Embed Size (px)

Citation preview

../ucsbwave-cmyk.png

1

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Optimal Execution with Dynamic Order FlowImbalance

Kyle Bechler

UC Santa Barbara

WCMFSeptember 27, 2014

joint w/Mike Ludkovski

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

1

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Outline

1 Order Flow

2 Dynamic Order Flow Model

3 Two-Step Approximation

4 Numerical Illustrations

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

2

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Tale of Two Costs

When executing a large order in an electronic market, there are twoprimary concerns:

1 Price ImpactSpatial effect: consume liquidity in terms of standing limit orders“Walking through the book” – receive worse price than currentbest bid/ask

2 Information LeakageTemporal effect: executed trade appears on the order tapeOther traders react and adjust their behavior (eg “front-running”) –will receive worse price in the future

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

2

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Tale of Two Costs

When executing a large order in an electronic market, there are twoprimary concerns:

1 Price ImpactSpatial effect: consume liquidity in terms of standing limit orders“Walking through the book” – receive worse price than currentbest bid/ask

2 Information LeakageTemporal effect: executed trade appears on the order tapeOther traders react and adjust their behavior (eg “front-running”) –will receive worse price in the future

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

3

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

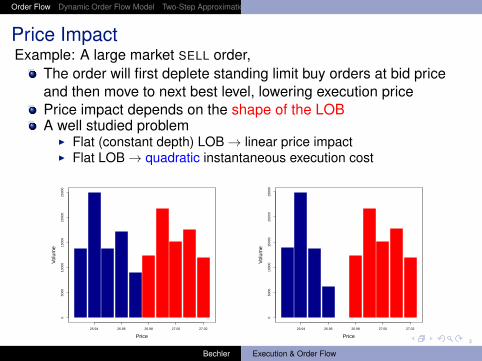

Price ImpactExample: A large market SELL order,

The order will first deplete standing limit buy orders at bid priceand then move to next best level, lowering execution pricePrice impact depends on the shape of the LOBA well studied problem

I Flat (constant depth) LOB→ linear price impactI Flat LOB→ quadratic instantaneous execution cost

26.94 26.96 26.98 27.00 27.02

050

0010

000

1500

020

000

2500

0

Price

Vol

ume

26.94 26.96 26.98 27.00 27.02

050

0010

000

1500

020

000

2500

0

Price

Vol

ume

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

4

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Information Leakage

Longer term impact causing others to behave differently (iepermanent market impact)Once other traders are aware of somebody selling, they will takeadvantageAdverse selection, predatory trading, etc.Algorithm should do the following:

I Attempt to hide overall intentionsI Consider the state of the liquidity provision process

Information cost requires looking at time series of orders

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

4

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Information Leakage

Longer term impact causing others to behave differently (iepermanent market impact)Once other traders are aware of somebody selling, they will takeadvantageAdverse selection, predatory trading, etc.Algorithm should do the following:

I Attempt to hide overall intentionsI Consider the state of the liquidity provision process

Information cost requires looking at time series of orders

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

5

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Order Flow

Participants fear that other traders are better informed⇒ When order flow is toxic market makers provide less liquidity

Toxicity is about the ratio of noise/informed traders, aka flowimbalance (NOT the same as static/volume LOB order imbalance)Not directly observable, and not obvious how to measure

Economics: VPIN by Easley, Lopez de Prado, O’Hara (2012abcd)(patented; http://en.wikipedia.org/wiki/Talk:VPIN)

I VPIN has a complicated way of classifying trades as buys/sells. Notsuitable for LOB data

I Claim: MMs widen spreads in response to toxic flowFinMath: Cartea, Jaimungal, Ricci (2011)

I Short term price drift driven by market order arrivalsI Result: MMs shift order placement when market order flow is

one-sided

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

5

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Order Flow

Participants fear that other traders are better informed⇒ When order flow is toxic market makers provide less liquidity

Toxicity is about the ratio of noise/informed traders, aka flowimbalance (NOT the same as static/volume LOB order imbalance)Not directly observable, and not obvious how to measureEconomics: VPIN by Easley, Lopez de Prado, O’Hara (2012abcd)(patented; http://en.wikipedia.org/wiki/Talk:VPIN)

