Embed Size (px)

Citation preview

Ophir Energy plcAnnual Report and Accounts 2011

Ophir Energy plc A

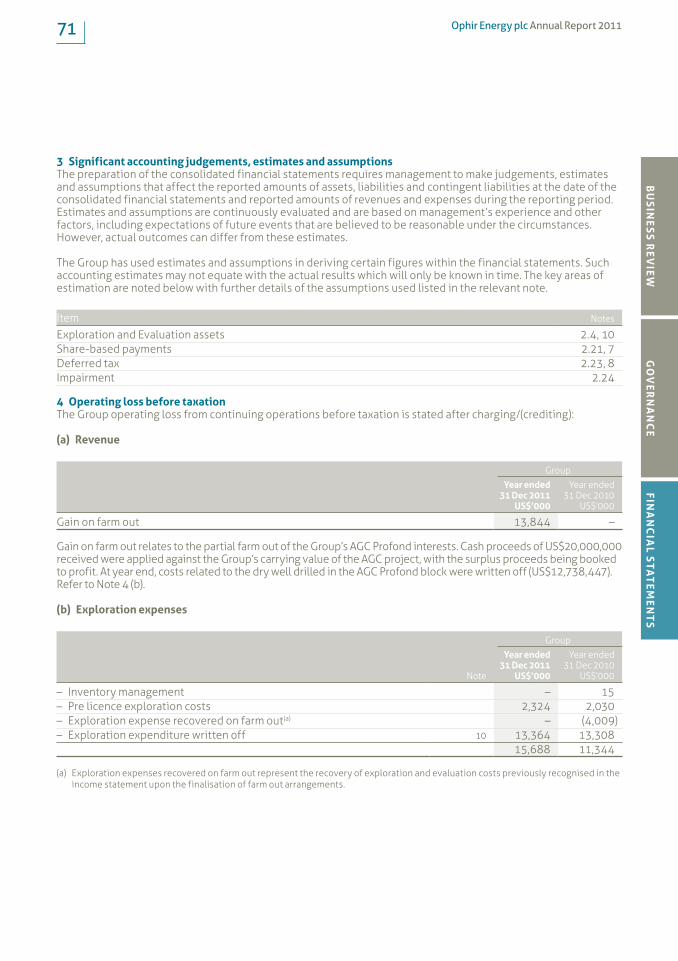

nnual Report and Accounts 2011

Ophir Energy plc is an international oil and gas exploration company with an extensive portfolio of interests spread across the continent of Africa.

Business Review01 Key highlights02 Chairman’sandChiefExecutiveOfficer’s

Joint Review06 Our strategy08 Review of operations20 Financial review22 Corporate and Social Responsibility26 Principal risks and uncertainties

Governance28 Board of Directors30 Corporate Directory31 Directors’ Report35 Corporate Governance Report45 Remuneration Report53 Statement of Directors’ Responsibilities54 Independent Auditor’s Report

Financial statements56 Group income statement and statement

of comprehensive income57 Group statement of changes in equity58 Company statement of changes in equity59 Groupstatementoffinancialposition60 Companystatementoffinancialposition61 Groupstatementofcashflows62 Companystatementofcashflows63 Notestothefinancialstatements91 Shareholder information

Ophir Energy plc Annual Report 201101B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

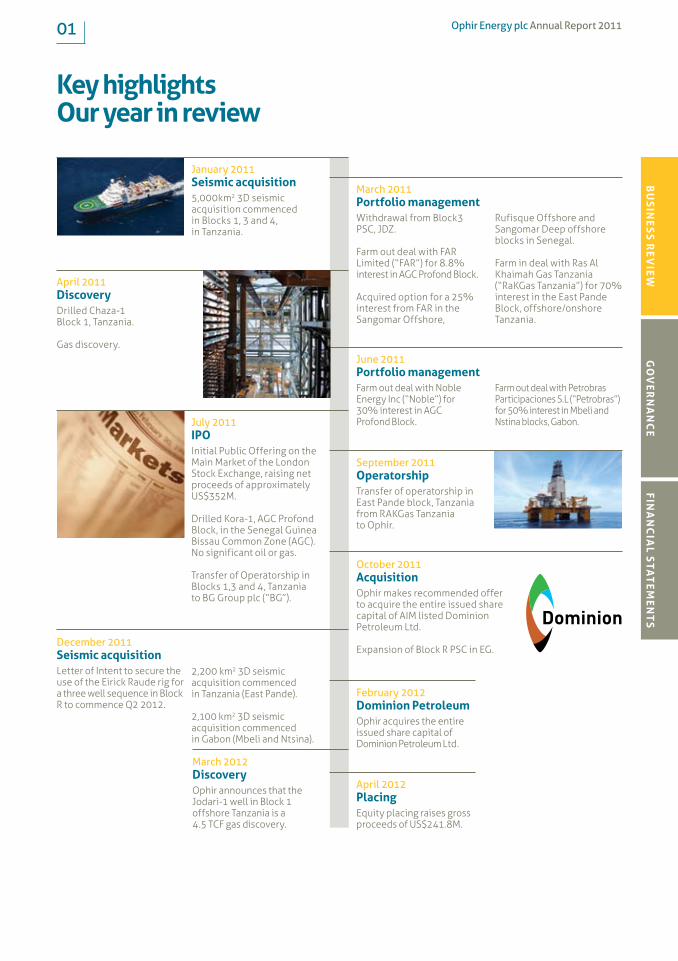

Key highlightsOur year in review

March 2011Portfolio managementWithdrawal from Block3 PSC, JDZ.

Farm out deal with FAR Limited (“FAR”) for 8.8% interest in AGC Profond Block.

Acquired option for a 25% interest from FAR in the Sangomar Offshore,

Rufisque Offshore and Sangomar Deep offshore blocks in Senegal.

Farm in deal with Ras Al Khaimah Gas Tanzania (“RaKGas Tanzania”) for 70% interest in the East Pande Block, offshore/onshore Tanzania.

January 2011Seismic acquisition5,000km2 3D seismic acquisition commenced in Blocks 1, 3 and 4, in Tanzania.

April 2011DiscoveryDrilled Chaza-1 Block 1, Tanzania.

Gas discovery.June 2011Portfolio managementFarm out deal with Noble Energy Inc (“Noble”) for 30% interest in AGC Profond Block.

Farm out deal with Petrobras Participaciones S.L (“Petrobras”) for 50% interest in Mbeli and Nstina blocks, Gabon.

September 2011OperatorshipTransfer of operatorship in East Pande block, Tanzania from RAKGas Tanzania to Ophir.

July 2011IPOInitial Public Offering on the Main Market of the London Stock Exchange, raising net proceeds of approximately US$352M.

Drilled Kora-1, AGC Profond Block, in the Senegal Guinea Bissau Common Zone (AGC). No significant oil or gas.

Transfer of Operatorship in Blocks 1,3 and 4, Tanzania to BG Group plc (“BG”).

2,200 km2 3D seismic acquisition commenced in Tanzania (East Pande).

2,100 km2 3D seismic acquisition commenced in Gabon (Mbeli and Ntsina).

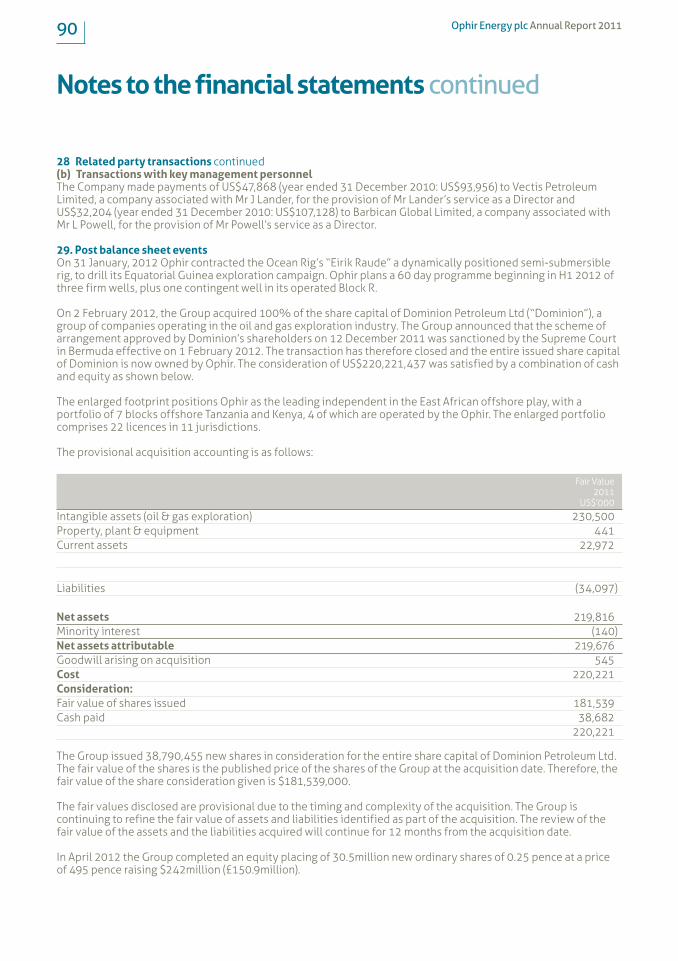

February 2012Dominion PetroleumOphir acquires the entire issued share capital of Dominion Petroleum Ltd.

October 2011AcquisitionOphir makes recommended offer to acquire the entire issued share capital of AIM listed Dominion Petroleum Ltd.

Expansion of Block R PSC in EG.December 2011Seismic acquisitionLetter of Intent to secure the use of the Eirick Raude rig for a three well sequence in Block R to commence Q2 2012.

April 2012PlacingEquity placing raises gross proceeds of US$241.8M.

March 2012DiscoveryOphir announces that the Jodari-1 well in Block 1 offshore Tanzania is a 4.5 TCF gas discovery.

Ophir Energy plc Annual Report 201102

mitigated through a series of farm out agreements. In 2012 the Group is undertaking the busiest drilling programme in its history, with drilling continuing in Tanzania, a rig procured for an imminent programme in Equatorial Guinea and nine wells expected to be spudded by the end of the year. The Group has recently announced the results of the Jodari-1 well drilled during January and February 2012. This was the first well drilled with BG as operator and resulted in the Group’s fourth successive, and largest in the Group’s history, gas discovery in its Tanzania blocks with a recoverable resource estimate of 3.4 TCF. Preparations are also underway for a 12 well programme in 2013. Ophir ended 2011 with net contingent (2C) resources of 210 mmboe and net risked prospective resources of 1,882 mmboe.

Portfolio ManagementOphir continues to actively manage its portfolio to best deploy its capital resources against the most prospective acreage and plays. In 2011 the Group farmed out interests in the Mbeli and Ntsina licences in Gabon to Petrobras and an interest in the AGC Profond licence to Noble Energy. The Group acquired interests in the East Pande licence in Tanzania by way of a farm in agreement with RAKGas and acquired five further exploration interests via the Dominion transaction in Block 7 (Tanzania), Blocks L9 and L15 (Kenya), Area 4B (Uganda) and Block 5 (DRC). Ophir currently has interests in 22 licences in 11 countries and jurisdictions, 14 of which are operated, 18 of which are offshore and 4 of which are onshore.

