Embed Size (px)

Citation preview

OG

C

1OG

C

BUNKER FUELS

Regulation and practice

David SpringettSGS MARINE SERVICESOctober 2012

© SGS Group Management Ltd. Geneva Switzerland 2012 Not to be reproduced without permission

Overview

Regulatory· ISO 8217 - 2010· ECA’s· Marpol

In real life· In practice· Cost implications

Not to be reproduced without permission 3

Engine manufacturers Shipping companies

Major refinersTesting agencies

ISO 8217

Who has set the Agenda?

Not to be reproduced without permission 4

2010 revision

Current edition ISO 8217 published June 2010

Superseded the third edition published in 2005.

2005 edition itself was a massive change from 1996 due to environmental requirements

2010 standard built on 2005 and addressed some issues.

Not to be reproduced without permission 5

2010 Revision part 2

These standards are always a consensus between various interests.

That consensus has shifted dramatically since 2005

The environmental content aligned with MARPOL VI and this link will remain solid as we move forward.

Standard amended slightly in July 2012 for H2S

Not to be reproduced without permission 6

So where do we stand? – 2010 vs 2005

Adoption of 2010 revision has been very slow Suppliers, are reacting to demand as and

when needed The ISO standard is NOT mandatory, although

Marpol is.· Only as a part of a contract or where locally

legislated Probably about 75-80% of bunker supplied in

2012 are to 2005 standard· Cost premium· Charter parties· Availability – see above

