Embed Size (px)

Citation preview

Oil & Tanker Trades OutlookVolume 22, No. 12 ISSN: 1363-9617

Tanker Supply and Demand (2017f)Crude Tanker Dwt Demand Growth 5.1% Crude Tanker Fleet Growth 5.7%

Product Tanker Dwt Demand Growth 3.6% Product Tanker Fleet Growth 4.3%

1

Tanker Market Indicators (Nov-17)VLCC Newbuild Price VLCC Average 1 year TC

MR Newbuild Price MR Average 1 year TC

$81.0m

December-2017

Average Tanker Earnings Index

$27,750/day

$13,750/day$33.5m

CONTENTS

Industry News p2

Market Outlook p3

VLCC Market p4-5

Suezmax Market p6-7

Aframax Market p8-9

Product Tanker Market p10-11

Timecharter Market p12

Tanker Fleet & Orderbook pi-xii

Sale & Purchase Market p13

Crude Oil Transport Costs p14

Economic & Financial Indicators p15

Global Oil Supply p16

Global Oil Demand p17

Seaborne Crude Imports p18

Seaborne Crude Exports p19

Seaborne Products Imports p20

Seaborne Products Exports p21

Refinery Capacity p22

Tanker Safety & Oil Spills p23

Tanker Outlook p24

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Nov

11

Nov

12

Nov

13

Nov

14

Nov

15

Nov

16

Nov

17

$/day

Rio De Janeiro

New York

Novorossiysk

Singapore

Fujairah

Philadelphia

Seria

Los Angeles

Mongstad

Fos

Primorsk

Rotterdam

Skikda

Jakarta

Augusta Agioi Theodoroi

Ras TanuraJamnagar

Lome

Sidi Kerir

Bonny Offshore

Ain SukhnaYanbu

Selection of major tanker ports

Sullom Voe

Houston

LOOP

St Eustatius

Quintero

Bonaire

Trieste

Curacao

Puerto La Cruz

San Lorenzo

Cap Limbe

Antwerp

Jeddah

Mina Al Ahmadi

Bombay

Dar Es Salaam

New York

Huizhou

Singapore

Fujairah

Philadelphia

Seria

Los AngelesChiba

Sydney

Jakarta

NingboJamnagar Kaohsiung

Kozmino

Houston

LOOP

St Eustatius

Quintero

Bonaire

Ulsan

Selection of major tanker ports

Curacao

Puerto La Cruz

San Lorenzo

Bombay

Rio De Janeiro

Clarksons Research is respected worldwide as the most authoritative provider of intelligence for the global shipping industry. Clarksons Research is part of the Clarksons group, the world’s largest provider of shipbroking and integrated shipping services. For more detail about the Clarksons group visit www.clarksons.com.

The leading online ship tracking systemTo find out more about the power of SeaNet, arrange a free trial or to subscribe, please visit www.clarksons.net/seanet

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Industry News

Nov-16 Nov-17Brent Blend 44.1 62.5

Short-Term 2017 2018EIA Short Term 53.9 57.3

Average F'cast* 53.6 56.9

Long-Term #IEA Current Pol. 136 2040IEA New Pol. 111 2040IEA Sus. Dev. 64 2040EIA Base Case 109 2040

Clarksons Research Page 2 Dec-17

Oil Price Trends & ForecastAverage Price, $/bbl

# IEA: November 2017, EIA: January 2017

* Average level of forecasts reported in Nov 2017.

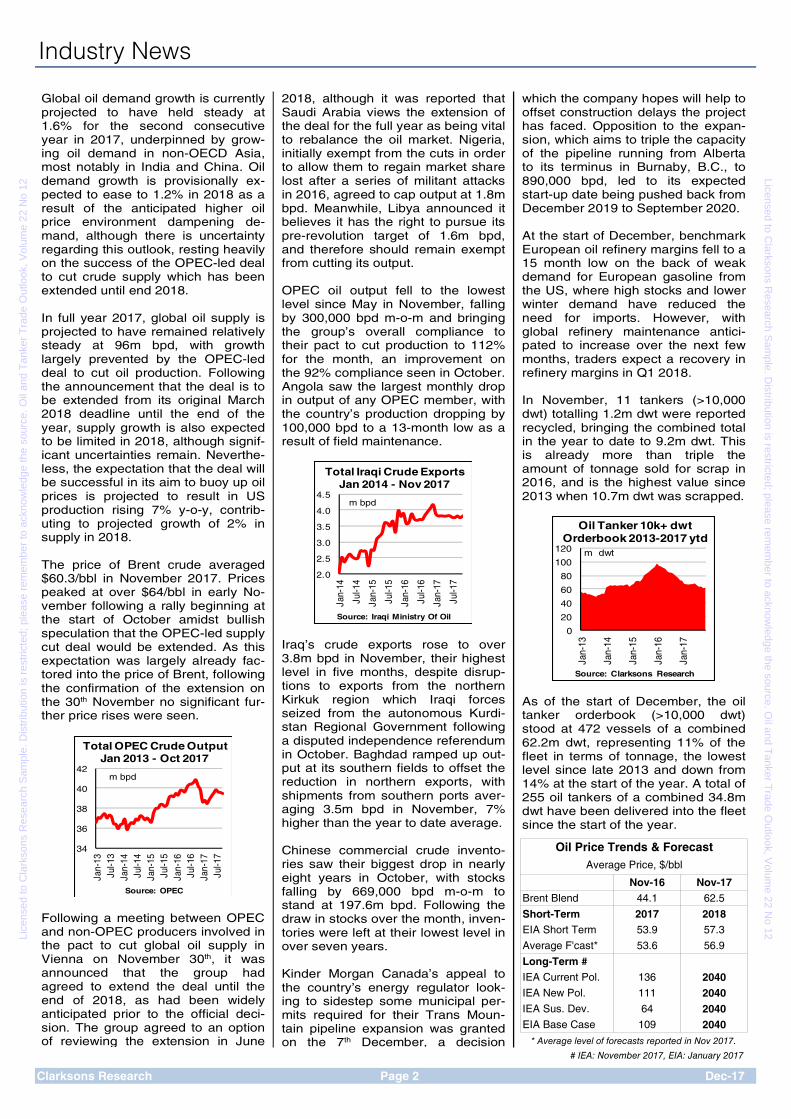

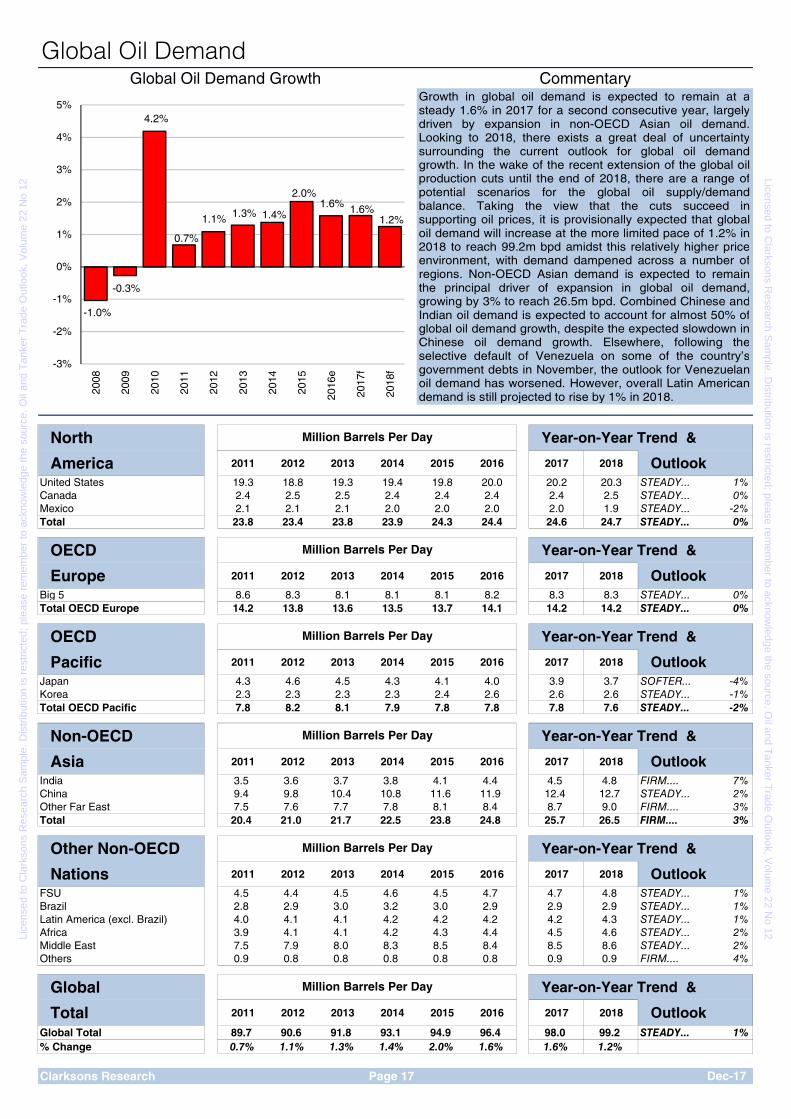

Global oil demand growth is currently projected to have held steady at 1.6% for the second consecutive year in 2017, underpinned by grow-ing oil demand in non-OECD Asia, most notably in India and China. Oil demand growth is provisionally ex-pected to ease to 1.2% in 2018 as a result of the anticipated higher oil price environment dampening de-mand, although there is uncertainty regarding this outlook, resting heavily on the success of the OPEC-led deal to cut crude supply which has been extended until end 2018. In full year 2017, global oil supply is projected to have remained relatively steady at 96m bpd, with growth largely prevented by the OPEC-led deal to cut oil production. Following the announcement that the deal is to be extended from its original March 2018 deadline until the end of the year, supply growth is also expected to be limited in 2018, although signif-icant uncertainties remain. Neverthe-less, the expectation that the deal will be successful in its aim to buoy up oil prices is projected to result in US production rising 7% y-o-y, contrib-uting to projected growth of 2% in supply in 2018. The price of Brent crude averaged $60.3/bbl in November 2017. Prices peaked at over $64/bbl in early No-vember following a rally beginning at the start of October amidst bullish speculation that the OPEC-led supply cut deal would be extended. As this expectation was largely already fac-tored into the price of Brent, following the confirmation of the extension on the 30th November no significant fur-ther price rises were seen.

34

36

38

40

42

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

Jan-

17Ju

l-17

Source: OPEC

m bpd

Total OPEC Crude OutputJan 2013 - Oct 2017

Following a meeting between OPEC and non-OPEC producers involved in the pact to cut global oil supply in Vienna on November 30th, it was announced that the group had agreed to extend the deal until the end of 2018, as had been widely anticipated prior to the official deci-sion. The group agreed to an option of reviewing the extension in June

2018, although it was reported that Saudi Arabia views the extension of the deal for the full year as being vital to rebalance the oil market. Nigeria, initially exempt from the cuts in order to allow them to regain market share lost after a series of militant attacks in 2016, agreed to cap output at 1.8m bpd. Meanwhile, Libya announced it believes it has the right to pursue its pre-revolution target of 1.6m bpd, and therefore should remain exempt from cutting its output. OPEC oil output fell to the lowest level since May in November, falling by 300,000 bpd m-o-m and bringing the group’s overall compliance to their pact to cut production to 112% for the month, an improvement on the 92% compliance seen in October. Angola saw the largest monthly drop in output of any OPEC member, with the country’s production dropping by 100,000 bpd to a 13-month low as a result of field maintenance.

