Embed Size (px)

Citation preview

Oil and Gas Industry Economic and

Fiscal Contributions in Colorado by County, 2014

Conducted by:

BUSINESS RESEARCH DIVISION Leeds School of Business

University of Colorado Boulder 420 UCB

Boulder, CO 80309-0420 Telephone: 303-492-3307 colorado.edu/business/brd

Research Team Richard Wobbekind Brian Lewandowski

Report for the Colorado Oil and Gas Association

December 2015

Business Research Division • Leeds School of Business • University of Colorado Boulder Page i

TABLE OF CONTENTS Table of Contents ................................................................................................................................................ i Executive Summary ............................................................................................................................................ 2 Methodology ...................................................................................................................................................... 3 Industry Employment, Firms, and Wages ........................................................................................................... 4 Oil and Gas Industry Economic Impact ............................................................................................................... 5

Commodity Prices ........................................................................................................................................... 5 Production and Value of Production .............................................................................................................. 8 Weld County Oil and Gas Production ........................................................................................................... 11

Oil and Gas Industry Public Revenue ................................................................................................................ 13 Property Taxes .............................................................................................................................................. 13 Public Leases and Royalties .......................................................................................................................... 14 Severance Taxes ........................................................................................................................................... 16 Distribution of Federal Mineral Lease Proceeds and State Severance Tax Revenue ................................... 18 Colorado Oil and Gas Converation Commission Taxes ................................................................................. 18 Income Taxes ................................................................................................................................................ 18

Conclusion ........................................................................................................................................................ 19 Bibliography ...................................................................................................................................................... 20 Appendix 1: Employment and Wages by County ............................................................................................. 22

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 2

EXECUTIVE SUMMARY The oil and gas industry, along with nearly all extraction industries, inherently provides substantial

economic benefits due to its integrated supply chain, high wage jobs, and propensity to sell nationally and

globally. Much of Colorado’s oil and gas is sold outside of the state, contributing wealth to owners,

employees, governments, and schools, all of which are beneficiaries of oil and gas revenues.

In 2014, Colorado’s upstream and midstream oil and gas industry includes drilling, extraction, support

activities, pipeline construction, and pipeline transportation. The industry recorded $15.8 billion in

production value, accounting for 38,650 direct jobs with average annual wages in excess of $105,000—

twice the average wage of all industries in Colorado. Collectively, this industry contributed nearly $4.1

billion in employee income to Colorado households in 2014.

Examining the multiplier effect of industry spending, or the churn of dollars spent along the industry supply

chain and by income earners, the total economic impact of the industry was $31.7 billion in 2014,

supporting 102,700 jobs and $7.6 billion in compensation.

The oil and gas industry contributed to public revenue in 2014, primarily through property, income, and

severance taxes and through public land leases and royalties. These revenue streams totaled nearly $1.2

billion in 2014. This industry is subject to taxes and assessments beyond what other industries contribute.

Ad valorem taxes, for instance, are 3 times higher for oil and gas production than for commercial property

within the state and 11 times higher than residential property. Oil and gas property taxes exceeded an

estimated $400 million in 2014. Severance taxes paid by the industry totaled $330 million in 2014. The

industry also paid $315 million in royalties, rents, and bonus to federal government in 2014, and nearly

$160 million in state royalties, rents, and bonuses.

As oil production ramps up in Colorado, the energy industry in the state is no longer dominated by gas

production. In 2014, oil accounted for 52% of sales-based value, natural gas accounted for 44%, and carbon

dioxide, 4%.

Industry activity peaked in 2014, with drilling and employment decreasing in 2015 based on lower oil and

gas prices. Overall, production continued to increase through mid-2015 primarily due to new production in

Weld County.

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 3

METHODOLOGY This study quantifies the economic impacts of oil and gas industry activity in Colorado by county using

publicly available industry data. The Bureau of Economic Analysis quantifies industry gross domestic

product (GDP). The Bureau of Labor Statistics and the Colorado Department of Labor and Employment

aggregate nonfarm employment and wages by industry and by county, and the U.S. Census Bureau

estimates nonemployer firms and receipts in Colorado by metropolitan statistical area (MSA).1 The Office of

Natural Resources Revenue publishes federal land leases, bonuses, and royalties by state, and the State

Land Board publishes commensurate data for state lands in Colorado. Other local sources, including the

Colorado Geological Survey; the Colorado Department of Local Affairs (DOLA), Division of Property

Taxation; and the Colorado Department of Revenue, provide estimates of the value of production, direct

industry assessed property values, and severance taxes, respectively, while the Colorado Oil and Gas

Conservation Commission (COGCC) publishes well activity and prices for oil and natural gas by county. This

study compiles the known economic contributions of the industry in Colorado by county and provides

estimates of economic metrics that are not quantified or published by government or by private data

repositories.

The authors completed a comprehensive Colorado oil and gas economic impact report commissioned by

the Colorado Oil & Gas Association (COGA) in 2011 and in 2013, and published in the journal Oil, Gas, and

Mining in 2013, that examined the industry, from drilling and extraction to refining and gasoline stations. In

2014, the American Petroleum Institute, commissioned a study that updated and built on the previous

work, deriving detailed county-level impacts for all counties in Colorado in 2013, focusing on a narrower

supply chain that included only upstream (drilling, extraction, and support activities) and midstream

(pipeline transportation) activities.2 This study current study was commissioned by the Colorado Oil and Gas

Association to again update the economic impact of upstream and midstream activities for 2014.

This study reports economic indicators and traces economic impacts to the county level, ranging from

employment, wages, and well activity to economic and fiscal impacts. Other metrics are available

exclusively at the state level, including federal distributions and price indices.

Total employment was calculated as the sum of employees and nonemployers (considered self-employed).

Publicly available employment and nonemployer data were used to estimate nonemployer detail that is not

1BLS definition of wages: “Under most State laws or regulations, wages include bonuses, stock options, severance pay, profit distributions, cash value of meals and lodging, tips and other gratuities, and, in some States, employer contributions to certain deferred compensation plans such as 401(k) plans.” Census Bureau definition of receipts: “Includes gross receipts, sales, commissions, and income from trades and businesses, as reported on annual business income tax returns. Business income consists of all payments received for services rendered. The composition of nonemployer receipts may differ from receipts data published for employer establishments. Nonemployer receipts may include commissions or earnings. In contrast, for employers the sales and receipts items published (for example, in the Economic Census) represents only the value of the goods involved in the transaction.”

2Includes the following North American Industry Classification System industries and codes: Extraction (211), Drilling wells

(213111), Support activities (213112), Oil and gas pipeline and related structures construction (23712), and Pipeline transportation (486).

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 4

disclosed. Much like employment numbers, wage data were collected and estimated for employees and the

self-employed in core oil and gas industries and related industries.