I VPIN has a complicated way of classifying trades as buys/sells. Notsuitable for LOB data

I Claim: MMs widen spreads in response to toxic flow

FinMath: Cartea, Jaimungal, Ricci (2011)I Short term price drift driven by market order arrivalsI Result: MMs shift order placement when market order flow is

one-sided

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

5

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Order Flow

Participants fear that other traders are better informed⇒ When order flow is toxic market makers provide less liquidity

Toxicity is about the ratio of noise/informed traders, aka flowimbalance (NOT the same as static/volume LOB order imbalance)Not directly observable, and not obvious how to measureEconomics: VPIN by Easley, Lopez de Prado, O’Hara (2012abcd)(patented; http://en.wikipedia.org/wiki/Talk:VPIN)

I VPIN has a complicated way of classifying trades as buys/sells. Notsuitable for LOB data

I Claim: MMs widen spreads in response to toxic flowFinMath: Cartea, Jaimungal, Ricci (2011)

I Short term price drift driven by market order arrivalsI Result: MMs shift order placement when market order flow is

one-sided

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

6

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

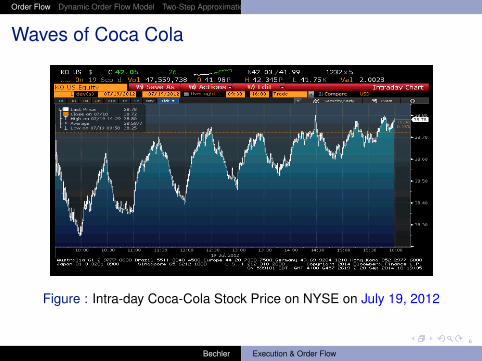

Waves of Coca Cola

Figure : Intra-day Coca-Cola Stock Price on NYSE on July 19, 2012

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

7

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Direction

ELO12: Flow imbalance, info leakage and optimal horizonI Static, one-period model

Aim: Incorporate concepts in a dynamic optimal executionframework

I Continuous trading rates (Almgren-Chriss,...)I Assume a parametric form for inventory risk (A-C, Gatheral-Schied)I No fill risk (in contrast to Cartea & Jaimungal, Gueant et al,

Bayraktar-L, ... )I Treat only market orders (in the future: hybrid models like in

Guilbaud & Pham, Carmona & Webster, ... )I (Order book resilience (Obizhaeva & Wang, Alfonsi et al))I (Empirical evidence: Farmer, Bouchaud, ... )

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

7

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Direction

ELO12: Flow imbalance, info leakage and optimal horizonI Static, one-period model

Aim: Incorporate concepts in a dynamic optimal executionframework

I Continuous trading rates (Almgren-Chriss,...)I Assume a parametric form for inventory risk (A-C, Gatheral-Schied)I No fill risk (in contrast to Cartea & Jaimungal, Gueant et al,

Bayraktar-L, ... )I Treat only market orders (in the future: hybrid models like in

Guilbaud & Pham, Carmona & Webster, ... )I (Order book resilience (Obizhaeva & Wang, Alfonsi et al))I (Empirical evidence: Farmer, Bouchaud, ... )

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

7

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Direction

ELO12: Flow imbalance, info leakage and optimal horizonI Static, one-period model

Aim: Incorporate concepts in a dynamic optimal executionframework

I Continuous trading rates (Almgren-Chriss,...)I Assume a parametric form for inventory risk (A-C, Gatheral-Schied)I No fill risk (in contrast to Cartea & Jaimungal, Gueant et al,

Bayraktar-L, ... )I Treat only market orders (in the future: hybrid models like in

Guilbaud & Pham, Carmona & Webster, ... )I (Order book resilience (Obizhaeva & Wang, Alfonsi et al))I (Empirical evidence: Farmer, Bouchaud, ... )

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

8

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Contributions

Introduce order flow imbalance as a state variableSuggest a simple mechanism for informational costs (inspired byELO12) – temporal impact beyond usual spatial impactEndogenize the execution horizon TDerive closed-form approximate strategies for the resultingoptimization problem