2.0

2.5

3.0

3.5

4.0

4.5

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Jul-1

7

Source: Iraqi Ministry Of Oil

m bpd

Total Iraqi Crude ExportsJan 2014 - Nov 2017

Iraq’s crude exports rose to over 3.8m bpd in November, their highest level in five months, despite disrup-tions to exports from the northern Kirkuk region which Iraqi forces seized from the autonomous Kurdi-stan Regional Government following a disputed independence referendum in October. Baghdad ramped up out-put at its southern fields to offset the reduction in northern exports, with shipments from southern ports aver-aging 3.5m bpd in November, 7% higher than the year to date average. Chinese commercial crude invento-ries saw their biggest drop in nearly eight years in October, with stocks falling by 669,000 bpd m-o-m to stand at 197.6m bpd. Following the draw in stocks over the month, inven-tories were left at their lowest level in over seven years. Kinder Morgan Canada’s appeal to the country’s energy regulator look-ing to sidestep some municipal per-mits required for their Trans Moun-tain pipeline expansion was granted on the 7th December, a decision

which the company hopes will help to offset construction delays the project has faced. Opposition to the expan-sion, which aims to triple the capacity of the pipeline running from Alberta to its terminus in Burnaby, B.C., to 890,000 bpd, led to its expected start-up date being pushed back from December 2019 to September 2020. At the start of December, benchmark European oil refinery margins fell to a 15 month low on the back of weak demand for European gasoline from the US, where high stocks and lower winter demand have reduced the need for imports. However, with global refinery maintenance antici-pated to increase over the next few months, traders expect a recovery in refinery margins in Q1 2018. In November, 11 tankers (>10,000 dwt) totalling 1.2m dwt were reported recycled, bringing the combined total in the year to date to 9.2m dwt. This is already more than triple the amount of tonnage sold for scrap in 2016, and is the highest value since 2013 when 10.7m dwt was scrapped.

0

20

40

60

80

100

120

Jan-

13

Jan-

14

Jan-

15

Jan-

16

Jan-

17Source: Clarksons Research

m dwt

Oil Tanker 10k+ dwt Orderbook 2013-2017 ytd

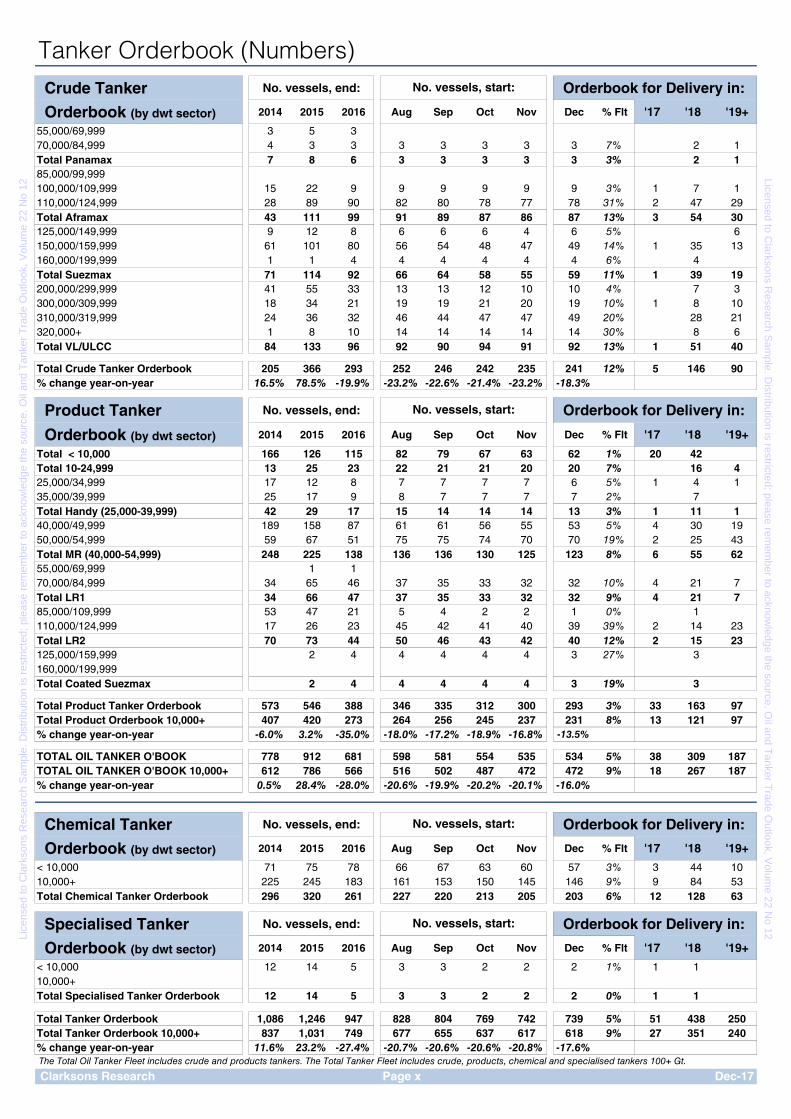

As of the start of December, the oil tanker orderbook (>10,000 dwt) stood at 472 vessels of a combined 62.2m dwt, representing 11% of the fleet in terms of tonnage, the lowest level since late 2013 and down from 14% at the start of the year. A total of 255 oil tankers of a combined 34.8m dwt have been delivered into the fleet since the start of the year.

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Market OutlookSupply-Demand Dynamics: Crude Tankers Supply-Demand Dynamics: Product Tankers

Crude Tanker Million Dwt Tanker Supply & Demand HighlightsDemand 2014 2015 2016 2017 2018

VLCC 163.1 166.4 176.2 185.0 194.8 FIRM.... 5.3%

Suezmax 52.6 54.6 56.8 60.7 63.7 FIRM.... 4.9%

Aframax 54.6 55.1 55.8 57.0 59.3 FIRM.... 3.9%

Panamax 3.5 3.4 3.1 3.1 3.1 STEADY... 0.0%

TOTAL 274.4 280.3 293.0 307.8 323.3 FIRM.... 5.0%% Change y-o-y -0.4% 2.2% 4.5% 5.1% 5.0%Demand derived from crude and DPP trade. Total includes Handysize dwt demand.

Product Tanker Million Dwt

Demand 2014 2015 2016 2017 2018

85-124,999 Dwt (LR2) 24.1 27.5 29.9 31.7 32.9 FIRM.... 3.7%

55-84,999 Dwt (LR1) 18.2 19.0 19.9 20.8 21.8 FIRM.... 4.6%

10-54,999 Dwt 69.5 73.9 75.6 77.5 80.1 FIRM.... 3.4%

TOTAL 111.8 120.3 125.4 130.0 134.7 FIRM.... 3.7%% Change y-o-y 1.5% 7.7% 4.2% 3.6% 3.7%Includes demand derived from DPP, CPP and veg oil trade.

Crude Fleet Million Dwt

Growth 2014 2015 2016 2017 2018

VLCC 189.8 192.8 207.3 220.3 229.4 FIRM.... 4.1%

Suezmax 69.2 70.6 74.1 80.4 83.8 FIRM.... 4.2%

Aframax 65.5 65.2 66.6 67.5 69.8 FIRM.... 3.5%

Panamax 6.0 5.5 5.6 5.5 5.3 SOFTER -5.2%

TOTAL 330.5 334.1 353.7 373.7 388.3 FIRM.... 3.9%% Change y-o-y 0.7% 1.1% 5.8% 5.7% 3.9%

Product Fleet Million Dwt

Growth 2014 2015 2016 2017 2018

85-124,999 Dwt (LR2) 28.1 31.0 34.4 37.4 38.1 STEADY... 2.0%

55-84,999 Dwt (LR1) 24.2 24.3 25.5 26.7 27.8 FIRM.... 4.4%

10-54,999 Dwt 81.2 86.1 90.3 92.6 94.1 STEADY... 1.6%

TOTAL 133.6 141.3 150.2 156.7 160.1 STEADY... 2.2%% Change y-o-y 3.9% 5.8% 6.3% 4.3% 2.2%

Tanker Million Dwt

Balance 2014 2015 2016 2017 2018

Total Demand 0% 4% 4% 5% 5%Total Supply 2% 2% 6% 5% 3%Note: Demand basis full year, fleet development basis end year. Product fleet definition as detailed on page 23.

Clarksons Research Page 3 Dec-17

Year-on-Year% Change

Supply/Demand

OutlookSTEADY...STEADY...

Year-on-Year% Change

Year-on-Year% Change

Year-on-Year% Change

• Despite firm tanker demand growth in the year to date, market conditions have worsened notably so far in 2017 due to rapid fleet expansion, with earnings falling y-o-y across all tanker sectors. VLCC spot earnings averaged $18,957/day in the first eleven months of the year, down 54% compared to full year 2016. Whilst a sea-sonal improvement in tanker market condi-tions is often seen in Q4, a significant pick-up in tanker earnings in the final quarter of 2017 does not appear to have material-ised, with VLCC spot earnings falling back below $10,000/day in early December. • In full year 2017, crude tanker dwt de-mand is expected to have risen by a firm 5.1%, largely supported by increased long-haul crude trade between the Atlantic Ba-sin and Asia. With OPEC’s decision in No-vember to extend their supply cut deal until end 2018, growing crude trade on long haul routes, particularly from the US, is expected to continue to support firm crude tanker dwt demand growth of 5% in 2018. • The crude tanker fleet is projected to have grown by 5.7% in full year 2017, weighing heavily on the market despite healthy demand growth. Fleet expansion is expected to slow to 3.9% in 2018, which has the potential to support a gradual im-provement in the market balance. • Product tanker dwt demand is currently expected to have expanded by 3.6% in full year 2017, supported by growing intra-Asian products trade and US products ex-ports. These factors are expected to con-tinue to drive products trade growth in 2018, with product tanker dwt demand ex-pected to grow by 3.7%. • The product tanker fleet is currently ex-pected to have expanded by a firm 4.3% in full year 2017, exerting further supply-side pressure. Fleet growth is expected to ease to 2.2% in 2018, which could start to help rebalance fundamentals.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2008

2009

2010

2011

2012

2013

2014

2015

2016

e

2017

f

2018

f

Demand Growth

Supply Growth

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2008

2009

2010

2011

2012

2013

2014

2015

2016

e

2017

f

2018

f

Demand Growth

Supply Growth

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

VLCC Market TrendsVLCC Market Long-Term VLCC Trends

VLCC Spot VLCC Market

Rates 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

280K Gulf - Europe 38 37 32 29 27 25 24 31 29 -6%270K Gulf - India 84 72 70 62 63 54 53 78 79 2%265K Gulf - S.Korea 61 57 56 49 49 39 42 64 64 -1%265K Gulf - Japan 63 59 59 51 52 42 44 67 67 -1%270K Gulf - Singapore 65 61 60 52 53 43 45 70 69 -1%280K Gulf - US Gulf 37 35 30 27 25 23 22 29 26 -9%260K WAF - India^ 5.11 3.76 2.87 2.62 2.68 2.25 2.37 3.20 3.06 -4%260K WAF - US Gulf 72 69 67 60 60 56 59 69 59 -14%260K WAF - East 64 62 62 56 55 50 52 67 70 4%275K Caribs - Singapore^ 6.85 4.73 4.00 3.37 3.16 3.20 3.66 4.15 4.45 7%^ Lump sum in million dollars

VLCC VLCC Market

Earnings* 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

Average Spot Earnings 64,846 41,488 18,957 15,330 13,909 8,741 8,120 21,430 18,686 -13%Spot Earnings Index 166 106 49 39 36 22 21 55 48 -13%1 Year T/C Rate (Modern)" 48,433 36,585 27,283 26,700 26,500 26,750 26,500 26,688 27,750 4%3 Year T/C Rate (Modern)" 42,707 33,019 28,753 29,275 29,500 29,500 29,500 29,313 29,250 0%

VLCC Spot VLCC Spot Demand

Demand** 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

MEG - China, Korea, Japan 53 52 47 53 43 38 53 62 34 -45%

MEG - Other Asia Pacific 25 23 21 24 27 15 20 21 15 -29%

MEG - India 12 14 19 17 24 25 25 14 25 79%

MEG - N. America 15 16 11 10 7 9 4 12 13 8%

Caribs - East/India 19 20 21 27 17 19 19 28 13 -54%

WAF - East 18 20 25 30 24 25 23 22 26 18%

WAF - India 9 7 6 7 6 4 7 7 4 -43%

UKC - East 3 7 7 8 6 4 5 5 6 20%

Others 16 16 18 12 17 14 17 24 18 -25%

Total Nos. 169 175 175 188 171 153 173 195 154 -21%

Total m. dwt 50.3 50.8 50.1 52.5 49.3 44.6 50.7 54.0 44.0

Clarksons Research Page 4

Average WS Average WS

SOFTER...STEADY...STEADY...

SOFTER...WEAKER...STEADY...STEADY...

WEAKER...FIRM....FIRM....

Average $/day Average $/day

WEAKER...WEAKER...FIRM....STEADY...

