Embed Size (px)

Citation preview

1IEA 2019. All rights reserved.IEA 2019. All rights reserved.

Oil 2019 – Analysis and Forecast to 2024Neil Atkinson, Kristine PetrosyanTokyo, 26 April 2019, The Institute of Energy Economics, Japan

IEA

IEEJ:April 2019 © IEEJ2019

2IEA 2019. All rights reserved. 2IEA 2019. All rights reserved.

Oil 2019Analysis and Forecast to 2024

IEEJ:April 2019 © IEEJ2019

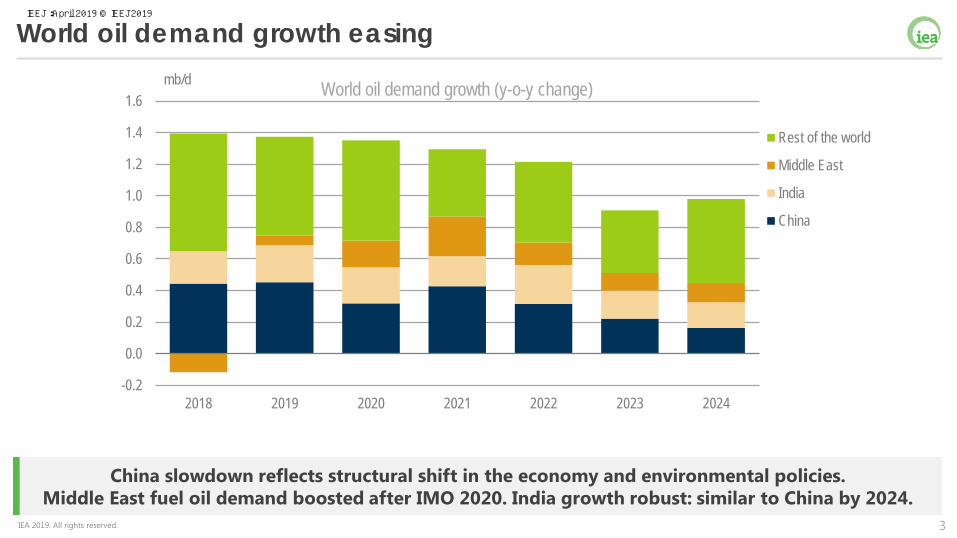

3IEA 2019. All rights reserved.

China slowdown reflects structural shift in the economy and environmental policies. Middle East fuel oil demand boosted after IMO 2020. India growth robust: similar to China by 2024.

World oil demand growth easing

World oil demand growth (y-o-y change)

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2018 2019 2020 2021 2022 2023 2024

mb/d

Rest of the world

Middle East

India

China

IEEJ:April 2019 © IEEJ2019

4IEA 2019. All rights reserved.

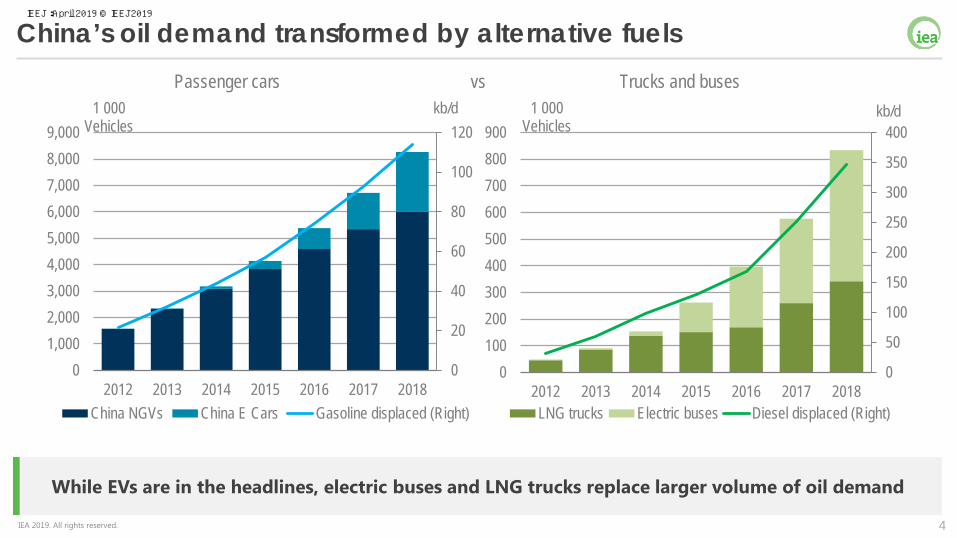

While EVs are in the headlines, electric buses and LNG trucks replace larger volume of oil demand

China’s oil demand transformed by alternative fuels

0

20

40

60

80

100

120

01,0002,0003,0004,0005,0006,0007,0008,0009,000

2012 2013 2014 2015 2016 2017 2018

kb/d1 000 Vehicles

China NGVs China E Cars Gasoline displaced (Right)

0

50

100

150

200

250

300

350

400

0100200300400500600700800900

2012 2013 2014 2015 2016 2017 2018

kb/d1 000 Vehicles

LNG trucks Electric buses Diesel displaced (Right)

Passenger cars vs Trucks and buses

IEEJ:April 2019 © IEEJ2019

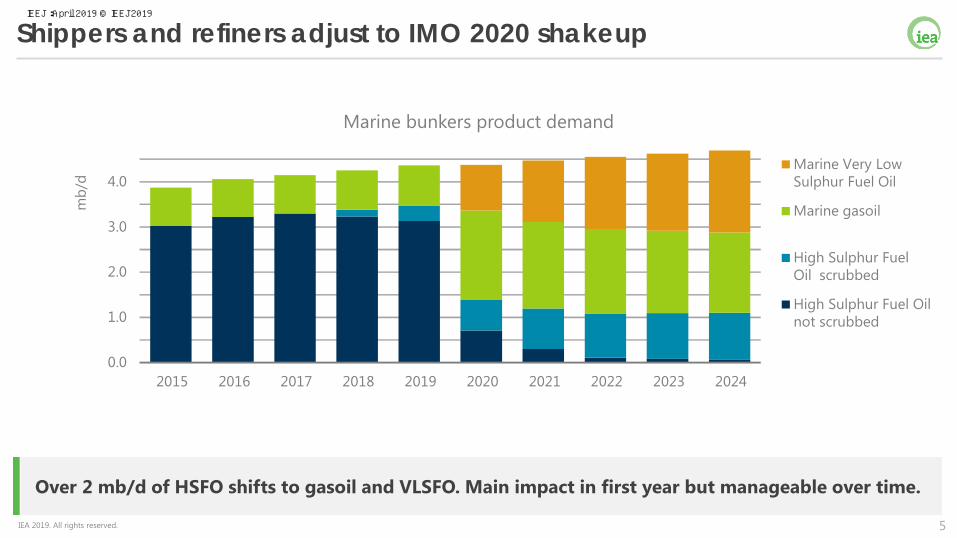

5IEA 2019. All rights reserved.

Over 2 mb/d of HSFO shifts to gasoil and VLSFO. Main impact in first year but manageable over time.

Shippers and refiners adjust to IMO 2020 shakeup

0.0

1.0

2.0

3.0

4.0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

mb/

d

Marine Very Low Sulphur Fuel Oil

Marine gasoil

High Sulphur Fuel Oil scrubbed

High Sulphur Fuel Oil not scrubbed

Marine bunkers product demand

IEEJ:April 2019 © IEEJ2019

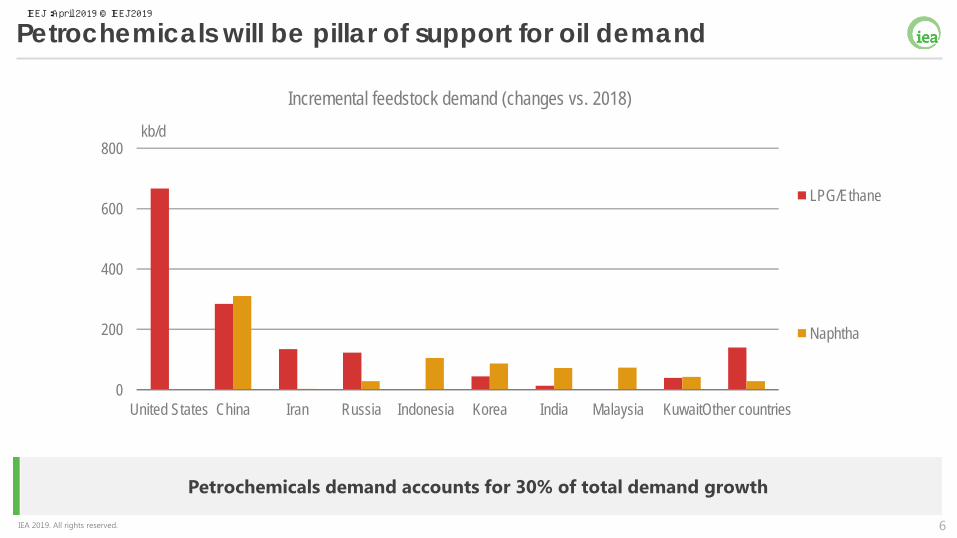

6IEA 2019. All rights reserved.

