Embed Size (px)

Citation preview

22nd Annual 22nd Annual Cancer Progress ConferenceCancer Progress Conference

Oncology Market Overview: Barriers, Challenges and Value

• Bill Bagwell, RPh, Senior Vice President, Clinical and Scientific Assessment, Kantar Health

• Rhoda Dunn, Account Director, Market Access, Kantar Health

1

ONCOLOGY MARKET OVERVIEW: BARRIERS, CHALLENGES AND VALUECancer Progress

March 9, 2011

© Copyright 2011 Kantar Health

KRAS

3© Copyright 2011 Kantar Health

EML4-ALKMAGE-3A

PARP

PI3

B-RAF

CD20

IGF-1R

ALK / c-Met

CYP17A1

CMS

4© Copyright 2011 Kantar Health

CERNICE

CT

AHRQ

PCORI

ICER

HEOR

HTA

QALY

Agenda

• Increasing prevalence in cancer offset by economic challenges and increasing competition

• R&D’s contribution to commercial success: Safety, efficacy and pharmacoeconomics

• Nothing in life is free… especially not pricing

5

© Copyright 2011 Kantar Health

INCREASING PREVALENCE IN CANCER OFFSET BY ECONOMIC CHALLENGES AND INCREASING COMPETITION

6

© Copyright 2011 Kantar Health

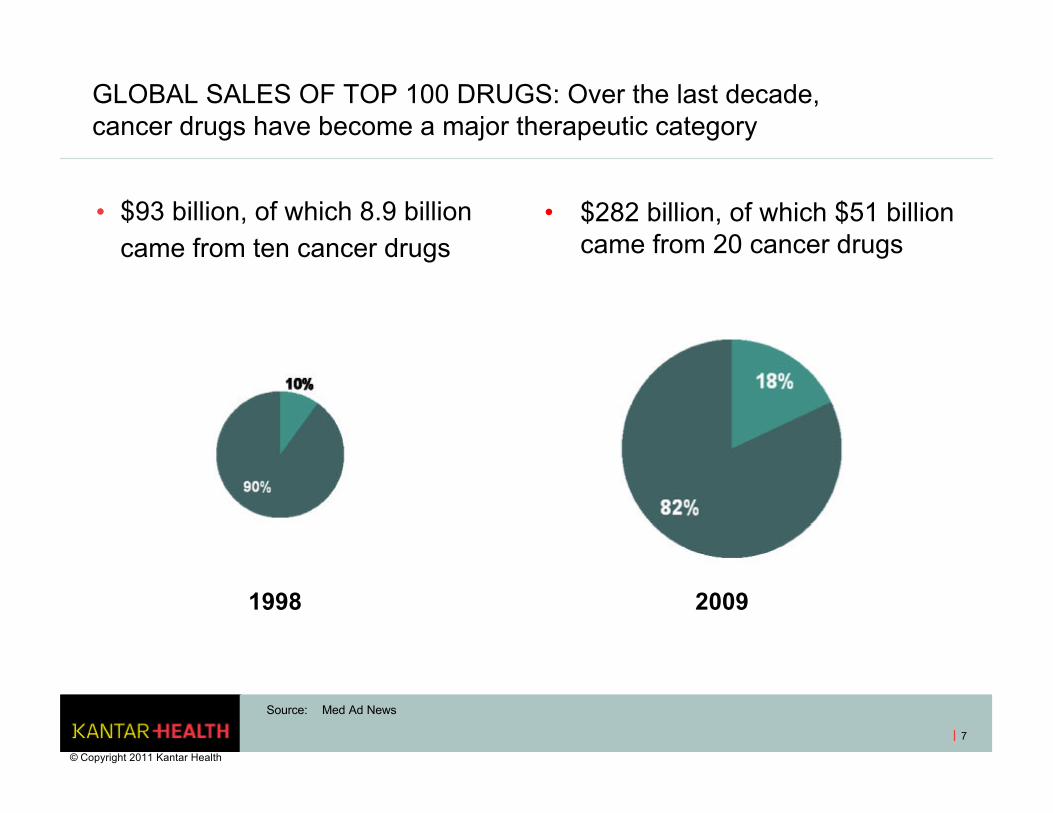

GLOBAL SALES OF TOP 100 DRUGS: Over the last decade, cancer drugs have become a major therapeutic category

7

• $93 billion, of which 8.9 billion came from ten cancer drugs

• $282 billion, of which $51 billion came from 20 cancer drugs

Source: Med Ad News

© Copyright 2011 Kantar Health

1998 2009

REVENUE PER CANCER PATIENT FUELS INNOVATION: But how sustainable is this growth?

8

Tot

al R

xs (

000s

) Ave. R

x Price ($ per R

x)

Note: Total Rx data in $ thousands, average price data $, for Top 10 branded products: Femara, Aromasin, Xeloda, Gleevec, Tarceva, Temodar, Sutent, Sprycel, Tykerb and Avastin

Source: Wolters Kluwer Source® Pharmaceutical Audit, Retail channel, © Copyright 2011 Kantar Health

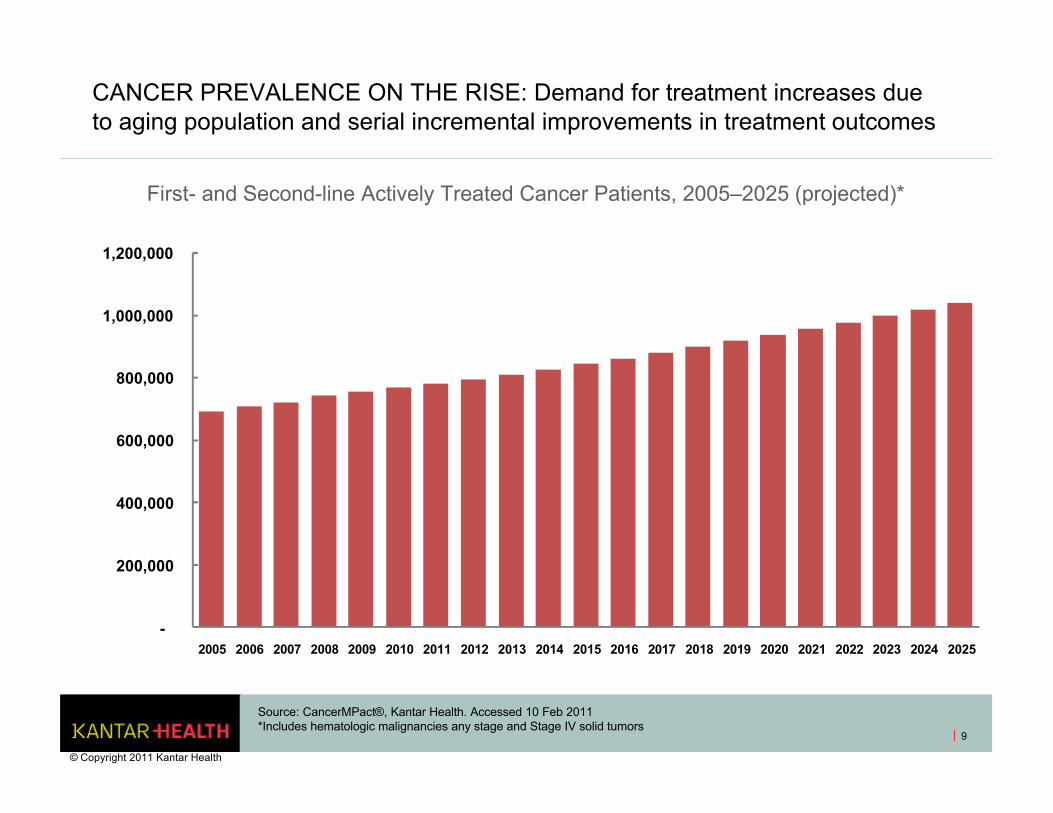

CANCER PREVALENCE ON THE RISE: Demand for treatment increases due to aging population and serial incremental improvements in treatment outcomes

9

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: CancerMPact®, Kantar Health. Accessed 10 Feb 2011*Includes hematologic malignancies any stage and Stage IV solid tumors

First- and Second-line Actively Treated Cancer Patients, 2005–2025 (projected)*

© Copyright 2011 Kantar Health

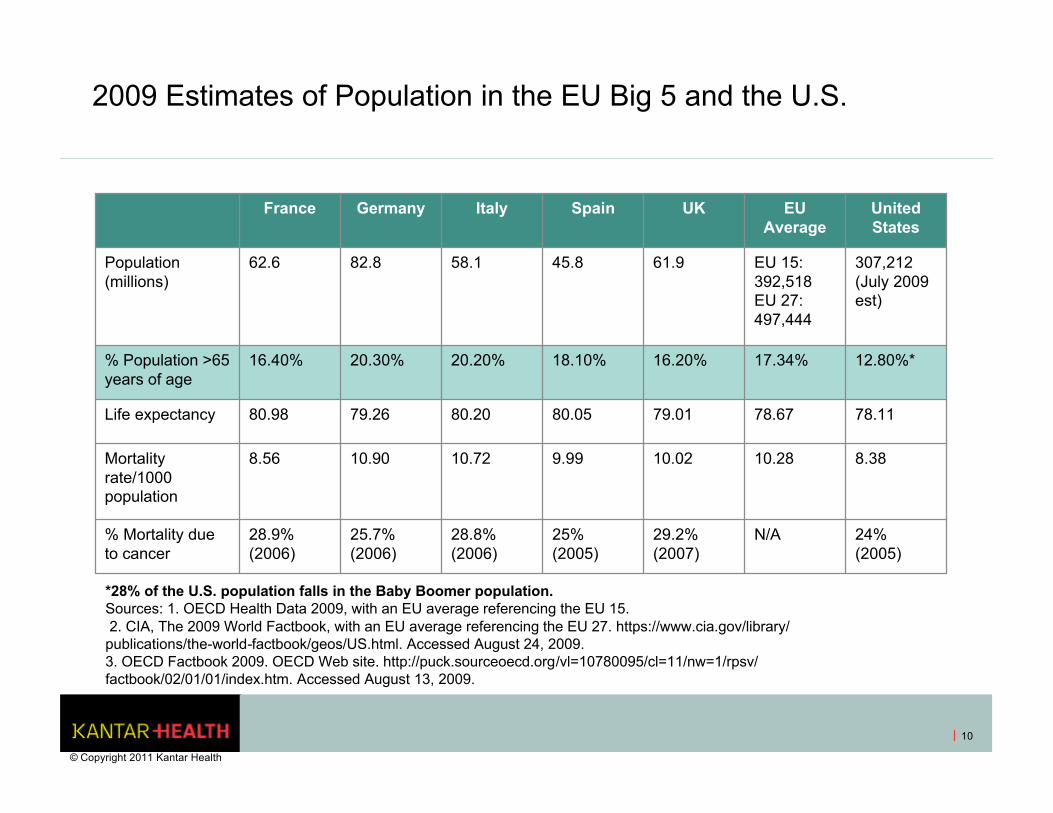

2009 Estimates of Population in the EU Big 5 and the U.S.

France Germany Italy Spain UK EU Average

United States

Population (millions)

62.6 82.8 58.1 45.8 61.9 EU 15: 392,518EU 27: 497,444

307,212 (July 2009 est)

% Population >65 years of age

16.40% 20.30% 20.20% 18.10% 16.20% 17.34% 12.80%*

Life expectancy 80.98 79.26 80.20 80.05 79.01 78.67 78.11

Mortality rate/1000 population

8.56 10.90 10.72 9.99 10.02 10.28 8.38

% Mortality due to cancer

28.9% (2006)

25.7% (2006)

28.8% (2006)

25% (2005)

29.2% (2007)

N/A 24% (2005)

*28% of the U.S. population falls in the Baby Boomer population.Sources: 1. OECD Health Data 2009, with an EU average referencing the EU 15.2. CIA, The 2009 World Factbook, with an EU average referencing the EU 27. https://www.cia.gov/library/

publications/the-world-factbook/geos/US.html. Accessed August 24, 2009. 3. OECD Factbook 2009. OECD Web site. http://puck.sourceoecd.org/vl=10780095/cl=11/nw=1/rpsv/factbook/02/01/01/index.htm. Accessed August 13, 2009.

