Embed Size (px)

Citation preview

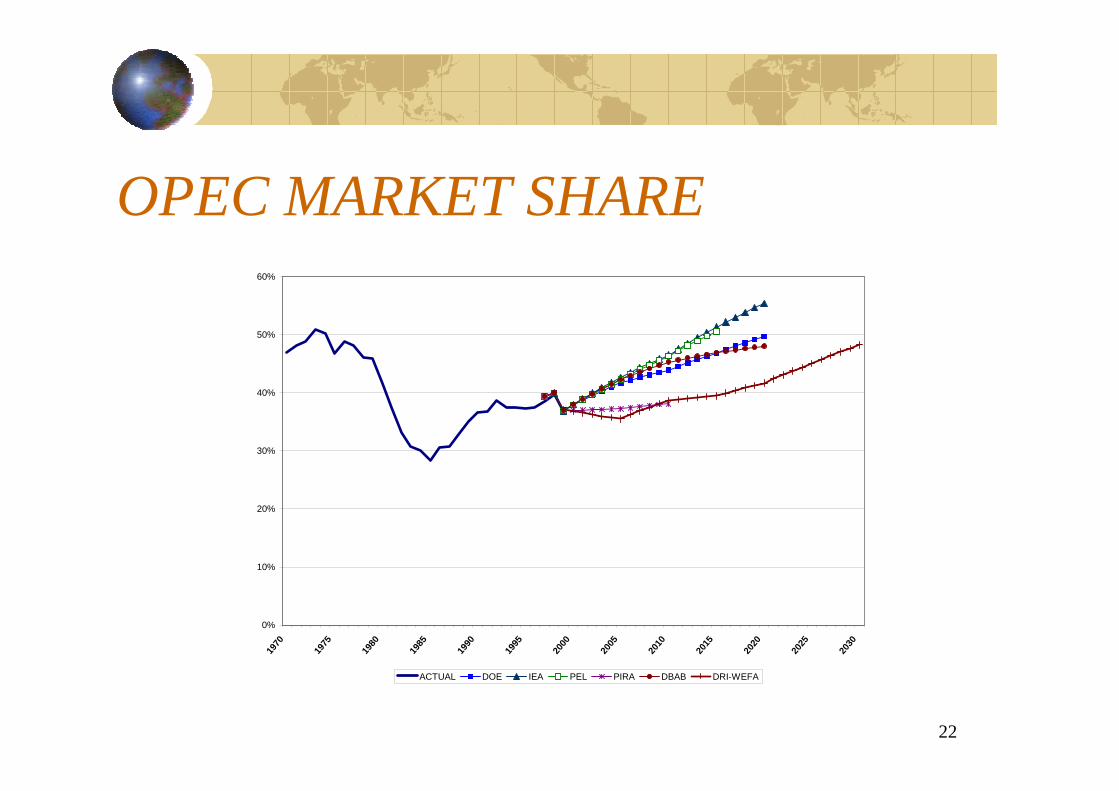

22

OPEC MARKET SHARE

0%

10%

20%

30%

40%

50%

60%19

70

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

ACTUAL DOE IEA PEL PIRA DBAB DRI-WEFA

23

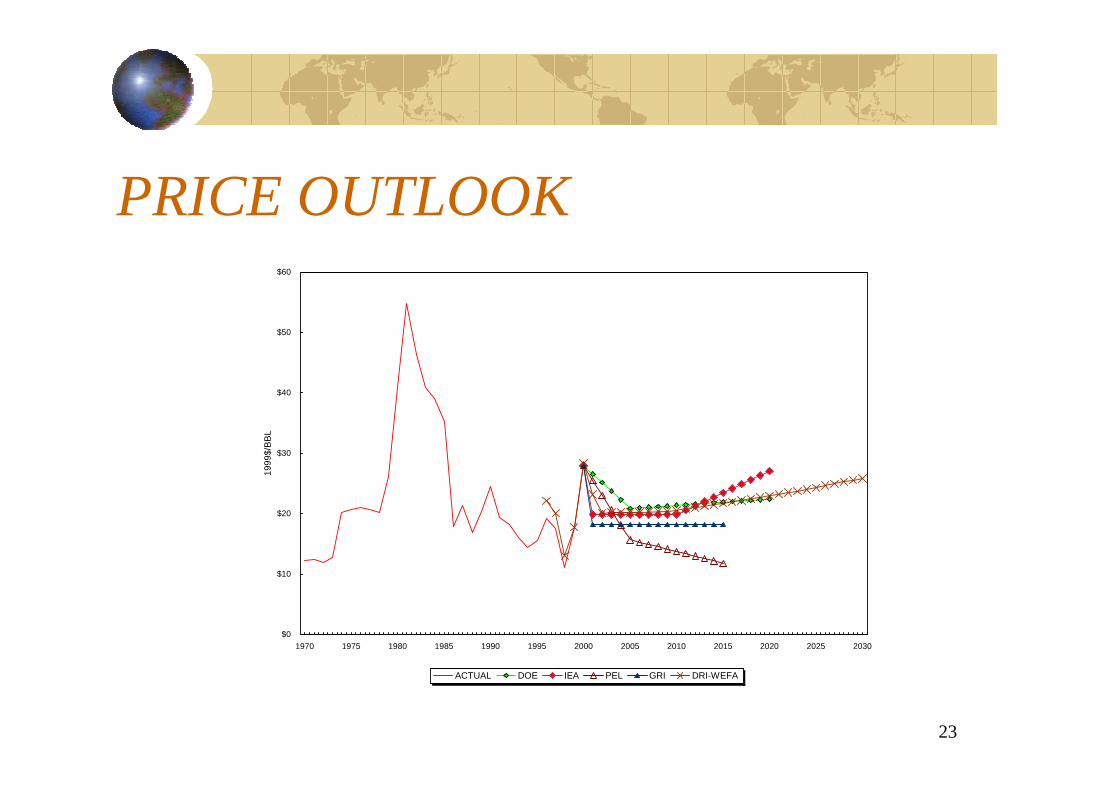

PRICE OUTLOOK

$0

$10

$20

$30

$40

$50

$60

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

1999

$/BB

L

ACTUAL DOE IEA PEL GRI DRI-WEFA

24

OPEC MARKET SHAREDEMAND LEVEL

MACROECONOMY• LEVEL OF GROWTH• POTENTIAL FOR NEW SHOCKS

NON-OPEC SUPPLY• PRICE/MNOC INVESTMENT• DEEPWATER, FSU• GTL, TAR SANDS

OPEC INVESTMENTPOLITICAL REGIME (VENEZUELA OR ALGERIA?)

• APPLIES TO NON-OPEC TOO

25

IMPORTANCE OF POLITICS“…there is no guarantee that the current free-market orientation of economic ideology will not swing back towards the left and greater governmental interference in markets or ownership of industry….Also, though, continuing economic problems due to international debt, the recession, bank failures, etc., may cause...policymakers in many developing countries to abandon efforts at market reform.” Lynch 1991

26

SHORT-TERM MARKET OUTLOOK

FEARS OF TIGHTENING LATE IN 2002GOOD OPEC DISCIPLINEECONOMIC RECOVERY (?)

POSSIBLE NEW COLLAPSE?VENEZUELA, ALGERIA, NIGERIA CHEATINGRUSSIA, OTHER NON-OPEC SOARINGPRICE IMPACT ON DEMAND

27

USABLE COMMERCIAL INVENTORIES

6

8

10

12

14

16

18Ja

n-85

Jan-

86

Jan-

87

Jan-

88

Jan-

89

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

DA

YS S

UPP

LY

Monthly 12-Mo. Avg.

