Embed Size (px)

Citation preview

CIMA OFFICIAL REVISION CARDS

OPERATIONAL LEVEL

SUBJECT F1

Financial Reporting and Taxation

2

FINANCIAL REPORTING AND TAXATION

British library cataloguing-in-publication data

A catalogue record for this book is available from the British Library.

Published by:Kaplan Publishing UK Unit 2 The Business Centre Molly Millars Lane Wokingham Berkshire RG41 2QZ

ISBN 978-1-78415-947-4

© Kaplan Financial Limited, 2017

Printed and bound in Great Britain.

The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited, all other Kaplan group companies, the International Accounting Standards Board, and the IFRS Foundation expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, consequential or otherwise arising in relation to the use of such materials. Printed and bound in Great Britain.

3

FINANCIAL REPORTING AND TAXATION

Acknowledgements

This Product includes propriety content of the International Accounting Standards Board which is overseen by the IFRS Foundation, and is used with the express permission of the IFRS Foundation under licence. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior written permission of Kaplan Publishing and the IFRS Foundation.

The IFRS Foundation logo, the IASB logo, the IFRS for SMEs logo, the “Hexagon Device”, “IFRS Foundation”, “eIFRS”, “IAS”, “IASB”, “IFRS for SMEs”, “IFRS”, “IASs”, “IFRSs”, “International Accounting Standards” and “International Financial Reporting Standards”, “IFRIC” and “IFRS Taxonomy” are Trade Marks of the IFRS Foundation.

Trade Marks

The IFRS Foundation logo, the IASB logo, the IFRS for SMEs logo, the “Hexagon Device”, “IFRS Foundation”, “eIFRS”, “IAS”, “IASB”, “IFRS for SMEs”, “NIIF” IASs” “IFRS”, “IFRSs”, “International Accounting Standards”, “International Financial Reporting Standards”, “IFRIC”, “SIC” and “IFRS Taxonomy”.

Further details of the Trade Marks including details of countries where the Trade Marks are registered or applied for are available from the Foundation on request.

This product contains material that is ©Financial Reporting Council Ltd (FRC). Adapted and reproduced with the kind permission of the Financial Reporting Council. All rights reserved. For further information, please visit www.frc.org.uk or call +44 (0)20 7492 2300.

4

FINANCIAL REPORTING AND TAXATION

How to use Revision Cards

The concept

• Revision Cards are a new and different way of learning, based upon research into learning styles and effective recall.

• The cards are in full colour and have text supported by a range of images, making them far more effective for visual learners and easier to remember.

• Unlike a bound text, Revision Cards can be rearranged and reorganised to appeal to kinaesthetic learners who prefer to learn by doing.

• Being small enough to carry around means that you can take them anywhere. This gives the opportunity to keep going over what you need to learn and so helps with recall.

• The content has been reduced down to the most important areas, making it far easier to digest and identify the relationships between key topics.

• Revision Cards, however you learn, whoever you are, wherever you are.........

5

FINANCIAL REPORTING AND TAXATION

How to use them

Revision Cards are a pack of approximately 52 cards, slightly bigger than traditional playing cards but still very easy to carry and so convenient to use when travelling or moving around. They can be used during the tuition period or at revision.

They are broken up into 3 sections. • An overview of the entire subject in a

mind map form (orange). • A mind map of each specific topic (blue). • Content for each topic presented so that

it is memorable (green).

Each one is a different colour, allowing you to sort them in many ways.

• Perhaps you want to get a more detailed feel for each topic, why not take all the green cards out of the pack and use those.

• You could create your own mind maps using the blue cards to explore how different topics fit together.

• And if there are some topics that you understand, take those out of the pack, leaving yourself only the ones you need to concentrate on.

There are just so many ways you can use them.

