Embed Size (px)

Citation preview

Open Water: A Path to Success for Incumbents and New PlayersTo succeed in the newly deregulated England market, water utilities need to upgrade their IT systems to improve the customer experience, develop differentiated offerings and enable competitive pricing.

Executive Summary The England water industry is set for deregu-lation in the downstream value chain starting April 2017 for all non-household customers. The changes stipulated by the UK Open Water program1 present both challenges and oppor-tunities for market participants. Regulatory agencies set the ball rolling with the publication of the “Water for Life” whitepaper in December 2011.2 Since then, a considerable amount of work has been done to develop the MAP4 (post-ven-dor MAP) market architecture plan.3

However, a recent independent review4 reveals further work is needed to open the market as planned. Additionally, market participants must be ready with their systems and processes before the go-live date of October 2016 for com-mencement of the pilot period.

In this white paper, we analyse similar market deregulation implementations in the UK, such as the Scottish open water market, and electric-

ity and gas deregulation. Based on our findings, we make recommendations for water utilities to succeed in a deregulated industry by taking a holistic approach.

Open Water: An Introduction Competition is not new to the UK water market. Two arrangements are currently available to non-household customers: “supplying for large users” and “supplying in a defined area.” For large water use (five million liters per year in England and 50 million liters per year in Wales), customers can choose their water supply services from over a dozen service providers.

With the defined-area arrangement, providers can deliver water and sewerage services or water-only services for a particular geography in which an existing appointed water company already operates. Roughly 14 companies are registered for this setup. Despite these options, only one large-use customer has switched from its existing supplier to date.

cognizant 20-20 insights | june 2016

• Cognizant 20-20 Insights

Other global deregulated markets have introduced innovative approaches to managing resources efficiently and delivering benefits to customers, including reduced bills, better services and a range of tariff options. For example, Scottish Water claims to have saved more than £72.6 million in water charges, more than £54 million in water efficiency, more than 24 billion liters of water volume and over 42,000 tonnes in CO

2 emissions.5

The intent of the Open Water program in England and Wales was to enable competition in the retail segment to supply water and waste-water management services to non-house-hold customers. In England, all non-household customers will be able to choose their suppliers, while in Wales, non-household customers who use more than the current 50 million liter-per-year cap will have supplier choice as per the existing arrangement.

After deregulation, the market will be separated into upstream and downstream segments (see Figure 1). Existing utilities – which will be known as wholesalers – will provide upstream services,

while both existing and new retailers will provide downstream services. The retail function of existing utilities will need to demonstrate an arm’s length relationship with the wholesale services side.

In addition to wholesalers and retailers, another participant in the deregulated scenario will be market operators (see Figure 2). Market operators will provide the operational capability needed to support the market, such as delivering IT systems that enable registration, customer switching and settlement between wholesalers and retailers.

Ofwat, the organisation responsible for economic regulation of the water sector in England and Wales, will continue to play an important role in market governance and will also be responsible for maintaining regulations, such as the Market Arrangements Code and the Wholesale-Retail Code, as well as providing charging rules, water supply and sewerage licenses, instrument of appointments, eligibility guidance, license appli-cation guidance, the interim supply code, the retail exit code, transition schemes, etc.

Figure 1

Water Value Chains Post Deregulation

Water Extraction Water TreatmentWater

Transmission,Distribution

Water RetailServices

Waste Water Disposal

Waste WaterTreatment

Waste Water Collection,

Transmission

Waste WaterRetail Services

Upstream/Wholesale Downstream/Retail

Non-Household Customers

Water Value Chain Waste-WaterValue Chain

Figure 2

Open Water Market Structure

Non-Household Customers

Wholesaler(Scottish Water)

Central Market Agency (Effective market

operation)

Water Industry Commission for Scotland

(Policy & licensing)

