Embed Size (px)

Citation preview

Oil Market Outlook

Oslo, May 2017

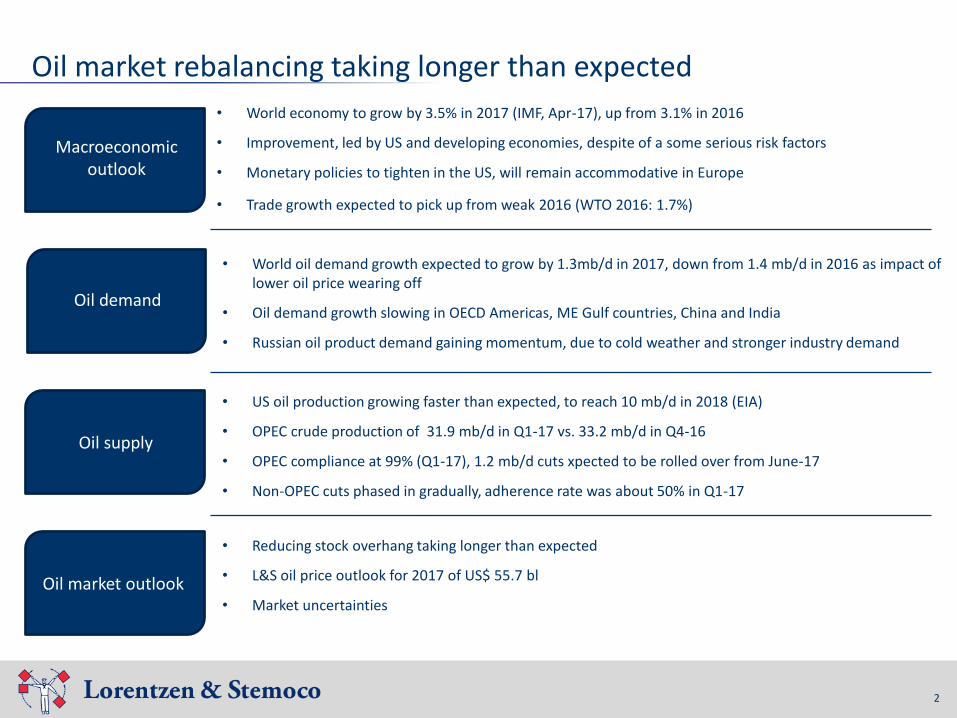

Oil market rebalancing taking longer than expected

2

• World oil demand growth expected to grow by 1.3mb/d in 2017, down from 1.4 mb/d in 2016 as impact of lower oil price wearing off

• Oil demand growth slowing in OECD Americas, ME Gulf countries, China and India

• Russian oil product demand gaining momentum, due to cold weather and stronger industry demand

• World economy to grow by 3.5% in 2017 (IMF, Apr-17), up from 3.1% in 2016

• Improvement, led by US and developing economies, despite of a some serious risk factors

• Monetary policies to tighten in the US, will remain accommodative in Europe

• Trade growth expected to pick up from weak 2016 (WTO 2016: 1.7%)

• US oil production growing faster than expected, to reach 10 mb/d in 2018 (EIA)

• OPEC crude production of 31.9 mb/d in Q1-17 vs. 33.2 mb/d in Q4-16

• OPEC compliance at 99% (Q1-17), 1.2 mb/d cuts xpected to be rolled over from June-17

• Non-OPEC cuts phased in gradually, adherence rate was about 50% in Q1-17

• Reducing stock overhang taking longer than expected

• L&S oil price outlook for 2017 of US$ 55.7 bl

• Market uncertainties

Oil market outlook

Oil supply

Oil demand

Macroeconomic outlook

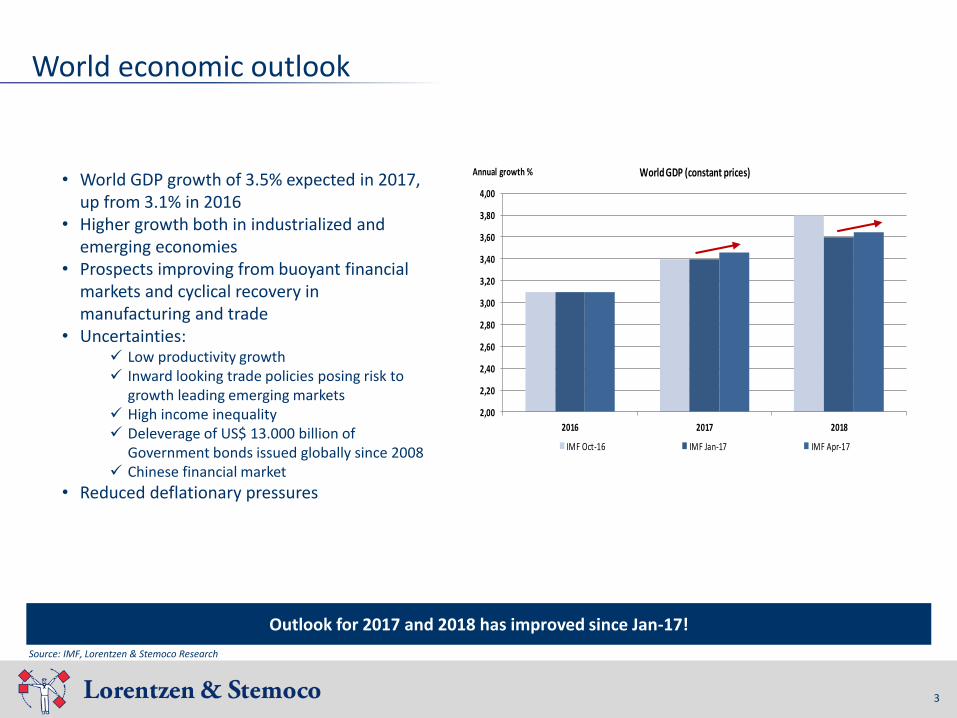

Outlook for 2017 and 2018 has improved since Jan-17!

