Embed Size (px)

Citation preview

Optimizing Your Payables Mix:

A Guide to Maximizing Automation & Financial Return in AP Andrea Eaton

Paymode-X from Bottomline Technologies, Inc.

Top 10 reasons to keep using checks

Agenda

• Payments in 2014: Bottomline’s study

• Opportunities and trends in AP

• Considerations for maximizing financial and

efficiency gains

• A checklist for your organization

• Q&A

Payments in 2014

Bottomline’s AP Benchmark Study

We provided clients with a complimentary

AP spend analysis so they can:

• Learn how their organization stacks up

against industry benchmarks

• Discover new opportunities for optimizing

working capital, driving efficiencies and

improving vendor satisfaction

This data gives us unique insight into

how payments are really made by

companies of all sizes, from all

industries.

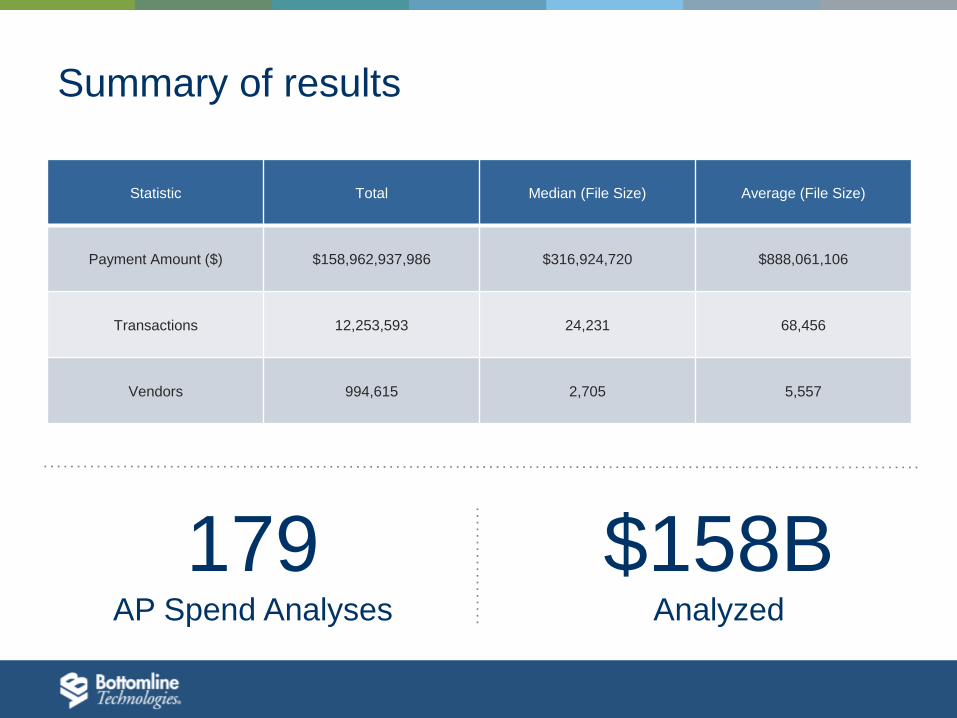

Summary of results

Statistic Total Median (File Size) Average (File Size)

Payment Amount ($) $158,962,937,986 $316,924,720 $888,061,106

Transactions 12,253,593 24,231 68,456

Vendors 994,615 2,705 5,557

$158B Analyzed

179 AP Spend Analyses

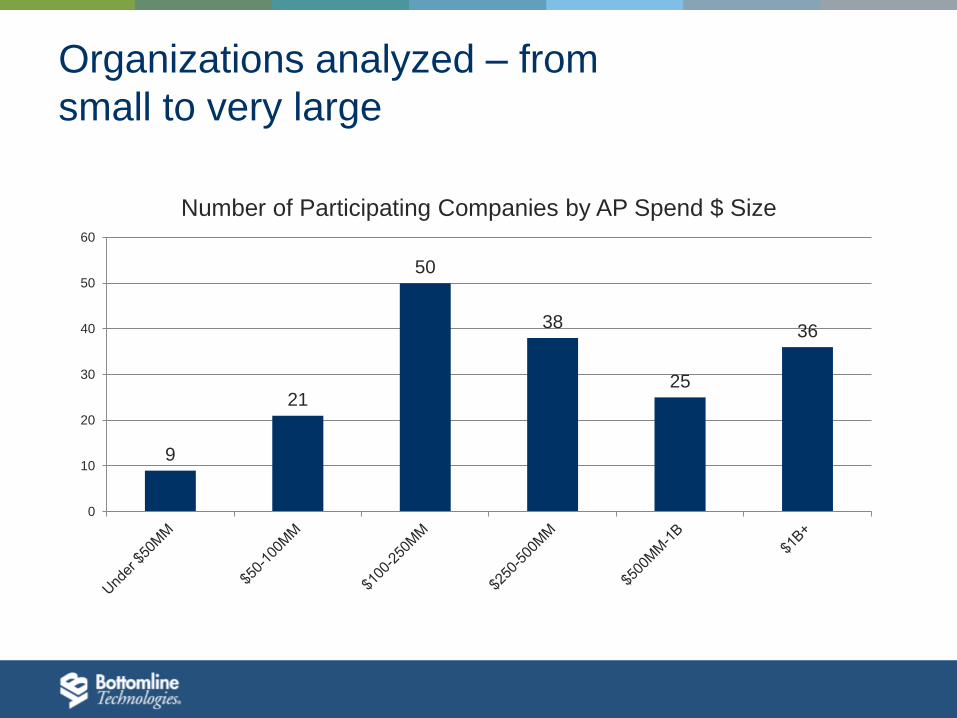

Organizations analyzed – from

small to very large

9

21

50

38

25

36

0

10

20

30

40

50

60

Number of Participating Companies by AP Spend $ Size

Payment methods

ACH (Automated Clearing House)

