-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

1/80

Oil CropsSituation and Outlook Yearbook

1970 73 76 79 82 85 88 91 94 97 20005

10

15

20

25

30

35

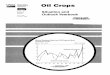

U.S. soybean oil prices sink to 30-year lowas surplus mounts

Cents/lb

Source: Economic Research Service, USDA.

United StatesDepartment ofAgriculture

EconomicResearch

Service

OCS-2001

October 2001

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

2/80

2 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

Oil Crops Situation and Outlook Yearbook. Market and Trade

Economics Division, Economic Research Service,

U.S. Department of Agriculture, October 2001, OCS-2001.

Contents

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . .3

U.S. Soybean Situation, 2001/02 . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . .4

World Oilseed and Protein Meal Situation . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . .6

World Vegetable Oil Situation . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . .10

Situation for Other U.S. Oil Crops . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .12

Cottonseed . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . .12

Peanuts . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . .12

Sunflowerseed . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . .13

Other Minor Oilseeds . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . .13

Other Fats and Oils Highlights . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .15

Special Articles

Soybean Production Costs and Export Competitiveness in the

United States,

Brazil, and Argentina . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . .16

Estimating Farm-Level Effects of Adopting Herbicide-Tolerant

Soybeans . . . . .25

List of Tables . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . .35

Report Coordinator

Mark Ash

(202) 694-5289

E-mail: [email protected]

Principal Contributors

Mark Ash (202) 694-5289 (Soybeans, Vegetable Oils)

Erik Dohlman (202) 694-5308 (Peanuts)

Mae Dean Johnson (202) 694-5299 (Statistics)

Editor

Martha R. Evans

Graphics, Table Design & Layout

Wynnice Pointer-Napper

Approved by the World Agricultural Outlook Board.

Summary released October 24, 2001. Summaries and full

text of Situation and Outlook reports may be accessed elec-

tronically via the ERS website at www.ers.usda.gov/.

To order, call 1-800-999-6779 in the United States or

Canada. Other areas please call (703) 605-6220. Or write

ERS-NASS, 5285 Port Royal Road, Springfield, VA 22161.

The U.S. Department of Agriculture (USDA) prohibits

discrimination in all its programs and activities on the basis of

race, color, national origin, sex, reli-gion, age, disability,

political beliefs, sexual orientation, or marital or family status.

(Not all prohibited bases apply to all programs). Persons with

disabilitieswho require alternative means for communication of

program information (braille, large print, audiotape, etc.) should

contact USDAs TARGET Center at(202) 720-2600 (voice and TDD).To

file a complaint of discrimination, write USDA, Director, Office of

Civil Rights, Room 326-W, Whitten Building, 14th and Independence

Avenue, SW,Washington, DC 20250-9410 or call (202) 720-5964 (voice

and TDD). USDA is an equal opportunity provider and employer.

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

3/80

Based largely on a record harvested area of 72.4 million

acres, U.S. soybean production in 2000 increased 104 mil-

lion bushels to a record 2,758 million bushels. With

stronger

demand for soybean meal in 2000/01, domestic soybean

crushing climbed to a record 1,641 million bushels from

1,578 million the previous year. The lowest prices in 3

decades and the rapid pace of Chinas soybean imports

helped lift foreign demand for U.S. exports in 2000/01 to

998 million bushels, surpassing the 1999/2000 record of 973

million. Consequently, record use of soybeans reduced U.S.

ending stocks to 248 million bushels from 290 million in

1999/2000. The 2000/01 U.S. average farm price was $4.55

per bushel compared with $4.63 the previous season.

Brisk soybean meal sales, particularly to the European

Union (EU), Indonesia, Egypt, and South Korea, helped

expand U.S. meal exports in 2000/01 to 7.6 million short

tons. Gradually improving livestock-price-to-feed-cost rela-

tionships expanded 2000/01 domestic disappearance of soy-bean

meal by 5 percent to 31.7 million tons. Despite a

bumper South American soybean harvest, relatively weak

growth in their output and exports of soybean meal helped

support the U.S. season-average price at $173.60 per ton.

A higher soybean crush pace in 2000/01 produced a record

U.S. soybean oil output of 18,433 million pounds. Low soy-

bean oil prices helped support steady growth in domestic

disappearance of soybean oil to 16,222 million pounds from

16,056 million in 1999/2000. However, estimated U.S.

exports only edged up to 1,402 million pounds from 1,376

million in 1999/2000. The large carryover and record output

raised stocks throughout the year, which had swelled to arecord

2,877 million pounds by September 30. The supply

glut depressed soybean oil prices in 2000/01 (averaging

14.15 cents per pound) to their lowest level in 30 years.

Virtually all of the increase in world oilseed production in

2000/01 was due to an 8-percent rise in global soybean pro-

duction to 173.4 million metric tons, which derived from a

record area in the United States and an almost ideal growing

season in South America. The growth in Chinas domestic

supplies was far exceeded by its import needs, which

swelled from 10.5 million to 13.2 million tons. Chinas

domestic consumption of soybean meal surged 19 percent to

nearly 15 million tons. And after the European Unionbanned the

use of meat and bone meal in all livestock feeds,

EU soybean imports expanded from 15.7 million to 18.4

million tons in 2000/01 and soybean meal imports rose from

19.8 million to 20.3 million tons. Despite strong consump-

tion growth, global ending stocks of soybeans rose to a

record 28.3 million tons.

Global output of soybean oil totaled 26.8 million tons, up

2 million tons from 1999/2000. However, world trade

expanded just 0.5 million tons to 7.8 million tons in spite

of

a large increase in Indian soybean oil imports. Indian soy-

bean oil imports increased from 0.8 million to 1.4 million

tons in 2000/01 because of poor domestic oilseed harvests,

strengthening consumption, and higher import tariffs on

competing vegetable oils. A moderating influence on global

soybean oil trade was the huge increase of Chinas domestic

production, which sharply curtailed its 2000/01 soybean oil

imports to just 80,000 tons from 1999/2000 imports of

556,000 tons.

A severe drought caused poor U.S. cotton yields and sub-

stantial area abandonment in 2000, resulting in only a

slight

increase in cottonseed output to 6.4 million short tons.

Weak

prices for cottonseed oil diminished crushing margins for

cottonseed, reducing crush to 2.7 million tons in 2000/01

from 3.1 million in 1999/2000. But, consumption of cotton-

seed in livestock feed and planting seed increased 7 percent

to 3.75 million tons. Firmer feed prices generally supportedthe

2000/01 average cottonseed price at $106 per ton.

U.S. peanut production fell sharply in 2000, down 563 mil-

lion pounds to 3,266 million. Although national plantings

were up slightly, extremely dry conditions in many areas of

the Southwest (New Mexico, Oklahoma, and Texas) during

the growing season raised abandonment and cut national

harvested acreage to 1.32 million acres, down 8 percent

from 1999. As in 1999, poor weather also cut the 2000 aver-

age peanut yield, which fell to 2,444 pounds per harvested

acre, down 223 pounds per acre (8 percent) from 1999, and

the lowest yield since 1995. Domestic food use of peanuts

weakened in 2000/01, falling to 2,170 million pounds from2,233

million in 1999/2000. Ample foreign harvests and a

tighter available U.S. supply reduced U.S. peanut exports to

520 million pounds from 727 million in 1999/2000, and the

smallest since 1980/81.

U.S. sunflower harvested acreage in 2000 fell to 2.6 million

acres, down nearly one-fourth from 1999. Domestic sun-

flowerseed production in 2000 was 3,544 million pounds,

down from the previous years 4,342 million. Sluggish

European demand curtailed 2000/01 oil-type sunflowerseed

exports to just 45 million pounds. In contrast, U.S. confec-

tionery seed exports increased (to the EU in particular) to

a

record 400 million pounds, in spite of a shorter domesticsupply.

But estimated sunflowerseed oil exports, which

make up the majority of crushers sales, fell again in

2000/01 to 554 million pounds. Very low soybean oil prices

pressured U.S. season-average prices for sunflowerseed and

sunflowerseed oil to $6.80 per hundredweight and 16.2

cents per pound, near historic lows.

