Embed Size (px)

Citation preview

Optimisation, Avoidance, Tax Evasion

Jean-François BrunGérard Chambas CERDI

Module 8

Introduction

Tax avoidance: unintentional failure to comply with tax obligations (failure to make declarations, etc.) Penalties with interest for late payment (administrative procedure)

Tax evasion: intentional failure to comply with tax rules to reduce the amount of taxes to be paid. Penalties and prosecution

Definition specific to each countryDistinction not always clear between avoidance and evasionFiscal optimization of multinationals: avoidance or evasion?In both cases: loss of revenue

EU Workshop Brussels 2014 2

Outline

I - WHO? People involved in tax evasion

II - WHY? The causes of tax evasion: shortcomings in the collection and gathering of information, controls and sanctions

III - WHAT? Fiscal Optimization: high demand for exemptions and ad hoc measures

IV - HOW? Operational guidelines to reduce tax evasion

EU Workshop Brussels 2014 3

I People involved in avoidance and tax evasion

• Large enterprises (manipulation of the result with transfer price, cost increases such as provisions, optimization)

• Medium-sized companies (often hidden in presumptive regimes, simple evasion methods such as false invoices)

• Liberal professions: declaration of lower amounts and failure to declare

EU Workshop Brussels 2014 4

I forms of avoidance and tax evasion

Other forms of tax evasion (e.g. VAT)

• Absence of declarations

• Submission of implausible declarations to avoid penalties and exploit the lack of reactivity

• Major falsifications (increase of VAT credits, sales without invoices)

EU Workshop Brussels 2014 5

I forms of avoidance and tax evasion

• Multinationals: fraud and optimization difficult to reduce

• Transfer prices

• Location of remuneration abroad (control of exchange)

• Lack of clarity in the mining sector

• Strategic behaviour as regards controls

EU Workshop Brussels 2014 6

What’s happening now with MNCs?

• Source: http://www.tackletaxhavens.com/the-solutions/unitary-tax/

EU Workshop Brussels 2014 7

II The causes of evasion: shortcomings in the gathering of information, controls and sanctions

• Shortcomings in collection and gathering information: connection between customs and tax administrations not operational

• Control programs biased with protected files, lack of transparency, risk analysis methods not implemented

• Incapacity to deal with transfer prices, lack of capacity

• Complexity of mechanisms at play (MNCs)

• Weak and/or non-implemented sanctions

EU Workshop Brussels 2014 8

II A specific factor of tax and customs evasion: corruption

Corruption frequently endemic, favorable to evasion

Evasion feeds corruption

Tangible progress in modern administrations (audits, computerization, automation of procedures, incentives, sanctions, control)

EU Workshop Brussels 2013 9

III Fiscal Optimisation: Challenges

• Exemptions easy to obtain (example, WAEMU has no common investment code)

• Possibility for large businesses to obtain adaptations to tax rules: specific regimes via conventions

• Use of complex mechanisms by MNCs, e.g. Ghana, SABMiller (Brewer) paid zero tax on profits for the period 2008-2010

• Google, average tax rate: 2.4% (double Irish Dutch sandwich, etc.)

• Developing countries defenceless

EU Workshop Brussels 2014 10

IV Operational guidelines for the reduction of evasion

• Use of legislation in tax code and procedures with automaticity and transparency

• Incentives must be in common law

• Ethics and transparency

• Computerization

• Simplified tax

• Modern administrative organization

• Civic education and communication

• Global fight against corruption

• Country by country reporting (CBCR)

EU Workshop Brussels 2014 11

IV Operational guidelines for the reduction of evasion

Transfer prices - definition

•“The price at which an enterprise transfers physical assets, intangible assets or provides services to affiliated enterprises” according to the OECD - import-export within the same group

•World trade: 1/3 is intra-company trade

•Provision of services concerned (administration costs, headquarters costs, royalties on patents or brands, etc.)

•Arm’s length principle

•Fixing transfer price affects the tax base of the countries concerned

EU Workshop Brussels 2014 12

IV Operational guidelines for the reduction of evasion

Transfer prices - the disadvantages

•System very favorable for MNCs

•Favors complex tax evasion or avoidance mechanisms and procedures (Google, etc.)

•Separate entities favorable to tax evasion and tax avoidance (Amazon UK, etc.)

•Major loss of revenue for states

•Difficult to eliminate. Comparability of data is a problem

•Need for dialogue between the tax administrations of different countries and capacity building in developing countries' revenue administrations

EU Workshop Brussels 2014 13

IV Operational guidelines for the reduction of evasion

The Need for Coordinated Global Action on Resource Transparency

• Crucial to ensure a level playing field for all companies in the industry

• Enhancing transparency on taxation, one of the key priorities during Britain's term as presidency of G8 group

• Important that also resource-rich developing countries are involved to implement disclosure requirements and support transparency in their national extractive industries.

