Embed Size (px)

Citation preview

Operating and

Financial Results

for the six months

ended 30 June 2016

25 August 2016

Disclaimer

The information in this presentation may include forward-looking statements, which are based on current expectations and

projections about future events. These statements may include, without limitation, any statements preceded by, followed by or

including words such as “target,” “expect,” “may,” “anticipate,” “estimate,” “will,” and other words and terms of similar

meaning or the negative thereof. These forward-looking statements, as well as those included in any other material discussed

at the meeting, are subject to risks, uncertainties and assumptions, including, among other things, the development of

Sibanye’s business, general economic conditions and actions of regulators. In light of these risks, uncertainties and

assumptions, the events in the forward-looking statements may not occur. No representation or warranty is made that any

forward-looking statement will come to pass and no reliance should be placed on any forward-looking statement. No one

undertakes to publicly update or revise any such forward-looking statement.

2

Agenda

1. Group Overview

2. Operational Review - Gold and Platinum Divisions

3. Financial Review

4. Conclusion

5. Questions

3

Group

Overview

4

Safety remains our number one priority

• Disappointing regression in the safety performance of the Gold Division requires

decisive action and has resulted in a review of Sibanye’s safety strategy

• Peter Turner has been appointed SVP: Safety, Health and Environment for the

group

• Sibanye is engaging with all stakeholders to jointly address the regression in

safety

• The regression in the safety performance of the Gold Division impacted

negatively on its potential

5Taking decisive action to improve safety

Section 54’s

• SA mining sector safety performance has regressed YoY and must improve

• Where necessary, management will, and does, stop unsafe working places, without

intervention from DMR

• Use of S54 stoppages where appropriate are respected

• However S54 stoppages are not always administered consistently, or in a manner

which will result in improved safety towards the goal of zero harm

• Industry, CoM and Sibanye are engaging with the DMR on the matter - a resolution

will require special leadership from industry, DMR and all other stakeholders

• What is required is to implement safety stoppages such that safety continues to

improve, while also reducing impact on operations

• Recent engagement with Minister of Mineral Resources constructive but greater

alignment across the board is required

6

Salient features*

7Solid operational performance supports increased dividend

• Operational performance:

– Gold production 5% higher to 23 229kg (746 800oz)

– Record attributable PGM (4E) production of 92 773oz for the June quarter

• Costs well managed

– AISC of R448 922/kg increased by 3%

• Operating profit 128% higher at R5.4 billion (US$350 million)

15

20

25

30

35

40

45

2 000

4 000

6 000

H1 2013 H2 2013 H1 2014 H2 2014 H1 2015 H2 2015 H1 2016

%

R m

illio

n

Sibanye operating profit and margin

Gold operating profit (Rm) Platinum operating profit (Rm) Group operating margin (%)

*for the six months ended 30 June 2016 relative to six months ended 30 June 2015

Maintaining operational efficiency and focus

• Risk of operational complacency

– Increased commodity prices and margins

– Significant phantom share scheme payouts to middle management

• Renewed focus on efficiencies and cost management

– Further Gold Division mining unit consolidation

– Capitalising on the higher than expected gold price through incremental mining initiatives

– Continuously driving productivity and efficiency improvements

– Closure of loss making production business units that are being cross-subsidised

– Ensuring platinum synergies are being realised

8

*30 June 2015 to 30 June 2016

Not falling prey to the “Eldorado syndrome”

Relative metal price performance

9Dollar prices improving – strong rand a headwind

Source: iNet as at 11 August 2016

-40

-30

-20

-10

0

10

20

30

40

50

60

Re

lative

pric

e p

erf

orm

an

ce

(%

)

Gold (US$/oz) Gold (R/kg) PGM (R/oz) PGM (US$/oz)

1 2831 205 1 222

1 1931 126 1 106

1 182

1 260

600

700

800

900

1 000

1 100

1 200

1 300

1 400

US$

/oz

Sibanye costs and revenue (US$/oz)