• Utilizes an electronic

network via daily batch with

1-2 day settlement delay

• Standardized payment files

with limited remittance

• Can be easily integrated

into AP systems

Wire Transfer

• Generally offer same day

settlement for buyer and

supplier

• High transaction fees to

send and receive

• Typically reserved for

large dollar or

international transactions

Traditional Check

• Most common form of B2B

payments, but highest cost

to process

• Suppliers will often permit

45-60 day payment terms

• Check payments take 3-5

days to settle, increasing

supplier’s DSO

Traditional P-Cards

• Most widely used card

payment product for

procurement of goods by

various channels

• Can replace the

traditional

PO/invoice/approval

process

• May have embedded

controls to ensure

compliance

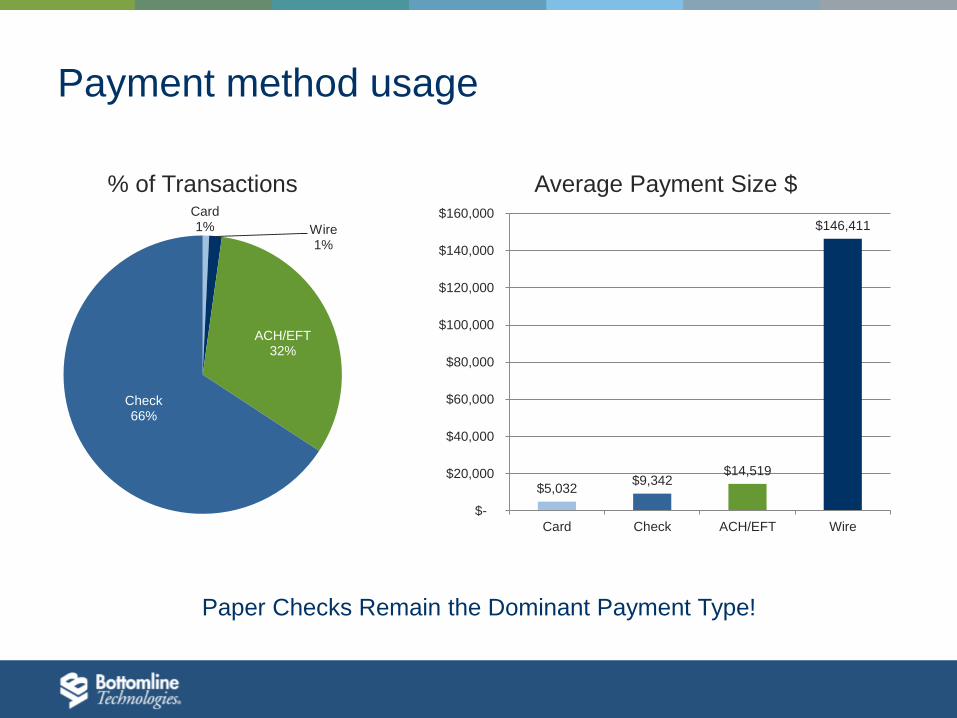

Payment method usage

$5,032 $9,342

$14,519

$146,411

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

Card Check ACH/EFT Wire

Average Payment Size $ Card 1% Wire

1%

ACH/EFT 32%

Check 66%

% of Transactions

Paper Checks Remain the Dominant Payment Type!

