Embed Size (px)

Citation preview

1

1

Offerte Pubbliche Iniziali (IPOs)

Corso di Corporate e Investment Banking

prof. Giancarlo Giudici

2014 MIP – Giancarlo Giudici2

Contents

• Going public: requirements, costs and benefits

• Initial Public Offerings: phases and roles

• Aftermarket performance

• Case studies (Twitter)

• Meeting with representatives from Borsa Italiana spa and underwriters

2

2014 MIP – Giancarlo Giudici3

Going public

• An Exchange is a MARKET where financial securities and other assets (such as commodities) are TRADED. Its main characteristics are:

– Transparent (quotes of trades are published)

– Anonymous (only market supervisors know the identity of traders)

– Regulated (as to protect investors)

– Centralised (all bids are managed centrally)

• Technically, the only difference between a company listed on an Exchange and a company non-listed is that its shares may be easily and freely traded, while for the latter it is more difficult and costly

• Yet, the listing has a number of consequences in a company…

2014 MIP – Giancarlo Giudici4

Requirements

• The main requirements in order to access the Exchange are generallyrelated to:

– Size of the company (expected capitalization, value of revenues / totalassets)

– Age of the company / profitability

– Auditing of balance accounts (and frequency)

– Floating capital (in order to provide liquidity for trades)

– Appointment of intermediates (sponsor, advisor, …)

– Market making provisions

– Corporate governance provisions

– Acceptance of internal codes

– …

Many Exchanges are segmented in’ main’ markets and ‘second’ markets. The requirements are typically less tight for the latter.

3

2014 MIP – Giancarlo Giudici5

Benefits

• The benefits related to the listing are generally divided into:

– FINANCIAL benefits: lower risk perceived by investors (thus lower cost of capital), larger contractual power towards banks, access to finance marketsin order to collect capital

– OPERATING benefits: marketing lever, visibility on key markets, ‘certification’ effect

– ORGANIZATION benefits: better control of information, incentives for managers, monitoring by professional investors and blockholders such asfunds

– TAX benefits: when acknowledged by authorities

• The decision is not only ‘if to go public’… but also ‘where to go public’: domestic vs. foreign market, ‘main’ vs. ‘second’ market’

• The timing is also fundamental

2014 MIP – Giancarlo Giudici6

Costs

• Costs are generally related to:

– Listing fees charged by the Exchange

– Costs of requirements (board composition, auditing, …)

– Cost of the ‘investor relator’ office

– Fees charged by legal and financial consultants

– Sensitivity to market turmoil

– Competitors’ spill-over of disclosed information

• One of the major issues for listed companies, especially small companies, is to attract the attention of the market, not to become a ‘penny stock’

4

2014 MIP – Giancarlo Giudici7

Other considerations

• One of the main differences between a listed company and a privately-owned company is the ownership structure.

• Often, the entrepreneur is willing to keep the whole control on the shareholding structure, avoiding any ‘external’ interference

• Moreover, a listed company is under scrutiny every day (by the market and by public authorities), while a privately-owned company may keep a certain degree of opacity related to accounts and managing choices

• This may help to explain why several large companies (e.g. Cargill, Trafigura, IKEA, Bosch, Rolex, Deloitte, Ferrero, Barilla, …) are not willing to go public, at the moment

Note that (at least in Italy and many EU countries) the pre-IPO controlling shareholders retain the majority of voting stock even after the listing! (very few become ‘public companies’)

2014 MIP – Giancarlo Giudici8

Motivations

Source: Bancel and Mittoo (2009)

5

2014 MIP – Giancarlo Giudici9

The way to the listing

• A company may join the Stock Exchange in one of the following ways:

1. Being already listed in another Exchange (‘dual listing’)

Example: Allianz (listed in Milan on MTA International segment), Luxottica (already listed in NY from 1991 and then in Milan in 2000)

2. After a spin-off from a listed company (or a merge: ‘reverse takeover’)

Examples: Delclima (spin-off De Longhi) – FiatIndustrial (spin-off Fiat) – Buzzi/Unicem (rev. takeover) – Merck/ScheringPlough (rev. takeover)

3. After a request for admission with no public offering

Example: Cattolica Assicurazioni – Banca Antonveneta

4. After a public offering (‘Initial Public Offering’ IPO), that is necessary to build up the floating capital

This is the most interesting and challenging case.