10

© Copyright 2011 Kantar Health

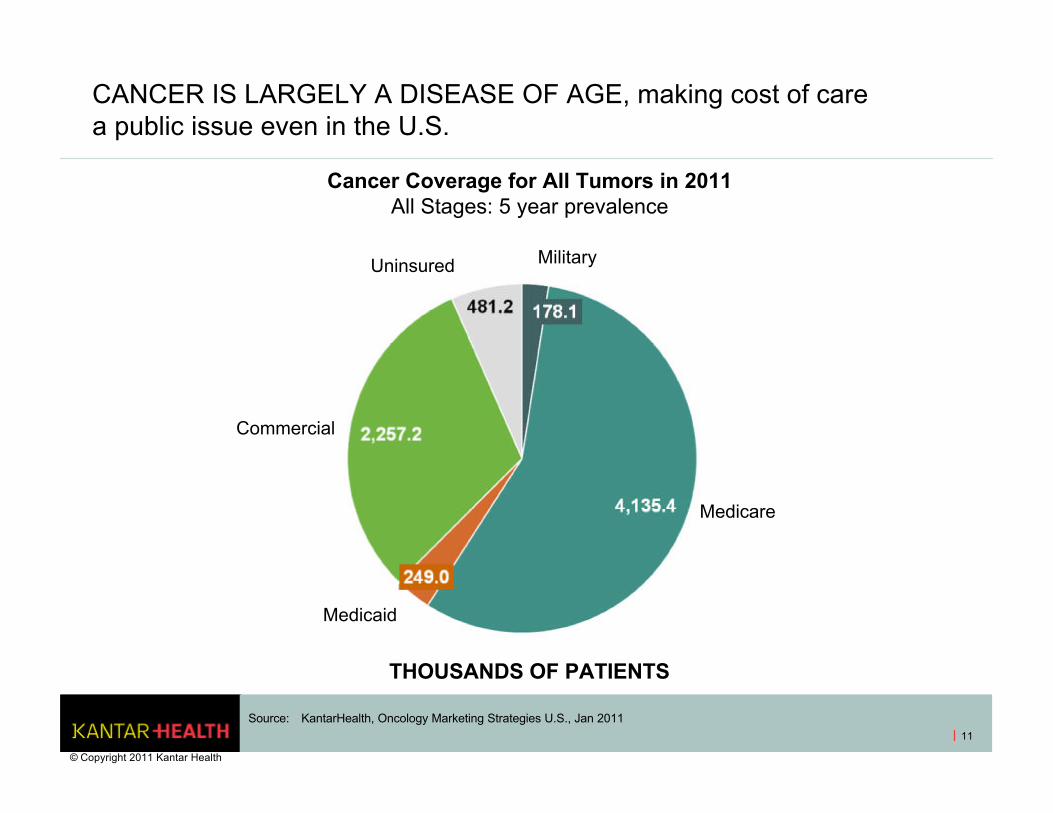

CANCER IS LARGELY A DISEASE OF AGE, making cost of care a public issue even in the U.S.

11

Commercial

Uninsured Military

Medicare

Medicaid

Cancer Coverage for All Tumors in 2011All Stages: 5 year prevalence

Source: KantarHealth, Oncology Marketing Strategies U.S., Jan 2011

© Copyright 2011 Kantar Health

THOUSANDS OF PATIENTS

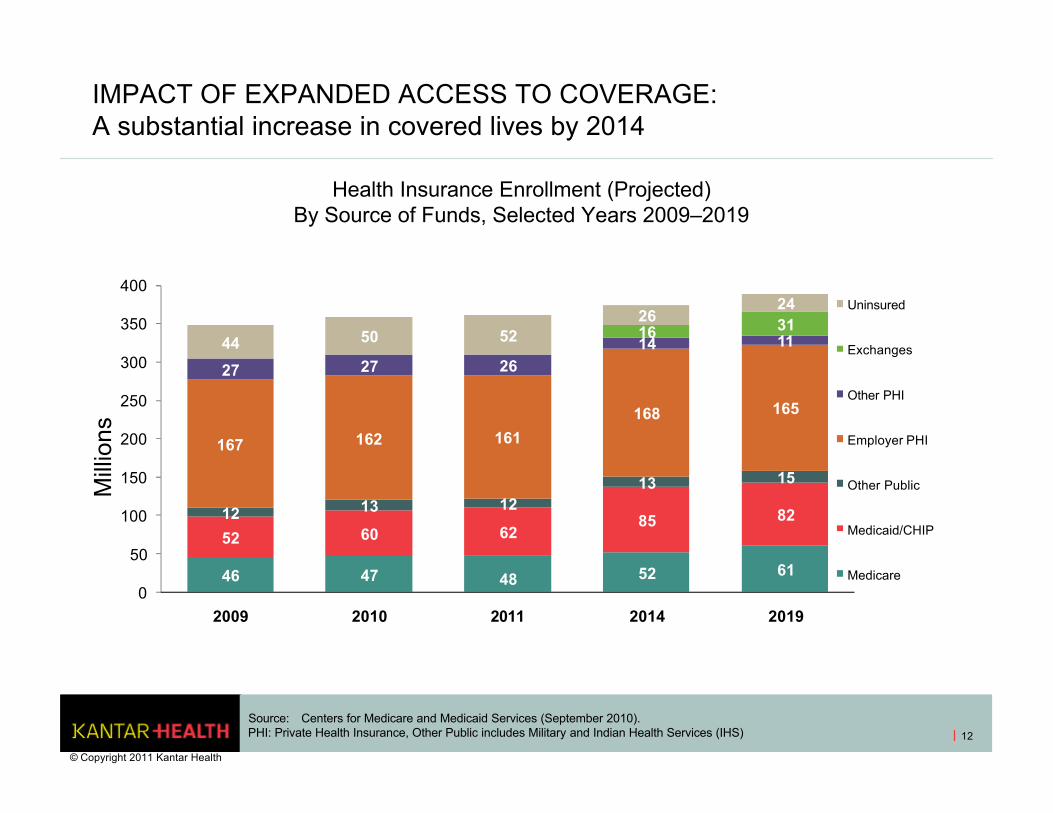

IMPACT OF EXPANDED ACCESS TO COVERAGE: A substantial increase in covered lives by 2014

12

Source: Centers for Medicare and Medicaid Services (September 2010).PHI: Private Health Insurance, Other Public includes Military and Indian Health Services (IHS)

46 47 48 52 61

52 60 6285 8212 13 1213 15

167 162 161

168 165

27 27 2614 1116 31

44 50 5226

24

0

50

100

150

200

250

300

350

400

2009 2010 2011 2014 2019

Uninsured

Exchanges

Other PHI

Employer PHI

Other Public

Medicaid/CHIP

Medicare

Health Insurance Enrollment (Projected)By Source of Funds, Selected Years 2009–2019

Mill

ions

© Copyright 2011 Kantar Health

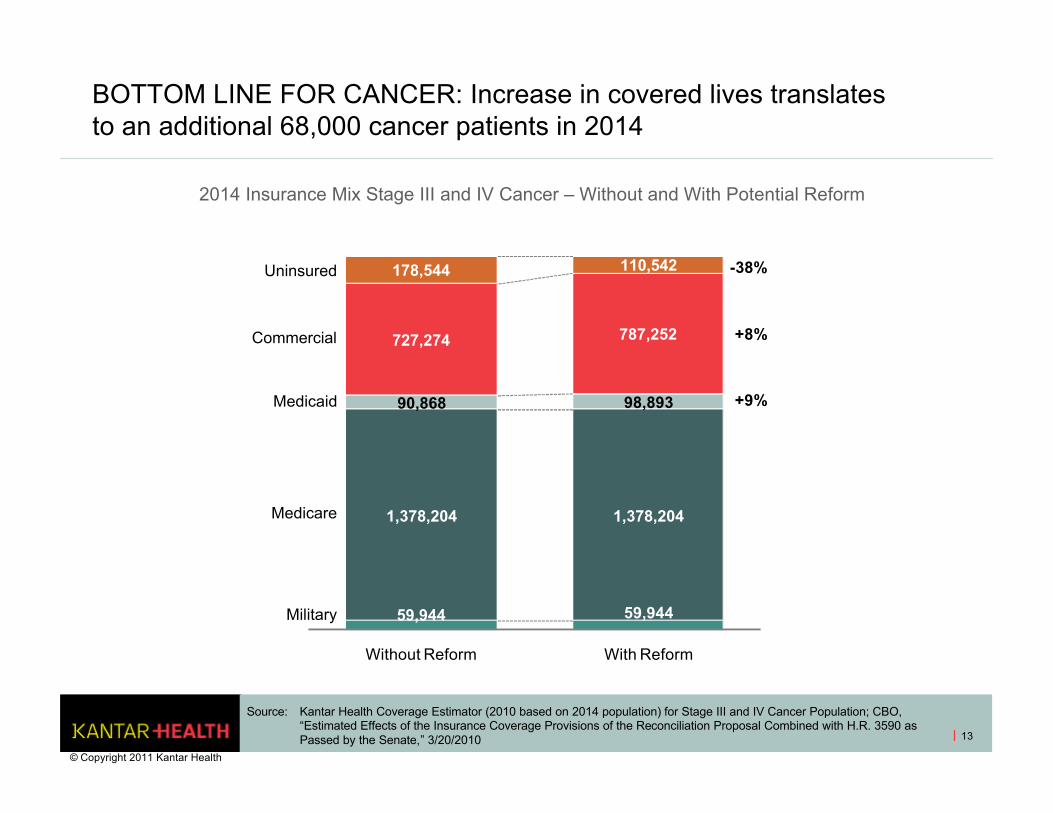

BOTTOM LINE FOR CANCER: Increase in covered lives translates to an additional 68,000 cancer patients in 2014

