Embed Size (px)

Citation preview

1

Ohio Society of CPAsManufacturing and Construction

ConferenceAugust 17, 2012

Domestic and International Tax Incentives

Michael A. Krajcer, JD, CPA

2

Topics of Discussion

1. Research and Development Tax Credits – Federal and State

2. Interest Charge Domestic International Sales Corporation – The Last Surviving Export Incentive

3

Federal & State Research & Development Tax Credits

OVERVIEW:

• Federal and state incentive intended to encourage domestic spending on research and development.

• Taxpayer favorable legislation has simplified the calculation of the credit and made it available to a larger population of taxpayers.

• Taxpayer favorable regulation has expanded the definition of research and development, so now more activity qualifies for the credit.

• Taxpayer favorable rulings from the courts have provided guidance on documentation requirements and clarification on several technical issues.

4

LEGISLATIVE HISTORYTHE HIGHLIGHTS

• Enacted in 1981, as a temporary provision.

• 1986 – added additional requirements to the definition of qualified activity.

• 1989 – replaced base period with base amount concept.

• Alternative Simplified Credit (“ASC”) added for years ending after December 31, 2006.

• ASC rate increased to 14% and AIRC eliminated, for years ending after December 31, 2008.

• Credit extended 15 times; currently to 12/31/2011.

5

BENEFITS OF THE CREDIT

FEDERAL:

• A federal income tax credit equal to 20% or 14% of the qualifying expenses.• Percentage depends on the calculation methodology elected

• R&D expenses must be reduced by the amount of the credit earned.

• The credit is non-refundable.

• The credit generally cannot offset AMT.

• Part of the General Business Credit – thus subject to a one year carryback and 20 year carryforward.

• Previous years unclaimed credits can be secured via amended returns• Subject to IRS Tier 1 scrutiny

6

BENEFITS OF THE CREDIT

STATE:

• The majority of the states offer a credit.

• Some state credits exceed the federal amount.

• Ohio provides for a 7% credit on the amount that qualifying expenditures .

• The Ohio R&D Tax Credit does not flow to shareholder as in other states but can be used to offset the CAT tax.

• Mr. Krajcer is working with State Legislators to revise flow-through and refund provisions.

7

FOR WHAT INDUSTRIES IS THE CREDIT APPLICABLE?

• Manufacturing

• Construction

• Software Developers

• Financial Institutions

• Life Sciences

• Architecture & Engineering Firms

• Oil & Gas

• Aerospace

• Polymer Sciences

• Pharmaceuticals

8

WHAT ACTIVITIES QUALIFY FOR THE CREDIT?

Activities must meet a four-part test:1. Business Component Test2. Technical Uncertainty3. Process of Experimentation4. Scientific Principles

9

WHAT ACTIVITIES QUALIFY FOR THE CREDIT?

Activities must meet a four-part test:1. Business Component Test

• A business component is any product, process, computer software, technique, formula, or invention, which is to be either held for sale, lease, or license by the company or used in the company's trade or business.

The improvement must be a functional improvement rather than

an aesthetic change.

