Embed Size (px)

Citation preview

Offshore – Wave Energy

EDP Group and Innovation

Agenda

Desenvolvimento Tecnológico

Offshore – Wind Energy

1

Offshore Energy – Final Remarks

USA

Leading energy utility in Portugal and key player in Iberia present in Brazil and growing in wind power in USA and EU

6% of EBITDA in 9M09

Presence in USA since 2007

Wind Power: 2.3 GW

# 3 wind operator (present in 8 states)

1% of EBITDA in 9M09

Presence since 2006 (France)

Wind Power: 0.27 GW

Other EU

Wind Power

15% of EBITDA in 9M09

Desenvolvimento Tecnológico

Brazil

SpainPortugal

Note: Data as of Sep-09

16% of EBITDA in 9M09

Listed subsidiary: Energias do Brasil (EDP has 72%)

Presence in Brazil since 1996

Hydro Power: 1.7 GW

2 electricity distribution concessions

51% of EBITDA in 9M09

Privatization in 1997 (IPO)

Single electricity distributor

Single electr. last resource supplier

Power generation: 9.7 GW

26% of EBITDA in 9M09

Presence in Spain since 2001

Power generation 5.2 GW

# 2 in gas distribution

Electricity distribution (Asturias)

2

15% of EBITDA in 9M09

Listed subsidiary: EDP Renováveis (EDP has 77.5%)

