Embed Size (px)

Citation preview

Old Mutual SA Businesses Day

28 May 2003

Richard Laubscher

Chief Executive

Programme

• The marketplace

• Nedcor’s position

• Strategic framework / SWOT

• Key drivers / issues

• Bancassurance

• Conclusion

The marketplace

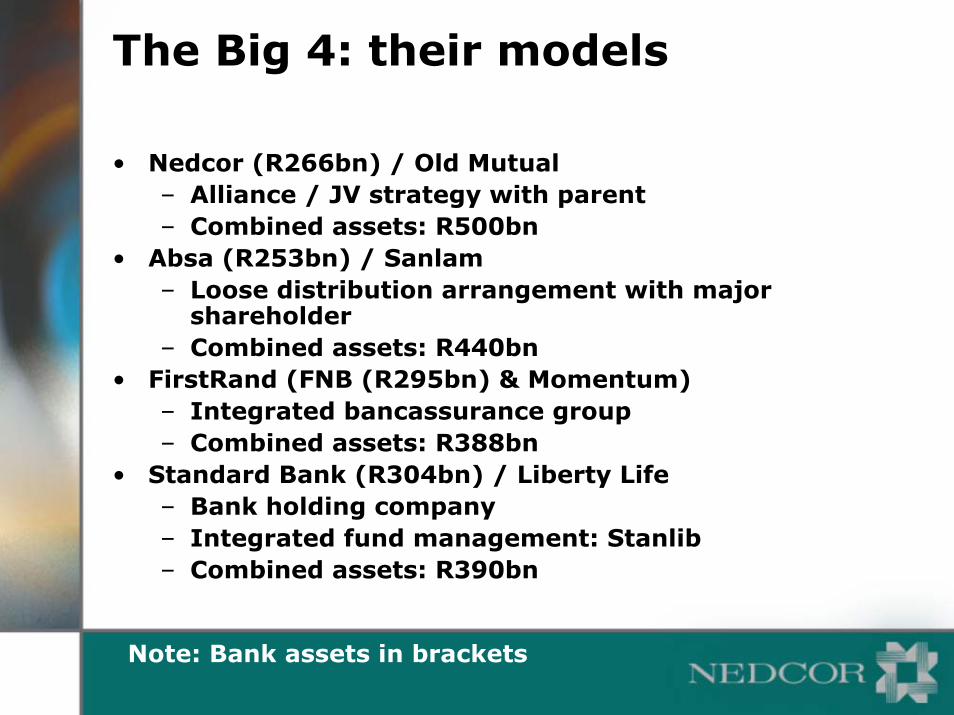

The Big 4: their models

• Nedcor (R266bn) / Old Mutual– Alliance / JV strategy with parent– Combined assets: R500bn

• Absa (R253bn) / Sanlam– Loose distribution arrangement with major

shareholder– Combined assets: R440bn

• FirstRand (FNB (R295bn) & Momentum)– Integrated bancassurance group– Combined assets: R388bn

• Standard Bank (R304bn) / Liberty Life– Bank holding company– Integrated fund management: Stanlib– Combined assets: R390bn

Note: Bank assets in brackets

Ranking the Big 4

1243Total bank assets *

3412Deposits **

3124Instalment credit **

3412Mortgage lending **

3421Other private sector loans **

1243Market capitalisation

3412SA-based 3rd party lending **

3421SA-based loans & advances **

Standard FirstRandBank

AbsaNedcorMeasure

* Source: Last annual/interim report

** Source: March DI 900 returns

Nedcor’s position

Structure

Capital One

JD Group

Old Mutual Group Schemes

R299m R72m

74.5%

DIVISIONS

R2 114m

100%/50%

70% 50.1%

R56mR206m

Stenham Gestinor & Chiswell

R354m

Amex/

Capital One

Contributions to F2002 core earnings shown above

BoE contributed R265m in its standalone form

The Big 4: Retail vs Corporate Banking

53475545Big 4 (weighted)

35064367525Standard Bank

11081197723Nedcor

11433674555FirstRand

55032682278Absa

RmCorporate (%)

Retail(%)

Corporate (%)

Retail(%)