Chairman’s and Chief Executive Officer’s Joint Review

2011 was dominated by Ophir’s IPO, which raised a total of US$384 million inclusive of the greenshoe. The IPO provided the Group with a strong cash position of US$396.6 million at year end.

Corporate Overview2011 saw Ophir successfully list on the main board of the London Stock Exchange. Ophir joined the FTSE 250 in November 2011. The IPO was set against a backdrop of turbulent capital markets and relatively low levels of new equity issuance and Ophir ended the year as the best performing IPO stock for 2011.

In October 2011 Ophir announced a proposal to acquire the share capital of AIM-listed Dominion Petroleum Ltd in an all-stock transaction. The acquisition closed in February 2012 and expanded

the Group’s portfolio in East Africa via the addition of five exploration licences, with three being complementary to Ophir’s existing deepwater portfolio. As a result Ophir now has one of the largest portfolios of operated and non-operated acreage in the exciting emerging offshore East African play.

Operationally, 2011 saw two wells completed. The Chewa-1 well in Tanzania was the third in a series of back-to-back gas discoveries in Tanzania. The Kora-1 well in the AGC joint development area was unsuccessful but costs were

Ophir Energy plc Annual Report 201103B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

Financial2011 was dominated by Ophir’s IPO, which raised a total of $384 million inclusive of the greenshoe. The IPO provided the Group with a strong cash position of $396.6 million at year end. A further equity placing in April 2012 raised an additional gross US$242 million. We are fully funded to finance the planned exploration programmes for the next 12 months.

Board, Management and StaffThe evolution of Ophir’s Board during 2011 reflects the transition to being a public company. During 2011 Dr Nick Cooper, Mr Ron Blakely and Mr Patrick Spink joined the Board while Mr Rajan Tandon appointed Mr Jaroslaw Paczek as his alternate. At IPO Mr Michael Cohen, Mr Mikki Xayiya left the Board, Ms Yvonne Holm and Mr John Morgan left later in the year. On behalf of the Board and shareholders the Chairman has thanked those that served on the Board for their contributions and has welcomed those that join the Board as we embark upon the next stage in Ophir’s growth.

Ophir’s senior management team was expanded in June 2011 with the appointment of Dr Nick Cooper as Chief Executive Officer, replacing Dr Alan Stein who held that position since formation of the Group in 2004. Alan remains an active member of the executive team but has signalled his intention to step down from the Board after the Annual General Meeting (“AGM”) in June 2012. In December 2011, Yvonne Holm resigned from her position of Chief Financial Officer and Director, and in January 2012, Lisa Mitchell, previously Ophir’s Group Financial Controller, was appointed as CFO.

At the heart of our Group is a small yet dedicated and extremely professional group of staff and associates who have consistently delivered outstanding performance.

This last year has seen the team raise the bar once again. Their tireless efforts might sometimes pass without comment but they are always appreciated. On behalf of the Board and shareholders we would like to offer them our thanks and admiration for another outstanding year for the Group.

This year of performance has been delivered without compromising on safety and we are pleased to report no lost time accidents or reported incidents across the diverse range of operations undertaken across the African continent in often challenging conditions.

Corporate ResponsibilityCorporate Responsibility forms a key part of Ophir’s operating culture. The Group strives to make a positive impact in the development of the countries in which it operates. Ophir’s goal is to establish a sustainable, balanced approach to its business which includes assisting local communities wherever possible through such initiatives as education, protection of the environment and the creation of broad, lasting economic development. We understand that by taking a pragmatic, long-term, positive approach to corporate responsibility it will provide lasting dividends to the Group and the countries in which we operate.

Ophir Energy plc Annual Report 201104

Chairman’s and Chief Executive Officer’s Joint Review continued

At the heart of our Company is a small yet dedicated and extremely professional group of staff and associates who have consistently delivered outstanding performance.

In Tanzania, Ophir has continued to be actively involved in the development of Mtwara port (and its attendant services). Ophir was responsible for the initial development of this facility in partnership with the Tanzanian authorities. In 2011 the port development scheme expanded rapidly as more oil and gas operating companies joined Ophir, resulting in the transformation of a previously underutilised port into a thriving operations base which has subsequently received ‘Duty Free’ status to underscore its importance

to the development of the Mtwara region. There has been a large positive impact in the local economy as the community shares in this development through training, employment and improved infrastructure. In December 2011, parts of the main city of Dar es Salaam suffered severe flooding, making many citizens homeless. Ophir assisted relocation efforts by swiftly donating 30 large water storage tanks to the victim’s resettlement site. This initiative secured adequate sanitation and was vital to reduce disease risk for the flood victims whilst in their temporary accommodation.

In Equatorial Guinea, Ophir continued its support of a nursery school in the village of Ebein Yenkeng. The Group also donated funding for a training seminar on social content which was provided to members of the Ministry of Mines, Minerals and Energy (“MMIE”) in Malabo. In addition, Ophir contributes to the Equatorial Guinean Hydrocarbon Technological Institute Educational Programme (“ITNHGE”), a collaborative educational initiative run for the benefit of adult students in Equatorial Guinea.

OutlookThe oil and gas industry’s focus on African exploration has risen dramatically in 2011 and early 2012. The pace of activity on both the East African offshore gas play and the West African pre-salt play have increased as major oil companies have entered the region and made significant discoveries. This has had important implications for Ophir’s portfolio.

In the East African gas play Anadarko and ENI are reported to have discovered more than 40 TCF of gas in Mozambique with the majority being found in extensive basin floor fans. This play has not yet been tested in Ophir’s Tanzanian acreage but it is thought to potentially extend into Block 1 and possibly Block 3. A new 3D seismic survey is currently being acquired in Block 1 to test this concept and initial results are anticipated mid-year.

Ophir Energy plc Annual Report 201105B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

In the adjacent Tanzania Block 2 Statoil’s recent Zafarani-1 discovery appears to have de-risked elements of the deeper Cretaceous play potential within Ophir’s acreage. Some of the wells in Ophir’s 2012 drilling programme will also test these deeper plays.

The industry’s appetite for the East African offshore gas play has been clearly demonstrated by the competitive bidding to acquire AIM-listed Cove Energy which has an 8.5% stake in the Anadarko operated block in Mozambique, to the south of BG/Ophir’s Block 1. If this appetite is sustained then it affords Ophir a degree of flexibility both in the way that it finances its exploration and appraisal activities in the play and in the way that it secures value for shareholders.

The Group now has one of the largest offshore acreage footprints in East Africa. In addition to the wells currently being drilled by the Ophir/BG joint venture in Blocks 1, 3 and 4, offset wells with relevance to Ophir acreage will be drilled in the next few months by Petrobras and Statoil in Tanzania, Anadarko and ENI in Mozambique and Apache in Kenya.

In West Africa, considerable recent success has occurred in the deepwater pre-salt play with notable successes by both Cobalt and Maersk in Angola. Ophir has a strong acreage position in this deepwater play, with four licences in Gabon and one in Congo-Brazzaville. In Gabon, the Group has recently completed two seismic programmes that will support both a pre-salt well with Petrobras in late 2012 on the Mbeli and Ntsina licences and also potential farm outs of the Manga and Gnondo licences.

In 2012 Q2, the Group will commence a three well programme in Equatorial Guinea targeting further gas discoveries to aggregate into an LNG development. Already the Group is planning for a further 12 well programme in 2013 contingent on additional financing.

The outlook for Ophir in 2012 is promising. The Group enters 2012 with an extensive portfolio of interests across some of the most interesting exploration plays in Africa. The Group is well placed to meet its exploration and appraisal forecast expenditure for at least the next 12 months.

Ophir Energy plc Annual Report 201106

Our strategy

Ophir Energy plc Annual Report 201107B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

Experienced and motivated management teamOphir has recruited and retained an experienced and motivated group of senior staff with a view to identifying attractive investment opportunities, decreasing exploration risk and adding value to its portfolio through the application of advanced geoscience technology.

Control over the pace and direction of explorationThe Company has, wherever practical, sought to accelerate its exploration activities, while maintaining high professional and corporate responsibility standards, demonstrating its commitment to realising value from its assets in a timely fashion on behalf of its shareholders and partners. The Company believes that continuation of this approach will enhance its ability to win new business in the future.

Active portfolio managementThe Company’s preference is to take significant initial interests in core projects whilst retaining the flexibility to divest by way of farm out or exchange of interests as the project matures if deemed appropriate.

The Company intends to expand its portfolio through investing in new ventures, particularly where the application of advanced geoscience technology can add significant value through the reduction of exploration risk.

In keeping with the Directors’ intentions to establish Ophir as a pre-eminent independent African energy company, Ophir expects to participate to the extent considered appropriate in the development of its petroleum discoveries with a view to establishing itself as a major oil and/or gas producer in the region.

The Company also periodically evaluates opportunities to acquire producing or near-producing assets that would complement its exploration portfolio.

Establish relationships in AfricaOphir’s overarching strategy has been to establish itself as a pre-eminent independent African energy company. The Company has access to an extensive network of relationships in Africa. In combination with these and the geoscience and commercial expertise of its management, the Company has acquired and developed an extensive portfolio of oil and gas interests in Africa.

Ophir Energy plc Annual Report 201108

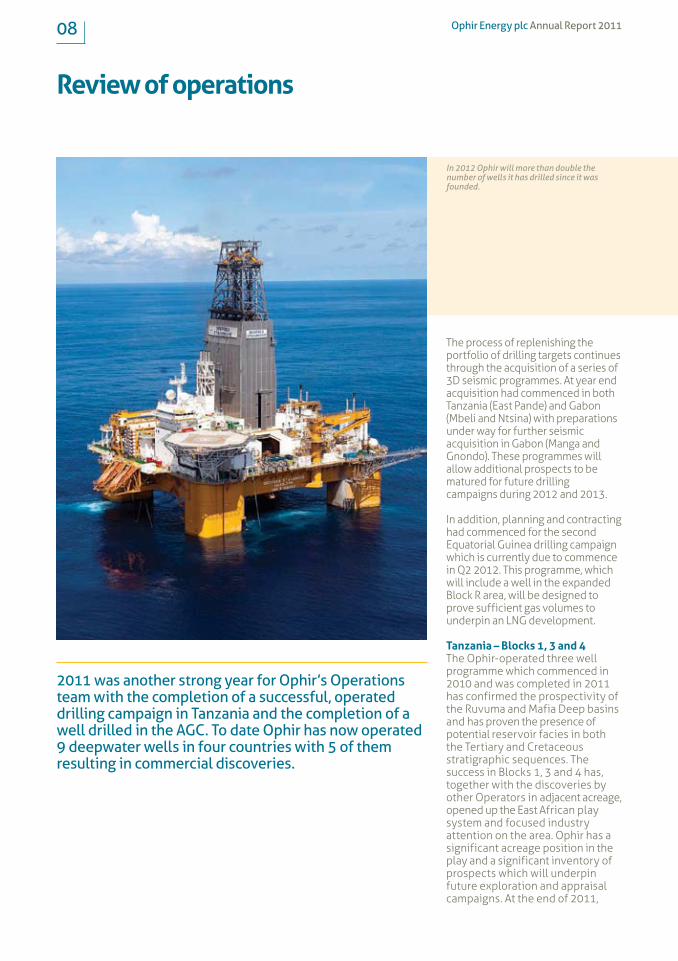

The process of replenishing the portfolio of drilling targets continues through the acquisition of a series of 3D seismic programmes. At year end acquisition had commenced in both Tanzania (East Pande) and Gabon (Mbeli and Ntsina) with preparations under way for further seismic acquisition in Gabon (Manga and Gnondo). These programmes will allow additional prospects to be matured for future drilling campaigns during 2012 and 2013.

