Embed Size (px)

Citation preview

Opportunistic Credit

May 11, 2016

Presented by: Francois Otieno Director of Fixed Income Segal Rogerscasey

Table of Contents

• Section I: The Opportunistic Credit Opportunity Set • Section II: Description of each Credit Opportunity • Section III: Market Factors Driving Opportunities within Credit • Section IV: Implementation Considerations

2

Section I

The Opportunistic Credit Opportunity Set

The Opportunistic Credit Universe

Corporate Debt • High Yield • Bank Loans/Leverage Loans • Private Debt • Direct Lending • NPLs and RPLs • Distressed

Securitized and Mortgage Debt

4

These bonds are typically rated below investment grade

In the event these bonds are not rated by

the rating agencies, they would still exhibit the characteristics of below investment grade companies

Securitized bonds are backed by a pool of assets while mortgage debt is simply the underlying debt of private commercial and residential properties

Managers are primarily looking for

opportunities in the junior tranches (below investment grade) of the securitized segment of the market

• Agency MBS • Non-Agency MBS • ABS • CMBS • Collateralized Loan Obligations (CLOs) • Commercial and Residential Mortgage Debt

Public (or Liquid) Debt

Private (or Illiquid) Debt • High Yield • Bank Loans/Leverage Loans • Distressed • Agency MBS • Non-Agency MBS • ABS, CMBS • CLOs

• Private Debt • Direct Lending • NPLs and RPLs • Commercial and Residential Mortgage Debt

The majority of these securities are publicly traded with low bid-ask spreads.

Very diverse buyer base

These are privately negotiated deals with unique and bespoke terms

Very thin secondary market for some of

these deals and non-existent for others

The Opportunistic Credit Universe (Cont’d)

5

• High Yield • Bank Loans • Agency MBS

• Distressed • CLOs (Junior debt and

Equity) • NPLs • Commercial & Residential

Mortgage Debt

• Private Debt • Direct Lending • Non-Agency MBS • ABS • CMBS

Risk/Return Continuum Highest Lowest

6

Opportunities exist in the credit market across the risk/return spectrum, depending on a client’s appetite for risk and liquidity

The Opportunistic Credit Universe (Cont’d)

Section II Description of each Credit Opportunity

Description of Each Credit Opportunity Set

Opportunities within Corporate Debt

8

Opportunities within Securitized and Mortgage Debt

9

Section III Market Factors Driving Opportunities within Credit

Market Factors Driving Opportunities within Credit

10

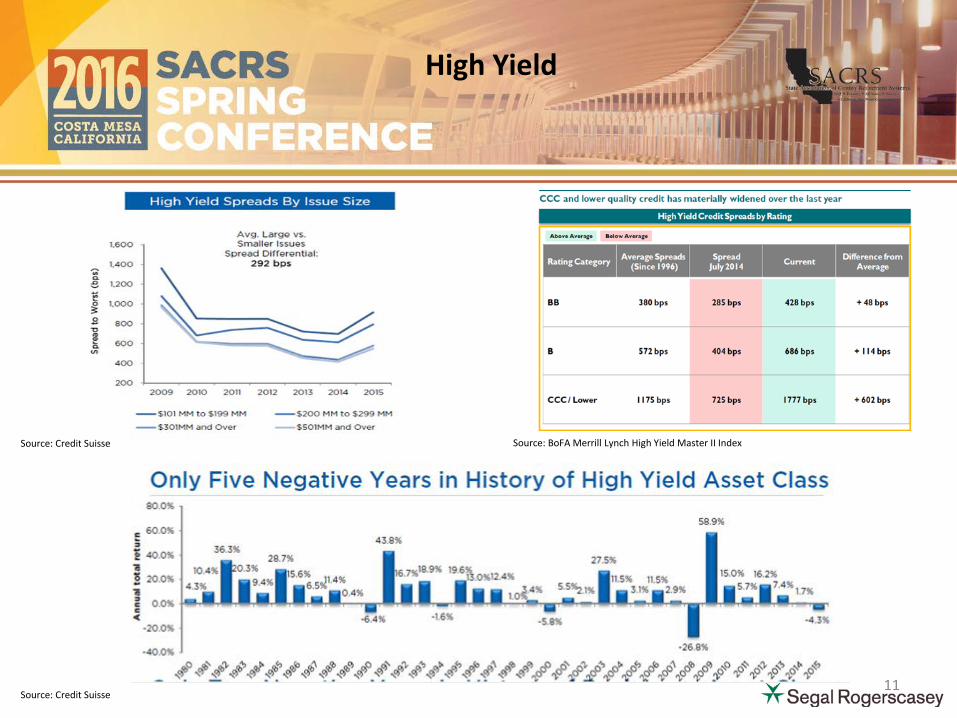

High Yield

Source: Credit Suisse

Source: Credit Suisse

Source: BoFA Merrill Lynch High Yield Master II Index

11

Source: Credit Suisse

Defaulted Debt by Sector

Defaulted Debt by Original Issue Rating

High Yield (Cont’d)

