Embed Size (px)

Citation preview

CEC Committee January 13, 2015

Department of Administration

Office

of

Group Insurance

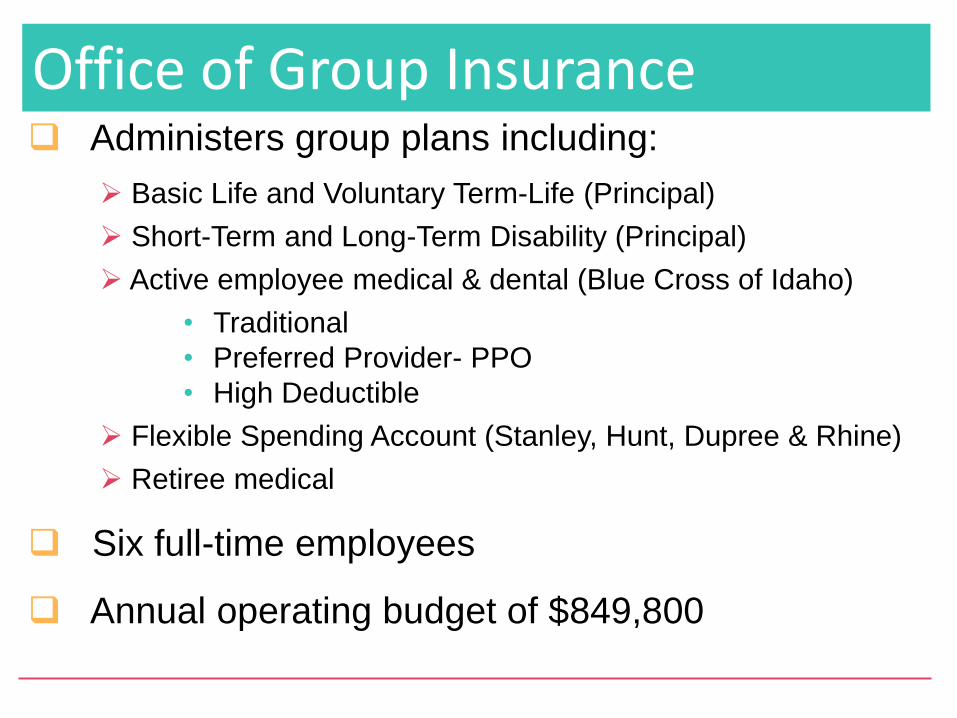

Office of Group Insurance Administers group plans including:

Basic Life and Voluntary Term-Life (Principal)

Short-Term and Long-Term Disability (Principal)

Active employee medical & dental (Blue Cross of Idaho)

• Traditional

• Preferred Provider- PPO

• High Deductible

Flexible Spending Account (Stanley, Hunt, Dupree & Rhine)

Retiree medical

Six full-time employees

Annual operating budget of $849,800

Agenda

• Plan Structure

• Grandfathered Status

• OGI Funding / ACA Impacts

• Reserves

• Talking Points

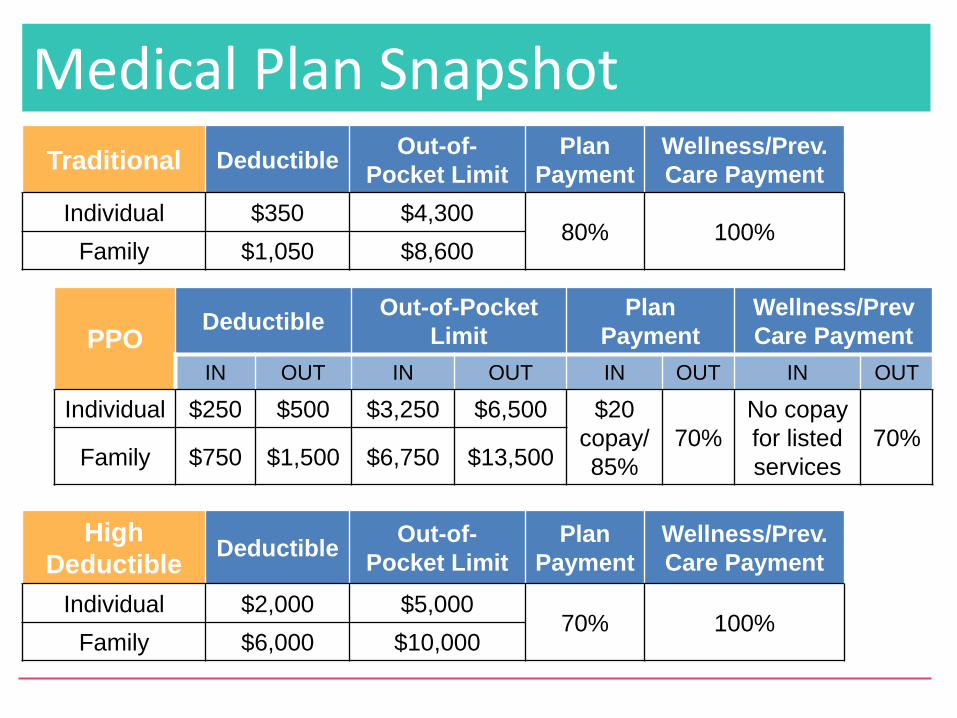

Medical Plan Snapshot

Traditional Deductible Out-of-

Pocket Limit

Plan

Payment

Wellness/Prev.