Banc-assurance

contribution

Total bank earningsTotal bank assets

Source: JP Morgan

Annual / Interim Reports

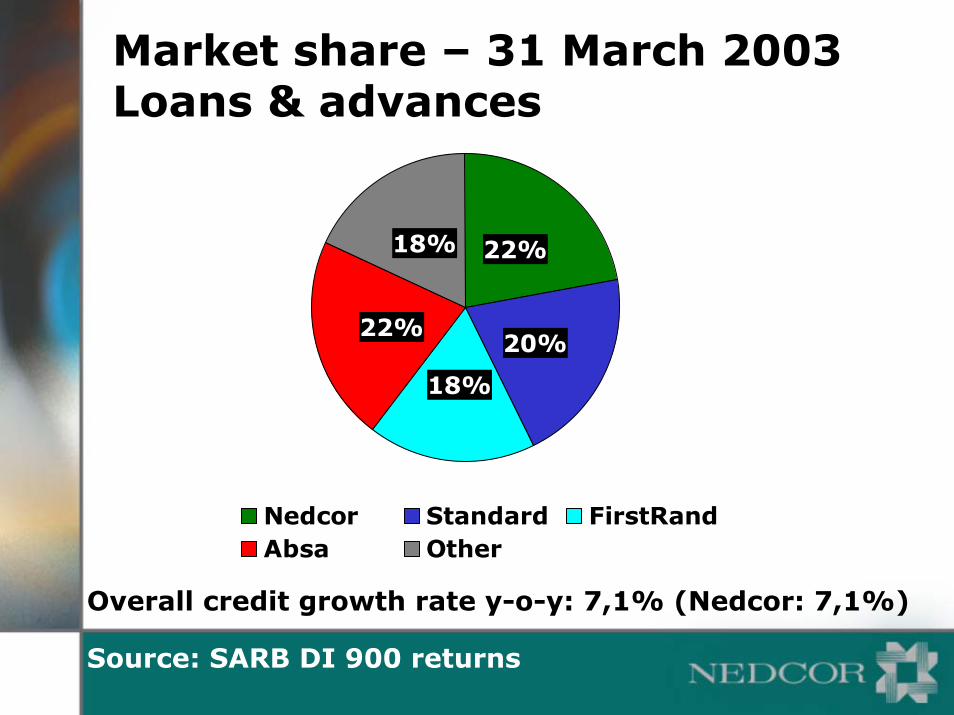

Market share – 31 March 2003Loans & advances

22%

20%

18%

22%

18%

Nedcor Standard FirstRandAbsa Other

Overall credit growth rate y-o-y: 7,1% (Nedcor: 7,1%)

Source: SARB DI 900 returns

Market share – 31 March 2003

12%

15%

18%

21%

24%

27%

30%

Jun-9

7Dec

-97

Jun-9

8Dec

-98

Jun-9

9Dec

-99

Jun-0

0Dec

-00

Jun-0

1Dec

-01

Jun-0

2Dec

-02

ABSA Firstrand Nedcor Standard

Mortgages

Growth rate: 11,4% y-o-y (Nedcor 11,0%)

Source: SARB DI 900 returns

14%

18%

22%

26%

30%

Jun-9

7Dec

-97

Jun-9

8Dec

-98

Jun-9

9Dec

-99

Jun-0

0Dec

-00

Jun-0

1Dec

-01

Jun-0

2Dec

-02

ABSA Firstrand Nedcor Standard

Market share – 31 March 2003

Loans to non-banks

Growth rate: 6,9% y-o-y (Nedcor 11,5%)

Source: SARB DI 900 returns

Market share – 31 March 2003

9%

12%

15%

18%

21%

24%

27%

30%

Jun-9

7O

ct-9

7Fe

b-98

Jun-9

8O

ct-9

8Fe

b-99

Jun-9

9O

ct-9

9Fe

b-00

Jun-0

0O

ct-0

0Fe

b-01

Jun-0

1O

ct-0

1Fe

b-02

Jun-0

2O

ct-0

2Fe

b-03

ABSA Firstrand Nedcor Standard

Instalment credit

Growth rate: 13,3% y-o-y (Nedcor 16,2%)