28

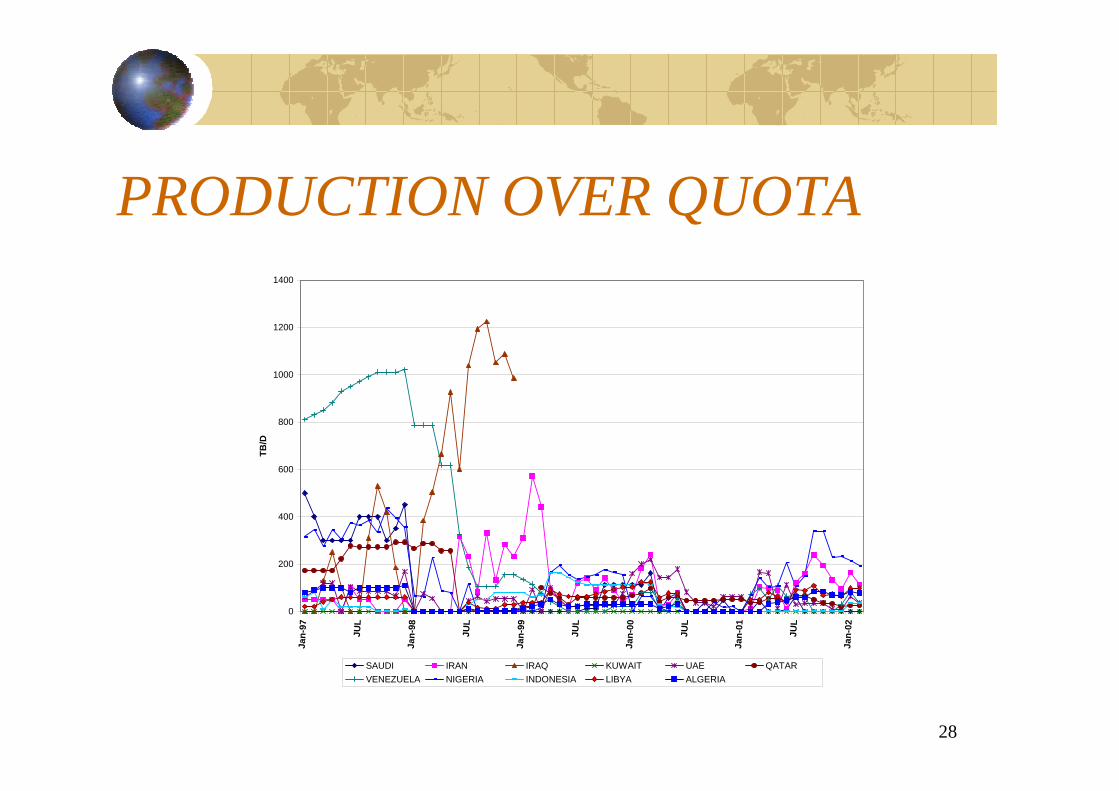

PRODUCTION OVER QUOTA

0

200

400

600

800

1000

1200

1400

Jan-

97

JUL

Jan-

98

JUL

Jan-

99

JUL

Jan-

00

JUL

Jan-

01

JUL

Jan-

02

TB/D

SAUDI IRAN IRAQ KUWAIT UAE QATARVENEZUELA NIGERIA INDONESIA LIBYA ALGERIA

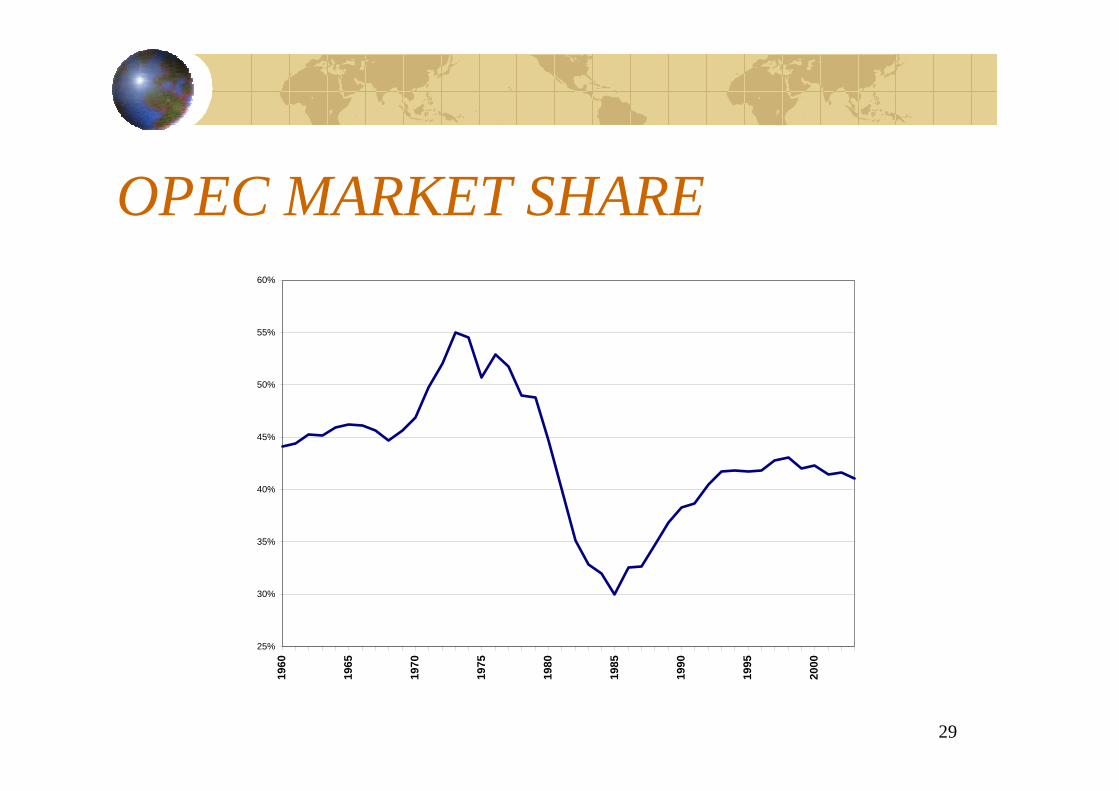

29

OPEC MARKET SHARE

25%

30%

35%

40%

45%

50%

55%

60%19

60

1965

1970

