Embed Size (px)

Citation preview

““State of the Aviation IndustryState of the Aviation Industry””Presentation to the ACI Airport Economics & Finance10th – 11th February

London, United Kingdom

Laurie N. Price

Director of Aviation Strategy

Mott MacDonald Aviation

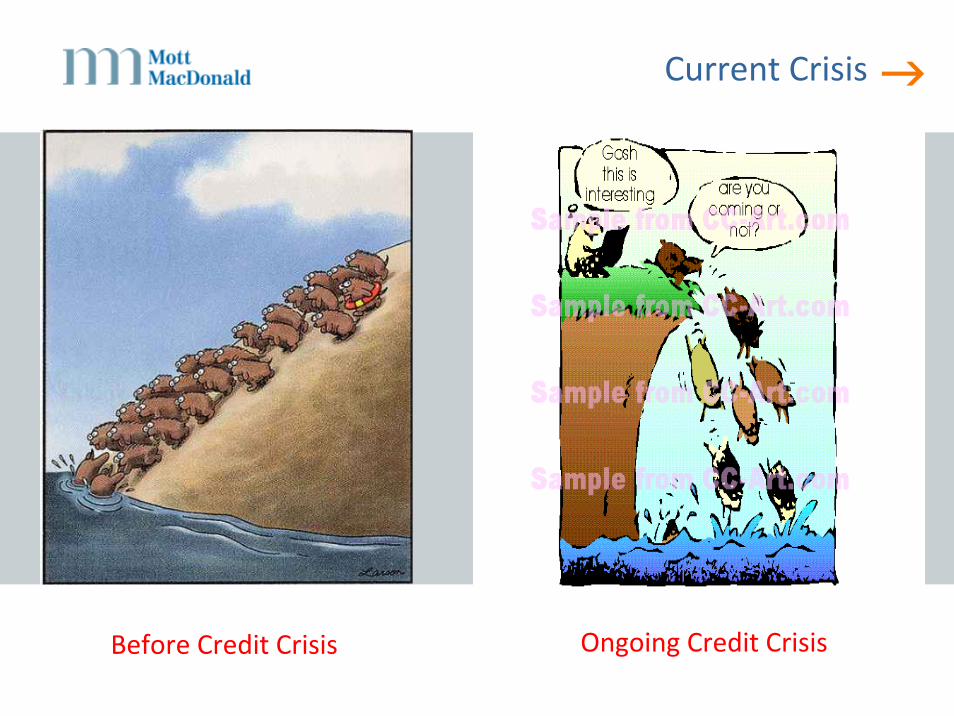

Current Crisis

Before Credit Crisis Ongoing Credit Crisis

Agenda

• Introduction to Mott MacDonald/Aviation Services

• Key Issues facing the industry

• Examples in the UK and Europe

• Demand

• Congestion

• Low Cost Carrier growth

• Environment

• Summary

• Conclusions

• Questions

Mott MacDonald Aviation Services

Policy &Development

Forecasting &Economics

ProjectManagement

Supervision &monitoring

TechnicalAdvisor

Transport &FacilitiesPlanning

Cost planningOperations &Performance

EngineeringDesign

Strategy

Environmental

Some Key Issues Facing theAir Transport Industry

• Economic Turbulence

• Fuel Prices

• Competition

• Security

• Environmental impact

• Taxation (APD vs ADT)

• Capacity – Runway/ATC

• Congestion

• Slots – Allocation/Availability

• Access to hub airports

• Pricing

• Demand – Maturity

• (De) Regulation

• EU / US Open Skies

• Market distortions

• Consolidation

• Financial performance

• Investment

• Returns

• GATT

• Labour and training

• Distribution – internet

• Frequency and capacity – aircraft size

Recent Developments

• 30 + airlines failed during 2008

• Fuel price fluctuation

• Market downturn

• Recession

• Industry losses mounting

• Calls for consolidation but regulatory issues

• Environmental militancy

• The Thai experience

• Taxation

Current Crisis

High Fuel Prices Have Caused Losses Forecast at USD5 billion for 2008

Net post‐tax profits, US$ billion

‐5.0

Globaltotal

Otherairlines

Asia Pacific airlines

US airlines European airlines

‐3.9 ‐0.1 ‐0.5‐0.5

Source: IATA

‐10%‐8%‐6%‐4%‐2%0%2%4%6%8%10%12%

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

% cha

nge ov

er year

Air freight FTKs

Passenger RPKsInternational RPKs and FTKs

Recession Reducing Business and Consumer Confidence has hit the Aviation Markets Hard