Economic Research Service/USDA Oil Crops Situation and

Outlook/OCS-2001/October 2001 n 3

Summary

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

4/80

Despite Strong U.S. Soybean Demand, HugeForeign Crops Squelch

2000/01 Prices

U.S. farmers planted a record 74.3 million acres of soybeans

in 2000, up 1 percent from 1999. Stronger corn prices and

optimal planting conditions in the spring limited the expan-

sion of soybean area, and plantings were 605,000 acres lessthan

farmers March intentions. Nearly all of the expansion

was in the Northern Plains and Lake States, where crop

rotations are still adjusting to incorporate more soybeans.

Farmers in Minnesota, Michigan, Wisconsin, Nebraska,

Kansas, South Dakota, and North Dakota each set State

records for soybean planting.

In the spring of 2000, warm and firm soils advanced U.S.

soybean planting well ahead of average. Throughout the

eastern Corn Belt, relatively mild temperatures and regular

precipitation early in the summer ensued, generating soy-

bean yields that neared or equaled records. However, on the

western and southern edges of the soybean belt,

soybeansstruggled through one of the hottest and driest summers

of

the last century. The worst yield damage occurred in

Kansas, Nebraska, and the lower Mississippi River Valley.

Although the national soybean yield improved from 36.6 to

38.1 bushels per acre, it was still suppressed well below

the

trend. Based largely on a record harvested area of 72.4 mil-

lion acres, U.S. soybean production in 2000 increased 104

million bushels to a record 2,758 million bushels. However,

lower beginning stocks raised total supplies just 45 million

bushels from 1999/2000.

After economic difficulties closed several U.S. crushingmills in

2000 (causing a 6-percent reduction in operating

capacity), soybean processing margins generally improved.

And, with stronger demand for soybean meal in 2000/01,

domestic soybean crushing climbed to a record 1,641 mil-

lion bushels from 1,578 million the previous year. The rapid

pace of Chinas soybean imports helped lift foreign demand

for U.S. exports in 2000/01 to 998 million bushels, surpass-

ing the 1999/2000 record of 973 million.

Consequently, U.S. ending stocks of soybeans fell to 248

million bushels from 290 million in 1999/2000. Yet, this

expansion of the demand base was possible only with the

lowest soybean prices in three decades. The 2000/01 U.S.average

farm price was $4.55 per bushel compared with

$4.63 the previous season. To supplement their cash receipts

from crop year 2000 soybeans, U.S. producers received

$2.54 billion of marketing loan benefits (averaging 93 cents

per bushel) on 2,730 million bushels. Producers also

received additional income in crop year 2000 from Oilseed

Program payments.

In June 2000, the government authorized $500 million in

Oilseed Program payments for producers of 2000-crop soy-

beans and minor oilseeds (Public Law 106-224). Payments

from this authorization were made to producers in February

2001. In August 2001, as part of an emergency package to

provide market loss assistance for the 2001 crop, the gov-

ernment authorized an additional $423.5 million for supple-

mental Oilseed Program payments (Public Law 107-25).

Soybean producers received $475 million in February pay-

ments and $404 million in August supplemental payments.

Strong Meal Demand Spurs Crushing

A record 39.4 million short tons of soybean meal was pro-

duced in 2000/01 because of a robust demand situation.

Domestic consumption of soybean meal grew solidly, as

livestock-price-to-feed-cost relationships gradually

improved. U.S. hog slaughter rates slowed and import

restrictions on EU pork exports favored U.S. exports. Thus,

hog prices rallied by about one-third between fall 2000

andspring 2001. In addition, soybean meal use increased

because of a very cold winter and a substantial drop in

wheat supplies that limited summer wheat feeding. As hog

slaughter rates slowed, higher feeding rates contributed to

a

5-percent expansion of U.S. soybean meal disappearance for

2000/01 to 31.7 million tons.

Brisk soybean meal sales, particularly to the European

Union (EU), Indonesia, Egypt, and South Korea, helped

expand U.S. exports in 2000/01 to 7.6 million short tons. A

shortage of protein feeds following the 6-month EU ban on

meat and bone meal boosted European soybean meal

demand. EU agriculture ministers subsequently agreed toextend

the ban beyond its original June 30 expiration. The

EU also prohibited meat and bone meal exports, of which

Indonesia had formerly been a major importer. U.S. soy-

beann meal exports also benefited from an Indonesian ban

on imports from South America, India, and China, which

was attributed to fears of transmitting the foot and mouth

disease that was present in those countries.

Central Illinois prices for high-protein soybean meal surged

from an October 2000 average of $171.50 per short ton to a

December peak of $196. But by the first quarter of 2001,

large expected South American crops and an uncertain out-

look for feed demand in Europe (due to incidences of foot

and mouth disease in several countries) weighed on prices.

Prices slid to $156 per short ton in March, the lowest level

since December 1999. Yet steady demand growth re-emerged

later in the spring and the seasonal crush decline prompted

a

recovery in soybean meal prices. For the entire 2000/01 sea-

son, the average U.S. price was $173.60 per ton. Despite

bumper South American soybean harvests, relatively weak

growth in their soybean meal output also supported prices.

4 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

U.S. Soybean Situation, 2001/02

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

5/80

Poor Soybean Oil Exports Swell Stocks,Prices Plunge

In contrast to the strength of the soybean meal market, weak

soybean oil demand limited the expansion of soybean crush-

ing. The share of soybean oil to total processing value fell

to

an all-time low of 27 percent in 2000/01. Despite a higher

crush pace in 2000/01, a lower oil extraction rate limited

growth in soybean oil output to 18,433 million pounds com-

pared with 17,825 million in 1999/2000. With very low oilprices,

soybean processors sacrificed maximum oil yields to

accelerate delivery of the more profitable meal to its

buyers.

Estimated domestic disappearance of soybean oil rose

steadily to 16,222 million pounds from 16,057 million in

1999/2000.

In spite of the low soybean oil prices, export gains were

hard to make. U.S. exports of soybean oil increased to

Canada, India, Pakistan, and North Africa but were offset by

sharp declines to China, Mexico, Turkey, and South Korea.

Total exports did not revive until near the end of the

season,

only edging up to 1,402 million pounds from 1,376 million

in 1999/2000. The large carryover and record output raised

stocks throughout the year, which had swelled to a record

2,877 million pounds by September 30.

The supply glut depressed soybean oil prices to their

lowestlevel in 30 years, averaging 14.15 cents per pound in

2000/01. Soybean oil prices bottomed out at 12.4 cents in

February 2001, which was 2.7 cents below February 2000.

By the summer, a seasonal weakening of the crush pace,

lower than expected soybean stocks, declining prospects for

2001 soybean production, and a strengthening of world

palm oil prices buoyed the value of soybean oil again.

Economic Research Service/USDA Oil Crops Situation and

Outlook/OCS-2001/October 2001 n 5

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

6/80

Global Soybean Output and Trade Surges

World oilseed production in 2000/01 increased 2 percent to

311 million metric tons. Virtually all of the increase was

due to an 8-percent rise in global soybean production to

173.4 million tons. The increase in soybean production

derived from a record area in the United States and analmost

ideal growing season in South America. Despite

growth in consumption, global ending stocks of soybeans

rose to a record 28.3 million tons. Although U.S. soybean

stocks declined, they were offset by an accumulation in

Argentina and China, which kept the pressure on world

prices. China was the worlds leading soybean importer in

2000/01, which alone accounted for 42 percent of the 7.4-

million-ton growth in world soybean imports. In contrast,

world soybean meal imports were up only 2 percent in

2000/01, as stronger European meal imports were partly

offset by lower Asian imports.