IPO in Jun-08

Wind Power: 4.9 GW

# 4 wind operator worldwide (present in 8 countries)

The global energy outlook is changing…

… making Renewables growth an unstoppable trend…

… in which EDP is uniquely positioned to create value

Global trends continue to support EDP’s clean energy focus

Desenvolvimento Tecnológico3

Global trend supports EDP’s Renewable Strategy

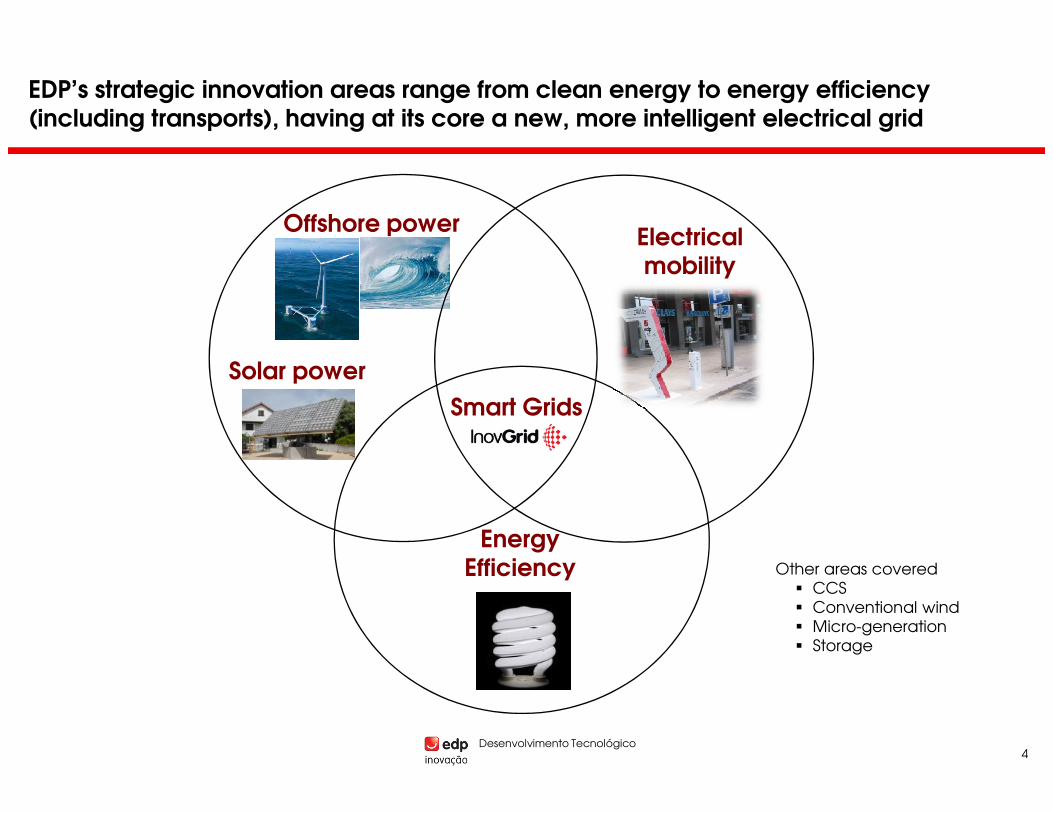

Offshore powerElectricalmobility

Smart Grids

Solar power

EDP’s strategic innovation areas range from clean energy to energy efficiency(including transports), having at its core a new, more intelligent electrical grid

Desenvolvimento Tecnológico

Energy Efficiency

Smart Grids

Other areas covered� CCS� Conventional wind� Micro-generation� Storage

4

Offshore – Wave Energy

EDP Group and Innovation

Agenda

Desenvolvimento Tecnológico

Offshore – Wind Energy

5

Offshore Energy – Final Remarks

Wave energy’s worldwide potential is vast. In particular the west coast of Europe is verysuitable for wave energy development

Resource and Market Potential

Desenvolvimento Tecnológico6

• Worlwide wave resource ranges 2 TW (15% in Europe)

• 200 GW of world installed capacity (feasible) until 2050

Source: DTI, Carbon Trust

Pri

ori

ty z

on

es*

Good sites Government support

250 MW Capacity

•New Decree-Law defining 250 MW to be attributed through 3 phases:

• Demonstration phase (20 MW)

• Pre-Commercial phase (100

1

+

Resource40 kW/m

Electrical

Portuguese case – good natural conditions, logistics and government commitment

Desenvolvimento Tecnológico7

Pri

ori

ty z

on

es*

Best classification

Worst classification

.

.

.

* Wave Energy Center study

3,5 to 4 GW of potential capacity alongside Portuguese coast, to be installed over the years

• Pre-Commercial phase (100 MW)

• Commercial phase (130 MW)15y feed-in tariff

•Feed-in-tariff, currently starting at ~€260 MWh, for 15y

Simple licensing process

•Simple licensing process (envisaged one-stop-shop approach)

2

3

networkalongcoast

GoodLogistics

Source: Wave Energy Centre, LNEG

Shoreline Devices

(Low depth)

Nearshore Devices

(Up to 20m depth)

Technology – proximity to shore / depth segmentation

Desenvolvimento Tecnológico8

Offshore Devices

(About 50m depth for floating devices)

Trends?

• The greatest potential is in offshore applications (more energy per meter, market is huge)

• Even onshore and nearshore devices are seen as development platforms for future offshore applications

Oscillating Water Column (onshore, nearshore or offshore)

Point Absorbers – Floating or submerged, usually hydraulic PTO

Technology – energy conversion principles

Desenvolvimento Tecnológico9

Articulated Overtopping (onshore, nearshore or offshore)

Technology – maturity in >10 years time

Desenvolvimento Tecnológico10

• Energy conversion principle not yet stabilized – There is a large number of

devices based in four or five conversion principles

• First demonstration projects at sea ongoing

How will technology evolve?

• Only one energy conversion principle, like in wind with horizontal axis turbines?

• Two or three conversion principles, segmented by resource characetristics, proximty to coast, etc. ?

10

More than 25 years experience and direct paticipation in several R&D and demonstration projects

Exploration (promotor)

Installation and maintenace

Enginering work focusing on installation

Production of ancillary equipments (e.g., substaions, connections)

System assemblyComponentsdevelopmentand production

Research & Development

Competences in assembly in complex system was already demonstrated in several industries

Experinced Renewable Energy promotors

National industry in metal-mechanics,

Civil engineering companies with

Good network of ports and

Existing know-how in components fabrication for onshore use, provides base for the offshore development, namely in

Value chain

National Competences

Degree

Already existing

Stages adding more valueSignificant opportunity for PT in wave energy technologies and services

