Embed Size (px)

Citation preview

1

On the Acquisition of Equity Carve-Outs

Chintal A. Desaia,*, Mark S. Klockb, Sattar A. Mansic

a Department of Economics and Finance, College of Business Administration, The University of Texas-Pan American, 1201 West University Drive, Edinburg, TX 78539-2999, USA b Department of Finance, School of Business, The George Washington University, 2201 G. Street, NW, Washington, DC 20052, USA c Department of Finance, Insurance, and Law, Pamplin College of Business, Virginia Tech, Blacksburg, VA 24061, USA

This version: May 24, 2011 Published in 35 Journal of Banking and Finance (2011), pp. 3432-2449

Abstract

We examine the role played by the parent’s motive in undertaking a carve-out; the parent’s post-IPO influence over the carved-out subsidiary; and anti-takeover provisions and industry structure of a carve-out on its acquisition likelihood and its acquisition premium. We find that the probability and hazard of a carve-out acquisition increase when the parent’s objective is to unlock the value of a subsidiary and when the parent and the subsidiary are tied with a product-market relationship. We also find that the post-IPO parent ownership significantly affects the acquisition likelihood and the level of acquisition premium. Additional analyses examining the post-IPO carve-out status suggest that the product-market relationship and post-IPO parent ownership increase the probability of re-acquisition.

JEL classification: G34; G32 Keywords: Equity carve-outs; Acquisition; Parent-subsidiary; Corporate restructuring * Corresponding author. Tel.: +1 956 665 7358; fax: +1 956 665 5020. E-mail addresses: [email protected] (C. Desai), [email protected] (M. Klock), [email protected] (S. Mansi). Acknowledgement The authors would like to thank the anonymous referee, the editor (Ike Mathur), Gregory Elliehausen, Bharat Jain, Gergana Jostova, Irvin Morgan, Christo Pirinsky, Robert Savickas, Emanuel Zur, and seminar participants at Florida State University (College of Law), George Washington University, Ohio University, University of Texas-Pan American, Midwest Finance Association (2007), and Southern Finance Association (2009) for their comments and suggestions. Ditina Desai contributed by proofreading the manuscript. This paper is partially based on Desai’s Ph.D. dissertation at The George Washington University. A portion of this research was completed while Desai was at University of Maryland, College Park. All remaining errors are the authors’ responsibility.

2

1. Introduction

An equity carve-out (ECO) is a form of corporate restructuring whereby the parent firm

offers a subset of its subsidiary’s common shares to the public.1 Research evidence indicates that

ECOs are temporary arrangements for the parent firms and the majority of ECOs are acquired

within a few years after their initial public offerings (IPOs).2 In such a scenario, do we know a

priori the factors which can predict the eventual acquisition of an ECO? And do these factors

have an impact on the ECO shareholders’ wealth, when it actually gets acquired? To our

knowledge, these questions have not been explored in the corporate restructuring literature and

we attempt to fill this gap. Specifically, we analyze the effects of: the parent’s motive for

conducting a carve-out; parental control on the post-IPO carve-out; anti-takeover provisions in

the charter of a carve-out; and industry structure of the carve-out on the likelihood of an

acquisition and the level of acquisition premium. Within the likelihood of acquisition, we look

into the probability of acquisition and the hazard of acquisition. We also assess the impact of our

chosen variables on the subsamples of ECOs that are either re-acquired by the parent firm or

acquired by a third-party.

The prior work of other scholars facilitates our research endeavors. For example, Perotti

and Rossetto’s (2007) theoretical model implies that the likelihood of an ECO acquisition

increases when the parent’s motive for conducting a carve-out is to unlock the value of its

subsidiary. As per the authors, prior to the carve-out, the parent is unaware of the “fair” value of

its synergy with the subsidiary, which precludes it from making an informed decision to keep

either full or no ownership in the subsidiary. Subsequent to the carve-out, market participants

1 For a review on ECOs and other forms of corporate restructuring, see Eckbo and Thorburn (2008). 2 For example, Klein et al. (1991) show that 44 of 52 ECOs in their sample are either re-acquired or sold off to a third-party by the parent firms.

3

assist the parent firm in ascertaining the value of its synergy with the subsidiary. If the synergy is

positive, then the parent firm decides to re-acquire the carved-out subsidiary, else if the synergy

is negative, then the parent decides to sell it off to a third-party. Based on the authors’ insights,

we posit that, if the parent’s motive is to unlock the value of its subsidiary, it is likely to be

interested in determining its synergy with the subsidiary. Therefore, this carved-out subsidiary’s

acquisition is imminent, either by the parent itself or by a third-party.

An equity carve-out differs substantially from other forms of corporate restructuring such

as spinoffs and asset sales in terms of the post-divestiture parent role in the subsidiary.3 Allen

and McConnell (1998) show that, on average, the parent retains 69% of the ownership in the

subsidiary. The ownership in an ECO provides required voting rights to the parent, which allows

it to appoint its nominee on the board and on the audit committee of the carve-out.4 The parent

firm, generally, appoints its past employees to key executive positions of the carve-out. In

addition, prior to a carve-out transaction, a parent can sign long-term business agreements with

the subsidiary, which allows it not only to preserve the existing synergy but also to exert undue

influence over the subsidiary.5 We hypothesize, as explained in Section 2.2, that the post-IPO

parental control can have an effect on the ECO’s acquisition.

3 In spinoffs, the parent firm distributes its ownership in the subsidiary on a pro-rata basis to its existing shareholders, whereas in the case of an asset sale, the parent firm sells its ownership in the subsidiary to a third-party on a private negotiation basis. In both cases the parent retains no ownership in the post-divesture subsidiary, suggesting minimal parent control. However, a few papers show the significant role of the parent in the spun-off subsidiary. For example, Wruck and Wruck (2002) show the involvement of the parent in appointing the top-management team of the spinoff. 4 Throughout the paper, the term ownership refers to the voting ownership rather than cash flow ownership since the former can have a significant impact on the acquisition event. The difference between the two is relevant only for equity carve-outs with dual class shares. 5 The long-term agreements with the parent firm can prevent an ECO from obtaining a better deal in an arm’s-length transaction. For example, the Appendix of Atanasov et al. (2010) provides the case of Coca-Cola’s (KO) influence over its partially-owned (49% ownership) subsidiary Coca-Cola Enterprises (CCE) through long-term business agreements.

4

The anti-takeover provisions and the industry in which an ECO operates can also play a

role in its acquisition. Field and Karpoff (2002) find that the probability of acquisition of an IPO

decreases when it employs takeover defenses in its charter. Takeover defenses might also affect

the level of acquisition premium; though the evidence is mixed. For example, Megginson (1990)

finds an increase in premium for firms with anti-takeover provisions, while Field and Karpoff

(2002) do not find any significant relation between the level of premium and anti-takeover

provisions. Regarding the relevance of the industry, Perotti and Rossetto (2007) conjecture that

ECOs operating in high-technology (hi-tech) industries have a longer time-to-acquisition due to a

higher level of valuation uncertainty in those industries. In contrast, hi-tech firms also offer

changes in technology and above-market returns which can increase the probability of their

acquisition (Kohers and Kohers, 2000).

Using a sample of 222 equity carve-outs (of which 137 are acquired) for the period of

1986 to 2004, we find that the likelihood of acquisition increases when the parent’s motive for

undertaking an ECO is to unlock its value, when the parent retains majority ownership in the

post-IPO carved-out subsidiary, and when the parent and the subsidiary are tied with product-

market relations. We also find some evidence that when the ECO operates in the hi-tech

industry, the likelihood of acquisition increases. Further, we find an inverse relation between the

level of acquisition premium and whether the parent ownership in the ECO is above 50% prior to

the acquisition. In terms of the differences between the parent re-acquisition and a third-party

acquisition, we find that the probability of re-acquisition increases when the parent’s motive is to

unlock value, when the parent retains majority ownership in the post-IPO carve-out, and when

the parent and ECO have an ongoing product-market connection.

5

Our results are robust to self-selection and endogeneity issues. Michaely and Shaw

(1995) find that the bigger and less profitable parent firms are likely to divest their subsidiaries

by conducting carve-outs instead of spinoffs. This choice of going public in the first place is

likely to induce self-selection bias in our estimation. To address this, we perform a two-stage

Heckman analysis for the probit models. In the first stage, we analyze the choice between a

carve-out and a spinoff, and in the second stage, given that the parent has selected to perform an

ECO, we analyze its likelihood of acquisition. In terms of endogeneity, the parent might be

anticipating the ECO’s future acquisition at the time of consummating the carve-out transaction,

and accordingly decides the post-IPO ownership in the carve-out. In that case, the retained

ownership in the carve-out is likely to be endogenously determined. We address this issue by

performing an instrumental variable probit analysis and bivariate probit analysis, which are

similar to that of a two-stage least squares analysis. In the first stage, we explain the parent’s

post-IPO ownership in a carve-out, and in the second stage, we use the predicted value of the

parent retained ownership for explaining the probability of an acquisition. We do not report these

results in this paper to economize on space, but they are available in Desai et al. (2011).

Our paper contributes to the corporate restructuring literature in at least four ways. First,

we undertake a comprehensive study by collectively analyzing the IPO and acquisition events of

a carve-out.6 Second, we assess the likelihood of acquisition of carve-outs by analyzing the

probability and the hazard of acquisition. The latter part, to our knowledge, has not been

investigated. Third, we explore the impact of contributory factors, other than the parent retained

6 Several studies seek to establish a link between the IPO and the acquisition events of a carve-out. For example, Klein et al. (1991) show that the probability of re-acquisition increases with the increase in post-IPO parent ownership. Hulburt (2003) finds that the parent firms of the ECOs that were subsequently acquired experience greater wealth gains at the time of carve-out announcements. Otsubo (2009) shows that the market participants anticipate a third-party acquisition and accordingly adjust the share price of the parent on a carve-out announcement.

6

ownership, such as the parent motives for conducting a carve-out, parent-subsidiary business

relations, anti-takeover provisions, and the industry in which the carve-out operates on the carve-

out’s acquisition. Lastly, we explain differences in the likelihood of acquisition and the

acquisition premium for the subsamples of parent re-acquisitions and third-party acquisitions.

The remainder of the paper is organized as follows: Section 2 illustrates our hypotheses,

and Section 3 highlights the data, variable measurements, and descriptive statistics. Section 4

provides the empirical results. Section 5 concludes the paper.

2. Hypotheses development

2.1. Reasons for conducting a carve-out and its acquisition

When conducting a carve-out, the parent firms incur a substantial amount of explicit costs

such as legal, underwriting, and filing fees. They also underprice in order to successfully

consummate the offering; Hogan and Olson (2004) show a first-day return of 13%. In addition,

there are costs due to the ‘disincentive’ effect (Perotti and Rossetto, 2007). Before a carve-out,

the operating profits of the wholly-owned subsidiary belong entirely to the parent firm. After a

carve-out, the parent firm incurs costs in operating the partially-owned subsidiary, but the profits

are pro-rata distributed to the shareholders which also include minority shareholders. Then, what

are the benefits for the parent firm in conducting an equity carve-out?

Schipper and Smith (1986) describe three main reasons for conducting a carve-out:

financing, restructuring, and unlocking the value. The financing reason involves the instances

when the parent conducts an ECO to finance its own or its subsidiary’s growth projects, to

discharge parent debt, or to raise funds to meet capital expenditure requirements. The

restructuring reason involves the instances when the parent carves out the subsidiary to gain from

7

the divestiture.7 Finally, the unlocking the value reason involves the cases when the parent

undertakes an ECO for investors to better understand the operations of the carve-out. At the time

of an IPO and subsequent to it, the subsidiary needs to comply with the Securities and Exchange

Commission (SEC) by filing forms such as registration statements, proxy statements, 10-Ks, and

annual reports. From these filings, the investors can obtain the relevant information about the

carved-out subsidiary.

As mentioned earlier, the theoretical insights of Perotti and Rossetto (2007) help establish

a possible linkage between the parent motive at the time of a carve-out and the subsequent

acquisition of the carve-out. They argue that the status of a subsidiary as a fully-integrated and

an independent identity are two extremes, and it depends on the synergy between the parent and

the subsidiary. By selling out full ownership in a subsidiary, the parent firm carries an

irreversible loss if it finds a positive synergy with the subsidiary in the future. At the same time,

by keeping the subsidiary fully-integrated, the parent firm is unable to assess the value of the

synergy. An ECO of the subsidiary provides the parent a better alternative. On the one hand,

carving out the subsidiary at the first stage causes the parent firm to incur costs related to the

public issue and the loss of operational efficiency. On the other hand, it helps the parent firm

determine the value of its synergy with the subsidiary more accurately while retaining control

(through a majority ownership) in the subsidiary. Therefore, the carve-out of a subsidiary

provides the parent firm with an indefinite American style option to buy back the remaining

ownership from the minority shareholders or to sell out its ownership to a third-party.

7 The divestiture gains hypothesis posits that the carve-outs help the parent firms improve investment efficiency, focus on their core businesses, and reduce agency costs by aligning managers’ and shareholders’ interests through writing effective contracts (Hulburt et al., 2002; Vijh, 2002).

8

The exercise of this option depends on the value of the underlying synergy between the

parent and subsidiary. These synergies (operational, financial, etc.) can be positive or negative.