Petrochemicals demand accounts for 30% of total demand growth

Petrochemicals will be pillar of support for oil demand

0

200

400

600

800

United States China Iran Russia Indonesia Korea India Malaysia KuwaitOther countries

kb/d

Incremental feedstock demand (changes vs. 2018)

LPG/Ethane

Naphtha

IEEJ:April 2019 © IEEJ2019

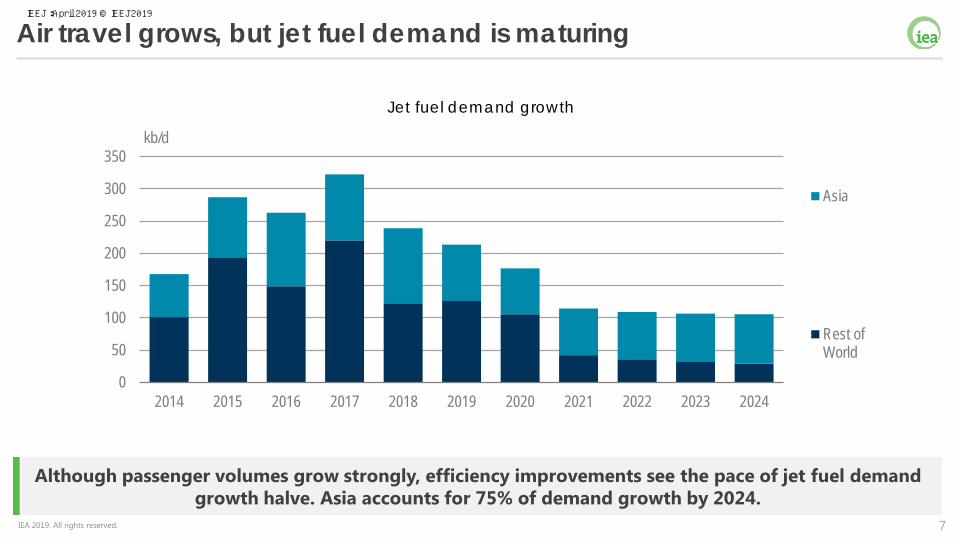

7IEA 2019. All rights reserved.

Although passenger volumes grow strongly, efficiency improvements see the pace of jet fuel demand growth halve. Asia accounts for 75% of demand growth by 2024.

Jet fuel demand growth

Air travel grows, but jet fuel demand is maturing

0

50

100

150

200

250

300

350

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

kb/d

Asia

Rest ofWorld

IEEJ:April 2019 © IEEJ2019

8IEA 2019. All rights reserved.

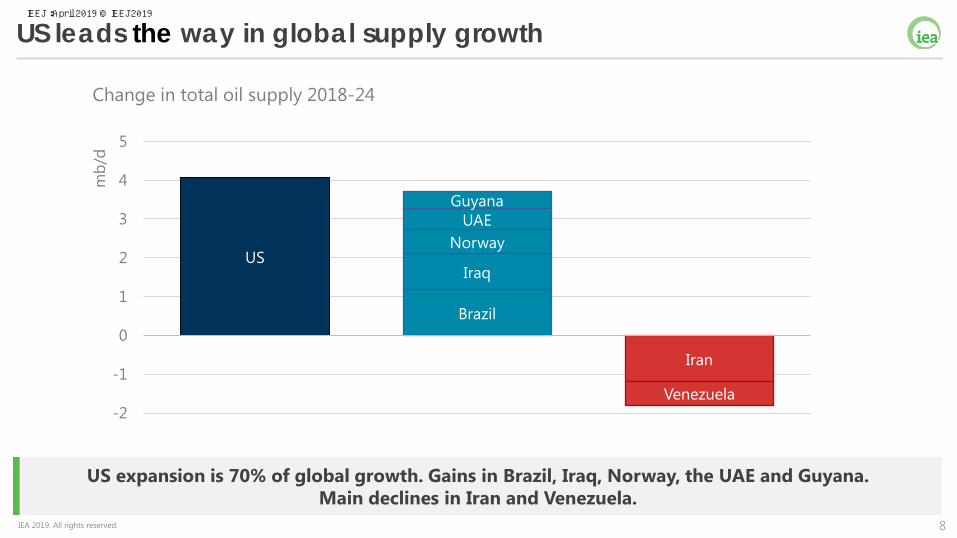

US expansion is 70% of global growth. Gains in Brazil, Iraq, Norway, the UAE and Guyana. Main declines in Iran and Venezuela.

US leads the way in global supply growth

Change in total oil supply 2018-24

US

Brazil

Iraq

NorwayUAE

Guyana

Iran

Venezuela-2

-1

0

1

2

3

4

5

mb/

d

IEEJ:April 2019 © IEEJ2019

9IEA 2019. All rights reserved.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

mb/d

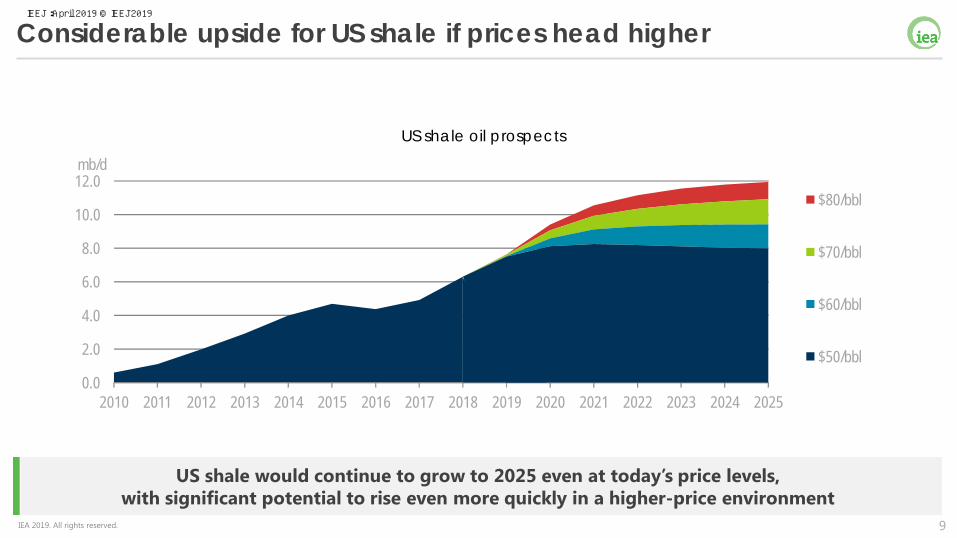

Considerable upside for US shale if prices head higher

US shale would continue to grow to 2025 even at today’s price levels,with significant potential to rise even more quickly in a higher-price environment

$80/bbl

$70/bbl

$60/bbl

$50/bbl

US shale oil prospects

IEEJ:April 2019 © IEEJ2019

10IEA 2019. All rights reserved.

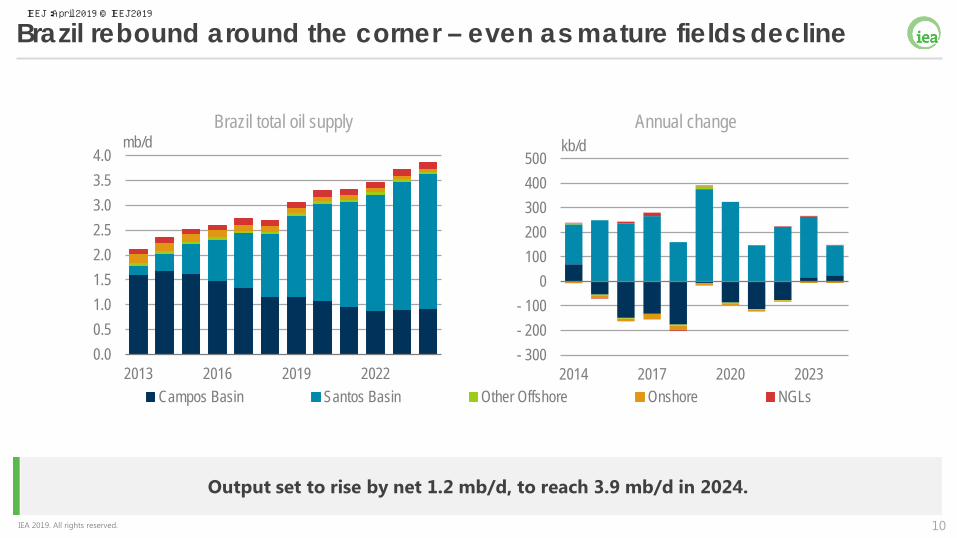

Brazil rebound around the corner – even as mature fields decline

Output set to rise by net 1.2 mb/d, to reach 3.9 mb/d in 2024.

