Embed Size (px)

Citation preview

Part III

Open MacroeconomicSystems of Debt Money

301

Chapter 10

Balance of Payments andForeign Exchange

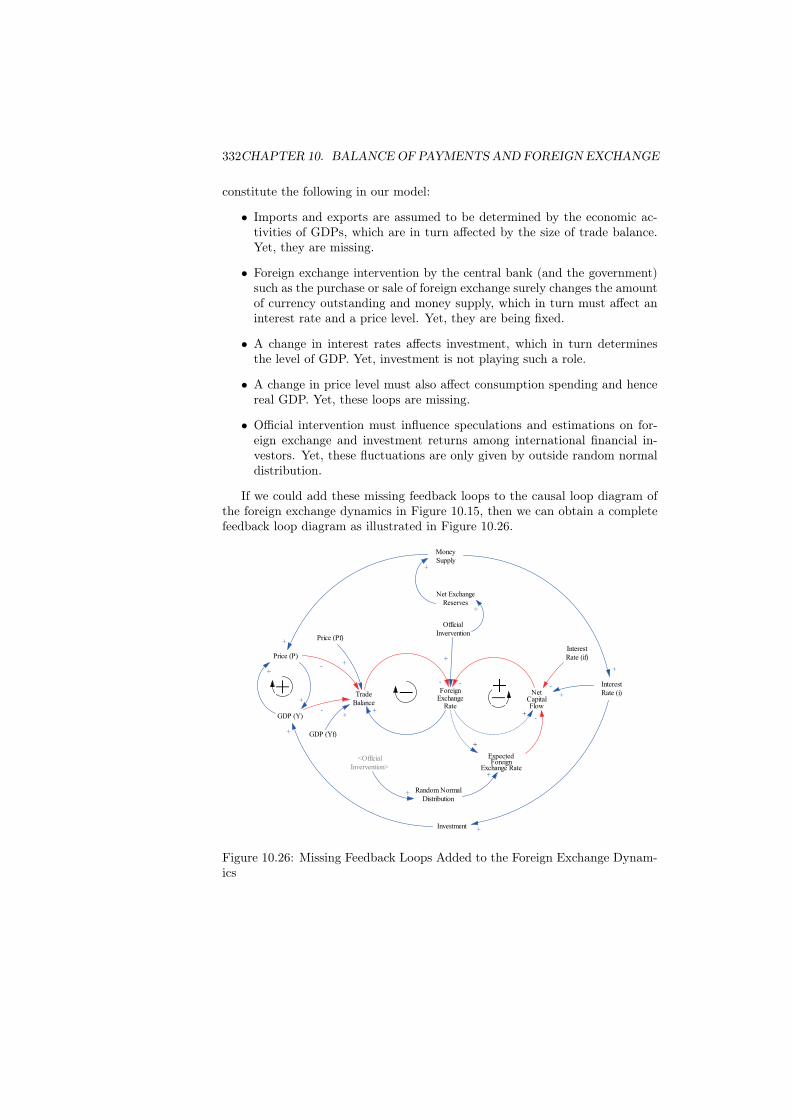

This chapter1 explores a dynamic determination process of foreign exchangerate in an open macroeconomy in which goods and services are freely traded andfinancial capital flows efficiently for higher returns. For this purpose it becomesnecessary to employ a new method contrary to a standard method of dealingwith a foreign sector as adjunct to macroeconomy; that is, an introduction ofanother macroeconomy as a foreign sector. Within this new framework of openmacroeconomy, transactions among domestic and foreign sectors are handledaccording to the principle of accounting system dynamics, and their balance ofpayments is attained. For the sake of simplicity of analyzing foreign exchangedynamics, macro variables such as GDP, its price level and interest rate aretreated as outside parameters. Then, eight scenarios are produced and examinedto see how exchange rate, trade balance and financial investment, etc. respondto such outside parameters. To our surprise, expectations of foreign exchangerate turn out to play a crucial role for destabilizing trade balance and financialinvestment. The impact of official intervention on foreign exchange and a pathto default is also discussed.

10.1 Open Macroeconomy as a Mirror Image

As a natural step of the research, we are now in a position to open our macroe-conomy to a foreign sector so that goods and services are freely traded and fi-nancial assets are efficiently invested for higher returns. The analytical methodemployed here is the same as the previous chapters; that is, the one based onthe principle of accounting system dynamics.

1It is based on the paper: Balance of Payments and Foreign Exchange Dynamics – SDMacroeconomic Modeling (4) – in “Proceedings of the 24th International Conference of theSystem Dynamics Society”, Boston, USA, July 29 - August 2, 2007. (ISBN 978-0-9745329-8-1)

304CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

The method requires to manipulate all transactions among macroeconomicsectors, and when applied to a foreign sector, it turns out to be necessary tointroduce another macroeconomy as a reflective image of domestic macroecon-omy. Contrary to a method employed in standard international economics text-books such as [44] and [47], a foreign sector is no longer treated as an additionalmacroeconomic sector adjunct to a domestic macroeconomy [Companion Model:ForeignExchange.vpm].

To understand this, for instance, consider a transaction of importing goods.They add to the inventory of importers (a red disk numbered 1 in Figure 10.2below), while the same amount is reduced from the inventory of foreign ex-porters (a red disk numbered 4 in Figure 10.3 below). To pay for the importedgoods, importers withdraw their deposits from their bank and purchase foreignexchange, (red disks numbered 2 and 3 in Figures 10.2 and 10.5 below), which isthen sent to the deposit account of foreign exporters’ bank that will notify thereceipts of export payments to exporters (red disks numbered 3 and 4 in Figures10.6 and 10.3 below). In this way, a mirror image of domestic macroeconomyis needed for a foreign country as well to describe even domestic transactionprocesses of goods and services. Similar manipulations are also needed for thetransactions of foreign direct and financial investment. Figure 10.1 expresses ourimage of modeling open macroeconomy by the principle of accounting systemdynamics.

Consumer( Househol d)

Pr oducer ( Fi r m)

Commer ci al Banks

Cent r al Bank

Gover nment

Nat i onalWeal t h

( Capi t alAccumul at i on)

Gr ossDomest i cPr oduct s

( GDP)

Labor & Capi t al

Wages & Di vi dens( I ncome)

Savi ng Loan

I nvest ment( PP&E)

I nvest ment( Housi ng)

I nvest ment( Publ i c

Faci l i t i es)

I ncome Tax Cor por at e Tax

Consumpt i on

Publ i cSer vi ces

Publ i cSer vi ces

Money Suppl y

Expor t

I mpor t

Pr oduct i on For ei gnConsumer

( Househol d)

For ei gnPr oducer

( Fi r m)

For ei gn Commer ci al Banks

For ei gn Cent r al Bank

For ei gn Gover nment

For ei gnNat i onalWeal t h

( Capi t alAccumul at i on)

For ei gnGr oss

Domest i cPr oduct s

( GDP)

For ei gn Labor& Capi t al

For ei gn Wages &Di vi dens ( I ncome)

For ei gnSavi ng

For ei gnLoan

For ei gnI nvest ment

( PP&E)

For ei gnI nvest ment( Housi ng)

For ei gn I nvest ment( Publ i c Faci l i t i es)

For ei gnI ncome Tax

For ei gnCor por at e Tax

For ei gnConsumpt i on

For ei gn Publ i cSer vi ces

For ei gn Publ i cSer vi ces

For ei gnMoneySuppl y

For ei gnPr oduct i on

Di r ect andFi nanci alI nvest ment

For ei gnI nvest ment

For ei gn Sec t or as an I mage of Domes t i c Macr oeconomy

Figure 10.1: Foreign Sector as a Mirror Image of Domestic Macroeconomy

10.2 Open Macroeconomic TransactionsModeling open macroeconomy was hitherto considered to be easily completedby merely adding a foreign sector. The introduction of a foreign country as amirror image of domestic macroeconomy makes our analysis rather complicated.To overcome the complexity, we are forced, in this chapter, to focus only on a

10.2. OPEN MACROECONOMIC TRANSACTIONS 305

mechanism of the transactions of trade and foreign investment in terms of thebalance of payments and dynamics of foreign exchange rate. For this purpose,transactions among five domestic sectors and their counterparts in a foreigncountry are simplified as follows.

Producers

Major transactions of producers are, as illustrated in Figure 10.2, summarizedas follows.

• GDP (Gross Domestic Product) is assumed to be determined outside theeconomy, and grows at a growth rate of 2% annually.

• Producers are allowed to make direct investment abroad as well as finan-cial investment out of their financial assets consisting of stocks, bondsand cash2, and receive investment income from these investment abroad.Meanwhile, they are also required to pay foreign investment income (re-turns) to foreign investors according to their foreign financial liabilitiesand equity.

• Producers now add net investment income (investment income receivedless paid) to their GDP revenues (the added amount is called GNP (GrossNational Product)), and deduct capital depreciation (the remaining amountis called NNP (Net National Product)).

• NNP thus obtained is completely paid out to consumers, consisting ofworkers and shareholders, as wages to workers and dividend to sharehold-ers.

• Producers are thus constantly in a state of cash flow deficits. To makenew investment, therefore, they have to borrow money from banks, butfor simplicity no interest is assumed to be paid to the banks.

• Producers imports goods and services according to their economic activi-ties, the amount of which is assumed to be 10% of GDP in this chapter.

• Similarly, their exports are determined by the economic activities of aforeign country, the amount of which is also assumed to be 10% of foreignGDP.

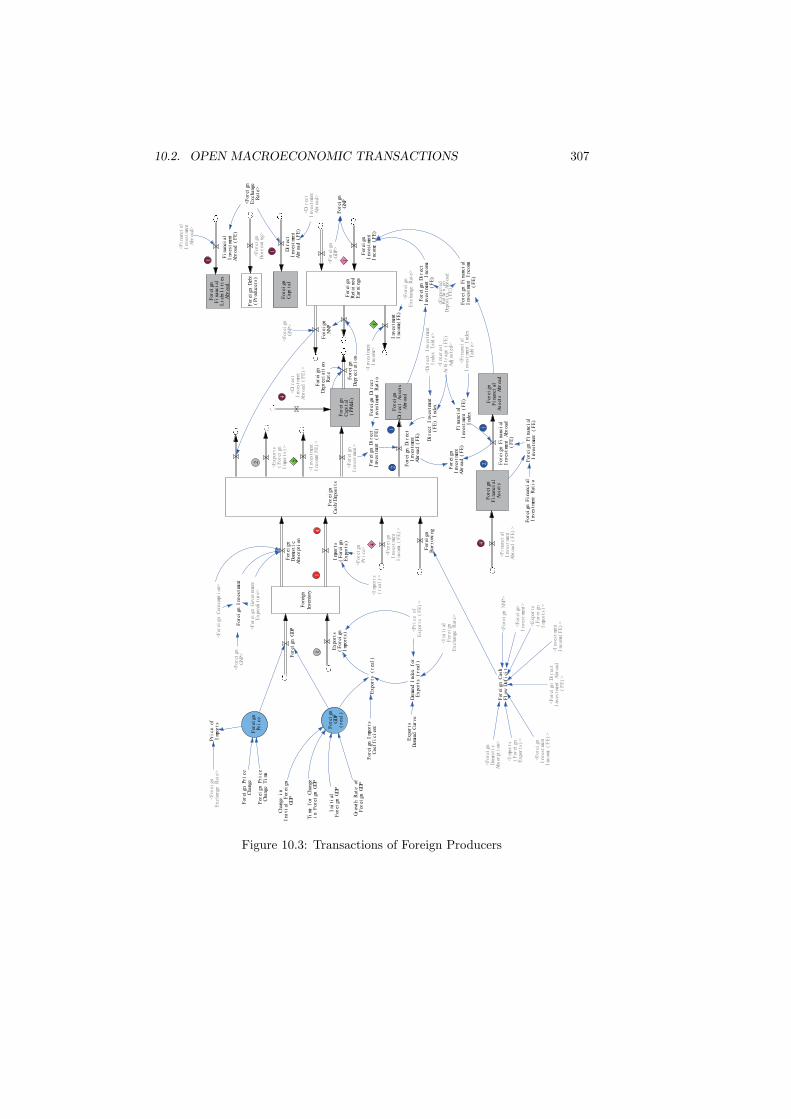

• Foreign producers are assumed to behave similarly as a mirror image ofdomestic producers as illustrated in Figure 10.3.

2In this chapter, financial assets are not broken down in detail and simply treated asfinancial assets. Hence, returns from financial investment are uniformly evaluated in terms ofdeposit returns.

306CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

Inve

ntory

Cas

h/D

epos

its

(P

rod

ucer

s)

1

2

Ex

por

ts

14

Di

rec

t A

sset

sA

broa

dD

ir

ect

Inv

estm

ent

Abr

oad

Di

rec

tI

nves

tmen

t

Fi

nanc

ial

Inv

estm

ent

Imp

orts

<For

eign

Ex

cha

nge

Rat

e>

Imp

orts

(

rea

l)

Pr

ice

ofE

xpo

rts

(

FE

)

<Pr

ice

ofI

mpor

ts>

Dem

and

Ind

exf

or

Imp

orts

Imp

orts

Dem

and

Cur

ve

<For

eign

Di

rec

tI

nves

tmen

tA

broa

d (

FE

)>

Pr

ice

Cha

nge

Pr

ice

Cha

nge

Ti

me

<Ex

por

ts(

rea

l)

>I

mpor

tsC

oef

fi

ci

ent

<Ini

tial

F

orei

gnE

xcha

nge

Rat

e>

Ret

aine

dE

arni

ngs

(P

rod

ucer

)

Inv

estm

ent

Inc

ome

For

eign

Inv

estm

ent

Inc

ome

<Inv

estm

ent

Inc

ome>

<For

eign

Inv

estm

ent

Inc

ome>

<Imp

orts

>

Fi

nanc

ial

Li

abi

li

ties

Abr

oad

12

For

eign

F

ina

nci

alI

nves

tmen

t A

broa

d

1

4

114

1

2

<Ex

pecte

dR

etur

n on

Dep

osi

tsA

broa

d>

GD

P(

rea

l)

Fi

nanc

ial

Asset

sA

broa

dF

ina

nci

alI

nves

tmen

tA

broa

d

<For

eign

Fi

nanc

ial

Inv

estm

ent

Abr

oad

(F

E)

>

Inv

estm

ent

Abr

oad

Fi

nanc

ial

Inv

estm

ent

Inc

ome

Ini

tial

G

DP

Gr

owth

R

ate

of

GD

P

<Int

eres

tA

rbi

trag

eA

djus

ted>

Cha

nge

in

Ini

tial

GD

P

Ti

me

for

Cha

nge

in

GD

P

Di

rec

tI

nves

tmen

tI

ndex

Di

rec

t I

nves

tmen

tI

ndex

T

abl

e

Fi

nanc

ial

Inv

estm

ent

Ind

ex

Fi

nanc

ial

I

nves

tmen

tI

ndex

T

abl

e

GD

P

<GD

P>

NN

P

<For

eign

Ex

cha

nge

Rat

e>

Inv

estm

ent

Dom

esti

cA

bsor

pti

on

<Inv

estm

ent>

Bor

row

ing

<Dom

esti

c

Abs

orpt

ion

>

<Ex

por

ts>

<NN

P>

<Imp

orts

>

<Inv

estm

ent>

Cas

h F

low

Def

ici

t

Cap

ita

l(

PP

&E

)

Deb

t(

Pr

oduc

ers)

<Bor

row

ing

>

<Gov

ernm

ent

Ex

pend

itu

re>

Pr

ice

<Pr

ice>

Fi

nanc

ial

Asset

s<I

nves

tmen

t I

ncom

e><F

orei

gn

Inv

estm

ent

Inc

ome>

<Di

rec

t I

nves

tmen

t A

broa

d>

Di

rec

tI

nves

tmen

tI

ncom

e

21

<For

eign

Inv

estm

ent

Inc

ome

(F

E)

>

Cap

ita

lF

orei

gn

Di

rec

tI

nves

tmen

t A

broa

d

<For

eign

Ex

cha

nge

Rat

e>

<For

eign

D

ir

ect

Inv

estm

ent

Abr

oad>

1

<For

eign

F

ina

nci

alI

nves

tmen

t A

broa

d>

Dep

rec

iat

ion

Dep

rec

iat

ion

Rat

e

Di

rec

tI

nves

tmen

tR

ati

o

Fi

nanc

ial

Inv

estm

ent

Rat

io

<Con

sum

pti

on>

GN

P

<GN

P>

<GN

P>

Figure 10.2: Transactions of Producers

10.2. OPEN MACROECONOMIC TRANSACTIONS 307

Fore

ign

Inve

ntory

For

eign

Cas

h/D

epos

its

14

1

2

For

eign

Di

rec

t A

sset

sA

broa

d

Ex

por

ts

(r

eal

)

For

eign

Pr

ice

For

eign

D

ir

ect

Inv

estm

ent

Abr

oad

(F

E)

Ex

por

ts(

For

eign

Imp

orts

)

Imp

orts

(F

orei

gnE

xpo

rts

)

<Pr

ice

ofE

xpo

rts

(

FE

)>

Dem

and

Ind

ex

for

Ex

por

ts

(r

eal

)

Ex

por

tsD

eman

d C

urv

e

Pr

ice

ofI

mpor

ts

<For

eign

Ex

cha

nge

Rat

e>

For

eign

D

ir

ect

Inv

estm

ent

(F

E)

For

eign

F

ina

nci

alI

nves

tmen

t (

FE

)

For

eign

I

mpor

tsC

oef

fi

ci

ent

<Di

rec

tI

nves

tmen

tA

broa

d>

<Imp

orts

(r

eal

)>

For

eign

Ret

aine

dE

arni

ngs

For

eign

Inv

estm

ent

Inc

ome

(F

E)

Inv

estm

ent

Inc

ome(

FE

)

<Inv

estm

ent

Inc

ome(

FE

)>

<For

eign

Inv

estm

ent

Inc

ome

(F

E)

>

<Ex

por

ts(

For

eign

Imp

orts

)>

<Ini

tial

For

eign

Ex

cha

nge

Rat

e>

For

eign

Fi

nanc

ial

Li

abi

li

ties

Abr

oad

Fi

nanc

ial

Inv

estm

ent

Abr

oad

(F

E)

1

4

12

1

2

1

4

<Ex

pecte

dR

etur

n on

Dep

osi

ts

Abr

oad

(F

E)

>

For

eign

GD

P(

rea

l)

<Fi

nanc

ial

Inv

estm

ent

Abr

oad>

For

eign

Fi

nanc

ial

Asset

s

Abr

oad

For

eign

F

ina

nci

alI

nves

tmen

t A

broa

d(

FE

)

For

eign

Inv

estm

ent

Abr

oad

(F

E)

For

eign

F

ina

nci

alI

nves

tmen

t I

ncom

e(

FE

)

Ini

tial

For

eign

G

DP

Gr

owth

R

ate

ofF

orei

gn

GD

P

<Int

eres

tA

rbi

trag

e (

FE

)A

djus

ted>

Cha

nge

in

Ini

tial

F

orei

gnG

DP

Ti

me

for

C

hang

ei

n F

orei

gn

GD

P

Di

rec

t I

nves

tmen

t(

FE

)

Ind

ex

<Di

rec

t I

nves

tmen

tI

ndex

T

abl

e>

Fi

nanc

ial

Inv

estm

ent

(F

E)

Ind

ex

<Fi

nanc

ial

Inv

estm

ent

Ind

exT

abl

e>

<For

eign

Pr

ice>

For

eign

G

DP

For

eign

Dom

esti

cA

bsor

pti

on

For

eign

I

nves

tmen

t

<For

eign

Ex

cha

nge

Rat

e>

<For

eign

GD

P>

For

eign

NN

P

For

eign

Cap

ita

l(

PP

&E

)

<For

eign

G

over

nmen

tE

xpe

ndi

tur

e>

<For

eign

Inv

estm

ent>

For

eign

C

ash

Fl

ow

Def

ici

t

<For

eign

Dom

esti

cA

bsor

pti

on>

<Imp

orts

(F

orei

gnE

xpo

rts

)>

<For

eign

N

NP

>

<For

eign

Inv

estm

ent>

<Ex

por

ts(

For

eign

Imp

orts

)>

For

eign

Bor

row

ing

For

eign

D

ebt

(P

rod

ucer

s)

<For

eign

Bor

row

ing

>

For

eign

Fi

nanc

ial

Asset

s

<For

eign

Inv

estm

ent

Inc

ome

(F

E)

>

<Inv

estm

ent

Inc

ome(

FE

)>

<For

eign

D

ir

ect

Inv

estm

ent

Abr

oad

(F

E)

>

For

eign

D

ir

ect

Inv

estm

ent

Inc

ome

(F

E)

<Inv

estm

ent

Inc

ome>

For

eign

Cap

ita

lD

ir

ect

Inv

estm

ent

Abr

oad

(F

E)

<Di

rec

tI

nves

tmen

tA

broa

d (

FE

)>

<For

eign

Ex

cha

nge

Rat

e>

<Fi

nanc

ial

Inv

estm

ent

Abr

oad

(F

E)

>

1

41

2

For

eign

Dep

rec

iat

ion

For

eign

Dep

rec

iat

ion

Rat

e

For

eign

D

ir

ect

Inv

estm

ent

Rat

io

For

eign

F

ina

nci

alI

nves

tmen

t R

ati

o

<For

eign

C

onsum

pti

on>

For

eign

GN

P

<For

eign

GN

P>

<For

eign

GN

P>

For

eign

P

ri

ce

Cha

nge

For

eign

P

ri

ce

Cha

nge

Ti

me

Figure 10.3: Transactions of Foreign Producers

308CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

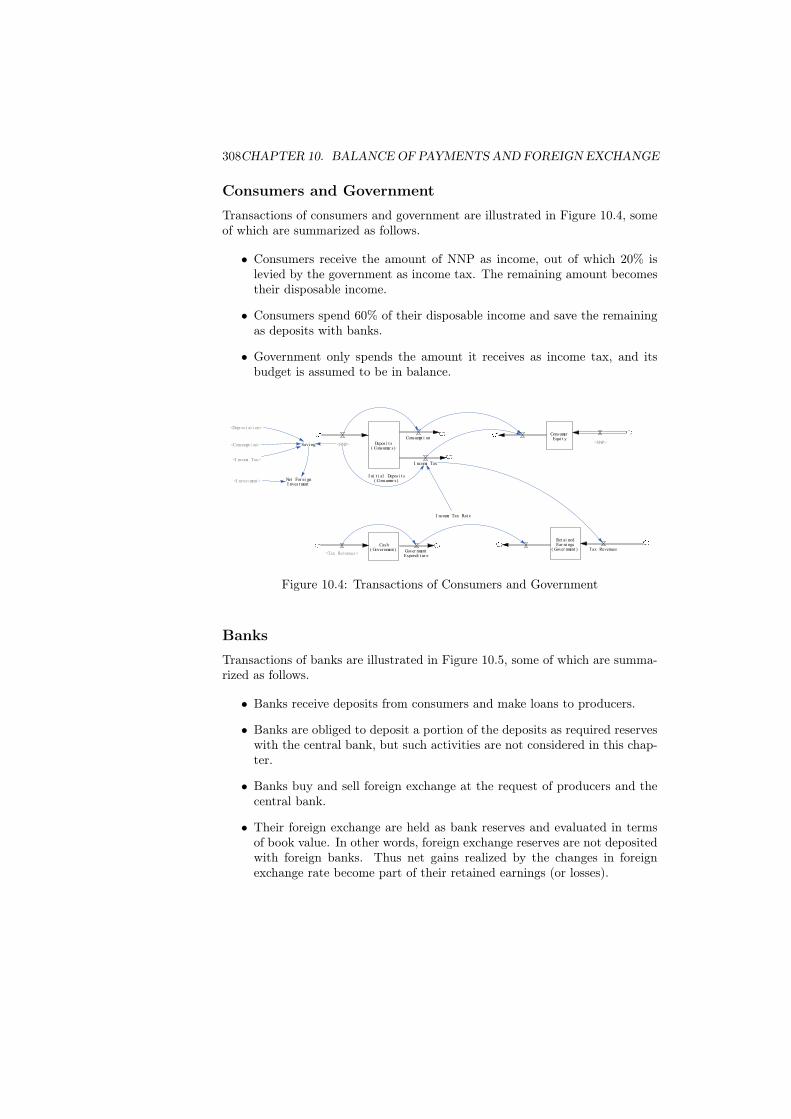

Consumers and GovernmentTransactions of consumers and government are illustrated in Figure 10.4, someof which are summarized as follows.

• Consumers receive the amount of NNP as income, out of which 20% islevied by the government as income tax. The remaining amount becomestheir disposable income.

• Consumers spend 60% of their disposable income and save the remainingas deposits with banks.

• Government only spends the amount it receives as income tax, and itsbudget is assumed to be in balance.

Deposi t s( Consumer s)

ConsumerEqui t y

I ni t i al Deposi t s( Consumer s)

Ret ai nedEar ni ngs

( Gover nment )Cash

( Gover nment )

I ncome Tax

Tax Revenues

I ncome Tax Rat e

<Tax Revenues>

Savi ng

<I ncome Tax>

Gover nmentExpendi t ur e

<NNP><NNP>

Consumpt i on

<Consumpt i on>

Net For ei gnI nvest ment

<I nvest ment >

<Depr eci at i on>

Figure 10.4: Transactions of Consumers and Government

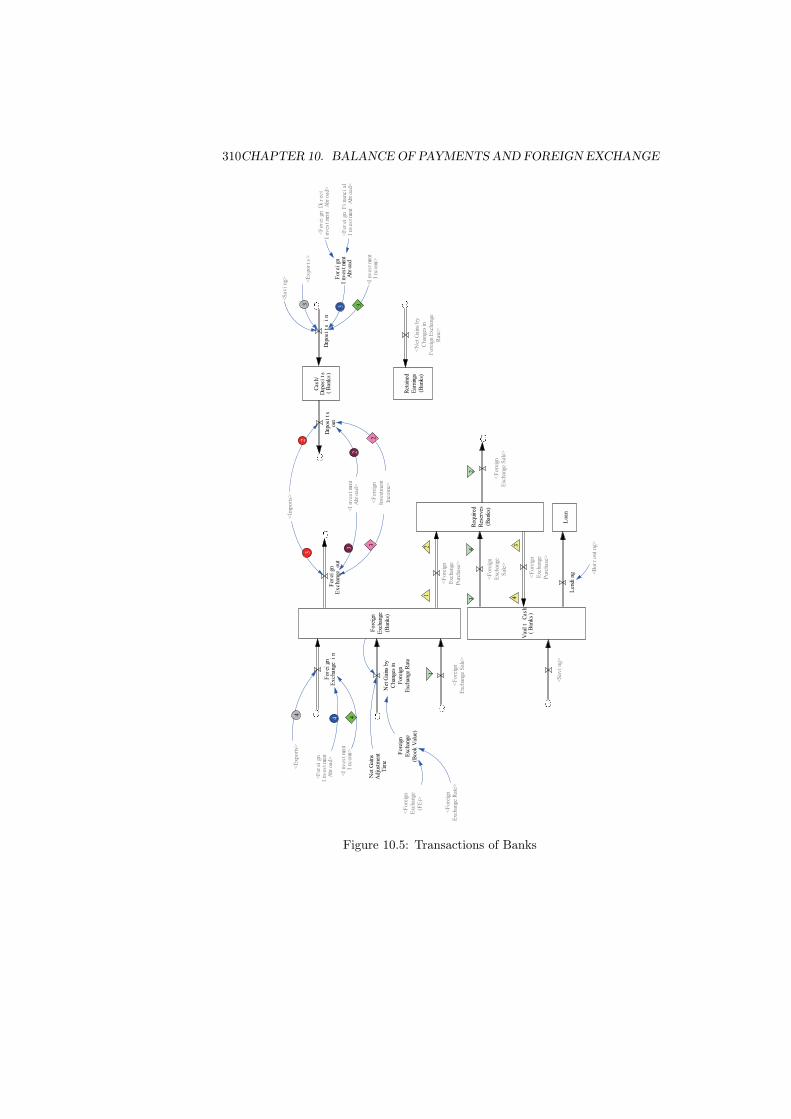

BanksTransactions of banks are illustrated in Figure 10.5, some of which are summa-rized as follows.

