Embed Size (px)

Citation preview

Oportunidades y Riesgos de las inversiones alternativas

Septiembre 2015

Joaquín Cortez H. Presidente Compañía de Seguros CorpVida S.A.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 2

Tabla de Contenidos

Inversiones Alternativas en Carteras de Institucionales

Tipos de Activos Alternativos

Oportunidades y Riesgos de los Activos Alternativos

Recomendaciones

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 3

Public Equities

Fixed Income

Alternatives

2006 2012

Cash

2011 2013 2014

YoY Change

2013-2014

+1%

+1%

-1%

-1%

Asset Allocation Fondos de Pensiones Estatales USA 2006-2014

Fuente: Cliffwater 2015, Report on State Pension Fund Allocation and Performance. September 2015.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 4

Activos Alternativos Globales

Fondos Soveranos Endowment & Foundations

Fondos de Pensiones

Total: MMUS$ 1.425.250 (100 Managers)

Compañías de Seguros

Total: MMUS$ 288.334 (25 Managers)

Total: MMUS$ 155.318 (25 Managers) Total: MMUS$ 80.725 (25 Managers)

Fuente: Global Alternatives Survey 2015, Towers Watson, Julio 2015

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 5

Private Equities

Real Estate/ Real Assets

Absolute Return

2007 2013

Natural Resources

2012 2014 Long Term Policy

Allocation

Educational Institutions

Mean

10%

9%

22%

13%

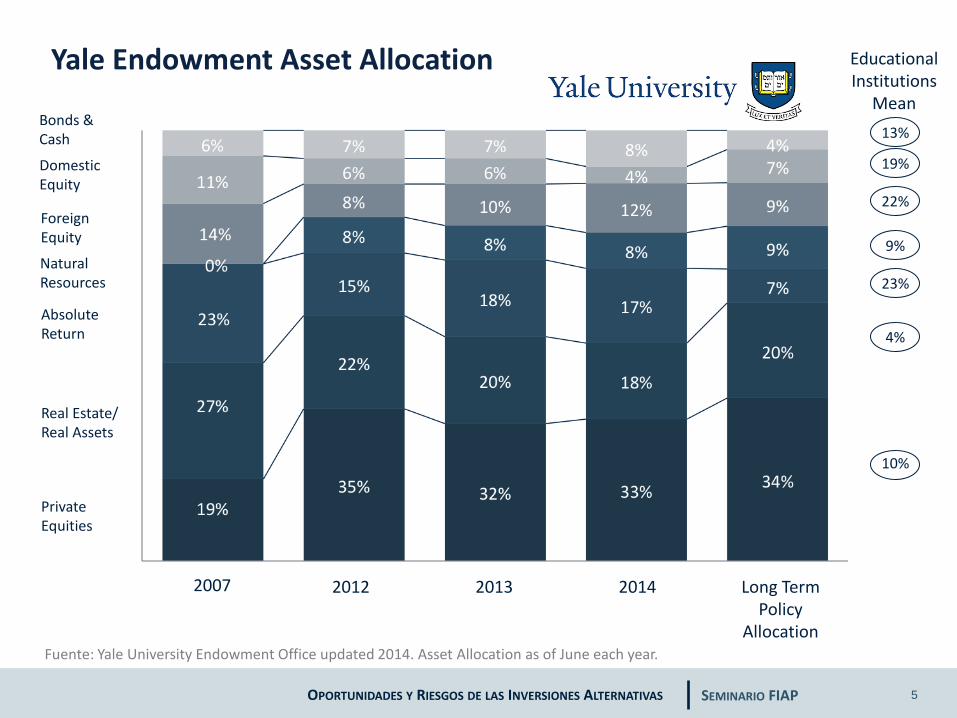

Yale Endowment Asset Allocation

Fuente: Yale University Endowment Office updated 2014. Asset Allocation as of June each year.

Foreign Equity

Domestic Equity

Bonds & Cash

19%

23%

4%

Yale Endowment Asset Allocation

“Hedge The heavy allocation to non-traditional asset classes stems from their return potential and diversifying power. Today's actual and target portfolios have significantly higher expected returns and lower volatility than the 1990 portfolio. Alternative assets, by their very nature, tend to be less efficiently priced than traditional marketable securities, providing an opportunity to exploit market inefficiencies through active management. The Endowment's long time horizon is well suited to exploiting illiquid, less efficient markets such as venture capital, leverage buyouts, oil and gas, timber, and real estate.”