13

2014 Insurance Mix Stage III and IV Cancer – Without and With Potential Reform

59,944 59,944

1,378,204 1,378,204

90,868 98,893

727,274 787,252

178,544 110,542

Without Reform With Reform

Military

Medicare

Medicaid

Commercial

Uninsured

+9%

-38%

+8%

Source: Kantar Health Coverage Estimator (2010 based on 2014 population) for Stage III and IV Cancer Population; CBO, “Estimated Effects of the Insurance Coverage Provisions of the Reconciliation Proposal Combined with H.R. 3590 as Passed by the Senate,” 3/20/2010

© Copyright 2011 Kantar Health

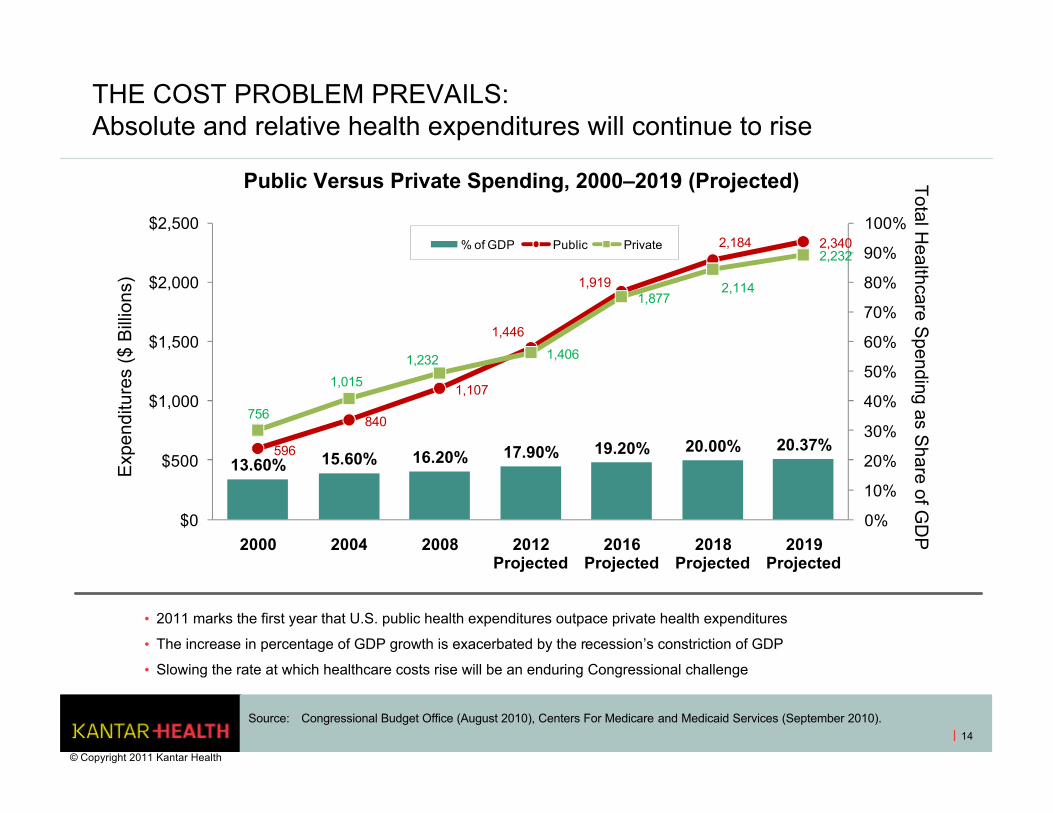

THE COST PROBLEM PREVAILS: Absolute and relative health expenditures will continue to rise

14

• 2011 marks the first year that U.S. public health expenditures outpace private health expenditures

• The increase in percentage of GDP growth is exacerbated by the recession’s constriction of GDP

• Slowing the rate at which healthcare costs rise will be an enduring Congressional challenge

13.60% 15.60% 16.20% 17.90% 19.20% 20.00% 20.37%596

840

1,107

1,446

1,919

2,184 2,340

756

1,015

1,232 1,406

1,8772,114

2,232

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$0

$500

$1,000

$1,500

$2,000

$2,500

2000 2004 2008 2012 Projected

2016 Projected

2018 Projected

2019 Projected

% of GDP Public Private

Source: Congressional Budget Office (August 2010), Centers For Medicare and Medicaid Services (September 2010).

Exp

endi

ture

s ($

Bill

ions

)T

otal Healthcare S

pending as Share of G

DP

Public Versus Private Spending, 2000–2019 (Projected)

© Copyright 2011 Kantar Health

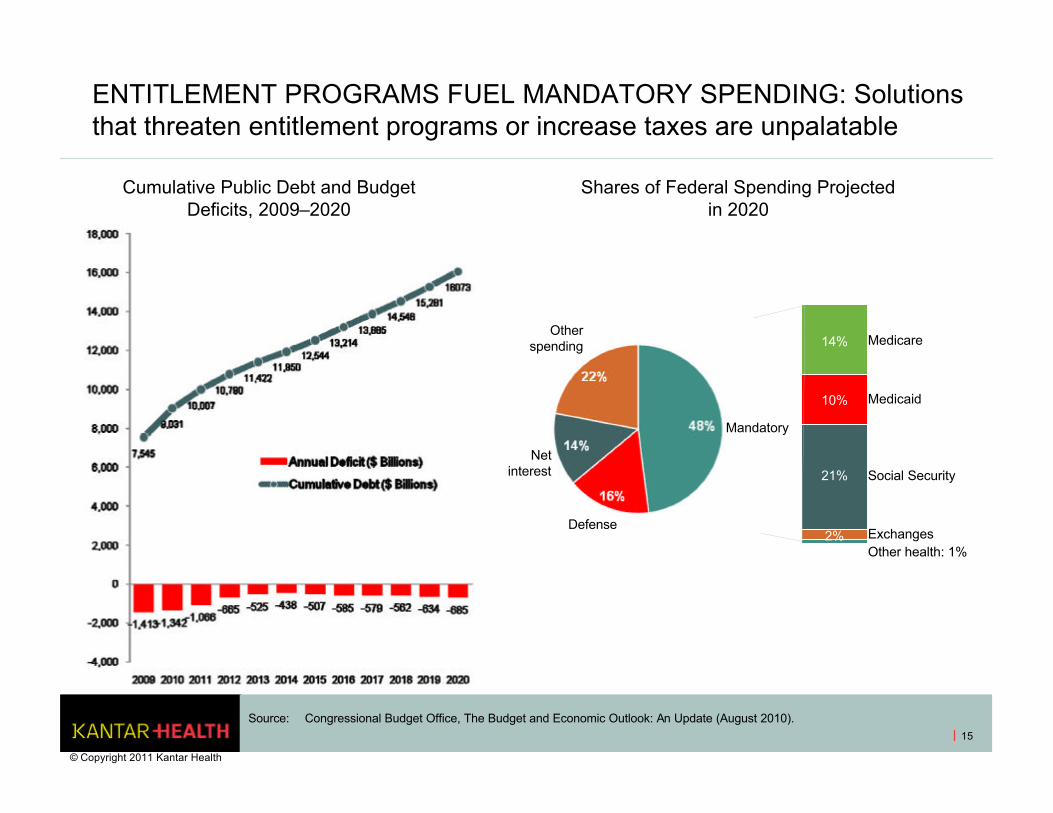

ENTITLEMENT PROGRAMS FUEL MANDATORY SPENDING: Solutions that threaten entitlement programs or increase taxes are unpalatable

15

Source: Congressional Budget Office, The Budget and Economic Outlook: An Update (August 2010).

Cumulative Public Debt and Budget Deficits, 2009–2020

Shares of Federal Spending Projected in 2020

Mandatory

Defense

Net interest

Other spending Medicare

Medicaid

Social Security

ExchangesOther health: 1%

14%

10%

21%

2%

© Copyright 2011 Kantar Health

R&D’S CONTRIBUTION TO COMMERCIAL SUCCESS: SAFETY, EFFICACY AND PHARMACOECONOMICS

© Copyright 2011 Kantar Health

16

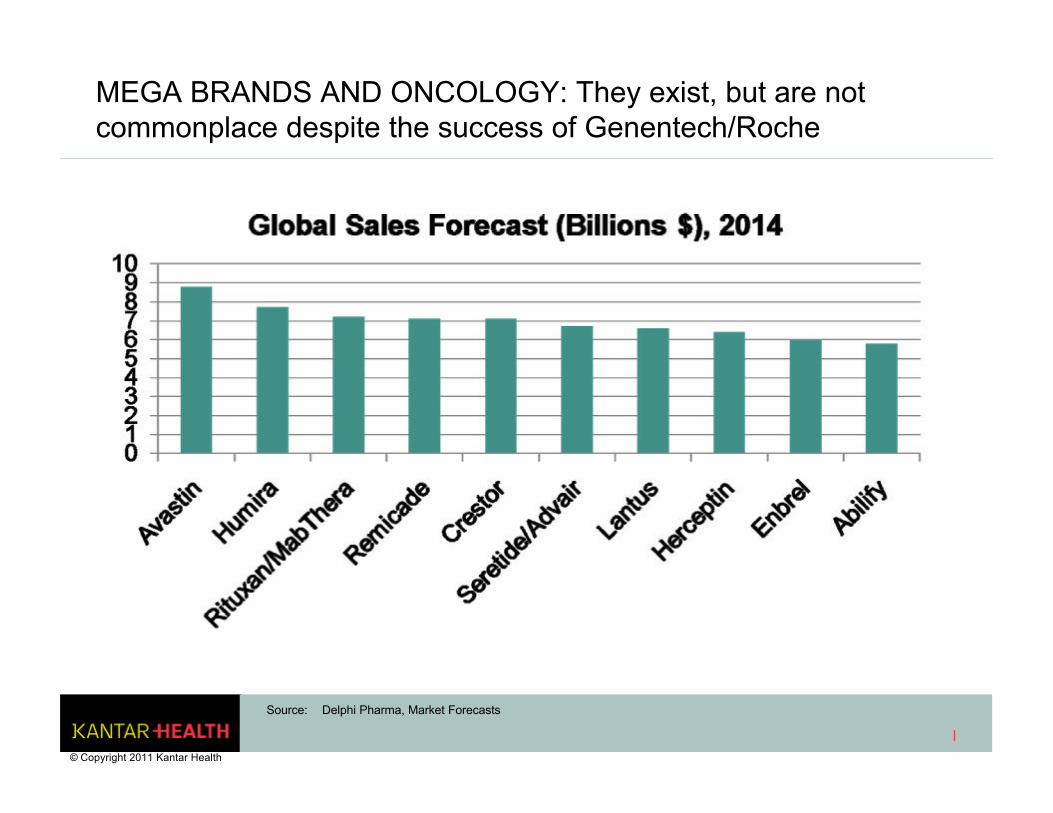

MEGA BRANDS AND ONCOLOGY: They exist, but are not commonplace despite the success of Genentech/Roche

