Embed Size (px)

DESCRIPTION

Techno-Economic Evaluation of Narrowband and Broadband Access Networks

Citation preview

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 1/20

1

I84

IEEE

JOURNAL ON

SELECTED

AREAS

IN

COMMUNICATIONS,

VOL. 14, NO. 6, AUGUST 1996

Techno-Economic Evaluation

of

and Broadband Access Network

and Evolution Scenario Assess

Borgar T.

Olsen, Alc ibiade Zaganiar is , Kje l l Stordahl , L. Aa. Ims,

D.

M y h r e , T. (averli , M. Tahkokorpi ,

I. Well ing, M . Drie skens , J. Kraushaar , J . M o n o n e n ,

M.

Lahteeno ja , S . Marka tos ,

M.

De Bortol i ,

U. Fer re ro , M. Rave ra ,

S .

Balzarett i , F. Fleuren , N. Gieschen , M . De Ol ive i ra Du a r t e ,

and

E.

de

Cast ro

Abstract-The pa pe r presents the main results obtained within

the Research in Advanced Communications in Europe (RACE)

project: 2087 TITAN (Tool for Introduction Scenarios and

Techno-Economic Evaluation of The Access Netw ork) regardin g

minimum-risk introductory routes for new narrowband

and

broadband services in the residential and small business market.

The project developed a methodology and a tool for techno-

economic evaluation of advanced narrowband and broadband

telecommunications networks and services.

Results from four extensive access network studies are

presented. For the narrowband services, optical access and

radio in the local loop have been assessed and compared to

conventional copper layout in a greenfield environment. Access

network upgrad e strategies for emerging new broadband services

have been evaluated in three studies, with technological options

ranging from enhanced copper to hybrid-fiber-coax (HFC) and

broadband passive optical networks. An extensive study on

different broadband access network upgrade alternatives

f o r

public network operators (PNO’s) were carried out, taking

into account the diversity of conditions met today by Europ ean

countries. In anoth er stud y, the effect of com petition in the access

network was modeled assuming two main operators sharing

the market. Broadband upgrade alternatives were evaluated

for a new cable operator, competing with the dominant public

network operator. In addition, video-on-demand

(VoD)

and

Inter net access upgrades have been analyzed.

The paper demonstrates the viability

of

techno-economic

studies for the access network, including in-depth analysis

of

the

time-dependence of component cost, tariffs, service-penetrations

and market shares. This work intends to support establishing

guidelines for strategic decisions regarding the development of

the access network alternatives of different operators.

I. INTRODUCTION

SSESSMENT of residential access network scenarios

A s increasingly important for the telecommunications

Manuscript received July

18.

1995: revised October 9, 1995.

B. T. Olscn,

L.

Aa. Ims, and

D.

Myhre are with Telenor Research and

Development, Kjeller, Norway.

A.

Zaganiaris

is

with CNET-France Tclecom, Lannion, France.

K. Stordahl and T. Overli are with Telenor, Networks Division, Oslo,

Norway.

M . Tahkokorpi and

1.

Welling are with Nokia Research, Helsinki, Finland.

M. Drieskens and J. Kraushaar are with Ericsson Raynet, Brussels, Belgium.

J. Mononen and M. L at eenoj a are with Telecom, Finland Research Centre,

S.

Markatos is with the University

of

Athens, Athens, Greece.

M. De Bortoli, U. Fenzro, M. Ravera, and S. Balzaretti are with CSELT,

F.

Fleuren is with KPN Research, Leidscendam, The Netherlands.

N. Gieschen is with Telekom, Berlin, Germany.

M .

De

Oliveira Duarte and

E.

de Castro are with the University of Aveiro,

Publisher Item Identifier S 0733-8716(96)04893-7.

Helsinki, Finland.

Turin, Italy.

Aveiro, Portugal.

operators [11-[4]. Fast improving technology gives birth to

new alternatives, although the society’s ability to fully exploit

them lags by years. An increasing number of field trials

world-wide is paving the way toward integrated broadband

communications, which are at an early stage

of

development.

Most of the advanced components needed are being produced

in already significant quantities, yet they are in the beginning

of the learning process which will drive the costs further down

Widespread competition and technological breakthroughs

focus the attention of the operators on satisfying new cus-

tomer needs, as a strategy to keep and expand their mar-

ket share and, consequently, their revenue base

[7].

Since

average growth of plain old telephony services

(POTS)

is

almost saturated in Europe, the long-term growth and f i -

nancial strength of the public network operators (PNO’s)

imply the emergence of additional revenues such as the

Internet access service [8]. Furthermore, some operators be-

lieve that the investment in fiber in the loop (FITL) sys-

tems is not likely to be recouped by telephony services

alone

[9].

With increasing pressure to minimize costs and

to maximize revenues, a large variety

of

access network

architectures and upgrade scenarios must be rigorously ex-

amined in order to determine the most appropriate ones for

the different demographic area types and service demand

profiles.

Customer applications are not well-defined, despite recent

field trials and market surveys. Forecasting the penetration

of

still uncertain services is extremely difficult but necessary

to undertake. Market surveys and extrapolations from current

household spending patterns are commonly used sources for

forecasting [lo]-[12].

The value of new information services, which can be

carried by the existing or new networks, is likely to be

considerably enhanced by the provision

of

access

to

wideband

signals.’ Wideband access on twisted copper pairs enable rapid

access to multimedia information resources. Video dial tone

services, requiring a 2-Mb/s transport facility, would further

enable many new applications such as video-on-demand (VoD)

and video games, as well as narrowcasting services like

teleworking, teleshopping, and telelearning.

~51,

VI

’Wideband, capacity 5

Mb/s.

0733-8716/96 05.00 996 IEEE

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO. Downloaded on June 16, 2009 at 10:41 from IEEE Xplore. Restrictions apply.

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 2/20

OLSEN

et ul : TECHNO-ECONOMIC

EVALUATION

OF

NARROWBAND AND BROADBAND

ACCESS NETWORK ALTERNATIVES

1185

=FPO=Flexibilily Point 0

-

.

-

-

-

LL2

LL1: Bus Sne

network]

L W

Star

Ciy

netwrk)

L L 9

Rhg

Interdty network

I

L3

Fig.

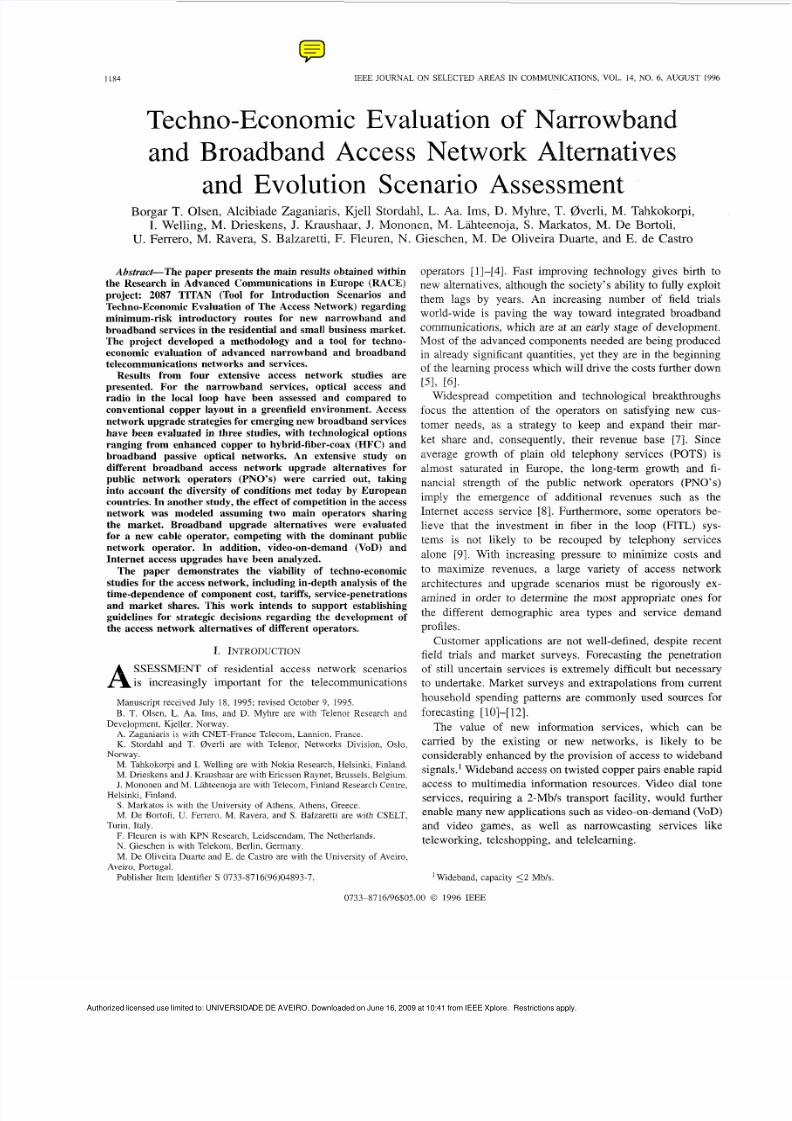

1.

the

distributions.

The

double-star geometrical model

(a)

and

the square

model (b) for

This paper presents a methodology and results for the

assessment of access network evolution for the residential

and small business market. Its objective is the estimate of

the economic viability of different access network projects.

The evaluation is carried out in several stages: calculation of

the installed first cost, running costs, life-cycle costs, the cash

balance, and other economic figures of merit of the invest-

ment projects. This enables the comparison of various access

network architectures through a glob al system assessment and

contributes to the identification of minimum -risk introduction

strategies [13], [14]. The methodology and the tool dev eloped

within this project are being validated by comparison to

operating European networks and field trials.

11. THE TITAN METHOD OLOGY

The TITAN Tool is intended to assess any kind

of

access

network architecture (e.g., star, bus, ring, or combinations),

as well as, a variety of services with any estimated evolution

within the desired study period. The flexibility of the study pe-

riod length allows the user to derive scenarios which take into

account network and service evolution. Different architectures

which can prov ide a selected group of services can be chosen.

The param eters relevant to the engineering of the netw ork,

such as subscriber density are initially defined. These serve

as inputs to one or mo re geometrical models which calculates

the overall cable length of the various sections of the network.

The most commonly used geometrical models, the double

star and the square model, is shown in Fig. 1 [15], [16].

The models assume two or more flexibility points (FP’s)

between the service access point (SAP) and the subscriber

premises. The SAP,

as used in this study, refers to the

localization of the concentrator in the network, as used in

some European countries. Each SAP typically serves a few

thousand subscribers.

The n umber of flexibility points and the link levels between

the flexibility points in the mo del may be changed if required.

The system cost is calculated by establishing a list of the

volumes of the cost items needed in different flexibility

points and link levels. The network and service evolution

is taken into account by forming a new list for each year

of the study period. The cost items (network equipment,

cables, installation, and civil works) are derived from an

integrated cost database developed w ithin the TITAN project,

containing data gathered from many European sources. Cost

elements of different technological maturity and commercial

availability are included in the database. By adding operation,

maintenance, and administration (OAM) costs, the life-cycle

costs are obtained. The service penetrations, which can be

provided over different network architectures, is estimated

through the Delphi survey described in the next section [lo],

[

121. Finally, the overall financial budget is derived for the

various architectures by integrating demand and tariff data

with the life-cycle cost.

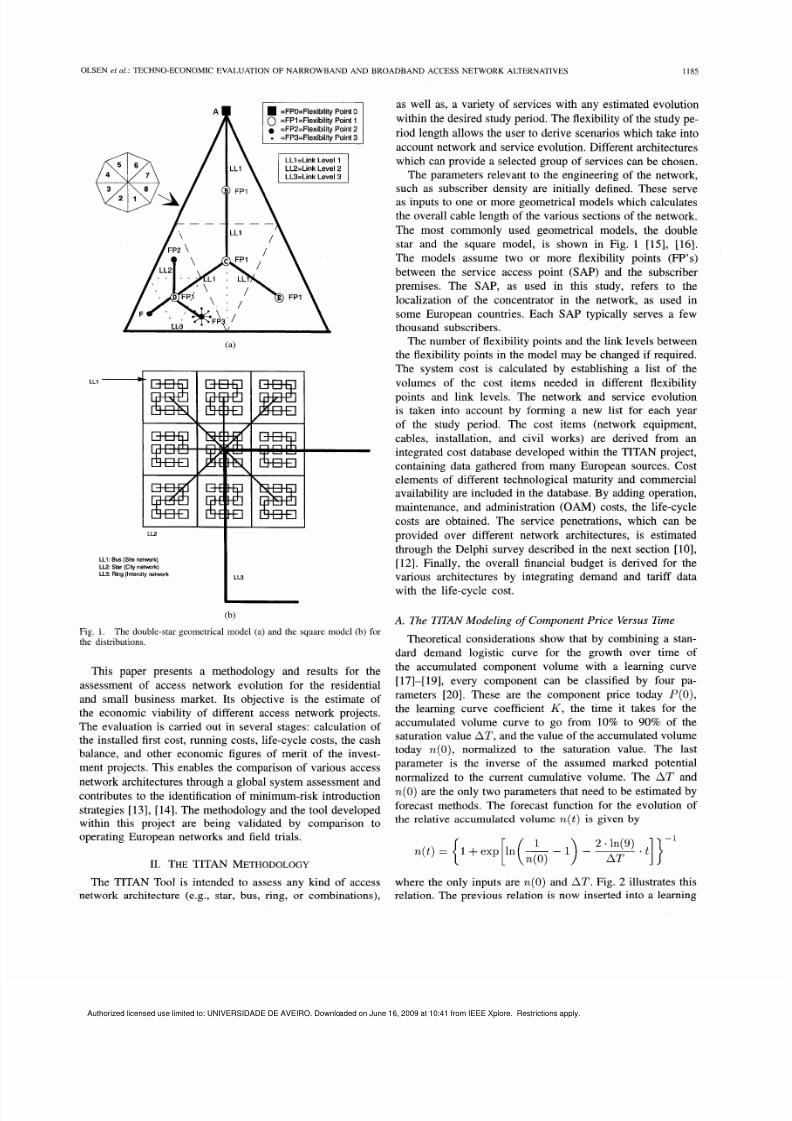

A The TITAN Modeling

of Component

Price Versus

Time

Theoretical considerations show that by combining a stan-

dard demand logistic curve for the growth over time of

the accumulated component volume with a learning curve

[17]-[19], every comp onent can be classified by fo ur pa-

rameters

[ 2 0 ] .