6

FINANCIAL REPORTING AND TAXATION

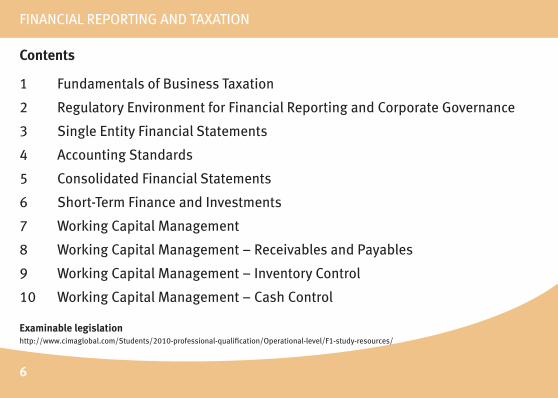

Contents

1 Fundamentals of Business Taxation

2 Regulatory Environment for Financial Reporting and Corporate Governance

3 Single Entity Financial Statements

4 Accounting Standards

5 Consolidated Financial Statements

6 Short-Term Finance and Investments

7 Working Capital Management

8 Working Capital Management – Receivables and Payables

9 Working Capital Management – Inventory Control

10 Working Capital Management – Cash Control

Examinable legislationhttp://www.cimaglobal.com/Students/2010-professional-qualification/Operational-level/F1-study-resources/

7

FINANCIAL REPORTING AND TAXATION

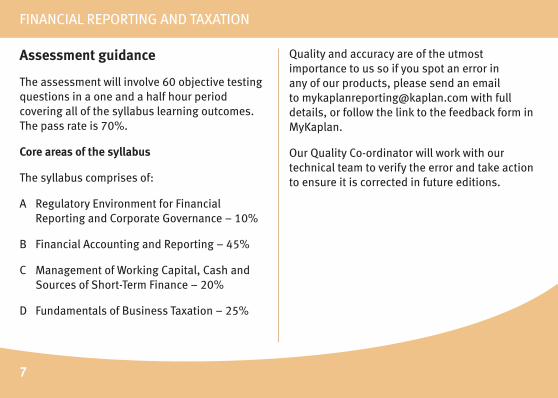

Assessment guidance

The assessment will involve 60 objective testing questions in a one and a half hour period covering all of the syllabus learning outcomes. The pass rate is 70%.

Core areas of the syllabus

The syllabus comprises of:

A Regulatory Environment for Financial Reporting and Corporate Governance – 10%

B Financial Accounting and Reporting – 45%

C Management of Working Capital, Cash and Sources of Short-Term Finance – 20%

D Fundamentals of Business Taxation – 25%

Quality and accuracy are of the utmost importance to us so if you spot an error in any of our products, please send an email to [email protected] with full details, or follow the link to the feedback form in MyKaplan.

Our Quality Co-ordinator will work with our technical team to verify the error and take action to ensure it is corrected in future editions.

