Embed Size (px)

Citation preview

§ CoreNet Capstone, Boston, MA

One Service Provider’s Perspective

What service provider trends do we see?

3

Trends we see

§ Many previously decentralized CRE operations are centralizing

§ CREs consolidating to fewer providers (second generation outsourcing, hybrid sourcing, etc.)

§ “Strategic planning” gaining ground

§ Heightened focus on soft skills – to accompany hard skills

§ Solutions focus

§ Global CRE management models

§ Commoditization potential

What do our customers expectand how are we delivering?

5

The service provider challenge

One off transactions

Single service out-task/outsource

Bundled services outsource

Full serviceoutsource - Domestic

Full servicecontracts - Global

Corporations buy

real estate services in

complex and inconsistent

ways.Service providers

must continually

interpret,

organize around, and

serve multiple -- and

ever-changing --

models

6

CRE

Technology

LeaseAdministration

StrategicPlanning

ProjectManagement

Transactions

Facilities Finance

The silo “double whammy”

ProjectManagement

Transactions

SP 1

SP 2

SP 3

SP 4

7

What Do Customers Expect?

ACCURACYLevel 1

AVAILABILITYLevel 2

PARTNERSHIPLevel 3

ADVICELevel 4

Source: Gallup Organization

8

How We Deliver

AccountManagement

Alliance Director

StrategicEvaluation

Team

? Dedicated? Variable

BrokerageNetwork

? Expert AdvisoryNetwork

? Dedicated? Variable Project

Management Network

? Expert AdvisoryNetwork

? Dedicated? Expert Advisory

Network

National Platform• Account Strategic

Evaluation Team

• Customer Satisfaction

• Best Practices Platform

• Consulting and Expertise Management

• Service Line Centers of Excellence

• Regional Operations Oversight

• IT

• HR

• Accounting

Project Management

Facility Management

CLIENT

StrategicPortfolio Svcs

TransactionManagement

? Dedicated? Variable

Consultants? Subject matter

specialists

9

Strategic Services

Portfolio and AssetSolutions

OrganizationalSolutions Operational Solutions

TCC’s Strategic Solutions Network – Representative Resources

Karen EllzeyDirector, Strategic Services Jennifer Dresback

Justin KowalchukArea Corporate Consultants

External Partners

• Organization StrategyEllzey, RODs, Sales, Other ADs

• Human Resource TransitionZita McLean, HR

• Technology SolutionsHowell, Sockwell

• Process OptimizationEllzey, Wojo, Others

• Portfolio StrategyEhrmann, Lynden, Dresback, Huaco, Zivalich, Holowink, Partners

• Capital MarketsMinter, et al

• Corporate FinanceMark Raggio

• LogisticsTony Kepano, Chainalytics

• Location Strategy/DemographicsKing White

• Economic IncentivesDavid Witcher

• Workplace EvolutionLance Wilken, Robyn Kaiser

• D&I - Various

• BenchmarkingSusan Wojo

• Tax ConsultingKeith McIntosh

• UtilitiesRon Herbst

• Operational ExcellenceWojo, RODs, ADs, others

• Portfolio and Lease SvcsWilkes, Chriss

• Strategic SourcingVince Dunavant

• Environmental ServicesNeil Holderidge

• Rick SchuknechtData Centers, Ops and Maintenance

Area/Regional/Sales Resources

What is the impact of Six Sigmaon the service provisioning?

“Voice of the Customer” Management Model

12

Sample Initiatives• Portfolio leases• Financial

structures• Site/campus

strategies• Relocation• Geographic risk

diversification• Space standards• Utilization/

AO strategies

Business SegmentInterviews

DEFINE the Customer, their Critical to Quality (CTQ) issues, and the Core Business Process involved.

DEFINE MEASURE ANALYZE IMPROVE CONTROL

MEASURE theperformance of theportfolio • Demand• Supply• Cost• Demographics• OtherBenchmark• Internal• External

ANALYZE the data collected and process map to determine root causes of defects and opportunities for improvement.

