Embed Size (px)

Citation preview

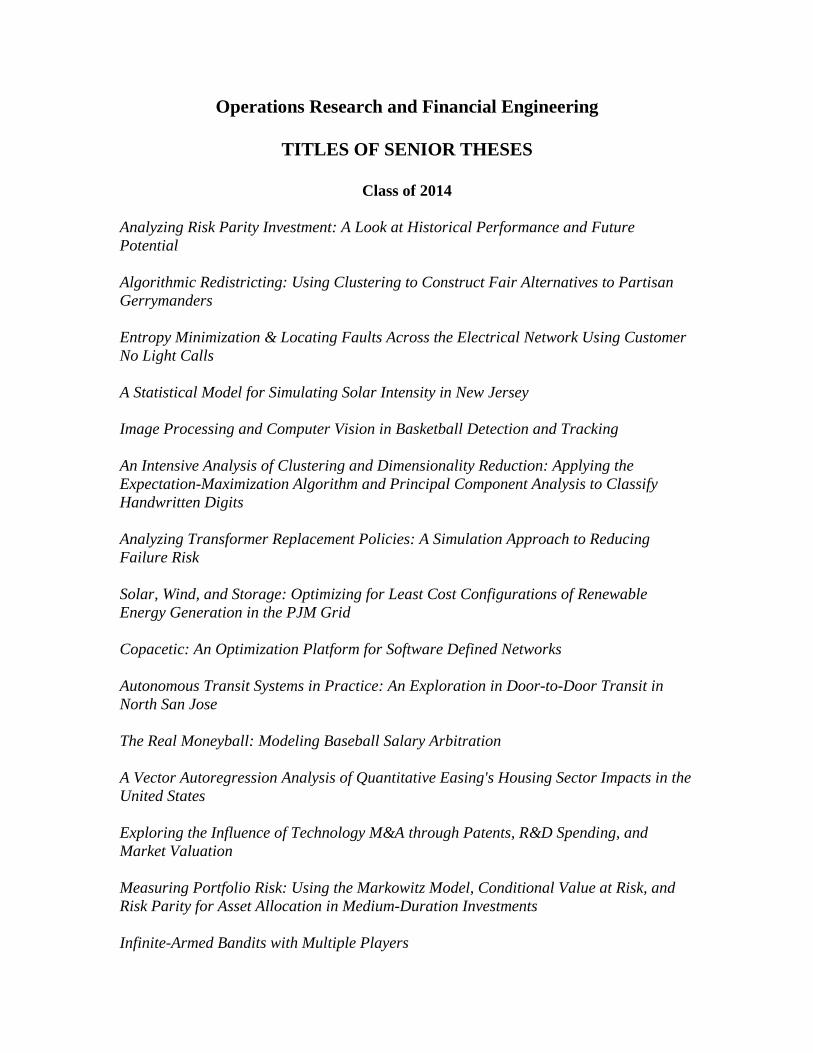

Operations Research and Financial Engineering

TITLES OF SENIOR THESES

Class of 2014

Analyzing Risk Parity Investment: A Look at Historical Performance and Future Potential Algorithmic Redistricting: Using Clustering to Construct Fair Alternatives to Partisan Gerrymanders Entropy Minimization & Locating Faults Across the Electrical Network Using Customer No Light Calls A Statistical Model for Simulating Solar Intensity in New Jersey Image Processing and Computer Vision in Basketball Detection and Tracking An Intensive Analysis of Clustering and Dimensionality Reduction: Applying the Expectation-Maximization Algorithm and Principal Component Analysis to Classify Handwritten Digits Analyzing Transformer Replacement Policies: A Simulation Approach to Reducing Failure Risk Solar, Wind, and Storage: Optimizing for Least Cost Configurations of Renewable Energy Generation in the PJM Grid Copacetic: An Optimization Platform for Software Defined Networks Autonomous Transit Systems in Practice: An Exploration in Door-to-Door Transit in North San Jose The Real Moneyball: Modeling Baseball Salary Arbitration A Vector Autoregression Analysis of Quantitative Easing's Housing Sector Impacts in the United States Exploring the Influence of Technology M&A through Patents, R&D Spending, and Market Valuation Measuring Portfolio Risk: Using the Markowitz Model, Conditional Value at Risk, and Risk Parity for Asset Allocation in Medium-Duration Investments Infinite-Armed Bandits with Multiple Players

Assessing Real-Time Transportation Demand: Building an Interactive, Three-Dimensional Visualization of Traffic Flows in New Jersey Improving Merton: an analysis of Merton’s original default risk model, its extensions, and potential areas of further improvement Can Alternative Dogs of the Dow Beat Hedge Funds? Keeping the Lights On: An Analysis of the Dynamic Allocation Problem of Assigning Utility Repair Trucks to Outages Predicting the Impact of the American Airlines-US Airways Merger on Domestic Airfares Community Detection and Homophily in Music Sharing Online Social Networks: A Study of This Is My Jam Portfolio Optimization from a Risk-Management Perspective A Mathematical Approach to Portfolio Optimization in Risk Management Examining Volatility in the Equity and Oil Markets Through Volatility Swaps and the Volatility Skew Chatty Stochastic Multi-Armed Bandits Uncovering Systemic Corruption in the ER: An Empirical Analysis of Motor Vehicle-Related Hospital Bills and their Impact on Insurance Companies Operations Research and Financial Engineering Thesis: A Different Approach to Modeling Changes in Stock Prices Approximate Dynamic Programming Applied to Biofuel Markets in the Presence of Renewable Fuel Standards Optimal Yield Commodity Indices in Context of the Open Interest Term Structure A Follow-Up Study on the Volume-Volatility Relation in the U.S. Municipal Bond Market Monte Carlo Simulation in Valuing Parisian and Parasian Barrier Options The Startup Spring: Leveraging Public Policy to Increase Capital Pools for Technology Startups in Turkey and Jordan Comparing Transfer Market Activity of Europe's Top Four Soccer Leagues No Classroom Left Uncovered: An Application of Queueing Theory to Public Schools’ Substitute Teacher Systems

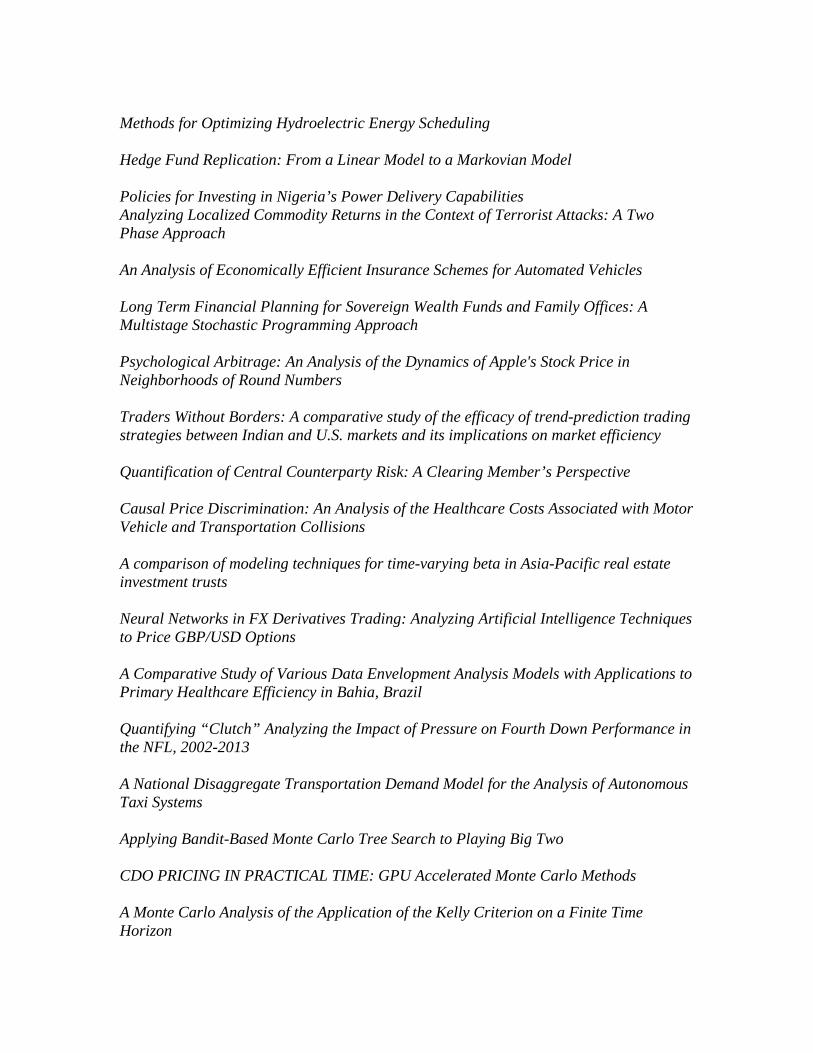

Methods for Optimizing Hydroelectric Energy Scheduling Hedge Fund Replication: From a Linear Model to a Markovian Model Policies for Investing in Nigeria’s Power Delivery Capabilities Analyzing Localized Commodity Returns in the Context of Terrorist Attacks: A Two Phase Approach An Analysis of Economically Efficient Insurance Schemes for Automated Vehicles Long Term Financial Planning for Sovereign Wealth Funds and Family Offices: A Multistage Stochastic Programming Approach Psychological Arbitrage: An Analysis of the Dynamics of Apple's Stock Price in Neighborhoods of Round Numbers Traders Without Borders: A comparative study of the efficacy of trend-prediction trading strategies between Indian and U.S. markets and its implications on market efficiency Quantification of Central Counterparty Risk: A Clearing Member’s Perspective Causal Price Discrimination: An Analysis of the Healthcare Costs Associated with Motor Vehicle and Transportation Collisions A comparison of modeling techniques for time-varying beta in Asia-Pacific real estate investment trusts Neural Networks in FX Derivatives Trading: Analyzing Artificial Intelligence Techniques to Price GBP/USD Options A Comparative Study of Various Data Envelopment Analysis Models with Applications to Primary Healthcare Efficiency in Bahia, Brazil Quantifying “Clutch” Analyzing the Impact of Pressure on Fourth Down Performance in the NFL, 2002-2013 A National Disaggregate Transportation Demand Model for the Analysis of Autonomous Taxi Systems Applying Bandit-Based Monte Carlo Tree Search to Playing Big Two CDO PRICING IN PRACTICAL TIME: GPU Accelerated Monte Carlo Methods A Monte Carlo Analysis of the Application of the Kelly Criterion on a Finite Time Horizon