Total cash cost - US$/oz Sustaining capital - US$/oz Gold price - US$/oz

1 116

1 014

1 242

1 0541 007

882 895922

Operationally leveraged to US$ gold price and rand

10Gold division operating margins maintained

* 2016 exchange rate of R15.00:US$

442 255 433 973

459 564462 891

470 349

505 094

600 267 606 379

250 000

350 000

450 000

550 000

650 000

R/k

g

Sibanye costs and revenue (R/kg)

Total cash cost - R/kg Sustaining capital - R/kg Gold price - R/kg

384 877365 076

467 302 409 027 420 811 402 797

454 282 443 912

AISC margin

Competitive global cost position maintained

11• Favourably positioned on the cost curveFavourably positioned on the cost curve

650

700

750

800

850

900

950

1000

1050

1100

1150

US$/o

z

H1 2016 reported AISC

Source: Company releases, Qinisele Resources Research

Salient features* continued

12Robust and flexible financial position

• Strong Balance Sheet despite net debt increasing to R4.4bn due to the

Aquarius acquisition, with Net Debt:EBITDA of 0.41x

• Stability agreement with unions – 3 year 2015 wage agreement secured

• Interim dividend for 2016 of 85 cps – R785 million

*For the six months ended 30 June 2016 relative to six months ended 30 June 2015

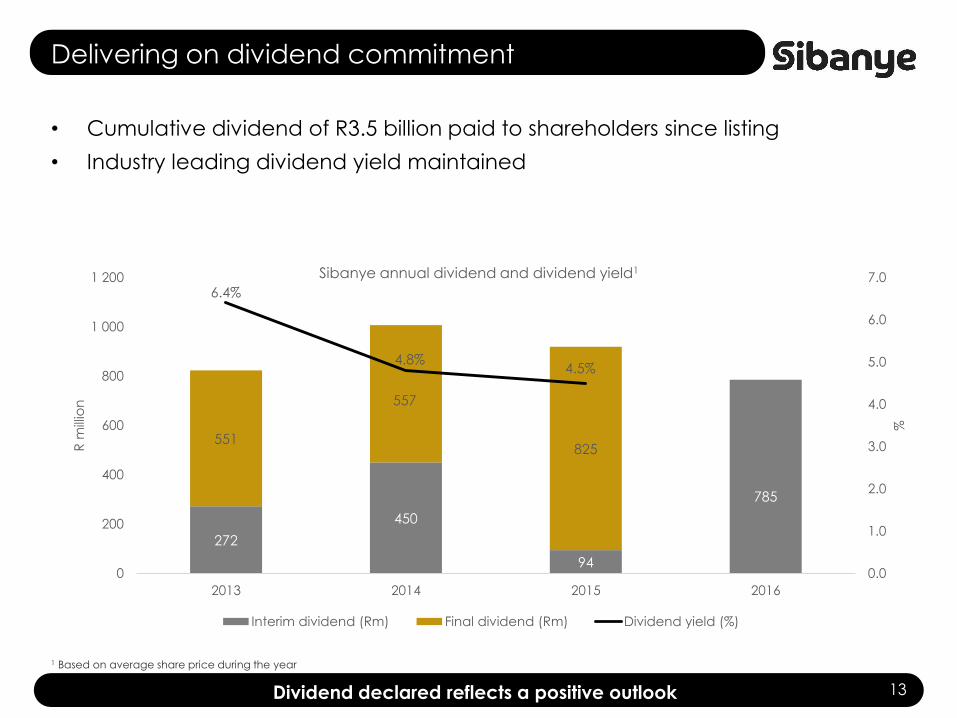

Delivering on dividend commitment

• Cumulative dividend of R3.5 billion paid to shareholders since listing

• Industry leading dividend yield maintained

Dividend declared reflects a positive outlook

1 Based on average share price during the year

13

272

450

94

785

551

557

825

6.4%

4.8%4.5%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0

200

400

600

800

1 000

1 200

2013 2014 2015 2016

%

R m

illio

n

Sibanye annual dividend and dividend yield1

Interim dividend (Rm) Final dividend (Rm) Dividend yield (%)