No of Fixtures, Avg. No of Fixtures

WEAKER!!...

FIRMER...

FIRMER...

WEAKER!!...

WEAKER!!...

WEAKER!!...

FIRMER...

^ Year to date. * Average Earnings are calculated as described in 'SIW Sources and Methods', which can be found on SIN. ** Spot demand is the average number of reported fixtures per month. "Timecharter rates represent owners' rates prior to start 2016.

Dec-17

FIRMER...

WEAKER...

WEAKER...

0

40

80

120

160

200

240

280

0

20

40

60

80

100

120

140

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep

-17

Nov

-17

US$,000/day

No. of Spot Fixtures (RHS)

VLCC Average Spot Earnings (LHS)

0

20

40

60

80

100

120

140

160

180

200

0

10

20

30

40

50

60

70

80

90

100

Nov

-07

Nov

-08

Nov

-09

Nov

-10

Nov

-11

Nov

-12

Nov

-13

Nov

-14

Nov

-15

Nov

-16

Nov

-17

US$,000/day

VLCC 1 Yr Timecharter Rate

(LHS)

N/B VLCC Price (RHS)

US$ m

5 Yr Old VLCC Price (RHS)

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

VLCC Market Trends

VLCC

Balance 2014 2015 2016 2017 2018 %

DemandMEG-China, Japan, Korea 7.8 8.1 8.6 8.5 8.7 3%MEG-Other Asia/Pacific" 3.3 3.5 3.8 3.6 3.8 4%MEG-N.America 1.9 1.6 1.8 1.8 1.9 3%Caribs-China/India 1.3 1.4 1.6 1.7 1.8 7%WAF-Far East 1.2 1.2 1.3 1.5 1.7 10%WAF-India 0.4 0.5 0.5 0.4 0.4 4%Other 1.2 1.6 1.6 1.9 2.0 7%

Total, m bpd # 17.1 18.0 19.0 19.4 20.3 4%Total, m dwt ~ # 163.1 166.4 176.2 185.0 194.8 5%% growth 0.9% 2.0% 5.9% 5.0% 5.3%~Derived from crude trade above and DPP trade. "South East Asia + India.

Supply*200,000-299,999 dwt # 61.6 62.2 69.4 0.0300,000-319,999 dwt # 117.7 122.7 130.2 0.0320,000 dwt & above # 14.7 15.0 15.0 0.0

Total # 193.9 199.9 214.7 226.0 235.1 4%Combos in Oil # 1.6 1.0 0.3 0.0 0.0 #DIV/0!Laid-up # 1.5 0.6 0.3 0.3 0.3 0%Long-term Storage # 4.2 7.5 7.3 5.4 5.4 0%Active Fleet # 189.8 192.8 207.3 220.3 229.4 4%% growth 2.2% 1.6% 7.5% 6.3% 4.1%

BalanceDemand Growth 1% 2% 6% 5% 5%

Supply Growth 2% 2% 8% 6% 4%

Balance -1% 0% -2% -1% 1%"Laid-up" includes vessels reported and confirmed to be in lay-up, remaining out of service for an extended period.

VLCC S&P 3 Month

Market # 2014 2015 2016 2017^ Jun Jul Sep Oct Nov

Newbuild Prices320k newbuild ($m) # 97.0 93.5 84.5 81.0 81.0 81.0 81.0 81.0 81.0 SAME... 0%

No. of Contracts Placed 32 69 14 45 1 4 9 0 4 FIRMER... 160%Est. Investment Value ($bn) 3.1 6.6 1.2 3.7 0.1 0.3 0.7 0.0 0.4 FIRMER... 173%

Secondhand Prices310k 5yo ($m) 77.0 80.0 60.0 63.0 65.0 64.0 61.0 63.0 63.0 WEAK... -3%

300k 10yo ($m) 52.0 55.0 40.0 38.0 41.0 40.0 37.0 38.0 38.0 WEAKER... -6%

265k 15yo ($m) 29.0 38.0 24.0 22.0 22.5 22.5 21.0 22.0 22.0 WEAK... -2%

No. of Sales 80 38 22 41 2 2 1 2 4 FIRMER... 40%5 Year Old/NB Price Ratio 79% 86% 71% 78% 80% 79% 75% 78% 78% WEAK... -3%

Demolition$/ldt 450 290 300 415 360 365 410 380 415 FIRMER... 7%

VLCC Scrap Value ($m) 19.1 12.2 12.6 17.4 15.1 15.3 17.1 15.9 17.4 FIRMER... 7%

No. Scrapped 8 2 2 11 0 2 3 0 1 WEAKER!!... -33%

Fleet

Profile 2014 2015 2016 2017^ Jun Jul Sep Oct Nov 2017 2018

Fleet Total 193.9 199.9 214.7 226.0 223.5 224.7 224.8 225.7 226.0 226.0 235.1Deliveries 7.6 6.2 14.3 14.6 1.2 1.8 1.5 0.9 0.9 14.9 13.0Scrapping 2.4 0.5 0.6 3.3 0.0 0.6 0.9 0.0 0.3 3.6 3.9Contracting 9.8 21.2 4.4 14.1 0.3 1.3 2.7 0.0 1.3

Orderbook 25.7 40.7 29.5 28.7 29.5 28.6 29.2 28.3 28.7

Clarksons Research Page 5 Dec-17

*End of year figure. ^Year to date/latest price. Fleet totals in metric tonnes, net of est. conversions and misc. changes, accounting for historical and expected delivery performance.

M. Bpd / M. Dwt Forecast

Number & Value Number & Value

Aug Trend

81.0

00.0

63.0

39.0

21.5

178%

405

4

M. Dwt M. Dwt, month end

16.9

0.0

28.0

Forecast*Aug

224.1

0.6

1.2

• The VLCC market weakened in November after firming considerably in October, although earnings remained elevated relative to the period between May and September this year. Average VLCC spot earnings fell by 13% m-o-m to $18,686/day in November, bringing average spot earnings in the first eleven months of the year to $18,957/day. This value represents a 54% decline in average earnings relative to full year 2016. • In full year 2017, VLCC dwt demand is pro-jected to have grown by a robust 5.0%. De-spite an expected decline in crude trade on ex-MEG routes due to the OPEC-led supply cuts, increased long-haul crude trade between the Atlantic basin and China is expected to lend support to VLCC dwt demand growth. In 2018, VLCC dwt demand growth is projected to remain relatively firm at around 5.3%. In spite of the decision by OPEC to extend their supply cut deal until end 2018, crude trade on VLCCs in 2018 is expected to grow fairly firm-ly, with dwt demand expected to continue to be supported by rising US exports and in-creased VLCC loading capability at some US ports, alongside continued overall growth in long-haul trade between the Atlantic basin and Asia. • In full year 2017, a total of 14.9m dwt is expected to be delivered into the VLCC fleet, contributing to projected active fleet growth of 6.3%. Active VLCC fleet growth is expected to slow to 4.1% in 2018, slightly slower than pro-jected growth in VLCC demand.

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Suezmax Market TrendsSuezmax Market Long-Term Suezmax Trends

Suezmax Spot Suezmax Market

Rates 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

130K WAF - USAC 82 72 75 64 63 61 70 81 81 1%

130K WAF - Med 83 75 78 66 65 64 72 84 83 -2%

130K Med - Med 89 81 81 68 69 74 76 91 86 -5%

140K Black Sea - Med 90 84 86 73 73 76 83 96 91 -5%

130K Caribs - US Gulf 98 74 79 73 73 68 81 83 86 5%

130K Gulf - WC India 91 79 81 73 70 70 70 89 96 7%

130K Gulf - China 83 78 79 68 69 69 73 82 87 6%

130K Gulf - Med. 48 44 36 28 28 26 31 39 41 6%

Suezmax Suezmax Market

Earnings* 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

Average Spot Earnings 46,713 27,567 15,774 10,498 10,322 10,722 11,990 18,748 16,759 -11%

1 Year T/C Rate (Modern)" 35,875 27,302 18,628 18,000 18,000 18,000 18,000 17,813 17,750 0%

3 Year T/C Rate (Modern)" 33,038 26,285 22,526 22,500 22,500 22,500 22,500 22,500 22,500 0%

Suezmax Spot Suezmax Spot Demand

Demand** 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

WAF - Med/UKC 45 29 28 36 24 25 33 24 22 -8%WAF - N. America 7 13 13 18 14 12 18 14 16 14%WAF - East 5 7 9 11 13 9 7 10 14 40%WAF - India 5 5 4 6 7 1 4 3 0 -100%MEG - Med 28 22 23 27 36 27 36 35 33 -6%

MEG - India 11 24 33 23 24 20 31 21 26 24%

MEG - East 5 8 11 12 18 9 14 11 10 -9%

Med/Black Sea - Med 28 28 30 28 33 40 30 31 27 -13%

Caribs - N. America 14 9 11 20 12 13 21 7 16 129%

Caribs - Med 9 8 9 6 12 6 9 9 9 0%

Others 78 78 95 100 103 101 99 100 81 -19%

Total Nos. 236 230 265 287 296 263 302 265 254 -4%

Total m. dwt 35.2 33.5 39.1 41.6 44.1 39.1 41.7 40.5 36.9 -9%

Clarksons Research Page 6

Average WS Average WS

STEADY...

STEADY...

SOFTER...

SOFTER...

No of Fixtures, Avg. No of Fixtures

WEAKER...

FIRMER...

FIRM....

FIRM....

FIRM....

Average $/day Average $/day

WEAKER...

STEADY...

WEAKER...

SOFTER...

WEAKER...

STEADY...

STEADY...

FIRMER...

^ Year to date. * Average Earnings are calculated as described in 'SIW Sources and Methods', which can be found on SIN. ** Spot demand is the average number of reported fixtures per month. "Timecharter rates represent owners' rates prior to start 2016.

Dec-17

FIRM....

FIRMER...FIRMER...WEAKER!!SOFTER...

WEAKER...

WEAKER...

0

25

50

75

100

125

150

175

200

225

250

275

300

325

0

5

10

15

20

25

30

35

40

45

50

55

60

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep

-17

Nov

-17

No of Spot Fixtures (RHS)

Suezmax Average Spot Earnings (LHS)

US$,000/day

0

20

40

60

80

100

120

0

10

20

30

40

50

60

Nov

-07

Nov

-08

Nov

-09

Nov

-10

Nov

-11

Nov

-12

Nov

-13

Nov

-14

Nov

-15

Nov

-16

Nov

-17

US$,000/day

Suezmax 1 Yr Timecharter Rate

(LHS)

N/B Suezmax Price (RHS)

US$ m

5 Yr Old Suezmax Price (RHS)

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Suezmax Market Trends

Suezmax

Balance 2014 2015 2016 2017 2018 %

DemandWAF-N America 0.3 0.3 0.4 0.4 0.4 0%MEG-Med 1.0 1.1 1.4 1.4 1.5 4%Caribs-N America 0.7 0.8 0.7 0.7 0.7 1%WAF-Med/UKC 1.1 1.3 0.9 0.9 0.9 4%MEG-India 0.8 0.8 0.9 0.9 1.0 6%Med/UKC- N America 0.2 0.2 0.3 0.3 0.3 0%Med/Black Sea-UKC 0.3 0.3 0.2 0.3 0.3 -3%Med/Black Sea-Med 0.8 0.9 0.9 0.9 0.9 -2%Others 2.7 2.8 2.9 3.0 2.9 -3%

Total, m bpd # 7.7 8.3 8.6 8.8 8.9 1%Total, m dwt ~ # 52.6 54.6 56.8 60.7 63.7 5%% growth 1.2% 3.9% 4.1% 6.8% 4.9%~Derived from crude trade above and DPP trade.

Supply*125,000-159,999 dwt # 62.6 64.2 68.1 0.0160,000-199,999 dwt # 11.7 11.7 11.9 0.0

Total # 74.4 75.9 80.0 86.9 90.3 4%Combos in Oil # 0.4 0.2 0.1 0.1 0.1 0%Laid-up & Long-term Storage # 0.1 0.0 0.3 0.1 0.1 0%Shuttle # 5.4 5.5 5.7 6.5 6.5 14%Active Fleet # 69.2 70.6 74.1 80.4 83.8 4%% growth 0.7% 2.0% 5.0% 8.4% 4.2%Fleet includes coated Suezmax tankers.