In addition, planning and contracting had commenced for the second Equatorial Guinea drilling campaign which is currently due to commence in Q2 2012. This programme, which will include a well in the expanded Block R area, will be designed to prove sufficient gas volumes to underpin an LNG development.

Tanzania – Blocks 1, 3 and 4The Ophir-operated three well programme which commenced in 2010 and was completed in 2011 has confirmed the prospectivity of the Ruvuma and Mafia Deep basins and has proven the presence of potential reservoir facies in both the Tertiary and Cretaceous stratigraphic sequences. The success in Blocks 1, 3 and 4 has, together with the discoveries by other Operators in adjacent acreage, opened up the East African play system and focused industry attention on the area. Ophir has a significant acreage position in the play and a significant inventory of prospects which will underpin future exploration and appraisal campaigns. At the end of 2011,

Review of operations

2011 was another strong year for Ophir’s Operations team with the completion of a successful, operated drilling campaign in Tanzania and the completion of a well drilled in the AGC. To date Ophir has now operated 9 deepwater wells in four countries with 5 of them resulting in commercial discoveries.

In 2012 Ophir will more than double the number of wells it has drilled since it was founded.

Ophir Energy plc Annual Report 201109B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

these are believed to contain more than 30TCF1 in gross un-risked prospective resources.

Each of the three Tanzanian deepwater wells have demonstrated the presence of multiple play systems, all with significant follow-up potential. Although each has encountered gas, the Group believes that, based upon detailed technical studies, liquids are also possible in the future. These studies have characterised a number of potential hydrocarbon source rocks, ranging in age from Permo-Triassic to Eocene. The three wells drilled to date have targeted the centre of the basin, where the main source intervals have been buried to a sufficient depth to generate gas (the “gas window”). To the east and west of this, the Group believes that the source intervals are less deeply buried and thus cooler. In these areas (the so-called “oil window”) the organic rich material (“kerogens”) in the rock may have generated liquids.

The Ophir-operated “Deepsea Stavanger” drilling campaign, which had commenced in 2010, continued into 2011 with further success at Chaza-1 in Block 1. The well was drilled in 982m of water, reached a TD at a depth of 4,933m and was completed as the third consecutive successful gas discovery in the programme. Chaza-1 encountered a gross 27m gas column in a Miocene channel system and, together with the discoveries at Pweza-1 and Chaza-1, takes the total contingent resources discovered in Blocks 1, 3 and 4 to 2.4TCF with a further 1.6TCF of low risk prospective resources.

1 Management estimate

Ophir Energy plc Annual Report 201110

Review of operations continued

Each of the three discoveries had an associated amplitude seismic anomaly which was interpreted to be a Direct Hydrocarbon indicator (“DHI”). Data from the wells has now been used to further calibrate the seismic attributes. This analysis will be used to further de-risk the exploration portfolio and focus the future drilling programme.

Blocks 1, 3 and 4 are large, with a combined area of more than 20,000km2 after the statutory relinquishments. The original 3D Kusini and Mafia 3D seismic programme covered 3,500km2 and delineate only a small portion of the possible play types. As a consequence a further seismic acquisition programme was planned outboard of the Mafia survey in Blocks 3 and 4 across the “Seagap Ridge”, a long-lived feature within the basin which it is believed could be the focus of both oil and gas generation and

migration. A further survey was also planned northwest of the Kusini survey in Block 1 to test the extension of the play system proven by Chaza-1. The second seismic programme operated by Ophir, which utilised the Fugro “GeoCaspian” vessel, commenced during January 2011 with acquisition of the Mafia East seismic survey in Blocks 3 and 4 where 3,250km2 of data were acquired in 44 days. The vessel subsequently moved to Block 1 where it acquired 1,900km2 of data in 35 days on the Kusini extension survey. The programme was completed on 8 April 2011 and the GeoCaspian released with no LTIs or security-related incidents. Pre-stack Depth Migration processing of these surveys was completed during the year and the data has been used to mature additional exploration prospects for inclusion in future drilling campaigns. Even after these new surveys, less than half the area

of the three PSAs has been covered with 3D data and further seismic acquisition is anticipated during 2012.

The Group was originally awarded a 100% interest in Block 1 on 29 October 2005. Blocks 3 and 4 were subsequently awarded on 19 June 2006, again on a 100% basis. TPDC has back-in rights of 12% in Block 1 and 15% in Blocks 3 and 4.

In April 2010 the Group entered into a farm out agreement with BG Group for a 60% interest in each Block, with Ophir retaining the remaining 40%. Under the terms of the farm out agreement BG had the right to take over Operatorship after the completion of the first three wells and the Mafia East/Kusini Extension 3D seismic acquisition programme and consequently on 1 July 2011 operatorship of all three Blocks was formally transferred to BG. As part of this arrangement

Ophir Energy plc Annual Report 201111B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

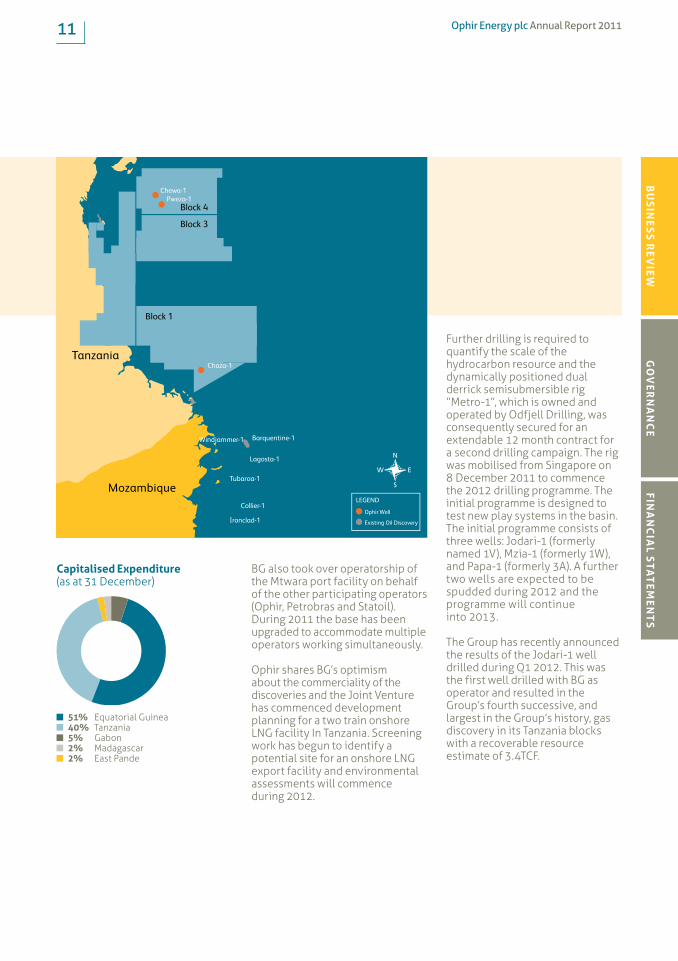

BG also took over operatorship of the Mtwara port facility on behalf of the other participating operators (Ophir, Petrobras and Statoil). During 2011 the base has been upgraded to accommodate multiple operators working simultaneously.

Ophir shares BG’s optimism about the commerciality of the discoveries and the Joint Venture has commenced development planning for a two train onshore LNG facility In Tanzania. Screening work has begun to identify a potential site for an onshore LNG export facility and environmental assessments will commence during 2012.

Further drilling is required to quantify the scale of the hydrocarbon resource and the dynamically positioned dual derrick semisubmersible rig “Metro-1”, which is owned and operated by Odfjell Drilling, was consequently secured for an extendable 12 month contract for a second drilling campaign. The rig was mobilised from Singapore on 8 December 2011 to commence the 2012 drilling programme. The initial programme is designed to test new play systems in the basin. The initial programme consists of three wells: Jodari-1 (formerly named 1V), Mzia-1 (formerly 1W), and Papa-1 (formerly 3A). A further two wells are expected to be spudded during 2012 and the programme will continue into 2013.

The Group has recently announced the results of the Jodari-1 well drilled during Q1 2012. This was the first well drilled with BG as operator and resulted in the Group’s fourth successive, and largest in the Group’s history, gas discovery in its Tanzania blocks with a recoverable resource estimate of 3.4TCF.

Capitalised Expenditure (as at 31 December)

51% Equatorial Guinea 40% Tanzania 5% Gabon 2% Madagascar 2% East Pande

Ophir Energy plc Annual Report 201112

Review of operations continued

Tanzania – East PandeOphir completed its farm in to the 7,500km2 East Pande Block on 29 March 2011. The Group now holds 70% equity, with Rakgas holding the remaining 30%, and Ophir has assumed operatorship of the Block. East Pande lies to the west of Blocks 1, 3 and 4 and is believed to contain the up-dip extension of the currently identified Tertiary and Cretaceous intraslope play systems, some of which have been proven in the deep water. Regional geoseismic studies suggest that the East Pande Block’s location towards the rim of the basin may be too mature for liquids and gas generation.

The 2D seismic data coverage in the Block is sparse at present although a number of potentially attractive leads have been identified at different stratigraphic levels. These leads are potentially large

with volume estimates in excess of 500mmbbls but are currently high risk due to the limited data coverage. A 12 month extension to the permit term was granted to allow Ophir sufficient time to acquire, process and interpret a 3D seismic survey with a view to entering the next PSA term and a future drilling programme.

At year end the contracting process was completed and Fugro were mobilising the MV “Geo Caribbean” to acquire a 2,100km2 3D survey. Data from this survey should be available in the first half of 2012 to facilitate a drilling campaign late in 2012 or early in 2013. Any discoveries in East Pande are likely to be close to the export pipeline which will be used to transport gas to any future onshore LNG plant supplied from Blocks 1, 3 and 4.

Tanzania

The success in Blocks 1, 3 and 4 has, together with the discoveries by other Operators in adjacent acreage, opened up the East African play system and focussed industry attention on the area.

Ophir Energy plc Annual Report 201113B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

Equatorial Guinea – Block RBlock R is located in the south eastern part of the Niger Delta, close to numerous oil and gas discoveries in the Nigerian sector. The licence, which covered an area of 1,674km2 at the start of 2011, was originally awarded in April 2006. Ophir drilled three wells on the Block in 2008, two of which (Fortuna-1 and Lykos-1) were commercial gas discoveries. The discoveries at Fortuna (269bcf of contingent resources, 572bcf of risked prospective resources) and Lykos (91bcf of contingent resources, 60bcf of risked prospective resources) have substantially de-risked a new play fairway at the front of the Niger Delta thrust belt. These discoveries, together with the additional 10TCF of unrisked prospective resources which had been identified prior to the addition of the former Block C, will, it is believed, be sufficient for a commercial export gas development. The gas is dry, with no CO2 or H2S, making it ideal for liquefaction.