Functionality Performance Reliability Quality

10

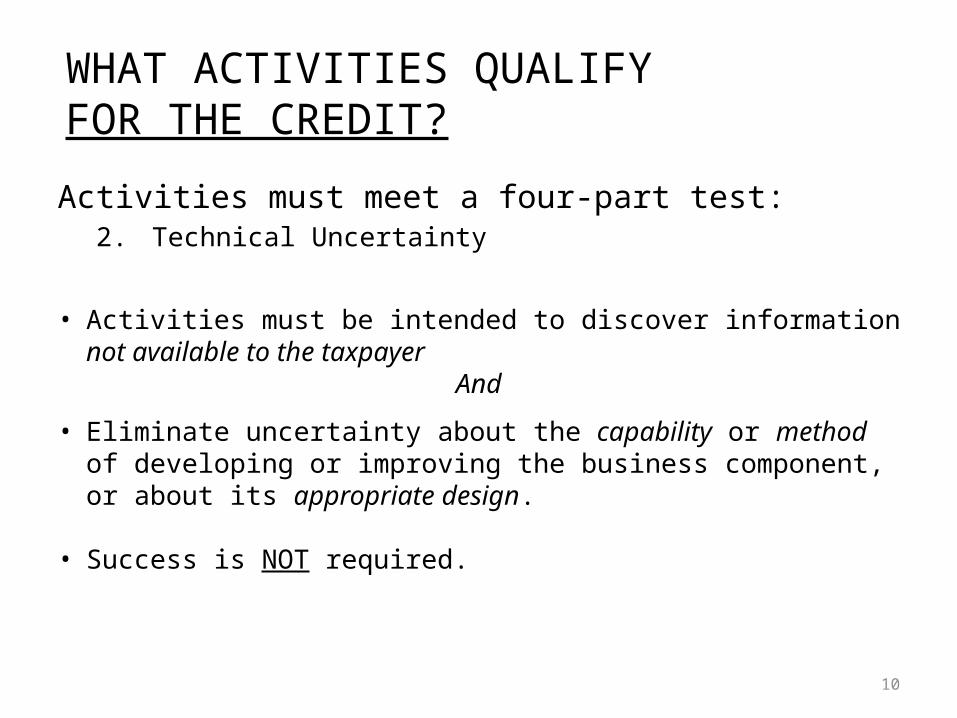

WHAT ACTIVITIES QUALIFY FOR THE CREDIT?

Activities must meet a four-part test:2. Technical Uncertainty

• Activities must be intended to discover information not available to the taxpayer

And

• Eliminate uncertainty about the capability or method of developing or improving the business component, or about its appropriate design.

• Success is NOT required.

11

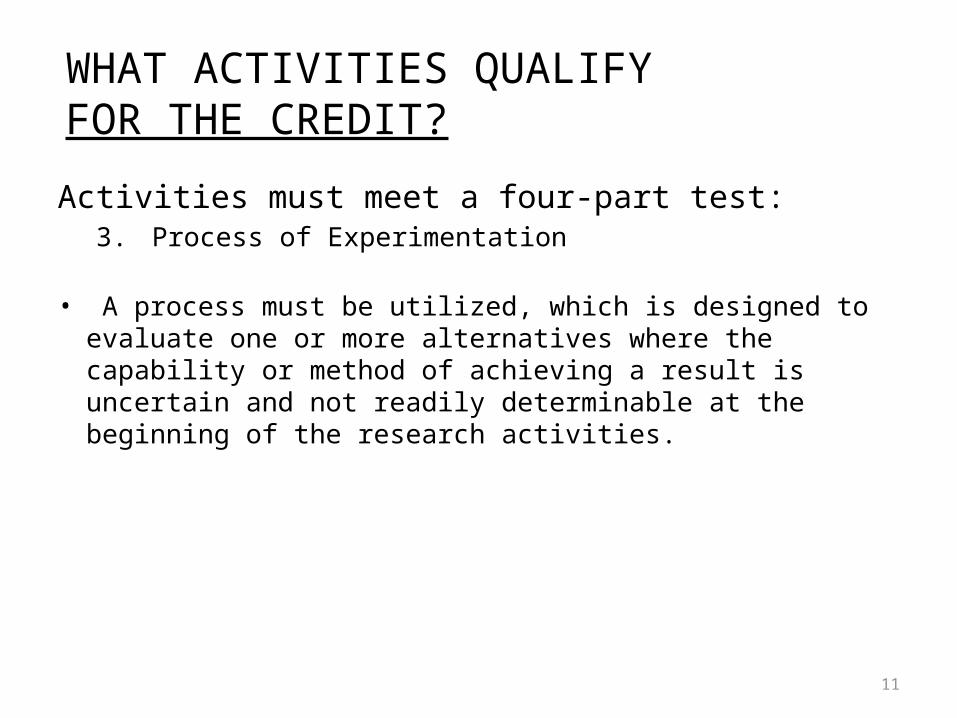

WHAT ACTIVITIES QUALIFY FOR THE CREDIT?

Activities must meet a four-part test:3. Process of Experimentation

• A process must be utilized, which is designed to evaluate one or more alternatives where the capability or method of achieving a result is uncertain and not readily determinable at the beginning of the research activities.

