Embed Size (px)

Citation preview

ONESOURCE Indirect Tax

CAMILO MARTINEZ – VAT BUSINESS CONSULTANT

ONESOURCE® Indirect Tax DeterminationWebinar – Brazil – March 21, 2013

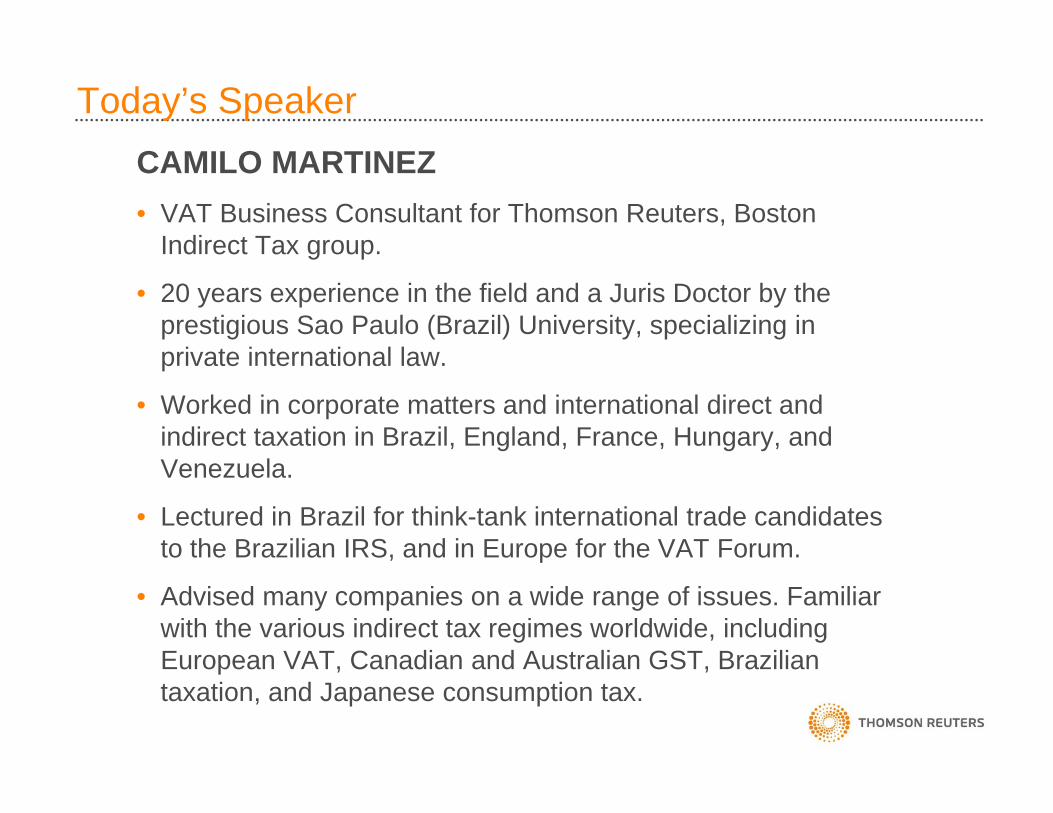

Today’s SpeakerCAMILO MARTINEZ• VAT Business Consultant for Thomson Reuters, Boston

Indirect Tax group.

• 20 years experience in the field and a Juris Doctor by the prestigious Sao Paulo (Brazil) University, specializing in private international law.

• Worked in corporate matters and international direct and indirect taxation in Brazil, England, France, Hungary, and Venezuela.

• Lectured in Brazil for think-tank international trade candidates to the Brazilian IRS, and in Europe for the VAT Forum.

• Advised many companies on a wide range of issues. Familiar with the various indirect tax regimes worldwide, including European VAT, Canadian and Australian GST, Brazilian taxation, and Japanese consumption tax.

