Embed Size (px)

Citation preview

OH 5-1

Agenda

Questions regarding Chapter 2 & 3 workbook

Chapter 4: Cost-Volume-Profit Relationships PowerPoint Workbook

Chapter 5: PowerPoint Workbook

Next week

OH 5-2

Cost-Volume-Profit Relationships

Controlling Foodservice Costs

4OH 5-2

OH 5-3

Chapter Learning Objectives

Explain Variable Costs

Describe the variable rate

Describe the components of the contribution margin

Describe the contribution margin

Calculate the variable cost and rate, contribution margin and rate, and calculate the break-even point in sales dollars and sales units

Determine which formula to use for various calculations

OH 5-4

Components of Sales

Dollar terms: Without understanding where sales revenue is spent, it is hard to control costs and create profitability.

Since profitability is why most operations are in business, formulas to calculate profit are needed.

OH 5-5

Variable Costs

Costs that will change with the increase or decrease in the volume of business

Examples: food & beverage costs, supplies, wages & benefits Do variable costs include salaried employees?

Actual cost of the product and service that is for sale

OH 5-6

Contribution Margin

Contribution Margin is composed of fixed costs and the profit generated by sales

Fixed costs: Examples: salaried employees & their benefits, rent,

equipment depreciation, insurance, utilities, etc.

Profit generated by sales – Bottom line

OH 5-7

Examples of Contribution Margin

Example of an actual Contribution Analysis used

Let’s turn to page 48 in the text; example problem

OH 5-8

Components of Sales

Percentage terms: The percent of each dollar in sales that goes towards different expenses is needed in forecasting, planning and analysis of financial data.

OH 5-9

Variable Rate and Contribution Rate

In Chapters 2, what was the formula we used to calculate the food cost percent?

When comparing variable rate and contribution rate to sales, we use the exact same formula.

Let’s turn to page 50 in the text book

The variable rate is the percent of costs that we can control

OH 5-10

Break-Even Point

This formula is used to calculate either the dollar sales, or unit sales, needed to break even in a business.

Let’s turn to page 52 of the text

How does profit fit into the break even analysis?

Why would you need to know the number of units to be sold in a break even analysis?

OH 5-11

Average Variable Costs

Average contribution margins take into account the number of sales of each item as well as the contribution margin of each item. This information is used to compare one item to another and to analyze overall financial data

Let’s turn to page 54 in the text, example problem

OH 5-12

Improving Profit by Changing the Break-Even Point

Three items we can control Raise prices

Variable cost

Evaluate quality

OH 5-13

Workbook Chapter 4

OH 5-14

Controlling Food Costs in Purchasing

Controlling Foodservice Costs

5OH 5-14

OH 5-15

Chapter Learning Objectives

Explain how a specification becomes a control in the purchasing function.

Explain the parts of a purchase specification and a purchase order (Purchase Specification).

Explain various purchasing methods and their effect on the price of goods.

Use formulas including:

Periodic ordering amount, Perpetual ordering amount, As purchased (AP), Edible portion (EP) for both food quantity and food cost.

OH 5-16

Chapter Learning Objectives continued

Calculate a yield test that identifies the difference between as purchased (AP) price and edible portion (EP) cost.

Identify factors that affect the purchase price of goods.

Distinguish between perishable and nonperishable goods and their relationship to the purchasing cycle.

Calculate the amount of goods to purchase for catered events.

OH 5-17

Who Purchases?

Purchasing agent

Manager

Chef

Head cook

Trusted staff member

The buyer maintains quality standards!

OH 5-18

Who Purchases? continued

The buyer is responsible for ensuring that quality standards are met during the purchasing and delivery process.

OH 5-19

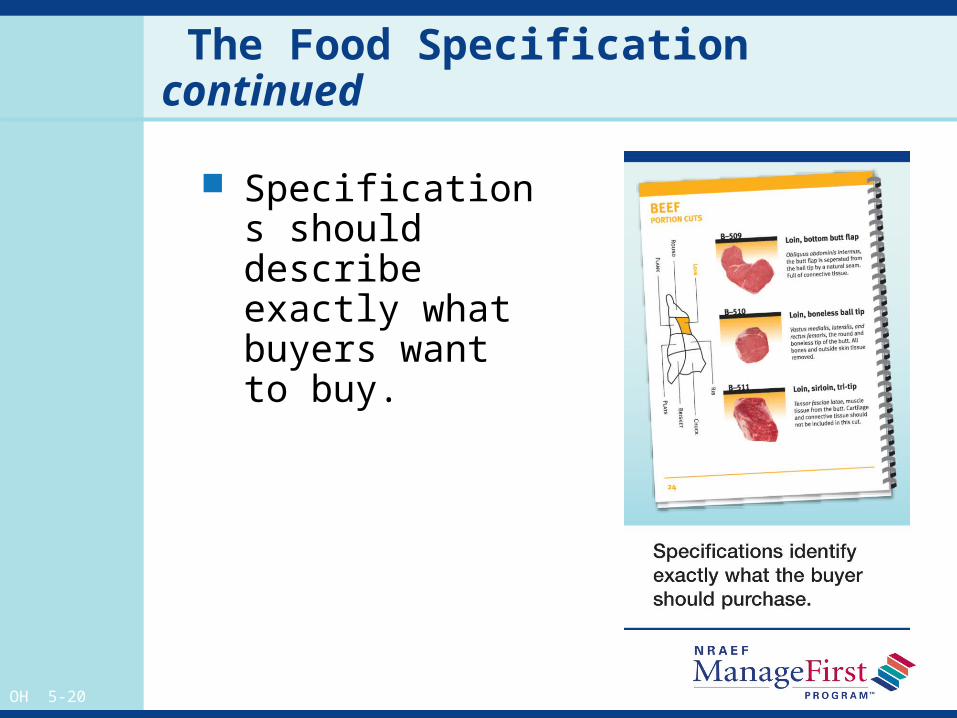

The Food Specification

Is a control device

Lists the product’s name

Lists its intended use

Identifies the desired brand and grade

Identifies the desired size

Identifies the desired variety

Identifies packing requirements

Details delivery requirements

Explains payment terms

OH 5-20

The Food Specification continued

Specifications should describe exactly what buyers want to buy.

