Embed Size (px)

Citation preview

1

HUNGARY Key Figures ____________________________________________________________________ 2

OVERVIEW _____________________________________________________________________ 3

1. Energy Outlook _______________________________________________________________ 4

2. Oil _________________________________________________________________________ 6 2.1 Market Features and Key Issues ________________________________________________________ 6 2.2 Oil Supply Infrastructure ______________________________________________________________ 8 2.3 Decision-making Structure for Oil Emergencies ___________________________________________ 10 2.4 Stocks ____________________________________________________________________________ 11

3. Other Measures _____________________________________________________________ 14 3.1 Demand Restraint ___________________________________________________________________ 14 3.2 Fuel switching ______________________________________________________________________ 15 3.3 Others ____________________________________________________________________________ 15

4. Natural gas _________________________________________________________________ 16 4.1 Market Features and key Issues ________________________________________________________ 16 4.2 Natural Gas Supply Infrastructure ______________________________________________________ 18 4.3 Emergency Policy for Natural Gas ______________________________________________________ 20

List of Figures

Total Primary Energy Supply ----------------------------------------------------------------------------------------------------------4 Electricity Generation, by Fuel Source ---------------------------------------------------------------------------------------------5 Oil Consumption, by Product ---------------------------------------------------------------------------------------------------------6 Oil Imports by Source, 1Q2011 -------------------------------------------------------------------------------------------------------7 Hungary Oil Infrastructure Map ------------------------------------------------------------------------------------------------------8 Refinery Output vs. Demand (kb/d) -------------------------------------------------------------------------------------------------9 Total Oil Stocks, by Type, end-June 2011 ---------------------------------------------------------------------------------------- 11 Compliance with IEA 90-Day Obligation ----------------------------------------------------------------------------------------- 12 Oil Consumption, by Sector --------------------------------------------------------------------------------------------------------- 14 Natural Gas Consumption, by sector --------------------------------------------------------------------------------------------- 16 Natural Gas Imports, by Source ---------------------------------------------------------------------------------------------------- 18 Natural Gas Transmission System ------------------------------------------------------------------------------------------------- 20 Monthly Natural Gas Supply, Demand* and Stock Levels ------------------------------------------------------------------ 21

2

HUNGARY

3

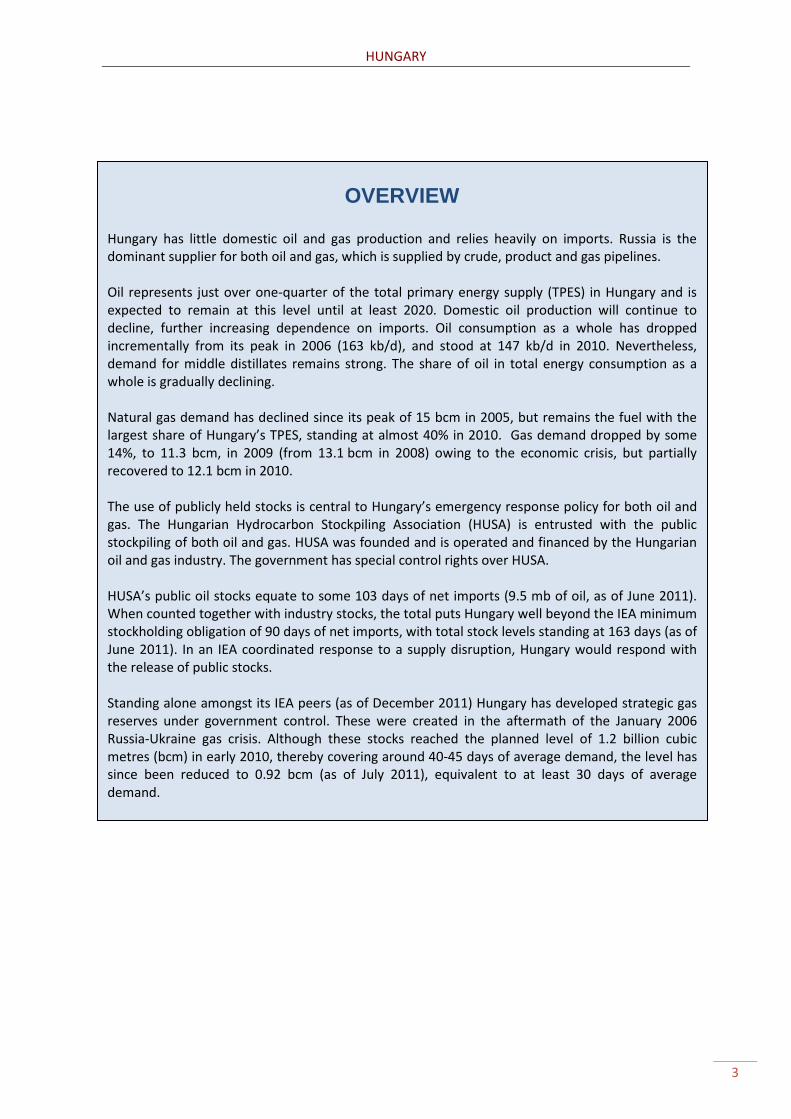

OVERVIEW Hungary has little domestic oil and gas production and relies heavily on imports. Russia is the dominant supplier for both oil and gas, which is supplied by crude, product and gas pipelines. Oil represents just over one-quarter of the total primary energy supply (TPES) in Hungary and is expected to remain at this level until at least 2020. Domestic oil production will continue to decline, further increasing dependence on imports. Oil consumption as a whole has dropped incrementally from its peak in 2006 (163 kb/d), and stood at 147 kb/d in 2010. Nevertheless, demand for middle distillates remains strong. The share of oil in total energy consumption as a whole is gradually declining. Natural gas demand has declined since its peak of 15 bcm in 2005, but remains the fuel with the largest share of Hungary’s TPES, standing at almost 40% in 2010. Gas demand dropped by some 14%, to 11.3 bcm, in 2009 (from 13.1 bcm in 2008) owing to the economic crisis, but partially recovered to 12.1 bcm in 2010. The use of publicly held stocks is central to Hungary’s emergency response policy for both oil and gas. The Hungarian Hydrocarbon Stockpiling Association (HUSA) is entrusted with the public stockpiling of both oil and gas. HUSA was founded and is operated and financed by the Hungarian oil and gas industry. The government has special control rights over HUSA. HUSA’s public oil stocks equate to some 103 days of net imports (9.5 mb of oil, as of June 2011). When counted together with industry stocks, the total puts Hungary well beyond the IEA minimum stockholding obligation of 90 days of net imports, with total stock levels standing at 163 days (as of June 2011). In an IEA coordinated response to a supply disruption, Hungary would respond with the release of public stocks. Standing alone amongst its IEA peers (as of December 2011) Hungary has developed strategic gas reserves under government control. These were created in the aftermath of the January 2006 Russia-Ukraine gas crisis. Although these stocks reached the planned level of 1.2 billion cubic metres (bcm) in early 2010, thereby covering around 40-45 days of average demand, the level has since been reduced to 0.92 bcm (as of July 2011), equivalent to at least 30 days of average demand.

HUNGARY

4

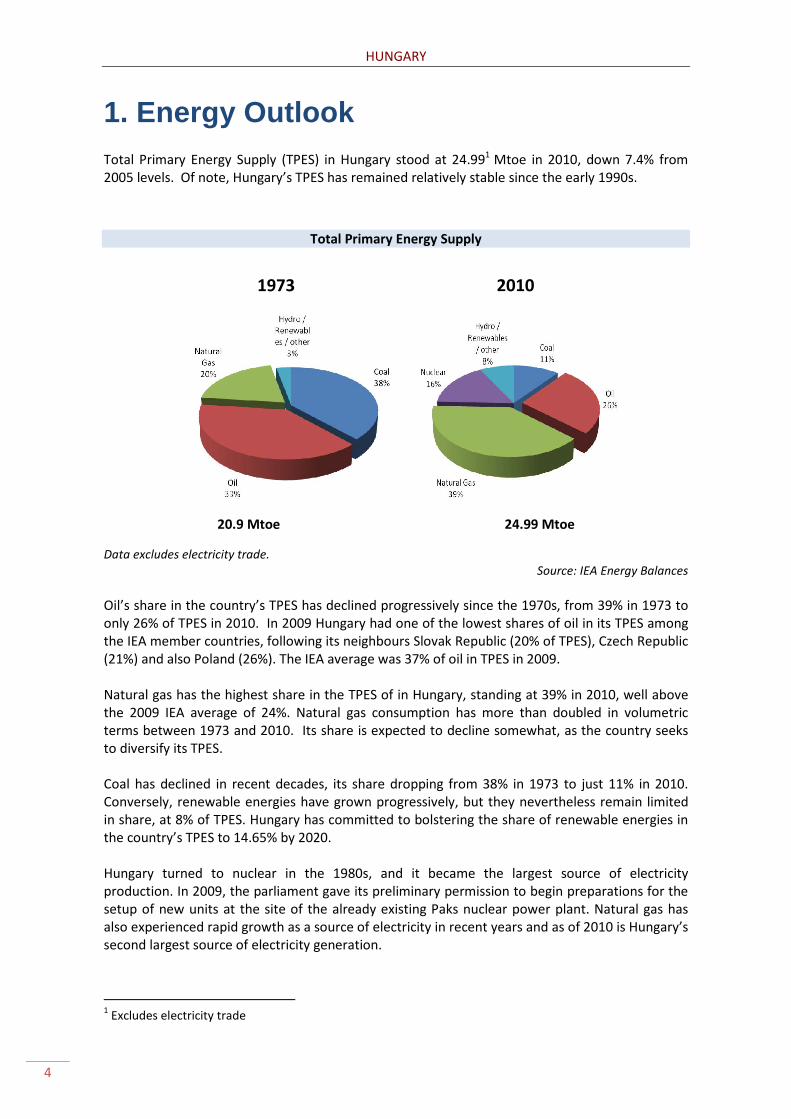

1. Energy Outlook Total Primary Energy Supply (TPES) in Hungary stood at 24.991 Mtoe in 2010, down 7.4% from 2005 levels. Of note, Hungary’s TPES has remained relatively stable since the early 1990s.