Licensed Suppliers/Retailers

Wholesalers

Non-HouseholdCustomers

Use and charge Information

Operations & service Information

Money

Retailer Retailer

Ofw

at

MarketOperator

Ofw

at

cognizant 20-20 insights 2

cognizant 20-20 insights 3

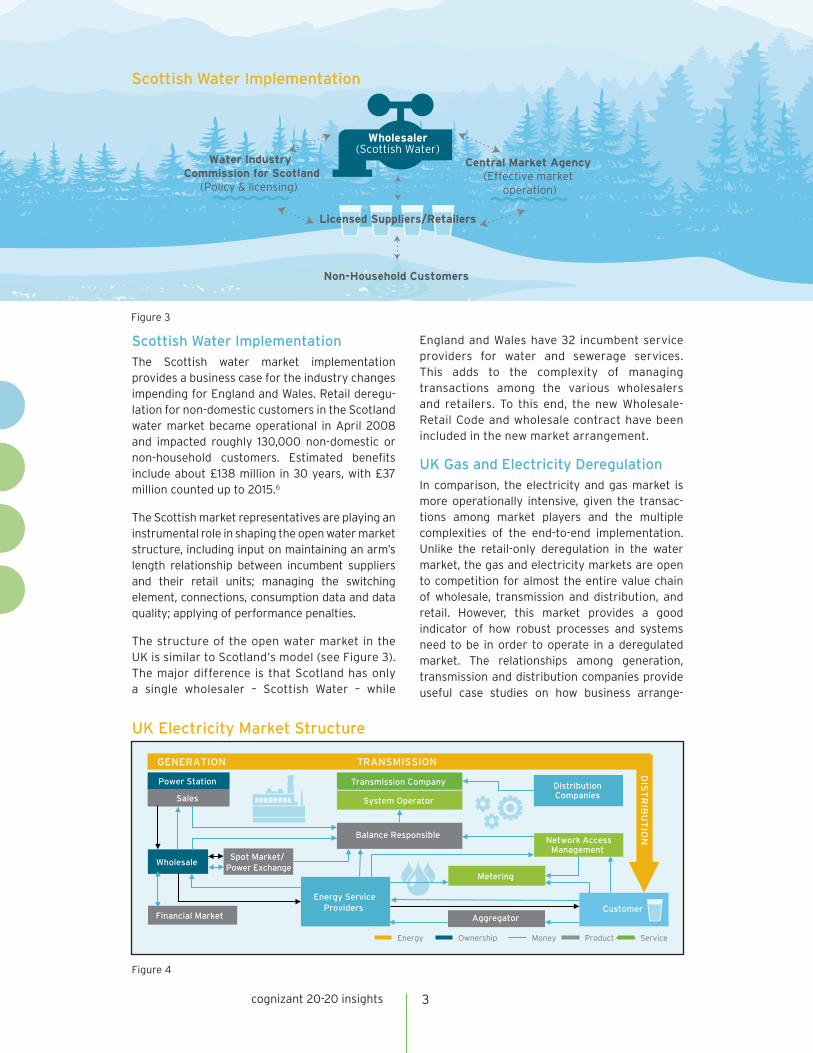

Scottish Water ImplementationThe Scottish water market implementation provides a business case for the industry changes impending for England and Wales. Retail deregu-lation for non-domestic customers in the Scotland water market became operational in April 2008 and impacted roughly 130,000 non-domestic or non-household customers. Estimated benefits include about £138 million in 30 years, with £37 million counted up to 2015.6

The Scottish market representatives are playing an instrumental role in shaping the open water market structure, including input on maintaining an arm’s length relationship between incumbent suppliers and their retail units; managing the switching element, connections, consumption data and data quality; applying of performance penalties.

The structure of the open water market in the UK is similar to Scotland’s model (see Figure 3). The major difference is that Scotland has only a single wholesaler – Scottish Water – while

England and Wales have 32 incumbent service providers for water and sewerage services. This adds to the complexity of managing transactions among the various wholesalers and retailers. To this end, the new Wholesale-Retail Code and wholesale contract have been included in the new market arrangement.