The percent of wages from oil and gas activities consistently exceeds the percent of employment from oil

and gas activities because oil and gas jobs tend to pay more than the average job. Average wages were

calculated by dividing the total wages of employees and the receipts of self-employed by the number of

employees and nonemployers.

An economic impact analysis was conducted using an input-output modeling software, IMPLAN.3 IMPLAN

generates industry multipliers based on trade flows and industry profiles of the study area. Multipliers refer

to the interindustry relationships within a study area in terms of input-output (I-O) economic impacts.4

Multipliers are useful for analyzing project decisions to understand the incremental impacts that such

activities have on the local economy. IMPLAN multipliers are static and thus do not consider large-scale

disruptive impacts on the economic fabric without calculating specific infrastructure changes.

For the purpose of this study, all multipliers comprise direct, indirect, and induced effects. Direct refers to

direct spending or employment in the study industry or firm. Indirect is the spending or employment in

related industries impacted by spending or employment in the study industry or firm. Induced refers to

changes in household expenditures impacted by spending or employment in the study industry or firm.

State and local fiscal impacts are quantified by identifying and aggregating publicly available data on

industry and production taxes, and estimating revenues for income and sales taxes.

INDUSTRY EMPLOYMENT, FIRMS, AND WAGES The upstream and midstream oil and gas industry includes drilling, extraction, support activities, pipeline

construction, pipeline transportation, and other related industries (e.g., company headquarters). These

industries in Colorado accounted for a combined 38,650 jobs in 2014, earning more than $4.06 billion

(Table 1).5 Average industry earnings of $105,168 were twice that of all industries in Colorado ($52,724)

and all private industries in Colorado ($53,070) in 2014.

3MIG, Inc., www.implan.com.

4Bureau of Economic Analysis, Regional Multipliers, http://www.bea.gov/scb/pdf/regional/perinc/meth/rims2.pdf, retrieved

January 20, 2010.

5Jobs include employees (nonfarm wage and salary earners) and proprietors (nonemployers).

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 5

TABLE 1: COLORADO OIL AND GAS INDUSTRY EMPLOYMENT, FIRMS, AND WAGES, 2014

County Employment Wages (Millions) Firms

Extraction 13,781 $1,765 475 Drilling 2,530 $223 88 Support Activities 15,756 $1,337 854 Pipeline Construction 3,819 $258 97 Pipeline Transportation 1,097 $128 64 Other 1,668 $352 7

Total 38,650 $4,065 1,584 Sources: Bureau of Labor Statistics, Quarterly Census of Employment and

Wages; and the U.S. Census Bureau, Nonemployer data.

OIL AND GAS INDUSTRY ECONOMIC IMPACT The oil and gas industry is a compilation of distinct activities with interrelated, cogent functions that

contributed $31.7 billion to Colorado’s economy in 2014 through direct and indirect activities (Table 2).

Mapping the industry illustrates the integrated supply chain within the state of Colorado, including oil and

gas drilling, extraction, support activities, transportation, pipeline construction, and other activities. Much

of the oil, gas, and CO2 is sold outside the state, resulting in outside industry investment.

TABLE 2: OIL AND GAS TOTAL ECONOMIC IMPACT (DIRECT, INDIRECT, INDUCED), 2014

Source Employment Employee Compensation (Millions)

Value Added (Millions)

Output (Millions)

Drilling and Extraction 52,551 $4,182.0 $8,309.8 $22,628.4 Support Activities 30,058 $2,056.6 $3,370.0 $5,194.2 Transportation 2,966 $231.6 $381.8 $965.1 Pipeline Construction 11,739 $594.7 $843.9 $1,953.6 Other 5,369 $534.6 $718.1 $951.8

Total 102,683 $7,599.4 $13,623.6 $31,693.1

TABLE 3: COLORADO OIL AND GAS EMPLOYMENT IMPACT (DIRECT, INDIRECT, AND INDUCED), 2014

Source Direct Indirect Induced Total

Drilling and Extraction 16,312 11,002 25,238 52,551

Support Activities 15,756 4,307 9,996 30,058

Transportation 1,097 743 1,127 2,966

Pipeline Construction 3,819 5,026 2,894 11,739

Other 1,668 1,103 2,598 5,369

Total 38,650 22,180 41,852 102,682

Commodity Prices

Prices for oil, natural gas, and gasoline began a sharp descent in 2014, impacting producers and consumers

differently. West Texas Intermediate (WTI) oil price peaked in 2014 at $107.95 on June 20; the average for

the year was $93.17 (Figure 1). Prices hit a record high on July 3, 2008, peaking at $145.31. By the end of

2014, the WTI spot price was $53.45, or 50.5% below the 2014 peak and 63.2% below the 2008 peak. This

price decline, which has continued into 2015, has had a bearing on investment (rig counts, employment),

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 6

value of production, and actual production. Prices from January to early November averaged $50.30, or

30.5% below the 10-year average, and were $44.23 on November 10, 2015. Prices have remained below

the 10-year average for 12 months.

FIGURE 1: WTI OIL SPOT PRICE, 2005-2015

The Henry Hub natural gas spot prices have been depressed for much longer than oil prices, generally

trending below the 10-year average since January 2009. The average weekly price in 2014 was $4.39, and

the average price in 2015 through November 6 was $2.74—62% below the 10-year average and 46% below

the 6-year average (Figure 2).

FIGURE 2: HENRY HUB NATUFRAL GAS SPOT PRICE, 2005–2015

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 7

The decrease in energy prices have impacted consumers most apparently in lower gasoline prices. Similar

to the peak in oil prices, gasoline prices peaked during summer 2008 as the nation was entrenched in the

recession (December 2007–June 2009, National Bureau of Economic Research). Nationally, prices peaked at

$4.17 per gallon compared to $4.03 in Colorado (Figure 3). Gasoline prices topped out at $3.71 in 2014 and

averaged $3.39 for the year. Prices in 2015 through November 9 year-to-date averaged $2.47 per gallon

and were $2.16 on the day of November 9, or 27% below the 10-year average and 30% lower year-over-

year.