These are the component price today

P(O),

the learning curve coefficient K , the time it takes for the

accumulated volume curve to go from 10% to 90% of the

saturation value AT, and the value of the accumulated volume

today

n O ) ,

normalized to the saturation value. The last

parameter is the inverse of the assumed marked potential

normalized to the current cumulative volume. The

AT

and

n(0) re the only two parameters that need to be estimated by

forecast methods. The forecast function for the evolution of

the

relative accumulated volume

n ( t )

s given

by

n( t )

=

+exp In - ~.

{

[ n;o)

) 22]}-l

where the only inputs are

n(0)

and

AT.

Fig.

2

illustrates this

relation. Th e previous relation is now inserted into a learning

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 3/20

I186

IEEE JOURNAL ON SELECTED AREAS IN COMMUNICATIONS, VOL. 14, NO. 6. AUGUST 1996

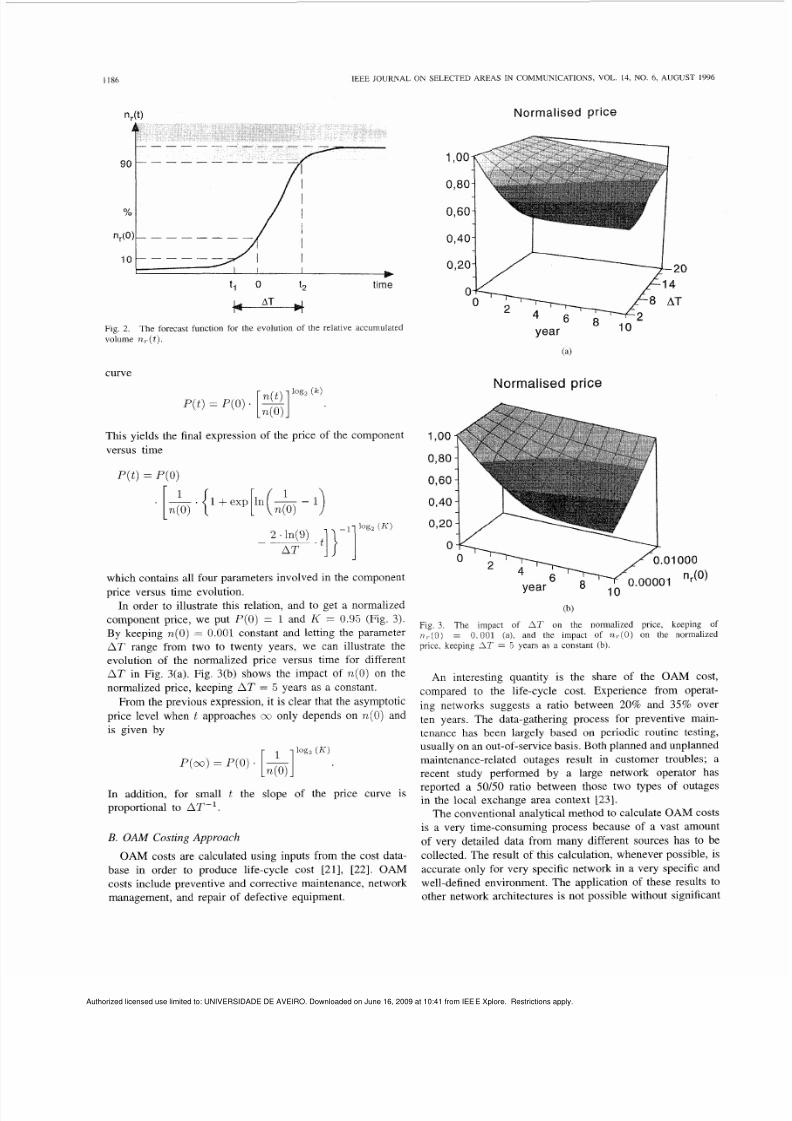

Normalised

price

1

oo

0 80

0,60

0,40

0,20

0

Fig

2

volume n, ( t )

The forecaat function for the evolution

of

the relative accumulated

curve

This yields the final expression of the price of the component

versus time

P ( t )= P(0)

which contains all four parameters involved in the component

price versus time evolution.

In order to illustrate this relation, and to get a normalized

component price, we put P(0) = and

K

= 0.95 (Fig. 3).

By keeping n(0)= 0.001 constant and letting the parameter

AT range from two to twenty years, we can illustrate the

evolution

of

the normalized price versus time for different

A T

in Fig. 3(a). Fig. 3(b) shows the impact of

n(0)

on the

normalized price, keeping A T

= 5

years

as

a constant.

From the previous expression, it is clear that the asymptotic

price level when t approaches only depends on

n(0)

and

is given by

In addition, for small t the slope of the price curve is

proportional to

AT-’.

B.

OAM Costing

Approach

OAM costs

are

calculated using inputs from the cost data-

base in order to produce life-cycle cost [21],

[22].

O A M

costs include preventive and corrective maintenance, network

management, and repair of defective equipment.

Normalised

price

(b)

Fig. 3. The impact of

AT

on the normalized price, keeping of

n, . (O)

= 0 . 0 0 1 (a),

and the impact

of n,.(O)

on the normalized

price. keeping

IT

= 5 years as a constant (b).

An interesting quantity is the share of the OAM cost,

compared to the life-cycle cost. Experience from operat-

ing networks suggests a ratio between

20

and 35% over

ten years. The data-gathering process for preventive main-

tenance has been largely based on periodic routine testing,

usually on an out-of- service basis. Both planned a nd unplanned

maintenance-related outage s result in customer troubles; a

recent study performed by a large network operator has

reported a 50150 ratio between those two types of outages

in the local exchange area context

[23].

The conv entional analytical method to calculate OAM costs

is a very time-consuming process because of a vast amount

of very detailed data from many different sources

has

to be

collected. The result of this calculation, whenever possible, is

accurate only for very specific network in a very specific and

well-defined environment. The application of these results to

other network architectures is not possible without significant

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO. Downloaded on June 16, 2009 at 10:41 from IEEE Xplore. Restrictions apply.

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 4/20

OLSEN et

ul.:

TECHNO-ECONOMIC EVALUATION

OF

NARROWBAND AND BROADBAND ACCESS NETWORK ALTERNATIVES

1187

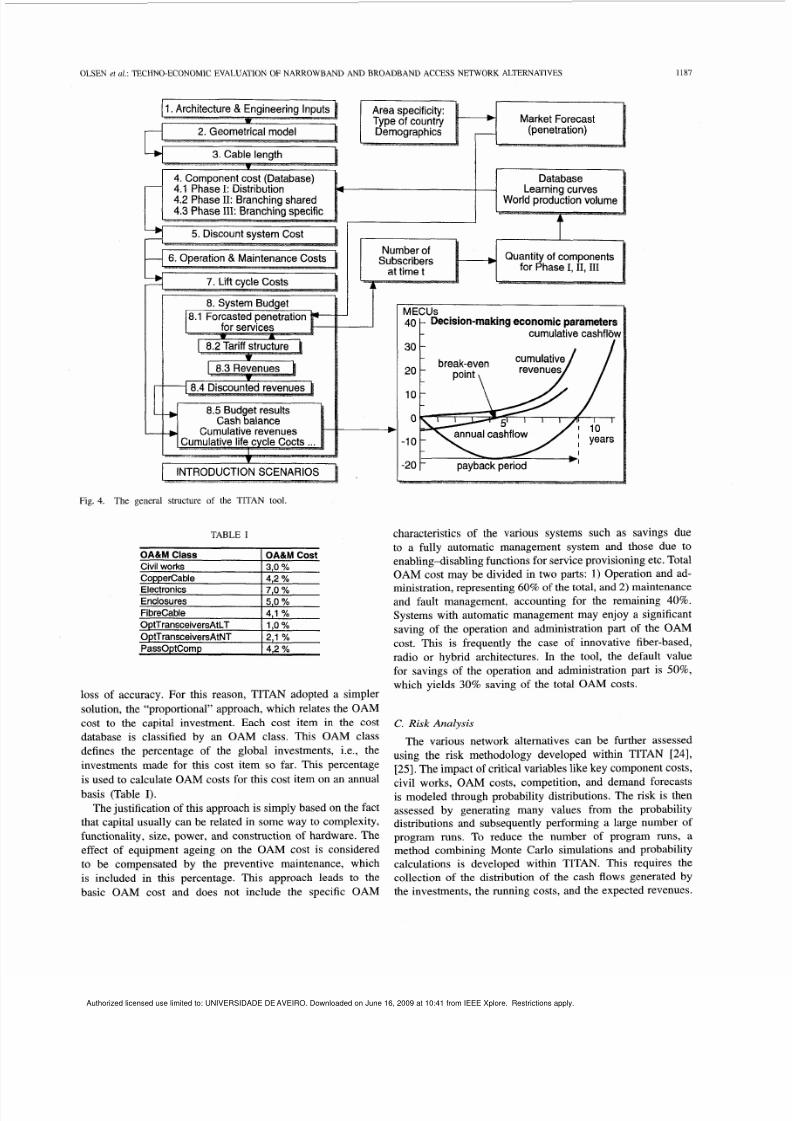

OA&M

Class

Civil

works

Coppercable

Electronics

Enclosures

Fibrecable

OptTransceiversAt T

OptTransceiversAtNT

PassOptComp

4.1

Phase

I:

Distribution

OA&M Cost

3 O

Yo

4,2Yo

7 O

o

5 O

4,l Yo

1

,o

Yo

2 l

4,2Yo

v

I INTRODUCTION SCENARIOS

Fig. 4. The general structure

of

the TITAN tool.

loss of accuracy. For this reason, TITAN adopted a simpler

solution, the “propo rtional” approach, which relates the O AM

cost to the capital investment. Each cost item in the cost

database is classified by an OAM class. This OAM class

defines the percentage of the global investments, i.e., the

investments made for this cost item so far. This percentage

is used to calculate OAM costs for this cost item on an annual

basis (Table I).

The justification of this approach is simp ly based on th e fact

that capital usually can be related in som e way to complexity,

functionality, size, power, and construction of h ardware. Th e

effect of equipment ageing on the OAM cost is considered

to be compensated by the preventive maintenance, which

is included in this percentage. This approach leads to the

basic OAM cost and does not include the specific OAM

MECUs

Decision-makingeconom ic p arameters

40 r cumulative cashflbw

30

20

10

-10

-20

-b

-

payback period

characteristics of the various systems such as savings due

to a fully automatic management system and those due to

enabling-disabling functions for service provisioning etc. Total

OAM cost may be divided in two parts:

1 )

Operation and ad-

ministration, representing 60 of the total, and 2) maintenance

and fault management, accounting for the remaining

40 .

Systems with automatic management may enjoy a significant

saving of the operation and administration part of the

OAM

cost. This is frequently the case of innovative fiber-based,

radio or hybrid architectures. In the tool, the default value

for savings of the operation and administration part is

50 ,

which yields 30 saving of the total OAM costs.

C. isk Analysis

The various network alternatives can be further assessed

using the risk methodology developed within TITAN

[24],

[25] . he impact of critical variables like key com pone nt costs,

civil works, OAM costs, competition, and demand forecasts

is mo deled through probability distributions. The risk is then

assessed by generating many values from the probability

distributions and subsequently performing a large num ber of

program runs. To reduce the number of program runs, a

method combining Monte Carlo simulations and probability

calculations is developed within TITAN. This requires the

collection of the distribution of the cash flows generated by

the investments, the running costs, and the expected revenues.

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO. Downloaded on June 16, 2009 at 10:41 from IEEE Xplore. Restrictions apply.