12

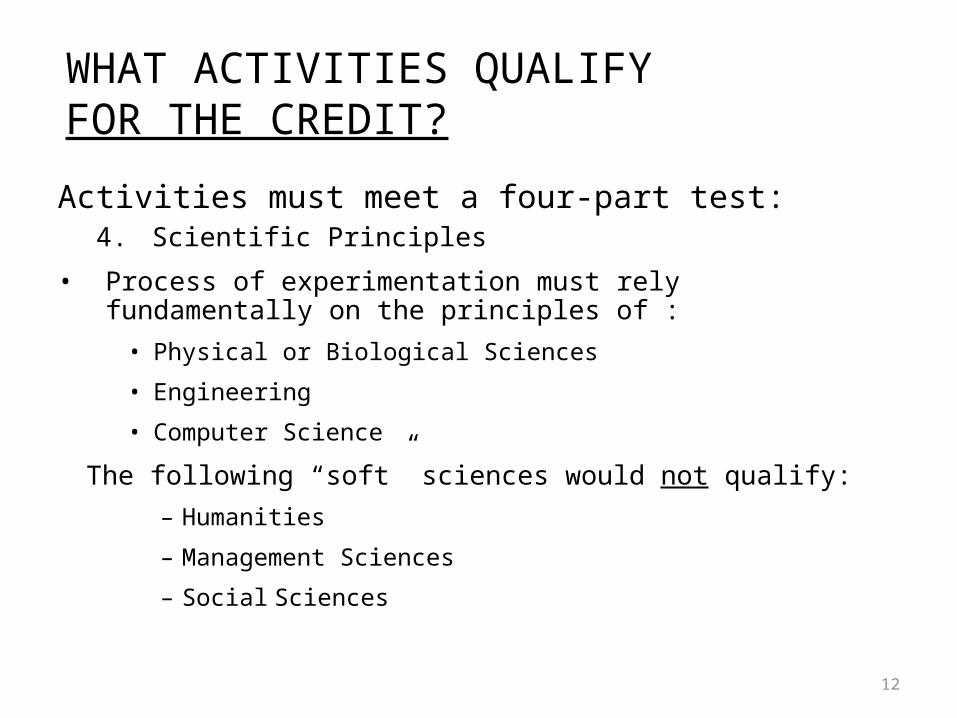

WHAT ACTIVITIES QUALIFY FOR THE CREDIT?

Activities must meet a four-part test:4. Scientific Principles

• Process of experimentation must rely fundamentally on the principles of :

• Physical or Biological Sciences

• Engineering

• Computer Science

The following “soft” sciences would not qualify:

– Humanities

– Management Sciences

– Social Sciences

13

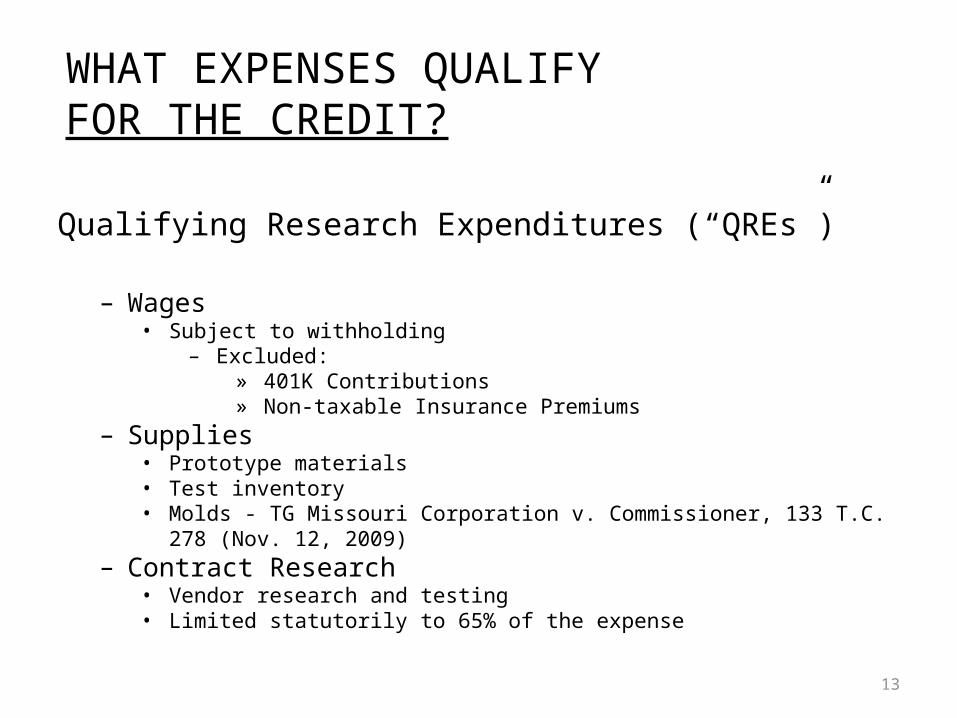

WHAT EXPENSES QUALIFY FOR THE CREDIT?