OH 5-21

Purchase Orders

The official written record of the items the buyer wants to purchase

OH 5-22

Purchase Order Information

A unique identification number

The name and address of the restaurant

Date of the order

Signature of the buyer

The supplier’s contact information

Date of delivery

The name, quantity, and delivery unit of each item ordered

Total (extended) cost of the order

OH 5-23

Ordering Methods page 21 workbook

Periodic order method – example p. 62 text

Minimum par level

Perpetual ordering method

Safety stock

OH 5-24

Inventory Methods page 21 workbook

Perpetual inventory method

Physical inventory method

OH 5-25

Purchase Methods page 23 in workbook

Competitive quotes Open bids Market Quotation

Sheet

Sealed bids

Cost-plus

Co-operative

One-stop shop

Contract

Warehouse buying

Standing order

Commissary/Centralized purchasing

On-Line purchasing

OH 5-26

What to Buy

Avoid buying the “cheapest.”

Use purchase specifications.

Buy at the best cost from sellers who meet or exceed the purchase specifications.

Consider both AP price and EP cost.

OH 5-27

Two Kinds of Costs

As purchased (AP)—the cost of food as delivered to the restaurant

Edible portion (EP)—the cost of food as served to the guest

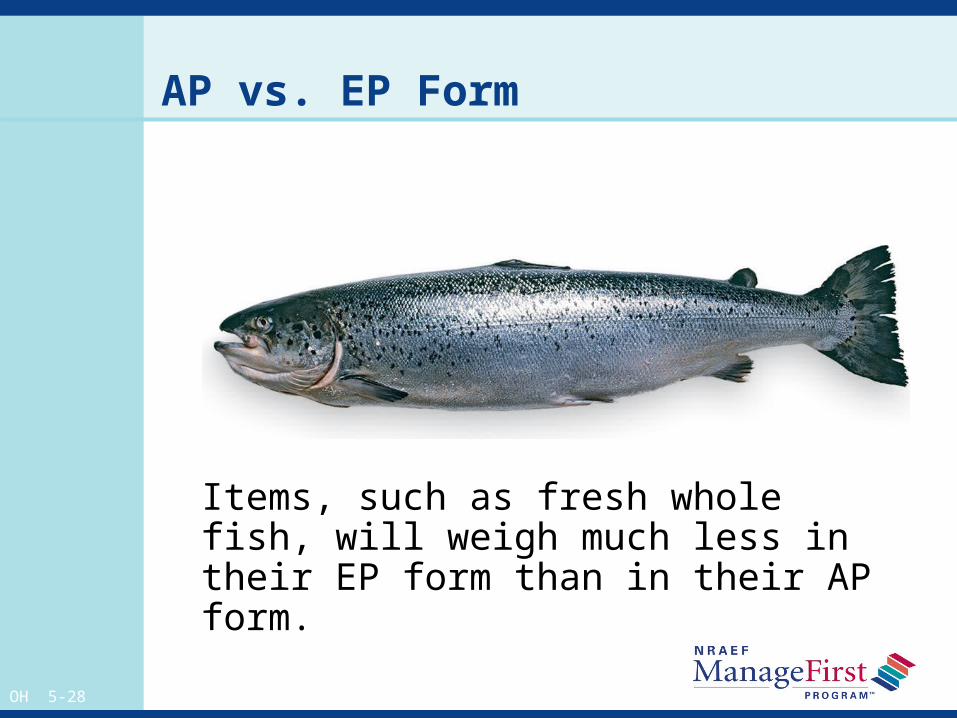

OH 5-28

AP vs. EP Form

Items, such as fresh whole fish, will weigh much less in their EP form than in their AP form.