Total Primary Energy Supply

1973 2010

20.9 Mtoe 24.99 Mtoe

Data excludes electricity trade. Source: IEA Energy Balances

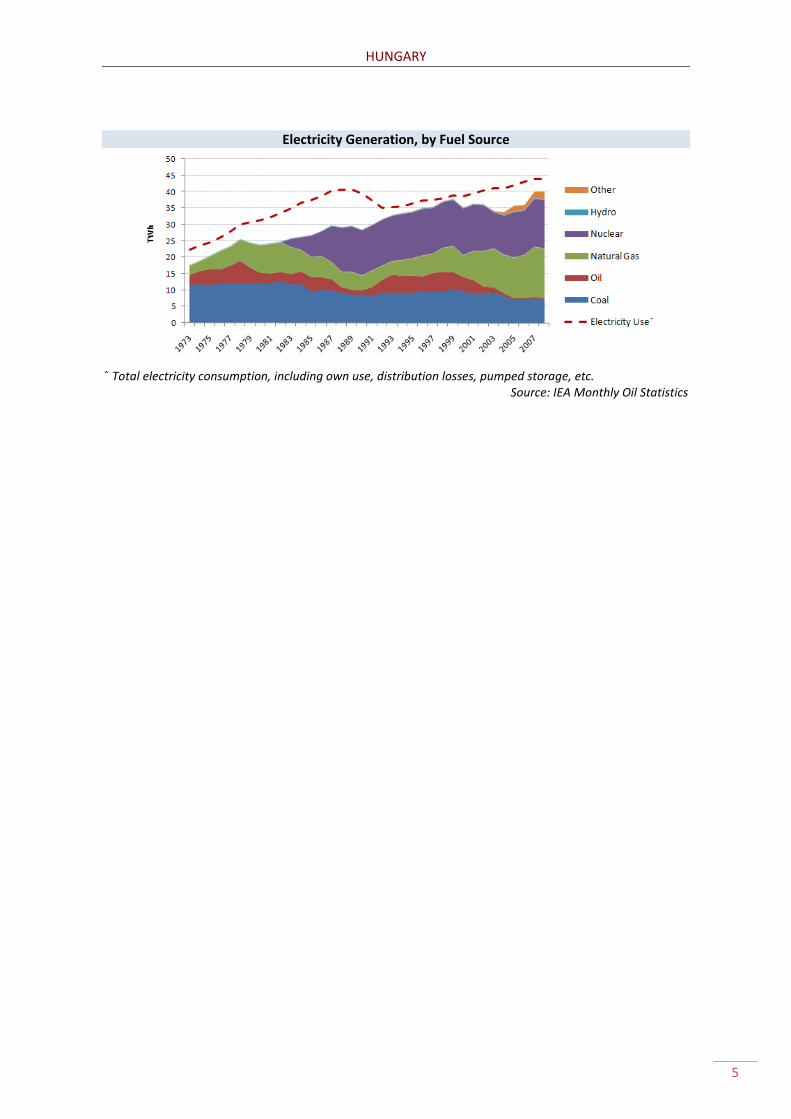

Oil’s share in the country’s TPES has declined progressively since the 1970s, from 39% in 1973 to only 26% of TPES in 2010. In 2009 Hungary had one of the lowest shares of oil in its TPES among the IEA member countries, following its neighbours Slovak Republic (20% of TPES), Czech Republic (21%) and also Poland (26%). The IEA average was 37% of oil in TPES in 2009. Natural gas has the highest share in the TPES of in Hungary, standing at 39% in 2010, well above the 2009 IEA average of 24%. Natural gas consumption has more than doubled in volumetric terms between 1973 and 2010. Its share is expected to decline somewhat, as the country seeks to diversify its TPES. Coal has declined in recent decades, its share dropping from 38% in 1973 to just 11% in 2010. Conversely, renewable energies have grown progressively, but they nevertheless remain limited in share, at 8% of TPES. Hungary has committed to bolstering the share of renewable energies in the country’s TPES to 14.65% by 2020. Hungary turned to nuclear in the 1980s, and it became the largest source of electricity production. In 2009, the parliament gave its preliminary permission to begin preparations for the setup of new units at the site of the already existing Paks nuclear power plant. Natural gas has also experienced rapid growth as a source of electricity in recent years and as of 2010 is Hungary’s second largest source of electricity generation.

1 Excludes electricity trade

HUNGARY

5

Electricity Generation, by Fuel Source

ˆ Total electricity consumption, including own use, distribution losses, pumped storage, etc.

Source: IEA Monthly Oil Statistics

HUNGARY

6

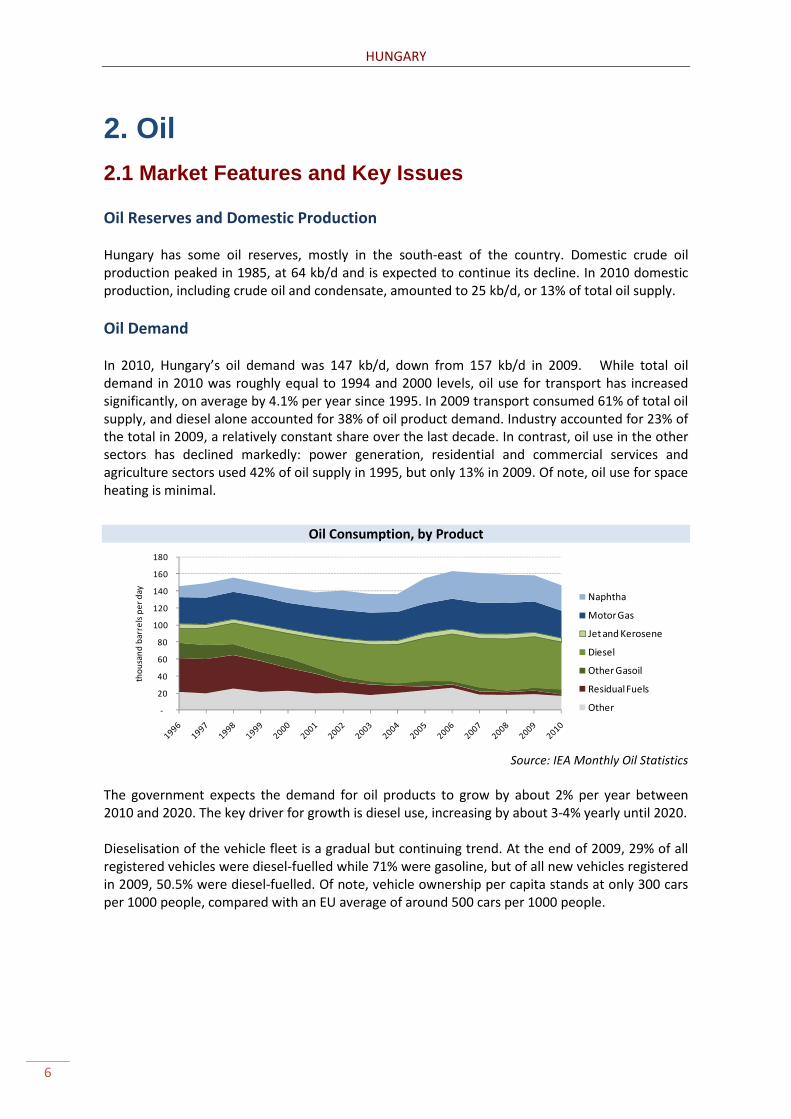

2. Oil 2.1 Market Features and Key Issues Oil Reserves and Domestic Production Hungary has some oil reserves, mostly in the south-east of the country. Domestic crude oil production peaked in 1985, at 64 kb/d and is expected to continue its decline. In 2010 domestic production, including crude oil and condensate, amounted to 25 kb/d, or 13% of total oil supply. Oil Demand In 2010, Hungary’s oil demand was 147 kb/d, down from 157 kb/d in 2009. While total oil demand in 2010 was roughly equal to 1994 and 2000 levels, oil use for transport has increased significantly, on average by 4.1% per year since 1995. In 2009 transport consumed 61% of total oil supply, and diesel alone accounted for 38% of oil product demand. Industry accounted for 23% of the total in 2009, a relatively constant share over the last decade. In contrast, oil use in the other sectors has declined markedly: power generation, residential and commercial services and agriculture sectors used 42% of oil supply in 1995, but only 13% in 2009. Of note, oil use for space heating is minimal.

Oil Consumption, by Product

-

20

40

60

80

100

120

140

160

180

thou

sand

bar

rels

per

day Naphtha

Motor Gas

Jet and Kerosene

Diesel

Other Gasoil

Residual Fuels

Other

Source: IEA Monthly Oil Statistics The government expects the demand for oil products to grow by about 2% per year between 2010 and 2020. The key driver for growth is diesel use, increasing by about 3-4% yearly until 2020. Dieselisation of the vehicle fleet is a gradual but continuing trend. At the end of 2009, 29% of all registered vehicles were diesel-fuelled while 71% were gasoline, but of all new vehicles registered in 2009, 50.5% were diesel-fuelled. Of note, vehicle ownership per capita stands at only 300 cars per 1000 people, compared with an EU average of around 500 cars per 1000 people.

