Embed Size (px)

Citation preview

Opportunities for the fermentation-based chemical industry

Dr. Willem Vaessen,

Chemicals Segment Leader, Deloitte NL

Hannover, 8th September 2016

An analysis of the market potential and competitiveness of North-West Europe

The full study is available on the website of Deloitte. The study was carried out by Deloitte and sponsored by Rabobank and other partners. Some selected data is used with the kind permission from LMC International

© 2015 Deloitte The Netherlands

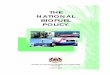

Chemicals derived from cane, beet, corn, tapioca, and wheat through fermentation are the primary focus on this study

1 2016-09-08 Fermentation Study Summary - Hannover

Note: Excludes streams of co-products

Primary focus is chemicals andbioethanol (fuel) is secondary

Sources (crops)

Feedstock(sugars and

starches)

Processingindustry

End-markets and applications

Cane Beet Corn TapiocaOther Starchy

cropsCellu-lose

Food (proces-sing) industry

Fermentation industry

Pharma Fuel ChemicalsFood Feed Dyes, etcMicro-

organisms

Catalytic conversion

Sugar Starches

Wheat

Fermentation-based chemical value chain – “Agri meets Chemicals”

© 2015 Deloitte The Netherlands

Crops and arable land use for fermentation-based chemicals will remain insignificant compared to food, feed and fuel while the added value is high

2 2016-09-08 Fermentation Study Summary - Hannover

Global fossil and biomass inputs and outputs (2013, in biomass equivalents)

• The fermentation-based chemical industry, while growing, is still small compared to petrochemicals• Oil and gas are mainly used for energy and only a small part for chemicals – ca. 3% and another 3% for the

energy required to make the chemicals• All figures are indicative; See separate table with detailed figures covering added value, arable land use

Agricultural produce:

~11 bn ton dry matter biomass

equivalents

Fossil materials (coal, oil &

gas):~35 bn ton dry mass biomass

equivalents

10

33 1.5

0.1

0.3

Sources

Usage

Note: All figures are indicative; Biofuel excludes wood; See separate table with detailed figures covering added value, arable land use Sources: FAO, IEA, EIA, Sanders & Bos (2013), Deloitte Analysis

Food and Feed Fuel (Energy) Chemicals

Fermentation-based

Products

0.4

0.1

© 2015 Deloitte The Netherlands

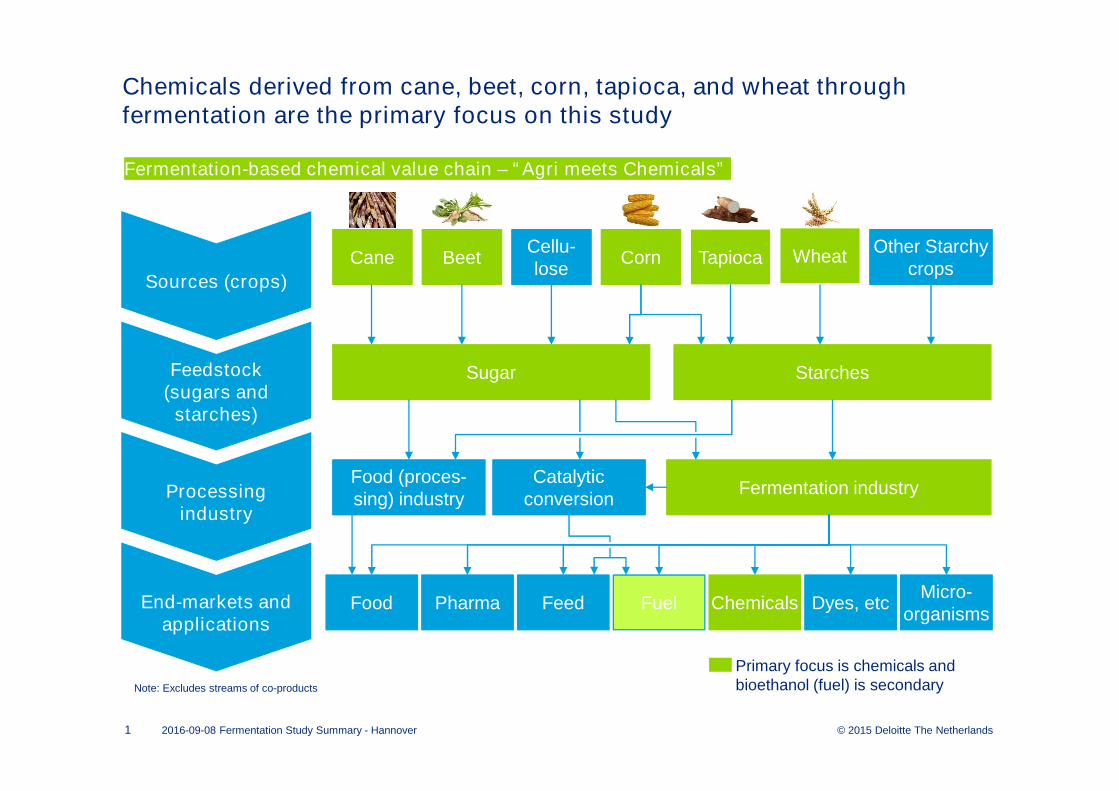

The study focuses on the regions with the highest concentration of carbohydrates of interest to the fermentation industry

Global production of carbohydrate feedstocks per region (mln ton CHEQ, 2012)

* Other coarse grains includes millet, oats, rye, triticale, buckwheat, fonio, canary seed, and quinoa; ** Other roots & tubers includes sweet potatoes, yams, taro, and yautiaSource: OECD-FAO Agricultural Outlook 2013, USDA nutrient database, Deloitte Analysis