Source: Delphi Pharma, Market Forecasts

© Copyright 2011 Kantar Health

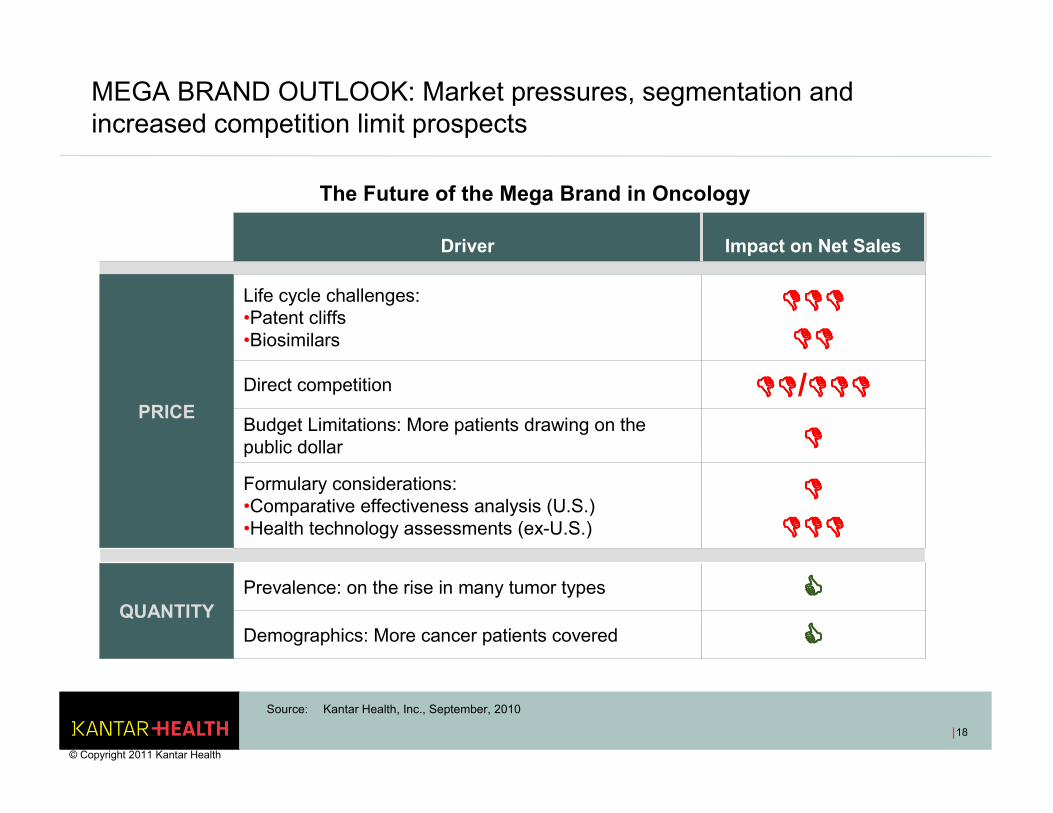

MEGA BRAND OUTLOOK: Market pressures, segmentation and increased competition limit prospects

The Future of the Mega Brand in Oncology

Source: Kantar Health, Inc., September, 2010

Driver Impact on Net Sales

PRICE

Life cycle challenges: •Patent cliffs•Biosimilars

������������

��������

Direct competition ��������/������������

Budget Limitations: More patients drawing on the public dollar ����

Formulary considerations:•Comparative effectiveness analysis (U.S.)•Health technology assessments (ex-U.S.)

����

������������

QUANTITYPrevalence: on the rise in many tumor types ����

Demographics: More cancer patients covered ����

18

© Copyright 2011 Kantar Health

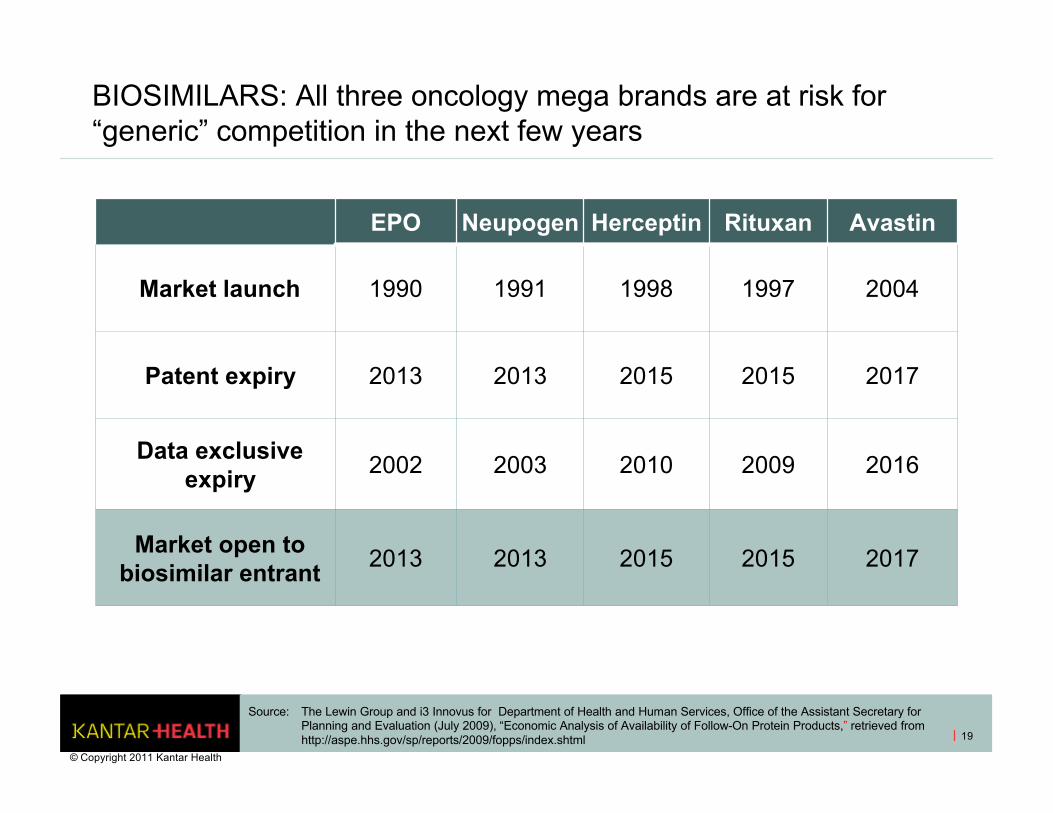

BIOSIMILARS: All three oncology mega brands are at risk for “generic” competition in the next few years

EPO Neupogen Herceptin Rituxan Avastin

Market launch 1990 1991 1998 1997 2004

Patent expiry 2013 2013 2015 2015 2017

Data exclusive expiry 2002 2003 2010 2009 2016

Market open to biosimilar entrant

2013 2013 2015 2015 2017

19

Source: The Lewin Group and i3 Innovus for Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation (July 2009), “Economic Analysis of Availability of Follow-On Protein Products,” retrieved from http://aspe.hhs.gov/sp/reports/2009/fopps/index.shtml

© Copyright 2011 Kantar Health

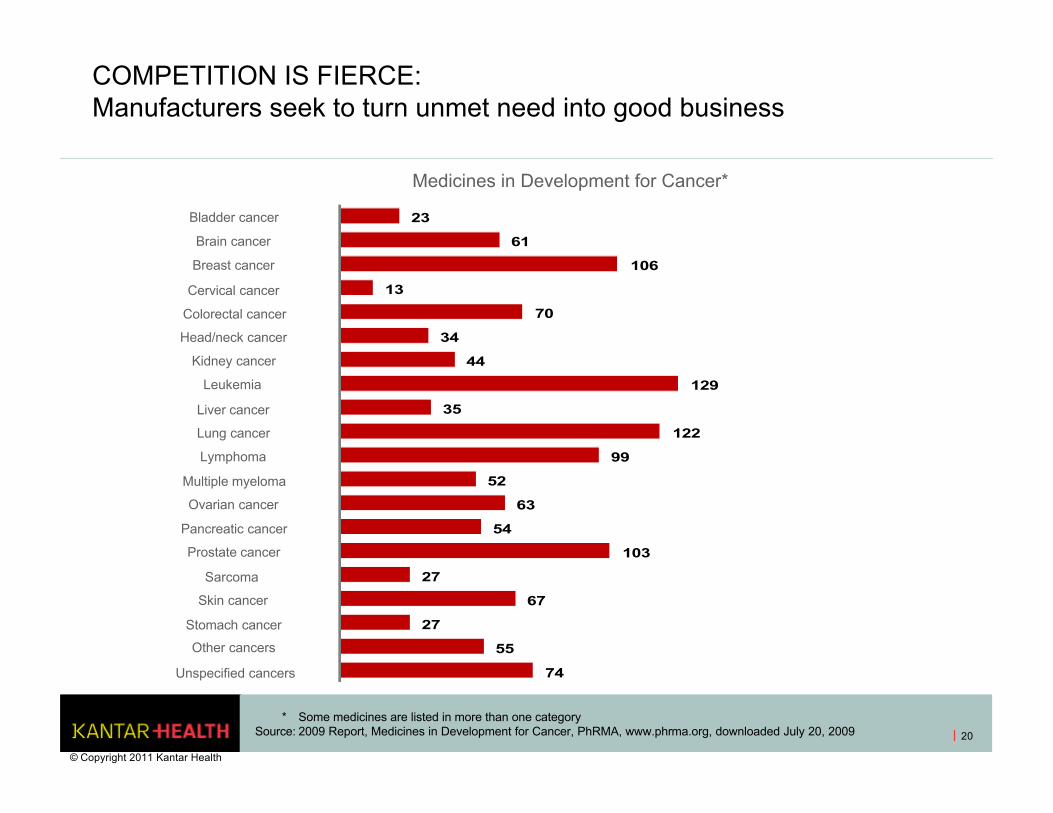

COMPETITION IS FIERCE: Manufacturers seek to turn unmet need into good business

20

* Some medicines are listed in more than one categorySource: 2009 Report, Medicines in Development for Cancer, PhRMA, www.phrma.org, downloaded July 20, 2009