HUNGARY

7

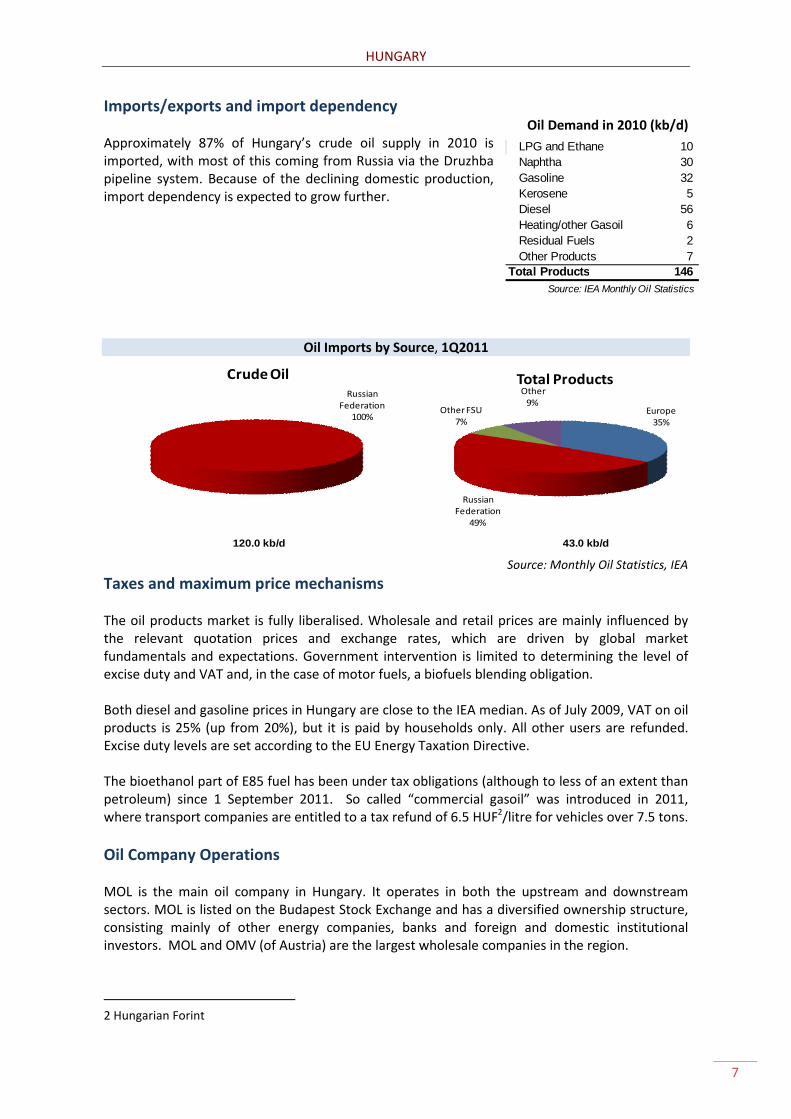

Imports/exports and import dependency Oil Demand in 2010 (kb/d)

Approximately 87% of Hungary’s crude oil supply in 2010 is imported, with most of this coming from Russia via the Druzhba pipeline system. Because of the declining domestic production, import dependency is expected to grow further.

Oil Imports by Source, 1Q2011

120.0 kb/d 43.0 kb/d

Russian Federation

100%

Crude Oil

Europe 35%

Russian Federation

49%

Other FSU7%

Other 9%

Total Products

Source: Monthly Oil Statistics, IEA

Taxes and maximum price mechanisms The oil products market is fully liberalised. Wholesale and retail prices are mainly influenced by the relevant quotation prices and exchange rates, which are driven by global market fundamentals and expectations. Government intervention is limited to determining the level of excise duty and VAT and, in the case of motor fuels, a biofuels blending obligation. Both diesel and gasoline prices in Hungary are close to the IEA median. As of July 2009, VAT on oil products is 25% (up from 20%), but it is paid by households only. All other users are refunded. Excise duty levels are set according to the EU Energy Taxation Directive. The bioethanol part of E85 fuel has been under tax obligations (although to less of an extent than petroleum) since 1 September 2011. So called “commercial gasoil” was introduced in 2011, where transport companies are entitled to a tax refund of 6.5 HUF2/litre for vehicles over 7.5 tons. Oil Company Operations MOL is the main oil company in Hungary. It operates in both the upstream and downstream sectors. MOL is listed on the Budapest Stock Exchange and has a diversified ownership structure, consisting mainly of other energy companies, banks and foreign and domestic institutional investors. MOL and OMV (of Austria) are the largest wholesale companies in the region.

2 Hungarian Forint

LPG and Ethane 10 Naphtha 30 Gasoline 32 Kerosene 5 Diesel 56 Heating/other Gasoil 6 Residual Fuels 2 Other Products 7

Total Products 146 Source: IEA Monthly Oil Statistics

HUNGARY

8

The retail market consists of numerous players. With 363 filling stations, MOL has the largest network. It is followed by Shell (249 stations), Agip (183), OMV (178) and Lukoil (75). In addition, there are some 600 white stations in Hungary, i.e. small private companies with just a few stations. The retail market consolidated from 2006, as OMV bought Q8, BP and Aral, while AGIP bought Tamoil and ExxonMobil, and Shell bought Total and Tesco’s supermarket stations.

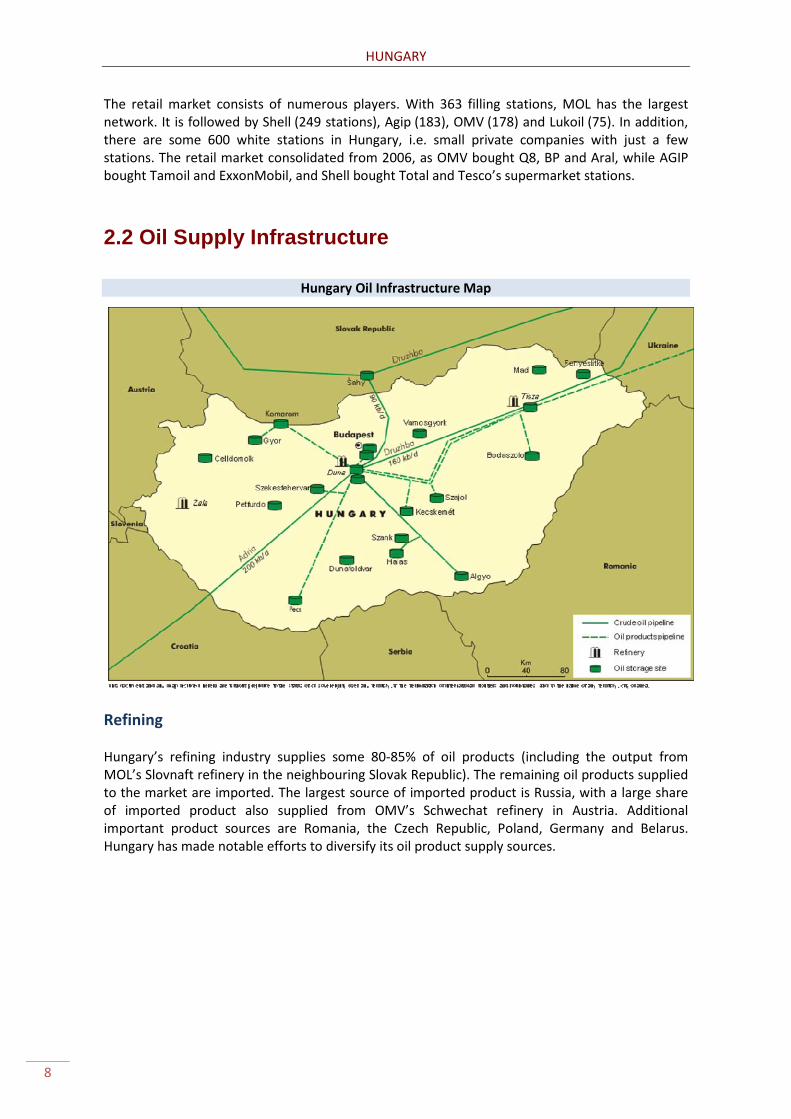

2.2 Oil Supply Infrastructure

Hungary Oil Infrastructure Map

Refining Hungary’s refining industry supplies some 80-85% of oil products (including the output from MOL’s Slovnaft refinery in the neighbouring Slovak Republic). The remaining oil products supplied to the market are imported. The largest source of imported product is Russia, with a large share of imported product also supplied from OMV’s Schwechat refinery in Austria. Additional important product sources are Romania, the Czech Republic, Poland, Germany and Belarus. Hungary has made notable efforts to diversify its oil product supply sources.

HUNGARY

9

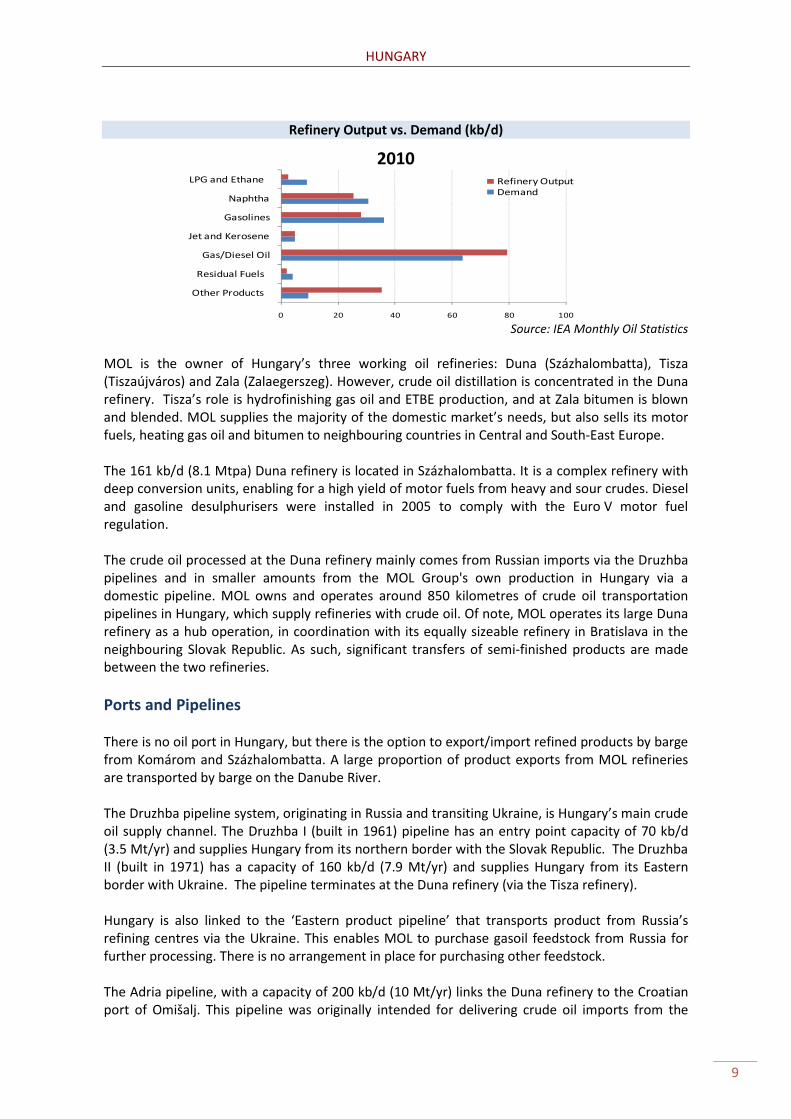

Refinery Output vs. Demand (kb/d)