• The Dodd Frank Act of 2009 in the US, requires large US and foreign oil, gas and mining companies listed on the US stock exchange to report payments on a project-by-project and country-by-country level.

EU Workshop Brussels 201414

IV Operational guidelines for the reduction of evasion

EU efforts to fight against tax evasion

•The 2012 Communication on “An Action Plan to strengthen the fight against tax fraud and tax evasion” with an action plan for 2013 & 2014

•The EU agreed on 9 April 2013 on a Country-by-Country Reporting (CBCR) for oil, gas and mining and forestry sectors

•The EU proposal goes further than the US legislation in that it also targets large non-listed companies, as well as loggers of primary forests.

EU Workshop Brussels 2014 15

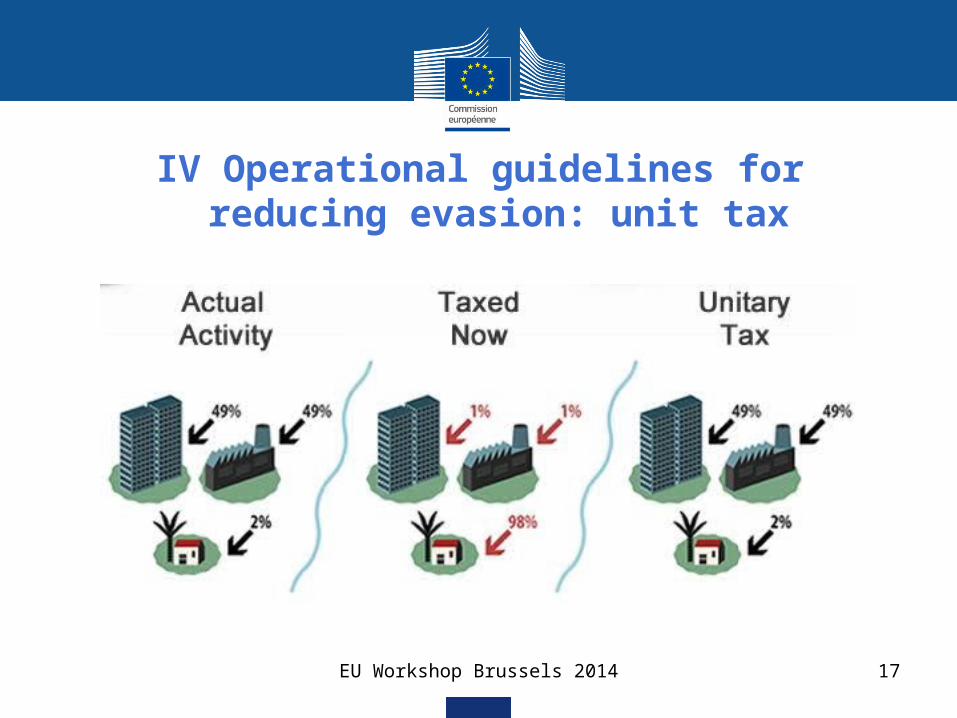

IV Operational guidelines for reducing evasion: unit tax

Unit tax - the principle

•The profit generated by the company considered as a whole (global profit)

•Does not seek to identify what amount of profit comes from which entity

•Global profit is apportioned according to a formula that takes account of the actual activity in different locations

•Taxation must be paid to the places where the profit is generated

•Formula based on actual indicators (employees, installed capital, etc.)

•SimplificationEU Workshop Brussels 2014 16

IV Operational guidelines for reducing evasion: unit tax

EU Workshop Brussels 2014 17

IV Operational guidelines for the reduction of evasion

Unit tax - the advantages•No need:

• to closely examine the internal accounts in detail, prices used• to negotiate adjustments based on the ALP• to examine “diversion” of profits, in particular, complex

techniques to place them into tax heavens.• to define rules of residence and source of profit

•Simplification for tax administration and entities subject to tax

EU Workshop Brussels 2014 18

Initiatives for transparency concerning revenue derived from natural resources (1)

The Extracting Industries Transparency Initiative (EITI) •Based on the willingness of countries to report (oil, gas, mines) but participation becomes mandatory (private - public) if the country adopts the initiative.