Medicines in Development for Cancer*

74

55

27

67

27

103

54

63

52

99

122

35

129

44

34

70

13

106

61

23

Unspecified cancers

Other cancers

Stomach cancer

Skin cancer

Sarcoma

Prostate cancer

Pancreatic cancer

Ovarian cancer

Multiple myeloma

Lymphoma

Lung cancer

Liver cancer

Leukemia

Kidney cancer

Head/neck cancer

Colorectal cancer

Cervical cancer

Breast cancer

Brain cancer

Bladder cancer

© Copyright 2011 Kantar Health

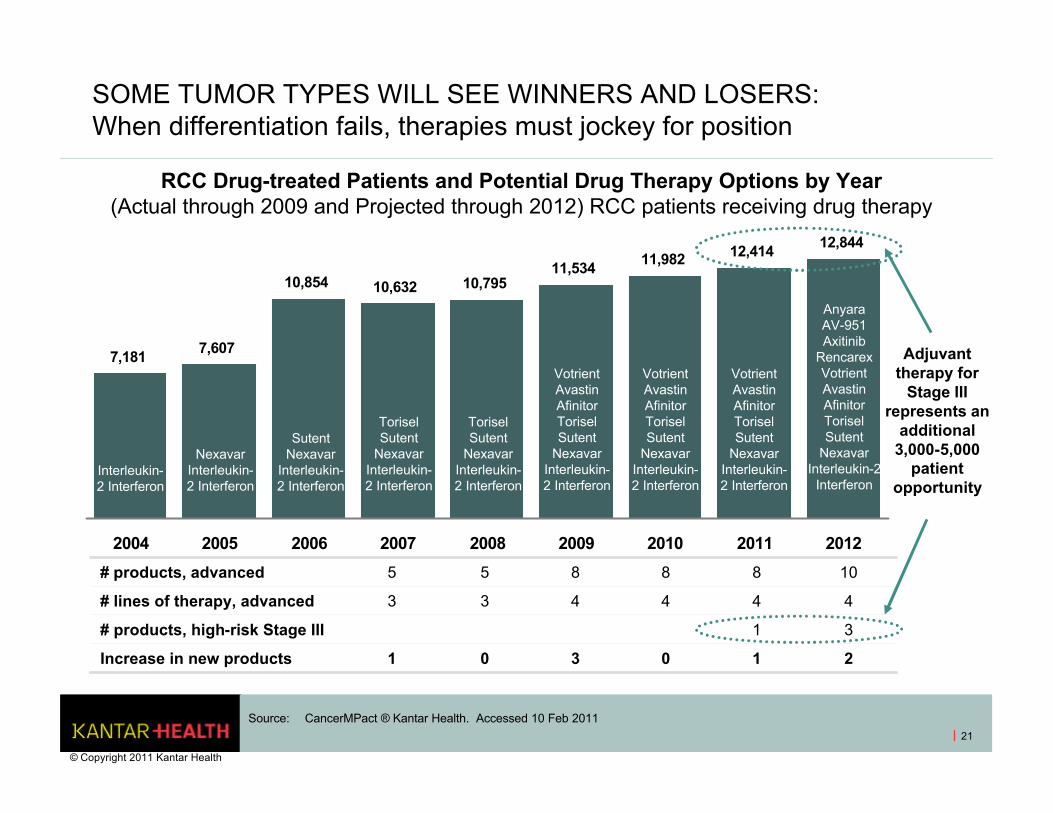

SOME TUMOR TYPES WILL SEE WINNERS AND LOSERS: When differentiation fails, therapies must jockey for position

21

7,181 7,607

10,854 10,632 10,79511,534 11,982 12,414 12,844

2004 2005 2006 2007 2008 2009 2010 2011 2012

Interleukin-2 Interferon

Nexavar Interleukin-2 Interferon

Sutent Nexavar

Interleukin-2 Interferon

Torisel Sutent

Nexavar Interleukin-2 Interferon

Torisel Sutent

Nexavar Interleukin-2 Interferon

VotrientAvastin Afinitor Torisel Sutent

Nexavar Interleukin-2 Interferon

Votrient Avastin Afinitor Torisel Sutent

Nexavar Interleukin-2 Interferon

Votrient Avastin Afinitor Torisel Sutent

Nexavar Interleukin-2 Interferon

AnyaraAV-951Axitinib

Rencarex Votrient Avastin Afinitor Torisel Sutent

Nexavar Interleukin-2

Interferon

# products, advanced 5 5 8 8 8 10

# lines of therapy, advanced 3 3 4 4 4 4

# products, high-risk Stage III 1 3

Increase in new products 1 0 3 0 1 2

Adjuvant therapy for

Stage III represents an

additional 3,000-5,000

patient opportunity

Source: CancerMPact ® Kantar Health. Accessed 10 Feb 2011

RCC Drug-treated Patients and Potential Drug Therapy Options by Year(Actual through 2009 and Projected through 2012) RCC patients receiving drug therapy

© Copyright 2011 Kantar Health

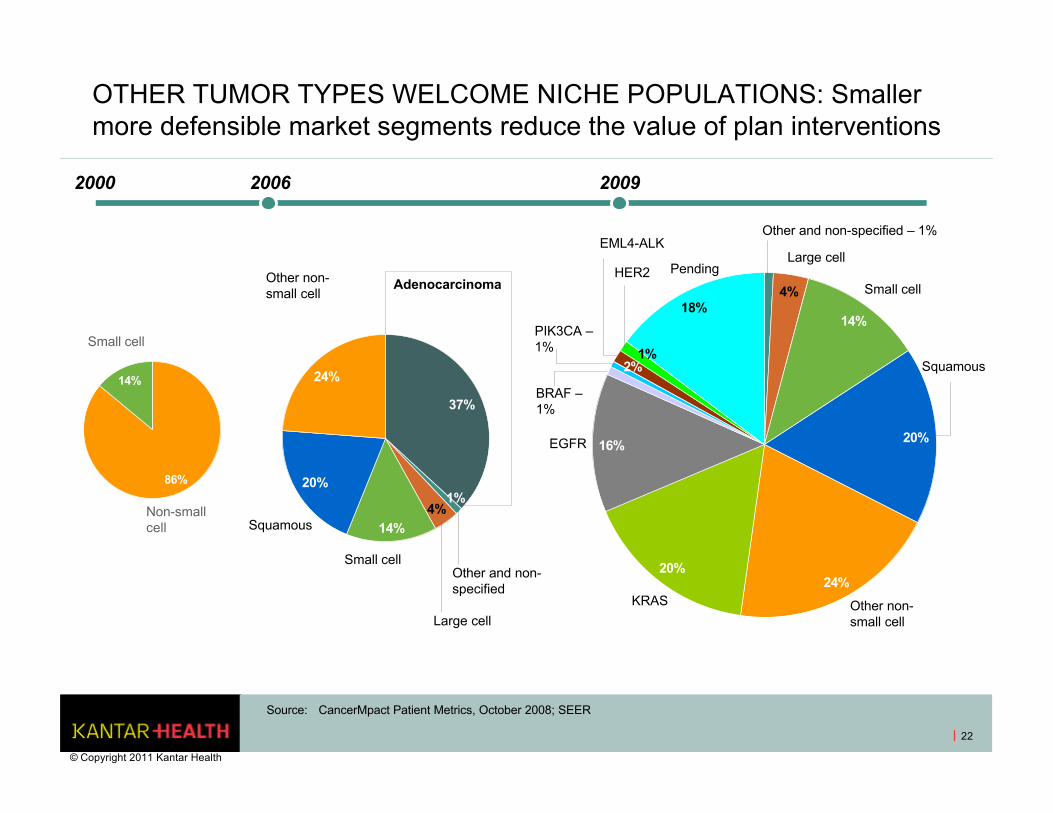

OTHER TUMOR TYPES WELCOME NICHE POPULATIONS: Smaller more defensible market segments reduce the value of plan interventions

22

86%

14%

37%

14%

20%

24%

1%4%

14%

20%

24%20%

16%

2%1%

18%4%

2000 2006 2009

Non-small cell

Small cell

Adenocarcinoma

Other and non-specified

Large cell

Small cell

Squamous

Other non-small cell

Other and non-specified – 1%

Large cell

Small cell

Squamous

Other non-small cell

KRAS

EGFR

BRAF –1%

PIK3CA –1%

EML4-ALK

HER2 Pending

Source: CancerMpact Patient Metrics, October 2008; SEER

© Copyright 2011 Kantar Health

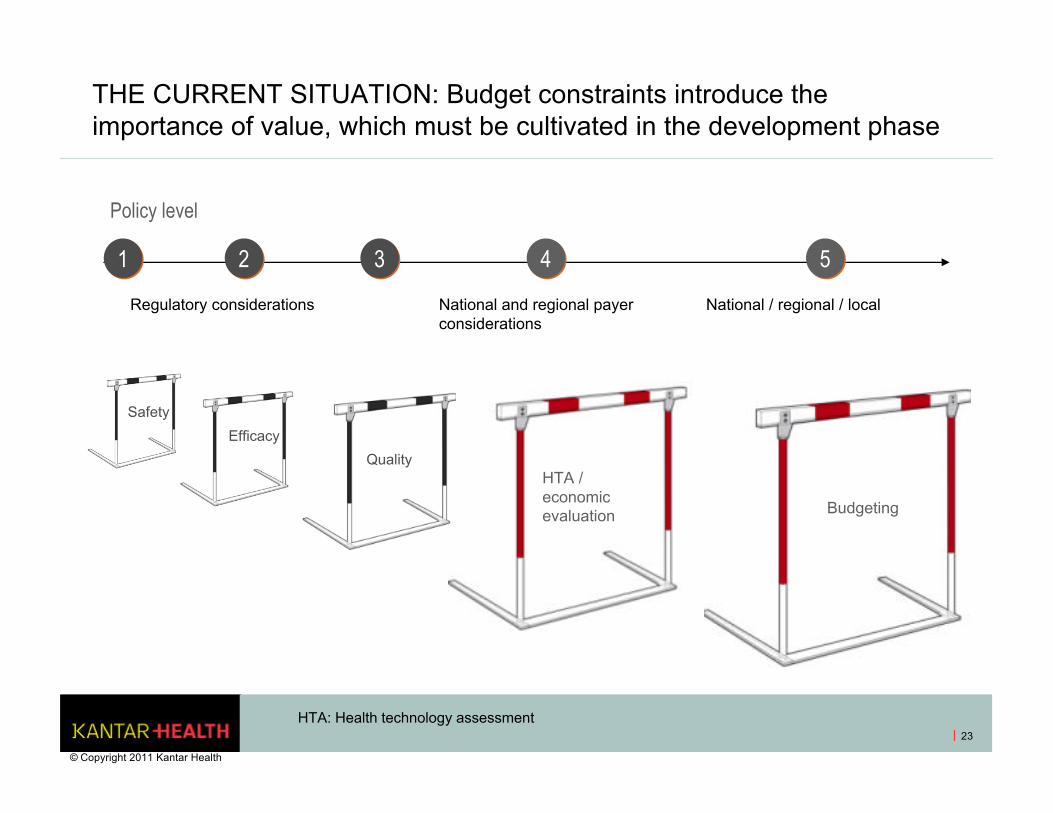

THE CURRENT SITUATION: Budget constraints introduce the importance of value, which must be cultivated in the development phase

