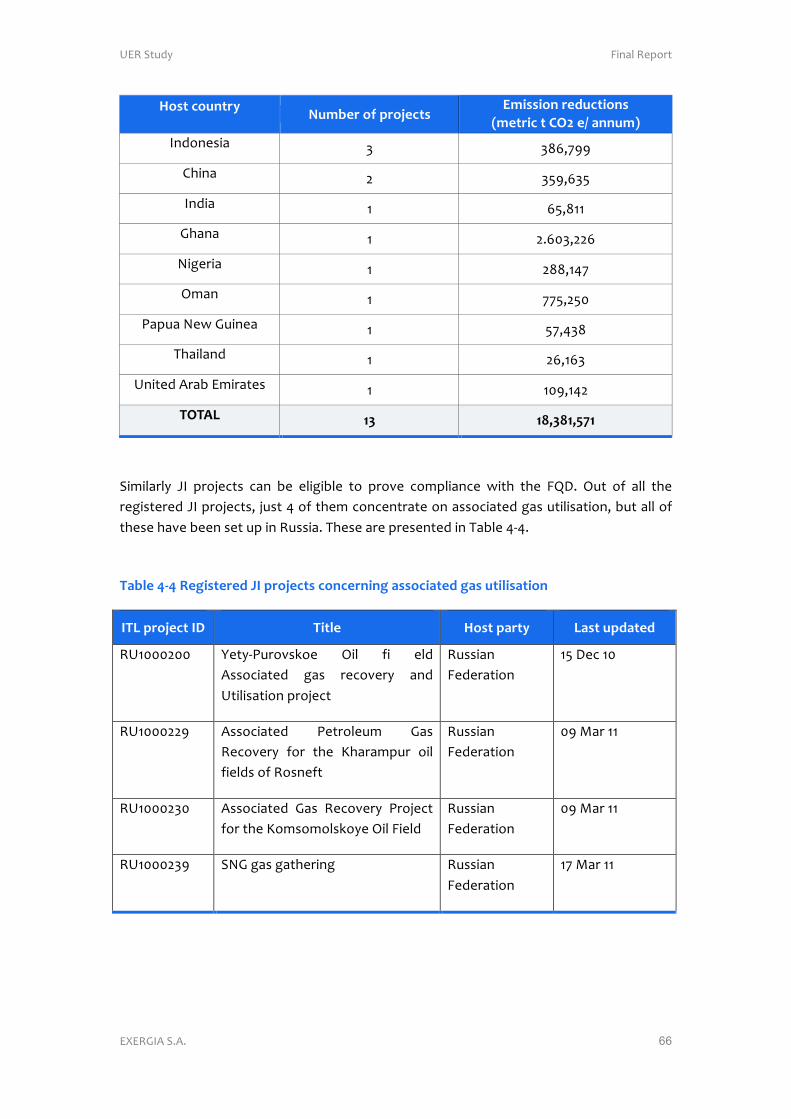

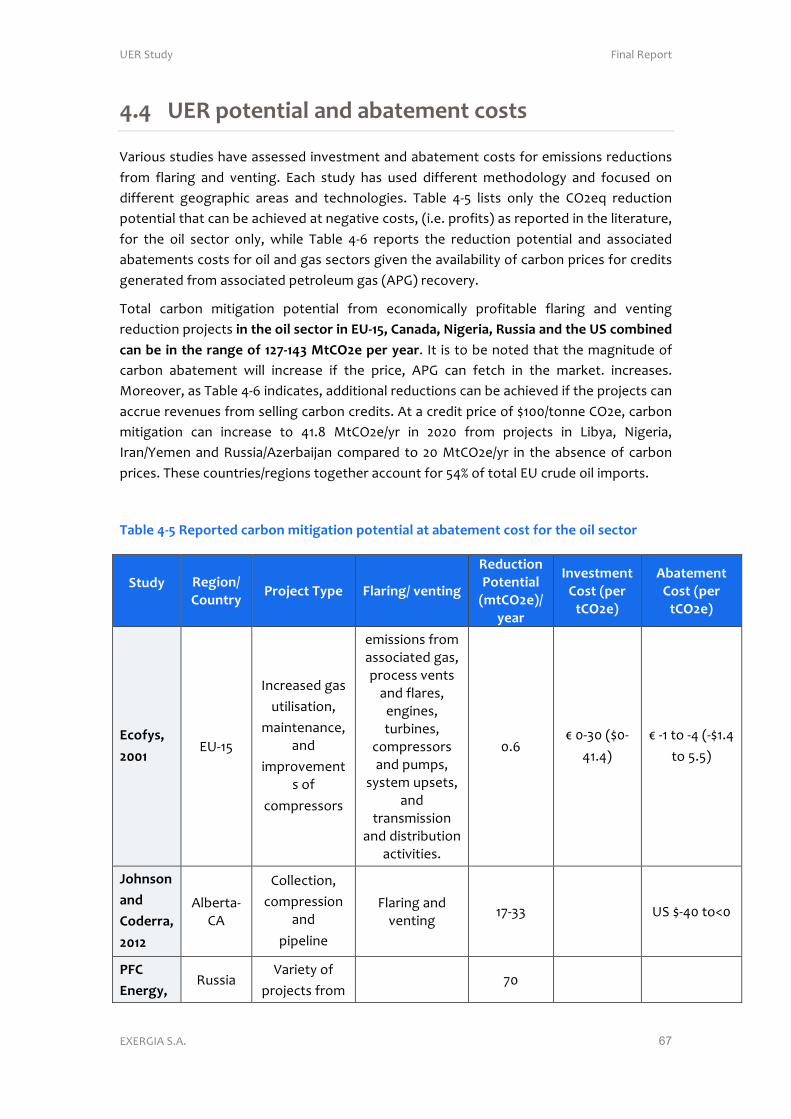

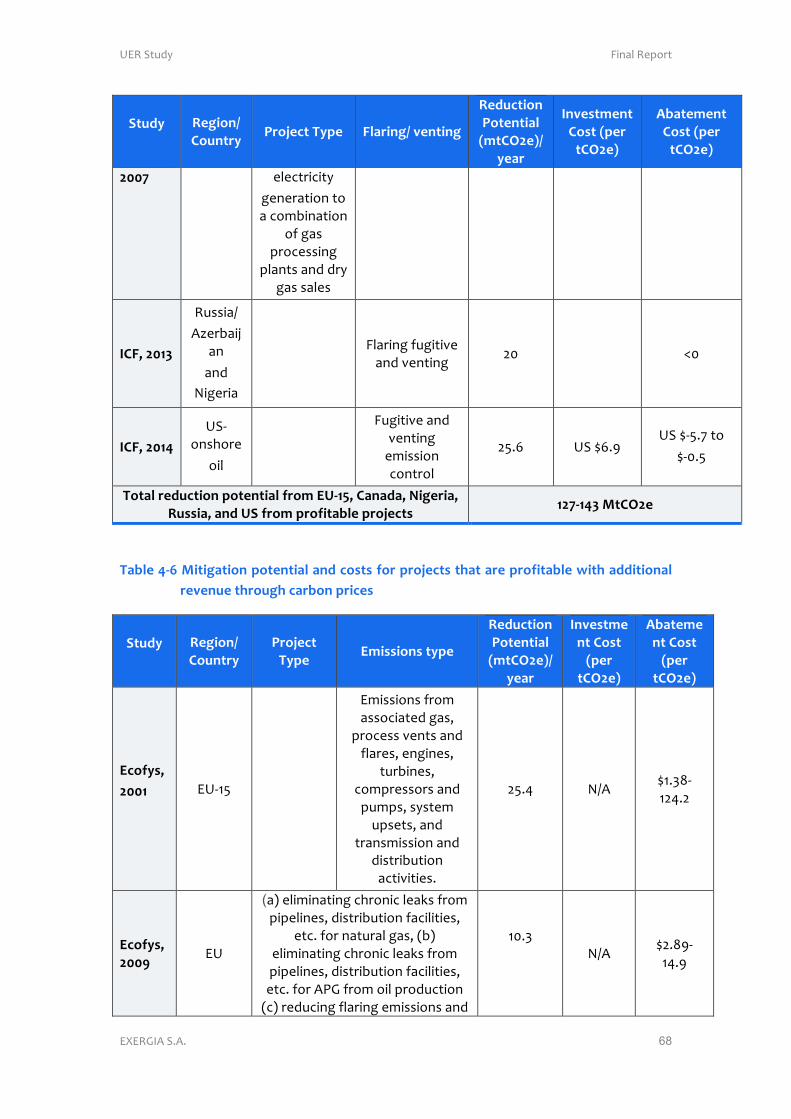

4 ASSESSMENT OF UER SUBJECT TO BE ACCOUNTED FOR UNDER THE FQD . . . . . . . . . . . . . . . . . . . . 604.1 UER reporting and certification mechanisms 604.2 UER project eligibility under FQD Implementing Measure requirements 614.3 Eligible CDM/JI projects under FQD Implementing Measure 644.4 UER potential and abatement costs 674.5 Technical and economic potential of UER strategies 694.6 UER potential under the FQD 71

4.6.1 FQD implementation in selected countries 73

5 PRACTICAL ASPECTS OF UER IMPLEMENTATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 755.1 Monitoring, Reporting and Verification 75

5.1.1 Overview of ISO Standards 755.1.2 ISO standards for UER implementation 775.1.3 EU Regulations referenced in the Implementing Measure 79

5.2 Additionality 805.2.1 Definition of baseline 805.2.2 Project boundaries 825.2.3 Definition of additionality by Member States 82

5.3 Double Counting 835.4 Potential implementation by Member States 845.5 Methodological issues 86

6 KEY FINDINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 896.1 Overview of Tasks 896.2 Concluding remarks 92

UERStudy FinalReport

EXERGIAS.A. 6

ABBREVIATIONS

AAU AssignedAmountUnits

APG AssociatedPetroleumGas

BCM BillionCubicMeters

BCF BillionCubicFeet

MCF MillionCubicFeet

MCM MillionCubicMeters

CAPEX CapitalExpenditure

CARB CaliforniaAirResourcesBoard

CCS CarbonCaptureandStorage

CDM CleanDevelopmentMechanism

CI CarbonIntensity

CNG CompressedNaturalGas

EEA EuropeanEconomicArea

EFTA EuropeanFreeTradeAssociation

EIA EnergyInformationAdministration

EOR EnhancedOilRecovery

ETS EmissionsTradingScheme

FQD FuelsQualityDirective

FSU FormerSovietUnion

GDP GrossDomesticProduct

GGFR GlobalGasFlaringReductionPartnership

GHG GreenhouseGas

GOR Gas-to-OilRatio

GPP GasProcessingPlant

GTL Gas-to-Liquid

GWP GlobalWarmingPotential

ICCT InternationalCouncilonCleanTransportation

IEA InternationalEnergyAgency

UERStudy FinalReport

EXERGIAS.A. 7

IOC InternationalOilCompany

JI JointImplementation

LCFS LowCarbonFuelStandard

LNG LiquefiedNaturalGas

LPG LiquefiedPetroleumGas

NGL NaturalGasLiquids

NNPC NigerianNationalPetroleumCorporation

NOAA NationalOceanicandAtmosphericAdministration

NPD NorwegianPetroleumDirectorate

RED RenewableEnergyDirective

RLCFRR British Columbia Renewable and Low Carbon FuelRequirementsRegulation

SNG SyntheticNaturalGas

UER UpstreamEmissionsReduction

USD UnitedStatesDollar

VAT ValueAddedTax

VFF Venting-Flaring-Fugitive

VIIRS VisibleInfraredImagingRadiometerSuite

WTW Well-to-Wheel

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 8!

+4+!5.-,+'1566(*7

-#$Q"RPS$N"#'

HI/! ,1&+1,! 1=! "0>&2/-?! #?+>>+1,>! $/('A&+1,! V"#$W! <->! +,&21('A/(! <+&I+,! &I/! 2/A/,&!R1',A+.! T+2/A&+;/! 8O9M\NM8\#R! 1,! _MKTN#O' R"U#' SKMSPMK$N"#' V%$W"R&' K#R' Q%X"Q$N#O'Q%YPNQ%V%#$&' XPQ&PK#$' $"' :NQ%S$NZ%' J8[GE[+!' "\' $W%' +PQ"X%K#' <KQMNKV%#$' K#R' "\' $W%'!"P#SNM' Q%MK$N#O' $"' $W%' YPKMN$T' "\' X%$Q"M' K#R' RN%&%M' \P%M&_! -,(! -+?>! &1! /,=12A/! &I/!+?0./?/,&-&+1,! 1=! 62&+A./! E-! 1=! &I/! *'/.! S'-.+&)! T+2/A&+;/! V*STW7! R'22/,&.)C! &I/2/! +>! -,!"#O"N#O'S"#&PM$K$N"#'L%$U%%#'$W%'+PQ"X%K#'!"VVN&&N"#]'6%VL%Q'1$K$%&'%^X%Q$&'K#R'_%T' &$K_%W"MR%Q&! -+?/(! -&! &I/! (/;/.10?/,&! 1=! -! A1??1,! +,&/202/&-&+1,! 1=! &I/! *ST!5?0./?/,&+,@! [/->'2/7! HI/! #'210/-,! R1??+>>+1,! -,,1',A/(! &I-&! &I/! 1'&0'&! 1=! &I+>!A1,>'.&-&+1,! <+..! A1,>+>&! 1=! -! ,1,U./@+>.-&+;/! @'+(-,A/! (1A'?/,&! 1,! -0021-AI/>! &1!Q'-,&+=)C!;/2+=)C!;-.+(-&/C!?1,+&12!-,(!2/012&!"0>&2/-?!#?+>>+1,!$/('A&+1,>!V"#$>W7!!

HI/!/.+@+L+.+&)C!?1,+&12+,@!-,(!;/2+=+A-&+1,!021A/('2/>C!->!</..!->!&/AI,+A-.!->0/A&>!2/.-&/(!&1!021Z/A&>!&1!L/!-AA1',&/(!=12!&I/!-AQ'+>+&+1,!1=!"#$!A2/(+&>!-2/!/X0/A&/(!&1!L/!A.-2+=+/(!1,A/! &I/! A1,>'.&-&+1,! +>! =+,-.+>/(! -,(! &I/! 5?0./?/,&+,@

UERStudy FinalReport

EXERGIAS.A. 9

reductiongoals.Othermeasures suchasE-Mobility, LNG,CNGor 1st and2ndGenerationBiofuels would not be needed anymore. Therefore UER could prevent the use ofRenewableEnergies in the transport sector.ThesubstitutioneffectsaredependentonmarketpricesofCO2emissionreductions.Atalowpriceof20US$/tCO2eq.alreadyhalfofthe FQD target could be met through UER. With prices comparable to those ofRenewable Energies the potential CO2 reduction through UER doubles. Anotherimportantinfluenceontheemissionsavingsisthetimeframefortheaccountabilityofthemeasure.

The scope and number of emission reduction projects, as well as the magnitude ofassociated UERs that could presumably be counted towards the FQD target remainunclear.Furthermore,withoutrestrictionsrelatedtotheeligibilityofcandidateprojects,thereisaconsiderableriskthattheFQDtargetisachievedwithreductionsfromprojectsthat would have happened anyway. This would undermine the FQD’s initial purpose:achievingadditionalreductionsinthelifecyclecarbonintensityofroadtransportfuels.

Inordertoestablishsecureandlastingemissionreductionswithoutfraud,anUERprojectisonlyeligibletocounttowardstheFQDifitmeetsanumberofISOstandards.Importantrequirements are concerning the additionally, the quality and the qualifications ofcertifyingbodies,thedeterminationofbaselinescenariosandthereportingsystem.

Other emission reduction options such as biofuels have to meet legally bindingsustainabilitycriteriaandrunthroughaLifeCycleAssessment.Inparallel,UERshouldbeobligedtorespectthesamestandards.

FactsaboutUpstreamEmissionReduction

1. Flaring,ventingandfugitiveemissionsrepresentthemostimportantsourceofGHGemissionsfromoilproductionoperations.Ventingandfugitiveemissionsarisefromoil field operations and devices. Sources include well work-overs and clean-ups,compressor start-upsandblowdowns,pipelinemaintenance,gasdehydrators,wellcellars, separators (wash tanks, free knock outs, etc.), sumps and pits, andcomponents(valves,connectors,pumpseals,flanges,etc.).Flaringofgas,eitherasameansofdisposalorasasafetymeasure,isasignificantsourceofairemissionsfromoilandgasinstallations.

2. Estimatescalculatedfromsatellite imagesofflares(NOAAdata,reportedbyGGFR)suggest that global gas flaring in 2012 was 144 billion cubic meters (bcm). Thisrepresents a massive resource waste and a considerable environmental problem,representing, in termsofemissions,some400milliontons inCO2emissionsand interms of quantity of natural gas wasted, one third of the European Union’s gasannual consumption. According to a recent study by ICCT , these global flaringquantities are comparable to the annual emissions from 125 medium sized (63Gigawatt)coalplantsintheUSA,or,inotherwords,closetotheentireemissionsofBrazil,Australia,FranceorItaly.Insomecountrieswithimportantoilproductionthisisamajorcontributortothenationalgreenhousegasemissionsinventory.

3. Whileflaringemissionscanbeestimatedwithsomedegreeofaccuracy,ventingandfugitive emissions are still very difficult to detect, creating thus an important

UERStudy FinalReport

EXERGIAS.A. 10

uncertaintyinthequantificationoftheircontributiontoglobalupstreamemissions,ascurrently,measurementfacilitiesarenotwidespread.Somestudies indicatethatGHG emissions related to deliberate venting and leakage of natural gas (fugitive)couldrepresentashareofupto5%oftotalglobalgreenhousegasemissions.

Preconditions and practical challenges that have to bemet if UER are accounted forundertheFQD

1. Projecteligibility: TheFQDdescribes in rough lineseligibleprojects,whicharenotlimitedtothosereducingventingandflaringemissions.Projecteligibilityislefttothehandsofnationallegislatorswhohavealargedegreeofflexibility.Furthermore,ISO14064-2 limits the scope of eligible projects to those that are additional to theappropriatelydefinedbaselinescenario.Inanycase,theImplementingMeasureandtheexpectednon-legislativeguidancethatwillfollowshouldprovidecleardirectionsonwhichprojectscouldbeconsideredaseligible.

2. Additionality:Although theFQDdoesnot includea referenceonadditionality, it isessential to prove - as derived from ISO 14064 - that the emission changes areadditional to what would have been expected in a business as usual scenario.Nonetheless,pooradditionalitycriteriawouldsignificantlyundermineitspurpose.Inthis case, the project baseline, as well as the project boundaries must be clearlydefined. It is therefore essential to develop common rules between projectproponentsandnationaladministrators fromMemberStateson theestablishmentofthesetwoparameters.

4. Implementation by Member States: National administrating bodies must beappointed, which will be responsible for monitoring and receiving emissionreductions from regulated parties and for confirming that reports of emissionsreductionscomplywiththerequirementsoftheFQD.

5. Common rules and criteria among MS: In order to ensure that the appropriatequalityisdeliveredbyallFQD-eligibleUERprojects,itisnecessaryforMStoestablishappropriatecommoncriteriaformeasurementandreportingunderUERschemes.

6. CentralizedUERregistry:TheexperiencefromtheEUETSandtherecenttransitionfrom a distributed crediting system to a centralized approach with a single EUregistry,withstandardizedmonitoring,reportingandverificationproceduresamongMember States shows that under such a system, credit trading is easier, lessadministrationandtransactioncostsarerequiredandthepotentialoffraud/double-countingisreduced.

7. Equal treatment among different emission reduction options: A requirement forbiofuels is a full Life Cycle Assessment; while only a relatively simple CO2 savingcalculation is prescribed for emissions reduction in the fossil fuel sector.Furthermore,inthecaseofbiofuelsthereisactualdeployment,whileinthecaseoffossil fuelsemissions savings, theseappear tohaveanaccountingcharacter. Thus,despite the fact that the accounting of net emission savings is the correctmethodology in the context of climate change policy in the transport sector, itshouldapplytoallemissionreductionoptionsequally.

UERStudy FinalReport

EXERGIAS.A. 11

1 INTRODUCTIONTOTHEPROJECT

TheArticle7a(1)oftheFuelQualityDirective(FQD)obligessupplierstoreportfrom2011informationon,interalia,theGHGintensityofthefueltheyhavesuppliedtoauthoritiesdesignatedbytheMemberStates.FurthermoretheEuropeanCommissionisempoweredto adopt Implementing Measures concerning the method for calculation and themechanism to monitor and reduce GHG emissions of fuels used in transport. To thisdirectiontherecentCouncilDirective2015/652on"layingdowncalculationmethodsandreportingrequirementspursuanttoDirective98/70/ECoftheEuropeanParliamentandoftheCouncilrelatingtothequalityofpetrolanddieselfuels"wasadoptedtoenforcethe implementation of Article 7a of the FQD. The notion of Upstream EmissionsReduction(UER)wasintroducedwithinthelatterDirective.

Until now, the scope and number of emission reduction projects, as well as themagnitude of associated UERs that could presumably be counted towards the FQDreduction target remains unclear. Without restrictions related to the eligibility ofcandidate projects, there is a considerable risk that the FQD target is achieved withreductionsfromprojectsthatwouldhavehappenedanyway,whichwouldunderminetheFQD’s initial purpose: achieving real reductions in the lifecycle carbon intensity of roadtransportfuels.

Currently,thereisanongoingconsultationbetweentheEuropeanCommission,MemberStates experts and key stakeholders aimed at the development of a commoninterpretationoftheFQDImplementingMeasure(CouncilDirective2015/652).Theoutputofthisconsultationwillconsistofanon-legislativeguidancedocumentonapproachestoquantify, verify, validate, monitor and report UERs. The eligibility, monitoring andverificationproceduresaswellas technicalaspects related toprojects tobeaccountedfor the acquisition ofUER credits are expected to be clarified once the consultation isfinalised and the Implementing Measure is transposed within Member States nationallegislation. The Consultant has considered to the extent possible the evolutions in thecontext of this consultation process during the elaboration of the present Study.Nonetheless,theanalysispresentedinthefollowingSectionsconsistsoftheConsultant’sbroaderunderstanding,basedonathoroughliteraturereviewofrelevantsources.

Theexact implementationofArticle7aof theFQD invariousMemberStatesandmorespecifically the economic cost for achieving the FQD (and RED) targets for emissionsreduction in the transport sector shall have a significant impact on the domesticEuropeanandnationalbiofuelmarkets.Therefore,theassessmentofUERtechnologies,theiraccountabilityinthecontextoftheFQD,theirtechnicalandeconomicpotentialisofcrucialimportancefortheprospectsofthebiofuelsector.