UK Gas and Electricity Deregulation In comparison, the electricity and gas market is more operationally intensive, given the transac-tions among market players and the multiple complexities of the end-to-end implementation. Unlike the retail-only deregulation in the water market, the gas and electricity markets are open to competition for almost the entire value chain of wholesale, transmission and distribution, and retail. However, this market provides a good indicator of how robust processes and systems need to be in order to operate in a deregulated market. The relationships among generation, transmission and distribution companies provide useful case studies on how business arrange-

Figure 3

Scottish Water Implementation

Non-Household Customers

Wholesaler(Scottish Water)

Central Market Agency (Effective market

operation)

Water Industry Commission for Scotland

(Policy & licensing)

Licensed Suppliers/Retailers

Wholesalers

Non-HouseholdCustomers

Use and charge Information

Operations & service Information

Money

Retailer Retailer

Ofw

at

MarketOperator

Ofw

at

Figure 4

UK Electricity Market Structure

DIS

TR

IBU

TIO

N

Power Station

Sales

Wholesale Spot Market/

Power Exchange

Financial Market

Transmission Company

System Operator

Balance Responsible

Energy Service Providers

Distribution Companies

Network Access Management

Metering

Aggregator Customer

GENERATION TRANSMISSION

Energy Ownership Money Product Service

cognizant 20-20 insights 4

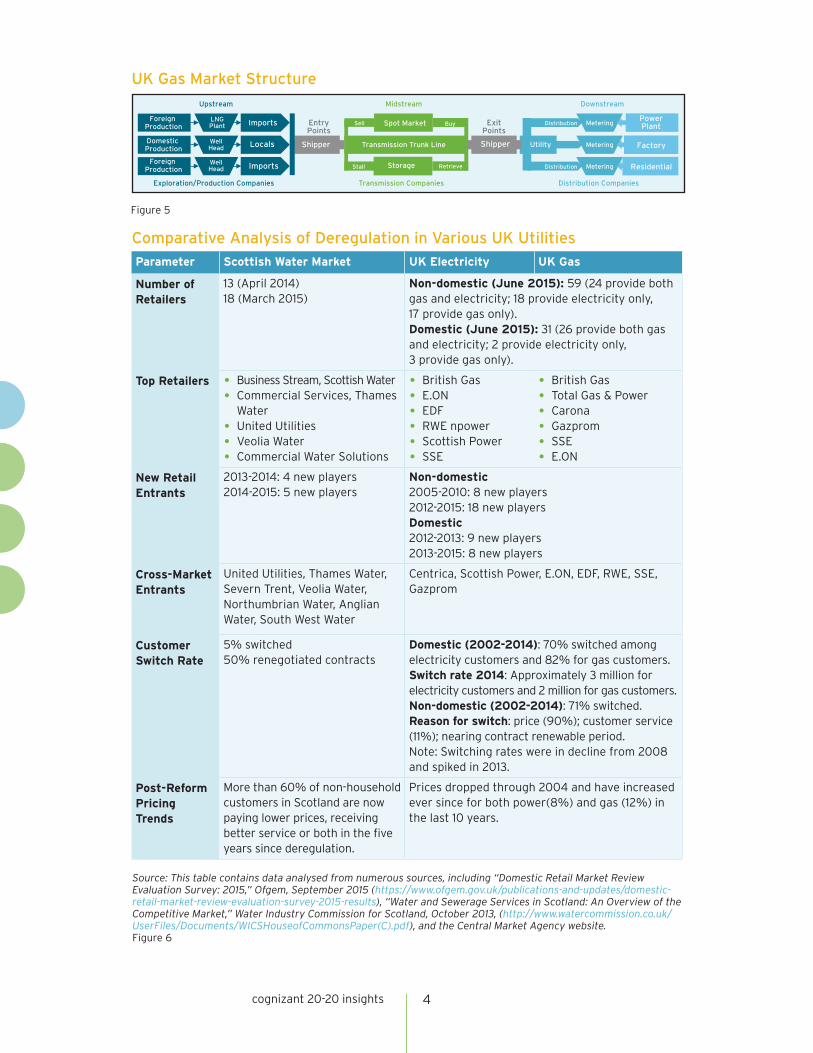

Source: This table contains data analysed from numerous sources, including “Domestic Retail Market Review Evaluation Survey: 2015,” Ofgem, September 2015 (https://www.ofgem.gov.uk/publications-and-updates/domestic-retail-market-review-evaluation-survey-2015-results), “Water and Sewerage Services in Scotland: An Overview of the Competitive Market,” Water Industry Commission for Scotland, October 2013, (http://www.watercommission.co.uk/UserFiles/Documents/WICSHouseofCommonsPaper(C).pdf), and the Central Market Agency website. Figure 6

Comparative Analysis of Deregulation in Various UK Utilities

Parameter Scottish Water Market UK Electricity UK Gas

Number of Retailers

13 (April 2014)18 (March 2015)

Non-domestic (June 2015): 59 (24 provide both gas and electricity; 18 provide electricity only, 17 provide gas only). Domestic (June 2015): 31 (26 provide both gas and electricity; 2 provide electricity only, 3 provide gas only).