The positive value of the synergy indicates that the parent is better off by keeping 100%

ownership in the carved-out subsidiary. Thus, the parent can achieve synergistic gains such as

lower transaction costs than what it would gain in arm’s length transactions, and it can avoid

losses due to the ‘disincentive’ effect. The negative value of the synergy implies that the parent

is better off by removing the carved-out subsidiary from its portfolio. Therefore, the parent may

decide to sell its ownership to a third-party. We conjecture that if the parent’s motive is to unlock

the value of a subsidiary, then its intentions are likely to ascertain its synergy with the subsidiary,

and it would like to possess the real option of re-acquiring or selling off the remaining portion of

the subsidiary. Therefore, our first hypothesis is:

H1 : The parent’s motive of unlocking the value of the subsidiary suggests a higher

likelihood of the ECO’s acquisition.

2.2. Post-IPO parental control and the acquisition of a carve-out

In this subsection, while forming the hypothesis on the relationship between the post-IPO

parental control and the acquisition of the carved-out subsidiary, we mainly refer to two

mechanisms by which the parent can exert its undue influence over the carve-out. These are

parent retained ownership and its ongoing business connections with the carve-out.

The parent firm obtains a real option to re-acquire or to sell off the remaining portion by

retaining the majority ownership in the carved-out subsidiary (Perotti and Rossetto, 2007). The

majority ownership also helps the parent firm obtain the approval of the ECO board with less

effort should it decide to re-acquire the subsidiary, because through majority ownership the

9

parent can appoint its nominees to the carve-out’s board. Even in the case of a third-party

acquisition, the bidder effectively needs to convince only one shareholder (the parent firm) to

tender shares, which increases the likelihood of acquisition. In addition, majority ownership

creates less-dispersed ownership in the carve-out, which helps mitigate the free-rider problem as

pointed out in Grossman and Hart (1980). Majority ownership also allows the parent firm to

appoint its past employees to the key management positions in the carve-out. These top

executives can potentially affect the outcome of a major corporate event such as acquisition.

Therefore, the majority ownership in a post-IPO carve-out suggests an increase in the likelihood

of a carve-out’s acquisition.

Further, the property rights theory of Grossman and Hart (1986) and Hart and Moore

(1990) suggests that when Company A and Company B have a business relationship and

Company A has incentives to control assets and resources of Company B, then Company A will

maintain ownership in Company B. For ECOs, based on the predictions of the property rights

theory, Boone (2003) finds that the parent firms maintain high ownership in carve-outs if they

have a product-market or financial relationship. Therefore, we conjecture that if the parent and

subsidiary are linked through long-term business relationships such as product-market and

financial, then the parent firms are likely to retain majority ownership in the subsidiary which

will increase its likelihood of acquisition. Therefore, our second hypothesis is:

H2 : Majority ownership by the parent firm in the post-IPO carve-out and ongoing

business connections between the parent and the ECO increase the likelihood of acquisition of

the ECO.

The parent through its control over the subsidiary can impact the level of acquisition

premium. In the case of re-acquisitions, it is reasonable to claim that the parent may expropriate

10

wealth of the minority shareholders. However, the incentive to expropriate minority shareholder

wealth will be weaker when the parent retains a larger fraction of the ECO because a smaller

fraction of any premium paid will accrue to the minority shareholders.8 Additionally, the parent

firm’s re-acquisition bid needs to be approved by a special committee of independent directors

who do not have any vested interest with the parent firm. Therefore, the difference in the

acquisition premium between a third-party acquisition and a parent re-acquisition might be

insignificant. Indeed, prior empirical findings suggest mixed views. On the one hand, Slovin and

Sushka (1998) analyze a sample of parent-subsidiary mergers that also includes mergers of

equity carve-outs. As per their study, for the period 1970-1993, the subsidiary announcement day

return is 19% for 105 parent re-acquisitions; whereas that statistic is 21% for 38 third-party

acquisitions, and the difference between the two is statistically insignificant. On the other hand,

Atanasov et al. (2010) show the instances when the parent firms deliberately transfer risk to the

publicly-traded subsidiaries and expropriate wealth from the minority shareholders. These mixed

findings preclude a decisive hypothesis about the minority wealth expropriation in the case of

equity carve-outs, and we rely on our data and analyses to guide us on this.

2.3. Anti-takeover provisions in a carve-out and its acquisition

Managers adopt anti-takeover provisions in the charter of a firm mainly to avoid the

external market for corporate control.9 Ambrose and Megginson (1992) show that the probability

of acquisition decreases when the firm uses blank-check preferred stock – a form of an anti-

takeover provision. Megginson (1990) reports that the trading price and the acquisition premium

8 We thank the referee for bringing this important point to our attention. 9 For a review on different forms of anti-takeover provisions, see Gompers et al. (2003). For the impact of anti-takeover provisions on the performance of a spin-off parent firm, see Chemmanur et al. (2010).

11

of the superior voting shares are higher than those of the otherwise equivalent class of restricted

voting shares. In the case of IPOs, Field and Karpoff (2002) show that the probability of

acquisition of an IPO decreases when it has anti-takeover provisions in its charter at the time of

the IPO. Therefore, our next hypothesis is:

H3 : Anti-takeover provisions in the charter of an ECO decrease the likelihood of its

acquisition, and increase the level of acquisition premium.

3. Data and variables

3.1. Data description

We obtain the initial sample of 619 equity carve-outs, offered over the sample period of

1986 to 2004, from the Security Data Corporation (SDC)’s new issues database and issues of the

‘Mergers and Acquisitions’ magazine.10 From this sample, we eliminate carve-outs for which

parents/carve-outs are mutual trusts, limited partnerships, foreign firms, finance firms, limited

liability firms, and joint venture firms. We also exclude observations which are unit offerings,

target stocks, spinoffs, and for which data are missing from the Center of Research in Security

Prices (CRSP) tapes for the parent/carve-out. This screening reduces our sample to 295 carve-

outs. Finally, we eliminate carve-outs for which the parent firms have already announced plans

to divest their remaining ownership11 (44 carve-outs) and the data are missing in the (Q-data)

microfiche (29 carve-outs). This yields a final sample of 222 carve-outs from 199 parent firms. It

contains wholly-owned (163 carve-outs) and partially-owned (59 carve-outs) subsidiaries.

10 The cutoff year of 2004 allows us to follow all carve-outs for at least a three-year period, which provides sufficient time for parents to fully divest or re-acquire their subsidiaries should they choose. 11 In these cases, the parent firms generally announced plans to divest their remaining portion within a year of IPO by tax-free spinoffs. For more on such carve-out/spinoff combination transactions, see Thompson and Apilado (2006).

12

For each carve-out, we collect the parent firm’s reason for conducting a carve-out from

news articles in LexisNexis®. The ownership, board composition, top management team, and

business relationship data are from SEC filings including proxy statements, 10-Ks, and

prospectuses. We collect merger announcement dates and merger related details such as offer

price, exchange ratio, and winning bidder from news articles in LexisNexis® and Factiva®, and

available proxy statements before the acquisition. In order to avoid errors due to discrepancies in

the Standard Industrial Classification (SIC) codes in the Compustat and CRSP databases (Kahle

and Walkling, 1996), we collect SIC codes primarily from LexisNexis® and SEC filings, and the

missing ones from SDC, Compustat, and CRSP, in that order. We obtain offer size data from

Factiva®, SEC filings, and SDC. Finally, we extract data on the time-to-acquisition, size of the

carve-out, and size of the parent firm from CRSP.

3.2. Dependent variables

For the logit analysis on the probability of acquisition, we follow Field and Karpoff

(2002) and assign a value of one to a carve-out that was acquired within five years from its IPO

date, and zero to a survived one. For the hazard analysis, we define Acquisition Time as the

number of months between the last and the first trading dates of a carve-out as given in CRSP.

For carve-outs which are actively traded as of December 31, 2007, we take this date as the last

available trading date.

For the analysis on acquisition premium, we use three approaches to compute the level of

premium. First, we consider the possibility of an information leakage prior to the merger

announcement (Schwert, 1996). The variable Acquisition Premium_42 is the ratio of the price

offered per share of a carve-out to the carve-out’s price per share on the 42nd trading day prior to

13

the merger announcement, minus one. For the stock-to-stock exchange, we compute the carve-

out offer price using the available exchange ratio and the bidder’s price on the announcement

day. For five acquired carve-outs, since we do not find the price on the 42nd trading day prior to

the announcement, we use the price on the sixth trading day prior to the announcement.

For the second and the third approach of computing the acquisition premium, we follow

Moeller (2005). We define Acquisition Premium_Returns as the buy and hold (excess) return

during the merger announcement date. Specifically, we compute the carve-out’s buy and hold

return for 11 trading days starting with the five trading days prior to the merger announcement

and subtract the buy and hold return on the CRSP value-weighted index for the same time

period. Finally, we define Acquisition Premium_06 which is similar to Acquisition Premium_42,

except that we compute the ECO price on the sixth instead of 42nd trading day prior to the merger

announcement.

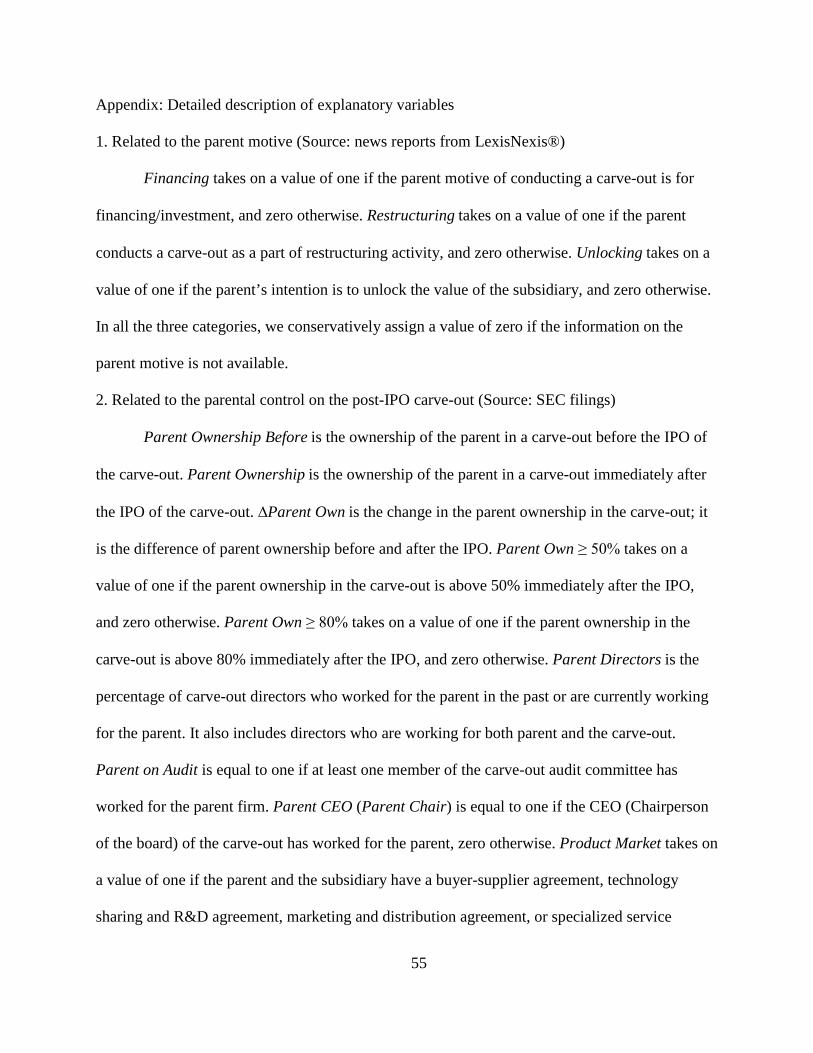

3.3. Explanatory variables

We group our explanatory variables into five sets of variables. The first set pertains to the

motive of the parent firm to undertake an equity carve-out. The second set consists of factors

through which the parent can exert control over the post-IPO carve-out. The third category

contains our proxies for the anti-takeover provisions in a carve-out and its industry structure. The

fourth category represents the set of control variables. Finally, the fifth category contains the set

of variables which are related to a merger transaction. The variable definitions, their detailed

description, and the data sources are available in the Appendix.

3.3.1. Factors related to the parent motive

14

We extensively review the news reports at the time of the IPO announcements and

identify three categories of reasons for conducting an equity carve-out. These are

financing/investing, restructuring, and unlocking the value.12 These are not mutually exclusive

categories due to the cases when the parent provides multiple reasons for conducting a carve-out.

There are also other instances when the reason for conducting a carve-out does not fall into any

of these three categories, for example, the reason of conducting a carve-out due to apartheid

concerns or to meet government regulations on an antitrust lawsuit; we note these cases under

the other category.

First, if a parent undertakes a carve-out for general corporate purposes, for working

capital, for repayment of debt, for capital expenditures, for possible acquisitions, or for taking

out the parent from financial distress, we consider these instances in the financing/investing

category. Second, we define the restructuring reason as the instances when the parent

consummates the carve-out transaction to focus on core business or as part of a larger

restructuring plan. Finally, the category of unlocking the value consists of the cases when the

parent undertakes a carve-out to create a liquid market for the subsidiary shares, to allow the

market to value the subsidiary, or to create a liquid market for employee shareholders.13

3.3.2. Factors related to the post-IPO parental control over the carve-out

We study the parental role in the post-IPO carve-out via equity ownership, board and

audit committee composition, top-management team, and long-term business relationships. The

12 For more detailed examples of the language used by parent firms when they announce carve-outs for unlocking the value, see Desai et al. (2011); Chemmanur and Liu (2011); and Nanda and Narayanan (1999). 13 We also define the parent’s motive to unlock the value by considering only those announcements in which the parent undertakes an ECO to allow the market to value the subsidiary. Our results remain qualitatively similar with this definition.