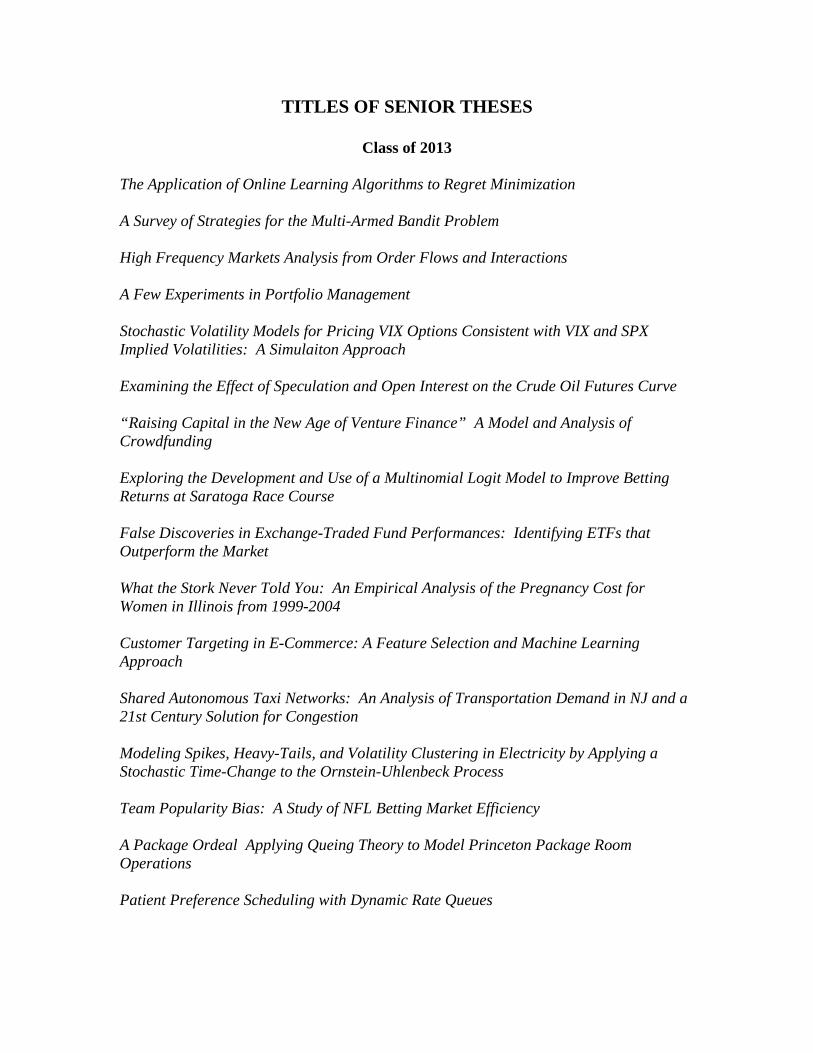

TITLES OF SENIOR THESES

Class of 2013

The Application of Online Learning Algorithms to Regret Minimization A Survey of Strategies for the Multi-Armed Bandit Problem High Frequency Markets Analysis from Order Flows and Interactions A Few Experiments in Portfolio Management Stochastic Volatility Models for Pricing VIX Options Consistent with VIX and SPX Implied Volatilities: A Simulaiton Approach Examining the Effect of Speculation and Open Interest on the Crude Oil Futures Curve “Raising Capital in the New Age of Venture Finance” A Model and Analysis of Crowdfunding Exploring the Development and Use of a Multinomial Logit Model to Improve Betting Returns at Saratoga Race Course False Discoveries in Exchange-Traded Fund Performances: Identifying ETFs that Outperform the Market What the Stork Never Told You: An Empirical Analysis of the Pregnancy Cost for Women in Illinois from 1999-2004 Customer Targeting in E-Commerce: A Feature Selection and Machine Learning Approach Shared Autonomous Taxi Networks: An Analysis of Transportation Demand in NJ and a 21st Century Solution for Congestion Modeling Spikes, Heavy-Tails, and Volatility Clustering in Electricity by Applying a Stochastic Time-Change to the Ornstein-Uhlenbeck Process Team Popularity Bias: A Study of NFL Betting Market Efficiency A Package Ordeal Applying Queing Theory to Model Princeton Package Room Operations Patient Preference Scheduling with Dynamic Rate Queues

Keeping Them Honest: How Medical Services can Maximize Profit while Maintaining Quality of Service with and Optimal Control Policy A Queueing Theory Approach to Modeling Toll Plaza Delay with Applications for Commute User Cost Optimization Three Angry Men: A Game Theoretic Analysis of How the Two-Sided Unanimous Verdict Rule Affects Outcomes in Jury Trials Alternative Investing: The Search for Profitable Trading Strategies in the U.S. Commodity Markets Liquidity and Investment Styles in the Commodity Futures Market New Opportunities in the Currency Carry Trade Are We There Yet? A Proposal for an Autonomous Taxi System in New Jersey and a Preliminary Foundation for Empty Vehicle Routing The Analytic GM: Using Data Mining to Predict NFL Performance Exploring Alternative Treatment for Bacterial Meningitis Through Optimal Dosing Strategy: Responding to Rising Antibiotic Resistance The Future of Solar: An Analysis of New Jersey's Market for Solar Renewable Energy Credits (SRECs) Nested Newsvendor Optimal Commitment Policies in Day-Ahead and Hour-Ahead Electric Capacity Forward Markets Replicating Electricity Spot Prices Through Inverse Optimization of Supply Shocks Methods of Pair Selection in Pairwise Comparisons for Efficient List Ranking Fishing Within the Limits: A Sustainable Fishing Model Forex Market Response: Analysis of Natural Disasters and Their Impact on the Foreign Exchange Market Analysis of Leveraged ETF Compounding Difference Accounting for Population Structure in Lasso Regression for Genome-Wide Association Studies Modeling Spikes, Heavy-Tails, and Volatility Clustering in Electricity by Applying a Stochastic Time-Change to the Ornstein-Uhlenbeck Process

Face Detection, Tracking Methods, and Image Processing: A MATLAB Approach Analyzing and Presenting Modern Temperature Trends The Linear Simplex Method: Investigations of Cycling and Application to Markov Decision Processes

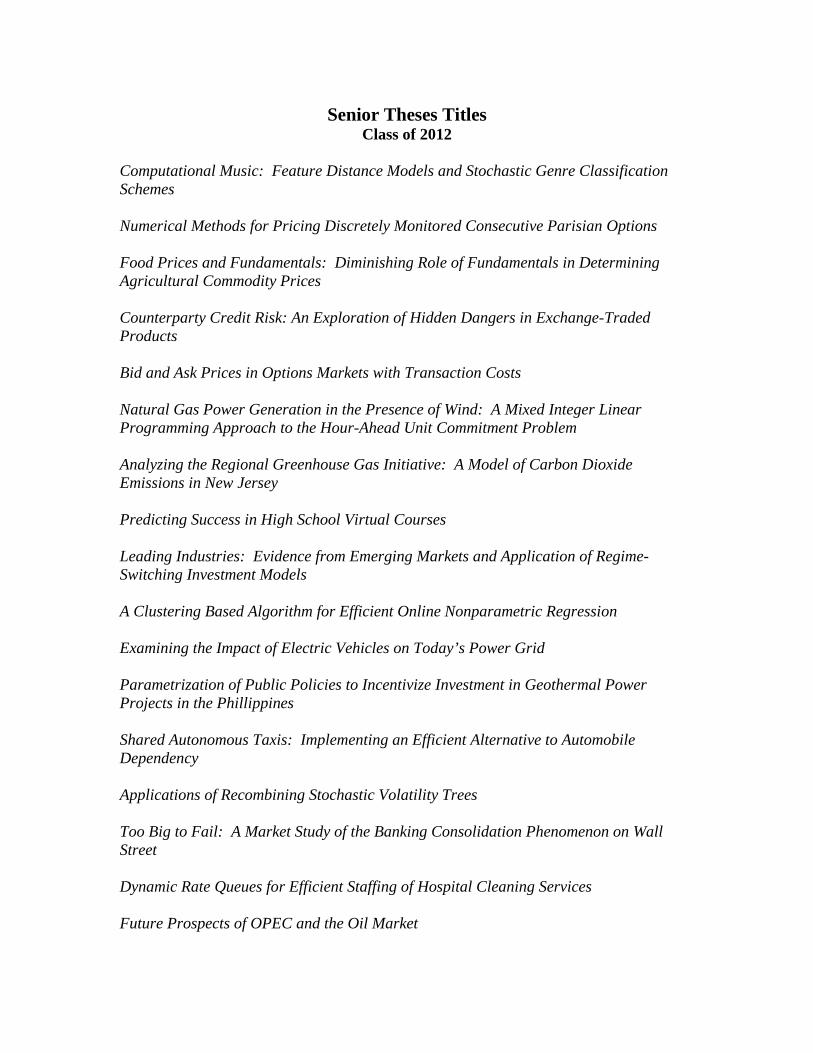

Senior Theses Titles Class of 2012

Computational Music: Feature Distance Models and Stochastic Genre Classification Schemes Numerical Methods for Pricing Discretely Monitored Consecutive Parisian Options Food Prices and Fundamentals: Diminishing Role of Fundamentals in Determining Agricultural Commodity Prices Counterparty Credit Risk: An Exploration of Hidden Dangers in Exchange-Traded Products Bid and Ask Prices in Options Markets with Transaction Costs Natural Gas Power Generation in the Presence of Wind: A Mixed Integer Linear Programming Approach to the Hour-Ahead Unit Commitment Problem Analyzing the Regional Greenhouse Gas Initiative: A Model of Carbon Dioxide Emissions in New Jersey Predicting Success in High School Virtual Courses Leading Industries: Evidence from Emerging Markets and Application of Regime-Switching Investment Models A Clustering Based Algorithm for Efficient Online Nonparametric Regression Examining the Impact of Electric Vehicles on Today’s Power Grid Parametrization of Public Policies to Incentivize Investment in Geothermal Power Projects in the Phillippines Shared Autonomous Taxis: Implementing an Efficient Alternative to Automobile Dependency Applications of Recombining Stochastic Volatility Trees Too Big to Fail: A Market Study of the Banking Consolidation Phenomenon on Wall Street Dynamic Rate Queues for Efficient Staffing of Hospital Cleaning Services Future Prospects of OPEC and the Oil Market