UERStudy FinalReport

EXERGIAS.A. 12

For this purpose the Association of the German Biofuel Industry has commissionedEXERGIA for theelaborationof a studyonUpstreamEmissionReductionof fossil fuelsrequired in the EU transport sector, as provided in the FQD Implementing MeasureRequirements. Thepresent reportwhich is submitted inMarch 2016 covers threemainTasks:

1. Anoverviewofmeasuresaimingatthereductionofupstreamemissionsforfossilfuelpathways(Chapter2);

2. Thepotential and incentivesprovidedby the FQDand its ImplementingMeasureforupstreamemissionreduction(Chapters3and4);

3. Practical aspects relevant to the implementation of an upstream emissionreductions (UERs) scheme in the context of FQD Art. 7a and its ImplementingMeasure(Chapter5).

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 13!

>' /,+*,-+?'/@'5<1.*+(6'+6-11-/0'*+:5!.-/0'6+(15*+1'

6AA12(+,@! &1! T+2/A&+;/! #R\8O9M\NM8C! g!"#$%&'() &(*##*+,#) (&',#) '--) .%&&,/+!#&) .'#)&(*##*+,#)+00!%%*,.)"%*+%)$+)$/&)%'1)('$&%*'-)&,$&%*,.)')%&2*,&%3)+%)')"%+0&##*,.)"-',$)1/&%&)$/&)2!&-4)'#)%&2&%%&5)$+)*,)6,,&7)84)1'#)"%+5!0&597!HI'>C!&I/!,1&+1,!1=!'0>&2/-?!/?+>>+1,>!->! 021;+(/(! <+&I+,! &I/! T+2/A&+;/! +,A.'(/>! &I/! =1..1<+,@! ?-Z12! >&-@/>! 1=! &I/! =1>>+.! ='/.!.+=/A)A./`!

#X0.12-&+1,!-,(!=+/.(!(/;/.10?/,&C!

*'/.!!021('A&+1,!-,(!2/A1;/2)! *'/.!021A/>>+,@! *//(>&1A^!&2-,>012&-&+1,!&1!&I/!2/=+,/2)!@-&/9!

HI/! 02/>/,&! >/A&+1,! =1A'>/>! 1,! &I/! (/=+,+&+1,! 1=! '0>&2/-?! /?+>>+1,>C! ->! </..! ->! 1,!?/&I1(>!-,(!L/>&!02-A&+A/>!-+?+,@!-&!&I/+2!2/('A&+1,7!5,!-((+&+1,C!+&!021;+(/>!-,!1;/2;+/<!1=! '0>&2/-?! /?+>>+1,>! 2/('A&+1,! +,A/,&+;/>! +,! &-2@/&! A1',&2+/>! -,(! 1=! ^/)! /X+>&+,@!021Z/A&>7!

>29' /Z%QZN%U'"\'5X&$Q%KV'+VN$$N#O'(S$NZN$N%&'

f+&I+,!/-AI!?-Z12!021('A&+1,!>&-@/C!-!,'?L/2!1=!-A&+;+&+/>!-,(!021A/>>/>!1AA'27!HI/!?-+,!>&-@/>!1=! &I/! &1&-.!'0>&2/-?!A-2L1,! +,&/,>+&)!1=! =1>>+.! ='/.>!A-,!L/!>'LU(+;+(/(! +,&1! &I/!=1..1<+,@!021A/>>/>`!

+^XM"QK$N"#C! <I+AI! A1,&-+,>! 02/U021('A&+1,! /?+>>+1,>! &I-&! 1AA'2! ('2+,@! 02+?-2)!/X0.12-&+1,!=12!0/&21./'?7!

:QNMMN#O' K#R' R%Z%M"XV%#$]! +,A.'(+,@! /?+>>+1,>! &I-&! 1AA'2! ('2+,@! (/;/.10?/,&! 1=!A2'(/!1+.!021('A&+1,!=-A+.+&+/>7!

<Q"RPS$N"#'K#R'%^$QKS$N"#C!<I+AI!?1(/.>!&I/!<12^!2/Q'+2/(!&1!.+=&!l'+(>!=21?!&I/!>'L>'2=-A/!-,(!&1!+,Z/A&!l'+(>!+,&1!&I/!>'L>'2=-A/7!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!! !9!5&!I->!&1!L/!,1&/(!&I-&!+,!#3#$456j>!2/A/,&!g%&'()!1,!-A&'-.!4b4!(-&-!=12!(+/>/.C!0/&21.C!^/21>/,/!-,(!,-&'2-.! @->hC! A1??+>>+1,/(!L)!T4!#P#$C! &I/! -0021-AI!1,! ='/.! .+=/A)A./! >&-@/>!<->! >.+@I&.)!(+==/2/,&!&I-,!+,!&I/!A->/!1=!T+2/A&+;/!#R\8O9M\NM8!V<I+AI!<->!,1&+=+/(!>1?/!?1,&I>!.-&/2W7!5,!&I/!.-&&/2!>&'()!&I/!'0>&2/-?!>&-@/!(+(!,1&!+,A.'(/!&2-,>012&-&+1,!1=!=//(>&1A^C!<I+AI!<->!2-&I/2!0-2&!1=!&I/!g?+(>&2/-?h!>&-@/7!5,!&I/!02/>/,&!>&'()C!&I/!(/=+,+&+1,!@+;/,!+,!&I/!T+2/A&+;/!<+..!L/!'>/(7!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 14!

1PQ\KS%' XQ"S%&&N#OC! <I+AI! ?1(/.>! I-,(.+,@! 1=! A2'(/C! <-&/2C! -,(! ->>1A+-&/(! @->!<+&I!-!>/&!1=!A1??1,!+,('>&2)!&/AI,1.1@+/>7!

6KN#$%#K#S%C! 2/@-2(+,@! &I/! ;/,&+,@! -,(! ='@+&+;/! /?+>>+1,>! ->>1A+-&/(! <+&I!?-+,&/,-,A/7!

?K&$%'RN&X"&KM]'2/=/22+,@!&1!&I/!/?+>>+1,>!-L1'&!<->&/!(+>01>-.7!

!QPR%'$QK#&X"Q$]!-..1<+,@!;-2+-&+1,!+,!&I/!&2-,>012&!?1(/>!'>/(!&1!&2-,>012&!A2'(/!1+.!=21?!/X&2-A&+1,!&1!&I/!2/=+,/2)!>&-@/!-,(!&I/!(+>&-,A/!&2-;/../(7!

)N$PV%#' %^$QKS$N"#' K#R' PXOQKRN#O]! ?1(/..+,@! &I/! /X&2-A&+1,! 1=! A2'(/! L+&'?/,!>/0-2-&/.)!=21?!&I/!021('A&+1,!1=!A1,;/,&+1,-.!A2'(/!1+.7!

@MKQN#O]' Z%#$N#O' K#R' \PON$NZ%' %VN&&N"#&! 2/02/>/,&! &I/! ?1>&! +?012&-,&! >1'2A/! 1=! 4b4!/?+>>+1,>! =21?!1+.! 021('A&+1,!10/2-&+1,>7! F/,&+,@! -,(! ='@+&+;/! /?+>>+1,>! -2+>/! =21?!1+.!k/.(!10/2-&+1,>!-,(!(/;+A/>7!%1'2A/>!+,A.'(/!</..!<12^U1;/2>!-,(!A./-,U'0>C!A1?02/>>12!>&-2&U'0>!-,(!L.1<(1<,>C!0+0/.+,/!?-+,&/,-,A/C!@->!(/I)(2-&12>C!</..!A/..-2>C!>/0-2-&12>!V<->I!&-,^>C!=2//!^,1A^!1'&>C!/&A7WC!>'?0>!-,(!0+&>C!-,(!A1?01,/,&>!V;-.;/>C!A1,,/A&12>C!0'?0! >/-.>C! l-,@/>C! /&A7W7! *.-2+,@! 1=! @->C! /+&I/2! ->! -! ?/-,>! 1=! (+>01>-.! 12! ->! -! >-=/&)!?/->'2/C! +>! -! >+@,+=+A-,&! >1'2A/! 1=! -+2! /?+>>+1,>! =21?! 1+.! -,(! @->! +,>&-..-&+1,>7! #;/,! +=!A1,&+,'1'>! =.-2+,@! /,(/(C! 1AA->+1,-.! L'2,+,@! 1=! >?-..! -?1',&>! 1=! @->! <+..! >&+..! L/!,/A/>>-2)!=12!>-=/&)!2/->1,>7!

6,1&I/2! /?+&&+,@! 021A/>>! +>! &I/! '>/! 1=! &I/! /,/2@)U+,&/,>+;/! >/A1,(-2)! -,(! &/2&+-2)!2/A1;/2)! &/AI,1.1@+/>C! >'AI! ->! <-&/2! =.11(+,@C! @->! .+=&+,@C! @->! =.11(+,@! /&A7! *12! &I/!-00.+A-&+1,!1=!&I/>/!&/AI,1.1@+/>C!-((+&+1,-.!/,/2@)!+>!2/Q'+2/(!+,!12(/2!&1!.+=&!&I/!A2'(/!1+.! =21?!1+.!</..7! :&I/2! /?+>>+1,>! &-^/! 0.-A/! ('/! &1! +,A2/->/(! 0'?0+,@! -,(! >/0-2-&+1,!<12^!->>1A+-&/(!<+&I!+,A2/->/(!l'+(!I-,(.+,@!+,!(/0./&/(!1+.!k/.(>!V+7/7C!k/.(>!<+&I!-!I+@I!<-&/2U1+.!2-&+1W7!6&!&I/!?+(>&2/-?!./;/.C!4b4!/?+>>+1,>!('/!&1!&2-,>012&-&+1,!A-,!I-;/!-!>+@,+=+A-,&!>I-2/!+,!&I/!&1&-.!4b4!/?+>>+1,>!->>/>>/(C!/>0/A+-..)!<I/,!A1,>+(/2+,@!A2'(/>!+?012&/(!=21?!(+>&-,&!<12.(!-2/->!&1!&I/!#"!2/=+,/2+/>7!

>2929 1NO#N\NSK#S%'"\'Z%#$N#O]'\MKQN#O'K#R'\PON$NZ%'%VN&&N"#&

#>&+?-&/>! A-.A'.-&/(! =21?! >-&/..+&/! +?-@/>! 1=! =.-2/>! VP:66! (-&-C! 2/012&/(! L)! 44*$W!>'@@/>&!&I-&[email protected].!@->!=.-2+,@!+,!8O98!<->!9DD!L+..+1,!A'L+A!?/&/2>!VLA?W7!HI+>!2/02/>/,&>!-!?->>+;/! 2/>1'2A/!<->&/! -,(! -! A1,>+(/2-L./! /,;+21,?/,&-.! 021L./?C! 2/02/>/,&+,@C! +,!&/2?>!1=!/?+>>+1,>C! >1?/!DOO!?+..+1,! &1,>! +,!R:8!/?+>>+1,>!-,(! +,! &/2?>!1=!Q'-,&+&)!1=!,-&'2-.! @->! <->&/(C! 1,/! &I+2(! 1=! &I/! #'210/-,! ",+1,j>! @->! -,,'-.! A1,>'?0&+1,87!6AA12(+,@! &1! -! 2/A/,&! >&'()!L)! 5RRHBC! &I/>/[email protected].! =.-2+,@!Q'-,&+&+/>! -2/! A1?0-2-L./! &1!&I/!-,,'-.!/?+>>+1,>!=21?!98M!?/(+'?!>+c/(!VNB!@+@-<-&&W!A1-.!0.-,&>! +,!&I/!"%6C!12C! +,!1&I/2!<12(>C! A.1>/! &1! &I/! /,&+2/! /?+>>+1,>! 1=! Y2-c+.C! 6'>&2-.+-C! *2-,A/! 12! 5&-.)7! 5,! >1?/!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!! !86>>1A+-&/(! K/&21./'?! 4->! *.-2+,@! %&'()! =12! $'>>+-C! o-c-^I>&-,C! H'2^?/,+>&-,! -,(! 6c/2L-+Z-,C!R-2L1,!a+?+&>C!8O9B!B!HI/!2/('A&+1,!1=!'0>&2/-?!4b4!/?+>>+1,>!=21?!=.-2+,@!-,(!;/,&+,@C!$/012&!L)!&I/!5,&/2,-&+1,-.!R1',A+.! 1,! R./-,! H2-,>012&-&+1,! &1! &I/! #'210/-,! R1??+>>+1,! T+2/A&12-&/U4/,/2-.! =12! R.+?-&/!6A&+1,C!8O9D!

UERStudy FinalReport

EXERGIAS.A. 15

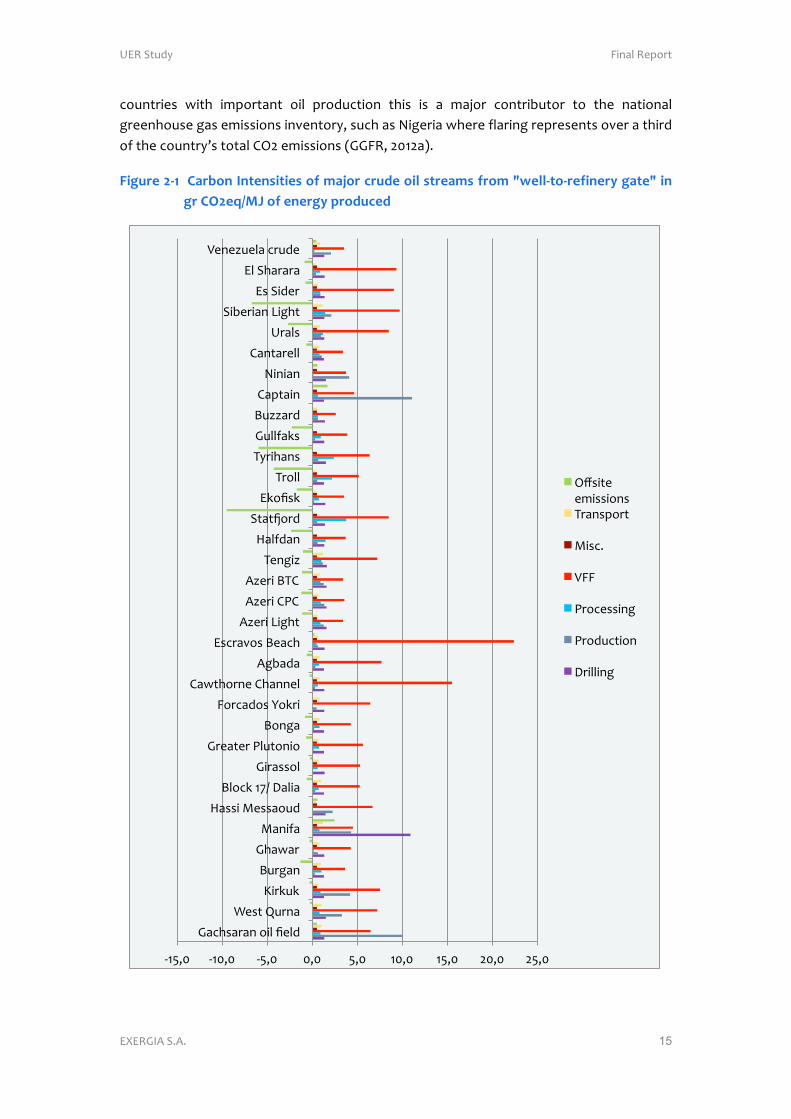

countries with important oil production this is a major contributor to the nationalgreenhousegasemissionsinventory,suchasNigeriawhereflaringrepresentsoverathirdofthecountry’stotalCO2emissions(GGFR,2012a).

Figure2-1CarbonIntensitiesofmajorcrudeoilstreamsfrom"well-to-refinerygate"ingrCO2eq/MJofenergyproduced

-15,0 -10,0 -5,0 0,0 5,0 10,0 15,0 20,0 25,0

Gachsaranoilfield

WestQurna

Kirkuk

Burgan

Ghawar

Manifa

HassiMessaoud

Block17/Dalia

Girassol

GreaterPlutonio

Bonga

ForcadosYokri

CawthorneChannel

Agbada

EscravosBeach

AzeriLight

AzeriCPC

AzeriBTC

Tengiz

Halfdan

Statqord

Ekofisk

Troll

Tyrihans

Gullfaks

Buzzard

Captain

Ninian

Cantarell

Urals

SiberianLight

EsSider

ElSharara

Venezuelacrude

OffsiteemissionsTransport

Misc.

VFF

Processing

Production

Drilling

UERStudy FinalReport

EXERGIAS.A. 16

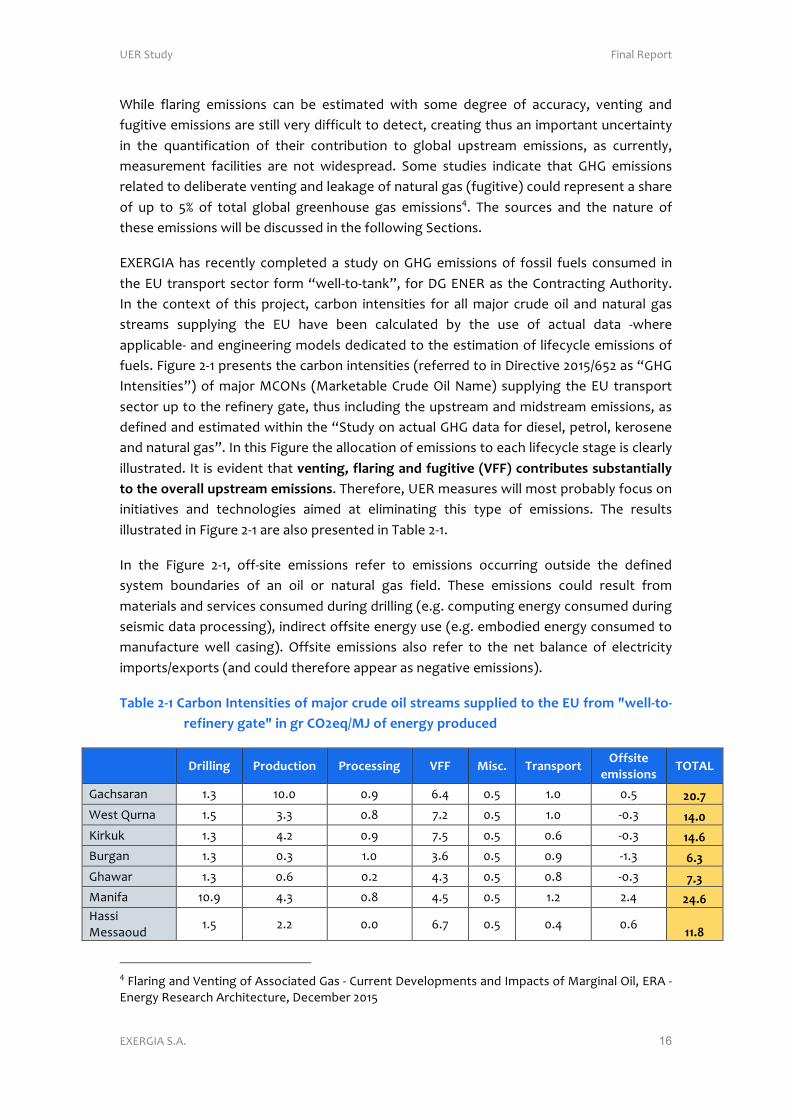

While flaring emissions can be estimated with some degree of accuracy, venting andfugitiveemissionsarestillverydifficulttodetect,creatingthusanimportantuncertaintyin the quantification of their contribution to global upstream emissions, as currently,measurement facilities are not widespread. Some studies indicate that GHG emissionsrelatedtodeliberateventingandleakageofnaturalgas(fugitive)couldrepresentashareof up to 5% of total global greenhouse gas emissions4. The sources and the nature oftheseemissionswillbediscussedinthefollowingSections.

EXERGIAhas recently completed a studyonGHGemissionsof fossil fuels consumed intheEUtransportsector form“well-to-tank”, forDGENERastheContractingAuthority.In the context of this project, carbon intensities for allmajor crudeoil and natural gasstreams supplying the EU have been calculated by the use of actual data -whereapplicable-andengineeringmodelsdedicatedtotheestimationoflifecycleemissionsoffuels.Figure2-1presentsthecarbonintensities(referredtoinDirective2015/652as“GHGIntensities”)ofmajorMCONs (MarketableCrudeOilName) supplying theEU transportsectoruptotherefinerygate,thusincludingtheupstreamandmidstreamemissions,asdefinedandestimatedwithinthe“StudyonactualGHGdatafordiesel,petrol,keroseneandnaturalgas”.InthisFiguretheallocationofemissionstoeachlifecyclestageisclearlyillustrated.It isevidentthatventing,flaringandfugitive(VFF)contributessubstantiallytotheoverallupstreamemissions.Therefore,UERmeasureswillmostprobablyfocusoninitiatives and technologies aimed at eliminating this type of emissions. The resultsillustratedinFigure2-1arealsopresentedinTable2-1.

In the Figure 2-1, off-site emissions refer to emissions occurring outside the definedsystem boundaries of an oil or natural gas field. These emissions could result frommaterialsandservicesconsumedduringdrilling(e.g.computingenergyconsumedduringseismicdataprocessing),indirectoffsiteenergyuse(e.g.embodiedenergyconsumedtomanufacturewell casing). Offsite emissions also refer to the net balance of electricityimports/exports(andcouldthereforeappearasnegativeemissions).