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 5/20

I188 IEEE JOURNAI

ON

SELECTED AREAS IN COMMUNICATIONS, VOL. 14, NO. 6, AUGUST 1996

For a given strategy, some probability measures on two

criteria commonly used in investment planning will give an

indication of whether it is worth investing or not: 1) The

present value of the cash

flows

(PVCF), or net present value

(NPV), and 2) the internal rate of return

I RR).

D.

The

Tool Description

Fig. 4 shows the general structure of the TITAN tool [20].

The tool is based on Excel@spreadsheet software. The central

part of the tool is the TITAN file, which contains macros

for the tool functionality. This is used in connection with

one database file and one or more main files. The tool has

two operating modes. The database mode is used for defining

cost components and services, and the main mode is used

for defining the architectures and service set and for actual

calculations and reporting.

The database contains several sections:

1) cost components, containing all component specific in-

2)

learning curve classes, which define a specific learning

3) volume classes, which define a specific market volume

4) OAM classes, which define a certain operations, admin-

5) write off period class which defines a component life-

6 uncertainty class, which defines the relative uncertainty

The main files are based on on e or more generalized access

network models. One such model is shown in Fig. 1. The m ain

sheet utilizes the geometrical model for calculation

of

cable

lengths and civil works. In this sheet, a “cost components”

section, also called “shopping list,” specifies all components

from the database used in this architecture. This section also

defines the point in time when each component is installed in

the network. The “shopping list” has been divided into sub-

sections according to the generic network model as described

above.

formation;

curve behavior;

evolution;

istration and maintenance behavior;

times for calculation

of

depreciation;

for the risk assessment.

111. FORECASTING

ERVICEEMAND

IN THE RESIDENTIAL

MARKET

The TITAN project has performed a comprehensive Delphi

survey in order to forecast the penetration of future services

and applications [lo] , [12]. The survey was performed in two

consecutive rounds among exp erts in ten European countries.

During the two rounds, the experts converged significantly

in their opinion about the servic e penetration forecasts. The

Delphi survey produced quantified information about the de-

velopment of new services and applications which requires

high capacity in the access network. The final results from

the survey give predictions of the future demand for wide and

broadband bearer serv ices 2 Demand h as been quantified in

terms of the number of subscribers to one or more services.

The growth of subscriber demand affects the amount

of

equipment required in the network and thus the discounted

’Broadband, cdpacity >2Mb/\

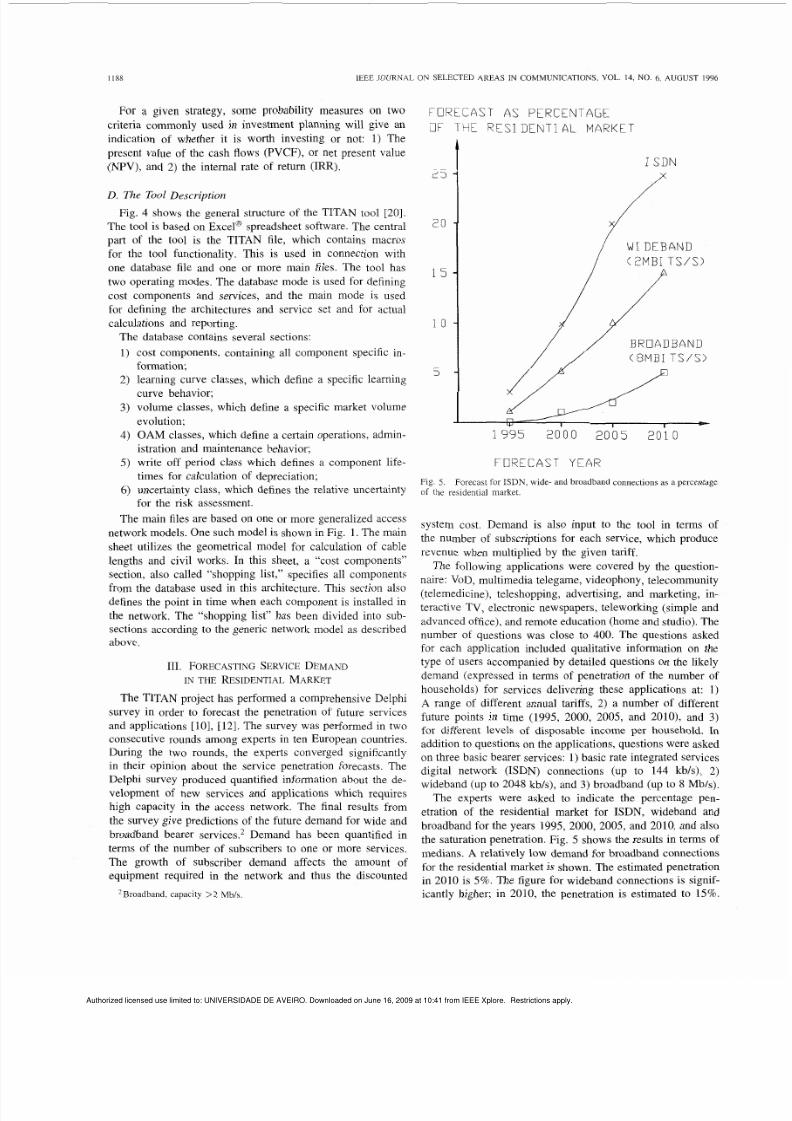

FCIRECAST A S

PERCENTAGE

3F THE R E S I D E N T I A L

MA R K E T

I SDN

W DEBAND

2 M B I

T S / S )

BROADBAND

8 M B I TS/ S>

//

I I I

1995 2000

2005

2010

F U R E C A S T Y E A R

Fig.

5.

of

the residential market.

Forecast for ISDN, wide- and broadband connections as a percentage

system cost. Demand is also input to the tool in terms of

the number of subscriptions for each service, which produce

revenue when multiplied by the given tariff.

The following applications were covered by the question-

naire: VoD, multimedia telegame, videophony, telecommunity

(telemedicine), telesh oppin g, advertising, an d marketing, in-

teractive TV, electronic newspapers, teleworking (simple and

advanced office), and remote edu cation (home and studio). The

number of questions was close to 400. The questions asked

for each application included qualitative information on the

type of users accompanied by detailed questions

on

the likely

demand (expressed in terms of penetration

of

the number of

households) for services delivering these applications at: 1)

A

range of different annual tariffs, 2) a number of different

future points in time (1995, 2000, 2005, and 2010), and 3)

for different levels of disposable income per household. In

addition to que stions on the applications, q uestions were asked

on three basic bearer services: 1 ) basic rate integrated services

digital network (ISDN) connections (up to

144 kb/s), 2)

wideband (up to 2048 kb/s), and 3) broadband (up to 8 Mb/s).

The experts were asked to indicate the percentage pen-

etration of the residential market for ISDN, wideband and

broadband for the years 1995, 2000, 2005, and 2010, and also

the saturation penetration. Fig. 5 shows the results in terms of

medians. A relatively low demand for broadband connections

for the residential m arket is sh own . The estimated penetration

in 2010 is 5%. The figure for w ideband connections is signif-

icantly higher; in 2010, the penetration is estimated to 15 .

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO. Downloaded on June 16, 2009 at 10:41 from IEEE Xplore. Restrictions apply.

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 6/20

OLSEN ef

al.:

TECHNO-ECONOMIC EVALUATlON OF NARROWBAND AND BROADBAND ACCESS NETWORK ALTERNATIVES

25

1189

X

I

SDN

I

t

LL

1000 2000 3000 4000

ANNUAL S U B S C R I P T I

ON

T A R 1

F F

( E CU)

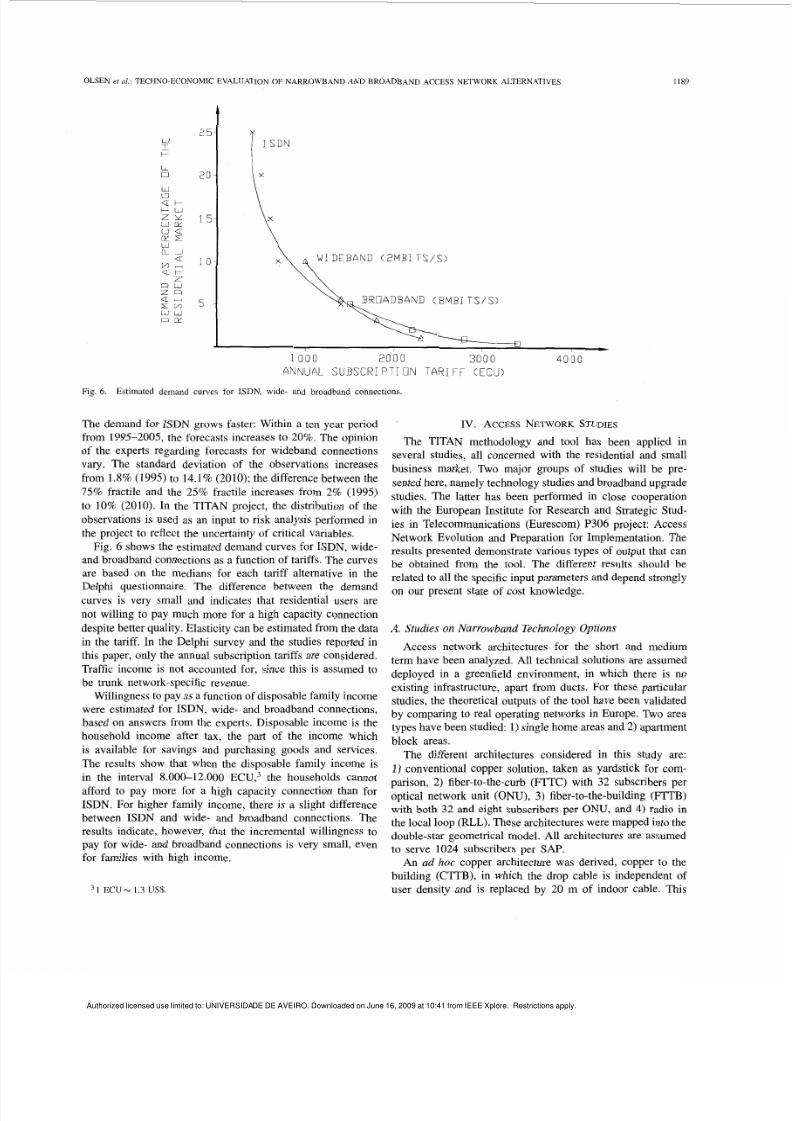

Fig.

6. Estimated demand curves for

ISDN,

wide- and broadband connections.

The demand for ISDN grows faster: Within a ten year period

from 1995-2005, the forecasts increases to

20 .

The opinion

of the experts regarding forecasts for wideband connections

vary. The standard deviation of the observations increases

from 1.8% (1 995) to

14.1%

(2010); the difference between the

75% fractile and the 25 fractile increases from 2% (1995)

to 10% (2010). In the TITAN project, the distribution of the

observations is used as an input to risk analysis performed in

the project to reflect the uncertainty of critical variables.

Fig. 6 shows the estimated demand curves for ISDN, wide-

and broadband co nnections as a fun ction of tariffs. The curves

are based on the medians for each tariff alternative in the

Delphi questionnaire. The difference between the demand

curves is very small and indicates that residential users are

not willing to pay much more for a high capacity connection

despite better quality, Elasticity can be estimated from the data

in the tariff. In the Delphi survey and the studies reported in

this paper, only the annual subscription tariffs are considered.

Traffic income is not accounted for, since this is assumed to

be trunk network-specific revenue.

Willingness to pay as a function of disposable family income

were estimated for ISDN, wide- and broadband connections,

based

on

answers from the experts. Disposable income is the

household income after tax, the part of the income which

is available for savings and purchasing goods and services.

The results show that when the disposable family income is

in the interval 8.000-12.000 ECU ,3 the households cannot

afford to pay more for a high capacity connection than for

ISDN. For higher family income, there is a slight difference

between ISDN and wide- and broadband connections. The

results indicate, however, that the incremental willingness to

pay for wide- and broadband connections is very small, even

for families with high income.

1 E C U N

1.3 US .

IV. ACCESSNETWORK TUDIES

The TITAN methodology and tool has been applied in

several studies, all concerned with the residential and small

business market. Two major groups of studies will be pre-

sented here, namely technology studies and broadband upgrade

studies. The latter has been performed in close cooperation

with the European Institute for Research and Strategic Stud-

ies in Telecommunications (Eurescom) P306 project: Access

Network Evolution and Preparation for Implementation. The

results presented demon strate various types of output that can

be obtained from the tool. The different results should be

related to all the specific input param eters and depend strongly

on our present state of cost knowledge.

A. Studies on Narrowband Technology Options

Access network architectures for the short and medium

term have been analyzed. All technical solutions are assumed

deployed in a greenfield environment, in which there is no

existing infrastructure, apart from ducts. For these particular

studies, the theoretical outputs

of

the tool have been validated

by comparing to real operating networks in Europe. Two area

types have been studied: 1) single home areas and 2) apartment

block areas.