3

Study focus

Total: 2,388 mln ton CHEQ

2016-09-08 Fermentation Study Summary - Hannover

24% 28%18%

24%

41%

31%

9%5%

11% 12%

21%

14%

19%

12%

11%

11%

7%

20%

41%

15%

43%34%

23%17%

38%

23%

61%52%

42%

70%

41%48%

54%

4%7%

26%

10%

30%

5%

9%

39%

8%

0%

25%

50%

75%

100%

Potatoes

98

4%

64100224

BarleyCassavaWheat

507

Sugar cane

4%

4%

43

Sugar beet

37

Sorghum Other roots

& tubers**

50

Other coarse grains*

66

4%

648 552

RiceCorn

3%

EU

SEA

BR

RoW

India

China

US

© 2015 Deloitte The Netherlands

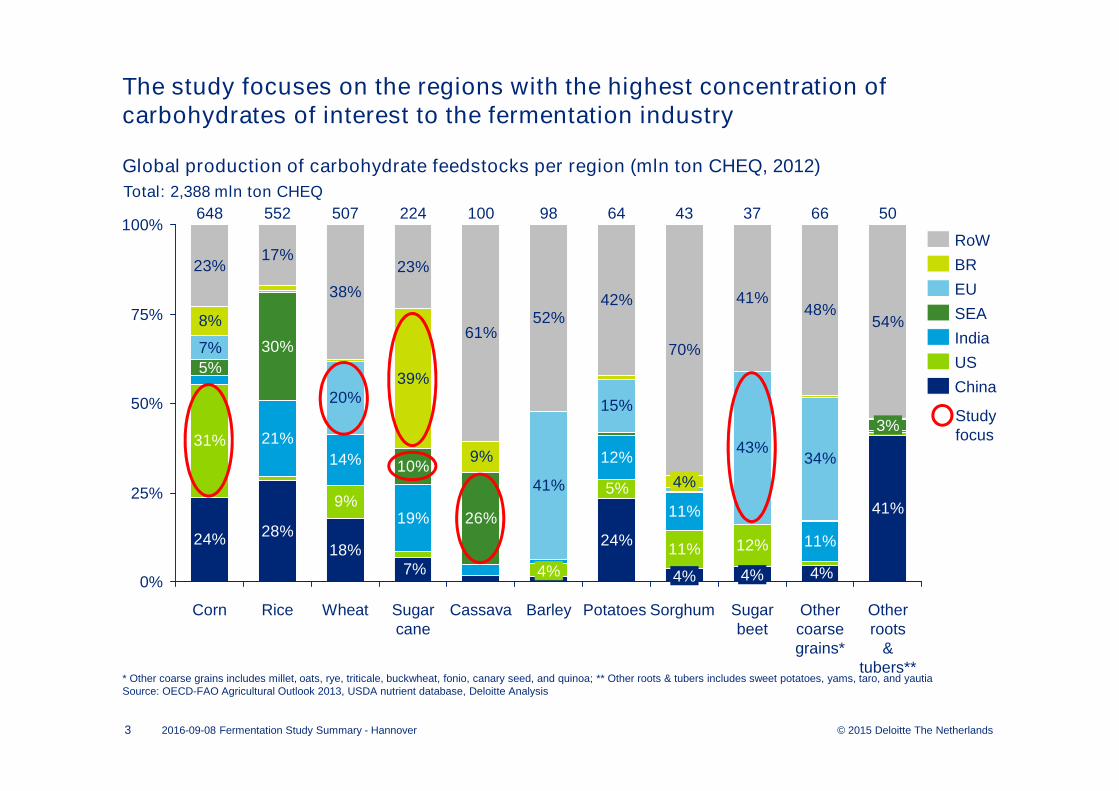

Only in the US, corn and other coarse grains are predominantly used for biofuel, while in the rest of the world the majority goes to food and feed

60% 80%0%

60%

40%

20%

20%

0%

100%

40% 100%

80%

40%

25%

212

US

27%

3%

63%

30%

5%

IN*

260

Rest of World*

10%

33%

52%65%

S-E Asia*

73%

14%

29

51%

55108

6%

73%

22%

8%

BR

8%

EU

4%160

24%

4%

13%

CN

17%

Global production and use of corn and other coarse grains (mln ton CHEQ, 2012)

* Excludes imported grains; Note: allocation based on 2013 data; Note 2: Coarse grains is an aggregate of corn (76% by mass), barley (12%), sorghum (5%), millet (3%), oats (2%), rye, triticale, buckwheat, fonio, canary seed, and qinoa; Source: FAO, OECD-FAO Agricultural Outlook 2013, USDA nutrient database, Deloitte Analysis

4

Food

Biofuel

Feed

Other

Export

2016-09-08 Fermentation Study Summary - Hannover

Corn

© 2015 Deloitte The Netherlands

80%

60%

40%

100%

20%0% 80%60%

0%

40% 100%

20%

4% 8%

44%

97%

56%

96%100%

92%

3%

PK Rest of world

7 42

MX

100%

BR

615

CNS-E AsiaIN

88 42 23

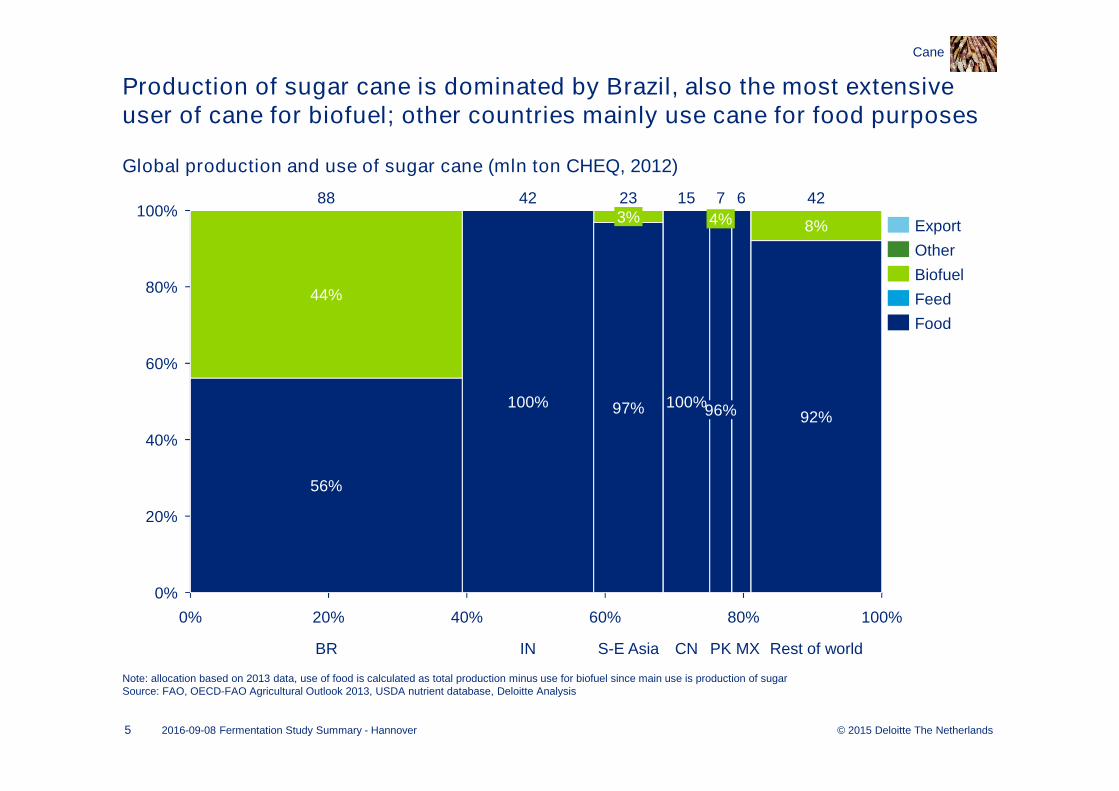

Note: allocation based on 2013 data, use of food is calculated as total production minus use for biofuel since main use is production of sugarSource: FAO, OECD-FAO Agricultural Outlook 2013, USDA nutrient database, Deloitte Analysis