Qualifying Research Expenditures (“QREs”)

– Wages• Subject to withholding

– Excluded:» 401K Contributions» Non-taxable Insurance Premiums

– Supplies• Prototype materials• Test inventory• Molds - TG Missouri Corporation v. Commissioner, 133 T.C. 278

(Nov. 12, 2009)– Contract Research

• Vendor research and testing• Limited statutorily to 65% of the expense

14

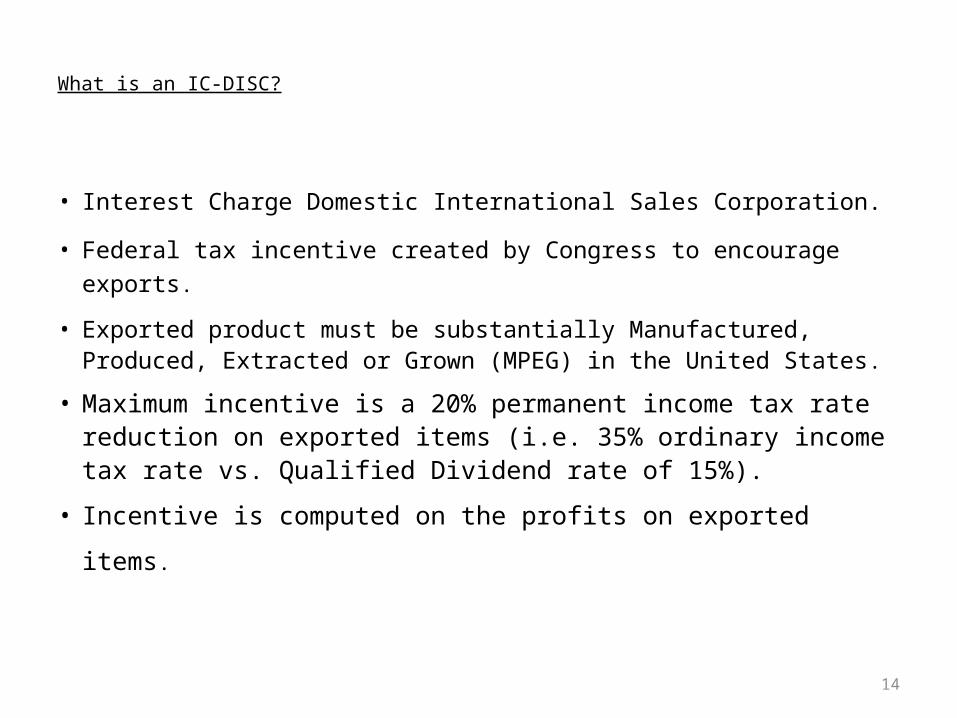

What is an IC-DISC?

• Interest Charge Domestic International Sales Corporation.

• Federal tax incentive created by Congress to encourage exports.

• Exported product must be substantially Manufactured, Produced, Extracted or Grown (MPEG) in the United States.

• Maximum incentive is a 20% permanent income tax rate reduction on exported items (i.e. 35% ordinary income tax rate vs. Qualified Dividend rate of 15%).

• Incentive is computed on the profits on exported items.