RevisionCards

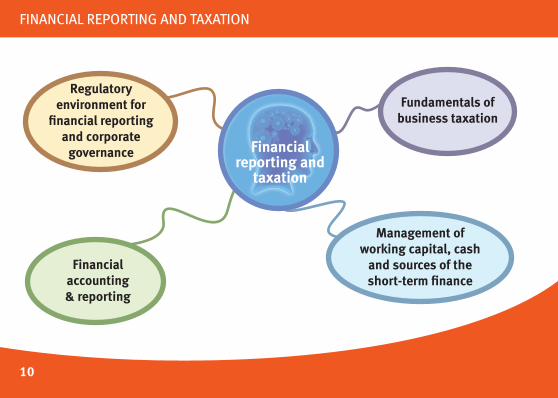

Overviewfinancial reporting and taxation

RevisionCards

FINANCIAL REPORTING AND TAXATION

10

Regulatory environment for

financial reporting and corporate

governance

Fundamentals of business taxation

Financial accounting & reporting

Management of working capital, cash

and sources of the short-term finance

Financial reporting and

taxation

Fundamentals of business taxation

financial reporting and taxation

RevisionCards

12

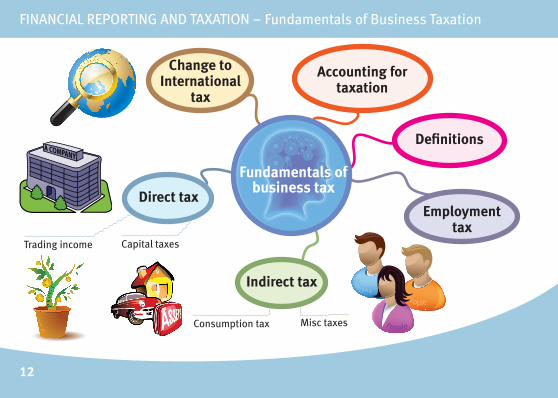

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

Trading income

Change to International

tax

Direct taxEmployment

tax

FOREIGN / OVERSEAS

Definitions

Capital taxes

Consumption tax Misc taxes

Indirect tax

Accounting for taxation

Fundamentals of business tax

13

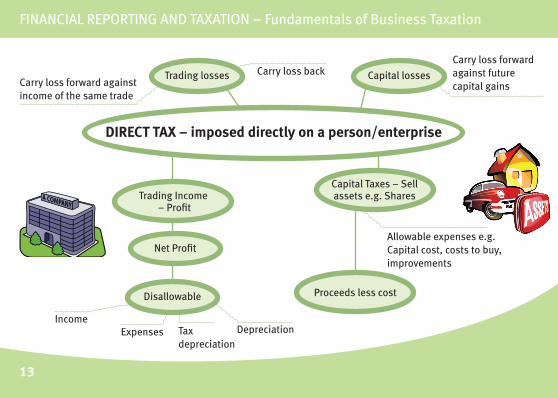

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

Carry loss backCarry loss forward against income of the same trade

Carry loss forward against future capital gains

Net Profit

IncomeExpenses

Allowable expenses e.g. Capital cost, costs to buy, improvements

Tax depreciation

Depreciation

DIRECT TAX – imposed directly on a person/enterprise

Trading losses Capital losses

Net Profit

Trading Income – Profit

Disallowable

Capital Taxes – Sell assets e.g. Shares

Proceeds less cost

14

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

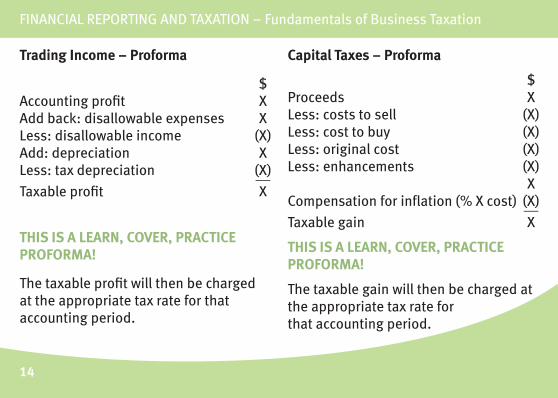

Trading Income – Proforma

$ Accounting profit X Add back: disallowable expenses X Less: disallowable income (X) Add: depreciation X Less: tax depreciation (X) __ Taxable profit X

THIS IS A LEARN, COVER, PRACTICE PROFORMA!

The taxable profit will then be charged at the appropriate tax rate for that accounting period.

Capital Taxes – Proforma

$ Proceeds X Less: costs to sell (X) Less: cost to buy (X) Less: original cost (X) Less: enhancements (X) X Compensation for inflation (% X cost) (X) __Taxable gain X

THIS IS A LEARN, COVER, PRACTICE PROFORMA!

The taxable gain will then be charged at the appropriate tax rate for that accounting period.

15

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

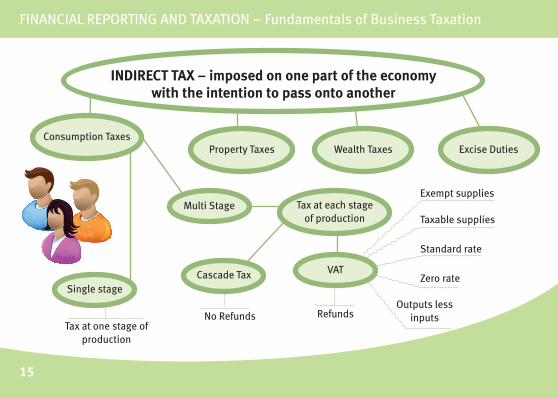

INDIRECT TAX – imposed on one part of the economy with the intention to pass onto another

Consumption TaxesProperty Taxes Wealth Taxes Excise Duties

Single stage

Tax at each stage of production

Multi Stage

Tax at one stage of production

Cascade Tax

No Refunds RefundsOutputs less

inputs

Taxable supplies

Standard rate

Zero rate

Exempt supplies

VAT

16

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

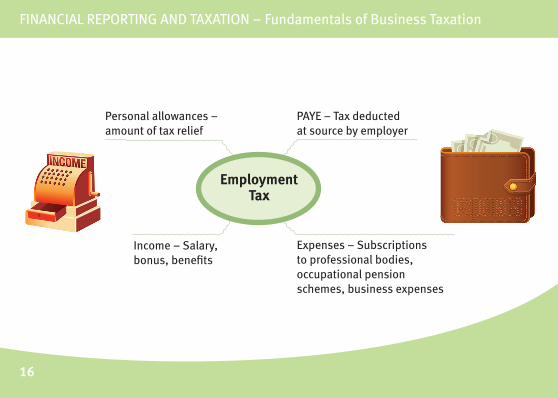

Employment Tax

Personal allowances – amount of tax relief

Income – Salary, bonus, benefits

Expenses – Subscriptions to professional bodies, occupational pension schemes, business expenses