Top Retailers • Business Stream, Scottish Water

• Commercial Services, Thames Water

• United Utilities

• Veolia Water

• Commercial Water Solutions

• British Gas

• E.ON

• EDF

• RWE npower

• Scottish Power

• SSE

• British Gas

• Total Gas & Power

• Carona

• Gazprom

• SSE

• E.ON

New Retail Entrants

2013-2014: 4 new players 2014-2015: 5 new players

Non-domestic2005-2010: 8 new players 2012-2015: 18 new players Domestic2012-2013: 9 new players 2013-2015: 8 new players

Cross-Market Entrants

United Utilities, Thames Water, Severn Trent, Veolia Water, Northumbrian Water, Anglian Water, South West Water

Centrica, Scottish Power, E.ON, EDF, RWE, SSE, Gazprom

Customer Switch Rate

5% switched 50% renegotiated contracts

Domestic (2002-2014): 70% switched among electricity customers and 82% for gas customers. Switch rate 2014: Approximately 3 million for electricity customers and 2 million for gas customers.Non-domestic (2002-2014): 71% switched.Reason for switch: price (90%); customer service (11%); nearing contract renewable period.Note: Switching rates were in decline from 2008 and spiked in 2013.

Post-Reform Pricing Trends

More than 60% of non-household customers in Scotland are now paying lower prices, receiving better service or both in the five years since deregulation.

Prices dropped through 2004 and have increased ever since for both power(8%) and gas (12%) in the last 10 years.

Figure 5

UK Gas Market Structure

Foreign Production

Foreign Production

Domestic Production

Imports

Locals

Imports

Shipper Transmission Trunk Line

Spot Market

Storage

Sell Buy

Stall Retrieve

Shipper

EntryPoints

ExitPoints

Utility

Distribution

Distribution

PowerPlant

Factory

Residential

Exploration/Production Companies Transmission Companies Distribution Companies

Upstream Midstream Downstream

LNGPlant

WellHead

WellHead

Metering

Metering

Metering

cognizant 20-20 insights 5

ments should be managed between wholesalers

and retailers.

• Electricity market: Unlike the big-bang approach used for the gas market, deregula-tion for the UK electricity market was phased in, beginning with large customers in 1990, and followed by medium-use custo mer in 1994 and all customers by 1998 (see Figure 4, page 3).

• The gas market: The UK gas market was deregulated in 1996 for all domestic and non-domestic customers, impacting roughly 874,000 non-domestic customers (see Figure 5, previous page).

Lessons Learned from Deregulation By analysing deregulation activity in related markets (see Figure 6, previous page), we can conclude that many retailers in the UK water market will encounter new market arrangements, including incumbent service providers, Scottish market retailers and perhaps a few cross-market players, such as electricity and gas providers that could sell packaged utility offerings of electricity, gas and water services. Almost all the retailers from the Scottish market have indicated interest in the England and Wales market. Though there is no clarity yet on which geographies the new retailers will target, incumbent players from England who are currently part of the Scottish market will have an upper hand given their experience in both geographies.

Retain and Win Customers with Differentiated Offerings

We estimate that customer switch rates under the new market arrangement will not be as high as what was witnessed in the electricity and gas markets, but would be similar to or higher than that in the Scottish market (almost 5% switched retailers and 50% renegotiated their contracts).

A survey by Consumer Council for Water (CCW), which included participants from non-household/non-domestic customer segments, shows that low-spend customers might switch suppliers if offered a better price; high-spend customers would also do so if offered better value for the money.7 New retailers, therefore, should offer not only competitive pricing but also differentiated service offerings.

Market it Right

In other markets, such as in Scotland, many customers were unaware of the new market

arrangement, and confusion persisted following deregulation.8 Although communicating the new market arrangement is considered the responsi-bility of regulatory bodies and the government, utilities can engage in proactive and multi-chan-nel marketing to build customer confidence and gain business.