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

9

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Execution Model

Inventory xt : liquidate x0

t 7→ xt is absolutely continuous; trading rate is αt

dxt = −αtdtUnaffected price St : martingale

Order flow imbalance Yt

Yt > 0: buyers-market; Yt < 0: sellers marketMain desired features:

I Mean-reverting to zeroI Stationary in long-runI Affected by execution algorithms

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

9

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Execution Model

Inventory xt : liquidate x0

t 7→ xt is absolutely continuous; trading rate is αt

dxt = −αtdtUnaffected price St : martingaleOrder flow imbalance Yt

Yt > 0: buyers-market; Yt < 0: sellers marketMain desired features:

I Mean-reverting to zeroI Stationary in long-runI Affected by execution algorithms

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

10

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Unaffected order flow: dY 0t = −βY 0

t dt + σ dWt

With execution:

dYt = (−βYt − φ(αt))dt + σ dWt

i.e. Yt = Y 0t +

∫ t0 e−β(t−s)αsds

Typical cases:I φ(α) = φt (deterministic information cost)I φ(α) = ηα (linear in trading rate)

Assume that flow is independent of price (empirical relationship isnot clear) - more on this later

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

11

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

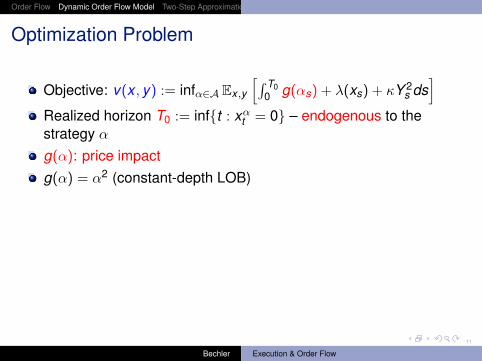

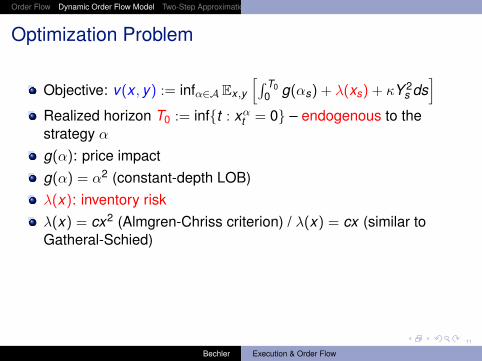

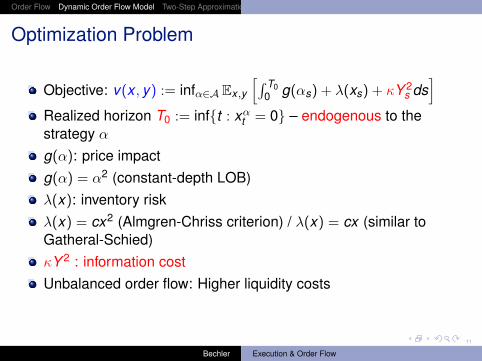

Optimization Problem

Objective: v(x , y) := infα∈A Ex ,y

[∫ T00 g(αs) + λ(xs) + κY 2

s ds]

Realized horizon T0 := inf{t : xαt = 0} – endogenous to thestrategy α

g(α): price impact

g(α) = α2 (constant-depth LOB)

λ(x): inventory risk

λ(x) = cx2 (Almgren-Chriss criterion) / λ(x) = cx (similar toGatheral-Schied)

κY 2 : information cost

Unbalanced order flow: Higher liquidity costs

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

11

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Optimization Problem

Objective: v(x , y) := infα∈A Ex ,y

[∫ T00 g(αs) + λ(xs) + κY 2

s ds]

Realized horizon T0 := inf{t : xαt = 0} – endogenous to thestrategy αg(α): price impactg(α) = α2 (constant-depth LOB)

λ(x): inventory risk

λ(x) = cx2 (Almgren-Chriss criterion) / λ(x) = cx (similar toGatheral-Schied)

κY 2 : information cost

Unbalanced order flow: Higher liquidity costs

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

11

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Optimization Problem

Objective: v(x , y) := infα∈A Ex ,y

[∫ T00 g(αs) + λ(xs) + κY 2

s ds]

