Embed Size (px)

Citation preview

OIL AND GASIN THE MEDITERRANEAN SEA: ARE THE RISKS WORTH THE BENEFITS?

2015

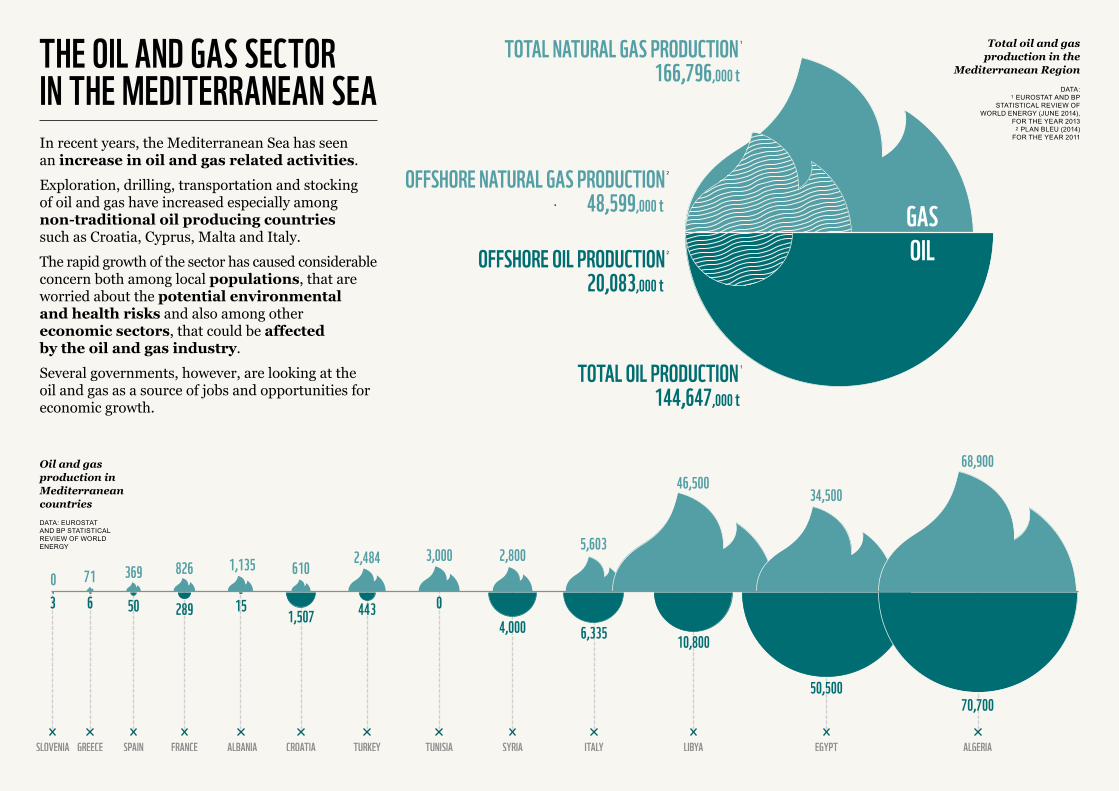

In recent years, the Mediterranean Sea has seen an increase in oil and gas related activities.Exploration, drilling, transportation and stocking of oil and gas have increased especially among non-traditional oil producing countries such as Croatia, Cyprus, Malta and Italy.The rapid growth of the sector has caused considerable concern both among local populations, that are worried about the potential environmental and health risks and also among other economic sectors, that could be affected by the oil and gas industry.Several governments, however, are looking at the oil and gas as a source of jobs and opportunities for economic growth.