5

Export

Other

Biofuel

Feed

Food

Production of sugar cane is dominated by Brazil, also the most extensive user of cane for biofuel; other countries mainly use cane for food purposes

Global production and use of sugar cane (mln ton CHEQ, 2012)

2016-09-08 Fermentation Study Summary - Hannover

Cane

© 2015 Deloitte The Netherlands

60%

40%

80%

20%

0%

100%80%60%40%20%0%

100% 4%

100%

RU

16 6

100%

24

100%

US

83%

UA

3

100%

13%

Rest of worldTREU

100%

6

Note: allocation based on 2013 data, use of food is calculated as total production minus use for biofuel and “other” since main use is production of sugarSource: FAO, OECD-FAO Agricultural Outlook 2013, USDA nutrient database, Suiker Unie, Deloitte Analysis

6

Export

Feed

Biofuel

Other

Food

The EU is the main producer of sugar beets and the only region where beets are directly used to produce biofuel

Global production and use of sugar beet (mln ton CHEQ, 2012)

2016-09-08 Fermentation Study Summary - Hannover

Beet

© 2015 Deloitte The Netherlands

Starch

Cleaning

Dry grinding

Wetting

Starch separation

Drying

Starch refining

Wheat

Corn, wheat, cane, cassava, and beet require different processes to produce sugar or starch

* Wet milling process ** Required for manually harvested cane only since a harvester machine cuts the cane during harvestingSource: Unica, Suiker Unie, Corn Refiners Association, Thai Tapioca Association, Overleggroep Producenten Natte Veevoeders

7

Carbohydrate production processes

HFCS, Starch

Cleaning

Steeping

Germ separation

Grinding

Syrup conversion

Starch separation

Syrup refining

Corn*

Washing

Cutting**

Crushing

Juice purification

Crystallisation

Evaporation

Centrifuging

Raw sugar

Sugar cane

Starch

Cleaning

Peeling & cutting roots

Rasping

Filtering

Settling & Drying

Centrifuging

Grinding

Cassava

Washing

Slicing

Juice extraction

Juice purification

Crystallisation

Evaporation

Centrifuging

White sugar

Sugar beet

2016-09-08 Fermentation Study Summary - Hannover

© 2015 Deloitte The Netherlands

1608050

1.000

60

500

13090

2.000

7040 14020 12010

1.500

30

2.500

0

0

110 150100Volume (mln ton w.s.e.)

Note: Production costs of raw sugar converted to w.s.e. multiplying by 1.087 (polarisation constant) and adding refining costs of $65 / ton, raw sugar volume converted to w.s.e. by dividing volume by 1.087; Note 2: Production costs for beet and cane include for both land and factory costs for labour, capital (incl. a.o. land rent and depreciation), input (incl. a.o.seeds, fertilizer, chemicals, and energy), and factory by-product revenueSource: LMC International Sugar & HFS report 2014, UNICA Harvest Reports 09/10 – 12/13, Deloitte Analysis

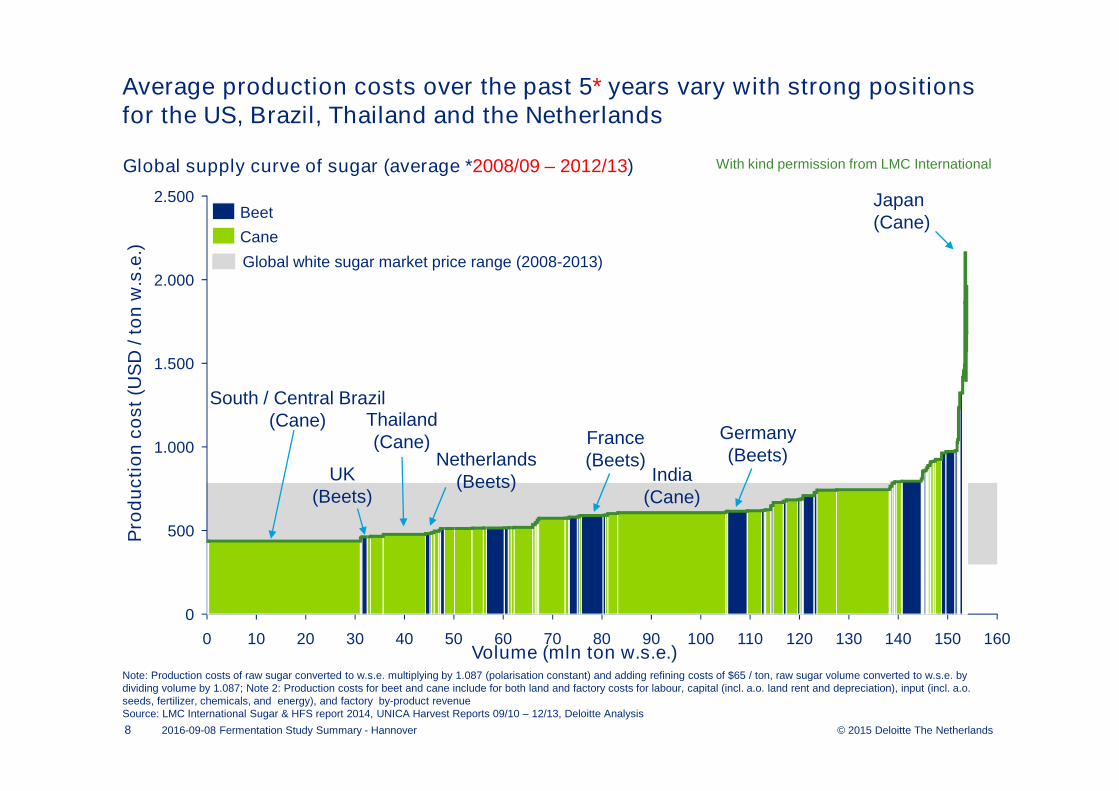

Average production costs over the past 5* years vary with strong positions for the US, Brazil, Thailand and the Netherlands

Pro

du

cti

on

co

st

(US

D / t

on

w.s

.e.)