FIGURE 3: NATIONAL AND COLORADO GASOLINE PRICES, 2005-2015

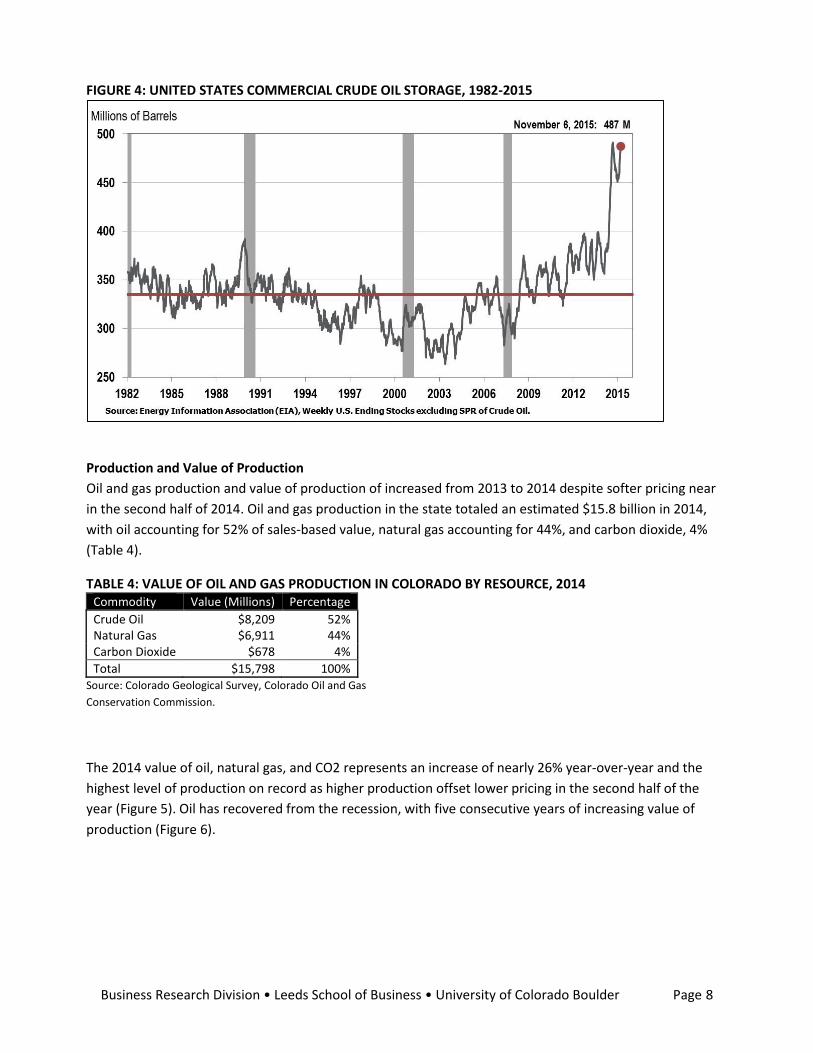

The price decline has been caused by a combination of factors, notably due to higher domestic oil

production, as well as softer global demand. Domestic crude oil storage spiked to record levels in 2015 in

the EIA’s storage statistics of weekly U.S. ending stocks (ending strategic petroleum reserves). The 2014

average reserves were 12% above the 33-year average, and the November 6, 2015, statistics reported oil

storage 45% above the long-term average (Table 4).

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 8

FIGURE 4: UNITED STATES COMMERCIAL CRUDE OIL STORAGE, 1982-2015

Production and Value of Production

Oil and gas production and value of production of increased from 2013 to 2014 despite softer pricing near

in the second half of 2014. Oil and gas production in the state totaled an estimated $15.8 billion in 2014,

with oil accounting for 52% of sales-based value, natural gas accounting for 44%, and carbon dioxide, 4%

(Table 4).

TABLE 4: VALUE OF OIL AND GAS PRODUCTION IN COLORADO BY RESOURCE, 2014 Commodity Value (Millions) Percentage

Crude Oil $8,209 52% Natural Gas $6,911 44% Carbon Dioxide $678 4%

Total $15,798 100% Source: Colorado Geological Survey, Colorado Oil and Gas

Conservation Commission.

The 2014 value of oil, natural gas, and CO2 represents an increase of nearly 26% year-over-year and the

highest level of production on record as higher production offset lower pricing in the second half of the

year (Figure 5). Oil has recovered from the recession, with five consecutive years of increasing value of

production (Figure 6).

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 9

FIGURE 5: VALUE OF COLORADO OIL AND GAS, 2004-2014

FIGURE 6: PERCENT CHANGE IN VALUE OF COLORADO OIL AND GAS, 2004-2014

Production value in Colorado has been volatile over the past seven years; much of the volatility is due to

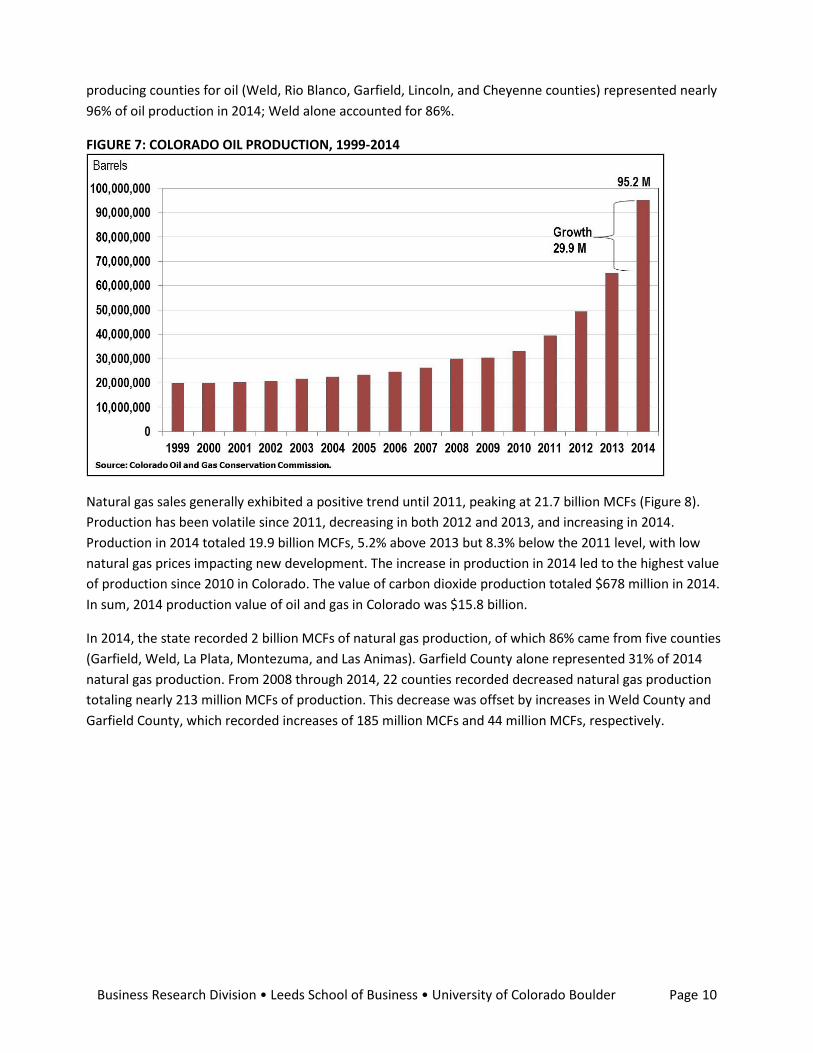

price swings. Oil production grew every year between 1999 and 2014, with sales totaling 95.2 million

barrels in 2014 (Figure 7). The greatest increase in both absolute and percentage growth came in 2014,

increasing by 29.9 million barrels, or nearly 45.8%. The increase in 2014 exceeded the total amount of 2008

production in Colorado. The value of sales was much more volatile, dipping 39% in 2009, then growing 45%

in 2010, 48% in 2011, 24% in 2012, 42% in 2013, and 36% in 2014 before falling in 2015. The top five

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 10

producing counties for oil (Weld, Rio Blanco, Garfield, Lincoln, and Cheyenne counties) represented nearly

96% of oil production in 2014; Weld alone accounted for 86%.

