Embed Size (px)

Citation preview

© OECD/IEA 2010

© OECD/IEA 2010

© OECD/IEA 2010

Plus ça change…An Outlook Similar, but Different, to 2009’s

Focus remains on market fundamentals, acknowledging that macro-economic & financial expectations have also played a role in 2008-2010

Starting points – price expectations are higher, while both demand and supply baselines have been raised

Economic recovery is underway, but uncertainties on the pace of that recovery keep the demand scenario approach in place.

Non-OECD remains the driver of demand growth, bringing the issues of data transparency and end-user price subsidies into sharper focus

Supply-side concerns are less intense than they were for MTOMR 2009

Both mature field decline and progress on new projects have benefited from higher spend and lower costs

But are costs and lead times about to be stretched once more?

OECD refining still a difficult business, and more rationalisation to come

Market balances look easier than in 2009, but much depends on sustaining investment & progress in embedding efficiency gains

© OECD/IEA 2010

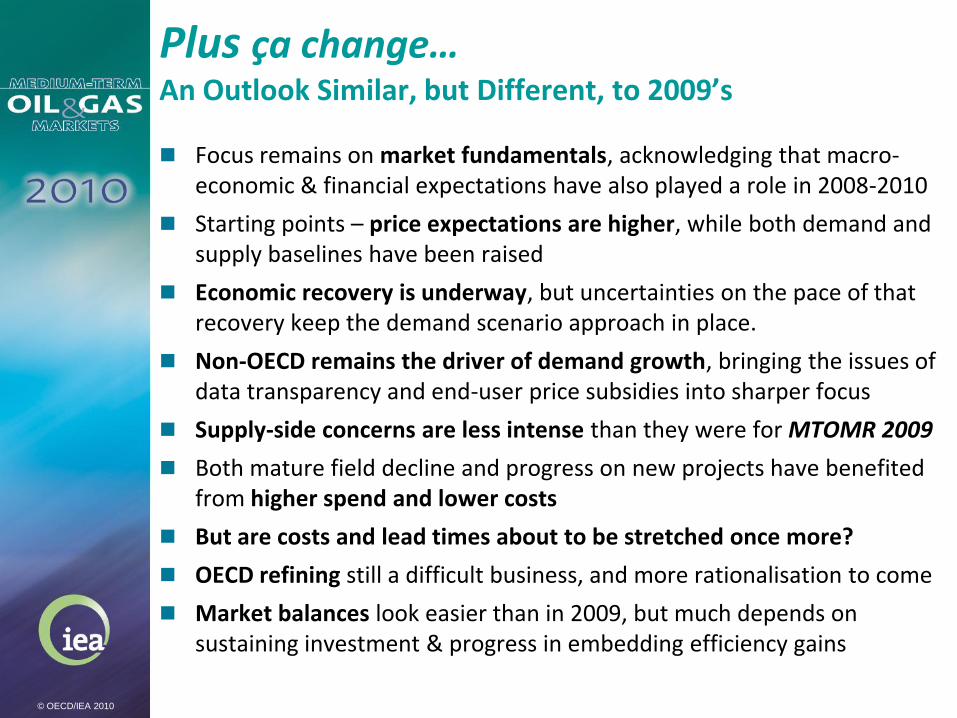

Oil Market Backdrop: Relative Stability Returns

Prices trend higher, but within $65-$85/bbl range since last June’s report

Backdrop of relative stability, unlike the volatile swings preceding last year’s report ($150/bbl in July 2008, $35/bbl in Feb 2009)

Comfortable OECD fundamentals & OPEC spare capacity countered by strong non-OECD demand growth, expectations for global economic recovery & ebb and flow in international financial markets

Balance of risks looking forward? Arguably, downside demand risks are countered by upside risk of supply curtailment & delay (though the supply outlook is now higher than last year)

NYMEX WTI vs S&P 500

30

40

50

60

70

80

90

Jan 09Apr 09Jul 09 Oct 09Jan 10Apr 10

US$/bbl

600

700

800

900

1000

1100

1200

1300Index

NYMEX WTI S&P 500 (RHS)