Fuente: Yale University Endowment Office updated 2012.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 7

Inversión de los Fondos de Pensiones Latinoamericanos en Activos Alternativo

Fuente: Superintendencias de Pensiones

Instrumento (MMUS$) Chile Perú Colombia

Instrumentos Alternativos Locales s/i 1.700,2 972,2

Instrumentos Alternativos Exterior s/i 596,9 1.992.7

Total Activos Alternativos 4.891,9 2.297,1 2.964,9

Total Fondos de Pensiones 155.952,1 38.056,0 52.842,24

Instrumento (% Fondo Pensiones) Chile Perú Colombia

Instrumentos Alternativos Locales s/i 4,47% 1,84%

Instrumentos Alternativos Exterior s/i 1,57% 3,77%

Total Activos Alternativos 3,14% 6,04% 5,61%

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 8

Inversión de los Fondos de Pensiones Chilenos en Activos Alternativos

Fuente: Superintendencia de Pensiones

Instrumento MMUS$ % Activos

Alternativos % Fondos de

Pensiones

Private Equity Internacional 1.472,1 30,1% 0,94%

Real Estate Local 606,8 12,4% 0,39%

Infrastructure 221,0 4,5% 0,14%

Debt 550,0 11,2% 0,35%

Small Caps 1.947,0 39,8% 1,25%

Others 94,9 1,9% 0,06%

Total Alternative Assets 4.891,9 100,0% 3,14%

Private Equity Promesado 884,3 - 0,57%

Total Alt. Assets con PE Promesado 5.776,2 - 3,70%

Francisco Murillo SURA Chile’s CEO

“Alternative investments could help improve future pensions in Chile, according to Sura Chile's CEO. Francisco Murillo told a seminar on alternative pension investments that investing in real estate, infrastructure, private equity and hedge funds could lead to higher investment returns for the country's six private pension fund managers (AFPs).”

Tamara Agnic Superintendenta de Pensiones Chile

Superintendencia de Pensiones de Chile evalua cambios al régimen de inversiones, reconociendo que existe espacio para incorporar nuevos instrumentos. Si bien para ello requiere un informe previo del Banco Central, la aprobación del Consejo Técnico de Inversiones (CTI) y el visado del Ministerio de Hacienda, admite que el tema está bajo análisis y que las AFP han manifestado "interés por invertir en activos alternativos, especialmente en private equity y private debt ”.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 11

Tabla de Contenidos

Inversiones Alternativas en Carteras de Institucionales

Tipos de Activos Alternativos

Oportunidades y Riesgos de los Activos Alternativos

Recomendaciones

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 12

Tipo de Activos Alternativos

Hedge Funds

Private Equity Commodities

Real Estate Deudas

Estructuradas

Infrastructure

Activos Alternativos

Definición de Hedge Funds

“Hedge Funds are investment pools that are relatively unconstrained in what they do. They are relatively regulated (for now), charge very high fees, will not necessarily give you your money back when you want it, and will generally not tell you what they do. They are supposed to make money all the time and when they fail at this, their investors redeem and go to someone else who has recently been making money. Every three or four years they deliver a one in a hundred year flood. They are generally run for rich people in Geneva, Switzerland, by rich people in Greenwich , Connecticut.”

Fuente: Cliff Asness cited in Andrew Ang. Asset Management: A Systematic Approach to Asset Investing. 2014.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 14

Tipos de Estrategias de Hedge Funds Direccionales y No Direccionales

Convertible Arbitrage Global Macro

Dedicated Short Bias Managed Futures

Equity Market Neutral

Long/Short Equity Hedge

Event Driven Multistrategy

Fixed Income Arbitrage Fund of Funds

Hedge Funds

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 15

Breakdown of Lipper Tass Live Funds by Category

En %

Fuente: Andrew Lo. Hedge Funds: An Analytic Perpective. Princeton University Press. 2010.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 16

Herramientas de los Hedge Funds

Principales Herramientas

Derivados

Leverage Posiciones

Cortas

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 17

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 18

¿Qué buscan los inversionistas de los Hedge Funds?