3

World economic outlook

Source: IMF, Lorentzen & Stemoco Research

• World GDP growth of 3.5% expected in 2017, up from 3.1% in 2016

• Higher growth both in industrialized and emerging economies

• Prospects improving from buoyant financial markets and cyclical recovery in manufacturing and trade

• Uncertainties: ✓ Low productivity growth✓ Inward looking trade policies posing risk to

growth leading emerging markets✓ High income inequality✓ Deleverage of US$ 13.000 billion of

Government bonds issued globally since 2008✓ Chinese financial market

• Reduced deflationary pressures

2,00

2,20

2,40

2,60

2,80

3,00

3,20

3,40

3,60

3,80

4,00

2016 2017 2018

Annual growth %

IMF Oct-16 IMF Jan-17 IMF Apr-17

World GDP (constant prices)

Lorentzen & Stemoco

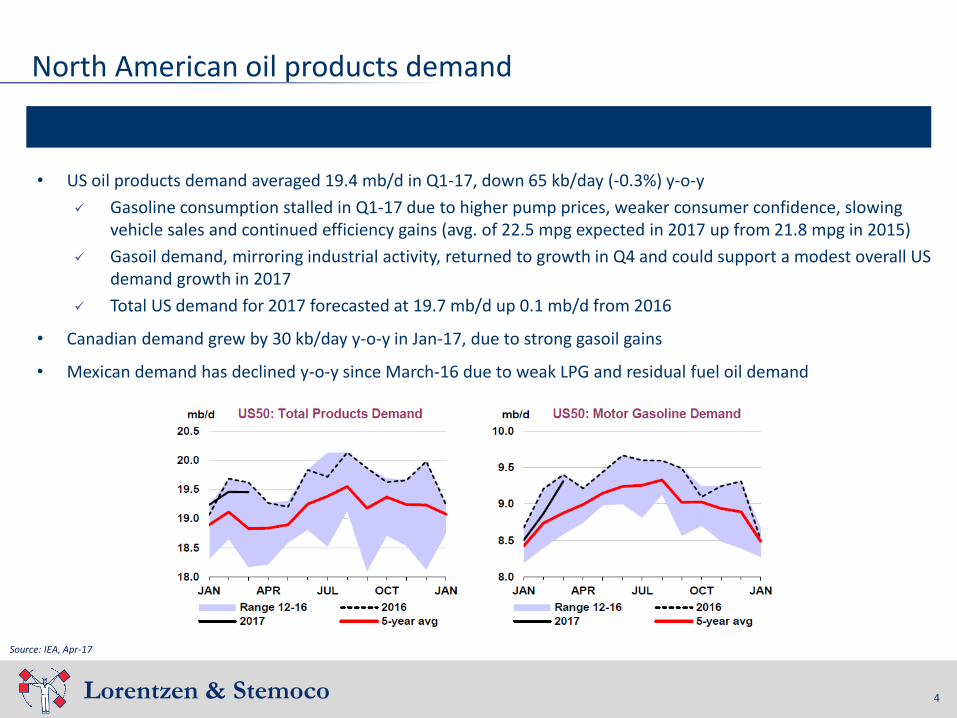

• US oil products demand averaged 19.4 mb/d in Q1-17, down 65 kb/day (-0.3%) y-o-y

✓ Gasoline consumption stalled in Q1-17 due to higher pump prices, weaker consumer confidence, slowing vehicle sales and continued efficiency gains (avg. of 22.5 mpg expected in 2017 up from 21.8 mpg in 2015)

✓ Gasoil demand, mirroring industrial activity, returned to growth in Q4 and could support a modest overall US demand growth in 2017

✓ Total US demand for 2017 forecasted at 19.7 mb/d up 0.1 mb/d from 2016

• Canadian demand grew by 30 kb/day y-o-y in Jan-17, due to strong gasoil gains

• Mexican demand has declined y-o-y since March-16 due to weak LPG and residual fuel oil demand