OH 5-29

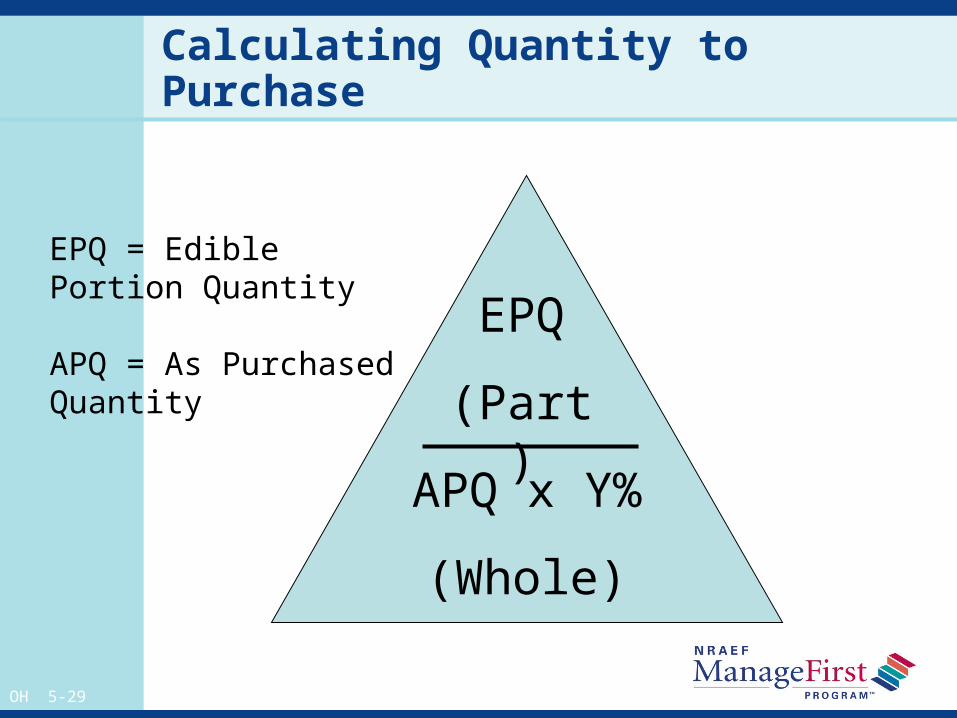

Calculating Quantity to Purchase

EPQ

(Part)

APQ x Y%

(Whole)

EPQ = Edible Portion Quantity

APQ = As Purchased Quantity

OH 5-30

Yield % Charts

Yield % Charts Approximate Weight/Each

Item description

Yield %

Other resources Book of Yields - Francis Talyn Lynch

Culinary Calculators

OH 5-31

Using Yield % Charts

Yield % charts are only approximate

You must do your own yield tests on the actual product you are using in order to get completely accurate figures.

Some factors that affect yield:

Employee skill level

Size of the product

Condition or quality of the product

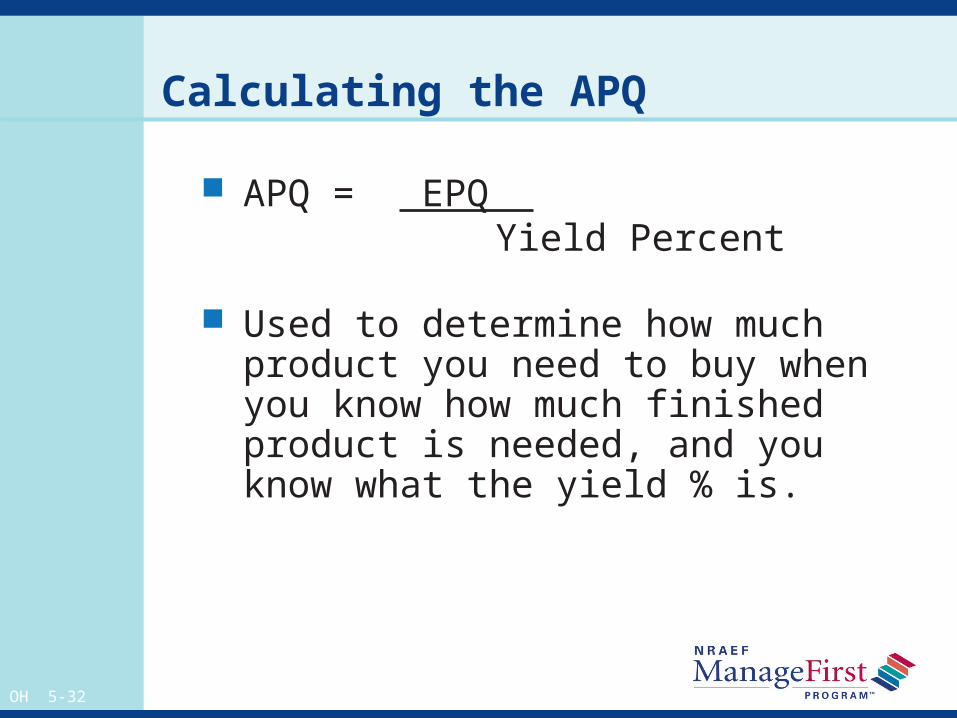

OH 5-32

Calculating the APQ

APQ = EPQ Yield Percent

Used to determine how much product you need to buy when you know how much finished product is needed, and you know what the yield % is.