BalanceDemand Growth 1% 4% 4% 7% 5%

Supply Growth 1% 2% 5% 8% 4%

Balance 1% 2% -1% -2% 1%"Laid-up" includes vessels reported and confirmed to be in lay-up, remaining out of service for an extended period.

Suezmax S&P 3 Month

Market # 2014 2015 2016 2017^ Jun Jul Sep Oct Nov

Newbuild Prices156-158K newbuild ($m) # 65.0 63.0 54.5 54.5 54.0 54.0 54.0 54.0 54.5 FIRM... 0%

No. of Contracts Placed 44 59 19 21 14 0 0 0 5 WEAKER!! -69%Est. Investment Value ($bn) 3.0 4.0 1.1 1.7 0.9 0.0 0.0 0.0 0.4 WEAKER!! -63%

Secondhand Prices160k 5yo ($m) 57.0 60.0 40.0 40.0 44.0 41.0 39.0 40.0 40.0 WEAK... -5%

150k 10yo ($m) 37.0 42.0 27.5 25.0 29.0 26.5 24.0 25.0 25.0 WEAKER... -8%

No. of Sales 35 39 17 25 4 1 0 2 4 SAME... 0%5 Year Old/NB Price Ratio 88% 95% 73% 73% 81% 76% 72% 74% 73% WEAKER... -5%

Demolition$/ldt 455 295 295 415 365 385 415 385 415 FIRM... 4%

Suezmax Scrap Value ($m) 10.0 6.5 6.7 9.5 8.2 8.3 9.4 8.7 9.5 FIRMER... 7%

No. Scrapped 7 0 1 11 1 2 1 0 2 WEAKER!! -50%

Fleet

Profile 2014 2015 2016 2017^ Jun Jul Sep Oct Nov 2017 2018

Fleet Total 74.4 75.9 80.0 87.0 85.1 85.5 86.5 87.0 87.0 86.9 90.3Deliveries 1.3 1.6 4.2 8.6 1.1 0.8 0.9 0.5 0.3 8.8 5.4Scrapping 1.1 0.0 0.1 1.7 0.1 0.3 0.1 0.0 0.3 1.9 2.1Contracting 6.9 9.3 3.0 3.1 2.1 0.0 0.0 0.0 0.7

Orderbook 11.1 18.2 15.1 9.6 11.7 11.0 9.7 9.2 9.6

Clarksons Research Page 7 Dec-17

2

415

*End of year figure. ^Year to date/latest price. Fleet totals in metric tonnes, net of est. conversions and misc. changes, accounting for historical and expected delivery performance.

M. Bpd / M. Dwt Forecast

Number & Value Number & Value

Aug Trend

54.0

Forecast*

Aug

85.7

0.6

0.5

0.3

40.0

25.0

1

10.6

74%

0.3

3

M. Dwt M. Dwt, month end

9.3

• After rising notably in October, average Suezmax spot earnings softened by 11% m-o-m in November to $16,759/day. Average Suezmax spot earnings in the first eleven months of the year stood at $15,774/day, down by 42% relative to the full year 2016 average, highlighting the difficult market conditions that have been prevalent in the year to date, largely as a result of robust fleet growth. • Suezmax dwt demand is currently expected to have expanded by a robust 6.8% in full year 2017, heavily supported by rising long-haul crude trade between the Atlantic Basin and Asia on the back of rising US and Brazilian output, alongside a recovery in Libyan output bolstering trade on ex-Med routes. In 2018, Suezmax dwt demand is still projected to grow firmly by 4.9%. Whilst the decision to extend the OPEC-led supply cuts until end 2018 could continue to limit Middle Eastern exports next year, growth in Suezmax dwt demand is expected to be supported by strong expansion in US exports to long-haul destinations such as China. • In full year 2017 the active Suezmax fleet is projected to have grown by a rapid 8.4% due to a record of 8.8m dwt expected to have been delivered into the fleet. In 2018, growth in the active Suezmax fleet is expected to slow to 4.2% as a result of an anticipated slowdown in deliveries to a more moderate total of 5.4m dwt.

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Aframax Market TrendsAframax Market Long-Term Aframax Trends

Aframax Spot Aframax Market

Rates 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

100K Baltic - UKC 93 82 83 71 63 60 77 96 77 -20%

100K Far East Russia - Korea~ 0.70 0.48 0.37 0.34 0.33 0.32 0.37 0.43 0.42 -3%

80K Med - Med 108 98 108 89 84 78 103 146 109 -25%

80K Med - Singapore~ 2.93 2.38 2.32 2.17 2.10 2.10 2.20 2.38 2.40 1%

80K UKC - UKC 111 106 104 100 98 90 106 120 101 -16%

80K Indonesia - Japan 113 102 102 97 86 83 102 109 113 3%

80K SE Asia - Australia 111 98 105 103 89 85 104 116 118 2%

80K Black Sea - Med 110 99 110 92 83 79 104 146 119 -18%

80K Gulf - Singapore 111 100 108 99 92 86 100 123 121 -2%

70K Caribs - US Gulf 133 107 118 95 89 96 149 128 110 -14%~ Lump sum in million dollars

Aframax Aframax Market

Earnings* 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

Average Spot Earnings 37,977 22,965 14,133 10,481 7,963 5,778 13,025 19,614 12,065 -38%

1 Year T/C Rate (Modern)" 26,712 21,488 15,535 15,000 14,625 14,500 14,725 15,000 15,125 1%3 Year T/C Rate (Modern)" 24,587 20,601 16,875 16,750 16,750 16,750 16,750 16,750 16,750 0%

Aframax Spot Aframax Spot Demand

Demand** 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

Intra Asia 64 66 61 52 73 61 59 58 39 -33%

Baltic - UKC 39 41 46 53 40 46 43 46 41 -11%

Caribs - N America 41 40 26 22 42 20 35 49 29 -41%

Med - Med 38 25 42 35 46 44 38 60 59 -2%

Black Sea - Med 23 23 29 28 29 25 23 24 30 25%

Black Sea/Med - UKC 3 3 6 5 3 8 4 3 3 0%

UKC - UKC 20 18 29 31 27 23 33 31 38 23%

MEG - East/India 10 11 15 15 7 17 11 12 6 -50%

Others 54 59 67 82 85 71 97 92 63 -32%

Total Nos. 293 285 321 323 352 315 343 375 308 -18%

Total m. dwt 29.7 28.8 32.3 33.8 35.2 30.6 34.7 36.7 29.3 -20%

Clarksons Research Page 8

Average WS Average WS

WEAKER...

WEAKER!!

WEAKER...

FIRM....

SOFTER….

STEADY...

WEAKER...

STEADY...

WEAKER...

Average $/day Average $/day

WEAKER!!STEADY...STEADY...

No of Fixtures, Avg. No of Fixtures

WEAKER!!

FIRMER...

WEAKER...

WEAKER!!

STEADY...

FIRMER...

^ Year to date. * Average Earnings are calculated as described in 'SIW Sources and Methods', which can be found on SIN. ** Spot demand is the average number of reported fixtures per month. Note: Fixtures refer to crude fixtures only. "Timecharter rates represent owners' rates prior to start 2016.

STEADY...

Dec-17

WEAKER!!

STEADY...

WEAKER!!

WEAKER...

WEAKER...

0

50

100

150

200

250

300

350

400

450

500

0

5

10

15

20

25

30

35

40

45

50

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep

-17

Nov

-17

US$,000/day

Aframax Average Spot Earnings (LHS)

No of Spot Fixtures (RHS)

0

10

20

30

40

50

60

70

80

90

0

10

20

30

40

50

60

Nov

-07

Nov

-08

Nov

-09

Nov

-10

Nov

-11

Nov

-12

Nov

-13

Nov

-14

Nov

-15

Nov

-16

Nov

-17

US$,000/day

Aframax 1 Yr Timecharter Rate

(LHS)

N/B Aframax Price (RHS)

US$ m

5 Yr Old Aframax Price (RHS)

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Aframax Market Trends

Aframax

Balance 2014 2015 2016 2017 2018 %

Crude DemandBaltic - UKC 1.3 1.4 1.5 1.6 1.6 1%UKC - UKC 2.2 2.1 2.3 2.3 2.3 0%Black Sea/Med-Med/UKC 1.5 1.5 1.3 1.5 1.5 1%Intra Asia 1.3 1.7 1.7 1.8 2.1 12%

Caribs - N America 1.5 1.4 1.4 1.2 1.1 -3%MEG - Asia/Australia 0.3 0.4 0.5 0.5 0.5 0%Others 2.4 2.2 2.3 2.3 2.2 -4%

Total, m bpd # 10.6 10.8 11.0 11.2 11.3 1%Total, m dwt ~ # 54.6 55.1 55.8 57.0 59.3 4%% growth -1.7% 0.9% 1.3% 2.2% 3.9%~Demand derived from crude trade above and DPP trade.

Supply*85,000-99,999 dwt # 8.4 8.1 7.9 0.0100,000-109,999 dwt # 55.0 57.1 60.7 0.0110,000-124,999 dwt # 33.5 34.4 36.2 0.0

Total # 96.9 99.6 104.9 108.7 111.8 3%Combos in Oil # 0.7 0.8 0.3 0.2 0.2 0%Laid-up & Long-term Storage # 0.5 0.7 0.8 0.8 0.8 0%Shuttle Tankers # 3.5 3.4 3.3 3.3 3.3 0%Products Tankers # 28.1 31.0 34.4 37.4 38.1 2%Active Crude Fleet # 65.5 65.2 66.6 67.5 69.8 3%% growth -2.6% -0.4% 2.1% 1.3% 3.5%

BalanceDemand Growth -2% 1% 1% 2% 4%Supply Growth -3% 0% 2% 1% 3%

Balance 1% 1% -1% 1% 0%

Aframax S&P 3 Month

Market # 2014 2015 2016 2017^ Jun Jul Sep Oct Nov

Newbuild Prices113-115K newbuild ($m) # 54.0 52.0 44.5 44.0 43.0 43.0 43.0 43.0 44.0 FIRM... 1%

No. of Contracts Placed 28 104 18 49 14 4 5 0 2 WEAKER!! -61%Est. Investment Value ($bn) 1.5 5.5 0.9 2.2 0.6 0.2 0.2 0.0 0.1 WEAKER!! -61%

Secondhand Prices105K 5yo, d/h ($m) 42.0 46.0 29.0 30.0 31.0 31.0 30.0 30.0 30.0 WEAK... -2%

105K 10yo, d/h ($m) 27.0 31.0 18.0 18.0 20.0 20.0 20.0 20.0 18.0 WEAK... -3%

95-97k 15 year old ($m) 14.0 18.0 13.0 10.0 12.0 12.0 10.0 10.0 10.0 WEAKER!! -17%

No. of Sales 72 46 37 35 3 2 2 3 3 WEAKER!! -11%5 Year Old/NB Price Ratio 78% 88% 65% 68% 72% 72% 70% 70% 68% WEAK... -3%

Demolition$/ldt 455 295 295 415 365 385 415 385 415 FIRM... 4%

Aframax Scrap Value ($m) 7.5 5.0 4.9 7.1 6.2 6.6 7.1 6.6 7.1 FIRM... 4%

No. Scrapped 22 3 6 29 3 4 3 4 5 WEAKER... -8%

Fleet

Profile 2014 2015 2016 2017^ Jun Jul Sep Oct Nov 2017 2018

Fleet Total 96.9 99.6 104.9 108.7 108.1 108.6 109.1 108.9 108.7 108.7 111.8Deliveries 1.9 3.6 5.9 7.1 0.7 0.9 0.9 0.2 0.3 7.5 6.5Scrapping 2.1 0.3 0.6 3.0 0.3 0.4 0.3 0.4 0.5 3.4 3.5Contracting 3.1 11.7 2.1 5.6 1.6 0.5 0.6 0.0 0.2

Orderbook 12.6 20.6 16.1 14.4 16.5 16.0 14.8 14.6 14.4

Clarksons Research Page 9 Dec-17

*End of year figure. ^Year to date/latest price. Fleet totals in metric tonnes, net of est. conversions and misc. changes, accounting for historical and expected delivery performance.

M. Bpd / M. Dwt Forecast

Number & Value Number & Value

Aug Trend

43.0

0

"Laid-up" includes vessels reported and confirmed to be in lay-up, remaining out of service for an extended period.