Source: SARB DI 900 returns

Market share – 31 March 2003

13%

16%

19%

22%

25%

28%

Jun-9

7O

ct-9

7Fe

b-98

Jun-9

8O

ct-9

8Fe

b-99

Jun-9

9O

ct-9

9Fe

b-00

Jun-0

0O

ct-0

0Fe

b-01

Jun-0

1O

ct-0

1Fe

b-02

Jun-0

2O

ct-0

2Fe

b-03

ABSA Firstrand Nedcor Standard

Deposits

Growth rate: 1,9% y-o-y (Nedcor –0,9%)

Source: SARB DI 900 returns

Net interest margin

Rbn %

50

70

90

110

130

150

170

190

210

1997 1998 1999 2000 2001 20022

2.5

3

3.5

4

4.5

AdvancesMargin

Growth rate: 103% y-o-y (Nedcor 217%)

Summary

• Volumes and market share achieved in all areas except retail

• Opportunities in retail and bancassurance to take market share to 23%

• Opportunities in margin normalisation• Focus on holding/gaining market share

while realising merger synergies

Strategic framework / SWOT

Strategy

SA Banking

Corporates

Individuals Treasury

Businesses

WealthManagement International

Peoples Bank

Bancassurance

AlliancesT&O platform Outsourcing

Strategic scorecard

AcquisitionsBoE (primarily Commercial)Imperial (Retail & Commercial)Gerrard Private Bank (Retail WM)FBC Fidelity (Retail)ENF (Corporate & Commercial)Didata (IT)AlliancesOld Mutual Bank/Bancassurance (Retail)Pick ’n Pay Go Banking (Retail)JD/Capital One microlending market(Peoples)Amex/Capital One (Retail)Outsourcing (IT)

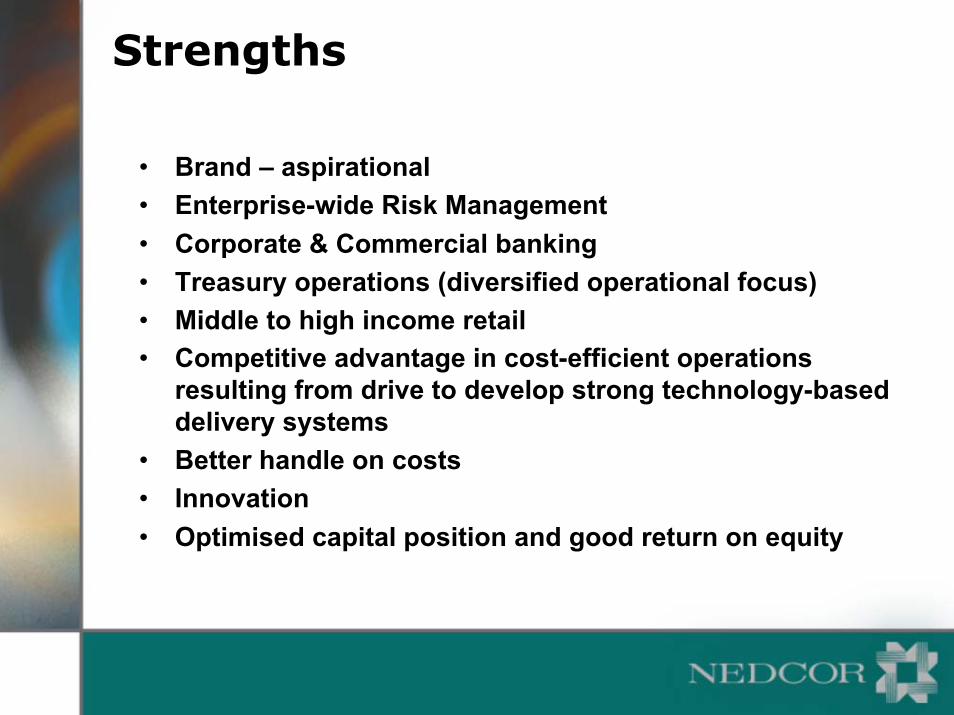

Strengths

• Brand – aspirational• Enterprise-wide Risk Management• Corporate & Commercial banking• Treasury operations (diversified operational focus)• Middle to high income retail• Competitive advantage in cost-efficient operations

resulting from drive to develop strong technology-based delivery systems

• Better handle on costs• Innovation• Optimised capital position and good return on equity