1975

1980

1985

1990

1995

2000

30

PAST AS PROLOGUE?VENEZUELAN BEHAVIOR UNDER GIUSTI

2000

2200

2400

2600

2800

3000

3200

3400

3600

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

TB/D

PRODUCTION QUOTA

31

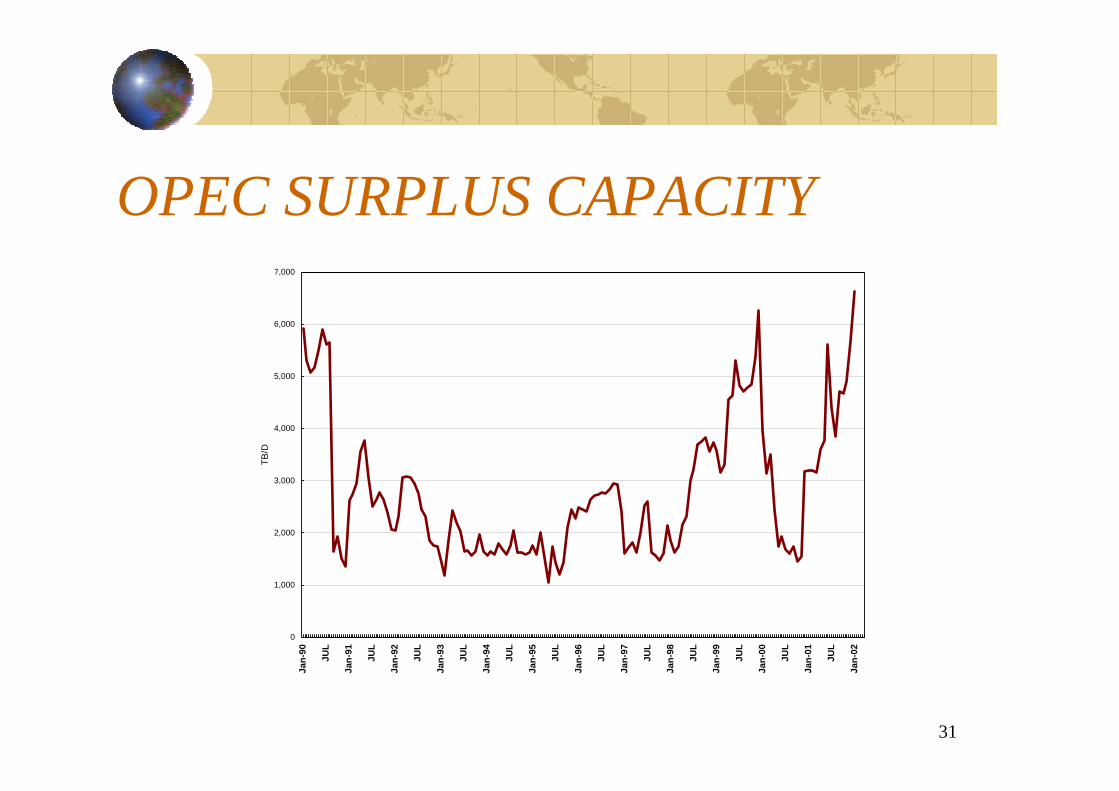

OPEC SURPLUS CAPACITY

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Jan-

90

JUL

Jan-

91

JUL

Jan-

92

JUL

Jan-