Equatorial Guinea has an established 3.4mmtpa LNG plant at Punta Europa (EGLNG 1) that is operated by Marathon with Sonagas, Mitsui and Marubeni as JV partners. Gas is transported from the Alba Field (Operated by Marathon with Gepetrol as a JV partner) by pipeline to the Punta Europa plant and the resulting LNG is sold to BG through a sale and purchase agreement where it is marketed to the Far East. The Government of Equatorial Guinea believe that sufficient gas has been discovered in the country to warrant a second LNG train and have publicly expressed their support for a second onshore plant, to be built adjacent to Train 1. The feedstock gas for this is likely to come principally from Block R, although the recent discoveries which have been made by Noble Energy in Block I may provide additional gas to the project over time.

Equatorial Guinea

Significant progress was made during 2011 on the commercialisation of the Fortuna and Lykos gas discoveries.

The necessary infrastructure and services are already being assembled in country to provide the support for the next phase of operations in Equatorial Guinea.

Ophir Energy plc Annual Report 201114

Significant progress was made during 2011 on the commercialisation of the Fortuna and Lykos gas discoveries. The Government of Equatorial Guinea (“GEG”) has established a project delivery team (“PDT”) which will be accountable for ensuring that the gas resources in the country are developed effectively. This team consists of representatives from the MMIE, the National Oil Company (GePetrol) and the National Gas Company (Sonagas). A Memorandum of Understanding (“MoU”) was signed on 31 March 2011 by the relevant stakeholders, including Ophir, committing to support the favoured development plan, which would see gas from Block R transported by a sub-sea pipeline to a newly constructed second LNG train at Punta Europa on Bioko Island. Subsurface and engineering studies have commenced on this.

To increase commercial optionality, Ophir has also explored the possibility of an alternative development utilising floating LNG (“FLNG”) technology. The dry nature of the gas, together with the benign metocean conditions in the Gulf of Guinea, makes this an ideal location for such a development. Ophir believes that FLNG technology is now sufficiently advanced to provide a viable alternative to a conventional onshore LNG scheme. It will continue to be carried as an alternate option

until the project Final Investment Decision (“FID”) which is currently planned for 2013. The current exploration term was extended by 12 months and now expires on 18 April 2013. This provides additional time for Ophir to carry out further exploration and appraisal drilling prior to the end of the exploration period. A further step in the commercialisation process occurred in November 2011 when Block C (located to the northwest of Block R) was appended to Block R. The additional new acreage, which covers an area of 773km2, increases the area of Block R to 2,447km2. The acreage had previously been relinquished by Repsol and Exxon and includes two gas discoveries (Oreja Marina and Estrela del Mar which together contain c. 250bcf of dry gas) as well as the Tonel prospect with prospective resources of 510bcf. Ophir has committed to drill a three well programme, including the Tonel prospect. The additional acreage increases the portfolio of drilling options available to Ophir as well as providing additional proven gas resources. These will

provide greater flexibility in reaching the 2.5TCF threshold volume which is believed to be necessary to commit to a Train 2 development.

At year end preparations were underway for a second drilling campaign which is expected to commence in Q2 2012. The sixth generation deepwater drill rig the “Eirik Raude” and ancillary services have been secured. The programme is likely to consist of 3 firm and one contingent well covering a mix of both exploration and appraisal targets.

Ophir has been able to retain a high equity in the project and now believes that 2012 will be the appropriate time to bring in a suitably qualified joint venture partner. Preliminary approaches have been received from a number of companies and it is hoped that a farm out will be concluded after the 2012 drilling programme.

Review of operations continued

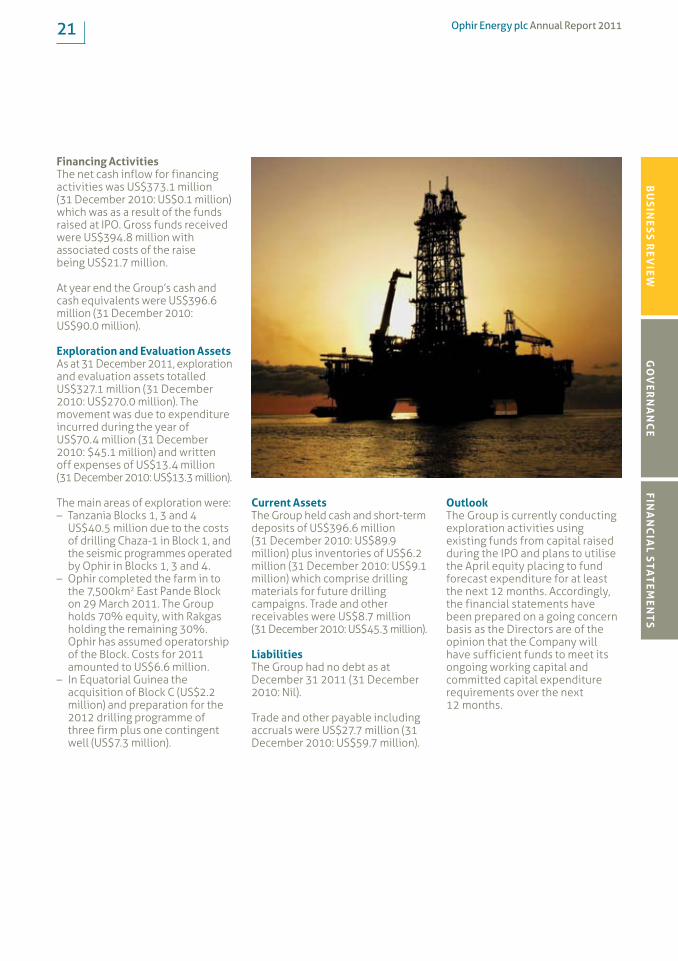

At year end preparations were underway for a second drilling campaign which is expected to commence in Q2 2012.

Ophir and its partners are using state-of-the-art rigs to drill safely and effectively in deep water.

Ophir Energy plc Annual Report 201115B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

migration” (“PSDM”) processing of the data which will take much of 2012 to complete. The terms of the Ntsina and Mbeli PSC’s will end in February 2014, allowing sufficient time to fully explore the pre-salt play.

Gabon – Manga, GnondoThe pre-salt play has more limited extent southward into Manga and Gnondo where the focus is instead on the post-salt stratigraphic section. Recent discoveries in Brazilian waters, in particular Petrobras’ 2010/11 Barra discovery, suggest that this play could have analogues in the North Gabon basin. The 3D seismic data is currently limited, particularly in the potentially attractive area to the west of the Loiret Dome where a series of stratigraphic onlap plays have been identified and leads identified. One of these, the Afo

structure, has the potential to be volumetrically significant. Ophir has consequently undertaken a 3D seismic programme in Manga in early 2012 to mature these into drillable prospects. The play system also extends into the southern part of the Ntsina Block and the 3D survey has extended into this Block.

Gabon – Ntsina, MbeliThe focus of exploration in Ntsina and Mbeli has switched to the pre-salt play which has recently come to prominence through a series of world-class discoveries in Brazil, and early in 2012 on the conjugate margin in Angola. Across the conjugate margin from Gabon, is Petrobras’ Carmopolis Field, with an estimated 1.7Bbbls in place. Until now, exploration of the pre-salt play in the North Gabon basin has been restricted by poor seismic imaging. Recent advances in seismic imaging technology now allow pre-salt traps to be effectively mapped.

Seismic and gravity gradiometry surveys have delineated a potentially significant pre-salt play system in the Blocks. The main focus of the seismic acquisition has been the Padouck Deep prospect which has the potential to contain ca. 1.3Bbbls. Based upon the relative immaturity of the play, Ophir elected to bring a JV partner with significant pre-salt experience and consequently concluded a farm out to Petrobras for 50% equity in each Block. Under the terms of the agreement Petrobras is funding the cost of a new 2,200km2 seismic survey designed to image the pre-salt play system. The survey has been acquired by PGS early in 2012 and a key component of this programme will be detailed “pre-stack depth

Gabon

Recent advances in seismic imaging technology now allow pre-salt traps to be effectively mapped. The main focus of the seismic acquisition has been the Padouck Deep prospect which has the potential to contain ca. 1.3Bbbls.

Ophir Energy plc Annual Report 201116

Review of operations continued

Acquisition of the two 3D surveys was completed in January 2012. Processed data will be available in early 2013. Once this has been interpreted a farminee will be sought for the next stage, to include potential drilling in 1H 2013.

AGC – AGC ProfondTwo farm outs were completed in 2011; the first of these was for 8.8% equity to FAR Limited in March 2011 with a further 17.5% being divested to Noble Energy in June 2011. The terms of these farm outs included promoted contributions to the costs of the first well on the Block, Kora-1 (up to a gross first well cost of $40 million, and should they elect to participate in petroleum operations, a promoted amount of the costs of any second well (uncapped) and US$35 million of appraisal expenditure on Ophir’s behalf).

The Kora-1 well was drilled to a total depth of 4,447.5mSS on 27 July 2011 and the rig was subsequently released on 31 July 2011 with no LTIs. The primary (Albian) and secondary (Coniacian and Barremian) reservoir intervals were penetrated close to their anticipated depths, but the well encountered a predominantly claystone and thinly bedded limestone sequence, rather than the prognosed sandstone reservoir facies. The well was plugged and abandoned and the technical assessment will continue through the first half of 2012 to characterise the remaining potential of the Block ahead of a drill or drop decision in mid-2012.

The Pachg Liba prospect, in the Gnondo block, is covered by a limited amount of 2D seismic data which, to this point, has precluded it from being matured to a drilling target. Acquisition of a prospect-specific 3D seismic survey would be very cost inefficient unless it can be included as part of a wider survey. The activity in the other Ophir-Operated Gabon blocks has allowed this survey to be included as part of the larger programme recorded in early 2012.

Ophir has undertaken a 3D seismic programme in Manga in early 2012 to mature these into drillable prospects.

AGC Profond

Ophir Energy plc Annual Report 201117B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

Somaliland – Block SL9 (Berbera)During 2011 Ophir’s geotechnical team continued its interpretation of the existing legacy data on Block SL9 and to fully integrate surface geological information with the seismic data which covers the Block. This will be used to determine possible future drill locations.

Ophir has continued to work closely with the Government of Somaliland to adapt the Petroleum Sharing Contract to reflect the expected work programme prior to the Group taking on a drilling commitment on the Block. The agreed amendments include the extension of the block via the addition of a vacant Block to the west of the Ophir acreage.

SADR – Daora, Haouza, Mahbes, MijekOphir continues to monitor activities and opportunities in SADR.

Congo-Brazzaville (Marine IX)

Congo-Brazzaville – Marine IXOphir assumed the role of Operator from 1 May 2011. Three play systems have been identified in the Block. These are: a Tertiary play system, as proven by the nearby Moho Bilondo discoveries, an Albian “raft” play, which was tested by Frida-1 and a pre salt “Gamba” play. Of these, the first two have been fully explored within the Block and the Group is confident that no potential remains. The pre-salt play, however, has not been explored to date and the JV has gained a 12month extension to the current PSC term in order to carry out a full prospectivity assessment of the block. As part of this assessment a gradiometry survey has been acquired in early January 2012 and once integrated with the existing seismic data a decision will be made regarding possible future drilling.