15

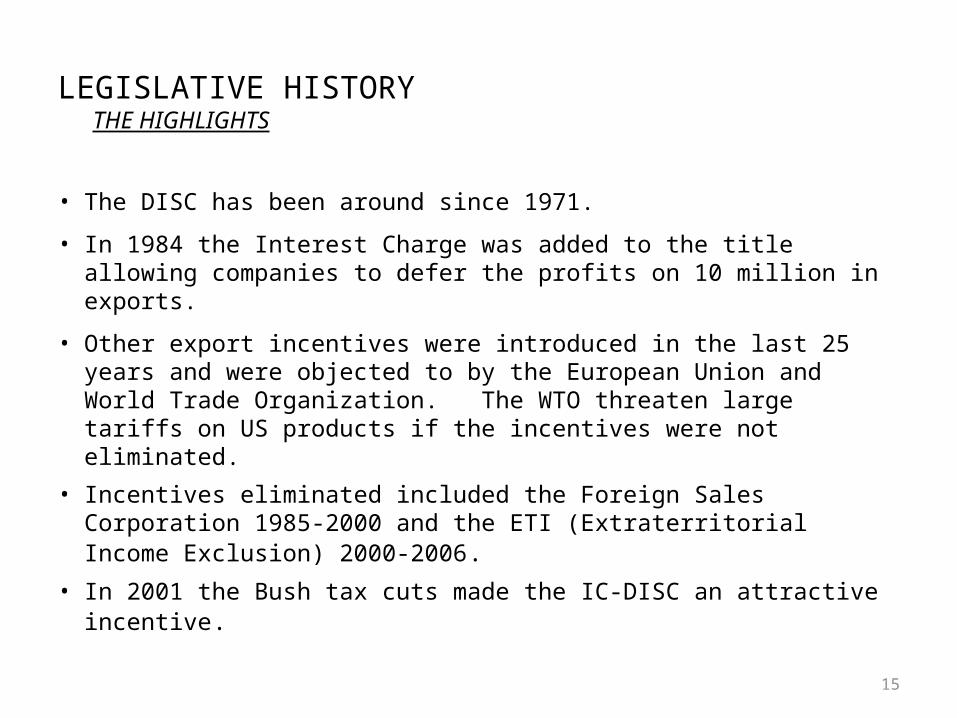

LEGISLATIVE HISTORYTHE HIGHLIGHTS

• The DISC has been around since 1971.

• In 1984 the Interest Charge was added to the title allowing companies to defer the profits on 10 million in exports.

• Other export incentives were introduced in the last 25 years and were objected to by the European Union and World Trade Organization. The WTO threaten large tariffs on US products if the incentives were not eliminated.

• Incentives eliminated included the Foreign Sales Corporation 1985-2000 and the ETI (Extraterritorial Income Exclusion) 2000-2006.

• In 2001 the Bush tax cuts made the IC-DISC an attractive incentive.

16

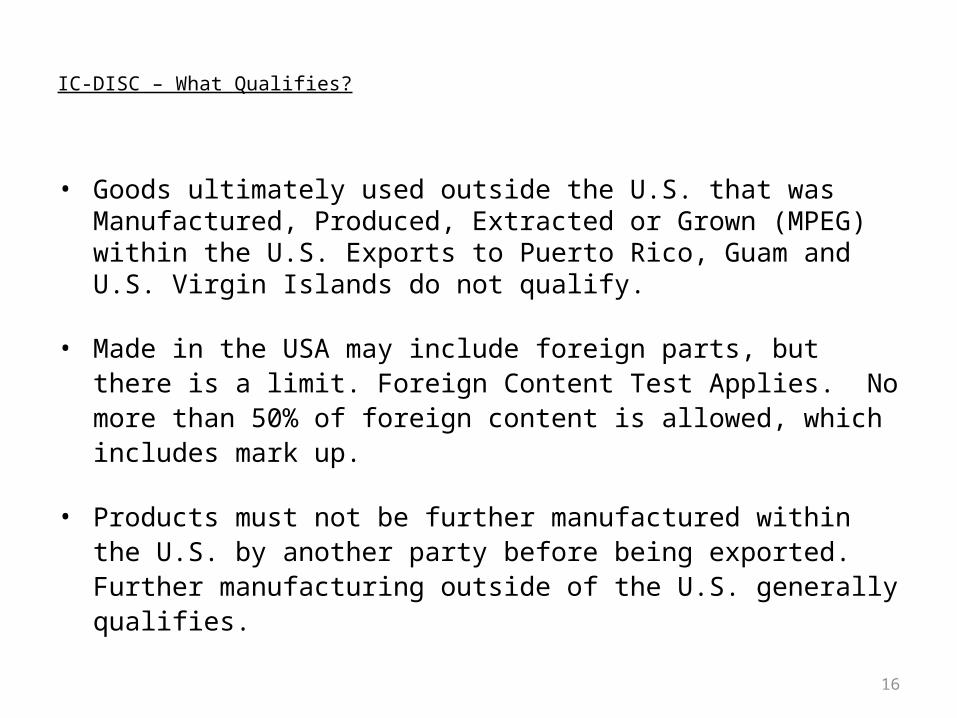

IC-DISC – What Qualifies?

• Goods ultimately used outside the U.S. that was Manufactured, Produced, Extracted or Grown (MPEG) within the U.S. Exports to Puerto Rico, Guam and U.S. Virgin Islands do not qualify.