Care Payment

Individual $350 $4,300 80% 100%

Family $1,050 $8,600

PPO Deductible

Out-of-Pocket

Limit

Plan

Payment

Wellness/Prev

Care Payment

IN OUT IN OUT IN OUT IN OUT

Individual $250 $500 $3,250 $6,500 $20

copay/

85%

70%

No copay

for listed

services

70% Family $750 $1,500 $6,750 $13,500

High

Deductible Deductible

Out-of-

Pocket Limit

Plan

Payment

Wellness/Prev.

Care Payment

Individual $2,000 $5,000 70% 100%

Family $6,000 $10,000

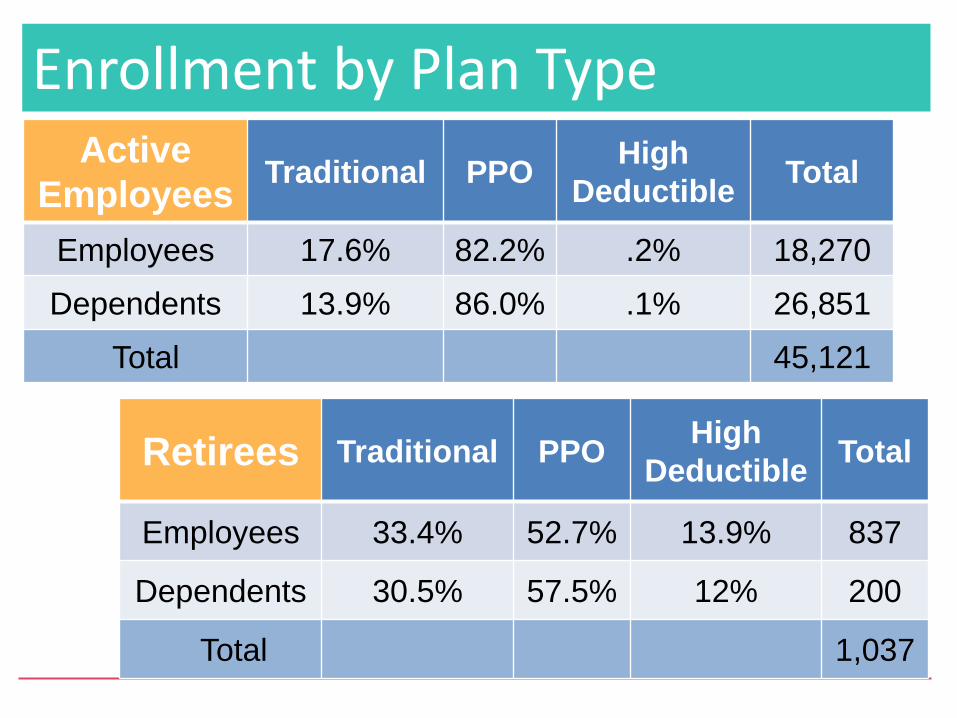

Enrollment by Plan Type Active

Employees Traditional PPO

High

Deductible Total

Employees 17.6% 82.2% .2% 18,270

Dependents 13.9% 86.0% .1% 26,851

Total 45,121

Retirees Traditional PPO High

Deductible Total