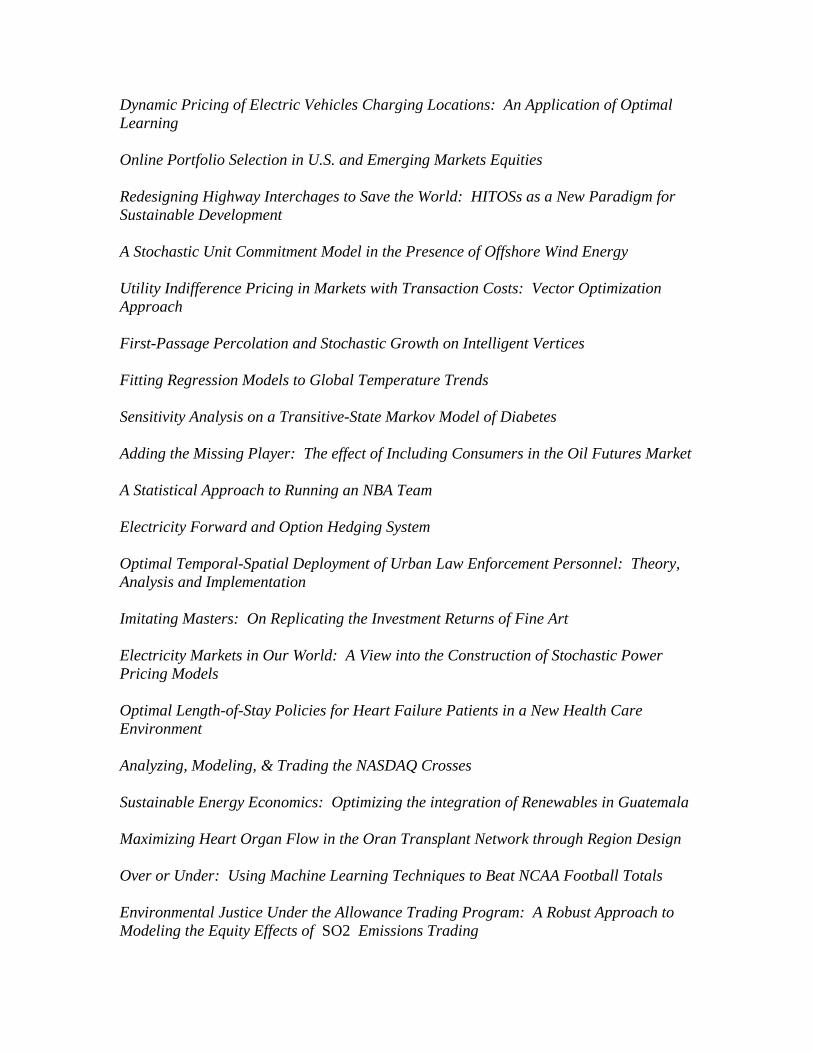

Dynamic Pricing of Electric Vehicles Charging Locations: An Application of Optimal Learning Online Portfolio Selection in U.S. and Emerging Markets Equities Redesigning Highway Interchages to Save the World: HITOSs as a New Paradigm for Sustainable Development A Stochastic Unit Commitment Model in the Presence of Offshore Wind Energy Utility Indifference Pricing in Markets with Transaction Costs: Vector Optimization Approach First-Passage Percolation and Stochastic Growth on Intelligent Vertices Fitting Regression Models to Global Temperature Trends Sensitivity Analysis on a Transitive-State Markov Model of Diabetes Adding the Missing Player: The effect of Including Consumers in the Oil Futures Market A Statistical Approach to Running an NBA Team Electricity Forward and Option Hedging System Optimal Temporal-Spatial Deployment of Urban Law Enforcement Personnel: Theory, Analysis and Implementation Imitating Masters: On Replicating the Investment Returns of Fine Art Electricity Markets in Our World: A View into the Construction of Stochastic Power Pricing Models Optimal Length-of-Stay Policies for Heart Failure Patients in a New Health Care Environment Analyzing, Modeling, & Trading the NASDAQ Crosses Sustainable Energy Economics: Optimizing the integration of Renewables in Guatemala Maximizing Heart Organ Flow in the Oran Transplant Network through Region Design Over or Under: Using Machine Learning Techniques to Beat NCAA Football Totals Environmental Justice Under the Allowance Trading Program: A Robust Approach to Modeling the Equity Effects of SO2 Emissions Trading

A Comparison of Methods of Pricing Spread Options in Markets with Transaction Costs Explaining Credit Default Swap Premia: Analyzing the Relationship Between Global CDS Spreads and Stochastically Modeled Default Probabilities Modeling Systemic Risk Using Networks Staffing Technical Support Centers: Forecasting for Multi-Class, Processor Sharing Queues with Dynamic Arrival Rates An In-Depth Analysis of the Employment Situation During the 2008 Recession Simulation Techniques for Bayesian Image Recovery in Lenz-Family Models Predatory Trading on Index Rebalance Dates: Flow Abnormalities and a Case for Front-Running Replication and Comparison of Commodity Futures Trading Strategies TDLoo: Getting a Grip on To-Do Lists Grid Impacts of Charging Electric Vehicles in Urban Areas: A Case Study of Queens, NY Harry Potter’s Life in the Fast Lane: Using ORFE Magic to Forecast Speeds on State Route 167 (Hermonie Granger’s Thesis for a Muggle Studies Degree)

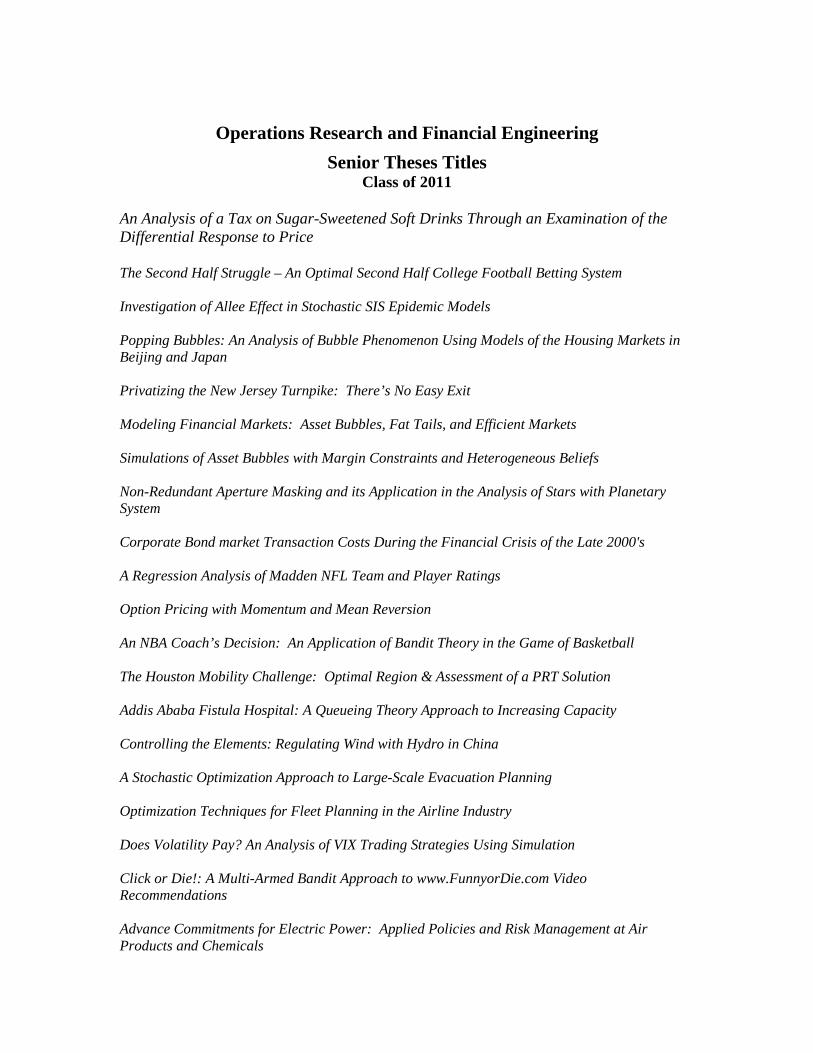

Operations Research and Financial Engineering Senior Theses Titles

Class of 2011

An Analysis of a Tax on Sugar-Sweetened Soft Drinks Through an Examination of the Differential Response to Price The Second Half Struggle – An Optimal Second Half College Football Betting System Investigation of Allee Effect in Stochastic SIS Epidemic Models Popping Bubbles: An Analysis of Bubble Phenomenon Using Models of the Housing Markets in Beijing and Japan Privatizing the New Jersey Turnpike: There’s No Easy Exit Modeling Financial Markets: Asset Bubbles, Fat Tails, and Efficient Markets Simulations of Asset Bubbles with Margin Constraints and Heterogeneous Beliefs Non-Redundant Aperture Masking and its Application in the Analysis of Stars with Planetary System Corporate Bond market Transaction Costs During the Financial Crisis of the Late 2000's A Regression Analysis of Madden NFL Team and Player Ratings Option Pricing with Momentum and Mean Reversion An NBA Coach’s Decision: An Application of Bandit Theory in the Game of Basketball The Houston Mobility Challenge: Optimal Region & Assessment of a PRT Solution Addis Ababa Fistula Hospital: A Queueing Theory Approach to Increasing Capacity Controlling the Elements: Regulating Wind with Hydro in China A Stochastic Optimization Approach to Large-Scale Evacuation Planning Optimization Techniques for Fleet Planning in the Airline Industry Does Volatility Pay? An Analysis of VIX Trading Strategies Using Simulation Click or Die!: A Multi-Armed Bandit Approach to www.FunnyorDie.com Video Recommendations Advance Commitments for Electric Power: Applied Policies and Risk Management at Air Products and Chemicals

Pricing Players: Valuing Major League Baseball’s Free Agents Using Auction Indicating Causes of Major Arm Surgeries for Professional Pitchers Using Basic Performance Statistics Zero Emission Vehicle Credits: An Analysis of the Potential Market Smart Home Appliances: Demand Management as Energy Storage Approximate Dynamic Programming for the Stochastic Load Curtailment Problem An attempt at a precise Digitalization of the Road Network of Burkina Faso Optimal Yield Management Strategy for the Concert Industry: The Newsvendor Problem with Pricing Judging the Judges: A Study of Analysts Performance from 2008-2010 Principal Component Analysis of Corporate Yield Spreads Portfolio Management Strategies for Illiquid Investments Out-of-the-Money Put Options on Nearby Oil Futures Model of Queueing Congestion at Airports: A Case Study on Hartsfield-Jackson Atlanta International Airport A Structural Model for the FCOJ Market Neighborhood Nukes: Great for America? Great for the Environment? Great for Al Qaeda? Markov Chain and Random Walk Analysis of Professional Squash Players Mean Field Variational Inference for Dirichlet Process Mixtures of Generalized Linear Models and Applications in Approximate Q-Learning Options Pricing and Volatility Modeling Through Risk-Neutral Approximations of GARCH Processes The Impact of Solar Energy on the Electricity Spot Market Predicting Politics: A Mathematical Approach to Parsing and Evaluating Presidential Campaign Speeches An Analysis of Derivative Opportunities in Islamic Finance

Cash Holidays and Stock Returns: An Individual Sector Analysis College Tuition: Modeling and Valuation of Contingent Claims The New Asian Option: Using Temperature and Rainfall to Predict and Hedge the Uncertainty in Chinese Tea Harvests Reconsidering Public University Debt Management in Light of the 2008 Financial Crisis: A Stochastic Optimization Approach Principal Component Analysis on the Volatility Term Structure of the United States Treasury and Swap Markets Set-Valued Deviation Measures and Portfolio Selection by Risk Minimization in Markets with Transaction Costs Solving the Stochastic Cash Balance Problem: An Application of Markov Decision Processes An Analysis of Wireless Telecommunication Churn Rates Using data Mining Methods Optimal Staffing in a Hospital’s Emergency Room Through Dynamic Optimization: A Queueing Perspective Profit vs. Altruism: Microfinance Today Expansion into Public Markets and the Developed World Forecasting Unemployment Rates with Spatial Autocorrelation and Regional Heterogeneity A Stochastic Dynamic Programming Model of Ancillary Storage Using Electric Vehicles to Offset Volatility from Wind Generation The Russell Reconstitution: Technical Trading Strategies Dissecting the Flash Crash: A Statistical Analysis of Equity, ETF, and Options Markets Implied Volatility of Options in Changing Market Conditions Bayesian Information Collection in Stochastic Optimization: An Aggregation-Based Approach Maintenance Scheduling for Caracas: Maintaining Power Plants in a Failing Grid

Optimal Investment Under Asymmetric Compensation Contracts in a Discrete-Time Framework Cell Charging Challenges: An Optimal Pricing Strategy for a Solar Mobile Charging System in Africa To Foul or Not: A Study in Basketball End-Game Strategy Superhedging in the Presence of Proportional Transaction Costs in a Multi-Period Setting with Multiple Risky Assests Forecasting MLB Starting Pitchers Future Performances with Regressions and Applied Time Series Analysis Lake Management: Endogenous and Optimal Learning to Reduce Uncertainty Set-Valued Average Value at Risk with Random Transaction Costs The Many Engines That Could: Transporting China’s Population in 2020, Gravity Forecasting Model for Commercial Airline and Rail Travel Winding up the Grid: Optimal Placement of Wind Farms in China