OH 5-33

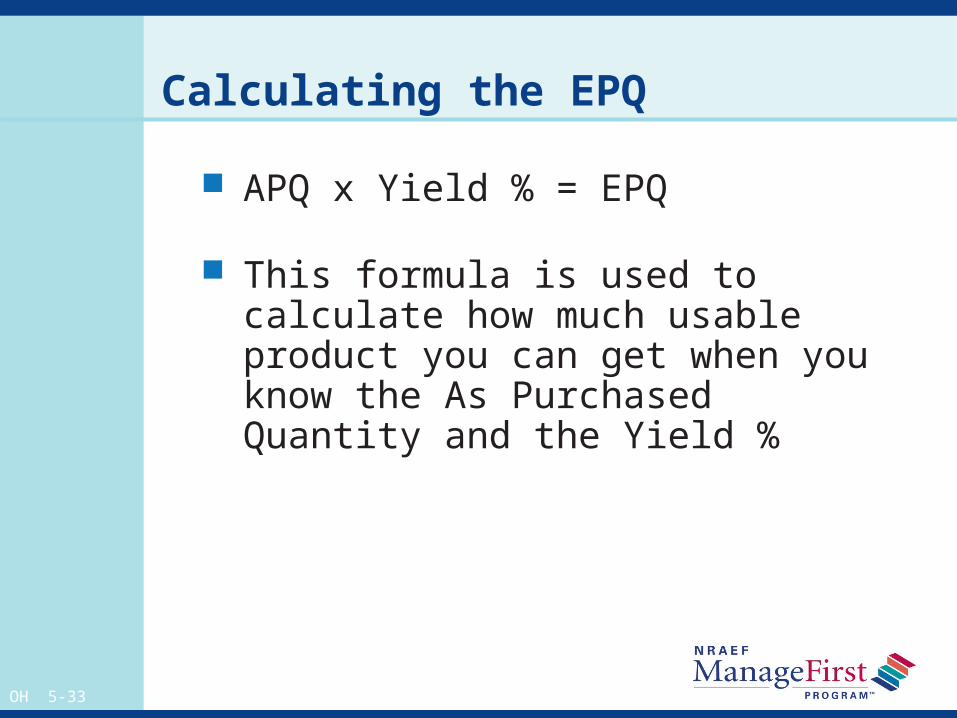

Calculating the EPQ

APQ x Yield % = EPQ

This formula is used to calculate how much usable product you can get when you know the As Purchased Quantity and the Yield %

OH 5-34

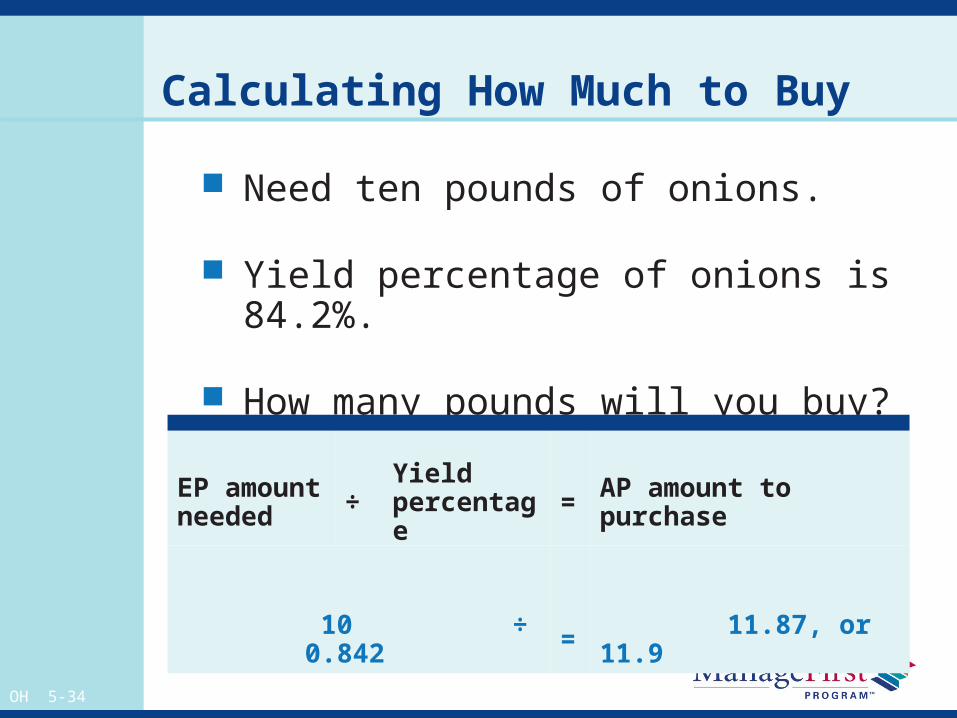

Calculating How Much to Buy

Need ten pounds of onions.

Yield percentage of onions is 84.2%.

How many pounds will you buy?

EP amount needed ÷ Yield

percentage = AP amount to purchase

10 ÷ 0.842 = 11.87, or 11.9

OH 5-35

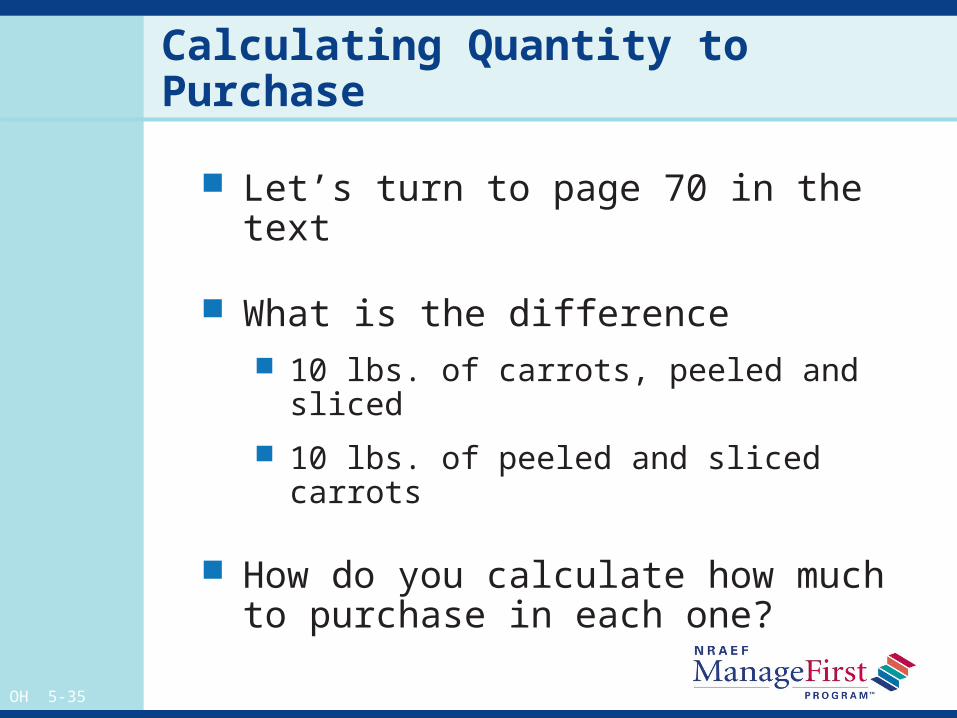

Calculating Quantity to Purchase

Let’s turn to page 70 in the text

What is the difference 10 lbs. of carrots, peeled and sliced

10 lbs. of peeled and sliced carrots

How do you calculate how much to purchase in each one?

