Embed Size (px)

Citation preview

Ontario Budget Announcement - 2015

ONTARIO BUDGET ANNOUNCEMENT - 2015

On April 23, 2015, Ontario’s Minister of Finance, Charles Sousa, presented his third budget entitled Building Ontario Up. The budget builds on the theme of last year’s budget and includes more spending and debt. Although there are no tax cuts, the government held the line on any further personal or corporate income tax increases.

HIGHLIGHTS:

Infrastructure will receive the largest portion of spending in the budget through:

• The investment of more than $130 billion over 10 years in public infrastructure, such as roads, bridges and transit

• More than $11 billion over 10 years in capital grants to school boards, to be used to build new schools in high growth areas, and improve the condition of existing structures

• $900 million over 10 years to maintain existing post secondary facilities

• More than $11 billion in hospital capital grants over 10 years

Minister Sousa also announced the government will continue to sell down provincial assets such as real estate holdings, including its pending sale of the LCBO’s head office lands and reducing ownership of Crown utility Hydro One. The province is working on plans to make Crown utility Hydro One public, starting with an initial offering of 15% of the common shares of Hydro One, followed with additional share sales over time, totaling up to 60%.

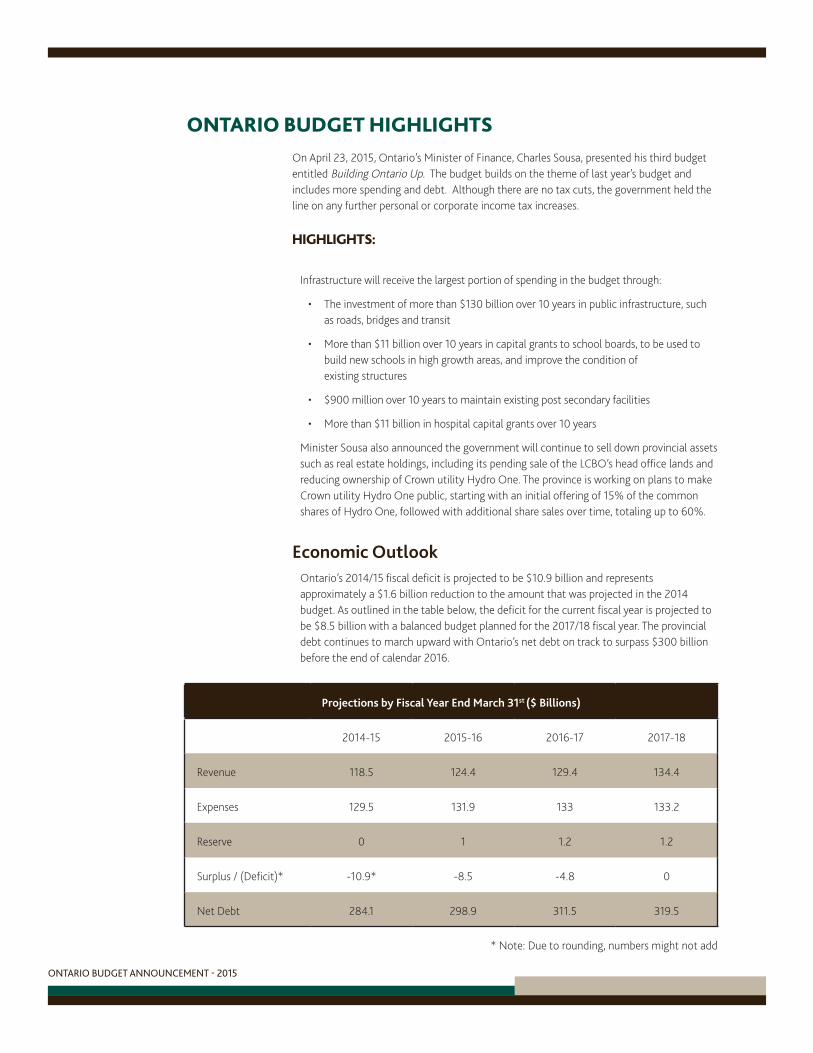

Economic OutlookOntario’s 2014/15 fiscal deficit is projected to be $10.9 billion and represents approximately a $1.6 billion reduction to the amount that was projected in the 2014 budget. As outlined in the table below, the deficit for the current fiscal year is projected to be $8.5 billion with a balanced budget planned for the 2017/18 fiscal year. The provincial debt continues to march upward with Ontario’s net debt on track to surpass $300 billion before the end of calendar 2016.