FIGURE 7: COLORADO OIL PRODUCTION, 1999-2014

Natural gas sales generally exhibited a positive trend until 2011, peaking at 21.7 billion MCFs (Figure 8).

Production has been volatile since 2011, decreasing in both 2012 and 2013, and increasing in 2014.

Production in 2014 totaled 19.9 billion MCFs, 5.2% above 2013 but 8.3% below the 2011 level, with low

natural gas prices impacting new development. The increase in production in 2014 led to the highest value

of production since 2010 in Colorado. The value of carbon dioxide production totaled $678 million in 2014.

In sum, 2014 production value of oil and gas in Colorado was $15.8 billion.

In 2014, the state recorded 2 billion MCFs of natural gas production, of which 86% came from five counties

(Garfield, Weld, La Plata, Montezuma, and Las Animas). Garfield County alone represented 31% of 2014

natural gas production. From 2008 through 2014, 22 counties recorded decreased natural gas production

totaling nearly 213 million MCFs of production. This decrease was offset by increases in Weld County and

Garfield County, which recorded increases of 185 million MCFs and 44 million MCFs, respectively.

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 11

FIGURE 8: COLORADO NATURAL GAS PRODUCTION, 1999-2014

Weld County Oil and Gas Production

From 2008 to 2014, more than 97% of the differential in annual oil production was attributable to Weld

County. Colorado recorded nearly 29.9 million barrels of oil production in 2008, of which Weld County

recorded 17.8 million barrels. In 2014, Colorado recorded 95.2 million barrels of production, of which Weld

County recorded 81.4 million barrels. Colorado oil production, excluding Weld County, remained fairly flat

over the decade (Figure 9). Weld County has continued to exhibit growth in monthly oil production despite

the decrease in oil prices, while the rest of the state has collectively decreased monthly production (Figure

10 ).

FIGURE 9: COLORADO (EXCLUDING WELD COUNTY) OIL PRODUCTION, 2000-2015

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 12

FIGURE 10: WELD COUNTY OIL PRODUCTION, 2000-2015

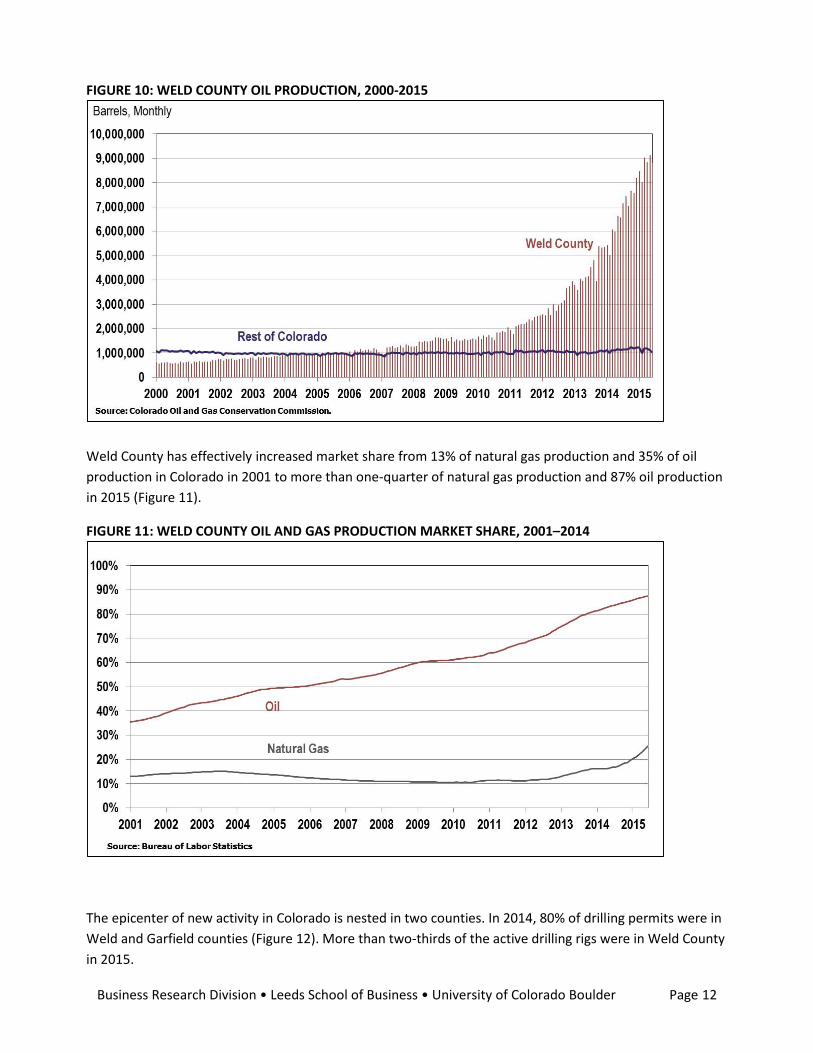

Weld County has effectively increased market share from 13% of natural gas production and 35% of oil

production in Colorado in 2001 to more than one-quarter of natural gas production and 87% oil production

in 2015 (Figure 11).