In Brazil, a shortage of corn supplies strengthened prices

rela-tive to soybeans, encouraging substantial interest in

domestic

corn production. Cotton area also increased. The December

rally in soybean prices came too late to permit a larger

expan-

sion of Brazilian area, so they only edged up 3 percent to

14.0

million hectares. Soybean planting began considerably

earlier

in 2000 than a year earlier when dry weather delayed

progress. Generous rainfall was very favorable for soybeans

in the major producing areas of the south and center-west,

although drought cut yields in the northern states. Based on

slight increases in area and yield, Brazils 2001 soybean

har-

vest grew to a record 38.4 million metric tons.

Between January and September 2001, Brazils exchange

rate depreciated about one-third, which made its crushers

exports more competitive against Argentinas, whose peso

was pegged to a strong U.S. dollar. A recovery in yields in

the three southernmost states also aided the crushing indus-

try, as nearly 60 percent of processing capacity is concen-

trated there. Yet, because of limited foreign demand for

soybean meal, Brazils 2000/01 soybean meal exports only

edged up to 10.25 million tons. In addition, on June 1 the

government began a program to ration Brazilian electrical

power use by up to 20 percent. Hydroelectric utilities pro-

duce 90 percent of Brazils electricity, and drought

critically

depleted the main reservoir levels. Operations by

domesticsoybean processors in the affected areas were disrupted

and

the 2000/01 crush rose only modestly to 22.2 million tons.

A weak economy slowed domestic soybean meal consump-

tion to 7.3 million tons from 7.2 million in 1999/2000.

With a soybean carryover slightly larger than the previous

season, greater supply availability helped boost Brazilian

exports to a record 15.0 million tons in 2000/01. In spite

of

higher demand, Brazils soybean stocks ending September

2001 remained at a relatively high 7.4 million tons, which

exceeded the stocks held in the United States. Some

Brazilian farmers held off marketing their new crop in

antic-

ipation of further weakening of the exchange rate and

weather problems in the United States.

A bumper Argentine soybean crop was possible in 2000/01

because of a reduction in sunflower area. Also, the rise in

soybean prices during planting encouraged more double

cropping after winter wheat, swelling total harvested area

by

20 percent to 10.3 million hectares. Abundant March-April

rains also helped produce excellent yields. Argentine soy-

bean farmers produced a record harvest of 26.7 million tons

in 2000/01, compared with 21.2 million a year earlier. By

itself, Argentina accounted for 41 percent of the worlds

expansion of soybean production in 2000/01.

However, Argentinas 2000/01 soybean crushing still only

edged up to 17.5 million tons from 17.1 million the

previousyear. Processing declined sharply between October 2000

and

April 2001, but accelerated somewhat in May-September

2001 following the newly harvested crop. Despite strong

European demand, Argentine processors were hurt by their

exclusion from Indonesian purchases. Indonesia temporarily

implemented a ban on purchases from countries where foot

and mouth disease was present. The disease was confirmed

in Argentina in March 2001. Argentine soybean meal pro-

duction in 2000/01 was limited by a slower crush pace, and

meal exports increased only slightly to 14 million tons.

Conversely, with much of current world demand being pro-

pelled by Chinas soybean imports, Argentine soybean

exports surged to 7.45 million tons.

Paraguays soybean-producing region experienced excellent

growing conditions in 2001, similar to the neighboring

areas of southern Brazil. Paraguayan rainfall was above

normal in January-February, and relatively dry weather

during March generally favored soybean harvesting.

Paraguays 2001 soybean production was a record 3.4 mil-

lion tons from a harvested area of 1.25 million hectares.

Consequently, Paraguay expanded its 2000/01 soybean

exports to 2.5 million tons.

Indias soybean harvest dropped again in 2000 to 5.25

million tons because of a weak start and early retreat of

thesummer monsoon. The shortage reduced Indian soybean

meal exports 300,000 tons in 2000/01 to 2.05 million.

Soybean meal exports were also slowed after late January

2001 by a severe earthquake in western India that damaged

the port of Kandla, which ships about two-thirds of Indias

exports. Meal stocks were stranded at the port and it took

several months to fully restore operating capacity. While

some deliveries of soybean meal were rerouted through other

ports, the disruption forced some crushers to temporarily

6 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

World Oilseed and Protein Meal Situation

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

7/80

shut down. The lack of a good conduit for exports reduced

soybean meal prices and encouraged an increase in domestic

meal consumption to 1.5 million tons.

In China, comparatively stronger prices in 2000 shifted

another 1.3 million hectares of farmland into soybean pro-

duction, mostly in lieu of corn. Drought cut yields in

north-

ern China and moderated the gain in domestic output from

14.3 million tons to 15.4 million. Yet, the growth in

Chinasdomestic supplies was far exceeded by its import needs,

which swelled from 10.5 million tons to 13.2 million.

Domestic consumption of soybean meal surged 19 percent

to nearly 15 million tons.

By early 2002, Chinas entry into the World Trade

Organization (WTO) will begin to reduce import barriers for

oilseed products. But during 2001, Chinas accession to the

WTO stalled pending resolution of several outstanding

issues. China subsequently agreed to limit its agricultural

subsidies to 8.5 percent of the value of agricultural

produc-

tion, which settled one of the last hurdles to WTO acces-

sion. However, the delay in implementing lower oilseedproduct

tariffs helped preserve crush margins for Chinas

soybean processors. As world soybean meal prices and

domestic consumption strengthened, Chinas 2000/01 soy-

bean crush soared 25 percent to 18.9 million tons. As a con-

sequence, soybean meal imports (most of which came from

India) were very slow, totaling just 125,000 tons compared

with 633,000 in 1999/2000.

Despite the rapid consumption rate, many of the higher soy-

bean imports added to Chinas ending stocks, which increased

to an estimated 4.9 million tons. Chinese buyers may have

desired larger stocks because a smaller 2001 soybean area

and a spring drought in northern China threatened the poten-tial

of the domestic 2001 crop. Soybean purchases may also

have been advanced by uncertainty about how Chinas

Government would ultimately administer new regulations on

imports of biotech crops. International prices and interest

rates were low, and Chinese storage capacity was abundant.

Late last year, the European feed market was thrown into

turmoil by new cases of bovine spongiform encephalopathy,

popularly known as mad cow disease. The spread of this

disease has been linked to the inclusion of infected tissues

in meat meal used in cattle feed. Scientists believe it is

pos-

sible that consuming infected beef can transmit a similarly

fatal, brain-damaging disease to humans. The crisis caused

EU beef sales to collapse. Among the measures taken by the

EU Farm Commission to limit the diseases spread and

restore consumer confidence in the safety of consuming

beef, was adopting a ban on the use of meat meal in all

live-

stock feeds.

The resulting protein meal deficit in Western Europe had to

be managed through imports. Climate limits the feasible

area that soybeans can be grown in Europe, and EU oilseeds

production for 2000 had already dropped by 14 percent. The

major beneficiary of the meat meal ban was soybean meal

consumption, which increased 4 percent in 2000/01 com-

pared with a 7-percent decline the previous year. The rela-

tive protein content of soybean meal compared to meat meal

helped drive this growth in consumption. Meat meal has a

high protein content (50-55 percent) compared with soybean

meal (44-48 percent). Another alternative was fish meal,

which was excluded from the overall ban, but is stillrestricted

in ruminant feeds.

During fall and winter, stronger soybean meal prices in

Rotterdam favored soybean imports from the United States.

The oil supplies generated by crushing soybean imports also

better compensated for the loss of fat supplies available

for

feed and food applications. Both France and Germany

restricted use of beef tallow in livestock feeds. Price

slip-

page in the spring accelerated soybean meal imports from

South America. EU soybean imports expanded from 15.7

million tons to 18.4 million in 2000/01, while soybean meal

imports rose from 19.8 million tons to 20.3 million. The EU

meat meal ban was countered throughout 2001 by the rela-tive

weakness of the euro. EU feed compounders have been

encouraged to substitute more dollar-denominated imports

of soybeans and soybean meal with domestically produced

grains, as reforms of the EUs Common Agricultural Policy

allowed internal grain prices to decline further.

The EU also prohibited exports of EU meat meal to prevent

their inclusion in feeds in Eastern Europe and elsewhere.