•Data per enterprise, per category of taxes (see below)

•Willingness to give a global vision of countries participating (summary report)

•23 countries applying the EITI, and 16 candidate countries in 2013, still few resource-rich countries

•Natural Resources Charter (NRC) establishes principles for better management – Revenue Watch Institute (RWI)

EU Workshop Brussels 2014 19

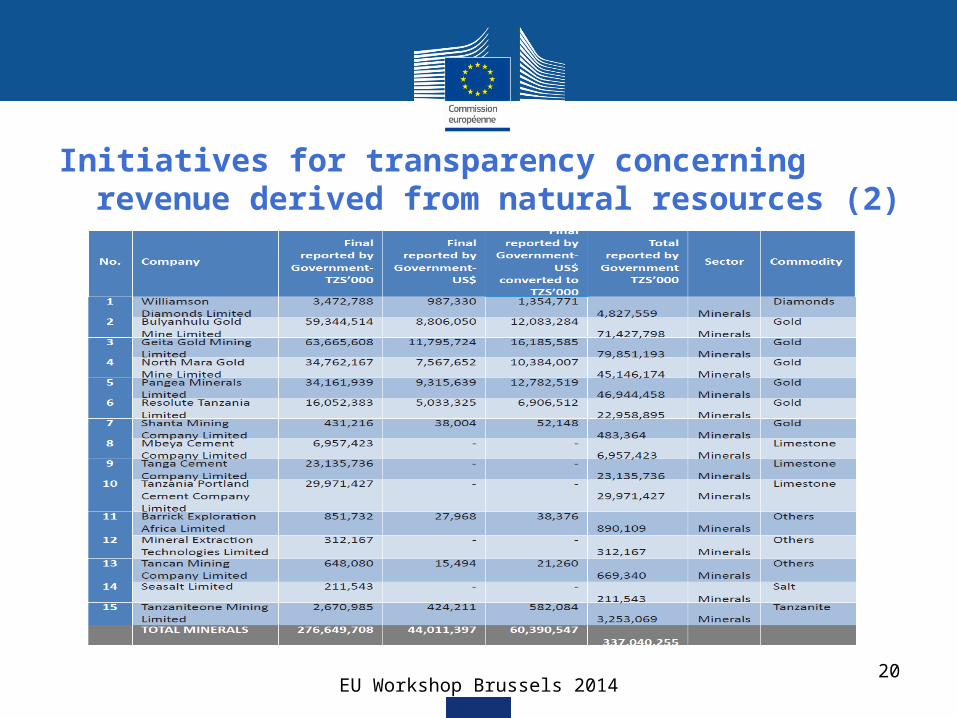

Initiatives for transparency concerning revenue derived from natural resources (2)

EU Workshop Brussels 201420

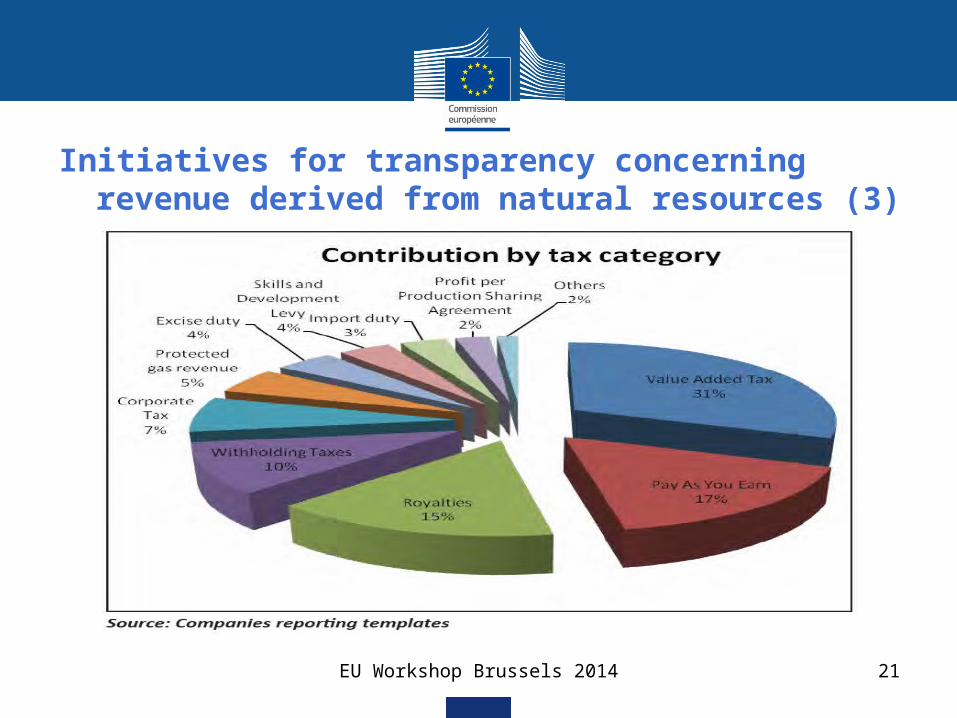

Initiatives for transparency concerning revenue derived from natural resources (3)

EU Workshop Brussels 2014 21

•Thank you for your attention

EU Workshop Brussels 2014 22