Desenvolvimento Tecnológico11

*Final evaluation depends on winning technologiesSource: Mckinsey PCTE study; Interviews with experts

metal-mechanics, hydraulics, power electronics is potentially competitive on international scale

Components developed through scale production*

companies with strong experience in construction of maritime infra-structure and strong knowledge in ocean activities

ports and shipyards, to be leveraged with service providing to these equipments

Lead the world in the development of technologies and services in wave energy conversion

Secure Nacional production of a significant part of the components used in the systems

Become a world refernce in engineering for wave energy installations

namely in applications regarding wave energy

Lead in the development installed capacity of offshore ancillary equipments

Ambition

Development Potential

Stronger Difficulties

Adapt ports and shipyards to service the wave energy projects

Diversify RE portfolio by gradually integrating wave energy projects alongside with mature technologies

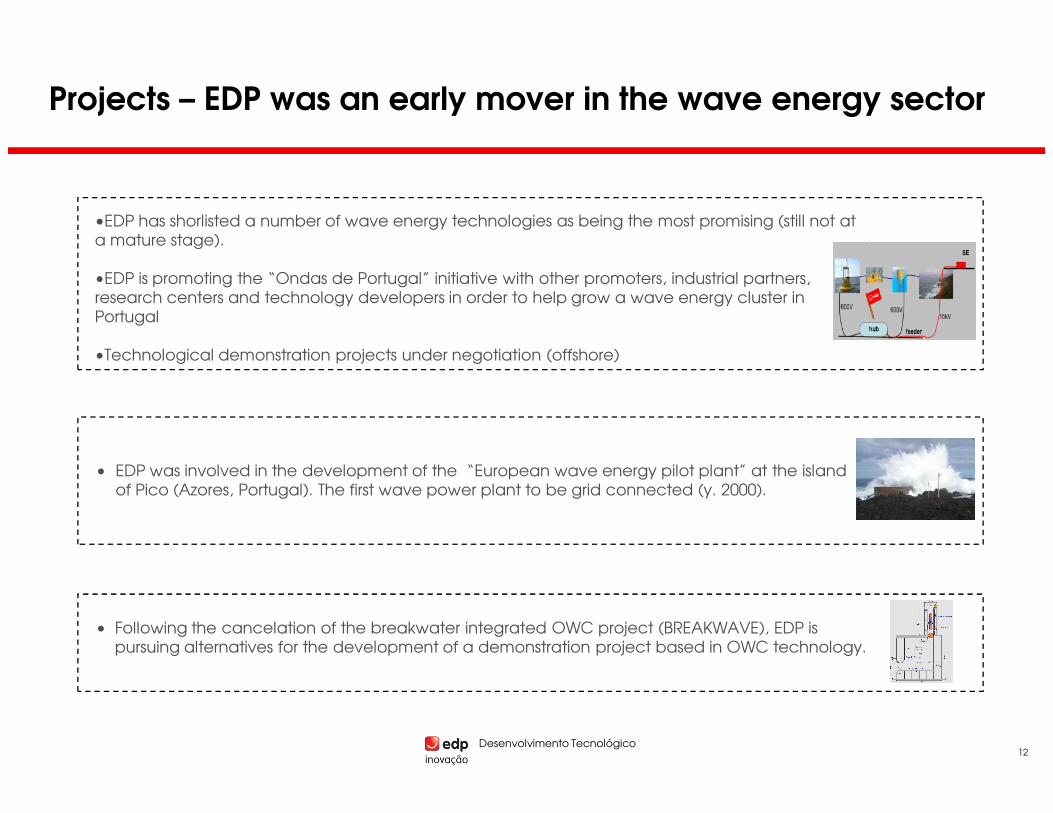

•EDP has shorlisted a number of wave energy technologies as being the most promising (still not at a mature stage).

•EDP is promoting the “Ondas de Portugal” initiative with other promoters, industrial partners, research centers and technology developers in order to help grow a wave energy cluster in Portugal

•Technological demonstration projects under negotiation (offshore)

Projects – EDP was an early mover in the wave energy sector

Desenvolvimento Tecnológico

• EDP was involved in the development of the “European wave energy pilot plant” at the island of Pico (Azores, Portugal). The first wave power plant to be grid connected (y. 2000).