The different architectures considered in this study are:

1) conventional copper solution, taken as yardstick for com-

parison, 2) fiber-to-the-curb (FTTC) with 32 subscribers per

optical network unit (ONU), 3) fiber-to-the-building (FTTB)

with both 32 and eight subscribers per ONU, and 4) radio in

the local loop (RL L). These arch itectures were mappe d into the

double-star geometrical model. All architectures are assumed

to serve 1024 subscribers per S AP.

An ad

hoc

copper architecture was derived, copper to the

building (CTTB), in which the drop cable is independent of

user density and is replaced by

20

m

of

indoor cable. This

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO. Downloaded on June 16, 2009 at 10:41 from IEEE Xplore. Restrictions apply.

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 7/20

1190

IEEE JOURNAL ON SELECTED AREAS IN COMMUNICATION S, VOL. 14, NO. 6, AUGUST 1996

ECURlSER

IO00

9uo

800

I00

WO

500

400

3

2

100

n

C opper m C 3 2

RLL

U l F C

mthout

Civil Works

u 1 F C mlh Civil Works minimum

c a x

ECUAJSER

1000

900

8

700

601

501

4 0 0

300

2 0 0

100

0

FTTB32 FTTB8 CTTB32 ClTB8

(b)

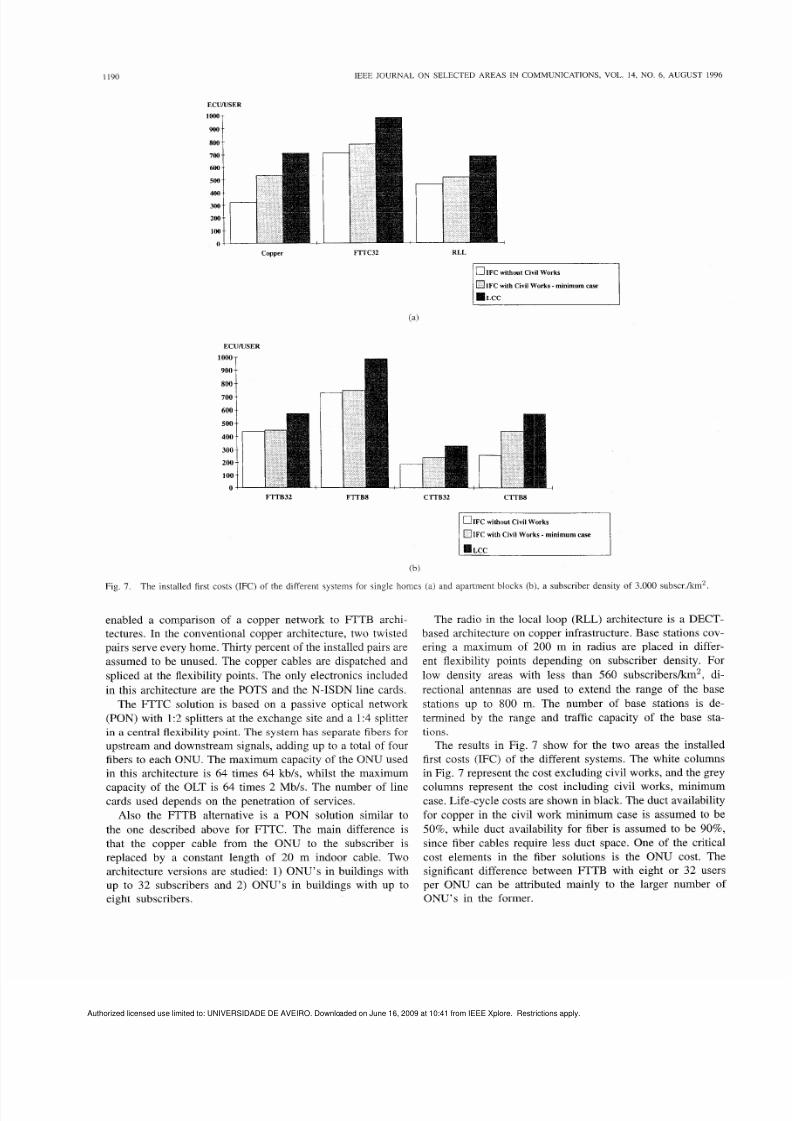

Fig. 7.

The installed first

costs (IFC)

of the different systems for single

homes (a)

and apartment blocks (b),

a

subscriber density

of 3.000

subscrkrn'.

enabled a comparison of a copper network to FTTB archi-

tectures. In the conventional copper architecture, two twisted

pairs serve every h ome. Th irty percent

of

the installed pairs are

assumed to be unused. The copper cables are dispatched and

spliced at the flexibility points. The only electronics included

in this architecture are the POTS and the N-ISDN line cards.

The FTTC solution is based

on

a passive optical network

(PON) with 1:2 splitters at the exchange site and a 1:4 splitter

in a central flexibility point. The system has separate fibers for

upstream and downstream signals, adding up to a total of four

fibers to each ON U. The maximum capacity of the ON U used

in this architecture is 64 times 64 kb/s, whilst the maximum

capacity of the OLT is 64 times

2

Mb/s. The number of line

cards used depends on the penetration of services.

Also the

FTTB

alternative is a

PON

solution similar to

the one described above for FTTC. The main difference

is

that the copper cable from the ONU to the subscriber is

replaced by a constant length of 20 m indoor cable. Two

architecture versions are studied: 1) ONU's in buildings with

up to 32 subscribers and

2)

ONU's in buildings with up to

eight subscribers.

The radio in the local loop (RLL) architecture

is

a DECT-

based architecture on copper infrastructure. Base stations cov-

ering a maximum of

200

m in radius are placed in differ-

ent flexibility points depending on subscriber density. For

low density areas with less than 560 subscribers/km2, di-

rectional antennas are used to extend the range of the base

stations up to 800 m. The number of base stations is de-

termined by the range and traffic capacity

of

the base sta-

tions.

The results in Fig. 7 show for the two areas the installed

first costs (IFC) of the different systems. The white columns

in Fig. 7 represent the cost excluding civil works, and the grey

columns represent the cost including civil works, minimum

case. Life-cycle costs are shown in black. Th e du ct availability

for copper in the civil work

minimum

case is assumed to be

50 , while duct availability for fiber is assumed to be 90 ,

since fiber cables require less duct space. One of the critical

cost elements in the fiber solutions is the ONU cost. The

significant difference between FTTB with eight or 32 users

per ONU can be attributed mainly to the larger number of

ONU's in the former.

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 8/20

OLSEN

et

al.: TECHNO-ECONOMIC EVALUATION OF NARROWBAND AND BROADBAND ACCESS NETWORK ALTERNATIVES

1191

4000 r

5 3500

e

3000

2500

c

E 2000

.-

U-

a,

v

rn

1500

3 1000

500

-

h

Access Alternatives

-

opper

-

- FTTC

- LL

- - - 4 - - - - *

. + -

II

0 I

30 100 300 1000 3000 10000 30000

Subscriber density (Subs/km2)

(4

Impact of Feed er Length

900

800

700

600

500

400

- - FTTC32

-

SS+Fibre

m

(I)

c

c 100

0

0

2500 5000 7500 1000

Feeder length

(rn)

(b)

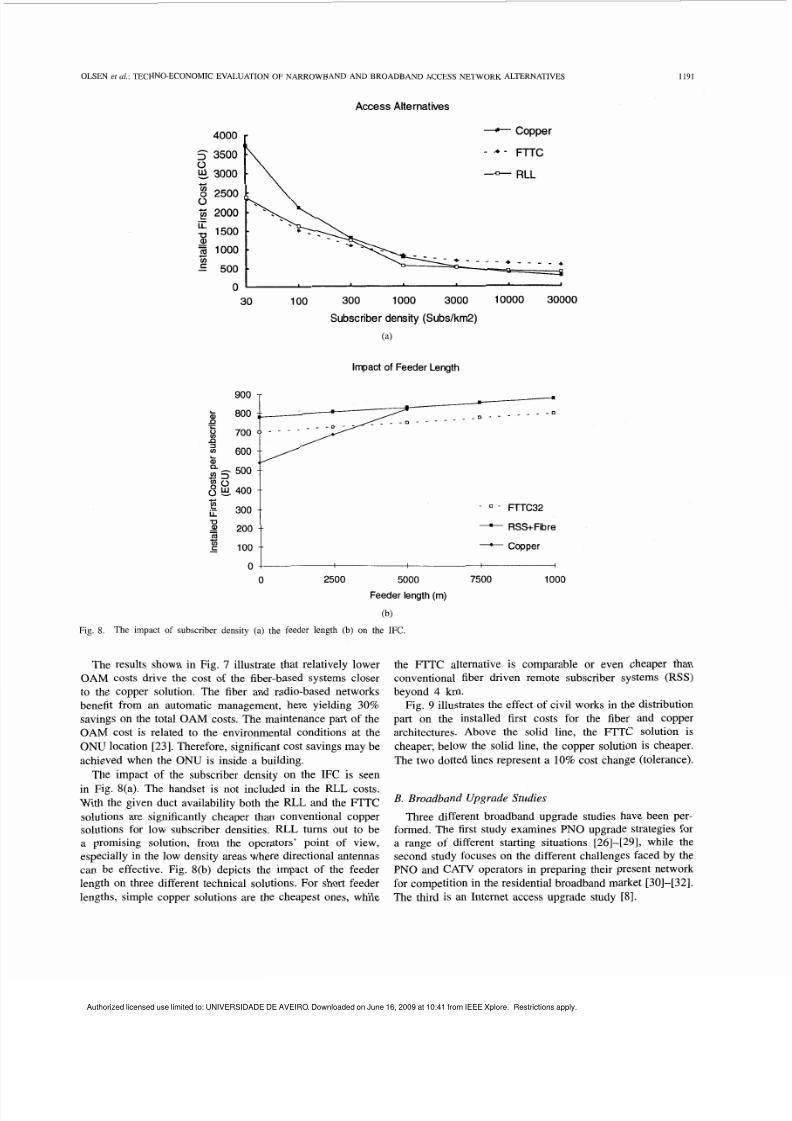

Fig. 8.

The impact

of

subscriber density (a) the feeder length (b) on the IFC.

The results shown in Fig. 7 illustrate that relatively lower

OAM costs drive the cost of the fiber-based systems closer

to the copper solution. The fiber and radio-based networks

benefit from an automatic management, here yielding 30%

savings on the total OAM costs. The maintenance part of the

OAM cost is related to the environmental conditions at the

ONU location [23]. Therefore, significant cost savings may be

achieved when the

ONU

is inside a building.

The impact of the subscriber density on the IFC is seen

in Fig. 8(a). The handset is not included in the RLL costs.

With the given duct availability both the RLL and the FTTC

solutions are significantly cheaper than conventional copper

solutions for low subscriber densities. RLL turns out to be

a promising solution, from the operators'

point of view,

especially in the low density areas w here directional antennas

can be effective. Fig. 8(b) depicts the impact of the feeder

length on three different technical solutions. For short feeder

lengths, simple copper solutions are the cheapest ones, w hile

the FTTC alternative is comparable or even cheaper than

conventional fiber driven remote subscriber systems (RSS)

beyond

4 km.

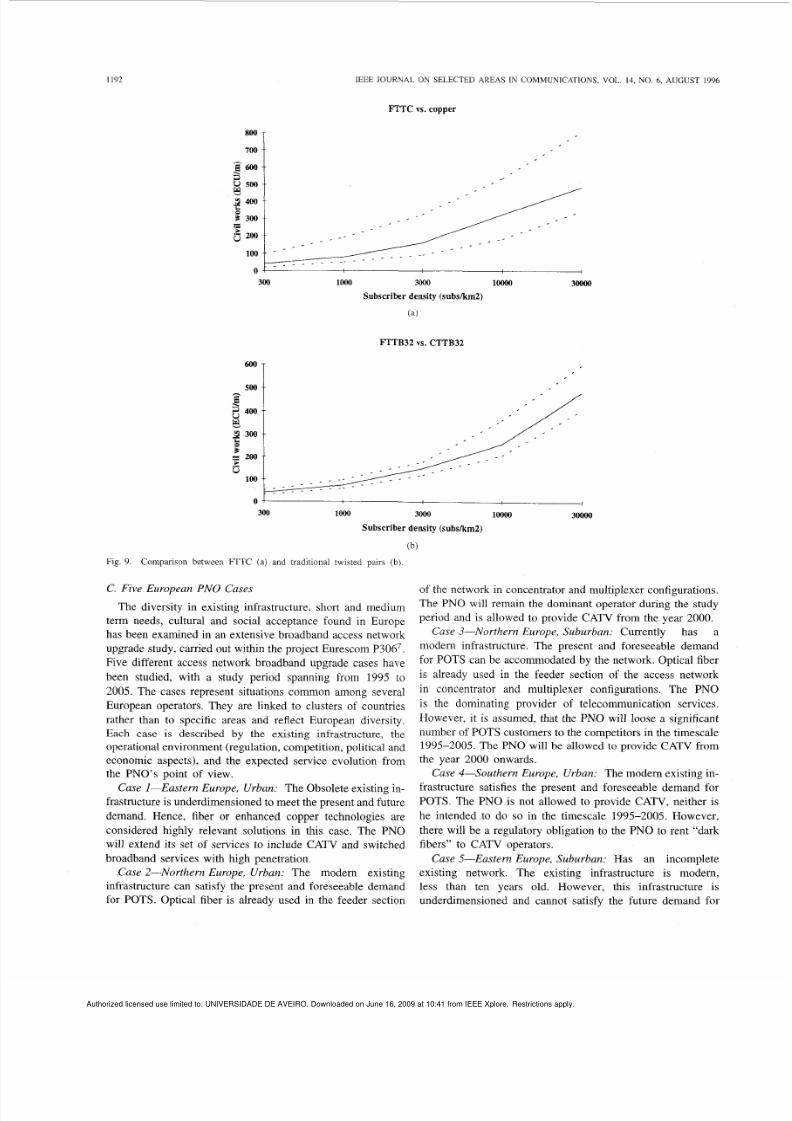

Fig. 9 illustrates the effect of civil works in the distribution

part on the installed first costs for the fiber and copper

architectures. Above the solid line, the FTTC solution is

cheaper; below the solid line, the copper solution is cheaper.