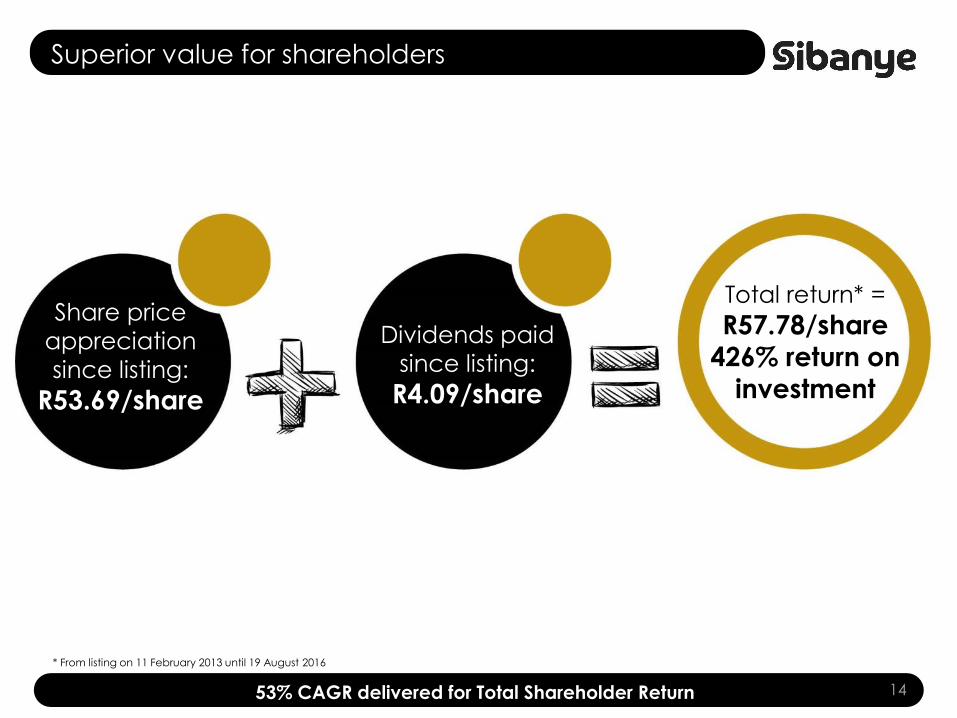

Superior value for shareholders

1453% CAGR delivered for Total Shareholder Return

Share price

appreciation

since listing:

R53.69/share

Dividends paid

since listing:

R4.09/share

Total return* =

R57.78/share

426% return on

investment

* From listing on 11 February 2013 until 19 August 2016

Value creation strategy – a changing landscape

• Sibanye investment case not

commodity specific but primary

focus is still gold and PGMs

• Fewer distressed sellers due to

corporate restructuring, deferral of

capital expenditure and recovery in

metal prices

• Increase in the number of parties

willing to transact

• But… sharp increase in share prices has resulted in less obvious value

opportunities

• Opportunities which offer cost and

operational synergies remain of

interest

15Value accretive acquisitions less prevalent

3 500

5 000

6 500

8 000

9 500

11 000

70

80

90

100

110

120

IMF non-fuel commodity index vs FTSE/JSE

General Mining Index

IMF non-fuel commodity index

FTSE/JSE General Mining index

Index Performance

IMF non-fuel

Commodity

Index

JSE FTSE

General

Mining Index

Since SGL Listing (25%) (39%)