Employees 33.4% 52.7% 13.9% 837

Dependents 30.5% 57.5% 12% 200

Total 1,037

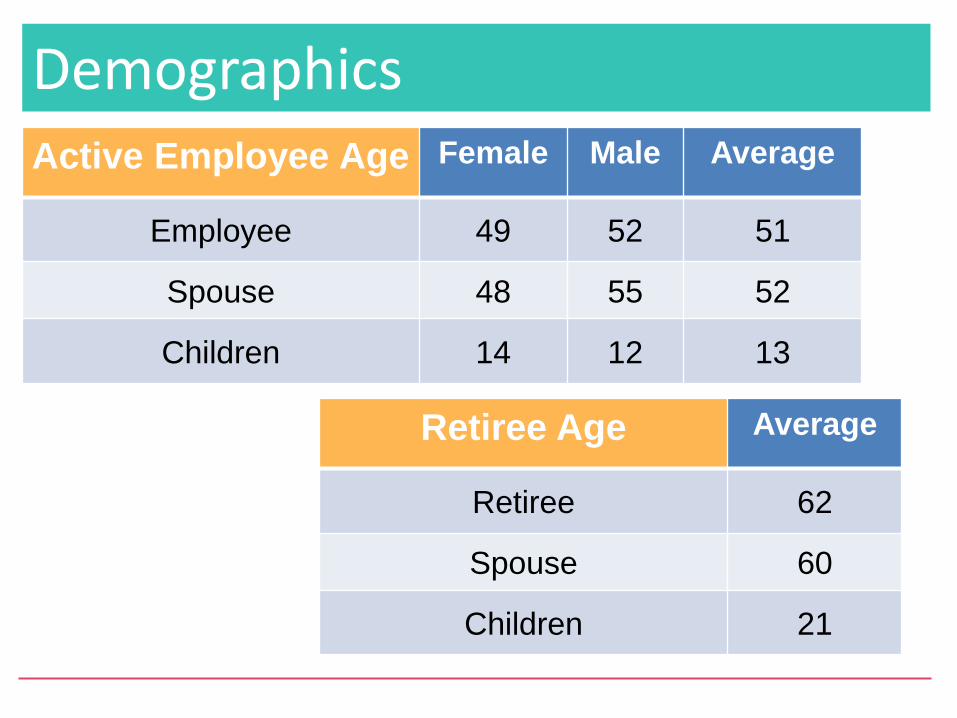

Demographics Active Employee Age Female Male Average

Employee 49 52 51

Spouse 48 55 52

Children 14 12 13

Retiree Age Average

Retiree 62

Spouse 60

Children 21

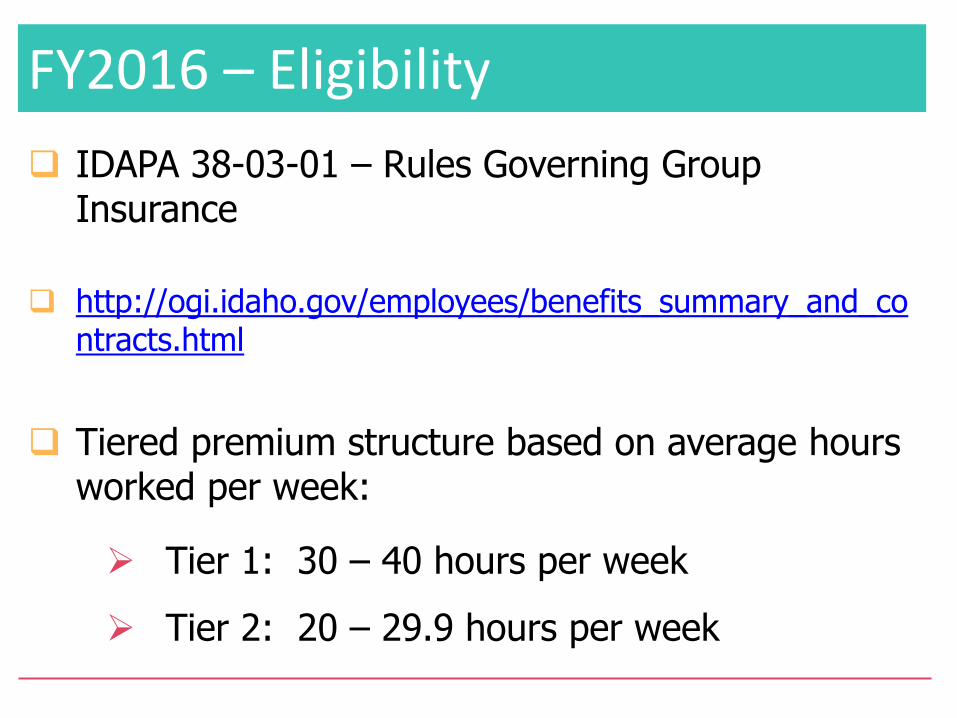

FY2016 – Eligibility

IDAPA 38-03-01 – Rules Governing Group Insurance

http://ogi.idaho.gov/employees/benefits_summary_and_co

ntracts.html

Tiered premium structure based on average hours worked per week:

Tier 1: 30 – 40 hours per week

Tier 2: 20 – 29.9 hours per week

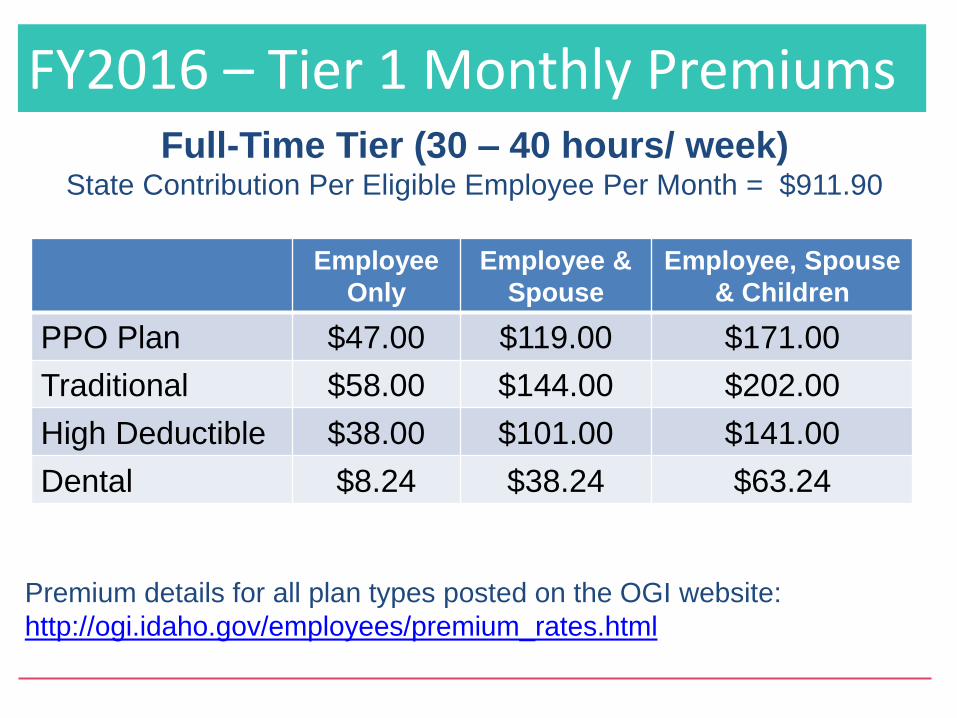

FY2016 – Tier 1 Monthly Premiums Full-Time Tier (30 – 40 hours/ week)