General outlook for BrazilOpportunities:• Collectively, US-headquartered companies are the

largest foreign investors in Brazil

• Economic development followed political stability

• Market of approx. 200 million people

Challenges:• Heavily regulated economy

• Foreign exchange controls

• Slow judiciary process

• Organized labor

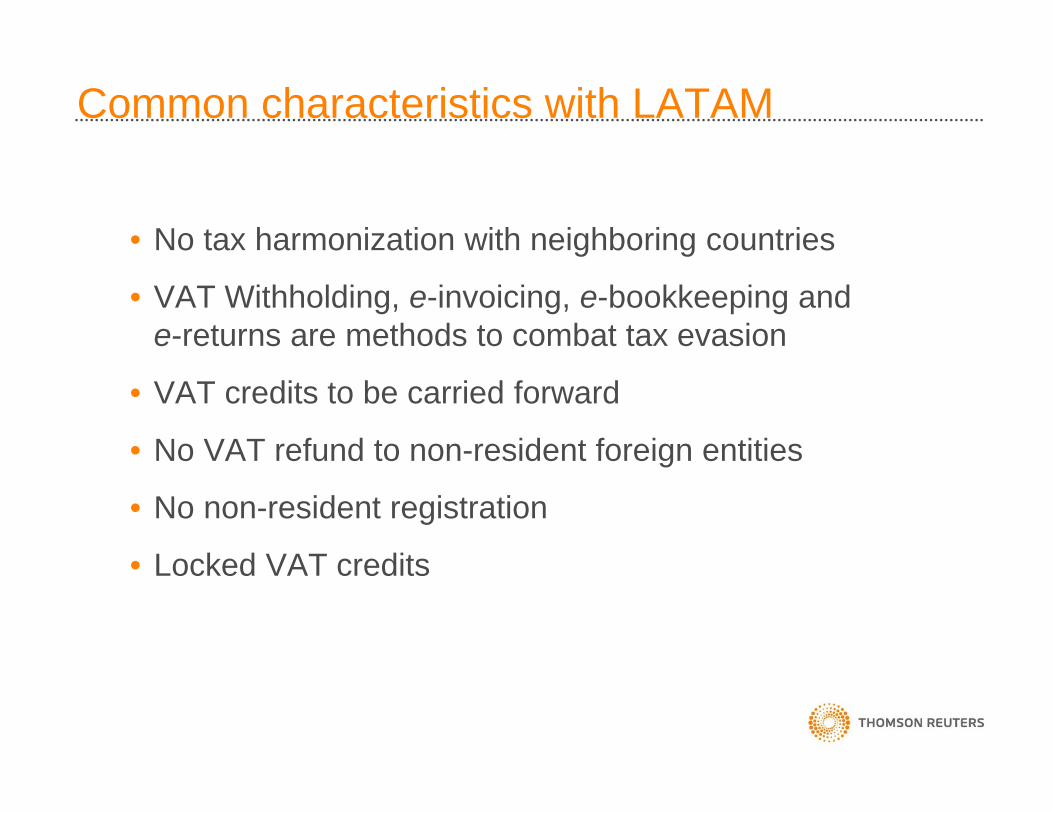

Common characteristics with LATAM

• No tax harmonization with neighboring countries

• VAT Withholding, e-invoicing, e-bookkeeping and e-returns are methods to combat tax evasion