Una combinación de: Retornos esperados positivos y Bajas correlaciones con activos tradicionales. (diversificación)

La pregunta es como se descubre este tipo de oportunidades.

Si estos fondos no fueran Hedge, en el sentido de tener bajas correlaciones con el mercado, podría implicar un cuestionamiento a su agregación de valor.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 19

Hedge Funds: Rentabilidad Anualizada, Riesgo y Correlaciones, a 10 Años a Septiembre de 2014 (en %)

Riesgo y Retorno

Retorno

Global Stocks

(MSCI ACWI)

Hedge Funds

(CS)

Bonds (Barclays

Aggregate)

3 Month Libor

Riesgo

Global Stocks 1,00 0,83 0,09 -0,06

Hedge Funds 1,00 0,01 0,00

Bonds 1,00 0,01

3 Mo. Libor 1,00

Correlaciones

Fuente: Cliffwater. Why Hedge Funds, October 2014.

Global Stocks

(MSCI ACWI)

Hedge Funds

(CS)

Bonds (Barclays

Aggregate)

3 Month Libor

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 20

Rentabilidad Anualizada, Riesgo y Correlaciones, a 10 Años a Septiembre de 2014 (en %)

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 21

Hedge Fund performance in good and bad times

Fuente: Ezra Zask . All About Hedge Funds. Datos trimestrales de 1998 hasta el 2011.

Ret

urn

(%

)

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 22

¿Cual sería el Beta si se considera existencia de activos ilíquidos y que Hedge Funds pueden suavizar los movimientos en los precios?

Fuente: Asness Clifford; Krail, Robert; & Liew, John “Do Hedge Funds Hedge”. Portfolio Management Journal, Fall 2001.

Agg

rega

te

Hed

ge F

un

d

Co

nve

rtib

le

Arb

itra

ge

Even

t D

rive

n

Equ

ity

Mkt

N

eutr

al

Fix.

Inco

me

Arb

itra

ge

Lon

g/S

ho

rt

Equ

ity

Simple Beta

Summed Beta

Emer

gin

g M

arke

ts

Glo

bal

M

acro

Man

aged

Fu

ture

s

Ded

icat

ed

Sho

rt B

ias

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 23

¿Qué esperan los inversionistas de Private Equity?

Atractiva rentabilidad

Alta dispersión y persistencia de retornos entre gestores

Retornos de PE son cíclicos y mejores retornos se obtienen en ciclos malos

Baja correlación a largo plazo con mercados públicos

Mejora del perfil de riesgo/retorno de la cartera de inversión

Diversificación de la cartera de inversión

Gestión activa de cartera y de las empresas que la componen de parte de los gestores

Exposición a empresas que no transan en bolsa y más pequeñas

Sectores diferentes a los que tradicionalmente dominan el mercado (financials, telecom y utilities)

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 24

Estrategias de Private Equity

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 25

US Private Equity Index and Selected Benchmark Statistics (as of December 2014)

INDEX 5 YEARS 10 YEARS 15 YEARS 20 YEARS

Cambridge Associates LLC US Private Equity Index 15.80 12.90 10.87 13.50

Barclays Government/Credit Bond Index 4.69 4.70 5.79 6.24

Dow Jones Industrial Average Index 14.22 7.91 5.44 10.48

Dow Jones US Small Cap Index 16.38 9.16 8.94 11.31

Russell 1000 Index 15.64 7.96 4.62 10.04

Russell 2000 Index 15.55 7.77 7.38 9.63

S&P 500 Index 15.45 7.67 4.24 9.85

Fuente: Cambrige Associates LLC, Barclays, Dow Jones Indexes, Frank Russell Company, and Standard & Poor`s. Note: The Cambrige Associates LLC US Private Equity Index is an end-to-end calculation based on data compiled from 1.206 US private equity funds(buyout, growth equity, private equity energy and mezzanine funds), including fully liquidated partnerships, formed between 1986 and 2014. Pooled end-to-end return, net of fees, expenses, and carried interest.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 26

Retornos cíclicos de Private Equity

Fuente: Altamar Private Equity.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 27