FIGURE 11: WELD COUNTY OIL AND GAS PRODUCTION MARKET SHARE, 2001–2014

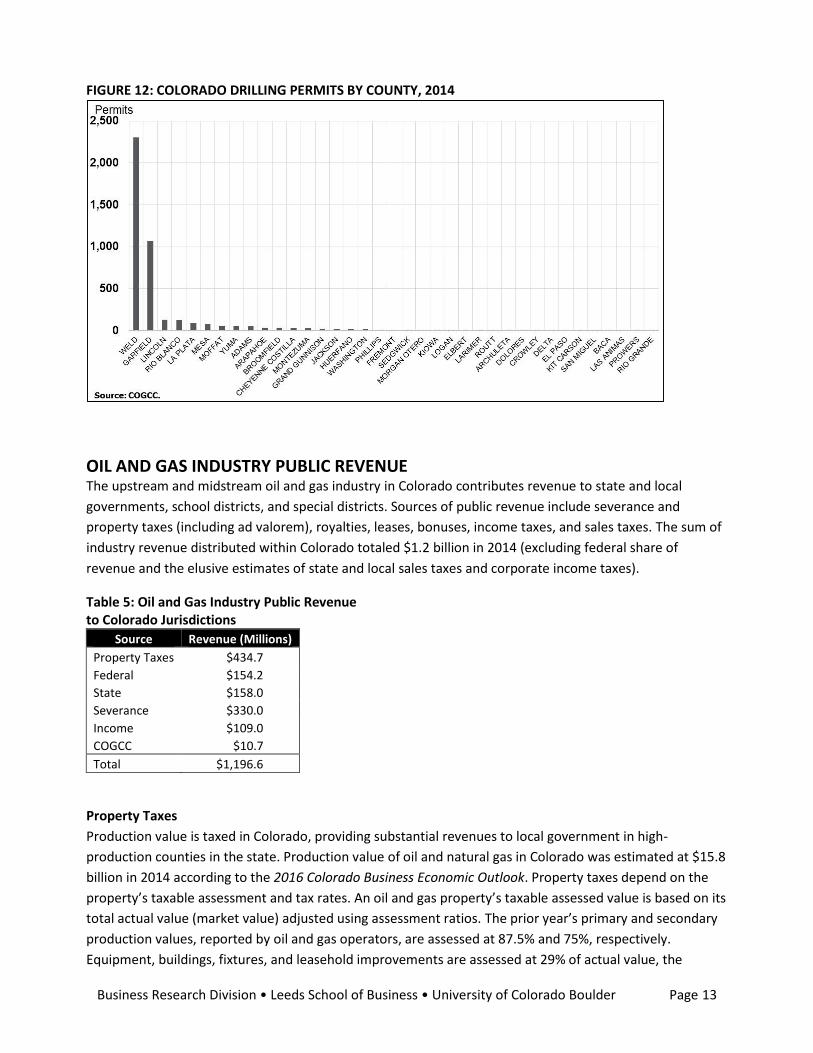

The epicenter of new activity in Colorado is nested in two counties. In 2014, 80% of drilling permits were in

Weld and Garfield counties (Figure 12). More than two-thirds of the active drilling rigs were in Weld County

in 2015.

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 13

FIGURE 12: COLORADO DRILLING PERMITS BY COUNTY, 2014

OIL AND GAS INDUSTRY PUBLIC REVENUE The upstream and midstream oil and gas industry in Colorado contributes revenue to state and local

governments, school districts, and special districts. Sources of public revenue include severance and

property taxes (including ad valorem), royalties, leases, bonuses, income taxes, and sales taxes. The sum of

industry revenue distributed within Colorado totaled $1.2 billion in 2014 (excluding federal share of

revenue and the elusive estimates of state and local sales taxes and corporate income taxes).

Table 5: Oil and Gas Industry Public Revenue to Colorado Jurisdictions

Source Revenue (Millions)

Property Taxes $434.7

Federal $154.2

State $158.0

Severance $330.0

Income $109.0

COGCC $10.7

Total $1,196.6

Property Taxes

Production value is taxed in Colorado, providing substantial revenues to local government in high-

production counties in the state. Production value of oil and natural gas in Colorado was estimated at $15.8

billion in 2014 according to the 2016 Colorado Business Economic Outlook. Property taxes depend on the

property’s taxable assessment and tax rates. An oil and gas property’s taxable assessed value is based on its

total actual value (market value) adjusted using assessment ratios. The prior year’s primary and secondary

production values, reported by oil and gas operators, are assessed at 87.5% and 75%, respectively.

Equipment, buildings, fixtures, and leasehold improvements are assessed at 29% of actual value, the

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 14

commercial property assessment ratio. The appropriate tax rates are then applied to the final assessed

property value. Publicly available assessed values and average mill levies were used to estimate property

tax revenues from oil and gas activities. Colorado’s statewide property tax estimates were calculated using

assessed property values and the total average county levy.

Total property taxes related to land, improvements, and personal property were estimated at $434.7

million in 2014. The majority of property taxes come from what is classified as land value. Based on the

assessed production value for the previous year, land contributed 87.6% of total 2014 oil and gas property

taxes. The ad valorem tax is impacted by both price and production.

Table 6: Estimated Oil and Gas Industry Property Taxes, 2010-2014

Year County City School District Total

2010 $109.9 $3.1 $144.5 $257.6

2011 $150.2 $4.4 $190.5 $345.1

2012 $166.7 $5.4 $221.3 $393.4

2013 $149.0 $5.1 $204.4 $358.5

2014 $184.3 $6.2 $244.1 $434.7 Data source: Colorado Department of Local Affairs, Division of Property Taxation, Annual Reports 2010-2014.

Calculated estimates by Business Research Division. Note: Excludes special districts.

Publicly available assessed values and average mill levies were used to estimate property tax revenues from

oil and gas activities. Colorado’s statewide industry property tax estimates were calculated using assessed

oil and gas property values by county, municipality within counties, and school districts within counties; and

their respective local mill levies, and then summed for the state. These property tax estimates excluded

special districts’ levies on production given the elusive assessed values within special districts.

Public Leases and Royalties

Oil and gas exploration and development on public lands provide additional public revenue through land

leases and royalties. Federal onshore leases generated revenue of $3.7 million in 2014, down from $4.2

million in 2014 (Figure 13).

Federal lease income includes fixed annual rent payments, generally between $1.50 and $2.00 per acre.

Additionally, for lands offered by competitive bidding, premiums paid above rent payments are called

bonuses, estimated at $2 million in 2014. Other revenue totaled $677,000 for the year.

In addition to lease revenue, oil and gas activity on public lands provides royalty revenue. On federal lands,

minimum annual royalty payments, much like rents, are required until production begins. When production

exceeds minimal levels, royalty payments are based on production volume and negotiated sales prices of

the oil and gas produced. Companies are allowed to deduct from royalty value costs associated with

transporting and processing the oil and gas. Royalties generated in Colorado from oil and gas activities on

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 15

federal onshore lands totaled nearly $308.3 million in 2014 (Figure 13).6 Federal royalties in 2014 exceeded

those generated in 2008, when royalties reached $303.9 million.