0.00.51.01.52.02.53.03.54.0

2013 2016 2019 2022

mb/d

Campos Basin Santos Basin Other Offshore Onshore NGLs

- 300- 200- 100

0 100 200 300 400 500

2014 2017 2020 2023

kb/dBrazil total oil supply Annual change

IEEJ:April 2019 © IEEJ2019

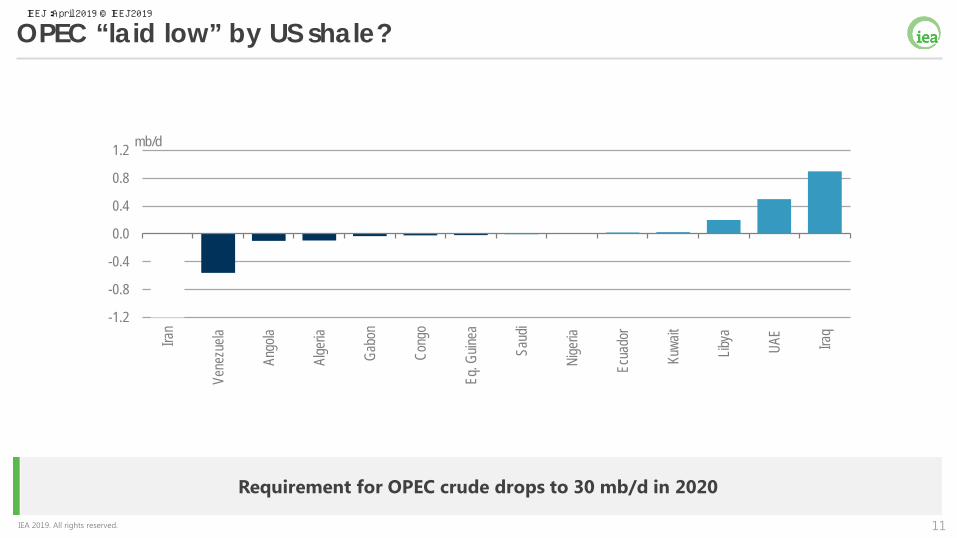

11IEA 2019. All rights reserved.

OPEC “laid low” by US shale?

Requirement for OPEC crude drops to 30 mb/d in 2020

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2Ira

n

Vene

zuela

Ango

la

Alge

ria

Gabo

n

Cong

o

Eq. G

uinea

Saud

i

Nige

ria

Ecua

dor

Kuwa

it

Libya

UAE

Iraq

mb/d

IEEJ:April 2019 © IEEJ2019

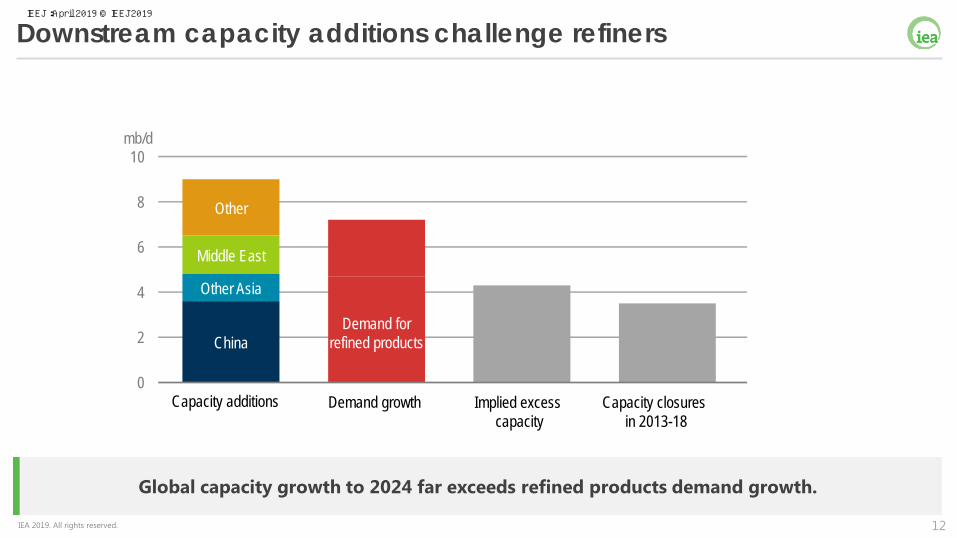

12IEA 2019. All rights reserved.

Downstream capacity additions challenge refiners

Global capacity growth to 2024 far exceeds refined products demand growth.

China

Other Asia

Middle East

Other

0

2

4

6

8

10

Capacity additions Demand growth Implied excess capacity

Capacity closuresin 2013-18

mb/d

Demand for refined products

IEEJ:April 2019 © IEEJ2019

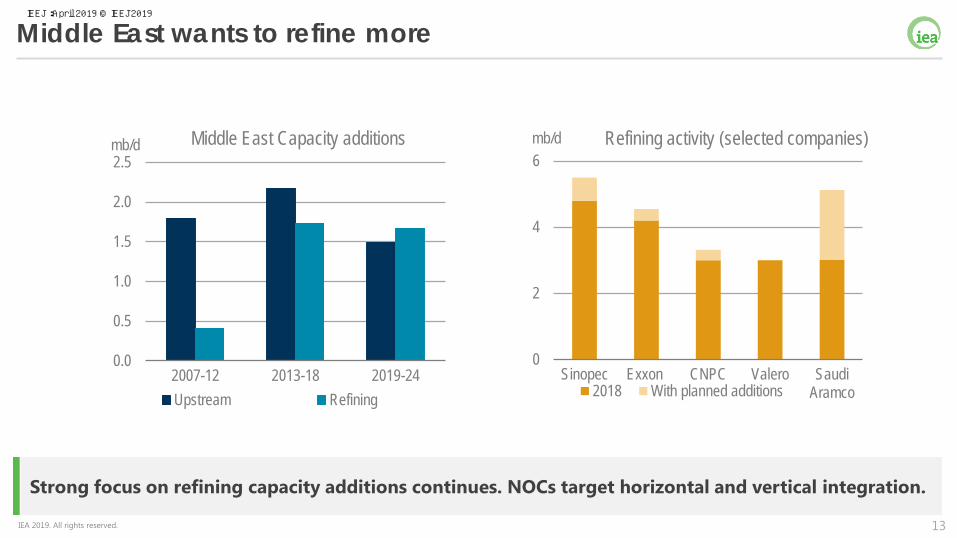

13IEA 2019. All rights reserved.

Strong focus on refining capacity additions continues. NOCs target horizontal and vertical integration.

Middle East wants to refine more

0.0

0.5

1.0

1.5

2.0

2.5

2007-12 2013-18 2019-24

mb/d Middle East Capacity additions

Upstream Refining

0

2

4

6

Sinopec Exxon CNPC Valero SaudiAramco

mb/d Refining activity (selected companies)

2018 With planned additions

IEEJ:April 2019 © IEEJ2019

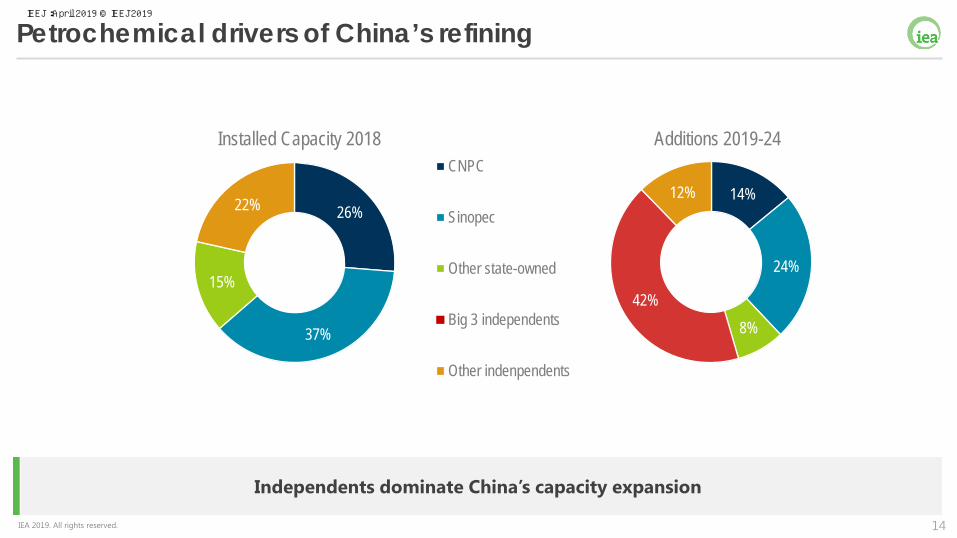

14IEA 2019. All rights reserved.