State Contribution Per Eligible Employee Per Month = $911.90

Employee

Only

Employee &

Spouse

Employee, Spouse

& Children

PPO Plan $47.00 $119.00 $171.00

Traditional $58.00 $144.00 $202.00

High Deductible $38.00 $101.00 $141.00

Dental $8.24 $38.24 $63.24

Premium details for all plan types posted on the OGI website:

http://ogi.idaho.gov/employees/premium_rates.html

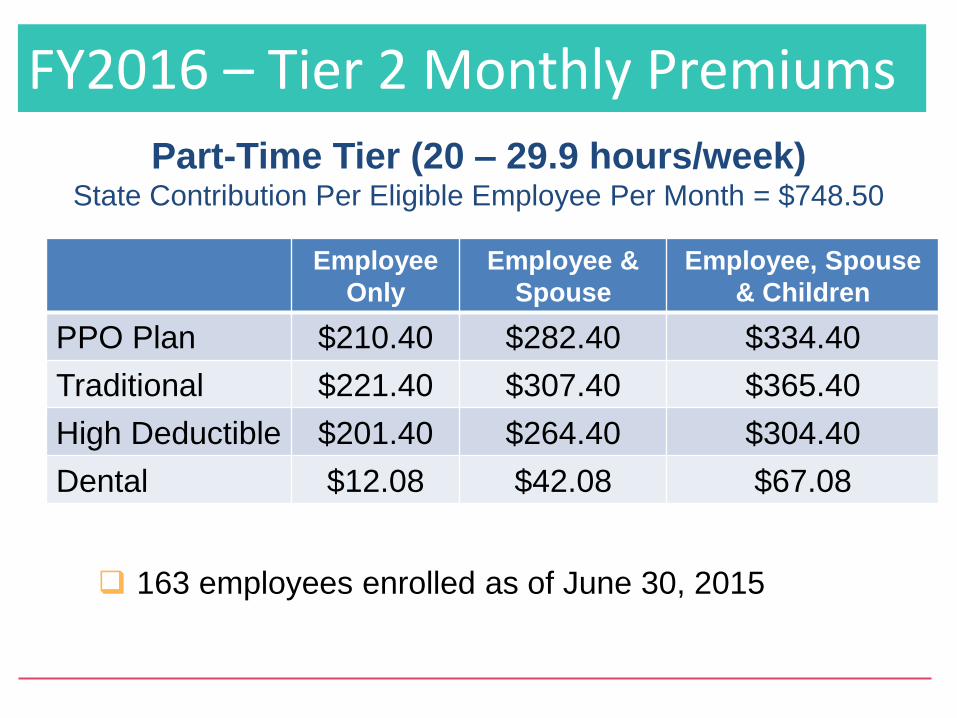

FY2016 – Tier 2 Monthly Premiums

Part-Time Tier (20 – 29.9 hours/week) State Contribution Per Eligible Employee Per Month = $748.50

Employee

Only

Employee &

Spouse

Employee, Spouse

& Children

PPO Plan $210.40 $282.40 $334.40

Traditional $221.40 $307.40 $365.40

High Deductible $201.40 $264.40 $304.40

Dental $12.08 $42.08 $67.08

163 employees enrolled as of June 30, 2015

Agenda

• Plan Structure

• Grandfathered Status

• OGI Funding / ACA Impacts

• Reserves

• Talking Points

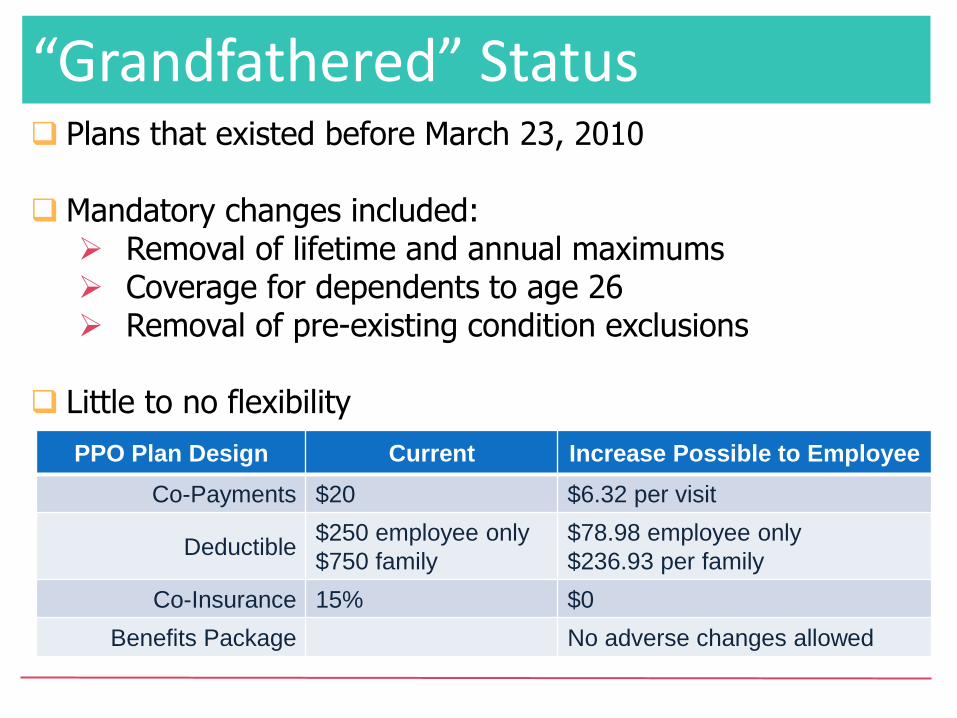

“Grandfathered” Status Plans that existed before March 23, 2010 Mandatory changes included:

Removal of lifetime and annual maximums Coverage for dependents to age 26 Removal of pre-existing condition exclusions