Realized horizon T0 := inf{t : xαt = 0} – endogenous to thestrategy αg(α): price impactg(α) = α2 (constant-depth LOB)λ(x): inventory riskλ(x) = cx2 (Almgren-Chriss criterion) / λ(x) = cx (similar toGatheral-Schied)

κY 2 : information cost

Unbalanced order flow: Higher liquidity costs

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

11

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Optimization Problem

Objective: v(x , y) := infα∈A Ex ,y

[∫ T00 g(αs) + λ(xs) + κY 2

s ds]

Realized horizon T0 := inf{t : xαt = 0} – endogenous to thestrategy αg(α): price impactg(α) = α2 (constant-depth LOB)λ(x): inventory riskλ(x) = cx2 (Almgren-Chriss criterion) / λ(x) = cx (similar toGatheral-Schied)κY 2 : information costUnbalanced order flow: Higher liquidity costs

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

12

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

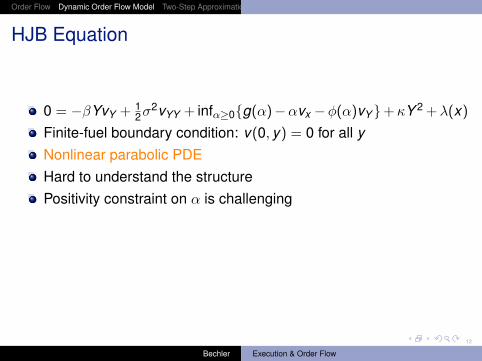

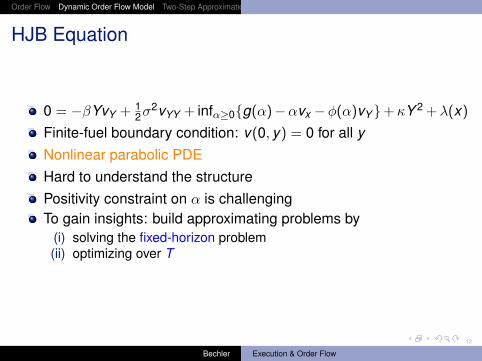

HJB Equation

0 = −βYvY + 12σ

2vYY + infα≥0{g(α)−αvx −φ(α)vY}+κY 2 +λ(x)Finite-fuel boundary condition: v(0, y) = 0 for all yNonlinear parabolic PDEHard to understand the structurePositivity constraint on α is challenging

To gain insights: build approximating problems by(i) solving the fixed-horizon problem(ii) optimizing over T

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

12

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

HJB Equation

0 = −βYvY + 12σ

2vYY + infα≥0{g(α)−αvx −φ(α)vY}+κY 2 +λ(x)Finite-fuel boundary condition: v(0, y) = 0 for all yNonlinear parabolic PDEHard to understand the structurePositivity constraint on α is challengingTo gain insights: build approximating problems by

(i) solving the fixed-horizon problem(ii) optimizing over T

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

13

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

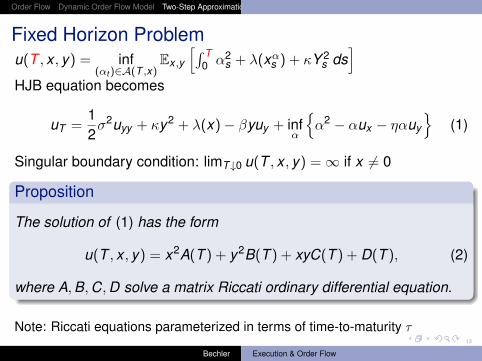

Fixed Horizon Problemu(T , x , y) = inf

(αt )∈A(T ,x)Ex ,y

[∫ T0 α2

s + λ(xαs ) + κY 2s ds

]HJB equation becomes

uT =12σ2uyy + κy2 + λ(x)− βyuy + inf

α

{α2 − αux − ηαuy

}(1)

Singular boundary condition: limT↓0 u(T , x , y) =∞ if x 6= 0

Proposition

The solution of (1) has the form

u(T , x , y) = x2A(T ) + y2B(T ) + xyC(T ) + D(T ), (2)

where A,B,C,D solve a matrix Riccati ordinary differential equation.