• Following the cancelation of the breakwater integrated OWC project (BREAKWAVE), EDP is pursuing alternatives for the development of a demonstration project based in OWC technology.

12

Enormous potential for value creation

• 3 to 5 GW of primary energy available, feasible 400 MW until 2020 and 1 GW until 2025

• Business in the range of1,5 Bi € in 2025 (80% exports)*

• 7.700 jobs*

• Opportunities in fabrication, engineering and O&M and environmental studies*

Technology uncertainty (it is still not clear what concepts will materialize in real business)

OWC Articulated

Point absorbers Overtopping

Ondas de Portugal, OdP – Open Technology Strategy

Desenvolvimento Tecnológico13

• Leveraging on existing know-how, attracting more kowledge, in a R&D intensive area

Ondas de Portugal, OdP

Main renewable energy promoters and relevant industrial partners, in close relation with the cientific community, together to generate critical mass and share risk in the development of

several promising wave energy and ancillary technologies

* Source: Inteli Study

Project Aguçadoura – First step under OdP scope

What?

• Aquisition of the company “Companhia de Energias Oceânicas (CEO) that owns the following assets:

• Aguçadoura land substation, installation / demonstration licences, offshore equipment

• Securing acquisition rights over the second generation of Pelamis Technology - P2

Who?

• EDP Inovação (52%)

• EFACEC (25%)

• Pelamis Wave Power (23%)

Desenvolvimento Tecnológico14

• Pelamis Wave Power (23%)

Offshore – Wave Energy

EDP Group and Innovation

Agenda

Desenvolvimento Tecnológico

Offshore – Wind Energy

15

Offshore Energy – Final Remarks

Key offshore wind advantages

Why Offshore Wind?

• Higher wind resource and less turbulence

• Large ocean areas available

• Best spots in wind onshore are becoming scarce

• Offshore wind, including deep offshore, has the capacity to deliver high quantities of energy

Desenvolvimento Tecnológico

energy

Why Floating Offshore Wind?

• Limited spots with shallow waters (mostly in the North Sea)

• Most of the resource is in deep waters

• Large ocean areas available

• Less restrictions for offshore deployments and reduced visual impacts

• Huge potential around the world: PT, Spain, UK, France, Norway, Italy, USA, Canada …

16

Resource and Market Potential

EU15 Potential• Good offshore wind resource (load factor > 3.000h)

• Offshore wind potential is mostly in transitional and deep waters(1) (~65 %)

• Energy Potential >700 TWh (~220 GW)

• Ports and docks available along European coast

Depth (m) 0 - 30 40 – 200 +

Offshore potential EU15

77 GW >140 GW

Mean Wind speed (50m)

(1)Analysis limited to 100m water depths

Source: Greenpeace & Garrad Hassan 2004; IEA; Global insight;

Desenvolvimento TecnológicoSource: DTI

0 105 km

Portuguese & Spanish Potential• Continental shelf ends near the coast

• Grid connection available near the coast

• Limited Potential for water depths < 40m

• 250 km of PT Costal Line suitable to be explored

• Energy Potential in PT >40 TWh (~12 GW)

• Energy Potential in SP >290 TWh (~98 GW)

European Bathymetry

Depth (m) 0 - 30 40 – 200 +

Offshore potential

PT 2 GW >10 GW

SP 18 GW >80 GW

Source: Univ.de Zaragoza – Evaluación Potencial Energías Renovables (2007)

Source: Greenpeace & Garrad Hassan 2004; IEA; Global insight;

17

Resource / Market Potential – Portugal

• Onshore wind energy limited to ~12 TWh

• Wind energy penetration will reduce to 17% by 2020(1)

- If new renewable energies are not introduced to energy mix production

• The deployment of commercial Offshore Wind farms in transitional waters (>40m, <

Desenvolvimento Tecnológico

Source: INETI

(1)Considering a grow rate of ~3% in energy consumption

Wind farms in transitional waters (>40m, < 60m) will:

• Enable Portugal to keep the leading position in renewable energy

• Maintain the wind energy penetration of 20% by 2020 and 2030

• If floating offshore wind is deployed the wind energy penetration will increase significantly

18

• Onshore wind energy limited to ~12 TWh

• Wind energy penetration will reduce to 17% by 2020(1)

- If new renewable energies are not introduced to energy mix production

• The deployment of commercial Offshore Wind farms in transitional waters (>40m, <

Resource / Market Potential – Portugal

Desenvolvimento Tecnológico

Source: INETI

Wind farms in transitional waters (>40m, < 60m) will:

• Enable Portugal to keep the leading position in renewable energy

• Maintain the wind energy penetration of 20% by 2020 and 2030

• If floating offshore wind is deployed the wind energy penetration will increase significantly

(1)Considering a grow rate of ~3% in energy consumption

19

Technology

Co

st

Floating

Jackets

MonoPiles

Monopiles• Basic extension of turbine

tower w/ transition piece

• Economically feasible in shallow water depths (10-30m)

Jackets• Economically feasible in

transitional water depths (30-50m)

Desenvolvimento Tecnológico

Water DepthSource: NREL

50m)

• Derivatives from Oil & Gas technology

• Beatrice successfully deployed (2 jackets x RePower 5M)

Floating• Economically feasible in

deep water (50-900m)

• Two prototypes have been deployed (Hywind and Blue H)

20

Technology – several projects with 1 common conversion principle

Floating offshore wind timeline

2007

• Statoil Hydro and Siemens sign agreement for Hywind project

• Sway raises €16.5M in private placement

Trade name WindFloat Hywind Blue H Sway

DeveloperPrinciple Power

(US)Statoil Hydro (NO) Blue H (NL)

Norwegian consortium (NO)

Foundation typeSemi-submersible (moored 4-6 lines)

Spar (moored 3 lines)

Tension Leg Platform

Hybrid Spar/TLP (single tendon)

Water Depths > 40 m >100 m > 40 m 100 m - 400 m

Desenvolvimento Tecnológico

private placement

2008

• Blue H half-scale prototype installation

• EDP and Principle Power partner to deploy WindFloat technology

2009

• Hywind full-scale prototype installation with 2.3MW turbine

Water Depths > 40 m >100 m > 40 m 100 m - 400 m

Turbine3-10MW

Existing technology!2.3 MW Siemens

2 bladed “Omega” under development

Multibrid Downwind under development

InstallationTow out fully commissioned

Dedicated vessel-tow out and upending

Tow out on buoyancy modules until connection

Dedicated vessel-tow out and upending

Turbine installation

Onshore Offshore Onshore Offshore

StrengthsDynamic motions, installation, overall simplicity of design

Existing turbine and hull technology,

well funded

First sub-scale demo deployed

Low steel weight

Challenges Steel costDynamic motions,

installation

Mooring cost, turbine design, turbine coupling with tendons

Installation and maintenance,

downwind 3-blade turbine

Stage of Development

Ready for prototype testing

Full-scale prototype installed in 2009

Half-scale prototype installed in 2008

Development of the concept

21

Experinced Renewable Energy promotors

Stages adding more value

Exploration (promotor)

Installation and maintenace

Enginering work focusing on installation

Production of ancillary equipments (e.g., substaions, connections)

Components development and fabrication

TowerNational

Competences Degree

Turbine Transitional depth(30-50m)

Deep waters (>50m)

Support structures

Already existing

Presence of National tower producers Existing know-

how in components fabrication for onshore use,

Value chain

Significant opportunity for PT in offshore wind support structures

Desenvolvimento Tecnológico

Technologies based in civil engineering achievable given Portuguese background

National experience only focusing site assembly

Good network of ports and shipyards, to be leveraged with service providing to these equipments

Civil engineering companies with strong experience in construction of maritime infra-structure

Attract to Portugal activities in the areas of research, development and demonstration in key offshore areas such as offshore turbines and support structures

Ambition

Become world experts in engineering for offshore energy installations

Development Potential

Stronger Difficulties

Technology transfer from O&G sector.Incentive would stimulate O&G companies interests to pursue RE tech.