Operations Research and Financial Engineering Senior Theses Titles

Class of 2010

Wheeling Paratransit through the 21st Century: Expansion of GPS Technology in Flexible Route Transportation Epidemiology of the H1N1 Pandemic Influenza From Smart Grid Vision to Reality: Agent-Based Modeling of the Smart Grid Building a Spot-Price Model for Natural Gas From Supply and Demand Fundamentals The Impacts of High-Frequency Trading An Investigation of Factors Affecting Real Estate Price in China Estimating the Risk and Return of Private Equity Investments Using Learning Curves to Optimize Government Subsidies for Photovoltaic Technology The Non-Default Component: The Influence of Liquidity Factors on Corporate Bond Spreads Updating of Entropy Pooling Approach View Confidence Levels Objectively via Model Averaging Simulation and Analysis of an Energy Portfolio Problem Using a Deterministic Linear Program Real-Time Dynamic Congestion Value Pricing, Express Toll Lane Design and Bus Lane Throughput Improvements for the New York-New Jersey Lincoln Tunnel The Impact of Emissions Leakage on Greenhouse Gas Regulation Excessively Conservative Attitudes to Financial Instruments and Low-Risk Hedging: A Contextual Model Proposed for the National Budget of Trinidad and Tobago Improving the Efficiency of the Major League Baseball Rule IV Draft: An Application of Machine Learning Navigation based Services: Request, Organization, Delivery and Consumption Language Processing Techniques for Text Classification with Applications to the Analysis of Financial News Leading to Trading Strategies Regime Identification in Stock Markets and its Applications in Stochastic Portfolio Optimization

Optimal Dosing Applied to Glycemic Control for Type 2 Diabetes Greening the Grid: Optimal Tax Policy for Wind and Solar Technology Characterization and Modeling of Shipping Pick-Up and Delivery Operations Transportation Shocks: Analyzing Transportation Networks for Increased Traffic Flow During the Olympic Games Sovereign Wealth Funds: Their Performance in Global Financial Markets and its Implications for Regulatory Controls Modeling Locational Spreads of Natural Gas Spot Prices: Impact of Pipeline Capacity, Gas Flow, Temperature, & Storage Level Personal Rapid Transit: Qualitative and Quantitative Tools for Analysis Gray Market: Building a Secondary Market for Private Company Equity Towards Optimizing a PRT Network Stochastic Games: The Analysis of Campaign Funds on the 2008 Presidential Race Wind and Pumped-Hydro Power Storage: Determining Optimal Commitment Policies with Knowledge Gradient Non-Parametric Estimation The Valuation of Natural Gas Storage: A Knowledge Gradient Approach with Non-Parametric Estimation Batteries: Storing Wind Utility Pricing of Collateralized Debt Obligations The Promise of Grid Storage: Applications, Regulation, and Revenue-Maximizing Policies for Energy Arbitrage Over the Counter Markets Powering America: Optimizing Electricity Generation for the United States Until 2030 Cuba after Castro: Modeling the Transformation from Collectivism to Capitalism Option-Implied Market Sentiment Stochastic Analysis of Number Games with Jackpots & Sales Forecasting Models for Lottery Operators Optimal Levels of Hourly Wind Generation Commitment and Reserve Portfolio Usage Utility Indifference Pricing Under Prospect Theory

Relative Pricing of Options and Defaultable Bonds under Stochastic Volatility Returns and Risks of the Chinese stock market -a Discrete State Hidden Markov Model Approach Network Failure Localization Using Noisy Search Techniques Game of Numbers: A Statistical Analysis of Rotisserie Fantasy Baseball Optimal Information Collection and Intervention Strategy for an Infectious Disease Outbreak at Princeton University: A Partially Observable Markov Decision Process 20% Wind Generation and the Energy Markets A Model and Simulation of the Effect of Wind on the Optimal Energy Portfolio

Operations Research and Financial Engineering Senior Theses Titles

Class of 2009

Panic on Wall Street: An Implied Volatility Analysis of the Financial Crisis of 2008 Utilizing Wind: Optimal Wind Farm Placement in the United States Reduced Form Pricing Model for Certified Emission Reduction Credits Analysis, Characterization, and Visualization of Freeway Traffic Data and the Effect of Driver Behaviors on Traffic Flows A Model for Pricing the Complex Implicit Options in Collar Offers Lost Decade: 1999 – 2008 The Case for Multi-Strategy Investment Management Stocking a Perishable Good: An Inventory Control Problem An Analysis of the Effects of News on Stock Returns Using Support Vector Machines Inducing Sustainability: Dynamic Firm Behavior Under Environmental Regulation Patterns of Fuel-Efficient Truck Fleet Driving and Routing: Analysis of GPS Data from the 2008 Oil Bubble Systematic Handicapping of Horse Races Using Regression and Applied Forecasting Techniques A Star Pattern Recognition Algorithm for Astronomical Images Using Triangles A Statistical Approach to Verbal Autopsies: Methods to Enhance Performance and Accuracy U.S. Ethanol Industry: Efficiency, Profitability and Possible Side Effects Comovements of High-Yield Bonds and Equity of Firms Under Varying Market Conditions Behavior of the Base Correlation Skew in CDOs During the Subprime Crisis Energy Resource Allocation Under Uncertainty: Optimal Policies for the Chinese Government Determinants of Stock market Returns in Emerging Markets Long-Term Performance and Option Pricing of Leveraged ETFs

Smart Electricity Meters: Smart Enough to Reduce CO2 Emissions? A Study on Advanced Metering and Other Emission Abatement Strategies in the U.S. SIZE MATTERS Is Big More Beautiful in Venture Capital Financing? Multi Objective Decision Making Using AHP Criteria to Solve an Advertising Planning Problem Combining Topic Features with Text Classification for Predicting Abnormal Returns Using News Articles Empirical Analysis of Deviations from Option Market Prices Using Stochastic Volatility Models Economics of the Nuclear Renaissance The Role of Energy Storage in Helping Global Energy Problems Become Gone With the Wind Credit Default Swap Indices: The Feedback Effect on Single-Name Credit Spreads R&D and Stock Markets: Modeling Prices and Predicting Crises Your Oil Highness: The Summer When Crude Was King An Analysis of the Crude Oil Bubble of 2008 A Statistical Analysis of CDO Price Variation and the Role of Risk Aversion Since the Onset of the Subprime Crisis GradeRank: A Mathematical Approach to Contextualizing Grades Modeling the Impacts of Policy on Forecasted Energy Demand in Highway Transportation Wind Farm Valuation Optimal Learning in the Two-Agent Newsvendor Problem Optimal Learning for Drug Design in Ewing’s Sarcoma Greed in Corporate America Help is on the Way: Dynamic Optimization of the Emergency Medical Services System in the City of Philadelphia Exercise Patterns of Executive Stock Options: An Empirical Analysis Forecasting the NBA: Optimal Betting Strategies in Basketball

Operations Research and Financial Engineering Senior Theses Titles

Class of 2008

Project-Based Transactions in the Cap and Trade Market for Carbon Emissions Covariate Selection for Intensity-Based Credit Risk Models Valuation of Swing Options using the Longstaff-Schwartz Method Ex Post Disaster Loans: Optimizing the Small Business Administration's Decision Making Process Optimal Risk Profiling Strategies and Testing Policies for Cardiovascular Disease in Female Patients in the United States Optimizing Equities Statistical Arbitrage with Dynamic Programming The VIX Index and its Options: An Empirical Investigation Unyoking the Cash Cow Who should Own the New Jersey Turnpike? Area-Wide Value Pricing in Manhattan: Implications for Travel in the New York Metropolitan Region Value Opportunities in Highway Infrastructure Analysis of GPS Data to Better Understand The Economics of Congested Highways Disease Dynamics on Topologically Self-Similar Networks Building A Market: How Artificial Agents Can Interact To Create A Realistic Model Raaga Classification Using Machine Learning Techniques Market Expectations during a Crisis: An Analysis of the Implied Volatility Surface of Crude Oil Options Dynamic Congestion Pricing for Parking: Case Study for San Francisco Demystifying Private Equity and Venture Capital via Portfolio Replication Strategies An Examination of the Ethanol Industry's Effect on Agriculture and the Corn-Soybean Planting Decision in the U.S.

The 2007 Subprime Mortgage Crisis: Valuation of Subprime Residential Mortgage-Backed Securities Designing the Perfect Team: Determining an Objective Strategy Towards Being an Efficient NBA General Manager Real Options Analysis as Applied to Research and Development Project Valuation in the Pharmaceutical Industry Forecasting Volatility: Option implied Volatility vs. Historic High-Frequency and Low-Frequency Volatility Trading Places: Optimal Exchange Mechanisms for Kidney Donor-Recipient Pairs

Operations Research and Financial Engineering Senior Theses Titles

Class of 2007

Recommendation Systems: Adapting Collaborative Filtering Models to Minimal Resource Environments An Approximate Dynamic Programming Approach for Routing a Bulk Carrier Vessel Probability Distribution Models for the Hurricane Damage Process Construction and Analysis of a Domestic Fashion Index A Binomial Approach to the Optimal Timing of Reverse Leveraged Buyouts and Their Post-OfferingPerformance Saving the Green: An Analysis of Hedging Strategies for the EU-ETS Carbon Dioxide Market “Super-Indexing the GSCT”: Portfolio Optimization in Commodity Futures Markets Top-Down or Bottom-Up? An Examination of Multi-Name Credit Derivative Pricing Models Striking a Balance Between Health Care Costs And Compliance Using Dynamic Programming Correlation Car Crash: Credit Crisis of May 2005 Dissecting the Collapse of Amaranth Advisors LLC (2006): Natural Gas Stochastic Volatility, Irrational Position-Sizing and Predatory Trading The Quadrivalent Human Papillomavirus Vaccine: A Cost-Benefit Analysis of Cervical Cancer Prevention Strategies Anticipating the Future: Financial Risk Management for Princeton University A Tour Through the Traveling Salesman Problem: An Implementation with Experiments Specific Weather Event Risk Hedging: An Examination of the Citrus Market Smart Cards: How Smart Are They? A New Look at Travel Behavior Distribution of Antiviral Drugs During Pandemic Influenza

Optimal-Server Staffing: Queueing Analysis of Airline Check-In and Baggage Handling Algorithms for Solving and Generating Sudoku Puzzles Optimal Exercise Patterns and Valuation of Employee Stock Options: An Approximate Dynamic Programming Approach The Client-Facing Apptroach to Mass Transit: Modeling Rliability on the Washington Metro Strategic Spending: Equilibrium Strategies in Multi-Period Campaign Spending Games Oil Supply Strategies: An Analysis of the Efficacy of Cooperative Solutions The Carry-To-Risk Portfolio Model: A Monte Carlo Approach to Optimality The Game Behind the Game: An Analysis of Baseball Player Evaluation Models Approximate Dynamic Programming for Equity Portfolio Selection Pricing Catastrophe Bonds and Industry Loss Warranties Within a Compound Poisson Process Framework Housing Futures And Options on the Chicago Mercantile Exchange: Trading Analysis and Implications for Business and Individuals Random Walk With a Movable Boundary Optimizing Seed Stock Levels in the Wireless Industry Dynamic Modeling of Optimal Housing Tenure Choice for Low-Income Households

Operations Research and Financial Engineering Senior Theses Titles

Class of 2006

Optimal Portfolio Rebalancing: An Approximate Dynamic Programming Approach Are Multiple Acts of Deception Preferable to One? A Comparison of Hierarchical and Centralized Resource Allocation Centralization and the Robustness of Military Supply Chains: A Scenario Analysis for the Design of Fuel Distribution Infrastructure Dynamic Jet Fuel Hedging Strategies Life Saving Decisions: A Model For Optimal Blood Inventory Management Towards an American Model: The Impact of Venture Capital Investment Characteristics on Performance: A Comparative Study of the United States, United Kingdom and Canada An Optimization Analysis of Eating at Popular Restaurant Chains A Dynamic Programming Approach to Decision Making in Texas Hold’em Poker Multivariate Analysis of NCAA Division I-A Football For The Purpose Of Predicting Games Portfolio Optimization Involving Short Sales The Interaction of Behavioral Agent Characteristics and Stock Prices: An Evaluation via Artificial Markets An Analysis of Market Efficiency in the National Basketball Association Betting Market The Effects of Uncertainty in Oil Reserves: Stochastic Resource Levels in Cournot Competition Revenue Management in Major League Baseball Forecasting Currency Volatility and Evaluating its Impact on Quantitative FX Strategies The Soccer World Cup: A Mathematical Approach