Note: Riccati equations parameterized in terms of time-to-maturity τ

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

14

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

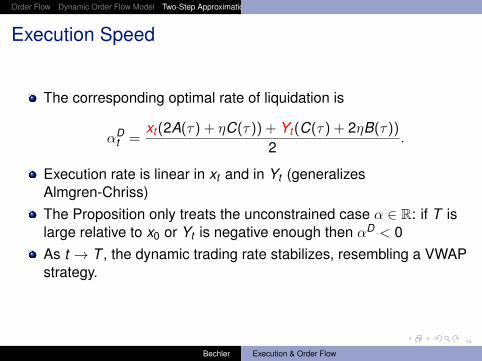

Execution Speed

The corresponding optimal rate of liquidation is

αDt =

xt(2A(τ) + ηC(τ)) + Yt(C(τ) + 2ηB(τ))

2.

Execution rate is linear in xt and in Yt (generalizesAlmgren-Chriss)The Proposition only treats the unconstrained case α ∈ R: if T islarge relative to x0 or Yt is negative enough then αD < 0As t → T , the dynamic trading rate stabilizes, resembling a VWAPstrategy.

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

15

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

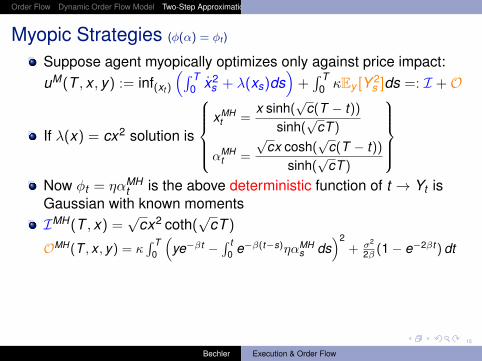

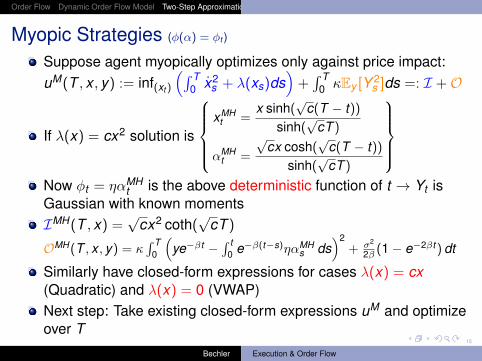

Myopic Strategies (φ(α) = φt )

Suppose agent myopically optimizes only against price impact:uM(T , x , y) := inf(xt )

(∫ T0 x2

s + λ(xs)ds)+∫ T

0 κEy [Y 2s ]ds =: I +O

If λ(x) = cx2 solution is

xMH

t =x sinh(

√c(T − t))

sinh(√

cT )

αMHt =

√cx cosh(

√c(T − t))

sinh(√

cT )

Now φt = ηαMH

t is the above deterministic function of t → Yt isGaussian with known momentsIMH(T , x) =

√cx2 coth(

√cT )

OMH(T , x , y) = κ∫ T

0

(ye−βt −

∫ t0 e−β(t−s)ηαMH

s ds)2

+ σ2

2β (1− e−2βt)dt

Similarly have closed-form expressions for cases λ(x) = cx(Quadratic) and λ(x) = 0 (VWAP)Next step: Take existing closed-form expressions uM and optimizeover T

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

15

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Myopic Strategies (φ(α) = φt )

Suppose agent myopically optimizes only against price impact:uM(T , x , y) := inf(xt )

(∫ T0 x2

s + λ(xs)ds)+∫ T

0 κEy [Y 2s ]ds =: I +O

If λ(x) = cx2 solution is

xMH

t =x sinh(

√c(T − t))

sinh(√

cT )

αMHt =

√cx cosh(

√c(T − t))

sinh(√

cT )

Now φt = ηαMH

t is the above deterministic function of t → Yt isGaussian with known momentsIMH(T , x) =

√cx2 coth(

√cT )

OMH(T , x , y) = κ∫ T

0

(ye−βt −

∫ t0 e−β(t−s)ηαMH

s ds)2

+ σ2

2β (1− e−2βt)dt

Similarly have closed-form expressions for cases λ(x) = cx(Quadratic) and λ(x) = 0 (VWAP)Next step: Take existing closed-form expressions uM and optimizeover T