It is a RISKY and COSTLY process, that not always is successful (seerecently SEA – Milan airports).

2014 MIP – Giancarlo Giudici10

IPO: process and phases

The IPO process is structured into several phases:

The strategic choice to start the process is taken together with:

- Legal advisors

- Tax advisors

- Financial advisors

Financial advisors may be selected after a ‘beauty contest’ amonginvestment banks.

Their role is very important, because they will be required to ‘underwrite’ the offering, guaranteeing that the IPO shares will be sold.

Selection of advisors

IPO prospectus

OfferingShare

allocationListing and aftermarket

6

2014 MIP – Giancarlo Giudici11

Hot issue markets

The flow of companies going public is cyclical.

It is typically related to:

- The market momentum (in ‘bullish’ periods, or ‘hot issue’ periods, companies obtain more generous valuation and investors are more willing to subscribe stock)

- Business trends (see the ‘dot.com’ bubble in 1999 and 2000, and the ‘social network’ mania in 2011 and 2012); in such occasions the market learns about the sector and information costs decrease

Source: Ritter et al. (2013)

2014 MIP – Giancarlo Giudici12

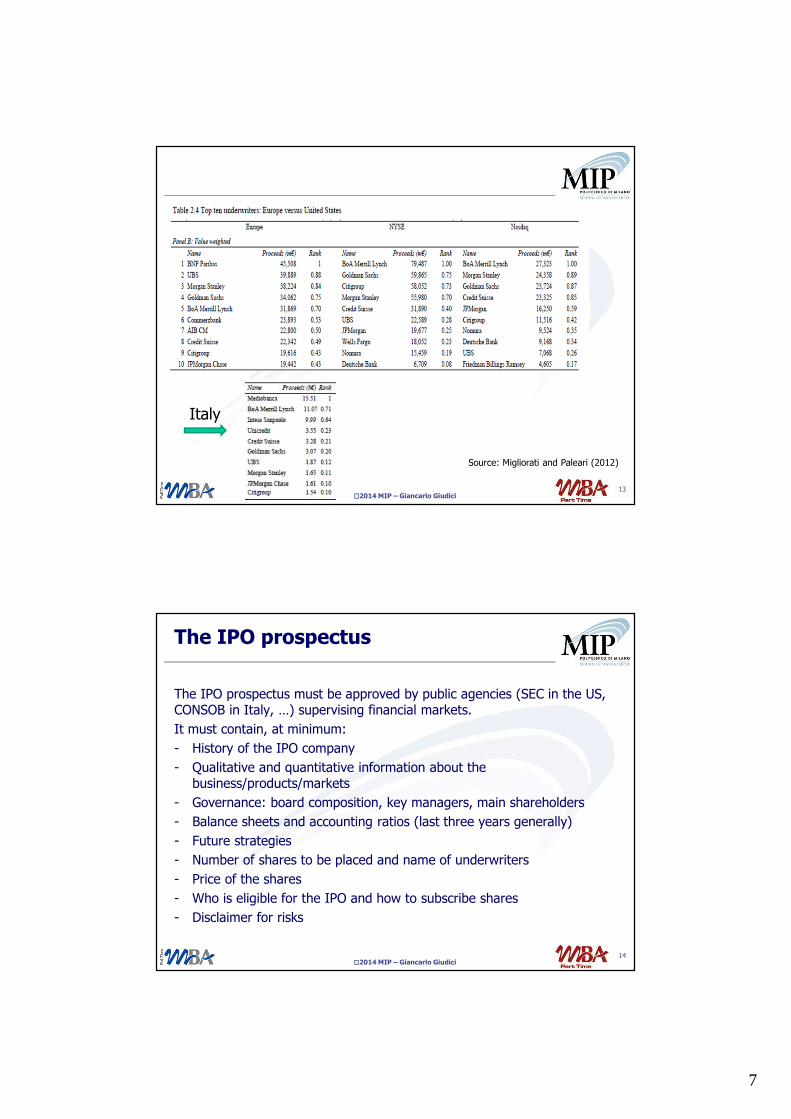

A business for bankers

Investment banks play an important (and profitable) role in IPOs.