4

North American oil products demand

Source: IEA, Apr-17

5Lorentzen & Stemoco

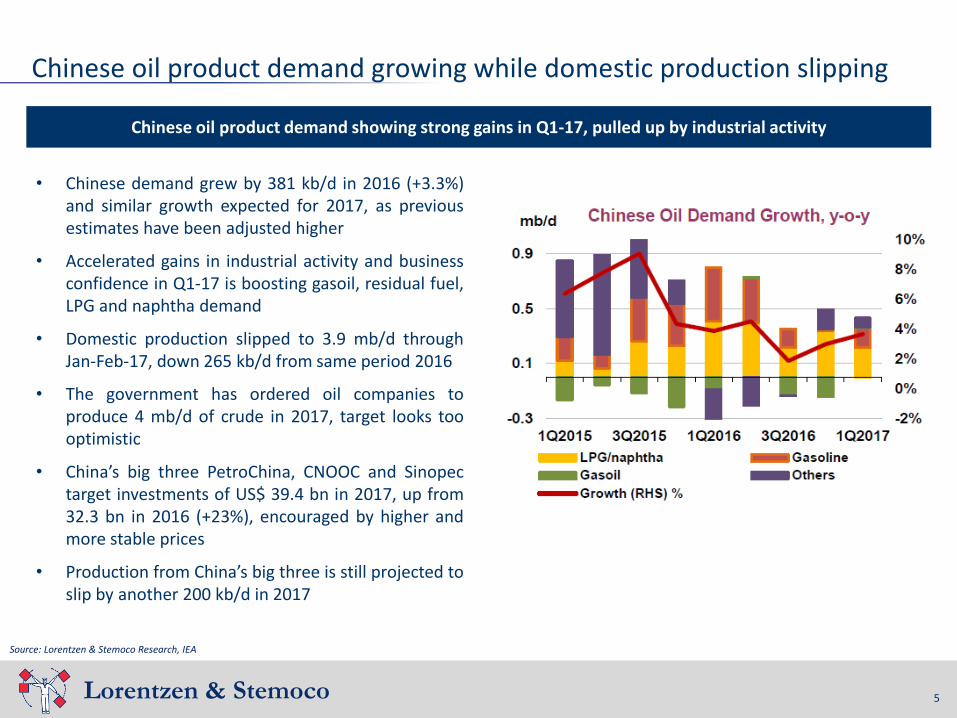

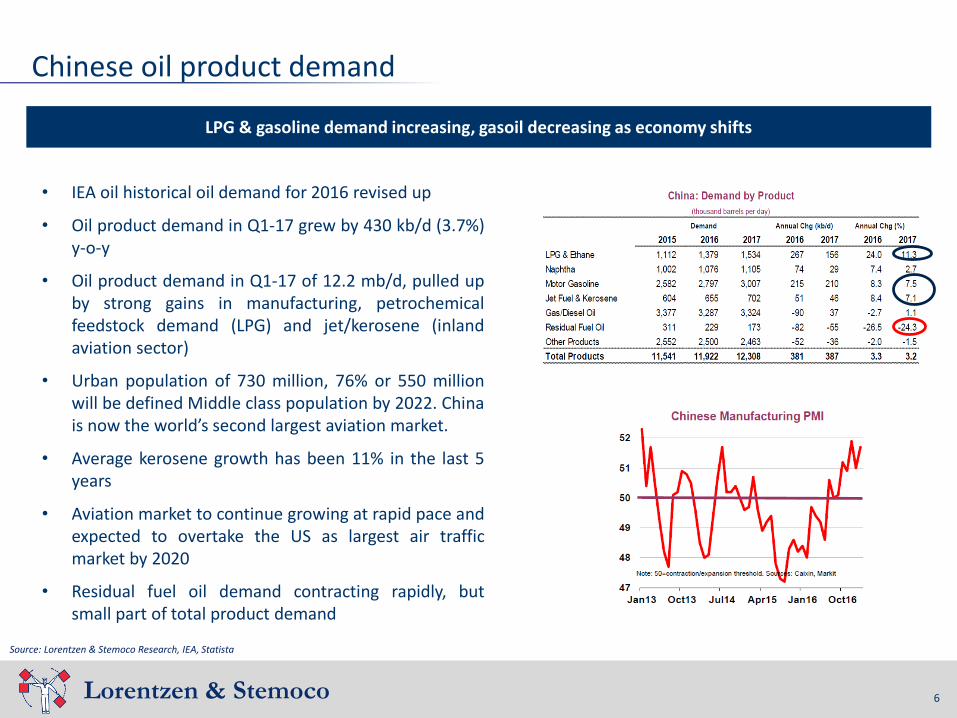

• Chinese demand grew by 381 kb/d in 2016 (+3.3%)and similar growth expected for 2017, as previousestimates have been adjusted higher

• Accelerated gains in industrial activity and businessconfidence in Q1-17 is boosting gasoil, residual fuel,LPG and naphtha demand

• Domestic production slipped to 3.9 mb/d throughJan-Feb-17, down 265 kb/d from same period 2016

• The government has ordered oil companies toproduce 4 mb/d of crude in 2017, target looks toooptimistic

• China’s big three PetroChina, CNOOC and Sinopectarget investments of US$ 39.4 bn in 2017, up from32.3 bn in 2016 (+23%), encouraged by higher andmore stable prices

• Production from China’s big three is still projected toslip by another 200 kb/d in 2017

5

Chinese oil product demand growing while domestic production slipping

Chinese oil product demand showing strong gains in Q1-17, pulled up by industrial activity

Source: Lorentzen & Stemoco Research, IEA

6Lorentzen & Stemoco 6

Chinese oil product demand

LPG & gasoline demand increasing, gasoil decreasing as economy shifts

Source: Lorentzen & Stemoco Research, IEA, Statista

• IEA oil historical oil demand for 2016 revised up

• Oil product demand in Q1-17 grew by 430 kb/d (3.7%)y-o-y

• Oil product demand in Q1-17 of 12.2 mb/d, pulled upby strong gains in manufacturing, petrochemicalfeedstock demand (LPG) and jet/kerosene (inlandaviation sector)

• Urban population of 730 million, 76% or 550 millionwill be defined Middle class population by 2022. Chinais now the world’s second largest aviation market.

• Average kerosene growth has been 11% in the last 5years

• Aviation market to continue growing at rapid pace andexpected to overtake the US as largest air trafficmarket by 2020

• Residual fuel oil demand contracting rapidly, butsmall part of total product demand

7Lorentzen & Stemoco

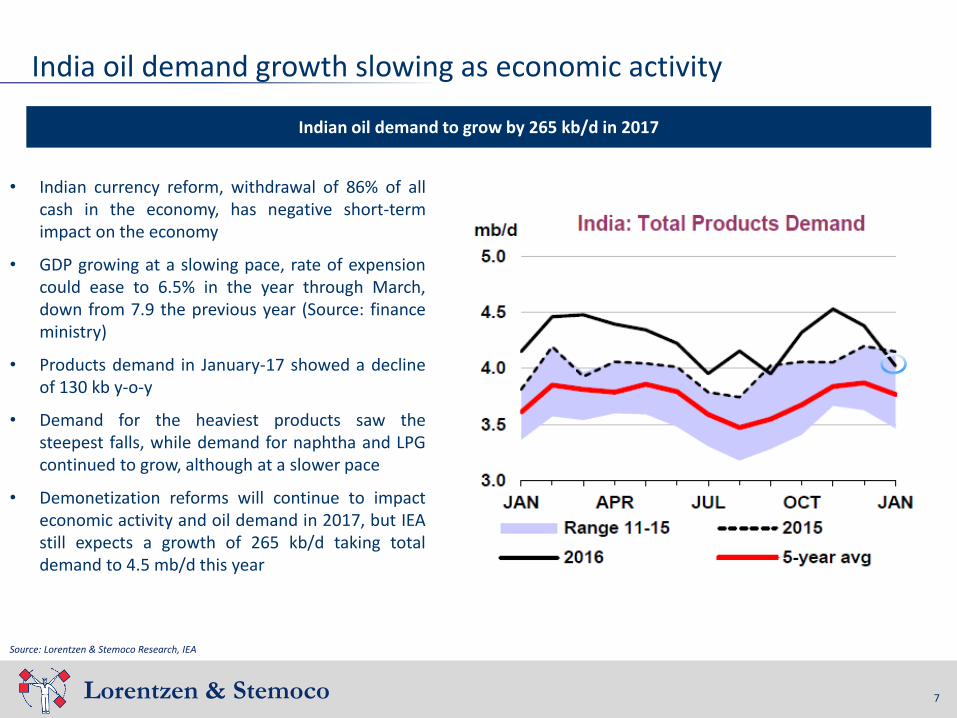

• Indian currency reform, withdrawal of 86% of allcash in the economy, has negative short-termimpact on the economy