Forecast*

15.3

0.0

30.0

20.0

12.0

4

415

0.0

108.5

0.7

0.6

M. Dwt M. Dwt, month end

70%

7.1

6

Aug

• In November, average Aframax spot earnings fell by 38% m-o-m to stand at $12,065/day. Although this value still represents an improvement relative to mid- 2017 when earnings dipped below $6,000/day, average Aframax spot earnings in the first eleven months of the year stood at $14,133/day, remaining relatively suppressed historically. • Crude Aframax dwt demand is currently expected to have grown by 2.2% in full year 2017, supported by expansion in intra-Asian and cross-Med crude trade. However, Aframax dwt demand growth is expected to be limited by declining trade on the Caribs-North America route as a result of lower Venezuelan exports. Caribs-North American crude trade is anticipated to decline further in 2018, although growing US crude exports alongside another year of firm intra-Asian crude trade growth, partly on the back of rising Chinese imports of Russian crude, is projected to support relatively healthy Aframax dwt demand growth of 3.9%. • In full year 2017, 3.7m dwt of crude Aframax tonnage is expected to have been delivered into the fleet, the highest volume for six years. However, projected scrapping totalling a relatively firm 2.6m dwt is expected to limit growth in the active crude Aframax fleet to 1.3%. In 2018, growth in the active crude Aframax fleet is expected to reach 3.5%.

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Product Tanker Market TrendsProducts Tanker Market Long-Term Product Tanker Trends

Clean Spot Clean Market

Rates 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

LR2 Gulf - Japan 75K 106 92 105 88 101 117 118 121 119 -2%LR1 Gulf - Japan 55K 118 100 119 109 115 127 137 121 125 4%MR USG - UKC 38K 101 83 103 122 96 109 85 76 130 70%MR UKC - USAC 37K 140 105 137 137 123 117 146 109 118 8%MR WC India - Japan 35K 124 107 145 130 135 146 164 164 173 5%Handy Med - Med 30K 163 135 153 138 129 118 159 154 143 -7%Dirty Med - USG 55K 124 103 118 115 106 108 114 111 116 4%

Product Average $/day Product Market

Earnings* 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

Clean 'MR' Spot Earnings 21,444 12,124 10,008 9,895 8,980 9,652 10,998 8,924 10,113 13%Clean 'Handy' Spot Earnings 22,094 8,962 6,730 4,596 3,325 1,223 6,681 6,201 4,094 -34%Dirty Ave. Spot Earnings 26,548 15,388 9,865 9,562 7,902 7,143 8,293 7,612 7,190 -6%LR1 74,000 dwt 1 Yr T/C" 23,567 18,116 13,075 13,250 13,000 12,625 13,075 13,438 13,438 0%MR 47-48,000 dwt 1 Yr T/C" 17,769 15,092 13,157 13,275 13,250 13,125 13,125 13,531 13,750 2%

Product Spot Product Spot Demand

Demand** 2015 2016 2017^ Jun Jul Aug Sep Oct Nov This Month

Intra - Asia 174 169 127 54 163 114 69 150 228 52%

MEG - East 67 79 83 90 96 73 65 78 72 -8%

Intra - MEG 48 54 53 51 46 58 55 53 50 -6%

Transatlantic 56 76 79 96 106 121 60 54 62 15%

Med - Med 66 74 110 109 116 89 119 105 109 4%

USG - S. America 43 57 58 82 50 55 38 56 64 14%

Baltic - UKC 39 45 53 49 43 48 58 46 46 0%

India - East 25 36 48 44 48 55 58 53 44 -17%

Black Sea - Med 24 33 43 47 40 34 50 39 51 31%

UKC - WAF 20 23 31 39 24 25 18 22 21 -5%

Others 292 346 361 339 359 390 343 371 364 -2%

Total Nos. 854 992 1047 1000 1091 1062 933 1027 1111 8%

Total m. dwt 49.1 55.9 58.1 55.1 60.8 59.9 52.3 56.9 62.0 9%

Clarksons Research Page 10

FIRMER...

^ Year to date. * Average Earnings are calculated as described in 'SIW Sources and Methods', which can be found on the Shipping Intelligence Network. ** Spot demand is the average number of reported clean products fixtures per month. "Timecharter rates represent owners' rates prior to start 2016.

Dec-17

STEADY...

FIRMER...

FIRMER...

No of Fixtures, Avg. No of Fixtures

SOFTER...

SOFTER...

SOFTER...

WEAKER...

FIRM....

STEADY...

FIRMER...

FIRMER...

FIRMER...WEAKER!!

STEADY...

FIRM....

SOFTER...

STEADY...

FIRMER...

Average WS Average WS

STEADY...FIRM....FIRMER...FIRMER...FIRM....SOFTER...

Average $/day

250

500

750

1000

1250

1500

1750

2000

0

5

10

15

20

25

30

35

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep

-17

Nov

-17

US$,000/day

Clean MR Spot Earnings (LHS)

No of Clean & Dirty Spot Fixtures (RHS)

Dirty Average Spot Earnings (LHS)

0

10

20

30

40

50

60

0

10

20

30

40

50

60

Nov

-07

Nov

-08

Nov

-09

Nov

-10

Nov

-11

Nov

-12

Nov

-13

Nov

-14

Nov

-15

Nov

-16

Nov

-17

US$,000/day

N/B MR Price (RHS)

5 Yr Old MR Price (RHS)

LR1 1 Yr Timecharter Rate

(LHS)MR 1 Yr Timecharter Rate

(LHS)

US$ m

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Product Tanker Market Trends

Products

Balance 2014 2015 2016 2017 2018 %

DemandIntra Asia" 3.5 3.7 4.0 4.2 4.3 3%Intra Europe/Baltic/Med 5.2 5.4 5.3 5.3 5.4 2%USG-S America 1.8 2.0 2.2 2.4 2.6 6%Transatlantic^ 1.7 1.7 1.7 1.6 1.6 1%Other 8.5 9.4 10.0 10.3 10.6 3%

Total, m bpd ~ 20.7 22.1 23.1 23.8 24.5 3%Total, m dwt ** # 111.8 120.3 125.4 130.0 134.7 4%% growth 1.5% 7.7% 4.2% 3.6% 3.7%"Includes Japan, Korea, Australia, India, China and other non-OECD Asian countries. ^both directions.

Supply* 10,000-54,999 dwt # 81.2 86.1 90.3 92.6 94.1 2%55,000-84,999 dwt # 24.2 24.3 25.5 26.7 27.8 4% 84,000-124,999 dwt # 28.1 31.0 34.4 37.4 38.1 2%

Total # 133.6 141.3 150.2 156.7 160.1 2%Combos in Oil # 0.0 0.0 0.0 0.0 0.0 0%Laid-up # 0.7 0.6 0.3 0.3 0.3 -4%Long-term Storage # 0.0 0.3 0.4 0.4 0.4 0%Active Fleet # 132.9 140.5 149.6 156.0 159.4 2%% growth 4.0% 5.8% 6.5% 4.3% 2.2%

BalanceDemand Growth 2% 8% 4% 4% 4%

Supply Growth 4% 6% 6% 4% 2%

Balance -2% 2% -2% -1% 1%

Products S&P

Market # 2014 2015 2016 2017^ Jun Jul Aug Sep Oct Nov

Newbuild Prices47-51K newbuild ($m) # 36.8 35.5 32.5 33.5 33.5 33.5 33.5 33.5 33.5 SAME... 0%

No. of Contracts Placed 120 189 32 84 20 20 3 0 1 WEAKER!! -91%Est. Investment Value ($bn) 4.3 6.8 1.1 2.8 0.7 0.7 0.1 0.0 0.0 WEAKER!! -91%

Secondhand Prices47K 5yo ($m) 25.0 29.0 22.0 24.0 25.0 24.0 24.0 24.0 24.0 WEAK... -1%

45K 10yo ($m) 16.0 19.5 15.5 16.3 16.0 16.0 16.3 16.3 16.3 FIRM... 2%

45K 15yo ($m) 10.0 12.0 10.0 9.0 9.0 9.0 9.0 9.0 9.0 SAME... 0%

No. of Sales 137 117 84 93 9 5 6 8 6 WEAKER!! -20%5 Year Old/NB Price Ratio 68% 82% 68% 72% 75% 72% 72% 72% 72% WEAK... -1%

Demolition$/ldt 455 295 295 415 365 385 415 385 415 FIRM... 4%

MR Scrap Value ($m) 4.2 2.9 2.8 3.9 3.4 3.6 3.9 3.6 3.9 FIRM... 4%

No. Scrapped 39 27 20 30 4 1 2 3 6 WEAKER!! -15%

Fleet

Profile# 2014 2015 2016 2017^ Jun Jul Aug Sep Oct Nov 2017 2018

Fleet Total 133.6 141.3 150.1 156.3 154.1 155.1 156.1 156.3 156.3 156.7 160.1Deliveries 6.5 8.8 9.9 8.0 0.8 1.0 0.8 0.4 0.6 8.6 5.7Scrapping 1.4 0.8 0.8 1.7 0.2 0.0 0.1 0.2 0.4 2.1 2.3Contracting 7.0 12.0 2.1 5.8 1.8 1.2 0.1 0.0 0.1

Orderbook 24.2 25.9 16.9 14.3 16.6 16.8 15.3 14.9 14.3

Clarksons Research Page 11 Dec-17

*End of year figure. ^ Year to date/latest price. Fleet totals in metric tonnes, net of est. conversions, and misc. changes, accounting for historical and expected delivery performance. #The product tanker fleet, as shown on this page and on page 3, includes some IMO II graded tankers as well as all IMO III graded vessels and all coated tankers; for full specification of the product tanker fleet see page 23.

M. Dwt M. Dwt, month end Forecast*

415

8

0.8

0.5

0.1

16.1

0.1

23.5

155.4

16.0

9.0

11

3.9

70%

Trend

33.5

3

M. Bpd / M. Dwt Forecast

Number & Value Number & Value 3 Month

**Product tanker demand derived from DPP, CPP and veg oil trade. ~ Includes all oil petroleum products trade. "Laid-up" includes vessels reported and confirmed to be in lay-up, remaining out of service for an extended period.

• Average clean MR spot earnings increased by 13% m-o-m in November to reach $10,113/day. This represents the highest level since April, with the exception of September when Hurricane Harvey led to a temporarily much tighter MR market. Overall, average clean MR earnings in the first eleven months of the year remained suppressed relative to the previous four years, standing at $10,008/day. • In full year 2017, product tanker dwt demand is projected to have grown by 3.6%, supported by growing products trade on intra-Asian and ex-USG routes. Products exports out of the USG are also expected to expand firmly in 2018 as US refinery capacity grows, with continued firm trade growth expected on routes to Latin America as refinery sectors in some countries in the region continue to struggle, supporting projected product tanker dwt demand growth of 3.7%. Products imports are also expected to grow into other developing regions including non-OECD Asia, the Middle East and Africa. • In full year 2017, the active product tanker fleet is expected to have expanded by a firm 4.3%, with 8.6m dwt projected to be delivered. Supply side pressure could potentially start to ease in 2018, with product tanker fleet growth expected to slow to 2.2%.