JDZOphir elected to withdraw from the JDZ PSC in March 2011. All the commitments had been fulfilled and the permit was exited in good standing.

Madagascar – Marovoay Block2011 has seen the interpretation of the airborne gradiometry survey in order to better define the subsurface structure. The data has been integrated with existing seismic data and at year end the final interpretation was underway. The JV faces a drill or drop decision in Q2 2012 and at that point will elect whether to drill a well on the Block or to farm out. On 17 November 2011, the Group and Octant Energy Madagascar Ltd entered into an Option agreement whereby Ophir Madagascar granted Octant Energy the right to farm in to the Marovay PSC for a 50% participating interest subject to the satisfaction of certain conditions precedent and the payment of certain exploration costs and expenses.

Madagascar Saharawi Arab Democratic Republic

Somaliland

Ophir Energy plc Annual Report 201118

Review of operations continued

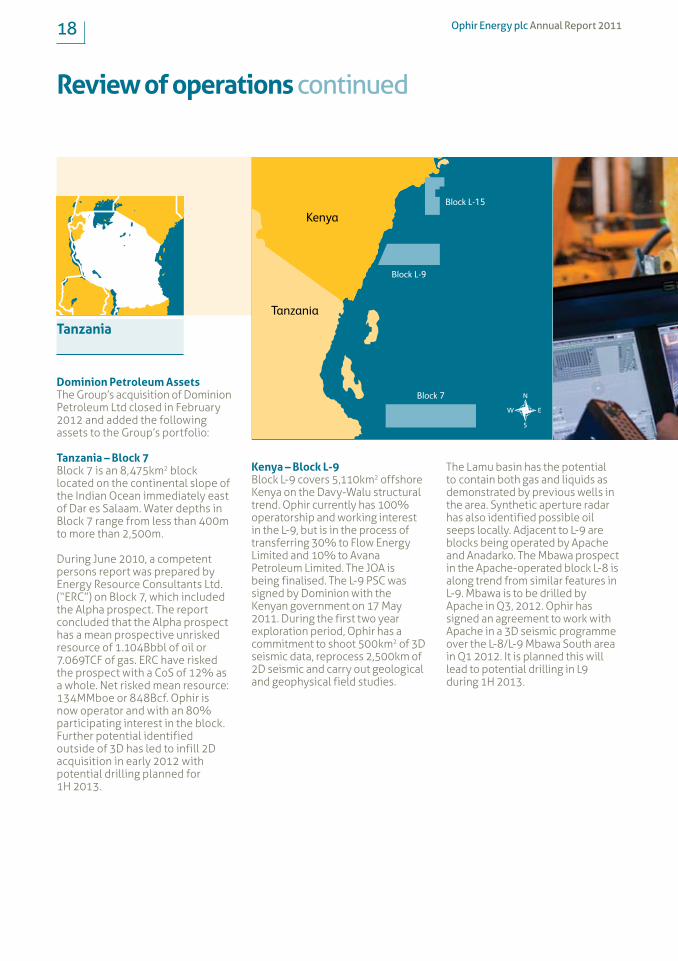

Kenya – Block L-9Block L-9 covers 5,110km2 offshore Kenya on the Davy-Walu structural trend. Ophir currently has 100% operatorship and working interest in the L-9, but is in the process of transferring 30% to Flow Energy Limited and 10% to Avana Petroleum Limited. The JOA is being finalised. The L-9 PSC was signed by Dominion with the Kenyan government on 17 May 2011. During the first two year exploration period, Ophir has a commitment to shoot 500km2 of 3D seismic data, reprocess 2,500km of 2D seismic and carry out geological and geophysical field studies.

The Lamu basin has the potential to contain both gas and liquids as demonstrated by previous wells in the area. Synthetic aperture radar has also identified possible oil seeps locally. Adjacent to L-9 are blocks being operated by Apache and Anadarko. The Mbawa prospect in the Apache-operated block L-8 is along trend from similar features in L-9. Mbawa is to be drilled by Apache in Q3, 2012. Ophir has signed an agreement to work with Apache in a 3D seismic programme over the L-8/L-9 Mbawa South area in Q1 2012. It is planned this will lead to potential drilling in L9 during 1H 2013.

Block 7

Block L-9

Block L-15

Tanzania

Kenya

Dominion Petroleum Assets The Group’s acquisition of Dominion Petroleum Ltd closed in February 2012 and added the following assets to the Group’s portfolio:

Tanzania – Block 7Block 7 is an 8,475km2 block located on the continental slope of the Indian Ocean immediately east of Dar es Salaam. Water depths in Block 7 range from less than 400m to more than 2,500m.

During June 2010, a competent persons report was prepared by Energy Resource Consultants Ltd. (“ERC”) on Block 7, which included the Alpha prospect. The report concluded that the Alpha prospect has a mean prospective unrisked resource of 1.104Bbbl of oil or 7.069TCF of gas. ERC have risked the prospect with a CoS of 12% as a whole. Net risked mean resource: 134MMboe or 848Bcf. Ophir is now operator and with an 80% participating interest in the block. Further potential identified outside of 3D has led to infill 2D acquisition in early 2012 with potential drilling planned for 1H 2013.

Tanzania

Ophir Energy plc Annual Report 201119B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

sedimentary rocks capable of generating oil. A satellite radar-imaging survey has suggested the presence of oil seeps on Lake Edward. During the second half of 2008, around 540km of 2D seismic was acquired on land and lake areas. Interpretation of the seismic has shown the presence of a deep sedimentary basin broken into fault blocks by numerous extensional faults.

In 2010, Dominion drilled the Ngaji-1 well to a total depth of 1,765m. The well did not identify hydrocarbons but did confirm the presence of high quality reservoir sands. On 27 April, 2011, Dominion applied for the renewal of the exploration licence for EA4B for the third two-year period, which expires in July 2013. This continues to be discussed with the Government of Uganda.

DRC – Block VBlock V in the Democratic Republic of Congo (“DRC”) incorporates 7,447km2 of land and lake areas. It lies to the west of and includes part of Lake Edward and adjoins EA4B in Uganda. Both blocks are part of the Albertine rift system of sedimentary basins where significant oil discoveries have been made since 2006. Ophir now holds a 46.75% participating interest in Block V with SOCO. During the first 5 year phase of the Block V PSC, Ophir and its partners are committed to an exploration programme which includes at least 300km of seismic data and two exploration wells.

Jurisdiction Asset OperatorParticipating Interest

Gross area (km2)

Tanzania Block 7 Dominion 80% 8,475

Kenya Block L-9 Dominion 60% 5,110

Kenya Block L-15 Dominion 100% 2,331

Uganda Area 4B Dominion 95% 486

DRC Block 5 SOCO 46.75% 7,447

Total 23,849

Ophir’s expansion in Tanzania and entry into Kenya ensures a level of exploration activity extending well beyond the current drilling programme.

Kenya – Block L–15Block L-15 of the Lamu Basin, offshore Kenya covers an area of 2,331km2 and lies to the north of L-9 and is also on the Davy-Walu structural trend. The only well in Block L-15 is Kofia-1, which was drilled by Union Oil in 1985 and encountered oil and gas shows in the Palaeogene and Upper Cretaceous intervals. The L-15 PSC was signed on 5 October, 2011 and Ophir now holds 100% working interest and operatorship in the block. Ophir is planning a 3D seismic programme in Q3 2012, with potential drilling in 2013.

Uganda – Exploration Area 4BExploration Area 4B (EA4B) is a 993km2 licence located in south-west Uganda and is inclusive of the majority of the Ugandan section of Lake Edward. Ophir now holds 100% participating interest and operatorship in EA4B. In early 2008, an airborne gravity and magnetic survey was acquired which proved a presence of substantial thickness of

Ophir Energy plc Annual Report 201120

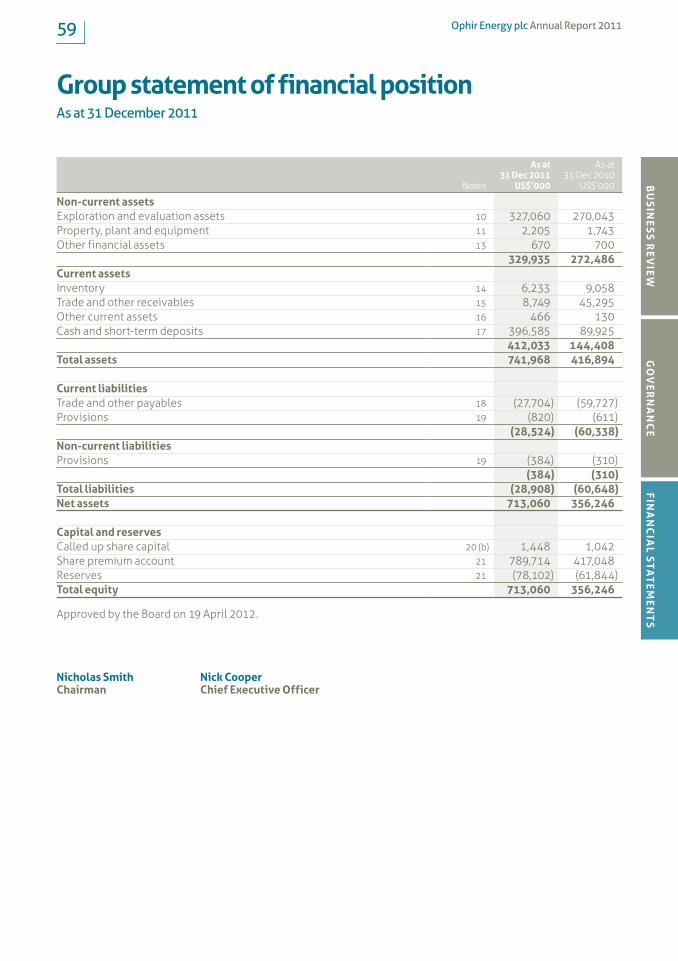

Overview2011 was a year of success for the Ophir Group, with an IPO and listing to the Main Board of the London Stock Exchange (“LSE”) on 13 July 2011. The Group issued 94,135,334 new shares and raised a total US$375 million (£235 million). An over-allotment (greenshoe) of 2,216,546 shares followed on 8 August 2011 raising a further US$8.9 million (£5.5 million). As the majority of the Group’s expenditure is incurred in US Dollars, the bulk of the proceeds of the capital raising were immediately converted to US Dollars.

The Group is currently conducting exploration and appraisal activities using existing funds from capital raised during the IPO. Following the successful capital raise in April 2012 of US$242 million, it will fund its planned activities for the 2012 financial year from current cash reserves.