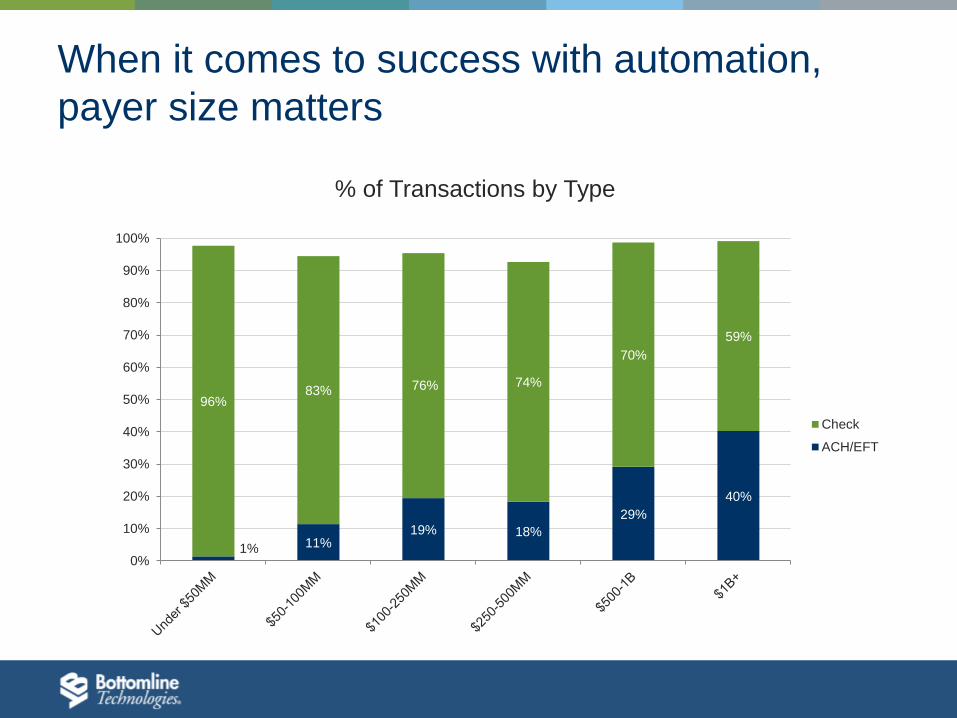

When it comes to success with automation,

payer size matters

1% 11% 19% 18%

29%

40%

96% 83% 76% 74%

70%

59%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Check

ACH/EFT

% of Transactions by Type

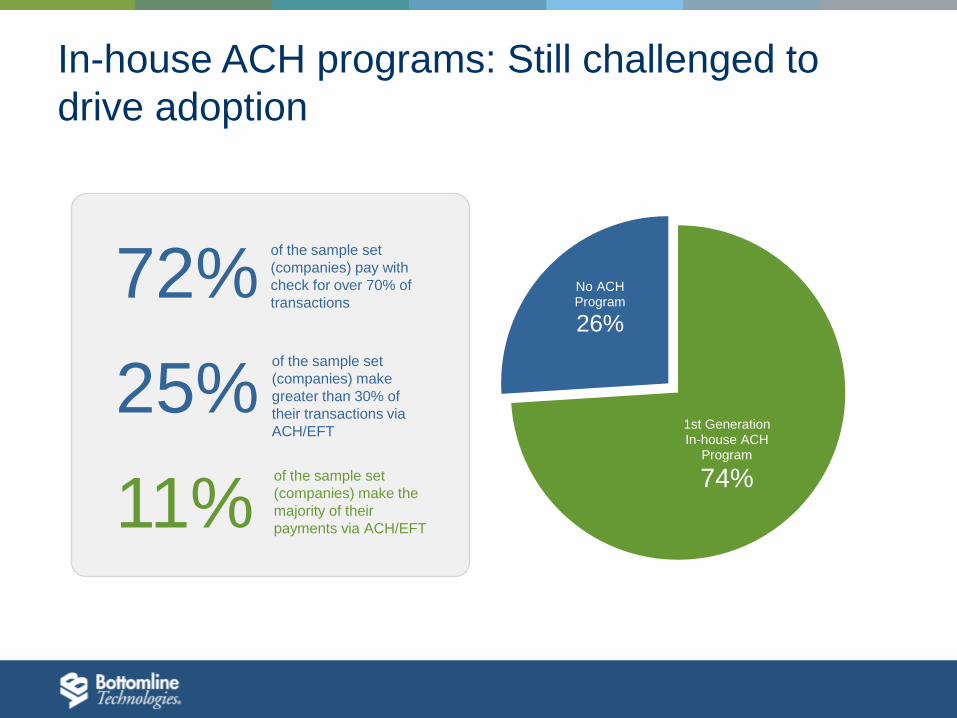

In-house ACH programs: Still challenged to

drive adoption

1st Generation In-house ACH

Program

74%

No ACH Program

26%

72%

25%

11%

of the sample set

(companies) pay with

check for over 70% of

transactions

of the sample set

(companies) make

greater than 30% of

their transactions via

ACH/EFT

of the sample set

(companies) make the

majority of their

payments via ACH/EFT

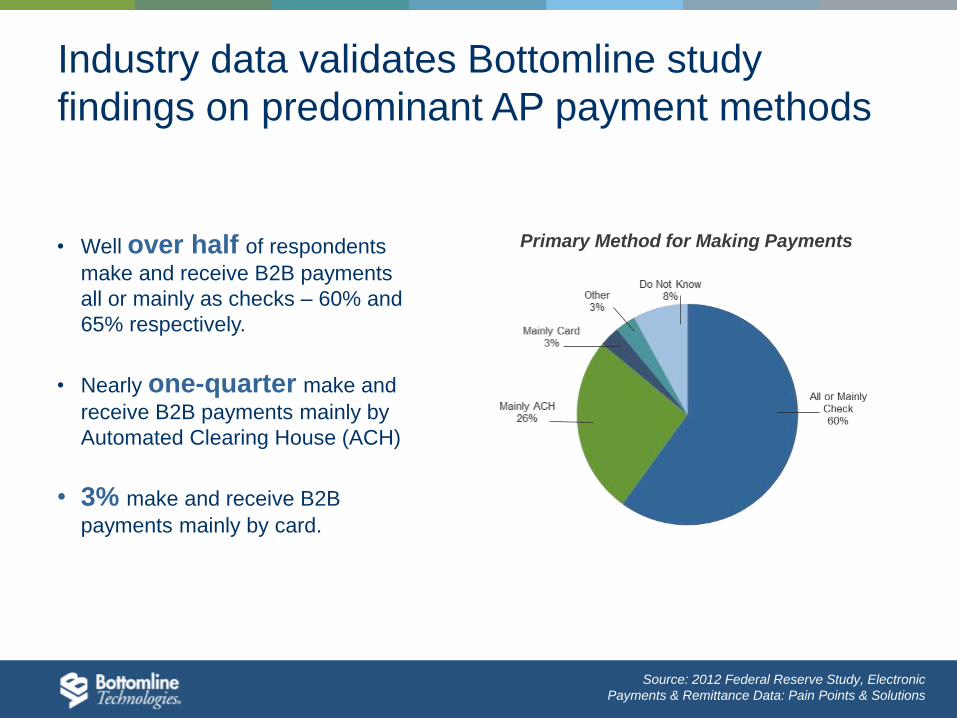

Industry data validates Bottomline study

findings on predominant AP payment methods

Source: 2012 Federal Reserve Study, Electronic

Payments & Remittance Data: Pain Points & Solutions

Primary Method for Making Payments • Well over half of respondents

make and receive B2B payments

all or mainly as checks – 60% and

65% respectively.

• Nearly one-quarter make and

receive B2B payments mainly by

Automated Clearing House (ACH)

• 3% make and receive B2B

payments mainly by card.

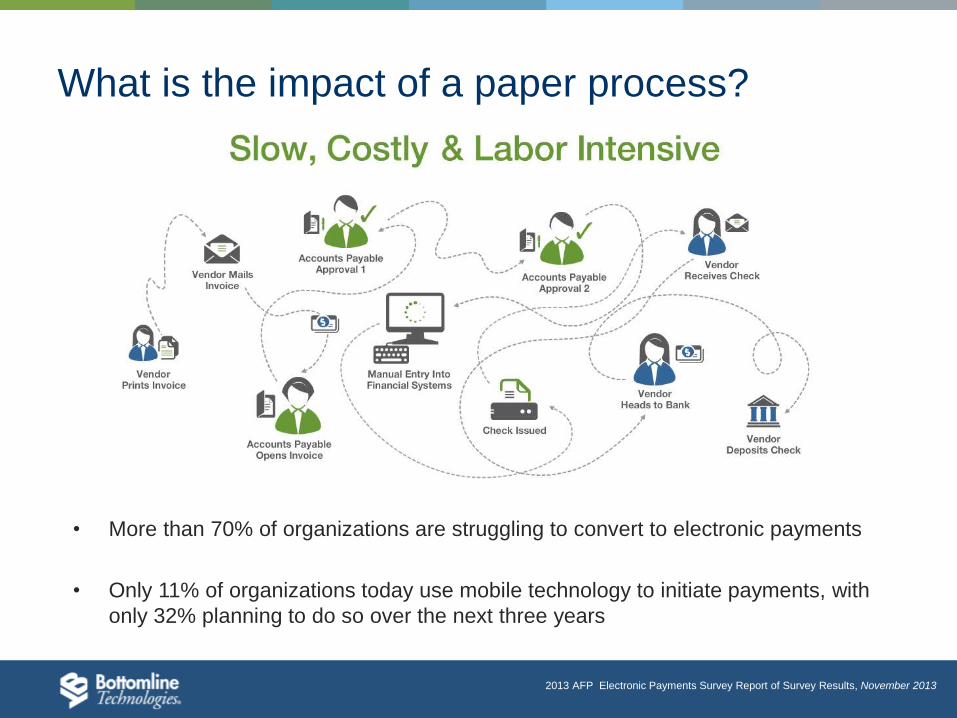

What is the impact of a paper process?

• More than 70% of organizations are struggling to convert to electronic payments

• Only 11% of organizations today use mobile technology to initiate payments, with