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

16

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

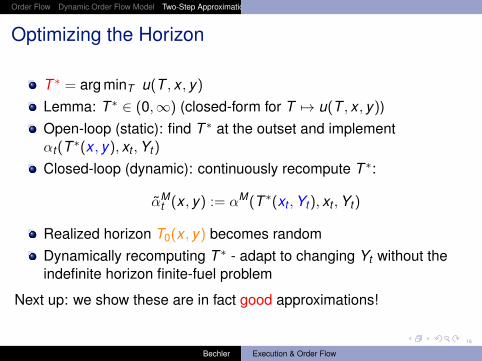

Optimizing the Horizon

T ∗ = arg minT u(T , x , y)Lemma: T ∗ ∈ (0,∞) (closed-form for T 7→ u(T , x , y))Open-loop (static): find T ∗ at the outset and implementαt(T ∗(x , y), xt ,Yt)

Closed-loop (dynamic): continuously recompute T ∗:

αMt (x , y) := αM(T ∗(xt ,Yt), xt ,Yt)

Realized horizon T0(x , y) becomes randomDynamically recomputing T ∗ - adapt to changing Yt without theindefinite horizon finite-fuel problem

Next up: we show these are in fact good approximations!

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

16

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Optimizing the Horizon

T ∗ = arg minT u(T , x , y)Lemma: T ∗ ∈ (0,∞) (closed-form for T 7→ u(T , x , y))Open-loop (static): find T ∗ at the outset and implementαt(T ∗(x , y), xt ,Yt)

Closed-loop (dynamic): continuously recompute T ∗:

αMt (x , y) := αM(T ∗(xt ,Yt), xt ,Yt)

Realized horizon T0(x , y) becomes randomDynamically recomputing T ∗ - adapt to changing Yt without theindefinite horizon finite-fuel problem

Next up: we show these are in fact good approximations!

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

17

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

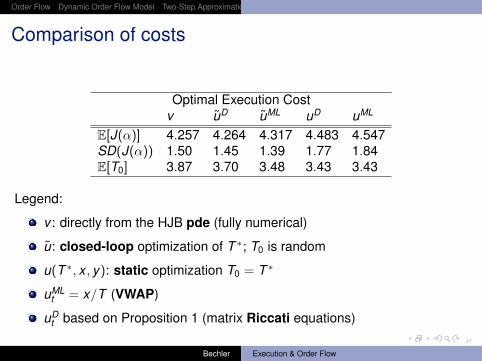

Comparison of costs

Optimal Execution Costv uD uML uD uML

E[J(α)] 4.257 4.264 4.317 4.483 4.547SD(J(α)) 1.50 1.45 1.39 1.77 1.84E[T0] 3.87 3.70 3.48 3.43 3.43

Legend:

v : directly from the HJB pde (fully numerical)

u: closed-loop optimization of T ∗; T0 is random

u(T ∗, x , y): static optimization T0 = T ∗

uMLt = x/T (VWAP)

uDt based on Proposition 1 (matrix Riccati equations)

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

18

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

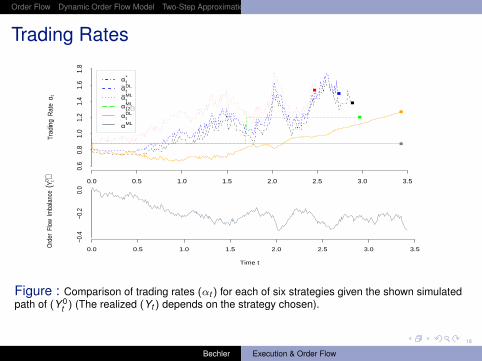

Trading Rates

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Trad

ing

Rat

e α

t

αt*

α~tDL

α~tML

α(2)ML

αtDL

αML

0.6

0.8

1.0

1.2

1.4

1.6

1.8

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Time t

Ord

er F

low

Imba

lanc

e (Y

t0 )

−0.4

−0.2

0.0

Figure : Comparison of trading rates (αt ) for each of six strategies given the shown simulatedpath of (Y 0

t ) (The realized (Yt ) depends on the strategy chosen).