Little to no flexibility

PPO Plan Design Current Increase Possible to Employee

Co-Payments $20 $6.32 per visit

Deductible $250 employee only

$750 family

$78.98 employee only

$236.93 per family

Co-Insurance 15% $0

Benefits Package No adverse changes allowed

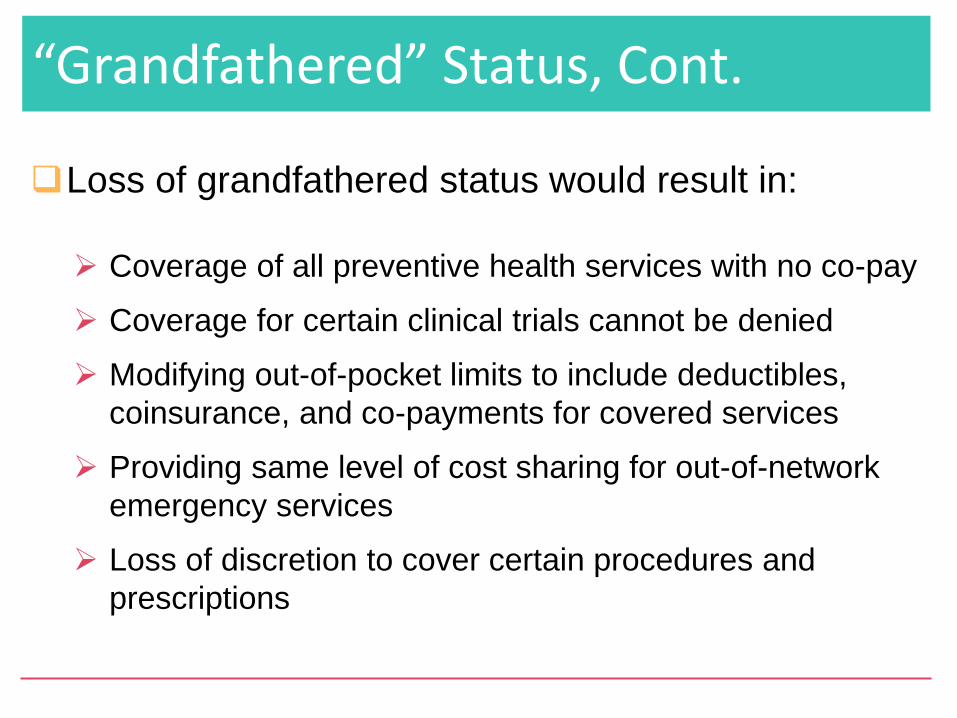

“Grandfathered” Status, Cont.

Loss of grandfathered status would result in:

Coverage of all preventive health services with no co-pay

Coverage for certain clinical trials cannot be denied

Modifying out-of-pocket limits to include deductibles,

coinsurance, and co-payments for covered services

Providing same level of cost sharing for out-of-network

emergency services

Loss of discretion to cover certain procedures and

prescriptions

Agenda

• Plan Structure

• Grandfathered Status

• OGI Funding / ACA Impacts

• Reserves

• Talking Points

OGI Funding

Fully insured plan that functions much like a self-insured plan

Maintain contractual (contingency) reserves

Costs are projected 12 months in advance and refined prior to each budget setting.

Actuarial projections (June and December)