• Made in the USA may include foreign parts, but there is a limit. Foreign Content Test Applies. No more than 50% of foreign content is allowed, which includes mark up.

• Products must not be further manufactured within the U.S. by another party before being exported. Further manufacturing outside of the U.S. generally qualifies.

17

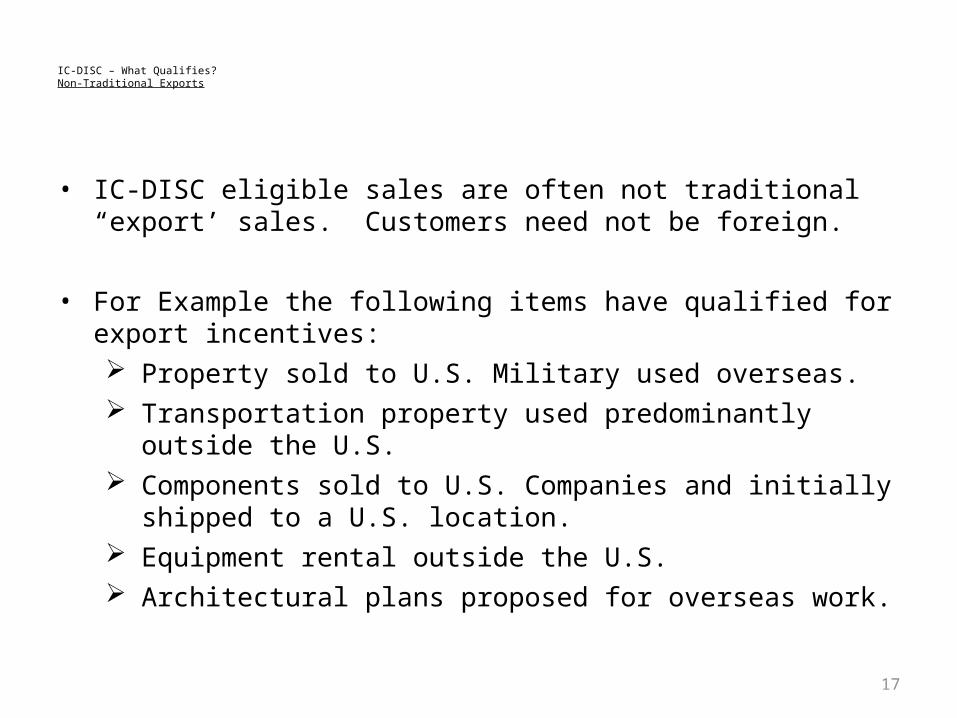

IC-DISC – What Qualifies?Non-Traditional Exports

• IC-DISC eligible sales are often not traditional “export’ sales. Customers need not be foreign.

• For Example the following items have qualified for export incentives: Property sold to U.S. Military used overseas. Transportation property used predominantly outside

the U.S. Components sold to U.S. Companies and initially

shipped to a U.S. location. Equipment rental outside the U.S. Architectural plans proposed for overseas work.

18

Steps to Implement an IC-DISC

• Requires setup of a C Corp. which elects treatment as an IC-DISC by filing Federal Form 4876-A within 90 days of setting up a corporation.

• Creation of specific inter-company agreements between the IC-DISC and the IC-DISC owners.

• Requires computation of the IC-DISC Commission (Multiple methods to compute the DISC commission).

• Annual filing of a 1120-IC-DISC tax return. Return due 9/15 each year. No extension required.

• No change in business operations needed. Transparent to customers.

• Requires journal entries and movement of cash between entities.