With trade exceeding 500,000 tons per year, the EU was for-

merly the worlds largest exporter of meat and bone meal.

But many countries, even after the EU export ban, prohib-

ited imports of meat and bone meal from any country,

regardless of origin. One major market to do this wasPoland,

which in calendar 2000 was importing nearly

300,000 tons of meat and bone meal. Consequently, 2000/01

soybean meal imports by all of Eastern Europe increased by

317,000 tons to 2.9 million.

Demand for soybeans and soybean meal by several Middle

East and North African nations has expanded strongly in

recent years. For 2000/01, soybean imports by Iran were up

130 percent from 2 years earlier and Egyptian imports

nearly doubled. Greater domestic crushing moderated

imports of soybean oil and meal in both countries. In

Tunisia and Algeria, where there are no domestic crushing

facilities, there also were strong gains in consumption and

imports of soybean meal.

An exception to improved soybean demand in the Middle

East was Turkey. After February 22, when the Turkish

Government allowed the countrys currency to float, its lira

lost about one-half of its value relative to the U.S.

dollar.

These events suddenly and sharply increased the cost of all

Turkeys imported goods, including agricultural products.

Over the last decade, Turkey became a significant importer

Economic Research Service/USDA Oil Crops Situation and

Outlook/OCS-2001/October 2001 n 7

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

8/80

of soybean meal and soybeans. But the countrys weaker

economy and more expensive feeds stalled poultry demand

in 2000/01. Turkish soybean meal imports fell to 470,000

tons from 509,000 in 1999/2000.

Weak Oil Prices Stifle Production andTrade of Rapeseed,

Sunflowerseed

Smaller European, Canadian, and Australian crops in

2000/01 reduced world rapeseed production by 4.7 milliontons to

37.7 million. Given abundant alternate sources of

vegetable oil, EU rapeseed prices at planting time had sunk

about 30 percent from a year earlier. In addition, direct

pay-

ments to EU oilseed producers were cut over the next 3

years by Agenda 2000 reforms to equal the area payment for

grains. The low rapeseed prices and declining subsidies

decreased EU rapeseed area 13 percent in 2000 to 3.1 mil-

lion hectares. EU rapeseed yields suffered in 2000 because

drier than normal spring weather was followed by excessive

harvest-time rain in northern France and western Germany.

These factors combined to slash the 2000 EU rapeseed crop

to 9.2 million tons from 11.4 million the previous year.

Eastern European producers responded to the same price

incentives by reducing rapeseed plantings by 15 percent,

lowering production to 2.2 million tons from 2.6 million in

1999/2000. World trade in rapeseed (which has a heavy

European orientation) fell 11 percent in 2000/01 to 9.6

million tons.

Similarly, relatively weak vegetable oil prices and a large

stock carryover encouraged Canadian farmers in 2000 to

shift more area from canola into barley and durum. Canola

area harvested fell 13 percent in Canada to 4.8 million

hectares. Cool temperatures slowed development and a late

spring frost in Alberta forced some replanting in June.

Canola production dropped back from a record 8.8 million

tons in 1999 to 7.1 million. Canadian 2000/01 exports

increased to 4.8 million tons, cutting ending stocks of

canola about in half from the previous year. Domestic crush-

ing increased negligibly.

The rapid expansion in Australian rapeseed area of recent

years was interrupted in 2000/01. Superior returns for

barley

slashed harvested rapeseed area to 1.3 million hectares,

down one-third from the 1999/2000 record. The area reduc-

tion cut Australian rapeseed production to 1.7 million tons,

compared with 2.4 million in 1999/2000. Exports anddomestic

crushing fell accordingly.

In India, a comparatively better profit outlook for wheat

and

persistence of last years dryness in the north reduced rape-

seed area from 5.6 million to 5.0 million hectares. A

contin-

uation of the drought depressed yields, cutting Indias

2000/01 rapeseed crop to 3.7 million tons from 5.1 million.

Among major rapeseed producers, China was an exception

to the crop reductions in 2000, as farmers there harvested a

record 7.5 million hectares. The 12-percent expansion in

area stemmed from strong internal crushing demand and a

withdrawal of government support for winter wheat and

early rice. A mild winter, adequate moisture, and improved

varieties raised Chinas 2000 rapeseed production 12 per-

cent to 11.4 million tons. A larger domestic harvest,

smaller

foreign crops, and larger soybean oil supplies reducedChinas

rapeseed imports to 2.4 million tons from 3.7 mil-

lion in 1999/2000.

Global sunflowerseed production in 2000/01 declined to

22.7 million tons from 27.2 million in 1999/2000. Area

reductions in the EU and Argentina and drought in Eastern

Europe were largely responsible. Weak demand in Western

Europe, brisk crushing of domestic harvests in the former

Soviet Union, and a small Argentine crop stalled global sun-

flowerseed exports near 3.4 million tons.

Scaled down planting and drought slashed 2000-crop sun-

flowerseed production in Romania, Turkey, Hungary,Bulgaria, and

Yugoslavia. Lower supplies in each of these

countries rationed crushing and cut their sunflowerseed

exports dramatically. The Russian harvest declined only

moderately to 3.9 million tons, compared with the bumper

1999 crop of 4.2 million. Despite a 20-percent reduction in

Russian sunflowerseed area, yields were quite good.

In contrast, larger sunflowerseed crops in Spain and Ukraine

helped offset reductions elsewhere. Spanish output recovered

from severe drought in 1999, although fewer plantings in

France and Italy moderated the increase in EU sunflowerseed

output. Similarly, good yields pushed Ukraine sunflowerseed

output up to 3.5 million tons from the previous harvest of

2.7million. Continuation of an export tax on Ukrainian sunflow-

erseed exports kept domestic crushing high.

Larger sunflowerseed oil output by Ukrainian and Russian

processors also eroded traditional Argentine markets.

Argentine sunflower area declined sharply in 2000/01 to 1.9

million hectares from 3.5 million because of much lower

vegetable oil prices. In addition, a dry spell during a

pivotal

stage in late February in western Buenos Aires and La

Pampa (the provinces where the majority of Argentinas

sunflowers are raised) hurt yields. Excess rainfall in March

and April delayed sunflower harvesting and extended the

crop damage. Consequently, Argentine sunflowerseed output

plunged to 3.1 million metric tons, the smallest since

1993/94 and down nearly one-half from a year earlier. Soft

European demand also undermined Argentine crushing and

exports of sunflowerseed, which slumped to 3.5 million and

100,000 tons, respectively.

Global cottonseed production edged up 0.5 million tons in

2000/01 to 33.4 million. The gain was mainly due to much

larger harvests in China and Brazil that offset smaller

losses

8 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

9/80

in India, Pakistan, and other countries. However, greater

feed usage of cottonseed trimmed global crush to 24.4 mil-

lion tons, which lowered 2000/01 supplies and consumption

of cottonseed oil and meal.

A larger peanut crop in China was the major reason that

global peanut production increased 7 percent in 2000/01 to

31.2 million tons. Chinas peanut area expanded 14 percent

to 4.9 million hectares, raising its output to a record 14.4

million tons. The bumper crop allowed a substantial increase

in peanut crushing in China. However, like 1999, Indias

peanut harvest was again damaged by drought, allowing

only a small increase from 5.5 million to 5.7 million tons

based on a slightly higher area. Expanded crushing in both

countries (which normally account for about 80 percent of

the world total) raised global production of peanut meal

out-

put by 4 percent to 5.5 million tons.

Economic Research Service/USDA Oil Crops Situation and

Outlook/OCS-2001/October 2001 n 9

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

10/80

World vegetable oil production expanded to 88.7 million

metric tons in 2000/01 from 85.9 million. Global output of

soybean oil totaled 26.8 million tons, up 2 million tons

from

1999/2000. However, in spite of a large increase in Indian

soybean oil imports, world trade expanded just 0.5 million

tons to 7.8 million tons. Exports increased minimally for

Argentina, Brazil, and the United States. Part of the reason

was that a huge increase in Chinas domestic soybean oil

production sharply curtailed its 2000/01 soybean oil imports

to just 80,000 tons from 1999/2000 imports of 556,000.