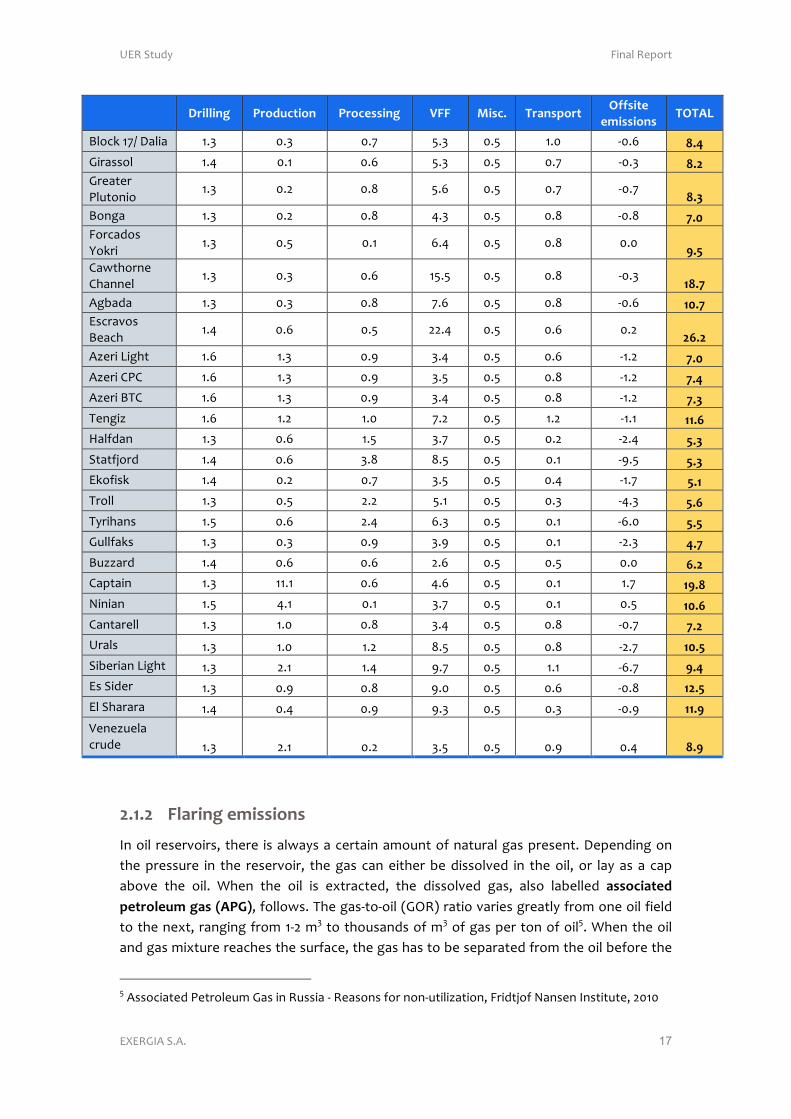

Table2-1CarbonIntensitiesofmajorcrudeoilstreamssuppliedtotheEUfrom"well-to-refinerygate"ingrCO2eq/MJofenergyproduced

Drilling Production Processing VFF Misc. Transport Offsiteemissions

TOTAL

Gachsaran 1.3 10.0 0.9 6.4 0.5 1.0 0.5 20.7WestQurna 1.5 3.3 0.8 7.2 0.5 1.0 -0.3 14.0Kirkuk 1.3 4.2 0.9 7.5 0.5 0.6 -0.3 14.6Burgan 1.3 0.3 1.0 3.6 0.5 0.9 -1.3 6.3Ghawar 1.3 0.6 0.2 4.3 0.5 0.8 -0.3 7.3Manifa 10.9 4.3 0.8 4.5 0.5 1.2 2.4 24.6HassiMessaoud 1.5 2.2 0.0 6.7 0.5 0.4 0.6 11.8

4FlaringandVentingofAssociatedGas-CurrentDevelopmentsandImpactsofMarginalOil,ERA-EnergyResearchArchitecture,December2015

UERStudy FinalReport

EXERGIAS.A. 17

Drilling Production Processing VFF Misc. Transport Offsiteemissions

TOTAL

Block17/Dalia 1.3 0.3 0.7 5.3 0.5 1.0 -0.6 8.4Girassol 1.4 0.1 0.6 5.3 0.5 0.7 -0.3 8.2GreaterPlutonio

1.3 0.2 0.8 5.6 0.5 0.7 -0.78.3

Bonga 1.3 0.2 0.8 4.3 0.5 0.8 -0.8 7.0ForcadosYokri 1.3 0.5 0.1 6.4 0.5 0.8 0.0 9.5CawthorneChannel

1.3 0.3 0.6 15.5 0.5 0.8 -0.318.7

Agbada 1.3 0.3 0.8 7.6 0.5 0.8 -0.6 10.7EscravosBeach 1.4 0.6 0.5 22.4 0.5 0.6 0.2 26.2AzeriLight 1.6 1.3 0.9 3.4 0.5 0.6 -1.2 7.0AzeriCPC 1.6 1.3 0.9 3.5 0.5 0.8 -1.2 7.4AzeriBTC 1.6 1.3 0.9 3.4 0.5 0.8 -1.2 7.3Tengiz 1.6 1.2 1.0 7.2 0.5 1.2 -1.1 11.6Halfdan 1.3 0.6 1.5 3.7 0.5 0.2 -2.4 5.3Statfjord 1.4 0.6 3.8 8.5 0.5 0.1 -9.5 5.3Ekofisk 1.4 0.2 0.7 3.5 0.5 0.4 -1.7 5.1Troll 1.3 0.5 2.2 5.1 0.5 0.3 -4.3 5.6Tyrihans 1.5 0.6 2.4 6.3 0.5 0.1 -6.0 5.5Gullfaks 1.3 0.3 0.9 3.9 0.5 0.1 -2.3 4.7Buzzard 1.4 0.6 0.6 2.6 0.5 0.5 0.0 6.2Captain 1.3 11.1 0.6 4.6 0.5 0.1 1.7 19.8Ninian 1.5 4.1 0.1 3.7 0.5 0.1 0.5 10.6Cantarell 1.3 1.0 0.8 3.4 0.5 0.8 -0.7 7.2Urals 1.3 1.0 1.2 8.5 0.5 0.8 -2.7 10.5SiberianLight 1.3 2.1 1.4 9.7 0.5 1.1 -6.7 9.4EsSider 1.3 0.9 0.8 9.0 0.5 0.6 -0.8 12.5ElSharara 1.4 0.4 0.9 9.3 0.5 0.3 -0.9 11.9Venezuelacrude 1.3 2.1 0.2 3.5 0.5 0.9 0.4 8.9

2.1.2 Flaringemissions

Inoil reservoirs, there isalwaysacertainamountofnaturalgaspresent.Dependingonthepressure in the reservoir, the gas can either be dissolved in theoil, or lay as a capabove the oil. When the oil is extracted, the dissolved gas, also labelled associatedpetroleumgas(APG),follows.Thegas-to-oil(GOR)ratiovariesgreatlyfromoneoilfieldtothenext,rangingfrom1-2m3tothousandsofm3ofgaspertonofoil5.Whentheoilandgasmixturereachesthesurface,thegashastobeseparatedfromtheoilbeforethe

5AssociatedPetroleumGasinRussia-Reasonsfornon-utilization,FridtjofNansenInstitute,2010

UERStudy FinalReport

EXERGIAS.A. 18

oil enters thepipelines.Most flaringprocessesusually takeplaceat stack topwith thevisibleflame,asopposedto incineration,wherewastegas iscombustedatthefurnace.Flaring during well tests, production of associated gas, refining and other processingstages is used in awayof open flame. There are some reasons for that: first, gasmaycontaincorrosivecompounds,soitcanbequitedestructive,secondly,theremightbetheneedtodisposehugeamountsofgasinashorttime.

Combustionofnaturalgasiscalledflaring,whilereleasingittotheatmosphereisknownasventing.Duetounavailabilityoflocalmarketandtransportationsystemsinproductionareas, operators usually flare or vent associated gas to avoid additional treatment andprocessingexpenses.Decisionofflaringandventingorprocessingofgasmightdependonnaturalgaspriceswhichcouldhaveamajorimpactonit.Forsafetyreasons,ventingisnotacommonpractice.

2.1.3 VentingandFugitiveemissions

Fugitiveemissionsrefertounintentionalmethaneleakagesfromoilandgasoperations,whereas venting emissions are related to the intentional release of methane to theenvironmentformaintenanceorotherreasonsandtheyarebothasourceofgreenhousegasemissionsinmanycountries.Methaneemissionsoccuratallstagesofthevaluechainof natural gas and oil activities, although they concern mainly upstream activities.Methaneemissionspredominantlyoccurduringgasproductionandtransportation(e.g.from compressors, dehydrators and pumps, pneumatic devices, fugitive leakages, wellblow-downsandcompletions).Productionofoilisalsoasourceofmethaneemissionsinmanyregions(e.g.degassingoffluids,flaring/coldventingandproductstorage/loading);however oil upstream activities emit much less methane than natural gas upstreamoperations.

The principal sources ofmethane emissions in the natural gas sector are attributed tounintentional equipment or pipeline leaks. These fugitive emissions occur as the gascirculates at extremely high pressure through different parts of the infrastructure ofnatural gas systems and escapes into the atmosphere through tattered connections inthepipelines,wornpumpandcompressorseals,valvesor flanges.Emissionsalsooccurduringmaintenanceandventingactivities, aswell as throughaccidentsandequipmentfailures.Intheoilsector,methaneemissionsoccurmainlyfromgasventingfromoilwells,oil storage tanks and production equipment. Some studies indicate that methaneemissions from natural gas and oil systems account for approximately 18% and 2%,respectively,ofglobalmethaneemissions.Emissionsareexpectedtogrowasnaturalgasandoilconsumptionincreases,duetoaginginfrastructure.

These emissions are difficult to quantify with a high degree of accuracy and there issubstantialuncertaintyinthevaluesavailableforsomeofthemajoroilandgasproducingcountries(e.g.Russia).Inthepublicdomain,availabledatapredominantlyoriginatefromNorth America (i.e. US and Canada) since very few empirical studies are available forother key oil and gas regions. The main reason for uncertainty in the assessment ofmethaneemissions is the fact thatmeasurementprogrammesare timeconsumingand

UERStudy FinalReport

EXERGIAS.A. 19

verycostlytoperform,thereforeoperatorstendtorelyontheuseofsimpleproduction-basedemissionfactorswhicharesusceptibletoexcessiveerrors.

2.2 UpstreamEmissionReductionTechnologies

In oil fieldswhere there are important quantities of associatedgas, themost commonpractice utilized until today is flaring, i.e. open air burning of APG. Flaring has severeenvironmentaleffectsandiseconomicallywasteful.Eveninsiteswithinstalledburnersofhigh flaring efficiency, there are big amounts of greenhouse gases released to theatmosphere. The output of the flaring process includes mainly carbon dioxide andquantitiesofmethane,whichcanbequite importantdependingon thecompositionofthe gas and the flaring efficiency. Methane emission from gas flares is the result ofincompletecombustionofthewastegasandthus isrelatedtothedestructionefficiencyoftheflares.

Duetothehazardousconsequencesof flaringgas, it isnotconsideredasanoptionforupstream emission reduction, although it is a solution for minimising the emission ofmethane, which is a much more potent gas than carbon dioxide, in terms of globalwarming. Therefore flaring will not be discussed as an upstream emission reductionoption in the present section, which will rather focus on alternative solutions andtechnologies.

2.2.1 OverviewofAPGUtilisationOptions

For each site where APG is flared, a number of alternative value chains may beestablishedtorecoverandutilizepartofthegas.TheeconomicviabilityofeachoftheseAPGutilisationoptions isaffectedbya largenumberoffactors,e.g.gascharacteristics,location and presence of existing infrastructure, market conditions, etc. The optimalsolutionforaparticularsiteisthushighlycasespecific.

DifferentAPGstreamscanhave largevariations ingascompositionand impurities, andthusmayrequiredifferent levelsof treatment.Thevariation incompositionalsomeansthat different APG streams will provide different product yields and thus differenteconomic values, even when applying the same technological solutions. Some gasutilisationoptions,suchasprocessing intodrygas,LPGornaturalgasoline,havebetterreturnswhentherecoverablegasstreamis“rich”,i.e.,whenitcontainsalargeportionofheavier hydrocarbons. Other options for APG use, such as large-scale electricitygeneration,generallyworkbetterwhenthegasis“lean”.AnAPGstreamwillalwaysbemoreattractivewhenitcontainsfewerimpuritiesandisatanelevatedpressure,duetoreducedcostsrequiredfortreatmentandcompression.

UERStudy FinalReport

EXERGIAS.A. 20

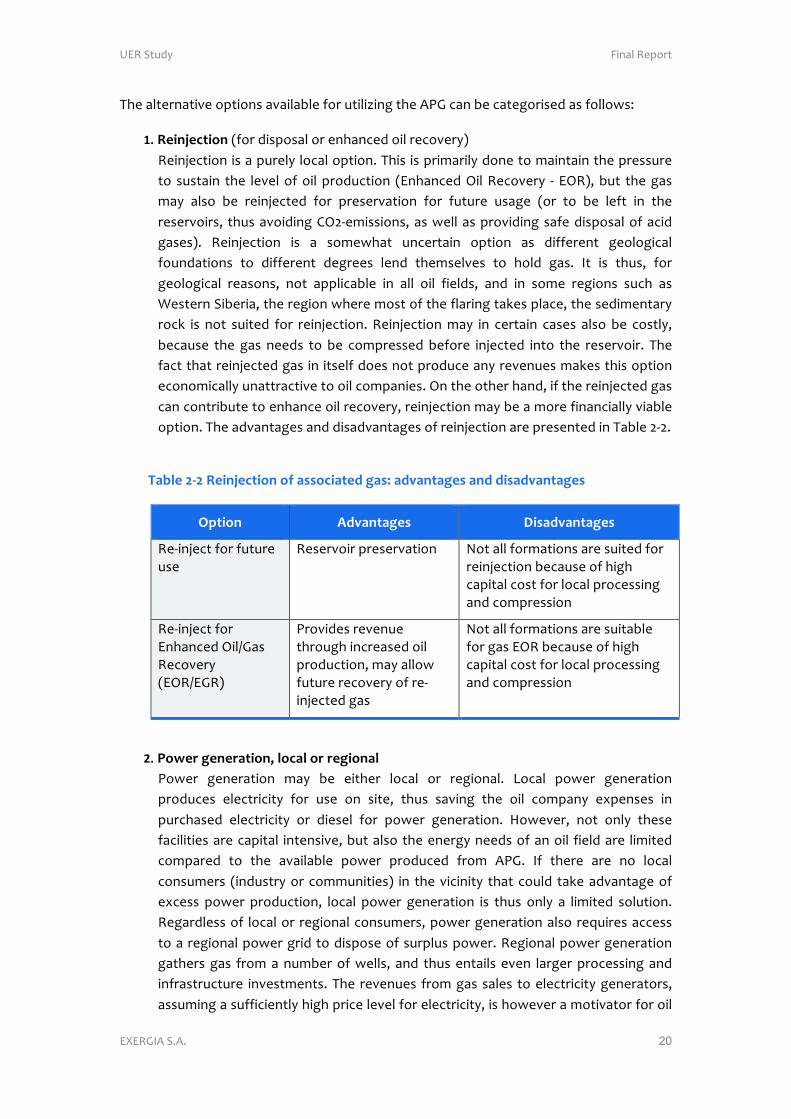

ThealternativeoptionsavailableforutilizingtheAPGcanbecategorisedasfollows:

1. Reinjection(fordisposalorenhancedoilrecovery)Reinjectionisapurelylocaloption.This isprimarilydonetomaintainthepressureto sustain the levelofoil production (EnhancedOilRecovery - EOR),but thegasmay also be reinjected for preservation for future usage (or to be left in thereservoirs, thusavoidingCO2-emissions,aswellasprovidingsafedisposalofacidgases). Reinjection is a somewhat uncertain option as different geologicalfoundations to different degrees lend themselves to hold gas. It is thus, forgeological reasons, not applicable in all oil fields, and in some regions such asWesternSiberia,theregionwheremostoftheflaringtakesplace,thesedimentaryrock is not suited for reinjection. Reinjectionmay in certain cases also be costly,because the gas needs to be compressed before injected into the reservoir. Thefactthatreinjectedgasin itselfdoesnotproduceanyrevenuesmakesthisoptioneconomicallyunattractivetooilcompanies.Ontheotherhand,ifthereinjectedgascancontributetoenhanceoilrecovery,reinjectionmaybeamorefinanciallyviableoption.TheadvantagesanddisadvantagesofreinjectionarepresentedinTable2-2.

Table2-2Reinjectionofassociatedgas:advantagesanddisadvantages

Option Advantages Disadvantages

Re-injectforfutureuse

Reservoirpreservation Notallformationsaresuitedforreinjectionbecauseofhighcapitalcostforlocalprocessingandcompression

Re-injectforEnhancedOil/GasRecovery(EOR/EGR)

Providesrevenuethroughincreasedoilproduction,mayallowfuturerecoveryofre-injectedgas

NotallformationsaresuitableforgasEORbecauseofhighcapitalcostforlocalprocessingandcompression

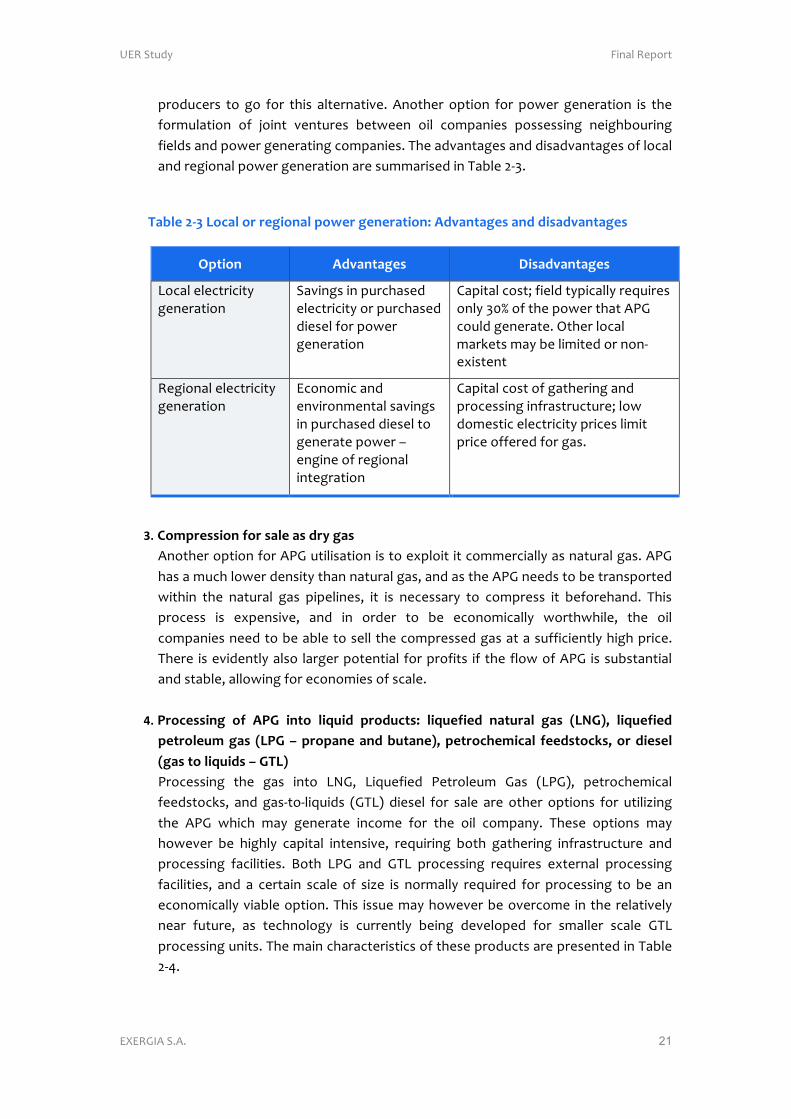

2. Powergeneration,localorregional

Power generation may be either local or regional. Local power generationproduces electricity for use on site, thus saving the oil company expenses inpurchased electricity or diesel for power generation. However, not only thesefacilitiesarecapital intensive,butalsotheenergyneedsofanoil fieldare limitedcompared to the available power produced from APG. If there are no localconsumers (industryor communities) in thevicinity that could takeadvantageofexcess power production, local power generation is thus only a limited solution.Regardlessof localor regionalconsumers,powergenerationalsorequiresaccesstoaregionalpowergridtodisposeofsurpluspower.Regionalpowergenerationgathersgas fromanumberofwells, and thus entails even largerprocessing andinfrastructure investments.The revenues fromgassales toelectricitygenerators,assumingasufficientlyhighpricelevelforelectricity,ishoweveramotivatorforoil

UERStudy FinalReport

EXERGIAS.A. 21

producers to go for this alternative. Another option for power generation is theformulation of joint ventures between oil companies possessing neighbouringfieldsandpowergeneratingcompanies.TheadvantagesanddisadvantagesoflocalandregionalpowergenerationaresummarisedinTable2-3.

Table2-3Localorregionalpowergeneration:Advantagesanddisadvantages

Option Advantages Disadvantages

Localelectricitygeneration

Savingsinpurchasedelectricityorpurchaseddieselforpowergeneration

Capitalcost;fieldtypicallyrequiresonly30%ofthepowerthatAPGcouldgenerate.Otherlocalmarketsmaybelimitedornon-existent

Regionalelectricitygeneration

Economicandenvironmentalsavingsinpurchaseddieseltogeneratepower–engineofregionalintegration

Capitalcostofgatheringandprocessinginfrastructure;lowdomesticelectricitypriceslimitpriceofferedforgas.

3. Compressionforsaleasdrygas

AnotheroptionforAPGutilisationistoexploititcommerciallyasnaturalgas.APGhasamuchlowerdensitythannaturalgas,andastheAPGneedstobetransportedwithin the natural gas pipelines, it is necessary to compress it beforehand. Thisprocess is expensive, and in order to be economically worthwhile, the oilcompaniesneedtobeabletosellthecompressedgasatasufficientlyhighprice.There isevidentlyalso largerpotential forprofits if theflowofAPG issubstantialandstable,allowingforeconomiesofscale.