Source: IATA

Oil Prices

Source: RBS

Brent Oil Price, US$ per Barrel

0

20

40

60

80

100

120

140

Jan‐

03Ju

l‐03

Jan‐

04Ju

l‐04

Jan‐

05Ju

l‐05

Jan‐

06Ju

l‐06

Jan‐

07Ju

l‐07

Jan‐

08Ju

l‐08

Jan‐

09Ju

l‐09

Jan‐

10

Futures curve end August

Futures curve end NovemberSpot price

end November

High Level of Aircraft Grounding

‐40

20

80

140

200

260

2006

2007

Apr‐0

8

May

‐08

Jun‐

08

Jul‐0

8

Aug‐0

8

Sep‐

08

Oct‐0

8Aircraft p

er m

onth

Deliveries Retirements Parked (net)

Monthly Average

Source: Ascend

Source: SRS Analyser

Growth in planned scheduled ASKs

‐15

‐10

‐5

0

5

10

Feb‐

07Ap

r‐07

Jun‐

07Au

g‐07

Oct‐0

7De

c‐07

Feb‐

08Ap

r‐08

Jun‐

08Au

g‐08

Oct‐0

8De

c‐08

Feb‐

09

% cha

nge ov

er year

WithinAsia Pacific

Within US

Global capacity

Cut Backs in Capacity, Particularly in US

Passenger Markets Likely to Fall 3% in 2009

‐4

0

4

8

12

16

1971

1975

1979

1983

1987

1991

1995

1999

2003

200720

0920

11

% cha

nge ov

er year

0

1

2

3

4

5

6

7

8

% cha

nge ov

er year

Global passenger kilometres flown(left scale)

World GDP (right scale)

Source: EIU/IATA

CO2 Emissions From Aviation Will FallDue to Recession and Fleet Changes

200

300

400

500

600

700

1995 1997 1999 2001 2003 2005 2007 2009 2011

Billion

s tonn

ekilometres

450

500

550

600

650

700

750

800

850

900

Million tonn

esCO

2

CO2 emissions(right scale)

Traffic volume (left scale)