2010

0 20 40 60 80 100

Other Products

Residual Fuels

Gas/Diesel Oil

Jet and Kerosene

Gasolines

Naphtha

LPG and Ethane Refinery OutputDemand

Source: IEA Monthly Oil Statistics

MOL is the owner of Hungary’s three working oil refineries: Duna (Százhalombatta), Tisza (Tiszaújváros) and Zala (Zalaegerszeg). However, crude oil distillation is concentrated in the Duna refinery. Tisza’s role is hydrofinishing gas oil and ETBE production, and at Zala bitumen is blown and blended. MOL supplies the majority of the domestic market’s needs, but also sells its motor fuels, heating gas oil and bitumen to neighbouring countries in Central and South-East Europe. The 161 kb/d (8.1 Mtpa) Duna refinery is located in Százhalombatta. It is a complex refinery with deep conversion units, enabling for a high yield of motor fuels from heavy and sour crudes. Diesel and gasoline desulphurisers were installed in 2005 to comply with the Euro V motor fuel regulation. The crude oil processed at the Duna refinery mainly comes from Russian imports via the Druzhba pipelines and in smaller amounts from the MOL Group's own production in Hungary via a domestic pipeline. MOL owns and operates around 850 kilometres of crude oil transportation pipelines in Hungary, which supply refineries with crude oil. Of note, MOL operates its large Duna refinery as a hub operation, in coordination with its equally sizeable refinery in Bratislava in the neighbouring Slovak Republic. As such, significant transfers of semi-finished products are made between the two refineries. Ports and Pipelines There is no oil port in Hungary, but there is the option to export/import refined products by barge from Komárom and Százhalombatta. A large proportion of product exports from MOL refineries are transported by barge on the Danube River. The Druzhba pipeline system, originating in Russia and transiting Ukraine, is Hungary’s main crude oil supply channel. The Druzhba I (built in 1961) pipeline has an entry point capacity of 70 kb/d (3.5 Mt/yr) and supplies Hungary from its northern border with the Slovak Republic. The Druzhba II (built in 1971) has a capacity of 160 kb/d (7.9 Mt/yr) and supplies Hungary from its Eastern border with Ukraine. The pipeline terminates at the Duna refinery (via the Tisza refinery). Hungary is also linked to the ‘Eastern product pipeline’ that transports product from Russia’s refining centres via the Ukraine. This enables MOL to purchase gasoil feedstock from Russia for further processing. There is no arrangement in place for purchasing other feedstock. The Adria pipeline, with a capacity of 200 kb/d (10 Mt/yr) links the Duna refinery to the Croatian port of Omišalj. This pipeline was originally intended for delivering crude oil imports from the

HUNGARY

10

Middle East or Africa to Hungary but has mainly been used in the opposite direction, transiting Russian crude oil to the Sisak refinery in Croatia. The Hungarian Administration indicates that in an emergency it would take around thirty days for the Adria pipeline to be reversed in order to transport crude oil from the Adriatic Sea to the Duna refinery. A further pipeline connection from the Duna refinery to Šahy (Slovak Republic) extends the Adria to the Slovak section of the Druzhba. This connection has a capacity of 90 kb/d (3.5 Mt/yr). Hungary also has an internal crude pipeline with a capacity of some 40 kb/d (2.0 Mt/yr), which connects the country’s crude fields in the Algyö region to the Duna refinery. MOL operates 1,356 km of domestic product pipelines to supply the main depots: Székesfehérvár, Pécs, Komárom, Szajol and Tiszaújváros. Storage Capacity Total storage capacity in Hungary stands at some 12.16 million barrels (of which 4.12 mb is for crude and 8.04 mb for products), spread over 10 sites. The operating depot system has been downsized, the result of network optimisation. As of 2011 MOL does not have any plans to change the system in the near future, although there are some closed depots which can be put back into operation within a relatively short timeframe. Of note, no Third Party Access exists for MOL’s terminals, even if they are unused. There are eight public storage terminals (customs warehouses) for finished products, located at Algyő, Csepel, Komárom, Pécs, Szajol, Székesfehérvár, Százhalombatta and Tiszaújváros. These are MOL depots, however MOL’s competitors also operates depots at other locations. Crude storage tanks are located at Százhalombatta, Tiszaújváros and Fényeslitke. They include storage facilities for commercial and strategic stockholding purposes. All customers (wholesalers, white pumpers, end-users, industrial customers and retail networks) are served from the depots. Crude oil stored at Tiszaújváros can be transported via pipeline to Százhalombatta. A few days’ outage can be covered with the existing storage facilities, and no expansion of storage facilities is planned by the industry.

2.3 Decision-making Structure for Oil Emergencies Energy supply is the declared responsibility of the Minister of National Development (‘the Minister’), in co-ordination with the Hungarian Hydrocarbon Stockpiling Association (HUSA) and the relevant stakeholders. Responsibilities include oil security, maintenance and improvement of the emergency response system, and co-ordination with the IEA. The oil National Emergency Strategy Organisation (NESO) is the key stakeholder body for emergency response and it operates under the supervision of the Minister. The political head of the system is the State Secretary for Energy, while the operational head is the Deputy State Secretary for Energy together with the director generals under his/her supervision. In a declared emergency, however, the NESO is directly led by the Minister. The NESO works in close cooperation with HUSA’s Board of Directors. The board includes: representatives of the Ministry of Public Administration and Justice; the Ministry of National Development; oil companies including MOL, ENI, Mabanaft and Shell; appointed expert members of certain partner ministries

HUNGARY

11

(e.g. the Ministry of Interior); the Hungarian Petroleum Association (MÁSz); and the Energy Centre. The legal basis for Hungary’s oil emergency response policy is Act No. XLIX / 1993 on the Emergency Stockholding of Imported Crude Oil and Oil Products (amended in 1997 and in 2004). It outlines the requirements in terms of emergency oil stockpiling held by the Hungarian Hydrocarbon Stockpiling Association (HUSA) and provides the Ministry of National Development with the statutory power to implement demand restraint or release strategic oil stocks in response to an IEA or EU declared emergency. The Act is in line with the relevant European directives (98/93/EC, 73/238/EC and 2006/67/EC). The roles and responsibilities of government Ministries during an emergency are allocated in Government Decree No. 212/2010. (VIII.1) Korm.

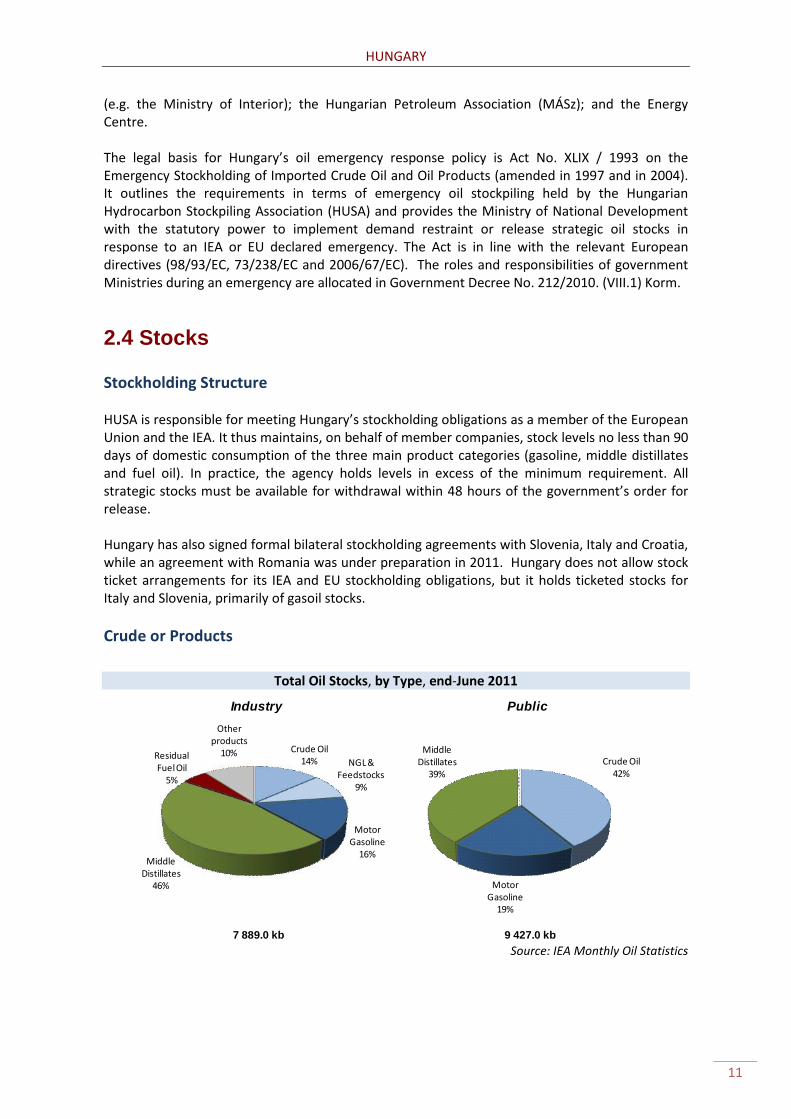

2.4 Stocks Stockholding Structure HUSA is responsible for meeting Hungary’s stockholding obligations as a member of the European Union and the IEA. It thus maintains, on behalf of member companies, stock levels no less than 90 days of domestic consumption of the three main product categories (gasoline, middle distillates and fuel oil). In practice, the agency holds levels in excess of the minimum requirement. All strategic stocks must be available for withdrawal within 48 hours of the government’s order for release. Hungary has also signed formal bilateral stockholding agreements with Slovenia, Italy and Croatia, while an agreement with Romania was under preparation in 2011. Hungary does not allow stock ticket arrangements for its IEA and EU stockholding obligations, but it holds ticketed stocks for Italy and Slovenia, primarily of gasoil stocks. Crude or Products