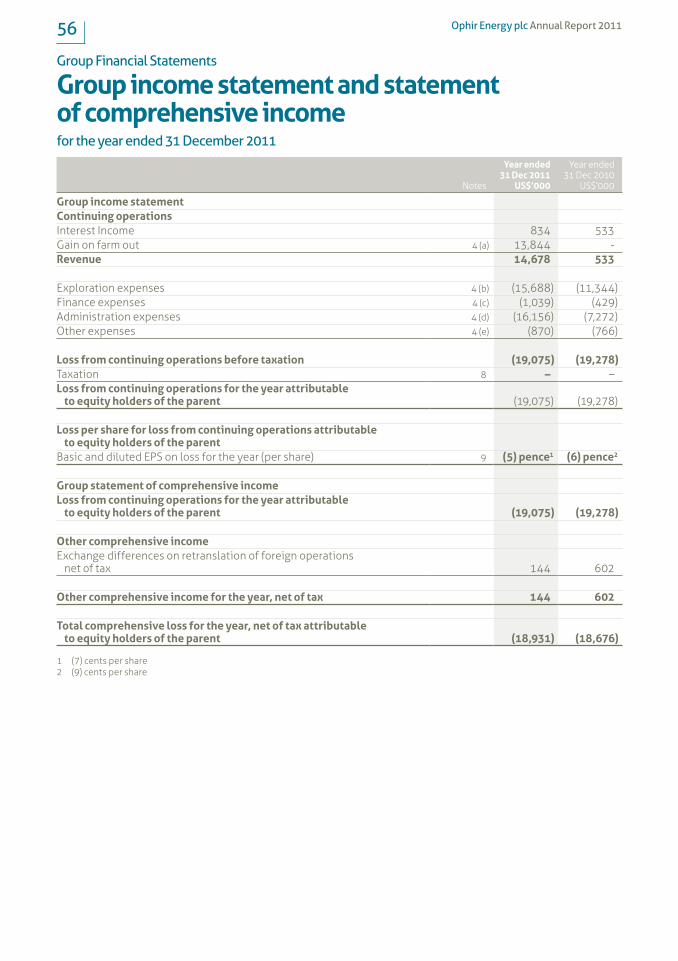

Result for the PeriodThe Group recorded a loss of US$19.1 million for the year ended 31 December 2011 (31 December 2010: US$19.3 million loss). No dividends were paid or declared by the Group during the period.

The loss for the period includes exploration expenditure expensed of US$15.7 million (31 December 2010: US$11.3 million), administrative costs of US$16.2 million (31 December 2010: US$7.3 million), finance costs of US$1.0 million (31 December 2010: US$0.5 million) and other costs of US$0.9 million (31 December 2010: US$0.8 million). The year end result was further impacted by a farm out gain of US$13.8 million (31 December 2010: Nil).

Gain on farm outThe gain on farm out relates to the partial farm out of the Group’s AGC Profond interests to Noble prior to spudding of the Kora-1 well in late June 2011. Cash proceeds of US$20 million received from Noble were applied against the Group’s carrying value of the AGC project, reducing its book value to nil at 31 December 2011, with surplus proceeds being recognised as a profit. The Kora-1 well, completed in early August, was subsequently an unsuccessful well. In accordance with the Group’s accounting policy, the Group’s share of well costs which were incurred of approximately US$12.7 million, were then written off to the Income Statement during the 2011 year.

Exploration expenditureExploration expenditure of US$15.7 million (31 December 2010: US$11.3 million) resulted from the Group’s exploration and appraisal activities in AGC Profond, Tanzania, Equatorial Guinea, Somaliland, Gabon, Congo and Madagascar. It comprises pre-licence exploration costs of US$2.3 million (31 December 2010: US$2.0 million) charged directly to the Income Statement. Unsuccessful exploration expenditure of US$13.4 million (31 December 2010: US$13.3 million) was written off in accordance with the Group’s accounting policy.

Administration expensesAdministrative expenses including personnel costs including share-based payments charges, administration costs, professional and corporate costs (audit, legal, other professional advisors’ costs and Directors’ fees) totalled US$16.2 million (31 December 2010: US$7.3 million). The result was impacted by 2010 bonuses payable in 2011, increased option incentive costs, additional personnel and administration costs associated with expansion of the Group’s operations and listing on the Main Board of the LSE and increased corporate related activity.

Finance expensesFinance costs for the period of US$1.0 million (31 December 2010: US$0.4 million) relate to foreign exchange losses arising on the fluctuation of the Group’s functional currency, the US Dollar, against other currencies.

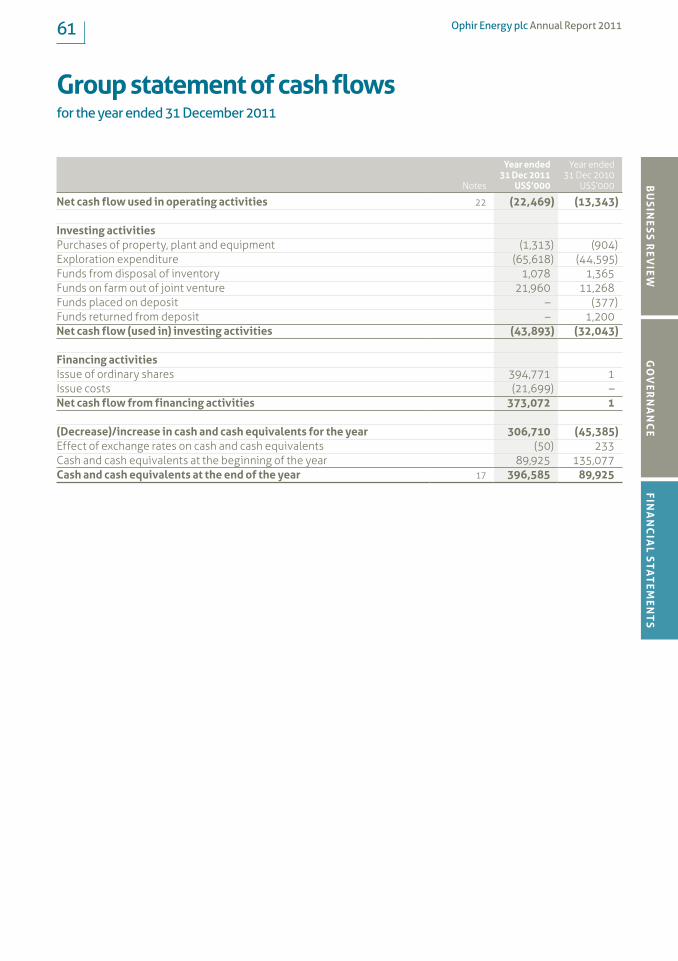

Cash flowOverall, the Group cash inflow was US$306.7 million (31 December 2010: outflow of US$45.4 million).

Operating Cash FlowThe Group’s net cash used in operating activities was US$22.5 million (31 December 2010: US$13.3 million). Of this, US$15.7 million related to exploration expenditure that was written off, predominantly attributed to AGC Kora-1 well costs (US$12.7 million) and pre-licence costs of US$2.3 million.

Investing activitiesCash flow used in investing was US$43.9 million (31 December 2010: US$32.0 million). Investment of US$65.6 million on exploration (31 December 2010: US$44.6 million) was offset by a cash inflow on farm out of the Group’s AGC interests to Noble of US$20.0 million (31 December 2010: US$11.3 million inflow net of farm out proceeds). The incurred exploration expenditure related to: – Planning and long lead items for

the BG joint venture and drilling programme in Blocks 1, 3 and 4 in Tanzania;

– Acquisition of Block C in Equatorial Guinea during November 2011, to the northwest of Block R, which was then appended to Block R; and

– Associated costs of the transfer and completed farm in to the East Pande block in Tanzania on 29 March 2011.

Financial review

Ophir Energy plc Annual Report 201121B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

Financing ActivitiesThe net cash inflow for financing activities was US$373.1 million (31 December 2010: US$0.1 million) which was as a result of the funds raised at IPO. Gross funds received were US$394.8 million with associated costs of the raise being US$21.7 million.

At year end the Group’s cash and cash equivalents were US$396.6 million (31 December 2010: US$90.0 million).

Exploration and Evaluation AssetsAs at 31 December 2011, exploration and evaluation assets totalled US$327.1 million (31 December 2010: US$270.0 million). The movement was due to expenditure incurred during the year of US$70.4 million (31 December 2010: $45.1 million) and written off expenses of US$13.4 million (31 December 2010: US$13.3 million).

The main areas of exploration were: – Tanzania Blocks 1, 3 and 4

US$40.5 million due to the costs of drilling Chaza-1 in Block 1, and the seismic programmes operated by Ophir in Blocks 1, 3 and 4.

– Ophir completed the farm in to the 7,500km2 East Pande Block on 29 March 2011. The Group holds 70% equity, with Rakgas holding the remaining 30%. Ophir has assumed operatorship of the Block. Costs for 2011 amounted to US$6.6 million.

– In Equatorial Guinea the acquisition of Block C (US$2.2 million) and preparation for the 2012 drilling programme of three firm plus one contingent well (US$7.3 million).

Current AssetsThe Group held cash and short-term deposits of US$396.6 million (31 December 2010: US$89.9 million) plus inventories of US$6.2 million (31 December 2010: US$9.1 million) which comprise drilling materials for future drilling campaigns. Trade and other receivables were US$8.7 million (31 December 2010: US$45.3 million).

LiabilitiesThe Group had no debt as at December 31 2011 (31 December 2010: Nil). Trade and other payable including accruals were US$27.7 million (31 December 2010: US$59.7 million).

OutlookThe Group is currently conducting exploration activities using existing funds from capital raised during the IPO and plans to utilise the April equity placing to fund forecast expenditure for at least the next 12 months. Accordingly, the financial statements have been prepared on a going concern basis as the Directors are of the opinion that the Company will have sufficient funds to meet its ongoing working capital and committed capital expenditure requirements over the next 12 months.

Ophir Energy plc Annual Report 201122

Corporate and Social Responsibility

All of Ophir’s employees and contractors are encouraged to work to the highest standards. These standards are reviewed and set by the Ophir HSE Committee which takes responsibility for monitoring group-level health, safety, security and environmental (“HSSE”) risk assessments in addition to reviewing reports on serious accidents and fatalities to ensure that management is responding appropriately. The Committee also ensures that the Company is fully compliant by commissioning periodic independent audits on HSE matters.

Ophir is committed to taking an active part in the development of the countries in which it operates. The Company conducts its operations in an ethical, responsible, apolitical, independent and transparent way. We manage our Corporate and Social Responsibility (“CSR”) with the same principles underlying the conduct of our core activities, which are determination, innovation and excellence.

Ophir operates in regions offering a great variety of geographical, cultural, economic and social environments. Africa is a mosaic of countries with contrasting levels of development, regulations, languages, traditions and expectations. Our long-term involvement with our host countries and local partners, as well as our multicultural team, are instrumental in ensuring we keep in tune and maintain an effective dialogue in line with our business objectives.

Ophir believes its presence is felt positively by its hosts as the Company strives to create value locally, benefiting not only the employees but the community at large. The Company ensures its projects will bring opportunities and its investment will make a positive difference.

Ophir focuses in the following areas: – Environment – Health and Safety – Education – Community Development

Environment: Before initiating any exploration project Ophir conducts comprehensive and integrated Environmental Impact Assessments (“EIA’s”). These assessments are repeated at each stage of the project using recognised consultants and methods. As a part of this process Ophir consults with local authorities, NGOs and communities to ensure we are in compliance with both industry best practices and any applicable local regulations and guidelines. Our environmental plan is implemented in association with our Corporate Health, Safety & Environmental Manual.

One of our initiatives for the conservation of the environment has been to support a research project in the Western Sahara. Since 2006 we have contributed to archaeological research conducted during various field missions by the University of East Anglia (United Kingdom) in the Tifariti Region of Western Sahara. This programme represents a valuable contribution to the preservation and knowledge of historical occupation in Western Sahara.