Global supply curve of sugar (average *2008/09 – 2012/13)

Thailand (Cane)

Netherlands (Beets)

Japan(Cane)

Cane

Beet

South / Central Brazil(Cane)

8

Global white sugar market price range (2008-2013)

India (Cane)

2016-09-08 Fermentation Study Summary - Hannover

UK(Beets)

France(Beets)

Germany(Beets)

With kind permission from LMC International

© 2015 Deloitte The Netherlands

20 17070 90

2.500

60

3.000

2.000

500

150130 140

0

100 12040

1.500

1.000

50 16011030 80100

Volume (mln ton w.s.e.)Note: Production costs of raw sugar converted to w.s.e. multiplying by 1.087 (polarisation constant) and adding refining costs of $65 / ton, raw sugar volume converted to w.s.e. by dividing volume by 1.087; Note 2: Production costs for beet and cane include for both land and factory costs for labour, capital (incl. a.o. land rent and depreciation), input (incl. a.o.seeds, fertilizer, chemicals, and energy), and factory by-product revenueSource: LMC International Sugar & HFS report 2014, UNICA Harvest Reports 09/10 – 12/13, Deloitte Analysis

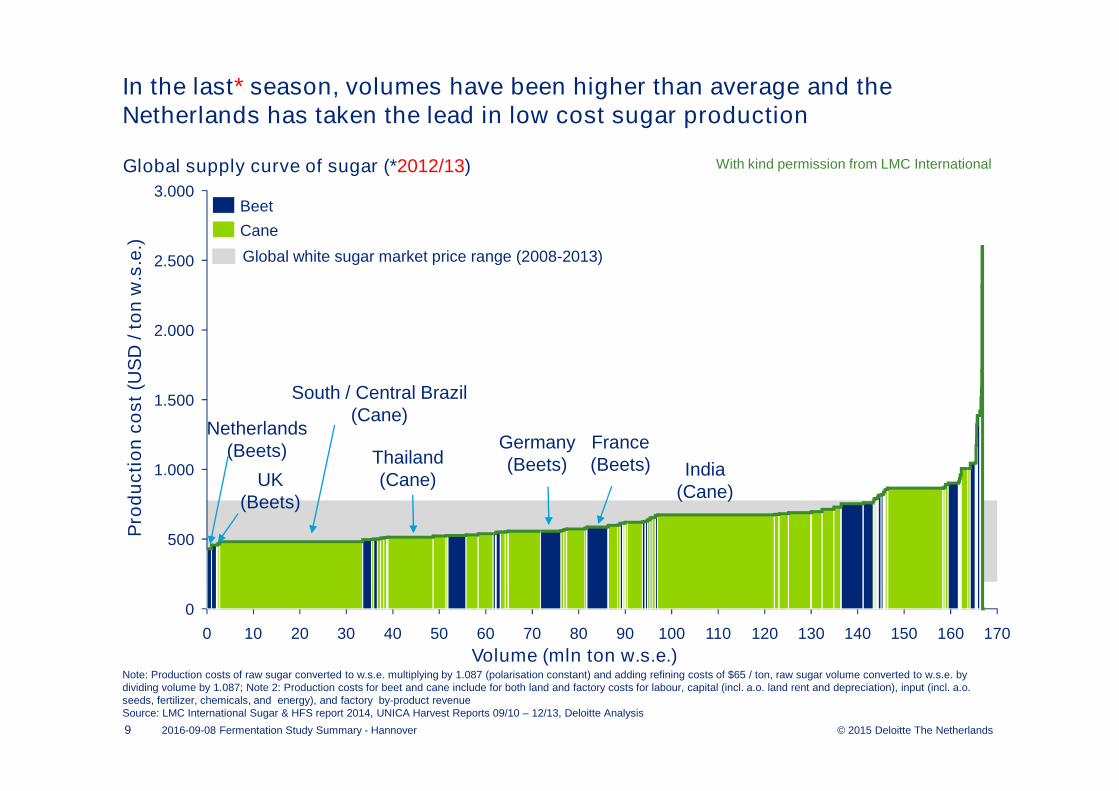

In the last* season, volumes have been higher than average and the Netherlands has taken the lead in low cost sugar production

Pro

du

cti

on

co

st

(US

D / t

on

w.s

.e.)

Global supply curve of sugar (*2012/13)

Thailand (Cane)

Netherlands (Beets)

South / Central Brazil(Cane)

9

India (Cane)

Cane

Beet

Global white sugar market price range (2008-2013)

2016-09-08 Fermentation Study Summary - Hannover

UK(Beets)

France(Beets)

Germany(Beets)