Independents dominate China’s capacity expansion

Petrochemical drivers of China’s refining

26%

37%

15%

22%

Installed Capacity 2018CNPC

Sinopec

Other state-owned

Big 3 independents

Other indenpendents

14%

24%

8%42%

12%

Additions 2019-24

IEEJ:April 2019 © IEEJ2019

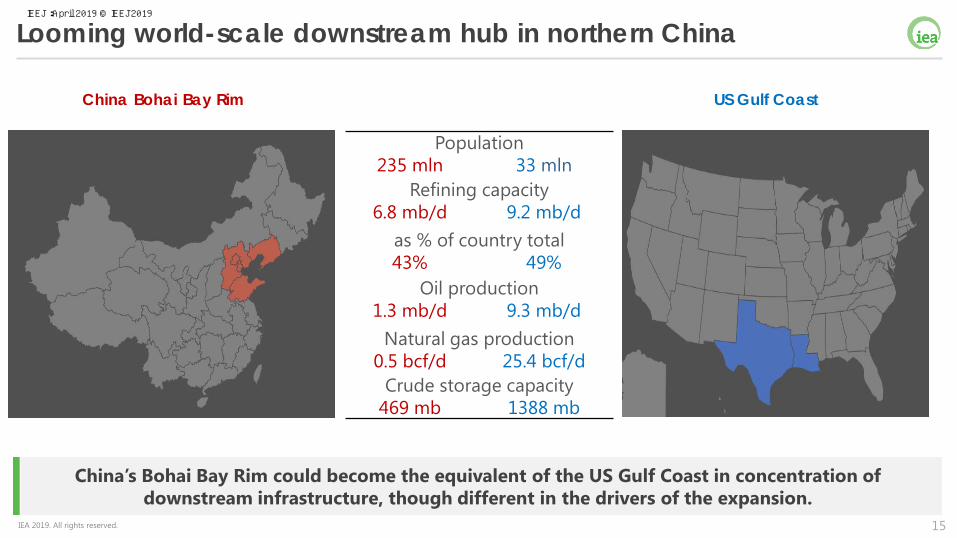

15IEA 2019. All rights reserved.

China’s Bohai Bay Rim could become the equivalent of the US Gulf Coast in concentration of downstream infrastructure, though different in the drivers of the expansion.

Looming world-scale downstream hub in northern China

China Bohai Bay Rim US Gulf Coast

Population235 mln 33 mln

Refining capacity6.8 mb/d 9.2 mb/d

as % of country total43% 49%

Oil production1.3 mb/d 9.3 mb/d

Natural gas production0.5 bcf/d 25.4 bcf/d

Crude storage capacity469 mb 1388 mb

IEEJ:April 2019 © IEEJ2019

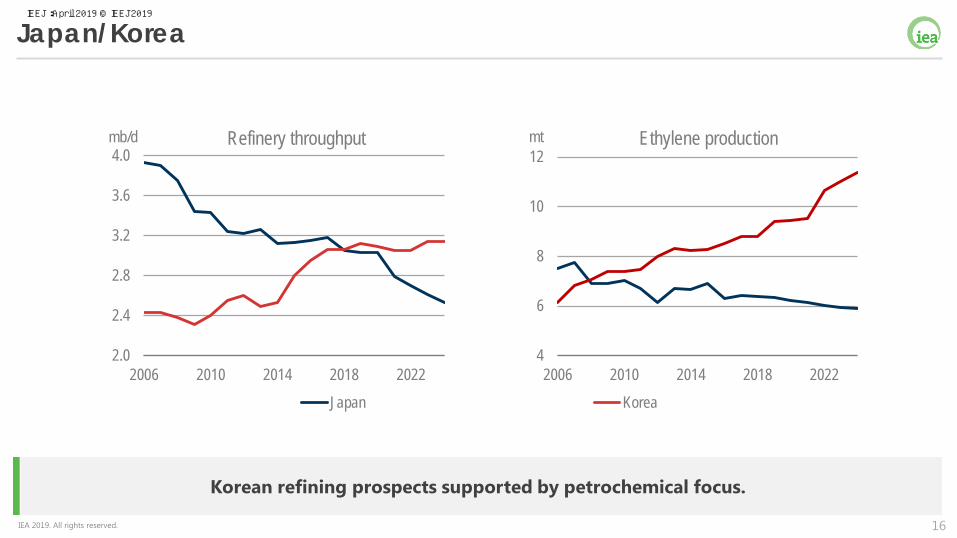

16IEA 2019. All rights reserved.

Korean refining prospects supported by petrochemical focus.

Japan/Korea

2.0

2.4

2.8

3.2

3.6

4.0

2006 2010 2014 2018 2022

mb/d Refinery throughput

Japan Korea

4

6

8

10

12

2006 2010 2014 2018 2022

mt Ethylene production

IEEJ:April 2019 © IEEJ2019

17IEA 2019. All rights reserved.

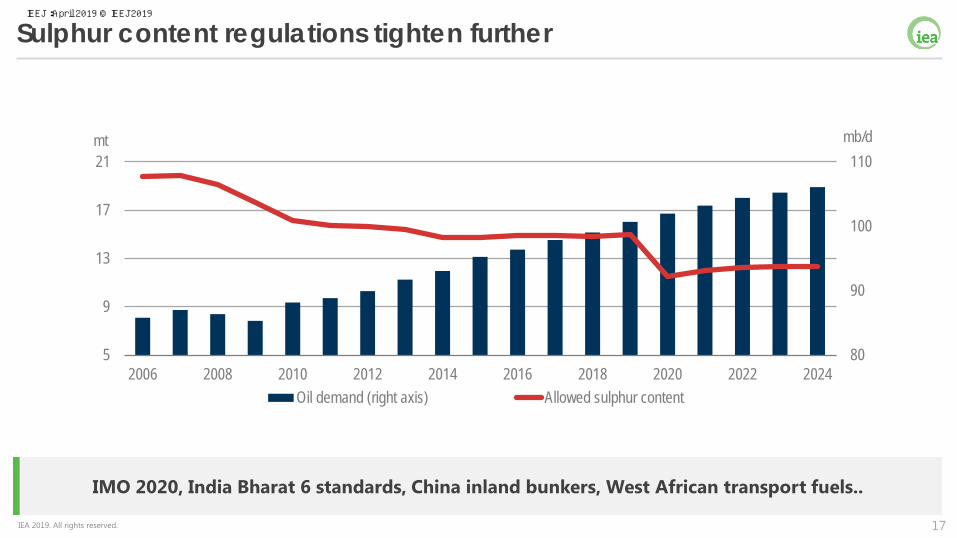

IMO 2020, India Bharat 6 standards, China inland bunkers, West African transport fuels..

Sulphur content regulations tighten further

80

90

100

110

5

9

13

17

21

2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

mt

Oil demand (right axis) Allowed sulphur content

mb/d

IEEJ:April 2019 © IEEJ2019

18IEA 2019. All rights reserved.

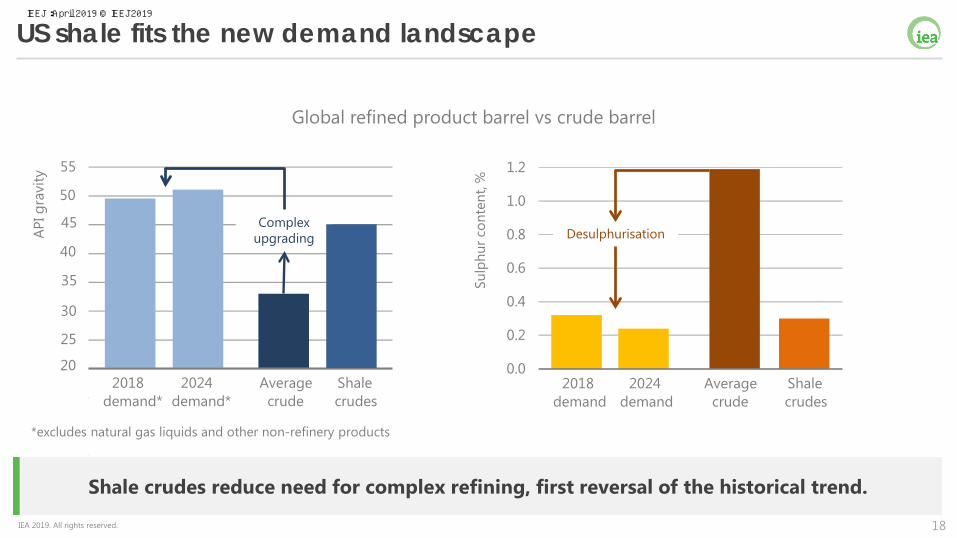

Shale crudes reduce need for complex refining, first reversal of the historical trend.