Worst ever 2‐year Revenue Outlook

Airline revenue growth, adjusted for inflation

‐15

‐10

‐5

0

5

10

15

20

1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

% cha

nge ov

er year

Source: EIU/IATA

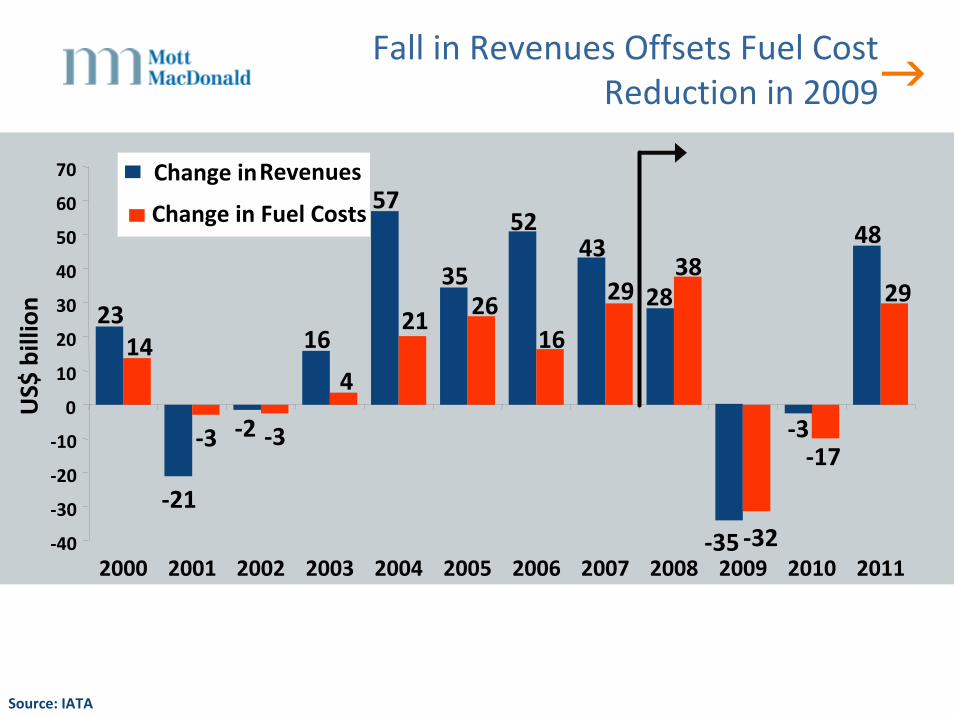

23

‐21

‐2

16

57

35

5243

28

‐35

‐3

48

144

21 2616

2938

29

‐17‐3 ‐3

‐32‐40

‐30

‐20

‐10

0

10

20

30

40

50

60

70

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

US$

billion

Change inRevenues

Change in Fuel Costs

Fall in Revenues Offsets Fuel Cost Reduction in 2009

Source: IATA

Losses Likely to Worsen in 2009 in All Regions, Except the US

Source: IATA

Net profit margins by region

‐5

‐4

‐3

‐2

‐1

0

1

2

3

4

2005 2006 2007 2008F 2009F

% of reven

ues

US

AsiaPacific

Europe

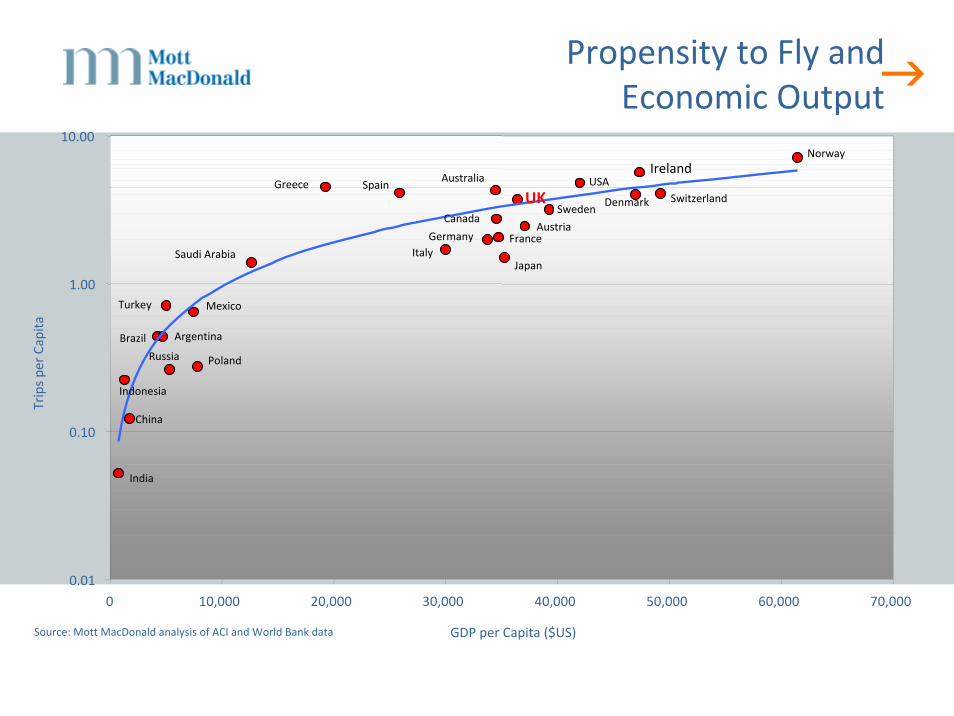

Propensity to Fly and Economic Output

0.01

0.10

1.00

10.00

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000

GDP per Capita ($US)

Trips pe

r Capita

NorwayIreland

USAGreece AustraliaSpain

SwitzerlandDenmarkUKSweden

CanadaAustria

FranceGermanyItaly

JapanSaudi Arabia

Turkey Mexico

ArgentinaBrazil

PolandRussia

Indonesia

China

India

Source: Mott MacDonald analysis of ACI and World Bank data

20‐year Forecast: Strong Long‐Term Growth

Source: Boeing current market outlook 2007

Terminal Passengers at UK Airports Annual Growth Rates

Source: CAA Airport Statistics , OPEC

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%19

73

1978

1983

1988

1993

1998

2003P

asse

nger

Ann

ual G

row

th R

ates

(%)

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

Cru

de O

il Pric

e An

nual

Gro

wth

Rat

es (%

)

1974 Fuel Crisis

1977 Bermuda II

1979 US Deregulation

1982 Falklands War

1983 Europe Deregulation

1985/86 Libya/Chernobyl

1991 Gulf War

1995 Introduction of Low‐Cost Airlines

1981 Fuel Crisis + Recession

1988 Lockerbie

2001 Terrorist Attacks

2003 Iraq War / SARS

Note: Historic oil price shown in US$ and the exchange rates between USD and GBP were not considered

Capacity and Demand Forecast in SE England(Assuming no new Runways)

The unmet demand by 2035/36 is in the region of 1.2 million slots– almost as big as the capacity of the 5 London airports today.

Source: CAA, Future of Air Transport White Paper and supporting documents

LHR LHR LHR LHR LHR

LGW LGW LGW LGW LGW

STN STN STN STN STN

LTN LTN LTN LTN LTN

LCY LCY LCY LCY LCY

Unmet

Unmet

Unmet

Unmet

0

400

800

1200

1600

2000

2400

2800

2007/08 2014/15 2021/22 2028/29 2035/36

Year

Air Transport Movem

ents Capacity

Demand for Slots

Capacity and Demand Forecast in SE England(Assuming new Runways at LHR, STN and LGW)

Even with new runways at Heathrow, Stansted and Gatwick,there is unmet demand of 540,000 slots by 2035/36.