15

most direct way the parent firm can exert control over the ECO is by retaining majority

ownership. We also define the reduction in parent ownership as the difference of parent

ownership before and after the IPO; a smaller value of this variable indicates a higher level of

parental control over the post-IPO carved-out subsidiary. To capture the non-linear relation

between the parent ownership and our dependent variables, we consider two indicator variables

reflecting whether the parent retains above 50% and above 80% ownership.

The ownership allows the parent firm to appoint its personnel as directors and top-

executives of the carve-out firm. Directors in the carve-out can be one of three types: insider,

outsider, or parent representative. Parent representative directors are current or past employees of

the parent firm. Following Boone (2003), we define the top-management team of a carve-out

being affiliated with the parent firm if the chairman, CEO, or president of a carve-out is either a

current or past employee of the parent firm. We also measure the parent influence over the audit

committee of the carve-out by identifying whether any of the parent’s past or current employees

serve on that committee.

We define a product-market relation between the parent firm and the ECO when they

have buyer-supplier, technology sharing and research and development, marketing and

distribution, or specialized service agreements (Boone, 2003). Similarly, we define a financial

relationship when the parent and the ECO are involved in a long-term financial agreement

through letters of credit, bank guarantees, or term loans (Boone, 2003). We also consider

industry relatedness of the parent and subsidiary to capture the possibility of parental

involvement in the subsidiary if they both are in the same industry.

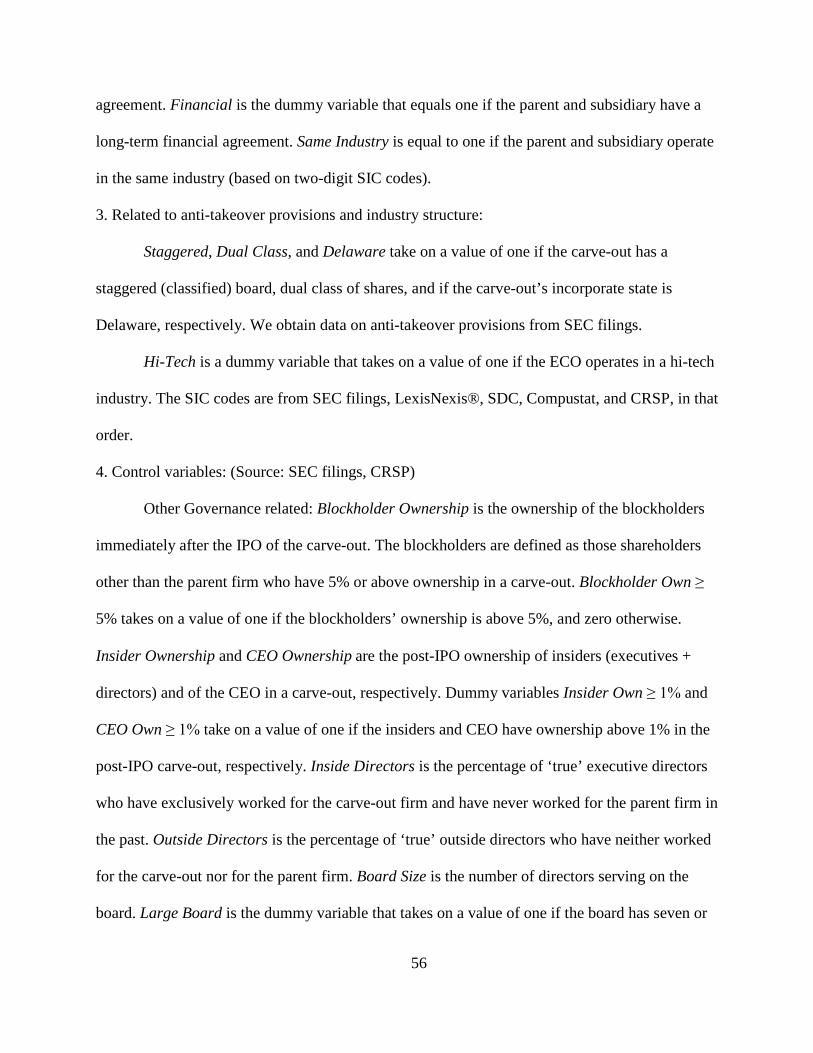

3.3.3. Factors related to anti-takeover provisions and industry structure of a carve-out

16

We use three types of anti-takeover provisions. These are whether a carve-out has a

staggered board, two classes of shares, and whether its state of incorporation is Delaware. We

restrict our analysis to only three anti-takeover defenses due to unavailability of (a) IPO

prospectuses for the ECOs prior to the year 1996 and (b) takeover defenses on standard

databases such as the Investor Responsibility Research Center (IRRC) for an ECO firm because

of its small size. Regarding the industry structure of a carve-out, we assign a dummy variable

that takes on a value of one if the firm operates in the hi-tech sector (SIC code of 28, 357, 36, 38,

or 737).14

3.3.4. Other control variables

Governance related: We measure ownership of the CEO, insiders (executives and

directors), and blockholders. Because ownership data are not reported when the insider/CEO

owns less than 1% and the blockholder owns less than 5% of the outstanding shares, we use both

continuous and indicator variables for insider/CEO and blockholder ownership. Regarding the

directors other than the parent directors, insider directors are the employees of the carve-out but

have no relationship with the parent firm. Outside directors are not the employees of the carve-

out or of the parent firm. We measure board size as the number of directors immediately after the

IPO. Board size is considered large when the number of directors is above the median board size.

We capture the CEO power by measuring whether she is also a chairperson of the board.

Size and performance related: We control for the relative size (ratio of the carve-out size

to the parent firm size), IPO offer size, and carve-out stock market performance in our analysis.

14 We follow the definition of a hi-tech industry in Benou et al. (2008), who in turn rely on the SDC. An example of a hi-tech carve-out is Networth Inc (SIC: 3577) which went public on 11/25/1992 and is in the business of computer peripheral equipments. Its parent, Tandem computers (SIC: 7377), also operates in a hi-tech industry.

17

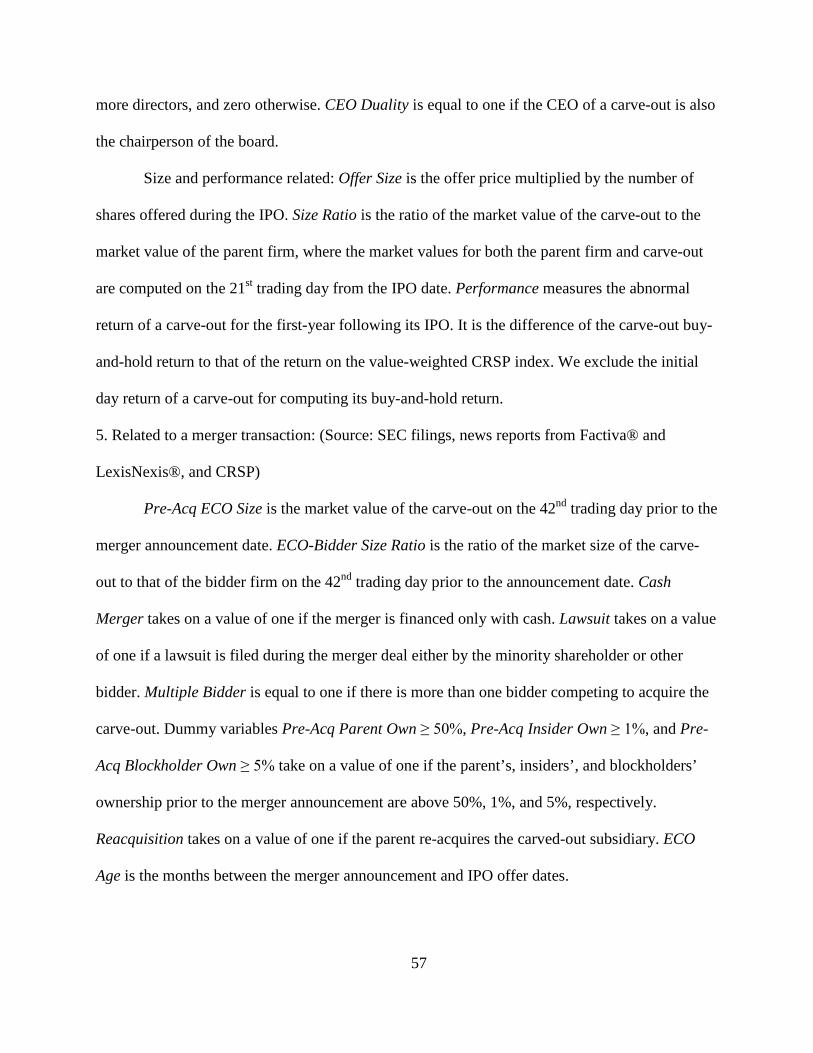

3.3.5. Factors related to a merger transaction

For analysis on the level of acquisition premium, we also control for variables that are

related to a merger transaction. These are whether a lawsuit is filed during the merger process,

the ratio of bidder size to target size, the carve-out size prior to its merger, whether more than

one bidder attempts to acquire the carve-out, and whether the transaction is financed through

only cash. All these factors are likely to impact the acquisition premium.

3.4. Descriptive statistics

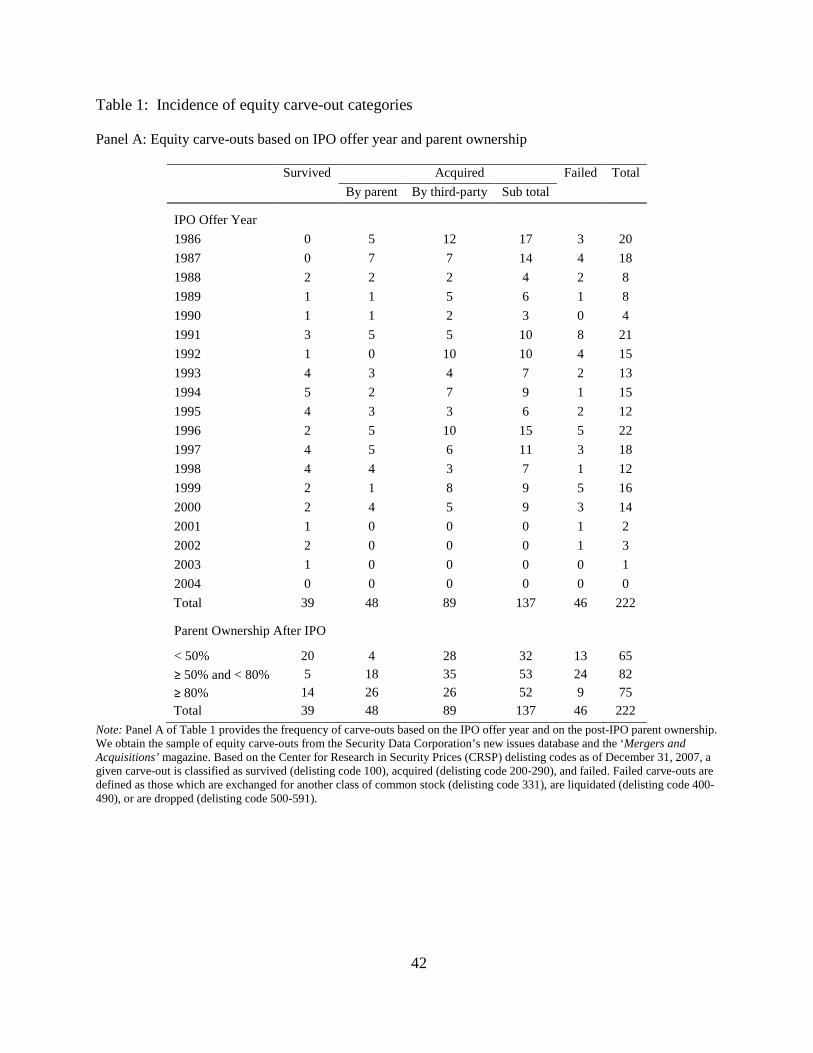

In Panel A of Table 1, we report the incidence of carve-outs based on offer year and post-

IPO parent firm’s ownership. We classify carve-outs into three categories based on the CRSP

delisting codes as of December 31, 2007: survived, acquired, and failed carve-outs. Survived

carve-outs with a delisting code of 100 represent 18% of the sample and are still actively traded

in the market. Acquired carve-outs with a delisting code between 200 and 290 represent 62% of

the sample and are acquired by either the parent firm (22%) or a third-party (40%), and trading

activities ceased after the acquisition date. Failed carve-outs represent the remaining 20% of the

sample (46 carve-outs); of which 44 carve-outs are delisted (delisting code between 500 and

591), one is liquidated (delisting code between 400 and 490) and one is exchanged for another

class of common stock (delisting code of 331).