New retailers should showcase their capabili-ties and reliability as a service provider to win customers, and offer them a quick, streamlined and hassle-free switching process. The CCW survey, however, emphasised the ineffective-ness of hard-sell marketing and the need to make a positive first impression on customers, as more than half said they would return to their incumbent supplier if service levels were not as they expected.

The importance of marketing is also underlined by research conducted by Social Market Research on small and medium-size customers in the Scottish water market, which found limited awareness among most respondents about the deregu-lated water market and their ability to switch suppliers. When customers were made aware of the available service offerings, they were willing to explore switching options.

Establish Competitive Pricing

Any new market arrangement implementa-tion is expected to provide monetary benefits, which can take multiple forms, such as efficient operations, lower retail prices for customers, investments, innovation, etc. The Scottish market study shows more than 60% of non-household customers in Scotland now pay lower prices, receive better service or a combination of the two in the five years since the market opened.9 A similar trend is playing out in the electricity and gas markets following deregulation.

Retailers that have already started setting up and aligning their retail operations with the open water initiative will have an upper hand in planning and setting retail prices. Because Ofwat will determine wholesale pricing rules, there will be little room for negotiation to increase the retail margin. As a result, each retailer must study its own customer base and service offerings and develop suitable pricing. To do this, utilities need to gain in-depth knowledge of customers so they can customise pricing and service offerings.

For further optimisation, the operational utilities across markets can partner to carry out joint

cognizant 20-20 insights 6

operations. A good example is Water2busi-ness, a joint venture between Bristol Water and Wessex Water, which will provide retail services to businesses across the UK.

Ensure Regulatory Compliance

Market participants will need to work within the regulatory framework defined in the new market structure. As mentioned above, incumbent retailers will need to maintain an arm’s length relationship with their wholesale businesses to ensure fair competition. This means setting up completely new facilities, teams, operations, processes, IT systems, etc. Scottish Water, for example, separated its retail business by setting up a new company, Business Stream, in 2006.

In Scotland, all retailers use standard forms, processed via central e-mail systems, which ensures incumbent retailers’ transactions are processed in the same way as any other retailer’s. Utilities such as United Utilities, Thames Commercial Services, Severn Trent Services, etc. have already set up separate business units.

Other regulations, such as those related to the wholesale contract, Wholesale-Retail Code and Market Arrangements Code of the new market arrangement and their ownership, are still being finalised as per the Market Architecture Plan (MAP). In addition, all market participants will need to conduct operational and regulatory reporting.

Looking Ahead: A Plan for SuccessProviders’ operational and customer service processes will be challenged by the new com-petitive market scenario. Retailers can follow a four-step process to ensure they can win and

retain customers in the deregulated landscape (see Figure 7).

• Strategise: Based on its capabilities, each retailer should define its business strategy and develop a plan as to which geographies or customers to target and which bottom lines to maintain. Because non-household customers’ requirements vary according to their operations, providers need to conduct customer profiling and segmentation to understand their needs and map their capabili-ties accordingly. Capability gaps should be filled through a mergers and acquisitions strategy or through partnerships with trusted third-parties and other utilities.

• Invest: The business strategy will determine investments to be made in people, processes and technology. Robust IT systems and processes, as well as skilled talent, will be key to smooth operations. Many utilities have already begun investing heavily to improve their various lines of business. Wholesalers will need to align their existing processes and systems with the new market scenario.

Defining new processes, such as customer onboarding, billing, switching, managing breakdowns, etc., will require investment. The systems impacted most heavily will be the customer information system (CIS), work management and contract management systems. Retailers and the market operator will need to set up all systems and processes for CIS, sales and marketing, regulatory compliance, wholesaler management, vendor management, etc. Both wholesalers and retailers will need to establish a strong communication system to

Figure 7

Open Water Approach

• Systems • Processes• Operations

OPERATE & MONITOR

• Target market areas• Customer profiling

and segmentation• Service offerings• Mergers and

acquisitions • Vendor/utility

tie-ups, partnerships

STRATEGISE

• Market• Bottom lines

INVEST

• Customer services• Sales planning• Marketing planning• Support functions • Operations planning• IT planning• Regulatory planning

PLAN

• Systems • Operations• Administration

• People• Process• Technology

• Skilled human resources

• Streamlined process• IT systems• Offices and

infrastructure

• Account management

• Customer service • Communications

management• Billing and payments• Work management

cognizant 20-20 insights 7

interact with each other and with the market operator.