• Banks receive deposits from consumers and make loans to producers.

• Banks are obliged to deposit a portion of the deposits as required reserveswith the central bank, but such activities are not considered in this chap-ter.

• Banks buy and sell foreign exchange at the request of producers and thecentral bank.

• Their foreign exchange are held as bank reserves and evaluated in termsof book value. In other words, foreign exchange reserves are not depositedwith foreign banks. Thus net gains realized by the changes in foreignexchange rate become part of their retained earnings (or losses).

10.3. THE BALANCE OF PAYMENTS 309

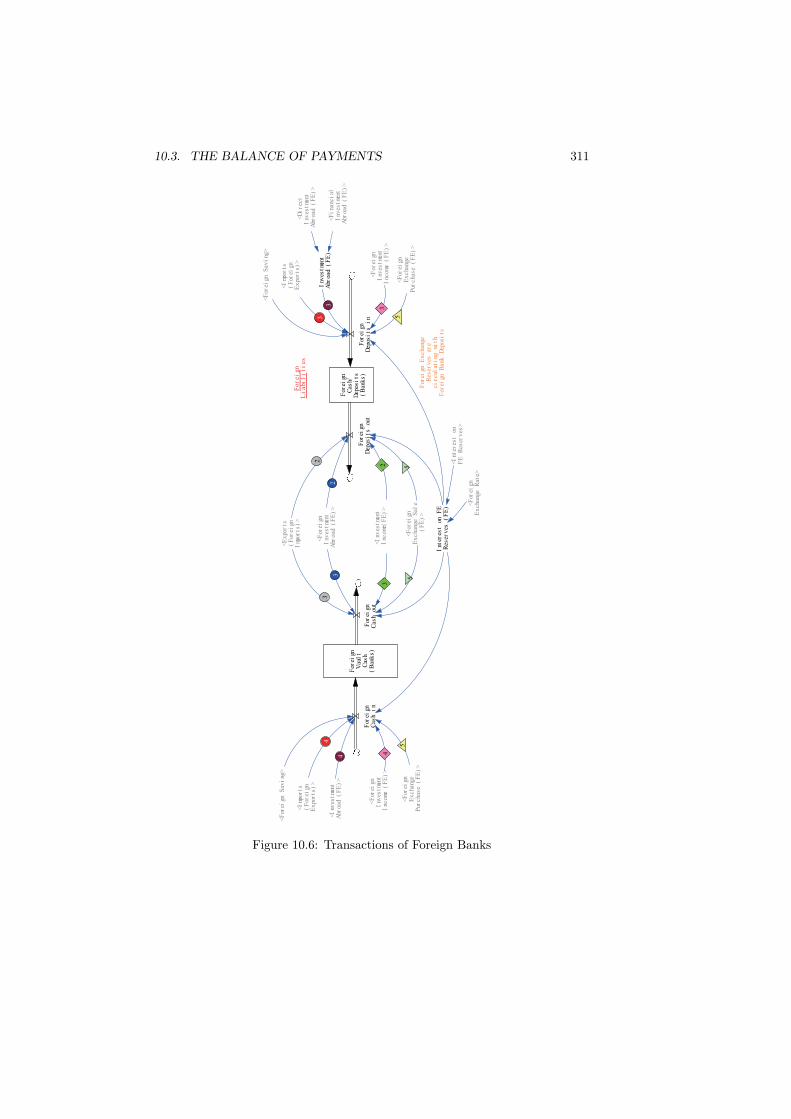

• Foreign currency is assumed to play a role of key currency or vehiclecurrency. Accordingly foreign banks need not set up foreign exchangeaccount. This is a point where a mirror image of open macroeconomicsymmetry breaks down, as illustrated in Figure 10.6.

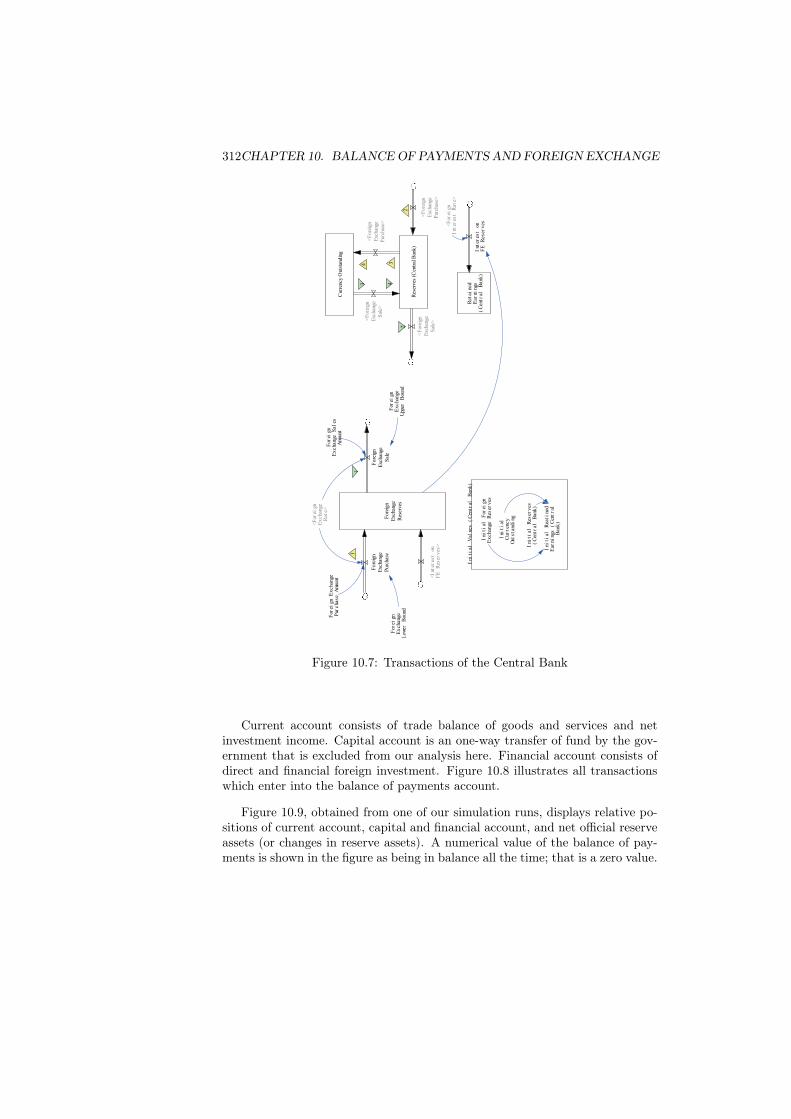

Central BankIn the integrated model of the previous chapter, the central bank played animportant role of providing a means of transactions and store of value; thatis, currency, and its sources of assets against which currency is issued wereassumed to be gold, loan and government securities. Transactions of the centralbank here are exceptionally simplified, as illustrated in Figure 10.7, so long asnecessary for the analytical purpose in this chapter.

• The central bank can control the amount of money supply through mon-etary policies such as the manipulation of required reserve ratio and openmarket operations. However, such a role of money supply by the centralbank is not considered here.

• The central bank is allowed to intervene foreign exchange market; thatis, it can buy and sell foreign exchange to keep a foreign exchange ratiostable. These transactions are manipulated with commercial banks, whichinescapably change the amount of currency outstanding and, hence, moneysupply. In this chapter, however, such an effect of money supply on interestrate is assumed to be out of consideration.

• Foreign exchange reserves held by the central bank is assumed to be de-posited with foreign banks so that it receives interest payments.

• The central bank of foreign country is excluded simply because foreigncurrency is assumed to be a vehicle currency, and it needs not to holdforeign reserves (that is, its own currency) to stabilize its own exchangerate in this simplified open macroeconomy.

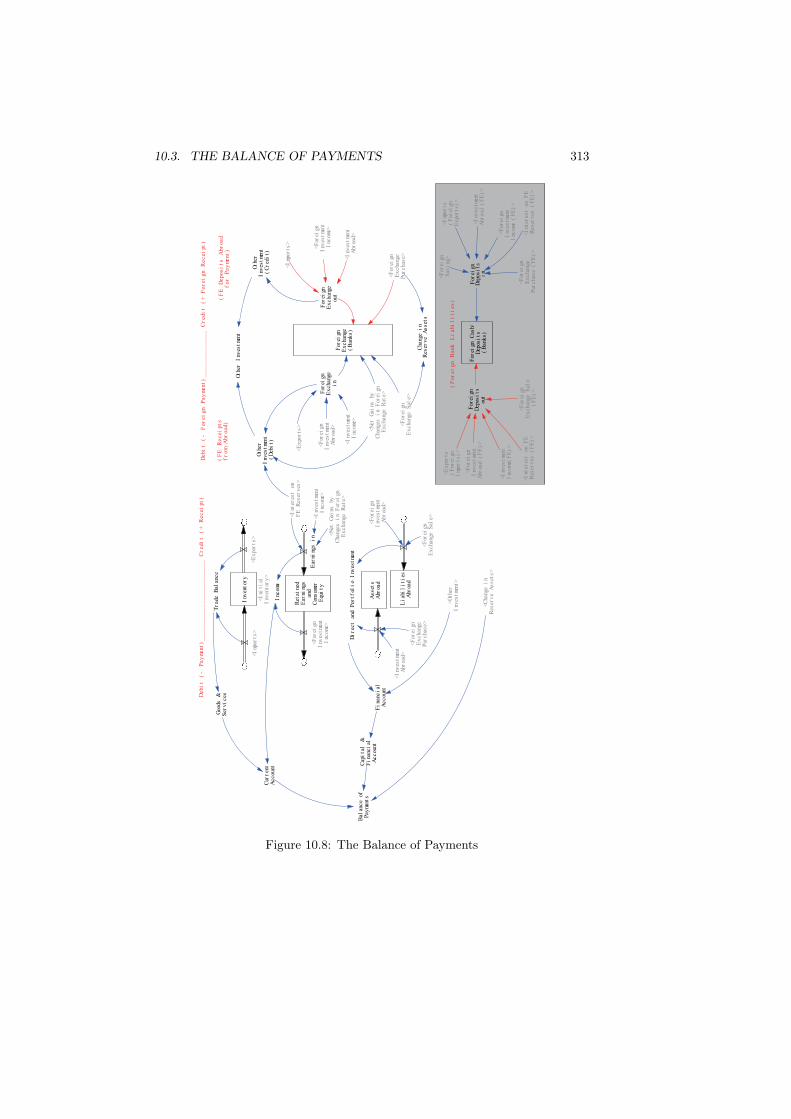

10.3 The Balance of PaymentsAll transactions with a foreign country such as foreign trade and foreign invest-ment (that is, payments and receipts of foreign exchange) are booked accordingto a double entry bookkeeping rule, and such a bookkeeping record is called thebalance of payments. According to [44] in page 295, all payments are recordedin the debit side with a minus sign, while all receipts are recorded in the creditside with plus sign. Hence, by definition, the balance of payments are keptin balance all the time. It consists of current account, capital and financialaccount, and net official reserve assets.

310CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

2

Req

uire

dR

eser

ves

(Ban

ks)

3

<F

ore

ign

Exc

hang

e S

ale>

2

<F

ore

ign

Exc

hang

eS

ale>

3

2

<F

ore

ign

Exc

hang

eP

urch

ase>

3

Fo

reig

nE

xcha

nge

(Ban

ks)

<E

xpo

rts>

<Im

po

rts>

3

11

<F

ore

ign

Exc

hang

eP

urch

ase>

<F

ore

ign

Exc

hang

e S

ale>

Fore

ign

Exc

hang

e(B

ook V

alue

)

<F

ore

ign

Exc

hang

e(F

E)>

Ret

aine

dE

arni

ngs

(Ban

ks)

Net

Gai

ns b

yC

hang

es in

Fo

reig

nE

xcha

nge

Rat

e

<N

et G

ains

by

Cha

nges

inF

ore

ign

Exc

hang

eR

ate>

Net

Gai

nsA

dju

stm

ent

Tim

e

<F

ore

ign

Inve

stm

ent

Inco

me>

<F

ore

ign

Exc

hang

e R

ate>

Cas

h/D

epos

its

(B

ank

s)

<Ex

por

ts>

Dep

osi

ts

in

Dep

osi

tsou

t

4

Vau

lt

Cas

h(

Ban

ks)

23

3<F

orei

gn

Fi

nanc

ial

Inv

estm

ent

Abr

oad>

4

34

23

4

4

For

eign

Ex

cha

nge

out

<Inv

estm

ent

Abr

oad>

For

eign

Ex

cha

nge

in

<Sav

ing

>

<Sav

ing

>

Len

ding

<Bor

row

ing

>

Loa

n

<Inv

estm

ent

Inc

ome>

<Inv

estm

ent

Inc

ome>

For

eign

Inv

estm

ent

Abr

oad

<For

eign

D

ir

ect

Inv

estm

ent

Abr

oad>

<For

eign

Inv

estm

ent

Abr

oad>

Figure 10.5: Transactions of Banks

10.3. THE BALANCE OF PAYMENTS 311

4

2

For

eign

Vau

lt

Cas

h(

Ban

ks)

For

eign

Cas

h/D

epos

its

(B

ank

s)

For

eign

Dep

osi

ts

in

For

eign

Dep

osi

ts

out

<Imp

orts

(F

orei

gnE

xpo

rts

)>

For

eign

Cas

h i

n

4

<Imp

orts

(F

orei

gnE

xpo

rts

)>

For

eign

Cas

h ou

t

Fo

re

ig

nL

ia

bi

li

ti

es

<Ex

por

ts(

For

eign

Imp

orts

)>

<Inv

estm

ent

Inc

ome(

FE

)>

33

3<F

ina

nci

alI

nves

tmen

tA

broa

d (

FE

)>

42

3

23

3

<For

eign

Inv

estm

ent

Abr

oad

(F

E)

>

<For

eign

Ex

cha

nge

Pur

cha

se

(F

E)

><F

orei

gnE

xcha

nge

Pur

cha

se

(F

E)

>

<For

eign

Ex

cha

nge

Sal

e(

FE

)>

Int

eres

t on

F

ER

eser

ves

(

FE

)

<Int

eres

t on

FE

R

eser

ves

>

<For

eign

Ex

cha

nge

Rat

e>

55

55

<For

eign

S

avi

ng>

<For

eign

S

avi

ng>

<For

eign

Inv

estm

ent

Inc

ome

(F

E)

>

<For

eign

Inv

estm

ent

Inc

ome

(F

E)

>

Inv

estm

ent

Abr

oad

(F

E)

<Di

rec

tI

nves

tmen

tA

broa

d (

FE

)>

<Inv

estm

ent

Abr

oad

(F

E)

>

For

eign

E

xcha

nge

Res

erv

es

are

ci

rcul

ati

ng

wi

thF

orei

gn

Ban

k

Dep

osi

ts

Figure 10.6: Transactions of Foreign Banks

312CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

Ini

tial

V

alue

s

(C

entr

al

Ban

k)

Fore

ign

Exc

hang

eR

eser

ves

Cur

renc

y O

utst

and

ing

Res

erve

s (C

entr

al B

ank)

Fore

ign

Exc

hang

eS

ale

1

<F

ore

ign

Exc

hang

eS

ale>2

<F

ore

ign

Exc

hang

eS

ale>

3

Fore

ign

Exc

hang

eP

urch

ase1

<F

ore

ign

Exc

hang

eP

urch

ase>

2

<F

ore

ign

Exc

hang

eP

urch

ase>

3

<For

eign

Ex

cha

nge

Rat

e>

For

eign

Ex

cha

nge

Low

er

Bou

nd

For

eign

Ex

cha

nge

Upp

er

Bou

nd

For

eign

E

xcha

nge

Pur

cha

se

Amo

unt

For

eign

Ex

cha

nge

Sal

esA

moun

t

4

4

Ret

aine

dE

arni

ngs

(C

entr

al

Ban

k)

Int

eres

t on

FE

R

eser

ves<F

orei

gnI

nter

est

Rat

e>

<Int

eres

t on

FE

R

eser

ves

>

Ini

tial

F

orei

gnE

xcha

nge

Res

erv

es

Ini

tial

Cur

ren

cy

Out

sta

ndi

ng

Ini

tial

R

eser

ves

(C

entr

al

Ban

k)

Ini

tial

R

eati

ned

Ear

ning

s

(C

entr

alB

ank

)

Figure 10.7: Transactions of the Central Bank

Current account consists of trade balance of goods and services and netinvestment income. Capital account is an one-way transfer of fund by the gov-ernment that is excluded from our analysis here. Financial account consists ofdirect and financial foreign investment. Figure 10.8 illustrates all transactionswhich enter into the balance of payments account.

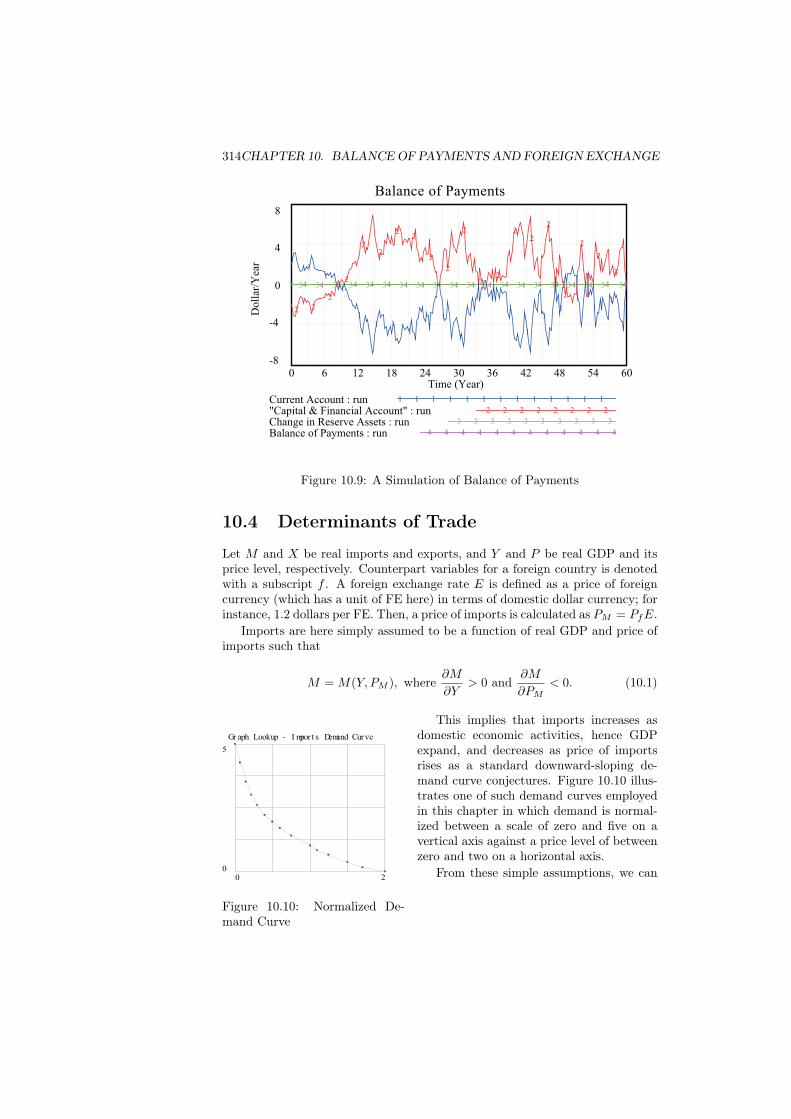

Figure 10.9, obtained from one of our simulation runs, displays relative po-sitions of current account, capital and financial account, and net official reserveassets (or changes in reserve assets). A numerical value of the balance of pay-ments is shown in the figure as being in balance all the time; that is a zero value.

10.3. THE BALANCE OF PAYMENTS 313

Inv

ento

ry

<Imp

orts

><E

xpo

rts

>

De

bi

t

(-

P

ay

me

nt

)_

__

__

__

__

__

__

__

__

__

__

__

_

Cr

edi

t

(+

R

ec

ei

pt

)

For

eign

Ex

cha

nge

(B

ank

s)

<Ex

por

ts>

<For

eign

Ex

cha

nge

Pur

cha

se>

<For

eign

Ex

cha

nge

Sal

e>

<For

eign

Inv

estm

ent

Inc

ome>

<Net

G

ains

by

Cha

nges

i

n F

orei

gnE

xcha

nge

Rat

e>

<Imp

orts

>

Oth

erI

nves

tmen

t(

Deb

it)

Oth

erI

nves

tmen

t(

Cr

edi

t)

Goo

ds

&S

erv

ices

Inc

ome

Di

rec

t an

d P

ortf

oli

o I

nves

tmen

t

Cha

nge

in

Res

erv

e A

sset

s

Tr

ade

Bal

ance

Fi

nanc

ial

Accou

nt

Cur

ren

tA

ccou

nt

Cap

ita

l

&F

ina

nci

alA

ccou

nt

Oth

er

Inv

estm

ent

Bal

ance

ofP

ayme

nts

<Oth

erI

nves

tmen

t>

For

eign

Ex

cha

nge

out

<Inv

estm

ent

Abr

oad>

For

eign

Ex

cha

nge

in

De

bi

t

(-

F

or

ei

gn

P

ay

me

nt

)_

__

__

__

__

__

__

_

Cr

edi

t

(+

F

or

ei

gn

R

ec

ei

pt

)

Ret

aine

dE

arni

ngs

and

Con

sum

erE

qui

ty

Ear

ning

s

in

<For

eign

Inv

estm

ent

Inc

ome>

<Net

G

ains

by

Cha

nges

i

n F

orei

gnE

xcha

nge

Rat

e>

Asset

sA

broa

d

<Inv

estm

ent

Abr

oad>

For

eign

C

ash/

Dep

osi

ts(

Ban

ks)

For

eign

Dep

osi

tsou

t

<Ex

por

ts(

For

eign

Imp

orts

)>

<For

eign

Ex

cha

nge

Sal

e(

FE

)>

<For

eign

Inv

estm

ent

Abr

oad

(F

E)

>

<Inv

estm

ent

Inc

ome(

FE

)>

For

eign

Dep

osi

tsi

n

<For

eign

Ex

cha

nge

Pur

cha

se

(F

E)

>

<Imp

orts

(F

orei

gnE

xpo

rts

)>

<For

eign

Ex

cha

nge

Pur

cha

se>

<For

eign

Ex

cha

nge

Sal

e>

<Cha

nge

in

Res

erv

e A

sset

s>

(F

or

ei

gn

B

an

k

Li

abi

li

ti

es

)(F

E

De

po

si

ts

A

br

oa

df

or

P

ay

me

nt

)

<Int

eres

t on

F

ER

eser

ves

(

FE

)>

<Int

eres

t on

FE

R

eser

ves

>

(F

E

Re

ce

ipt

sf

ro

m

Abr

oa

d)

Li

abi

li

ties

Abr

oad

<Ini

tial

Inv

ento

ry

>

<Int

eres

t on

F

ER

eser

ves

(

FE

)>

<For

eign

Sav

ing

>

<Inv

estm

ent

Inc

ome>

<For

eign

Inv

estm

ent

Inc

ome

(F

E)

>

<For

eign

Inv

estm

ent

Abr

oad>

<Inv

estm

ent

Abr

oad

(F

E)

>

<For

eign

Inv

estm

ent

Abr

oad>

<Inv

estm

ent

Inc

ome>

Figure 10.8: The Balance of Payments

314CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

Balance of Payments

8

4

0

-4

-8

4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 43 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3

2 22

2

22

22

2

2

2

22

22

2

2

2

2

2

11

1

1

11 1

1

1 1

1

11

1

1

11

11

1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Current Account : run 1 1 1 1 1 1 1 1 1 1 1 1 1

"Capital & Financial Account" : run 2 2 2 2 2 2 2 2

Change in Reserve Assets : run 3 3 3 3 3 3 3 3 3 3

Balance of Payments : run 4 4 4 4 4 4 4 4 4 4 4 4

Figure 10.9: A Simulation of Balance of Payments

10.4 Determinants of Trade

Let M and X be real imports and exports, and Y and P be real GDP and itsprice level, respectively. Counterpart variables for a foreign country is denotedwith a subscript f . A foreign exchange rate E is defined as a price of foreigncurrency (which has a unit of FE here) in terms of domestic dollar currency; forinstance, 1.2 dollars per FE. Then, a price of imports is calculated as PM = PfE.

Imports are here simply assumed to be a function of real GDP and price ofimports such that

M = M(Y, PM ), where∂M

∂Y> 0 and

∂M

∂PM< 0. (10.1)

Gr aph Lookup - I mpor t s Demand Curve

5

00 2

Figure 10.10: Normalized De-mand Curve

This implies that imports increases asdomestic economic activities, hence GDPexpand, and decreases as price of importsrises as a standard downward-sloping de-mand curve conjectures. Figure 10.10 illus-trates one of such demand curves employedin this chapter in which demand is normal-ized between a scale of zero and five on avertical axis against a price level of betweenzero and two on a horizontal axis.