FIGURE 13: FEDERAL ROYALTIES, RENTS, BONUSES, AND OTHER REVENUES, 2008–2014

The State of Colorado also leases land. The State Land Board auctions leases to determine the rents oil and

gas companies pay for state parcels. The base rate, $1.50 per acre until changed to $2.50 per acre in 2011,

is collected and classified as rental income. Similar to federal lease bonuses, premiums bid over the base

price, classified as bonus revenue, are also lease income. The State of Colorado received almost $52.7

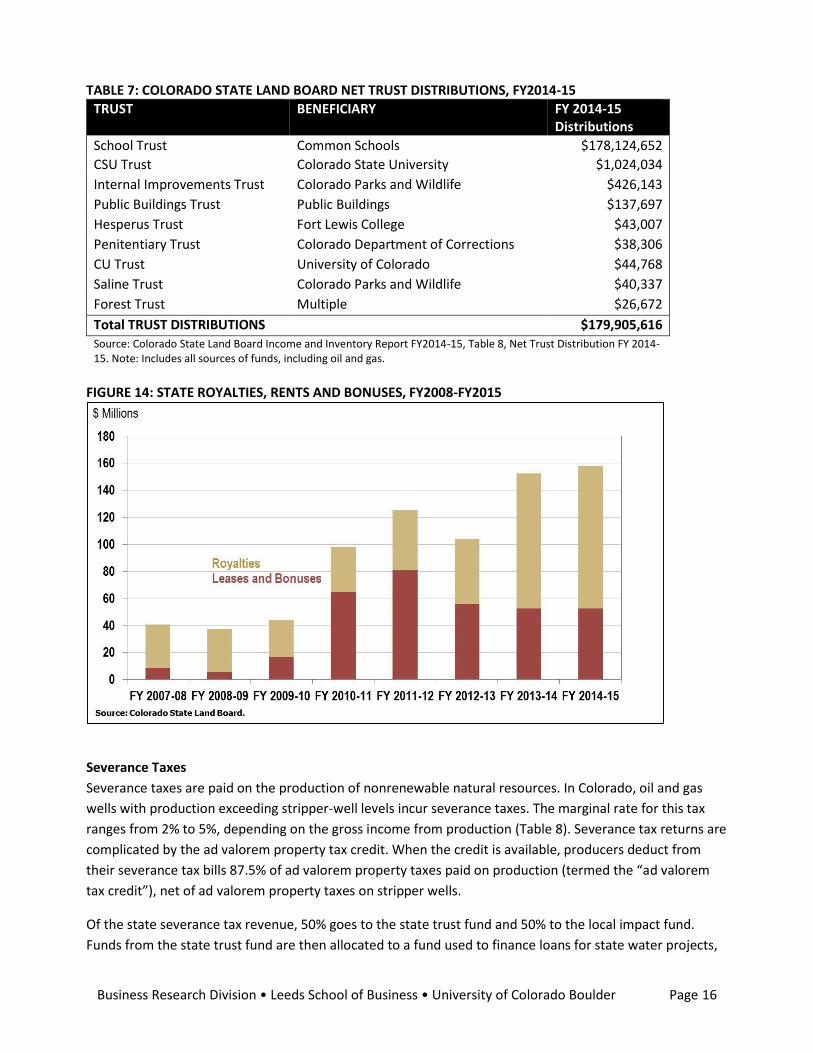

million in state lease revenue from oil and gas in 2014 (Figure 14).

When mineral resources are discovered on state land, oil and gas companies pay Colorado monthly

royalties based on production volume and sales prices. For the state’s ownership share, Colorado charges a

portion of proceeds from oil and gas sales; the full royalty rate was 12.5% until the State Land Board

authorized a change to 16.67% in June 2010. State royalties totaled nearly $105.4 million in 2014 (Figure

14).

The largest beneficiaries of State Land Board Trust distributions in fiscal year 2014-15 included schools

($178 million), Colorado State University ($1 million), and State Parks and Wildlife ($0.5 million) (Table 7).

6Includes carbon dioxide gas, coalbed methane, oil, processed (residue) gas, unprocessed (wet) gas, gas plant products, and fuel gas.

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 16

TABLE 7: COLORADO STATE LAND BOARD NET TRUST DISTRIBUTIONS, FY2014-15

TRUST BENEFICIARY FY 2014-15 Distributions

School Trust Common Schools $178,124,652

CSU Trust Colorado State University $1,024,034

Internal Improvements Trust Colorado Parks and Wildlife $426,143

Public Buildings Trust Public Buildings $137,697

Hesperus Trust Fort Lewis College $43,007

Penitentiary Trust Colorado Department of Corrections $38,306

CU Trust University of Colorado $44,768

Saline Trust Colorado Parks and Wildlife $40,337

Forest Trust Multiple $26,672

Total TRUST DISTRIBUTIONS $179,905,616 Source: Colorado State Land Board Income and Inventory Report FY2014-15, Table 8, Net Trust Distribution FY 2014-15. Note: Includes all sources of funds, including oil and gas.

FIGURE 14: STATE ROYALTIES, RENTS AND BONUSES, FY2008-FY2015

Severance Taxes

Severance taxes are paid on the production of nonrenewable natural resources. In Colorado, oil and gas

wells with production exceeding stripper-well levels incur severance taxes. The marginal rate for this tax

ranges from 2% to 5%, depending on the gross income from production (Table 8). Severance tax returns are

complicated by the ad valorem property tax credit. When the credit is available, producers deduct from

their severance tax bills 87.5% of ad valorem property taxes paid on production (termed the “ad valorem

tax credit”), net of ad valorem property taxes on stripper wells.

Of the state severance tax revenue, 50% goes to the state trust fund and 50% to the local impact fund.

Funds from the state trust fund are then allocated to a fund used to finance loans for state water projects,

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 17

administered by the Colorado Water Conservation Board and an operational account used for programs

administered by the Colorado Department of Natural Resources. The local impact fund share, meanwhile, is

distributed either to local government grant projects (70%) or directly to local governments (30%).

TABLE 8: SEVERANCE TAX RATES Total Gross Income Range Corresponding Severance Tax Under $25,000 2% of gross income $25,000 - $99,999 $500 plus 3% of the excess over $24,999 $100,000 - $299,999 $2,750 plus 4% of the excess over $99,999 $300,000 and over $10,750 plus 5% of the excess over $299,999

Source: Colorado Department of Revenue, Form DR 0021D.

In 2014, monthly severance taxes fluctuated between a low of $18 million and a high of $54 million (Figure 15). The monthly average in 2014 was $28 million. Removing seasonality, the 12-month total was $330 million from January 2014 to December 2014. This is nearly double the 2013 level, when severance taxes totaled $171 million. FIGURE 15: SEVERANCE TAX COLLECTIONS, 2005–2014 (NOMINAL)

TABLE 9: SEVERANCE TAXES, FY2008–FY2012, IN THOUSANDS (NOMINAL) Year Severance Taxes

2005 $160 2006 $168 2007 $112 2008 $254 2009 $152 2010 $85 2011 $163 2012 $135 2013 $171 2014 $330 Source: Colorado Department of Revenue.

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 18

Given that severance taxes are based on the value of production, which is impacted largely by prices, total

oil and gas severance taxes have followed a lagged trajectory related to prices (Figure 16).

FIGURE 16: COLORADO SEVERANCE TAXES AND WTI OIL SPOT PRICE, 2005-2015

Distribution of Federal Mineral Lease Proceeds and State Severance Tax Revenue

The direct distribution of federal mineral lease proceeds and state severance tax revenues is mandated by

Colorado statute and administered by DOLA. Two separate statutes allocate state proceeds generated from

the production of mineral resources in Colorado to local governments.