93

JUL

Jan-

94

JUL

Jan-

95

JUL

Jan-

96

JUL

Jan-

97

JUL

Jan-

98

JUL

Jan-

99

JUL

Jan-

00

JUL

Jan-

01

JUL

Jan-

02

TB/D

32

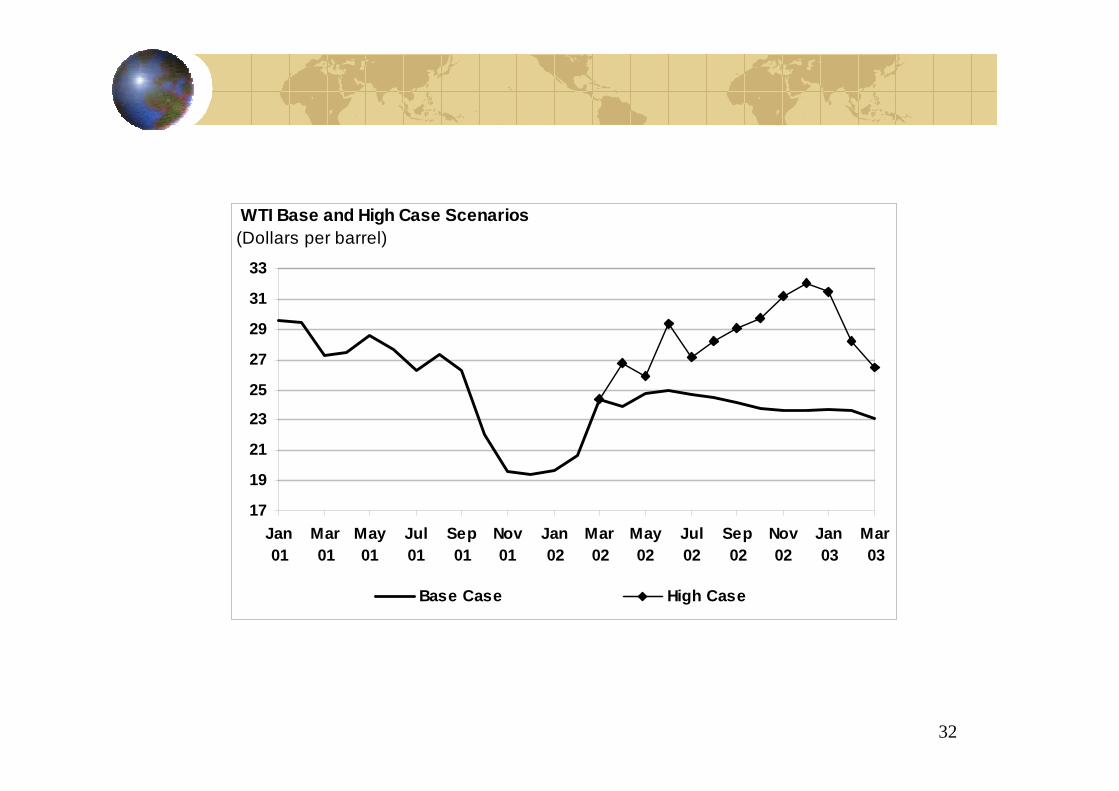

17

19

21

23

25

27

29

31

33

Jan01

Mar01

May01

Jul01

Sep01

Nov01

Jan02

Mar02

May02

Jul02

Sep02

Nov02

Jan03

Mar03

Base Case High Case

WTI Base and High Case Scenarios(Dollars per barrel)