ONTARIO BUDGET HIGHLIGHTS

Projections by Fiscal Year End March 31st ($ Billions)

2014-15 2015-16 2016-17 2017-18

Revenue 118.5 124.4 129.4 134.4

Expenses 129.5 131.9 133 133.2

Reserve 0 1 1.2 1.2

Surplus / (Deficit)* -10.9* -8.5 -4.8 0

Net Debt 284.1 298.9 311.5 319.5

* Note: Due to rounding, numbers might not add

ONTARIO BUDGET ANNOUNCEMENT - 2015

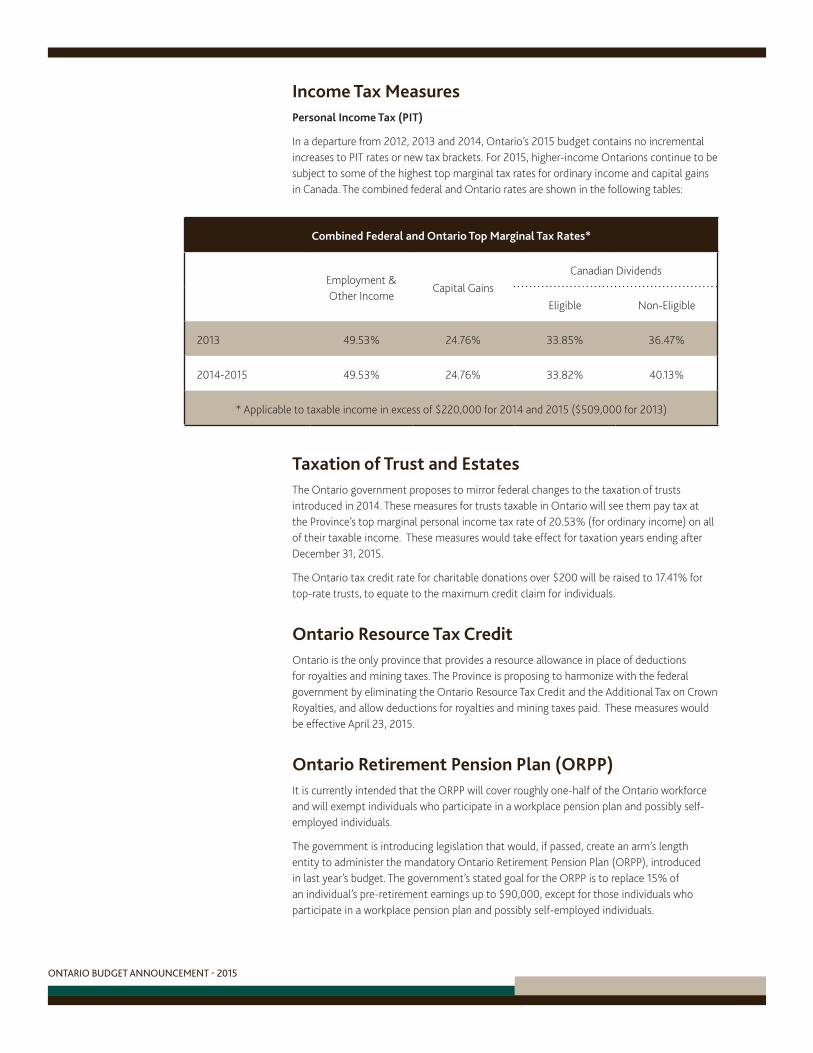

Income Tax MeasuresPersonal Income Tax (PIT)