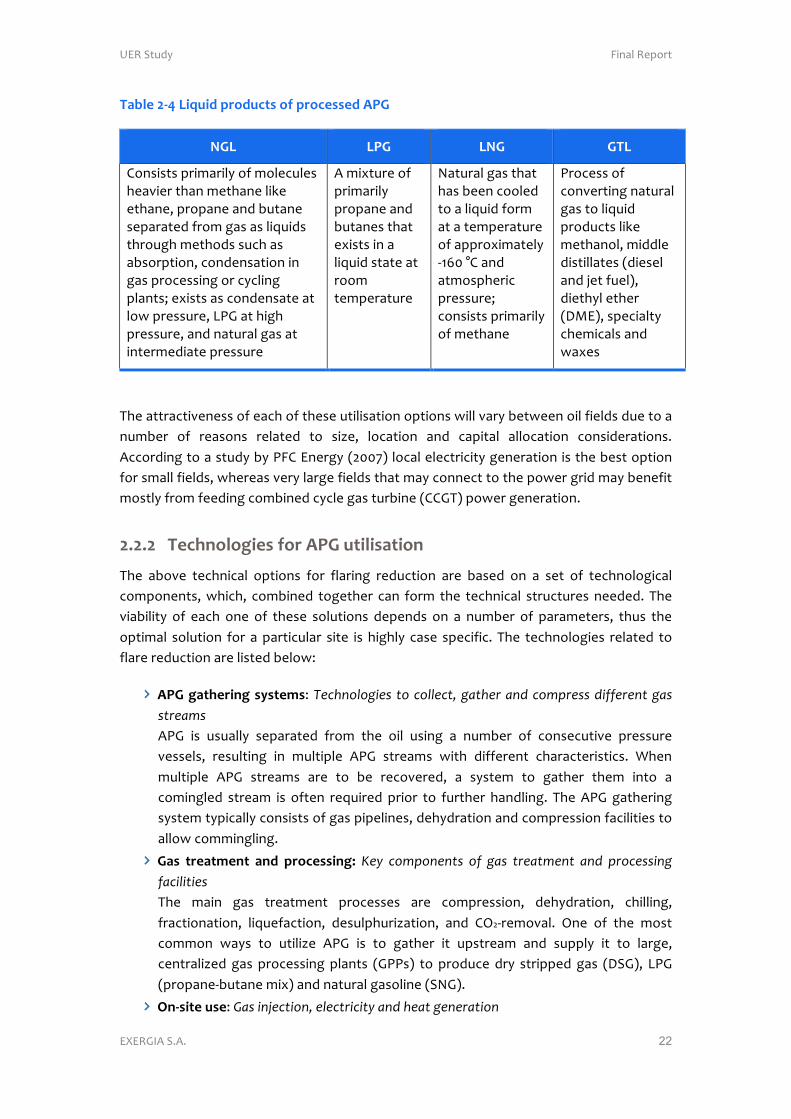

4. Processing of APG into liquid products: liquefied natural gas (LNG), liquefiedpetroleumgas (LPG–propaneandbutane),petrochemical feedstocks,ordiesel(gastoliquids–GTL)Processing the gas into LNG, Liquefied Petroleum Gas (LPG), petrochemicalfeedstocks, and gas-to-liquids (GTL) diesel for sale are other options for utilizingthe APG which may generate income for the oil company. These options mayhowever be highly capital intensive, requiring both gathering infrastructure andprocessing facilities. Both LPG and GTL processing requires external processingfacilities, and a certain scale of size is normally required for processing to be aneconomicallyviableoption.This issuemayhoweverbeovercome in therelativelynear future, as technology is currently being developed for smaller scale GTLprocessingunits.ThemaincharacteristicsoftheseproductsarepresentedinTable2-4.

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 22!

.KLM%'>cC'BNYPNR'XQ"RPS$&'"\'XQ"S%&&%R'(<I'

0IB' B<I' B0I' I.B'

R1,>+>&>!02+?-2+.)!1=!?1./A'./>!I/-;+/2!&I-,!?/&I-,/!.+^/!/&I-,/C!0210-,/!-,(!L'&-,/!>/0-2-&/(!=21?!@->!->!.+Q'+(>!&I21'@I!?/&I1(>!>'AI!->!-L>120&+1,C!A1,(/,>-&+1,!+,!@->!021A/>>+,@!12!A)A.+,@!0.-,&>n!/X+>&>!->!A1,(/,>-&/!-&!.1<!02/>>'2/C!aK4!-&!I+@I!02/>>'2/C!-,(!,-&'2-.!@->!-&!+,&/2?/(+-&/!02/>>'2/!

6!?+X&'2/!1=!02+?-2+.)!0210-,/!-,(!L'&-,/>!&I-&!/X+>&>!+,!-!.+Q'+(!>&-&/!-&!211?!&/?0/2-&'2/!

P-&'2-.!@->!&I-&!I->!L//,!A11./(!&1!-!.+Q'+(!=12?!-&!-!&/?0/2-&'2/!1=!-0021X+?-&/.)!U9NO!tR!-,(!-&?1>0I/2+A!02/>>'2/n!A1,>+>&>!02+?-2+.)!1=!?/&I-,/!

K21A/>>!1=!A1,;/2&+,@!,-&'2-.!@->!&1!.+Q'+(!021('A&>!.+^/!?/&I-,1.C!?+((./!(+>&+..-&/>!V(+/>/.!-,(!Z/&!='/.WC!(+/&I).!/&I/2!VT[#WC!>0/A+-.&)!AI/?+A-.>!-,(!<-X/>!!

HI/!-&&2-A&+;/,/>>!1=!/-AI!1=!&I/>/!'&+.+>-&+1,!10&+1,>!<+..!;-2)!L/&<//,!1+.!=+/.(>!('/!&1!-!,'?L/2! 1=! 2/->1,>! 2/.-&/(! &1! >+c/C! .1A-&+1,! -,(! A-0+&-.! -..1A-&+1,! A1,>+(/2-&+1,>7!6AA12(+,@!&1!-!>&'()!L)!K*R!#,/2@)!V8OOEW!.1A-.!/./A&2+A+&)!@/,/2-&+1,!+>!&I/!L/>&!10&+1,!=12!>?-..!=+/.(>C!<I/2/->!;/2)!.-2@/!=+/.(>!&I-&!?-)!A1,,/A&!&1!&I/!01</2!@2+(!?-)!L/,/=+&!?1>&.)!=21?!=//(+,@!A1?L+,/(!A)A./!@->!&'2L+,/!VRR4HW!01</2!@/,/2-&+1,7!!

>2>2> .%SW#"M"ON%&'\"Q'(<I'P$NMN&K$N"#'HI/! -L1;/! &/AI,+A-.! 10&+1,>! =12! =.-2+,@! 2/('A&+1,! -2/! L->/(! 1,! -! >/&! 1=! &/AI,1.1@+A-.!A1?01,/,&>C!<I+AIC! A1?L+,/(! &1@/&I/2! A-,! =12?! &I/! &/AI,+A-.! >&2'A&'2/>! ,//(/(7! HI/!;+-L+.+&)! 1=! /-AI! 1,/! 1=! &I/>/! >1.'&+1,>! (/0/,(>! 1,! -! ,'?L/2! 1=! 0-2-?/&/2>C! &I'>! &I/!10&+?-.! >1.'&+1,! =12! -! 0-2&+A'.-2! >+&/! +>! I+@I.)! A->/! >0/A+=+A7! HI/! &/AI,1.1@+/>! 2/.-&/(! &1!=.-2/!2/('A&+1,!-2/!.+>&/(!L/.1<`!

(<I'OK$W%QN#O'&T&$%V&`!:&0/,+-+.*&#) $+)0+--&0$4).'$/&%)',5)0+("%&##)5*22&%&,$).'#)#$%&'(#!6K4! +>! '>'-..)! >/0-2-&/(! =21?! &I/! 1+.! '>+,@! -! ,'?L/2! 1=! A1,>/A'&+;/! 02/>>'2/!;/>>/.>C! 2/>'.&+,@! +,! ?'.&+0./! 6K4! >&2/-?>! <+&I! (+==/2/,&! AI-2-A&/2+>&+A>7! fI/,!?'.&+0./! 6K4! >&2/-?>! -2/! &1! L/! 2/A1;/2/(C! -! >)>&/?! &1! @-&I/2! &I/?! +,&1! -!A1?+,@./(! >&2/-?! +>! 1=&/,! 2/Q'+2/(! 02+12! &1! ='2&I/2! I-,(.+,@7! HI/! 6K4! @-&I/2+,@!>)>&/?!&)0+A-..)!A1,>+>&>!1=!@->!0+0/.+,/>C!(/I)(2-&+1,!-,(!A1?02/>>+1,!=-A+.+&+/>!&1!-..1<!A1??+,@.+,@7!

IK&' $Q%K$V%#$' K#R' XQ"S%&&N#Oa' ;&3) 0+("+,&,$#) +2) .'#) $%&'$(&,$) ',5) "%+0&##*,.)2'0*-*$*&#!!HI/! ?-+,! @->! &2/-&?/,&! 021A/>>/>! -2/! A1?02/>>+1,C! (/I)(2-&+1,C! AI+..+,@C!=2-A&+1,-&+1,C! .+Q'/=-A&+1,C! (/>'.0I'2+c-&+1,C! -,(! R:8U2/?1;-.7! :,/! 1=! &I/! ?1>&!A1??1,! <-)>! &1! '&+.+c/! 6K4! +>! &1! @-&I/2! +&! '0>&2/-?! -,(! >'00.)! +&! &1! .-2@/C!A/,&2-.+c/(! @->! 021A/>>+,@! 0.-,&>! V4KK>W! &1! 021('A/! (2)! >&2+00/(! @->! VT%4WC! aK4!V0210-,/UL'&-,/!?+XW!-,(!,-&'2-.!@->1.+,/!V%P4W7!

/#c&N$%'P&%`!<'#)*,=&0$*+,4)&-&0$%*0*$3)',5)/&'$).&,&%'$*+,)!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 23!

HI/! -?1',&! 1=! /XA/>>! @->! 1,U>+&/! A-,! L/! 2/('A/(! L)! 2/U+,Z/A&+1,! -,(! -((+&+1,-.!/./A&2+A+&)!-,(!I/-&!@/,/2-&+1,7!$/U+,Z/A&+1,!?-)!/.+?+,-&/!-..!=.-2+,@!1,U>+&/C!<I+./!&I/! .->&! &<1!@->! 10&+1,>! ,12?-..)!<+..! 1,.)! 1==/2! -! 0-2&+-.! >1.'&+1,!('/! &1! .+?+&/(!(/?-,(!=12!I/-&!-,(!01</2!.1A-..)7!!

!"#Z%Q&N"#'XQ"S%&&%&`!>+,?&%#*+,)+2)6@<)*,$+)&A.A)&-&0$%*0*$3)',5)-*B!*5)2!&-#!!6!,'?L/2!1=!&/AI,1.1@+/>!-2/!-;-+.-L./!&1!A1,;/2&!6K4!=2-A&+1,>!2/>'.&+,@!=21?!@->!&2/-&?/,&! -,(\12! 021A/>>+,@! +,&1! 01&/,&+-..)! ?12/! ;-.'-L./! 021('A&>C! >'AI! ->!/./A&2+A+&)C!I/-&C!0/&21AI/?+A-.>!-,(!.+Q'+(!='/.>C!->!</..!->!;-2+1'>!/,/2@)U+,&/,>+;/!+,('>&2+-.!021('A&>!>'AI!->!=/2&+.+c/2!-,(!>&//.7!

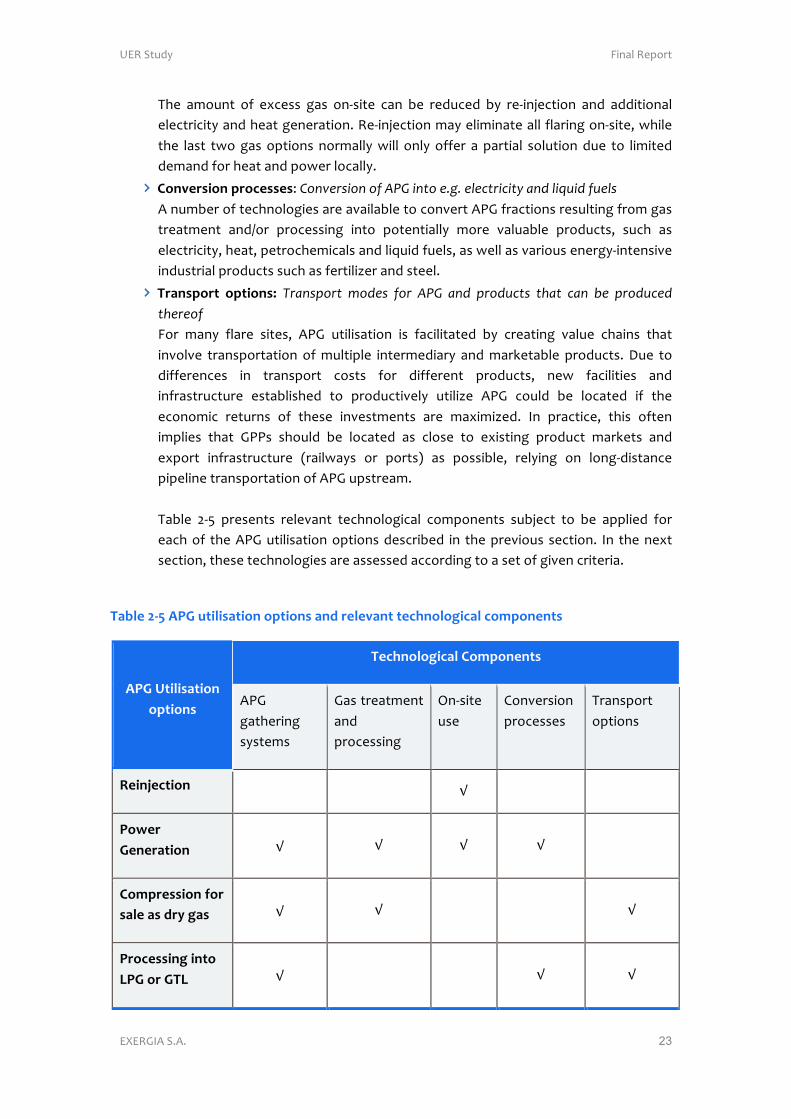

.QK#&X"Q$' "X$N"#&a' :%',#"+%$) (+5&#) 2+%) 6@<) ',5) "%+5!0$#) $/'$) 0',) C&) "%+5!0&5)$/&%&+2!!*12! ?-,)! =.-2/! >+&/>C! 6K4! '&+.+>-&+1,! +>! =-A+.+&-&/(! L)! A2/-&+,@! ;-.'/! AI-+,>! &I-&!+,;1.;/! &2-,>012&-&+1,! 1=!?'.&+0./! +,&/2?/(+-2)! -,(!?-2^/&-L./! 021('A&>7! T'/! &1!(+==/2/,A/>! +,! &2-,>012&! A1>&>! =12! (+==/2/,&! 021('A&>C! ,/<! =-A+.+&+/>! -,(!+,=2->&2'A&'2/! />&-L.+>I/(! &1! 021('A&+;/.)! '&+.+c/! 6K4! A1'.(! L/! .1A-&/(! +=! &I/!/A1,1?+A! 2/&'2,>! 1=! &I/>/! +,;/>&?/,&>! -2/! ?-X+?+c/(7! 5,! 02-A&+A/C! &I+>! 1=&/,!+?0.+/>! &I-&! 4KK>! >I1'.(! L/! .1A-&/(! ->! A.1>/! &1! /X+>&+,@! 021('A&! ?-2^/&>! -,(!/X012&! +,=2->&2'A&'2/! V2-+.<-)>! 12! 012&>W! ->! 01>>+L./C! 2/.)+,@! 1,! .1,@U(+>&-,A/!0+0/.+,/!&2-,>012&-&+1,!1=!6K4!'0>&2/-?7!!H-L./! 8UM! 02/>/,&>! 2/./;-,&! &/AI,1.1@+A-.! A1?01,/,&>! >'LZ/A&! &1! L/! -00.+/(! =12!/-AI!1=! &I/!6K4!'&+.+>-&+1,!10&+1,>!(/>A2+L/(! +,! &I/!02/;+1'>! >/A&+1,7! 5,! &I/!,/X&!>/A&+1,C!&I/>/!&/AI,1.1@+/>!-2/!->>/>>/(!-AA12(+,@!&1!-!>/&!1=!@+;/,!A2+&/2+-7!!!

.KLM%'>cF'(<I'P$NMN&K$N"#'"X$N"#&'K#R'Q%M%ZK#$'$%SW#"M"ONSKM'S"VX"#%#$&'

(<I'5$NMN&K$N"#'"X$N"#&'

.%SW#"M"ONSKM'!"VX"#%#$&'

6K4!@-&I/2+,@!>)>&/?>!

4->!&2/-&?/,&!-,(!021A/>>+,@!

:,U>+&/!'>/!

R1,;/2>+1,!021A/>>/>!

H2-,>012&!10&+1,>!

*%N#`%S$N"#' ! ! u! ! !

<"U%Q'I%#%QK$N"#' u! u! u! u! !

!"VXQ%&&N"#'\"Q'&KM%'K&'RQT'OK&' u! u! ! ! u!

<Q"S%&&N#O'N#$"'B<I'"Q'I.B' u ! ! u! u!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 24!

>2>2A (LK$%V%#$'"X$N"#&'\"Q'V%$WK#%'%VN&&N"#&'

HI/2/! -2/! ,'?/21'>! &/AI,1.1@+A-.! 10&+1,>! =12! 2/('A+,@! ?/&I-,/! ./-^-@/>! +,! 1+.! -,(!,-&'2-.!@->! +,=2->&2'A&'2/7!6L-&/?/,&!10&+1,>! =12!L1&I! >/A&12>! A-,!L/!(+;+(/(! +,&1! &<1!?-+,!A-&/@12+/>`!

+YPNXV%#$' !WK#O%&[5XOQKR%&`! *12! ,-&'2-.! @->C! 2/0.-A+,@! I+@IUL.//(! 0,/'?-&+A!(/;+A/>!s!<I+AI!-2/!(/>+@,/(!&1!2/./->/!@->!('2+,@!&I/!A1'2>/!1=!&I/+2!10/2-&+1,!s!<+&I! .1<UL.//(!0,/'?-&+A! (/;+A/>!<1'.(! 2/('A/! &I/! />A-0/!1=!?/&I-,/! +,&1! &I/!-&?1>0I/2/! L)! -0021X+?-&/.)! Nm! =21?! -! L->/.+,/! >A/,-2+1N7! HI+>! A-,! -.>1! L/!-AI+/;/(!L)!>'L>&+&'&+,@!A1?02/>>/(!-+2!=12!,-&'2-.!@->!<+&I+,!0,/'?-&+A!>)>&/?>C!&I1'@I! -&! -! ?'AI! I+@I/2! A1>&7! 5,! &I/! 1+.! >/A&12C! -L-&/?/,&! A-,! L/! -AI+/;/(! L)!+,>&-..+,@!;-01'2!2/A1;/2)!',+&>!&1!A-0&'2/!,-&'2-.!@->!&I-&! +>!;/,&/(!('2+,@!A2'(/!1+.!>&12-@/C!<I+AI!A-,!&I/,!L/!'>/(!&1!021('A/!/,/2@)7!

!WK#O%&' N#' /X%QK$N"#KM' <QKS$NS%&`! gK'?0U(1<,h! &/AI,+Q'/>C! <I+AI! 2/?1;/!,-&'2-.! @->! =21?! >/A&+1,>! 1=! &I/! 0+0/.+,/! L/=12/! ?-+,&/,-,A/! 12! 2/0-+2C! A1'.(!2/('A/! &I/! -?1',&!1=!?/&I-,/! 2/./->/(! +,! &I/! -&?1>0I/2/!L)! -0021X+?-&/.)! Dm!=21?!-!L->/.+,/!>A/,-2+1E7!6.>1C!&I/2/!-2/!,/<!02-A&+A/>!<I+AI!/,-L./!?-+,&/,-,A/!-,(! 2/0-+2>! &1! L/! ',(/2&-^/,! <+&I1'&! >I'&&+,@! (1<,! -,(! ;/,&+,@! @->! =21?! &I/!0+0/.+,/7! HI/! ?/&I-,/! ;/,&/(! ('2+,@! 1+.! 021('A&+1,! A-,! L/! A-0&'2/(! -,(!>/Q'/>&/2/(!12!'>/(!+,!/,/2@)!'>/>7!!

HI/2/!/X+>&!-.>1!1&I/2!/?+>>+1,!?+&+@-&+1,! &/AI,+Q'/>!<I+AI!-2/!,1&!<+(/.)!'>/(7!fI+./!&I/2/! +>! I+@I! 01&/,&+-.! =12! -L-&/?/,&! 1=! ?/&I-,/! /?+>>+1,>! ?-+,.)! +,! &I/! ,-&'2-.! @->!>/A&12C! &I/)! -2/!,1&! A'22/,&.)! -00.+/(! ->! &I/)! -2/!021I+L+&+;/.)! A1>&.)! -,(\12! &/AI,+A-..)!2/>&2+A&+;/!&1!L/!=/->+L./!-&!-!.-2@/!>A-./7!!

>2>2C (&&%&&V%#$'"\'5+*'.%SW#"M"ON%&'

F-2+1'>! ^/)! (2+;/2>! &I-&! (/&/2?+,/! &I/! +?0./?/,&-&+1,! 1=! -,! ->>1A+-&/(! @->! '&+.+>-&+1,!021Z/A&!A-,!L/!+(/,&+=+/(7!HI/>/!-2/!L2+/=.)!02/>/,&/(!L/.1<`!

!KXN$KM' S"&$' e!(<+4f2! 600-2/,&.)C! +>! &I/! ?1>&! A2+&+A-.! =-A&12! (/&/2?+,+,@! &I/!=/->+L+.+&)!-,(!;+-L+.+&)!1=!-!021Z/A&7!R6K#3! +>! 2/.-&/(!&1!-!>/2+/>!1=!021Z/A&! 2/.-&/(!AI-2-A&/2+>&+A>! (/0/,(+,@! 1,! &I/! 021Z/A&! &)0/! -,(!?12/! +?012&-,&.)! &I/! ,/&L-A^!;-.'/!1=!&I/!/,(!021('A&7!

IK&' S"VX"&N$N"#' K#R' SWKQKS$%QN&$NS&2! o/)! ->0/A&>!1=! &I/!@->! A1?01>+&+1,! +,A.'(/!&I/! 6K4! 02/>>'2/! -,(! ;1.'?/! ->! </..! ->! &I/! RBv! A1,&/,&7! HI/! A1,&-?+,-,&>!A1,&/,&! +>! -.>1! >+@,+=+A-,&n! &I/! I+@I! R:8! -,(! b8%! A1,&/,&! ./-(! &1! +,A2/->/(! A1>&!&I21'@I! -((+&+1,-.! 021A/>>+,@C! +?0-A&! 1,!?-&/2+-.! >/./A&+1,C!<->&/! (+>01>-.! VR:8!-,(! >'.0I'2W7! HI/2/=12/C! +&! +>! />>/,&+-.! &1! L/! -L./! &1! ^,1<! 12! />&+?-&/! &I/! @->!A1?01>+&+1,!1;/2!&I/!=+/.(!.+=/7!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!! !N![/&I-,/!/?+>>+1,>!?+&+@-&+1,!10&+1,>!+,!&I/[email protected].!1+.!-,(!,-&'2-.!@->!+,('>&2+/>C!$1L+,>1,!/&7-.C!5R*!R1,>'.&+,@!E!K'?0(1<,!&/AI,+Q'/>!-2/!'>/(!&1!2/?1;/!@->!=21?!>/A&+1,>!1=!&I/!0+0/.+,/!12!-!A.1>/(!AI-?L/2!<+&I!-!;-A''?!0'?07!#K6!V8OONW!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 25!