US shale fits the new demand landscape

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2018demand

2024demand

Averagecrude

Shalecrudes

Sulp

hur c

onte

nt, %

20

25

30

35

40

45

50

55

2024demand*

Averagecrude

Shalecrudes

APIg

ravi

ty

2018demand*

Complex upgrading Desulphurisation

*excludes natural gas liquids and other non-refinery products

Global refined product barrel vs crude barrel

IEEJ:April 2019 © IEEJ2019

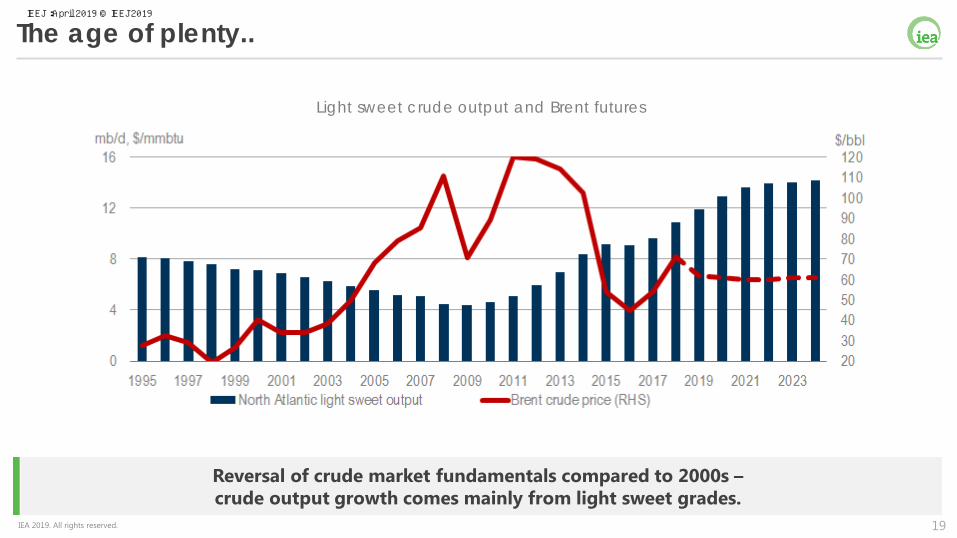

19IEA 2019. All rights reserved.

Reversal of crude market fundamentals compared to 2000s –crude output growth comes mainly from light sweet grades.

The age of plenty..

Light sweet crude output and Brent futures

IEEJ:April 2019 © IEEJ2019

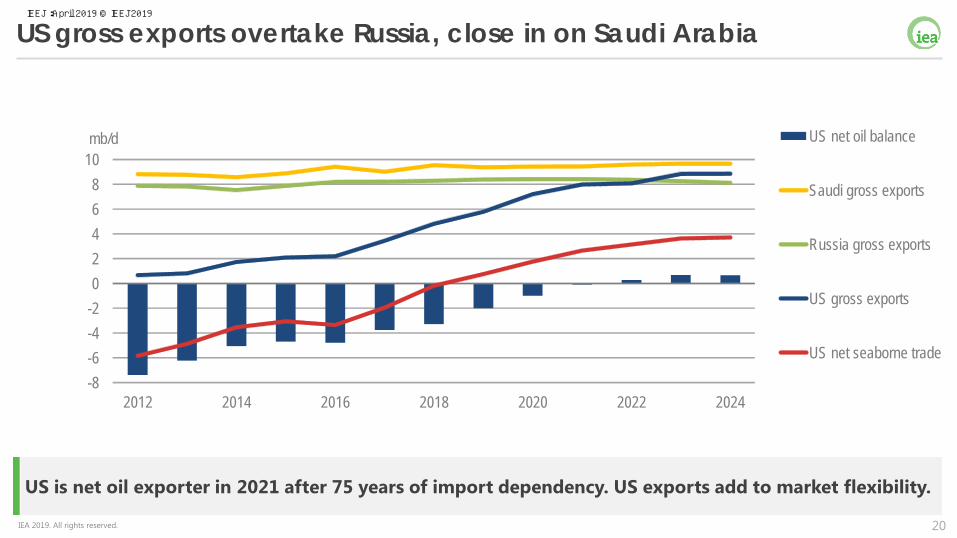

20IEA 2019. All rights reserved.

US gross exports overtake Russia, close in on Saudi Arabia

US is net oil exporter in 2021 after 75 years of import dependency. US exports add to market flexibility.

-8-6-4-202468

10

2012 2014 2016 2018 2020 2022 2024

mb/d US net oil balance

Saudi gross exports

Russia gross exports

US gross exports

US net seaborne trade

IEEJ:April 2019 © IEEJ2019

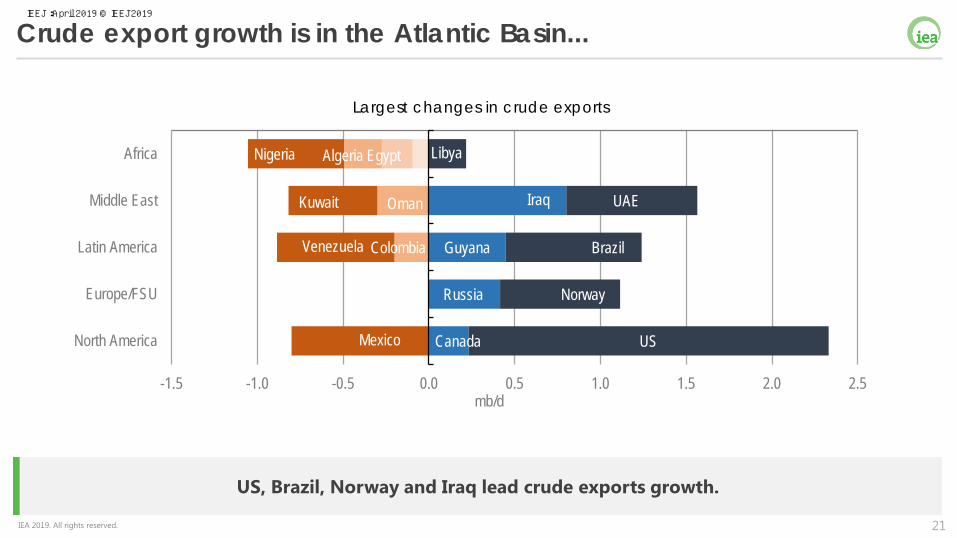

21IEA 2019. All rights reserved.

US, Brazil, Norway and Iraq lead crude exports growth.

Crude export growth is in the Atlantic Basin...

Algeria

Oman

Nigeria

Kuwait

Venezuela

Mexico

Egypt

UAE

Colombia

Russia

Canada

Guyana

Libya

Iraq

Brazil

Norway

US

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

Africa

Middle East

Latin America

Europe/FSU

North America

mb/d

Largest changes in crude exports

IEEJ:April 2019 © IEEJ2019

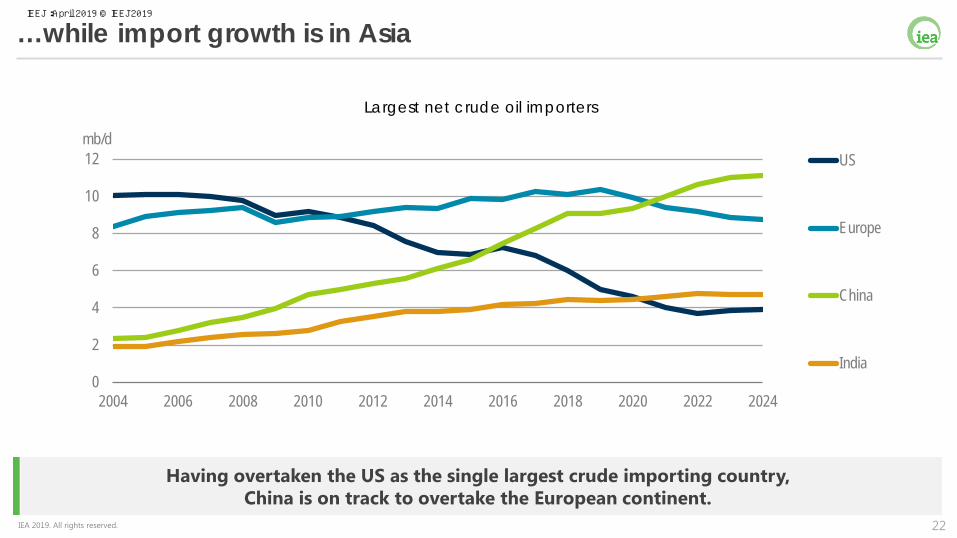

22IEA 2019. All rights reserved.