Total Oil Stocks, by Type, end-June 2011

Industry

7 889.0 kb

Public

9 427.0 kb

Crude Oil42%

Motor Gasoline

19%

Middle Distillates

39%

Crude Oil14% NGL &

Feedstocks9%

Motor Gasoline

16%Middle

Distillates46%

Residual Fuel Oil

5%

Other products

10%

Source: IEA Monthly Oil Statistics

HUNGARY

12

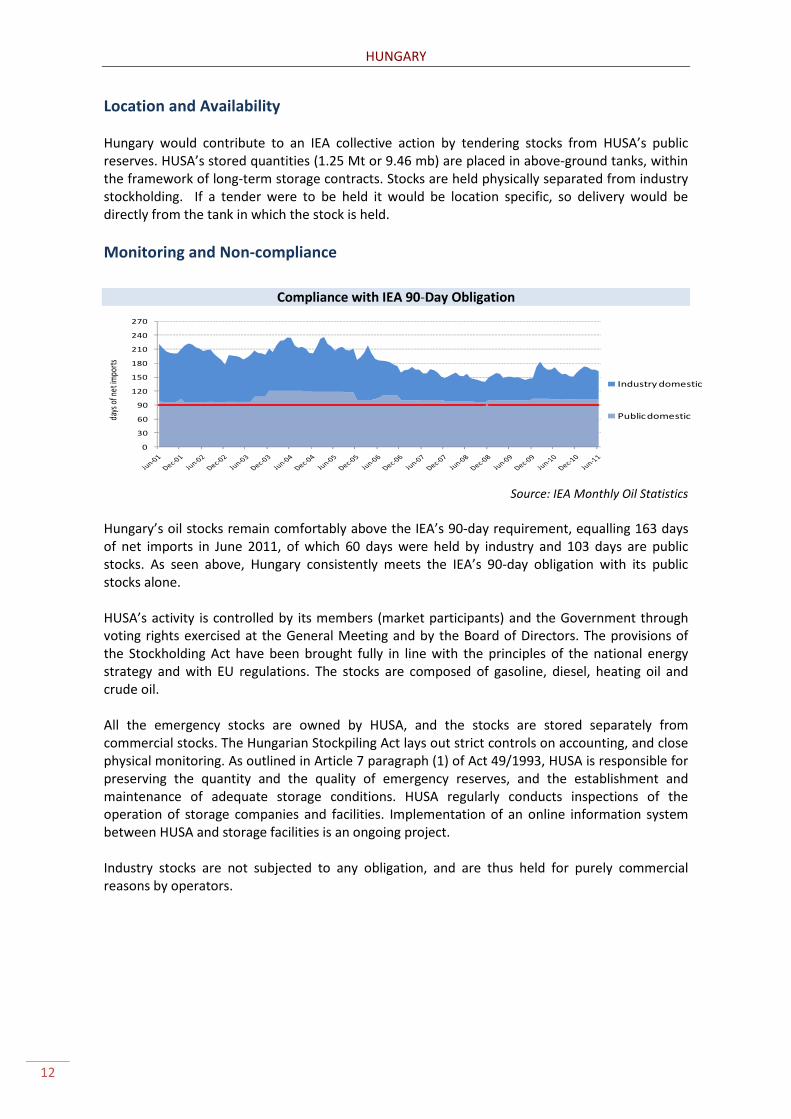

Location and Availability Hungary would contribute to an IEA collective action by tendering stocks from HUSA’s public reserves. HUSA’s stored quantities (1.25 Mt or 9.46 mb) are placed in above-ground tanks, within the framework of long-term storage contracts. Stocks are held physically separated from industry stockholding. If a tender were to be held it would be location specific, so delivery would be directly from the tank in which the stock is held. Monitoring and Non-compliance

Compliance with IEA 90-Day Obligation

0

30

60

90

120

150

180

210

240

270

days

of n

et im

ports

Industry domestic

Public domestic

Source: IEA Monthly Oil Statistics

Hungary’s oil stocks remain comfortably above the IEA’s 90-day requirement, equalling 163 days of net imports in June 2011, of which 60 days were held by industry and 103 days are public stocks. As seen above, Hungary consistently meets the IEA’s 90-day obligation with its public stocks alone. HUSA’s activity is controlled by its members (market participants) and the Government through voting rights exercised at the General Meeting and by the Board of Directors. The provisions of the Stockholding Act have been brought fully in line with the principles of the national energy strategy and with EU regulations. The stocks are composed of gasoline, diesel, heating oil and crude oil. All the emergency stocks are owned by HUSA, and the stocks are stored separately from commercial stocks. The Hungarian Stockpiling Act lays out strict controls on accounting, and close physical monitoring. As outlined in Article 7 paragraph (1) of Act 49/1993, HUSA is responsible for preserving the quantity and the quality of emergency reserves, and the establishment and maintenance of adequate storage conditions. HUSA regularly conducts inspections of the operation of storage companies and facilities. Implementation of an online information system between HUSA and storage facilities is an ongoing project. Industry stocks are not subjected to any obligation, and are thus held for purely commercial reasons by operators.

HUNGARY

13

Stock and Timeframe Drawdown In the event of a supply disruption, the drawdown of the stocks is ordered by the Minister, on the basis of consultations with the NESO members. As HUSA is a member of NESO, the drawdown process can be started immediately. Following the declaration of an oil supply disruption HUSA member companies have 48 hours to declare their quota (i.e. the amount they have the right to purchase from the stockdraw), after which those not exerting their right forgo all access to the stockdraw. The Minister then has the right to choose how to allocate any unclaimed stocks, either by awarding pre-emptive purchase rights to selected consumers or by asking HUSA to call for tenders from its member companies. Up to 2011 the Hungarian Stockpiling Act did not allow for these emergency stocks to be tendered to companies that are not HUSA members, including foreign companies. However, this might change in 2012, when Hungary implements the new EU Council Directive 2009/119/EC, which obliges Hungary to change its legislation. Because of its size in the Hungarian market, MOL is generally entitled to approximately 80% of product volumes being tendered. Of note, MOL is the only crude oil importer and refining company in Hungary, and thus is the only company with a right to a crude tender. The time lag for physical delivery of stocks to market after a release decision depends on the type of stock released. The time lag would be used to fulfil the stockdraw regulations (allocation for the member companies, signing commercial contracts, presenting bank guarantees, etc). Physical deliveries are possible within 48-72 hours following a stock draw decision. Financing and Fees HUSA is an independent, not-for-profit company. It is financed by compulsory membership of all crude and oil product and gas traders in Hungary. Membership levies are proportionate to the percentage of oil and gas the company puts in circulation on the domestic market. Storage costs (including the renting fee of capacities) account for 75-80% of HUSA’s yearly budget. Financing costs (acquisition loans, interest on stock financing loans) account for 18-23%, and some 1-2% is attributed to the cost of operation. The purchase and storage of stocks are financed by short- and medium-term bank loans. Interest payments and storage costs are covered by members’ contribution fees paid. Total operational costs stood at € 43 million in 2010 (i.e., some € 4.50 a barrel), of which € 16.5 million was for crude stocks.