• GDP growing at a slowing pace, rate of expensioncould ease to 6.5% in the year through March,down from 7.9 the previous year (Source: financeministry)

• Products demand in January-17 showed a declineof 130 kb y-o-y

• Demand for the heaviest products saw thesteepest falls, while demand for naphtha and LPGcontinued to grow, although at a slower pace

• Demonetization reforms will continue to impacteconomic activity and oil demand in 2017, but IEAstill expects a growth of 265 kb/d taking totaldemand to 4.5 mb/d this year

7

India oil demand growth slowing as economic activity

Indian oil demand to grow by 265 kb/d in 2017

Source: Lorentzen & Stemoco Research, IEA

OPEC & non-Opec country agreed production cuts

8

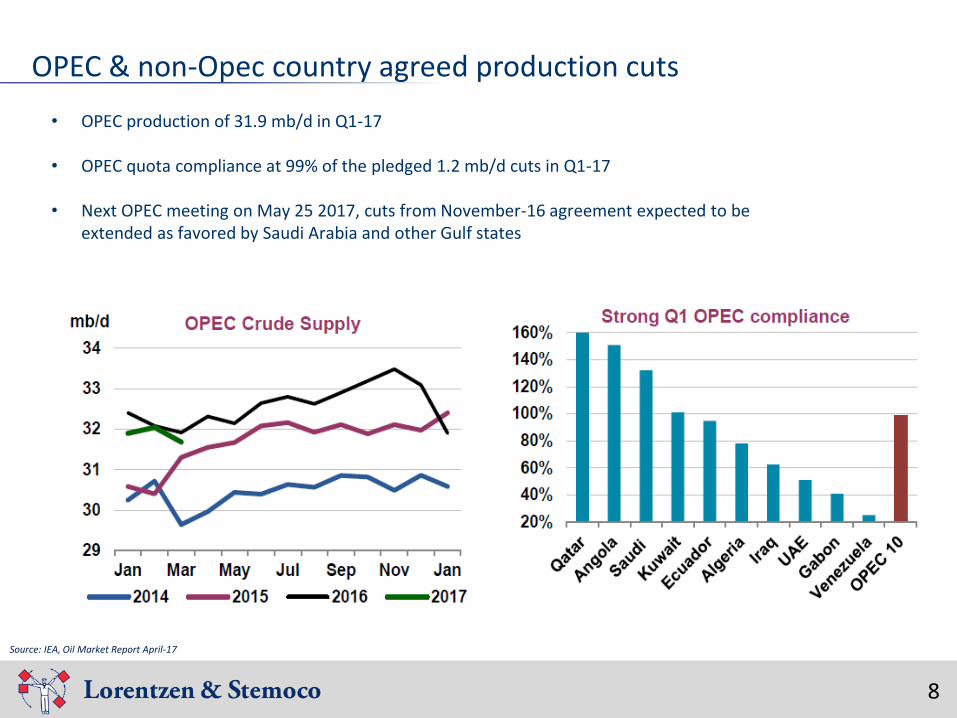

• OPEC production of 31.9 mb/d in Q1-17

• OPEC quota compliance at 99% of the pledged 1.2 mb/d cuts in Q1-17

• Next OPEC meeting on May 25 2017, cuts from November-16 agreement expected to be extended as favored by Saudi Arabia and other Gulf states

Source: IEA, Oil Market Report April-17

Non-OPEC crude supply commitments

9

Source: IEA Oil Market Report April-17

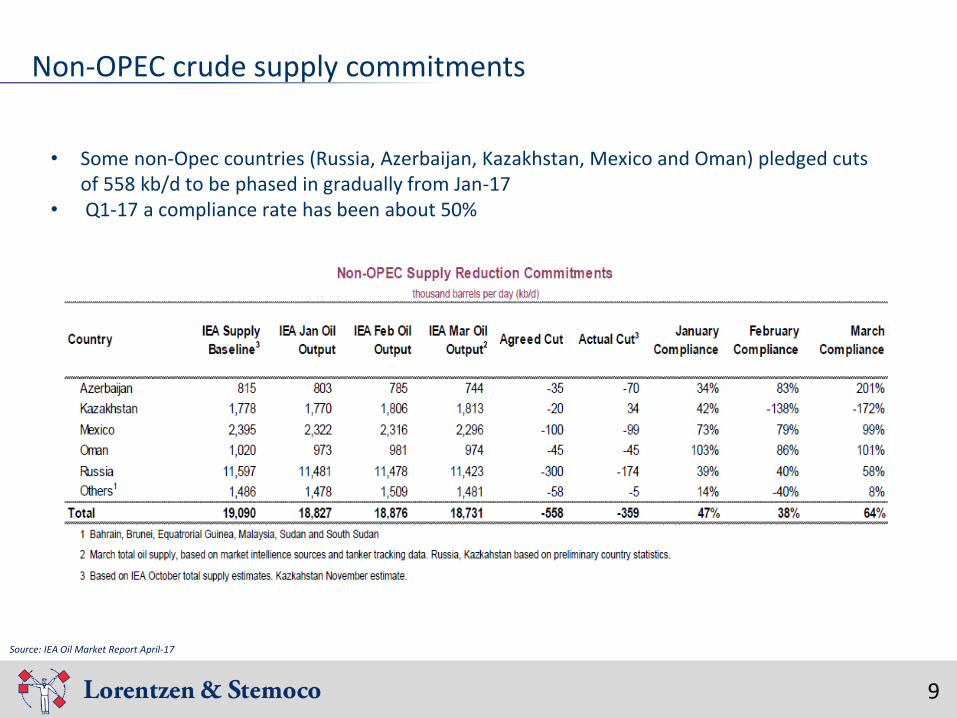

• Some non-Opec countries (Russia, Azerbaijan, Kazakhstan, Mexico and Oman) pledged cuts of 558 kb/d to be phased in gradually from Jan-17