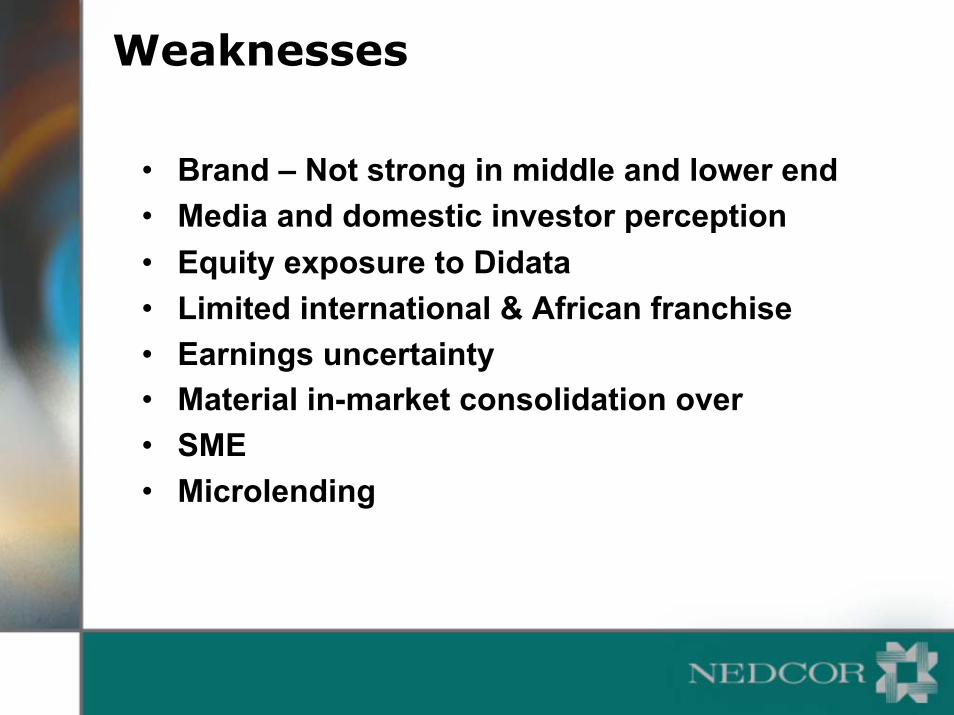

Weaknesses

• Brand – Not strong in middle and lower end• Media and domestic investor perception• Equity exposure to Didata• Limited international & African franchise• Earnings uncertainty• Material in-market consolidation over• SME• Microlending

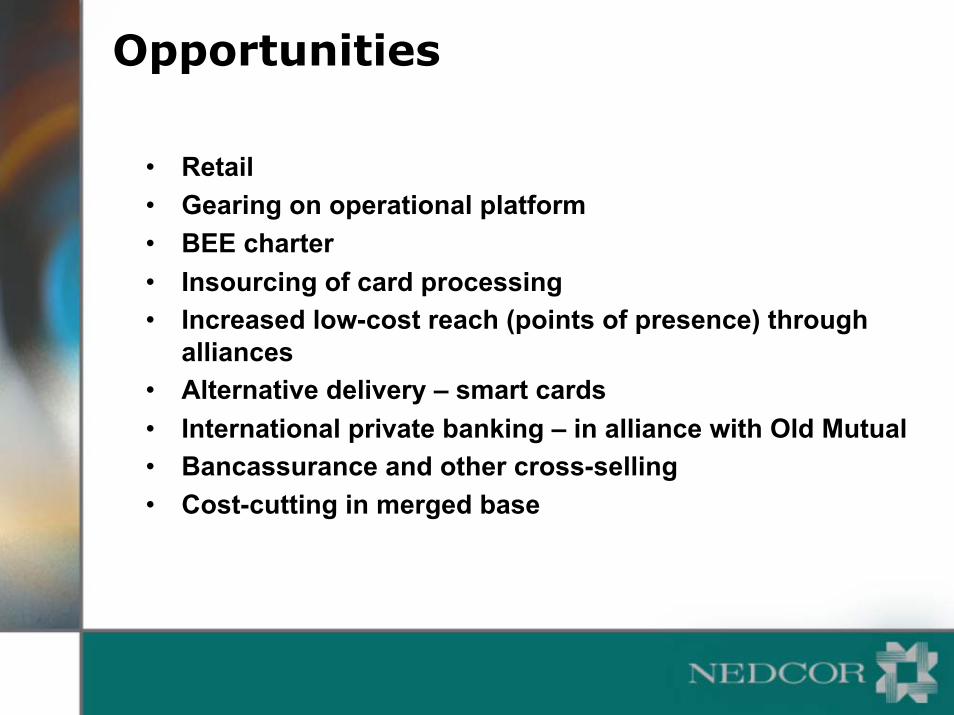

Opportunities

• Retail• Gearing on operational platform• BEE charter• Insourcing of card processing• Increased low-cost reach (points of presence) through