GLOBAL COORDINATOR: supervises the whole process

UNDERWRITER: guarantees the placement of IPO shares, on a ‘best effort’ basis, or on a ‘stand-by commitment’ basis (may be one or more, if the offering is large and covers several countries)

MARKET MAKER: provides liquidity displaying bid and ask orders where lacking, in the aftermarket

In Italy they act also as:

- SPONSOR: they certify that the IPO company complies with listing requirements

- NOMAD (nominated advisor), for IPOs on the AIM Italy

The fee requested by investment banks in an IPO may easily account for 4% to 7% of the IPO proceeds.

7

2014 MIP – Giancarlo Giudici13

Source: Migliorati and Paleari (2012)

Italy

2014 MIP – Giancarlo Giudici14

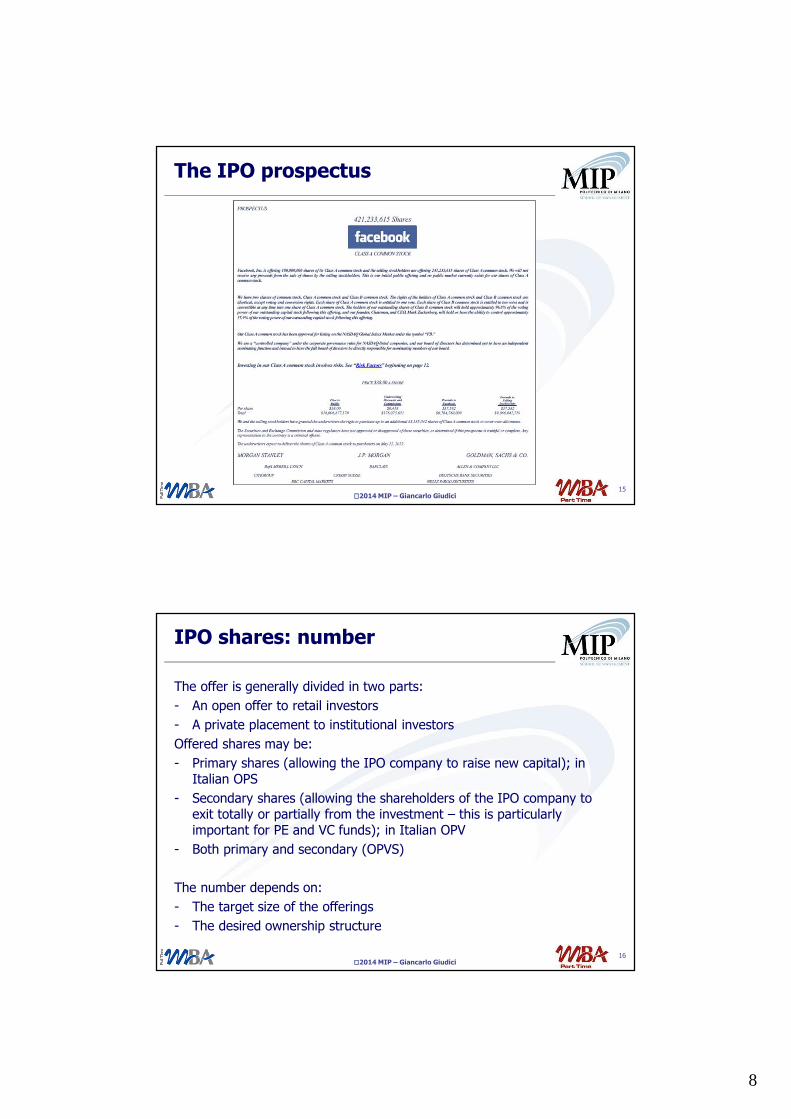

The IPO prospectus

The IPO prospectus must be approved by public agencies (SEC in the US, CONSOB in Italy, …) supervising financial markets.

It must contain, at minimum:

- History of the IPO company

- Qualitative and quantitative information about the business/products/markets

- Governance: board composition, key managers, main shareholders

- Balance sheets and accounting ratios (last three years generally)

- Future strategies

- Number of shares to be placed and name of underwriters

- Price of the shares

- Who is eligible for the IPO and how to subscribe shares

- Disclaimer for risks

8

2014 MIP – Giancarlo Giudici15

The IPO prospectus

2014 MIP – Giancarlo Giudici16

IPO shares: number

The offer is generally divided in two parts:

- An open offer to retail investors

- A private placement to institutional investors

Offered shares may be:

- Primary shares (allowing the IPO company to raise new capital); in Italian OPS

- Secondary shares (allowing the shareholders of the IPO company to exit totally or partially from the investment – this is particularlyimportant for PE and VC funds); in Italian OPV

- Both primary and secondary (OPVS)

The number depends on:

- The target size of the offerings

- The desired ownership structure

9

2014 MIP – Giancarlo Giudici17

IPO shares: pricing

The decision about the share offer price is crucial.