Total Plan Costs vs. Contributions

239,990,000 262,600,000

288,160,000 305,410,000

-

100,000,000

200,000,000

300,000,000

400,000,000

Other

EmployeeContributions

ACA Fees

StateContributions

Total PlanCosts

9.73% 6%

9.42%

* Total Plan Costs include premiums, co-pays and deductibles

* Other includes retiree and cobra contributions

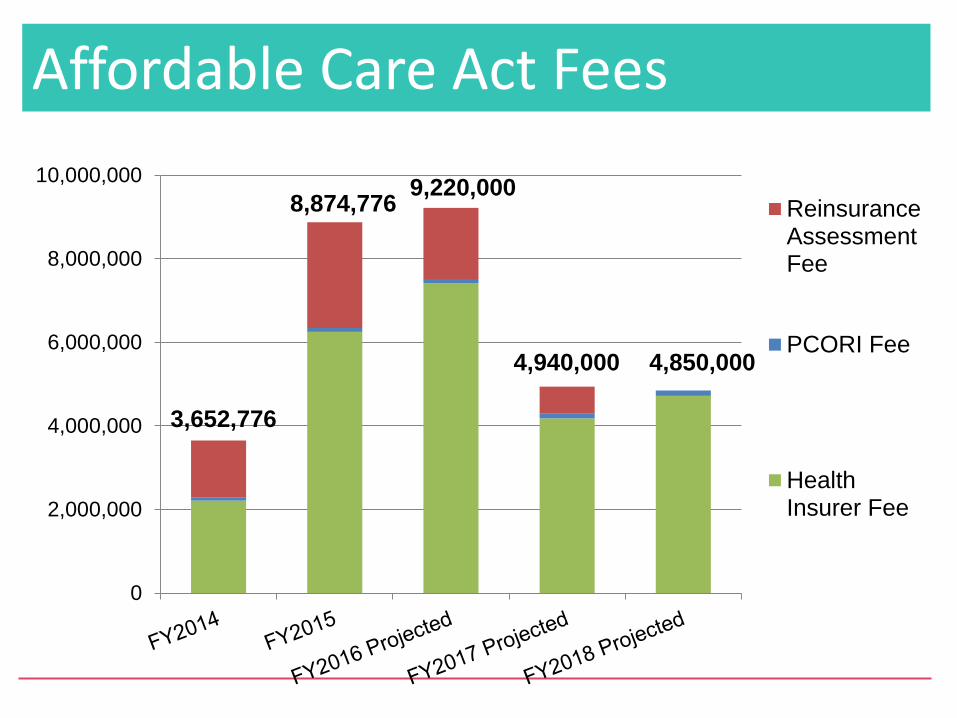

Affordable Care Act Fees

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

ReinsuranceAssessmentFee

PCORI Fee

HealthInsurer Fee

4,850,000 4,940,000

9,220,000 8,874,776

3,652,776

Agenda

• Plan Structure

• Grandfathered Status

• OGI Funding / ACA Impacts

• Reserves

• Talking Points

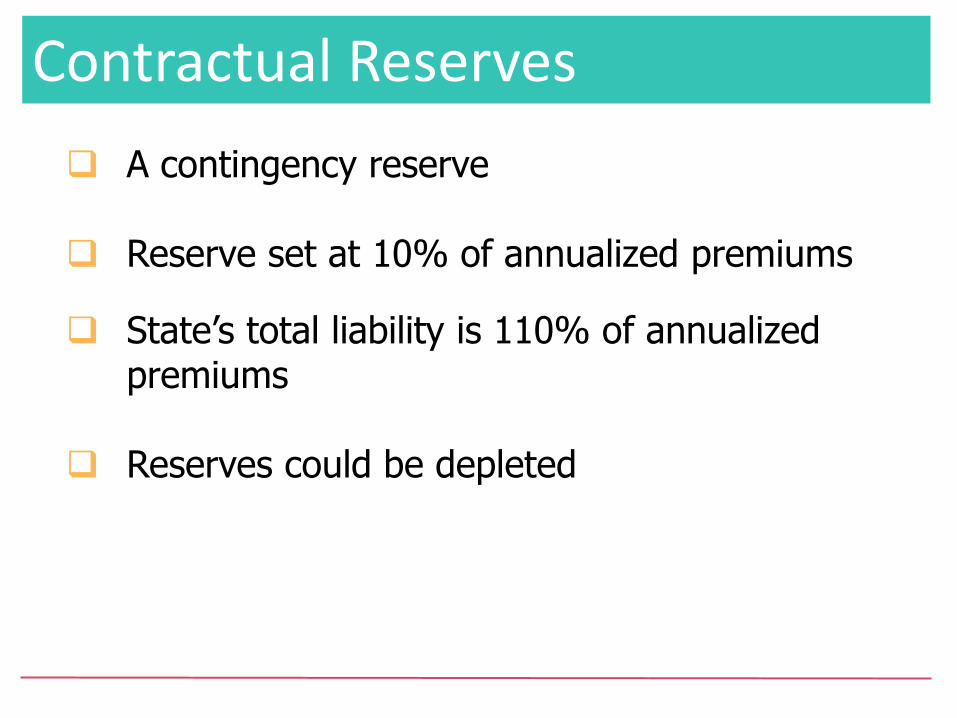

Contractual Reserves

A contingency reserve

Reserve set at 10% of annualized premiums

State’s total liability is 110% of annualized premiums