Having overtaken the US as the single largest crude importing country, China is on track to overtake the European continent.

…while import growth is in Asia

0

2

4

6

8

10

12

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

mb/dUS

Europe

China

India

Largest net crude oil importers

IEEJ:April 2019 © IEEJ2019

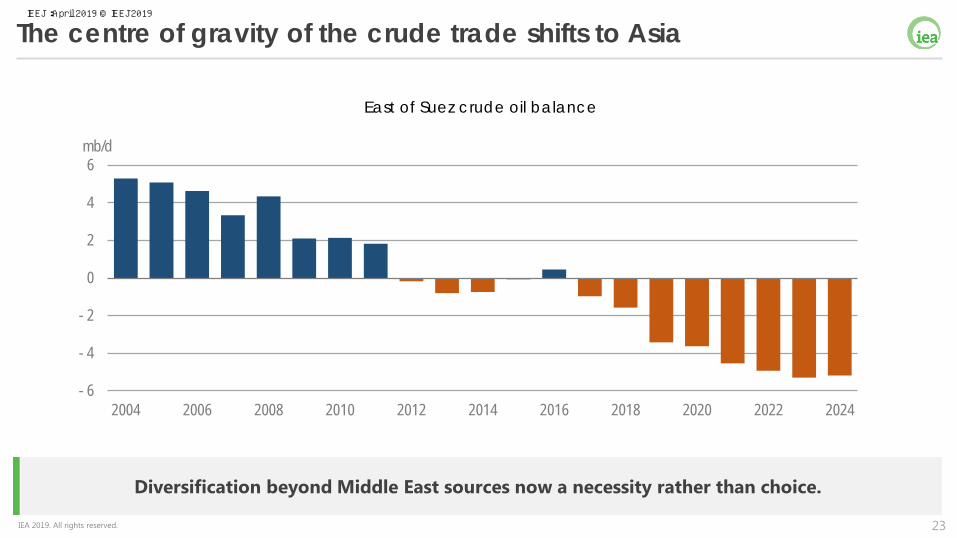

23IEA 2019. All rights reserved.

Diversification beyond Middle East sources now a necessity rather than choice.

The centre of gravity of the crude trade shifts to Asia

East of Suez crude oil balance

- 6

- 4

- 2

0

2

4

6

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

mb/d

IEEJ:April 2019 © IEEJ2019

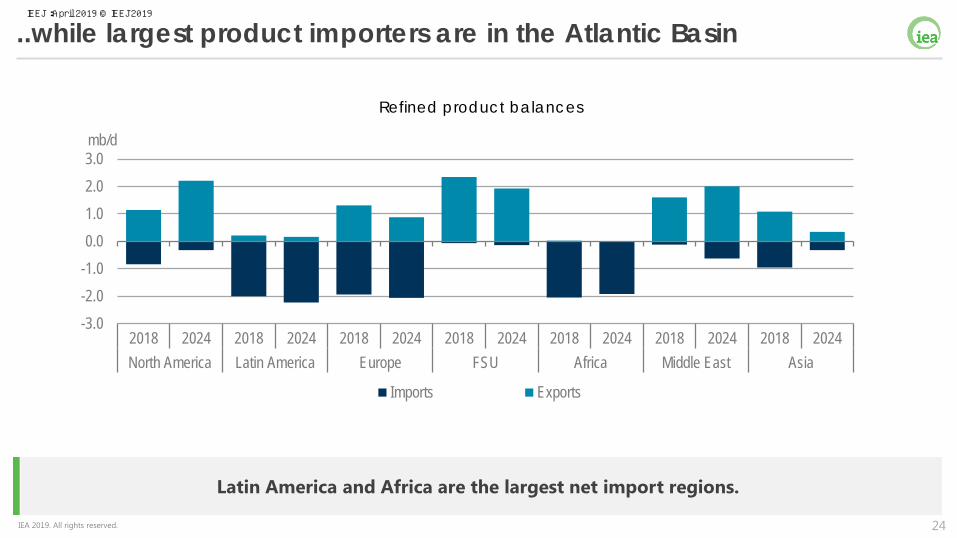

24IEA 2019. All rights reserved.

Latin America and Africa are the largest net import regions.

..while largest product importers are in the Atlantic Basin

-3.0-2.0-1.00.01.02.03.0

2018 2024 2018 2024 2018 2024 2018 2024 2018 2024 2018 2024 2018 2024North America Latin America Europe FSU Africa Middle East Asia

mb/d

Imports Exports

Refined product balances

IEEJ:April 2019 © IEEJ2019

25IEA 2019. All rights reserved.

Conclusions

• The United States to provide 70% of the increase in global oil supply over next five years, with Iraq, Brazil, Norway & Guyana other major contributors

• Global oil demand growth to slow modestly, but still average 1.2 mb/d, with petrochemicals a key driver

• The oil industry needs to do more to cut its carbon footprint, including on flaring & methane leakages, and use of CCUS, EOR, hydrogen & renewables

• While there may be teething problems, refiners & shippers are relatively well prepared to respond to the new IMO bunker fuel regulations

• The 2nd wave of the US shale revolution is coming – it will shake-up international oil & gas trade flows, with profound implications for the geopolitics of energy

IEEJ:April 2019 © IEEJ2019

26IEA 2019. All rights reserved. 26IEA 2019. All rights reserved.

Oil Market ReportApril 2019

IEEJ:April 2019 © IEEJ2019

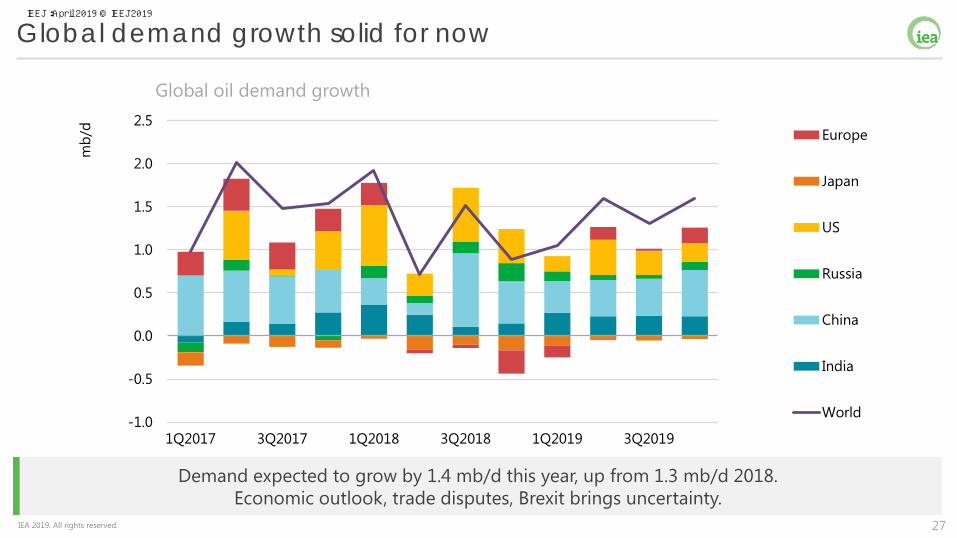

27IEA 2019. All rights reserved.

Global demand growth solid for now

Demand expected to grow by 1.4 mb/d this year, up from 1.3 mb/d 2018. Economic outlook, trade disputes, Brexit brings uncertainty.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1Q2017 3Q2017 1Q2018 3Q2018 1Q2019 3Q2019

mb/

d Europe

Japan

US

Russia

China

India

World

Global oil demand growth

IEEJ:April 2019 © IEEJ2019

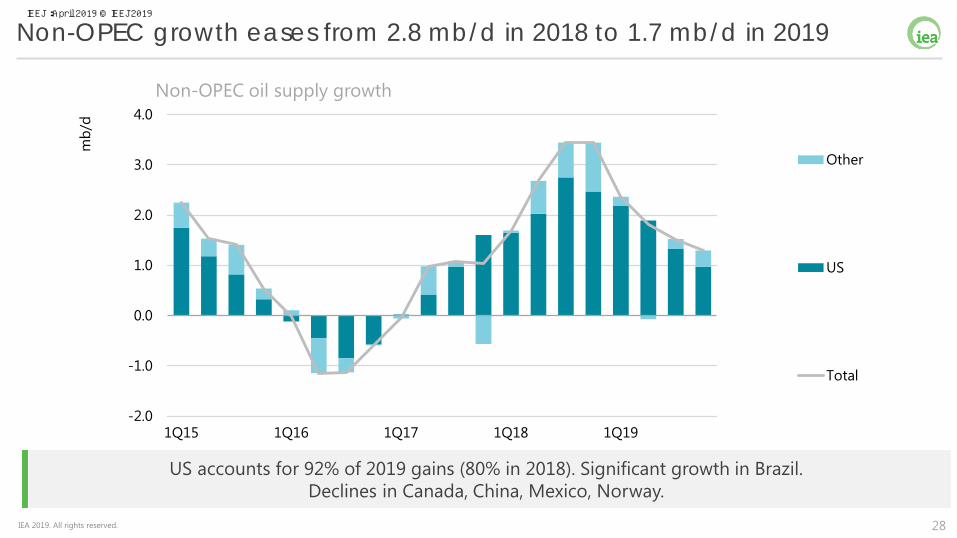

28IEA 2019. All rights reserved.