The two dotted lines represent a

10

cost change (tolerance).

B Broadband Upgrade Studies

Three different broadband upgrade studies have been per-

formed. The first study examines PN O upgrade strategies for

a range of different starting situation s [26]-[29], wh ile the

second study focuses on the different challenges faced by the

PNO and CATV operators in preparing their present network

for com petition in the residential broadband market [30]-[32].

The third is an Internet access upgrade study [SI.

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO. Downloaded on June 16, 2009 at 10:41 from IEEE Xplore. Restrictions apply.

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 9/20

I192

IEEE JOURNAL ON SELECTED AREAS IN COM MUNICATIONS, VOL. 14, NO. 6, AUGUST

1996

FTTC

vs.

copper

700 i

Or

I

300 loo0

3Ooo

loo00

3

Subscriber

density

subskm2)

(a)

FTTB32

vs.

CTTB32

“

I

loo0

3000 loo00 3ooO

00

Subscriber

density

(subs )

(b)

Fig. 9.

Comparison between

FTTC

(a) and traditional twisted pairs (b)

C. Five European PN O Cases

The diversity in existing infrastructure, short and medium

term needs, cultural and social acceptance found in Europe

has been examined in an extensive broadband access network

upgrade study, carried out w ithin the project Eurescom P3 067.

Five different access network broadband upgrade cases have

been studied, with a study period spa nning from 1995 to

2005. The cases represent situations common among several

European operators. They are linked to clusters of countries

rather than to specific areas and reflect European diversity.

Each case

is

described by the existing infrastructure, the

operational environment (regulation, competition, political and

economic aspects), and the expected service evolution from

the PNO’s point of view.

Case 1-Eastern Europe, Urb an: The Obsolete existing in-

frastructure is underdimensioned to meet the present and future

demand. Hence, fiber or enhanced copper technologies are

considered highly relevant solutions in this case. The PNO

will extend its set of services to include CATV and switched

broadband services with high penetration.

Case 2-Northern Europe, Urba n: The modern existing

infrastructure can satisfy the present and foreseeable demand

for POTS. Optical fiber is already used in the feeder section

of the network in concentrator and multiplexer configurations.

The PN O w ill remain the dominant operator during the study

period and is allowed to provide CATV from the year 2000.

Case 3-Northern Europe, Suburban: Currently has a

modem infrastructure. The present and foreseeable demand

for POTS

can

be accommo dated by the network. Optical fiber

is already used in the feeder section of the access network

in concentrator and multiplexer configurations. The PNO

is the dominating provider of telecommunication services.

However, it is assumed, that the PNO will loose a significant

number of PO TS customers to the competitors in the timescale

1995-2005. The PN O will be allowed to provide CATV from

the year 2000 onwards.

Case 4-Southern Europe, Urba n: The mo dern existing in-

frastructure satisfies the present and foreseeable demand for

POTS. The PNO is not allowed to provide CATV, neither is

he intended to do so in the timescale 1995-2005. However,

there will be a regulatory obligation to the PNO to rent “dark

fibers” to CATV operators,

Case 5-Eastern Europe, Subu rban: Has an incomplete

existing network. The existing infrastructure is modern,

less than ten years old. However, this infrastructure is

underdimensioned and cannot satisfy the future demand for

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO. Downloaded on June 16, 2009 at 10:41 from IEEE Xplore. Restrictions apply.

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 10/20

OLSEN

et ul.:

TECHNO-ECONOMIC EVALUATION

OF

NARROWBAND AND BROADBAND ACCESS NETWORK ALTERNATIVES

1193

70,000~~

60 000/0

50 000~~

40 000~0

l o ~ o o o / o . . . . . . . . .

go ooo/o

. . . . . . . . . . . . . . . . . . . .

80,~oo/o . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . .

OTS

ISDN

CATV

2 Mb/s

asymmetric

- Mb/s symmetric

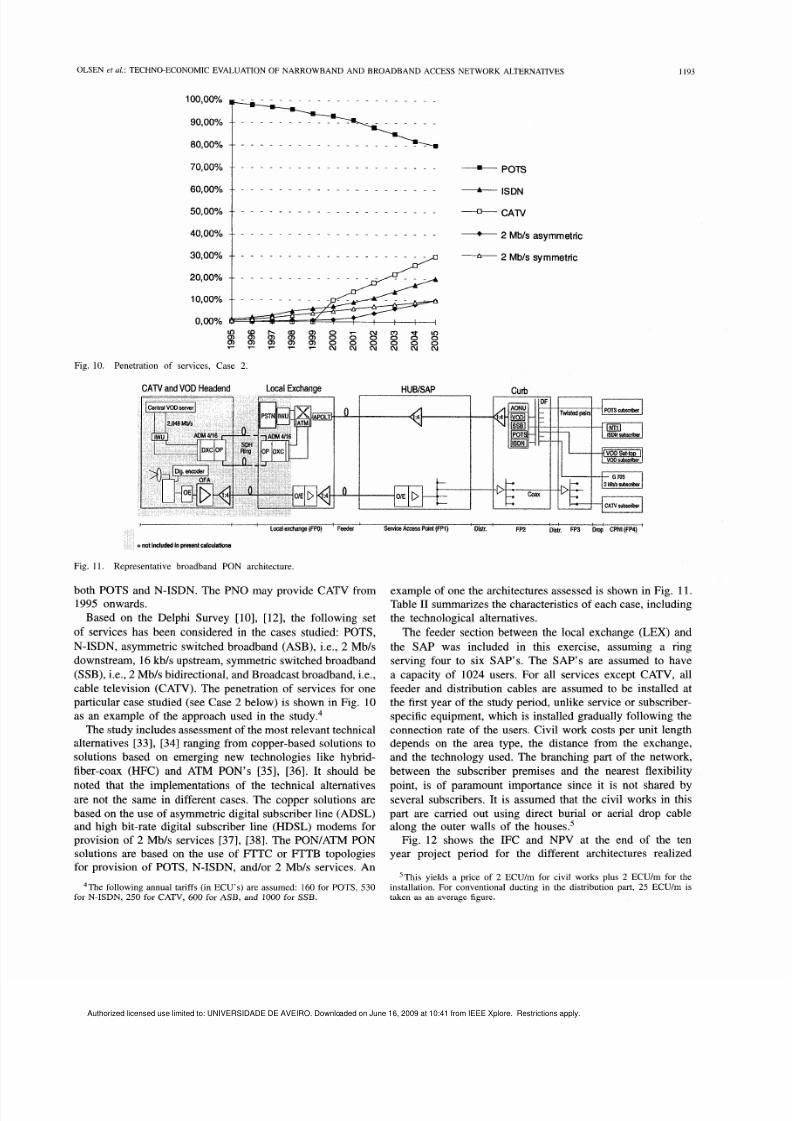

Fig. 10.

Penetration of services, Case 2.

CATVand

VOD

Headend

Local Exchanae

curb

=not

~ ~ i n ~ ~ ~ t ~ ~ ~

Fig. 11. Representative broadband

PON

architecture.

both POTS and N-ISDN. The PNO may provide CATV from

1995 onwards.

Based on the Delphi Survey [lo], [12], the following set

of

services has been considered in the cases studied: POTS,

N-ISDN , asymm etric switched broadband (ASB), i.e.,

2

Mb/s

downstream, 16 kb/s upstream, symmetric switched broadband

(SSB ), i.e.,

2

Mb/s b idirectional, and Bro adcast broadband, i.e.,

cable television (CATV). The p enetration of services for one

particular case studied (see Case 2 below) is show n in Fig. 10

as an example of the approach used in the study.4

The study includes assessment of the mo st relevant technical

alternatives [33], [34] ranging from copper-based solutions to

solutions based on emerging new technologies like hybrid-

fiber-coax

(HFC)

and ATM

PON’s

[35], [36]. It should be

noted that the implementations of the technical alternatives

are not the same in different cases. The copper solutions are

based on the use

of

asymm etric digital subscriber line (AD SL)

and high bit-rate digital subscriber line (HDSL) modems for

provision of 2 Mb/s services [37], [38]. The PON/ATM PON

solutions are based on the use of FTTC or FTTB topologies

for provision of POTS, N-ISDN, and/or 2 Mb/s services. An

4The following annual tanffs (in ECU’s) are assumed: 160 for POTS, 530

for N-ISDN, 250 for CATV, 600 for

ASB,

and 1000 for

SSB.

example of one the architectures assessed is sho wn in Fig. 1 1.

Table

I1

summ arizes the characteristics of each case, including

the technological alternatives.

The feeder section between the local exchange

(LEX)

and

the SAP was included in this exercise, assuming a ring

serving four to six SAP’s. The SAP’s are assumed to have

a capacity of 1024 users. For all services except CATV, all

feeder and distribution cables are assumed to be installed at

the first year of the study period, unlike service or subscriber-

specific equipment, which is installed gradually following the

connection rate of the users. Civil work costs per unit length

depends on the area type, the distance from the exchange,

and the technology used. The branching part of the network,

between the subscriber premises and the nearest flexibility

point, is of paramount importance since it is not shared by

several subscribers. It is assumed that the civil works in this

part are carried out using direct burial or aerial drop cable

along the outer walls

of

the houses.5

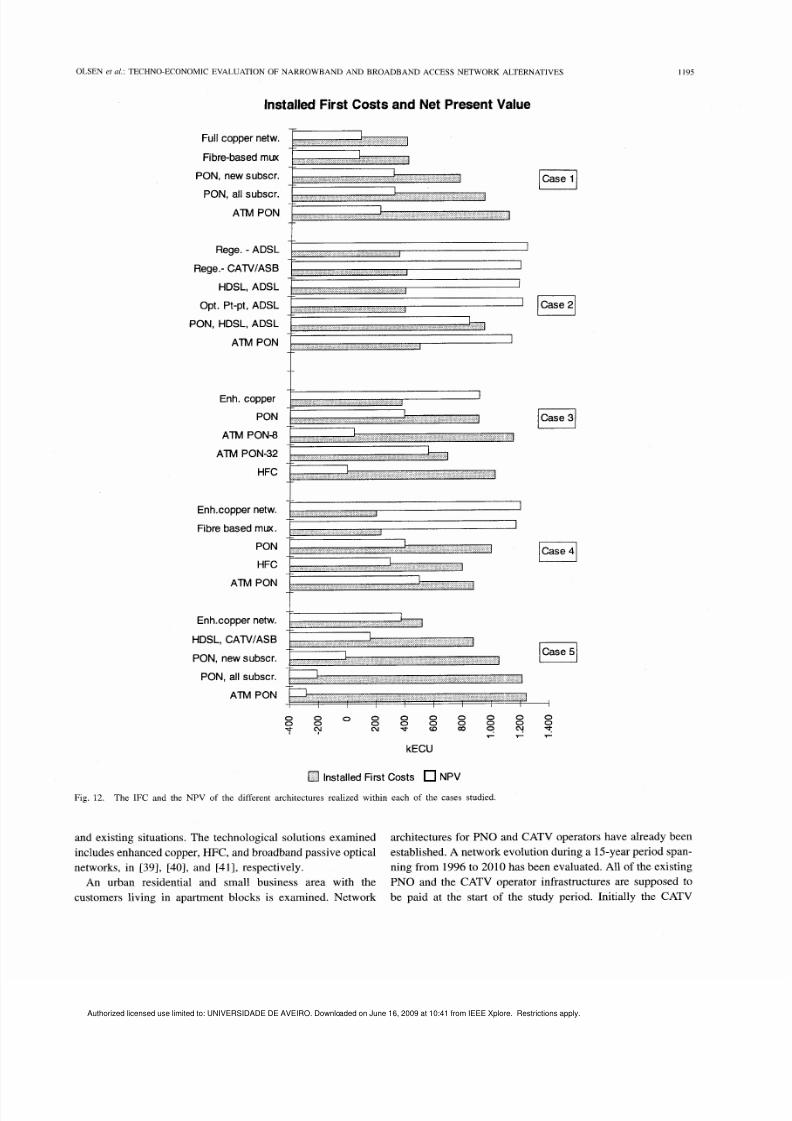

Fig.