• VAT credits to be carried forward

• No VAT refund to non-resident foreign entities

• No non-resident registration

• Locked VAT credits

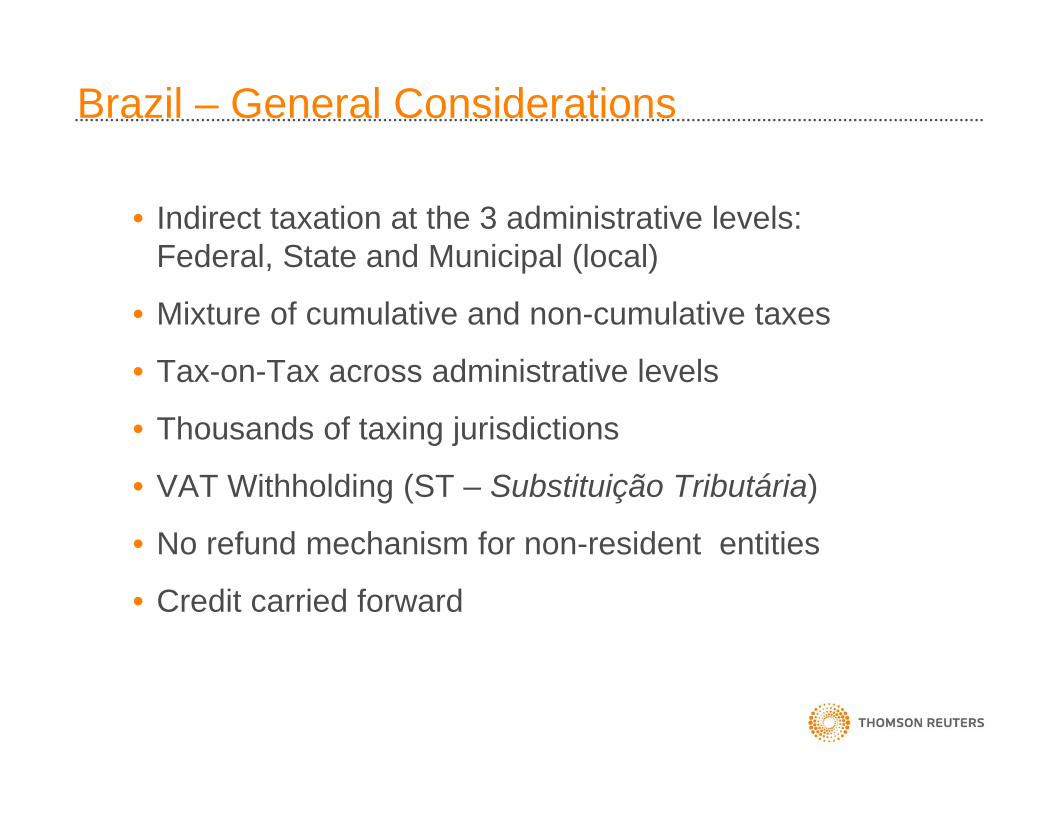

Brazil – General Considerations

• Indirect taxation at the 3 administrative levels: Federal, State and Municipal (local)

• Mixture of cumulative and non-cumulative taxes

• Tax-on-Tax across administrative levels

• Thousands of taxing jurisdictions

• VAT Withholding (ST – Substituição Tributária)

• No refund mechanism for non-resident entities

• Credit carried forward

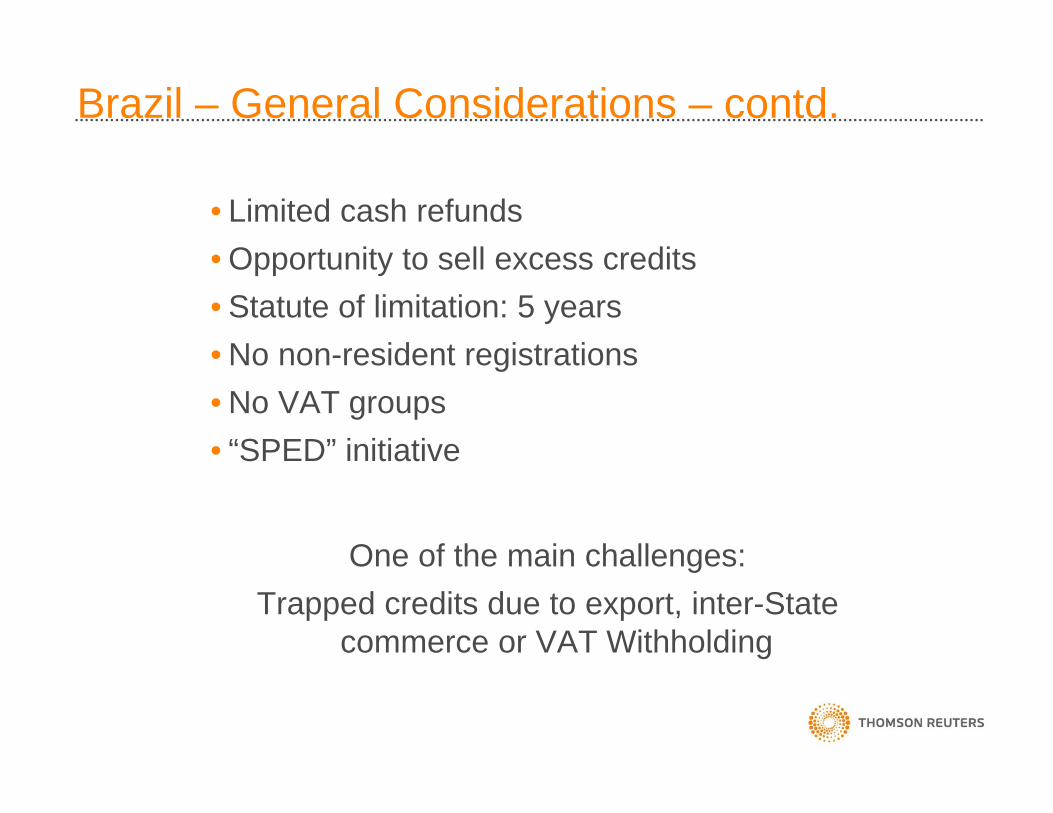

Brazil – General Considerations – contd.