With kind permission from LMC International

© 2015 Deloitte The Netherlands

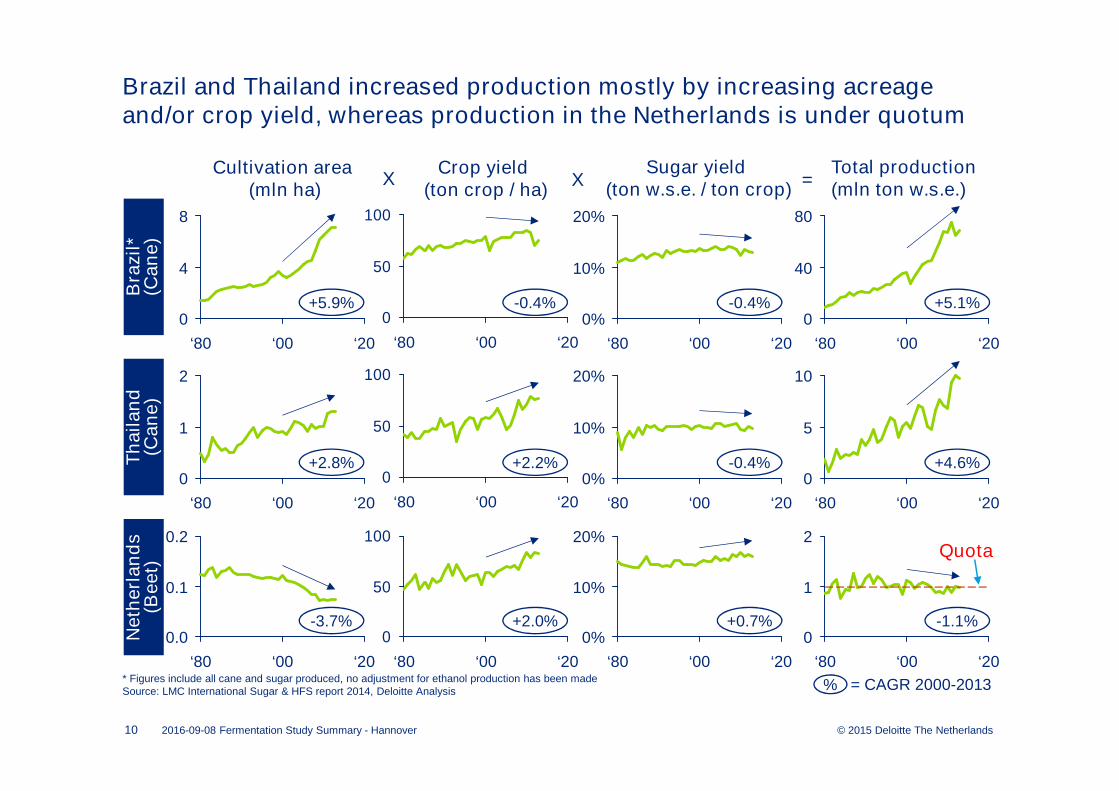

Brazil and Thailand increased production mostly by increasing acreage and/or crop yield, whereas production in the Netherlands is under quotum

10

* Figures include all cane and sugar produced, no adjustment for ethanol production has been madeSource: LMC International Sugar & HFS report 2014, Deloitte Analysis

‘00‘80

0

‘20

8

4

Cultivation area(mln ha)

Crop yield (ton crop / ha)

Total production (mln ton w.s.e.)

Sugar yield (ton w.s.e. / ton crop)

Bra

zil

* (C

an

e)

Th

ail

an

d

(Ca

ne)

Neth

erl

an

ds

(Beet)

0

50

100

‘80 ‘00 ‘20

0%

‘20‘00

20%

10%

‘80 ‘80

80

40

0

‘20‘00

X X =

2

1

0

‘20‘00‘80

0

50

100

‘20‘80 ‘00

10%

0%

20%

‘80 ‘20‘00 ‘80 ‘00

10

5

0

‘20

0.2

0.1

0.0

‘20‘80 ‘00

0

50

100

‘20‘00‘80

20%

‘20

10%

0%

‘00‘80 ‘00‘80

1

‘20

0

2

+5.9%

+2.8%

-3.7%

-0.4%

+2.2%

+2.0%

% = CAGR 2000-2013

-0.4%

-0.4%

+0.7%

+5.1%

+4.6%

-1.1%

2016-09-08 Fermentation Study Summary - Hannover

Quota

© 2015 Deloitte The Netherlands

481

0

250

500

750

1980 1985 1990 1995 2000 2005 2010 2015

+6.0%

281

0

250

500

750

1980 1985 1990 1995 2000 2005 2010 2015

+1.5%

429

513

0

250

500

750

1980 1985 1990 1995 2000 2005 2010 2015

+3.7%

Since 2000 the production costs in Brazil have increased significantly more than in the Netherlands, resulting in a higher price level

11

Production costs (USD / ton w.s.e., 1980-2013)

Note: cost levels same as previously definedSource: LMC International Sugar & HFS report 2014, Deloitte Analysis

Brazil – Cane Netherlands – Beets

Thailand – Cane

% = CAGR 2000-2013

TotalCost

Crop Cost

TotalCost

Crop Cost

TotalCost

Crop Cost

575

308

0

250

500

750

1980 1985 1990 1995 2000 2005 2010 2015

+1.5%EU – Beets

TotalCost

Crop Cost

2016-09-08 Fermentation Study Summary - Hannover

149

267

© 2015 Deloitte The Netherlands

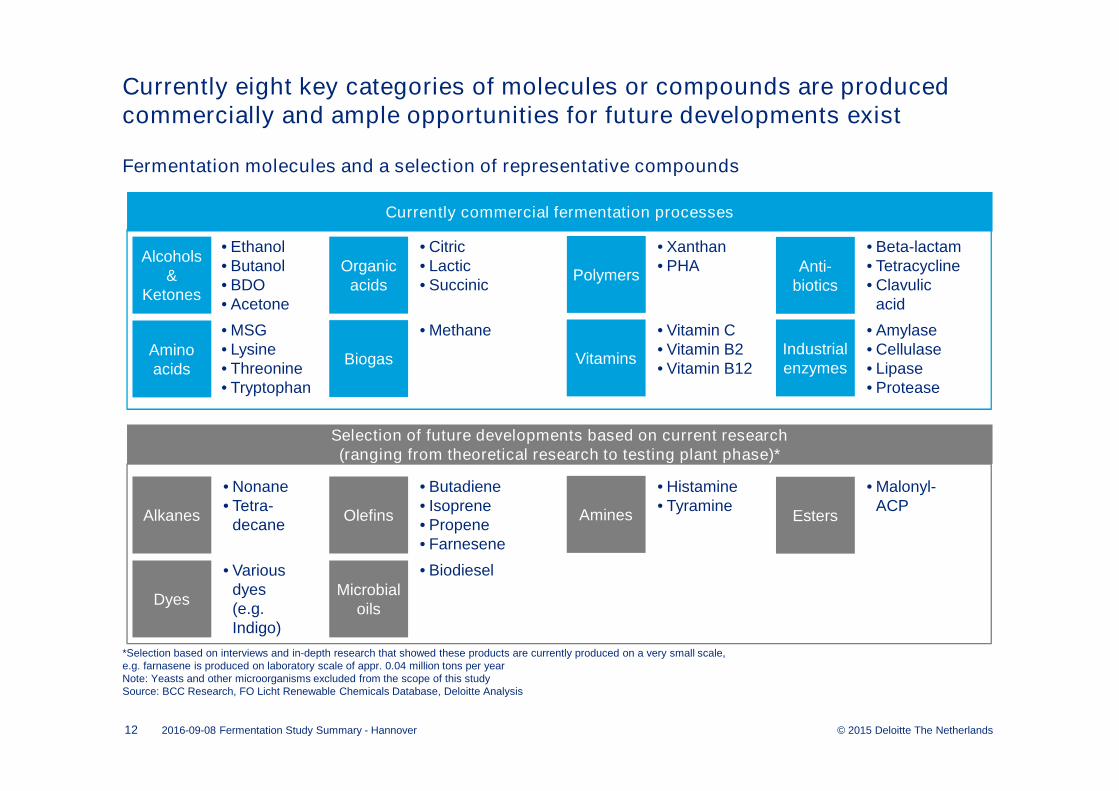

Currently eight key categories of molecules or compounds are produced commercially and ample opportunities for future developments exist