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

19

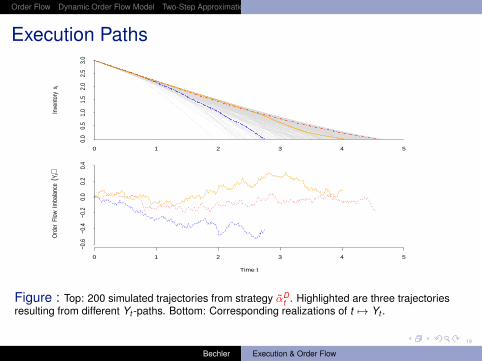

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Execution PathsIn

vent

ory

x t

0 1 2 3 4 5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0 1 2 3 4 5

Time t

Ord

er F

low

Imba

lanc

e (Y

t)

−0.6

−0.4

−0.2

0.0

0.2

0.4

Figure : Top: 200 simulated trajectories from strategy αDt . Highlighted are three trajectories

resulting from different Yt -paths. Bottom: Corresponding realizations of t 7→ Yt .

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

20

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

More on Static T ∗ (Optimal Execution Horizon byELO12)

ELO12 (essentially) considered minT≥0{Ex ,y [|YαT |] + c

√T}

⇒ myopic trading based on constant participation strategy αt = x/T ;explicit timing costs (rather than inventory risk)Only terminal information costs |YT |Discuss the statically optimized T ∗ aboveOur setup is effectively a dynamic extension of the aboveone-period model

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

21

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Work in Progress

http://arxiv.org/abs/1409.2618

Empirical measurement of order flow and its stylized featuresAt what time-scale is order flow imbalance to be measured?Perhaps information leakage φ(α) depends on Yt?Consider correlated St and Yt

Thank You!

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

21

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

Work in Progress

http://arxiv.org/abs/1409.2618

Empirical measurement of order flow and its stylized featuresAt what time-scale is order flow imbalance to be measured?Perhaps information leakage φ(α) depends on Yt?Consider correlated St and Yt

Thank You!

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

22

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

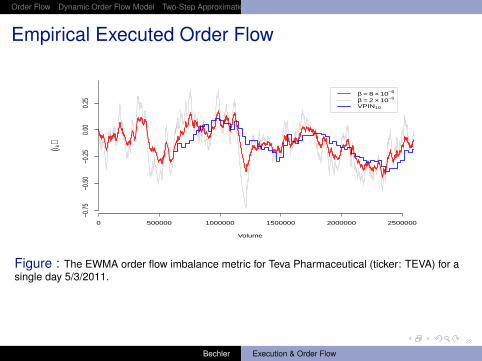

Empirical Executed Order Flow

0 500000 1000000 1500000 2000000 2500000

Volume

(I k)

−0.7

5−0

.50

−0.2

50.

000.

25β = 8 × 10−6

β = 2 × 10−5

VPIN10

Figure : The EWMA order flow imbalance metric for Teva Pharmaceutical (ticker: TEVA) for asingle day 5/3/2011.

Bechler Execution & Order Flow

../ucsbwave-cmyk.png

23

Order Flow Dynamic Order Flow Model Two-Step Approximation Numerical Illustrations

References

R. Cont, A. Kukanov and S. StoikovThe price impact of order book eventshttp://papers.ssrn.com/sol3/papers.cfm?abstract_id=1712822 (2012)

D. Easley, M. López de Prado and M. O’HaraFlow Toxicity and Liquidity in a High Frequency WorldReview of Financial Studies, (2012) 25, 1457–1493.

D. Easley, M. López de Prado and M. O’HaraOptimal Execution Horizonhttp://papers.ssrn.com/sol3/papers.cfm?abstract_id=2038387 (2012)

J. Gatheral and A. SchiedDynamical models of market impact and algorithms for order executionhttp://papers.ssrn.com/sol3/papers.cfm?abstract_id=2034178 (2013)

A. Cartea, S. Jaimungal and J. RicciBuy low sell high: a high frequency trading perspectivehttp://papers.ssrn.com/sol3/papers.cfm?abstract_id=1964781 (2011)

Bechler Execution & Order Flow