OH 5-36

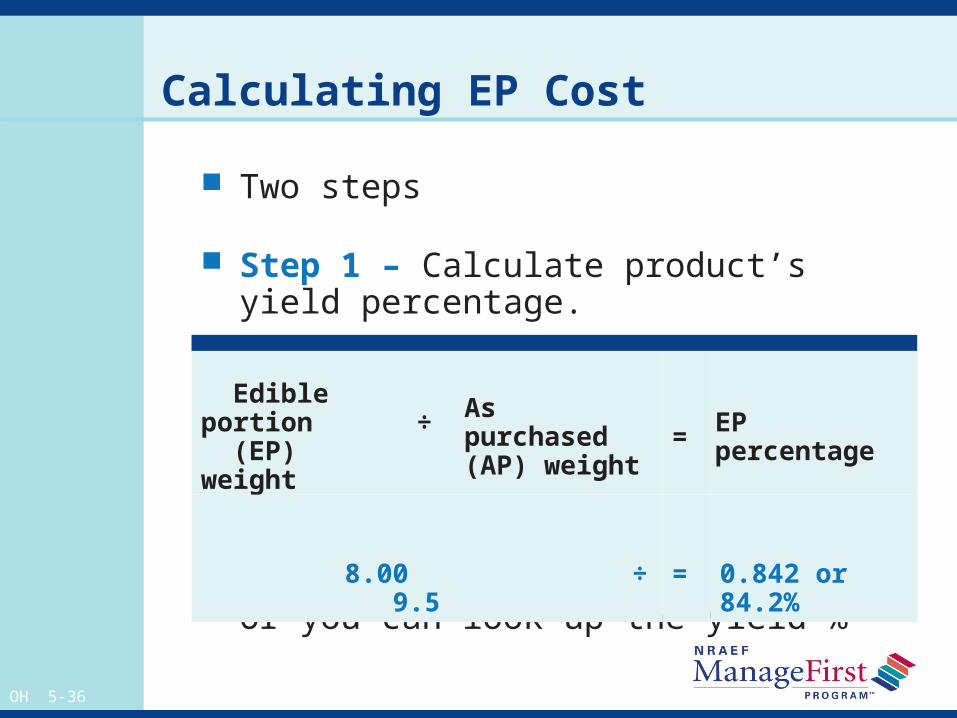

Calculating EP Cost

Two steps

Step 1 – Calculate product’s yield percentage.

Or you can look up the yield %

Edible portion

(EP) weight÷ As purchased

(AP) weight = EP percentage

8.00 ÷ 9.5 = 0.842 or 84.2%

OH 5-37

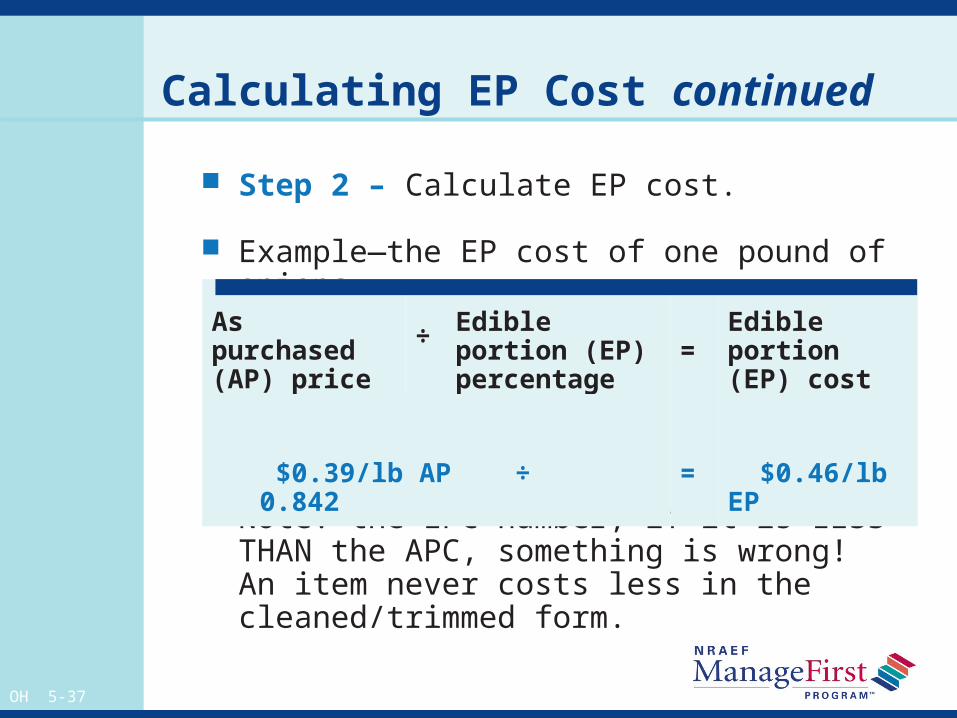

Calculating EP Cost continued

Step 2 – Calculate EP cost.

Example—the EP cost of one pound of onions

Note: the EPC number, if it is LESS THAN the APC, something is wrong! An item never costs less in the cleaned/trimmed form.