*Selection based on interviews and in-depth research that showed these products are currently produced on a very small scale, e.g. farnasene is produced on laboratory scale of appr. 0.04 million tons per yearNote: Yeasts and other microorganisms excluded from the scope of this studySource: BCC Research, FO Licht Renewable Chemicals Database, Deloitte Analysis

• Ethanol• Butanol• BDO• Acetone

Amino acids

Organic acids

BiogasIndustrial enzymes

Polymers

Vitamins

Anti-biotics

Alcohols &

Ketones

12

Currently commercial fermentation processes

Fermentation molecules and a selection of representative compounds

• MSG• Lysine• Threonine• Tryptophan

• Citric• Lactic• Succinic

• Methane

• Xanthan• PHA

• Vitamin C• Vitamin B2• Vitamin B12

• Beta-lactam• Tetracycline• Clavulic

acid

• Amylase• Cellulase• Lipase• Protease

Selection of future developments based on current research (ranging from theoretical research to testing plant phase)*

• Nonane• Tetra-

decaneOlefins Amines EstersAlkanes

• Butadiene• Isoprene• Propene• Farnesene

• Histamine• Tyramine

• Malonyl-ACP

Dyes

• Various dyes (e.g. Indigo)

Microbial oils

• Biodiesel

2016-09-08 Fermentation Study Summary - Hannover

© 2015 Deloitte The Netherlands

4.000

0

5.000

200160120

2.500

140110

4.500

1809080 130 1701007030

22.500

5040

3.500

2.000

500

1.500

60 2100 10 20 190

3.000

150

1.000

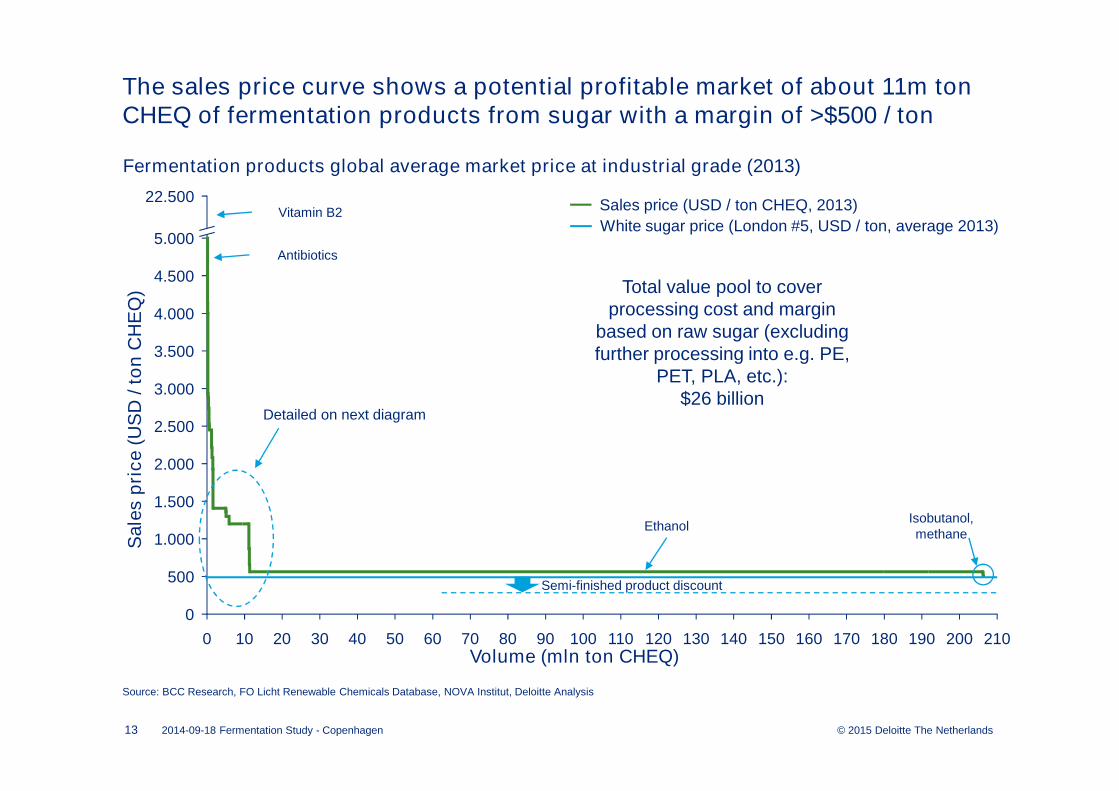

The sales price curve shows a potential profitable market of about 11m ton CHEQ of fermentation products from sugar with a margin of >$500 / ton

Sale

s p

ric

e (

US

D /

to

n C

HE

Q)

Fermentation products global average market price at industrial grade (2013)

2014-09-18 Fermentation Study - Copenhagen13

Ethanol

Vitamin B2

Antibiotics

Sales price (USD / ton CHEQ, 2013)

White sugar price (London #5, USD / ton, average 2013)

Detailed on next diagram

Total value pool to cover processing cost and margin

based on raw sugar (excluding further processing into e.g. PE,

PET, PLA, etc.):$26 billion

Isobutanol, methane

Semi-finished product discount

Volume (mln ton CHEQ)

Source: BCC Research, FO Licht Renewable Chemicals Database, NOVA Institut, Deloitte Analysis

© 2015 Deloitte The Netherlands

12

0

111098732 4

500

1.000

1

4.500

1.500

2.000

5

2.500

0

3.000

5.000

6

3.500

4.000

22.500

Volume (mln ton CHEQ)

The majority of the volume of this potential market (89%) is currently in five products, namely, lysine, MSG, citric acid, lactic acid, and glutamic acid

14 2014-09-18 Fermentation Study - Copenhagen

Sale

s p

ric

e (

US

D /

to

n C

HE

Q)

Vitamin B2

Antibiotics

Sales price (USD / ton CHEQ, 2013)

White sugar price (London #5, USD / ton, average 2013)

Glutamic acid

MSGCitric acid

Fermentation products global average market price at industrial grade (2013)

Total value pool to cover processing cost and margin

based on raw sugar (excluding further processing into e.g. PE,

PET, PLA, etc.):$12 billion

PDO, Threonine, Itaconic acid

Vitamin B12, Iso-ascorbic acid, Xanthan, Vitamin C, Succinic acid, PHA

Tryptophan, enzymes

Gluconic acid, Acetone, N-butanol

LysineFatty alcohols

BDO

Source: BCC Research, FO Licht Renewable Chemicals Database, NOVA Institut, Deloitte Analysis