Dynamic Optimal Portfolio Rebalancing: Strategies for Corporate Finance Mergers and Acquisitions: A Behavioral Economics Approach A Parametric Analysis of Private Equity Performance An Investigation of Efficiency in National Football League In-Game Betting Markets Improving the Spatial Accuracy of Digital Maps: An Algorithm to Align the Road Network to Real GPS Data Fueling Change in The United States: An Analysis of Gasoline Price Elasticity Optimal Gambling Strategies & Their Financial Applications Can PRT Perform? Surge Management Analysis Applied The Valuation of Real-Time Information for Road Surface Navigation Systems News or Noise: Text Classification of Financial News Using Support Vector Machines Modeling Treatment Patterns & Outcomes of Schizophrenic Patients Interest Rate Model Calibration: An Analysis of Rank vs. Stability Path Theory: A Model of Pedestrian Route Choice The Effect of Political Reforms on Interest Rates as Turkey Negotiates Accession to the European Union Dynamic Optimal Staffing of Police Patrol Services Asymmetric Objectives & Inefficient Markets: A Non-Parametric Predictor for Major League Baseball Games And the Evaluation of Betting Lines Volatility Dynamics in the Money Market Evaluating the Hedge Fund Hype: Is There A True Performance Profile of Hedge Funds? A Modern Examination of Lee’s Investor Sentiment Theory behind the Closed-End Fund Discount Discipling The World From Home: A Relative Efficiency Analysis of International Student Ministry in United States Universities

Analizing Exercise Behavior After IPO Lockups: A Theoretical Incentive Model to Optimize Shareholder Exercise Strategy Empirical Analysis of Executive Stock Option Block Exercise Pricing Crash Options Under Jump Diffusion Models A Discrete Model for Real Options and a Fair Gamble Applications of the Beer Distribution Game in Supply Chain Decision Making Modeling the Allocation of Trailers in the Southeastern United States for Future Hurricane Preparation Approximate Dynamic Programming Methods For Speeder Apprehension Measuring Risk in Sectors of the S&P 500: Value-at-Risk and Expected Shortfall Using GARCH Path Estimation Using Cellular Handover An Optimization Model for Evaluating Earthquake Mitigation Strategies in San Francisco Optimal Trading: Dynamic Stock Liquidation Strategies The Value of Marriage: Valuing the Pacification Effect on Young Men Forecasting Motion Picture Box-Office Returns and Analysis of the Hollywood Stock Exchange Investigating the Risk-neutral Intensity Process for the Electricity and Other Sectors A Physical Approach to Asset Bubbles

Operations Research and Financial Engineering Senior Theses Titles

Class of 2005

Playing Games with the Environment: A Quantitative Analysis of CO2 Abatement Strategies

The Stock Market Overreaction Mystery: Human Judgment Bias in Financial Decision-Making The Structure and Effectiveness of Price Hedging Contracts Implemented by Independent Oil and Gas Producers Modeling Optimal Stocking Strategy for Booksellers with Emphasis on Browse Purchase Optimal High School Sizes in Relation to School Demographics Risk Assessment in the California Energy Crisis Investment Under Uncertainty: Optimal Strategies of CO2 Emitting Firms Under the Kyoto Global Emissions Trading Market U. S. Trust Fund Management: Federal Spending Under the Influence of Trust Fund Surpluses Insights into the Nature of Successful Acquisitions: An Empirical Approach Approximate Dynamic Programming for Aerial Refueling A Method to March Madness: Logistic Regression and the NCAA Tournament A Model for the Dynamic Management of Power Transformers Below the Financial Mendoza Line: Identifying Relocation and Contraction Candidates in Major-League Baseball An Analysis of the Practical Application of Pari-mutuel Pricing Systems Valuing Executive Stock Options with Blackout Periods The Wisdom of Gamblers? An Analysis of Efficiency in NFL Betting Markets and a Profitable Betting Algorithm Google Versus Goldman: Can Dutch Auctions Revolutionize Wall Street?

Effects of Nonstationary Emergency Call Arrival Rates on an Ambulance Response System Catastrophic Bonds Linked to Terrorism: Quantifying and Pricing Terrorism Risk in the United States A Queuing Theory Analysis of the Princeton University Office of Information Technology Help Desk Center The Wealth of Nations: An Analysis to the Correlation between United States Economic Indicators and the Probability of Default of Emerging Market Countries Exploring American Demand for Canadian Pharmaceuticals: A Balance between Capital Market Theory A Moral Responsibility Identity in Print: Authorship Attribution Using Markov Chains of liberal and Grammatical Components Risk Measures and Capital Regulation Describing the Dependence Structures between Temperature and Natural Gas Prices Interaction-Induced Enhancement of Portfolio Credit Risk Credit Spread Dynamics and the Macro-Economy: An Empirical Investigation An Investigation of Incomplete Information Models of Default: A Case Study of Enron’s Collapse Neural Networks: An Analysis of the Types of Networks to use with Specific Stock Industries Revenue Maximization for Software; Dynamically Solving the Versioning and Pricing Problems Hello, Is Anybody In There? The Search for the Optimal Route-Planning and Decision-Making Method for Autonomous Ground Vehicle Control Information Acquisition and Baseball= A Study of the Statistical Value of Batting Average Modeling the Spread of HIV-AIDS and the Financial Resource Needs in China The Washington Road Tunnel Project: Integrating the Campus of Princeton University

How Much are they Really Worth? Optimization of the NBA Free Agent Market Managing Terrorist Risk at Sea Ports: A National Security Dilemma Buying and Selling Movies: An Analysis of the Hollywood Stock Exchange Measuring the Relative Accessibility of the Princeton Campus for People with Disabilities Optimization Strategies for Portfolios Containing Hedge Funds: An Investigation of Modern Portfolio Theory and the Effects of Regime Shifts Stochastic Modeling of the PCS Loss Index: A Sensitivity Analysis and its Implications for Catastrophe Bond Pricing Models Putting a Price on Performance: A Study of Risk Hedging in Major League Baseball Migration and Institutionalized Exclusion in Shanghai Cities of Foam: Exploring Nigeria’s Potential for Privatized, Low- Cost Housing Development Ideal Damping Factor for Simulating Portfolio Returns: A Market Representative Approach

Operations Research and Financial Engineering Senior Theses Titles

Class of 2004

The End of Congestion: Developing a Large Scale “Floating Car Data” System Evolving Signals to Solve a Coordination Problem Competition in the Airline Industry: The Battle Between Legacy And Low Cost Carriers Capacity Constraints in Repeated Competition: An Extended Game Theory Approach to Duopoly Stochastic Transportation Networks: Distribution of Link and Path Travel Times Modeling the Impact of Funding on Tuberculosis Control in India Proposed Changes to Princeton Dining Services Under a Four Year Residential College System Modernizing Stocks and “Barry Bonds”: Evaluating Players and Optimal Team Strategy in Baseball Free Agent Markets Stocks and “Barry Bonds”: Evaluating Players and Optimal Team Strategy in Baseball Free Agent Markets Stochastic Efficiency in Portfolio Optimization: Properties and Computation Learning to Buy Futures: An Approximate Dynamic Programming Approach Improving the Lots: Actuarial Testing, Survival Analysis, and Megan’s Law Credit Risk Extensions to the Markovian Model An Epidemiological Study on the Growing Problem of Obesity in China A Statistical Analysis of 1990s New Yorker Fiction Evaluation and Improvement of Technical Trading Rules on the Foreign Exchange Market An Analysis of Expected Shortfall as a Method of Measuring Risk in Credit Portfolios Real Options: A Comparative Evaluation of Existing Models

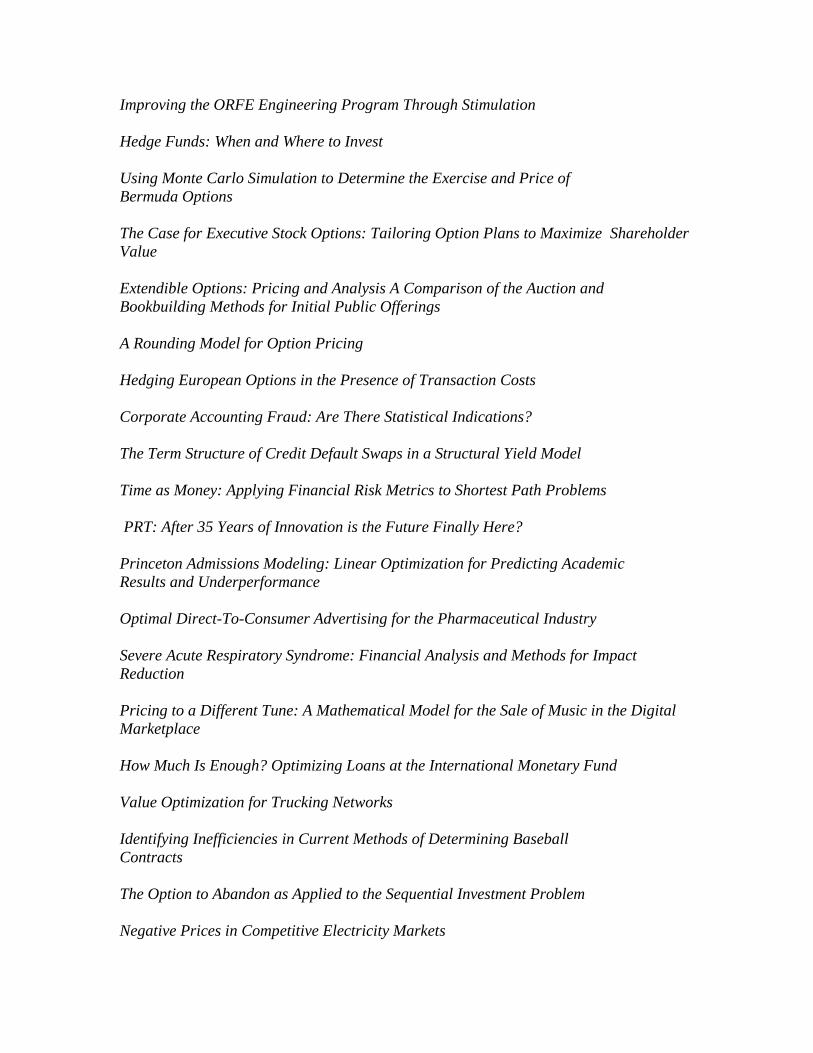

Improving the ORFE Engineering Program Through Stimulation Hedge Funds: When and Where to Invest Using Monte Carlo Simulation to Determine the Exercise and Price of Bermuda Options The Case for Executive Stock Options: Tailoring Option Plans to Maximize Shareholder Value Extendible Options: Pricing and Analysis A Comparison of the Auction and Bookbuilding Methods for Initial Public Offerings A Rounding Model for Option Pricing Hedging European Options in the Presence of Transaction Costs Corporate Accounting Fraud: Are There Statistical Indications? The Term Structure of Credit Default Swaps in a Structural Yield Model Time as Money: Applying Financial Risk Metrics to Shortest Path Problems PRT: After 35 Years of Innovation is the Future Finally Here? Princeton Admissions Modeling: Linear Optimization for Predicting Academic Results and Underperformance Optimal Direct-To-Consumer Advertising for the Pharmaceutical Industry Severe Acute Respiratory Syndrome: Financial Analysis and Methods for Impact Reduction Pricing to a Different Tune: A Mathematical Model for the Sale of Music in the Digital Marketplace How Much Is Enough? Optimizing Loans at the International Monetary Fund Value Optimization for Trucking Networks Identifying Inefficiencies in Current Methods of Determining Baseball Contracts The Option to Abandon as Applied to the Sequential Investment Problem Negative Prices in Competitive Electricity Markets