China has not yet gained accession to the World Trade

Organization, which also limited issuance of the countrys

oil import quotas.

Palm Oil Exporters Seek MarketsFor Bumper Output

World palm oil output for 2000/01 expanded to 23.7 million

tons, up from 21.8 million in 1999/2000. Malaysian palm

oil production in 2000/01 surged from 10.5 million tons to11.9

million. Similarly, Indonesian output expanded to 7.6

million tons from 7.2 million based on a larger area of

mature trees that were planted about 5 years ago. Early in

2000/01, low producer prices encouraged brisk demand for

palm oil by many of the major importers, including India,

the European Union, China, and the Middle East. World

trade surged to 16.5 million tons, compared with 14.3 mil-

lion in 1999/2000. As palm oil output slowed in the latter

stage of the season, global ending stocks dipped to 2.9 mil-

lion tons from the 1999/2000 record of 3.0 million.

When palm oil surpluses accumulate, the area devoted to oil

palm plantations will not decline significantly, unlike land

planted to annual oilseed crops. Once land is cleared and

trees are planted, palm oil producers have quite low mar-

ginal production costs. Low prices hurt producers short-

term profits, reduce the fertilizer and labor expenses

incurred, and defer the expansion of new plantations. But

existing palm plantations resist taking productive trees out

of production. With no immediate supply response, palm oil

prices must fall sharply to clear the market, so they can

expand market share at the expense of rival vegetable oil

producers until prices improve. In February 2001, Malaysian

crude palm oil prices bottomed out at $193 per metric ton,

own 37 percent from a year earlier.

Malaysian palm oil exports expanded by 1.7 million tons in

2000/01 to 10.55 million. But exports had slowed following

an April 1 tariff hike by India, which stalled the decline

in

stocks. India is Malaysias largest foreign market for palm

oil. Also in early 2001, Indonesias unstable political envi-

ronment and ethnic violence caused its foreign exchange

rate to fall to its lowest value since the 1998 financial

crisis.

Growing supplies and currency depreciation intensified the

pressure on palm oil producers to export and increased the

competition with Malaysia. Indonesian palm oil exports

climbed to 4.45 million tons from 4.0 million in 1999/2000.

In response to the continuing high level of stocks,

Malaysias Government developed schemes to subsidize

replanting of 200,000 hectares of older palm trees and burn

600,000 tons of palm oil in electric power plants. These

measures were intended to support short-term prices by

reducing annual supplies more than 1 million tons.

However, Malaysia has few diesel-fueled electric generators

and burned just 100,000 tons of palm oil. Indonesias

Government pledged cooperation with Malaysias goals of

lowering foreign import barriers and supporting prices. On

March 1, Indonesia implemented a higher export tax on

crude palm oil and lowered its refined palm oil tax to help

develop its domestic refining industry. Later in the year, a

peaceful change of government helped strengthen the

exchange rate. Even Thailand, a minor palm oil producer,promoted

domestic use with tax waivers on biodiesel. Yet, a

cyclical slowing of output provided the most effective boost

to palm oil prices, which rose to $337 per ton by August

2001 and cooled interest in the stock-reduction plans.

Indian Import Tariffs Reorient WorldVegetable Oil Trade

Indias oilseed production for 2000/01 was estimated at 20.7

million tons, down 7 percent from the previous year and 17

percent from 2 years earlier. The shortfall of domestic

oilseed crushing has contributed to a rising tide of Indian

vegetable oil imports, which alone comprised 18 percent of

the world imports in 2000/01.

The Government of India tried to aid domestic oilseed farm-

ers by again raising import tariffs on vegetable oil. Indias

last tariff hikes on April 1, 2001, raised import duties on

crude palm oil and crude sunflowerseed oil to 75 percent

and refined palm oil to 85 percent. India maintains higher

tariffs for refined oils to promote its domestic refining

industry. However, poor domestic oilseed crops, steeply dis-

counted prices, and robust consumption growth nullified the

impact of higher palm oil tariffs. Indian palm oil imports

still expanded to a record 4.2 million tons.

In contrast, with the 1994 Uruguay Round Agreement,

Indias market access commitments eliminated all quantita-

tive restrictions on imports and bound the maximum tariff

on soybean oil imports at 45 percent. Soybean oil imports

quickly became the preferred source for covering Indias

acute vegetable oil deficit. Border prices for palm oil were

discounted $75-$80 per ton to soybean oil, but the Indian

tariff differential nearly equalized domestic prices of palm

oil and soybean oil. By August 2001, the price discount for

10 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

World Vegetable Oil Situation

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

11/80

Malaysian palm oil against U.S. soybean oil had narrowed

to about $40 per ton. Indian consumption is very price sen-

sitive, so a small change in that price wedge can cause a

substantial substitution between vegetable oils.

Indian soybean oil imports increased from 0.8 million to 1.4

million tons in 2000/01. India typically imports soybean oil

between May and September, so Argentina and Brazil usu-

ally supply most of them. U.S. soybean oil exporters had

anegligible share of this trade, but they may soon benefit

competitively in other foreign markets as India absorbs

more supplies from South America. Conversely, lower avail-

able sunflowerseed oil supplies from Argentina and higher

import duties made them less price competitive for India.

Indias 2000/01 sunflowerseed oil imports dropped to

475,000 tons from 570,000 tons in 1999/2000.

When Indias partial retreat from the market created favor-

ably low international prices, other countries were encour-

aged to expand their 2000/01 imports. European Union

imports of palm oil increased 9 percent to 2.9 million tons.

China does not produce palm oil but is a leading consuming

country. Palm oil imports by China swelled to 1.8 million

tons from 1.2 million in 1999/2000. Import quotas were

more available for palm oil than for soybean and rapeseed

oil, which help protect Chinas oilseed processors.

Both the gains in world trade for soybean oil and palm oilwere

aided by lower quantities of sunflowerseed oil and

rapeseed oil. World sunflowerseed oil output in 2000/01

declined 1.3 million tons to 8.3 million and exports (mainly

by Argentina) plummeted 0.8 million tons to 2.9 million.

Likewise, global production of rapeseed oil fell 0.4 million

tons in 2000/01 to 13.2 million, and exports dropped 0.3

million tons to 2.6 million.

Economic Research Service/USDA Oil Crops Situation and

Outlook/OCS-2001/October 2001 n 11

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

12/80

Cottonseed

Feed Use of Cottonseed EclipsesCrush Demand

U.S. farmers planted 15.6 million acres of cotton in 2000,

the second largest area ever. However, a repeat of late-sum-mer

heat and drought resulted in substantial area abandon-

ment. The adverse weather also produced below-average

dryland cotton yields in Texas and the Delta, although these

yields were somewhat better than in 1999. Factoring in an

improved seed-to-lint ratio, 2000 cottonseed output

increased only slightly to 6.4 million short tons. However,

there was no serious deficit in cottonseed supplies because

of a record volume of imports from Australia.

In fact, ending stocks of cottonseed rose to 424,000 tons

because of a sharp reduction in crushing. Oil processors

used 2.7 million tons of seed in 2000/01, down from 3.1

million in 1999/2000. Weak prices for cottonseed oil dimin-

ished crushing margins for cottonseed. Ample supplies of

competing oils cut 2000/01 domestic disappearance of cot-

tonseed oil 23 percent to 649 million pounds, the lowest

usage since 1986/87. Similarly, demand for cottonseed oil

exports remained slow, sliding to 131 million pounds from

141 million in 1999/2000. But, consumption of cottonseed

in livestock feed and planting seed increased 7 percent to

3.75 million tons. U.S. cottonseed exports (mostly to

Mexico) also edged up from 198,000 tons to 235,000.

Firmer feed prices generally supported the 2000/01 average

cottonseed price at $106 per ton. The Government alsoapproved

$84.7 million of supplemental payments to U.S.

producers and first handlers of the 2000 cottonseed crop.