In a departure from 2012, 2013 and 2014, Ontario’s 2015 budget contains no incremental increases to PIT rates or new tax brackets. For 2015, higher-income Ontarions continue to be subject to some of the highest top marginal tax rates for ordinary income and capital gains in Canada. The combined federal and Ontario rates are shown in the following tables:

Combined Federal and Ontario Top Marginal Tax Rates*

Employment & Other Income

Capital GainsCanadian Dividends

Eligible Non-Eligible

2013 49.53% 24.76% 33.85% 36.47%

2014-2015 49.53% 24.76% 33.82% 40.13%

* Applicable to taxable income in excess of $220,000 for 2014 and 2015 ($509,000 for 2013)

Taxation of Trust and EstatesThe Ontario government proposes to mirror federal changes to the taxation of trusts introduced in 2014. These measures for trusts taxable in Ontario will see them pay tax at the Province’s top marginal personal income tax rate of 20.53% (for ordinary income) on all of their taxable income. These measures would take effect for taxation years ending after December 31, 2015.

The Ontario tax credit rate for charitable donations over $200 will be raised to 17.41% for top-rate trusts, to equate to the maximum credit claim for individuals.

Ontario Resource Tax CreditOntario is the only province that provides a resource allowance in place of deductions for royalties and mining taxes. The Province is proposing to harmonize with the federal government by eliminating the Ontario Resource Tax Credit and the Additional Tax on Crown Royalties, and allow deductions for royalties and mining taxes paid. These measures would be effective April 23, 2015.

Ontario Retirement Pension Plan (ORPP)It is currently intended that the ORPP will cover roughly one-half of the Ontario workforce and will exempt individuals who participate in a workplace pension plan and possibly self-employed individuals.

The government is introducing legislation that would, if passed, create an arm’s length entity to administer the mandatory Ontario Retirement Pension Plan (ORPP), introduced in last year’s budget. The government’s stated goal for the ORPP is to replace 15% of an individual’s pre-retirement earnings up to $90,000, except for those individuals who participate in a workplace pension plan and possibly self-employed individuals.

ONTARIO BUDGET ANNOUNCEMENT - 2015

The government has committed to introduce the ORPP by January 1, 2017. Proposed contribution rates would be the same for employers and employees, with a maximum combined rate of 3.8%. This would mean an additional annual payroll tax total of up to $1,710 each.

For both employers and employees, such ORPP contributions will be in addition to existing Canada Pension Plan and Employment Insurance premiums. Taking into account the existing 1.95% Ontario Employer Health Tax (EHT) levy, Ontario employers could be subject to provincial-specific payroll taxes equal to 3.85% of remuneration. It is yet to be determined how Ontario employers will cope with the increased payroll tax burden.

Before January 2017, the Province will introduce legislation that would finalize the details of the plan.