US accounts for 92% of 2019 gains (80% in 2018). Significant growth in Brazil. Declines in Canada, China, Mexico, Norway.

Non-OPEC growth eases from 2.8 mb/d in 2018 to 1.7 mb/d in 2019

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

1Q15 1Q16 1Q17 1Q18 1Q19

mb/

d

Other

US

Total

Non-OPEC oil supply growth

IEEJ:April 2019 © IEEJ2019

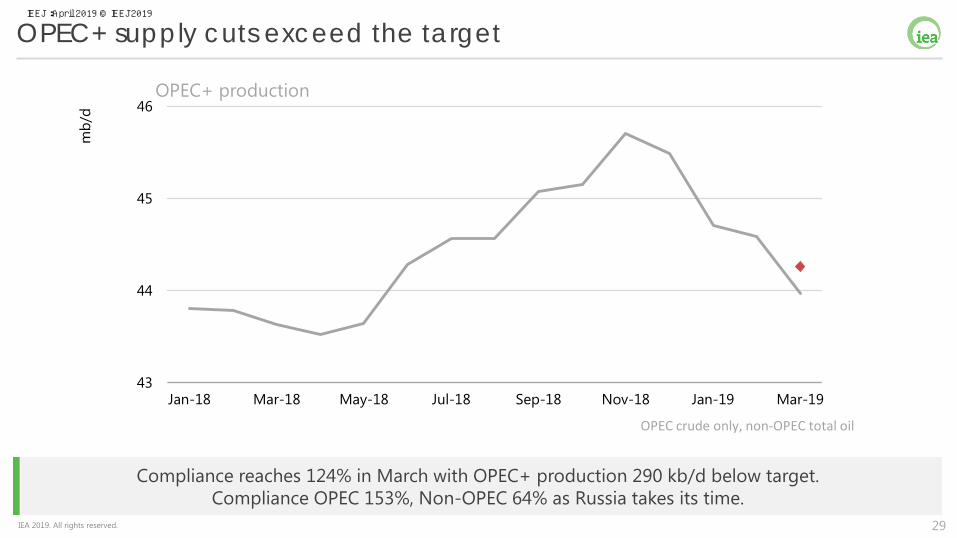

29IEA 2019. All rights reserved.

Compliance reaches 124% in March with OPEC+ production 290 kb/d below target. Compliance OPEC 153%, Non-OPEC 64% as Russia takes its time.

OPEC+ supply cuts exceed the target

43

44

45

46

Jan-18 Mar-18 May-18 Jul-18 Sep-18 Nov-18 Jan-19 Mar-19

mb/

d

OPEC crude only, non-OPEC total oil

OPEC+ production

IEEJ:April 2019 © IEEJ2019

30IEA 2019. All rights reserved.

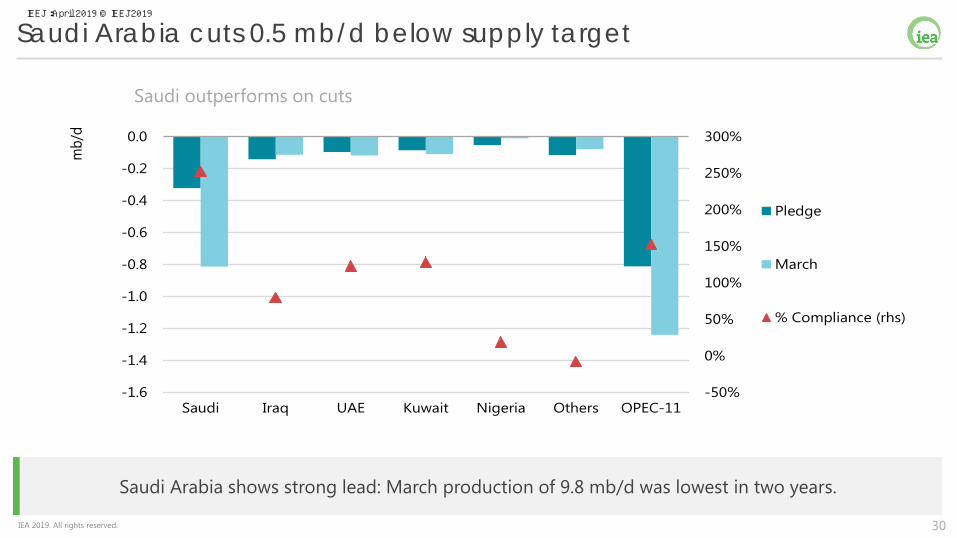

Saudi Arabia shows strong lead: March production of 9.8 mb/d was lowest in two years.

Saudi Arabia cuts 0.5 mb/d below supply target

-50%

0%

50%

100%

150%

200%

250%

300%

-1.6

-1.4

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

Saudi Iraq UAE Kuwait Nigeria Others OPEC-11

mb/

d

Pledge

March

% Compliance (rhs)

Saudi outperforms on cuts

IEEJ:April 2019 © IEEJ2019

31IEA 2019. All rights reserved.

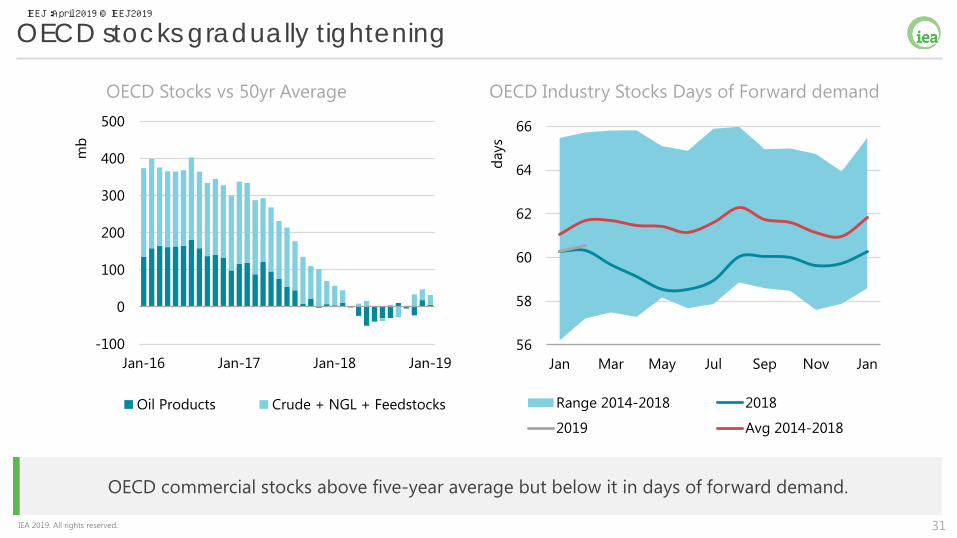

OECD commercial stocks above five-year average but below it in days of forward demand.