12

Bank Loans

Source: Credit Suisse 13

Annual High Yield Default Rates

Annual Bank Loan Default Rates

High Yield default rates are the highest since 2009, but largely concentrated in the Energy/Commodity related sectors as well as in the metals/mining, representing over 80% of total defaults

Bank Loan default rates have remained relatively low, largely due to the fact that bank loan indices has very little exposure to Energy/Commodity related sectors

High Yield vs Bank Loans: Default Rate Comparison

Source: Credit Suisse 14

Recovery rates for bonds in 2015 was 37 cents on the dollar, while recovery rates for Loans was 58 cents on the dollar

Today 15.3% of the high yield market is considered distressed, the highest level since the 2008 financial crisis

Distressed Debt

15

Heavy concentration to the Energy and Commodities sectors in the high yield index

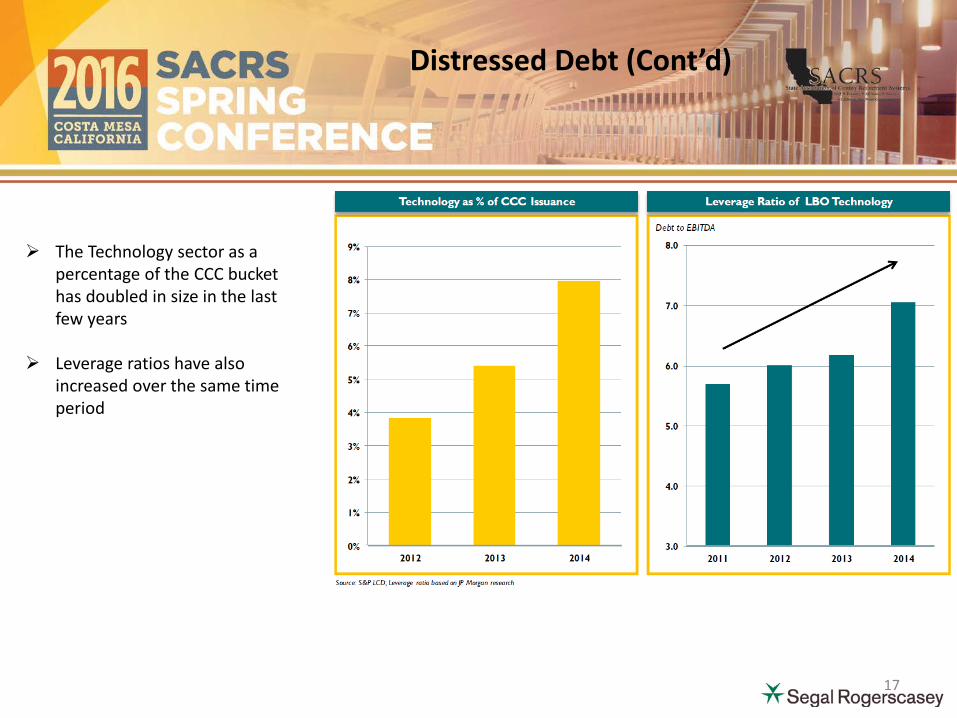

Distressed Debt (Cont’d)

16

The Technology sector as a percentage of the CCC bucket has doubled in size in the last few years

Leverage ratios have also

increased over the same time period

Distressed Debt (Cont’d)