• Q1-17 a compliance rate has been about 50%

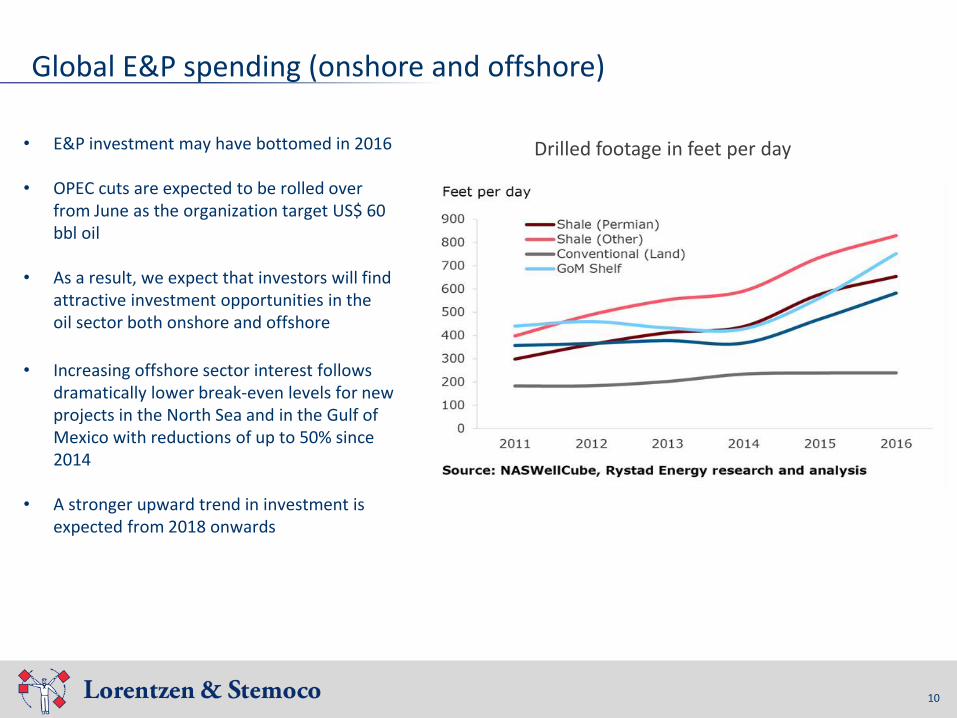

Global E&P spending (onshore and offshore)

10

• E&P investment may have bottomed in 2016

• OPEC cuts are expected to be rolled over from June as the organization target US$ 60 bbl oil

• As a result, we expect that investors will find attractive investment opportunities in the oil sector both onshore and offshore

• Increasing offshore sector interest follows dramatically lower break-even levels for new projects in the North Sea and in the Gulf of Mexico with reductions of up to 50% since 2014