[Insert Table 1 about here]

In terms of the year-wise distribution of the sample, the majority of ECOs are in the years

1996, 1991, and 1986, with 22, 21, and 20 carve-outs, respectively. The subsample of acquired

18

ECOs display that 17, 15, and 14 transactions are in the years 1986, 1996, and 1987,

respectively. In the period from 2001 to 2004, there are only seven carve-outs in our sample.15

We also examine the incidence of carve-outs for the parent ownership after the IPO. We

divide the sample into three categories: those with post-IPO parent ownership less than 50%,

between 50% and 80%, and more than 80%. The largest number of deals occurred in the

ownership category between 50% and 80% (about 37%), followed by the greater than 80%

category (about 34%), and the less than 50% category (about 29%). The parent firms retained

majority (above 50%) ownership in 77% of acquired carve-outs, whereas, in survived carve-outs

that statistic is only 49%. This difference of parent ownership in survived and acquired carve-

outs suggests a possible relation between parent ownership and carve-out acquisition. Similar to

the findings of Klein et al. (1991), 92% of the re-acquired carve-outs in our sample have parent

ownership above 50%, which suggests that the probability of re-acquisition of carve-out

increases with the post-IPO parent ownership.

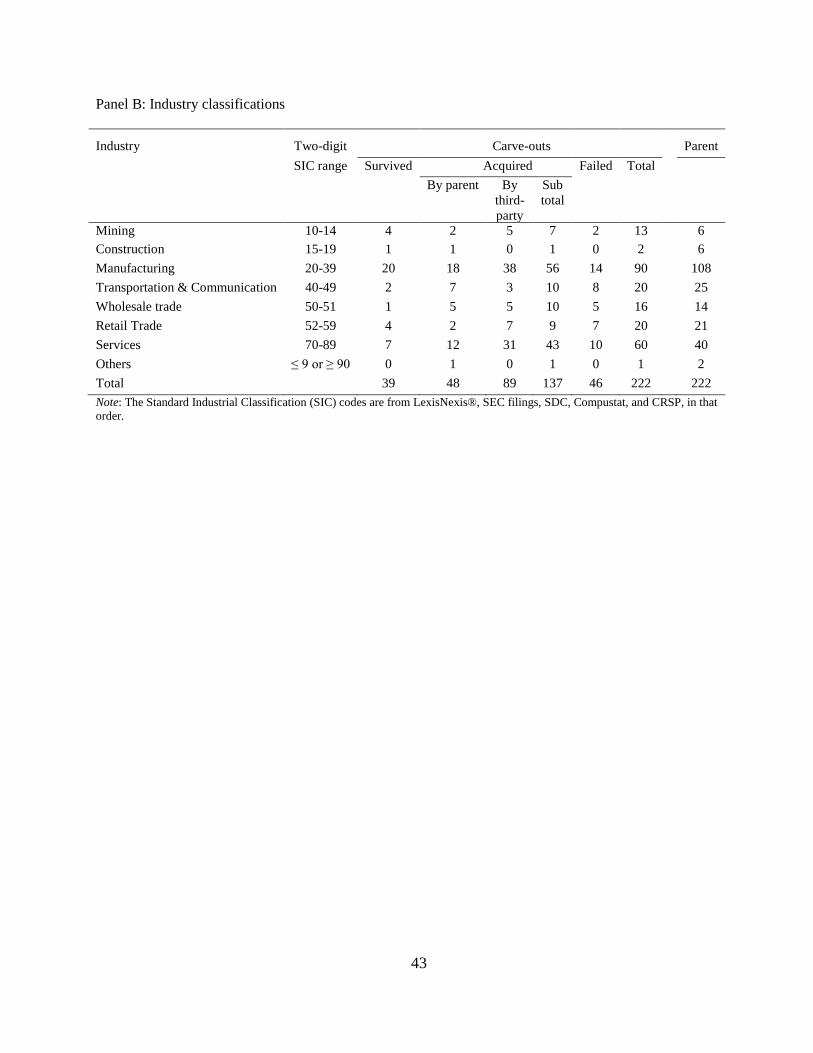

In Panel B of Table 1, we show the incidence of carve-outs and parent firms based on

industry using two-digit SIC codes. Although there are 199 parent firms which conducted a total

of 222 carve-outs, for simplicity we consider a combination of one parent firm and one carve-

out. The majority of the ECOs operate in the manufacturing industry (41%) and service industry

(27%). Also, these industries significantly represent the acquired carve-outs sample with 41%

and 31% of the sample, respectively. Based on our sample, 72% of the carve-outs operating in

the service industry and 62% operating in the manufacturing industry are eventually acquired.

Among the parent firms, 49% and 18% of sample firms operate in the manufacturing and service

sectors, respectively. 15 During this period, we exclude 13 observations of carve-out/spinoff combination in which the parents have already indicated the intent to divest their remaining portion.

19

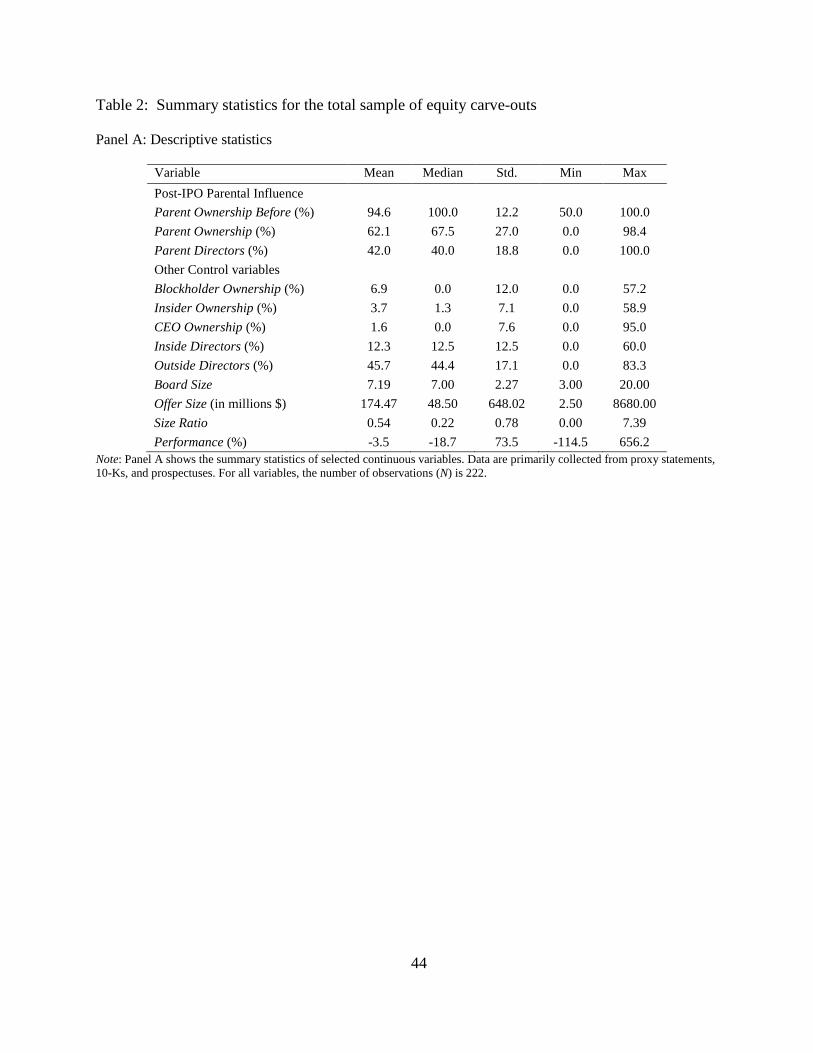

In Panel A of Table 2, we report summary statistics of variables pertaining to post-IPO

parental influence on the carve-out and our chosen controls for the total sample. The parent

ownership prior to the carve-out has a mean of around 95% and median of 100%, whereas parent

ownership subsequent to the carve-out has a mean of 62% and median of 68%. The high post-

IPO parent ownership in a carve-out suggests that the parent firm has an interest in controlling

the subsidiary, which might not be possible through other forms of restructuring such as spinoffs

and asset sales.16 The parent representative directors constitute, on average, 42% of the carve-out

board, which indicates the possibility of the parent firm’s role in the operating and strategic

decisions of a carve-out. Blockholder ownership has a mean of around 7%. Similarly, insider and

CEO ownership in a post-IPO carve-out on average are around 4% and 2%, respectively. The

number of directors serving on the carve-out has a median of seven. The carve-out offer size has

a mean of $174.5 million, a median of $48.5 million, and minimum and maximum values of $2.5

million and $8.7 billion, respectively. The median size of a carve-out is 22% that of the parent

firm. For our sample firms, the average first year excess return over the value-weighted CRSP

index return has a mean of -3.5%, which shows that in the short-run the ECOs tend to

underperform.

[Insert Table 2 about here]

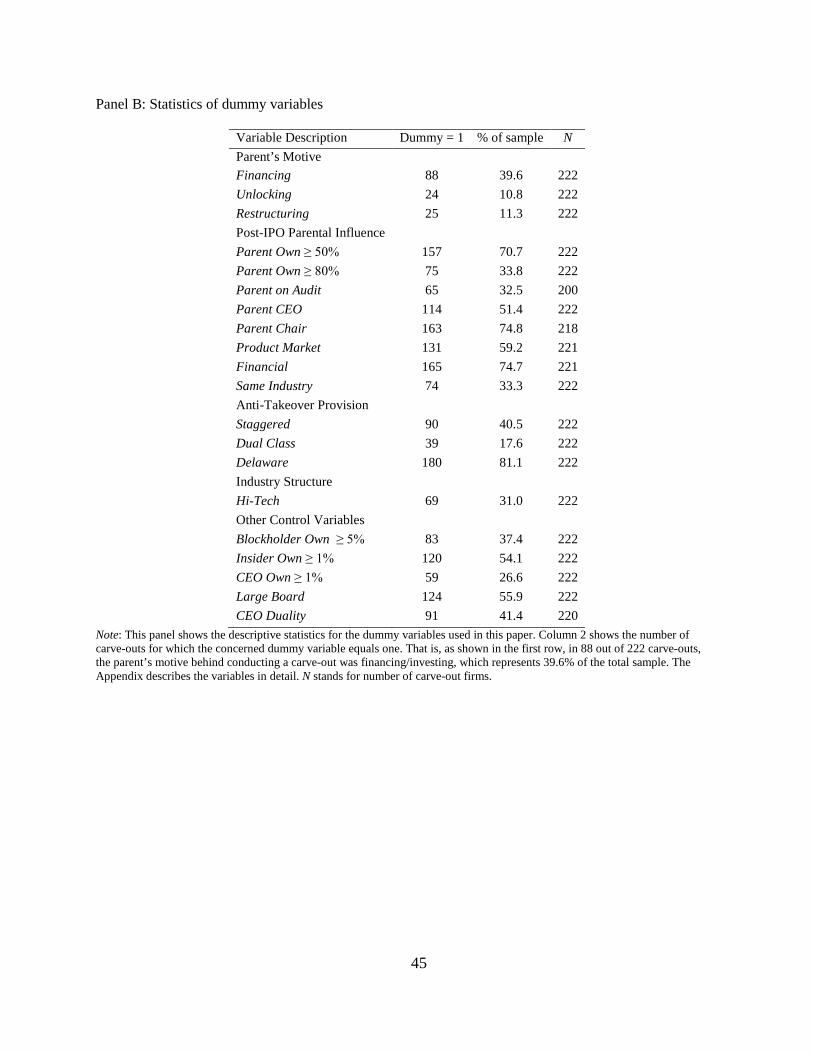

Panel B of Table 2, we report summary statistics of dummy variables that proxy for the

parent’s motive and its influence, anti-takeover provisions, industry structure and other control

variables. In around 40% of our sample firms, the reason for conducting a carve-out is for

financing related or for investment related activities. We also note that in around 11% of our

16 We also notice that in 13 out of 222 carve-outs the parent retained no ownership after the IPO of the subsidiary. In four of these carve-outs, the parent and subsidiary are tied through product-market agreements, and in none of these 13 carve-outs, the parent’s motive for undertaking a carve-out is to unlock the subsidiary’s value.

20

sample firms the parent conducts a carve-out to unlock the subsidiary’s value. In 157 out of 222

equity carve-outs, parent ownership is above 50%; the board-chairperson and CEO are

associated with the parent firm in 75% and 51% of carve-outs, respectively. These numbers

suggest the parent firm's involvement in the operating and strategic decisions of the publicly-

traded subsidiary. Regarding the business relationships, 59% of the carve-outs in our sample are

linked to their parent firms through product-market agreements and 75% are linked through

financial agreements. These statistics on business relationships suggest an alternative

mechanism, other than ownership, by which the parent firm can control the subsidiary (Atanasov

et al. 2010). In 33% of our sample firms, the ECO and parent have the same two-digit SIC code.

In our sample around 41% (18%) of ECOs use a staggered board (dual class shares). We

also observe that 69 carve-outs operate in the hi-tech industry, representing 31% of our sample.