PAYE – Tax deducted at source by employer

17

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

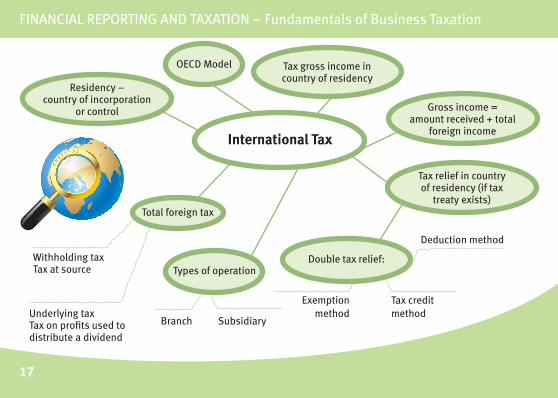

International Tax

Residency – country of incorporation

or control

Tax gross income in country of residency

Gross income = amount received + total

foreign income

Total foreign tax

Tax relief in country of residency (if tax

treaty exists)

Double tax relief:

Tax credit method

Exemption method

FOREIGN / OVERSEAS

Withholding taxTax at source

Underlying taxTax on profits used to distribute a dividend

OECD Model

Deduction method

Branch Subsidiary

Types of operation

18

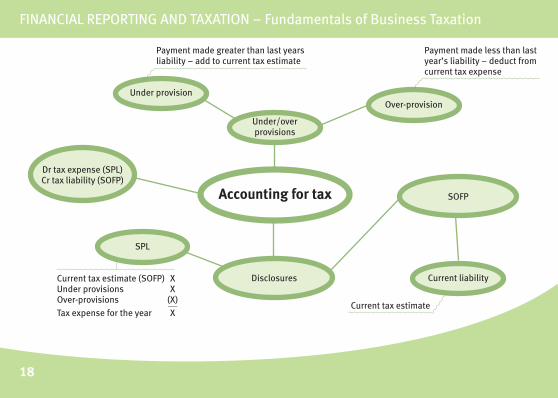

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

Payment made less than last year’s liability – deduct from current tax expense

Current tax estimate (SOFP) XUnder provisions XOver-provisions (X) __Tax expense for the year X

Under provision

Under/over provisions

SPL

Disclosures Current liability

Payment made greater than last years liability – add to current tax estimate

Dr tax expense (SPL)Cr tax liability (SOFP)

Over-provision

Accounting for tax

Current tax estimate

SOFP

19

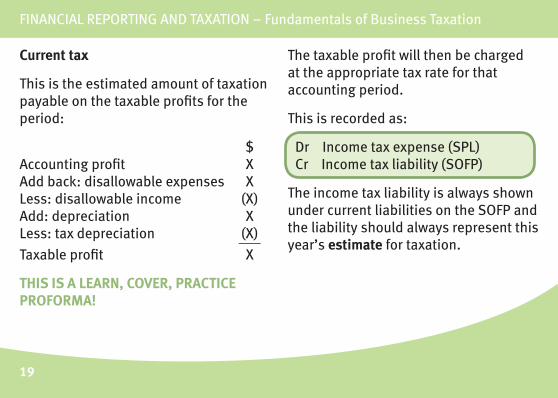

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

Current tax

This is the estimated amount of taxation payable on the taxable profits for the period:

$ Accounting profit X Add back: disallowable expenses X Less: disallowable income (X) Add: depreciation X Less: tax depreciation (X) ___ Taxable profit X

THIS IS A LEARN, COVER, PRACTICE PROFORMA!

The taxable profit will then be charged at the appropriate tax rate for that accounting period.

This is recorded as:

Dr Income tax expense (SPL) Cr Income tax liability (SOFP)

The income tax liability is always shown under current liabilities on the SOFP and the liability should always represent this year’s estimate for taxation.