- Too low: dilution effect for existing shareholders / lower collection of capital

- Too high: risk of IPO failure

A first evaluation is carried out with traditional DCF methodologies.

A comparison with other listed similar companies is carried out (‘peer’ approach).

The prospectus generally details an indicative price range.

The final offer price is decided AFTER the offering, in order to take intoaccount:

- Late adjustments of the market

- Informal feedback from investors

In small IPOs the prospectus may report a fixed offer price.

2014 MIP – Giancarlo Giudici18

Example of peer approach

Prospectus price range: € 3.2 – € 4.3 8.4x – 10.2x EBITDA14.8x – 19.9x earnings

The IPO has been withdrawn for scarce demand!

10

2014 MIP – Giancarlo Giudici19

The ‘green shoe’ option

The company ‘Green Shoe’ in 1960 went public, allowing the underwriterto have the option to increase the IPO size.

Such option is now common in all IPO and is called ‘green shoe’ option.

It allows the underwriter to place more shares, in case of oversubscription.

Generally the option is related to 10%/15% of the IPO size.

The green shoe option may be exercised in 30 days after the listing.

This allows the underwriter to:

- Raise extra revenues from IPO commissions, related to the exercise of the green shoe option

- Increase the offer size, in case of strong demand

2014 MIP – Giancarlo Giudici20

Lock-up provisions

Another common features for IPOs is the ‘lock-up’ agreement.

In order to signal positive expectations about the IPO company value in the future, existing shareholders declare to refrain from selling additionalshares after the listing, for some months.

Otherways, they could have an incentive to rapidly sell their shares, if theyknow that the company is overvalued.