Although the parent firms generally retain significant ownership in the ECO, we also observe a

notable presence of blockholder, insider (executives plus directors), and CEO ownership in 37%,

54%, and 27% of our sample firms, respectively. Finally, in 91 out of 220 carve-outs, the CEO is

also the chairperson of the board. Out of 222 carve-outs, we could not obtain data on audit

committee, business relationship, chairperson’s affiliation with parent, and CEO duality for 22,

one, four, and two carve-outs, respectively.17

[Insert Table 3 about here]

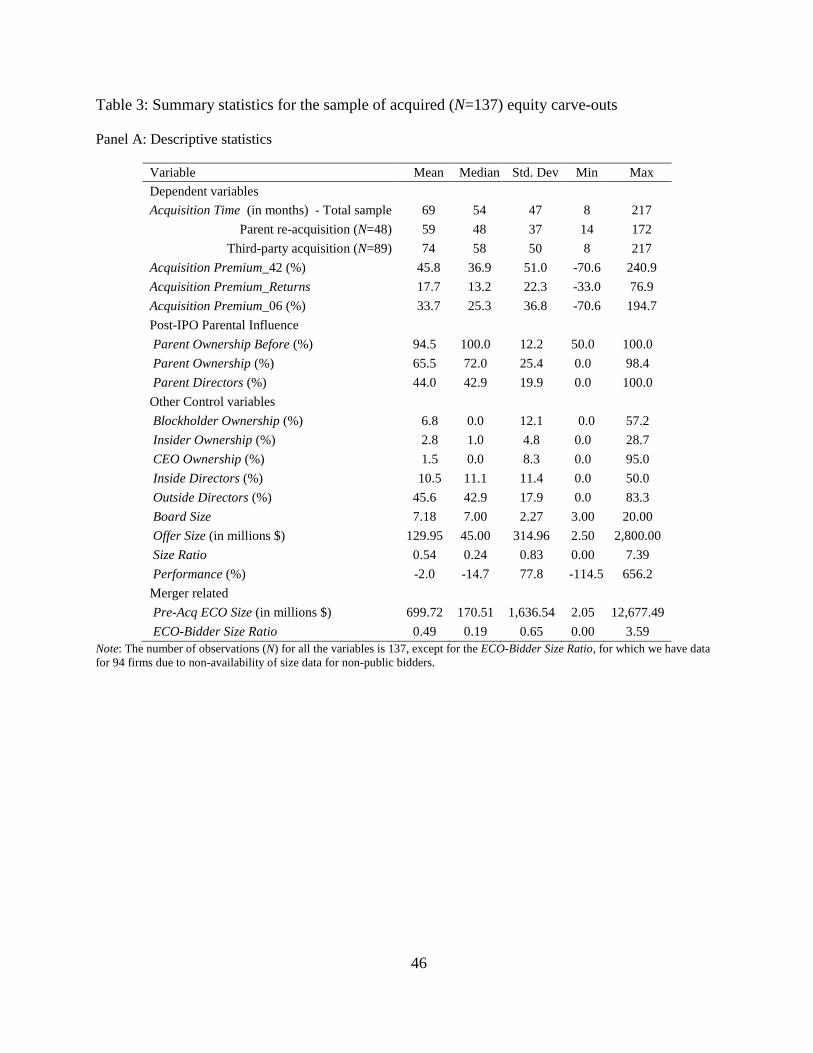

In Table 3, we report statistics similar to those reported in Table 2 for the sample of

acquired carve-outs. As shown in Panel A of Table 3, the mean and median time-to-acquisition

are 69 and 54 months, respectively. The minimum and maximum time-to-acquisition is eight and

217 months, respectively. Out of 137 acquired carve-outs, 48 are re-acquired by the parent firm, 17 In empirical analyses, we conservatively assign values of zero for these missing data; results remain the same without such adjustment.

21

and 89 are acquired by a third-party. The average and median time-to-acquisition in the case of

parent re-acquisitions are 59 and 48 months, respectively, whereas those statistics are 74 and 58

months, respectively for third-party acquisitions. These differences suggest that the re-

acquisitions tend to occur sooner than the third-party acquisitions. The average and median

acquisition premium, based on the price of the ECO on the 42nd trading day prior to the merger

announcement date, are 46% and 37%, respectively. However, when we compute the premium

using the price of the target on the sixth trading day prior to the announcement those statistics are

34% and 25%, respectively; this lower level of premium suggests a possible information leakage

prior to the merger (Schwert, 1996). The median post-IPO parent ownership in acquired carve-

outs is 72%.

As shown in Panel B of Table 3, around 77% of acquired carve-outs have majority parent

ownership. We also observe that around 56% of the acquired carve-outs have parent ownership

above 50% prior to their acquisition. In our sample of acquired carve-outs, 31% have the parent

and carve-out in the same industry and 16% have dual-class shares. Finally, 58% of carve-out

mergers in our sample are financed through only cash, and in around 11% of mergers a lawsuit is

filed either by a competing bidder or by the minority shareholders.

4. Results

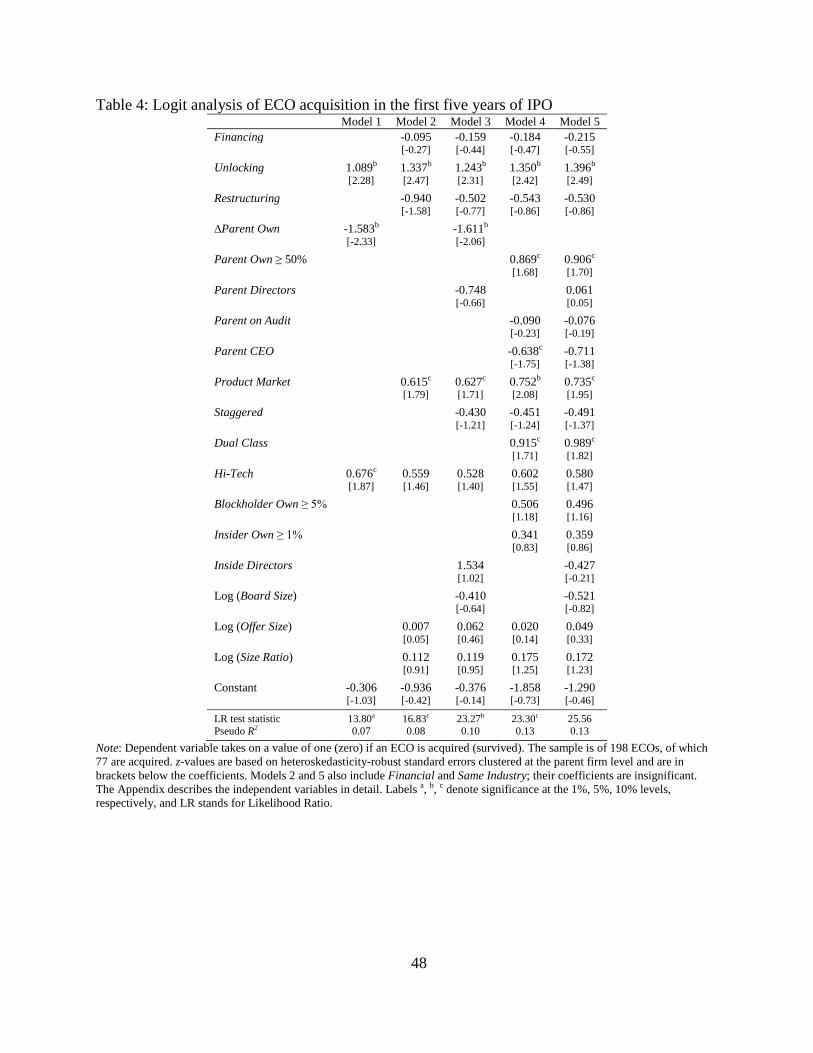

4.1. Likelihood of acquisition: Probability of acquisition

In Table 4, we report the results of the logit analysis in which the dependent variable

Acquired takes on a value of one if the carve-out is acquired and zero if the carve-out is traded in

the market (‘survived’), within five years of its IPO offer date.18 For this analysis, following

18 Because our cut-off date is 12/31/2007, we could not follow one carve-out (IPO offer date 11/20/2003) for the full

22

Field and Karpoff (2002), we ignore the carve-outs which are delisted or have gone bankrupt

(‘failed’) within five years of their IPOs (24 observations). Since we are restricting this sample to

carve-outs that are acquired within five years of IPOs, our overall sample is of 198 carve-outs, of

which 77 are acquired.

Our primary specification (Model 1) is:

𝐴𝑐𝑞𝑢𝑖𝑟𝑒𝑑𝑖 =𝑒𝑦𝑖

1 + 𝑒𝑦𝑖

(1)

Where, 𝑦𝑖 = A0 + A1 × 𝑈𝑛𝑙𝑜𝑐𝑘𝑖𝑛𝑔𝑖 + A2 × ∆𝑃𝑎𝑟𝑒𝑛𝑡 𝑂𝑤𝑛𝑖 + A3 × (𝐻𝑖 − 𝑇𝑒𝑐ℎ)𝑖

[Insert Table 4 about here]

As reported in Model 1, the coefficient of 1.089 on the dummy variable

Unlocking indicates that when the reason for undertaking a carve-out is to unlock the value, the

odds of that carve-out to get acquired increase by a factor of 2.97 over the instance when the

reason is other than to unlock the value. In terms of the probability, if the reason for undertaking

a carve-out is to unlock the value, then the probability of acquisition for that carve-out changes

from 0.5 to 0.75; this change is significant at the 5% level (z-value: 2.28).19,20 The coefficient of

-1.583 on ∆Parent Own suggests that an additional one-percentage decline in the post-IPO parent

ownership in a carve-out causes a reduction of 0.791% in the probability of acquisition of this

carve-out.21 The coefficient of 0.676 on Hi-Tech shows that if the carve-out operates in the hi-

five years. 19 More precisely, the increase in odds is equal to 𝑒1.089 = 2.97. Assuming that if there are reasons other than to unlock the value, then the probability of acquisition p1 = 0.5, and the odds = 1. When the reason is to unlock the value, the new odds = 2.97, which will make new p1 = 0.748. 20 In all our multivariate analyses, t and z values are based on heteroskedasticity-robust standard errors clustered at the parent firm level. 21 More precisely, assuming that before the IPO, the parent owns 100% of the subsidiary. In the first case, the parent retains 81% (i.e. it sells 19% of its ownership in IPO) of the subsidiary, and in the second case, the parent retains 80%. Thus, ∆Parent Own in the first (second) case is 19% (20%), and the change in ∆Parent Own is equal to 0.01, and the new odds = 𝑒−1.583 × 0.01 = 0.9843. Therefore, the new probability of acquisition is 0.4960, which was previously 0.5.

23

tech industry, then there is approximately a 66%(34%) chance that this carve-out will be

acquired(survived). This result supports findings of Kohers and Kohers (2000) who conjecture

that the likelihood of acquisition will be higher in the hi-tech industry due to above-average

returns in that industry.

In Models 2 to 5, we change our primary specification to incorporate other factors of

interest and controlling variables. As mentioned in Section 2.2, the parent is likely to retain

majority ownership in the carved-out subsidiary if it has business relations with the subsidiary. In

that case, the effect of post-IPO parent ownership may confound the effect of ongoing business

connections on the carve-out’s acquisition. Therefore, to separate these two effects, we exclude

∆Parent Own and include variables related to the business relationships in Model 2. The

coefficient of 0.615 on dummy variable Product Market indicates that the odds of acquisition

increase by a factor of 1.85 when the parent and subsidiary are connected through a product-

market relationship, and this change is significant at the 10% level (z-value: 1.79).

In Models 4 and 5, we use a dummy variable Parent Own ≥ 50% instead of a continuous

variable ∆Parent Own. As shown in Model 4, the coefficient of 0.869 on Parent Own ≥ 50%

suggests that the odds of ECO acquisition increase by a factor of 2.38 when the parent retains

majority ownership in the post-IPO carve-out, and this difference is significant at the 10% level.

In Models 2 and 5, we include variables Financial and Same Industry. For brevity, we do not

show their coefficients, due to their statistical insignificance.

As shown in Model 4, the coefficient of 0.915 on Dual Class indicates that the odds of

acquisition increase by a factor of 2.50 when the carve-out has dual class shares compared to the

case when it has shares with only one class. This change is significant at the 10% level. In

addition, in unreported regressions, when we add the variable Dual Class in our Models 1 to 3,

24

we find its insignificant impact on the likelihood of acquisition in Models 1 and 3, and in Model

2, its impact is significant at the 10% level. This counterintuitive finding to our hypothesis H3, at

first, suggests that the anti-takeover provisions actually increase the likelihood of acquisition in

the case of carve-outs. One plausible explanation for this finding is: in examining the SEC

filings, we find that in the case of ECOs with dual class shares, the parent firm generally retains

full ownership of the superior voting shares while it retains minimal or no ownership of the

inferior voting shares. In this manner, the parent voting ownership increases significantly

whereas its cash flow ownership is negligible. We define the ownership based on the voting

rights. Therefore, this effect of dual class shares is possibly the effect of parent ownership in the

post-IPO carve-out.22 If we examine the effect of another form of anti-takeover provision

(Staggered) in Models 3 to 5, it is negative albeit statistically insignificant. Therefore, we do find

some support of our hypothesis H3.

In an unreported analysis, we also test the difference between the estimated coefficients

of various categories of parent motives. For example, in Model 2, the test of difference of

estimated coefficients for Unlocking and Financing has a 𝜒2 value of 6.02 with a p-value of

0.01. Similarly, the estimated coefficient for Unlocking is significantly higher than that of the

Restructuring, with a 𝜒2 value of 6.74; whereas there is no significant difference in the estimated

coefficients of Financing and Restructuring (𝜒2 = 1.82). These results suggest that the

probability of acquisition significantly increases when the parent’s motive is to unlock the value

of the subsidiary compared to that when the motive is either to finance or to restructure the

operations.