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Tanker Timecharter Market

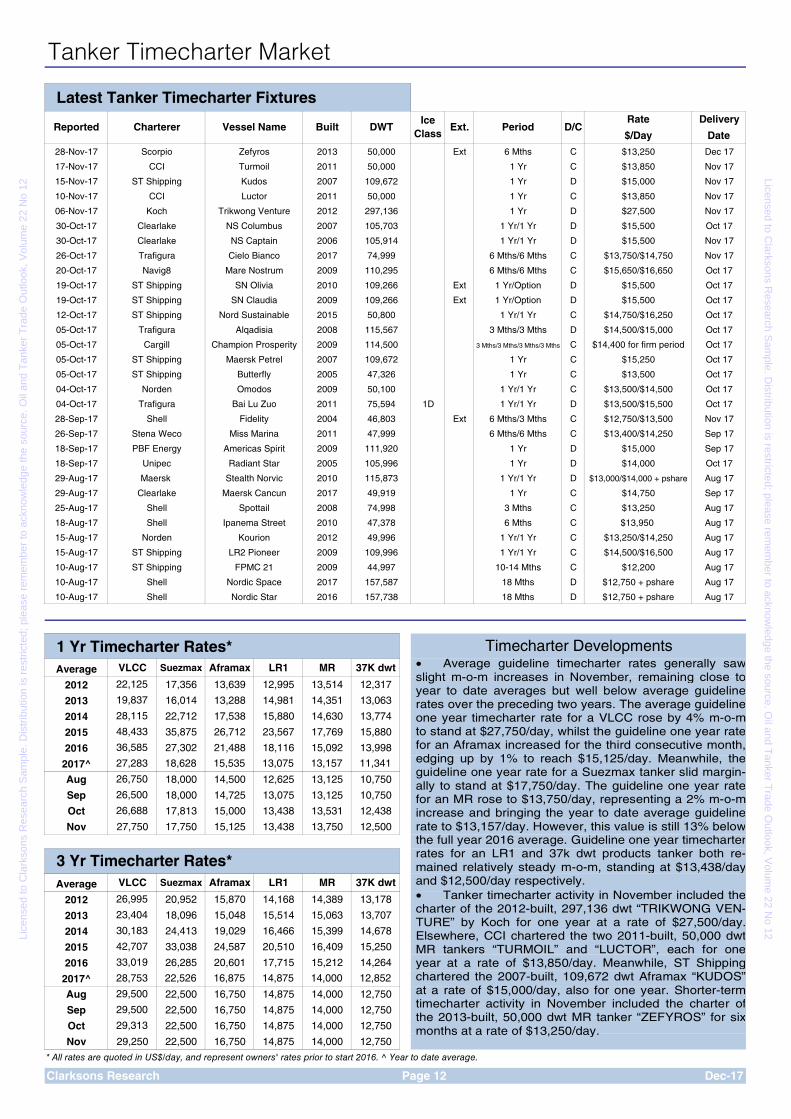

Latest Tanker Timecharter FixturesRate Delivery

$/Day Date

28-Nov-17 2013 Ext 6 Mths C $13,250 Dec 17

17-Nov-17 2011 1 Yr C $13,850 Nov 17

15-Nov-17 2007 1 Yr D $15,000 Nov 17

10-Nov-17 2011 1 Yr C $13,850 Nov 17

06-Nov-17 2012 1 Yr D $27,500 Nov 17

30-Oct-17 2007 1 Yr/1 Yr D $15,500 Oct 17

30-Oct-17 2006 1 Yr/1 Yr D $15,500 Nov 17

26-Oct-17 2017 6 Mths/6 Mths C $13,750/$14,750 Nov 17

20-Oct-17 2009 6 Mths/6 Mths C $15,650/$16,650 Oct 17

19-Oct-17 2010 Ext 1 Yr/Option D $15,500 Oct 17

19-Oct-17 2009 Ext 1 Yr/Option D $15,500 Oct 17

12-Oct-17 2015 1 Yr/1 Yr C $14,750/$16,250 Oct 17

05-Oct-17 2008 3 Mths/3 Mths D $14,500/$15,000 Oct 17

05-Oct-17 2009 3 Mths/3 Mths/3 Mths/3 Mths C $14,400 for firm period Oct 17

05-Oct-17 2007 1 Yr C $15,250 Oct 17

05-Oct-17 2005 1 Yr C $13,500 Oct 17

04-Oct-17 2009 1 Yr/1 Yr C $13,500/$14,500 Oct 17

04-Oct-17 2011 1 Yr/1 Yr D $13,500/$15,500 Oct 17

28-Sep-17 2004 Ext 6 Mths/3 Mths C $12,750/$13,500 Nov 17

26-Sep-17 2011 6 Mths/6 Mths C $13,400/$14,250 Sep 17

18-Sep-17 2009 1 Yr D $15,000 Sep 17

18-Sep-17 2005 1 Yr D $14,000 Oct 17

29-Aug-17 2010 1 Yr/1 Yr D $13,000/$14,000 + pshare Aug 17

29-Aug-17 2017 1 Yr C $14,750 Sep 17

25-Aug-17 2008 3 Mths C $13,250 Aug 17

18-Aug-17 2010 6 Mths C $13,950 Aug 17

15-Aug-17 2012 1 Yr/1 Yr C $13,250/$14,250 Aug 17

15-Aug-17 2009 1 Yr/1 Yr C $14,500/$16,500 Aug 17

10-Aug-17 2009 10-14 Mths C $12,200 Aug 17

10-Aug-17 2017 18 Mths D $12,750 + pshare Aug 17

10-Aug-17 2016 18 Mths D $12,750 + pshare Aug 17

1 Yr Timecharter Rates*Average VLCC Suezmax Aframax LR1 MR 37K dwt

2012 22,125 17,356 13,639 12,995 13,514 12,317

2013 19,837 16,014 13,288 14,981 14,351 13,063

2014 28,115 22,712 17,538 15,880 14,630 13,774

2015 48,433 35,875 26,712 23,567 17,769 15,880

2016 36,585 27,302 21,488 18,116 15,092 13,998

2017^ 27,283 18,628 15,535 13,075 13,157 11,341

Aug 26,750 18,000 14,500 12,625 13,125 10,750

Sep 26,500 18,000 14,725 13,075 13,125 10,750

Oct 26,688 17,813 15,000 13,438 13,531 12,438

Nov 27,750 17,750 15,125 13,438 13,750 12,500

Average VLCC Suezmax Aframax LR1 MR 37K dwt

2012 26,995 20,952 15,870 14,168 14,389 13,178

2013 23,404 18,096 15,048 15,514 15,063 13,707

2014 30,183 24,413 19,029 16,466 15,399 14,678

2015 42,707 33,038 24,587 20,510 16,409 15,250

2016 33,019 26,285 20,601 17,715 15,212 14,264

2017^ 28,753 22,526 16,875 14,875 14,000 12,852

Aug 29,500 22,500 16,750 14,875 14,000 12,750

Sep 29,500 22,500 16,750 14,875 14,000 12,750

Oct 29,313 22,500 16,750 14,875 14,000 12,750

Nov 29,250 22,500 16,750 14,875 14,000 12,750

* All rates are quoted in US$/day, and represent owners' rates prior to start 2016. ^ Year to date average.

Clarksons Research Page 12

Timecharter Developments

3 Yr Timecharter Rates*

Dec-17

Shell Nordic Space 157,587

Shell Nordic Star 157,738

ST Shipping LR2 Pioneer 109,996

ST Shipping FPMC 21 44,997

Shell Ipanema Street 47,378

Norden Kourion 49,996

Clearlake Maersk Cancun 49,919

Shell Spottail 74,998

Unipec Radiant Star 105,996

Maersk Stealth Norvic 115,873

Stena Weco Miss Marina 47,999

PBF Energy Americas Spirit 111,920

Trafigura Bai Lu Zuo 75,594 1D

Shell Fidelity 46,803

ST Shipping Butterfly 47,326

Norden Omodos 50,100

Cargill Champion Prosperity 114,500

ST Shipping Maersk Petrel 109,672

ST Shipping Nord Sustainable 50,800

Trafigura Alqadisia 115,567

ST Shipping SN Olivia 109,266

ST Shipping SN Claudia 109,266

Trafigura Cielo Bianco 74,999

Navig8 Mare Nostrum 110,295

Clearlake NS Columbus 105,703

Clearlake NS Captain 105,914

CCI Luctor 50,000

Koch Trikwong Venture 297,136

CCI Turmoil 50,000

ST Shipping Kudos 109,672

Ext. Period D/C

Scorpio Zefyros 50,000

Reported Charterer Vessel Name Built DWTIce

Class

• Average guideline timecharter rates generally sawslight m-o-m increases in November, remaining close toyear to date averages but well below average guidelinerates over the preceding two years. The average guidelineone year timecharter rate for a VLCC rose by 4% m-o-mto stand at $27,750/day, whilst the guideline one year ratefor an Aframax increased for the third consecutive month,edging up by 1% to reach $15,125/day. Meanwhile, theguideline one year rate for a Suezmax tanker slid margin-ally to stand at $17,750/day. The guideline one year ratefor an MR rose to $13,750/day, representing a 2% m-o-mincrease and bringing the year to date average guidelinerate to $13,157/day. However, this value is still 13% belowthe full year 2016 average. Guideline one year timecharterrates for an LR1 and 37k dwt products tanker both re-mained relatively steady m-o-m, standing at $13,438/dayand $12,500/day respectively. • Tanker timecharter activity in November included thecharter of the 2012-built, 297,136 dwt “TRIKWONG VEN-TURE” by Koch for one year at a rate of $27,500/day.Elsewhere, CCI chartered the two 2011-built, 50,000 dwtMR tankers “TURMOIL” and “LUCTOR”, each for oneyear at a rate of $13,850/day. Meanwhile, ST Shippingchartered the 2007-built, 109,672 dwt Aframax “KUDOS”at a rate of $15,000/day, also for one year. Shorter-termtimecharter activity in November included the charter ofthe 2013-built, 50,000 dwt MR tanker “ZEFYROS” for sixmonths at a rate of $13,250/day.

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

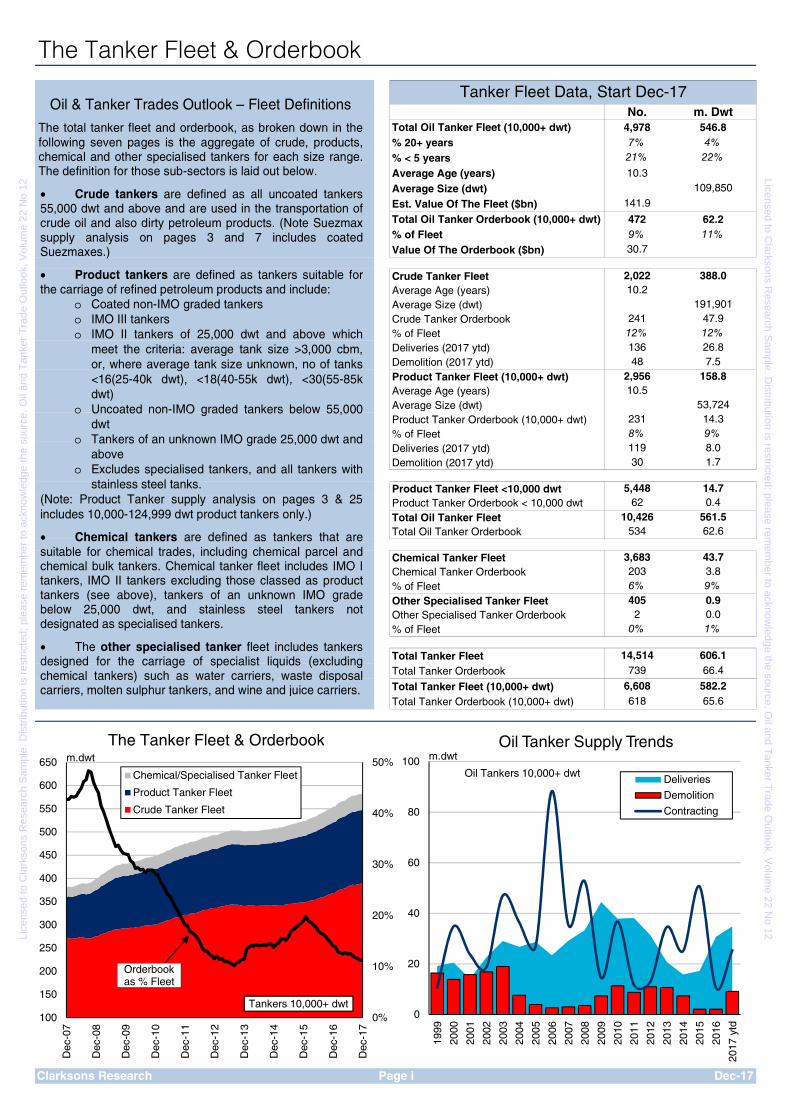

The Tanker Fleet & Orderbook

No. m. Dwt Total Oil Tanker Fleet (10,000+ dwt) 4,978 546.8 % 20+ years 7% 4% % < 5 years Average Age (years) 10.3

Average Size (dwt) Est. Value Of The Fleet ($bn) Total Oil Tanker Orderbook (10,000+ dwt) 472 62.2