YTD 8% 29%

Sibanye Gold

Division

Operational review

Solid operational performance

• Regression in safety performance a major concern

• Gold Division production of 23 229kg (746 800oz) - 5% higher year-on-year

• Opportunity loss of 1 268kg (40 700oz) as a result of operational disruptions

• Cooke 4 continues to underperform – Section 189 notification issued

• Operations seasonally better in second half – guidance maintained

17

1.50

1.70

1.90

2.10

2.30

2.50

2.70

2.90

3.10

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

Mar-14 June-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

g/tkg

Gold division quarterly production and yield

UG Production Surface Production Yield

Gold Division safety trends

18Good safety performance has recently regressed

0.00

0.10

0.20

0.30

FIFR – peer comparison

Sibanye Peer 1 Peer2

* Rates expressed per million man hours worked

0

5

10

15

20

LDIFR – peer comparison

Sibanye Peer 1 Peer2

11.56

6.76

4.73 5.26 5.796.90

6.13 5.876.74 7.22

0

3

6

9

12

Lost day injury frequency rate*

LDIFR Australian Benchmark

0.24

0.150.18

0.120.14

0.17

0.100.12

0.06

0.13

0.00

0.10

0.20

0.30

Fatal injury frequency rate*

FIFR US Mining Industry

Robust financial results

• Significant increase in operating profit driven by higher gold price and production

– operating profit 125% higher at R5.3bn (US$346m)

• Costs well managed, despite the impact of strike action and safety stoppages

– TCC increased 4% to R381 635/kg – down 17% in US$ terms to US$772/oz

– AISC increased 3% to R448 922/kg – down 20% in US$ terms to US$908/oz

• Organic projects at Kloof, Driefontein and Burnstone approved in 2015 – extend

Divisional LoM and offer significant gold price leverage

19

300 000

340 000

380 000

420 000

460 000

500 000

0

500

1 000

1 500

2 000

2 500

3 000

Mar-14 June-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

R/k

g

Rm

Gold Division operating profit and AISC

Operating profit AISC

Investing in organic growth

• Approval of R3.6 billion for capital growth projects given in mid-2015

• Projects fundamentally robust in lower price environment (meet 15% (real after

tax) hurdle rate at gold price of R450,000/kg)

• Significantly leveraged - at gold price of R600 000/kg NPV is approximately R7

billion with IRRs between 20% and 30%

• Organic projects offer best return with lowest risk

– well known and understood ore bodies and mining conditions

– financed from operational cash flow

– extend lives of existing operations – enhancing ROIC

20Investing in sustainable value

Gold projects

21Low risk, leveraged organic growth

Project metrics

(at R450 000/kg)Unit

Kloof 4 Below

Infrastructure

Driefontein 5

Below

Infrastructure

Burnstone

Project life Year 2015 to 2033 2015 to 2042

to 2038 (23 years

at the 3km

radius)

Project capital cost* Rm 691 1 016 1 852

Gold ounces produced** Moz 0.616 1.861 1.727

IRR (at R450 000/kg) % >15% >15% >15%

IRR (at R600 000/kg) % 21% 27% 34%

NPV (at R600 000/kg)*** Rm 1 170 2 510 3 380

* Costs in 2015 money terms as at time of the feasibility study** Reserves estimated at R450 000/kg *** Using an 8% real discount rate

LoM reserve production profiles

22Extending the operating life through value accretive investment

0

10 000

20 000

30 000

40 000

50 000

60 000

kg

Pre-feasibilities studies

undertaken

De Bron

Beisa

Pending capital approval

WRTRP

Projects in development

Burnstone

Below infrastructure projects

Kloof

Driefontein

Surface reserves in LoM

Kloof

Driefontein

Cooke

Beatrix

Underground reserves in LoM

Kloof

Driefontein

Cooke

Beatrix

Note: Project profile is based on pre-feasibility and feasibility studies as at December 2015

Based on Reserves declared as at 31 December 2015

Assumptions: Gold price: R430 000/kg, Uranium R1,455/lb (real 2015 terms)

Gold Fields plan

31 000kg (1Moz)

F2016 outlook*

23A very solid outlook

• Gold production forecast: approximately 50 000 kg (1.6Moz)

• Forecast Total cash cost: approximately R355 000/kg (US$760/oz)

• Forecast All-in sustaining cost: approximately R425 000/kg (US$910/oz)

• Forecast capital expenditure: approximately R3.9 billion (US$270 million)