22 For example, in our sample of 39 ECOs with dual class shares, the average parent ownership is 82.6% and for 183 ECOs without dual class shares, that statistic is 57.7%; the difference is significant at the 1% level.

25

Overall, the results reported in Table 4 indicate that the probability of ECO acquisition

increases when the parent’s motive for conducting a carve-out is to unlock the value, with the

increase in parent ownership in the post-IPO carve-out, and when the parent and subsidiary are

connected through a product-market agreement. These findings support our hypotheses H1 and

H2.

4.2. Robustness check

Our results of the logit analysis on the ECO acquisition can potentially produce biased

results if we ignore the fact that at the time of making the subsidiary a public company, the

parent could choose whether to conduct a carve-out or to conduct a spinoff. In addition, if the

parent decides to conduct a carve-out, then it can determine the level of ownership it needs to

retain in the carved-out subsidiary. If we ignore the former, i.e., the choice between a carve-out

and a spinoff, our results are likely to be biased due to self-selection. And if we ignore the latter,

i.e., the possibility that the parent ownership in the post-IPO carve-out is endogenously

determined, our results may be incorrect due to endogeneity. To check our results for sample

selection bias we merge our carve-out sample with a sample of spinoffs and perform a two-step

Heckman procedure. To check our results for endogeneity bias, we repeat our analysis using

exogenous instrumental variables. Our results remain the same under both sets of analyses and

there is no indication that our findings are affected by selection or endogeneity bias. Details of

these tests are in Desai et al. (2011).

4.3. Likelihood of acquisition: Time-to-acquisition

26

After an IPO, a carve-out can be actively traded, failed, or acquired in the market. The

right-censored observations in our dataset are those ECOs that are either actively traded or failed

as of the cut-off date, December 31, 2007. The usefulness of estimating the parameters using the

survival (failure) / time-to-event analysis over the logit or probit analysis is its ability to

incorporate information of right-censored observations and the time till the carve-out survives in

the market before its acquisition.23 We use a dichotomous variable describing the status of a

carve-out as either acquired or not-acquired (both failed and survived). When interpreting the

results of the survival analysis, we refer to the probability of failure for a carve-out as the

probability of its being acquired.

We use non-parametric and semi-parametric approaches of survival analysis to assess the

impact of our selected variables on the failure and hazard functions.24 The non-parametric

technique helps us analyze the differences in failure functions of groups based on a dummy

variable. The semi-parametric approach allows us to model the impact of utilize more than one

explanatory variables for analyzing their impact on the hazard rate of acquisition. Both

approaches make no assumptions regarding the distribution of time-to-acquisition.

4.3.1. Non-parametric analysis

The non-parametric analysis involves plotting Kaplan-Meier (K-M) failure function

estimates for groups based on the parent’s motive for conducting a carve-out, post-IPO parent

ownership, business relationship of parent and subsidiary, and industry structure of a carve-out; 23 For an application of survival analysis, see Cleves et al. (2004). 24 If t = 0 is the IPO date and t = T is the acquisition date which is a random variable, then the survival function S(t) of a carve-out is defined as the probability of its surviving until time t. Mathematically, S(t) = P(T ≥ t). The failure function is a complement of a survival function. It is the cumulative probability of failure (in our case, acquisition of a carve-out) at any given time t. Mathematically, F(t) = 1 – P(T ≥ t). The hazard function h(t) --- also known as the hazard, hazard rate --- is the probability of a carve-out to get acquired at this infinitesimal time-interval conditional on its surviving until the beginning of the interval, divided by the duration of this time-interval.

27

and then conducting statistical tests to determine whether the differences in the failure functions

are significant. We find that the probability of acquisition at any given time is higher when the

parent’s motive for conducting a carve-out is to unlock the value of the subsidiary than when the

parent does not report this motive, and this difference is statistically significant at the 1% level.

We also find that the probability of acquisition at any given time is higher for the carve-outs with

post-IPO parent ownership above fifty percent than that for the carve-outs with post-IPO

ownership below fifty percent, and this difference is also statistically significant at the 1% level.

Furthermore, the probability of acquisition is consistently higher for ECOs with a product-

market relationship with the parent than for ECOs without such product-market relationship with

the parent, and this difference is statistically significant at the 5% level. We find that firms

operating in a hi-tech industry have a higher estimated probability of acquisition. However, this

last result is not statistically significant, though it is close with a p-value of 10.3%. Finally, we

also observe that the probability of acquisition is lower when the parent’s motive is to restructure

the operations than that when the parent’s motive is other than to restructure the operations; the

difference of these two failure functions is significant at the 5% level. The actual failure function

plots and statistical test values are in Desai et al. (2011).

4.3.2. Semi-parametric analysis

We perform a semi-parametric technique using the Cox Proportional Hazard model. This

assumes that the baseline hazard, or the inherent risk of acquisition in the absence of all control

variables, is the same for each ECO.

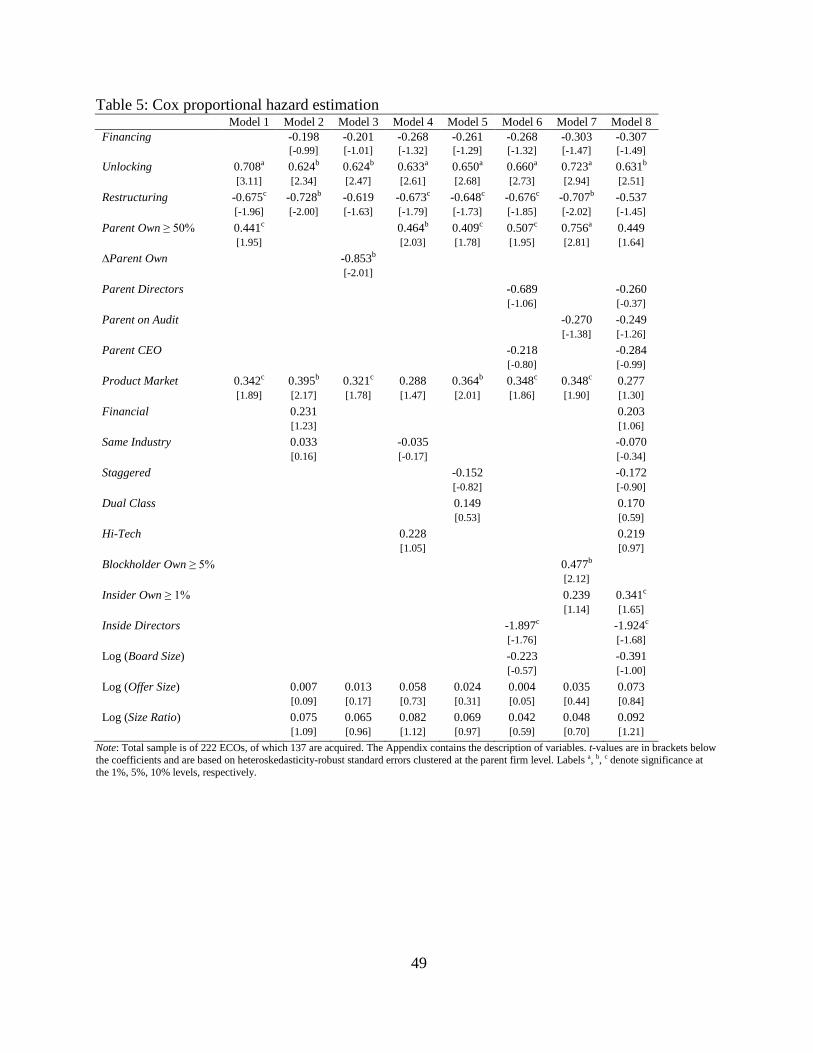

[Insert Table 5 about here]

28

In Model 1 of Table 5, we use variables which have a significant effect on the K-M

failure function estimates as discussed in Section 4.3.1. Mathematically, it is

ℎ𝑖(𝑡) = ℎ0(𝑡) × 𝑒𝑥𝑝[𝐴1 × (𝑈𝑛𝑙𝑜𝑐𝑘𝑖𝑛𝑔𝑖) + 𝐴2 × (𝑅𝑒𝑠𝑡𝑟𝑢𝑐𝑡𝑢𝑟𝑖𝑛𝑔𝑖) + 𝐴3

× (𝑃𝑎𝑟𝑒𝑛𝑡 𝑂𝑤𝑛 ≥ 50%𝑖) + 𝐴4 × (𝑃𝑟𝑜𝑑𝑢𝑐𝑡 𝑀𝑎𝑟𝑘𝑒𝑡𝑖)]

(2)

where, hi(t) is the hazard of acquisition for a given carve-out i at time t and h0(t) is the

baseline hazard function. We define the log of the relative hazard (LRH) as the natural logarithm

of the ratio of hi(t) to h0(t). That is,

𝐿𝑅𝐻 = 𝐴1 × (𝑈𝑛𝑙𝑜𝑐𝑘𝑖𝑛𝑔𝑖) + 𝐴2 × (𝑅𝑒𝑠𝑡𝑟𝑢𝑐𝑡𝑢𝑟𝑖𝑛𝑔𝑖) + 𝐴3 × (𝑃𝑎𝑟𝑒𝑛𝑡 𝑂𝑤𝑛 ≥ 50%𝑖)

+ 𝐴4 × (𝑃𝑟𝑜𝑑𝑢𝑐𝑡 𝑀𝑎𝑟𝑘𝑒𝑡𝑖)

(3)

The results of Model 1 indicate that the hazard (risk) of acquisition increases when (a) the

parent’s motive is to unlock the value; (b) the post-IPO parent ownership is above 50%; and (c)

the parent and the carve-out are tied through a product-market business agreement. The hazard of

acquisition decreases when the parent’s reason for conducting a carve-out is to restructure its

own and the subsidiary’s operations. First, the coefficient of 0.708 on Unlocking indicates that

the estimated hazard ratio of the groups based on the dummy Unlocking is 2.03.25 Therefore, the

hazard of acquisition for the carve-outs which are undertaken by the parent with a motive of

unlocking the value is 2.03 times higher than that of carve-outs where the parent undertakes the

carve-out transaction for reasons other than to unlock the value, and the difference between these

two hazard rates is significant at the 1% level (t-value: 3.11). This result supports the validity of

our hypothesis H1.

Second, the coefficient of 0.441 on Parent Own ≥ 50% shows that the risk of acquisition

for a carve-out with a majority ownership by the parent is 1.55 times higher than that for a carve-

25 More precisely, it is 𝑒0.708 = 2.0299.

29

out with less than majority ownership by the parent. This difference in hazard rates is significant

at the 10% level (t-value: 1.95). We also find that the hazard of acquisition for a carve-out

having a product-market relationship with the parent firm is higher than that for a carve-out

without such a relation, albeit the difference is significant at the 10% level. These findings

support our hypothesis H2.

Finally, the coefficient of -0.675 on the dummy Restructuring indicates that the risk of

acquisition for a carve-out in which the parent’s motive is to restructure the operations is 0.51

times that of the carve-outs in which the parent’s motive is other than the restructuring. It is

likely that when the parent with a restructuring motive consummates the equity carve-out

transaction, their main purpose is to achieve the benefits of divestitures (Hulburt et al., 2002;

Vijh, 2002) and not to prepare the carve-out for acquisition.

In Model 2, we exclude variables related to the parent ownership and include variables

measuring the ongoing financial relationship between the parent and the carved-out subsidiary,

industry relatedness, and size related controls in our Model 1. In Model 3, we modify Model 1 by

using a continuous variable reflecting the change in parent ownership before and after the IPO of

the carve-out (∆Parent Own). The coefficient of -0.853 suggests that when the parent sells an

additional percentage point of shares of subsidiaries in the IPO (i.e., the parent reduces its

ownership in the subsidiary by an additional percentage point), the hazard of the carve-out

acquisition decreases by 0.85%.26 This finding supports our hypothesis H2.

26 More precisely, refer to footnote 21, let the change in ∆Parent Own is equal to 0.01. Based on our Model 3,

𝜕(𝐿𝑅𝐻)𝜕(∆𝑃𝑎𝑟𝑒𝑛𝑡 𝑂𝑤𝑛)

= −0.853. Since the baseline hazard h0(t) remains constant, after some minor algebra we find that ℎ2(𝑡)ℎ1(𝑡)

= 𝑒𝑥𝑝(0.01 × −0.853) = 0.9915, where h2(t) and h1(t) are the hazard rates for the second and the first cases, respectively.

30

In Models 4 to 8, we add our proxies for the anti-takeover provisions, the industry

structure of the carve-outs, and other controlling factors. As shown in Model 7, at first look it

seems that the post-IPO blockholder ownership increases the hazard of acquisition. However,

when we exclude the parent ownership, the blockholder ownership loses its significance. For this

reason, we show it for only one of our specifications. As shown in Models 6 and 8, the carve-

outs with a higher percentage of inside directors tend to survive longer. Intuitively, inside

directors are those who never worked for the parent firms before. While going over the proxy

statements of these firms, we observe that these inside directors are the entrepreneurs who have

worked in the carve-out firm from its inception. At some point in the life of the carve-out, the

parent firm took over the carve-out and made it a wholly-owned subsidiary. If the carve-out

board is dominated with such founding executives as directors, it is likely that the carve-out will

survive longer in the market since the inside directors’ prime objective is likely to grow the

carve-out and not to prepare it for an acquisition. Finally, although we do not find any

statistically significant impact of our chosen anti-takeover provisions on the hazard of ECO

acquisition, the signs of their coefficients are worth mentioning. As shown in Models 5 and 8,

the coefficient of Dual Class is positive, which suggests that the presence of this anti-takeover

provision in a carve-out increases the hazard of its acquisition. As explained earlier, this positive

sign may be due to the significant voting ownership of the parent firm in a carve-out with dual

class shares. The coefficient of Staggered is negative but statistically insignificant, which to

some extent supports our hypothesis H3.