17

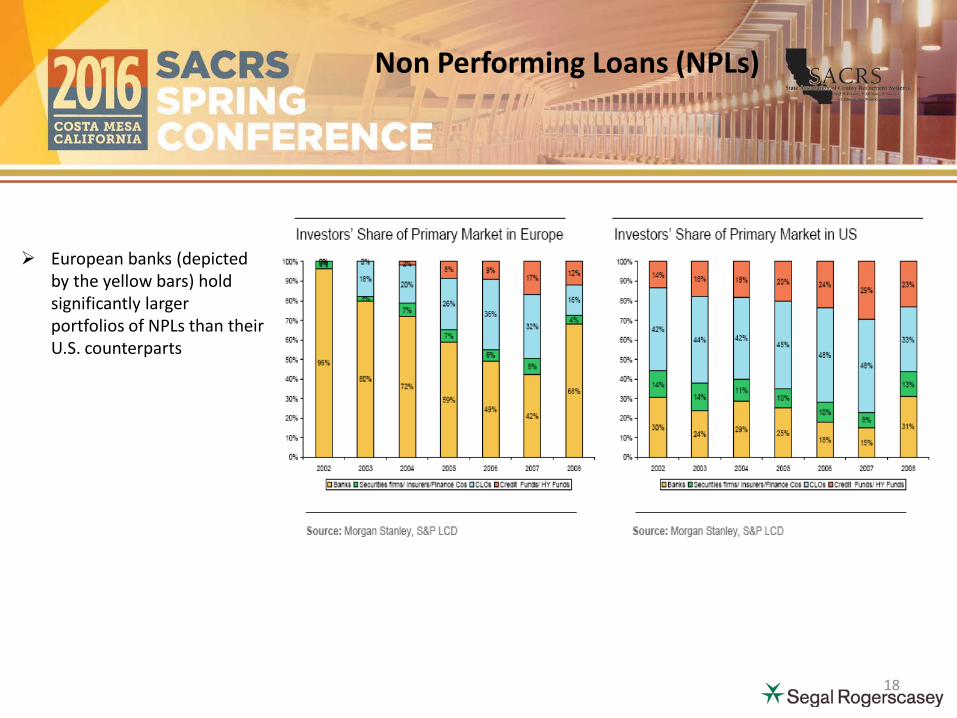

European banks (depicted by the yellow bars) hold significantly larger portfolios of NPLs than their U.S. counterparts

Non Performing Loans (NPLs)

18

Process of Securitization

This exhibit is a generic representation of the mechanics of securitization

Opportunistic Credit managers generally identify the BB/Ba (or below) rating category as the “sweet spot”

19

Legacy Non-Agency MBS represent the opportunity set. There has been virtually NO issuance since 2008 93% of the market is rated below investment grade, including over 80% rated CCC or below

Non-Agency MBS

Source: PIMCO, JPMorgan, Deutsche Bank, Bank of America/Merrill Lynch

20

Collateralized Loan Obligations (CLOs)

CLOs 2.0 represent the new wave of opportunities within the CLO market

Junior debt and Equity

tranches offer some of the most attractive risk/adjusted returns

21

Section IV Implementation Considerations

22

No one single product or strategy will capture the full breadth of the Credit opportunity set Each manager has a bias towards certain segments of the credit market. In fact, some strictly specialize in one area and others

employ a multi-strategy approach Even within each sector or sub-sector, opportunities vastly differ by manager

Implementation Considerations

23

Manager B

Manager E

Manager A

Manager C

Manager I Manager D

Manager H

Manager K

Manager G

Manager J

Manager F

Liquidity Continuum of Manager “Fund Structures” Least Liquid Most Liquid

Implementation Considerations (Cont’d)

24

“Daily” “Monthly” “Quarterly” “Semi-Annual or Longer”

Specialized Approach Pros: Primary focus and expertize of the firm and critically

important to its overall business Competitive advantage in sourcing deals Greater likelihood of generating stronger returns for this

specific sleeve

Cons: This narrowly focused area of the credit opportunity set

may be out of the favor at a particular time during the economic and market cycle, hence, hindering performance

With a specialized manager program, a client will pay

incentive fees to the best performer(s) in spite of the fact that other specialist managers within the program may have performed poorly

Multi-Strategy Approach Pros: Ability to make quick tactical adjustments to portfolio

structure in order to take advantage of market opportunities as they present themselves

Incentive fees are paid at the aggregate portfolio level Better suited for smaller clients or clients that do not

have the internal resources to conduct due diligence on a large number of managers

Cons: It is very difficult to identify managers with strong

expertize across the full credit spectrum Risk of strategy teams defecting

Implementation Considerations (Cont’d)

25

Implementation Considerations (Cont’d)

The majority of Opportunistic Credit strategies are managed in a closed end vehicle and some managers offer multiple vehicles

Terms do vary widely across managers The underlying vehicles and fee structures will generally dictate where the investment resides within a

broader asset allocation framework 26