HUNGARY

14

3. Other Measures

3.1 Demand Restraint

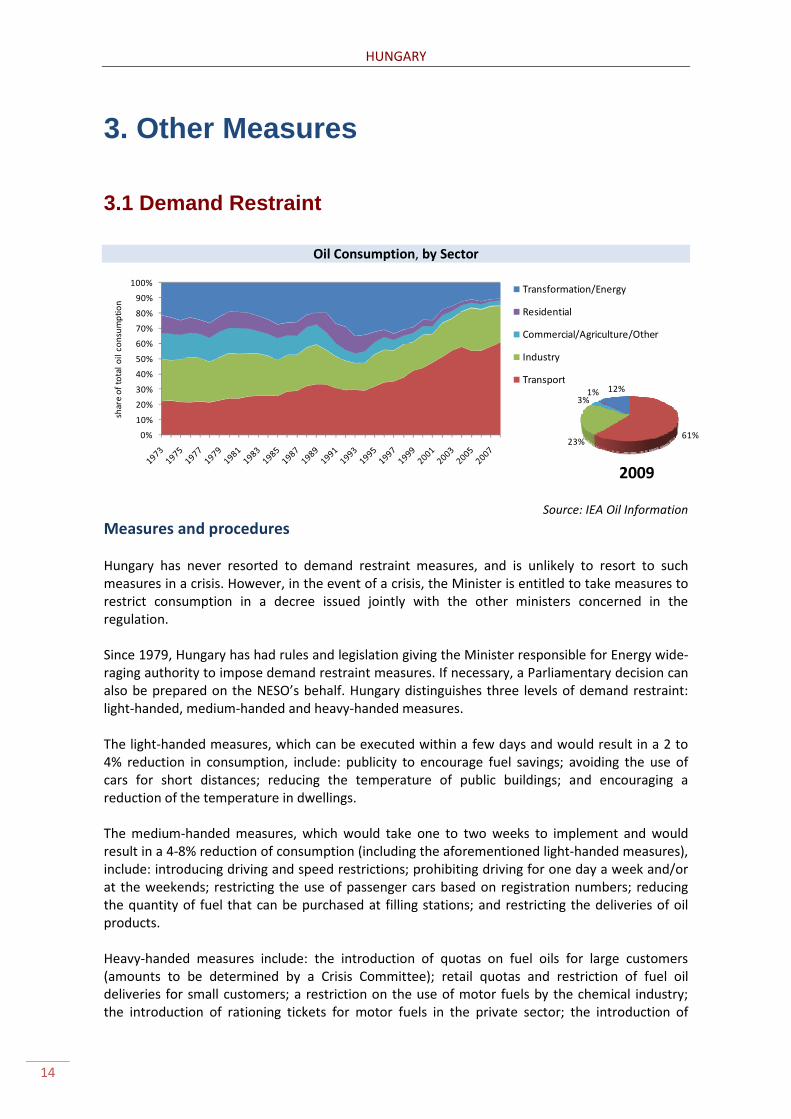

Oil Consumption, by Sector

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

shar

e of

tota

l oil

cons

umpt

ion

Transformation/Energy

Residential

Commercial/Agriculture/Other

Industry

Transport

61%23%

3%1% 12%

2009

Source: IEA Oil Information

Measures and procedures Hungary has never resorted to demand restraint measures, and is unlikely to resort to such measures in a crisis. However, in the event of a crisis, the Minister is entitled to take measures to restrict consumption in a decree issued jointly with the other ministers concerned in the regulation. Since 1979, Hungary has had rules and legislation giving the Minister responsible for Energy wide-raging authority to impose demand restraint measures. If necessary, a Parliamentary decision can also be prepared on the NESO’s behalf. Hungary distinguishes three levels of demand restraint: light-handed, medium-handed and heavy-handed measures. The light-handed measures, which can be executed within a few days and would result in a 2 to 4% reduction in consumption, include: publicity to encourage fuel savings; avoiding the use of cars for short distances; reducing the temperature of public buildings; and encouraging a reduction of the temperature in dwellings. The medium-handed measures, which would take one to two weeks to implement and would result in a 4-8% reduction of consumption (including the aforementioned light-handed measures), include: introducing driving and speed restrictions; prohibiting driving for one day a week and/or at the weekends; restricting the use of passenger cars based on registration numbers; reducing the quantity of fuel that can be purchased at filling stations; and restricting the deliveries of oil products. Heavy-handed measures include: the introduction of quotas on fuel oils for large customers (amounts to be determined by a Crisis Committee); retail quotas and restriction of fuel oil deliveries for small customers; a restriction on the use of motor fuels by the chemical industry; the introduction of rationing tickets for motor fuels in the private sector; the introduction of

HUNGARY

15

quotas on motor fuels in the public sector; and the allocation of quotas on motor fuels for the trading and services sector. The impact of the heavy-handed measures has not been quantified and could take 2-3 months to have an effect.

3.2 Fuel switching There is virtually no ability to switch from oil to other fuels. A limited amount of fuel switching from natural gas to oil exists.

3.3 Others Hungary does not have any potential for increased indigenous production in an emergency; the Hungarian oil fields produce at full capacity.

HUNGARY

16

4. Natural gas

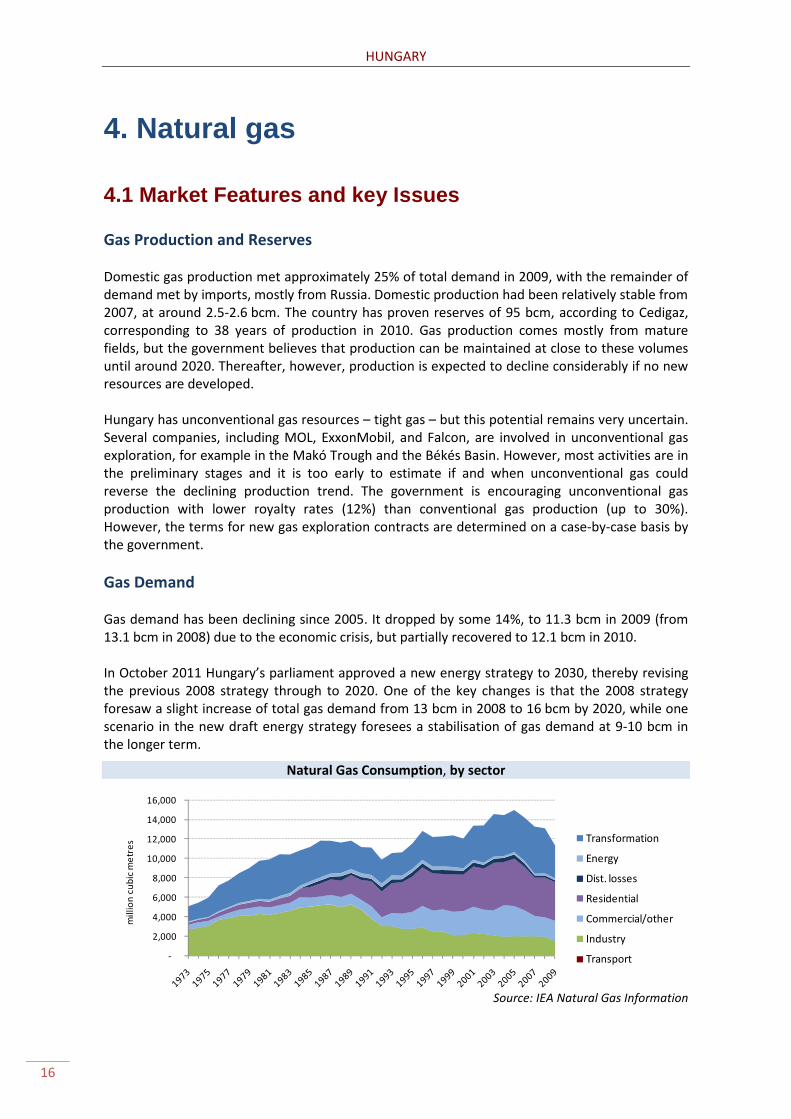

4.1 Market Features and key Issues Gas Production and Reserves Domestic gas production met approximately 25% of total demand in 2009, with the remainder of demand met by imports, mostly from Russia. Domestic production had been relatively stable from 2007, at around 2.5-2.6 bcm. The country has proven reserves of 95 bcm, according to Cedigaz, corresponding to 38 years of production in 2010. Gas production comes mostly from mature fields, but the government believes that production can be maintained at close to these volumes until around 2020. Thereafter, however, production is expected to decline considerably if no new resources are developed. Hungary has unconventional gas resources – tight gas – but this potential remains very uncertain. Several companies, including MOL, ExxonMobil, and Falcon, are involved in unconventional gas exploration, for example in the Makó Trough and the Békés Basin. However, most activities are in the preliminary stages and it is too early to estimate if and when unconventional gas could reverse the declining production trend. The government is encouraging unconventional gas production with lower royalty rates (12%) than conventional gas production (up to 30%). However, the terms for new gas exploration contracts are determined on a case-by-case basis by the government. Gas Demand Gas demand has been declining since 2005. It dropped by some 14%, to 11.3 bcm in 2009 (from 13.1 bcm in 2008) due to the economic crisis, but partially recovered to 12.1 bcm in 2010. In October 2011 Hungary’s parliament approved a new energy strategy to 2030, thereby revising the previous 2008 strategy through to 2020. One of the key changes is that the 2008 strategy foresaw a slight increase of total gas demand from 13 bcm in 2008 to 16 bcm by 2020, while one scenario in the new draft energy strategy foresees a stabilisation of gas demand at 9-10 bcm in the longer term.