As purchased (AP) price

÷

Edible portion (EP) percentage = Edible portion

(EP) cost

$0.39/lb AP ÷ 0.842 = $0.46/lb EP

OH 5-38

Other Factors Affecting Purchasing

Management complacency

Payment history

Gift acceptance policies

OH 5-39

When to Buy

Purchase perishable items daily or every few days.

Purchase nonperishable items weekly or monthly.

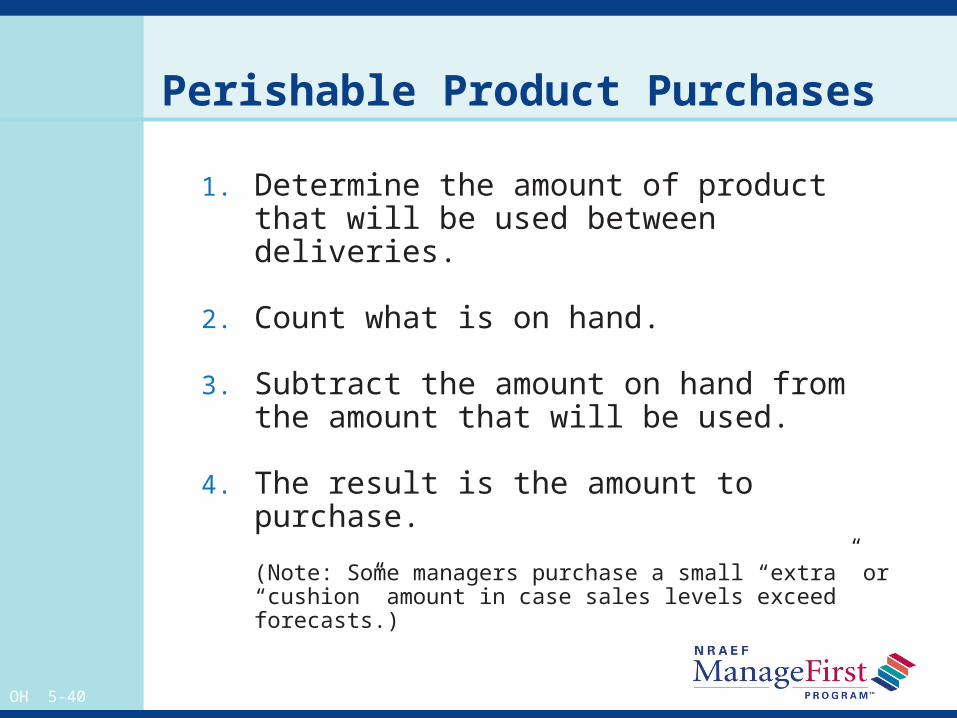

OH 5-40

Perishable Product Purchases

1. Determine the amount of product that will be used between deliveries.

2. Count what is on hand.

3. Subtract the amount on hand from the amount that will be used.

4. The result is the amount to purchase.

(Note: Some managers purchase a small “extra” or “cushion” amount in case sales levels exceed forecasts.)

OH 5-41

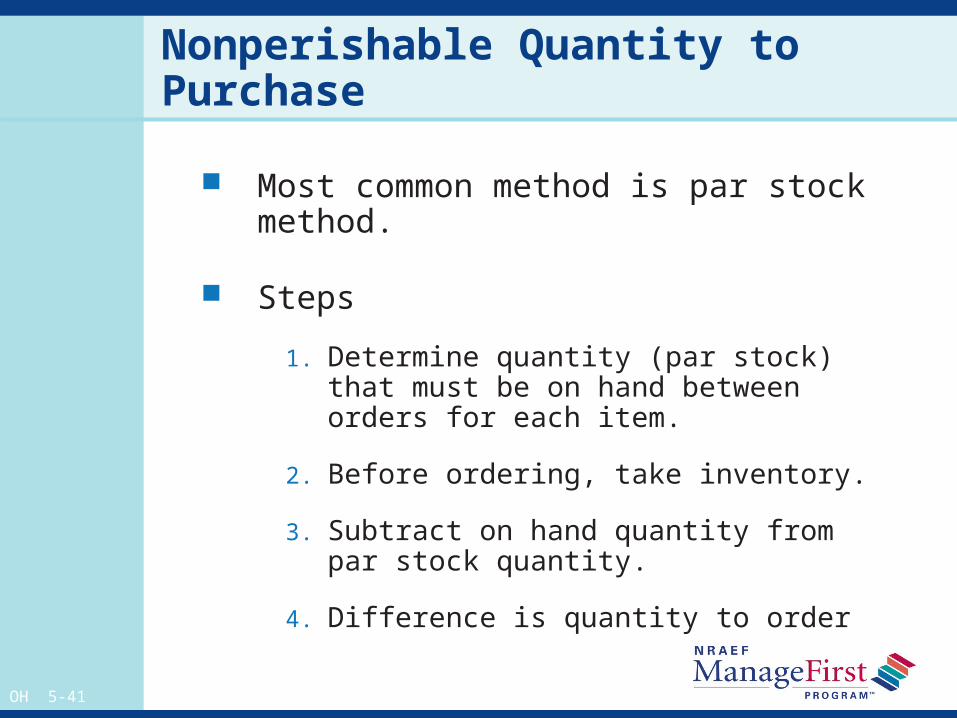

Nonperishable Quantity to Purchase

Most common method is par stock method.