Lactic acid

© 2015 Deloitte The Netherlands

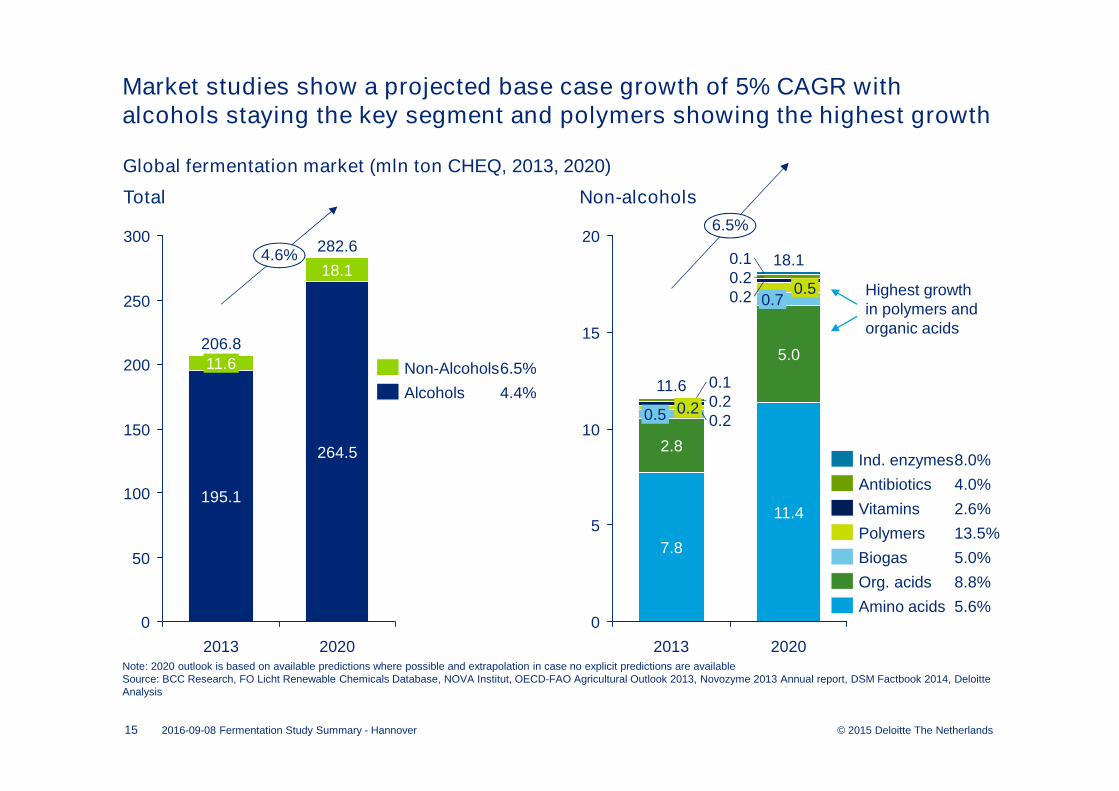

Market studies show a projected base case growth of 5% CAGR with alcohols staying the key segment and polymers showing the highest growth

15

300

250

50

100

200

150

0

4.6%282.6

206.8

2013 2020

195.1

11.6

18.1

264.5

Global fermentation market (mln ton CHEQ, 2013, 2020)

20

15

10

5

0

0.2

0.1

7.8

0.1

0.5 0.2 0.2

2013

11.6

2.8

6.5%

2020

18.1

11.4

5.0

0.70.5

0.20.2

Amino acids 5.6%

Org. acids 8.8%

Biogas 5.0%

Polymers 13.5%

Vitamins 2.6%

Antibiotics 4.0%

Ind. enzymes8.0%

Alcohols 4.4%

Non-Alcohols6.5%

Note: 2020 outlook is based on available predictions where possible and extrapolation in case no explicit predictions are availableSource: BCC Research, FO Licht Renewable Chemicals Database, NOVA Institut, OECD-FAO Agricultural Outlook 2013, Novozyme 2013 Annual report, DSM Factbook 2014, Deloitte Analysis

Total Non-alcohols

2016-09-08 Fermentation Study Summary - Hannover

Highest growth in polymers and organic acids

© 2015 Deloitte The Netherlands

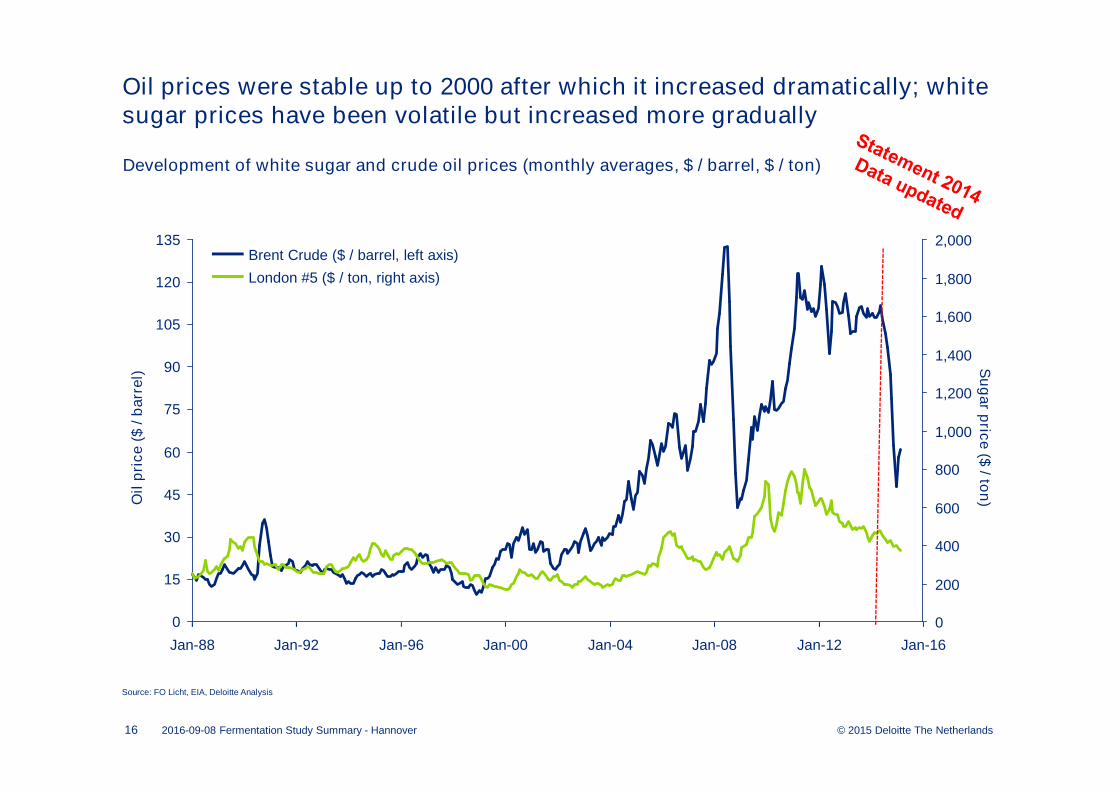

Oil prices were stable up to 2000 after which it increased dramatically; whitesugar prices have been volatile but increased more gradually