* Assuming average of R14:50/US$ for F2016

Sibanye Platinum

Division

Operational review

Safety performance - our key focus

Safety a priority – trends remain positive 25

12-month

LTIFR

3-month

LTIFR

Actual Target Actual Target

Kroondal 2.57 3.00 2.55 3.00

Mimosa 1.36 0.00 0.92 0.00

Platinum Mile 0.00 0.00 0.00 0.00

0.04 0.04 0.04 0.03

0.50

0.00 0.00 0.00 0.00 0.00 0.0

0.1

0.2

0.3

0.4

0.5

0.6

Sibanye Pt − FIFR

1.82 2.00

1.61 1.64

1.99

1.18

2.29

1.14

1.58

0.40

0.0

0.5

1.0

1.5

2.0

2.5

Sibanye Pt − SIFR

4.71

3.64

2.39 2.06

3.48

2.37 2.67

2.28 1.97 2.00

0.0

1.0

2.0

3.0

4.0

5.0

Sibanye Pt − LDIFR

Good operationally but prices have the final say

• A good safety performance delivered for the June 2016 quarter

• Excellent quarterly production of 92,773oz (4E) and good unit cost control from Kroondal and Mimosa

• Prevailing PGM prices remain low, squeezing margins

– poor supply discipline has amplified price pressure

– recent rand strength a further headwind

• Difficult decisions required as depletion of the resource without returns is not sustainable

26

• Section 11 approval for Rustenburg acquisition anticipated during 4Q16

• Kroondal not involved in upcoming platinum sector wage negotiations

• Rustenburg conventional shafts performance of significant concern – engaging with Anglo

• Despite synergies expected from consolidation of the Rustenburg region, tough decisions for the benefit of all stakeholders may still be required

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

180 000

200 000

Ma

r-20

12

Ju

n-2

012

Se

p-2

01

2

De

c-2

01

2

Ma

r-20

13

Ju

n-2

013

Se

p-2

01

3

De

c-2

01

3

Ma

r-20

14

Ju

n-2

014

Se

p-2

01

4

De

c-2

01

4

Ma

r-20

15

Ju

n-2

015

Se

p-2

01

5

De

c-2

01

5

Ma

r-20

16

Ju

n-2

016

Quarterly 4E ounce production

Kroondal Mimosa

Kroondal: record production offsets unit cost inflation

• Kroondal delivered consistently high production of 60,707oz (4E attributable) despite the impact of unprotected strike action and S54 work stoppages:

– 6% CAGR in 4E PGM production since 2011

– despite mining cost inflation, real unit cost increases have been negated (R9,661/oz (4E) for the quarter)

• Controlling unit cost inflation by increasing throughput has limited scope

• At current prices (post purchase of concentrate (PoC) agreement), Kroondal is marginal

– combining the Kroondal and Rustenburg operations and Sibanye group will deliver significant long term, sustainable cost and operational benefits. In the near term however, operational intervention may be required

Combining Kroondal with Rustenburg to deliver further improvements 27

6 000

7 000

8 000

9 000

10 000

11 000

12 000

13 000

14 000

60 000

70 000

80 000

90 000

100 000

110 000

120 000

130 000

R/4

E o

z

PG

M o

z(4

E)

PGM (4E) Ounces PGM basket price (at 100%) Opex + capital

Note: Revenue pre-PoC

Kroondal: pressure remains on production and costs

• Significant business interruptions experienced

and expected to continue:

– regulatory stoppages

• S54 notices have resulted in estimated revenue loss of R135m for 12 months to June 2016

– community-led protests

• 39 community led protests over the last 52-weeks, with at least 30 being non-mine related

– industrial action

• recent unprotected AMCU strike

resulted in estimated revenue losses

of R56m

External issues are a significant impediment to sustainability 28

135

56

8

Revenue losses due to external factors (Rm)

Section 54s

Unprotected labour action

Community disruptions

• Basket cost inflation above Consumer Price Index (CPI)