Not to be reproduced without permission 7

10

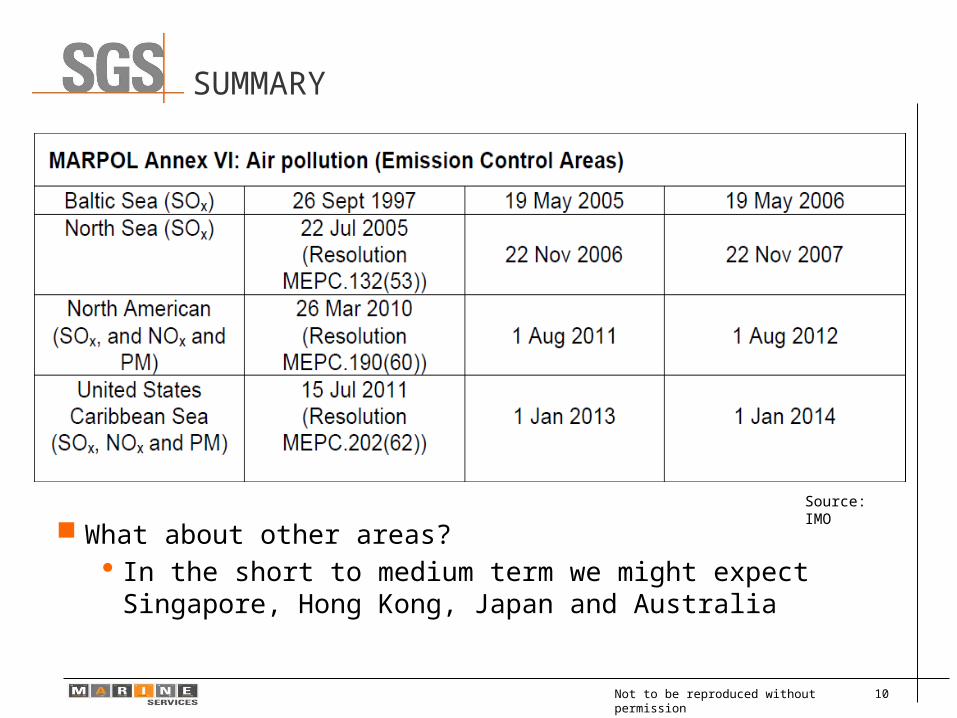

SUMMARY

Not to be reproduced without permission

What about other areas?· In the short to medium term we might expect Singapore,

Hong Kong, Japan and Australia

Source: IMO

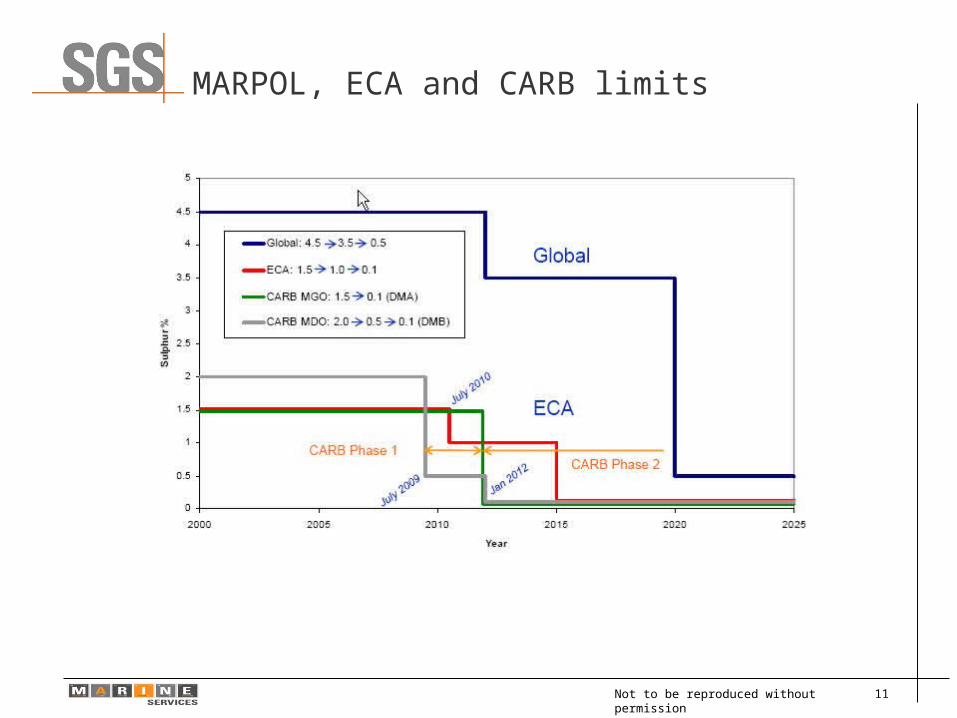

MARPOL, ECA and CARB limits

Not to be reproduced without permission 11

USA/Canada ECA

Source: US EPA

Reductions in 2020320 000 MT NOX = 23%90 000 MT PM = 74%920 000 MT SOX = 86%According to EPA

Cost = $3.2 BillionBenefit = $20 Billion

Not to be reproduced without permission 12

13

Industry Challenges (1)

Increased costs are the biggest challenge of all

Total world bunker market approx 200 million tonnes· Asia approx 70 million tonnes. · USA 25 million tonnes

– Fairly equally divided between USEC,USWC,USGC· ARA 24 million tonnes· Med – 16 million tonnes· Russia 10 million tonnes

If ECA’s are implemented in the regions· As above, estimated between $75 and $200 a tonne extra just to

reach 1% Numerous Quality challenges

Not to be reproduced without permission

Hot Spots

The most common quality challenges can be split into two main categories

Quality itself........· Sulphur· Catfines (Al+Si)· Others, such as viscosity,

density etcBunker with care..........

meeting that quality has a cost

Not to be reproduced without permission 14

15

Meeting Sulphur requirements Main Regional challenges

· UAE - Fujairah· Korea - Busan· USWC – Long Beach· USEC - New York, Miami· USGC – Houston· Italy

Cost estimates for even 1% sulphur are probably between $75 and $200 per tonne – possibly achieved by.........· Naturally low sulphur crudes· Re-direct land based fuel to sea· Re-blending· Desulphurisation

The IMO 2020 regulation for 0.5% would basically require distillates· About 200 million tonnes of it....· And this causes capacity issues

At 4.5% Sulphur was not critical – it is when we get down to 0.5%

Not to be reproduced without permission

16

Aluminium and Silicon (Catfines)

Two Issues· Local refining· Extra risk with lower sulphur

blends – increased use of slurry oils

Main regional challenges· ARA· Houston· USEC

Most engine manufacturers recommend 15ppm Al+Si· A purifier usually removes only

60-70%· Settlement in service tanks can

be an issue

Not to be reproduced without permission

17

Other Issues

Density· Increased use of slurry oil as a

blending component Stability

· Increased use of other resources Chemical Contamination

· Possible sharp practice Ignition quality

· CCAI· · · · Usually between 800 and 880.· Not always a reliable indicator

Not to be reproduced without permission

18

Practical supply issues Utility demand is declining in USA

· Advent of LNG and renewables– LNG raises its own challenges

Residual fuel production declining accordingly Sulphur levels in imported US fuel oil

· Approx 70% over 1%· Canada, Mexico, Russia· Most of the 30% low sulphur oil was from

Algeria/North Africa/ARA Japan - post Fukushima Where does that leave us?