% of Fleet 9% 11% Value Of The Orderbook ($bn)

Crude Tanker Fleet Average Age (years)

Average Size (dwt) Crude Tanker Orderbook % of Fleet

Deliveries (2017 ytd) Demolition (2017 ytd)

Product Tanker Fleet (10,000+ dwt)Average Age (years)Average Size (dwt)Product Tanker Orderbook (10,000+ dwt)% of FleetDeliveries (2017 ytd)Demolition (2017 ytd)

Product Tanker Fleet <10,000 dwtProduct Tanker Orderbook < 10,000 dwtTotal Oil Tanker FleetTotal Oil Tanker Orderbook

Chemical Tanker FleetChemical Tanker Orderbook

% of Fleet Other Specialised Tanker Fleet

Other Specialised Tanker Orderbook% of Fleet

Total Tanker FleetTotal Tanker Orderbook

Total Tanker Fleet (10,000+ dwt)Total Tanker Orderbook (10,000+ dwt)

Clarksons Research

65.6

62.6

618

0.4

6% 9%0.9

606.1739

6,608

Tanker Fleet Data, Start Dec-17

21% 22%

109,850

582.2

12%

2,022 388.010.2

66.4

26.8

2,956 158.8

191,901241 47.912%

7.5136

53,724231 14.38% 9%

30 1.7119 8.0

5,448 14.7

3,683 43.7

6210,426 561.5

534

0.00% 1%

203 3.8

405

141.9

30.7

10.5

2

48

14,514

Page i Dec-17

0%

10%

20%

30%

40%

50%

100

150

200

250

300

350

400

450

500

550

600

650

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

m.dwt

Chemical/Specialised Tanker Fleet

Product Tanker Fleet

Crude Tanker Fleet

Tankers 10,000+ dwt

The Tanker Fleet & Orderbook

Orderbook as % Fleet

Oil & Tanker Trades Outlook – Fleet Definitions

The total tanker fleet and orderbook, as broken down in the following seven pages is the aggregate of crude, products, chemical and other specialised tankers for each size range. The definition for those sub-sectors is laid out below.

• Crude tankers are defined as all uncoated tankers 55,000 dwt and above and are used in the transportation of crude oil and also dirty petroleum products. (Note Suezmax supply analysis on pages 3 and 7 includes coated Suezmaxes.)

• Product tankers are defined as tankers suitable for the carriage of refined petroleum products and include:

o Coated non-IMO graded tankers o IMO III tankers o IMO II tankers of 25,000 dwt and above which

meet the criteria: average tank size >3,000 cbm, or, where average tank size unknown, no of tanks <16(25-40k dwt), <18(40-55k dwt), <30(55-85k dwt)

o Uncoated non-IMO graded tankers below 55,000 dwt

o Tankers of an unknown IMO grade 25,000 dwt and above

o Excludes specialised tankers, and all tankers with stainless steel tanks.

(Note: Product Tanker supply analysis on pages 3 & 25 includes 10,000-124,999 dwt product tankers only.)

• Chemical tankers are defined as tankers that are suitable for chemical trades, including chemical parcel and chemical bulk tankers. Chemical tanker fleet includes IMO I tankers, IMO II tankers excluding those classed as product tankers (see above), tankers of an unknown IMO grade below 25,000 dwt, and stainless steel tankers not designated as specialised tankers.

• The other specialised tanker fleet includes tankers designed for the carriage of specialist liquids (excluding chemical tankers) such as water carriers, waste disposal carriers, molten sulphur tankers, and wine and juice carriers.

0

20

40

60

80

100

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

ytd

m.dwtOil Tanker Supply Trends

Deliveries

Demolition

Contracting

Oil Tankers 10,000+ dwt

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Tanker Fleet By Size (Numbers)Crude Tanker No. vessels, end: Fleet Growth %

Fleet (by dwt sector) 2014 2015 2016 Jun Jul Aug Sep Oct Nov Dec Year on Year

55,000/69,999 49 42 44 45 45 46 46 46 45 45 FIRM.... 4.7%70,000/84,999 44 45 45 44 44 44 44 44 44 44 STEADY... -2.2%Total Panamax 93 87 89 89 89 90 90 90 89 89 STEADY... 1.1%85,000/99,999 62 59 57 55 53 51 50 49 47 45 WEAKER... -21.1%100,000/109,999 362 362 369 367 367 365 361 360 358 358 SOFTER... -3.2%110,000/124,999 213 214 225 239 242 246 248 252 253 254 FIRMER... 13.4%Total Aframax 637 635 651 661 662 662 659 661 658 657 STEADY... 0.9%125,000/149,999 106 108 111 113 113 112 113 112 114 113 STEADY... 0.9%150,000/159,999 292 300 320 344 350 354 354 360 361 361 FIRMER... 12.8%160,000/199,999 66 66 67 67 67 67 67 67 67 67 STEADY... 1.5%Total Suezmax 464 474 498 524 530 533 534 539 542 541 FIRMER... 8.6%200,000/299,999 209 210 234 247 250 253 249 248 250 249 FIRM.... 6.4%300,000/309,999 175 178 187 194 194 194 194 197 198 198 FIRM.... 5.9%310,000/319,999 202 216 231 236 237 238 240 240 240 242 FIRM.... 5.7%320,000+ 45 46 46 46 46 46 46 46 46 46 STEADY...Total VL/ULCC 631 650 698 723 727 731 729 731 734 735 FIRM.... 5.6%

Total Crude Tanker Fleet 1,825 1,846 1,936 1,997 2,008 2,016 2,012 2,021 2,023 2,022 FIRM.... 4.6%% change year-on-year -1.1% 1.2% 4.9% 6.3% 6.5% 6.4% 5.7% 5.5% 5.3% 4.6%

Product Tanker No. vessels, end: Fleet Growth %

Fleet (by dwt sector) 2014 2015 2016 Jun Jul Aug Sep Oct Nov Dec Year on Year

Total < 10,000 5,301 5,353 5,411 5,431 5,438 5,441 5,438 5,448 5,450 5,448 STEADY... 0.8%Total 10-24,999 273 270 271 276 276 276 275 276 277 277 STEADY... 2.2%25,000/34,999 121 115 112 111 111 111 111 111 111 112 STEADY... -1.8%35,000/39,999 334 340 348 350 350 350 350 350 350 349 STEADY... 0.6%Total Handy (25,000-39,999) 455 455 460 461 461 461 461 461 461 461 STEADY...40,000/49,999 961 1,036 1,099 1,120 1,123 1,127 1,126 1,126 1,125 1,125 STEADY... 2.5%50,000/54,999 321 343 360 364 367 367 369 372 374 375 FIRM.... 4.2%Total MR (40,000-54,999) 1,282 1,379 1,459 1,484 1,490 1,494 1,495 1,498 1,499 1,500 STEADY... 2.9%55,000/69,999 37 35 34 34 34 34 34 34 33 33 STEADY... -2.9%70,000/84,999 294 296 312 319 319 323 324 326 327 327 FIRM.... 4.8%Total LR1 331 331 346 353 353 357 358 360 360 360 FIRM.... 4.0%85,000/109,999 180 199 225 238 240 241 241 243 243 241 FIRM.... 7.6%110,000/124,999 79 86 91 93 93 96 98 99 100 101 FIRMER... 12.2%Total LR2 259 285 316 331 333 337 339 342 343 342 FIRMER... 8.9%125,000/159,999 8 8 10 10 10 10 10 10 10 11 FIRMER... 22.2%160,000/199,999 5 5 5 5 5 5 5 5 5 5 STEADY...Total Coated Suezmax 13 13 15 15 15 15 15 15 15 16 FIRMER... 14.3%

Total Product Tanker Fleet 7,914 8,086 8,278 8,351 8,366 8,381 8,381 8,400 8,405 8,404 STEADY... 1.6%Total Product Fleet 10,000+ 2,613 2,733 2,867 2,920 2,928 2,940 2,943 2,952 2,955 2,956 FIRM.... 3.2%% change year-on-year 3.4% 4.6% 4.9% 4.4% 4.3% 4.2% 3.9% 3.9% 3.7% 3.2%

TOTAL OIL TANKER FLEET 9,739 9,932 10,214 10,348 10,374 10,397 10,393 10,421 10,428 10,426 STEADY... 2.2%TOTAL OIL TANKER FLEET 10,000+ 4,438 4,579 4,803 4,917 4,936 4,956 4,955 4,973 4,978 4,978 FIRM.... 3.8%% change year-on-year 1.5% 3.2% 4.9% 5.2% 5.2% 5.1% 4.6% 4.5% 4.3% 3.8%

Chemical Tanker No. vessels, end: Fleet Growth %

Fleet (by dwt sector) 2014 2015 2016 Jun Jul Aug Sep Oct Nov Dec Year on Year

< 10,000 1,985 2,009 2,040 2,052 2,054 2,059 2,059 2,063 2,065 2,068 STEADY... 1.2%10,000+ 1,431 1,485 1,557 1,585 1,592 1,598 1,605 1,609 1,611 1,615 FIRM.... 3.1%Total Chemical Tanker Fleet 3,416 3,494 3,597 3,637 3,646 3,657 3,664 3,672 3,676 3,683 STEADY... 2.1%

Specialised Tanker No. vessels, end: Fleet Growth %

Fleet (by dwt sector) 2014 2015 2016 Jun Jul Aug Sep Oct Nov Dec Year on Year

< 10,000 382 382 389 390 388 389 389 390 390 390 STEADY...10,000+ 17 16 15 15 15 15 15 15 15 15 STEADY...Total Specialised Tanker Fleet 399 398 404 405 403 404 404 405 405 405 STEADY...

Total Tanker Fleet 13,554 13,824 14,215 14,390 14,423 14,458 14,461 14,498 14,509 14,514 STEADY... 2.2%Total Tanker Fleet 10,000+ 5,886 6,080 6,375 6,517 6,543 6,569 6,575 6,597 6,604 6,608 FIRM.... 3.8%% change year-on-year 1.3% 3.3% 4.9% 5.0% 5.0% 4.9% 4.6% 4.5% 4.2% 3.8%

Clarksons Research The Total Oil Tanker Fleet includes crude and products tankers. The Total Tanker Fleet includes crude, products, chemical and specialised tankers 100+ Gt.

No. vessels, start:

No. vessels, start:

No. vessels, start:

No. vessels, start:

Dec-17Page ii

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Tanker Fleet By Size (Dwt)Crude Tanker Million Dwt, end: Fleet Growth %

Fleet (by dwt sector) 2014 2015 2016 Jun Jul Aug Sep Oct Nov Dec Year on Year

55,000/69,999 3.2 2.8 2.9 3.0 3.0 3.0 3.0 3.0 3.0 3.0 FIRM.... 4.9%70,000/84,999 3.3 3.3 3.3 3.3 3.3 3.3 3.3 3.3 3.3 3.3 STEADY... -2.2%Total Panamax 6.5 6.1 6.2 6.2 6.2 6.3 6.3 6.3 6.2 6.2 STEADY... 1.1%85,000/99,999 6.0 5.7 5.5 5.3 5.1 4.9 4.8 4.7 4.5 4.3 WEAKER... -21.0%100,000/109,999 38.3 38.3 39.1 38.9 38.9 38.7 38.3 38.2 38.0 38.0 SOFTER... -3.2%110,000/124,999 24.4 24.5 25.8 27.4 27.7 28.2 28.4 28.9 29.0 29.1 FIRMER... 13.2%Total Aframax 68.8 68.6 70.4 71.6 71.7 71.8 71.5 71.8 71.5 71.4 STEADY... 1.4%125,000/149,999 15.5 15.8 16.2 16.5 16.5 16.4 16.5 16.4 16.7 16.5 STEADY... 1.0%150,000/159,999 45.9 47.2 50.3 54.1 55.1 55.7 55.7 56.6 56.8 56.8 FIRMER... 12.8%160,000/199,999 10.9 10.9 11.1 11.1 11.1 11.1 11.1 11.1 11.1 11.1 STEADY... 1.5%Total Suezmax 72.3 73.9 77.6 81.7 82.7 83.2 83.3 84.1 84.6 84.4 FIRMER... 8.8%200,000/299,999 61.9 62.2 69.4 73.3 74.2 75.1 73.9 73.6 74.2 74.0 FIRM.... 6.5%300,000/309,999 53.3 54.3 57.0 59.1 59.1 59.1 59.1 60.0 60.3 60.3 FIRM.... 5.9%310,000/319,999 64.0 68.5 73.2 74.8 75.1 75.4 76.1 76.1 76.1 76.7 FIRM.... 5.7%320,000+ 14.7 15.0 15.0 15.0 15.0 15.0 15.0 15.0 15.0 15.0 STEADY...Total VL/ULCC 193.9 199.9 214.7 222.3 223.5 224.7 224.1 224.8 225.7 226.0 FIRM.... 5.6%