Re-engineering Portfolio Theory: Optimizing the Diversification of Moet Hennessy-Louis Vuitton (LVMH)

Operations Research and Financial Engineering Senior Theses Titles

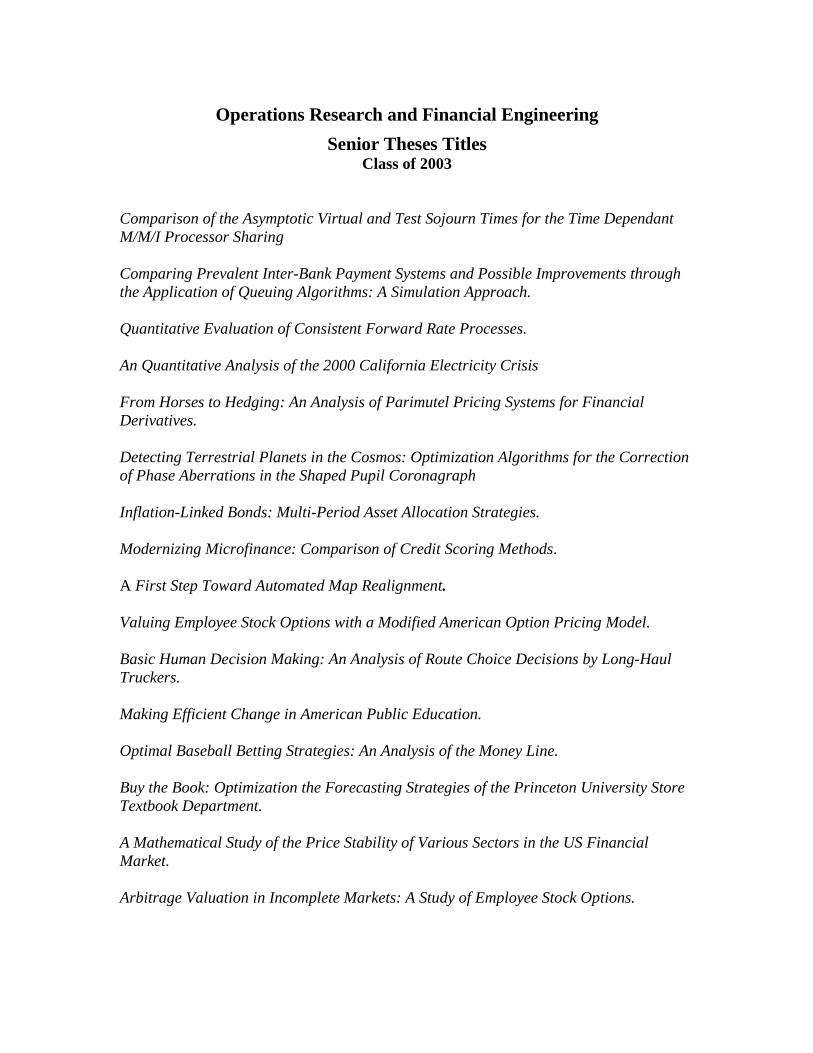

Class of 2003

Comparison of the Asymptotic Virtual and Test Sojourn Times for the Time Dependant M/M/I Processor Sharing

Comparing Prevalent Inter-Bank Payment Systems and Possible Improvements through the Application of Queuing Algorithms: A Simulation Approach. Quantitative Evaluation of Consistent Forward Rate Processes. An Quantitative Analysis of the 2000 California Electricity Crisis From Horses to Hedging: An Analysis of Parimutel Pricing Systems for Financial Derivatives. Detecting Terrestrial Planets in the Cosmos: Optimization Algorithms for the Correction of Phase Aberrations in the Shaped Pupil Coronagraph Inflation-Linked Bonds: Multi-Period Asset Allocation Strategies. Modernizing Microfinance: Comparison of Credit Scoring Methods. A First Step Toward Automated Map Realignment. Valuing Employee Stock Options with a Modified American Option Pricing Model. Basic Human Decision Making: An Analysis of Route Choice Decisions by Long-Haul Truckers. Making Efficient Change in American Public Education. Optimal Baseball Betting Strategies: An Analysis of the Money Line. Buy the Book: Optimization the Forecasting Strategies of the Princeton University Store Textbook Department. A Mathematical Study of the Price Stability of Various Sectors in the US Financial Market. Arbitrage Valuation in Incomplete Markets: A Study of Employee Stock Options.

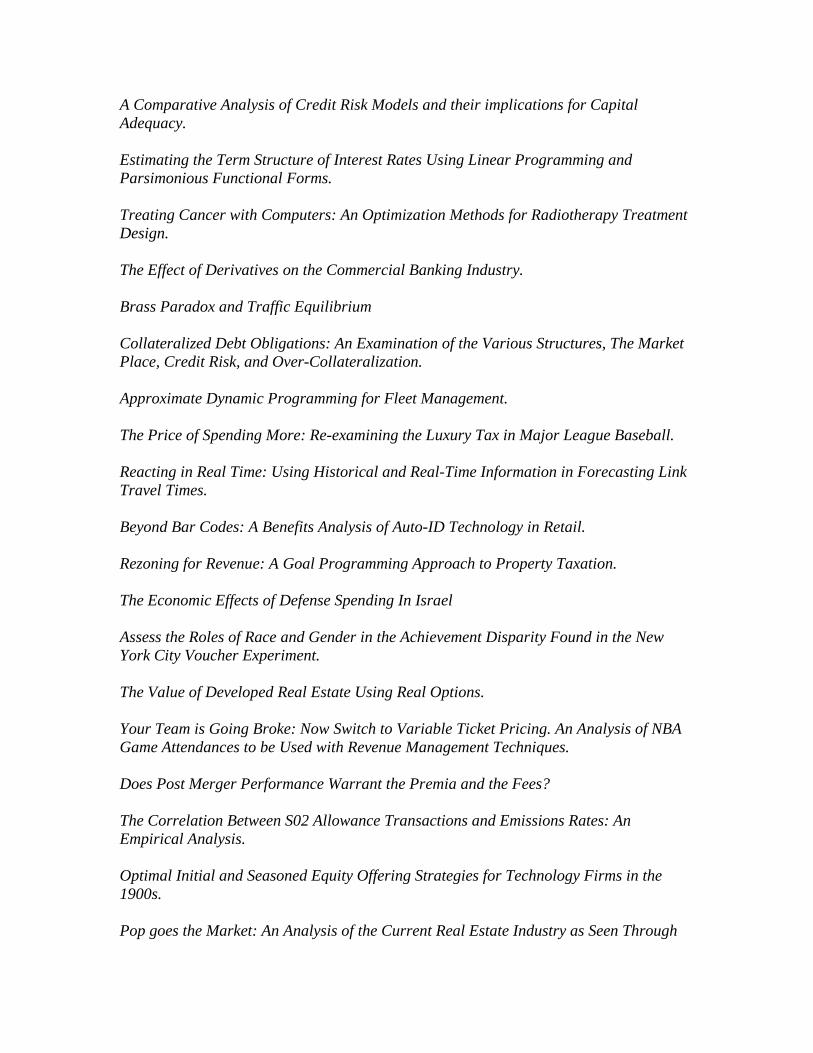

A Comparative Analysis of Credit Risk Models and their implications for Capital Adequacy. Estimating the Term Structure of Interest Rates Using Linear Programming and Parsimonious Functional Forms. Treating Cancer with Computers: An Optimization Methods for Radiotherapy Treatment Design. The Effect of Derivatives on the Commercial Banking Industry. Brass Paradox and Traffic Equilibrium Collateralized Debt Obligations: An Examination of the Various Structures, The Market Place, Credit Risk, and Over-Collateralization. Approximate Dynamic Programming for Fleet Management. The Price of Spending More: Re-examining the Luxury Tax in Major League Baseball. Reacting in Real Time: Using Historical and Real-Time Information in Forecasting Link Travel Times. Beyond Bar Codes: A Benefits Analysis of Auto-ID Technology in Retail. Rezoning for Revenue: A Goal Programming Approach to Property Taxation. The Economic Effects of Defense Spending In Israel Assess the Roles of Race and Gender in the Achievement Disparity Found in the New York City Voucher Experiment. The Value of Developed Real Estate Using Real Options. Your Team is Going Broke: Now Switch to Variable Ticket Pricing. An Analysis of NBA Game Attendances to be Used with Revenue Management Techniques. Does Post Merger Performance Warrant the Premia and the Fees? The Correlation Between S02 Allowance Transactions and Emissions Rates: An Empirical Analysis. Optimal Initial and Seasoned Equity Offering Strategies for Technology Firms in the 1900s. Pop goes the Market: An Analysis of the Current Real Estate Industry as Seen Through

the Patterns of Past Bubbles. Achieving Road Safety through Information: Bringing Real-Time Weather Data to In- Vehicle Navigation Systems. Price Volatility Risk Management in the Ethanol Industry. Assimilating Distributed Expert Knowledge: The Updateability of Map Information. Taking AIM at Stock Price Fluctuations: Applications of Financial Engineering and Artificial Intelligence Methodology to Correlate Stock Prices and News Events. Speculation, Liquidity, and Information: The Puzzle of Chinese B-Shares The Influence of Nationally Recognized Statistical Rating Organization: An Analysis of the Effects of Different Types of Moody’s Rating Downgrades on the Equity Market.