OECD stocks gradually tightening

OECD Stocks vs 50yr Average OECD Industry Stocks Days of Forward demand

-100

0

100

200

300

400

500

Jan-16 Jan-17 Jan-18 Jan-19

mb

Oil Products Crude + NGL + Feedstocks

56

58

60

62

64

66

Jan Mar May Jul Sep Nov Jan

days

Range 2014-2018 2018

2019 Avg 2014-2018

IEEJ:April 2019 © IEEJ2019

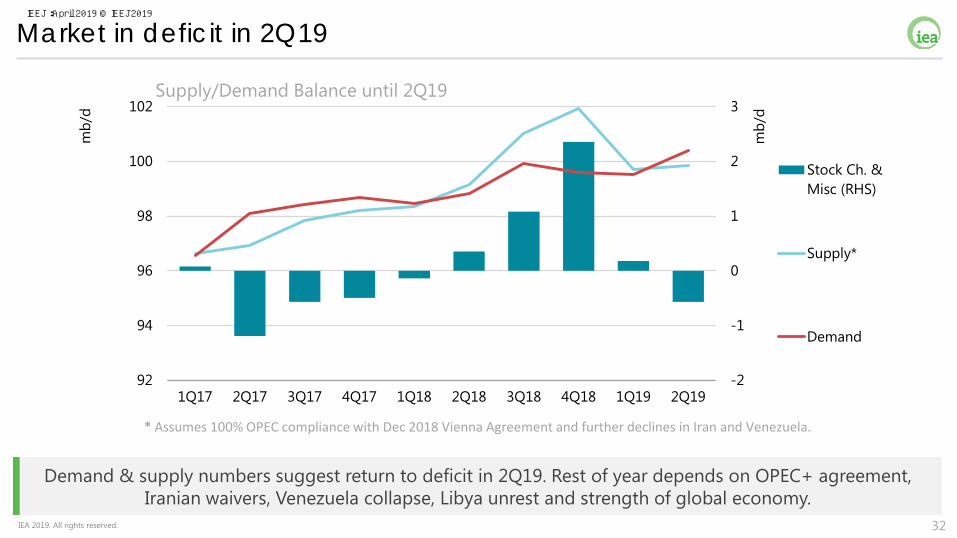

32IEA 2019. All rights reserved.

Demand & supply numbers suggest return to deficit in 2Q19. Rest of year depends on OPEC+ agreement, Iranian waivers, Venezuela collapse, Libya unrest and strength of global economy.

Market in deficit in 2Q19

Supply/Demand Balance until 2Q19

-2

-1

0

1

2

3

92

94

96

98

100

102

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19

mb/

d

mb/

d

Stock Ch. &Misc (RHS)

Supply*

Demand

* Assumes 100% OPEC compliance with Dec 2018 Vienna Agreement and further declines in Iran and Venezuela.

IEEJ:April 2019 © IEEJ2019

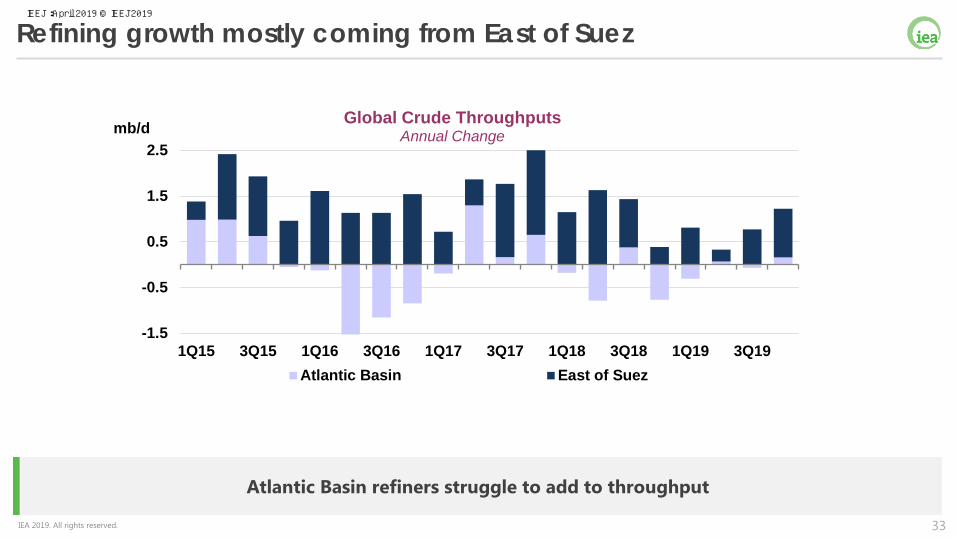

33IEA 2019. All rights reserved.

Atlantic Basin refiners struggle to add to throughput

Refining growth mostly coming from East of Suez

-1.5

-0.5

0.5

1.5

2.5

1Q15 3Q15 1Q16 3Q16 1Q17 3Q17 1Q18 3Q18 1Q19 3Q19

mb/d Global Crude ThroughputsAnnual Change

Atlantic Basin East of Suez

IEEJ:April 2019 © IEEJ2019

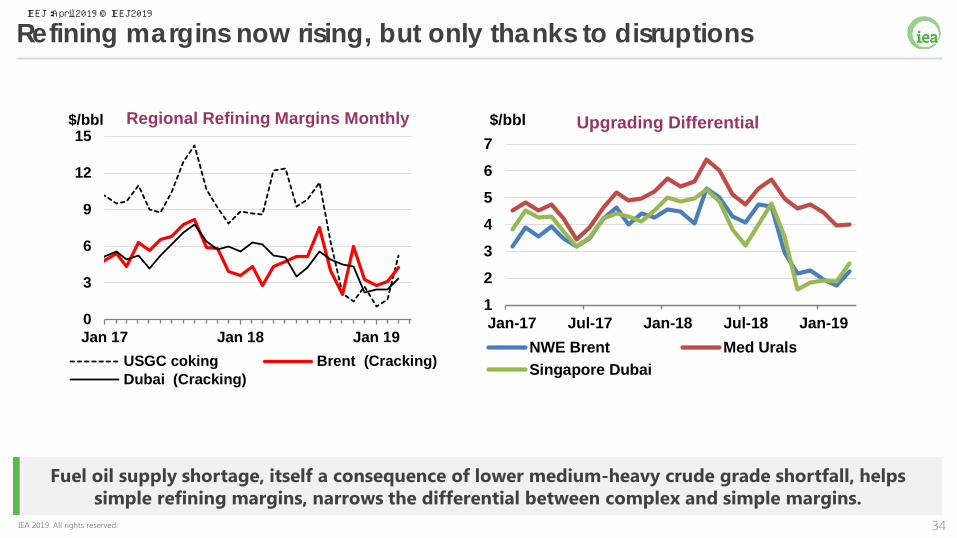

34IEA 2019. All rights reserved.

Fuel oil supply shortage, itself a consequence of lower medium-heavy crude grade shortfall, helps simple refining margins, narrows the differential between complex and simple margins.

Refining margins now rising, but only thanks to disruptions

0

3

6

9

12

15

Jan 17 Jan 18 Jan 19

$/bbl Regional Refining Margins Monthly

USGC coking Brent (Cracking)Dubai (Cracking)

1234567

Jan-17 Jul-17 Jan-18 Jul-18 Jan-19

$/bbl Upgrading Differential

NWE Brent Med UralsSingapore Dubai

IEEJ:April 2019 © IEEJ2019

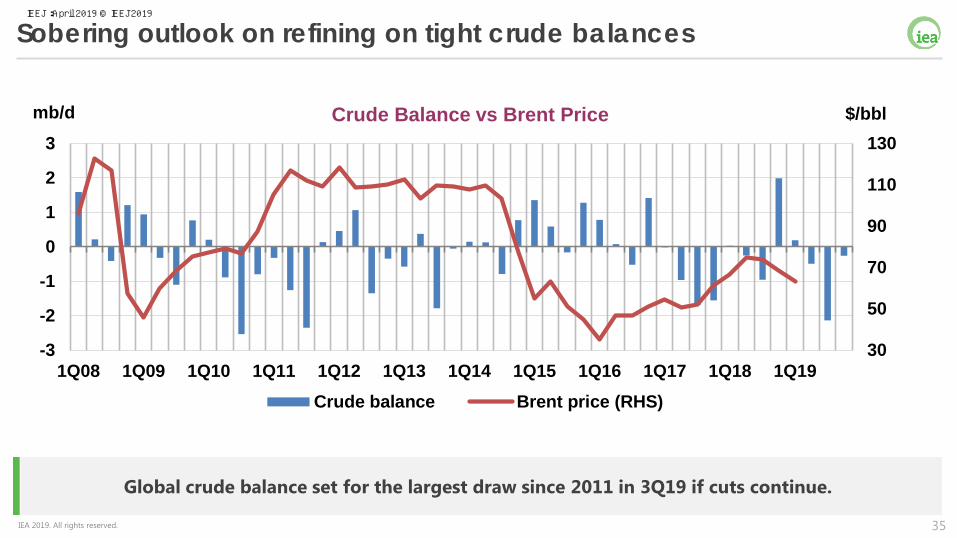

35IEA 2019. All rights reserved.

Global crude balance set for the largest draw since 2011 in 3Q19 if cuts continue.

Sobering outlook on refining on tight crude balances

30

50

70

90

110

130

-3

-2

-1

0

1

2

3

1Q08 1Q09 1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19

Crude Balance vs Brent Price

Crude balance Brent price (RHS)

mb/d $/bbl

IEEJ:April 2019 © IEEJ2019

36IEA 2019. All rights reserved.

www.iea.orgIEA

IEEJ:April 2019 © IEEJ2019

Contact :[email protected]