Market operator systems and processes are defined in the Open Water market codes. Retailers and wholesalers will need to work closely with the market operator to understand how access and communications will work. Another major investment for retailers is related to office space and infrastructure. The decision to establish a single location or multiple ones will depend on the company’s operational model.

• Plan: Once the systems and processes are in place, utilities should plan how their systems, operations and administration will work to meet their targets. These include customer service activities, customer queries, mainte-nance work, etc. Operations planning will be required for account management and related

daily operations, as well as support functions, such as human resources, finance, administra-tion, legal, regulatory, etc. As most systems and processes will be IT-intensive, substantial IT planning will be necessary.

• Operate and monitor: Once the market goes live or utilities are in operation, emphasis needs to be placed on running operations as planned, along with a strong monitoring framework to track operations against the plan. The most critical systems and processes will be those with direct customer touchpoints, such as websites, telephony, customer service, CIS, sales and marketing. Back-end systems and processes, such as account management, communica-tions management, billing and payments, work management, etc., should enable the front-end systems mentioned above.

Footnotes1 “Open Water,” UK Government, http://www.open-water.org.uk/.

2 “Water for Life,” Department for Environment Food and Rural Affairs, December 2011, https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/228861/8230.pdf.

3 “Post Vendor MAP” Open Water, September 2015, http://www.open-water.org.uk/download-documents/?cat=post-vendor-map.

4 “Retail Market Opening Programme Review,” UK Government, May 28, 2015, http://www.ofwat.gov.uk/wp-content/uploads/2015/11/rpt_com201506baselinereview.pdf.

5 Business Stream website, http://www.business-stream.co.uk/about-us/what-we-do.

6 “Water and Sewerage Services in Scotland: An Overview of the Competitive Market,” Water Industry Commission for Scotland, October 2013, http://www.watercommission.co.uk/UserFiles/Documents/WICSHouseofCommonsPaper(C).pdf.

7 “Uncharted Waters: Non-Household Customers’ Expectations for Competition in the Water Industry,” Consumer Council for Water, March 2014, http://www.ccwater.org.uk/blog/2014/06/19/uncharted-waters-non-household-customers-expectations-for-competition-in-the-water-industry/.

8 “Navigating Unfamiliar Waters: SMEs’ Awareness and Experience of the Water Market in Scotland,” Social Market Research, March 2013.

9 “Water and Sewerage Services in Scotland: An Overview of the Competitive Market,” Water Industry Commission for Scotland, October 2013, http://www.watercommission.co.uk/UserFiles/Documents/WICSHouseofCommonsPaper(C).pdf.

cognizant 20-20 insights 8

References

• “Market Blueprint,” Open Water, January 2014, http://www.open-water.org.uk/media/1041/market-blueprint.pdf.

• Jochen Kreusel, “Entering a New Epoch,” Transmission & Distribution World, April 1, 2015, http://tdworld.com/sponsored-articles/entering-new-epoch.

• “Central Market Agency: Business Review, 2014-2015,” Central Market Agency, 2015, http://www.cmascotland.co.uk/kcfinder/upload/files/Business%20Review/CMA%20Business%20Review-2014-15(1).pdf.

• “Retail Energy Markets in 2015,” Ofgem, September 2015, https://www.ofgem.gov.uk/publications-and-updates/retail-energy-markets-2015.

• “Market Operator Target Operating Model,” OpenWater, January 2014, http://www.open-water.org.uk/media/1042/market-operator-target-operating-model.pdf.

• “Water and Sewerage Retail Competition in Scotland,” Water Industry Commission for Scotland, February 2012, http://www.watercommission.co.uk/UserFiles/Documents/Water%20and%20sewerage%20competition%20in%20Scotland.pdf.

• “Comments from Scottish Water on Open Water Market Architecture Plan,” Scottish Water, July 2014, http://www.open-water.org.uk/media/1253/140814-comments-from-scottish-water-on-open-water-market-architecture-plan-final.pdf.