only 32% planning to do so over the next three years

2013 AFP Electronic Payments Survey Report of Survey Results, November 2013

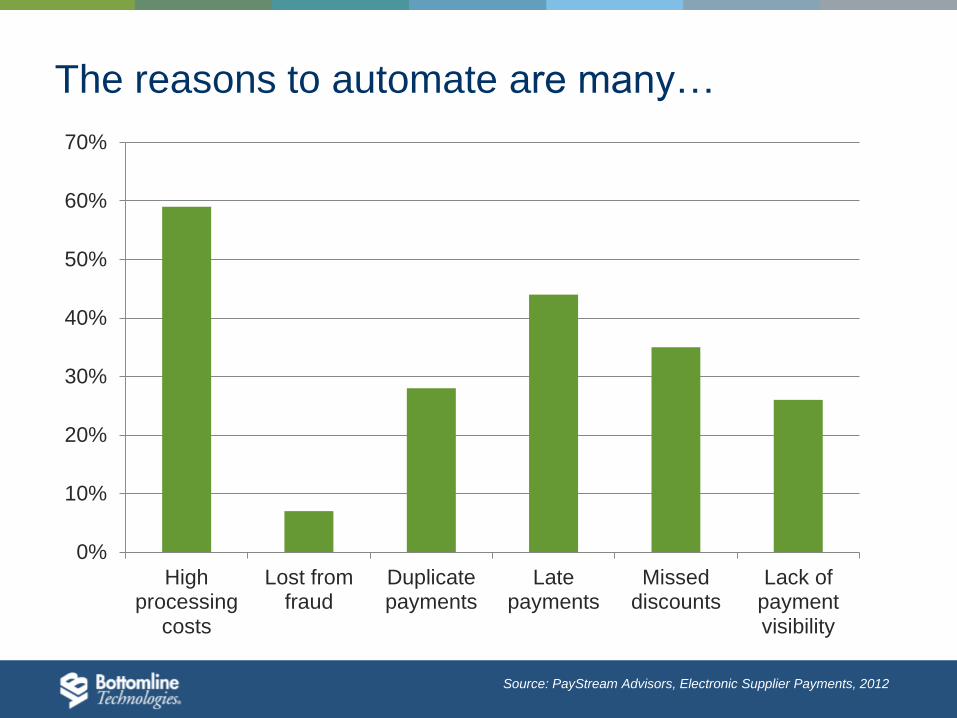

The reasons to automate are many…

0%

10%

20%

30%

40%

50%

60%

70%

Highprocessing

costs

Lost fromfraud

Duplicatepayments

Latepayments

Misseddiscounts

Lack ofpaymentvisibility

Source: PayStream Advisors, Electronic Supplier Payments, 2012

But most organizations run into the same barriers

Difficulty convincing

suppliers to accept

electronic payments

Shortage of IT

resources for

implementation

Lack of standard

format for remittance

information

Lack of integration

between e-payment &

accounting system

74% 71% 70% 66%

AFP Study November 2013

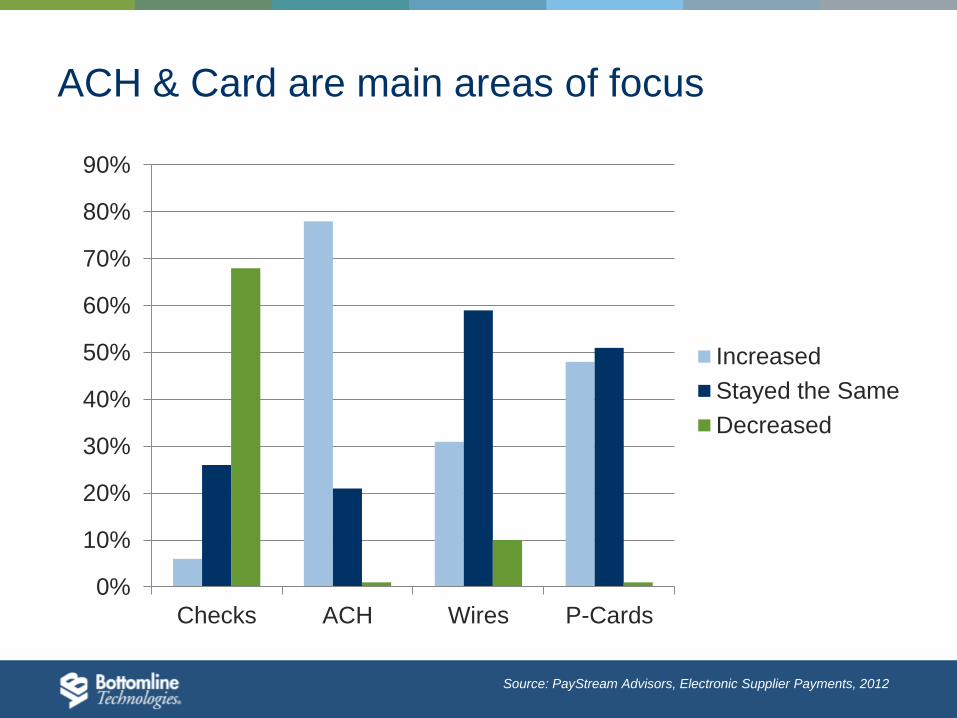

ACH & Card are main areas of focus

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Checks ACH Wires P-Cards

Increased

Stayed the Same

Decreased

Source: PayStream Advisors, Electronic Supplier Payments, 2012

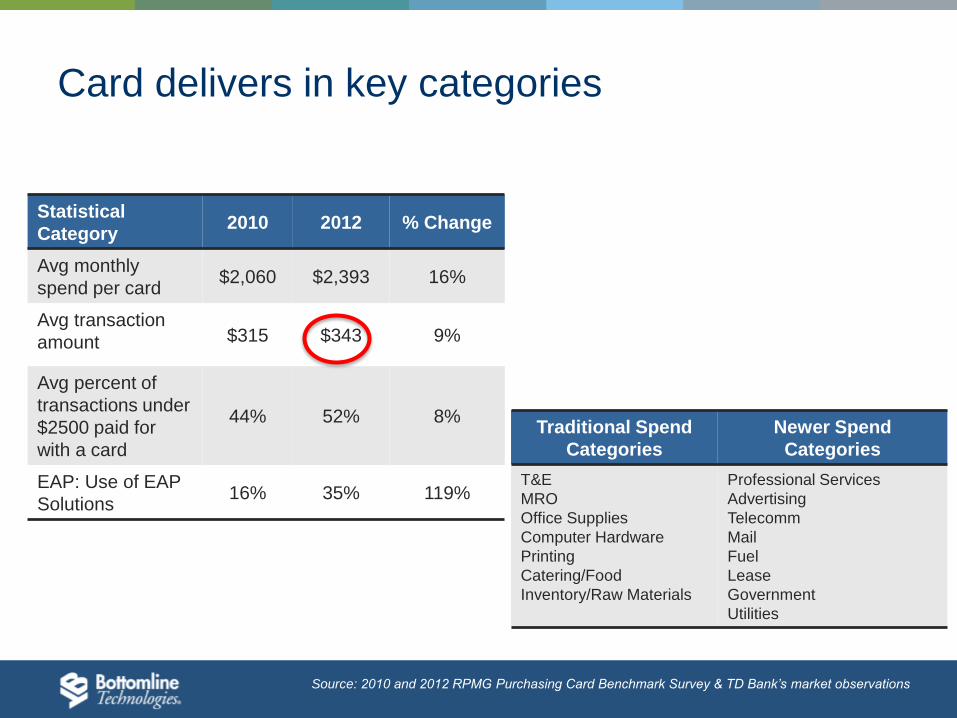

Card delivers in key categories

Statistical

Category 2010 2012 % Change

Avg monthly

spend per card $2,060 $2,393 16%

Avg transaction

amount $315 $343 9%

Avg percent of

transactions under

$2500 paid for

with a card

44% 52% 8%

EAP: Use of EAP

Solutions 16% 35% 119%

Traditional Spend

Categories

Newer Spend

Categories

T&E

MRO

Office Supplies

Computer Hardware

Printing

Catering/Food

Inventory/Raw Materials

Professional Services

Advertising

Telecomm

Fuel

Lease

Government

Utilities

Source: 2010 and 2012 RPMG Purchasing Card Benchmark Survey & TD Bank’s market observations