33

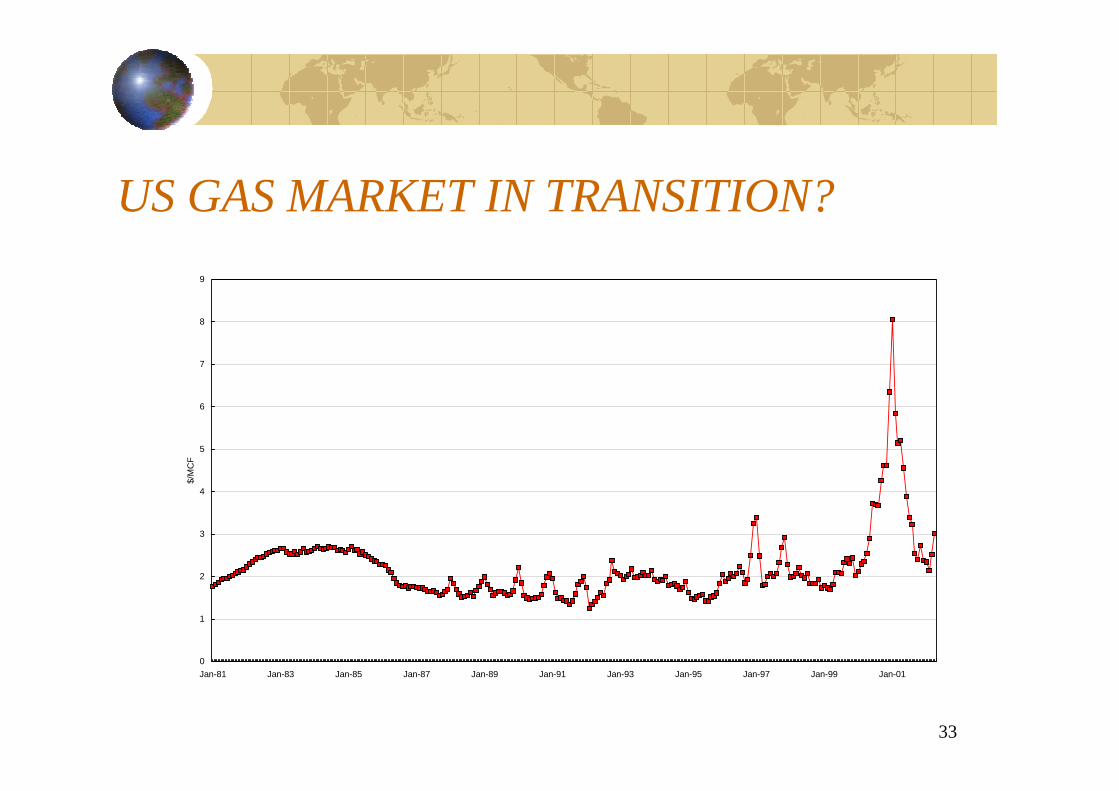

US GAS MARKET IN TRANSITION?

0

1

2

3

4

5

6

7

8

9

Jan-81 Jan-83 Jan-85 Jan-87 Jan-89 Jan-91 Jan-93 Jan-95 Jan-97 Jan-99 Jan-01

$/M

CF

34

US Decline Rates Have Increased

The evidence of serious supply constraints have been strong since 1996.