onshore use, provides base for the offshore development

Lead in installed capacity of offshore ancillary equipments

Adapt ports and shipyards to service the offshore energy projects

Diversify RE portfolio by gradually integrating offshore energy projects alongside with mature technologies

22

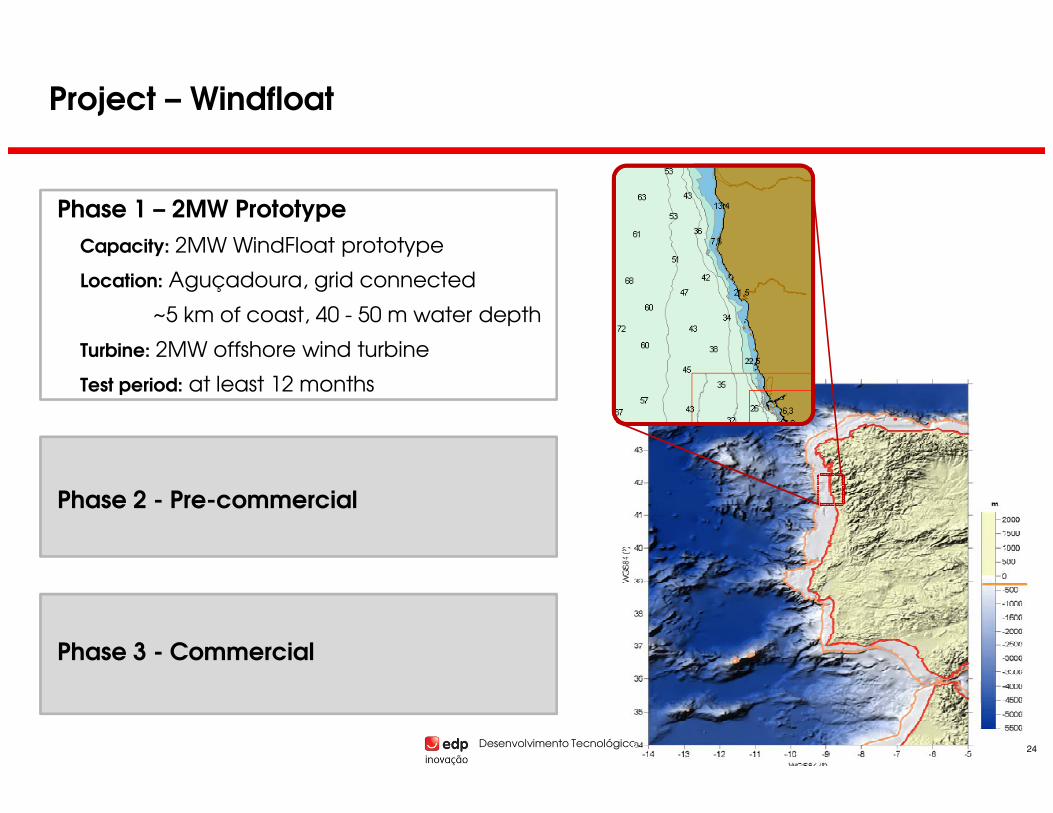

Project – Windfloat

Turbine Agnostic• Conventional (3-blade, upwind)

• No major redesign

- Control system – software

- Tower – structural interface

High Stability Performance• Static Stability - Water Ballast

- ≈ ½ of hull displacement

• Dynamic Stability - Heave Plates

Desenvolvimento Tecnológico

• Dynamic Stability - Heave Plates

- Move platform natural response above the wave excitation (entrained water)

- Viscous damping reduces platform motions

• Efficiency – Closed-loop Active Ballast System

Depth Flexibility (>40m)

Assembly & Installation

• Port assembly

• No specialized vessels required, conventional tugs

• Industry standard mooring equipment

23

Project – Windfloat

Phase 1 – 2MW Prototype

Capacity: 2MW WindFloat prototype

Location: Aguçadoura, grid connected

~5 km of coast, 40 - 50 m water depth

Turbine: 2MW offshore wind turbine

Test period: at least 12 months

Desenvolvimento Tecnológico

Phase 2 - Pre-commercial

Phase 3 - Commercial

24

Offshore – Wave Energy

EDP Group and Innovation

Agenda

Desenvolvimento Tecnológico

Offshore – Wind Energy

25

Offshore Energy – Final Remarks

Type Commercial/mature Pre-commercial Demonstration Phase

•Conventional Hydro

•Mini-Hydro

•Onshore Wind •Offshore Wind

•Micro-Wind

•Offshore wind (floating)