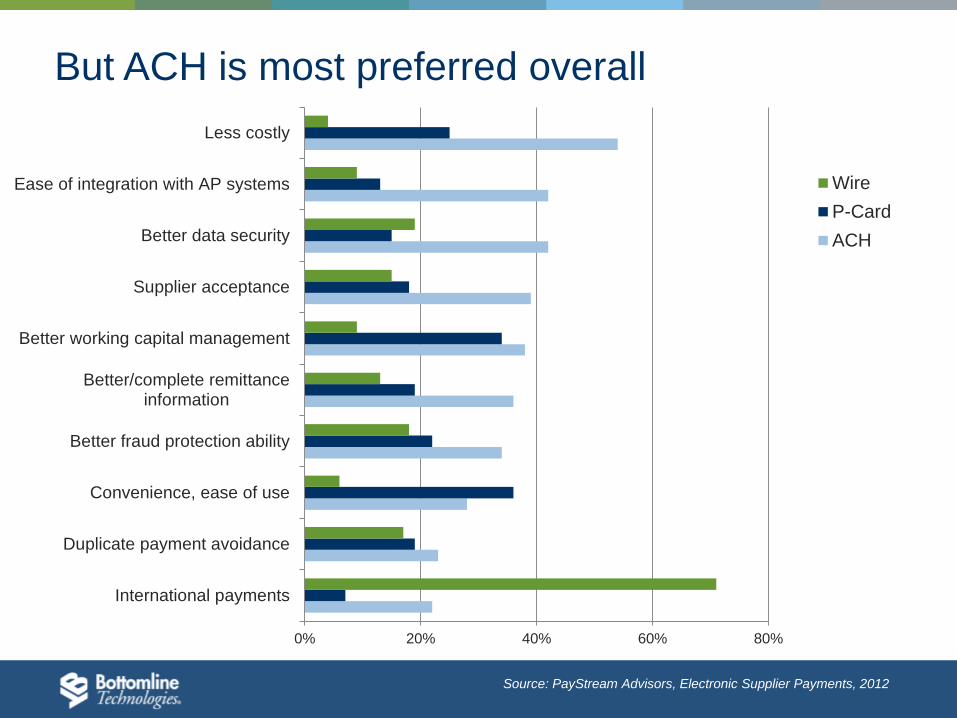

0% 20% 40% 60% 80%

International payments

Duplicate payment avoidance

Convenience, ease of use

Better fraud protection ability

Better/complete remittanceinformation

Better working capital management

Supplier acceptance

Better data security

Ease of integration with AP systems

Less costly

Wire

P-Card

ACH

But ACH is most preferred overall

Source: PayStream Advisors, Electronic Supplier Payments, 2012

Opportunities & Trends in AP

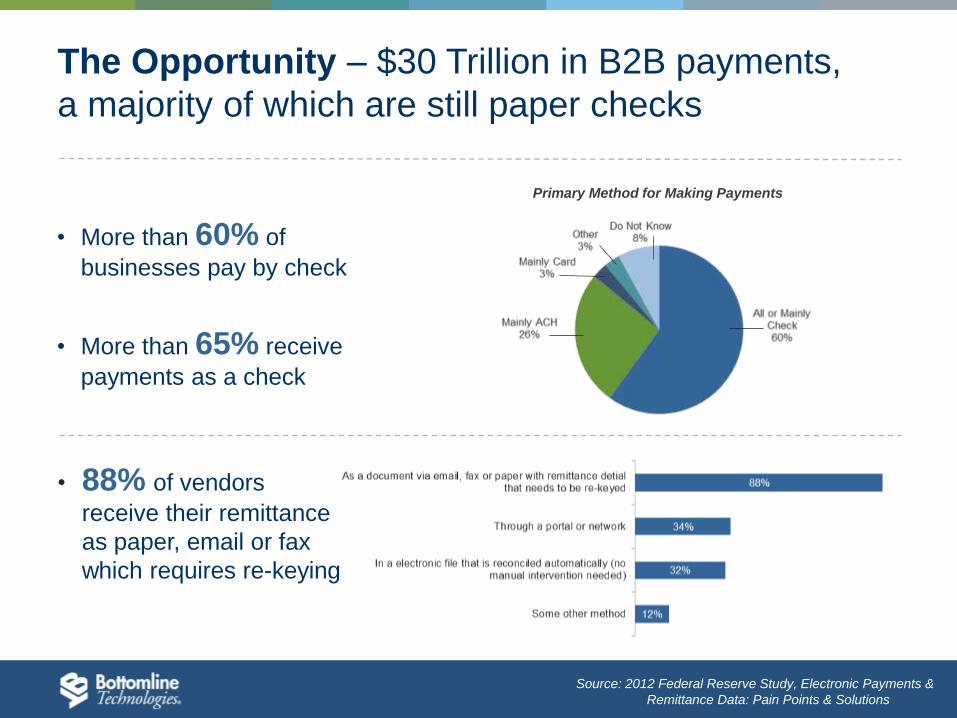

The Opportunity – $30 Trillion in B2B payments,

a majority of which are still paper checks

• More than 60% of

businesses pay by check

• More than 65% receive

payments as a check

Source: 2012 Federal Reserve Study, Electronic Payments &

Remittance Data: Pain Points & Solutions

Primary Method for Making Payments

• 88% of vendors

receive their remittance

as paper, email or fax

which requires re-keying

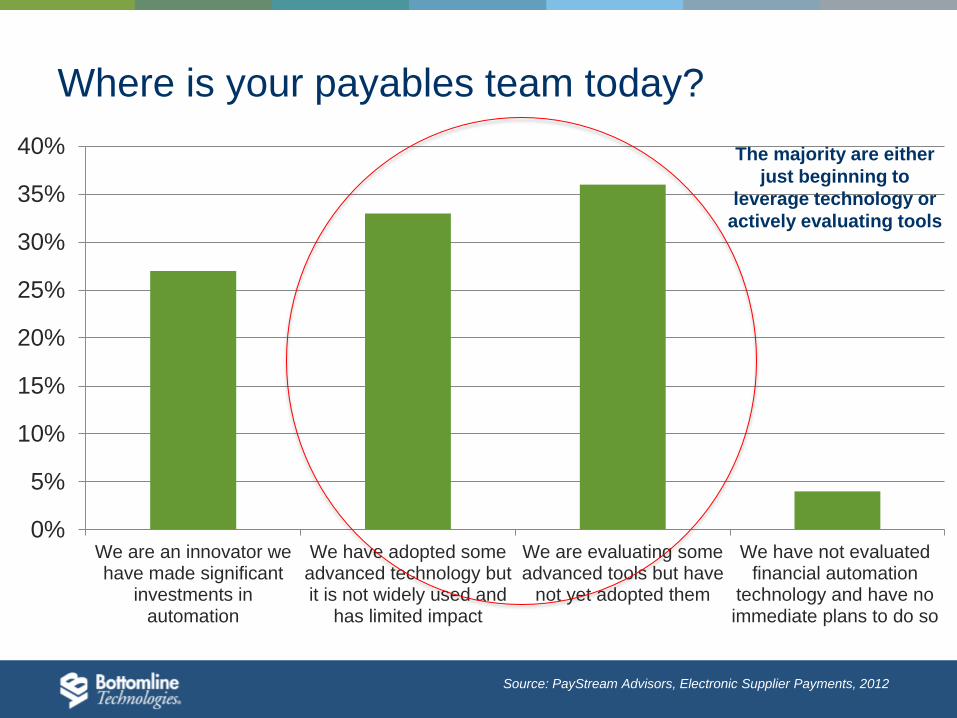

Where is your payables team today?