23

HTA / economic evaluation Budgeting

Quality

Policy level

Regulatory considerations National and regional payer considerations

National / regional / local

11 33 44 5522

Safety

Efficacy

HTA: Health technology assessment

© Copyright 2011 Kantar Health

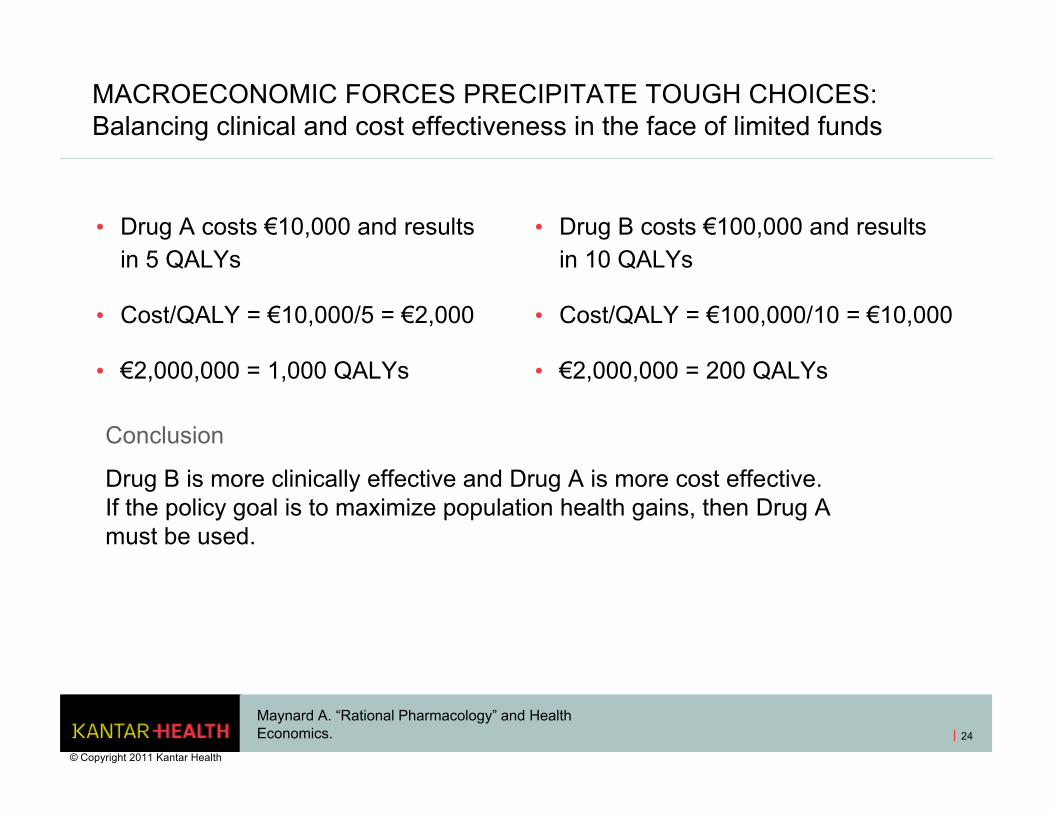

MACROECONOMIC FORCES PRECIPITATE TOUGH CHOICES: Balancing clinical and cost effectiveness in the face of limited funds

• Drug A costs €10,000 and results in 5 QALYs

• Cost/QALY = €10,000/5 = €2,000

• €2,000,000 = 1,000 QALYs

• Drug B costs €100,000 and results in 10 QALYs

• Cost/QALY = €100,000/10 = €10,000

• €2,000,000 = 200 QALYs

Conclusion

Drug B is more clinically effective and Drug A is more cost effective. If the policy goal is to maximize population health gains, then Drug A must be used.

Maynard A. “Rational Pharmacology” and Health Economics.

© Copyright 2011 Kantar Health

24

PILLARS OF VALUE: Consider your audience

• Safety

• Efficacy

• Tolerability

• Quality of life

• Disinvestment (i.e., decreased utilization of healthcare goods and services)

• Practice economics

© Copyright 2011 Kantar Health

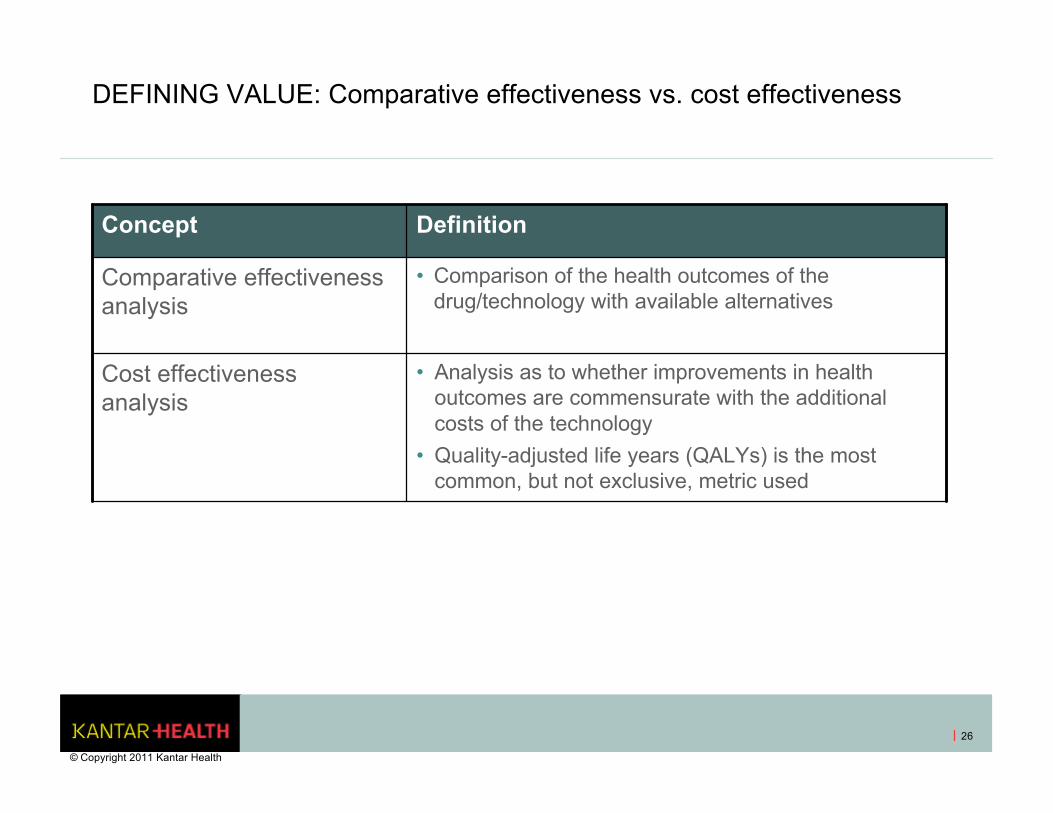

DEFINING VALUE: Comparative effectiveness vs. cost effectiveness

Concept Definition

Comparative effectiveness analysis

• Comparison of the health outcomes of the drug/technology with available alternatives

Cost effectiveness analysis

• Analysis as to whether improvements in health outcomes are commensurate with the additional costs of the technology

• Quality-adjusted life years (QALYs) is the most common, but not exclusive, metric used

© Copyright 2011 Kantar Health

26

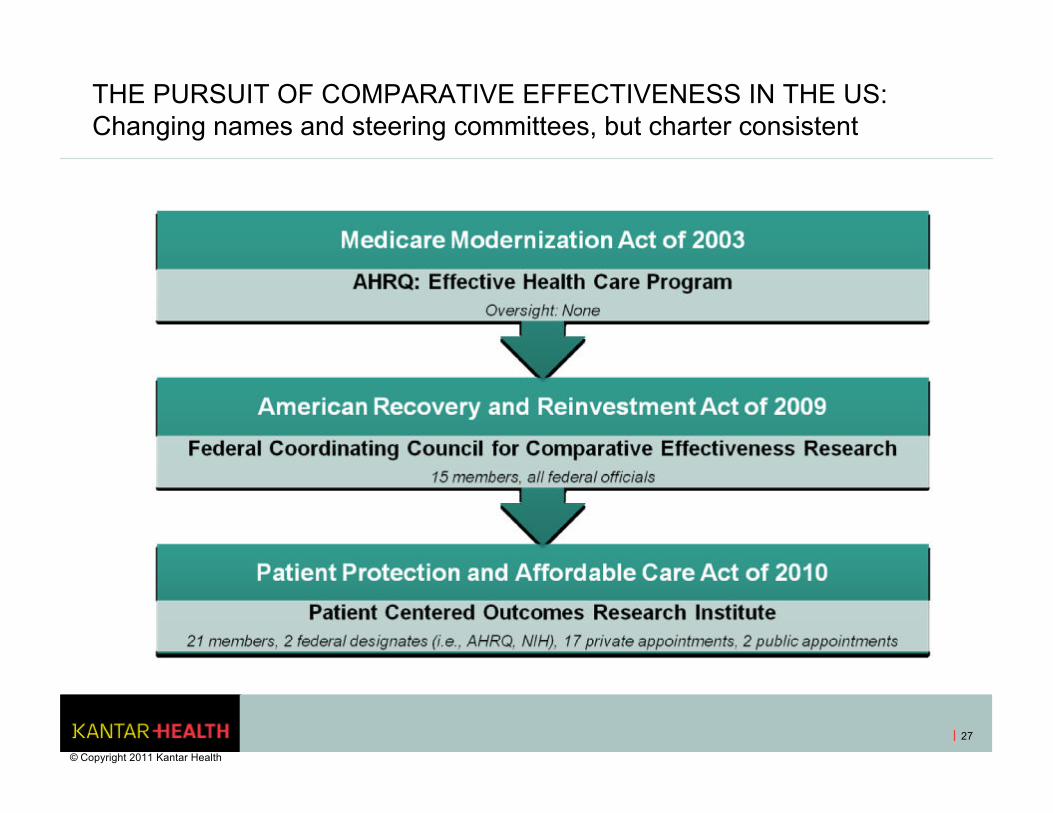

THE PURSUIT OF COMPARATIVE EFFECTIVENESS IN THE US: Changing names and steering committees, but charter consistent