Payments were made to cotton ginners who distributed them

to producers. The average payment rate was approximately

$13 per ton of cottonseed.

Peanuts

On December 13, 1999, the U.S. Department of Agriculture

(USDA) announced a national peanut poundage quota for

the 2000 marketing year of 1.18 million short tons (2.360

billion pounds), the same as for the 1999 marketing year.

The quota equaled the estimated quantity of peanuts neededfor

domestic edible and related uses, excluding seed, in the

2000 marketing year and allowed for potential underdeliver-

ies of up to 18,500 short tons. The national average support

price for 2000/01 quota peanuts was announced as $610 per

short ton. The support price for additional peanuts was $132

per short ton. Both were unchanged from 1999. Following

losses on the 1999 crop, producers were spared from a

higher marketing assessment in 2000 when Congress autho-

rized payment of the 1999 losses with assessments from

previous years and future assessments to be collected

through 2002.

2000 Peanut Plantings Up butProduction Declines

U.S. peanut area planted in 2000, at 1.54 million acres,was up 1

percent from plantings in 1999. Although

national plantings were up slightly, extremely dry condi-

tions in many areas of the Southwest (New Mexico,

Oklahoma, and Texas) during the growing season raised

abandonment and cut national harvested acreage to 1.32

million acres, down 8 percent from 1999. For the 2000

crop year, 205,000 planted acres were not harvested com-

pared with 84,000 acres in 1999.

As in 1999, poor weather also cut the 2000 average peanut

yield, which fell to 2,444 pounds per harvested acre, down

223 pounds per acre (8 percent) from 1999, and the lowest

yield since 1995. As a result, U.S. peanut production

fellsharply in 2000, down 563 million pounds to 3,266 million.

Output fell by 304 million pounds in the Southwest and 292

million pounds in the Southeast (Alabama, Florida, Georgia,

and South Carolina), but production from the Virginia-North

Carolina region was up 6 percent from 1999.

Despite the harvest problems, the peanut buyback provision

met quota needs by converting 224 million pounds of addi-

tionals for domestic use. Although less than 5 percent of

total supply, peanut imports in 2000 rose to 211 million

pounds (farmer stock equivalent). Imports increased 33

million

pounds from the year before and were the largest since the

record 1980/81 imports of 401 million. The smaller U.S. har-

vest mostly reduced the ending stocks from a quite large

1999/2000 carryover of 1,233 million to 1,116 million

pounds.

But lower demand offset part of the decline in supply, and

the

2000/01 national average farm price for peanuts strengthened

only slightly to 25.7 cents per pound from 25.4 cents the

pre-

vious season. The smaller crop reduced the farm value of the

2000 peanut crop to $839 million, off $134 million from

1999, and the lowest farm value since 1983.

U.S. Food Use of Peanuts Weakens

Domestic food use of peanuts waned in 2000/01, falling to2,170

million pounds from 2,233 million in 1999/2000.

However, overall food use in 2000 was still relatively

strong

compared with the 1990-99 average of 2,095 million

pounds. Rising peanut butter imports partly contributed to

the drop in peanuts processed for domestic use.

Individual categories of primary product use in 2000/01 saw

consumption of peanuts for peanut butter (the major use in

the United States) fall more than 2 percent to 753 million

12 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

Situation for Other U.S. Oil Crops

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

13/80

pounds. Consumption for snack peanuts dropped more than 8

percent to 362 million pounds, and other use fell by 1 per-

cent to 20 million pounds. Peanut use for candy was

virtually

unchanged at 355 million pounds, while in-shell peanut use

was up by nearly 5 million pounds to 150 million.

Lower Exports and Domestic Crush ContributeTo Decline in Peanut

Disappearance

Ample foreign harvests and a tighter supply of export

addi-tionals reduced U.S. peanut exports to 520 million pounds

from 727 million in 1999, and the smallest since 1980/81. On

an in-shell basis, peanuts crushed in 2000/01 totaled 548

mil-

lion pounds, 23 percent below the previous season and 29

percent below the 1990-99 average of 774 million pounds.

With the reduced crush, U.S. peanut oil production fell to

179 million pounds, down from 229 million pounds the pre-

vious year. Nevertheless, a large jump in peanut oil

importsto a record 79 million poundshelped raise

domestic consumption of peanut oil to the highest level

since 1975. Most peanut oil imports came from Argentina.

Peanut oil prices declined to 32.2 cents per pound, downfrom

33.6 cents per pound in 1999 and their lowest level

since 1992.

Peanut meal production also declined, from 146,000 short

tons in 1999 to 115,000 short tons in 2000. Ending stocks

remained unchanged at a low level of 2,000 short tons and

exports declined from 6,500 to 5,700 short tons. Peanut

meal prices rebounded slightly from the previous year, up 4

percent to a season-average $153.60 per short ton.

Sunflowerseed

Despite Smaller Crop, Poor Crush DemandSlashes Sunflowerseed

Prices

Farmers in the Northern Plains switched from sunflowers to

soybeans, canola, and flax in 2000 because of fears that the

sunflower disease that afflicted the 1999 crop could return.

Thus, U.S. sunflower harvested acreage fell to 2.6 million

acres, down nearly one-fourth from 1999. Oil-type sunflow-

ers accounted for most of the decline in total harvested

area, falling 0.6 million acres as confection varieties

declined another 0.2 million acres. While North Dakota

comprised 60 percent of the reduction in sunflower acreage,

planting declined in other States, as well. The recovery

from a low 1999 sunflowerseed yield moderated the declinein

production to 3,544 million pounds from the previous

years 4,342 million.

Sluggish European demand curtailed oil-type sunflowerseed

exports to just 45 million pounds. In contrast, U.S. confec-

tionery seed exports increased (to the EU in particular) to

a

record 400 million pounds, in spite of a shorter domestic

supply. Domestic use of confectionery sunflowerseed fell

sharply to 363 million pounds, keeping ending stocks at a

relatively high 159 million.With sharply lower seed supplies

and falling oil prices, domestic sunflowerseed crushers were

in no stronger position than foreign processors.

Sunflowerseed oil exports, which make up the majority of

crushers sales, fell again in 2000/01 to 554 million pounds.

Greater supplies of mid-oleic varieties (NuSun) supported

domestic sunflowerseed oil consumption equal to the previ-

ous seasons level of 385 million pounds. But very low soy-

bean oil prices pressured U.S. prices for sunflowerseed

andsunflowerseed oil near historic lows of $6.80 per hundred-

weight and 16.2 cents per pound, respectively. Producers of

oil-type and confection sunflowerseed received $132.2 mil-

lion of marketing loan benefits for the 2000 crop. In addi-

tion, producers received Oilseed Program payments of $12.7

million in February 2001 and supplemental payments of

$10.8 million in August 2001.

Other Minor Oilseeds

Canola

Canola plantings swelled 46 percent in 2000 to a record 1.6

million acres. Combined with relatively normal yields,

theadditional acreage pushed U.S. canola production to a

record 2,017 million pounds. A larger harvest trimmed

Canadian imports to 479 million pounds from 534 million

the previous season. In fact, U.S. canola seed exports

jumped from 299 million to 486 million pounds. Foreign

sales are mostly to Canadian crushing plants, although ship-

ments to Mexico grew rapidly in 2000/01. Larger supplies

and less processing of sunflowerseed also helped domestic

canola seed crushing expand to 1.7 billion pounds.

Consequently, U.S. ending stocks of canola fell from 109

million pounds to 84 million. The slowdown in Canadian

crushing also stalled the growth in U.S. imports of canola

meal and canola oil. Canola producers received $70.8 mil-

lion of marketing loan benefits for the 2000 crop. In addi-

tion, producers received Oilseed Program payments of $5.7

million in February 2001 and supplemental payments of

$4.8 million in August 2001.