Reports and photos can be viewed on http://www.cru.uea.ac.uk/~e118/WS/WSahara.htm.

Ophir Energy plc Annual Report 201123B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

Health and safety: Ophir’s operations are conducted in accordance with local and international health and safety best practices.

The Company offices in Gabon and Equatorial Guinea have implemented mosquito eradication programmes.

Ophir also provides internationally accredited driving and first aid courses to all local employees as part of the comprehensive training programme tailored for the staff. Ophir also expects its subcontractors and suppliers to provide a safe and healthy working environment for their employees and to provide appropriate training and personal protective equipment.

Education: Ophir encourages an atmosphere of continuous improvement. The Company contributes to the ITNHGE Programme, a collaborative educational initiative run for the benefit of adult students in Equatorial Guinea. A group of 46 students enrolled in the full time intensive English programme and completed their first semester in May 2008 in Malabo.

Ophir runs a comprehensive training programme for the Equatorial Guinean staff consisting of English language courses as well as IT and word processing classes.

Ophir fully sponsored the construction of a two classroom nursery school equipped with 20 desks in the village of Ebein Yenkeng in the Niefang Region, Central South Equatorial Guinea. Stage 1 has been completed; Stage 2 is progressing.

Ophir is funding a cultural exchange programme between Gabon and South Africa under the auspices of the South African Embassy for the Nelson Mandela School in Libreville.

Community development: Ophir is proud to help local communities develop in its project areas.

In Equatorial Guinea, where Ophir has invested heavily over the last few years, we have been actively involved in community development. In addition to the construction of a school (details above) we have also acquired and installed four electricity generators into hospitals in Evinayong, Kogo Mbini and Acurenam.

Ophir has also been active in Tanzania for a number of years. Ophir has invested in excess of US$10 million in the development of the Mtwara port. Approximately half of this sum was spent in the local community providing a major boost to the area. As expected the entire project was backed up by a comprehensive Environmental Impact Assessment.

Ophir has an office in Mtwara. During its recent drilling campaign offshore Tanzania Ophir provided accommodation in Mtwara for over 60 workers. To accommodate these people during the drilling phase Ophir rented 13 residential properties. Prior to occupation all of the properties underwent a full refurbishment to ensure they were fully compliant with international housing standards. As a result of this work the landlords have seen the value of their rented properties increase substantially – a good result for both parties.

Ophir has also supported other schemes in the Mtwara port town. For example it has begun funding of a local maternity clinic. Funds go towards providing essential drugs and baby equipment.

Ophir sponsored and provided the materials for an art competition between a number of schools in Mtwara.

Ophir Energy plc Annual Report 201124

Corporate and Social Responsibility continued

On 21 December 2011, devastating floods hit parts of the city of Dar es Salaam, Tanzania, impacting the lives of many local people, some losing not only their properties and belongings, but also having to deal with the loss of lives due to the tragic event.

Many of those affected by the floods were relocated to the Mabwepande area in Bunju Juu, north of Dar es Salaam. It was planned that around 2,000 families would relocate to this area, where temporary shelters were set up by the Red Cross until more permanent arrangements could be made.

To assist in the relocation efforts Ophir Energy has donated 30 water storage tanks with a capacity of 5,000 litres each to the site. These tanks will be used to move and store water, thus securing adequate sanitation which is vital to prevent disease and ensure the survival of the flood victims. Ophir Energy is committed to supporting the communities in this time of need.

Ophir is currently assessing the best way to contribute to community development and to support local initiatives via a charitable programme which would channel future donations to individuals or small organisations.

Ophir sponsored a local art competition in Mtwara from 30 January 2012 to 3 February 2012 that provided primary school students in grades 5 to 7 with the opportunity to learn about the oil and gas industry and its benefits to Mtwara and the community.

They were then given the chance to express their knowledge and thoughts of the industry through art. Throughout the process, regional officials, teachers and parents/guardians were also encouraged to learn more about Ophir and the oil and gas industry and its contribution to the community. The theme of the competition was, “What does the oil and gas industry look like/mean to you?”

A total of 60 students participated in the competition, 15 from four schools in Mtwara, these schools including Chuno Primary School; Ligula Primary School; Mivinjeni Primary School and Shangani Primary School.

After all the entries had been submitted, Ophir’s judging panel agreed on those which they thought were the most creative and the winners were selected. The Regional Commissioner attended the award ceremony for all schools, presenting

the winning students with rucksacks and stationery supplies on behalf of Ophir. All students were awarded certificates of participation to show Ophir’s appreciation for taking part in this initiative. Further to this, each school was presented with a cheque from the Regional Commissioner on behalf of Ophir, for an amount depending on where they were placed in the competition. Ophir hopes that this donation will assist the schools in maintaining a high standard of education for the youth of Mtwara.

In 2010, Ophir Congo (Marine IX) Limited and joint venture partners Premier Oil plc and Kufpec Congo (Marine IX) Limited began funding a community project in the remote village of Tchisseka, Brazzaville, Congo. The first stage of this project consisted of funding the restoration of the Tchisseka Health Care Centre. Restoration began on 30 August, 2010, with the completely restored Tchisseka Health Care Centre being delivered to the population of Tchisseka on 10 January 2011.

The second stage of this social project is underway at the moment. This stage involves the construction of an accommodation site for the doctors and nurses set to work in the Tchisseka Health Care Centre. The facility will be equipped with solar panels providing electrical supplies for sustainability and because of the remoteness of this facility. Construction of the accommodation unit is continuing and is expected to be completed in May 2012.

Ophir Energy plc Annual Report 201125B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

Helping out with the provision of materials and facilities for education is one of the worthwhile contributions Ophir makes to the communities in which it works, the benefits of which are immediate and obvious.

HSE highlightsThe high levels of Ophir Energy operated exploration activities experienced in 2010 spilled over into 2011. During 2011 the Company carried out a number of drilling and seismic acquisition programmes.

These exploration activities are summarised below and were completed without any significant occupational health and safety incidents (LTIs) or offshore security incidents (piracy). With regard to HSE issues in general it is important to highlight that several of Ophir’s exploration projects are carried out in offshore areas affected by Somali piracy risk, therefore Ophir and its contractors meticulously plan and execute a full security plan offshore to protect personnel and assets. Although acts of piracy are reported to occur on a fairly regular basis in the Somali Basin/Indian Ocean, none of these incidents has adversely affected Ophir’s operations.

2011 HSE operational summary1. Tanzania – Drilling in Blocks 1

and 4 carried over into Q 1–2 of 2011. This Ophir Energy operated drilling was carried out simultaneously with shooting of 3D seismic in the same areas. In addition to normal HSE considerations these activities required a high degree of maritime security co-ordination given the current risk of piracy in the region. Mid-year Ophir handed over operatorship of Blocks 1, 3 and 4 to the BG Group, this included operatorship of the

shore base at Mtwara. Also in Tanzania in late Q4 2011 we initiated a Fugro 3D seismic programme in the Ophir operated East Pande block. This seismic was completed in early 2012. The operations in Tanzania were all subject to the normal EIA and piracy risk assessments. The security plans were successfully enforced using a close partnership of Tanzanian Navy and private security contractors operating with strict rules of engagement and behaving in accordance with the UN’s voluntary principles on human rights.

2. AGC (Senegal /Guinea Bissau) – Ophir drilled one well offshore Senegal /Guinea Bissau in the joint development zone known as the AGC. Prior to drilling a consultation process including a compliant EIA was issued including oil spill response planning and safety risk assessments (narco - trafficking/robbery). A security plan was designed and executed in conjunction with service companies (rig and supply vessels) and HASSMAR (Senegalese body responsible for the environment and security of its offshore areas). The

security plan was used not only to ensure safe conditions in the drilling area , it was also used to protect the personnel and assets during the mobilisation and demobilisation phase as people and equipment were moved into the project area from the Gulf of Guinea and back out of the project area on completion of the well. The Kora 1 drilling programme was completed with zero LTIs.

3. Gabon – Ophir planned (EIA completed and risk assessments carried out) and initiated a 3D seismic programme in late Q4. The programme was concluded without incident in February 2012.

Corporately the Ophir Energy Group recorded a zero rate for LTIs over the 2011 calendar year.

Ophir is working to further expand its HSE and CSR reporting procedures by widening the scope of reporting to include all services companies and contractor personnel employed on projects and to further refine the Company KPIs it employs in these reporting procedures. Ophir expects to complete these changes within the coming months.

Ophir is working to further expand its HSE and CSR reporting procedures by widening the scope of reporting to include all services companies and contractor personnel.

Ophir Energy plc Annual Report 201126

Principal risks and uncertainties Risk management

Ophir is committed to maintaining a balanced portfolio and to managing risks in a proactive and effective manner. The key elements Ophir risk management processes are: – Risk assessment – Risk analysis and evaluation – Risk mitigations – Risk monitoring and reviewing – Communication and consultation

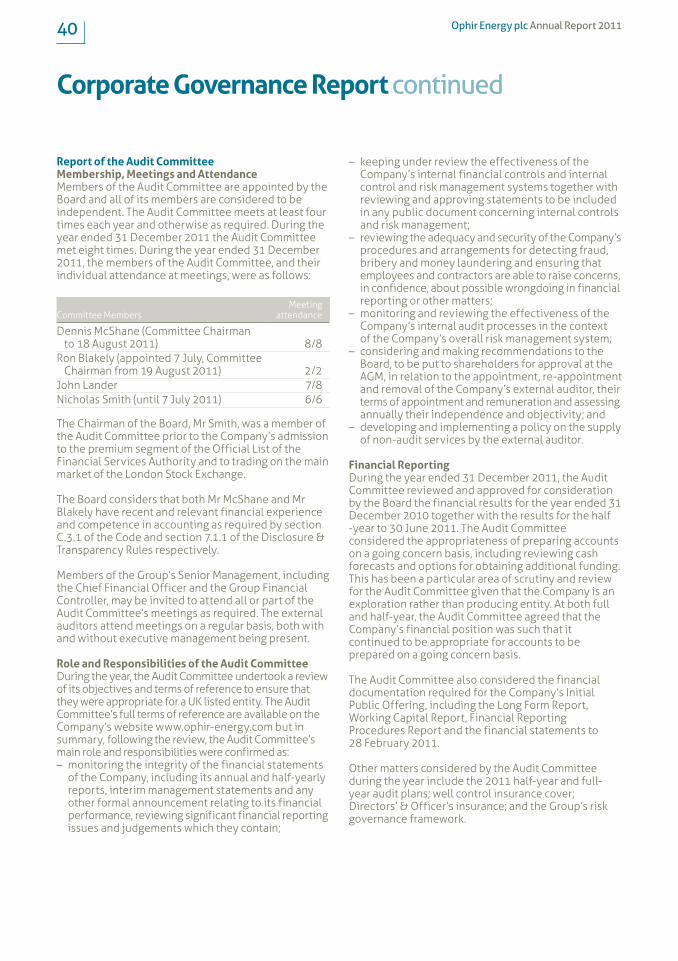

Responsibility for identifying and managing risks lies with Ophir’s Executive Directors, Senior Management Team and Country Managers. The Executive Directors continually monitor the Group’s risk exposures and report to the Audit Committee and Board of Directors on a six monthly basis, or more frequently as required.