27

© Copyright 2011 Kantar Health

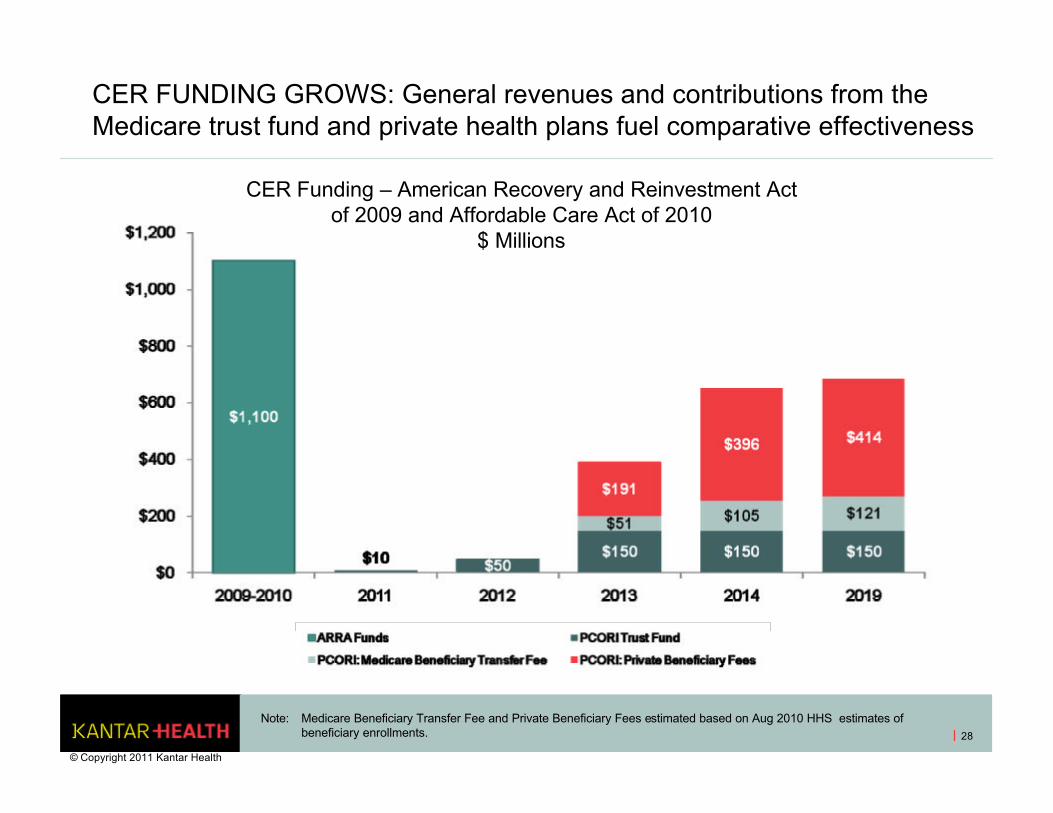

CER FUNDING GROWS: General revenues and contributions from the Medicare trust fund and private health plans fuel comparative effectiveness

28

Note: Medicare Beneficiary Transfer Fee and Private Beneficiary Fees estimated based on Aug 2010 HHS estimates of beneficiary enrollments.

CER Funding – American Recovery and Reinvestment Act of 2009 and Affordable Care Act of 2010

$ Millions

© Copyright 2011 Kantar Health

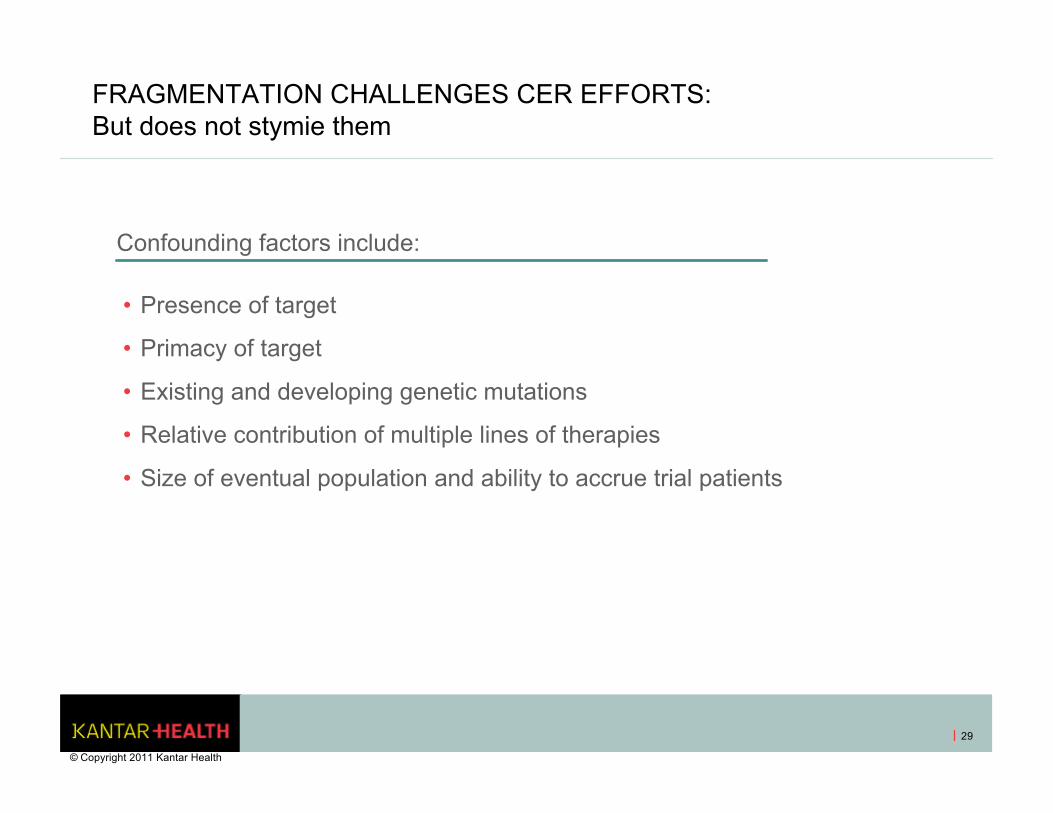

FRAGMENTATION CHALLENGES CER EFFORTS: But does not stymie them

Confounding factors include:

• Presence of target

• Primacy of target

• Existing and developing genetic mutations

• Relative contribution of multiple lines of therapies

• Size of eventual population and ability to accrue trial patients

29

© Copyright 2011 Kantar Health

THERE IS NO SUCH THING AS FREE…ESPECIALLY NOT PRICING

© Copyright 2011 Kantar Health

30

31

© Copyright 2011 Kantar Health

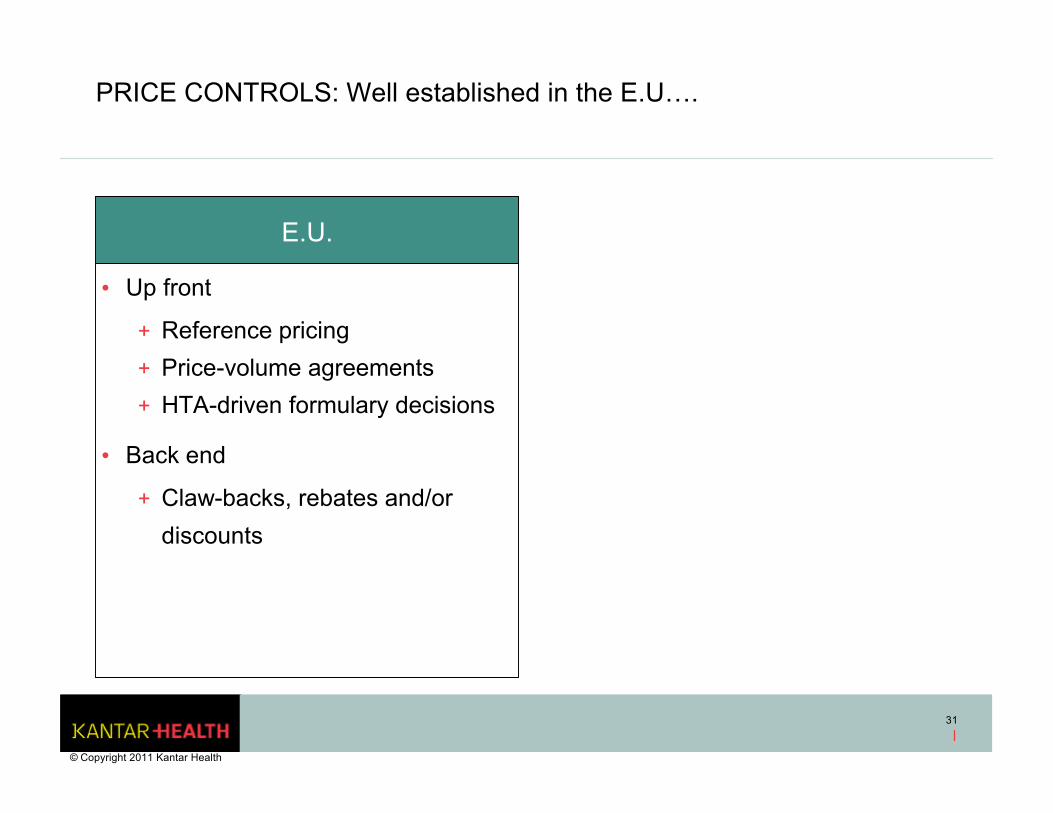

E.U.

• Up front

+ Reference pricing

+ Price-volume agreements

+ HTA-driven formulary decisions

• Back end

+ Claw-backs, rebates and/or

discounts

PRICE CONTROLS: Well established in the E.U….