THE OIL AND GAS SECTOR IN THE MEDITERRANEAN SEA

SLOVENIA

03

GREECE

716

SPAIN

369

50

FRANCE

826

289

ALBANIA

1,135

15

CROATIA

610

1,507

TURKEY

2,484

443

TUNISIA

3,000

0

SYRIA

2,800

4,000

ITALY

5,603

6,335

LIBYA

46,500

10,800

EGYPT

34,500

50,500

ALGERIA

68,900

70,700

166,796thousands tons of oil equivalent

NATU

RAL G

AS PR

ODUC

TION 2

013

(esp

ress

ed in

thou

sand

s ton

s of o

il eq

uiva

lent

)OIL

PROD

UCTIO

N 201

3

NATURAL GAS PRODUCTION 2013IN MEDITERRANEAN COUNTRIES

166,796thousands tons of oil equivalent

NATURAL GAS PRODUCTION 2013IN MEDITERRANEAN COUNTRIES

DATA: EUROSTAT AND BP STATISTICAL REVIEW OF WORLD ENERGY

Oil and gas production in Mediterranean countries

SLOVENIA

03

GREECE

716

SPAIN

369

50

FRANCE

826

289

ALBANIA

1,135

15

CROATIA

610

1,507

TURKEY

2,484

443

TUNISIA

3,000

0

SYRIA

2,800

4,000

ITALY

5,603

6,335

LIBYA

46,500

10,800

EGYPT

34,500

50,500

ALGERIA

68,900

70,700

NATU

RAL G

AS PR

ODUC

TION 2

013

(esp

ress

ed in

thou

sand

s ton

s of o

il eq

uiva

lent

)OIL

PROD

UCTIO

N 201

3

TOTAL NATURAL GAS PRODUCTION 1

166,796,000 t

TOTAL OIL PRODUCTION 1

144,647,000 t

OFFSHORE NATURAL GAS PRODUCTION 2

48,599,000 t

OFFSHORE OIL PRODUCTION 2

20,083,000 t

GASOIL

Total oil and gas production in the

Mediterranean RegionDATA:

1 EUROSTAT AND BP STATISTICAL REVIEW OF

WORLD ENERGY (JUNE 2014), FOR THE YEAR 2013

2 PLAN BLEU (2014)FOR THE YEAR 2011

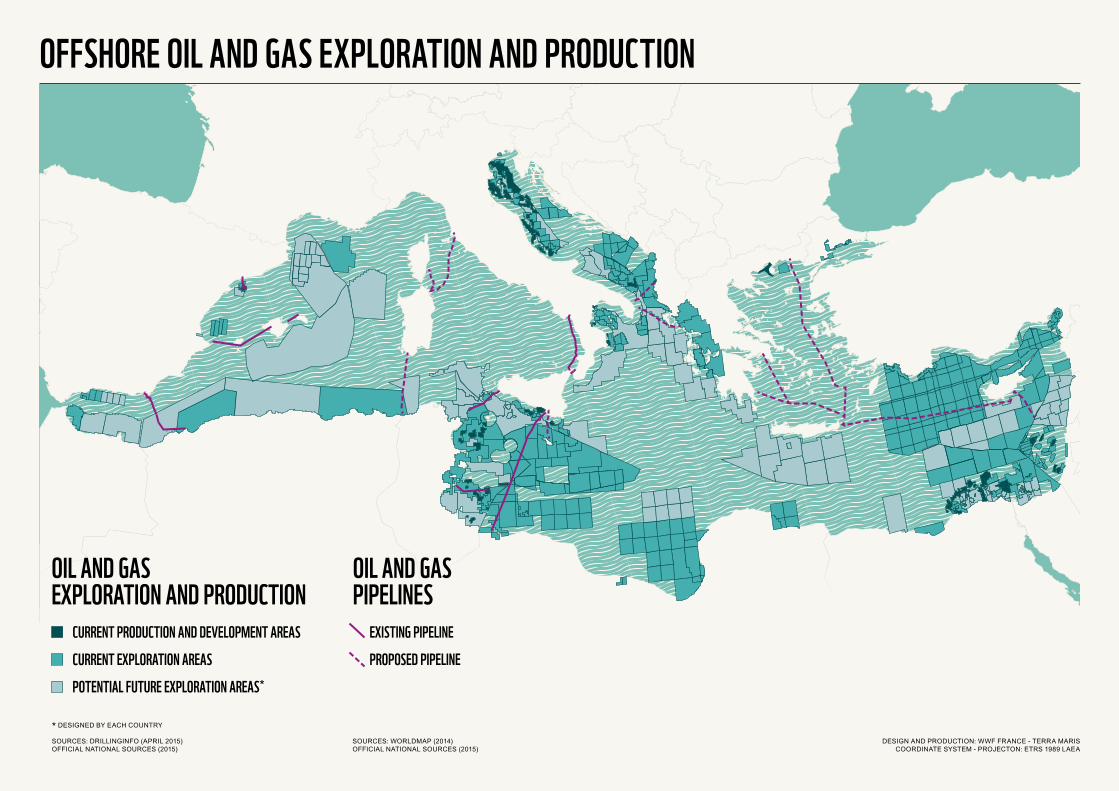

OIL AND GASEXPLORATION AND PRODUCTION

EXISTING PIPELINE

PROPOSED PIPELINE

OIL AND GASPIPELINES

CURRENT PRODUCTION AND DEVELOPMENT AREAS

CURRENT EXPLORATION AREAS

POTENTIAL FUTURE EXPLORATION AREAS*

DESIGN AND PRODUCTION: WWF FRANCE - TERRA MARIS COORDINATE SYSTEM - PROJECTON: ETRS 1989 LAEA

* DESIGNED BY EACH COUNTRY

SOURCES: DRILLINGINFO (APRIL 2015) OFFICIAL NATIONAL SOURCES (2015)

SOURCES: WORLDMAP (2014) OFFICIAL NATIONAL SOURCES (2015)

OFFSHORE OIL AND GAS EXPLORATION AND PRODUCTION

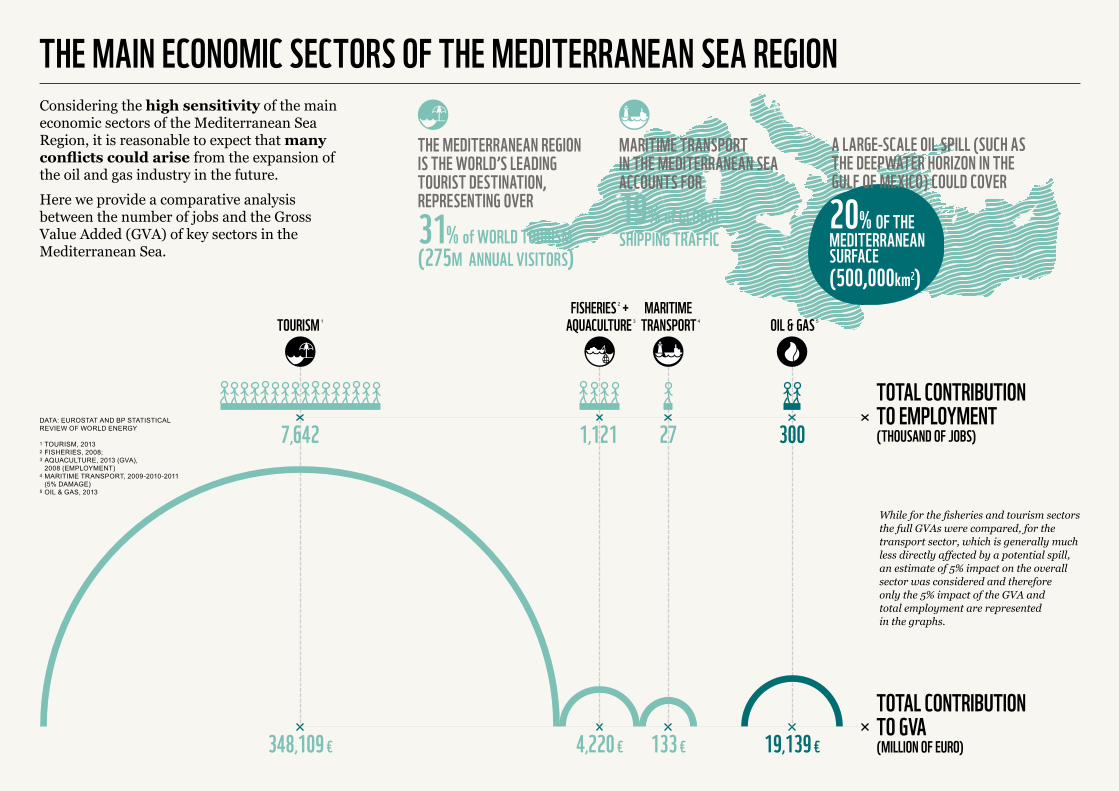

THE MAIN ECONOMIC SECTORS OF THE MEDITERRANEAN SEA REGION

20% OF THEMEDITERRANEAN SURFACE(500,000km2)