0%

5%

10%

15%

20%

25%

30%

35%

40%

We are an innovator wehave made significant

investments inautomation

We have adopted someadvanced technology butit is not widely used and

has limited impact

We are evaluating someadvanced tools but have

not yet adopted them

We have not evaluatedfinancial automation

technology and have noimmediate plans to do so

The majority are either

just beginning to

leverage technology or

actively evaluating tools

Source: PayStream Advisors, Electronic Supplier Payments, 2012

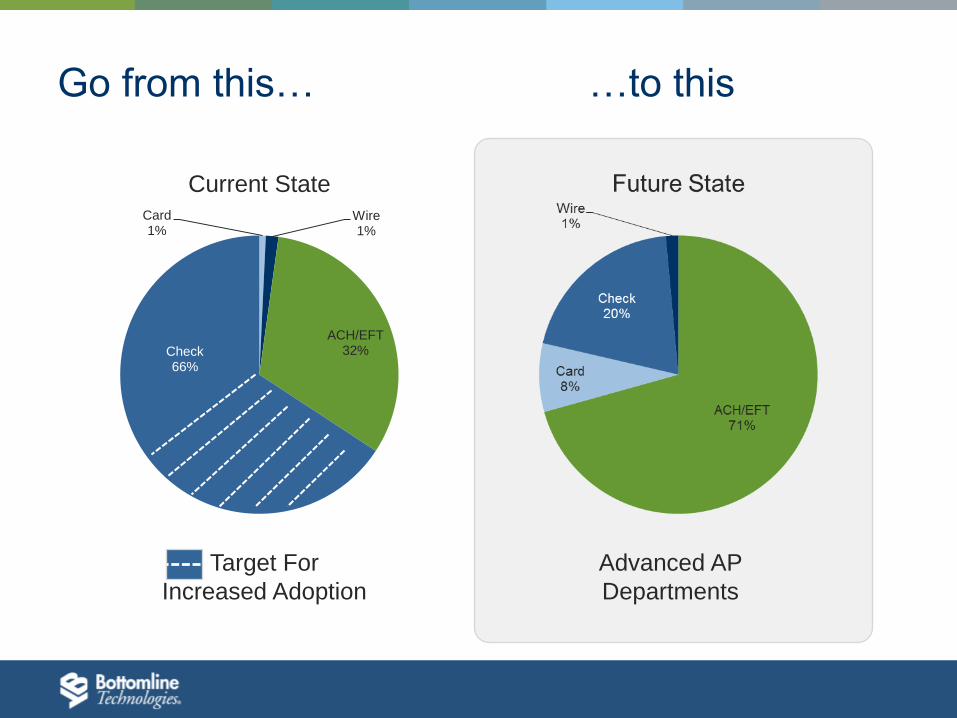

Go from this… …to this

Card 1%

Wire 1%

ACH/EFT 32% Check

66%

Current State

Advanced AP

Departments

Target For

Increased Adoption

Employing a comprehensive payables strategy

is best practice

• One off payments

• Unbanked

• Emergency low dollar payments

• Repetitive payments

• High dollar payments

• International payments

• Payments requiring same day settlement

• Int’l payments if ACH can’t be used

Card ACH/EFT

Wires

• Small, one off payments

• Travel and expense

• Bypass approval process

Checks

Industry trend: AP becomes a profit center

Working Capital

Optimization

Rebates

Discounts Cost-

Savings

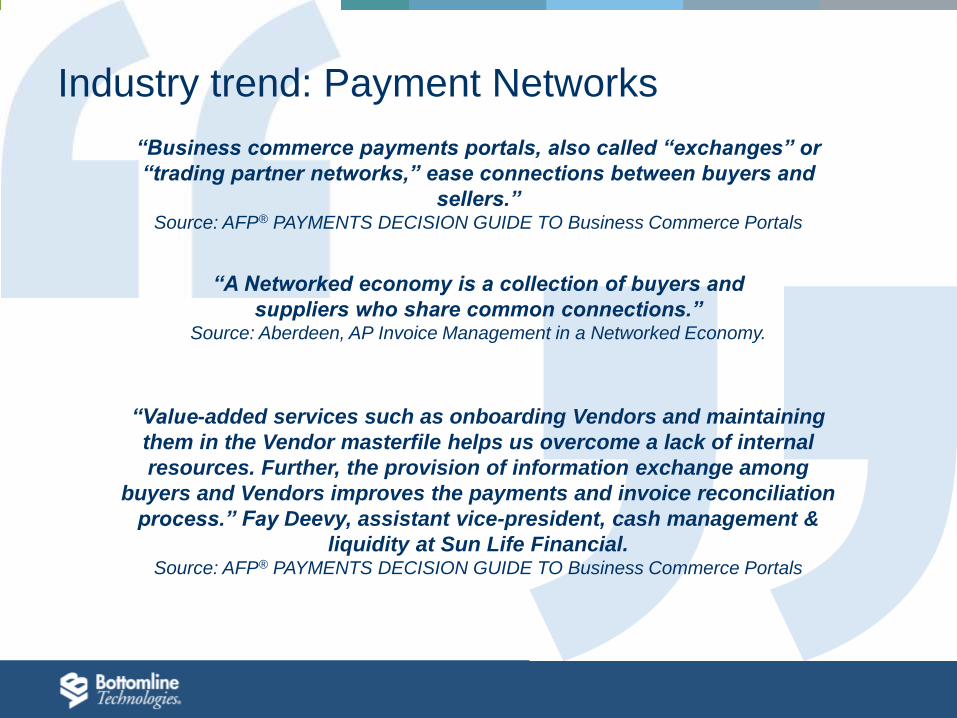

“Business commerce payments portals, also called “exchanges” or

“trading partner networks,” ease connections between buyers and

sellers.” Source: AFP® PAYMENTS DECISION GUIDE TO Business Commerce Portals

“A Networked economy is a collection of buyers and

suppliers who share common connections.” Source: Aberdeen, AP Invoice Management in a Networked Economy.

“Value-added services such as onboarding Vendors and maintaining

them in the Vendor masterfile helps us overcome a lack of internal

resources. Further, the provision of information exchange among

buyers and Vendors improves the payments and invoice reconciliation

process.” Fay Deevy, assistant vice-president, cash management &

liquidity at Sun Life Financial. Source: AFP® PAYMENTS DECISION GUIDE TO Business Commerce Portals

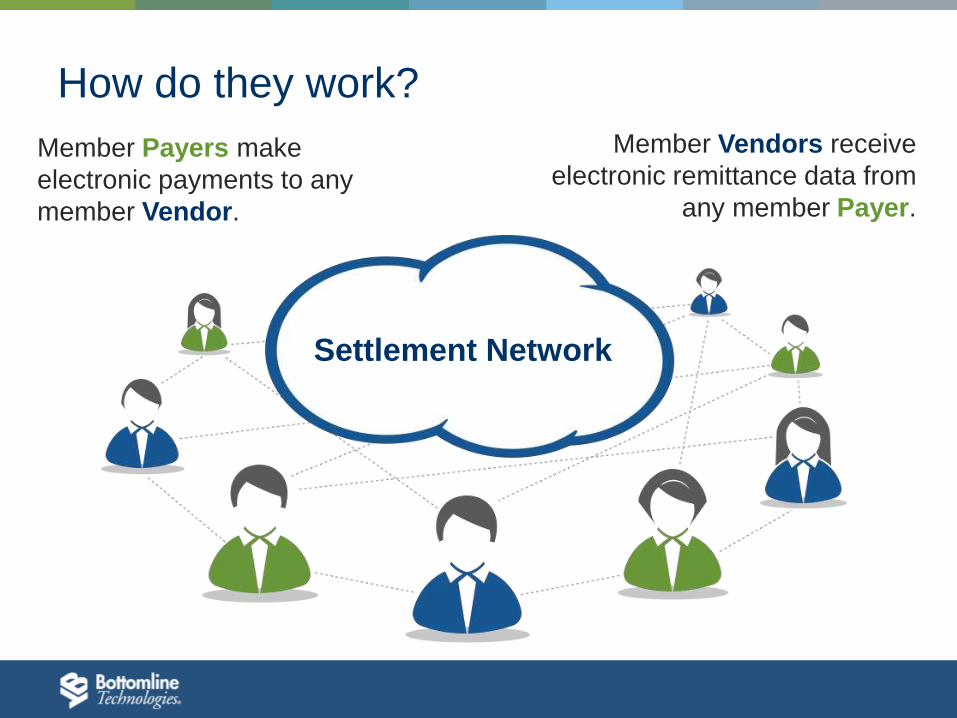

Industry trend: Payment Networks

Member Payers make

electronic payments to any

member Vendor.

Member Vendors receive

electronic remittance data from

any member Payer.

Settlement Network

How do they work?