• A stronger upward trend in investment is expected from 2018 onwards

Drilled footage in feet per day

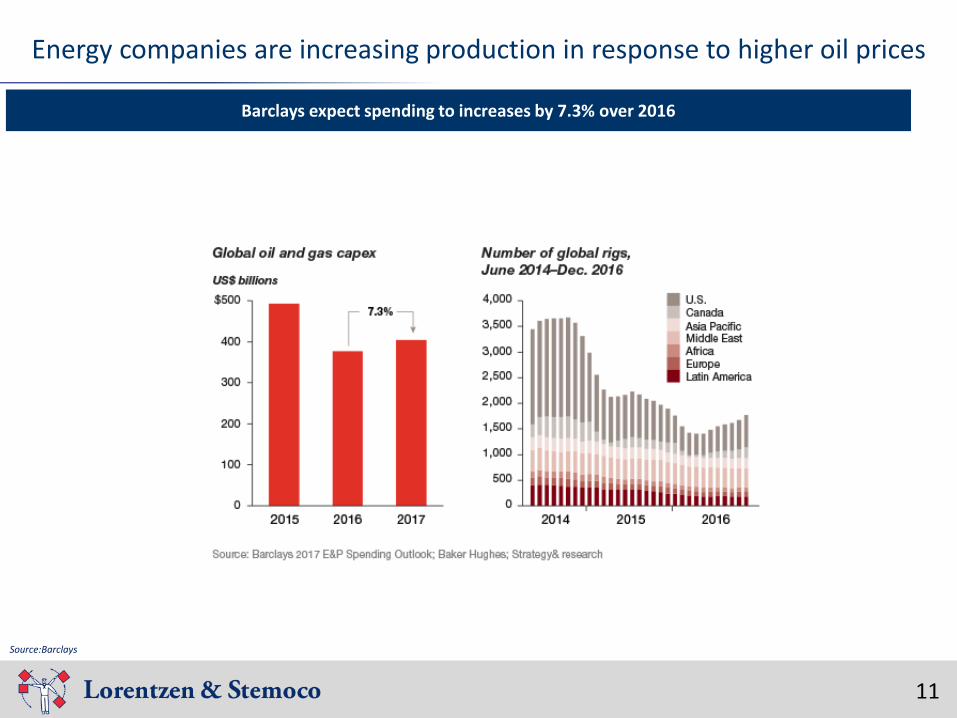

Energy companies are increasing production in response to higher oil prices

11

Source:Barclays

Barclays expect spending to increases by 7.3% over 2016

Lorentzen & Stemoco

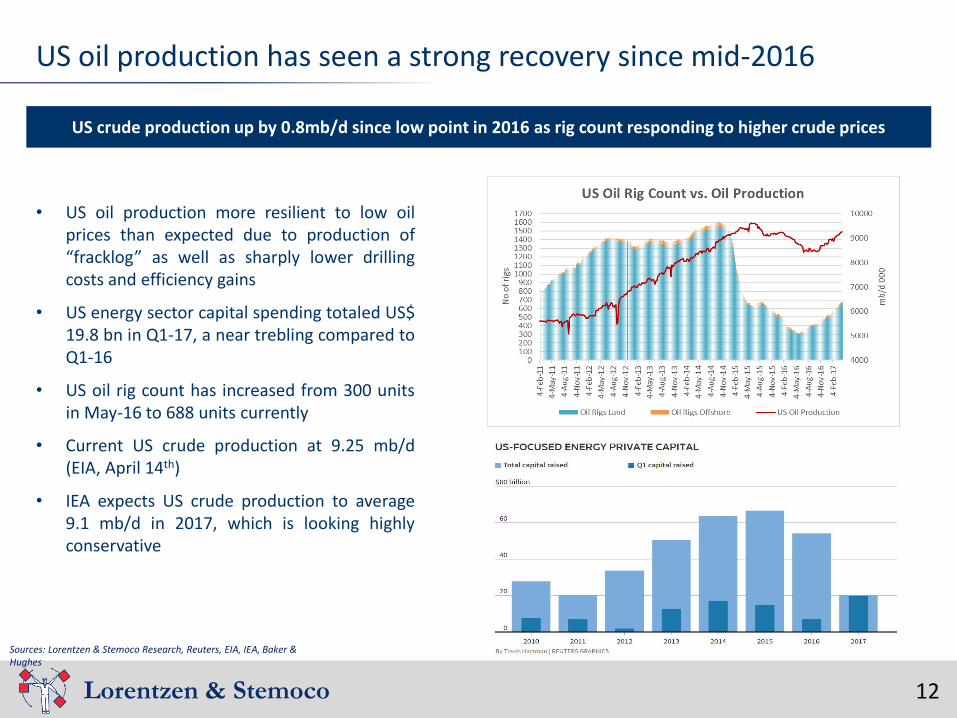

US crude production up by 0.8mb/d since low point in 2016 as rig count responding to higher crude prices

12

US oil production has seen a strong recovery since mid-2016

Sources: Lorentzen & Stemoco Research, Reuters, EIA, IEA, Baker &Hughes

• US oil production more resilient to low oilprices than expected due to production of“fracklog” as well as sharply lower drillingcosts and efficiency gains

• US energy sector capital spending totaled US$19.8 bn in Q1-17, a near trebling compared toQ1-16

• US oil rig count has increased from 300 unitsin May-16 to 688 units currently

• Current US crude production at 9.25 mb/d(EIA, April 14th)

• IEA expects US crude production to average9.1 mb/d in 2017, which is looking highlyconservative

Lorentzen & Stemoco

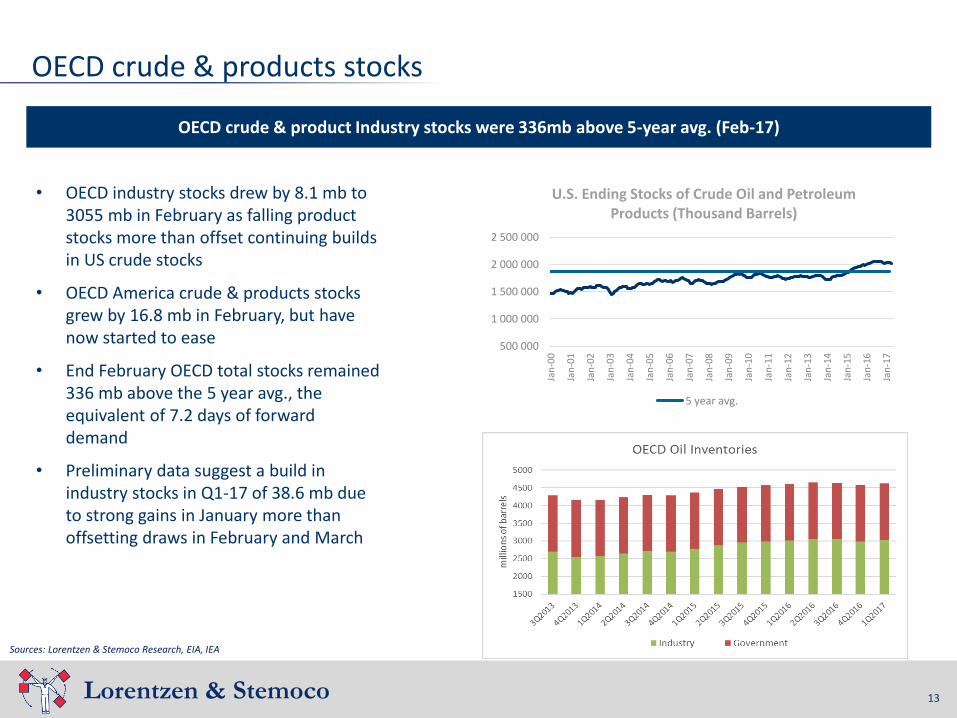

OECD crude & product Industry stocks were 336mb above 5-year avg. (Feb-17)

13

OECD crude & products stocks

• OECD industry stocks drew by 8.1 mb to 3055 mb in February as falling product stocks more than offset continuing builds in US crude stocks

• OECD America crude & products stocks grew by 16.8 mb in February, but have now started to ease

• End February OECD total stocks remained 336 mb above the 5 year avg., the equivalent of 7.2 days of forward demand

• Preliminary data suggest a build in industry stocks in Q1-17 of 38.6 mb due to strong gains in January more than offsetting draws in February and March

Sources: Lorentzen & Stemoco Research, EIA, IEA

500 000

1 000 000

1 500 000

2 000 000

2 500 000

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

U.S. Ending Stocks of Crude Oil and Petroleum Products (Thousand Barrels)

5 year avg.