Natural Gas Consumption, by sector

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

mill

ion

cubi

c m

etre

s Transformation

Energy

Dist. losses

Residential

Commercial/other

Industry

Transport

Source: IEA Natural Gas Information

HUNGARY

17

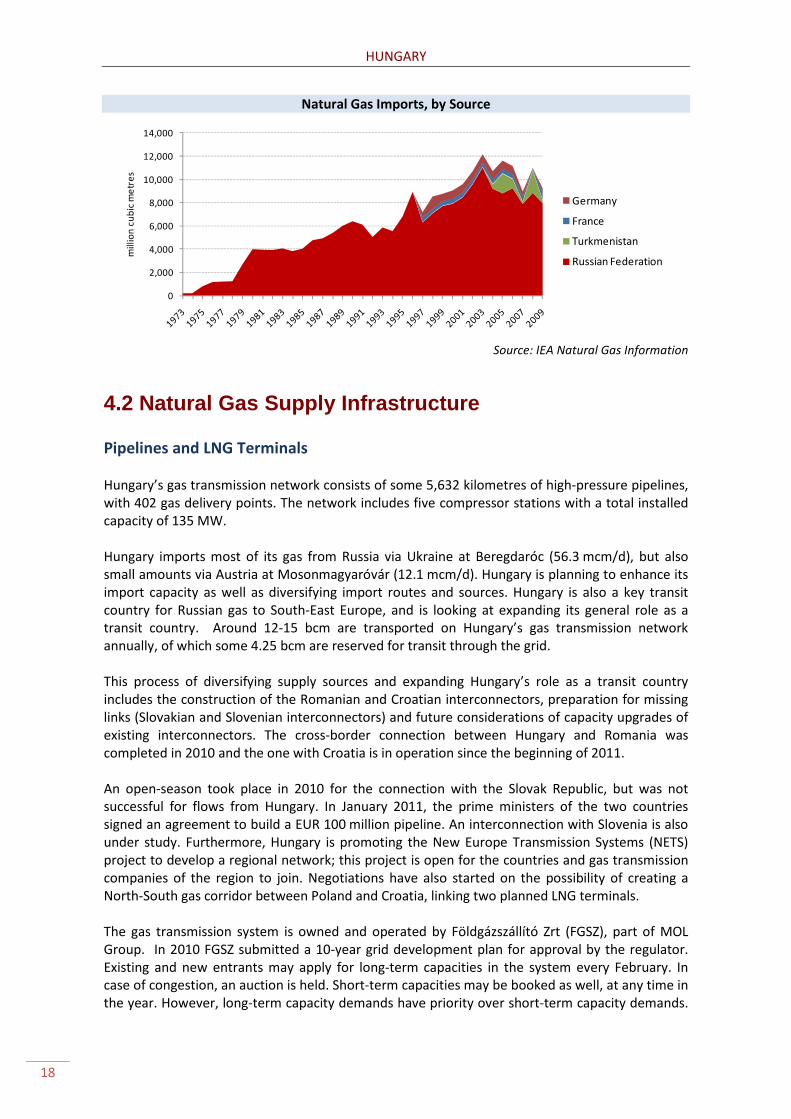

The residential sector is the largest consumer of natural gas in Hungary, standing at some 35% of total gas demand in 2009. As such, the supplies of natural gas are of paramount importance in the cold winter months, as many homes depend on gas for residential use and heating. Equally important, the transformation sector accounted for around 30% of gas demand. The commercial sector accounted for 17% of gas demand, and industry accounted for another 13%. It is worth noting that the industrial sector and power producers were particularly affected by the recession in 2009. Gas consumption in the power sector fell by 4% in 2008 and by 28% in 2009, and gas consumption by industry underwent a 26% decline. Future gas demand in Hungary faces considerable uncertainty. The residential and commercial sectors have high potential for energy savings, with energy efficiency measures expected to save an estimated 1.5-2 bcm per year by 2030. However, consumption in power generation is expected to grow further within the same timeframe (by another 3.5-4 bcm per year), as many new “mid-merit” and “peaking” gas-fired plants are under construction or are planned. Peak demand in winter is typically 75-80 mcm/d (it was 74.3 mcm/d in 2009). The historical record for peak demand was 91.7 mcm/d, reached in 2005. Government estimates indicate that peak demand could reach 100 mcm/d by 2020. Typical winter demand is usually met as follows: imports 40-50 mcm/d, domestic production 8-10 mcm/d and storage withdrawal 20 mcm/d. The storage withdrawal capacity and imports vary according to the shippers’ demand. In 2011 import capacity stands at 68.3 mcm/d, domestic production can reach 10.5 mcm/d and storage withdrawal around 80 mcm/d, including 20 mcm/d of strategic storage. Hungary can thus meet its gas demand in an N-1 situation. Hungary’s power sector is heavily dependent on natural gas. Almost a third of Hungary’s electricity was produced from natural gas in 2010. Import Dependency Hungary imports approximately 75% of its natural gas demand. Net imports of gas in 2010 amounted to around 9.4 bcm, down from 9.6 bcm in 2009 and 11.4 bcm in 2008. More than 80% of imports come from Russia, with small amounts also coming from other former Soviet Union countries, France and Germany. Imports from Western Europe have increased incrementally since 2008, as traders have taken the opportunity of cheaper spot gas from this region. Yet despite the Russia-Ukraine crisis in early 2009, Russian and Russia-transiting Turkmen gas still account for most of the supplies, and have actually increased as a share of total imports to Hungary. As of 1 July 2010, 20% of the import capacity is reserved for short-term capacity booking contracts.

HUNGARY

18

Natural Gas Imports, by Source

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000m

illio

n cu

bic

met

res

Germany

France

Turkmenistan

Russian Federation

Source: IEA Natural Gas Information

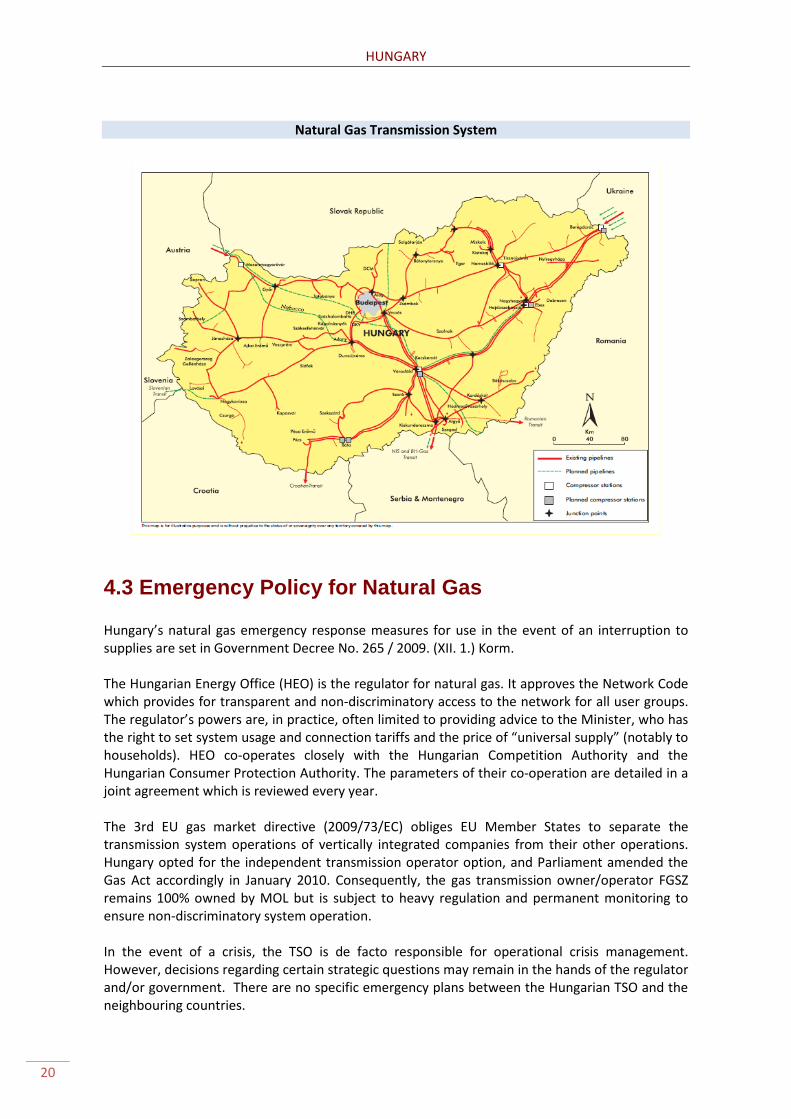

4.2 Natural Gas Supply Infrastructure Pipelines and LNG Terminals Hungary’s gas transmission network consists of some 5,632 kilometres of high-pressure pipelines, with 402 gas delivery points. The network includes five compressor stations with a total installed capacity of 135 MW. Hungary imports most of its gas from Russia via Ukraine at Beregdaróc (56.3 mcm/d), but also small amounts via Austria at Mosonmagyaróvár (12.1 mcm/d). Hungary is planning to enhance its import capacity as well as diversifying import routes and sources. Hungary is also a key transit country for Russian gas to South-East Europe, and is looking at expanding its general role as a transit country. Around 12-15 bcm are transported on Hungary’s gas transmission network annually, of which some 4.25 bcm are reserved for transit through the grid. This process of diversifying supply sources and expanding Hungary’s role as a transit country includes the construction of the Romanian and Croatian interconnectors, preparation for missing links (Slovakian and Slovenian interconnectors) and future considerations of capacity upgrades of existing interconnectors. The cross-border connection between Hungary and Romania was completed in 2010 and the one with Croatia is in operation since the beginning of 2011. An open-season took place in 2010 for the connection with the Slovak Republic, but was not successful for flows from Hungary. In January 2011, the prime ministers of the two countries signed an agreement to build a EUR 100 million pipeline. An interconnection with Slovenia is also under study. Furthermore, Hungary is promoting the New Europe Transmission Systems (NETS) project to develop a regional network; this project is open for the countries and gas transmission companies of the region to join. Negotiations have also started on the possibility of creating a North-South gas corridor between Poland and Croatia, linking two planned LNG terminals. The gas transmission system is owned and operated by Földgázszállító Zrt (FGSZ), part of MOL Group. In 2010 FGSZ submitted a 10-year grid development plan for approval by the regulator. Existing and new entrants may apply for long-term capacities in the system every February. In case of congestion, an auction is held. Short-term capacities may be booked as well, at any time in the year. However, long-term capacity demands have priority over short-term capacity demands.

HUNGARY

19

If booked capacity is not nominated, the Transmission System Operator (TSO) has to offer available capacity to system users. An open season procedure is used in the case of new international pipelines or interconnectors. Of note, companies can only book pipeline capacity if they have a gas purchase contract. Storage Gas storage is crucial because of the high dependence of Hungary’s electricity sector on gas-fired power plants, and because of the high volumes of relatively inflexible residential demand. Hungary has five commercial storage facilities, with a total working capacity of 5.43 bcm and a withdrawal capacity of 72.0 mcm/d at the beginning of winter. All commercial storage can be accessed by third parties. Following the supply interruption of January 2006, the Hungarian Parliament approved a new law, Act No. XXVI, 2006 on Safety Stockpiling of Natural Gas in February 2006. According to the Act a strategic underground gas storage of 1.2 bcm was to be built, so as to provide Hungary with 40-45 days of autonomy if the main import source from Russia failed. The strategic storage facility is located at Szöreg and initially had a 1.2 bcm working capacity and a withdrawal rate of 20 mcm/d for at least 45 days. The stockpile aims to protect households as well as customers who cannot switch to other energy sources. MOL won the tender for the construction of the facility. The Hungarian Hydrocarbon Stockpiling Association (HUSA) and MOL established MMBF Zrt to own and operate the storage facility, which was completed in 2010. The gas is owned by HUSA. In June 2010, Hungary amended the legislation with a view to allowing for a reduction in the minimum strategic stockholding level, the level of which is to be determined on a yearly basis by the Minister. As of May 2011, some 280 mcm had been sold with a view to bringing stocks in line with declining gas consumption, bringing the country’s strategic stock levels down to 0.92 bcm. This sale also helped alleviate high household gas prices.