alliances• Alternative delivery – smart cards• International private banking – in alliance with Old Mutual• Bancassurance and other cross-selling• Cost-cutting in merged base

Threats

• Foreign entrants• Prescribed lending and regulatory issues

– Community Reinvestment Act– BEE

• AIDS• Managing alliances without complete control• Internationalisation of information technology

processing is an unproven strategy• Mortgage originators and integrators

Summary

• Middle and underserved market segments require further focus

• Limit international expansion, but focus on wealth management, Asian trade finance and insourcing

• Extraneous factors, regulatory and accounting issues to be managed

Key drivers / issues

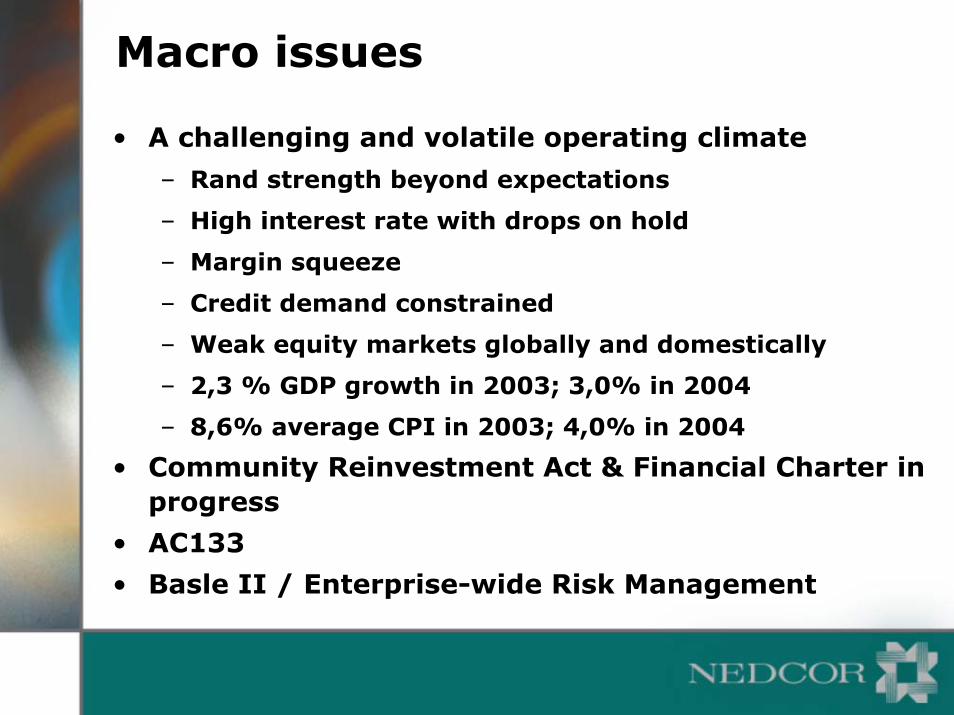

Macro issues

• A challenging and volatile operating climate

– Rand strength beyond expectations

– High interest rate with drops on hold

– Margin squeeze

– Credit demand constrained

– Weak equity markets globally and domestically

– 2,3 % GDP growth in 2003; 3,0% in 2004

– 8,6% average CPI in 2003; 4,0% in 2004

• Community Reinvestment Act & Financial Charter in progress

• AC133

• Basle II / Enterprise-wide Risk Management

Nedcor’s experience

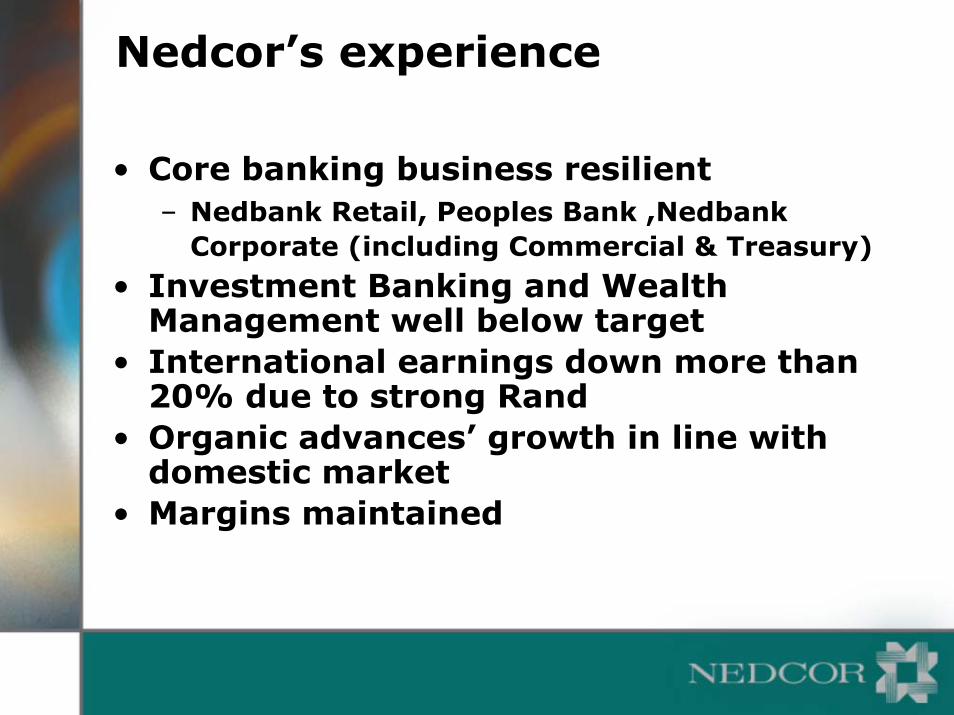

• Core banking business resilient– Nedbank Retail, Peoples Bank ,Nedbank

Corporate (including Commercial & Treasury)

• Investment Banking and Wealth Management well below target

• International earnings down more than 20% due to strong Rand

• Organic advances’ growth in line with domestic market

• Margins maintained

Nedcor’s experience (cont.)

• Non-interest revenue well below expectations– Private equity, investment banking assets,