Oil market outlook

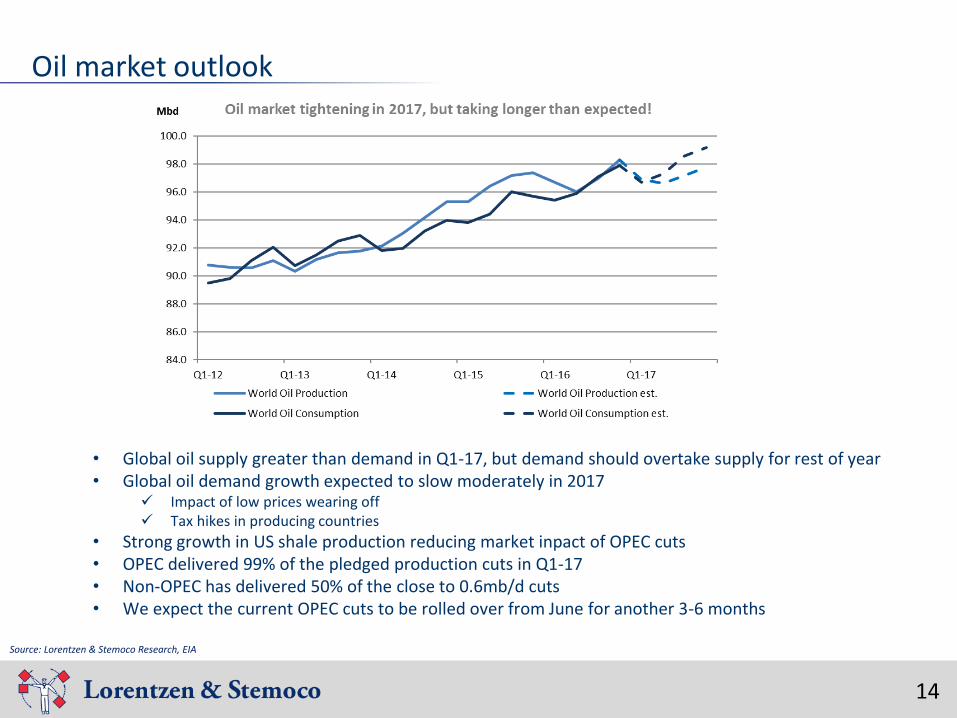

14

• Global oil supply greater than demand in Q1-17, but demand should overtake supply for rest of year• Global oil demand growth expected to slow moderately in 2017

✓ Impact of low prices wearing off✓ Tax hikes in producing countries

• Strong growth in US shale production reducing market inpact of OPEC cuts• OPEC delivered 99% of the pledged production cuts in Q1-17• Non-OPEC has delivered 50% of the close to 0.6mb/d cuts • We expect the current OPEC cuts to be rolled over from June for another 3-6 months

Source: Lorentzen & Stemoco Research, EIA

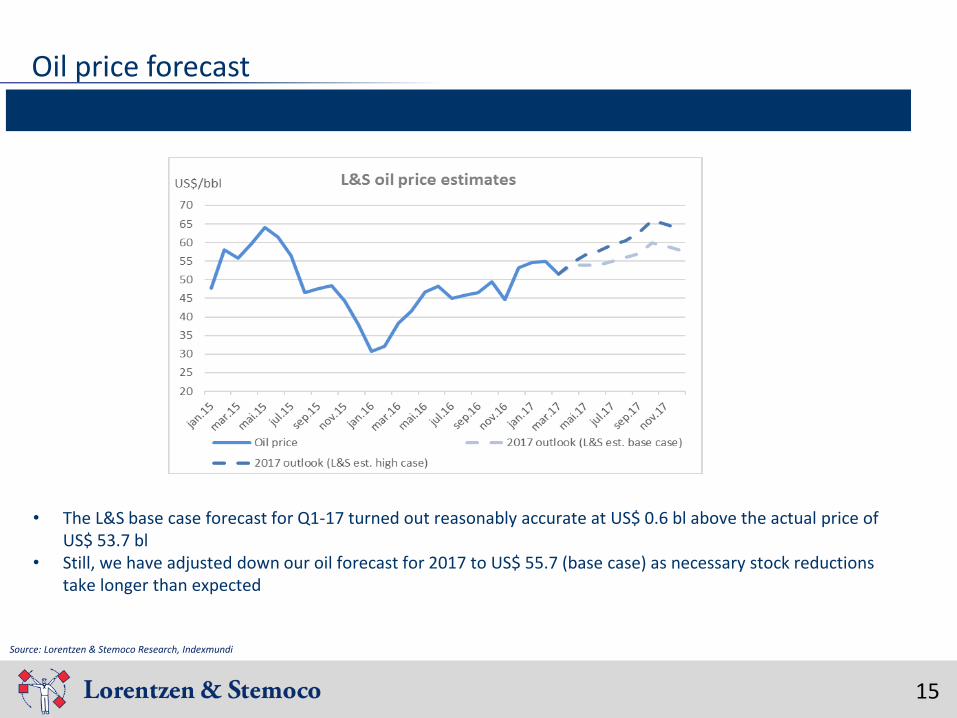

Oil price forecast

15

Source: Lorentzen & Stemoco Research, Indexmundi

• The L&S base case forecast for Q1-17 turned out reasonably accurate at US$ 0.6 bl above the actual price of US$ 53.7 bl

• Still, we have adjusted down our oil forecast for 2017 to US$ 55.7 (base case) as necessary stock reductions take longer than expected

16Lorentzen & Stemoco

2017:

• We expect the price of Brent Blend to average US$ 55.7 bbl (base case)

• Market uncertainties:

✓ Degree of OPEC and Non-OPEC continued adherence to announced production cuts

✓ Will OPEC and non-OPEC cuts be rolled forward from June?