HUNGARY

20

Natural Gas Transmission System

4.3 Emergency Policy for Natural Gas Hungary’s natural gas emergency response measures for use in the event of an interruption to supplies are set in Government Decree No. 265 / 2009. (XII. 1.) Korm. The Hungarian Energy Office (HEO) is the regulator for natural gas. It approves the Network Code which provides for transparent and non-discriminatory access to the network for all user groups. The regulator’s powers are, in practice, often limited to providing advice to the Minister, who has the right to set system usage and connection tariffs and the price of “universal supply” (notably to households). HEO co-operates closely with the Hungarian Competition Authority and the Hungarian Consumer Protection Authority. The parameters of their co-operation are detailed in a joint agreement which is reviewed every year. The 3rd EU gas market directive (2009/73/EC) obliges EU Member States to separate the transmission system operations of vertically integrated companies from their other operations. Hungary opted for the independent transmission operator option, and Parliament amended the Gas Act accordingly in January 2010. Consequently, the gas transmission owner/operator FGSZ remains 100% owned by MOL but is subject to heavy regulation and permanent monitoring to ensure non-discriminatory system operation. In the event of a crisis, the TSO is de facto responsible for operational crisis management. However, decisions regarding certain strategic questions may remain in the hands of the regulator and/or government. There are no specific emergency plans between the Hungarian TSO and the neighbouring countries.

HUNGARY

21

In the case of natural gas, the structure of the natural gas NESO is similar to the oil NESO, but the crisis committee includes partners from the natural gas industry such as FGSZ and EoN and other relevant authorities.

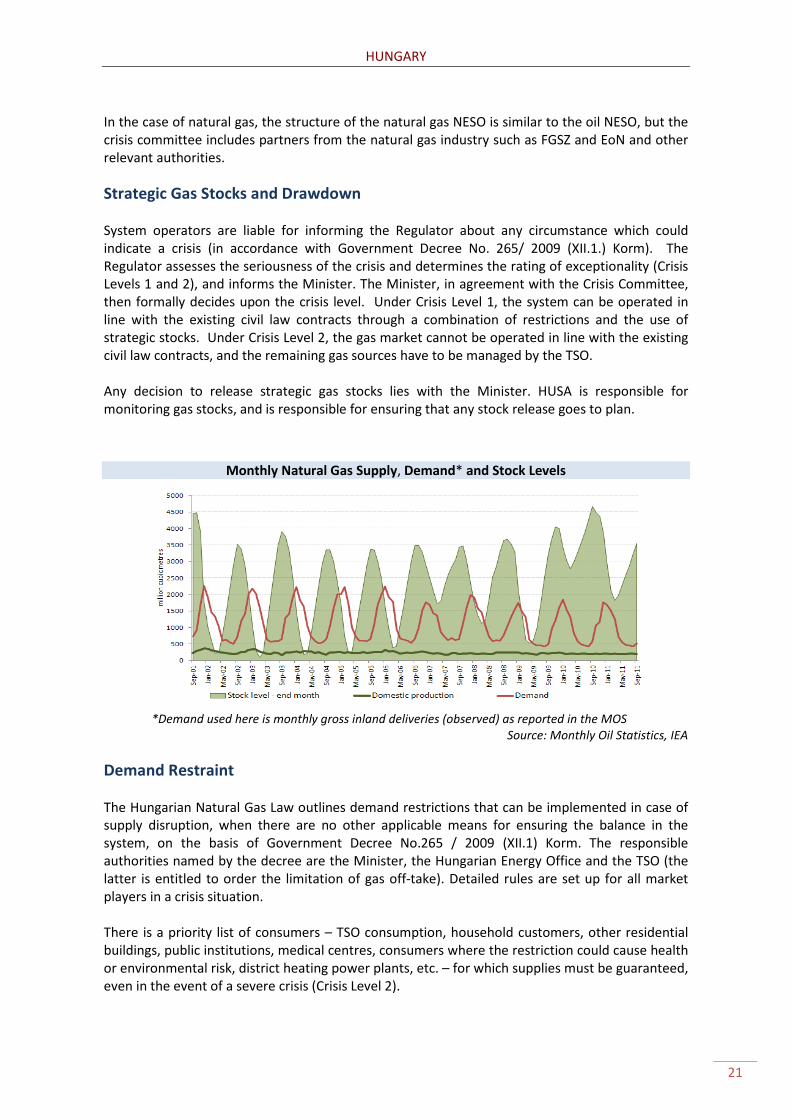

Strategic Gas Stocks and Drawdown System operators are liable for informing the Regulator about any circumstance which could indicate a crisis (in accordance with Government Decree No. 265/ 2009 (XII.1.) Korm). The Regulator assesses the seriousness of the crisis and determines the rating of exceptionality (Crisis Levels 1 and 2), and informs the Minister. The Minister, in agreement with the Crisis Committee, then formally decides upon the crisis level. Under Crisis Level 1, the system can be operated in line with the existing civil law contracts through a combination of restrictions and the use of strategic stocks. Under Crisis Level 2, the gas market cannot be operated in line with the existing civil law contracts, and the remaining gas sources have to be managed by the TSO. Any decision to release strategic gas stocks lies with the Minister. HUSA is responsible for monitoring gas stocks, and is responsible for ensuring that any stock release goes to plan.

Monthly Natural Gas Supply, Demand* and Stock Levels

*Demand used here is monthly gross inland deliveries (observed) as reported in the MOS

Source: Monthly Oil Statistics, IEA

Demand Restraint The Hungarian Natural Gas Law outlines demand restrictions that can be implemented in case of supply disruption, when there are no other applicable means for ensuring the balance in the system, on the basis of Government Decree No.265 / 2009 (XII.1) Korm. The responsible authorities named by the decree are the Minister, the Hungarian Energy Office and the TSO (the latter is entitled to order the limitation of gas off-take). Detailed rules are set up for all market players in a crisis situation. There is a priority list of consumers – TSO consumption, household customers, other residential buildings, public institutions, medical centres, consumers where the restriction could cause health or environmental risk, district heating power plants, etc. – for which supplies must be guaranteed, even in the event of a severe crisis (Crisis Level 2).

HUNGARY

22

The other consumers can have their gas supplies curtailed, and are divided into eight specific “limitation” categories. These categories are prioritised, depending on the size and nature of the consumption sectors. Consumers in higher limitation categories can have their gas supplies limited only if all limitations for lower limitation categories have been exhausted. The first category consists of consumers which must be able to reduce consumption and switch to other fuels within four hours of notification. According to the TSO’s website they have a capacity of 760,167 m3/h. Additional demand restraint measures at the government’s disposal in a crisis are: reducing the opening hours and heating temperature of public buildings; appointing free public holidays; and removing the excise tax on imported fuel oils to incentivise fuel switching from natural gas. Fuel switching The Hungarian Electricity Law (Act No. LXXXVI / 2007) obliges power-plants with over 50 MW output to hold so-called normative and emergency oil stocks, both of which must correspond to a minimum of eight days of average fuel consumption. These power plants account for around 10-12% of total booked gas supply capacity. Some 34 kb/d of gas could be switched to oil in the event of a crisis. Interruptible contracts The TSO has indicated that the total volume of interruptible contracts could amount to some 5-6 mcm/d. However, the TSO has also indicated that it only knows the interruptible capacities and that the interruptible volumes are known and handled by the traders. Surge production For gas, the “normal” natural gas production level stands at around 7.5-8 mcm/day. In the event of an emergency, production can be increased by 0.5 mcm/day over a maximum period of 2-3 months.

Compliance with EU legislation All European Union Member States are required to comply with Regulation No. 994/2010/EC concerning measures to safeguard security of gas supply. By end-2011, each Member State was to designate a Competent Authority that would ensure the implementation of the measures provided for in the regulation. Of note, the regulation requires European Union Member States to undertake a risk assessment of their gas system.

INTERNATIONAL ENERGY AGENCY

The International Energy Agency (IEA), an autonomous agency, was established in November 1974. Its primary mandate was – and is – two-fold: to promote energy security amongst its member countries through collective response to physical disruptions in oil supply, and provide authoritative

research and analysis on ways to ensure reliable, affordable and clean energy for its 28 member countries and beyond. The IEA carries out a comprehensive programme of energy co-operation among its member countries, each of which is obliged to hold oil stocks equivalent to 90 days of its net imports. The Agency’s aims include the following objectives:

n Secure member countries’ access to reliable and ample supplies of all forms of energy; in particular, through maintaining effective emergency response capabilities in case of oil supply disruptions.

n Promote sustainable energy policies that spur economic growth and environmental protection in a global context – particularly in terms of reducing greenhouse-gas emissions that contribute to climate change.

n Improve transparency of international markets through collection and analysis of energy data.

n Support global collaboration on energy technology to secure future energy supplies and mitigate their environmental impact, including through improved energy

efficiency and development and deployment of low-carbon technologies.

n Find solutions to global energy challenges through engagement and dialogue with non-member countries, industry, international

organisations and other stakeholders. IEA member countries:

Australia Austria

Belgium Canada

Czech RepublicDenmark

Finland France

GermanyGreece

HungaryIreland

ItalyJapan

Korea (Republic of)LuxembourgNetherlandsNew Zealand NorwayPolandPortugalSlovak RepublicSpainSwedenSwitzerland

TurkeyUnited Kingdom

United States

The European Commission also participates in

the work of the IEA.

Please note that this publication is subject to specific restrictions that limit its use and distribution.

The terms and conditions are available online at www.iea.org/about/copyright.asp

© OECD/IEA, 2012International Energy Agency

9 rue de la Fédération 75739 Paris Cedex 15, France

www.iea.org