11

2014 MIP – Giancarlo Giudici21

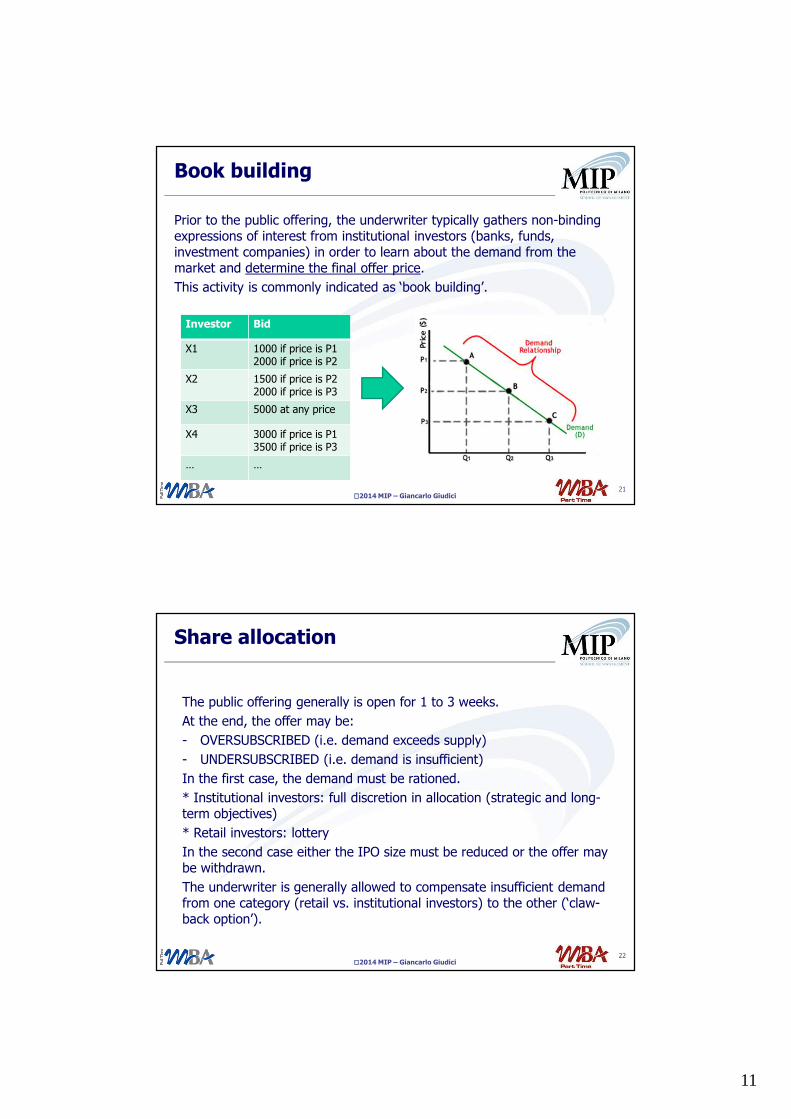

Book building

Prior to the public offering, the underwriter typically gathers non-bindingexpressions of interest from institutional investors (banks, funds, investment companies) in order to learn about the demand from the market and determine the final offer price.

This activity is commonly indicated as ‘book building’.

Investor Bid

X1 1000 if price is P12000 if price is P2

X2 1500 if price is P22000 if price is P3

X3 5000 at any price

X4 3000 if price is P13500 if price is P3

… …

2014 MIP – Giancarlo Giudici22

Share allocation

The public offering generally is open for 1 to 3 weeks.

At the end, the offer may be:

- OVERSUBSCRIBED (i.e. demand exceeds supply)

- UNDERSUBSCRIBED (i.e. demand is insufficient)

In the first case, the demand must be rationed.

* Institutional investors: full discretion in allocation (strategic and long-term objectives)

* Retail investors: lottery

In the second case either the IPO size must be reduced or the offer maybe withdrawn.

The underwriter is generally allowed to compensate insufficient demandfrom one category (retail vs. institutional investors) to the other (‘claw-back option’).

12

2014 MIP – Giancarlo Giudici23

The first day of listing

After the allotment of shares, trading may start.

The IPO share return of the first day of the listing is often positive. Thisphenomenon is called ‘underpricing’. In fact, it means that on average IPO shares are sold at a discount compared to the equilibrium market value.

Some examples: Yoox (Italy, 2010) = +8.9% Mutuionline (Italy, 2007) = +10,2% Tiscali (Italy, 1999) = +48% Linkedin (USA, 2012) = +109% Yahoo! (USA, 1996) = +154% MP3.com (USA, 1999) = +126%

Yet the initial underpricing is not always positive: FriendFinder (USA, 2011) = -22% Damiani (Italy, 2008) = -5.9% SARAS (Italy, 2006) = -11.8%

Commonly, in the short run after the listing underwriters engage in trading IPO shares on the market, in order to stabilize the price (and support it in case of negative returns). Investors selling IPO shares immediately afterthe listing are called ‘flippers’.

2014 MIP – Giancarlo Giudici24

Source: Jay Ritter

13

2014 MIP – Giancarlo Giudici25

Theories about IPO underpricing

There is a massive literature explaining IPO underpricing:

- Market fads and irrational behavior

- Underwriters want to ‘leave a good taste in investors’ mouth’

- Rationing effect: IPOs must be on average underpriced to stimulatedemand from uninformed investors (‘winner’s curse’)

- A costly signal to the market

- Compensation to professional investors for revealing demand duringbook building and participating in all IPOs

- Avoidance of possibile litigation with IPO subscribers

- Bribery and corruption

2014 MIP – Giancarlo Giudici26

Trading IPO shares

There is evidence that trading IPO shares is profitable for investmentbanks acting as underwriters. As well as they over-allot shares in the offering shares.

How is this ‘naked’ position (short selling) covered?

In case of positive returns, underwriters exercise the ‘green shoe’ option, this allowing to cover the overallotment and earn profits on the commissions.

In case of negative returns, underwriters buy shares in the open market, this allowing to cover the overallotment. They earn a capital gain (in sucha case they buy at lower prices compared to the IPO price).

It seems a win-win strategy!

14

2014 MIP – Giancarlo Giudici27

IPO performance in the long-run

Remarkably, IPO shares tend to underperform the market index return in the long run.

Source: Ritter (1991)

2014 MIP – Giancarlo Giudici28

Long run underperformance

Possible explanations:

- IPOs are more risky than the average market portfolio, and the probability to survive is lower

- ‘Window of opportunity’: poor operating performance after the listing; according to this theory IPO companies are taken public when the value of future growth opportunities is over

- IPO analysts’ overoptimism (may be opportunistic or not)