advisory fees and trading profits– One-off items in NIB in F2002

• Credit quality satisfactory and provisions stable

• Expense growth in line with expectations– Additional expense reduction drive due to

subdued income• Taxation increased significantly

Nedcor’s experience (cont.)

• Translation losses• AC133 impact not accounted for• Capital adequacy expected to remain

sound• Group integration on track

– Synergy estimates unchanged from R110m in F2003 growing to R905m in F2006

Capital adequacy

2002 2001Rbn %* Rbn %*

– Ordinary capital& reserves 12,5 6,0 14,1 8,6

– Preference capital 2,0 1,0 – –Tier 1 14,5 7,0 14,1 8,6– Callable notes 6,0 2,6 2,0 1,2– Other 2,5 1,4 2,6 1,6Tier 2 8,5 4,0 4,6 2,8Total 23,0 11,0 18,7 11,4*Percentage of risk-weighted assets

AC 133 (IAS 39) – recognition and measurement of financial instruments

• Deviation from standard IAS approach• Applicable on year-ends commencing 1

July 2002 (IAS only in 2005)– Complex, rule-based– Components approach– Form over substance– Inconsistent measurement bases– Increased use of fair value– Geared to sophisticated financial

environment and data

Core earnings to headline earnings

Dec Dec% 2002 2001

change Rm Rm

Core earnings 9 3 366 3 093

Translation gains/(losses) (1 011 1 096

General risk provision 400 (400Merger costs (170 –

Headline earnings -32 2 585 3 789

Headline eps -35 1 022 1 574

)

))

Translation gains / losses

31 Dec 2002Offshore capital of USD 200m = R1 720m(Closing exchange rate = 8.60)

31 Dec 2003Offshore capital of USD 200m = R1 600m(Closing exchange rate = 8.00)

If an “integrated operation” as defined:Translation loss recognised inincome statement = R 120m