For all our specifications, we perform a global test to check the proportionality

assumption as suggested in Cleves et al. (2004). An unreported 𝜒2 statistic suggests that in all

31

our models we fail to reject the null hypothesis that the log of the proportional hazard is constant

over time, suggesting that our models are well-specified.

Overall, the results of the Cox proportional hazard analysis suggest that the time-to-

acquisition has a positive relation with the parent motive to unlock the value, majority ownership

by the parent in the post-IPO carve-out, and the ongoing product-market association between the

parent and the ECO. These results support our hypotheses H1 and H2. Also, the time-to-

acquisition has an inverse relationship with the parent motive to restructure the operations.

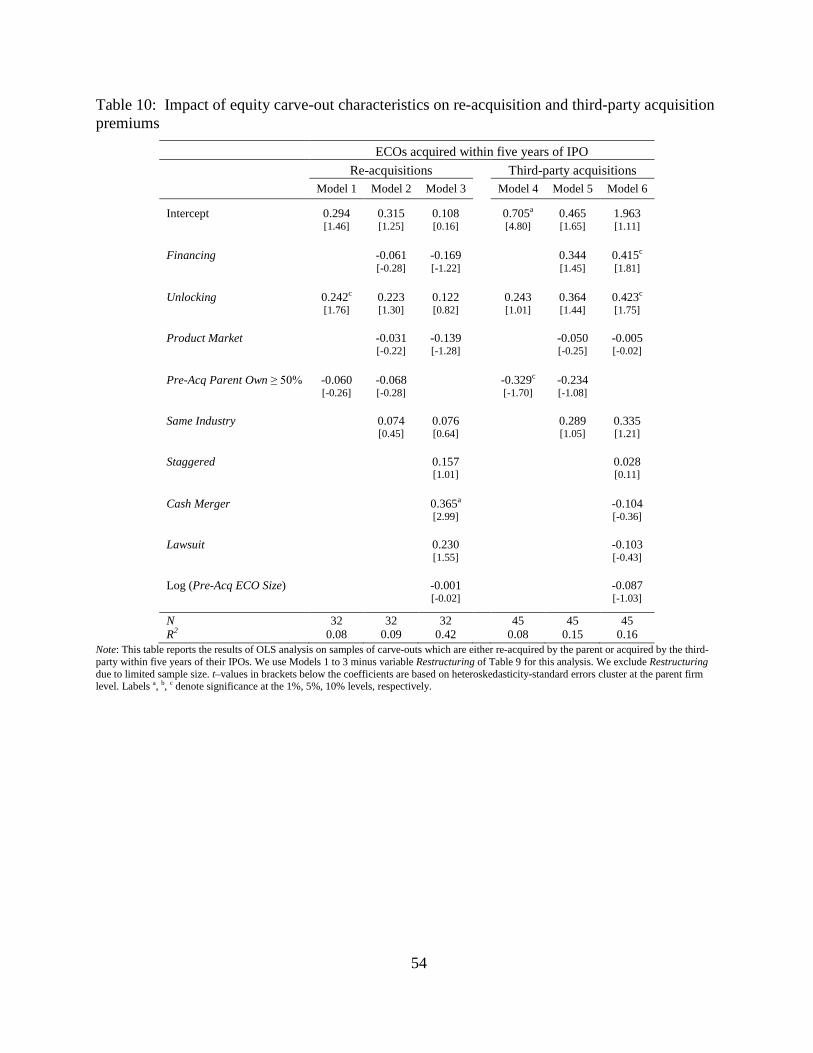

4.4. Analysis on parent-reacquisition versus third-party acquisition

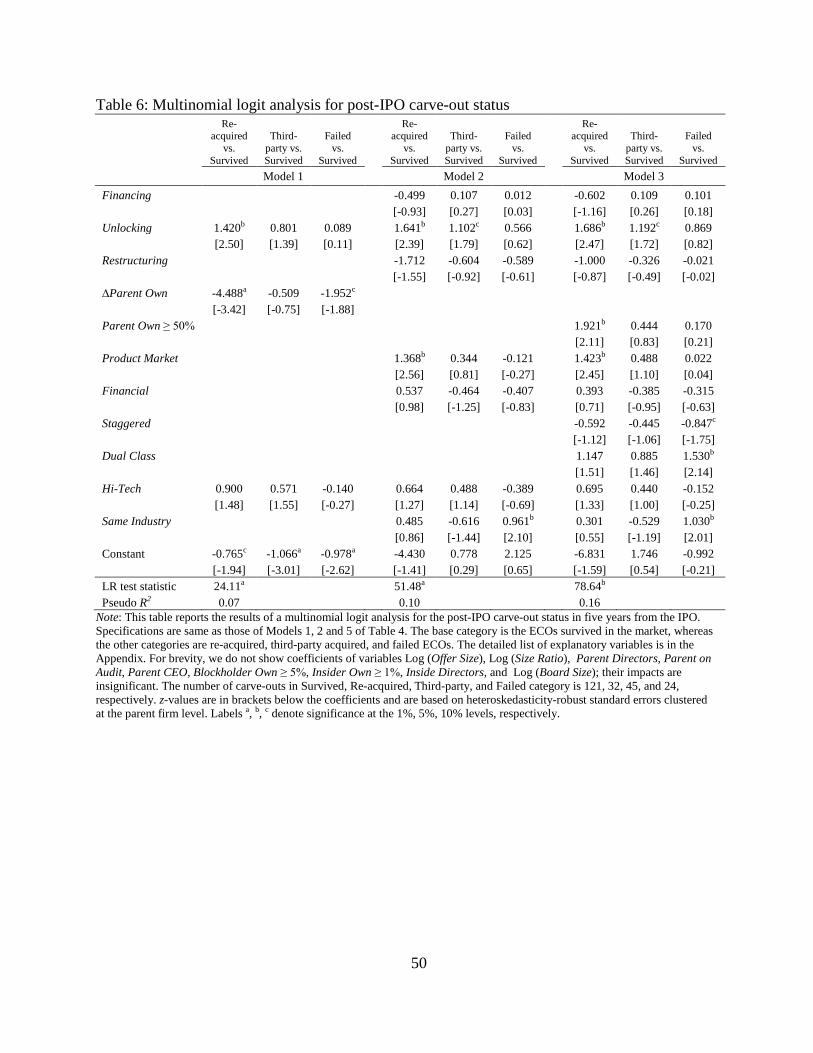

4.4.1. Multinomial analysis on post-IPO carve-out status

To assess whether our chosen factors have a different impact on the probability of re-

acquisition, third-party acquisition, or failure of a carve-out compared to the survived one, we

perform the multinomial logit analysis and report the findings in Table 6. The base category for

this analysis is those carve-outs which survived within the five years of their IPOs. For brevity,

we report results of only three specifications: Models 1, 2, and 3 of Table 6 are the same as

Models 1, 2, and 5 of Table 4, respectively. Models 2 and 3 of Table 6 include variables Log

(Offer Size) and Log (Size Ratio), and Model 3 includes Parent Directors, Parent on Audit,

Parent CEO, Blockholder Own ≥ 5%, Insider Own ≥ 1%, Inside Directors, and Log (Board

Size). We do not report their coefficients due to their statistical insignificance.

[Insert Table 6 about here]

As shown in Model 1, compared to the likelihood of an ECO’s survival in the market, the

likelihood of its re-acquisition increases when the parent’s motive is to unlock the value of the

subsidiary and when the parent sells fewer shares of the ECO during the IPO. The coefficients of

32

1.420 on Unlocking suggests that when the reason for undertaking a carve-out is to unlock the

value of the subsidiary, the odds of that carve-out to get re-acquired versus to be alive in the

market (base category) increase by 4.14; this increase is significant at the 5% level (z-value:

2.50). We also find some evidence that the parent’s motive to unlock subsidiary value increases

the probability of third-party acquisitions versus the base category as shown in Models 2 and 3.

These findings support our conjecture based on the insight of Perotti and Rossetto (2007). An

equity carve-out helps the parent ascertain its synergy with the subsidiary. Depending on positive

or negative value of the synergy, the parent takes the decision to re-acquire or to sell-off the

remaining portion to a third-party. Therefore, the probability of re-acquisition as well as that of

third-party acquisition increases when the parent’s motive is to unlock the value of the

subsidiary.

Regarding the impact of post-IPO parental control on the status of the carve-out, we find

evidence that post-IPO parent ownership and ongoing business connection between the parent

and the subsidiary have a positive impact on the probability of re-acquisition. As shown in

Model 3, the statistical significance of the coefficient on Parent Own ≥ 50% indicates that the

probability of the parent re-acquiring the ECO versus the ECO surviving independently in the

market significantly increases when the parent retains majority ownership in the post-IPO carve-

out; the coefficient on Parent Own ≥ 50% is insignificant when we compare the third-party

acquisition versus the base (survived) category or the failed ECO category versus the base

category. This result supports the findings of Klein et al. (1991).27 Finally, as shown in Model 2,

the coefficient of 1.368 on the dummy variable Product Market suggests that the odds of a parent

re-acquiring the carved-out subsidiary over the carve-out maintaining status as an independent 27 In their sample of 52 equity carve-outs, Klein et al. (1991) find that 25 firms have the parent retained ownership above 80%. Of these 25 carve-outs, 17 were subsequently re-acquired by the parent firm.

33

identity in the market increase by 3.93, when the parent and the carved-out subsidiary have an

ongoing product-market relationship and this increase is statistically significant at the 5% level.

Overall, our results of the multinomial logit analysis show that the probability of re-

acquisition over the ECO remaining alive in the market increases when the parent’s motive is to

unlock the value, when the parent retains majority ownership in the post-IPO carve-out, and

when the parent and carved-out subsidiary have an ongoing product-market relationship.

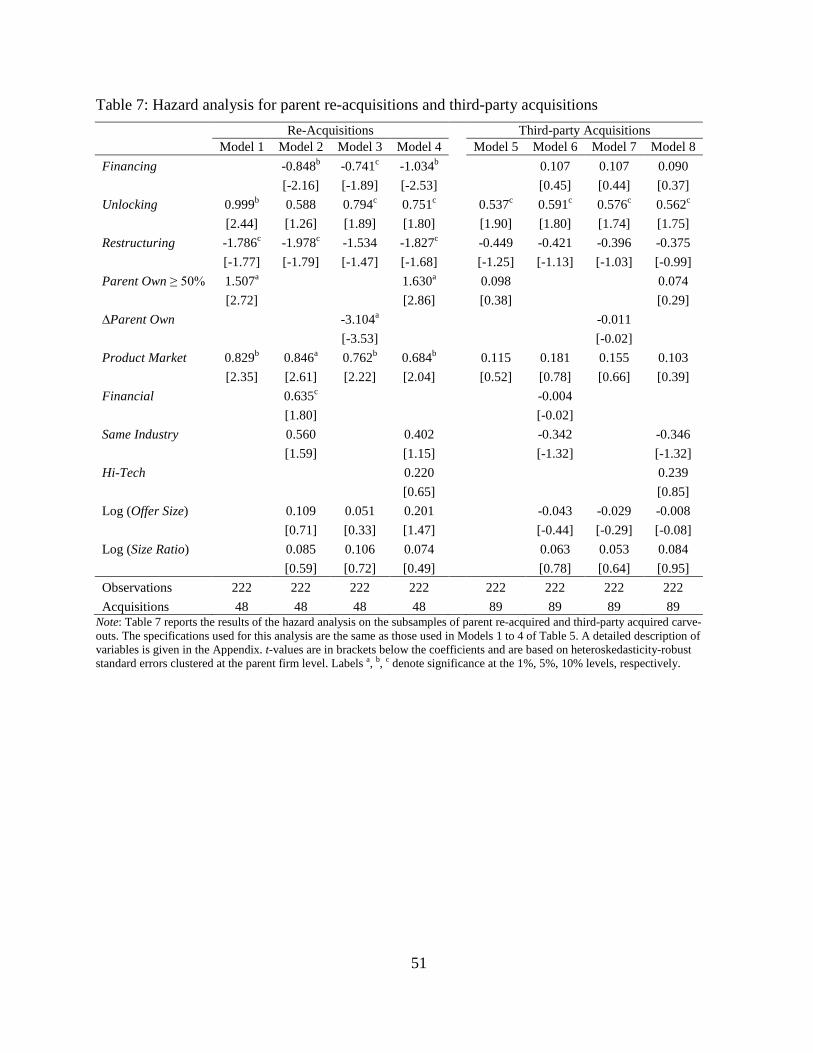

4.4.2. Time-to-acquisition for re-acquisition and third-party acquisition

We also perform the hazard analysis on the subsamples of re-acquisitions and third-party

acquisitions and report the results in Table 7. The specifications for this analysis are the same as

those for Models 1 to 4 of Table 5.