0%

5%

10%

15%

20%

25%

30%

14% 15% 17% 17% 18% 20% 23% 23% 26% 27% 28%

90 91 92 93 94 95 97 98 99 00 01

US Deliverability and Utilization

40

4244

4648

50

5254

5658

60

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Bcfd

70%

75%

80%

85%

90%

95%

100%

Deliverability

Deliverability Utilization

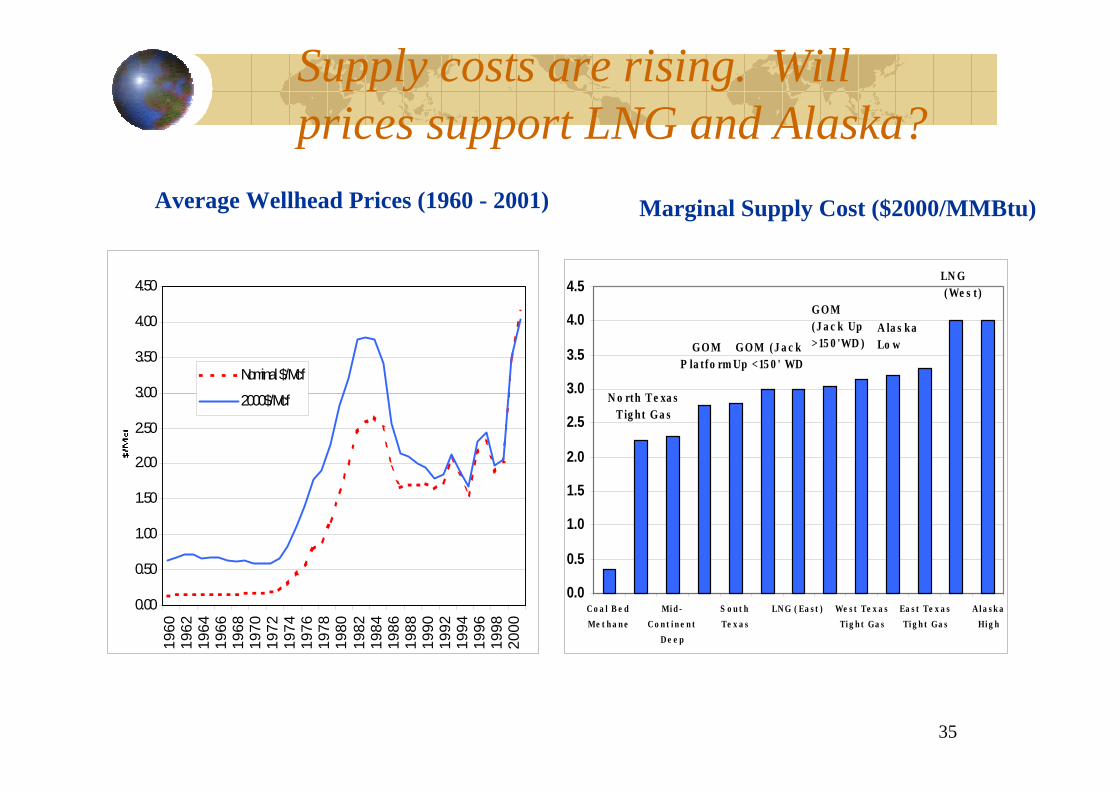

35

Supply costs are rising. Will prices support LNG and Alaska?

Average Wellhead Prices (1960 - 2001) Marginal Supply Cost ($2000/MMBtu)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Nominal $/Mcf

2000$/Mcf

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

C o a l B e dMe t h a n e

Mi d -C o n t i n e n t

D e e p

S o u t hTe x a s

LN G ( Ea s t ) We s t Te x a sTi g h t Ga s

Ea s t Te x a sTi g h t Ga s

A l a s k aHi g h

N o rth Te xa s Tig ht Ga s

GOM P la t fo rm

GOM (J a c kUp <15 0 ' WD

GOM (J a c k Up >15 0 'WD )

A la s ka Lo w

LN G (We s t )

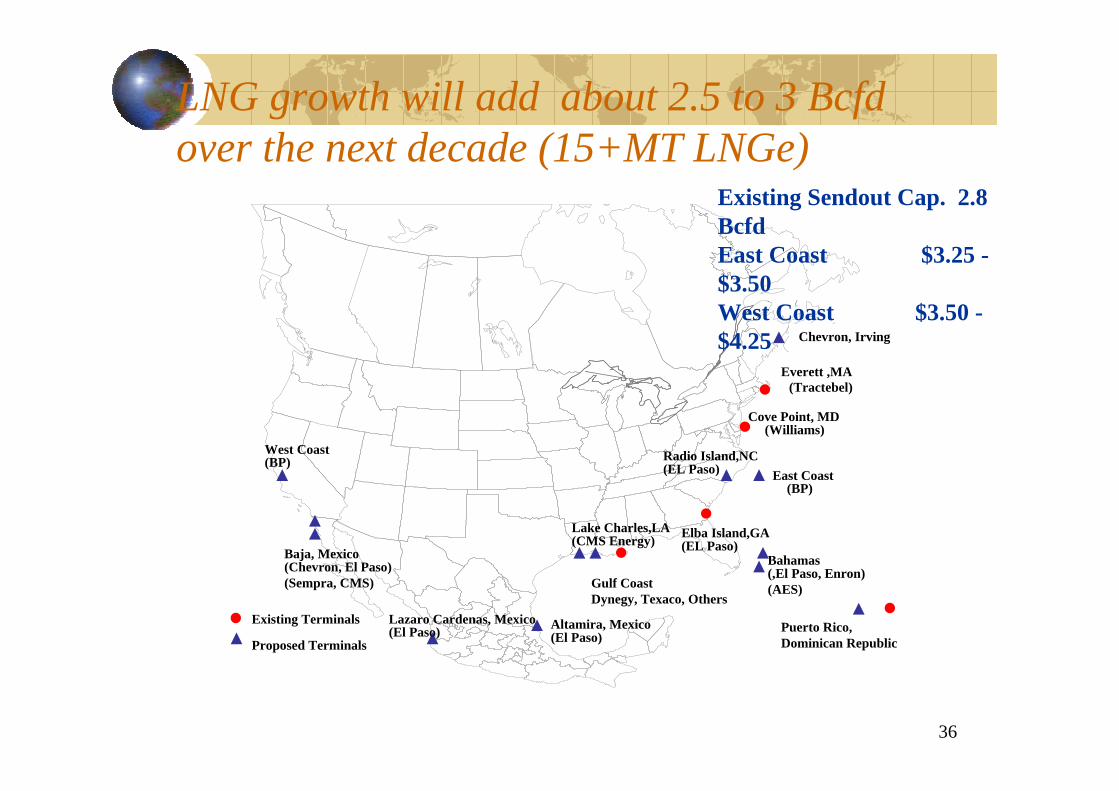

36

LNG growth will add about 2.5 to 3 Bcfdover the next decade (15+MT LNGe)