12

shows the IFC and NPV at the end of the ten

year project period for the different architectures realized

5This

yields

a

price of 2 ECU/m for civil works plus 2 ECU/m for the

installation. For conventional ducting in

the

distribution part, 25 ECU/m

is

taken

as

an average figure.

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 11/20

IEEE JOURWAL ON SELECTED AREAS IN COMMUNICATIONS,

VOL.

14, NO. 6, AUGUST 1996

75

Case and

area type

provision.

increasing. POTS

penetration.Low effect

of

competition.

1

Eastern Europe,

urban

2

Northern Europe,

urban

3

Northern Europe,

suburban

4

Southern Europe,

urban

5

Eastern Europe,

suburban

Area

typefhouslng

structure

(user‘s distrib.:

single homes-

buildings ( ))

20-80

20-80

80 20

20 80

20-80

TABLE

I1

Quaiitv

of

existing

I

Operational

infrastructure

Duct availability

f

bre-copper

Y o )

60-30

90 50

90-50

90-50

0-0

Network

coverage

environment

(regulation, competition,

political and economic

aspects)

40

Low POTS penetration,

increasing rapidly. Low

level

of

competition.

Technical alternatives

considered

1.

Enhanced copper network

2.

Fibre-based multiplexer

3.

PON for new customers

4. PON for all customers

5. ATM PON

IA . Regenerator and enh. copper

1B .

Regenerator, CATVIASB

2. Enhanced copper network

3. Optical point-to-point, ADSL

4. PON and enh. copper network

5.

ATM PON

1. Enhanced copper network

2.

PON

3.

ATM PON (8 or

32

subdONU)

4. Hybrid Fibre Coax

1. Enhanced copper network

2. Fibre-basedmultiplexer

3.

PON

4.

Hybrid Fibre Coax

5.

ATM PON

1. Enhanced copper network

2.

Enhanced copper netw., CATV

3. PON for new customers

4. PON for all customers

5. ATM PON

within each of the cases studied. The IFC is discounted and

include cables, equipment, installation, and civil works. The

NPV shown is the cumulative sum of the discounted cash

flows from the start

of

the model year to the final year, not

including the residual value

of

the project. All

of

the upgrade

projects, except two of the Case

4

upgrades, seem to be heavy

projects with investments comparable to the establishment of

the present day narrowband networks. The payback periods

of

such upgrade projects typically are in the range of five to ten

years, indicating that access network broadband upgrades are

likely to be long-term projects.

The dwelling distribution and duct availability greatly in-

fluences the range and variation of the costs. However, for

some of these cases, the civil works play a less important

role comp ared to greenfield deploy ment. For all cases studied,

the IFC and the life cycle costs are only weakly dependent

on the subscriber density, since all cases represent upgrad-

ing architectures in a nongreenfield situation. The effect

of

dwelling distribution is shown in Case 3, in particular, where

the majority of the users live in single homes. The main

differences between Cases

2

and 3 are the dwe lling distribution

and the civil works as described in Table I. Although in Case

5 all the ducts have to be created, the fact that the majority of

users live in large buildings compensates for high additional

civil works as compared to Case 3. Also, in Case 1, the

duct availability is relatively lower, with the housing structure

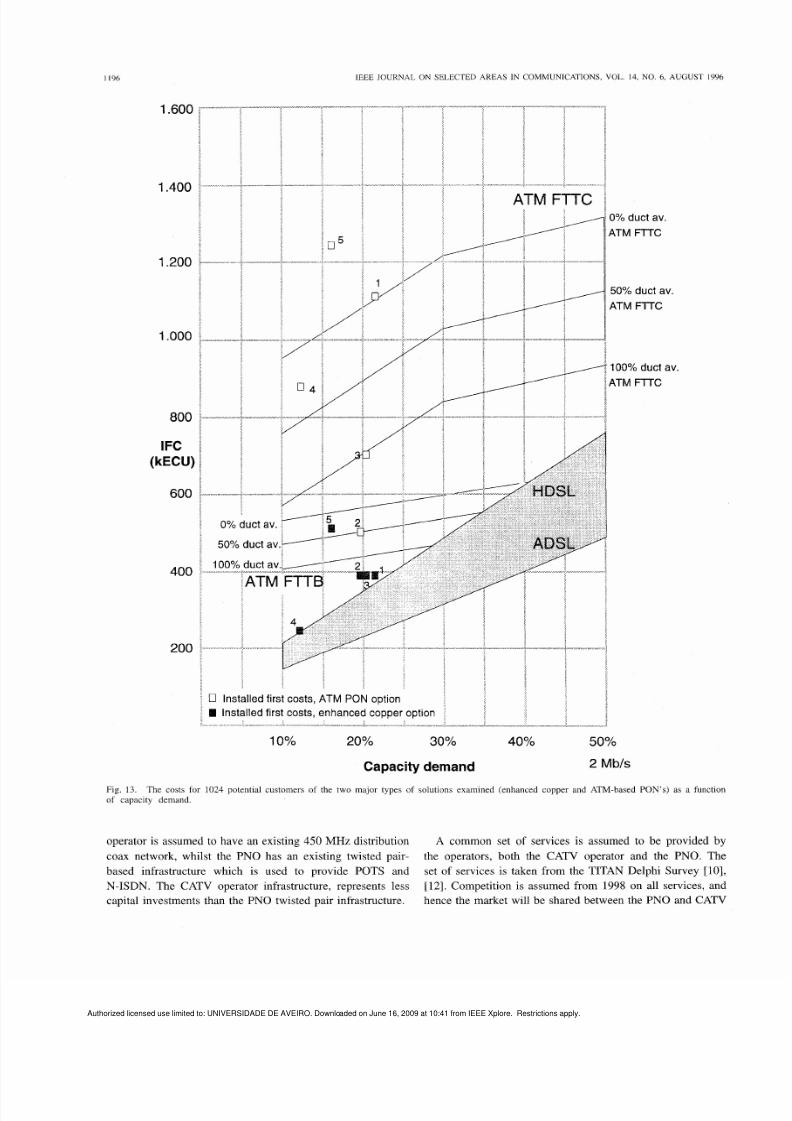

having a similar compensating impact. Fig.

13

depicts the

costs of the two major types of solutions examined+nhanced

copp er and ATM -based PON’s-as a func tion of the avera ge

capacity demand. The IFC for ATM PON in FTTC and

FTTB configurations are included for three degrees of duct

availability, 0 ,

50 ,

and 100 . The figure shows that the

low demand for broadband services in the pure residential

areas favors the copper-based solutions, while high capacity

demand would have favored more aggressive fiber based

access network solutions. The upfront costs are lower for the

copper-based solutions, whilst the marginal costs of providing

more bandw idth are smaller for the fiber-based solutions. Th e

break-even point indicates the capacity limit beyond which

the demand can justify the deployment

of

optical solutions

in pure economical terms. In general, if the demand is high

enough, the fiber-based solutions will probably be the most

cost-effective solution. In conclusion, the average capacity

demand is a very important parameter

to

take into account

in strategic considerations.

Fig. 13 also depicts the influence on the overall costs

of the sharing of network termination equipment. The IFC

for ATM PON’s with eight and

32

subscribers sharing one

ONU are shown. This confirms that the degree of customer

sharing of optical network terminations is an important

aspect of a cost-effective broadband upgrade with PON’s.

For all solutions and cases, the costs

of

electronics are

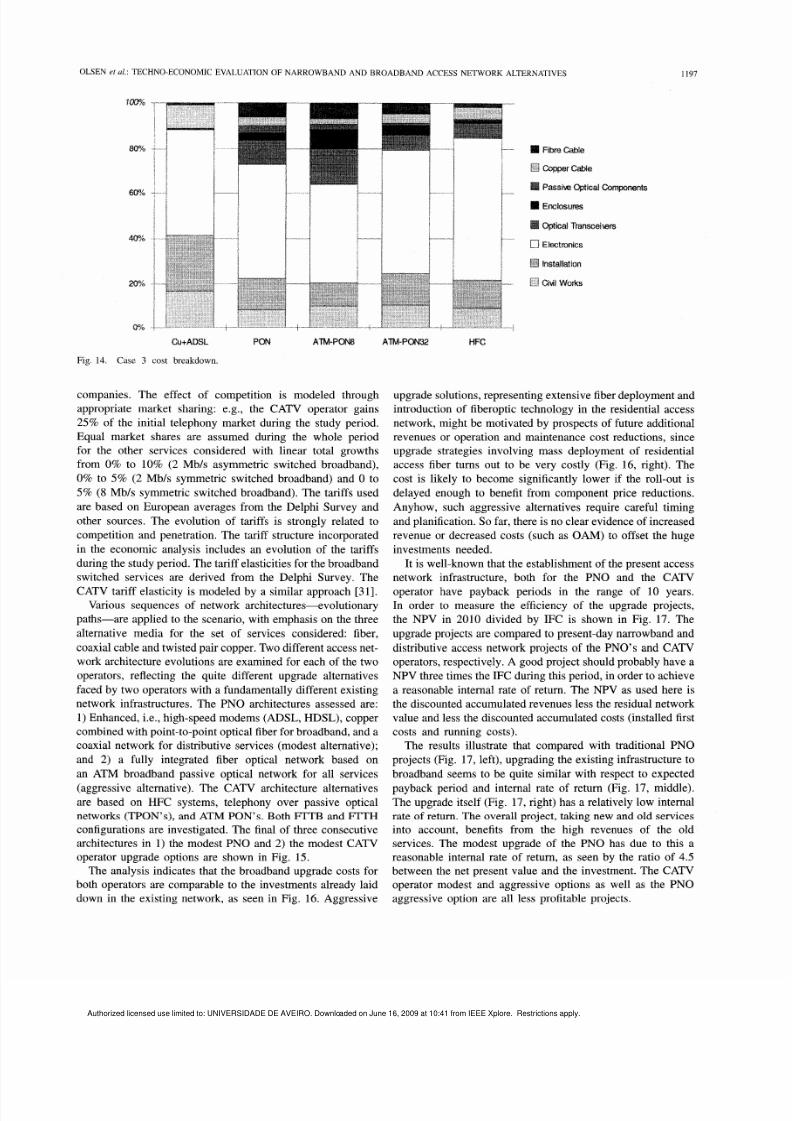

dominant. This is shown in the cost-breakdown of the

different solutions for Case

3

in Fig. 14.

D . CATV

Operator and PNO Broadband Upgrade Strategies

An analysis of a selected broadband access netw ork up-

grade alternatives for PNO’s and CATV operators has been

performed, taking the effect of comp etition into account [3 ],

[32]. The competitor’s different existing access networks call

for quite different upgrade strategies, highlighting the impor-

tance of exam ining the com petitors’ technological alternatives

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 12/20

OLSEN et al.: TECHNO-ECONOMIC EVALUATION

OF

NARROW BAND AND BROADBA ND ACCESS NETWORK ALTERNATIVES

1195

Fig. 12.

Installed First Co sts and Net Pres ent Value

Full copper netw.

Fibre-based

rnux

PON, new subscr.

PON, all subscr.

ATM PON

Rege. - ADSL

Rege.- CAlV /AS B

HDSL, ADSL

Opt. P t-pt, ADSL

PON, HDSL, ADSL

ATM PON

Enh. copper

PON

ATM PONS

ATM PON-32

HFC

Enh.copper netw.

Fibre based

mux.

PON

HFC

ATM PON

Enh.copper netw.

HDSL, CAlV/ASB

PON, new subsc r.

PON, all subscr.

ATM PON

kECU

0 Installed First Costs NPV

The IFC and the NPV ot the different architectures realized within each of the cases studied

and existing situations. The technological solutions examined

includes enhanced copper, HFC, and broadband p assive optical

networks, in [39], [40], and [41], respectively.

An urban residential and small business area with the

customers living in apartment blocks is examined. Network

architectures for PNO and CATV operators have already been

established. A network evolution during a 15-year period span-

ning from 1996 to 2010 has been evaluated. All of the existing

PNO

and the CATV operator infrastructures are supposed to

be paid at the start of the study period. Initially the CATV

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 13/20

IEEE

JOURNAL ON SELECTED AREAS IN COMMUN ICATIONS, VOL. 14, NO. 6, AUGUST 1996

I96

1.600

1.400

1.200

1 ooo

800

IFC

kECU)

600

400

200

--

--

0

duct av.

50

duct av

100

duct ac

ATM

nstalled

first

costs, ATM PON option

nstalled first costs, enhanced copper option

lxxi

~

~-

X I l l l l

10 20

30

Capacity demand

ATM

FTTC

0 duct av.

ATM FTTC

50 duct av.

ATM FTTC

100°/o

duct av.

ATM

FTTC

Fig.

13.

of capacity demand.

The costs for 1024 potential customers of the two major types of solutions examined (enhanced copper and ATM-based PON's) as a function

operator

is

assumed to have an existing

450

MHz distribution

coax network, whilst the PNO has an existing twisted pair-

based infrastructure which is used

to

provide POTS and

N-ISDN. The CATV operator infrastructure, represents less

capital investments than the PNO twisted pair infrastructure.