•Solar PV – Cristalinesilicon

•Concentrated Solar Power

•Solar PV- Thin films•Solar PV – Nano thin films•Solar PV Concentratted

Wind

Solar

Hydro

Technology – Deep offshore wind likely to develop first

Desenvolvimento Tecnológico26

silicon•Solar PV- Thin films •Solar PV Concentratted

•Biomass/waste combustion

•Biomass cofiring

•Biogas

•Tidal

•Wave

•Ocean biomass•Salinity gradient•Ocean thermal

•Conventional geothermal•Enhanced

geothermal

Solar

Bio

Ocean

Geothermal

Technology Development Gap

Visibility over final technological

solution

Waves

•Conversion principle not yet stabilized

Deep Offshore WindMain

differences

•Conversion principle stabilized•Technology challenges:

•Wind turbine and maritime environment•Adapt wind turbine to platform motion (pitch)•O&M operations

•Cost challenge: Low cost O&G structure

Technology – Deep offshore wind likely to develop first

Desenvolvimento Tecnológico27

Time to market(expected)

Initiatives in place

•>10 years

•Severeal tens of initiatives in place with different kinds of maturities•Typical technology developer is a startup company with limited access to funding (some exceptions)

•Cost challenge: Low cost O&G structure

•5 to 10 years

•Less than 10 initiatives in place, tipically associated with credible players(StatoilHydro, Siemens, new trubine manufacturers, etc.).•There are also exceptions

Technology

•Onshore wind with high growth rate

•Offshore wind in shallow Tec

hn

olo

gy

D

ev

elo

pm

en

t

•Onshore wind continues with high growth rate

•Shallow Offshore wind increases significantly its growth rate

•Deep offshore wind with first commercial deployments

•Onshore wind reaches the limit of its potential.

•Shallow Offshore wind reduces its growth rate

•Deep offshore wind with high growth rate

•Wave energy with first commercial deployments

Different maturities between wind and wave technology suggest the following commercialization path:

1) onshore wind 2)offshore wind 3) deep offshore wind 4) waves

M1 – Milestones

Short/Medium Term

•Solve issues in offshore wind

•First successful demonstration projects and technology cost reduction in deep offshore wind

• Wave conversion principles stabilized

M1

M2

Desenvolvimento Tecnológico

Focus: Efficiency

Focus: Efficacy

•Offshore wind in shallow waters in expansion

•Deep offshore wind in demonstration stage

•Wave energy finalysing R&D and starting demo. Phase (redesigning after 1st sea test)

De

ve

lop

me

nt

Short Term Medium Term Long Term

•Wave energy focusing on demonstration in real sea conditions

Deep offshore has the highest growth capacity in medium term. Long term potential for wave is huge.