Operations Research and Financial Engineering Senior Theses Titles

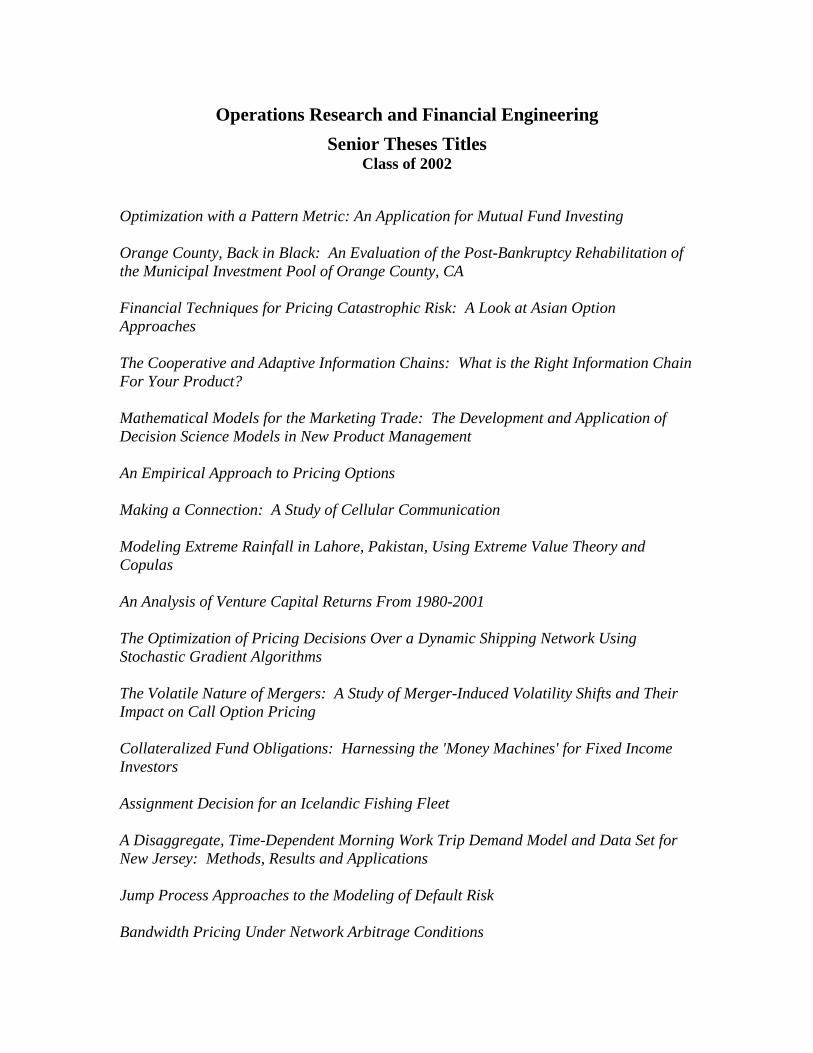

Class of 2002

Optimization with a Pattern Metric: An Application for Mutual Fund Investing Orange County, Back in Black: An Evaluation of the Post-Bankruptcy Rehabilitation of the Municipal Investment Pool of Orange County, CA Financial Techniques for Pricing Catastrophic Risk: A Look at Asian Option Approaches The Cooperative and Adaptive Information Chains: What is the Right Information Chain For Your Product? Mathematical Models for the Marketing Trade: The Development and Application of Decision Science Models in New Product Management An Empirical Approach to Pricing Options Making a Connection: A Study of Cellular Communication Modeling Extreme Rainfall in Lahore, Pakistan, Using Extreme Value Theory and Copulas An Analysis of Venture Capital Returns From 1980-2001 The Optimization of Pricing Decisions Over a Dynamic Shipping Network Using Stochastic Gradient Algorithms The Volatile Nature of Mergers: A Study of Merger-Induced Volatility Shifts and Their Impact on Call Option Pricing Collateralized Fund Obligations: Harnessing the 'Money Machines' for Fixed Income Investors Assignment Decision for an Icelandic Fishing Fleet A Disaggregate, Time-Dependent Morning Work Trip Demand Model and Data Set for New Jersey: Methods, Results and Applications Jump Process Approaches to the Modeling of Default Risk Bandwidth Pricing Under Network Arbitrage Conditions

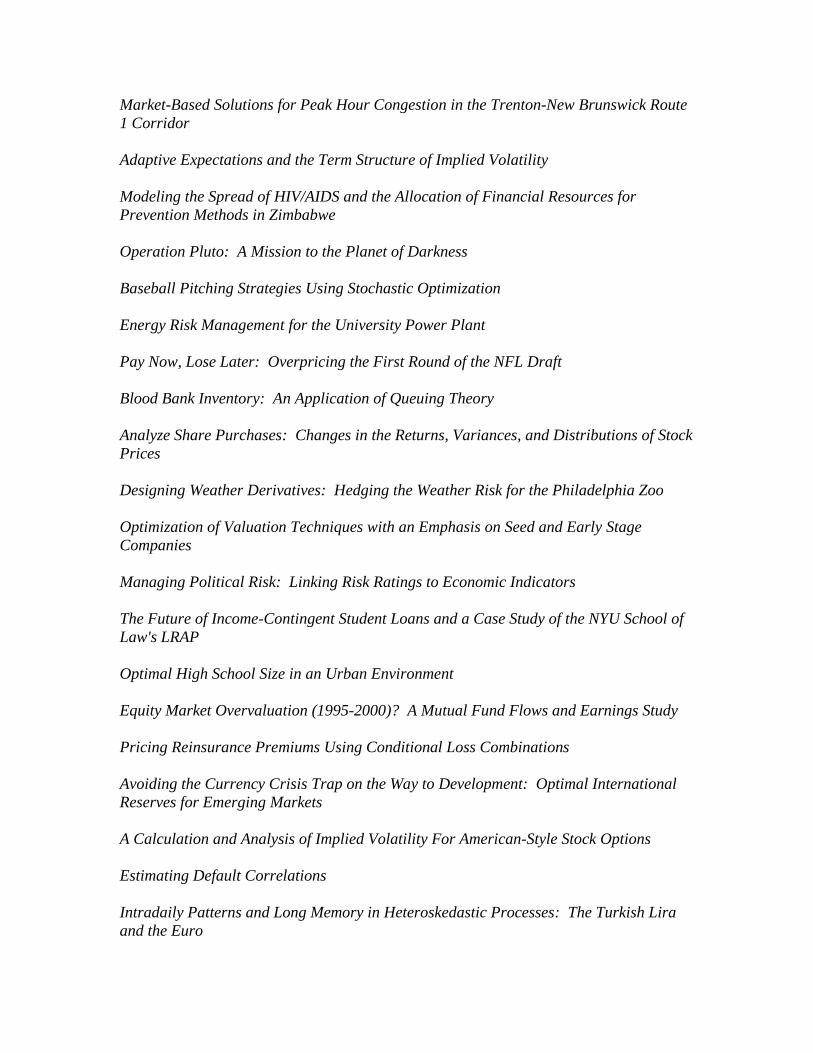

Market-Based Solutions for Peak Hour Congestion in the Trenton-New Brunswick Route 1 Corridor Adaptive Expectations and the Term Structure of Implied Volatility Modeling the Spread of HIV/AIDS and the Allocation of Financial Resources for Prevention Methods in Zimbabwe Operation Pluto: A Mission to the Planet of Darkness Baseball Pitching Strategies Using Stochastic Optimization Energy Risk Management for the University Power Plant Pay Now, Lose Later: Overpricing the First Round of the NFL Draft Blood Bank Inventory: An Application of Queuing Theory Analyze Share Purchases: Changes in the Returns, Variances, and Distributions of Stock Prices Designing Weather Derivatives: Hedging the Weather Risk for the Philadelphia Zoo Optimization of Valuation Techniques with an Emphasis on Seed and Early Stage Companies Managing Political Risk: Linking Risk Ratings to Economic Indicators The Future of Income-Contingent Student Loans and a Case Study of the NYU School of Law's LRAP Optimal High School Size in an Urban Environment Equity Market Overvaluation (1995-2000)? A Mutual Fund Flows and Earnings Study Pricing Reinsurance Premiums Using Conditional Loss Combinations Avoiding the Currency Crisis Trap on the Way to Development: Optimal International Reserves for Emerging Markets A Calculation and Analysis of Implied Volatility For American-Style Stock Options Estimating Default Correlations Intradaily Patterns and Long Memory in Heteroskedastic Processes: The Turkish Lira and the Euro

Operations Research and Financial Engineering Senior Theses Titles

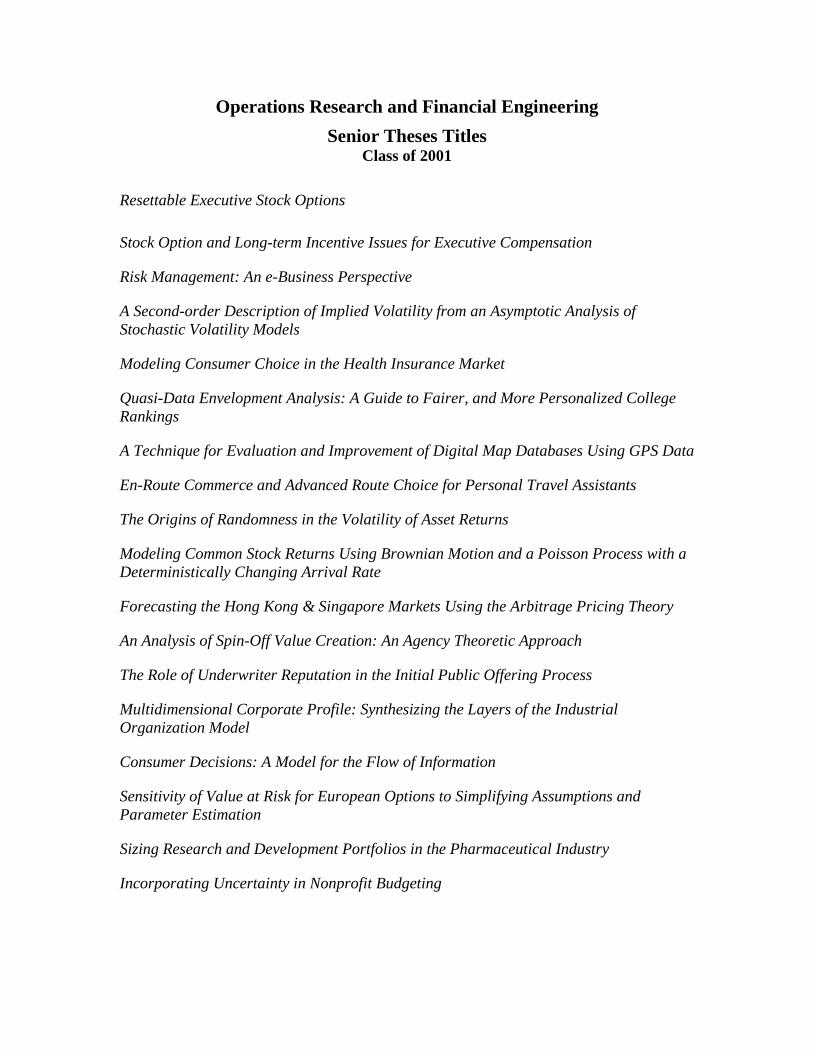

Class of 2001

Resettable Executive Stock Options

Stock Option and Long-term Incentive Issues for Executive Compensation

Risk Management: An e-Business Perspective

A Second-order Description of Implied Volatility from an Asymptotic Analysis of Stochastic Volatility Models

Modeling Consumer Choice in the Health Insurance Market

Quasi-Data Envelopment Analysis: A Guide to Fairer, and More Personalized College Rankings

A Technique for Evaluation and Improvement of Digital Map Databases Using GPS Data

En-Route Commerce and Advanced Route Choice for Personal Travel Assistants

The Origins of Randomness in the Volatility of Asset Returns

Modeling Common Stock Returns Using Brownian Motion and a Poisson Process with a Deterministically Changing Arrival Rate

Forecasting the Hong Kong & Singapore Markets Using the Arbitrage Pricing Theory

An Analysis of Spin-Off Value Creation: An Agency Theoretic Approach

The Role of Underwriter Reputation in the Initial Public Offering Process

Multidimensional Corporate Profile: Synthesizing the Layers of the Industrial Organization Model

Consumer Decisions: A Model for the Flow of Information

Sensitivity of Value at Risk for European Options to Simplifying Assumptions and Parameter Estimation

Sizing Research and Development Portfolios in the Pharmaceutical Industry

Incorporating Uncertainty in Nonprofit Budgeting

Application of Stochastic Dominance and Exponentially Weighted Moving Averages on the Pharmaceutical and Biotechnology Industries

Multi Product Inventory With Substitution In An Electronic Commerce Setting

Learning to fly: An Adaptive Dynamic Programming Approach for the Air Mobility Command Problem

The Future of the Strategic Petroleum Reserve

Impact of Alternative Energy Resources on OPEC Strategy: A Dynamic Model

A Practical Approach to Corporate Default Probability

A New Look at Tender Offer Premiums and Their Predictive Power

The Sound of Money: A Financial Engineering Approach to Recording Contract Profit Maximization

Mixed-Integer Programming in Portfolio Construction

Experiments in Electronic Publishing: Pricing Serial Novels?