16

Oil

pri

ce (

$ /

barr

el)

Source: FO Licht, EIA, Deloitte Analysis

0

15

30

45

60

75

90

105

120

135

1,600

Jan-92Jan-88 Jan-96 Jan-00

1,400

1,800

Jan-12Jan-08Jan-04 Jan-16

2,000

800

400

600

200

0

1,000

1,200

Development of white sugar and crude oil prices (monthly averages, $ / barrel, $ / ton)

Su

gar p

rice ($

/ ton

)

London #5 ($ / ton, right axis)

Brent Crude ($ / barrel, left axis)

2016-09-08 Fermentation Study Summary - Hannover

© 2015 Deloitte The Netherlands

As a result, in the past fifteen years the sugar price decreased relative tocrude oil, creating an opportunity for sugar in the biobased economy

17

Rati

o L

on

do

n #

5 /

Bre

nt

cru

de (

US

D/G

J /

US

D/G

J)

Source: FO Licht, EIA, Deloitte Analysis

0

3

6

9

12

15

Jan-00 Jan-04Jan-96 Jan-16Jan-08Jan-92 Jan-12Jan-88

Ratio London #5 (USD/GJ) / Brent Crude (USD/GJ)• Stable oil prices• Volatile, harvest dependent sugar prices

• Sharply increasing oil prices• Moderately increasing sugar prices

Development of price ratio of white sugar over crude oil (monthly averages, USD/GJ / USD/GJ )

Recent drop in oil prices

2016-09-08 Fermentation Study Summary - Hannover

?

© 2015 Deloitte The Netherlands

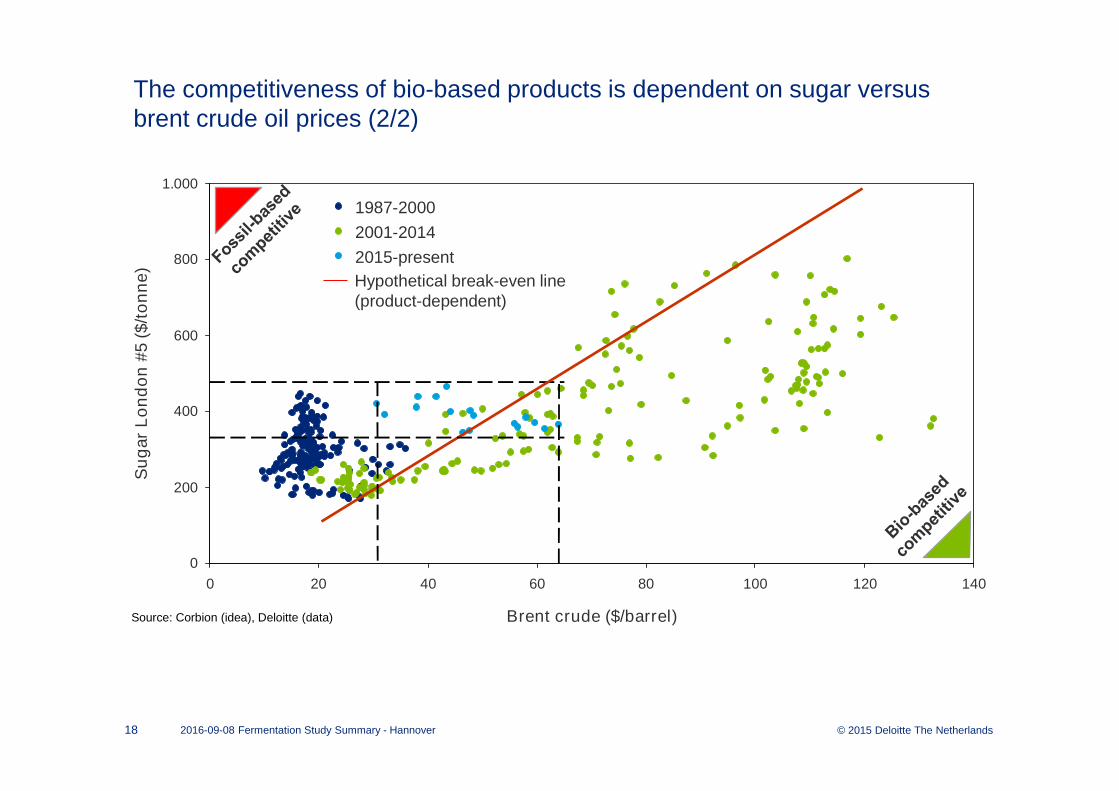

The competitiveness of bio-based products is dependent on sugar versus brent crude oil prices (2/2)

2016-09-08 Fermentation Study Summary - Hannover18

0

200

400

600

800

1.000

0 20 40 60 80 100 120 140

Su

gar

Lo

nd

on

#5 (

$/t

on

ne

)

Brent crude ($/barrel)

1987-2000

2001-2014

2015-present

Hypothetical break-even line (product-dependent)

Source: Corbion (idea), Deloitte (data)

© 2015 Deloitte The Netherlands

In a nutshell… a positive picture for NW-EU

1. NW-EU and sugar beets have surprisingly strong competitive position

2. Due to de-regulation additional volumes will come on the market in 2017

3. The current market for biobased chemicals is still relatively small, but expected to grow with 6.5% CAGR until 2020

4. Biobased chemicals are an attractive market with high economic value-add ($12 billion / annum) in 2013

5. Each product needs it own business case

6. Land use for functional molecules will remain insignificant

7. Sugar has become cheaper compared to oil … until 20142016-09-08 Fermentation Study Summary - Hannover19

© 2015 Deloitte The Netherlands

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 200,000 professionals are committed to becoming the standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

.

20 2016-09-08 Fermentation Study Summary - Hannover