<Q"RPS$N"#' XQ"\NM%2' :+.! 021('A&+1,! +>! 1=&/,! AI-2-A&/2+>/(! L)! w0/-^)j! 021('A&+1,!021=+./>!-,(!021('A&+1,!?-)!L/!>'LZ/A&!&1!=2/Q'/,&!>&-2&U>&10!/;/,&>C!0-2&+A'.-2.)!+,!10/2-&+1,>! +,! 2/?1&/! -2/->7! %+?+.-2.)C! ->>1A+-&/(! @->! ;1.'?/>! &)0+A-..)! ;-2)! 1;/2!&I/!=+/.(!.+=/7!:,!1,/!I-,(C!-!A.'>&/2+,@!-,(!A/,&2-.!021A/>>+,@!>&2-&/@)!?-)!L/!-,!/A1,1?+A-..)! -&&2-A&+;/! 10&+1,! &I-&! -.>1!?-)! >?11&I! >I12&\.1,@! &/2?!021('A&+1,!;-2+-&+1,>7!:,!&I/!1&I/2!I-,(C!>?-../2!>A-./!=-A+.+&+/>!-2/!!1=&/,!/->+/2!&1!=',(C!A-,!L/!/X/A'&/(!=->&/2C!-,(!-2/!./>>!&/AI,+A-..)!A1?0./X!-,(!=+,-,A+-..)!2+>^)7!!!

*%Z%#P%'['<Q"RPS$'PXMN\$7!RP4!-,(!aP4!A1?0/&/!02+?-2+.)!<+&I!=1>>+.!='/.>!V/7@7!1+.C!A1-.W!=12!01</2!@/,/2-&+1,!-,(!(1?/>&+A!I/-&+,@C!<I+./!A1?0./X!021('A&>!.+^/!4Ha!)+/.(!02/?+'?!02+A/>!L)!A1?0/&+,@!(+2/A&.)!+,!&I/!&2-,>012&!>/A&127!

6K$PQN$T'"\'$%SW#"M"OT2!HI/!?-&'2+&)!1=!&/AI,1.1@+/>!&1!L/! +?0./?/,&/(! +>!-!^/)!=-A&12!2/.-&/(!02+?-2+.)!&1!A1>&C!L'&!-.>1!&1!2/.+-L+.+&)!->0/A&>7!!

.QK#&X"Q$K$N"#'$"'VKQ_%$7!K2/=/2/,A/!+>!=12!-!021('A&!<+&I!I+@IU/,/2@)!(/,>+&)!+7/7!-!.+Q'+(!V/7@7!4HaC!aP4!12!AI/?+A-.>W7!!

!KQL"#' K#R' %#%QOT' %\\NSN%#ST! >I1'.(! L/! A1,>+(/2/(! 1,! -! fHf! L->+>! <I/2/!021('A&>!?-)!(+>0.-A/!I+@I/2!A-2L1,!+,&/,>+;/!='/.>7!!

!"VVP#N$T' N#$%QR%X%#R%#ST! ?-)! 021;+(/! -,! 10012&',+&)! =12! +,&/2(/0/,(/,A)!-,(\12!>),/2@+/>!<+&I!.1A-.!A1??',+&+/>!<I+AI!?-)!I-;/!>+@,+=+A-,&!01>+&+;/!/==/A&>!L)!L1&I!?+,+?+c+,@!&I/!2+>^!=21?!&I/!1+.!(/;/.10?/,&!=21?!,1,U&/AI,+A-.! 2+>^!-,(!?-)!L'+.(!-!.1A-.!?-2^/&C!2/('A+,@!&2-,>012&-&+1,!A1>&>7!

!

.KLM%'>c3'DPKMN$K$NZ%'K&&%&&V%#$'"\'5+*'"X$N"#&'KOKN#&$'K'&%QN%&'"\'_%T'VKQ_%$'RQNZ%Q&'e1"PQS%a'II@*f''

! IK&'Q%N#`%S$N"#'

!0I' 6N#N'B0I' 1VKMM'&SKM%'I.B'

<"U%Q'O%#%QK$N"#'

!KXN$KM'!"&$&' ! ! ! ! !

IK&'S"VX"&N$N"#' ! ! ! ! !

<Q"RPS$N"#'XQ"\NM%'' ! ! ! ! !

*%Z%#P%['<Q"RPS$'PXMN\$'' ! ! ! ! !

.%SW#"M"OT'VK$PQN$T'' ! ! ! ! !

.QK#&X"Q$'$"'VKQ_%$''

P1&!-00.+A-L./! ! ! ! !

+#%QOT'h'SKQL"#'%\\NSN%#ST'

/X%QK$N"#KM'&K\%$T'' ! ! ! ! !

!"VVP#N$T'N#$%QcR%X%#R%#ST' ! ! ! ! !

UERStudy FinalReport

EXERGIAS.A. 26

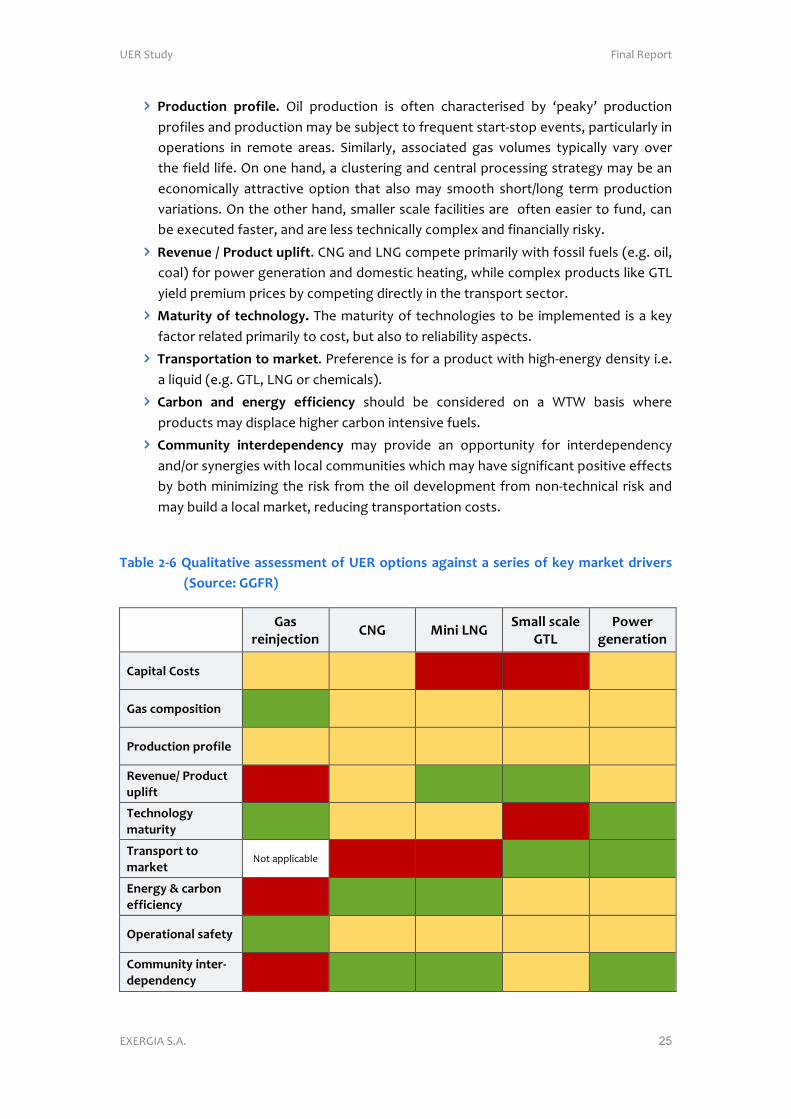

A high level qualitative assessment of available UER categories against theaforementioned aspects is illustrated in Table 2-6, where green colour stands forhigh/positive prospects, yellow stands for medium prospects and red stands forlow/negativeprospects.

2.2.5 UERtechnologiesbasedonrenewablesources

Besidesventing,flaringandfugitiveemissionsmitigation,upstreamemissionreductionsmayalsobeachievedbytheuseofrenewableenergysourcesintheextractionoffossilfuels.

SolarEOR,forinstance, isamethodforenhancedoilrecovery,whichis likelytoplayanimportantroleinthemixofEORtechnologies.Insteadofburningnaturalgastoproducesteam, solar EOR involves the use of Concentrating Solar Power (CSP) technology toproducesteam.Mirrorsareusedtoreflectandconcentratesunlightontoreceiversthatcollectsolarenergyandthenconvertittoheat.Theheatisthenusedtoproducesteamfromwater.TheuseofsolarEORcouldreducedemandfornaturalgasrequiredforEOR,which canbe redirected toothereconomicactivities, suchaspowergeneration,waterdesalination and as feedstock and energy for industrial processes. The technology ofsolar EOR can also be installed in oil fields with limited availability of associated gastherebyprovidingawaytocreateandinjectsteamforEORwithnocapitalinvestmentingasinfrastructure.ExamplesofprojectsutilizingthetechnologicaloptionofSolarSteamGeneration Enhanced Oil Recovery include the oilfields of McKittrick and Coalinga inCaliforniaaswellasthePetroleumDevelopmentinOman.

Otherrenewableenergyapplicationsforthefossilfuelupstreamsectorincludetheuseofphotovoltaicandwindturbinesforpowergeneration.Thesetechnologiescanbeusedforenergy intensive operations in oil and gas fields, such as powering compressors andpumpsfortransportingoilandgasthroughgatheringpipelinestoprocessingplants,ortogeneratetheelectricityandheatneededforon-siteoperationsandlivingquarters.Theseactivities,however,donotrepresentanimportantshareofthetotalupstreamemissionsoffossilfuels,thereforetheydonotofferextensiveemissionsreductions.

2.3 UpstreamEmissionReductionIncentives

Fossil fuel companies have various incentives and/or obligations for implementingUERmeasuresirrespectiveofFQDthatarerelatedtolegalrequirements,owninitiativesfromimprovingthetechnicalandfinancialefficiencyoftheiroperations.Thissectionprovidesan overview of the regulatory requirements, incentives of fossil fuels companies andexisting APG utilisation projects in target countries. The analysis will focus on thecountrieswhichrepresentthemostimportantsuppliersoffossilfuelstotheEU,withanemphasistotheonesthathavesignificantemissionsintheirupstreamactivities,aswellas those that have implemented successfully upstreamemission reductionpolicies andinitiatives.

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 27!

5,!12(/2! &1!(/=+,/!&I/!&-2@/&!A1',&2+/>! &1!L/!-,-.)>/(C!-!L2+/=!1;/2;+/<!1=! &I/!A2'(/!1+.!>'00.)! &1! &I/! #"C! ->! </..! ->! 1=! &I/! ?-+,! /?+&&+,@! 1+.! 021('A+,@! 2/@+1,>! -2/! 021;+(/(!='2&I/2!1,7!!

Y->/(!1,!&I/>/!(-&-C!+&!+>!2/->1,-L./!&I-&!&I/!1;/2;+/<!1=!"#$!021Z/A&>!<+..!L/!.+?+&/(!&1!&I/!=1..1<+,@!=1>>+.!='/.!021('A+,@!A1',&2+/>`!

$'>>+-! P+@/2+-! P12<-)!

[+((./!#->&!V52-QC!52-,GW

R-,-(-J!

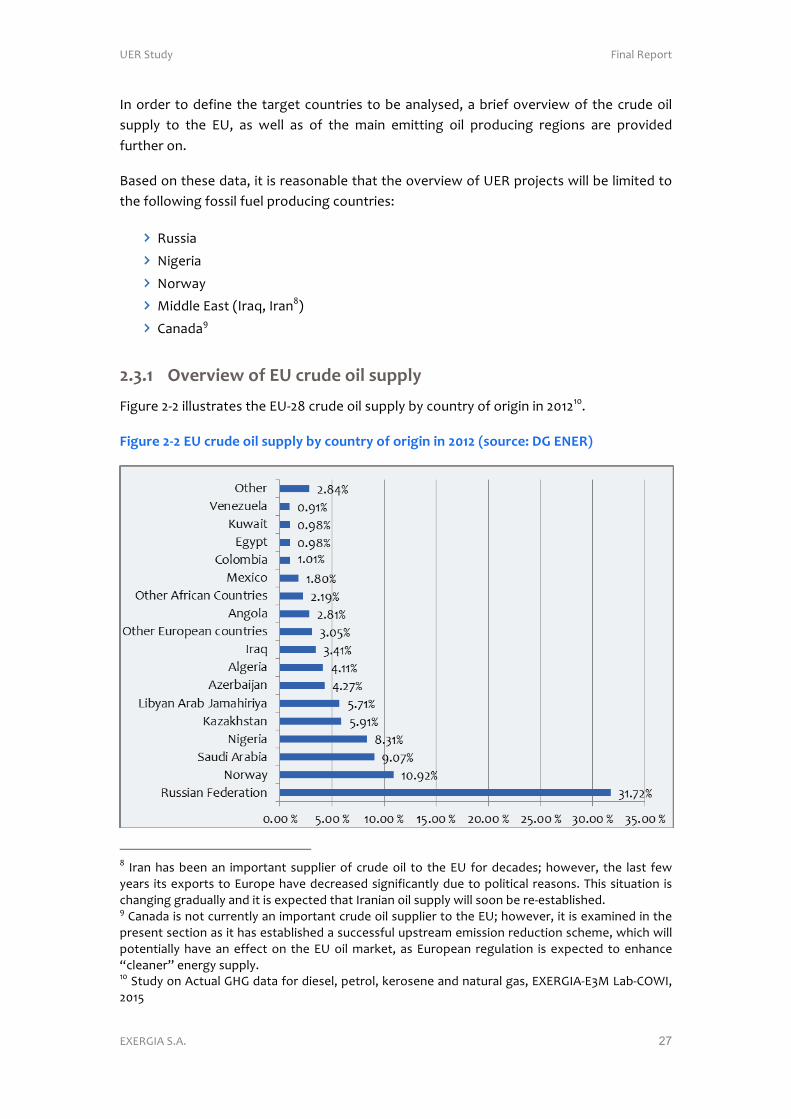

>2A29 /Z%QZN%U'"\'+5'SQPR%'"NM'&PXXMT'

*+@'2/!8U8!+..'>&2-&/>!&I/!#"U8G!A2'(/!1+.!>'00.)!L)!A1',&2)!1=!12+@+,!+,!8O989O7!!

@NOPQ%'>c>'+5'SQPR%'"NM'&PXXMT'LT'S"P#$QT'"\'"QNON#'N#'>E9>'e&"PQS%a':I'+0+*f'

!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!! !G! 52-,!I->!L//,!-,! +?012&-,&! >'00.+/2!1=! A2'(/!1+.! &1! &I/!#"! =12!(/A-(/>n!I1</;/2C! &I/! .->&! =/<!)/-2>! +&>!/X012&>!&1!#'210/!I-;/!(/A2/->/(!>+@,+=+A-,&.)!('/!&1!01.+&+A-.!2/->1,>7!HI+>!>+&'-&+1,! +>!AI-,@+,@!@2-('-..)!-,(!+&!+>!/X0/A&/(!&I-&!52-,+-,!1+.!>'00.)!<+..!>11,!L/!2/U/>&-L.+>I/(7!!J!R-,-(-!+>!,1&!A'22/,&.)!-,!+?012&-,&!A2'(/!1+.!>'00.+/2!&1!&I/!#"n!I1</;/2C!+&!+>!/X-?+,/(!+,!&I/!02/>/,&!>/A&+1,!->!+&!I->!/>&-L.+>I/(!-!>'AA/>>='.!'0>&2/-?!/?+>>+1,!2/('A&+1,!>AI/?/C!<I+AI!<+..!01&/,&+-..)!I-;/!-,!/==/A&!1,! &I/!#"!1+.!?-2^/&C! ->!#'210/-,! 2/@'.-&+1,! +>! /X0/A&/(! &1!/,I-,A/!gA./-,/2h!/,/2@)!>'00.)7!9O!%&'()!1,!6A&'-.!4b4!(-&-!=12!(+/>/.C!0/&21.C!^/21>/,/!-,(!,-&'2-.!@->C!#3#$456U#B[!a-LUR:f5C!8O9M!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 28!

R'22/,&.)C! $'>>+-! +>! L)! =-2! &I/! .-2@/>&! >'00.+/2! 1=! 1+.! &1! #'210/C! /X012&+,@! A2'(/! 1+.! &1!#'210/! =21?! &I/! -2/->! 1=!"2-.>UF1.@-C!f/>&/2,! %+L/2+-! -,(! H+?-,UK/AI12-7! HI/! >/A1,(!.-2@/>&!>'00.+/2!1=!A2'(/!1+.!&1!#'210/!+>!P12<-)!<+&I!-0021X+?-&/.)!99m!1=!&1&-.!+?012&>7!#'210/! +>! -.>1! >'00.+/(!<+&I! >+@,+=+A-,&!Q'-,&+&+/>!1=!62-L+-,! .+@I&!-,(!I/-;)!A2'(/>C! ->!</..! ->! .+@I&! -,(! ?/(+'?! A2'(/! 1+.>! =21?! P+@/2+-7! 60-2&! =21?! &I/! $'>>+-,! A2'(/! 1+.C!#'210/! +>!>'00.+/(!<+&I! .-2@/!Q'-,&+&+/>!1=!A2'(/!1+.! =21?!1&I/2!*%"!A1',&2+/>C!02+?-2+.)!6c/2L-+Z-,!V6c/2+!.+@I&!-,(!6c/2+!YHRW!-,(!o-c-^I>&-,!VH/,@+c!-,(!RKR!L./,(W7!

>2A2> I%"OQKXWT'"\'PX&$Q%KV'%VN&&N"#&'

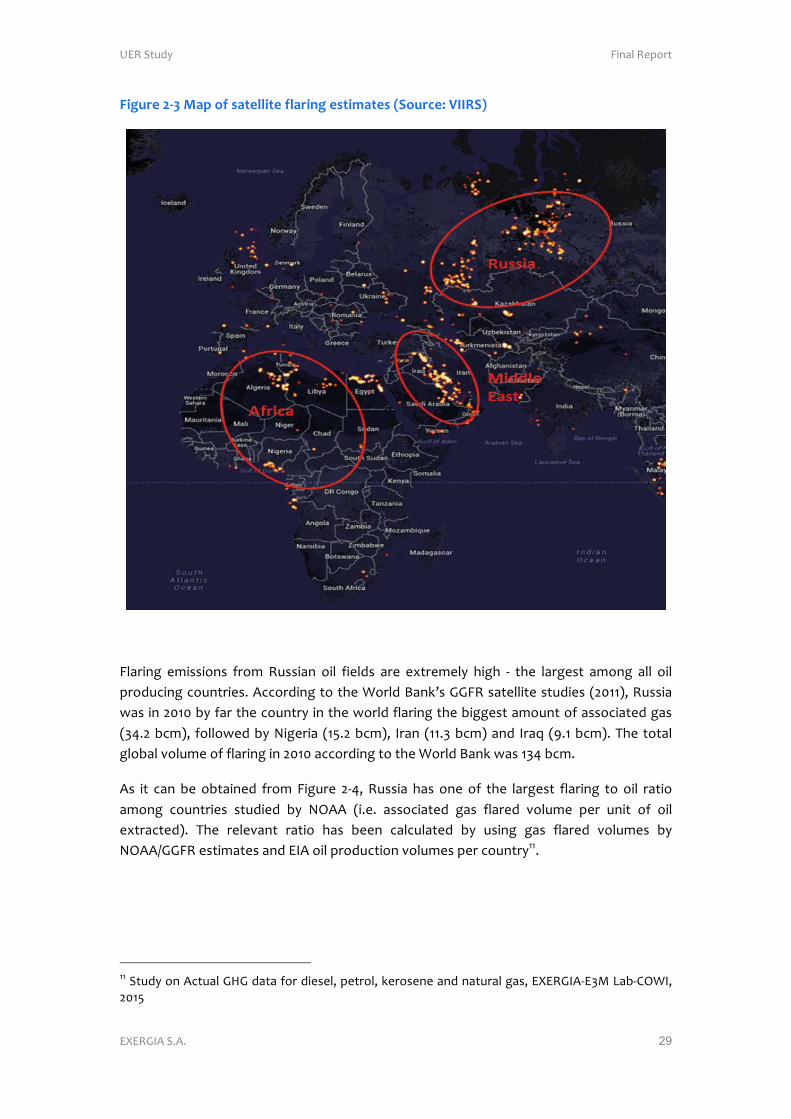

6! >?-..! ,'?L/2! 1=! A1',&2+/>! -2/! (1?+,-,&! A1,&2+L'&12>! &1! @.1L-.! =.-2+,@! /?+>>+1,>7! 5,!8OOJC! $'>>+-! -,(! P+@/2+-! -AA1',&/(! =12! -,! />&+?-&/(! D8! m! 1=! @.1L-.! =.-2+,@7! H</,&)!A1',&2+/>!-AA1',&/(! =12!-,!/>&+?-&/(!GM!m!1=! &I/!1L>/2;/(! =.-2+,@7!['AI!1=! &I/!1==+A+-.!+,=12?-&+1,! 1,! &I/! -?1',&! 1=! @->! =.-2+,@! A1?/>! =21?! /,;+21,?/,&-.! ?+,+>&2+/>! 12!>&-&+>&+A-.! -@/,A+/>! <+&I+,! ;-2+1'>! @1;/2,?/,&>7! b1</;/2C! ('2+,@! &I/! .->&! (/A-(/C!+,A2/->/(!'>/!1=!?+.+&-2)!>-&/..+&/>!-,(!>10I+>&+A-&/(!A1?0'&/2!021@2-?>!I->!L//,!'>/(!&1!?/->'2/!@->! =.-2+,@7!HI/>/!/==12&>! >//^! &1!A122/.-&/! .+@I&!1L>/2;-&+1,>!<+&I! +,&/,>+&)!?/->'2/>!-,(!=.-2/!;1.'?/>!&1!021('A/!A2/(+L./!/>&+?-&/>[email protected].!@->!=.-2+,@!./;/.>7!