Steps

1. Determine quantity (par stock) that must be on hand between orders for each item.

2. Before ordering, take inventory.

3. Subtract on hand quantity from par stock quantity.

4. Difference is quantity to order

OH 5-42

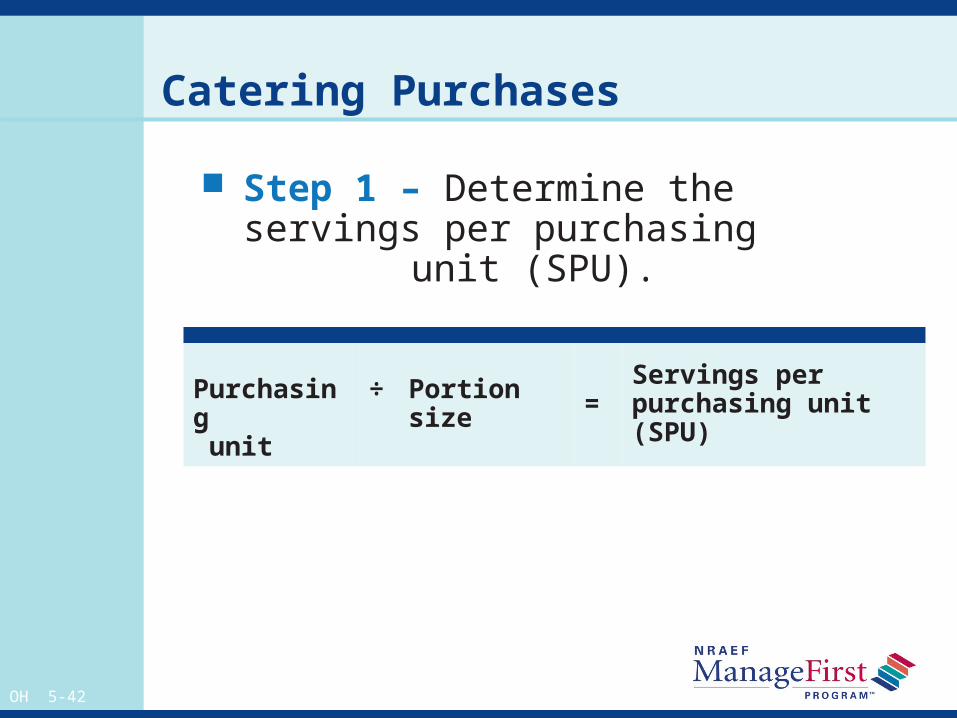

Catering Purchases

Step 1 – Determine the servings per purchasing unit (SPU).

Purchasing

unit

÷ Portion size = Servings per

purchasing unit (SPU)

OH 5-43

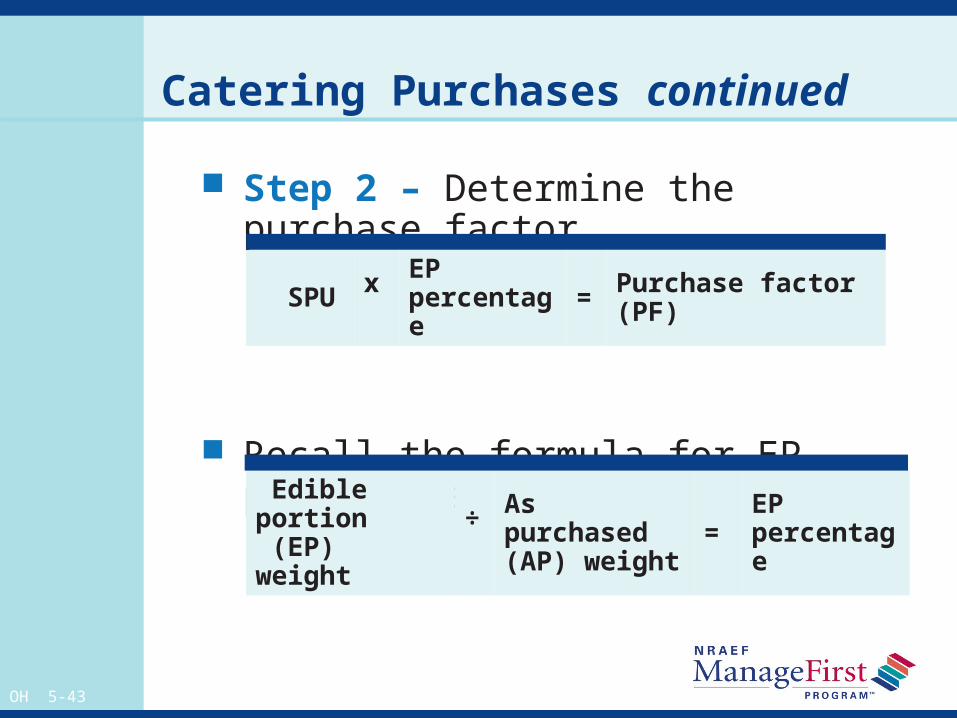

Catering Purchases continued

Step 2 – Determine the purchase factor.

Recall the formula for EP percentage.

SPU x EP percentage = Purchase factor

(PF)