Spanish 21: An Investigation of Optimal Playing Strategies

The Economic Impact of Charter Schools and Educational Vouchers on the Princeton Regional School District Parity in the National Football League: The Change in Competitive Balance as a Result of the 1993 Collective Bargaining Agreement

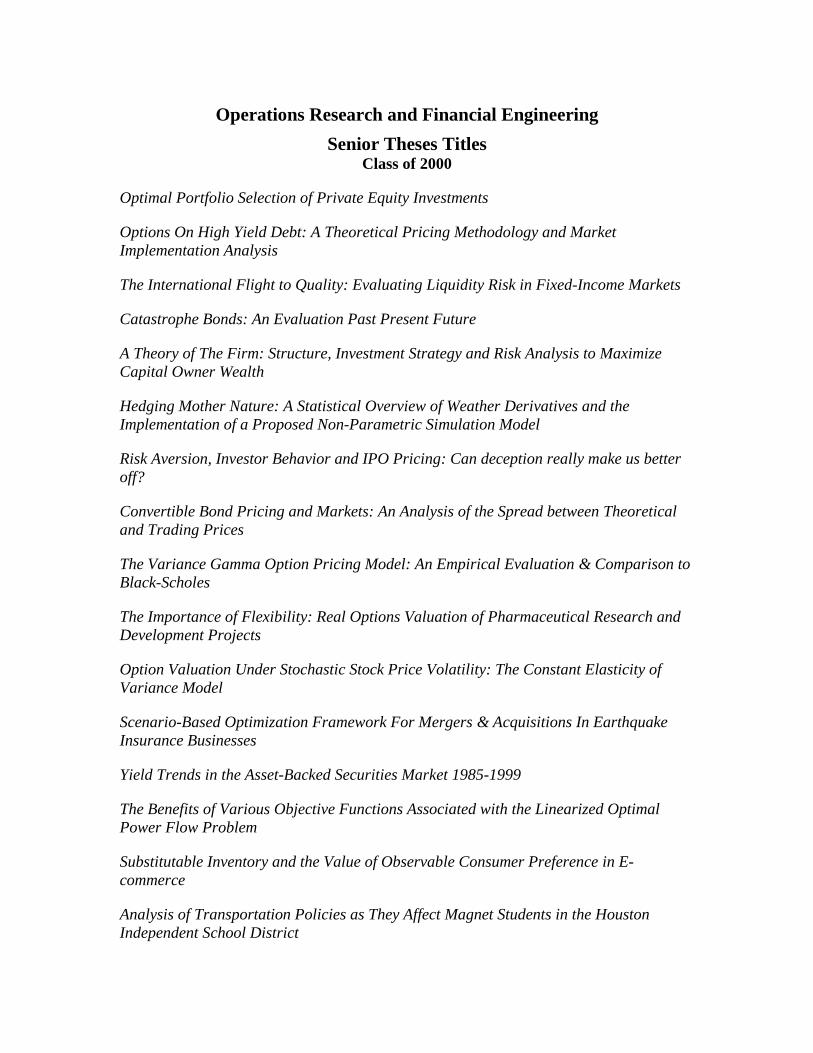

Operations Research and Financial Engineering Senior Theses Titles

Class of 2000

Optimal Portfolio Selection of Private Equity Investments

Options On High Yield Debt: A Theoretical Pricing Methodology and Market Implementation Analysis

The International Flight to Quality: Evaluating Liquidity Risk in Fixed-Income Markets

Catastrophe Bonds: An Evaluation Past Present Future

A Theory of The Firm: Structure, Investment Strategy and Risk Analysis to Maximize Capital Owner Wealth

Hedging Mother Nature: A Statistical Overview of Weather Derivatives and the Implementation of a Proposed Non-Parametric Simulation Model

Risk Aversion, Investor Behavior and IPO Pricing: Can deception really make us better off?

Convertible Bond Pricing and Markets: An Analysis of the Spread between Theoretical and Trading Prices

The Variance Gamma Option Pricing Model: An Empirical Evaluation & Comparison to Black-Scholes

The Importance of Flexibility: Real Options Valuation of Pharmaceutical Research and Development Projects

Option Valuation Under Stochastic Stock Price Volatility: The Constant Elasticity of Variance Model

Scenario-Based Optimization Framework For Mergers & Acquisitions In Earthquake Insurance Businesses

Yield Trends in the Asset-Backed Securities Market 1985-1999

The Benefits of Various Objective Functions Associated with the Linearized Optimal Power Flow Problem

Substitutable Inventory and the Value of Observable Consumer Preference in E-commerce

Analysis of Transportation Policies as They Affect Magnet Students in the Houston Independent School District

The Application of Minimum Cost Machine Scheduling Algorithms to Job Shop Manufacturing

Analysis of the Sampling Mechanism for Providing Travel Time Information

Forecasting Professional Football Scores and Optimizing a Portfolio of Wagers on NFL Games

A Report From The Flight Deck: An Empirical Analysis of the Fractional Jet Ownership Industry

The Feasibility and Effectiveness of the Planned Comprehensive Mass Transit System in Denver

The Application of Constrained Optimization Towards Improved Statistical Analysis of fMRI Images

Elements of Automated Intelligent Vehicles: Image Recognition and Collision Avoidance

Bandwidth Allocation in Packet Networks Using Class and Delay Based Queueing

Improving Individual Decision-Making Through Increased Access to Information

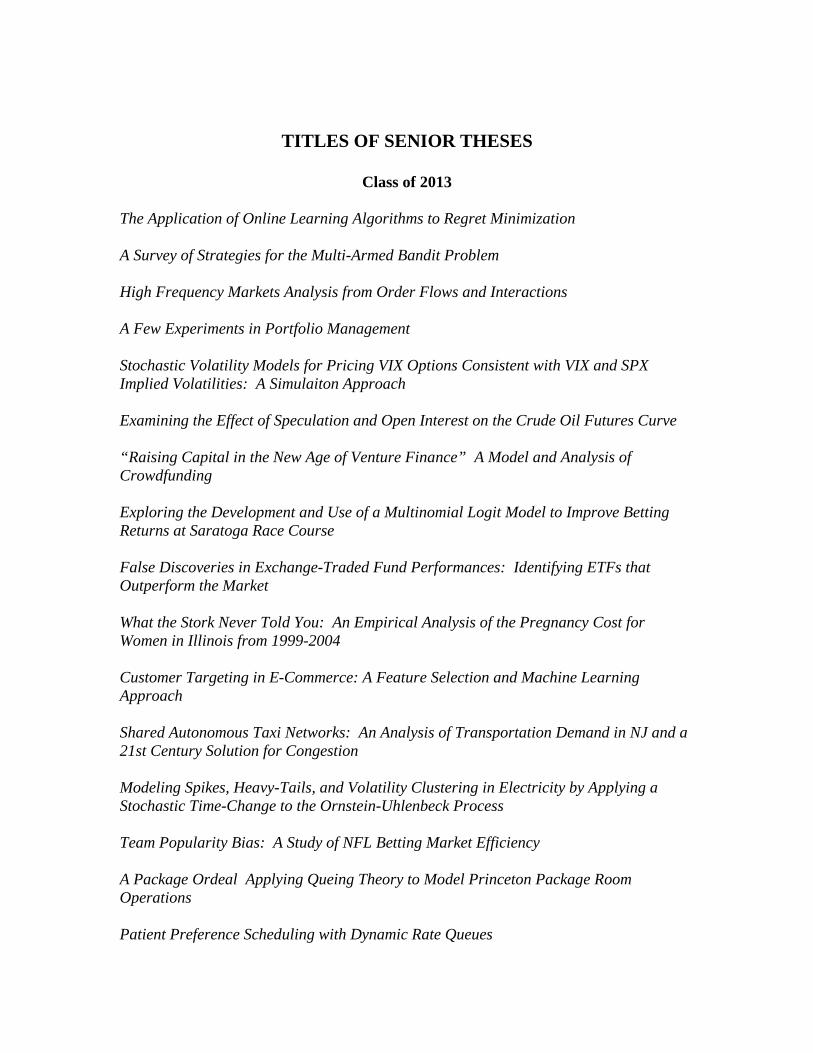

TITLES OF SENIOR THESES

Class of 2013

The Application of Online Learning Algorithms to Regret Minimization A Survey of Strategies for the Multi-Armed Bandit Problem High Frequency Markets Analysis from Order Flows and Interactions A Few Experiments in Portfolio Management Stochastic Volatility Models for Pricing VIX Options Consistent with VIX and SPX Implied Volatilities: A Simulaiton Approach Examining the Effect of Speculation and Open Interest on the Crude Oil Futures Curve “Raising Capital in the New Age of Venture Finance” A Model and Analysis of Crowdfunding Exploring the Development and Use of a Multinomial Logit Model to Improve Betting Returns at Saratoga Race Course False Discoveries in Exchange-Traded Fund Performances: Identifying ETFs that Outperform the Market What the Stork Never Told You: An Empirical Analysis of the Pregnancy Cost for Women in Illinois from 1999-2004 Customer Targeting in E-Commerce: A Feature Selection and Machine Learning Approach Shared Autonomous Taxi Networks: An Analysis of Transportation Demand in NJ and a 21st Century Solution for Congestion Modeling Spikes, Heavy-Tails, and Volatility Clustering in Electricity by Applying a Stochastic Time-Change to the Ornstein-Uhlenbeck Process Team Popularity Bias: A Study of NFL Betting Market Efficiency A Package Ordeal Applying Queing Theory to Model Princeton Package Room Operations Patient Preference Scheduling with Dynamic Rate Queues

Keeping Them Honest: How Medical Services can Maximize Profit while Maintaining Quality of Service with and Optimal Control Policy A Queueing Theory Approach to Modeling Toll Plaza Delay with Applications for Commute User Cost Optimization Three Angry Men: A Game Theoretic Analysis of How the Two-Sided Unanimous Verdict Rule Affects Outcomes in Jury Trials Alternative Investing: The Search for Profitable Trading Strategies in the U.S. Commodity Markets Liquidity and Investment Styles in the Commodity Futures Market New Opportunities in the Currency Carry Trade Are We There Yet? A Proposal for an Autonomous Taxi System in New Jersey and a Preliminary Foundation for Empty Vehicle Routing The Analytic GM: Using Data Mining to Predict NFL Performance Exploring Alternative Treatment for Bacterial Meningitis Through Optimal Dosing Strategy: Responding to Rising Antibiotic Resistance The Future of Solar: An Analysis of New Jersey's Market for Solar Renewable Energy Credits (SRECs) Nested Newsvendor Optimal Commitment Policies in Day-Ahead and Hour-Ahead Electric Capacity Forward Markets Replicating Electricity Spot Prices Through Inverse Optimization of Supply Shocks Methods of Pair Selection in Pairwise Comparisons for Efficient List Ranking Fishing Within the Limits: A Sustainable Fishing Model Forex Market Response: Analysis of Natural Disasters and Their Impact on the Foreign Exchange Market Analysis of Leveraged ETF Compounding Difference Accounting for Population Structure in Lasso Regression for Genome-Wide Association Studies

Modeling Spikes, Heavy-Tails, and Volatility Clustering in Electricity by Applying a Stochastic Time-Change to the Ornstein-Uhlenbeck Process Face Detection, Tracking Methods, and Image Processing: A MATLAB Approach Analyzing and Presenting Modern Temperature Trends The Linear Simplex Method: Investigations of Cycling and Application to Markov Decision Processes

![UNIT CLASSIC UPPER GRADES - TouchMathrty \12 ¢£ ]818 CLASSIC UPPER GRADES 6 MIXED OPERATIONS WITH WHOLE NUMBERS UNIT MODULE TITLES 1: Relationships of Operations 2: Two–Four Digits](https://img.pdfslide.us/doc/110x75/604475fe8574f45c093aa962/unit-classic-upper-grades-touchmath-rty-12-818-classic-upper-grades-6-mixed.jpg)