– utility tariff escalation substantially in excess of CPI

– wage inflation higher than CPI

• The actions of key stakeholders, who currently benefit from the North West PGM

mines, threaten the sustainability of the mines

• Kroondal’s position is by no means unique in the industry

Mimosa: notable performance despite headwinds

• Mimosa production of 29,491oz (4E attributable), was well above nameplate capacity

– and has been consistently so in a very complex environment – a remarkable achievement

• Consistent quarterly production increases resulted in a c.3% reduction in annual real cash costs and a c.14% reduction in real US$ costs over last 3 years. Mimosa reported a cash

operating cost of US$766/oz (4E) for the quarter

• Progress is being made to expand production by 25% in a capital efficient manner, with a focus on reducing the required spend to well below existing estimates and reduce unit costs so as to deliver a robust IRR

• Base metal revenue adds approx. 22% to PGM revenue reported below

A solid operation with growth potential 29

* Excludes base metal revenue

0

200

400

600

800

1 000

1 200

1 400

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

US$

/4E o

z

PG

M o

z(4

E)

PGM (4E) Ounces PGM basket price (at 100%)* Opex + capital

F2016 outlook*

• PGM production forecast: approximately 260 000oz (4E)

• Average cash operating cost of R10 600/oz (US$735/oz)

• Forecast capital expenditure: approximately R225 million (US$15 million)

• Continued integration of acquired platinum assets - low PGM prices and

operational disruptions a near term challenge

• Rustenburg acquisition on track for completion in Dec 2016 quarter

– completion of Rustenburg transaction will enable realisation of main synergies

30

*For the 9 months ended 31 December 2016 (attributable)Assuming average of R14:50/US$ for F2016

Financial

Review

31

Reconciliation of earnings

32Different earnings measures impacted by various extra-ordinary items

333

1 114

38

2 152

338

38

(819)

(1 177)

(153)

(85)

0

500

1 000

1 500

2 000

2 500

3 000

Profit

attributable

to owners

Gain on

disposal of

PPE, net of

tax

Impairment Headline

earnings

Loss on

financial

instruments

Gain on

foreign

exchange

Restructuring

and

transaction

costs

Share of

results of

associates,

after tax

Other and

tax effect

Normalised

earnings

Six months ended 30 June 2016

Rand million US$ million

Net operating profit 3 447.5 224.2

(Loss)/gain on financial instruments

(1 177.0) (76.5)

Net other costs (493.0) (32.0)

Profit before non-recurring items

1 777.5 115.7

Impairment (819.1) (53.3)

Other non-recurringitems

(99.4) (6.4)

Profit before royalties and taxation

859.0 56.0

Income statement

33Share scheme benefited from significant share price appreciation

Six months ended 30 June 2016

Rand million US$ million

Net operating profit 3 447.5 224.2

(Loss)/gain on financial instruments

(1 177.0) (76.5)

Net other costs (493.0) (32.0)

Profit before non-recurring items

1 777.5 115.7

Impairment (819.1) (53.3)

Other non-recurringitems

(99.4) (6.4)

Profit before royalties and taxation

859.0 56.0

Cash-settled share options

• SGL Phantom Share Scheme replaced the Gold Fields equity-settled share plans

• Cash-settled share options are valued at the end of each reporting period

• Significant increase in the fair value of the share-based payment obligation mainly due to the significant increase in Sibanye’s share price.

• Share price increased by approximately 120% during the 2016 interim period (over 500% from issue in May 2013 to end June 2016).

• Approximately 70% of Share Scheme rights vested during the period - R1,490 million (US$97 million) in cash payments.

• Outstanding liability at 30 June 2016 – R346m. Maximum remaining liability = R745 million

Impairment

• Despite joint efforts of stakeholders, the Cooke 4 Operation has been unable to meet required production and cost targets, and has continued to

operate at a loss.

• A decision was taken to impair the Cooke 4 Operation’s mining assets by R816.7 million (US53.1million).