Explicación del Outperformance

Principales Razones

Premios por Liquidez

Factores de Riesgo

omitidos Habilidad

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 28

Tabla de Contenidos

Inversiones Alternativas en Carteras de Institucionales

Tipos de Activos Alternativos

Oportunidades y Riesgos de los Activos Alternativos

Recomendaciones

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 29

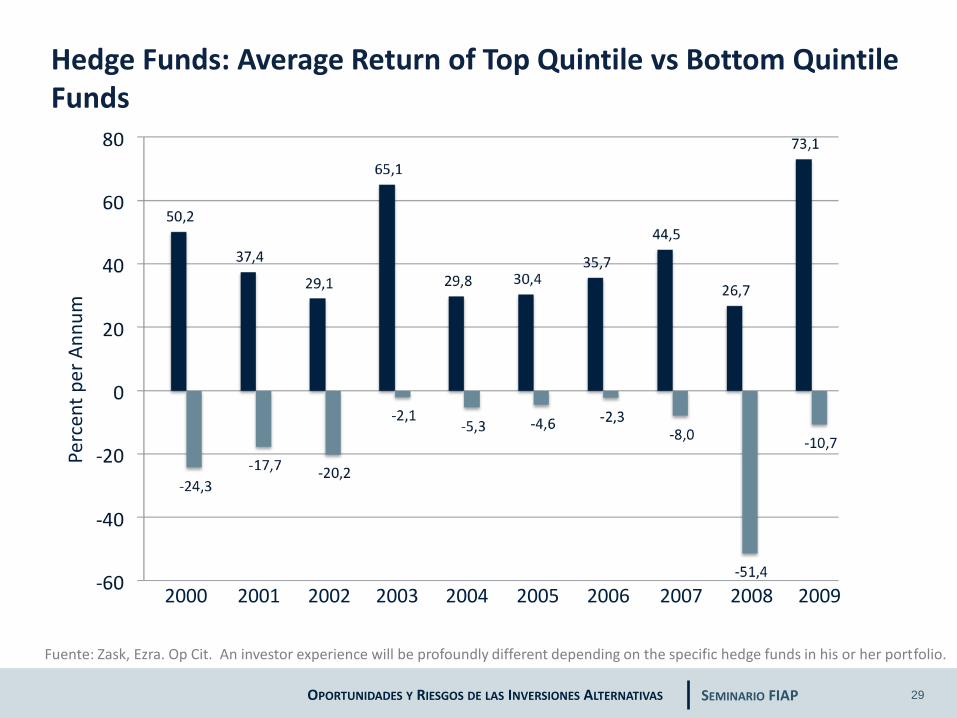

Hedge Funds: Average Return of Top Quintile vs Bottom Quintile Funds

Fuente: Zask, Ezra. Op Cit. An investor experience will be profoundly different depending on the specific hedge funds in his or her portfolio.

2000 2001 2002 2003 2004 2005

Perc

ent

per

An

nu

m

2006 2007 2008 2009

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 30

Retornos Históricos de Private Equity

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 31

Private Equity: Selecting the right fund managers is vital for generating alpha

Fuente: “Private Equity Study: Finding Alpha 2.0” Oliver Gottschalg, HEC-Paris; Golding Capital Partners, November 2011. Note: Analysis includes only fund managers with at least 20 realized transactions; analysis based on gross deal returns, not net of fees to LPs

Bottom 5%

Bottom 10%

Bottom 25%

Bottom 50%

Top 50%

Top 25%

PE

alp

ha

gen

erat

ed (

%)

Top 10%

Top 5%

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 32

¿Cómo invertir en buenos managers?

Fuente: Preqin.

Primer Cuartil Fondos

Segundo Cuartil Fondos

Tercer Cuartil Fondos

Cuarto Cuartil Fondos

The Succesor fund from a top quartile manager has a 40% likehood to become top quartile.