LHR LHRLHR LHR LHR

LGW LGW

LGW

LGW LGWSTN STN

STN

STN STN

LTN LTN

LTN

LTN LTN

LCY LCY

LCY

LCY LCYUnmet

Unmet

Unmet

0

400

800

1200

1600

2000

2400

2800

2007/08 2014/15 2021/22 2028/29 2035/36

Year

Air Transport M

ovem

ents Capacity

Demand for Slots

Source: CAA, Future of Air Transport White Paper and supporting documents

Change in the Market Impacts Infrastructure Requirements

Regional airline growth

– Smaller aircraft

– Lower Pax per ATM

– More ATMs

Low cost carriers

– Increased utilisation

– Lower costs

– More slot demand

2. Each new LCC based aircraft requires up to 2500 slots

EU Low Cost Market Share

Airport Congestion in Europe

• EC Study found:

– Air traffic forecast to grow by 2.3 times between 2003 and 2025

– More than 60 EC airports will be congested by 2025

– Top 20 saturated for 10 hours a day

– Planned capacity increases will notmeet forecast demand

• Situation in the UK is already critical in the South East of England

Aviation Environment

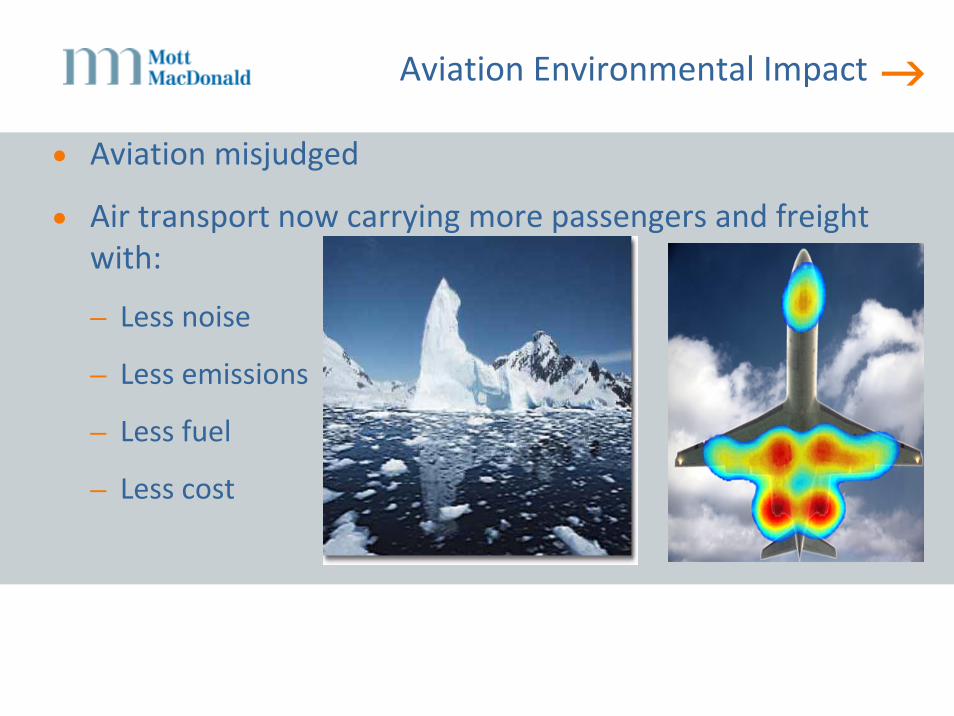

Aviation Environmental Impact

• Aviation misjudged

• Air transport now carrying more passengers and freight with:

– Less noise

– Less emissions

– Less fuel

– Less cost

Air Travel Increasingly Fuel Efficient

Source: Airbus Global Market Forecast 2006‐2025

0.0

5.0

10.0

15.0

20.0

25.0

(1) E

nerg

y Ind

(2) R

d Tra

ns(3

) Oth

ener

gy(4

) Con

sum

er fu

el(5

) Man

ufac

t(6

) Indu

stry

(7) B

io m

ass

(8) M

arine

Tra

ns

(9) A

viatio

n

%

26%

2%

18%

EU CO2 Emissions Aviation Just 2%!!!

Source: European Environment Agency

Noise Improvements

Source: Boeing

Summary

• Demand will return

• Increasing segmentation

• Increasing consolidation

• Increasing congestion

• Regulators not keeping pace

• Poor record in promoting aviation positive record on environmental impact

• Infrastructure investment remains key – runway, ATM, surface access

Any Questions?

Thank you

www.mottmac.com