• “Wholesale and Retail Charges: A Consultation,” Ofwat, January 2014, http://www.ofwat.gov.uk/con-sultation/wholesale-and-retail-charges-a-consultation/.

• “Consultation on Wholesale and Retail Charges for 2015-16 and Charges Scheme Rules,” Ofwat, May 2014, http://www.ofwat.gov.uk/wp-content/uploads/2015/10/pap_con20140530charges.pdf.

• “Draft Determination Representation: Annex RNHH02--Additional Costs of Market Opening,” Thames Water, October 2014, http://www.thameswater.co.uk/ofwat/Appendices/Appendix%20E/RNHH02.pdf.

• “Ofwat’s Review of Competition in the Water and Sewerage Industries: Part II,” Ofwat, May 2008, http://s3-eu-west-1.amazonaws.com/media.aws.stwater.co.uk/upload/pdf/Competition_consultation_part_II.pdf.

• “Default Tariffs in the Contestable Retail Market for Water and Sewerage Services: The Design and Implementation Issues,” Economic Insight Ltd., August 2012, https://www.thameswater.co.uk/your-business/business-regulatory-safeguards-in-deregulated-markets.pdf.

• Ruud Weijermars, “Value Chain Analysis of the Natural Gas Industry,” Journal of Natural Gas Science and Engineering, Vol. 2, May 2010, http://www.alboran.com/files/2013/07/ES-3.pdf.

• “Domestic Retail Market Report,” Ofgem, June 2007, https://www.ofgem.gov.uk/ofgem-publica-tions/38491/drmr-march-2007doc-v9-final.pdf.

About Cognizant

Cognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process services, dedicated to helping the world’s leading companies build stronger businesses. Head-quartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technol-ogy innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 100 development and delivery centers worldwide and approxi-mately 233,000 employees as of March 31, 2016, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world. Visit us online at www.cognizant.com or follow us on Twitter: Cognizant.

World Headquarters500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233Fax: +1 201 801 0243Toll Free: +1 888 937 3277Email: [email protected]

European Headquarters1 Kingdom StreetPaddington CentralLondon W2 6BDPhone: +44 (0) 20 7297 7600Fax: +44 (0) 20 7121 0102Email: [email protected]

India Operations Headquarters#5/535, Old Mahabalipuram RoadOkkiyam Pettai, ThoraipakkamChennai, 600 096 IndiaPhone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060Email: [email protected]

© Copyright 2016, Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

About the AuthorsAnkit Pande is a Consultant within Cognizant Business Consulting’s Energy and Utilities Practice. He has over five years of experience in the energy & utility and retail domains in the IT services and consulting industry. At Cognizant, Ankit provides consulting and big IT project implementations that include process improve-ments, business analysis and digital transformation. He has strong experience in work management, asset management, customer experience management and operations management in the utilities industry (water, electricity and gas). Ankit holds a PGDISEM from the National Institute of Industrial Engineering (NITIE Mumbai) and a B.TECH in production engineering from the College Of Engineering, Pune. He can be reached at [email protected].

Gaurav Hegishte is a Consultant within Cognizant Business Consulting’s Energy and Utilities Practice. He has over five years of experience in the product and resources industry. At Cognizant, Gaurav provides services to utility clients related to process improvement and digital transformation. He holds a PGDIM in industrial management from the National Institute of Industrial Engineering (NITIE Mumbai). Gaurav can be reached at [email protected].

Puneet Kohli is a Senior Consultant within Cognizant Business Consulting’s Energy and Utilities Practice. He has over eight years of experience in energy and utility consulting, operations and maintenance in the energy industry. At Cognizant, Puneet provides process improvement and digital transformation services to clients. He holds a PGDM from the Indian School of Business. Puneet can be reached at [email protected].

Codex 1930

![Strategic Path Planning on the Basis of Risk vs. TimePath planning and collision prevention for single and multiple players has been exten-sively studied [2]. But strategic path planning](https://img.pdfslide.us/doc/110x75/5fb1cb68d2f3055f491276a7/strategic-path-planning-on-the-basis-of-risk-vs-time-path-planning-and-collision.jpg)