• Limited cash refunds• Opportunity to sell excess credits• Statute of limitation: 5 years• No non-resident registrations• No VAT groups• “SPED” initiative

One of the main challenges:Trapped credits due to export, inter-State

commerce or VAT Withholding

S

EW

N

BRAZIL

Tax Description

IPI(Imposto sobreProdutosIndustrializados)

• Non‐cumulative tax on manufacturing and importation of goods

PIS (Programa de Integração Social)

• Gross‐receipt tax• Cumulative or non‐Cumulative

COFINS (Contribuição para o Financiamento da Seguridade Social)

• Gross‐receipt tax• Cumulative or non‐Cumulative

BR Federal Taxes in Determination1 Jurisdiction

BRAZILTax Description

ICMS(Imposto sobre a Circulação de Mercadorias e Serviços)

• Non‐cumulative tax on goods and selected services

• Telecommunications,Utilities, inter‐State and inter‐Municipal transportation

ICMS‐ST(Imposto sobre a Circulação de Mercadorias e Serviços –SubstituiçãoTributária)

• Non‐cumulative tax on goods• VAT withtholding perception• Arbitrary profit marginsproduct and/or industry driven

• Bilateral or multilateral State agreements

BR State Taxes in Determination26 + 1 Jurisdictions

BRAZILTax Description

ISS(Imposto sobreServiços)

• Cumulative tax on most services

• Thousands of tax jurisdictions

• Harmonization by Federal Law

BR Municipal Tax in Determination5,000+ Jurisdictions

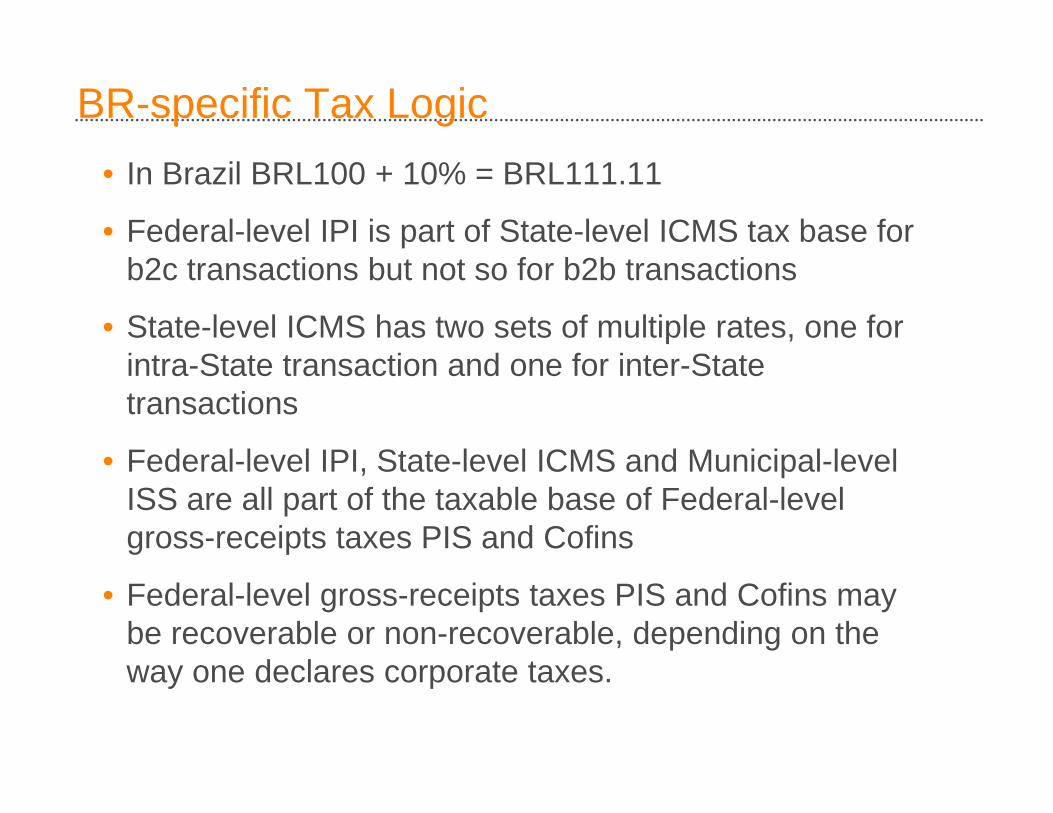

BR-specific Tax Logic• In Brazil BRL100 + 10% = BRL111.11

• Federal-level IPI is part of State-level ICMS tax base for b2c transactions but not so for b2b transactions

• State-level ICMS has two sets of multiple rates, one for intra-State transaction and one for inter-State transactions

• Federal-level IPI, State-level ICMS and Municipal-level ISS are all part of the taxable base of Federal-level gross-receipts taxes PIS and Cofins

• Federal-level gross-receipts taxes PIS and Cofins may be recoverable or non-recoverable, depending on the way one declares corporate taxes.