A LARGE-SCALE OIL SPILL (SUCH AS THE DEEPWATER HORIZON IN THE GULF OF MEXICO) COULD COVER

TOURISM 1 OIL & GAS

5

FISHERIES 2 +

AQUACULTURE 3

MARITIME TRANSPORT

4

348,109 € 4,220 € 133 € 19,139 €

TOTAL CONTRIBUTIONTO GVA(MILLION OF EURO)

TOTAL CONTRIBUTIONTO EMPLOYMENT(THOUSAND OF JOBS)7,642 1,121 27 300

Considering the high sensitivity of the main economic sectors of the Mediterranean Sea Region, it is reasonable to expect that many conflicts could arise from the expansion of the oil and gas industry in the future.Here we provide a comparative analysis between the number of jobs and the Gross Value Added (GVA) of key sectors in the Mediterranean Sea.

DATA: EUROSTAT AND BP STATISTICAL REVIEW OF WORLD ENERGY

1 TOURISM, 20132 FISHERIES, 2008; 3 AQUACULTURE, 2013 (GVA),

2008 (EMPLOYMENT)4 MARITIME TRANSPORT, 2009-2010-2011

(5% DAMAGE)5 OIL & GAS, 2013

While for the fisheries and tourism sectors the full GVAs were compared, for the transport sector, which is generally much less directly affected by a potential spill, an estimate of 5% impact on the overall sector was considered and therefore only the 5% impact of the GVA and total employment are represented in the graphs.

THE MEDITERRANEAN REGION IS THE WORLD’S LEADING TOURIST DESTINATION, REPRESENTING OVER

31% of WORLD TOURISM (275M ANNUAL VISITORS)