Chevron, Irving

Everett ,MA(Tractebel)

Cove Point, MD(Williams)

East Coast(BP)

Radio Island,NC(EL Paso)

Elba Island,GA(EL Paso)

Bahamas(,El Paso, Enron)(AES)

Lake Charles,LA(CMS Energy)

Altamira, Mexico(El Paso)

Lazaro Cardenas, Mexico(El Paso)

West Coast(BP)

Baja, Mexico(Chevron, El Paso)(Sempra, CMS)

Existing Terminals

Proposed TerminalsPuerto Rico, Dominican Republic

Gulf CoastDynegy, Texaco, Others

Existing Sendout Cap. 2.8BcfdEast Coast $3.25 -$3.50West Coast $3.50 -$4.25

37

Demand side response will limit gas price increases

Delivered Gas Prices that Make Coal Competitive

Conventional Coal $3.80 delivered.

New Source Review

Refurbished coal capacity is competitive at $2.70 per MMBtudelivered (10% capacity increase).

Transport reactor is being tested using oil cracking technology to gasify coal.

3.80

3.20

2.70

2.00

2.20

2.40

2.60

2.80

3.00

3.20

3.40

3.60

3.80

4.00

ConventionalCoal

TransportReactor

RefurbishedCoal

$/M

MBt

u

38

US Natural Gas Use in Ammonia Production Decreases With High Gas Prices in 2000 and 2001 (Bcf/day)

0

0.5

1

1.5

2

1994 1995 1996 1997 1998 1999 2000 2001

39

Gas consumption for power generationis a major source of growth and uncertainty

Gas consumption for power generation is the major source of growth (60% of total).Since gas is the marginal fuel, slight changes in generation from other fuels or changes in the electric power growth rate has a major impact.Projected growth rates for power generation range from 1.8% to 2.8% per year.Scenarios range from optimism to pessimism about coal, nuclear, and power growth rates.

Annual Growth 2000-10

0

500

1000

1500

2000

Shakeout Reference Crunch

MMcf

d

Power Total

2010 Gas Consumpton

24

25

26

27

28

29

30

Shakeout Reference Crunch

Trill

ion

Btu

40

Both supply and demand side uncertainties create a great deal of uncertainty

Prices in 2010 ($1.90 to $3.65 per MMBtu)Need to develop deep wells offshore and onshore, LNG terminals will have to be builtGrowth in supply depends on new discoveriesDemand response

Coal fired plants are likely to play a larger role than many projectIncreased efficiency in industrial sector

Environmental Regulations

$2000/MMBtu2000

(Actual) 2005 2010 2015 2020

AEO 3.69 2.48 2.67 2.81 3.11AGA 3.69 2.39 2.46 2.55DRI*WEFA 3.69 2.91 2.95 3.07 3.16GRI 3.69 2.12 2.09 2.00NPC (Ref) 3.69 2.64 3.13 3.67NPC (High) 3.69 2.90 3.65 4.37NPC (Low) 3.69 2.26 2.28 3.07NRCan* 3.69 2.12 2.12

Average 2.53 2.94 3.08 2.80Deflator 1.00 1.14 1.26 1.41 1.57* Forecast were developed in 1999.

Average Wellhead Prices

41

CONCLUSION (1):THINGS HAVE CHANGED

MARKETS TIGHTER THAN BEFORECAPACITY UTILIZATION VERY HIGH COMPARED TO 1980S, EARLY 1990S

OPEC MORE COHESIVEPOLITICAL TREND REVERBERATING TOWARDS INTERVENTION IN MARKETS

42

CONCLUSION (2):THE MORE THEY ARE THE SAME

PRICE EFFECTS STILL POWERFULAND UNDERESTIMATED

GOVERNMENTS NOT AS BAD AS BEFOREUNCERTAINTIES ENORMOUS

POLICY, PRICE, TECHNOLOGY, EVEN GDP GROWTH

ANALYSIS IS THE ANSWER (RELATIVELY)