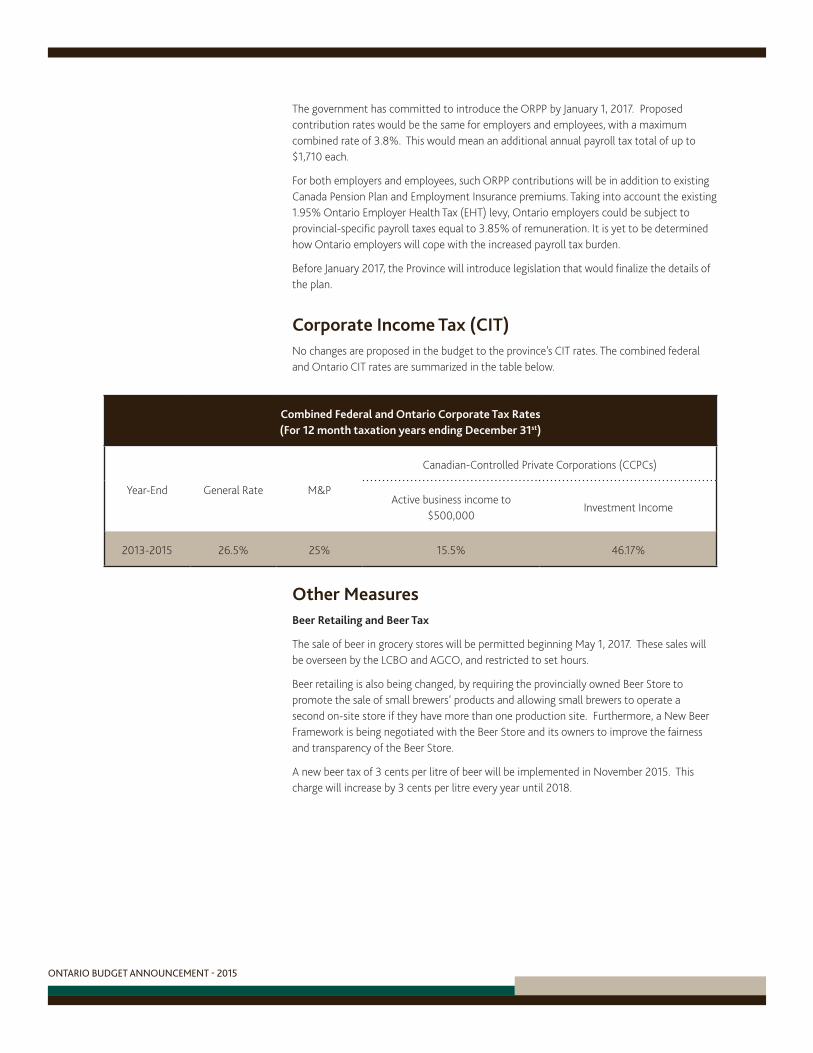

Corporate Income Tax (CIT)No changes are proposed in the budget to the province’s CIT rates. The combined federal and Ontario CIT rates are summarized in the table below.

Combined Federal and Ontario Corporate Tax Rates(For 12 month taxation years ending December 31st)

Year-End General Rate M&P

Canadian-Controlled Private Corporations (CCPCs)

Active business income to $500,000

Investment Income

2013-2015 26.5% 25% 15.5% 46.17%

Other MeasuresBeer Retailing and Beer Tax

The sale of beer in grocery stores will be permitted beginning May 1, 2017. These sales will be overseen by the LCBO and AGCO, and restricted to set hours.

Beer retailing is also being changed, by requiring the provincially owned Beer Store to promote the sale of small brewers’ products and allowing small brewers to operate a second on-site store if they have more than one production site. Furthermore, a New Beer Framework is being negotiated with the Beer Store and its owners to improve the fairness and transparency of the Beer Store.

A new beer tax of 3 cents per litre of beer will be implemented in November 2015. This charge will increase by 3 cents per litre every year until 2018.

ONTARIO BUDGET ANNOUNCEMENT - 2015

Enhanced Audit Activity for BusinessesThe province will, together with the Canada Revenue Agency (CRA), continue enhanced audit activities to address underground economic activities, aggressive corporate tax avoidance, EHT, Land Transfer Tax and Tobacco Tax.

Ontario will also consult with businesses on technology-based approaches to stop electronic sales suppression at point-of-sale terminals. Furthermore, it will be illegal to use, manufacture, or distribute electronic sales suppression technologies.

How MNP Can Help: In the event that audit activity is initiated by the tax authorities, our team of experienced advisors can provide assistance to minimize your tax exposure and correspond with the CRA or other authorities to achieve the optimal outcome.