A common set of services is assumed to be provided by

the operators, both the CATV operator and the PNO. The

set of services is taken from the TITAN Delphi Survey

[lo],

[12].

Competition is assumed from

1998

on all services, and

hence the market will be shared between the PNO and CATV

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 14/20

OLSEN

et

al.: TECHNO-ECONOMIC EVALUATION OF NARROWBAND AND BROADBAND ACCESS NETWORK ALTERNATIVES

1197

Fig. 14. Case 3 cost

breakdown.

companies. The effect of competition is modeled through

appropriate market sharing: e.g., the CATV operator gains

25

of the initial telephony market during the study period.

Equal market shares are assumed during the whole period

for the other services considered with linear total growths

from

0

to 10 (2 Mb/s asymmetric switched broadband),

0 to 5

(2

Mb/s symmetric switched broadband) and 0 to

5

(8 Mb/s symm etric switched broadband). The tariffs used

are based on European averages from the Delphi Survey and

other sources. The evolution of tariffs is strongly related to

competition and p enetration. The tariff structure incorporated

in the economic analysis includes an evolution of the tariffs

during the study period. The tariff elasticities for the broadb and

switched services are derived from the Delphi Survey. The

CATV tariff elasticity is mod eled by a similar approach [31].

Various sequences of network architectures-evolutionary

paths-are applied to the scenario, with emp hasis on the three

alternative media for the set of services considered: fiber,

coaxial cable and twisted pair copper. Two d ifferent access net-

work architecture evolutions are examined for each of the two

operators, reflecting the quite different upgrade alternatives

faced by two o perators with a fundam entally different existing

network infrastructures. The PNO architectures assessed are:

1) Enhanced, i.e., high-speed modems (A DSL,

HDSL),

copper

combined with point-to-point optical fiber for broadband, an d a

coaxial network for distributive services (modest alternative);

and 2) a fully integrated fiber optical network based on

an ATM broadband passive optical network for all services

(aggressive alternative). The CATV architecture alternatives

are based on HFC systems, telephony over passive optical

networks (TPON’s), and ATM PON’s. Both FTTB and FTTH

configurations are investigated. The final of three consecutive

architectures in 1) the mod est PNO and

2)

the modest CATV

operator upgrade options are shown in Fig.

15.

The analysis indicates that the broadban d upgrade costs for

both o perators are comparable to the investmen ts already laid

down in the existing network, as seen in Fig. 16. Aggressive

upgrade solutions, representing extensive fiber deployment and

introduction of fiberoptic technology in the residential access

network, might be motivated by prospects of future additional

revenues or operation and maintenance cost reductions, since

upgrade strategies involving mass deployment of residential

access fiber turns out to be very costly (Fig. 16, right). The

cost is likely to become significantly lower if the roll-out is

delayed enough to benefit from component price reductions.

Anyhow, such aggressive alternatives require careful timing

and planification. So far, there is no clear eviden ce of increased

revenue or decreased costs (such as OAM) to offset the huge

investments needed.

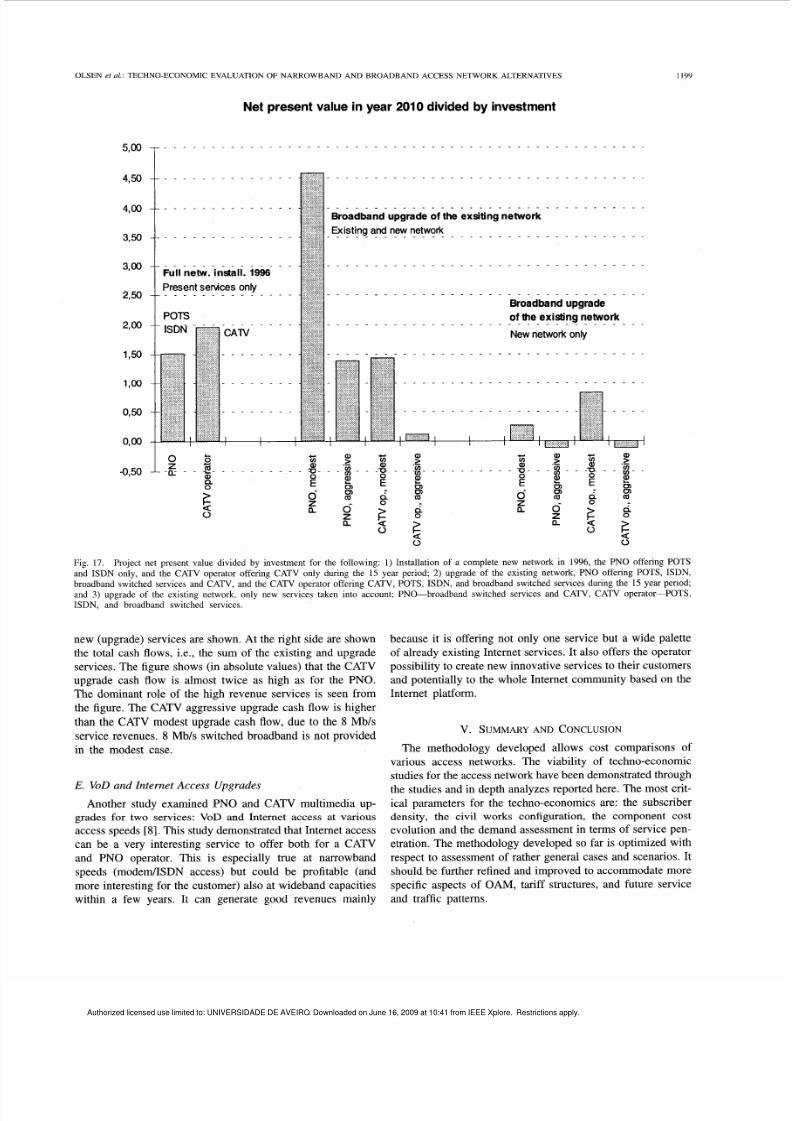

It is well-known that the establishment

of

the present access

network infrastructure, both for the PNO and the CATV

operator have payback periods in the range of 10 years.

In order to measure the efficiency of the upgrade projects,

the NPV in 2010 divided by IFC is shown in Fig. 17. The

upgrade projects are compared to present-day narrowband and

distributive access netw ork projects of the PNO’s and CATV

operators, respectively. A good p roject should probably have a

NPV three times the IFC during this period, in order to achieve

a reasonable internal rate of return. The NPV as used here is

the discounted accum ulated revenues less the residual network

value and less the discounted accumulated costs (installed first

costs and running costs).

The results illustrate that compared with traditional PNO

projects (Fig. 17, left), upgrading the existing infrastructure to

broadband seems to be quite similar with respect to expected

payback period and internal rate

of

return (Fig. 17, middle).

The upg rade itself (Fig. 17, right) has a relatively low internal

rate of return. The overall project, taking new and old services

into account, benefits from the high revenues of the old

services. The modest upgrade of the PNO has due to this a

reasonable internal rate of return, as seen by the ratio

of 4.5

between the net present value an d the investment. The CATV

operator modest and aggressive options as well as the PNO

aggressive option are all less profitable projects.

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 15/20

119X

IEEE JOURNAL

ON SELECTED

AREAS IN COMMUNICATIONS, VOL.

14

NO.

6,

AUGUST

1996

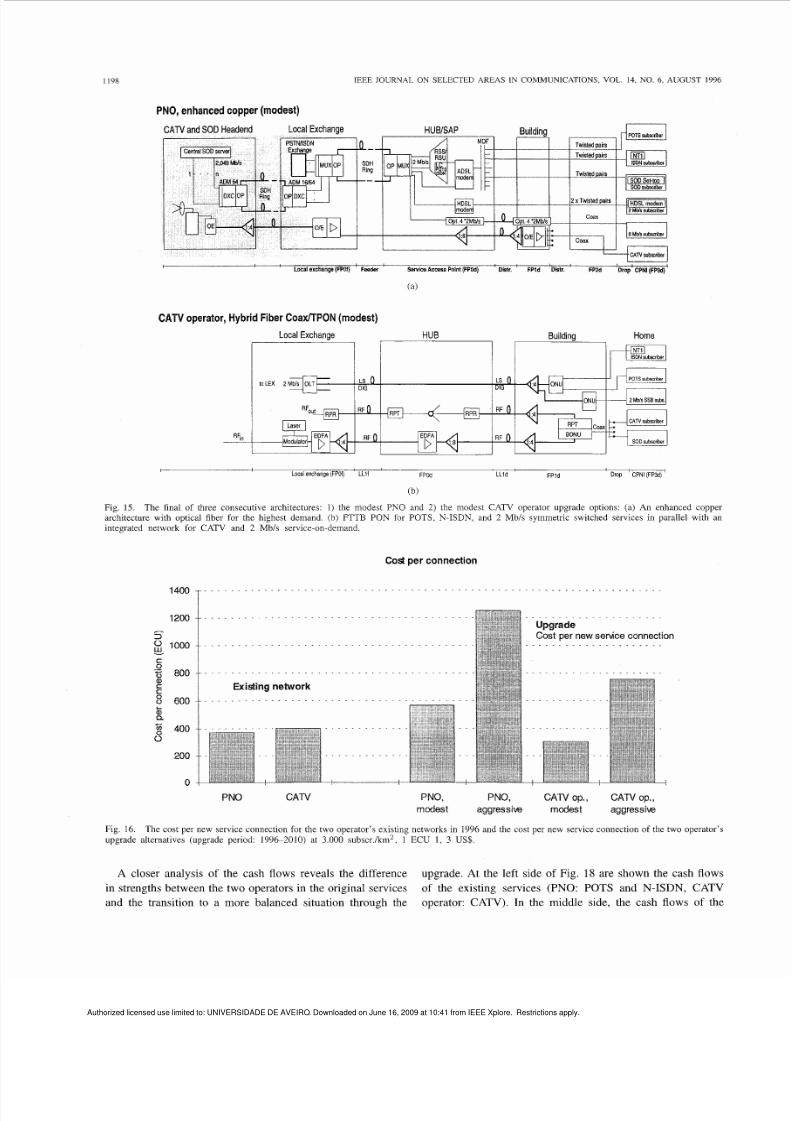

PNO, enhanced copper

(modest)

' Locelexcharqe(mD1) Fssder servicaAccssePolnt(Fwd)

DMr. '

FPld

Dlolr.

'

(a)

CATV

operato r, Hybr id Fiber CoaxfTPON (modes t)

I

Loca exchange(FPC ' LLl l FPW LLld FPld

Drop

CPNI (FPBd)'

(b)

Fig. 15. The final of three consecutive architectures: 1) the modest PNO and 2) the modest CATV operator upgrade options: (a) An enhanced copper

architecture with optical fiber for the highest demand. (b) F?TB PON for POTS. N-ISDN, and 2 Mb/s symmetric switched services in parallel with an

integrated network for CATV and 2 Mh/s service-on-demand.

Cost

per

connection

. . . . . . . . . . . . . . . . . . . . . . . . . . . .

I4Oo T

1200

c

2

1000

C

W

c

g a00

8 600

g 400

a

+-

200

j . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . .

Existing

network

. . . . . . . . . . . .

-

PNO

C A N

. .

. . . . . . . . . . . . . . . . . . .

Upgrade

Cost per new service connection

. . . . . . . . . . . . . . . . . . . .

PNO,

PNO

CATV

op. CATV op.,

modest aggressiw modest

aggressive

Fig. 16.

upgrade alternatives (upgrade period: 1996-2010) at 3.000 subscr,/km2, 1 ECU 1, 3 US .

The cost per new service connection for the two operator's existing networks in 1996 and the cost per new service connection

of

the two operator's

A closer analysis

of

the cash flows reveals the difference

in strengths between the two operators in the original services

and the transition to a more balanced situation through the

upgrade. At the left side

of

Fig.

18

are shown the cash flows

of

the existing services (PNO: POTS and N-ISDN, CATV

operator:

CATV).

In the middle side, the cash flows

of

the

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 16/20

OLSEN ef

al.:

TECHNO-ECONOMIC EVALUATION OF NARROWBAND AND BROADBAND

ACCESS

NETWORK ALTERNATIVES

1199

Net present value in year

2010

divided

by

investment

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Broadband upgrade

of

the exsiting network

Exist ing and new network

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Broadband upgrade

of the existing network

New network only

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . .

. . . . . . . . . . . . . . . . . .

. . . . . . .

L

2

. . . . . . . . .

4

a

z

a

z 4

d

z

a

Fig. 17. Project net present value divided by investment for the following:

1)

Installation of

a

complete new network in 1996, the PNO offering POTS

and ISDN only, and the CATV operator offering CATV only during the 15 year period; 2) upgrade of the existing network, PNO offering POTS, ISDN,

broadband switched services and CATV, and the CATV operator offering CATV, POTS, ISDN, and broadband switched services during the 15 year period;

and

3)

upgrade of the existing network, only new services taken into account: PNO-broadband switched services and CATV, CATV operator-POTS,

ISDN, and broadband switched services.

new (up grade) services are shown. At the right side are shown

the total cash flows, i.e., the sum of the existing and upgrade

services. The figure shows (in ab solute values) that the CATV

upgrade cash flow is almost twice as high as for the PNO.