20

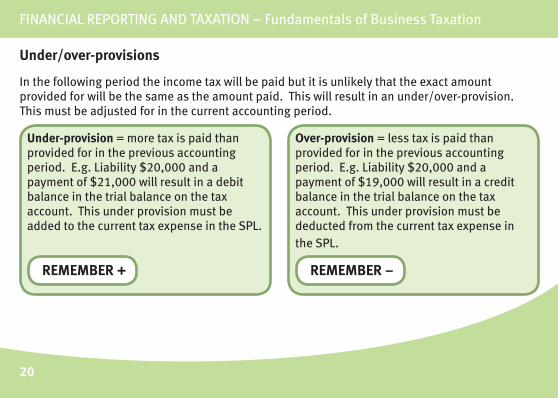

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

Under/over-provisions

In the following period the income tax will be paid but it is unlikely that the exact amount provided for will be the same as the amount paid. This will result in an under/over-provision. This must be adjusted for in the current accounting period.

Under-provision = more tax is paid than provided for in the previous accounting period. E.g. Liability $20,000 and a payment of $21,000 will result in a debit balance in the trial balance on the tax account. This under provision must be added to the current tax expense in the SPL.

Over-provision = less tax is paid than provided for in the previous accounting period. E.g. Liability $20,000 and a payment of $19,000 will result in a credit balance in the trial balance on the tax account. This under provision must be deducted from the current tax expense in the SPL.

REMEMBER –REMEMBER +

21

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

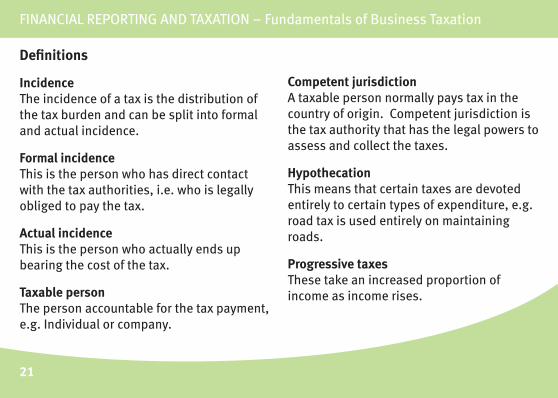

Definitions

IncidenceThe incidence of a tax is the distribution of the tax burden and can be split into formal and actual incidence.

Formal incidenceThis is the person who has direct contact with the tax authorities, i.e. who is legally obliged to pay the tax.

Actual incidenceThis is the person who actually ends up bearing the cost of the tax.

Taxable personThe person accountable for the tax payment, e.g. Individual or company.

Competent jurisdictionA taxable person normally pays tax in the country of origin. Competent jurisdiction is the tax authority that has the legal powers to assess and collect the taxes.

HypothecationThis means that certain taxes are devoted entirely to certain types of expenditure, e.g. road tax is used entirely on maintaining roads.

Progressive taxesThese take an increased proportion of income as income rises.

22

FINANCIAL REPORTING AND TAXATION – Fundamentals of Business Taxation

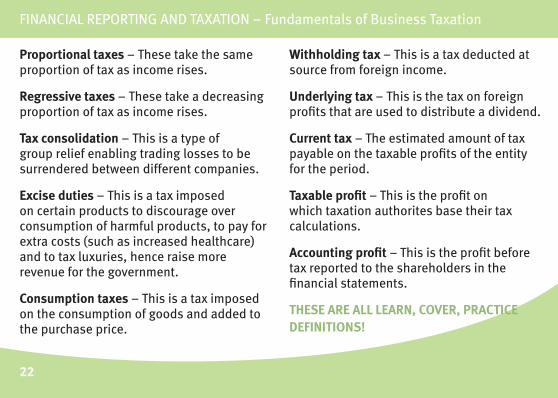

Proportional taxes – These take the same proportion of tax as income rises.

Regressive taxes – These take a decreasing proportion of tax as income rises.

Tax consolidation – This is a type of group relief enabling trading losses to be surrendered between different companies.

Excise duties – This is a tax imposed on certain products to discourage over consumption of harmful products, to pay for extra costs (such as increased healthcare) and to tax luxuries, hence raise more revenue for the government.

Consumption taxes – This is a tax imposed on the consumption of goods and added to the purchase price.

Withholding tax – This is a tax deducted at source from foreign income.

Underlying tax – This is the tax on foreign profits that are used to distribute a dividend.

Current tax – The estimated amount of tax payable on the taxable profits of the entity for the period.

Taxable profit – This is the profit on which taxation authorites base their tax calculations.

Accounting profit – This is the profit before tax reported to the shareholders in the financial statements.

THESE ARE ALL LEARN, COVER, PRACTICE DEFINITIONS!