La consistencia en performance de los Top Manager es relativamente alta

1er Cuartil

2do Cuartil

3er Cuartil

4to Cuartil

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 33

Persistence of Private Equity appears to be slipping

Fuente: Preqin; Bain Analysis Note: Analysis includes buyout funds with investment region focus of North America, Central and South America, Western Europe, and Central and Eastern Europe; includes 125 fund pairings with the “predecessor fund’s vintage: 2000 and prior” and 93 fund pairings with the “predecessor fund’s vintage: 2001 and after”

Predecessor fund’s vintage 2000 and prior

Predecessor fund’s vintage 2001 and after

10 percentage Point drop in Top-quatile persistence

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 34

Over time, the way private equity creates value has shifted

Fuente: Goldman Sachs; BCG-IESE estimate.

Leverage Era (1980s)

Multiple Expansion Era (1990s)

Earnings Growth Era

(2000s)

Operational Improvement

Era (2010s)

Leverage

Multiple Arbitrge

Operational Improvement

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 35

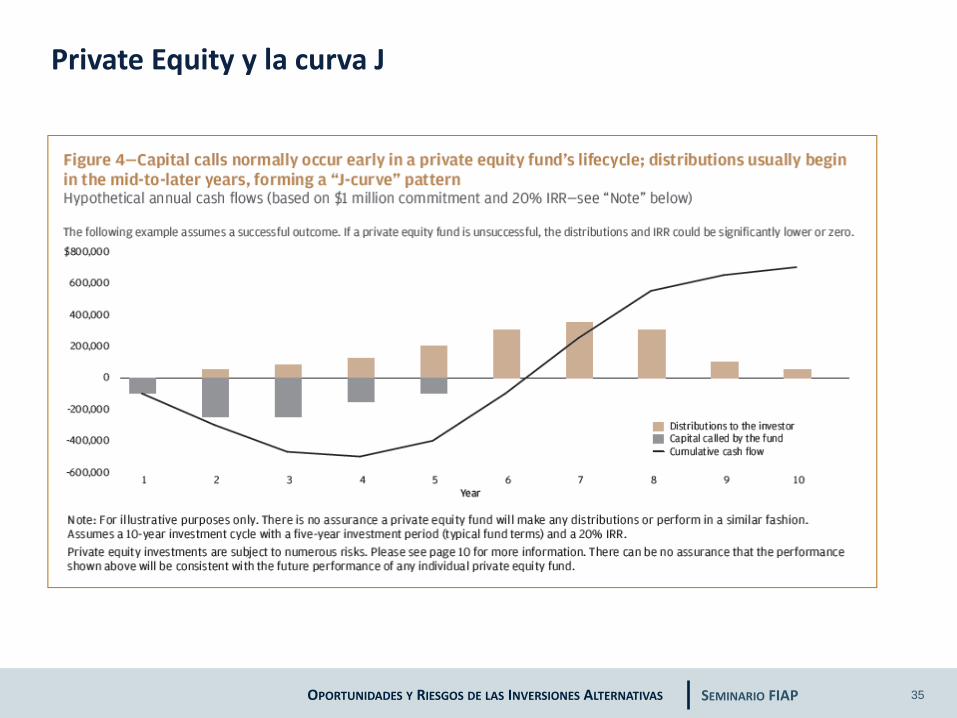

Private Equity y la curva J

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 36

Tabla de Contenidos

Inversiones Alternativas en Carteras de Institucionales

Tipos de Activos Alternativos

Oportunidades y Riesgos de los Activos Alternativos

Recomendaciones

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 37

Recomendaciones

Activos alternativos son populares entre inversionistas institucionales por cuanto contribuyen a mejorar el retorno y perfil de riesgo de un portafolio.

Tanto en el caso de Hedge Funds (HF) como en el de PE la selección de fondos es crucial. Se trata de elegir aquellos que en el futuro estarán el el primer cuartil

En el caso de los HF, los inversionistas deben considerar los riesgos asociados a la construcción del portafolio y a una mala selección de fondos. La falta de persistencia no facilita esta labor.

Una correcta construcción del portafolio debe considerar diversificación entre las diferentes estrategias de los HF. Incluir una o dos estrategias en el portafolio puede terminar aumentando el riesgo, ya que cada una de estas tiene su propio ciclo. Invertir a través de Funds of Funds puede ser una buena alternativa.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 38

Recomendaciones

En el caso de PE, la selección de gestores también es clave en el proceso. No es suficiente con utilizar el track record para seleccionar los fondos. También es necesario someter a los GP a un adecuado due diligence enfocado a conocer sus capacidades operacionales.