· Pre 2015– Europe ECA experience

· Post 2015?

Not to be reproduced without permission

19

Future solutions?

Fuel is almost 50% of ship operating costs LNG

· Not the answer to all the issues· Short sea trading

– Ferries, Regular trade· Very expensive to fit/retrofit

“Scrubbing” technology· Open and closed systems, various brands – Alfa-laval, Hamworthy,

Wartsila.MAN etc· Verification/ wash water content.........· SCR · Expensive

Low Sulphur fuel· Distillates

Oil, Gas & Chemicals Services

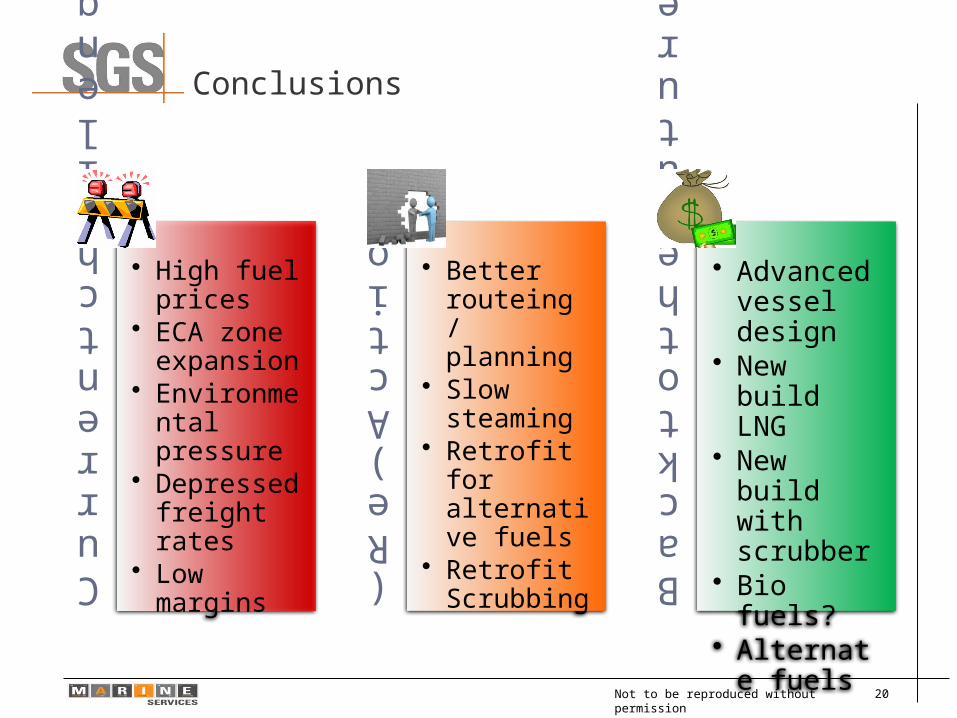

Conclusions

20Not to be reproduced without permission

Current challenges• High fuel

prices• ECA zone

expansion• Environmen

tal pressure• Depressed

freight rates• Low

margins

(Re)Action• Better

routeing / planning

• Slow steaming

• Retrofit for alternative fuels

• Retrofit Scrubbing

Back to the future?• Advanced

vessel design

• New build LNG

• New build with scrubber

• Bio fuels?• Alternate

fuels

SGS Marine Services

A global network – the largest coverageOperating to Industry and SGS internal standards IFIA certified – plus local qualificationsOn going training – experienced personnelSGS Ethics policyMajor client portfolioDedicated teams

21

copyright Portpictures.nl

Not to be reproduced without permission

SGS Marine Services

Quantity Inspections· SGS presence in all major ports with SGS personnel to

IFIA/local standards· Single point contact

Quality testing· Routine analysis – dedicated labs· Dispute analysis – SGS ISO 17025 network· Forensic testing – SGS M-Scan

Lubricating oil testing – SGS VernolabEnvironmental testingSpecialist work – P&I, NDT, HACCP etc