19

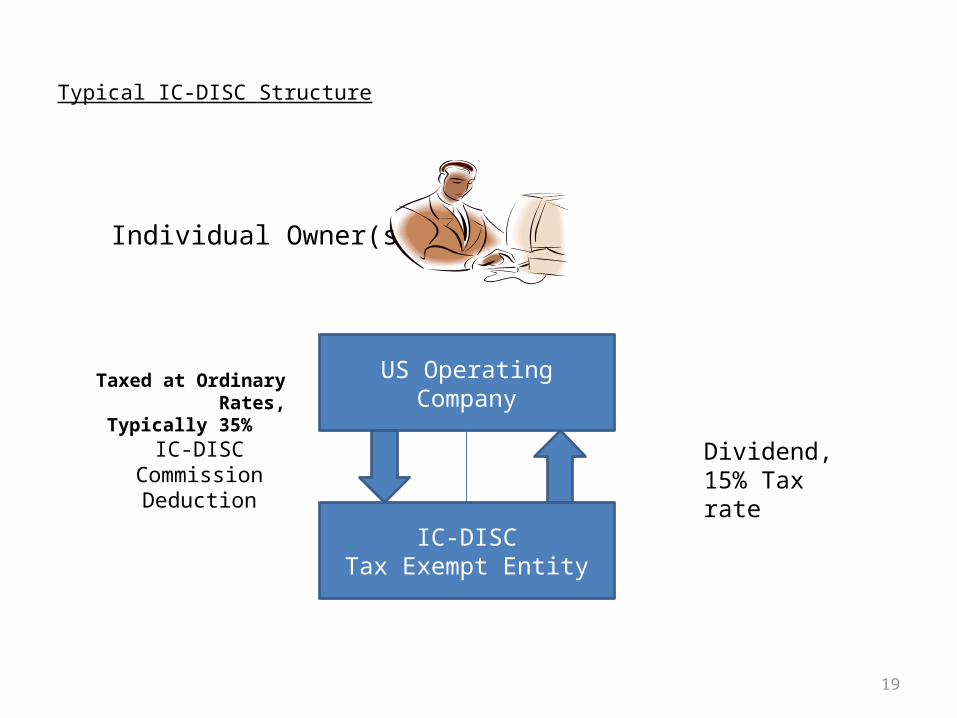

Typical IC-DISC Structure

Individual Owner(s)

US Operating Company

IC-DISCTax Exempt Entity

Taxed at Ordinary Rates,Typically 35%

IC-DISC Commission Deduction

Dividend, 15% Tax rate

20

Example of DISC Benefits

Without IC-DISC With IC-DISC Net Savings

Export Sales 5,000,000 5,000,000

Net Margin 20% 20%

Net Profit 1,000,000 1,000,000

IC-DISC Commission (50% Method)

500,000

Taxable Income 1,000,000 500,000

Tax Rate 35% 35%

a) Corp. Level Taxation 350,000 175,000 175,000

Div. To Shareholder 0 500,000

Tax Rate 15% 15%

b) Shareholder Level Taxation

0 75,0000 (75,000)

c) Total taxation (c=a+b)

350,000 250,000 100,000

21

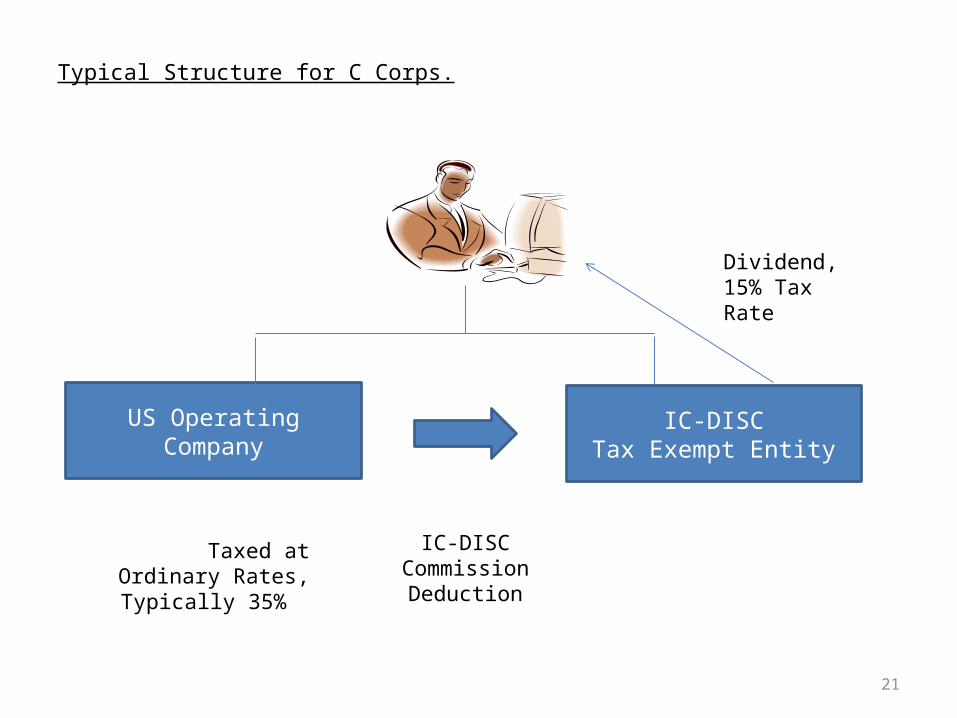

Typical Structure for C Corps.