Flaxseed

Likewise, U.S. flax acreage surged 39 percent from 1999 to

536,000 acres. With a relatively normal yield of 20.8

bushels per acre, 2000 flaxseed output rose to 10.7 million

bushels from 7.9 million in 1999. The comparatively large

domestic crop sharply reduced imports from Canada from

6.6 million bushels to 2.8 million. Canada itself (the

worldslargest flaxseed producing country) slashed acreage in

2000

given its own huge carryover from the previous season.

Consequently, U.S. flaxseed exports also expanded sharply

in 2000/01 to more than 1 million bushels. Ending stocks

dropped from 1.8 million bushels to 1.3 million. But the

still-high Canadian flaxseed surpluses depressed U.S. farm

prices again in 2000/01, which dropped from $3.79 per

bushel to $3.30 and well below the $5.21 marketing loan

rate. As a result, flaxseed producers received $21.8 million

Economic Research Service/USDA Oil Crops Situation and

Outlook/OCS-2001/October 2001 n 13

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

14/80

in marketing loan benefits for the 2000 crop. Producers also

received Oilseed Program payments of $1.3 million in

February 2001 and supplemental payments of $1.1 million

in August 2001.

U.S. farmers decreased safflower plantings in 2000 by 22

per-

cent to 215,000 acres. Safflowerseed yields (at 1,434 pounds

per acre) fell off from a very high 1999 level, so

production

declined 30 percent to 283 million pounds. The smaller har-

vest helped reduce an unusually large stock carryover from

1999/2000 (82 million pounds) to less burdensome 57 mil-

lion. Exports of safflowerseed and safflowerseed oil both

fell

to their lowest levels since the mid-1980s. Although

safflower

producers received no direct payments under the marketing

loan program because of the high price of safflowerseed

rela-

tive to the 9.3-cents-per-pound loan rate, producers

received

Oilseed Program payments of $1.7 million in February 2001

and supplemental payments of $1.4 million in August 2001.

14 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

15/80

Corn Oil

U.S. corn oil production fell in 2000/01 to 2,403 million

pounds from 2,501 million a year earlier. Production incen-

tives in 2000/01 were diminished by a sharp fall in the

price

of corn oil, which slumped from 17.8 cents to 13.5 cents per

pound. Domestic corn oil output also declined as a conse-quence

of a reduced grind by dry corn millers, whose sales

suffered from concerns over the possible presence in their

products of an unapproved, genetically modified corn vari-

ety. This same process separates the corn germ, from which

corn oil is extracted, from the other corn components.

Large world supplies of competing vegetable oils curtailed

demand for U.S. corn oil exports from 970 million to 944

mil-

lion pounds. Yet, a low price (an unusual discount against

soy-

bean oil for the first half of 2000/01) encouraged a high rate

of

domestic consumption for this byproduct. U.S. corn oil

disap-

pearance swelled to 1,638 million pounds from 1,470 million

in 1999/2000.

Imported Oils

World coconut oil output, particularly in the Philippines,

continued a comeback in 2000/01. Production rose from 3.3

million tons in 1999/2000 to 3.4 million. In fact, the

supply

situation has quickly turned from a deficit into a surplus.

Coconut oil prices (Rotterdam) plunged to an average of

$319 per ton in 2000/01, compared with $539 and $748 in

the 2 previous years. The easing of prices swelled U.S.

coconut oil imports to 1,096 million pounds from 926 mil-

lion in 1999/2000. This allowed domestic disappearance of

coconut oil to recover to 965 million pounds and a rebuild-

ing of ending stocks to 260 million pounds.

World production of olive oil rebounded 8.5 percent in

2000/01 to 2.56 million tons. The EU accounts for about

three-fourths of world output, with Tunisia, Syria, and

Turkey

accounting for much of the remainder. More than 70 percent

of world consumption of olive oil also occurs in the

European

Union. Yet, the United States is a major import market.

Health

conscious consumers strongly raised U.S. olive oil imports

to

468 million pounds from 417 million in 1999/2000. The

strength of the dollar versus the euro in 2001 also enhanced

the purchasing power of U.S. consumers of olive oil.

Animal Fats

A decline in U.S. cattle slaughter slowed edible tallow pro-

duction in 2000/01 to 1,814 million pounds from 1,810 mil-

lion in 1999/2000. By the summer, tallow prices gradually

firmed, averaging 13.4 cents per pound in 2000/01 compared

with 13.2 cents the previous season. However, very low veg-

etable oil prices still pressured the value of tallow.

Domestic

tallow disappearance fell 5 percent to 1,503 million pounds

as

a decline in edible use offset gains in industrial use.

The major factor buoying the edible tallow price was

stronger foreign demand. The EU Commission exempted

animal fats from its ban on animal protein in feeds, requir-

ing only that they be completely filtered. But, EU beef pro-

duction fell and because no meat meal could be sold,

rendering of tallow in Europe also declined sharply. And

despite a lack of evidence that beef tallow can transmit

BSE,France and Germany adopted their own feeding restrictions

on tallow. So, lower tallow consumption favored imports of

cheaper substitutes such as palm stearin. As European

exports faded, U.S. edible tallow exports helped make up

the difference by swelling to 332 million pounds in 2000/01

compared with 224 million the previous year.

Output of lard by U.S. renderers fell to 1,050 million

pounds

in 2000/01, from 1,069 million a year earlier. After June

2001, lard prices began recovering from the very low levels

of

the previous year, and the 2000/01 average price firmed to

14.6 cents per pound from 13.6 cents in 1999/2000. The rela-

tively low prices encouraged a near-record domestic disap-

pearance of lard, which rose to 964 million pounds from 886

million in 1999/2000. In contrast, U.S. lard exports fell by

half in 2000/01 to 93 million pounds. Weak sales to Mexico

(which imported more tallow, instead) and Hong Kong were

largely responsible for the decline.

End Uses of Fats and Oils

Low prices in calendar year 2000 encouraged a surprisingly

strong response for U.S. oils and fats consumption. U.S.

output of salad and cooking oils rose a robust 19-percent to

9,155 million pounds. Domestic consumption surged 19 per-

cent to 9,522 million pounds. On a per capita basis,

U.S.consumption for these uses increased from 29.4 pounds in

1999 to an all-time high of 30.5 pounds. Exports of salad

oils also rebounded to 734 million pounds. Production of

baking and frying fats also increased substantially in 2000,

rising 11 percent to 6,593 million pounds. U.S. per capita

consumption of shortenings jumped to 23.7 pounds from

21.6 pounds in 1999.

A 6-year slide in domestic margarine production ended in

2000, as output rose from 2,274 million to 2,398 million

pounds. Total margarine consumption also recovered by 5

percent to 2,353 million pounds and per capita consumption

edged up to 8.5 pounds.

Conversely, consumption of oils for inedible uses dropped 5

percent in 2000 to 6,416 million pounds. Lower consump-

tion of oils for soap and fatty acids outweighed negligible

increases in animal feeds and paints. After a strong

increase

in 1999, the inedible consumption of soybean oil was

unchanged in 2000 at 588 million pounds. Consumption of

linseed oil declined 2 percent to 81 million pounds.

Economic Research Service/USDA Oil Crops Situation and

Outlook/OCS-2001/October 2001 n 15

Other Fats and Oils Highlights

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

16/80

Introduction

The competitiveness of U.S. agricultural products in export

markets is an ongoing concern for domestic producers and

U.S. policymakers. The United States has long been the

worlds leading exporter of soybeans, corn, and wheat, but it

has faced increased competition from other exporters for

global market share of these commodities.

This situation is exemplified by the declining share of U.S.

soybean and product exports in global markets since 1980,

despite increased domestic production and aggregate

exports. For example, the U.S. share of global soybean

andsoymeal exports (in soybean equivalents) has declined from

about 55 percent in 1980 to slightly over one-third in 2000,

whereas Brazil and Argentinas combined share of global

soy complex exports has grown from about 31 percent to

nearly 50 percent (fig. A-1).2

Competitiveness in commodity markets of course reflects the

influence of many different factors. These include relative

resource endowments and agro-climatic conditions, but also

the impact of macroeconomic policies (affecting exchange

rates, work incentives, investment, energy costs and

availabil-

ity, etc.), sector-specific policies (e.g., credit subsidies,

import

or export taxes on inputs or final products), infrastructure

(forstorage and transportation), and supporting institutions

(e.g.,

credit, regulatory, news and information, etc.) that help

mar-

kets to work effectively. Export shares and growth trends

also

depend on domestic demand, relative returns to other crops,

and other conditions.