The dominant role of the high revenue services is seen from

the figure. The CATV ag gressive upgrade cash flow is higher

than the CATV mo dest upgrade cash flow, due to the

8

Mb/s

service revenues.

8

Mb/s switched broadband is not provided

in the modest case.

E VoD

and

Internet Access

Upgrades

Another study examined PNO and CATV multimedia up-

grades for two services:

VoD

and Internet access at various

access speeds [8]. This study dem onstrated that Internet access

can be a very interesting service to offer both for a CATV

and PNO operator. This is especially true at narrowband

speeds (modem/lSDN access) but could be profitable (and

more interesting for the customer) also at wideban d capacities

within a few years. It can generate good revenues mainly

because it is offering not only one service but a wide palette

of already existing Internet services. It also offers the op erator

possibility to create new innovative services to their custom ers

and potentially to the who le Internet community based on the

Internet platform.

v . SUMMARY AND CONCLUSION

The methodology developed allows cost comparisons of

various access networks. The viability of techno-economic

studies for the access network have been dem onstrated through

the studies and in depth an alyzes reported here. The m ost crit-

ical parameters for the techno-economics are: the subscriber

density, the civil works configuration, the component cost

evolution and the dem and assessment in terms of service pen-

etration. The m ethodology developed

so

far is optimized with

respect to assessment of rather g eneral cases and scen arios. It

should be further refined and improved to accommo date more

specific aspects of O AM , tariff structures, and future service

and traffic patterns.

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO Downloaded on June 16 2009 at 10:41 from IEEE Xplore Restrictions apply

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 17/20

I200

IEEE JOURNAL ON SELECTED AREAS IN COMMUNICATIONS, VOL. 14, NO. 6, AUGUST 1996

Cash

flow

in

year 2010

2 200.000ECU

N

m

X 150.000ECU

c

.-

-

.K

U

al

K

v

100.000ECU

8

5

5

50.000ECU

OECU

Existing

senices

(CATV, POTS and

ISDN)

Upgrade

.

g g

> a

t

Q

v

a

U

e

d

?

Q

0

a

v

.-

2

m

m

m

d

>

5

P

a

_ _

-

P

a

(3

Fig.

18.

The

cash flow in year

2010

of

the

CATV operator and

PNO

projects.

for

existlng services, the network upgrade, and the total network

If only POTS and N-ISDN services are taken into account,

the copper network is m ost often the cheapest solution. Higher

civil works costs favor fiber-sharing solutions, such as FTTC

or FTTB with

32

users per ONU. In low density areas, the

RLL and FTT C/B are significantly cheaper than the equivalent

copper cable alternatives analyzed here. Nevertheless, the

service provision capability of RLL is relatively limited.

The examination of the five European cases highlights

the importance of the existing network infrastructure for an

appro priately phased introduction of FITL in already well-

equipp ed areas. The introduction strategies in all cases greatly

depends on dwelling distribution. The demand for new POT S

lines is one of the main driving forces in Eastern European

countries and in some o ther developing areas. Introduction of

FITL in developed countries, where a good existing copper

network is available, might be advisable starting directly with

broadband FITL systems.

The study of CATV operator and PNO strategies shows that

the upgrade costs for both operators are high and comparable

to the investments already laid dow n in the existing network.

Compared with traditional PNO projects, the upgrade projects

are seemingly quite similar with respect to expected payback

periods and internal rates of return. T he results fro m the study

reveal the difference in strengths between the two operators in

the original revenue base an d the transition to a more balanc ed

revenue base situation through the broad band upgrade.

Internet access has been shown to be a potentially more lu-

crative new service than plain VoD. This could pave operators

a profitable path to wide- and broadband network upgrades.

In general, the broadband upgrade studies demonstrate that

future-proof integrated access technologies like ATM PON

and HFC systems can be economically viable under some

circumstances. The cost difference between optical and en-

hanced copper technologies

is

relatively small for some

of

the analyzed cases. This is likely to favor the introduction of

future-proof integrated access technologies.

The extensive fiber deployment and introduction of fiberop-

tic technology in the residential access network might be

motivated by prospects of future additional revenues or opera-

tion and maintenance cost reductions, since upgrade strategies

involving mass deployment of residential access fiber turns out

to be very costly. The cost is likely to become significantly

lower if the system introduction is delayed enough to benefit

from component price reductions.

So

far, there is no clear

Authorized licensed use limited to: UNIVERSIDADE DE AVEIRO. Downloaded on June 16, 2009 at 10:41 from IEEE Xplore. Restrictions apply.

7/18/2019 Olsen Duarte Et Ali IEEE JSAC 1996

http://slidepdf.com/reader/full/olsen-duarte-et-ali-ieee-jsac-1996 18/20

OLSEN et

ul.:

TECHNO-ECONOMIC EVALUATION OF NARROW BAND AND BR OADBA ND ACCESS NETWORK ALTERNATIVES

1201

evidence of increased revenue

or

decreased costs (such as

OAM) to offset the huge investments needed.

Rolling out fiber remains a key decision

of

great strategic

importance in access network upgrading, due to the expected

longer lifetime of o ptical cable infrastructure as com pared to

the system technologies.

ACKNOWLEDGMENT

TITAN is project

2087 of

the European RACE program.

This paper is also based on results achieved in the Eurescom

P306 project. The authors gratefully acknowledge the support

of the European Com mission and Eurescom 6 in carrying out

this work. Members of RA CE 20 87/TITAN : A. Zaganiaris,

D.

Joram (CNET-France Telecom-F),

B .

T. Olsen, K. Stordahl,

L.

A. Ims, T. gverli (Telenor Research-N),

S .

Markatos

(Univ. of Athens-GR), M . Tahkoko rpi, M. Kalervo, I. Welling

(Nokia-FIN),

J.

Mononen, M. Liihteenoja (Telecom Finland-

FIN), N. Kerteux (MET-F), M. De Bortoli, U. Ferrero, M.

[I41

D.

Gardan, A. Zaganiaris, A. Madani, R. Madigou, and

D.

Machon,

“Techno-economics of advanced optical subscriber networks,” in

Proc.

IEEE GLOBECOM’89,

Dallas, TX, Nov. 27-30, 1989.

[IS] A. Zaganiaris, D. Gardan, A. Roosma, M. Potts, R. Beeler, and A.

Socard, “Fiber to the home, A techno-economic evaluation within

Europe, by RACE program,” in Proc. ISSLS’91 Amsterdam, The

Netherlands, Apr. 22-26, 1991.

[16] T. P. Wright, “Factors affecting the cost of airplanes,”

J

Aeronautic

Science, vol. 3, no. 4, pp. 122-128, 1936.

[17] J. R. Crawford, “Learning curve, ship curve, ratios, related data,”

Lockheed Aircraft Corporation, 1944.

[

181 L. E. Yelle, “The learning curve: Historical review and comprehensive

survey,” Decision Science, vol. 10, no. 2, pp. 302-328, 1979.

[19] B. T. Olsen, A. Zaganiaris, N. Gieschen, M. Tahkokorpi, M. Drieskens,

and

S.

Markatos, “RACE 2087/TITAN: Tool for introduction scenarios

and techno-economic studies for the access network,” in

Proc. M C E

Open Workshop Broudhund Access, Nijmegen, The Netherlands, June

7-8,

1993.

[20] A. Zaganiaris, N. Gieschen, B. T. Olsen, K. Stordahl, M. Tahkokorpi,

M. Drieskens, and A. Ajibulu, “A methodology for achieving life-cycle

costs of optical access networks-from RACE 2087/TITAN,” in

Proc.

l l t h Annu Conf: EFOC’93,

the Hague, The Netherlands, June 30-July

2, 1993.

[21] A. Zaganiaris, M. Tahkokorpi, M . Drieskens,

J.

Van Hoecke, B. T.

Olsen,

S .

Markatos, and

M .

De Bortoli, “Life-cycle costs and economical

Ravera,

S .

Balzaretti, (CSELT-I), M. Drieskens,

J.

Kraushaar,

J.

van (Raynet-B), N. Gieschen (DBP-Telekom-D)

F.

Fleuren (KPN-NL), M. De Oliveira Duarte, E. de Castro,

budget of optical and hybrid access networks,” in Proc. 5th IEEE Con

OpticaUHybrid

Access

Networks ,

Montreal, Canada, Sept. 7-9, 1993.

[22] R. Diaz de la Iglesia, “Service-affecting optoelectronic failures in FITL

systems: Downtime, repair actions and maintenance expenses,”

IEEE J

M. J. Oliveira (Univ. Aveiro-P), and R. Diaz de la Iglesia

(Telefonica-SP).

Select. Areas Commun., vol. 12, no. 2, Feb. 1994.

[23] A. Zaganiaris, U. Ferrero, S. Balzaretti, M. Tahkokorpi, M. Kalervo,

B.

T.

Olsen, and K. Stordahl, “Methodology for risk assessment and

REFERENCES

111 P. Kaiser and T. Swanenburg, “Introduction to the 2nd RACE/Bellcore

workshop on optical networks,” in Proc.

2nd

RACE/Bellcore Workshop

Opt. Networks , Red Bank, NJ, Feb. 17-19, 1993.

[2] J Stern, “The evolution of broadband multimedia networks,” in

Proc.

6th Int. IEEE Workshop OAN’94, Kyoto, Japan, Oct. 16-19, 1994.

[3] H. L. Lemberg, “Evolution of optical fiber-based access networks in

the US., ” in

Proc.

6th

lnt.

IEEE Workshop OAN’94, Kyoto, Japan, Oct.

16-19, 1994.

[4] A. Cook and J. Stern, “Optical fiber access-Perspectives toward the

21st century,”

lEEE Commun Mug. ,

vol. 32, no. 2, pp. 78-86, Feb.

1994.

[SI D. P. Reed, Residential Fiber Optic Networks: An Engineering and

Economic Anulysis.

[6] P. LeBel and R. Oliver, “Residential broadband architectures strategies

and economics,” in Proc. 7th Int. IEEE Workshop OAN’95, Nuremberg,

Germany, Sept. 24-27, 1995.

[7] J.

Saijonmaa, M. Tahkokorpi, and 1. Welling, “Cost

of

investment

and revenue modeling and analysis of various networked multimedia

services in PTO and CATV operator environments,”

in

Proc. TELE-

COM ’95, Technol. Sum mit,

Geneva, Switzerland, Oct. 3-1 1, 1995, pp.

629-633.

[8] K. W. Lu, M. 1. Eiger, and

H.

L. Lemberg, “System and cost analysis

of broadband fiber loop architectures,” IEEE J Select. Areas Commun.,

vol.

8,

no.

6,

pp. 1058-1067, June 1990.

[9]

K.

Stordahl and

E.

Murphy, “Methods for forecasting long term demand

for wide and broadband services in the residential market,”

IEEE

Commun Mag., vol. 33 , no. 2, pp. 44449, Feb. 1995.

[IO] D. P. Luck, “Broadband to the home: Evolution scenarios for Australia,”

in Proc. 13th Annu Con EFOC&N’95, Brighton, UK, June 27-30,

199.5,

[ 1

11 K. Stordahl, B. T. Olsen, E. Murphy, A. Zaganiaris, E. Castro, and M.

Ravera, “Delphi survcy: Forecasting demand for wide- and broadband

services. From RACE 2087/TITAN,” in

Proc. 6th Inte.

IEEE

Workshop

OAN’94,

Kyoto, Japan, Oct. 16-19, 1994.

1121 D. P. Malley and 0

K.

Tonguz, “Fiber in the loop: Where and when is it

feasible,” IEEE J. Select. Areas Commun., vol. 10, no. 9, pp. 1523-1544,

Dec. 1992.

[I31 T. Miki, “Toward the service-rich era,” IEEE Commun. Mug., vol. 32,

no. 2, pp. 34-39, Feb. 1994.

Norwood, MA: Artech, 1992.

6This does not imply that it reflects a common technical po3ition of all the

Eurescom sharcholderdparties.

_.

techno-economic evaluation

of

optical access networks,” in Pmc. 20th

ECOC’94, Florence, Italy, Sept. 25-29, 1994.

[24] A. Zaganiaris, B. T. Olsen, K. Stordahl,

M.

De Bortoli, and M.

Tahkokorpi, “Life-cycle cost and risk assessment of the access network.

From RACE 2087/TITAN.” in Proc. 6th Int Workshoa OAN’94, Kyoto,

Japan, Oct. 16-19, 1994.

L. Ims, D. Myhre, B. T. Olsen, J . Mononen,

M.

Lathenooia, U. Ferrero,

A. Zaganiaris, K. Szomolanyi, and I. Orfanos, “Advanced multiservice

scenarios for EuroDe,” in Proc. 13thAnnu.

Conf:

EFOCdtN’95. Brighton.

UK, June 27-30,

~

1995.

L.

A. Ims,

B. T