US Operating Company IC-DISCTax Exempt Entity

Taxed at Ordinary Rates,Typically 35%

Dividend, 15% Tax Rate

IC-DISC Commission Deduction

22

IC-DISC Commission

• IC-DISC commissions need to be computed by qualified DISC experts.

• Certain firms and CPAs will do the most basic calculations to compute a DISC commission but they are not capturing all of the DISC benefit.

• Sophisticated calculation engines can maximize tax savings by dramatically increasing the IC-DISC benefit using the intended, allowable, complex methods in the regulations (TxT Analysis).

23

IC-DISC Commission

• Loss Exclusion – Loss transactions may be excluded, allowing benefit to be derived from profitable transactions.

• Marginal Costing – In conjunction with TxT Analysis, marginal costing is an element of the IC-DISC regulations which allows less profitable transactions to derive IC-DISC benefit largely as if they were as profitable as an average transaction.

• Marginal costing can be applied at transactional, product, product line levels. Software is needed to optimize marginal benefits in conjunction with the loss exclusion.

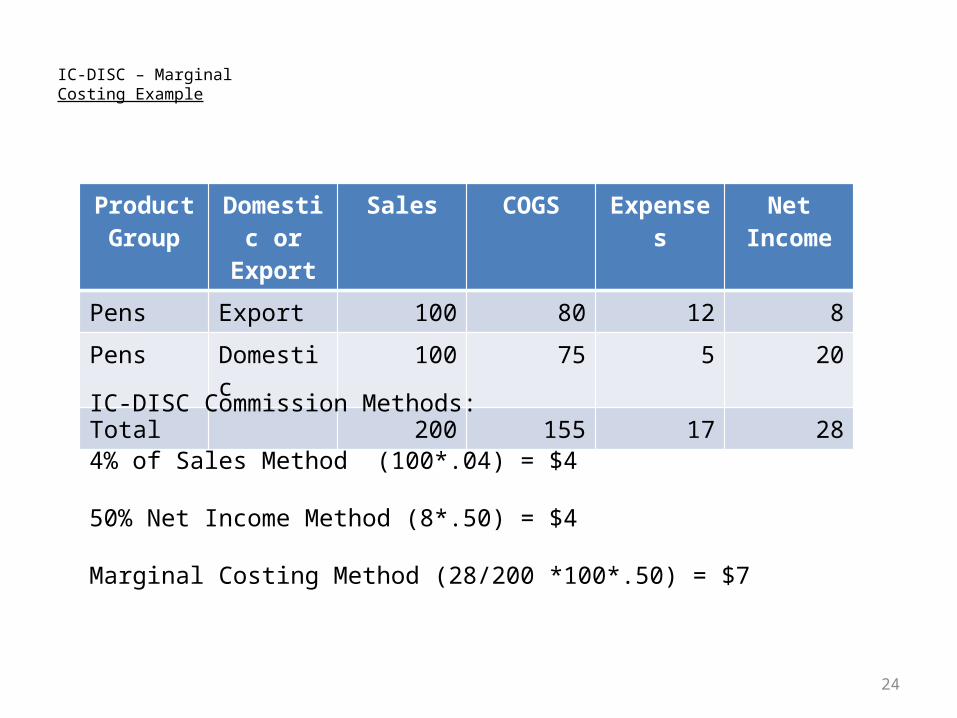

24

IC-DISC – Marginal Costing Example

Product Group

Domestic or Export

Sales COGS Expenses Net Income

Pens Export 100 80 12 8Pens Domestic 100 75 5 20Total 200 155 17 28

IC-DISC Commission Methods:

4% of Sales Method (100*.04) = $4

50% Net Income Method (8*.50) = $4

Marginal Costing Method (28/200 *100*.50) = $7

25

Legislative Backdrop and Outlook

• The qualified dividend rate expires with the bush tax cuts on December 31, 2012.

• Bothe political parties have indicated strong support of the qualified dividend rate and encouraging exports.

• As long as the spread remains between the ordinary income tax rate and qualified dividends the DISC will be alive well past December 31, 2012.

26

Questions

Thank You

Michael Krajcer, JD, CPA3979 Idlewild DriveCleveland, OH 44116Office: (440) 331-0714Cell: (216) 308-1564