Portions of the distribution are allocated based on formulaic calculations and result in the direct

distributions to Colorado counties, municipalities, and school districts. The factors used in the distribution

are measures of resident energy employees, mining and well permits, amount of mineral production,

population, and miles of roads. For an illustration of the Department of Local Affairs portion of

distributions, visit https://www.colorado.gov/pacific/dola/direct-distribution-counties-municipalities.

Colorado Oil and Gas Converation Commission Taxes

Oil and gas companies pay COGCC a conservation levy every quarter for the environmental response fund

and for commission expenses. As of July 2007, the charge is 0.07% of oil, natural gas, and CO2 production

sales, less exemptions. The levy rate is designed to meet the expenses of the agency. COGCC levy revenues

fluctuate in tandem with production values as a result of the formula (Price multiplied by production

multiplied by levy). The levy totaled $10.7 million in 2014.

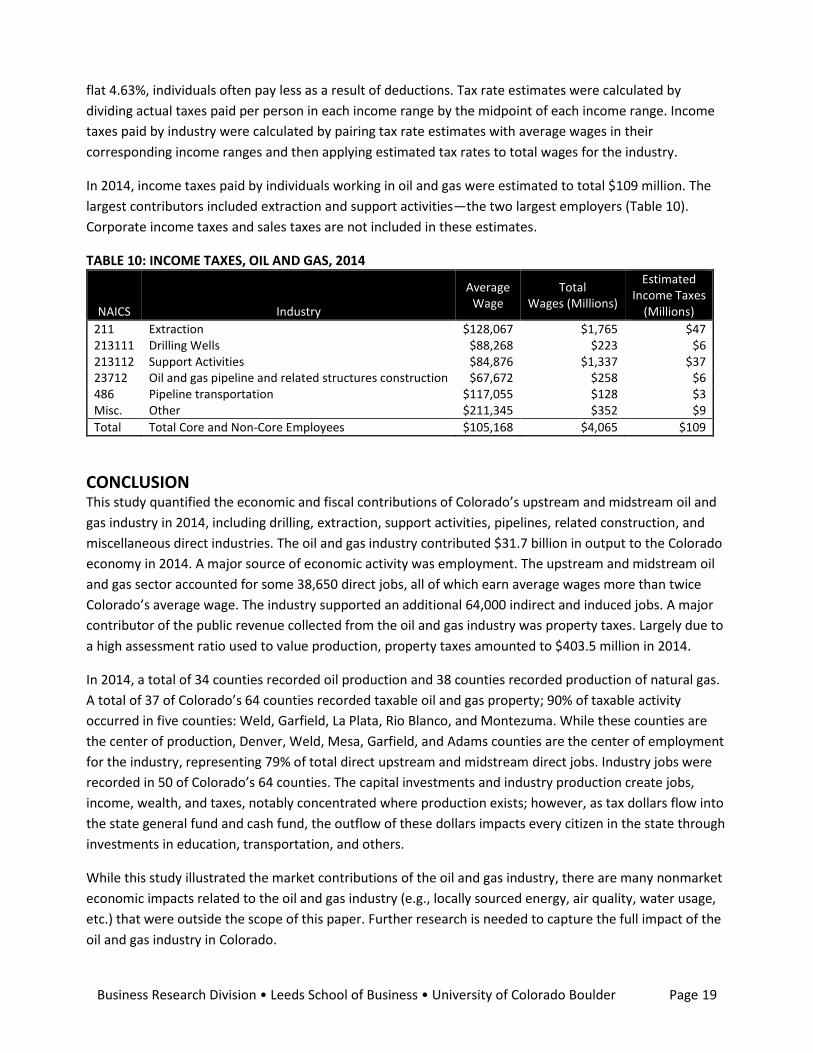

Income Taxes

Because average wages for jobs in oil and gas tend to be higher than those of the average job in Colorado,

income taxes paid per worker may also higher than average. Although Colorado’s state income tax rate is a

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 19

flat 4.63%, individuals often pay less as a result of deductions. Tax rate estimates were calculated by

dividing actual taxes paid per person in each income range by the midpoint of each income range. Income

taxes paid by industry were calculated by pairing tax rate estimates with average wages in their

corresponding income ranges and then applying estimated tax rates to total wages for the industry.

In 2014, income taxes paid by individuals working in oil and gas were estimated to total $109 million. The

largest contributors included extraction and support activities—the two largest employers (Table 10).

Corporate income taxes and sales taxes are not included in these estimates.

TABLE 10: INCOME TAXES, OIL AND GAS, 2014

NAICS Industry

Average Wage

Total Wages (Millions)

Estimated Income Taxes

(Millions)

211 Extraction $128,067 $1,765 $47 213111 Drilling Wells $88,268 $223 $6 213112 Support Activities $84,876 $1,337 $37 23712 Oil and gas pipeline and related structures construction $67,672 $258 $6 486 Pipeline transportation $117,055 $128 $3 Misc. Other $211,345 $352 $9

Total Total Core and Non-Core Employees $105,168 $4,065 $109

CONCLUSION This study quantified the economic and fiscal contributions of Colorado’s upstream and midstream oil and

gas industry in 2014, including drilling, extraction, support activities, pipelines, related construction, and

miscellaneous direct industries. The oil and gas industry contributed $31.7 billion in output to the Colorado

economy in 2014. A major source of economic activity was employment. The upstream and midstream oil

and gas sector accounted for some 38,650 direct jobs, all of which earn average wages more than twice

Colorado’s average wage. The industry supported an additional 64,000 indirect and induced jobs. A major

contributor of the public revenue collected from the oil and gas industry was property taxes. Largely due to

a high assessment ratio used to value production, property taxes amounted to $403.5 million in 2014.

In 2014, a total of 34 counties recorded oil production and 38 counties recorded production of natural gas.

A total of 37 of Colorado’s 64 counties recorded taxable oil and gas property; 90% of taxable activity

occurred in five counties: Weld, Garfield, La Plata, Rio Blanco, and Montezuma. While these counties are

the center of production, Denver, Weld, Mesa, Garfield, and Adams counties are the center of employment

for the industry, representing 79% of total direct upstream and midstream direct jobs. Industry jobs were

recorded in 50 of Colorado’s 64 counties. The capital investments and industry production create jobs,

income, wealth, and taxes, notably concentrated where production exists; however, as tax dollars flow into

the state general fund and cash fund, the outflow of these dollars impacts every citizen in the state through

investments in education, transportation, and others.

While this study illustrated the market contributions of the oil and gas industry, there are many nonmarket

economic impacts related to the oil and gas industry (e.g., locally sourced energy, air quality, water usage,

etc.) that were outside the scope of this paper. Further research is needed to capture the full impact of the

oil and gas industry in Colorado.