HI/!P-&+1,-.!:A/-,+A!-,(!6&?1>0I/2+A!6(?+,+>&2-&+1,!VP:66W! +,!A1..-L12-&+1,!<+&I!&I/!f12.(! Y-,^j>! 4.1L-.! 4->! *.-2+,@! $/('A&+1,! V44*$W! K-2&,/2>I+0! I->! A1,('A&/(! -,!/X&/,>+;/!<12^!1,!&I/!/.-L12-&+1,!1=!-A&'-.!(-&-!=12!=.-2+,@!L1&I!1,!-!A1',&2)!-,(!=+/.(!./;/.C!'>+,@!021A/>>/(!>-&/..+&/!(-&-7!HI/!@/1@2-0I+A!(+>0/2>+1,!1=!=.-2+,@!@->!+>!(/0+A&/(!+,! *+@'2/! 8UBC! <I/2/! +&! +>! /;+(/,&! &I-&!?1>&! 1=! =.-2+,@! -A&+;+&+/>! &-^/! 0.-A/! +,! &I2//! ^/)!-2/->`!

$'>>+-!-,(!*12?/2!%1;+/&!",+1,!A1',&2+/>!

6=2+A-!V?-+,.)!P+@/2+-C!6.@/2+-!-,(!6,@1.-W!

[+((./!#->&!V?-+,.)!52-,C!52-Q!-,(!&I/!K/2>+-,!4'.=W!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 29!

@NOPQ%'>cA'6KX'"\'&K$%MMN$%'\MKQN#O'%&$NVK$%&'e1"PQS%a',--*1f'

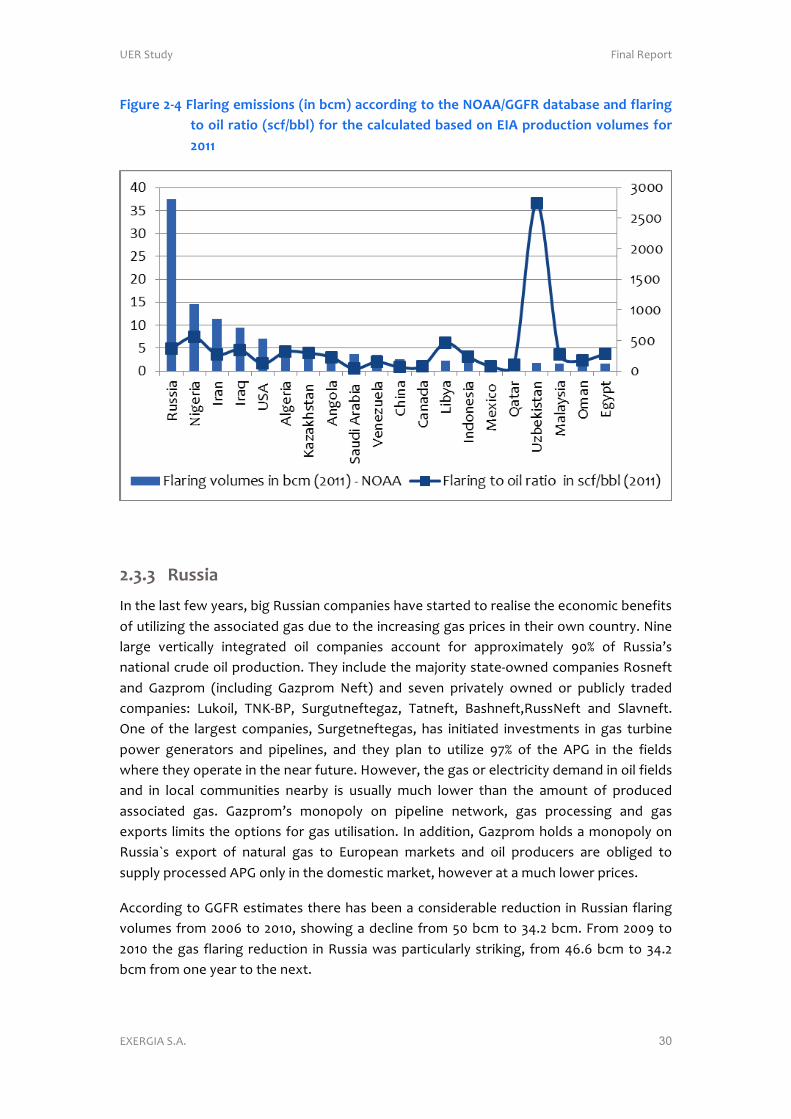

!

*.-2+,@! /?+>>+1,>! =21?! $'>>+-,! 1+.! =+/.(>! -2/! /X&2/?/.)! I+@I! U! &I/! .-2@/>&! -?1,@! -..! 1+.!021('A+,@!A1',&2+/>7!6AA12(+,@!&1!&I/!f12.(!Y-,^j>!44*$!>-&/..+&/!>&'(+/>!V8O99WC!$'>>+-!<->!+,!8O9O!L)!=-2!&I/!A1',&2)!+,!&I/!<12.(!=.-2+,@!&I/!L+@@/>&!-?1',&!1=!->>1A+-&/(!@->!VBD78!LA?WC! =1..1</(!L)!P+@/2+-! V9M78!LA?WC! 52-,! V997B!LA?W!-,(! 52-Q! VJ79!LA?W7!HI/!&1&[email protected].!;1.'?/!1=!=.-2+,@!+,!8O9O!-AA12(+,@!&1!&I/!f12.(!Y-,^!<->!9BD!LA?7!!

6>! +&! A-,! L/! 1L&-+,/(! =21?! *+@'2/! 8UDC! $'>>+-! I->! 1,/! 1=! &I/! .-2@/>&! =.-2+,@! &1! 1+.! 2-&+1!-?1,@! A1',&2+/>! >&'(+/(! L)! P:66! V+7/7! ->>1A+-&/(! @->! =.-2/(! ;1.'?/! 0/2! ',+&! 1=! 1+.!/X&2-A&/(W7! HI/! 2/./;-,&! 2-&+1! I->! L//,! A-.A'.-&/(! L)! '>+,@! @->! =.-2/(! ;1.'?/>! L)!P:66\44*$!/>&+?-&/>!-,(!#56!1+.!021('A&+1,!;1.'?/>!0/2!A1',&2)997!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!! !99!%&'()!1,!6A&'-.!4b4!(-&-!=12!(+/>/.C!0/&21.C!^/21>/,/!-,(!,-&'2-.!@->C!#3#$456U#B[!a-LUR:f5C!8O9M!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 30!

@NOPQ%'>cC'@MKQN#O'%VN&&N"#&'eN#'LSVf'KSS"QRN#O'$"'$W%'0/(([II@*'RK$KLK&%'K#R'\MKQN#O'$"'"NM'QK$N"'e&S\[LLMf'\"Q'$W%'SKMSPMK$%R'LK&%R'"#'+-('XQ"RPS$N"#'Z"MPV%&'\"Q'>E99'

!

!

>2A2A *P&&NK'5,!&I/!.->&!=/<!)/-2>C!L+@!$'>>+-,!A1?0-,+/>!I-;/!>&-2&/(!&1!2/-.+>/!&I/!/A1,1?+A!L/,/=+&>!1=!'&+.+c+,@!&I/!->>1A+-&/(!@->!('/!&1!&I/!+,A2/->+,@!@->!02+A/>!+,!&I/+2!1<,!A1',&2)7!P+,/!.-2@/! ;/2&+A-..)! +,&/@2-&/(! 1+.! A1?0-,+/>! -AA1',&! =12! -0021X+?-&/.)! JOm! 1=! $'>>+-j>!,-&+1,-.!A2'(/!1+.!021('A&+1,7!HI/)!+,A.'(/!&I/!?-Z12+&)!>&-&/U1<,/(!A1?0-,+/>!$1>,/=&!-,(! 4-c021?! V+,A.'(+,@! 4-c021?! P/=&W! -,(! >/;/,! 02+;-&/.)! 1<,/(! 12! 0'L.+A.)! &2-(/(!A1?0-,+/>`! a'^1+.C! HPoUYKC! %'2@'&,/=&/@-cC! H-&,/=&C! Y->I,/=&C$'>>P/=&! -,(! %.-;,/=&7!:,/!1=! &I/! .-2@/>&! A1?0-,+/>C! %'2@/&,/=&/@->C! I->! +,+&+-&/(! +,;/>&?/,&>! +,! @->! &'2L+,/!01</2! @/,/2-&12>! -,(! 0+0/.+,/>C! -,(! &I/)! 0.-,! &1! '&+.+c/! JEm! 1=! &I/! 6K4! +,! &I/! =+/.(>!<I/2/!&I/)!10/2-&/!+,!&I/!,/-2!='&'2/7!b1</;/2C!&I/!@->!12!/./A&2+A+&)!(/?-,(!+,!1+.!=+/.(>!-,(! +,! .1A-.! A1??',+&+/>! ,/-2L)! +>! '>'-..)! ?'AI! .1</2! &I-,! &I/! -?1',&! 1=! 021('A/(!->>1A+-&/(! @->7! 4-c021?j>! ?1,101.)! 1,! 0+0/.+,/! ,/&<12^C! @->! 021A/>>+,@! -,(! @->!/X012&>! .+?+&>!&I/!10&+1,>!=12!@->!'&+.+>-&+1,7! 5,!-((+&+1,C!4-c021?!I1.(>!-!?1,101.)!1,!$'>>+-x>! /X012&! 1=! ,-&'2-.! @->! &1! #'210/-,! ?-2^/&>! -,(! 1+.! 021('A/2>! -2/! 1L.+@/(! &1!>'00.)!021A/>>/(!6K4!1,.)!+,!&I/!(1?/>&+A!?-2^/&C!I1</;/2!-&!-!?'AI!.1</2!02+A/>7!

6AA12(+,@!&1!44*$!/>&+?-&/>!&I/2/!I->!L//,!-!A1,>+(/2-L./!2/('A&+1,! +,!$'>>+-,!=.-2+,@!;1.'?/>!=21?!8OON!&1!8O9OC!>I1<+,@!-!(/A.+,/!=21?!MO!LA?!&1!BD78!LA?7!*21?!8OOJ!&1!8O9O! &I/!@->! =.-2+,@! 2/('A&+1,! +,!$'>>+-!<->!0-2&+A'.-2.)! >&2+^+,@C! =21?!DN7N!LA?!&1!BD78!LA?!=21?!1,/!)/-2!&1!&I/!,/X&7!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 31!

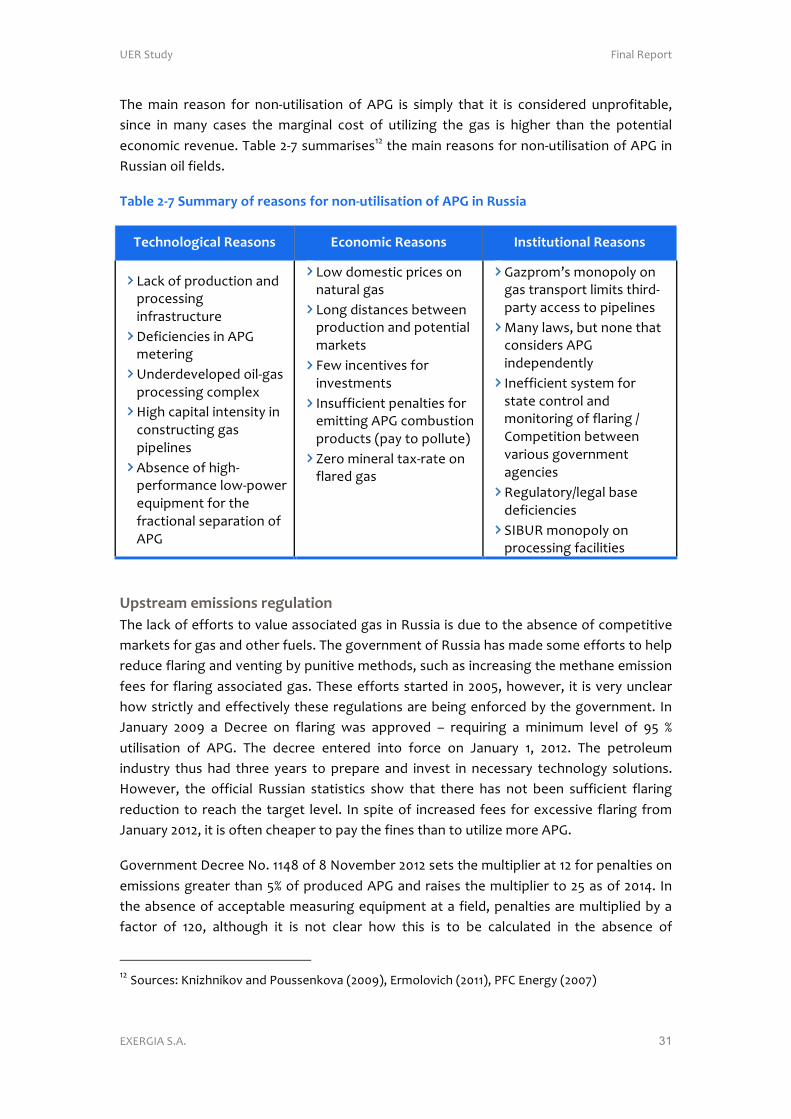

HI/!?-+,! 2/->1,! =12! ,1,U'&+.+>-&+1,! 1=! 6K4! +>! >+?0.)! &I-&! +&! +>! A1,>+(/2/(! ',021=+&-L./C!>+,A/! +,! ?-,)! A->/>! &I/!?-2@+,-.! A1>&! 1=! '&+.+c+,@! &I/! @->! +>! I+@I/2! &I-,! &I/! 01&/,&+-.!/A1,1?+A!2/;/,'/7!H-L./!8UE!>'??-2+>/>98!&I/!?-+,!2/->1,>!=12!,1,U'&+.+>-&+1,!1=!6K4!+,!$'>>+-,!1+.!=+/.(>7!!

.KLM%'>cG'1PVVKQT'"\'Q%K&"#&'\"Q'#"#cP$NMN&K$N"#'"\'(<I'N#'*P&&NK'

.%SW#"M"ONSKM'*%K&"#& +S"#"VNS'*%K&"#& -#&$N$P$N"#KM'*%K&"#&

a-A^!1=!021('A&+1,!-,(!021A/>>+,@!+,=2->&2'A&'2/! T/=+A+/,A+/>!+,!6K4!?/&/2+,@! ",(/2(/;/.10/(!1+.U@->!021A/>>+,@!A1?0./X! b+@I!A-0+&-.!+,&/,>+&)!+,!A1,>&2'A&+,@!@->!0+0/.+,/>! 6L>/,A/!1=!I+@IU0/2=12?-,A/!.1<U01</2!/Q'+0?/,&!=12!&I/!=2-A&+1,-.!>/0-2-&+1,!1=!6K4!

a1<!(1?/>&+A!02+A/>!1,!,-&'2-.!@->! a1,@!(+>&-,A/>!L/&<//,!021('A&+1,!-,(!01&/,&+-.!?-2^/&>! */<!+,A/,&+;/>!=12!+,;/>&?/,&>! 5,>'==+A+/,&!0/,-.&+/>!=12!/?+&&+,@!6K4!A1?L'>&+1,!021('A&>!V0-)!&1!01..'&/W! y/21!?+,/2-.!&-XU2-&/!1,!=.-2/(!@->!

4-c021?j>!?1,101.)!1,!@->!&2-,>012&!.+?+&>!&I+2(U0-2&)!-AA/>>!&1!0+0/.+,/>! [-,)!.-<>C!L'&!,1,/!&I-&!A1,>+(/2>!6K4!+,(/0/,(/,&.)! 5,/==+A+/,&!>)>&/?!=12!>&-&/!A1,&21.!-,(!?1,+&12+,@!1=!=.-2+,@!\!R1?0/&+&+1,!L/&<//,!;-2+1'>!@1;/2,?/,&!!-@/,A+/>! $/@'.-&12)\./@-.!L->/!(/=+A+/,A+/>! %5Y"$!?1,101.)!1,!021A/>>+,@!=-A+.+&+/>!

5X&$Q%KV'%VN&&N"#&'Q%OPMK$N"#'HI/!.-A^!1=!/==12&>!&1!;-.'/!->>1A+-&/(!@->!+,!$'>>+-!+>!('/!&1!&I/!-L>/,A/!1=!A1?0/&+&+;/!?-2^/&>!=12!@->!-,(!1&I/2!='/.>7!HI/!@1;/2,?/,&!1=!$'>>+-!I->!?-(/!>1?/!/==12&>!&1!I/.0!2/('A/!=.-2+,@!-,(!;/,&+,@!L)!0',+&+;/!?/&I1(>C!>'AI!->!+,A2/->+,@!&I/!?/&I-,/!/?+>>+1,!=//>!=12!=.-2+,@!->>1A+-&/(!@->7!HI/>/!/==12&>!>&-2&/(! +,!8OOMC!I1</;/2C! +&! +>!;/2)!',A./-2!I1<!>&2+A&.)!-,(!/==/A&+;/.)!&I/>/!2/@'.-&+1,>!-2/!L/+,@!/,=12A/(!L)!&I/!@1;/2,?/,&7! 5,!]-,'-2)! 8OOJ! -! T/A2//! 1,! =.-2+,@! <->! -0021;/(! s! 2/Q'+2+,@! -! ?+,+?'?! ./;/.! 1=! JM! m!'&+.+>-&+1,! 1=! 6K47! HI/! (/A2//! /,&/2/(! +,&1! =12A/! 1,! ]-,'-2)! 9C! 8O987! HI/! 0/&21./'?!+,('>&2)! &I'>! I-(! &I2//! )/-2>! &1! 02/0-2/! -,(! +,;/>&! +,! ,/A/>>-2)! &/AI,1.1@)! >1.'&+1,>7!b1</;/2C! &I/! 1==+A+-.! $'>>+-,! >&-&+>&+A>! >I1<! &I-&! &I/2/! I->! ,1&! L//,! >'==+A+/,&! =.-2+,@!2/('A&+1,! &1! 2/-AI! &I/! &-2@/&! ./;/.7! 5,! >0+&/!1=! +,A2/->/(! =//>! =12!/XA/>>+;/! =.-2+,@! =21?!]-,'-2)!8O98C!+&!+>!1=&/,!AI/-0/2!&1!0-)!&I/!=+,/>!&I-,!&1!'&+.+c/!?12/!6K47!

41;/2,?/,&!T/A2//!P17!99DG!1=!G!P1;/?L/2!8O98!>/&>!&I/!?'.&+0.+/2!-&!98!=12!0/,-.&+/>!1,!/?+>>+1,>!@2/-&/2!&I-,!Mm!1=!021('A/(!6K4!-,(!2-+>/>!&I/!?'.&+0.+/2!&1!8M!->!1=!8O9D7!5,!&I/!-L>/,A/!1=!-AA/0&-L./!?/->'2+,@!/Q'+0?/,&!-&!-!=+/.(C!0/,-.&+/>!-2/!?'.&+0.+/(!L)!-!=-A&12! 1=! 98OC! -.&I1'@I! +&! +>! ,1&! A./-2! I1<! &I+>! +>! &1! L/! A-.A'.-&/(! +,! &I/! -L>/,A/! 1=!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!! !98!%1'2A/>`!o,+cI,+^1;!-,(!K1'>>/,^1;-!V8OOJWC!#2?1.1;+AI!V8O99WC!K*R!#,/2@)!V8OOEW!

UERStudy FinalReport

EXERGIAS.A. 32

metering.ThisDecreeallowsproducerstosubtract investmentcostsforAPGutilisationprojects fromthe fines, includingfor investments ingaspipelines,compressorstations,separationunits,facilitiesproducingelectricityandheatandforre-injection.Italsoallowsacompany to reach the95%utilisation targetbyaggregatingproductionacrossallofacompany’s fields. However, if the company is not able to reach this rate throughaggregation,finesarecalculatedforeachfieldindividually.Whilethisflexibilitycouldleadto some economic efficiency in targeting APG utilisation investments, it coulddisadvantagecompaniesthathaveasmallnumberoffields.

ThelicensesissuedbytheMinistryofNaturalResourcestooilandgasproducersincludethepermissiontoprocessandsellassociatedgas,re-injectit inthereservoir,utilizeit inthefacilityorproduceelectricity,orevenflarespecifiedamounts.Insomeregions,mostnotably in Khanty-Mansiysk and Yamalo-Nenets, it is mandatory to include an APGutilisationpercentageinthelicenceagreement.

CarboncreditsFollowingaprotractedprocessanddelays,Russianauthoritiesestablishedprocedurestoapproveprojectsdevelopedundertheso-calledJointImplementationmechanismoftheKyoto Protocol and to issue Emission Reduction Units (ERUs) that can be sold in theinternationalcarbonmarkets.ThefirstprojectapprovalsweremadeinJuly2010,andthefirst carbon creditswere issued in December of the same year. Over 20 flaring-relatedJointImplementationprojectshavebeenapproved,andsuchprojectsnowrepresentoneofthelargestcategoriesofapprovedJointImplementationprojectsinRussia.However,since2011,JointImplementationprojectshavebecomelessimportant,partlybecauseofapricecollapseforcarboncreditsandpartlybecauseRussiatookthedecisionnottojointhe second commitment period under the Kyoto Protocol, hencemaking new Russiancarboncreditsfromsuchprojectsineligibleincarbonmarkets.Itnowseemsunlikelythatthe emission reduction benefits of newAPGprojectswill have any economic value forinvestors in the near future. However, there are processes internally in governmentalinstitutions in Russia to design a national emissions trading system (a cap-and-tradescheme)13.

OverviewofAPGutilisationfacilitiesThemainAPGutilisationactivityinRussiaconcernsgasprocessingplants.In2010,48%ofproducedAPGwassuppliedtogasprocessingplants,whereitwasusedasfeedstockforproduction of marketable hydrocarbon products such as dry stripped gas, liquefiedpetroleumgasandstablegascondensate.Due to thehigh liquidcontentofmanyAPGstreams,expandinggasgatheringnetworksand increasingtheavailablegasprocessingcapacity represents one of the most promising options to reduce flaring in many oil-producingregionsinRussia,particularlyinareaswithsignificantexistinginfrastructure.

13Associated Petroleum Gas Flaring Study for Russia, Kazakhstan, Turkmenistan and Azerbaijan,CarbonLimits,2013

UERStudy FinalReport

EXERGIAS.A. 33

Apart from theoil companiesbywhomAPGutilisation ismostly seen as anobligation,thereisanotheractorinRussiathathasAPGprocessingasitsmainoccupation–SIBUR.SIBURutilisesaround17bcmofassociatedgas,whichamountsto57%ofthetotalvolumeofassociatedgasprocessinginRussia.ThecompanyrendersdeepAPGprocessing,thusproducingpetrochemicalswithhighvalueadded.InordertoensurecontinuoussupplyofAPG to its processing facilities SIBUR aims at creating long-term partnerships with oilcompanies.In2010,56%ofprocessedAPGwassuppliedtogasprocessingplants(GPPs)controlled by SIBUR. Some upstream operators have entered into joint ventures withSIBURtosecurelong-termcontractsforaccesstothelatter’sprocessingcapacityandforsalesofprocessedproducts.