Reserves could be depleted

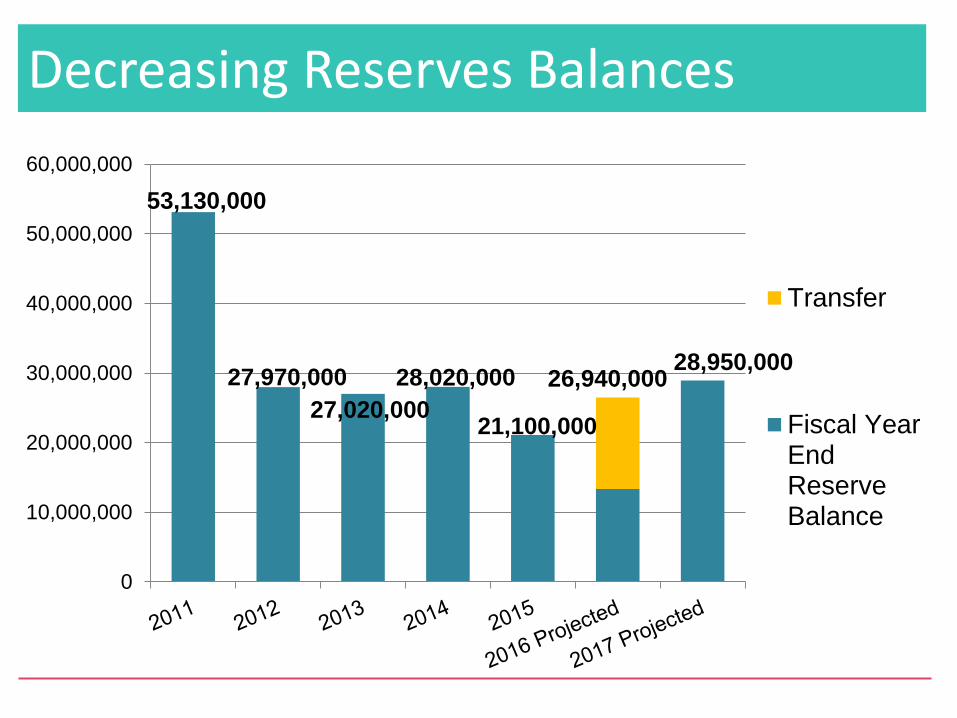

Decreasing Reserves Balances

53,130,000

27,970,000

27,020,000

28,020,000

21,100,000

26,940,000 28,950,000

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

Transfer

Fiscal YearEndReserveBalance

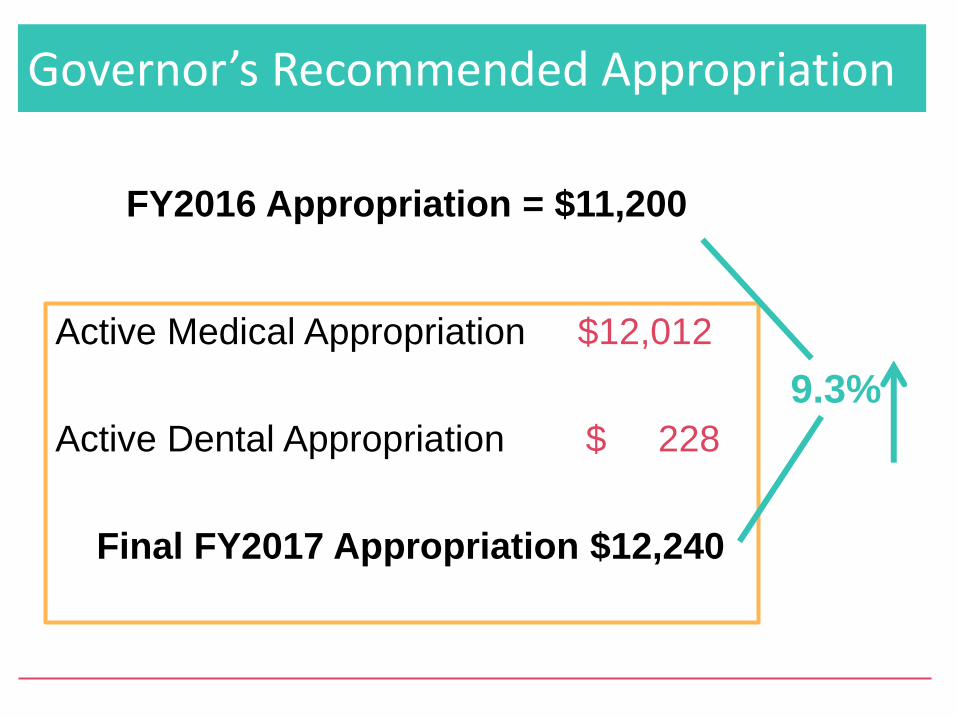

Governor’s Recommended Appropriation

FY2016 Appropriation = $11,200

Active Medical Appropriation $12,012

Active Dental Appropriation $ 228

Final FY2017 Appropriation $12,240

9.3%

Agenda

• Plan Structure

• Grandfathered Status

• OGI Funding / ACA Impacts

• Reserves

• Talking Points

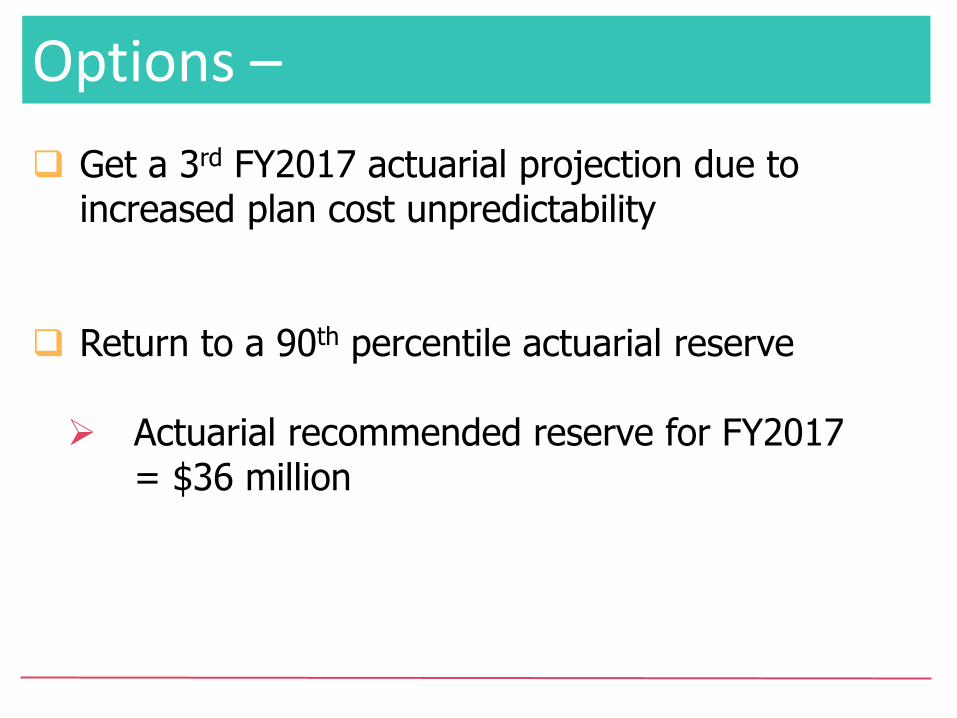

Options –

Get a 3rd FY2017 actuarial projection due to increased plan cost unpredictability

Return to a 90th percentile actuarial reserve Actuarial recommended reserve for FY2017