22Not to be reproduced without permission

SGS – your single source for multiple services

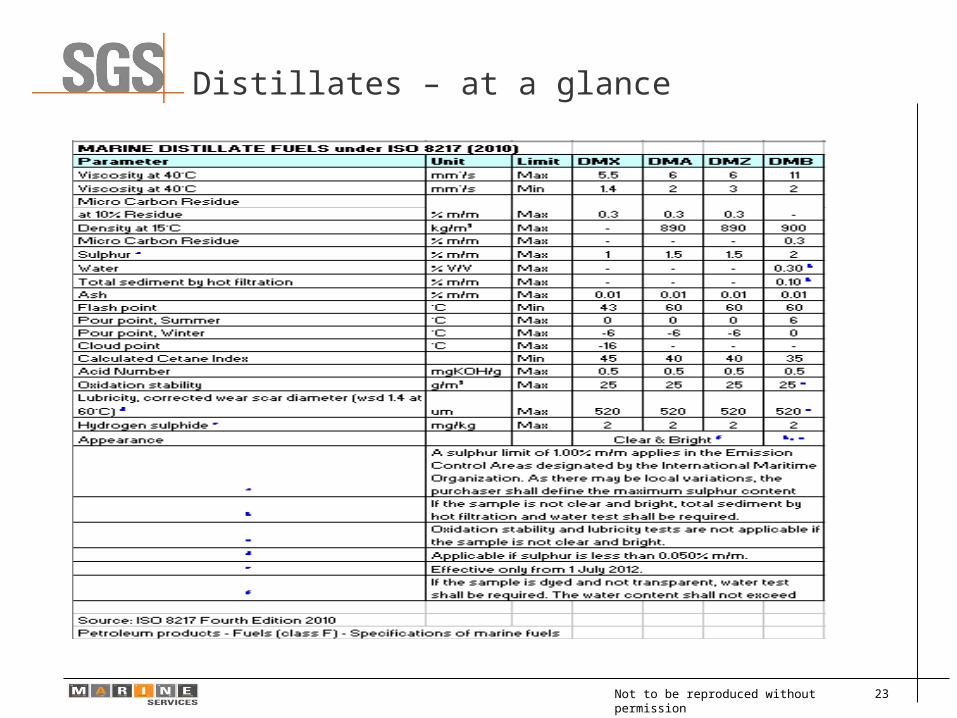

Distillates – at a glance

Not to be reproduced without permission 23

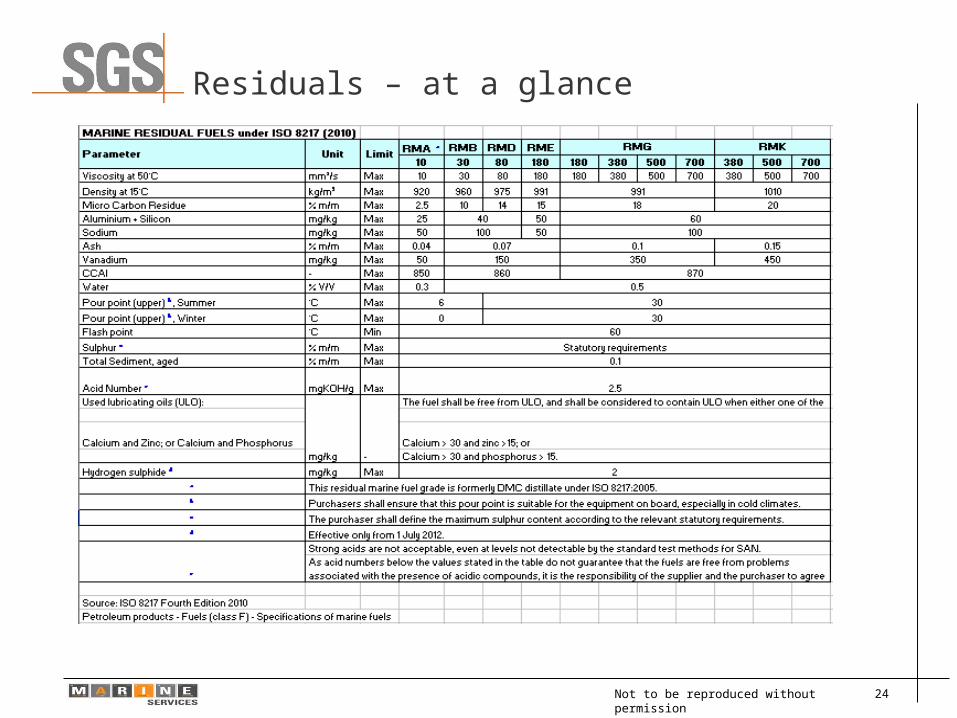

Residuals – at a glance

Not to be reproduced without permission 24

Oil, Gas & Chemicals Services 25

WWW.SGS.COM/OGC

© SG

S SA

201

1. A

LL R

IGHT

S RE

SERV

ED.