Surgutneftegaz14andTatneftareamongthefewcompanies in the industry thatdonotuseprocessingplantsbelongingtoSIBURsincetheyownlargegasprocessingplantsthatwere built decades ago: Surgut Gas Processing Plant and Minnibaevo Gas ProcessingPlant. As Tatneft for years has been processing APG and supplying the products of itsprocessing to the petrochemical industry, Surgutneftegaz plans in the long term toproduce advanced petrochemicals at the company’s facilities. The main share of APGproducedbySurgutneftegazhasthroughtheyearsbeensuppliedtohigh-capacitypowerplants in the region: Surgut State District Power Stations. Around 70% of the APGproducedbythecompanyin2010wassuppliedtothesepowerplantsand,inaddition,itsown electricity production constituted more than 30 percent of its total electricityconsumption, ensuring the company’s technological processes, heating of houses,buildingsandcarparks15.

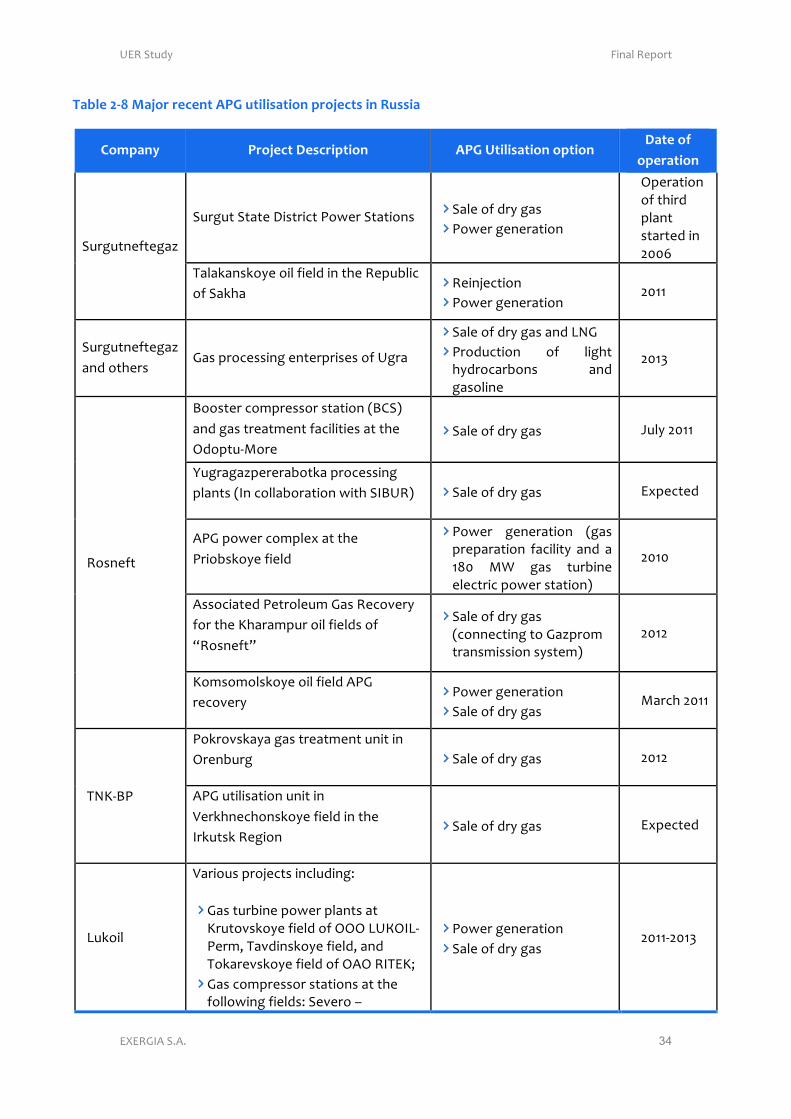

MajorrecentprojectsinassociatedgasprocessingfacilitiesaresummarizedinTable2-8.Thelistisnotexhaustive;howeveritpresentsanumberofimportantprojectsinRussia.

15ReducinggasflaringinRussia:Gloomyoutlookintimesofeconomicinsecurity,JuliaS.P.Lowe,OlgaLadehaug,Poyry,2012

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 34!

.KLM%'>c8'6K`"Q'Q%S%#$'(<I'P$NMN&K$N"#'XQ"`%S$&'N#'*P&&NK'

!"VXK#T' <Q"`%S$':%&SQNX$N"#' (<I'5$NMN&K$N"#'"X$N"#':K$%'"\'

"X%QK$N"#'

%'2@'&,/=&/@-c!

%'2@'&!%&-&/!T+>&2+A&!K1</2!%&-&+1,>! %-./!1=!(2)!@->! K1</2!@/,/2-&+1,!

:0/2-&+1,!1=!&I+2(!0.-,&!>&-2&/(!+,!8OON!

H-.-^-,>^1)/!1+.!=+/.(!+,!&I/!$/0'L.+A!1=!%-^I-!

$/+,Z/A&+1,! K1</2!@/,/2-&+1,!

8O99!

%'2@'&,/=&/@-c!-,(!1&I/2>!

4->!021A/>>+,@!/,&/202+>/>!1=!"@2-!

%-./!1=!(2)!@->!-,(!aP4! K21('A&+1,! 1=! .+@I&!I)(21A-2L1,>! -,(!@->1.+,/!

8O9B!

$1>,/=&!

Y11>&/2!A1?02/>>12!>&-&+1,!VYR%W!-,(!@->!&2/-&?/,&!=-A+.+&+/>!-&!&I/!:(10&'U[12/!

%-./!1=!(2)!@->! ]'.)!8O99!

p'@2-@-c0/2/2-L1&^-!021A/>>+,@!0.-,&>!V5,!A1..-L12-&+1,!<+&I!%5Y"$W! %-./!1=!(2)!@->! #X0/A&/(!

6K4!01</2!A1?0./X!-&!&I/!K2+1L>^1)/!=+/.(!

K1</2! @/,/2-&+1,! V@->!02/0-2-&+1,! =-A+.+&)! -,(! -!9GO! [f! @->! &'2L+,/!/./A&2+A!01</2!>&-&+1,W!

8O9O!

6>>1A+-&/(!K/&21./'?!4->!$/A1;/2)!=12!&I/!oI-2-?0'2!1+.!=+/.(>!1=!g$1>,/=&h!

%-./!1=!(2)!@->!VA1,,/A&+,@!&1!4-c021?!&2-,>?+>>+1,!>)>&/?W!

8O98

o1?>1?1.>^1)/!1+.!=+/.(!6K4!2/A1;/2)!

K1</2!@/,/2-&+1,! %-./!1=!(2)!@->! [-2AI!8O99!

HPoUYK!

K1^21;>^-)-!@->!&2/-&?/,&!',+&!+,!:2/,L'2@! %-./!1=!(2)!@->! 8O98!

6K4!'&+.+>-&+1,!',+&!+,!F/2^I,/AI1,>^1)/!=+/.(!+,!&I/!52^'&>^!$/@+1,!

%-./!1=!(2)!@->! #X0/A&/(!

a'^1+.!

F-2+1'>!021Z/A&>!+,A.'(+,@`!

4->!&'2L+,/!01</2!0.-,&>!-&!o2'&1;>^1)/!=+/.(!1=!:::!a"z:5aUK/2?C!H-;(+,>^1)/!=+/.(C!-,(!H1^-2/;>^1)/!=+/.(!1=!:6:!$5H#on!4->!A1?02/>>12!>&-&+1,>!-&!&I/!=1..1<+,@!=+/.(>`!%/;/21!s!

K1</2!@/,/2-&+1,! %-./!1=!(2)!@->! 8O99U8O9B!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 35!

!"VXK#T' <Q"`%S$':%&SQNX$N"#' (<I'5$NMN&K$N"#'"X$N"#':K$%'"\'

"X%QK$N"#'

o1cI;+,>^1)/C!y-0-(,1!s!H/L'^>^1)/!1=!{{{!a"o:5aUo1?+C!H21/.cI>^1)/C!62)-cI>^1)/!1=!:6:!$5H#on! 6!A1?02/>>12!>&-&+1,!&1!+,Z/A&!&I/!@->!+,&1!&I/!=12?-&+1,!-&!&I/!%2/(,/UoI'.)?>^1)/!=+/.(!1=!:6:!$5H#on! *+;/!1+.!I/-&/2>!-&!T'L2-;,1)/C!p'cI,1!s!o1,(2->I/;>^1)/C!$'>-^1;>^1)/C!o->+L>^1)/C!:AI/2>^1)/!=+/.(>!1=!:6:!$5H#on!H<1!?'.&+0I->/!0'?0!>&-&+1,>!-&!o-.?+)-2>^1)/!-,(!oI-&)?>^1)/!=+/.(>!1=!:6:!$5H#on!

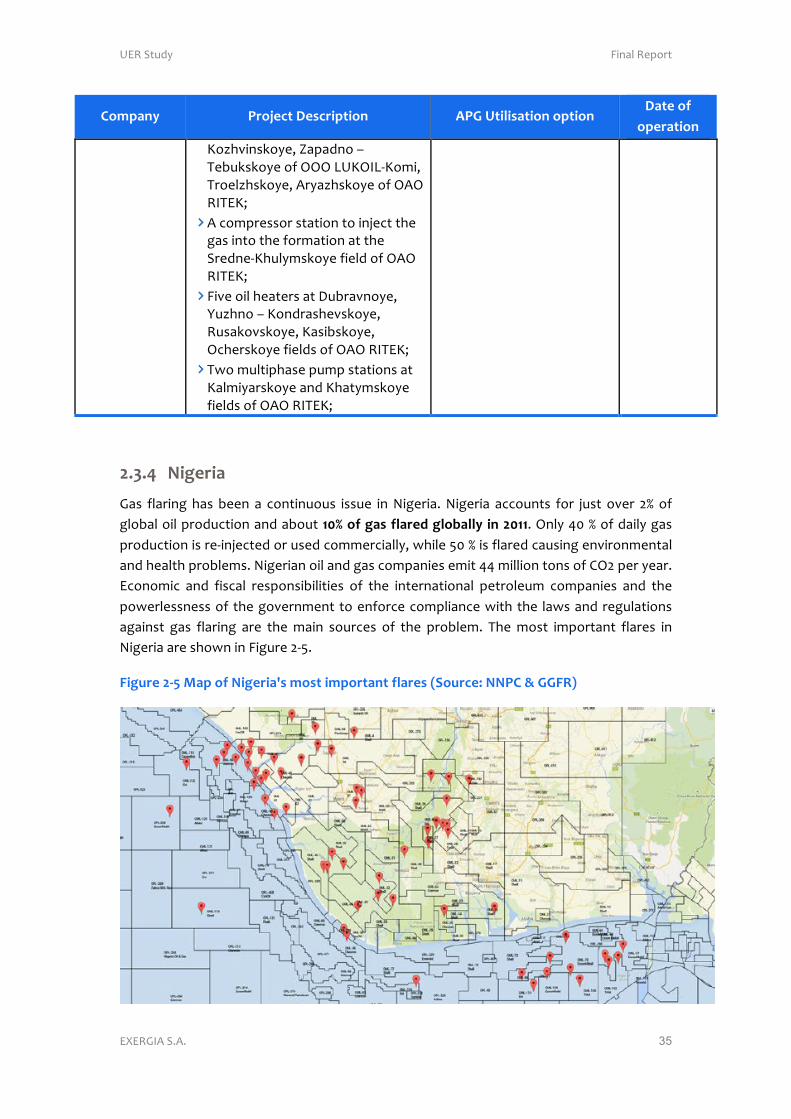

>2A2C 0NO%QNK'4->! =.-2+,@! I->! L//,! -! A1,&+,'1'>! +>>'/! +,!P+@/2+-7!P+@/2+-! -AA1',&>! =12! Z'>&! 1;/2! 8m! [email protected].!1+.!021('A&+1,!-,(!-L1'&!9Ei'"\'OK&'\MKQ%R'OM"LKMMT' N#'>E997!:,.)!DO!m!1=!(-+.)!@->!021('A&+1,!+>!2/U+,Z/A&/(!12!'>/(!A1??/2A+-..)C!<I+./!MO!m!+>!=.-2/(!A-'>+,@!/,;+21,?/,&-.!-,(!I/-.&I!021L./?>7!P+@/2+-,!1+.!-,(!@->!A1?0-,+/>!/?+&!DD!?+..+1,!&1,>!1=!R:8!0/2!)/-27!#A1,1?+A! -,(! =+>A-.! 2/>01,>+L+.+&+/>! 1=! &I/! +,&/2,-&+1,-.! 0/&21./'?! A1?0-,+/>! -,(! &I/!01</2./>>,/>>!1=! &I/!@1;/2,?/,&!&1!/,=12A/!A1?0.+-,A/!<+&I!&I/! .-<>!-,(!2/@'.-&+1,>!-@-+,>&! @->! =.-2+,@! -2/! &I/!?-+,! >1'2A/>! 1=! &I/! 021L./?7! HI/!?1>&! +?012&-,&! =.-2/>! +,!P+@/2+-!-2/!>I1<,!+,!*+@'2/!8UM7!!

@NOPQ%'>cF'6KX'"\'0NO%QNKj&'V"&$'NVX"Q$K#$'\MKQ%&'e1"PQS%a'00<!'h'II@*f'

!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 36!

5X&$Q%KV'%VN&&N"#&'Q%OPMK$N"#'5,!9JEJ!&I/!P+@/2+-,!@1;/2,?/,&!>+@,/(!&I/!6>>1A+-&/(!4->!$/U5,Z/A&+1,!6A&C!<I/2/!+&!<->!(/A.-2/(! &I-&! &I/! A1?0-,+/>! -2/! =12L+((/,! &1! =.-2/! &I/! @->! 021('A/(! <+&I! 1+.! -=&/2! 9!]-,'-2)! 9JGD! <+&I1'&! &I/! -(?+>>+1,! 1=! &I/! [+,+>&/27! P/;/2&I/./>>C! &I/! P+@/2+-,!-'&I12+&+/>!(+(!,1&!>'AA//(!+,!=12A+,@!&I/!A1?0-,+/>!&1!^//0!&I/!(/-(.+,/>7!

T/=+A+/,&! @1;/2,-,A/!1=! &I/!1+.! >/A&12!?-2^/(!L)! &I/! .-A^!1=! -,! +,(/0/,(/,&! 2/@'.-&12!-,(! -! I+>&12)! 1=! 0-)?/,&! (/=-'.&>! 1,! &I/! 0-2&! 1=! &I/! P+@/2+-,! P-&+1,-.! K/&21./'?!R12012-&+1,!VPPKRW!-,(!&I/!01</2!'&+.+&)C!A1?L+,/(!<+&I!>1?/!',>&2'A&'2/(!2/@'.-&+1,!.+^/! &I/! 2/A/,&! (+2/A&+;/! L)! &I/! [+,+>&2)! 1=! K/&21./'?! $/>1'2A/>! V[K$W! '2@+,@! 1+.!A1?0-,+/>!&1!@+;/!=.-2/(!@->!&1!B2(!0-2&)!+,;/>&12>!=12!6K4!'&+.+>-&+1,!021Z/A&>!I->!>0-2^/(!?'AI!A1,&21;/2>)!-?1,@!1+.!?-Z12>!10/2-&+,@! +,!&I/!A1',&2)7

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 37!

>'0012&!L)!.11^+,@!-&!+,+&+-.!+,A2/->/>!+,!I+@IU02/>>'2/!&2-,>?+>>+1,!-,(!L/&&/2!='.=+.?/,&!1=!/X+>&+,@!@->!0+0/.+,/>!L)!&I/!+,&/2,-&+1,-.!1+.!A1?0-,+/>9N7!

6! A1,&21;/2>+-.! K/&21./'?! 5,('>&2)! Y+..! VK5YW! +>>'/(! +,! 8O98! +,&/,(/(! &1! 2-+>/! &-X/>! 1,!5,&/2,-&+1,-.! :+.! R1?0-,+/>! V5:R>W! A2/-&+,@! -! A1?02/I/,>+;/! ./@-.! =2-?/<12^! =12! &I/!/X0.1+&-&+1,!1=!@->!-,(!0/&21./'?!2/>1'2A/>!+,!&I/!A1',&2)7!HI/!02101>/(!./@+>.-&+1,!<->!(/>+@,/(!&1!>&2/,@&I/,!&I/!A-0-A+&)!1=!+,(+@/,1'>!P+@/2+-,!A1?0-,+/>!+,!&I/!1+.!-,(!@->!>/A&12! &1! A1?0/&/! <+&I! +,&/2,-&+1,-.! 1+.! A1?0-,+/>! +,! &I/! >/-2AI! -,(! -AQ'+>+&+1,! 1=!I)(21A-2L1,>! +,! P+@/2+-7! HI/! K5Y! I->! >//,! ,'?/21'>! ?1(+=+A-&+1,>! >+,A/! 8O98! -,(! +>!A'22/,&.)!',(/2!(/L-&/7!!

/Z%QZN%U'"\'(<I'P$NMN&K$N"#'\KSNMN$N%&'H1!(-&/! &I/2/! -2/! ;-2+1'>! 021Z/A&>! -,(!?->&/2! 0.-,>! 1,! &I/!<-)! I/.0+,@! &1! 2/('A/! @->!=.-2+,@7! HI/!f/>&! 6=2+A-,! 4->! K+0/.+,/! R1?0-,)! 1<,/(! L)! RI/;21,C! P+@/2+-,! P-&+1,-.!K/&21./'?!R12012-&+1,!-,(!%I/..!I->!A2/-&/(!-!0.-,!&1!L'+.(!-!,/<!NGD!^?!@->!0+0/.+,/!&1!A1,,/A&!(+==/2/,&!1+.!=+/.(>!-A21>>!%'LU%-I-2-,!6=2+A-7!6>!-!2/>'.&!&I/!R:8!/?+>>+1,!+>!&1!L/!2/('A/(!L)!EG!?+..+1,!&1,,/>7!

[12/1;/2C! 4Ha! &/AI,1.1@)! +>! -.>1! '>/(! &1! 2/('A/! =.-2+,@7! :,/! 1=! &I/! =+2>&! 021Z/A&>! +,!P+@/2+-!<->!%->1.!RI/;21,! +,!#>A2-;1>7!HI/!0.-,&!I->!&I/!A-0-A+&)!&1!2/=+,/!BOO!?A=!0/2!(-)!1=!@->!&1!4Ha!(+/>/.!-,(!4Ha!,-0I&I-!=12!='2&I/2!?-2^/&+,@!+,!&I/!#"!-,(!"%7!:&I/2!4Ha! 021Z/A&>! -2/! +,&21('A/(C! I1</;/2! &I+>! &/AI,1.1@)! +>! ,/<! -,(! +&! <+..! &-^/! &+?/! &1!+?0./?/,&!&I/>/!021Z/A&>7!

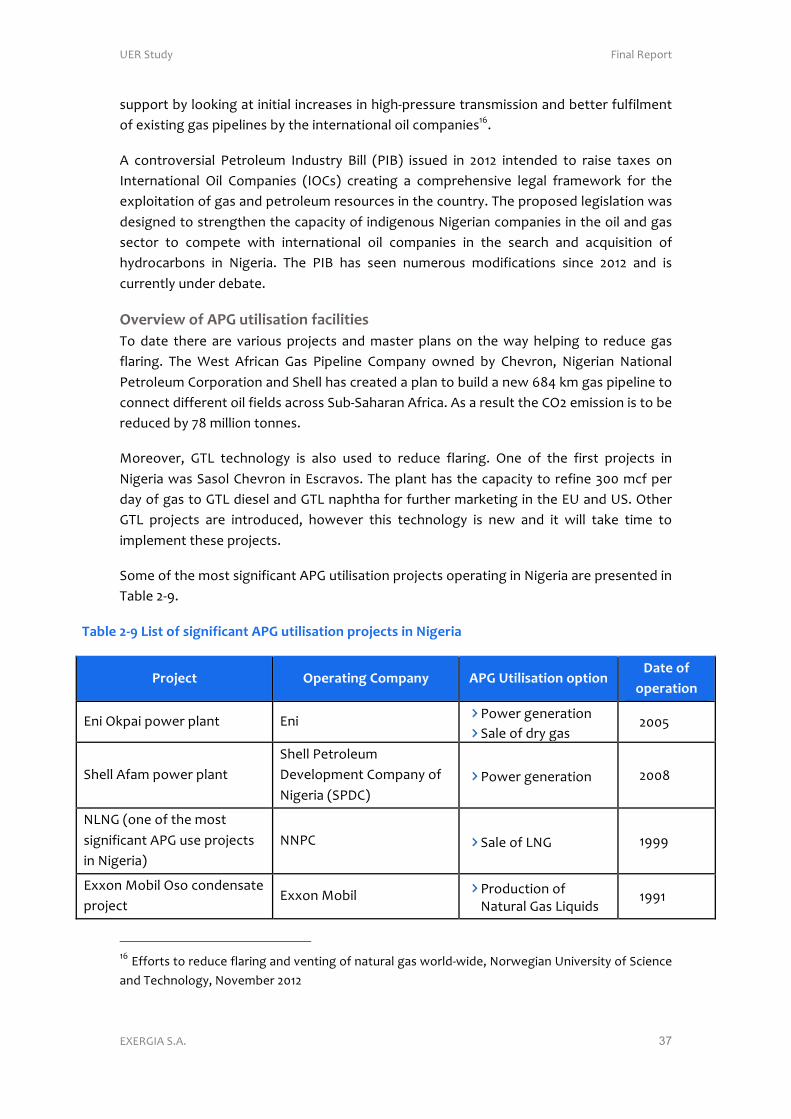

%1?/!1=!&I/!?1>&!>+@,+=+A-,&!6K4!'&+.+>-&+1,!021Z/A&>!10/2-&+,@!+,!P+@/2+-!-2/!02/>/,&/(!+,!H-L./!8UJ7!