However, in its simplest terms, international market compet-

itiveness is the ability to deliver a product at the lowest

costi.e., with the lowest combined farm-level production,

transportation, and marketing costs. On this basis, analysis

of 1998/99 cost structures underlying soybean production,

transportation, and marketing from principal growing

regions to a common export destination, Rotterdam, sug-

gests that the United States lagged slightly behind

Argentina

and Brazil in soybean export cost competitiveness.

At the farm level, soybean producers in the U.S. Heartland

had the highest overall average costs of production at $5.11

per bushel, ranging from 18 to 25 percent above those of

Argentine or Brazilian competitors.3

Total production costs were lowest in Argentinas central

soybean growing region (southern Santa Fe and northern

Buenos Aires Provinces) and in Brazils interior expansion

zone (the State of Mato Grosso), at about $3.90 per bushel

in both regions (fig. A-2). Production costs in Brazils

coastal State of Parana (in its traditional agricultural

heart-

land) were estimated at $4.16 per bushel. High imputed land

costs in the United States account for much of the

difference

in overall production costs. The U.S. production cost disad-

vantage is partially mitigated by internal transportation

and

marketing cost savings. In Brazil and Argentina, these costs

are two to three times higher, on average, than in the

United

States, despite important efficiency gains in recent years.

16 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

1 Economists in the Market and Trade Economics Division,

Economic

Research Service, USDA.2 The U.S. share of world corn exports

fell from an average of 67 percent

during 1980-89 to 61 percent during 1998-2000. The U.S. share of

world

wheat exports fell from an average of 34.3 percent during

1980-89 to 22.8

percent during 1998-2000. Source: USDA, PS&D database.

3 The Heartland is defined as western Ohio, Indiana, Illinois,

Iowa, north-

ern Missouri, western Kentucky, and parts of Nebraska,

Minnesota, and

South Dakota.

Special Article

Soybean Production Costs and Export Competitiveness in the

United States, Brazil, and Argentina

Erik Dohlman, Randall Schnepf, and Chris Bolling1

Abstract: Argentina and Brazil have become increasingly strong

competitors to the United

States in international soybean and soybean product markets, as

evidenced by steady market

share gains in recent decades. A comparison of combined

marketing, transportation, and

farm-level production costs in the late 1990s reveals that

Brazil and Argentina maintained a

competitive advantage over the United States in production

costs, mainly due to higher

imputed land values in the United States. The U.S. production

cost disadvantage was partially

offset by lower internal transportation and marketing costs, but

Brazil and Argentina have

reduced these costs considerably in recent years.

Key words: Brazil, Argentina, agriculture, soybeans, production

costs, competitiveness.

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

17/80

Freight charges to Rotterdam are also higher from South

America. As a result, the delivered cost of Argentine and

Brazilian soybeans at Rotterdam ranged from 2 to 12 per-

cent less than U.S. costs in 1998/99.

Methodology Behind theCost Comparisons

The export cost competitiveness of U.S., Brazilian, and

Argentine soybean producers is examined by comparing the

components and distribution of farm-level production costs,

the costs of internal marketing and transportation, and

ship-

ping costs to a common export destination. Cost data for

eachcountry were from local 1998/99 marketing years, the most

recent year for which detailed comparisons were possible.

First, production costs were separated into their variable-

and fixed-cost components. Variable costs include the use of

inputs such as seed, fertilizer, chemicals, fuel, machine

repair, interest on operating capital, and other direct

costs

incurred during crop production. Land costse.g., rental,

maintenance, etc.are not included with variable costs of

production, but are combined with fixed production costs

following Economic Research Service (ERS) methodology

that uses land rental rates to value the opportunity cost of

all

land farmed. Fixed costs include costs that are not directlytied

to the production decision, such as land payments on

principal, interest and taxes, depreciation of machinery and

equipment, and farm overhead.

Cost data from the U.S. Heartland region, where most U.S.

soybean production takes place, were chosen to represent

the United States. U.S. data are based on surveys by the

National Agricultural Statistics Service (NASS), using the

Agricultural Resource Management Study (ARMS). The

data are compiled and published by ERS for regional and

national aggregates.4 For Brazil, data from USDA and

Brazilian Government sources were compiled for two

regions: the State of Parana, a leading soybean producer in

the South; and Mato Grosso, the largest soybean producing

State in the Center-West.

In Argentina, average variable cost-of-production data for

northern Buenos Aires/southern Santa Fe (the heart of the

corn-soybean region) were obtained fromMargenes

Agropecuarios (January 1999) based on no-till, Roundup

Ready soybean production for high-yielding corn and soy-

bean land. The lower end of the average yield range of 3.4

to 3.8 tons per hectare (50.6 to 56.5 bushels per acre) was

used in the per-bushel cost calculations. Argentine land

rents

are also based on data fromMargenes Agropecuarios (July

1999) for rental rates in the northern Buenos Aires produc-

tion region. Other fixed cost data were adapted from Vieira

and Williams (1996). A detailed and comparable breakdown

of variable production costs for the Buenos Aires/Santa Fe

region was not available, but the distribution of variable

pro-

duction costs based on suggested practices in the northern

Province of Chaco was available, and is presented in table

A-1 for comparison purposes.5

Internal marketing and transportation costs in the United

States and Brazil are estimated by calculating the average

Economic Research Service/USDA Oil Crops Situation and

Outlook/OCS-2001/October 2001 n 17

4 For soybean cost-of-production data, see

http://www.ers.usda.gov/

data/costsandreturns/car/soybean2.htm.5 Chaco is primarily a

cotton growing region, but soybean production has

emerged there in the past decade. According to Hinrichsen

(2001), 350,000

hectares of soybeans were planted in Chaco in 1999, making it

the fifth

leading soybean Province in Argentina, by area planted.

1964 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98

20000

20

40

60

80

100

Figure A-1

U.S. share of world soybean and soymeal market has steadily

eroded*

% of global exports

Other

U.S.

Argentina

Brazil

*Soybeans and soymeal as soybean equivalents.

Source: USDA, Aug. 10, 2001.

-

7/29/2019 Oil Crops_Situation and Outlook Yearbook, 2001

18/80

monthly spread between farm-level soybean prices and the

f.o.b. (free on board) port prices during calendar years

1998

and 1999. These spreads should reflect differences in trans-

portation, storage, drying, loading and unloading, taxes,

and

other costs associated with bringing soybeans from farm to

cargo vessel. Port prices are from the U.S. Gulf ports and

the port of Rio Grande in Brazil.6

For Argentina, monthly farm-level prices were not avail-

able, so internal marketing and transportation costs were

estimated in two steps. First, port and associated charges

(including a 3-percent export tax) were estimated as the

dif-

ference between f.o.b. port prices and f.a.s. (free

alongside

ship) Rosario terminal pricesreflecting port charges

(loading, export tax, and quality control). Next, costs of

bringing soybeans from farm to port were estimated using

information from other sources on internal transportationcharges

at the average distance to port in 1998, plus esti-

mates of other marketing costs (loading/unloading, and bro-

kers commission).7

18 n Oil Crops Situation and Outlook/OCS-2001/October 2001

Economic Research Service/USDA

Figure A-2

Argentina's and Brazil's main agricultural production zones

South

BA

SF

MT

PR

Center-West

Brazil

Pampas

ArgentinaMT = Mato GrossoPR = Parana

SF = Santa FeBA = Buenos Aires

Source: Economic Research Service, USDA.

7 Estimates of freight and other charges from farm to port are

based on

data from the Brazilian oilseed crushing association (ABIOVE),

cited in

Verheijden and Reca (1998), and data provided by the Argentine

brokerage

firm Cortina-Beruatto (Frogone, 2001).