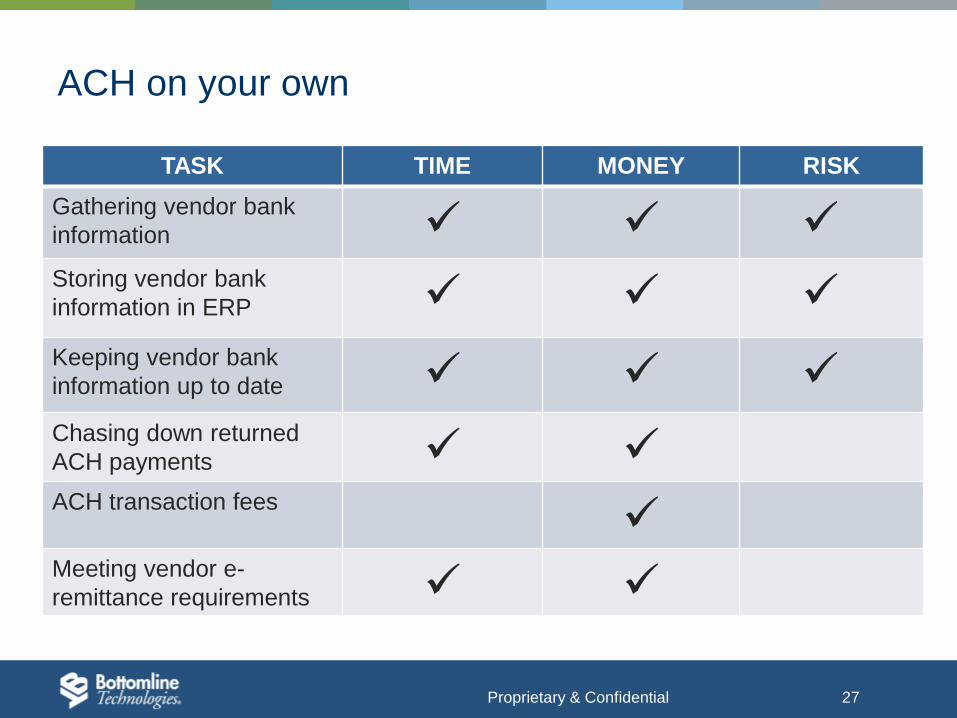

ACH on your own

TASK TIME MONEY RISK

Gathering vendor bank

information Storing vendor bank

information in ERP Keeping vendor bank

information up to date Chasing down returned

ACH payments ACH transaction fees

Meeting vendor e-

remittance requirements

Proprietary & Confidential 27

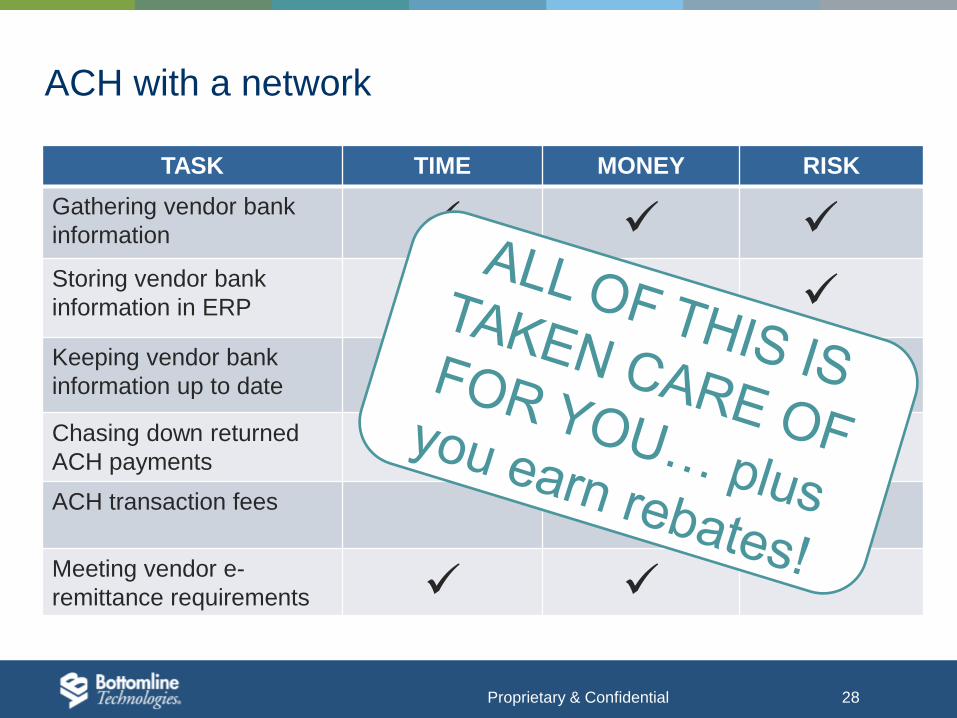

ACH with a network

TASK TIME MONEY RISK

Gathering vendor bank

information Storing vendor bank

information in ERP Keeping vendor bank

information up to date Chasing down returned

ACH payments ACH transaction fees

Meeting vendor e-

remittance requirements

Proprietary & Confidential 28

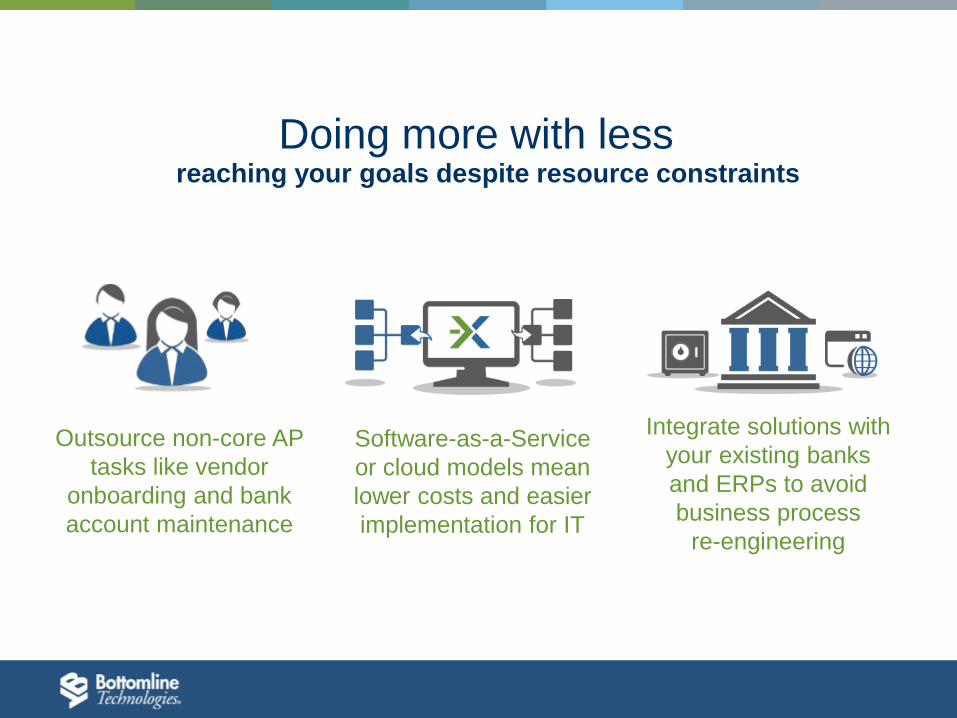

Software-as-a-Service

or cloud models mean

lower costs and easier

implementation for IT

Integrate solutions with

your existing banks

and ERPs to avoid

business process

re-engineering

Outsource non-core AP

tasks like vendor

onboarding and bank

account maintenance

reaching your goals despite resource constraints

Doing more with less

What are network members experiencing?

“Value-added services such as onboarding Vendors

and maintaining them in the Vendor master file

helps us overcome a lack of internal resources.

Further, the provision of information exchange

among Buyers and Vendors improves the payments

and invoice reconciliation process.”