From these simple assumptions, we can

10.4. DETERMINANTS OF TRADE 315

derive the following relations:

M = M(Y, PM ) = M(Y, PfE), (10.2)

∂M

∂Pf=

∂M

∂PM

∂PM

∂Pf=

∂M

∂PME < 0 (10.3)

∂M

∂E=

∂M

∂PM

∂PM

∂E=

∂M

∂PMPf < 0 (10.4)

These relations imply that imports decrease as foreign price of imports increasesand/or foreign exchange rate appreciates.

In our model, imports function is further simplified as a product of importsdetermined by the size of GDP and a normalized demand curve such that

M = M(Y, PM ) = M(Y )D(PM ) = mYD(PfE) (10.5)

where m is a constant coefficient of imports on GDP.Exports are nothing but imports of a foreign country, and similarly deter-

mined as a mirror image of domestic imports function such that

X = X(Yf , PM,f ), where∂X

∂Yf> 0 and

∂X

∂PM,f< 0. (10.6)

This implies that exports increase as foreign economic activities, hence foreignGDP, expand, and decreases as price of imports in a foreign country rises as astandard downward-sloping demand curve conjectures.

Price of imports in a foreign country is calculated by a domestic price andforeign exchange rate such that PM,f = P/E. Hence, we obtain the followingrelations:

X = X(Yf , PM,f ) = X(Yf , P/E), (10.7)

∂X

∂P=

∂X

∂PM,f

∂PM,f

∂P=

∂X

∂PM,f

1

E< 0 (10.8)

∂X

∂E=

∂X

∂PM,f

∂PM,f

∂E=

∂X

∂PM,f(− P

E2) > 0. (10.9)

Thus, exports decrease as a domestic price rises. Meanwhile, whenever foreignexchange appreciates, our products become cheaper in a foreign country andexports increase.

Exports are similarly broken down as a product of foreign imports and nor-malized demand curve of foreign country, which is assumed to be exactly thesame as domestic demand curve for imports.

X = X(Yf , PM,f ) = X(Yf )D(PM,f ) = mfYfD(P/E) (10.10)

where mf is a constant import coefficient of a foreign country.

316CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

Let us define trade balance as

TB(E;Y, Yf , P, Pf ) = X(E;Yf , P )−M(E;Y, Pf ) (10.11)

Then we have∂TB

∂Y= −∂M

∂Y< 0,

∂TB

∂Yf=

∂X

∂Yf> 0, (10.12)

∂TB

∂P=

∂X

∂P< 0,

∂TB

∂Pf= − ∂M

∂Pf> 0. (10.13)

∂TB

∂E=

∂X

∂E− ∂M

∂E> 0. (10.14)

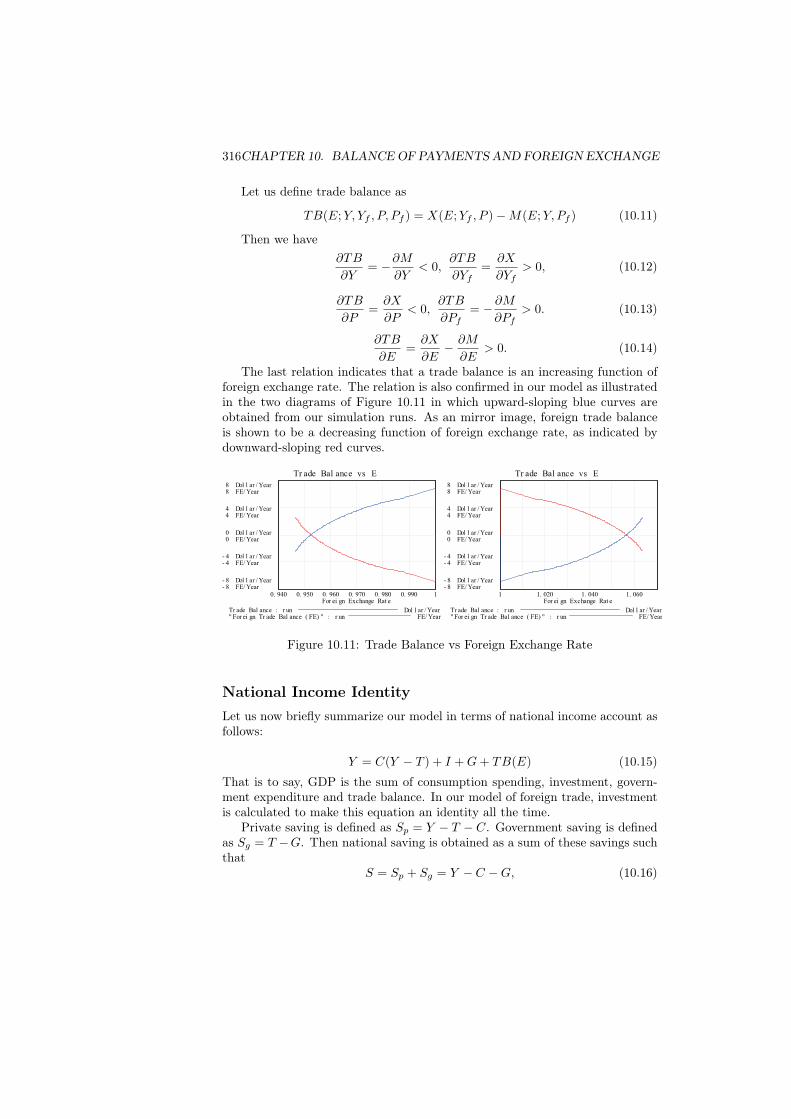

The last relation indicates that a trade balance is an increasing function offoreign exchange rate. The relation is also confirmed in our model as illustratedin the two diagrams of Figure 10.11 in which upward-sloping blue curves areobtained from our simulation runs. As an mirror image, foreign trade balanceis shown to be a decreasing function of foreign exchange rate, as indicated bydownward-sloping red curves.

Tr ade Bal ance vs E

8 Dol l ar / Year8 FE/ Year

4 Dol l ar / Year4 FE/ Year

0 Dol l ar / Year0 FE/ Year

- 4 Dol l ar / Year- 4 FE/ Year

- 8 Dol l ar / Year- 8 FE/ Year

0. 940 0. 950 0. 960 0. 970 0. 980 0. 990 1For ei gn Exchange Rat e

Tr ade Bal ance : r un Dol l ar / Year" For ei gn Tr ade Bal ance ( FE) " : r un FE/ Year

Tr ade Bal ance vs E

8 Dol l ar / Year8 FE/ Year

4 Dol l ar / Year4 FE/ Year

0 Dol l ar / Year0 FE/ Year

- 4 Dol l ar / Year- 4 FE/ Year

- 8 Dol l ar / Year- 8 FE/ Year

1 1. 020 1. 040 1. 060For ei gn Exchange Rat e

Tr ade Bal ance : r un Dol l ar / Year" For ei gn Tr ade Bal ance ( FE) " : r un FE/ Year

Figure 10.11: Trade Balance vs Foreign Exchange Rate

National Income IdentityLet us now briefly summarize our model in terms of national income account asfollows:

Y = C(Y − T ) + I +G+ TB(E) (10.15)That is to say, GDP is the sum of consumption spending, investment, govern-ment expenditure and trade balance. In our model of foreign trade, investmentis calculated to make this equation an identity all the time.

Private saving is defined as Sp = Y − T − C. Government saving is definedas Sg = T −G. Then national saving is obtained as a sum of these savings suchthat

S = Sp + Sg = Y − C −G, (10.16)

10.5. DETERMINANTS OF FOREIGN INVESTMENT 317

which reduces toS − I = TB(E). (10.17)

Saving less investment is called net foreign investment, which is equal to tradebalance. This becomes another way of describing the above national incomeidentity in terms of net foreign investment and trade balance.

10.5 Determinants of Foreign InvestmentForeign investment consists of direct investment and financial investment suchas stocks, bonds and cash, which constitute financial assets. In this chapterfinancial assets are not specified without losing generality as already mentionedin the footnote above. Foreign investments are here assumed to be determinedon a principle of foreign exchange market efficiency under the uncovered interestrate parity (UIP) condition as explained in standard textbooks such as [44] and[57].

Let i and R be interest rate and a rate of return from financial investment,and Ee be an expected foreign exchange rate. A rate of return from a bankdeposit is the same as the interest rate:

R = i (10.18)

An expected return from a deposit with a foreign bank is calculated as

Rf = (1 + if )Ee

E− 1 (10.19)

Thus we obtain∂Rf

∂E= − (1 + if )Ee

E2< 0 (10.20)

∂Rf

∂Ee=

(1 + if )

E> 0 (10.21)

This implies that a rate of return from foreign financial investment decreases ifforeign exchange rate appreciates, but it increases when foreign exchange rateis expected to appreciate.

Let us define an expected return arbitrage as

A(E,Ee; i, if ) = Rf (E,Ee; if )−R(i) (10.22)

and net capital flow(NCF ) as

NCF = Foreign Investment Abroad − Investment Abroad (10.23)

This is the amount of capital we receive from foreign country’s investment lessthe amount we invest abroad. Under the assumption of an efficient financialmarket, if expected returns are greater in a foreign country and an expectedreturn arbitrage becomes positive, then financial capital continues to outflow

318CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

until the arbitrage ceases to exist. In a similar fashion, if expected returns aregreater in a domestic market and an expected return arbitrage becomes negative,then financial capital continues to inflow until the arbitrage disappears. Hence,so long as a foreign exchange market is efficient, the relation between net capitalflow and an expected return arbitrage become as follows:

!NCF < 0 if A > 0NCF > 0 if A < 0

(10.24)

It is unrealistic, however, to assume an indefinite outflow of capital even ifA > 0, or an indefinite inflow of capital even if A < 0. So it is assumed herethat the maximum amount of direct and financial investment made availableper year is a finite portion of domestic investment and financial assets. Yet,actual amount of financial investment is further assumed to be dependent ona level of an expected return arbitrage by its factor. Figure 10.12 illustratestable functions of investment levels that are assumed in our model in terms ofexpected return arbitrate.

Gr aph Lookup - Di r ect I nvest ment I ndex Tabl e

1. 2

- 0. 4- 0. 2 0. 2

Gr aph Lookup - Fi nanci al I nvest ment I ndex Tabl e

1. 1

- 1. 1- 0. 2 0. 2

Figure 10.12: Direct and Financial Investment Indices

Specifically, left-hand diagram shows a table function of direct investment,which assumes that between the arbitrage range of -0.01 and 0.01 direct in-vestment is not made. Right-hand diagram shows a table function of financialinvestment, which assumes that between the arbitrage range of -0.01 and 0.01financial capital flows slowly between a portion of -0.02 and 0.02. These as-sumptions are made to reflects a realistic situation in which direct investmentis not so sensitive to the arbitrage values compared with financial investment.

In this way net capital flow could be described as a function of an expectedreturn arbitrage such that

NCF = NCF (A(E,Ee)), where∂NCF

∂A< 0 (10.25)

It is important to note, however, that this functional relation holds only in the

10.6. DYNAMICS OF FOREIGN EXCHANGE RATES 319

neighborhood of equilibrium, so do the following relations as well.

∂NCF

∂E=

∂NCF

∂A

∂A

∂E=

∂NCF

∂A

∂Rf

∂E> 0 (10.26)

∂NCF

∂Ee=

∂NCF

∂A

∂A

∂Ee=

∂NCF

∂A

∂Rf

∂Ee< 0 (10.27)

Whenever a foreign exchange rate begins to appreciate, an expected returnarbitrage declines, and capital begins to inflow, causing a positive net capitalflow. When foreign exchange rate is expected to appreciate, an expected returnarbitrage increases and capital begins to outflow, causing a negative net capitalflow. In this way, changes in a foreign exchange rate and its expectations playa crucial role for financial investment.

It is examined in our model that these relations only hold in the neigh-borhood of equilibrium. In Figure 10.13, net capital flow is shown to be an

NCF vs E

0

- 1

- 2

- 3

- 40. 940 0. 950 0. 960 0. 970 0. 980 0. 990 1

For ei gn Exchange Rat e

Dol

lar

/Yea

r

Net Capi t al I nf l ow : r un

NCF vs E

6

4. 5

3

1. 5

01 1. 010 1. 020 1. 030 1. 040 1. 050 1. 060 1. 070

For ei gn Exchange Rat e

Dol

lar

/Yea

r

Net Capi t al I nf l ow : r un

Figure 10.13: Net Capital Inflow vs Foreign Exchange Rate

increasing function only when a foreign exchange rate is around the equilib-rium; that is, between 0.983 and 1.018. This may indicate a limitation of theabove mathematical method of economic analysis which has been dominantlyused in many textbooks. In other words, mutually interdependent economic be-haviors cannot be fully captured unless they are simulated in a system dynamicsmodel such as the one in this chapter.

10.6 Dynamics of Foreign Exchange RatesHow are the foreign exchange rate and its expectations determined, then? For-eign exchange rate is here simply assumed to be determined by the excess de-mand for foreign exchange; that is, a standard logic of price mechanism ineconomic theory. From the left-hand diagram of Figure 10.8, demand for for-eign exchange is shown to stem from the need for payments due to imports,direct and financial investment abroad, and foreign investment income, as wellas foreign exchange purchase by the central bank. Supply of foreign exchange

320CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

results from the receipts from foreign country due to exports, foreign direct andfinancial investment abroad, and investment income from abroad, as well asforeign exchange sale by the central bank.