The principal risks of the Group are summarised as follows:

Type Risk Mitigants

Strategic Political risk – The Group maintains a balanced asset portfolio across different jurisdictions in a region where the Group is most accustomed to operating.

– The Group strives continually to maintain positive relationships in all host countries that it operates. Ophir aims to work to the highest industry standards with all regulators and compliance with the Company’s licence and PSC obligations is closely monitored.

Reliance on key personnel

– Ophir is reliant on a small team of experienced oil and gas professionals for its operational success. In order to retain, motivate and recruit suitably qualified employees it ensures its remuneration packages are competitive. It has established a long- term incentive programme for executives and deferred share plan for staff.

Investment decisions

– The Group and its advisors are experienced within the industry in which it operates and complete a proper review against the Group’s strategy and investment criteria. Full due diligence is undertaken upon all potential new entries. The current portfolio is closely monitored.

Type Risk Mitigants

Operational Drilling operations risk

– The Group maintains clearly defined operational procedures that should always be followed.

– The contracting and procurement process ensures suitably qualified contractors are employed.

– Regular training in the processes and continual monitoring of adherence are undertaken.

Ophir operates in the inherently risky upstream oil and gas sector and effective risk management is an essential process for the Group to deliver its strategic and operational objectives.

Ophir Energy plc Annual Report 201127B

US

INE

SS

RE

VIE

WG

OV

ER

NA

NC

EFIN

AN

CIA

L STA

TE

ME

NT

S

Type Risk Mitigants

Operationalcontinued

HSE incident risk

– The Group maintains a comprehensive system of HSE procedures that should always be followed. The systems are overseen by the HSE Committee which regularly meets to review and monitor compliance.

– Comprehensive Environmental Impact Assessments are performed. Oil spill and emergency response plans are in place, regular training in the procedures occurs.

Discovery risk and success rate

– The Group has a technically and regionally experienced management and geoscience team who have a proven track record of success. To reduce risk, substantial technical analysis is undertaken to evaluate and manage opportunities.

– All exploration and appraisal programmes are consistently reviewed and monitored before being recommended to the Board for approval.

Insurable risks – Comprehensive insurance programmes are maintained in accordance with industry standards.

Availability of rigs and services

– Regular market review of services and rig availability occurs. Experienced advisors are used to ensure a rapid response to opportunities and an ability to close binding agreements quickly.

– A dedicated drilling project manager and C&P manager ensure a clear contracting strategy and project plan are produced early in the procurement planning stage.

Type Risk Mitigants

Financial Counterparty credit risk

– The Group closely monitors all trade debtors which are subject to internal credit review.

Liquidity risk – The Group has a formal annual budget process and regularly forecasts cash requirements to ensure underlying liquidity requirements are met. Actual vs budget analysis reporting occurs monthly and is monitored by senior management and reported to the Board.

Interest rate and foreign exchange risk

– The Group reports and manages its business in US Dollars. Cash balances are primarily held in US Dollars to provide a natural hedge. Small balances are retained in other currencies for operating and administrative needs.

– The Group holds cash balances in short-term deposits; there were no hedges in 2011.

Type Risk Mitigants

External Sovereign risk – The Group recognises that there is an inherent political risk associated with the countries in which it operates. The Group regularly monitors and reviews all jurisdictions in which it operates. The Group’s personnel are experienced within the industry and maintain close relations on the ground within each jurisdiction.

Legal, regulatory or litigation risk

– Ophir’s activities are subject to various different jurisdictional laws, tax regimes and regulations. The Group employs suitably experienced and qualified staff and advisors who can assess, and where necessary respond to external risks.

– The Group’s key policies and procedures have considered requirements of the UK Bribery Act.

– The Group maintains a Business Code of Conduct and ensures proper training for employees occurs.

Investor and stakeholder sentiment

– The Group fosters strong relations with the local communities and host country governments in jurisdictions that it operates. It continually interacts with all relevant stakeholders.

– The Company maintains regular dialogue with all key shareholders. The Company has established investor relations and a corporate affair function during 2012 and ensures all material information is released to the market on a timely basis.

Ophir Energy plc Annual Report 201128

Directors at year end

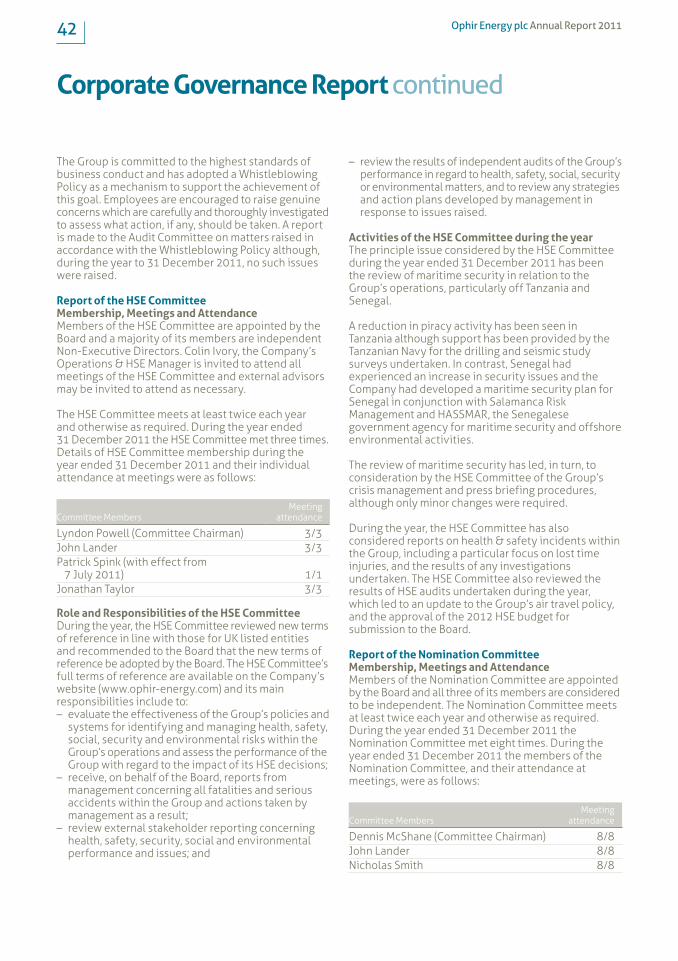

Nicholas SmithNon-Executive ChairmanMr Smith (age 60) was appointed to the Board of the Company as a Non-Executive Director in October 2007 and served as Chairman of the Audit and Nomination Committees until September 2009 when he was appointed as Chairman of the Board. Mr Smith is a member of the Remuneration and Nomination Committees and was a member of the Audit Committee until 7 July 2011.

Mr Smith trained as a chartered accountant with Ernst & Young. He joined the Jardine Fleming Group in 1986 serving, from 2003, as chief financial officer and as a member of the Executive Committee. Mr Smith became a director of Robert Fleming International Ltd in 1998 and the Director of Origination – Investment Banking serving until 2000. Mr Smith currently serves as a non-executive director for Asian Citrus Holdings Ltd, PLUS Markets Group plc, Sorbic International Ltd., Japan Opportunities Fund II Limited and Schroder Asia Pacific Fund plc.

Alan SteinExecutive Deputy Chairman & FounderDr Stein (age 47) was one of the Company’s founding Directors in 2004.

Dr Stein began his career in the UK as a geologist with oil consultants Dolan & Associates where he worked on projects in Europe, Australia and the Far East. In 1992, he established Dolan & Associates’ first international office in Australia and in 1994 was one of the founding partners of the IKODA consultancy group which had offices in London and Perth. In 1996 he was one of the founding directors of FIL which acquired interests in offshore Mauritania. These interests were sold to Fusion Oil & Gas plc (Fusion) and Dr Stein was appointed managing director of Fusion in 1998 and remained until that

company’s sale in December 2003. Dr Stein is non-executive chairman of Neon Energy Limited, an ASX-listed petroleum exploration and production company headquartered in Perth, Australia.

Dr Stein has notified the Board that, while continuing to make himself available for advice and guidance, he will not be seeking re-election at the Company’s AGM in 2012.

Nicholas CooperChief Executive OfficerDr Cooper (age 44) was appointed to the Board as Managing Director on 1 June 2011 and has formally assumed the role of Chief Executive Officer in December 2011.

Dr Cooper began his career as a geophysicist with BG and Amoco in the UK and various international locations. He spent two years with the energy team at Booz-Allen & Hamilton, advising on upstream oil and gas development projects. In 1999, Dr Cooper completed an MBA at INSEAD and went on to join the oil and gas team at Goldman Sachs where he held the position of Vice President. In early 2005 he co-founded and became CFO of Salamander Energy plc, the Asia-focused exploration and production company, which has grown from start-up to FTSE 250 constituent.

Jonathan TaylorExecutive Director & Founder In 2004, Mr Taylor (age 46) was one of the founding Directors of Ophir, serving initially as its Technical Director and is a member of the HSE Committee.

Mr Taylor has over 20 years of experience in a range of technical and asset management roles in Africa, Europe, the Far East and the Middle East, for Amerada Hess Ltd, Clyde Petroleum plc and Gulf Canada Resources Ltd. Mr Taylor was appointed as Exploration Director of Fusion in November 1998, resigning in March 2004 to found Ophir.

Dennis McShaneSenior Independent DirectorMr McShane (age 56) was appointed to the Board as a Non-Executive Director in October 2007 and as Senior Independent Director in November 2009. Mr McShane is Chairman of the Nomination Committee and a member of the Audit and Remuneration Committees, having also served as Chairman of the Audit Committee from September 2009 to 18 August 2011.

Mr McShane is a founding principal of Midas Resource Partners. From September 2004 to November 2008 Mr McShane was a senior executive of the Ferrexpo group of companies serving as executive director of finance and business strategy. He led the successful initial public offering of Ferrexpo plc on the Official List of the London Stock Exchange in June 2007. Prior to joining Ferrexpo, Mr McShane was an investment banker with JPMorgan Chase & Co (JPM) emerging markets investment banking and mining and metals practices in London. In 2002, he became head of mining and metals in JPM’s Asia-Pacific practice, based in Sydney. He attended Harvard Business School and the State University of New York.

Ronald BlakelyIndependent Non-Executive DirectorMr Blakely (age 63) was appointed as a Non-Executive Director of the Company on 7 July 2011 and as Chairman of the Audit Committee in September 2011.

Mr Blakely is a retired former executive whose career spanned more than 38 years with Royal Dutch Shell companies. At time of retirement in October 2008 he was Executive Vice President Global Downstream Finance. In previous roles he has been CFO of Shell Oil Products in the USA and CFO of Shell Canada, a then Canadian public integrated oil and gas company. He is a graduate of the University of Guelph with a major

Board of Directors

Ophir Energy plc Annual Report 201129

in Economics and a member of the Society of Management Accountants of Alberta. Mr Blakely is currently the non-executive chairman of the Board of Oil Sands Quest, a Calgary based company.

John LanderIndependent Non-Executive DirectorMr Lander (age 68) was appointed as a Non-Executive Director of the Company in November 2008. He is Chairman of the Remuneration Committee and a member of the Audit, Nominations and HSE Committees.