The Financial Services Charter

• Ownership– Peoples Bank = 30%– Quaystone Asset Management = 50%– Nedcor = 17% +

• Banking services to PDIs– Peoples Bank– JD– Aplitec– Pick ‘n Pay Go Banking

The Financial Services Charter(continued)

• Employment Equity– AIC = 49% of total staff– 20% of management– Females = 63% of total staff– Female = 35% of management

• Empowerment alliances• Empowerment financing

– Southern Sun/Tsogo Sun

– African Legend/Caltex

– Harmony/Armgold

– Shell/Thebe

– Total/Tosaco

– MTN

The Financial Services Charter(continued)

• Procurement• Awards

–2001• Enterprise Development Forum (EDF), Black

Business Executive Circle and Black Business Council - Empowerment Company of the Year

• Business Map - Empowerment Deal of the Year

–2002• Black Management Forum - Most Progressive

Company of the Year• Black Business Quarterly - Financier of the Year

Award

Summary

• Environment remains challenging requiring additonal focus on cost optimisation

• Accounting issues leading to volatility in earnings but aimed at fair value balance sheet representation

• Well positioned as regards Financial Services Charter

Bancassurance

Gerrard Private Bank

• 25,5 % interest held by Old Mutual• Fairbairn Trust business incorporated• A range of banking, treasury, trust and

discretionary asset management products• Target market: clients with investable

assets of at least £50 000• Based in Isle of Man and Jersey, with Rep

offices in SA and Honk Kong• 2002 Awards:

– Best offshore banking group– Best offshore product range

Nedcor Wealth Management

Jointly-owned Businesses with Old Mutual

Private Clients

(South Africa)

Wholly-owned Businesses

International Companies

(On and Offshore)

Credit Protection

(South Africa)

Retail Investment Products & Services

• Scope of offering to High Net Worth Individuals:– Discretionary Portfolio Management– Private Banking– Other Investment Products– Fiduciary Services:Trusts, Wills,

Estates

Complete offeringboth onshore & offshore

No. of staff 554/Clients 17500/AUM R23bn

Nedcor Wealth Management

Jointly-owned Businesses with Old Mutual

Private Clients

(South Africa)

Wholly-owned Businesses

International Companies

(On and Offshore)

Credit Protection

(South Africa)

Retail Investment Products & Services

• Scope of providing banking customers with credit protection– Nedbank customers– JV and Alliances – Other banks customers

No. of staff 105 / Premium income R491m / EV R44m

Nedbank

• 150 Personal Financial Planners• Branch-based insurance specialists• 50% of overall insurance product sold is

sourced from Old Mutual• F2002 contribution of R110m provides

vast scope for growth

Peoples Bank

• Old Mutual Group Schemes (“OMGS”)• Public and private sector entities targeted• Pre-packaged insurance product provided

by OMGS– 16 000 assurance policies sold in F2002– 68 000 credit life policies sold in F2002– 80 advisers

• Banking product provided by Peoples Bank– 12 000 new accounts in F2002– 41 dedicated OMGS staff

• Joint client education undertaken

Old Mutual Bank

• Division of Nedbank Ltd – 50/50 JV

• Leverage dominant Old Mutual brand

• Banking products, systems and processes supplied by Nedcor

• Sales, marketing and channel management supplied by Old Mutual

• 2 million OMPF customers

• 300 000 ex-Permanent Bank customers

• Huge intermediary network

• Established branch distribution network

• No need to use expensive originators for mortgages

Summary

• Focus on greater share of customer wallet for Old Mutual and Nedcor

• Numerous initiatives with Old Mutual aimed at premium generation and commission income

• Two-way focus on cross-selling both insurance and bank products

• Opportunities for rationalisation of product factories and leverage of distribution channels

Conclusion

Key targets

• RoE 25% (21,9%)• RoA 2% (1,6%)• Cost-to-income ratio < 50% (55,4%)• Non-interest revenue : net interest income

> 50% (52,4%)• Provisions : average advances < 0,7%

(1%)• Capital adequacy 12% (11%)

RoE and RoA must be viewed in the light of the inflation level

Conclusion

• Challenging environment• Maintain/grow market share while

completing merger• Opportunity in retail, bancassurance and

cost reductions• Limited conventional offshore aspirations• Low-cost expanded reach