Hence, excess demand for foreign exchange is calculated as follows:

Excess Demand for Foreign Exchange= Imports - Exports

+ Investment Abroad - Foreign Investment Abroad+ Foreign Investment Income - Investment Income+ Foreign Exchange Purchase - Foreign Exchange Sale

= − Trade Balance (TB)

− Net Capital Flow (NCF )

− Net Investment Income (NII)

+ Net Exchange Reserves (NER)

(10.28)

Net investment income is derived from the financial assets invested abroadand here assumed to be dependent only on domestic and foreign interest rates.Net exchange reserves depend on the official foreign exchange intervention.Therefore, NII and NER are not dependent on foreign exchange rate and itsexpectations.

With these relations taken into consideration, dynamics of foreign exchangerate is mathematically expressed as a function of excess demand for foreignexchange, which in turn becomes a function of E and Ee as follows:

dE

dt= Ψ(−TB(E)−NCF (E,Ee)−NII +NER) = Ψ(E,Ee) (10.29)

On the other hand, a formation of expected foreign exchange rates is difficultto formalize. Here it is simply assumed that actual expectations of foreignexchange rate fluctuates randomly around the current exchange rate by thefactor of random normal distribution of Nrandom(m, sd) where (m, sd) denotesmean and standard deviation, and accordingly an expected foreign exchangerate is obtained as an adaptive expectation against the actual expectation ofrandom normal distribution.

Mathematically, dynamics of the expected foreign exchange rate thus definedis described as

dEe

dt= Φ(Nrandom(m, sd)E − Ee) = Φ(E,Ee) (10.30)

Thus, expected foreign exchange rate can be easily adjusted to the actual trendsand volatilities of various economic situations by refining values in mean andstandard deviation. Figure 10.14 illustrates how foreign exchange rate and itsexpectation are modeled in our economy.

10.6. DYNAMICS OF FOREIGN EXCHANGE RATES 321

Fore

ign

Exc

hang

eR

ate

Cha

nge

in F

ore

ign

Exc

hang

e R

ate

Fore

ign

Exc

hang

e (F

E)

<E

xport

s (F

ore

ign

Import

s)>

<Im

port

s (F

ore

ign

Exp

ort

s)>

Sup

ply

of F

ore

ign

Exc

hang

e

Dem

and for

Fore

ign

Exc

hang

e

Sup

ply

of F

ore

ign

Exc

hang

eD

eman

d for

Fore

ign

Exc

hang

e

Fo

reig

nE

xcha

nge

Rat

io

<F

ore

ign

Exc

hang

e S

ale>

<F

ore

ign

Exc

hang

eP

urch

ase>

Fore

ign

Exc

hang

eS

ale

(FE

)F

ore

ign

Exc

hang

eP

urch

ase

(FE

)

Initi

al F

ore

ign

Exc

hang

e R

ate

(Bal

ance

of P

aym

ents

(F

E))

<In

vest

men

tIn

com

e(F

E)>

Exp

ecte

d F

ore

ign

Exc

hang

e R

ate

Cha

nge

in E

xpec

ted

Fore

ign

Exc

hang

e R

ae

Adju

stm

ent

Tim

e of

Fore

ign

Exc

hang

eE

xpec

tatio

n

Ad

just

men

tT

ime

of F

E

<F

ore

ign

Inve

stm

ent

Inco

me

(FE

)>

<F

ore

ign

Inve

stm

ent

Abro

ad (

FE

)><

Inve

stm

ent

Abro

ad (

FE

)>

Exp

ecte

d C

hang

ein

FE

R

mea

n

stan

dar

ddev

iatio

n

seed

s

Eff

ect

on

Fore

ign

Exc

hang

e R

ate

Des

ired

Fore

ign

Exc

hang

e R

ate

Rat

io E

last

icity

(E

ffec

t on

Fore

ign

Exc

hang

e R

ate)

Figure 10.14: Determination of Foreign Exchange

Now dynamic modeling of foreign exchange rate in our open macroeconomyis complete. It consists of three equations: (10.15), (10.29), and (10.30), outof which three variables E,Ee and TB are determined, given parameters out-side such as GDP, its price level and interest rate, as well as random normaldistribution of expected foreign exchange rate. Schematically, it is written as

(Y, Yf , P, Pf , i, if , Nrandom) =⇒ (E,Ee, TB) (10.31)

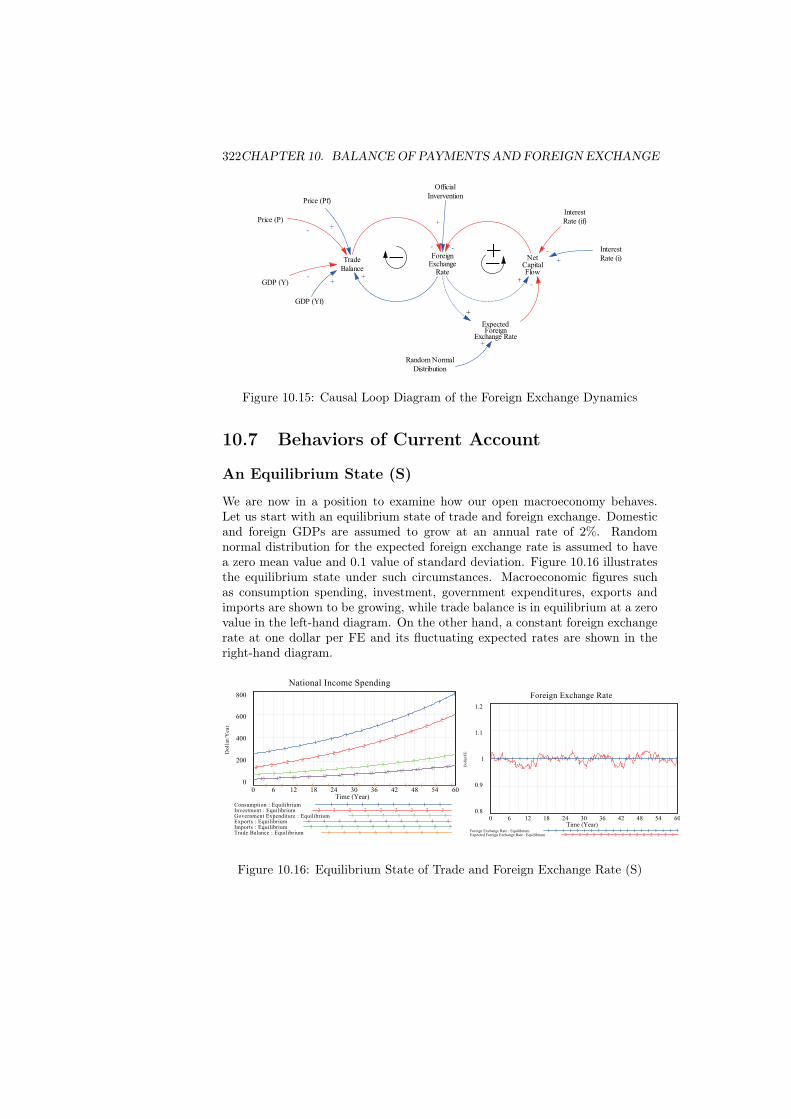

Figure 10.15 draws a theoretical gist of our open macroeconomic framework asa simplified causal loop diagram of the dynamics of foreign exchange rate in ouropen macroeconomy.

322CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

GDP (Y)

TradeBalance

ForeignExchange

Rate-

-

+

Random NormalDistribution

ExpectedForeign

Exchange Rate+

NetCapitalFlow

-

-

+

InterestRate (i)+

Price (P)

-

OfficialInvervention

+

+

GDP (Yf)

Price (Pf)

InterestRate (if)

+

+

-

Figure 10.15: Causal Loop Diagram of the Foreign Exchange Dynamics

10.7 Behaviors of Current Account

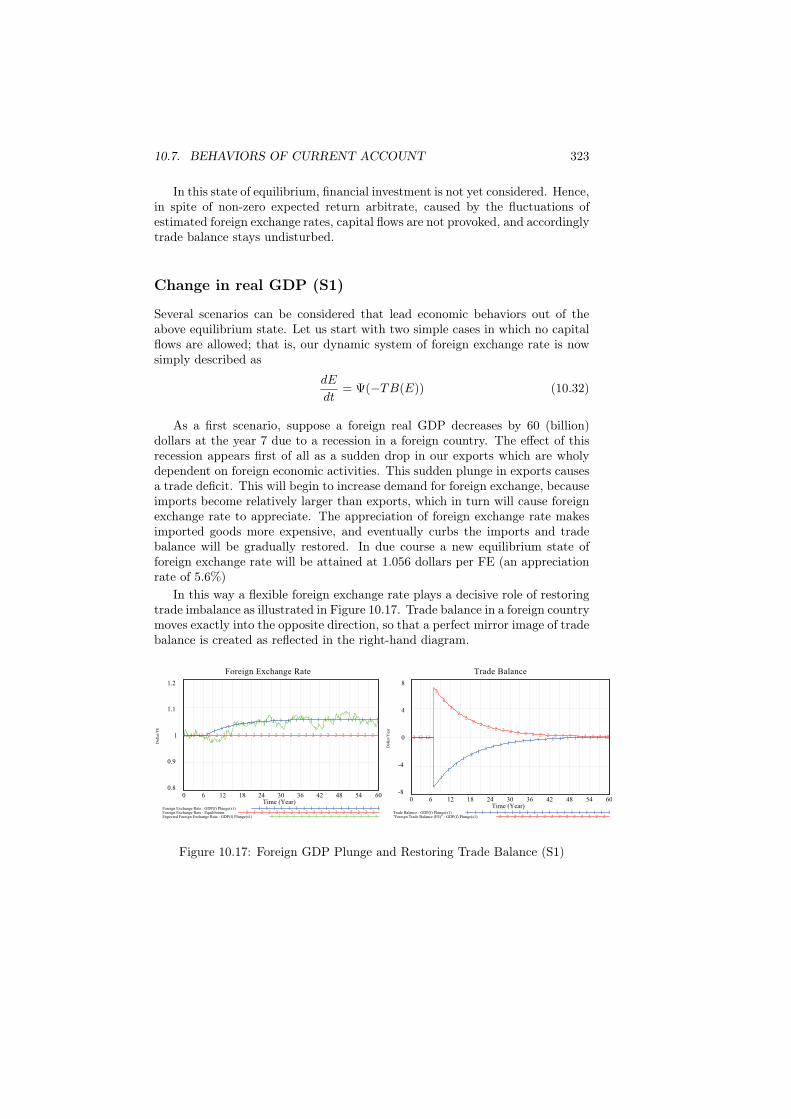

An Equilibrium State (S)

We are now in a position to examine how our open macroeconomy behaves.Let us start with an equilibrium state of trade and foreign exchange. Domesticand foreign GDPs are assumed to grow at an annual rate of 2%. Randomnormal distribution for the expected foreign exchange rate is assumed to havea zero mean value and 0.1 value of standard deviation. Figure 10.16 illustratesthe equilibrium state under such circumstances. Macroeconomic figures suchas consumption spending, investment, government expenditures, exports andimports are shown to be growing, while trade balance is in equilibrium at a zerovalue in the left-hand diagram. On the other hand, a constant foreign exchangerate at one dollar per FE and its fluctuating expected rates are shown in theright-hand diagram.

National Income Spending

800

600

400

200

06 6 6 6 6 6 6 6 6 6 6 6 6

5 5 5 5 5 5 5 5 5 5 5 5 5

4 4 4 4 4 4 4 4 4 4 4 4 4

3 3 3 3 3 3 3 3 3 3 3 3 3

2 22

22

22

22

22

22

11

11

11

11

11

1

1

1

1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Consumption : Equilibrium 1 1 1 1 1 1 1 1Investment : Equilibrium 2 2 2 2 2 2 2 2 2Government Expenditure : Equilibrium 3 3 3 3 3 3 3Exports : Equilibrium 4 4 4 4 4 4 4 4 4 4Imports : Equilibrium 5 5 5 5 5 5 5 5 5 5Trade Balance : Equilibrium 6 6 6 6 6 6 6 6

Foreign Exchange Rate

1.2

1.1

1

0.9

0.8

22 2

22 2

2

22 2 2

2

22

2 2 2

2 2

2 22

2 22 21 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Doll

ar/F

E

Foreign Exchange Rate : Equilibrium 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Expected Foreign Exchange Rate : Equilibrium 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Figure 10.16: Equilibrium State of Trade and Foreign Exchange Rate (S)

10.7. BEHAVIORS OF CURRENT ACCOUNT 323

In this state of equilibrium, financial investment is not yet considered. Hence,in spite of non-zero expected return arbitrate, caused by the fluctuations ofestimated foreign exchange rates, capital flows are not provoked, and accordinglytrade balance stays undisturbed.