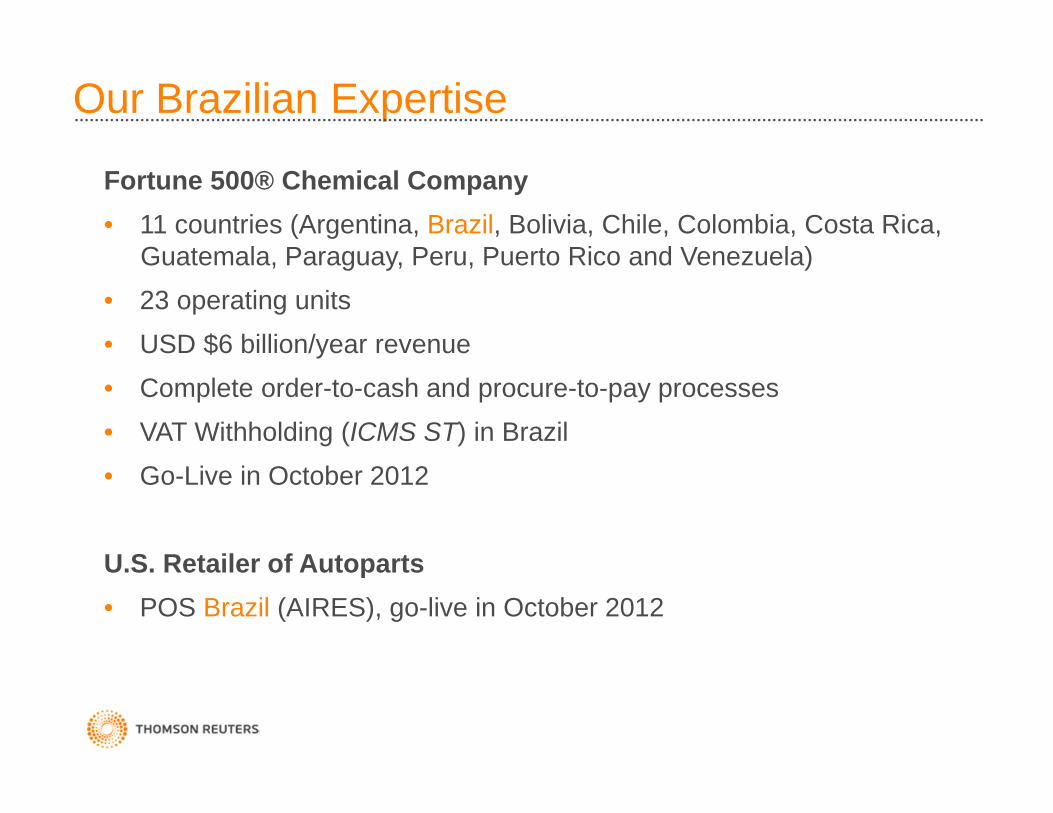

Our Brazilian Expertise

Fortune 500® Chemical Company• 11 countries (Argentina, Brazil, Bolivia, Chile, Colombia, Costa Rica,

Guatemala, Paraguay, Peru, Puerto Rico and Venezuela)• 23 operating units• USD $6 billion/year revenue• Complete order-to-cash and procure-to-pay processes• VAT Withholding (ICMS ST) in Brazil• Go-Live in October 2012

U.S. Retailer of Autoparts• POS Brazil (AIRES), go-live in October 2012

FILENAME CONFIDENTIAL – NOT FOR REDISTRIBUTION 13

Brazil1000+ employees

Santiago, Chile182 employees

Cochabamba, Bolivia

51 employees

Note: Included TRTA-dedicated GGO employees

Brazil and LATAM Employee Base

Mexico City, Mexico

100 employees

Lima, Peru105 employees

Buenos Aires, Argentina263 employees

BRAZIL

LATAM

FILENAME CONFIDENTIAL – NOT FOR REDISTRIBUTION 14

Contact Information

OR

Contact us (888) 885-0206

15