M2 – Milestones

Medium/Long Term

•Technology consolidationand cost reduction in deepoffshore wind

•Succes in wave energydemonstration projects andprospects for cost reduction

28

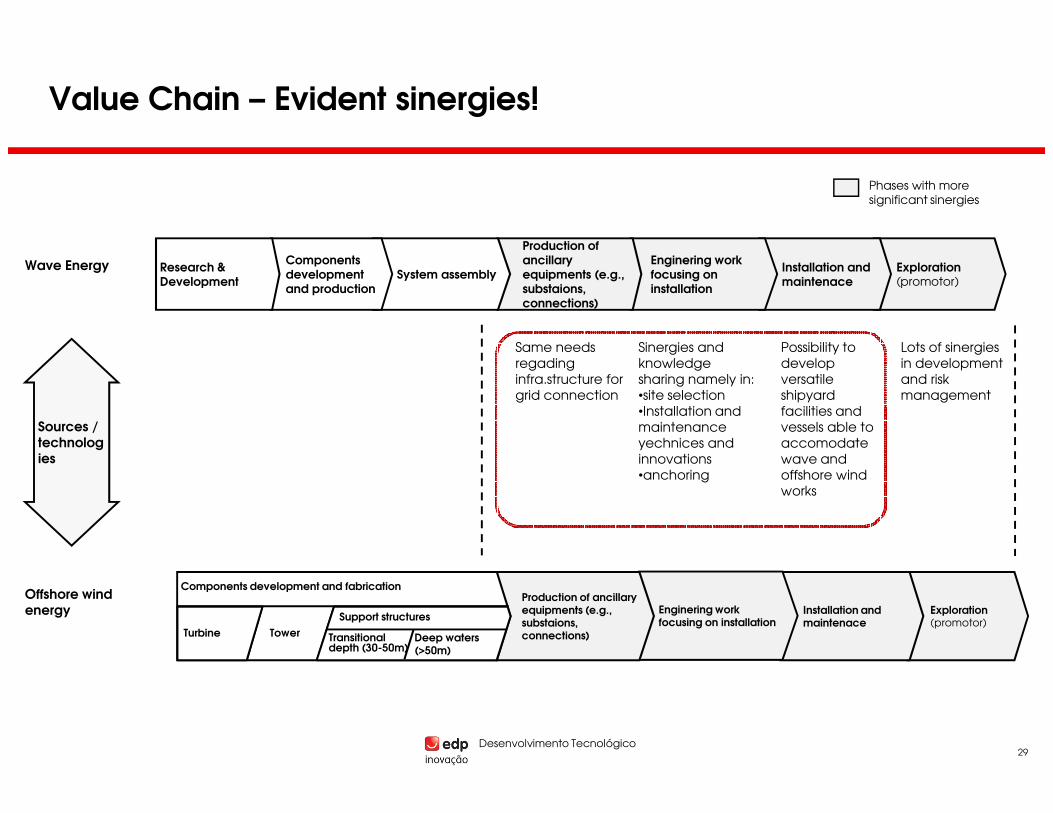

Phases with more significant sinergies

Wave Energy

Same needs regading infra.structure for grid connection

Lots of sinergies in development and risk management

Sinergies and knowledge sharing namely in:•site selection•Installation and

Possibility to develop versatile shipyard facilities and

Exploration (promotor)

Installation and maintenace

Enginering work focusing on installation

Production of ancillary equipments (e.g., substaions, connections)

System assemblyComponents development and production

Research & Development

Value Chain – Evident sinergies!

Desenvolvimento Tecnológico29

Sources / technologies

Offshore wind energy

•Installation and maintenance yechnices and innovations•anchoring

facilities and vessels able to accomodate wave and offshore wind works

Exploration (promotor)

Installation and maintenace

Enginering work focusing on installation

Production of ancillary equipments (e.g., substaions, connections)

Components development and fabrication

TowerTurbine Transitional depth (30-50m)

Deep waters (>50m)

Support structures

Project – Instituto de Energias Offshore

What?

Creation of a knowledge and operational support centre for offshore energy projects (waveenergy and offshore wind :

• Applied R&D and technology observatory in the offshore area

• Numerical and laboratory support to technology developers

• Operational support in tank and sea testing

• Support to industrialization

Who?

• EDP

• Efacec

• Martifer

• Galp

Desenvolvimento Tecnológico30

• Galp

• WavEC, U. Aveiro

•EDP believes that Offshore Wind and Wave Energy, together with otheremerging renewables, will be one of the most important growth vectors for the company in the future

•Offshore wind is closer to be a reality, but wave energy also has long termpotential

Conclusions

Desenvolvimento Tecnológico31

•Wave Energy already has a support scheme in place (although needs some clarification). Offshore wind needs to have a regulatory framework in place

• There are evident sinergies in offshore energy: offshore wind and waveshould be tackled together, namely with initiatives like IEO and commondemonstration sites

•Offshore energy (waves + wind) may still not play a decisive role in 2020 targets, but constitutes a significant opportunity for Portugal in the future, namely in technology development.