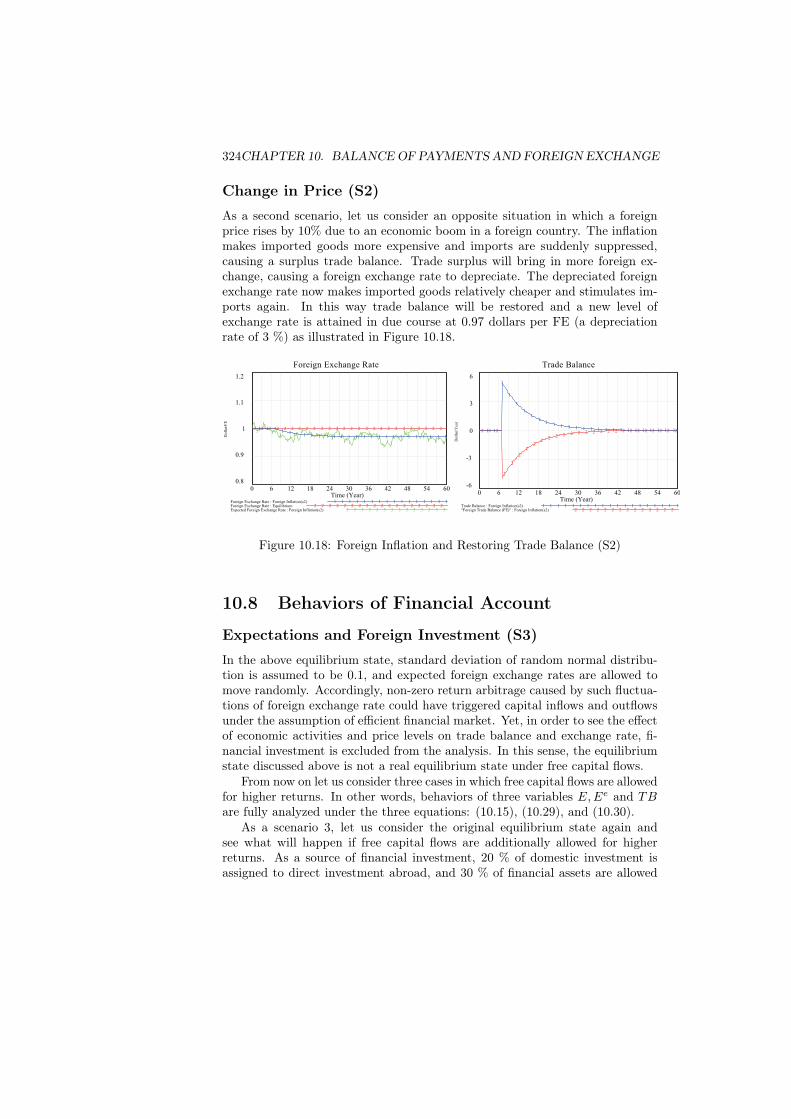

Change in real GDP (S1)

Several scenarios can be considered that lead economic behaviors out of theabove equilibrium state. Let us start with two simple cases in which no capitalflows are allowed; that is, our dynamic system of foreign exchange rate is nowsimply described as

dE

dt= Ψ(−TB(E)) (10.32)

As a first scenario, suppose a foreign real GDP decreases by 60 (billion)dollars at the year 7 due to a recession in a foreign country. The effect of thisrecession appears first of all as a sudden drop in our exports which are wholydependent on foreign economic activities. This sudden plunge in exports causesa trade deficit. This will begin to increase demand for foreign exchange, becauseimports become relatively larger than exports, which in turn will cause foreignexchange rate to appreciate. The appreciation of foreign exchange rate makesimported goods more expensive, and eventually curbs the imports and tradebalance will be gradually restored. In due course a new equilibrium state offoreign exchange rate will be attained at 1.056 dollars per FE (an appreciationrate of 5.6%)

In this way a flexible foreign exchange rate plays a decisive role of restoringtrade imbalance as illustrated in Figure 10.17. Trade balance in a foreign countrymoves exactly into the opposite direction, so that a perfect mirror image of tradebalance is created as reflected in the right-hand diagram.

Foreign Exchange Rate

1.2

1.1

1

0.9

0.8

33

3 3 3

3

3 3 3 3 33

33

3 3 3

33

33

33

3 3 3

2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 21 1 1 11

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/FE

Foreign Exchange Rate : GDP(f) Plunge(s1) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Foreign Exchange Rate : Equilibrium 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Expected Foreign Exchange Rate : GDP(f) Plunge(s1) 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3

Trade Balance

8

4

0

-4

-8

2 2 2

2

2

22

22

22 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 21 1 1

1

1

1

11

11

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Trade Balance : GDP(f) Plunge(s1) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1"Foreign Trade Balance (FE)" : GDP(f) Plunge(s1) 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Figure 10.17: Foreign GDP Plunge and Restoring Trade Balance (S1)

324CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

Change in Price (S2)As a second scenario, let us consider an opposite situation in which a foreignprice rises by 10% due to an economic boom in a foreign country. The inflationmakes imported goods more expensive and imports are suddenly suppressed,causing a surplus trade balance. Trade surplus will bring in more foreign ex-change, causing a foreign exchange rate to depreciate. The depreciated foreignexchange rate now makes imported goods relatively cheaper and stimulates im-ports again. In this way trade balance will be restored and a new level ofexchange rate is attained in due course at 0.97 dollars per FE (a depreciationrate of 3 %) as illustrated in Figure 10.18.

Foreign Exchange Rate

1.2

1.1

1

0.9

0.8

33

33

33

3 33 3

33

3 33 3 3

33

33

33

3 3 3

2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 21 1 1 11 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/FE

Foreign Exchange Rate : Foreign Inflation(s2) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Foreign Exchange Rate : Equilibrium 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Expected Foreign Exchange Rate : Foreign Inflation(s2) 3 3 3 3 3 3 3 3 3 3 3 3 3 3

Trade Balance

6

3

0

-3

-6

2 2 2

2

2

2

22

22 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 21 1 1

1

1

1

11

11 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Trade Balance : Foreign Inflation(s2) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1"Foreign Trade Balance (FE)" : Foreign Inflation(s2) 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Figure 10.18: Foreign Inflation and Restoring Trade Balance (S2)

10.8 Behaviors of Financial Account

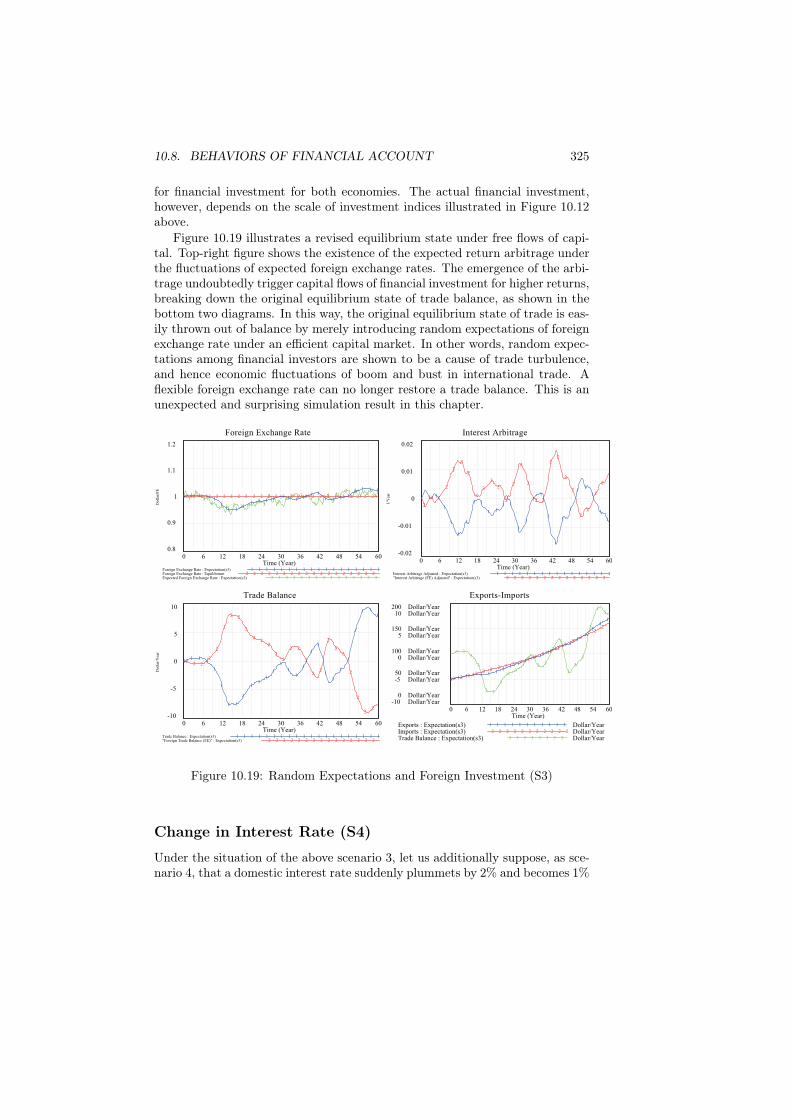

Expectations and Foreign Investment (S3)In the above equilibrium state, standard deviation of random normal distribu-tion is assumed to be 0.1, and expected foreign exchange rates are allowed tomove randomly. Accordingly, non-zero return arbitrage caused by such fluctua-tions of foreign exchange rate could have triggered capital inflows and outflowsunder the assumption of efficient financial market. Yet, in order to see the effectof economic activities and price levels on trade balance and exchange rate, fi-nancial investment is excluded from the analysis. In this sense, the equilibriumstate discussed above is not a real equilibrium state under free capital flows.

From now on let us consider three cases in which free capital flows are allowedfor higher returns. In other words, behaviors of three variables E,Ee and TBare fully analyzed under the three equations: (10.15), (10.29), and (10.30).

As a scenario 3, let us consider the original equilibrium state again andsee what will happen if free capital flows are additionally allowed for higherreturns. As a source of financial investment, 20 % of domestic investment isassigned to direct investment abroad, and 30 % of financial assets are allowed

10.8. BEHAVIORS OF FINANCIAL ACCOUNT 325

for financial investment for both economies. The actual financial investment,however, depends on the scale of investment indices illustrated in Figure 10.12above.

Figure 10.19 illustrates a revised equilibrium state under free flows of capi-tal. Top-right figure shows the existence of the expected return arbitrage underthe fluctuations of expected foreign exchange rates. The emergence of the arbi-trage undoubtedly trigger capital flows of financial investment for higher returns,breaking down the original equilibrium state of trade balance, as shown in thebottom two diagrams. In this way, the original equilibrium state of trade is eas-ily thrown out of balance by merely introducing random expectations of foreignexchange rate under an efficient capital market. In other words, random expec-tations among financial investors are shown to be a cause of trade turbulence,and hence economic fluctuations of boom and bust in international trade. Aflexible foreign exchange rate can no longer restore a trade balance. This is anunexpected and surprising simulation result in this chapter.

Foreign Exchange Rate

1.2

1.1

1

0.9

0.8

33

33

3 3 3 3 33 3

33

33 3 3

33

33

33

3 3 32 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 21 1 1 11

11 1

11 1 1 1 1 1 1 1

1 11 1 1 1

11 1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/FE

Foreign Exchange Rate : Expectation(s3) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Foreign Exchange Rate : Equilibrium 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Expected Foreign Exchange Rate : Expectation(s3) 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3

Interest Arbitrage

0.02

0.01

0

-0.01

-0.02

2

2 2

2

2

2

2

2

2

2

2

2

2

2

2

2 2

22

2

2

22

2

2

1 1 1

1

1

1

1

1 1

1 11 1

1

1

11

1

1

1

1

11

1

1

1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

1/Y

ear

Interest Arbitrage Adjusted : Expectation(s3) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1"Interest Arbitrage (FE) Adjusted" : Expectation(s3) 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Trade Balance

10

5

0

-5

-10

22 2

2

2

2

2 2

2

22

2

22

2 2

2

22

2

22

2

2

22

11 1

1

1

1

1 1

1

11

1

1

1

11

1

1

1

11

1

1

1

1 11

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Trade Balance : Expectation(s3) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1"Foreign Trade Balance (FE)" : Expectation(s3) 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Exports-Imports

200 Dollar/Year10 Dollar/Year

150 Dollar/Year5 Dollar/Year

100 Dollar/Year0 Dollar/Year

50 Dollar/Year-5 Dollar/Year

0 Dollar/Year-10 Dollar/Year

3 33

3

3 3

3

33

3

3

3 3

3

3

3

3

3

3

33

2 2 2 2 2 2 2 2 2 22

22

22

22

22

22

1 1 1 1 1 1 11

11

11 1

11

1 11

11

11

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Exports : Expectation(s3) Dollar/Year1 1 1 1 1 1 1 1 1 1 1

Imports : Expectation(s3) Dollar/Year2 2 2 2 2 2 2 2 2 2 2

Trade Balance : Expectation(s3) Dollar/Year3 3 3 3 3 3 3 3

Figure 10.19: Random Expectations and Foreign Investment (S3)