[Insert Table 7 about here]

As shown in Table 7, the hazard of re-acquisition and third-party acquisition increase

when the parent’s motive is to unlock the value of the subsidiary. These findings further support

our conjecture based on Perotti and Rossetto’s (2007) model. When the parent undertakes a

carve-out to unlock the value of a subsidiary, the acquisition of the subsidiary is imminent, either

by the parent or by a third-party. We also find statistically significant positive impacts of parent

ownership and its product-market relationship with the subsidiary on the hazard of a carve-out in

the case of re-acquisitions. We, however, do not find a statistically significant impact of these

two variables in the case of third-party acquisitions.

The differences in coefficients’ signs on Financing for re-acquisitions and for third-party

acquisitions are noteworthy. We find that when the parent consummates a carve-out transaction

for financing related purposes, the hazard of re-acquisition is lower than that when the parent

34

undertakes a carve-out for purposes other than financing and this difference is statistically

significant; however, the hazard of a third-party acquisition is actually higher, albeit the

difference is statistically insignificant. A possible explanation for this is that when the parent

undertakes a carve-out to finance the operations, it views the subsidiary mainly for a means of

financing rather than for the synergistic gains. Therefore, the parent is less likely to be interested

in re-acquiring the subsidiary and more likely to be interested in selling the remaining portion of

the ECO to a third-party in the future. Overall, to a large extent, the results of the hazard analysis

on the subsamples of re-acquisitions and third-party acquisitions support our earlier results of

multinomial analysis on the post-IPO carve-out status.

4.5. Acquisition premium

As shown earlier in Table 3, the mean and median time-to-acquisition of acquired carve-

outs is approximately five years from their IPO dates. If our objective is to determine ex-post the

impact of our chosen variables at the time of the IPO on the level of the acquisition premium,

then we need to consider the carve-outs that are acquired closer to their IPO dates. Therefore, for

the purpose of analysis in this subsection, we focus only on those carve-outs that are acquired

within five years of their IPO dates. In addition, for brevity, we report results using Acquisition

Premium_42 as a measure of the level of premium.28

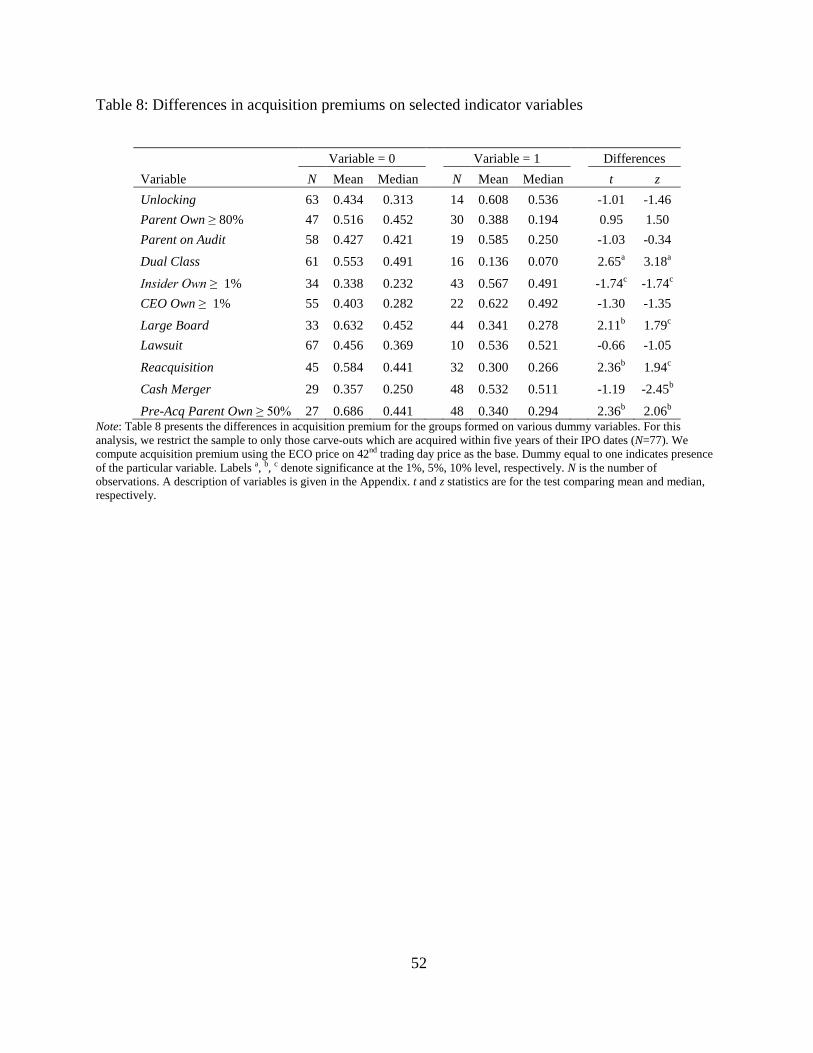

4.5.1. Univariate analysis

In Table 8, we report the results of a univariate analysis comparing the mean and median

acquisition premium for the groups based on selected dummy variables for the sample of carve-

28 We find qualitatively similar results when we use Acquisition Premium_Returns and Acquisition Premium_06.

35

outs acquired within five years of an IPO (N=77).29 The mean and median acquisition premium

for the carve-outs with dual class voting shares (N=16) are 13.6% and 7% respectively, whereas

the same statistics are 55.3% and 49.1% for carve-outs with one class of voting shares (N=61).

The differences are statistically significant at the 1% level with t and z values of 2.65 and 3.18,

respectively. These results, at a first glance, suggest that the anti-takeover provisions in a carve-

out seem to reduce its acquisition premium. However, as mentioned earlier, the effect of dual

class shares might be actually the effect of parent ownership since the parent can use dual class

of shares to retain a large percentage of voting rights in a carve-out.

[Insert Table 8 about here]

We find that the parent ownership in a carve-out prior to the merger is likely to impact

the level of acquisition premium. For example, the mean and median acquisition premium for the

group of carve-outs in which the parent ownership prior to the acquisition is above 50% (N=48)

are 34% and 29.4%, respectively. The same statistics for the other group of carve-outs with

parent ownership below 50% prior to the merger (N=27) are 68.6% and 44.1%, respectively. The

differences of mean and median acquisition premium for these two groups are statistically

significant at the 5% level. The mean and median acquisition premium for the group of carve-

outs which are acquired by a third-party (N=45) are 58.4% and 44.1%, respectively.

Interestingly, the mean and median acquisition premium for carve-outs which are re-acquired by

the parent firms (N=32) are 30% and 26.6%, respectively. The differences of acquisition

premium between third-party acquisition and the parent re-acquisition are statistically

significant. These results, at first glance, indicate the possibility of self-dealing by the parent.

Considering the small sample size and the previous finding that the acquisition premium is lower 29 The results of univariate analysis for the total sample of acquired carve-outs (N=137) are similar to those reported here for the sample of acquired carve-outs within five years of IPO; they are available in Desai et al. (2011).

36

when the parent owns majority ownership in a carve-out prior to its merger, we need to test this

claim in a multivariate setting before forming a conclusion.

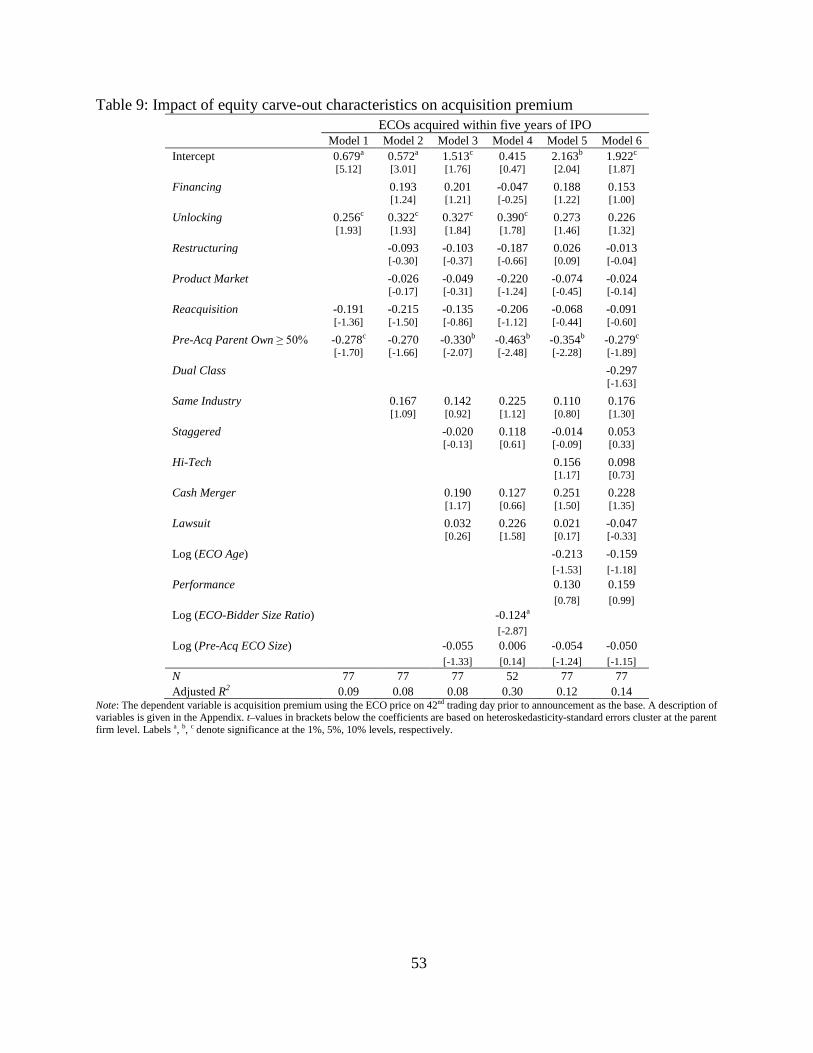

4.5.2. Multivariate analysis

In this subsection, we report the results of an ordinary least squares (OLS) analysis

assessing the impact of our chosen independent variables on the level of acquisition premium on

a subsample of carve-outs which are acquired within five years of their IPOs. Our primary

specification (Model 1) is

𝐴𝑐𝑞𝑢𝑖𝑠𝑖𝑡𝑖𝑜𝑛 𝑃𝑟𝑒𝑚𝑖𝑢𝑚_42𝑖

= B0 + B1 × 𝑈𝑛𝑙𝑜𝑐𝑘𝑖𝑛𝑔𝑖 + B2 × 𝑅𝑒𝑎𝑐𝑞𝑢𝑖𝑠𝑖𝑡𝑖𝑜𝑛𝑖+B3

× 𝑃𝑟𝑒 − 𝐴𝑐𝑞 𝑃𝑎𝑟𝑒𝑛𝑡 𝑂𝑤𝑛 ≥ 50%𝑖 + 𝜀𝑖

(4)

[Insert Table 9 about here]

As shown in Model 1 of Table 9, the coefficient of 0.256 on Unlocking indicates that the

level of acquisition premium when the parent’s motive is to unlock the value of a subsidiary is

25.6% higher than the premium paid when the parent’s motive is other than to unlock the value

of a subsidiary; the difference is significant at the 10% level (t-value: 1.93). The coefficient of -

0.278 on Pre-Acq Parent Own ≥ 50% suggests that carve-outs with majority parent ownership

prior to the merger earn a lower acquisition premium to the magnitude of 27.8% than those

carve-outs in which the parent firms do not have majority ownership prior to the merger. This

difference is statistically significant at the 10% level (t-value: 1.70). The coefficient of -0.191 on

Reacquisition indicates that the level of acquisition premium when the parent re-acquires the

carved-out subsidiary is 19.1% lower than that when a third-party acquires the carve-out;

37

however the difference is statistically insignificant. In Model 2, we include variables pertaining

to financing and restructuring motive of the parent in conducting a carve-out, ongoing business

relationship, and industry relatedness. We find results similar to those of Model 1.

In Models 3 to 6, we add various controls to assess the robustness of our primary

specification. In Model 4, we include the ratio of target and bidder size as one of the controls and

find it has a negative relation with the level of acquisition premium. Since there are several non-

public acquirers in our sample, our sample size in Model 4 is only 52. In addition, we initially

find the impact of our proxy for the carve-out’s market performance (Performance) to be

significant on the level of acquisition premium. However, after performing a test identifying

influential observations, we find that two observations are dominant in increasing the t-value.

When we exclude those two observations, we find the impact of Performance to be insignificant.

Therefore, in all our analyses we Winsorize the values of Performance at the one percentile

upper level. We do not find consistency in the coefficient sign for our proxy for anti-takeover

provision – Staggered. Also, it is statistically insignificant, which suggests that in our sample, we

do not find an impact of staggered board on the level of acquisition premium. In addition, as

shown in Model 6, the effect of having dual class shares on the level of acquisition premium is

statistically insignificant.

Overall, the results of OLS on the acquisition premium suggest that the acquisition

premium is related to whether the parent has above majority ownership prior to the merger, and

whether the parent consummates a carve-out transaction to unlock the value. In all the

regressions, we find that in the case of a re-acquisition the estimated acquisition premium is

lower than that in the case of a third-party acquisition, but the difference between the two is not

38