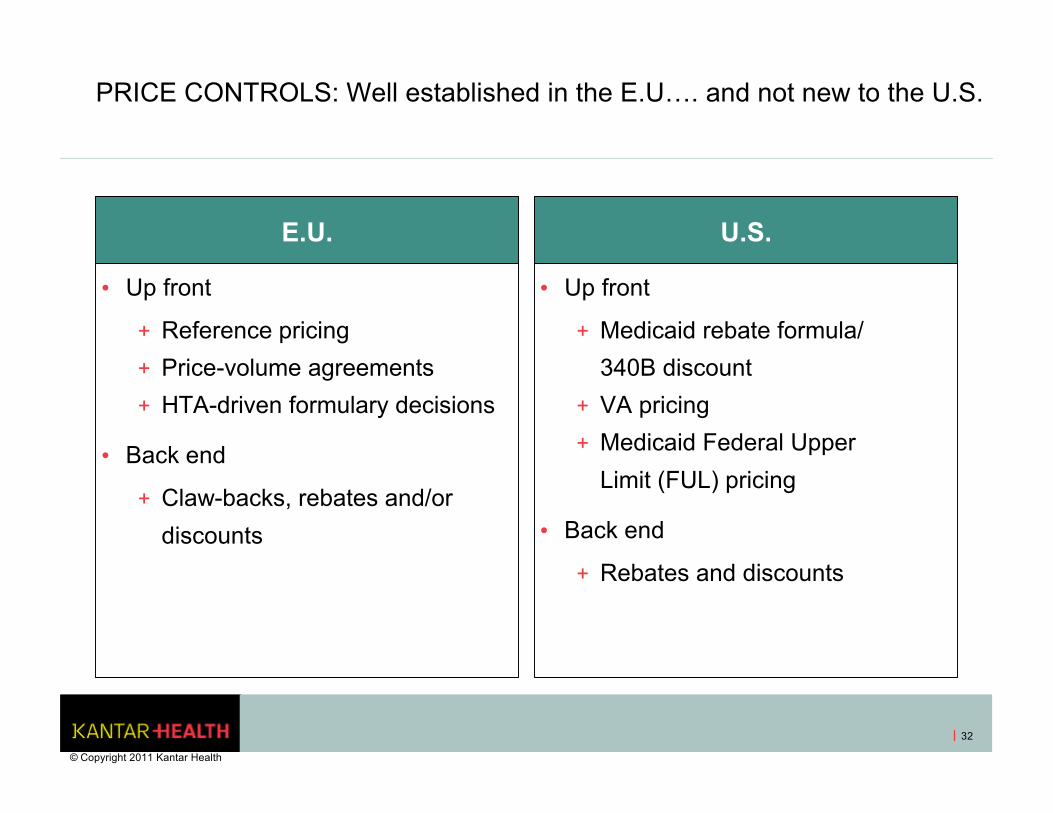

PRICE CONTROLS: Well established in the E.U…. and not new to the U.S.

E.U.

• Up front

+ Reference pricing

+ Price-volume agreements

+ HTA-driven formulary decisions

• Back end

+ Claw-backs, rebates and/or

discounts

U.S.

• Up front

+ Medicaid rebate formula/

340B discount

+ VA pricing

+ Medicaid Federal Upper

Limit (FUL) pricing

• Back end

+ Rebates and discounts

32

© Copyright 2011 Kantar Health

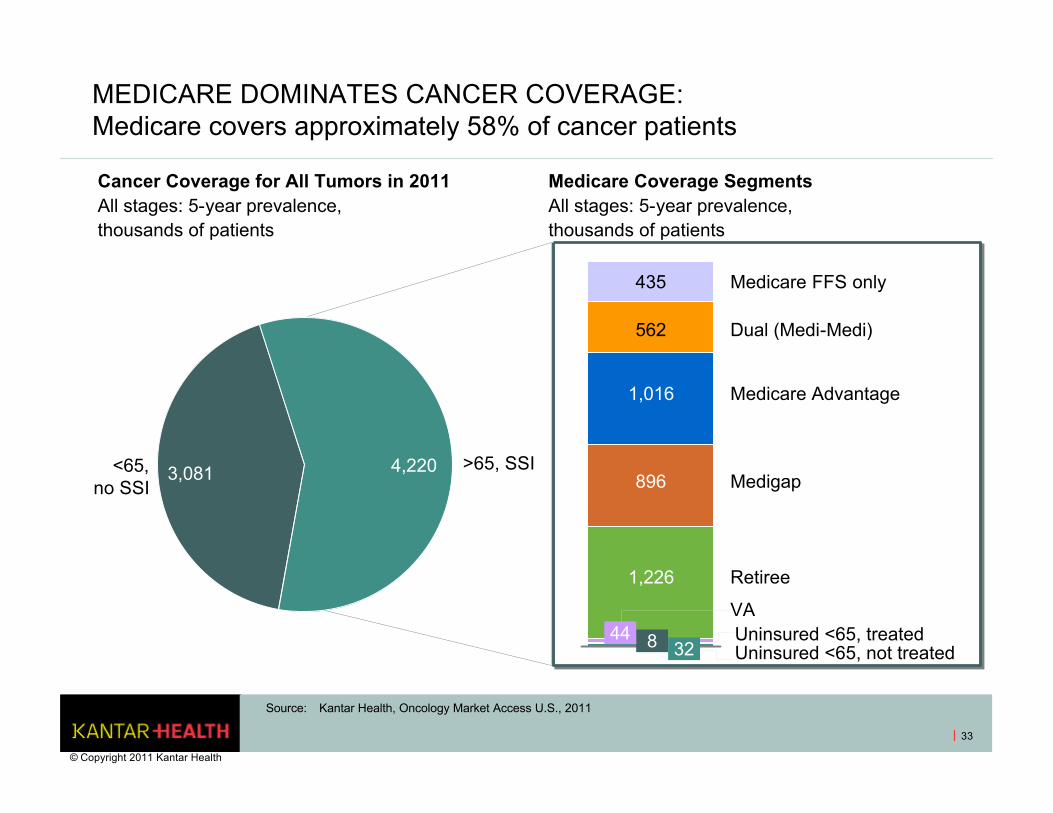

<65, no SSI

>65, SSI3,081 4,220

MEDICARE DOMINATES CANCER COVERAGE: Medicare covers approximately 58% of cancer patients

33

Medicare FFS only

Dual (Medi-Medi)

VA

Medicare Advantage

Medigap

Retiree

Source: Kantar Health, Oncology Market Access U.S., 2011

Cancer Coverage for All Tumors in 2011All stages: 5-year prevalence, thousands of patients

Medicare Coverage SegmentsAll stages: 5-year prevalence, thousands of patients

Uninsured <65, treatedUninsured <65, not treated

8

1,226

896

1,016

562

4432

435

© Copyright 2011 Kantar Health

34

393 Vintage Park Dr., Suite 250Foster City, California 94404, U.S.A.Tel: (650) 403-7012Fax: (650) 403-7062 E-mail: [email protected]: www.kantarhealth.com

Please contact us if you have any questions.

US:

Rhoda [email protected]

Bill [email protected]

© Copyright 2011 Kantar Health

35

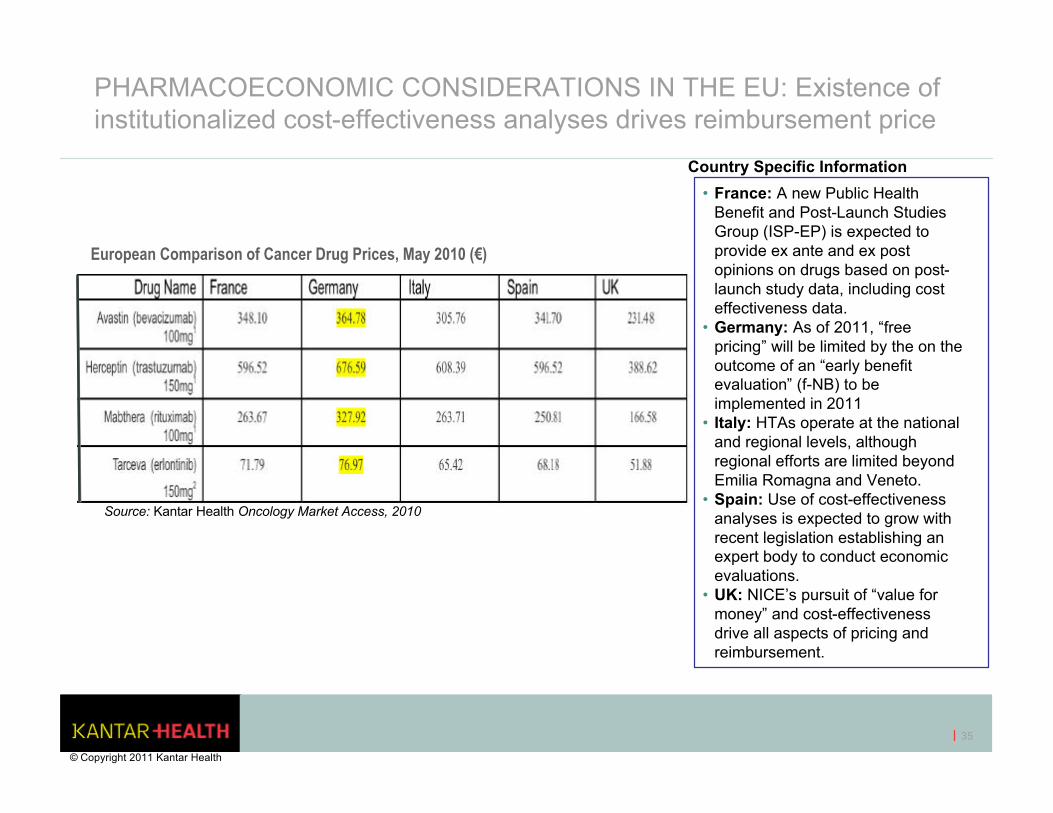

PHARMACOECONOMIC CONSIDERATIONS IN THE EU: Existence of institutionalized cost-effectiveness analyses drives reimbursement price

European Comparison of Cancer Drug Prices, May 2010 (€)

Source: Kantar Health Oncology Market Access, 2010

Country Specific Information

• France: A new Public Health Benefit and Post-Launch Studies Group (ISP-EP) is expected to provide ex ante and ex post opinions on drugs based on post-launch study data, including cost effectiveness data.

• Germany: As of 2011, “free pricing” will be limited by the on the outcome of an “early benefit evaluation” (f-NB) to be implemented in 2011

• Italy: HTAs operate at the national and regional levels, although regional efforts are limited beyond Emilia Romagna and Veneto.

• Spain: Use of cost-effectiveness analyses is expected to grow with recent legislation establishing an expert body to conduct economic evaluations.

• UK: NICE’s pursuit of “value for money” and cost-effectiveness drive all aspects of pricing and reimbursement.

© Copyright 2011 Kantar Health

22nd Annual 22nd Annual Cancer Progress ConferenceCancer Progress Conference

Oncology Market Overview: Barriers, Challenges and Value

• Bill Bagwell, RPh, Senior Vice President, Clinical and Scientific Assessment, Kantar Health

• Rhoda Dunn, Account Director, Market Access, Kantar Health

36