-100

0

100

200

300

400

500

600

700

800

2013 2014 2015 2016

%

Sibanye

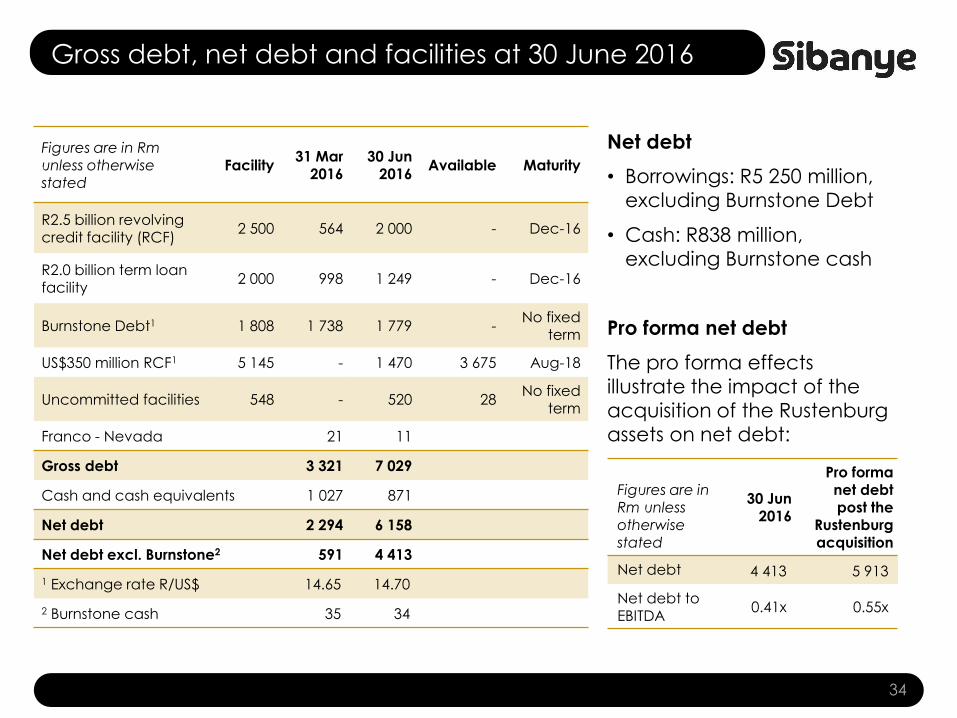

Gross debt, net debt and facilities at 30 June 2016

Figures are in Rm unless otherwise stated

Facility31 Mar

201630 Jun

2016Available Maturity

R2.5 billion revolving credit facility (RCF)

2 500 564 2 000 - Dec-16

R2.0 billion term loan

facility 2 000 998 1 249 - Dec-16

Burnstone Debt1 1 808 1 738 1 779 -No fixed

term

US$350 million RCF1 5 145 - 1 470 3 675 Aug-18

Uncommitted facilities 548 - 520 28No fixed

term

Franco - Nevada 21 11

Gross debt 3 321 7 029

Cash and cash equivalents 1 027 871

Net debt 2 294 6 158

Net debt excl. Burnstone2 591 4 413

1 Exchange rate R/US$ 14.65 14.70

2 Burnstone cash 35 34

34

Figures are in Rm unless otherwise stated

30 Jun 2016

Pro forma net debt post the

Rustenburg acquisition

Net debt 4 413 5 913

Net debt to EBITDA

0.41x 0.55x

Net debt

• Borrowings: R5 250 million,

excluding Burnstone Debt

• Cash: R838 million,

excluding Burnstone cash

Pro forma net debt

The pro forma effects

illustrate the impact of the

acquisition of the Rustenburg

assets on net debt:

Conclusion

Conclusion

• Operational performance solid – regression in safety performance impacting

production and being addressed

• Commitment to industry leading dividend demonstrated again

• Cost management and capital discipline critical during periods of high margin

– intensify cost management

– no cross subsidisation of loss making production – supply discipline

• Value accretive M&A opportunities less prevalent

• Integration of platinum division – low PGM prices and operational disruptions a

near term challenge

– completion of Rustenburg transaction will enable realisation of main

synergies

36Addressing operational challenges – outlook positive

Questions

37