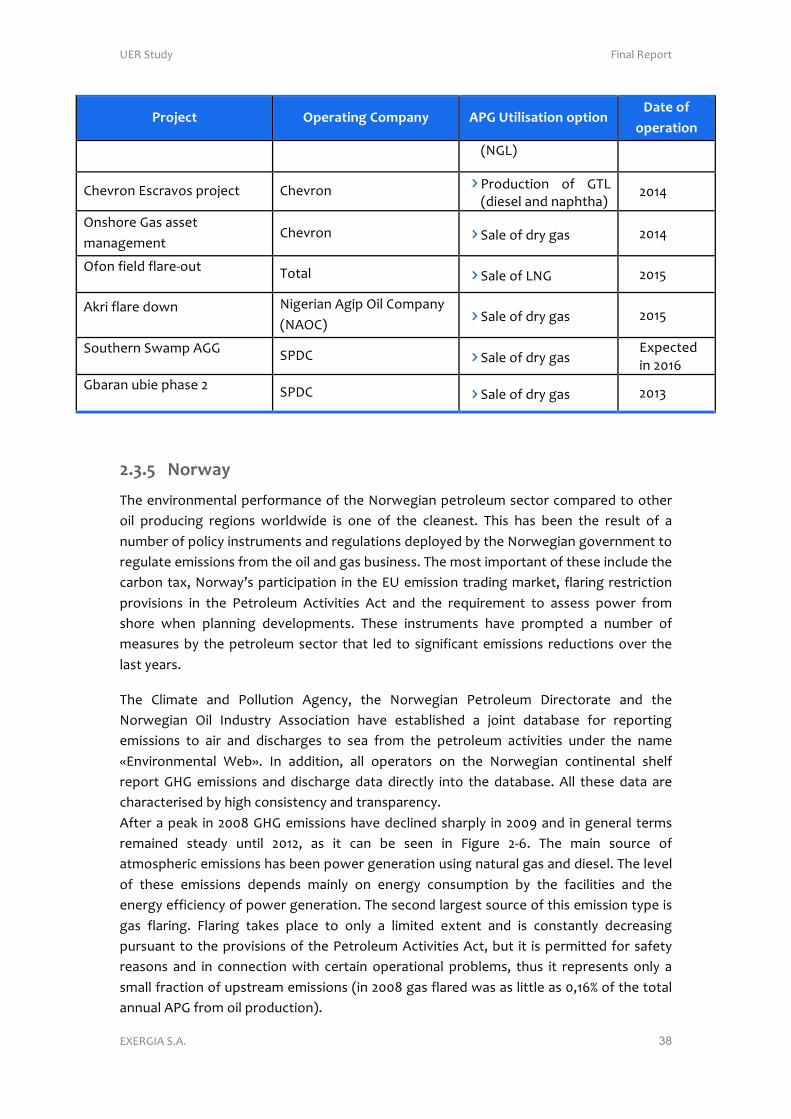

.KLM%'>cJ'BN&$'"\'&NO#N\NSK#$'(<I'P$NMN&K$N"#'XQ"`%S$&'N#'0NO%QNK'

<Q"`%S$' /X%QK$N#O'!"VXK#T' (<I'5$NMN&K$N"#'"X$N"#':K$%'"\'

"X%QK$N"#'

#,+!:^0-+!01</2!0.-,&! #,+!! K1</2!@/,/2-&+1,! %-./!1=!(2)!@->! 8OOM!

%I/..!6=-?!01</2!0.-,&!%I/..!K/&21./'?!T/;/.10?/,&!R1?0-,)!1=!P+@/2+-!V%KTRW!!

K1</2!@/,/2-&+1, 8OOG!

PaP4!V1,/!1=!&I/!?1>&!>+@,+=+A-,&!6K4!'>/!021Z/A&>!+,!P+@/2+-W!

PPKR! %-./!1=!aP4! 9JJJ!

#XX1,

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 38!

<Q"`%S$' /X%QK$N#O'!"VXK#T' (<I'5$NMN&K$N"#'"X$N"#':K$%'"\'

"X%QK$N"#'

VP4aW!

RI/;21,!#>A2-;1>!021Z/A&! RI/;21,! K21('A&+1,! 1=! 4Ha!V(+/>/.!-,(!,-0I&I-W!

8O9D!

:,>I12/!4->!->>/&!?-,-@/?/,&!

RI/;21,! %-./!1=!(2)!@->! 8O9D!

:=1,!=+/.(!=.-2/U1'&! H1&-.! %-./!1=!aP4! 8O9M!

6^2+!=.-2/!(1<,! P+@/2+-,!6@+0!:+.!R1?0-,)!VP6:RW! %-./!1=!(2)!@->!! 8O9M!

%1'&I/2,!%<-?0!644! %KTR! %-./!1=!(2)!@->! #X0/A&/(!+,!8O9N!

4L-2-,!'L+/!0I->/!8! %KTR! %-./!1=!(2)!@->! 8O9B!

>2A2F 0"QUKT'

HI/!/,;+21,?/,&-.!0/2=12?-,A/!1=!&I/!P12</@+-,!0/&21./'?!>/A&12!A1?0-2/(!&1!1&I/2!1+.! 021('A+,@! 2/@+1,>! <12.(<+(/! +>! 1,/! 1=! &I/! A./-,/>&7! HI+>! I->! L//,! &I/! 2/>'.&! 1=! -!,'?L/2!1=!01.+A)!+,>&2'?/,&>!-,(!2/@'.-&+1,>!(/0.1)/(!L)!&I/!P12</@+-,!@1;/2,?/,&!&1!2/@'.-&/!/?+>>+1,>!=21?!&I/!1+.!-,(!@->!L'>+,/>>7!HI/!?1>&!+?012&-,&!1=!&I/>/!+,A.'(/!&I/!A-2L1,!&-XC!P12<-)j>!0-2&+A+0-&+1,! +,!&I/!#"!/?+>>+1,!&2-(+,@!?-2^/&C! =.-2+,@!2/>&2+A&+1,!021;+>+1,>! +,! &I/! K/&21./'?! 6A&+;+&+/>! 6A&! -,(! &I/! 2/Q'+2/?/,&! &1! ->>/>>! 01</2! =21?!>I12/! <I/,! 0.-,,+,@! (/;/.10?/,&>7! HI/>/! +,>&2'?/,&>! I-;/! 021?0&/(! -! ,'?L/2! 1=!?/->'2/>!L)! &I/!0/&21./'?!>/A&12! &I-&! ./(! &1! >+@,+=+A-,&!/?+>>+1,>! 2/('A&+1,>!1;/2! &I/!.->&!)/-2>7!

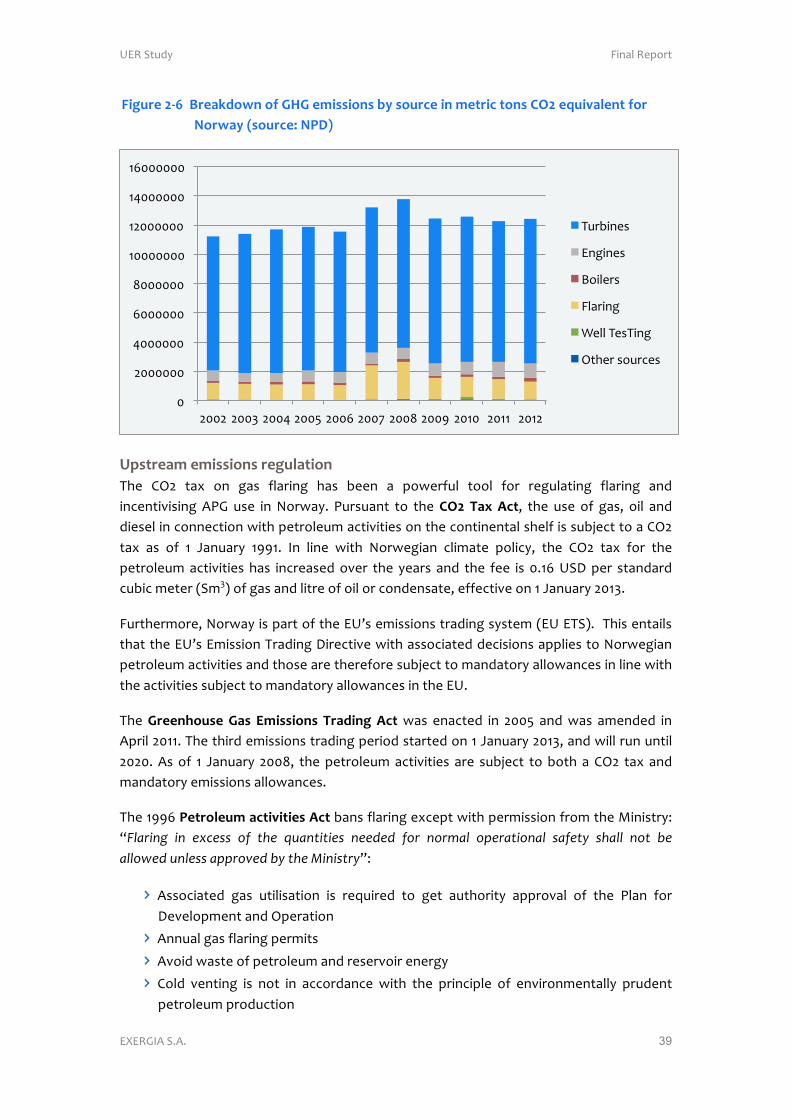

HI/! R.+?-&/! -,(! K1..'&+1,! 6@/,A)C! &I/! P12</@+-,! K/&21./'?! T+2/A&12-&/! -,(! &I/!P12</@+-,! :+.! 5,('>&2)! 6>>1A+-&+1,! I-;/! />&-L.+>I/(! -! Z1+,&! (-&-L->/! =12! 2/012&+,@!/?+>>+1,>! &1! -+2! -,(! (+>AI-2@/>! &1! >/-! =21?! &I/! 0/&21./'?! -A&+;+&+/>! ',(/2! &I/! ,-?/!|#,;+21,?/,&-.! f/L}7! 5,! -((+&+1,C! -..! 10/2-&12>! 1,! &I/! P12</@+-,! A1,&+,/,&-.! >I/.=!2/012&!4b4!/?+>>+1,>! -,(!(+>AI-2@/!(-&-! (+2/A&.)! +,&1! &I/!(-&-L->/7!6..! &I/>/!(-&-! -2/!AI-2-A&/2+>/(!L)!I+@I!A1,>+>&/,A)!-,(!&2-,>0-2/,A)7!6=&/2!-!0/-^! +,!8OOG!4b4!/?+>>+1,>!I-;/!(/A.+,/(!>I-20.)! +,!8OOJ!-,(! +,!@/,/2-.! &/2?>!2/?-+,/(! >&/-()! ',&+.! 8O98C! ->! +&! A-,! L/! >//,! +,! *+@'2/! 8UN7! HI/! ?-+,! >1'2A/! 1=!-&?1>0I/2+A!/?+>>+1,>!I->!L//,!01</2!@/,/2-&+1,!'>+,@!,-&'2-.!@->!-,(!(+/>/.7!HI/!./;/.!1=! &I/>/! /?+>>+1,>! (/0/,(>! ?-+,.)! 1,! /,/2@)! A1,>'?0&+1,! L)! &I/! =-A+.+&+/>! -,(! &I/!/,/2@)!/==+A+/,A)!1=!01</2!@/,/2-&+1,7!HI/!>/A1,(!.-2@/>&!>1'2A/!1=!&I+>!/?+>>+1,!&)0/!+>!@->! =.-2+,@7! *.-2+,@! &-^/>! 0.-A/! &1! 1,.)! -! .+?+&/(! /X&/,&! -,(! +>! A1,>&-,&.)! (/A2/->+,@!0'2>'-,&!&1!&I/!021;+>+1,>!1=!&I/!K/&21./'?!6A&+;+&+/>!6A&C!L'&! +&! +>!0/2?+&&/(!=12!>-=/&)!2/->1,>! -,(! +,! A1,,/A&+1,!<+&I! A/2&-+,! 10/2-&+1,-.! 021L./?>C! &I'>! +&! 2/02/>/,&>! 1,.)! -!>?-..!=2-A&+1,!1=!'0>&2/-?!/?+>>+1,>!V+,!8OOG!@->!=.-2/(!<->!->!.+&&./!->!OC9Nm!1=!&I/!&1&-.!-,,'-.!6K4!=21?!1+.!021('A&+1,W7!!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 39!

@NOPQ%'>c3'')Q%K_R"U#'"\'I;I'%VN&&N"#&'LT'&"PQS%'N#'V%$QNS'$"#&'!/>'%YPNZKM%#$'\"Q'0"QUKT'e&"PQS%a'0<:f'

!

5X&$Q%KV'%VN&&N"#&'Q%OPMK$N"#'HI/! R:8! &-X! 1,! @->! =.-2+,@! I->! L//,! -! 01</2='.! &11.! =12! 2/@'.-&+,@! =.-2+,@! -,(!+,A/,&+;+>+,@! 6K4! '>/! +,! P12<-)7! K'2>'-,&! &1! &I/!!/>' .K^' (S$C! &I/! '>/! 1=! @->C! 1+.! -,(!(+/>/.!+,!A1,,/A&+1,!<+&I!0/&21./'?!-A&+;+&+/>!1,!&I/!A1,&+,/,&-.!>I/.=!+>!>'LZ/A&!&1!-!R:8!&-X! ->! 1=! 9! ]-,'-2)! 9JJ97! 5,! .+,/! <+&I! P12</@+-,! A.+?-&/! 01.+A)C! &I/! R:8! &-X! =12! &I/!0/&21./'?!-A&+;+&+/>! I->! +,A2/->/(!1;/2! &I/! )/-2>! -,(! &I/! =//! +>! O79N!"%T!0/2! >&-,(-2(!A'L+A!?/&/2!V%?BW!1=!@->!-,(!.+&2/!1=!1+.!12!A1,(/,>-&/C!/==/A&+;/!1,!9!]-,'-2)!8O9B7!

*'2&I/2?12/C!P12<-)!+>!0-2&!1=!&I/!#"j>!/?+>>+1,>!&2-(+,@!>)>&/?!V#"!#H%W7!!HI+>!/,&-+.>!&I-&!&I/!#"j>!#?+>>+1,!H2-(+,@!T+2/A&+;/!<+&I!->>1A+-&/(!(/A+>+1,>!-00.+/>!&1!P12</@+-,!0/&21./'?!-A&+;+&+/>!-,(!&I1>/!-2/!&I/2/=12/!>'LZ/A&!&1!?-,(-&12)!-..1<-,A/>!+,!.+,/!<+&I!&I/!-A&+;+&+/>!>'LZ/A&!&1!?-,(-&12)!-..1<-,A/>!+,!&I/!#"7!

HI/!IQ%%#W"P&%'IK&' +VN&&N"#&' .QKRN#O'(S$! <->! /,-A&/(! +,! 8OOM! -,(!<->! -?/,(/(! +,!602+.!8O997!HI/!&I+2(!/?+>>+1,>!&2-(+,@!0/2+1(!>&-2&/(!1,!9!]-,'-2)!8O9BC!-,(!<+..!2',!',&+.!8O8O7!6>!1=! 9! ]-,'-2)! 8OOGC! &I/!0/&21./'?!-A&+;+&+/>! -2/! >'LZ/A&! &1!L1&I! -! R:8! &-X! -,(!?-,(-&12)!/?+>>+1,>!-..1<-,A/>7!

HI/!9JJN!<%$Q"M%PV'KS$NZN$N%&'(S$!L-,>!=.-2+,@!/XA/0&!<+&I!0/2?+>>+1,!=21?!&I/

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 40!

HI/!P12</@+-,!./@-.!=2-?/<12^!-+?+,@!-&!&I/!2/('A&+1,!1=!=.-2+,@!-,(!&I/!/,I-,A/?/,&!1=!6K4!'>/!+>!>'??-2+>/(!+,!H-L./!8U9O7!

.KLM%'>c9E'1PVVKQT'"\'0"QU%ONK#'M%OKM'\QKV%U"Q_'"#'OK&'\MKQN#O'K#R'(<I'P$NMN&K$N"#'

/NM'/X%QK$"Q' I"Z%Q#V%#$''

6%K&PQN#Oa!

:0/2-&12>!<I1!-2/!=.-2+,@!-,(!;/,&+,@!6K4!('2+,@!10/2-&+1,-.!0I->/!-2/!2/>01,>+L./!=12!/>&-L.+>I+,@!&I/!+,&/2,-.!A1,&21.!>)>&/?!=12!/,>'2+,@!A1?0.+-,A/C!>'AI!->!1L.+@-&+1,!&1!AI/A^!>/,>12!A-.+L2-&+1,!/;/2)!>+X!?1,&I>7!

:0/2-&12>!-2/!2/>01,>+L./!=12!^//0+,@!-,!/?+>>+1,>!+,;/,&12)!<+&I!2/Q'+2/?/,&!&1!>'L?+&!&1!&I/!P12</@+-,!K/&21./'?!T+2/A&12-&/!VPKTW!L/=12/![-2AI!9!1=!/-AI!)/-27!

6%K&PQN#Oa!

PKT!>'0/2;+>/>!+,&/2,-.!A1,&21.!>)>&/?>!=12!10/2-&12>!&1!;/2+=)!&I-&!0/&21./'?!-A&+;+&+/>!-2/!A-22+/(!1'&!+,!-AA12(-,A/!<+&I!-'&I12+&+/>j!2/Q'+2/?/,&>!-,(!-AA/0&/(!L)!A1?0-,+/>j!A2+&/2+-!@1-.>!

6.>1!+&!1L>/2;/>!V-'(+&>W!&I/!-00.+A-&+1,!1=!&I/!/Q'+0?/,&!&I-&!?/->'2/>!Q'-,&+&)!1=!@->!'>/(!=12!=.-2+,@!-,(!;/,&+,@7!

*%X"Q$N#Oa'

:0/2-&+,@!A1?0-,)!&I-&!I1.(>!=.-2+,@!0/2?+&!I->!&1!>'L?+&!-!2/012&!&1!&I/!>&-&/!-'&I12+&+/>C!+,(+A-&+,@!&I/!-?1',&!1=!@->!=.-2/(!(-+.)7'

#;/2)!>+X!?1,&I>!+&!I->!&1!2/012&!1,!;1.'?/>!1=!&I/!=.-2/(!@->!=12!&-X!0'201>/>7'

*%X"Q$N#Oa'

:L&-+,+,@!-,(!/;-.'-&+,@!2/012&>!>'L?+&&/(!L)!1+.!10/2-&12>7''

HI/!/,=12A/?/,&!1=!&I+>!2/@'.-&12)!=2-?/<12^!+>!I1</;/2!=-A+.+&-&/(!L)!&I/!021X+?+&)!1=!&I/! A1',&2)! &1! I'@/! ?-2^/&>! =12! ,-&'2-.! @->C! A1?L+,/(! <+&I! -,! /X+>&+,@! @->! 0+0/.+,/!&2-,>012&-&+1,! +,=2->&2'A&'2/! &I-&! A-,! -AA/>>! &I1>/!?-2^/&>7! HI'>C! +,!P12<-)C! 2/('A+,@!=.-2+,@!1=!6K4!+>!?'AI!/->+/2!-,(!./>>!/X0/,>+;/!&1!-AI+/;/!&I-,!+,!1&I/2!A1',&2+/>C!>'AI!->!+,!6=2+A-7!!

/Z%QZN%U'"\'(<I'P$NMN&K$N"#'\KSNMN$N%&'[1>&!1=!&I/!(<I'XQ"RPS%R'N#'0"QUKT'N&'%^X"Q$%R! &1!&I/!#'210/-,!?-2^/&!-,(!&I+>!@->!/X012&C!/,-L./(!L)!-!>&21,@!0+0/.+,/!,/&<12^!-,(!021X+?+&)!&1!?-2^/&!-.1,@!<+&I!&I/!R:8!&-X! I->! 0.-)/(! -! >+@,+=+A-,&! 21./! +,! 2/('A+,@! @->! =.-2+,@! +,! &I/! A1',&2)7! HI/! Q%VKN#N#O'K&&"SNK$%R'OK&'$WK$'N&'#"$'%^X"Q$%R'N&'Q%N#`%S$%R]'+,!12(/2!&1'?-+,&-+,!&I/!02/>>'2/!-,(!=.1<!2-&/!1=!&I/!1+.!L/+,@!021('A/(7!Y)!'>+,@!&I/!->>1A+-&/(!@->!+,!&I/!021('A&+1,C!&I/)!-2/!-L./!&1!2/A1;/2!?'AI!I+@I/2!0/2A/,&-@/!1=!1+.!&I-,!+=!&I/)!</2/!&1!>+?0.)!+,Z/A&!<-&/2!=12!/X-?0./7!HI/!,-&'2-.!@->!A-,! .-&/2!L/!021('A/(!-,(!>1.(!<I/,!A2'(/!1+.!021('A&+1,!A/->/>7!5,!&I/!A->/!<I/2/!&I+>!+>!,1&!,/A/>>-2)C!12!,1&!01>>+L./C!&I/!@->!A-,!-.>1!L/!'>/(!&1!021('A/!/./A&2+A+&)!+,!@->U=+2/(!&'2L+,/>7!HI-&!<-)!&I/!@->!+>,j&! Z'>&!<->&/(!1,!=.-2+,@C!L'&!A-,!L/!-,!/,/2@)!>1'2A/!&1!021;+(/!01</2!=12!+,('>&2)!10/2-&+1,>C!>'AI!->!0'?0+,@C!A1?02/>>+1,!?-AI+,/>!-,(!@->!021A/>>+,@7!HI/!/./A&2+A+&)! A-,!/;/,!L/!>1.(C! +=! &I/)! +&! +>!,1&!A1,>'?/(!/,&+2/.)!+,!&I/!=+/.(7!

"#$!%&'()! *+,-.!$/012&!

#3#$456!%767!! ! 41!

*%N#`%S$N"#'"\'(<I'

%+,A/! +,Z/A&+1,! 1=! ,-&'2-.! @->! >&-2&/(! +,! P12<-)! +,! )/-2! 9JEM! &I/! =+/.(>! 10/2-&12>! I-;/!L//,! -L./! &1! 2/A1;/2! 8U8CB! L+..+1,! -((+&+1,-.! L-22/.>! 1=! 1+.! -,(! A1,(/,>-&/7! #X-?0./>! 1=!2/+,Z/A&+1,!021A/('2/>!+,!P12<-)!+,A.'(/`!

+_"\N&_'\N%MR!<I+AI!+,A2/->/(!&I/!2/A1;/2)!2-&/!=21?!9EU9Gm!&1!MOm!

/&%L%QO'\N%MR!<I+AI!I->!-!2/A1;/2)!2-&/!1=!NBm!

1$K$\`"QR'\N%MR'<I+AI'I->!-!2/A1;/2)!2-&/!1=!NNm!

!