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 20

BIBLIOGRAPHY Bureau of Labor Statistics, Quarterly Census of Employment and Wages. www.bls.gov (accessed November

4, 2015). Colorado Department of Local Affairs. May 2015. 2014 Forty-Fourth Annual Report. Division of Property

Taxation. Colorado Department of Local Affairs. 2015. Severance Direct Distribution and Federal Mineral Lease

Distributions. https://dola.colorado.gov/sdd/sdd_tier1.jsf (accessed October 18, 2015). Colorado Department of Local Affairs. Flowchart of Severance Tax Distributions.

https://drive.google.com/file/d/0B6P5TF4k2v8qRHpXLWVxdFJkTDA/view?pli=1 (accessed September 12, 2015).

Colorado Department of Revenue. Federal AGI and Tax, All Full-year Resident Returns, 2012 Individual

Income Tax Returns. Office of Research and Analysis. https://www.colorado.gov/pacific/revenue/statistics-income, accessed August 2, 2015.

Colorado Oil and Gas Conservation Commission. Colorado Oil and Gas Information System.

http://cogcc.state.co.us/ (accessed November 22, 2015). _________. Staff Report, October 26, 2015. http://cogcc.state.co.us/ (accessed November 22, 2015). Colorado State Board of Land Commissioners. Income & Inventory Report Fiscal Year 2014−15.

https://drive.google.com/file/d/0BxRIvx2vXq4FUmV3V2tmcld5MU0/view?pli=1 (accessed October 27, 2015).

Lewandowski, Brian and Richard Wobbekind. July 2013. Assessment of Oil and Gas Industry 2012 Industry

Economic and Fiscal Impacts in Colorado. Business Research Division, Leeds School of Business, University of Colorado Boulder.

_________. “Assessment of Oil and Gas Industry Economic and Fiscal Impacts in Colorado.” Oil, Gas, and

Mining, volume 1, issue 1, https://www.oilgasandmining.com/. IMPLAN Group LLC, IMPLAN System (data and software),16905 Northcross Dr., Suite 120, Huntersville, NC

28078 www.IMPLAN.com. Nonemployer Statistics. U.S. Census Bureau. http://www.census.gov/econ/nonemployer/index.html

(accessed August 17, 2015). Office of Natural Resources Revenue. States and Offshore Regions Statistics.

http://statistics.onrr.gov/ReportTool.aspx (accessed October 2, 2015). 2016 Colorado Business Economic Outlook. University of Colorado Boulder, Leeds School of Business.

(accessed December 1, 2015). U.S. Bureau of Labor Statistics. http://www.bls.gov/data/.

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 21

U.S. Census Bureau. Nonemployer Statistics Definitions. www.census.gov/econ/nonemployer/definitions.htm, retrieved January 18, 2014.

U.S. Energy Information Administration. April 2015. Annual Energy Outlook 2015 with Projections to 2040.

http://www.eia.gov/forecasts/aeo/pdf/0383(2015).pdf (accessed November 28, 2015). U.S. Energy Information Administration. November 10, 2015. Short-Term Energy Outlook.

http://www.eia.gov/forecasts/steo/ (accessed November 16, 2015). Wobbekind, Richard and Brian Lewandowski. December 2011. Assessment of Oil and Gas Industry Economic

and Fiscal Impacts in Colorado in 2010. Business Research Division, Leeds School of Business, University of Colorado Boulder.

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 22

APPENDIX 1: EMPLOYMENT AND WAGES BY COUNTY The upstream and midstream (pipeline) oil and gas industry comprised 38,650 workers (employees and

proprietors) in 2014 earning nearly $4.1 billion in wages and salaries and in proprietor income.

TABLE 11: COLORADO UPSTREAM AND MIDSTREAM O&G EMPLOYMENT AND WAGES, 2014 County Employment Wages (Millions) Average Wages

Adams 1,589 $115.4 $72,603 Alamosa 0 $0.0 $0 Arapahoe 980 $103.6 $105,712 Archuleta 22 $1.1 $49,763 Baca <10 <1,000,000 $0 Bent 0 $0.0 $0 Boulder 363 $16.3 $44,853 Broomfield 66 $9.4 $143,681 Chaffee <10 <1,000,000 $0 Cheyenne 113 $6.3 $55,549 Clear Creek <10 <1,000,000 $0 Conejos 0 $0.0 $0 Costilla 0 $0.0 $0 Crowley 0 $0.0 $0 Custer 0 $0.0 $0 Delta 14 $1.1 $75,850 Denver 12,737 $2,061.5 $161,850 Dolores 294 $21.5 $73,183 Douglas 666 $83.4 $125,274 Eagle 235 <1,000,000 $0 Elbert 75 $4.5 $59,640 El Paso 146 $8.6 $59,273 Fremont <10 <1,000,000 $0 Garfield 2,325 $188.1 $80,888 Gilpin 0 $0.0 $0 Grand <10 <1,000,000 $0 Gunnison <10 <1,000,000 $0 Hinsdale 0 $0.0 $0 Huerfano <10 <1,000,000 $0 Jackson 28 $1.2 $43,057 Jefferson 984 $126.1 $128,196 Kiowa 12 <1,000,000 $0 Kit Carson 115 $8.3 $72,293 Lake 19 <1,000,000 $0 La Plata 737 $51.7 $70,105 Larimer 566 $24.0 $42,398 Las Animas 469 $41.1 $87,618 Lincoln 0 $0.0 $0 Logan 334 $21.4 $64,139 Mesa 3,345 $247.2 $73,914 Mineral 0 $0.0 $0 Moffat 94 $5.7 $61,123 Montezuma 239 $19.6 $82,295 Montrose 15 <1,000,000 $0 Morgan 449 $36.6 $81,653 Otero 53 $2.8 $53,017 Ouray 10 <1,000,000 $0

Business Research Division • Leeds School of Business • University of Colorado Boulder Page 23

Park <10 <1,000,000 $0 Phillips 17 $1.0 $58,837 Pitkin <10 <1,000,000 $0 Prowers 101 $4.6 $45,670 Pueblo <10 <1,000,000 $0 Rio Blanco 650 $53.1 $81,562 Rio Grande 0 $0.0 $0 Routt 26 $1.4 $53,895 Saguache 0 $0.0 $0 San Juan 0 $0.0 $0 San Miguel <10 <1,000,000 $0 Sedgwick <10 <1,000,000 $0 Summit 0 $0.0 $0 Teller <10 <1,000,000 $0 Washington 47 $6.1 $130,317 Weld 10,348 $767.3 $74,149 Yuma 326 $20.0 $61,473

Total 38,650 $4,064.8 $105,168 Sources: BLS, Colorado Department of Labor and Employment, Census, and BRD analyses.