IMPROVE the target process by designing creative solutionsto fix and prevent problems.

CONTROL the improvements to keep the process on the new course.

Adapted from DMAIC Approach, http://www.ge.com/capital/vendor/dmaic.htm

Sample Measures • Demand/supply• Demographics• Occupancy/utilization• Rental rates v.

market• Lease expirations• Costs• Efficiency

(sf/workstation)• Cost/workstation• Vacancy by segment• Annual cost of

vacancy

Key Findings

• Most BU are well below the 90% target

• 25 percent leases are set to expire by 2008. • Four percent of leases represent 65 percent of

lease commitment

Six Sigma Thinking

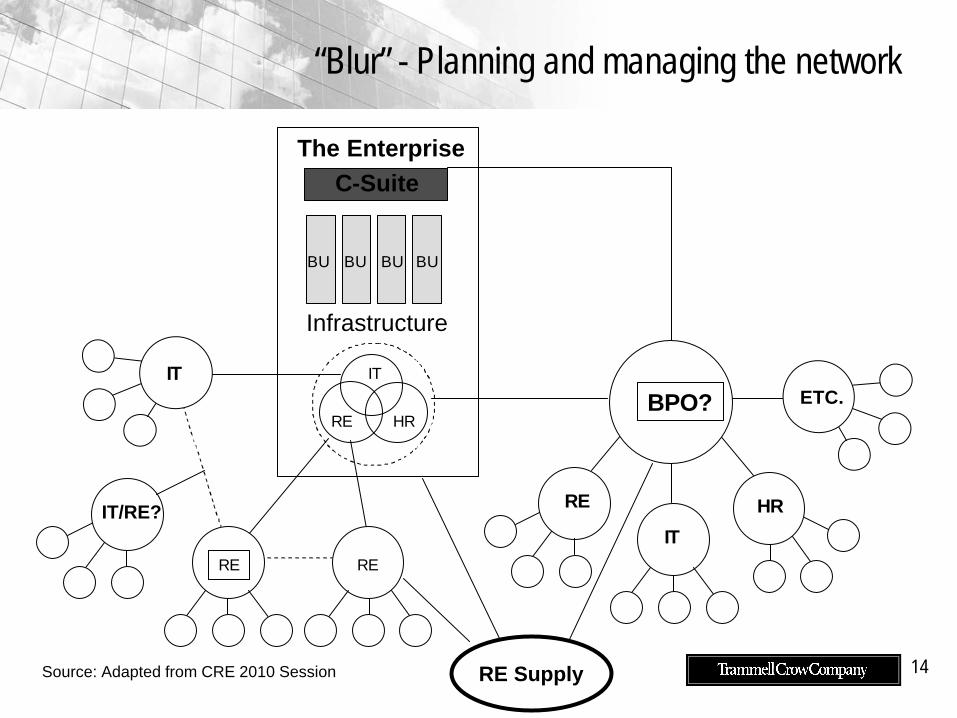

What about the “network” ofservice providers?

14

Infrastructure

C-Suite

BU BU BU BU

RE HR

IT

IT

RE HR

BPO? ETC.IT

IT/RE?

RE Supply

The Enterprise

RERE

Source: Adapted from CRE 2010 Session

“Blur” - Planning and managing the network

15

Partnering with Other Providers | TCC & JLL Working Together

Collaboration andconsistency• Project planning and

prioritization• Strategic sourcing• Franchise protection• Vacancy reduction• Q & P initiatives

Shared portfolio-wideresources• Energy• Environmental• EIMC• Facility Partner Q&P

initiative leaders• Engineering R&D

Shared KPI goals2002 – No shared goals2003 – 30% shared goals2004 – Approaching 50%

16

Recent Joint Briefing on Alternative Workplace

What leadership skills arenecessary to succeed – and how to prepare?

• Synthesizers

• Strategists

• Communicators

• Relationship builders

• Facilitators

• Problem solvers

• Advisors/consultants

• Integrators

What everyone is looking for…on both sides of the relationship