– Fay Deevy, Assistant Vice-President, Cash Management &

Liquidity at Sun Life Financial

Proprietary & Confidential 31

“Eliminating the full time responsibility of housing bank

information and easy installation are things that

attracted us.”

– Mary Clark, Director AP at Glimcher Realty Trust

Proprietary & Confidential 32

Proprietary & Confidential 33

“We had been receiving ACH payments through the network for

a while and knew it to be a valuable service from a vendor’s

perspective. This was a key factor that led us to choosing it as

the means to convert our own AP checks to electronic

payments.

Our vendor onboarding campaign is now under way and is

exactly what we wanted. We’re moving away from paper at a

controlled pace.. it’s very exciting!”

– Shelly Whiting, Director of Accounting at

Compass Minerals

Maximize financial and efficiency gains

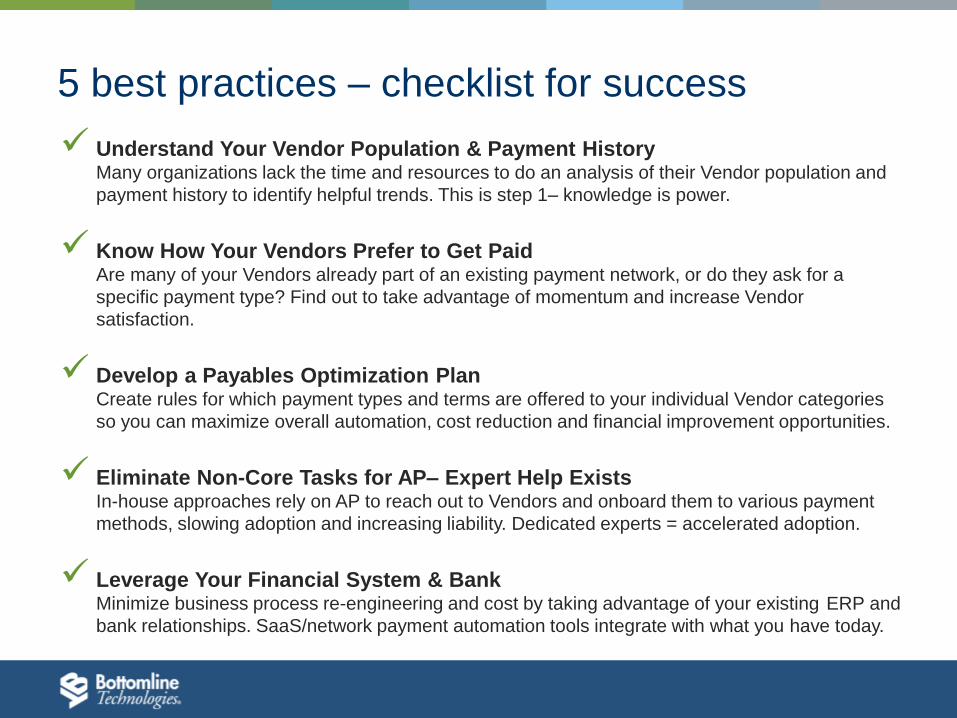

5 best practices – checklist for success

Understand Your Vendor Population & Payment History Many organizations lack the time and resources to do an analysis of their Vendor population and

payment history to identify helpful trends. This is step 1– knowledge is power.

Know How Your Vendors Prefer to Get Paid Are many of your Vendors already part of an existing payment network, or do they ask for a

specific payment type? Find out to take advantage of momentum and increase Vendor

satisfaction.

Develop a Payables Optimization Plan

Create rules for which payment types and terms are offered to your individual Vendor categories

so you can maximize overall automation, cost reduction and financial improvement opportunities.

Eliminate Non-Core Tasks for AP– Expert Help Exists In-house approaches rely on AP to reach out to Vendors and onboard them to various payment

methods, slowing adoption and increasing liability. Dedicated experts = accelerated adoption.

Leverage Your Financial System & Bank

Minimize business process re-engineering and cost by taking advantage of your existing ERP and

bank relationships. SaaS/network payment automation tools integrate with what you have today.

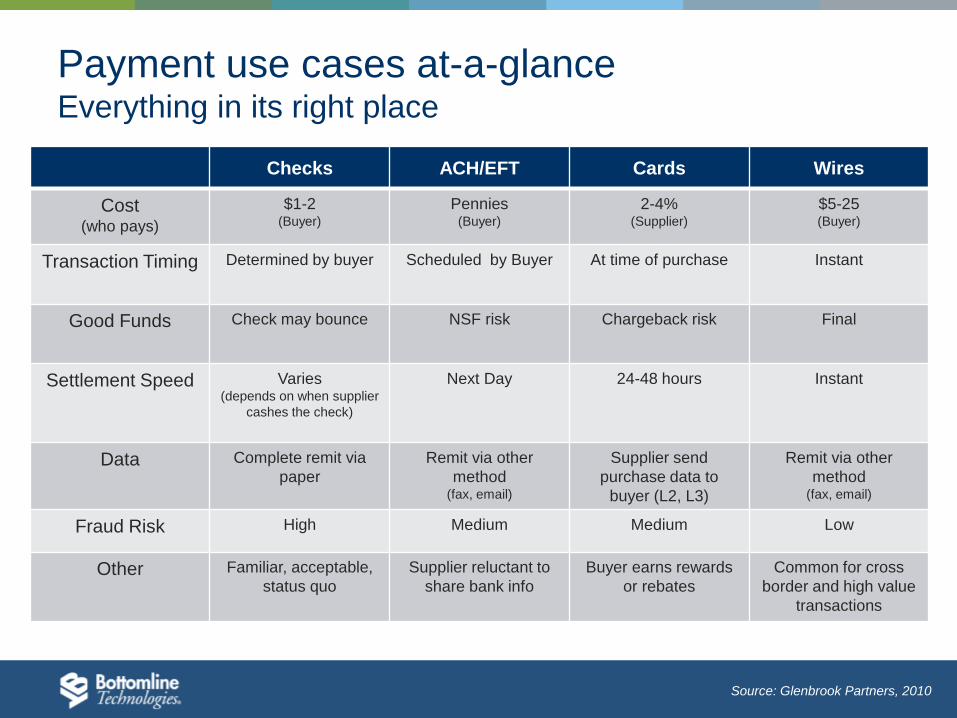

Checks ACH/EFT Cards Wires

Cost (who pays)

$1-2 (Buyer)

Pennies (Buyer)

2-4% (Supplier)

$5-25 (Buyer)

Transaction Timing Determined by buyer Scheduled by Buyer At time of purchase Instant

Good Funds Check may bounce NSF risk Chargeback risk Final

Settlement Speed Varies (depends on when supplier

cashes the check)

Next Day 24-48 hours Instant

Data Complete remit via

paper

Remit via other

method (fax, email)

Supplier send

purchase data to

buyer (L2, L3)

Remit via other

method (fax, email)

Fraud Risk High Medium Medium Low

Other Familiar, acceptable,

status quo

Supplier reluctant to

share bank info

Buyer earns rewards

or rebates

Common for cross

border and high value

transactions

Source: Glenbrook Partners, 2010

Payment use cases at-a-glance Everything in its right place

• Aite Group estimates that

approximately 33% of small

businesses currently bank via a

mobile device

• While an additional 31% are

interested in doing so.

• Approximately 54% will bank

via mobile by 2015.

Keep mobile on your radar

Aite Group, 2012 Small-Business Mobile Banking: A Promising Opportunity

Questions?

Contact information