Source: P latts

Crude Futures

Front Month Close

30

50

70

90

110

130

150

Jan 04 Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10

$/bbl

NYMEX WTI ICE Brent

Source: P latts

© OECD/IEA 2010

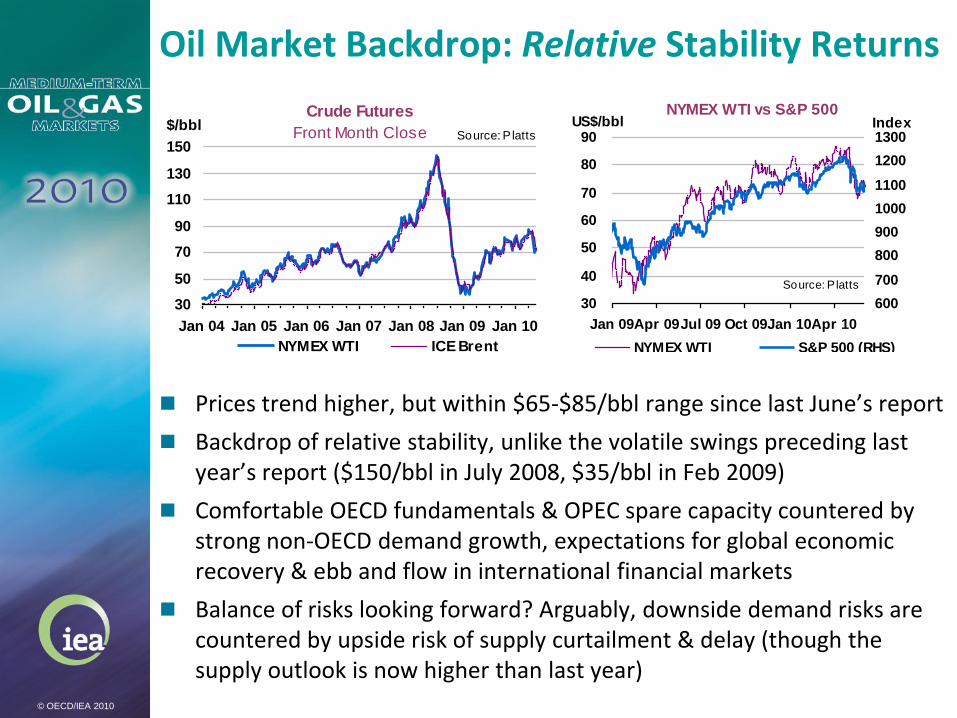

Key Assumptions for the 2015 Outlook

Price based on the futures strip, averaging $85/bbl for later years

In real terms, $76/bbl on average for the outlook period

Economic uncertainty, albeit with global recovery now entrenched, sees 2 GDP cases retained

This year we sensitise the pace of oil intensity reduction to GDP growth

Lower GDP could weaken reductions in oil intensity to 2% annually versus 3% in base case

97.19

57.54

76.5679.41 81.20 82.89 84.15 85.63

47.33

54.6259.81

63.41 65.33 67.21 68.5856.34

71.5075.06

77.17 78.69 80.4281.82

40

50

60

70

80

90

100

110

2008 2009 2010 2011 2012 2013 2014 2015

$/bbl'IEA Average Import Price'

Assumption (nominal)

Apr 2010 Apr 2009 Nov 2009

Global GDP: Base vs. Lower Case

(1)

-

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014 2015

% Chg

Low GDP Base GDP

Global Oil Intensity (2007 = 100)

80

85

90

95

100

2007 2008 2009 2010 2011 2012 2013 2014 2015

Base Case Lower Case

© OECD/IEA 2010

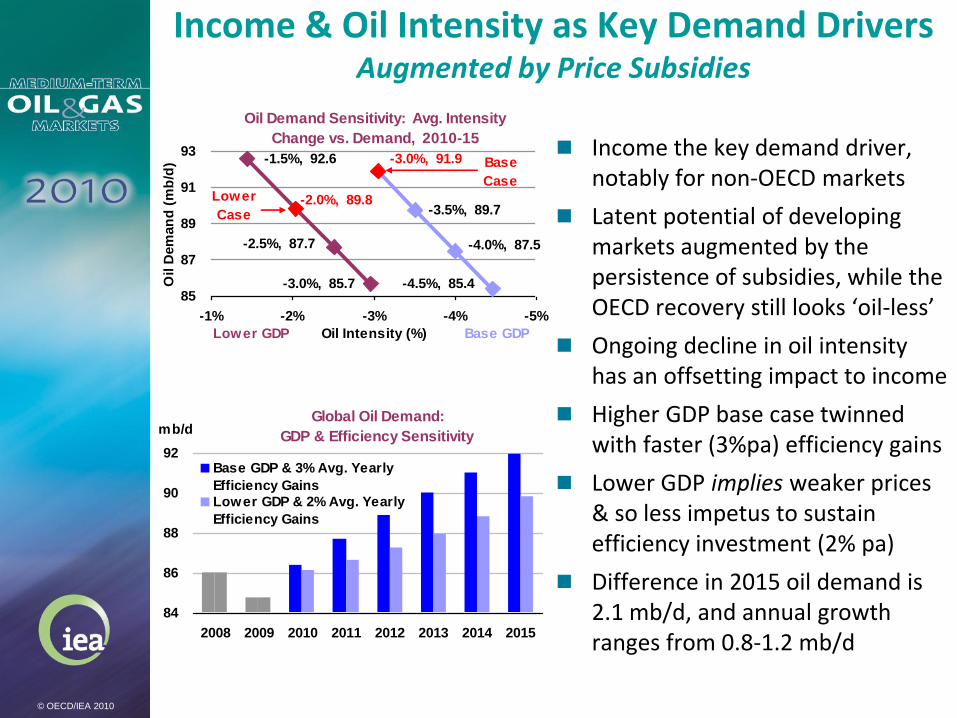

Income & Oil Intensity as Key Demand DriversAugmented by Price Subsidies

Income the key demand driver, notably for non-OECD markets

Latent potential of developing markets augmented by the persistence of subsidies, while the OECD recovery still looks ‘oil-less’