Corporate Tax Credit ChangesApprenticeship Training Tax Credit

• General tax credit rate decreased from 35% to 25% and rate for small businesses with salaries under $400,000 per year decreased from 45% to 30%

• Annual maximum credit per apprentice decreased from $10,000 to $5,000

• Eligibility period decreased from first 48 months to first 36 months of an apprenticeship program

• Effective for apprentices who commenced an apprenticeship program after April 23, 2015

Ontario Interactive Digital Media Tax Credit

• Tax credit restricted to entertainment products and educational products for children under the age of 12, with certain products specifically excluded

• Product certification requirements changed to focus on labour costs

• Effective for expenditures incurred after April 23, 2015

Ontario Production Services Tax Credit

• This refundable tax credit decreased from 25% to 21.5%

• The credit and expenditures also restricted based on salaries and contracts with non-arm’s length parties

• Effective after April 23, 2015

Ontario Computer Animation and Special Effects Tax Credit

• This refundable tax credit decreased from 20% to 18%, effective after April 23, 2015

ONTARIO BUDGET ANNOUNCEMENT - 2015

Ontario Film and Television Tax Credit

• Government equity investments will continue not to be taxed as other forms of government assistance, in contrast with the Federal amendment of this credit

Ontario Sound Recording Tax Credit

• This tax credit eliminated for eligible sound recordings commenced after April 23, 2015

How MNP Can Help: Although the benefit of these credits have been significantly reduced (or eliminated in some cases) in this budget, our tax experts can still help your businesses maximize any eligible tax claims under these or other provincial programs.

Municipal Electricity Utilities

• Transfer tax on the fair market value of electricity assets sold to the private sector reduced from 33% to 22%

• The Electricity Act, 1998, amended to prevent avoidance of payments in lieu of taxes (“PILs”) through dispositions of partnership interests made directly or indirectly to a person or partnership who is not subject to PILs.

ONTARIO BUDGET ANNOUNCEMENT - 2015

MNP is a leading national accounting, tax and business consulting firm in Canada. We proudly serve and respond to the needs of our clients in the public, private and not-for-profit sectors. Through partner-led engagements, we provide a collaborative, cost-effective approach to doing business and personalized strategies to help organizations succeed across the country and around the world.

ABOUT MNP

Regional Tax Contacts

Name Region Phone Number

Don Carson GTA 416.263.6930

Glenn Willis GTA 416.515.3850

Eddy Burello GTA 647.943.4081

Allen Church GTA-West 416.641.4941

Alex Makuz GTA-West 416.641.4944

Rachelle Siksna GTA-West 416.641.4956

Rosario Suppa GTA-West 416.641.4948

Dave Thompson GTA-West 416.641.4935

Bryan Walters Hamilton / Burlington 289.293.2314

Kal Ruprai Indirect Tax - Toronto 416.596.1711

Tim Bloos Int'l Tax - Toronto 416.515.3888

John Durland Int'l Tax - Toronto 416.263.6921

Frank Kacsandi Int'l Tax - Toronto 416.515.3818

Andrew Lam Int'l Tax - Toronto 416.263.6989

Kevyn Nightingale Int'l Tax - Toronto 416.515.3881

Mark Pearlman Int'l Tax - Toronto 416.260.3510

Michael Shumate Int'l Tax - Toronto 416.260.3509

Steve Blazino NW Ontario 807.623.2141

Gavin Miranda Ottawa 613.691.4224

Bill Mitchell SW Ontario 519.772.2968

Tim Edworthy SW Ontario 519.772.7498

Martin Hengeveld SW Ontario 519.772.7479

Linda Quinn SW Ontario 519.772.7483

David Webb SW Ontario 519.772.7464

Praxity AISBL is a global alliance of independent firms. Organised as an international not-for-profit entity under Belgium law, Praxity has its executive office in Epsom. Praxity – Global Alliance Limited is a not-for-profit company registered in England and Wales, limited by guarantee, and has its registered office in England. As an Alliance, Praxity does not practice the profession of public accountancy or provide audit, tax, consulting or other professional services of any type to third parties. The Alliance does not constitute a joint venture, partnership or network between participating firms. Because the Alliance firms are independent, Praxity does not guarantee the services or the quality of services provided by participating firms.

Visit us at MNPtax.ca