En el caso de los inversionistas institucionales, es importante moverse por la curva de aprendizaje: Fund of Funds, Buyouts, Midmarket, Growth Equity, etc. En mi opinión Venture Capital (VC) no constituye una sub clase de activo apropiada para institucionales.

El porcentaje a invertir en este tipo de fondos esta en alguna medida limitado por las necesidades de liquidez, no obstante la existencia de Fondos Secundarios.

Los Fondos Secundarios y en alguna medida los PE FoF permiten manejar la curva J por lo cual deben formar parte de los portafolios.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 39

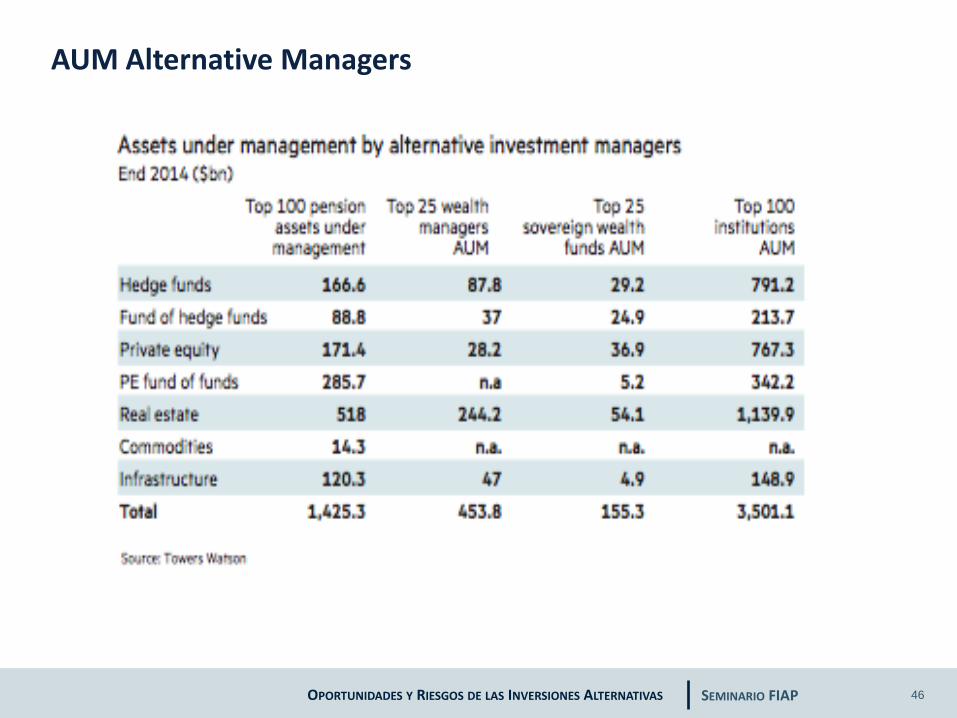

Principales Managers de Inversiones Alternativas en el Mundo

Nota: Considera los activos gestionados en Hegde Funds; Hedge Fund of Fund; Private Equity; Private Equity Fund of Fund; Real Estate; Infrastructure; & illiquid Credit. Cifras en US$ Billion. Fuente: Cliffwater 2015 Report on State Pension Fund Allocation and Performance. September 2015.

Blackstone

JP Morgan

Carlyle

UBS Global Ass.

Macquarie

Bridge Water

Goldman Sachs

CBRE

AXA

TPG

Oportunidades y Riesgos de las inversiones alternativas

Septiembre 2015

Joaquín Cortez H. Presidente Compañía de Seguros CorpVida S.A.

Anexos Oportunidades y Riesgos de las inversiones alternativas

Septiembre 2015

Joaquín Cortez H. Presidente Compañía de Seguros CorpVida S.A.

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 42

Return Private Equity versus Benchmarks

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 43

Return Private Equity versus Benchmarks

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 44

Return Private Equity

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 45

Return Private Equity

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 46

AUM Alternative Managers

OPORTUNIDADES Y RIESGOS DE LAS INVERSIONES ALTERNATIVAS SEMINARIO FIAP 47

Correlación con Otras Clases de Activos