✓ Pace of recovery in US shale production

✓ Oil stocks, when will inventories reduce to “normal” levels around the 5 year average

2017 onwards

• Cost of developing N. Sea offshore fields reduced by 50% since 2014

• Energy efficiency of world economy improving, slowing demand in high growth countries

• Environmental concerns slow down transportation sector demand (diesel ban/restrictions in large cities through substitution (LNG/CNG fuel, electric propulsion)

• Renewable energy (wind and solar) becoming profitable without subsidies at current oil prices

• Depletion rates of large fields masked by boost in production from many small fields

16

Oil market outlook summary

Slower pace of oil demand growth ahead!

Source: Lorentzen & Stemoco Research

This presentation is provided by Lorentzen & Stemoco AS or an affiliated company and has been prepared for information purposes only. This presentation is not a solicitation of any offer to buy or sell anysecurity, commodity or instrument or related derivative or to participate in any trading strategy. Any such offer would be made only after a prospective participant has completed its own independentinvestigation of the instrument or trading strategy and received all information it required to make its own investment decision, including, where applicable, a review of any prospectus, prospectus supplement,offering circular or memorandum describing such instrument or trading strategy (where such information would supersede this presentation, and to which prospective participants are referred).

This presentation is confidential, and may not be reproduced or distributed, in whole or in part, without the prior written consent of Lorentzen & Stemoco AS.

This presentation is based on information obtained from sources which Lorentzen & Stemoco AS believes to be reliable but Lorentzen & Stemoco AS does not represent or warrant its accuracy or completenessand disclaims any and all liability related thereto. Please note that all prices and special levels are indicative, and may not be up to the date specified in this presentation, while the opinions and estimatescontained herein represent the view as of the date of the presentation and may be subject to change without any prior notice.

Please note that past performance of a market, company or financial instrument is not necessarily a guide to future performance.

Estimates provided in this presentation are prepared by Lorentzen & Stemoco AS. Lorentzen & Stemoco AS expressively disclaim any and all liabilities for any and all losses related to investments caused by ormotivated by this presentation. Any person receiving this presentation is deemed to have accepted this disclaimer that shall apply even if the estimates or opinions shown turn out to be to erroneous orincomplete or is based upon incorrect or incomplete facts, interpretations or assessments or assumptions by Lorentzen & Stemoco AS, and irrespective of whether Lorentzen & Stemoco AS or any person relatedto Lorentzen & Stemoco AS can be blamed for the incident.

Lorentzen & Stemoco AS and/or its employees may have investments in companies/financial instruments featured in this presentation, and may elect to sell or buy additional financial instruments at any time.Lorentzen & Stemoco AS may also have other financial interests in transactions involving these companies/financial instruments. Lorentzen & Stemoco AS may have or has acted as advisor to, broker or managerfor a number companies mentioned in this presentation. For an overview of the companies to whom Lorentzen & Stemoco AS has provided advisory, brokering, consultancy or other services to over the latest 12months, please see contact Lorentzen & Stemoco AS and find the relevant department on www.lorstem.com

This presentation does not provide individually tailored investment advice or offer tax, regulatory, accounting or legal advice. The assets, securities, commodities or other instruments (or related derivatives)discussed in this presentation may not be suitable for all investors. This presentation has been prepared and issued for distribution to professional investors only and all recipients should seek independentinvestment advice prior to making any investment decision based on any information contained in this presentation. Prior to entering into any proposed transaction, recipients should determine, in consultationwith their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences, of the transaction.

Distribution in the United States

This presentation was prepared for information purposes only by Lorentzen & Stemoco AS, a foreign broker-dealer that is not registered in the United States. Lorentzen & Stemoco AS’ presentations areintended for distribution in the United States solely to "major U.S. institutional investors" in reliance on the exemption from broker-dealer registration provided by Rule 15a-6 of the United States SecuritiesExchange Act of 1934, as amended and may not be furnished to any other person in the United States. Each major U.S. institutional investor that receives a copy of a Lorentzen & Stemoco AS presentation by itsacceptance thereof represents and agrees that it shall not distribute or provide copies to any other person. Any U.S. recipient of presentation that desires to effect transactions in any securities discussed withinthis presentation should do so through Lorentzen & Stemoco AS and shall be advised on how to proceed through a U.S. registered broker-dealer.

Financial statements included in the presentation, if any, may have been prepared in accordance with non-U.S. accounting standards that may not be comparable to the financial statements of United Statescompanies. It may be difficult to compel a non-U.S. company and its affiliates to subject themselves to U.S. laws or the jurisdiction of U.S. courts.

This presentation is issued by Lorentzen & Stemoco AS. Lorentzen & Stemoco AS is a company established under the laws of Norway being licensed and supervised by Norwegian regulators, and all mattersrelating to this presentation shall be governed by the laws of Norway.

Disclaimer

17

Oslo (Head office)Lorentzen & Stemoco ASMunkedamsveien 45,0250 OsloNorway

Tel +47 2252 7700

AthensLorentzen & Stemoco (Athens) LtdLeof Karamanli 25166 73 VoulaGreece

Tel +30 210 89 000 59

SingaporeLorentzen & Stemoco Singapore8 Eu Tong Sen street,#21-98 Office 1 The Central059818 SingaporeSingapore

Tel +65 6349 8400

ShanghaiLorentzen & Stemoco Shanghai Representative OfficeRoom 2701, Shanghai Central Plaza381 Huai Hai Zhong Road200020 ShanghaiChina

Tel +86 21 6391 5880

LondonLorentzen & Stemoco UK Ltd5th Floor, Dacre House19 Dacre StreetLondon SW1H ODJEngland

Tel +44 20 7799 4444

Hong KongLorentzen & Stemoco (Greater China) Hong Kong LtdFlat A, 22F Sing Ho Finance Building166-168 Gloucester Road Wan HaiHong Kong

Tel +852 2530 2164

For more information on Lorentzen & Stemoco and our global representation visit us at Lorstem.com

New York CityLorentzen & Stemoco AS (USA)8 East 41st ST, 8th FloorNew York, NY 10017

Tel +1 212 684 2503

1818