Edible portion (EP) weight

÷

As purchased (AP) weight = EP

percentage

OH 5-44

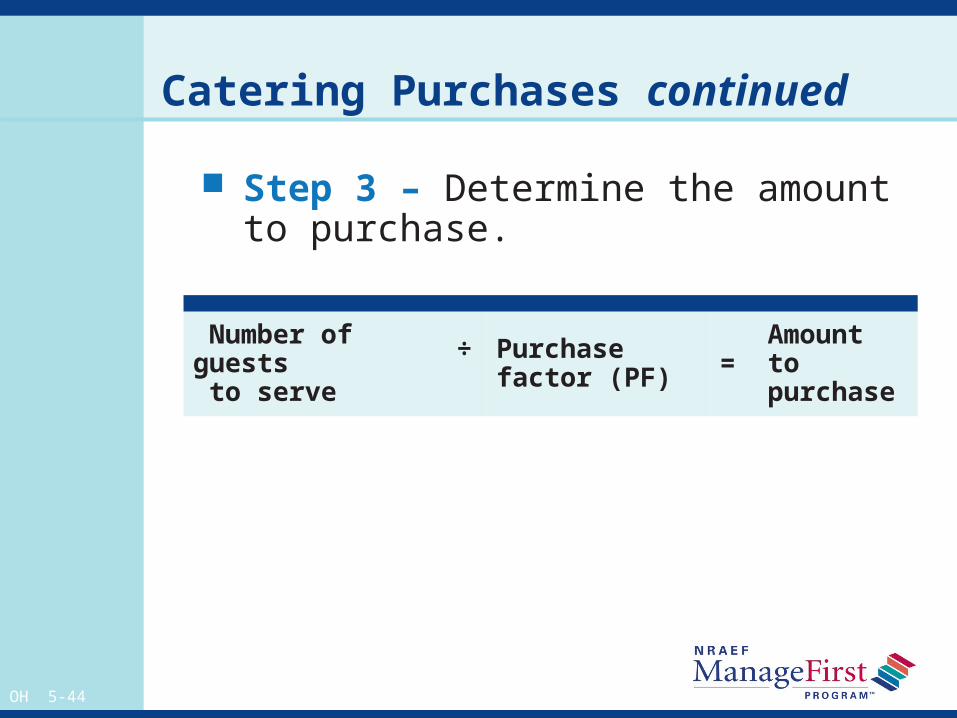

Catering Purchases continued

Step 3 – Determine the amount to purchase.

Number of guests to serve

÷

Purchase factor (PF) = Amount to

purchase

OH 5-45

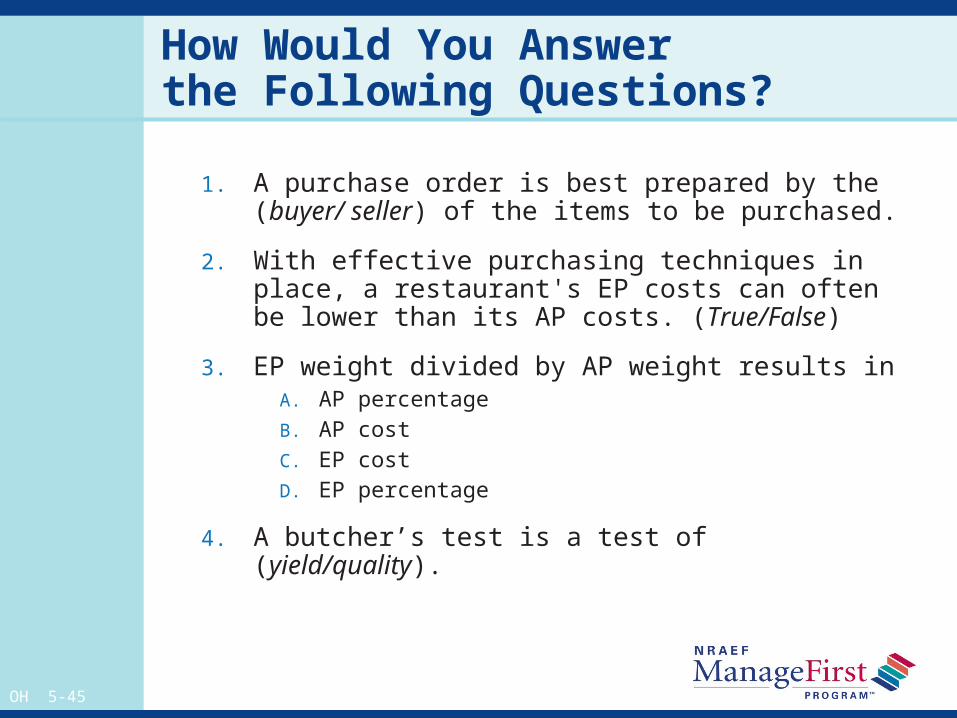

How Would You Answer the Following Questions?

1. A purchase order is best prepared by the (buyer/ seller) of the items to be purchased.

2. With effective purchasing techniques in place, a restaurant's EP costs can often be lower than its AP costs. (True/False)

3. EP weight divided by AP weight results in A. AP percentageB. AP costC. EP costD. EP percentage

4. A butcher’s test is a test of (yield/quality).

OH 5-46

Key Term Review

As served (AS)

Buyer

Commissary

Competitive quotes

Cost plus

Invoice

OH 5-47

Key Term Review continued

Market quotation sheet

Nonperishable goods

One-stop shop

Par stock

Perishable goods

Purchase order

Quotes

OH 5-48

Key Term Review continued

Sealed bid

Specification

Standing order

Yield chart

Yield percentage

Yield test

OH 5-49

Chapter Learning Objectives— What Did You Learn?

Explain how a specification becomes a control in the purchasing function.

Explain the parts of a purchase specification and of a purchase order.

Explain various purchasing methods and their effect on the price of goods.

Calculate a yield test that identifies the difference between AP price and EP cost.

OH 5-50

Chapter Learning Objectives—What Did You Learn? continued

Identify factors that affect the purchase price of goods.

Distinguish between perishable and nonperishable goods and their relationship to the purchasing cycle.

Calculate the par stock amount of an item to order.

Calculate the amount to purchase, using EP amount and yield percent.

OH 5-51

Calculate the amount of goods to purchase for catered events.

Calculate a butcher test, or meat yield test.

Describe the proper procedures for receiving goods.

Chapter Learning Objectives—What Did You Learn? continued