= $36 million

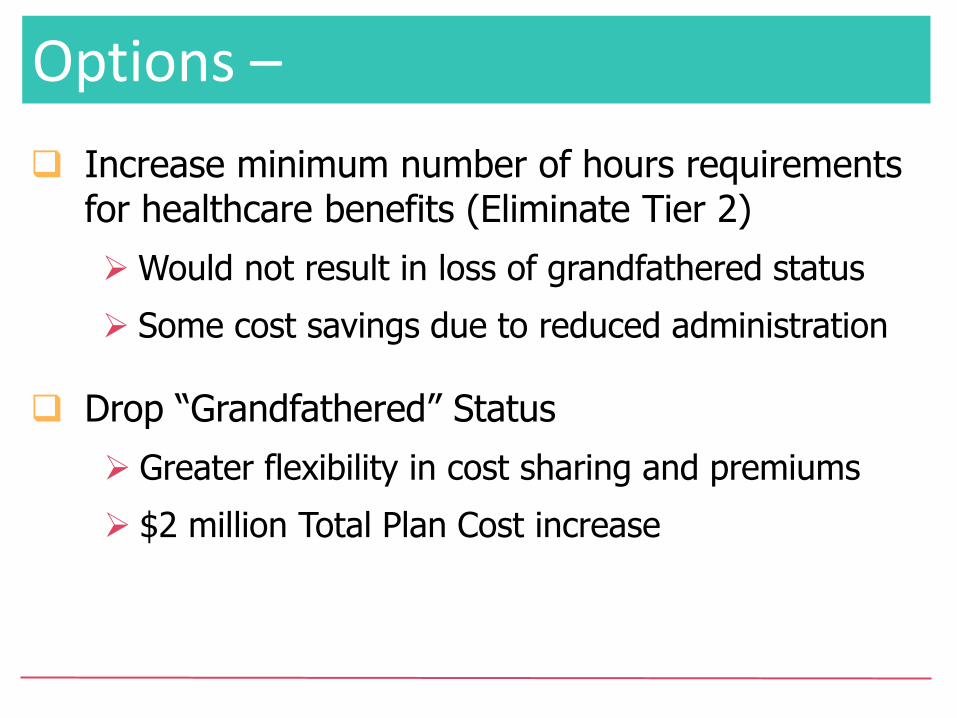

Options –

Increase minimum number of hours requirements for healthcare benefits (Eliminate Tier 2)

Would not result in loss of grandfathered status

Some cost savings due to reduced administration

Drop “Grandfathered” Status

Greater flexibility in cost sharing and premiums

$2 million Total Plan Cost increase

Alternatives – Self Funding Self-Insured Plans

Potential on-going cost savings

Avoids ACA fees

Could maintain “grandfathered” status

Complex administration

Requires a trust, re-insurance and HIPAA compliance

Start-up and operational costs

Premium tax savings; Department of Insurance budget considerations

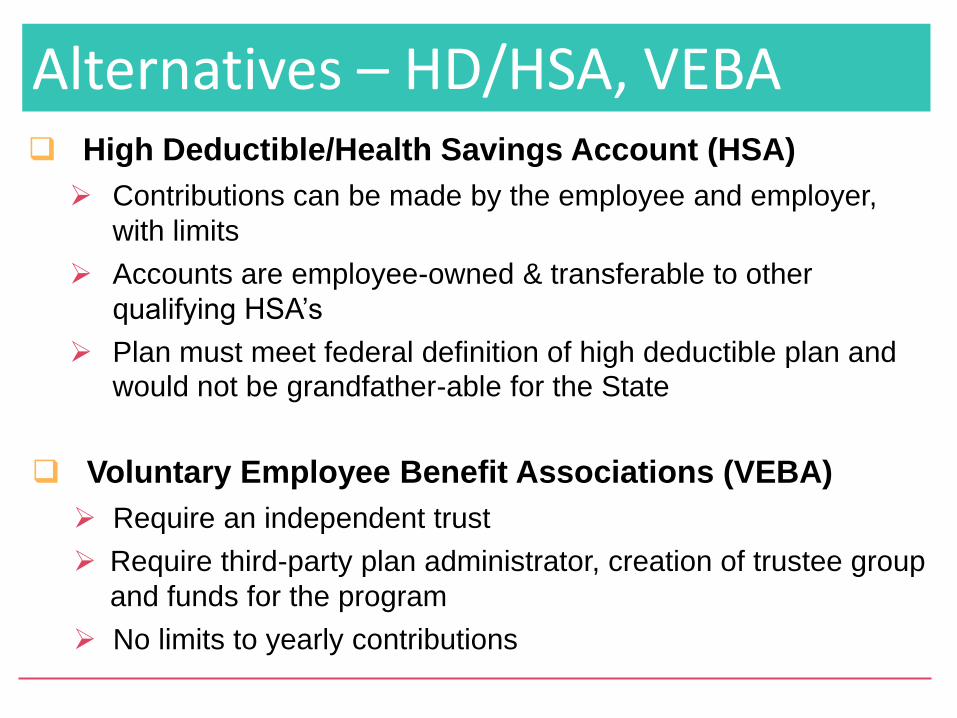

Alternatives – HD/HSA, VEBA High Deductible/Health Savings Account (HSA)

Contributions can be made by the employee and employer,

with limits

Accounts are employee-owned & transferable to other

qualifying HSA’s

Plan must meet federal definition of high deductible plan and

would not be grandfather-able for the State

Voluntary Employee Benefit Associations (VEBA)

Require an independent trust

Require third-party plan administrator, creation of trustee group

and funds for the program

No limits to yearly contributions

Group Insurance Advisory Committee

Members:

Senator Fred Martin

Representative Phylis King

Director Robert L. Geddes

Dick Humiston, Retired Employee

Roxanne Lopez, Tax Commission, Active Employee

Andrea Patterson, Judiciary Representative

Website: http://ogi.idaho.gov/giac

Questions?

Office of Group Insurance

Phone Numbers (208) 332-1860 (in the Treasure Valley) (800) 531-0597 (outside the Treasure Valley) (208) 332-1888 (fax) Street Address 304 North 8th Street, Room 434 Boise, ID 83702 Email Address [email protected]