MARITIME TRANSPORT IN THE MEDITERRANEAN SEA ACCOUNTS FOR

19% of GLOBAL SHIPPING TRAFFIC

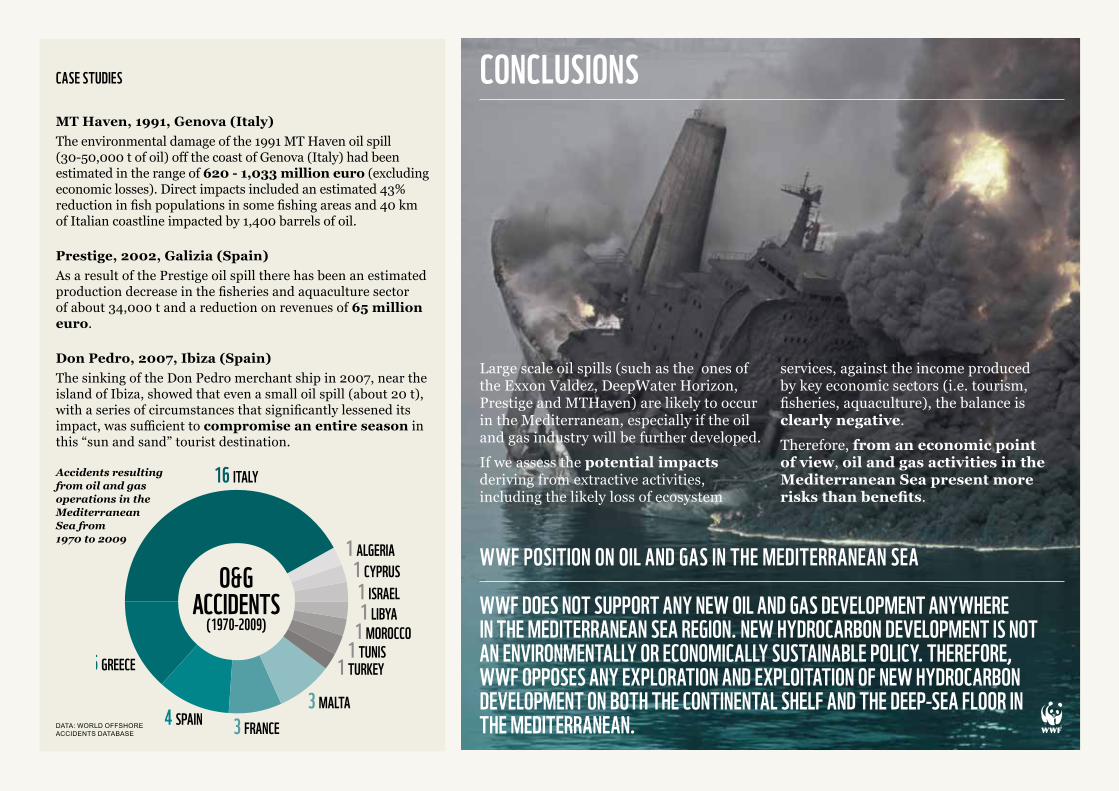

CONCLUSIONS

WWF POSITION ON OIL AND GAS IN THE MEDITERRANEAN SEA

CASE STUDIES

WWF DOES NOT SUPPORT ANY NEW OIL AND GAS DEVELOPMENT ANYWHERE IN THE MEDITERRANEAN SEA REGION. NEW HYDROCARBON DEVELOPMENT IS NOT AN ENVIRONMENTALLY OR ECONOMICALLY SUSTAINABLE POLICY. THEREFORE, WWF OPPOSES ANY EXPLORATION AND EXPLOITATION OF NEW HYDROCARBON DEVELOPMENT ON BOTH THE CONTINENTAL SHELF AND THE DEEP-SEA FLOOR IN THE MEDITERRANEAN.

MT Haven, 1991, Genova (Italy)The environmental damage of the 1991 MT Haven oil spill (30-50,000 t of oil) off the coast of Genova (Italy) had been estimated in the range of 620 - 1,033 million euro (excluding economic losses). Direct impacts included an estimated 43% reduction in fish populations in some fishing areas and 40 km of Italian coastline impacted by 1,400 barrels of oil.

Prestige, 2002, Galizia (Spain)As a result of the Prestige oil spill there has been an estimated production decrease in the fisheries and aquaculture sector of about 34,000 t and a reduction on revenues of 65 million euro.

Don Pedro, 2007, Ibiza (Spain)The sinking of the Don Pedro merchant ship in 2007, near the island of Ibiza, showed that even a small oil spill (about 20 t), with a series of circumstances that significantly lessened its impact, was sufficient to compromise an entire season in this “sun and sand” tourist destination.

Accidents resulting from oil and gas operations in the Mediterranean Sea from 1970 to 2009

Large scale oil spills (such as the ones of the Exxon Valdez, DeepWater Horizon, Prestige and MTHaven) are likely to occur in the Mediterranean, especially if the oil and gas industry will be further developed. If we assess the potential impacts deriving from extractive activities, including the likely loss of ecosystem

services, against the income produced by key economic sectors (i.e. tourism, fisheries, aquaculture), the balance is clearly negative.Therefore, from an economic point of view, oil and gas activities in the Mediterranean Sea present more risks than benefits.

DATA: WORLD OFFSHORE ACCIDENTS DATABASE

O&GACCIDENTS

(1970-2009)

16 ITALY

5 GREECE

4 SPAIN 3 FRANCE3 MALTA

1 TURKEY1 TUNIS

1 MOROCCO1 LIBYA1 ISRAEL

1 CYPRUS1 ALGERIA

Why we are hereTo stop the degration of the planet’s natural environment and to build a future in which humans live in harmony with nature.

wwf.panda.org

WWF Mediterranean Marine Initiative, Via Po, 25/c – 00198 Rome (Italy)

Developed in collaboration with: Source International Design and layout: Tangerine Lab, Editing: Rottermaier - Servizi Letterari

Oil and gas map: DrillingInfo (2015) – ALES database

RECYCLED100%

![Crude Assay Report · 15 Vacuum Gas Oil Cuts - Gas Oil [325-370°C] 15 16 Vacuum Gas Oil Cuts - Gas Oil 1[370 - 540°C] 16 17 Vacuum Gas Oil Cuts - Heavy Vacuum Gas Oil [370 - 548°C]](https://img.pdfslide.us/doc/110x75/5e68681c2598ff04995c67bc/crude-assay-report-15-vacuum-gas-oil-cuts-gas-oil-325-370c-15-16-vacuum-gas.jpg)