Total Crude Tanker Fleet 341.5 348.5 368.9 381.8 384.1 385.9 385.2 386.9 387.9 388.0 FIRM.... 5.4%% change year-on-year 0.2% 2.1% 5.9% 7.1% 7.2% 7.4% 6.5% 6.3% 6.1% 5.4%

Product Tanker Million Dwt, end: Fleet Growth %

Fleet (by dwt sector) 2014 2015 2016 Jun Jul Aug Sep Oct Nov Dec Year on Year

Total < 10,000 14.2 14.3 14.5 14.6 14.6 14.6 14.6 14.7 14.7 14.7 STEADY... 1.4%Total 10-24,999 4.0 4.0 4.0 4.1 4.1 4.1 4.1 4.1 4.1 4.1 STEADY... 2.4%25,000/34,999 3.8 3.6 3.5 3.5 3.5 3.5 3.5 3.5 3.5 3.5 STEADY... -1.5%35,000/39,999 12.6 12.8 13.1 13.2 13.2 13.2 13.2 13.2 13.2 13.2 STEADY... 0.6%Total Handy (25,000-39,999) 16.3 16.4 16.6 16.7 16.7 16.7 16.7 16.7 16.7 16.7 STEADY... 0.2%40,000/49,999 44.4 48.2 51.3 52.3 52.4 52.6 52.6 52.6 52.6 52.6 STEADY... 2.6%50,000/54,999 16.4 17.5 18.4 18.6 18.7 18.7 18.8 19.0 19.1 19.1 FIRM.... 4.1%Total MR (40,000-54,999) 60.8 65.7 69.6 70.9 71.2 71.4 71.4 71.6 71.6 71.7 FIRM.... 3.0%55,000/69,999 2.4 2.3 2.2 2.2 2.2 2.2 2.2 2.2 2.2 2.2 SOFTER... -3.1%70,000/84,999 21.8 21.9 23.1 23.7 23.7 24.0 24.0 24.2 24.2 24.2 FIRM.... 4.8%Total LR1 24.2 24.3 25.4 25.9 25.9 26.2 26.3 26.4 26.4 26.4 FIRM.... 4.1%85,000/109,999 19.1 21.1 24.0 25.4 25.7 25.8 25.8 26.0 26.0 25.8 FIRM.... 7.9%110,000/124,999 9.1 9.9 10.4 10.7 10.7 11.0 11.2 11.3 11.5 11.6 FIRMER... 12.0%Total LR2 28.1 31.0 34.4 36.1 36.3 36.8 37.0 37.3 37.4 37.4 FIRMER... 9.2%125,000/159,999 1.3 1.3 1.6 1.6 1.6 1.6 1.6 1.6 1.6 1.7 FIRMER... 22.4%160,000/199,999 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 STEADY...Total Coated Suezmax 2.1 2.1 2.4 2.4 2.4 2.4 2.4 2.4 2.4 2.5 FIRMER... 14.3%

Total Product Tanker Fleet 149.8 157.7 167.0 170.6 171.2 172.1 172.5 173.2 173.4 173.5 FIRM.... 4.2%Total Product Fleet 10,000+ 135.6 143.4 152.5 156.0 156.5 157.5 157.8 158.5 158.7 158.8 FIRM.... 4.4%% change year-on-year 3.9% 5.7% 6.3% 5.7% 5.5% 5.6% 5.3% 5.2% 5.0% 4.4%

TOTAL OIL TANKER FLEET 491.3 506.2 535.9 552.4 555.3 558.1 557.7 560.1 561.3 561.5 FIRM.... 5.0%TOTAL OIL TANKER FLEET 10,000+ 477.1 491.9 521.4 537.8 540.6 543.4 543.1 545.4 546.6 546.8 FIRM.... 5.1%% change year-on-year 1.3% 3.1% 6.0% 6.7% 6.7% 6.9% 6.1% 5.9% 5.8% 5.1%

Chemical Tanker Million Dwt, end: Fleet Growth %

Fleet (by dwt sector) 2014 2015 2016 Jun Jul Aug Sep Oct Nov Dec Year on Year

< 10,000 8.3 8.4 8.5 8.6 8.6 8.6 8.6 8.7 8.7 8.7 STEADY... 2.0%10,000+ 29.9 31.6 33.4 34.2 34.4 34.5 34.7 34.8 34.9 35.0 FIRM.... 5.2%Total Chemical Tanker Fleet 38.2 40.0 42.0 42.8 43.0 43.2 43.3 43.5 43.5 43.7 FIRM.... 4.6%

Specialised Tanker Million Dwt, end: Fleet Growth %

Fleet (by dwt sector) 2014 2015 2016 Jun Jul Aug Sep Oct Nov Dec Year on Year

< 10,000 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 STEADY... 0.6%10,000+ 0.4 0.4 0.4 0.4 0.4 0.4 0.4 0.4 0.4 0.4 STEADY...Total Specialised Tanker Fleet 0.9 0.9 0.9 0.9 0.9 0.9 0.9 0.9 0.9 0.9 STEADY... 0.4%

Total Tanker Fleet 530.4 547.0 578.8 596.1 599.1 602.1 601.9 604.5 605.7 606.1 FIRM.... 5.0%Total Tanker Fleet 10,000+ 507.4 523.8 555.2 572.4 575.4 578.3 578.1 580.6 581.9 582.2 FIRM.... 5.1%% change year-on-year 1.3% 3.2% 6.0% 6.6% 6.6% 6.8% 6.1% 5.9% 5.7% 5.1%

Clarksons Research

Million Dwt, start:

Million Dwt, start:

Million Dwt, start:

Million Dwt, start:

The Total Oil Tanker Fleet includes crude and products tankers. The Total Tanker Fleet includes crude, products, chemical and specialised tankers 100+ Gt.

Dec-17Page iii

Lice

nsed

to C

lark

sons

Res

earc

h S

ampl

e. D

istr

ibut

ion

is r

estr

icte

d; p

leas

e re

mem

ber

to a

ckno

wle

dge

the

sour

ce. O

il an

d T

anke

r T

rade

Out

look

, Vol

ume

22 N

o 12

Licensed to Clarksons R

esearch Sam

ple. Distribution is restricted; please rem

ember to acknow

ledge the source. Oil and T

anker Trade O

utlook, Volum

e 22 No 12

Tanker Fleet By Age (Numbers)

Crude Tanker Age Profile (years) No. vessels Fleet Ratios

Fleet (by dwt sector) 20 + 15-19 10-14 5-9 0-4 20 + 15-19 10-14 5-9 0-4 Dec15yrs+ /Fleet

O'bk /15yrs+

55,000/69,999 11% 27% 47% 4% 11% 5 12 21 2 5 45 38%70,000/84,999 23% 59% 14% 5% 10 26 6 2 44 23% 30%Total Panamax 6% 25% 53% 9% 8% 5 22 47 8 7 89 30% 11%85,000/99,999 62% 24% 2% 11% 28 11 1 5 45 87%100,000/109,999 3% 21% 42% 30% 5% 10 74 149 108 17 358 23% 11%110,000/124,999 0% 6% 36% 36% 22% 1 14 91 91 57 254 6% 520%Total Aframax 6% 15% 37% 31% 11% 39 99 241 204 74 657 21% 63%125,000/149,999 19% 28% 20% 19% 13% 21 32 23 22 15 113 47% 11%150,000/159,999 1% 14% 18% 37% 30% 4 52 65 133 107 361 16% 88%160,000/199,999 12% 43% 42% 3% 8 29 28 2 67 12% 50%Total Suezmax 5% 17% 22% 34% 23% 25 92 117 183 124 541 22% 50%200,000/299,999 4% 24% 17% 33% 22% 11 59 42 81 56 249 28% 14%300,000/309,999 8% 28% 28% 22% 15% 15 55 56 43 29 198 35% 27%310,000/319,999 6% 17% 47% 30% 14 42 113 73 242 6% 350%320,000+ 2% 13% 57% 28% 1 6 26 13 46 2% 1400%Total VL/ULCC 4% 18% 20% 36% 23% 26 129 146 263 171 735 21% 59%

Total Crude Tanker Fleet 5% 17% 27% 33% 19% 95 342 551 658 376 2,022 22% 55%

Product Tanker Age Profile (years) No. vessels Fleet Ratios

Fleet (by dwt sector) 20 + 15-19 10-14 5-9 0-4 20 + 15-19 10-14 5-9 0-4 Dec15yrs+ /Fleet

O'bk /15yrs+

Total < 10,000 66% 5% 7% 13% 10% 3,581 255 379 707 526 5,448 70% 2%Total 10-24,999 34% 10% 17% 24% 16% 93 27 46 67 44 277 43% 17%25,000/34,999 31% 25% 24% 12% 8% 35 28 27 13 9 112 56% 10%35,000/39,999 6% 17% 42% 22% 13% 21 58 148 77 45 349 23% 9%

Total Handy (25,000-39,999) 12% 19% 38% 20% 12% 56 86 175 90 54 461 31% 9%40,000/49,999 8% 10% 29% 26% 27% 91 118 326 290 300 1,125 19% 25%50,000/54,999 19% 53% 27% 72 200 103 375

Total MR (40,000-54,999) 6% 8% 27% 33% 27% 91 118 398 490 403 1,500 14% 59%55,000/69,999 6% 15% 39% 36% 3% 2 5 13 12 1 33 21%70,000/84,999 1% 3% 39% 43% 14% 2 11 127 140 47 327 4% 246%

Total LR1 1% 4% 39% 42% 13% 4 16 140 152 48 360 6% 160%85,000/109,999 4% 11% 21% 32% 32% 10 27 50 76 78 241 15% 3%110,000/124,999 1% 10% 55% 34% 1 10 56 34 101 1% 3900%

Total LR2 3% 8% 18% 39% 33% 11 27 60 132 112 342 11% 105%125,000/159,999 55% 9% 36% 6 1 4 11160,000/199,999 20% 80% 1 4 5 20%

Total Coated Suezmax 6% 63% 6% 25% 1 10 1 4 16 6% 300%

Total Product Tanker Fleet 46% 6% 14% 20% 14% 3,836 530 1,208 1,639 1,191 8,404 52% 7%Total Product Fleet 10,000+ 9% 9% 28% 32% 22% 255 275 829 932 665 2,956 18% 44%

TOTAL OIL TANKER FLEET 38% 8% 17% 22% 15% 3,931 872 1,759 2,297 1,567 10,426 46% 11%TOTAL OIL TANKER FLEET 10,000+ 7% 12% 28% 32% 21% 350 617 1,380 1,590 1,041 4,978 19% 49%

Chemical Tanker Age Profile (years) No. vessels Fleet Ratios

Fleet (by dwt sector) 20 + 15-19 10-14 5-9 0-4 20 + 15-19 10-14 5-9 0-4 Dec15yrs+ /Fleet

O'bk /15yrs+

< 10,000 39% 9% 18% 25% 9% 806 182 382 515 183 2,068 48% 6%10,000+ 8% 12% 24% 40% 16% 136 193 386 642 258 1,615 20% 44%

Total Chemical Tanker Fleet 26% 10% 21% 31% 12% 942 375 768 1,157 441 3,683 36% 15%

Specialised Tanker Age Profile (years) No. vessels Fleet Ratios

Fleet (by dwt sector) 20 + 15-19 10-14 5-9 0-4 20 + 15-19 10-14 5-9 0-4 Dec15yrs+ /Fleet

O'bk /15yrs+

< 10,000 81% 3% 2% 6% 9% 314 12 6 22 36 390 84% 1%10,000+ 33% 20% 20% 13% 13% 5 3 3 2 2 15 53%

Total Specialised Tanker Fleet 79% 4% 2% 6% 9% 319 15 9 24 38 405 82% 1%