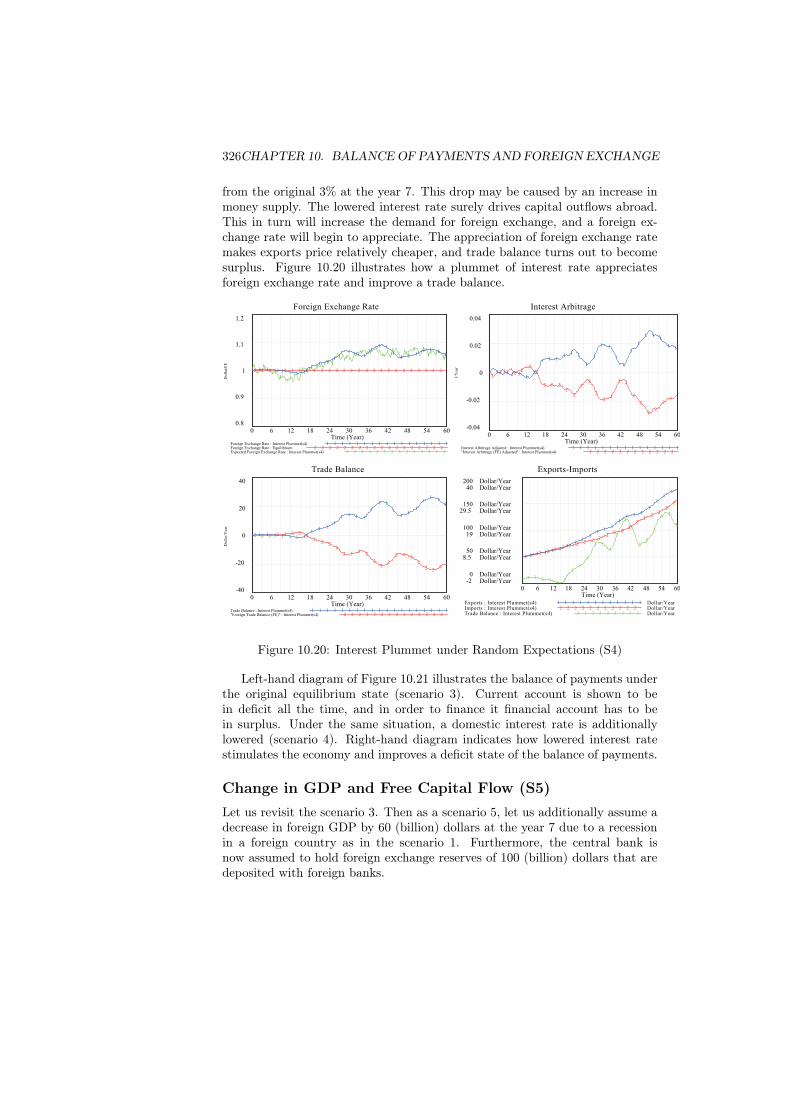

Change in Interest Rate (S4)

Under the situation of the above scenario 3, let us additionally suppose, as sce-nario 4, that a domestic interest rate suddenly plummets by 2% and becomes 1%

326CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

from the original 3% at the year 7. This drop may be caused by an increase inmoney supply. The lowered interest rate surely drives capital outflows abroad.This in turn will increase the demand for foreign exchange, and a foreign ex-change rate will begin to appreciate. The appreciation of foreign exchange ratemakes exports price relatively cheaper, and trade balance turns out to becomesurplus. Figure 10.20 illustrates how a plummet of interest rate appreciatesforeign exchange rate and improve a trade balance.

Foreign Exchange Rate

1.2

1.1

1

0.9

0.8

33

33

3

33 3 3

3 3

3 33 3 3 3

3 3 3 33

33 3

3

2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 21 1 1 1 1 1 1 11

1 11

1 11 1

11 1

11 1 1

1 1 11

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/FE

Foreign Exchange Rate : Interest Plummet(s4) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Foreign Exchange Rate : Equilibrium 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Expected Foreign Exchange Rate : Interest Plummet(s4) 3 3 3 3 3 3 3 3 3 3 3 3 3 3

Interest Arbitrage

0.04

0.02

0

-0.02

-0.04

22 2 2

22

2

2 2 22

2

22

2

22

2 2

2

2

22

22

1 1 11 1

11

1 1 11 1 1

1

1

1 1

1

1

1

1

1 11

1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

1/Y

ear

Interest Arbitrage Adjusted : Interest Plummet(s4) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1"Interest Arbitrage (FE) Adjusted" : Interest Plummet(s4) 2 2 2 2 2 2 2 2 2 2 2 2

Trade Balance

40

20

0

-20

-40

2 2 2 2 2 2 22

22 2

2

2 22

2

22

2

2 22

22 2

2

1 1 1 1 1 1 1 11

1 11

1 1 1 1

1

1 1

11

11

11 1

1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Trade Balance : Interest Plummet(s4) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1"Foreign Trade Balance (FE)" : Interest Plummet(s4) 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Exports-Imports

200 Dollar/Year40 Dollar/Year

150 Dollar/Year29.5 Dollar/Year

100 Dollar/Year19 Dollar/Year

50 Dollar/Year8.5 Dollar/Year

0 Dollar/Year-2 Dollar/Year

3 3 3 33

3

33

3

3 33

3

3

3

33

3

33

3

2 2 2 2 2 2 2 2 2 2 22

2 22

22

22

22

1 1 1 1 1 11

11

11

11

11 1 1

1

11

1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Exports : Interest Plummet(s4) Dollar/Year1 1 1 1 1 1 1 1 1 1 1 1Imports : Interest Plummet(s4) Dollar/Year2 2 2 2 2 2 2 2 2 2 2Trade Balance : Interest Plummet(s4) Dollar/Year3 3 3 3 3 3 3 3 3

Figure 10.20: Interest Plummet under Random Expectations (S4)

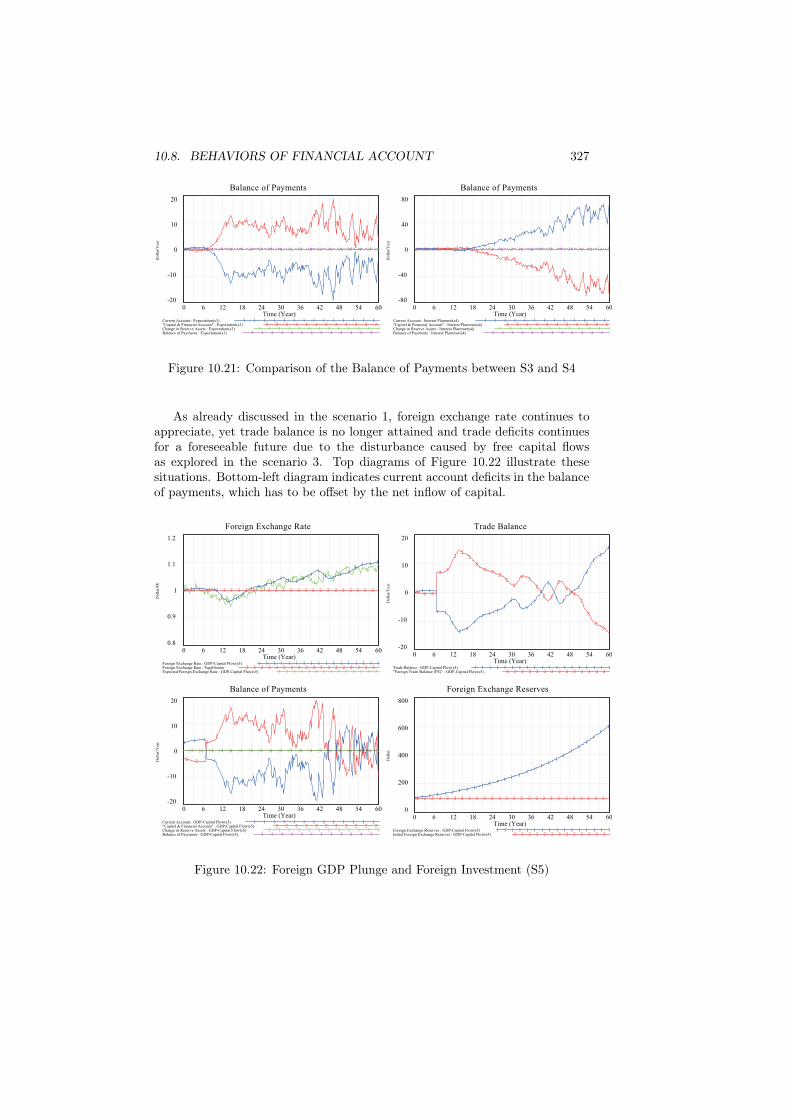

Left-hand diagram of Figure 10.21 illustrates the balance of payments underthe original equilibrium state (scenario 3). Current account is shown to bein deficit all the time, and in order to finance it financial account has to bein surplus. Under the same situation, a domestic interest rate is additionallylowered (scenario 4). Right-hand diagram indicates how lowered interest ratestimulates the economy and improves a deficit state of the balance of payments.

Change in GDP and Free Capital Flow (S5)Let us revisit the scenario 3. Then as a scenario 5, let us additionally assume adecrease in foreign GDP by 60 (billion) dollars at the year 7 due to a recessionin a foreign country as in the scenario 1. Furthermore, the central bank isnow assumed to hold foreign exchange reserves of 100 (billion) dollars that aredeposited with foreign banks.

10.8. BEHAVIORS OF FINANCIAL ACCOUNT 327

Balance of Payments

20

10

0

-10

-20

4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 43 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 32 2 2

2

2 22

22

22

22

2

2 2

2

2

2

2

1 1 1

1

1 1 1 1 11

1

11

1 1

1

11

1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Current Account : Expectation(s3) 1 1 1 1 1 1 1 1 1 1 1 1 1 1"Capital & Financial Account" : Expectation(s3) 2 2 2 2 2 2 2 2 2 2 2 2Change in Reserve Assets : Expectation(s3) 3 3 3 3 3 3 3 3 3 3 3 3 3Balance of Payments : Expectation(s3) 4 4 4 4 4 4 4 4 4 4 4 4 4

Balance of Payments

80

40

0

-40

-80

4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 43 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 32 2 2 2 2 22

22 2

22 2

2

2 2

22

22

1 1 1 1 1 11 1 1

1 1

1 11

1 1

11

1

1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Current Account : Interest Plummet(s4) 1 1 1 1 1 1 1 1 1 1 1 1 1"Capital & Financial Account" : Interest Plummet(s4) 2 2 2 2 2 2 2 2 2 2 2Change in Reserve Assets : Interest Plummet(s4) 3 3 3 3 3 3 3 3 3 3 3 3Balance of Payments : Interest Plummet(s4) 4 4 4 4 4 4 4 4 4 4 4 4

Figure 10.21: Comparison of the Balance of Payments between S3 and S4

As already discussed in the scenario 1, foreign exchange rate continues toappreciate, yet trade balance is no longer attained and trade deficits continuesfor a foreseeable future due to the disturbance caused by free capital flowsas explored in the scenario 3. Top diagrams of Figure 10.22 illustrate thesesituations. Bottom-left diagram indicates current account deficits in the balanceof payments, which has to be offset by the net inflow of capital.

Foreign Exchange Rate

1.2

1.1

1

0.9

0.8

33

33

3 3 3 33

3 3

33

33 3 3

33

33

33 3

3 3

2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 21 1 1 1 1

11

11

1 1 11

1 1 11

11

1 11 1

11 1 1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/FE

Foreign Exchange Rate : GDP-Capital Flow(s5) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Foreign Exchange Rate : Equilibrium 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Expected Foreign Exchange Rate : GDP-Capital Flow(s5) 3 3 3 3 3 3 3 3 3 3 3 3 3 3

Trade Balance

20

10

0

-10

-20

2 2 2

22

22

2

22 2

22

2

2 2

2

2 2

2

22

2

2

22

1 1 1

1 1

1

11

1

11

11

11

1

1

1

1

11

11

1

11

1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Trade Balance : GDP-Capital Flow(s5) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1"Foreign Trade Balance (FE)" : GDP-Capital Flow(s5) 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Balance of Payments

20

10

0

-10

-20

4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 4 43 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3

2 2

22

22

2

2

2

2

2

2

2

2

22

22

2

211 1

1

11 1 1 1

1

1

1

1

1

1

1

1

1

1

1

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

/Yea

r

Current Account : GDP-Capital Flow(s5) 1 1 1 1 1 1 1 1 1 1 1 1 1"Capital & Financial Account" : GDP-Capital Flow(s5) 2 2 2 2 2 2 2 2 2 2 2Change in Reserve Assets : GDP-Capital Flow(s5) 3 3 3 3 3 3 3 3 3 3 3 3Balance of Payments : GDP-Capital Flow(s5) 4 4 4 4 4 4 4 4 4 4 4 4

Foreign Exchange Reserves

800

600

400

200

0

2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 21 1 1 1 1 1 1 1 1 1 1 1 1 11

11

11

11

11

11

11

0 6 12 18 24 30 36 42 48 54 60Time (Year)

Do

llar

Foreign Exchange Reserves : GDP-Capital Flow(s5) 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Initial Foreign Exchange Reserves : GDP-Capital Flow(s5) 2 2 2 2 2 2 2 2 2 2 2 2 2

Figure 10.22: Foreign GDP Plunge and Foreign Investment (S5)

328CHAPTER 10. BALANCE OF PAYMENTS AND FOREIGN EXCHANGE

Bottom-right diagram shows that foreign exchange reserves by the centralbank continues to grow at a rate of the foreign interest rate of 3 %. From awell-known principle of a doubling time of exponential growth, the reserves keepdoubling approximately every 23 years.

10.9 Foreign Exchange Intervention

Official Intervention and Default (S6)

In the scenario 5 above, our macroeconomy continues to suffer from a continualdepreciation of domestic currency (or an appreciation of foreign exchange rate),and deficits in trade and accordingly in current account. Surely, such a criticalmacroeconomic situation in a competitive international economic environmentcannot be left uncontrolled. To prevent such an economic crisis let us introduce,as scenario 6, an official intervention to the foreign exchange market; specifically,the central bank (and government) begins to sell foreign exchange in order toreduce foreign exchange rate, say, to 1.02 dollars per FE; that is, by 2 % of theoriginal equilibrium exchange rate.