Ongoing decline in oil intensity has an offsetting impact to income

Higher GDP base case twinned with faster (3%pa) efficiency gains

Lower GDP implies weaker prices & so less impetus to sustain efficiency investment (2% pa)

Difference in 2015 oil demand is 2.1 mb/d, and annual growth ranges from 0.8-1.2 mb/d

Oil Demand Sensitivity: Avg. Intensity

Change vs. Demand, 2010-15

-3.5%, 89.7

-4.0%, 87.5

-4.5%, 85.4

-2.5%, 87.7

-3.0%, 85.7

-3.0%, 91.9 -1.5%, 92.6

-2.0%, 89.8

85

87

89

91

93

-5%-4%-3%-2%-1%

Oil Intensity (%)

Oil D

em

an

d (

mb

/d) Base

CaseLower

Case

Lower GDP Base GDP

Global Oil Demand:

GDP & Efficiency Sensitivity

84

86

88

90

92

2008 2009 2010 2011 2012 2013 2014 2015

mb/d

Base GDP & 3% Avg. Yearly

Efficiency Gains

Lower GDP & 2% Avg. Yearly

Efficiency Gains

© OECD/IEA 2010

Average Global Oil Demand Growth 1997-2003/2003-2009/2009-2015 Average Global Oil Demand Growth 2000-2005/2005-2010/2010-2015thousand barrels per day thousand barrels per day

(mb/d)

1997-2003 1.01 1.3%

2003-2009 0.82 1.0%

2009-2015 1.19 1.4%

Avg Global Demand Growth

51

-154-92

934 -1

207 199

15

308

-213

-58

134

279 307

5283 109

North America

Latin America Africa

Middle East

Europe FSU

442

616 634

Asia

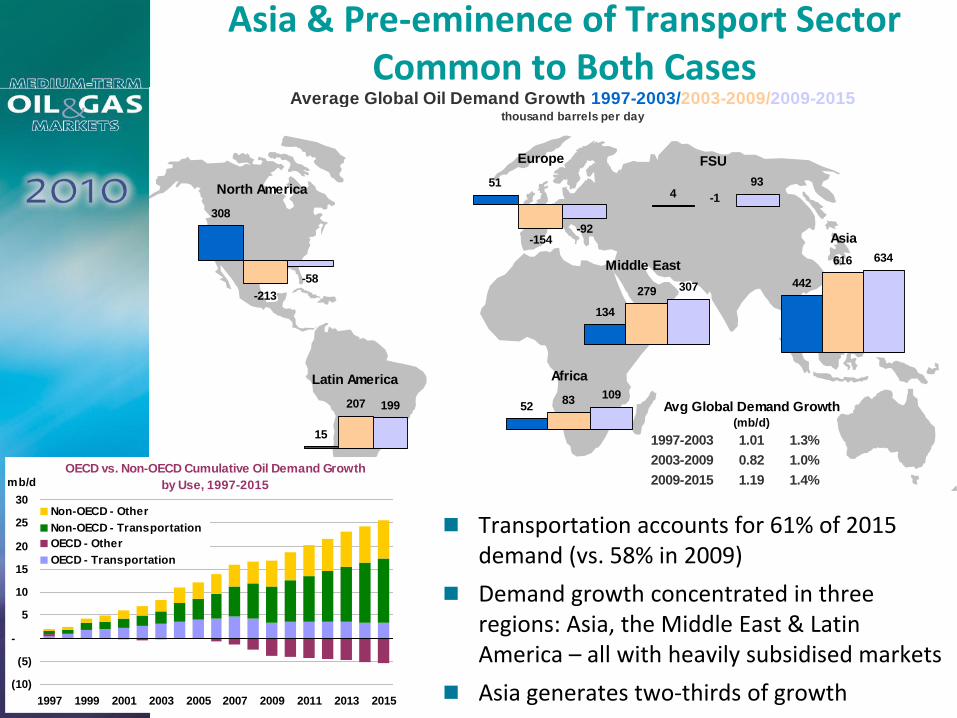

Asia & Pre-eminence of Transport Sector Common to Both Cases

Transportation accounts for 61% of 2015 demand (vs. 58% in 2009)

Demand growth concentrated in three regions: Asia, the Middle East & Latin America – all with heavily subsidised markets

Asia generates two-thirds of growth

OECD vs. Non-OECD Cumulative Oil Demand Growth

by Use, 1997-2015

(10)

(5)

-

5

10

15

20

25

30

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

mb/d

Non-OECD - Other

Non-OECD - Transportation

OECD - Other

OECD - Transportation

© OECD/IEA 2010

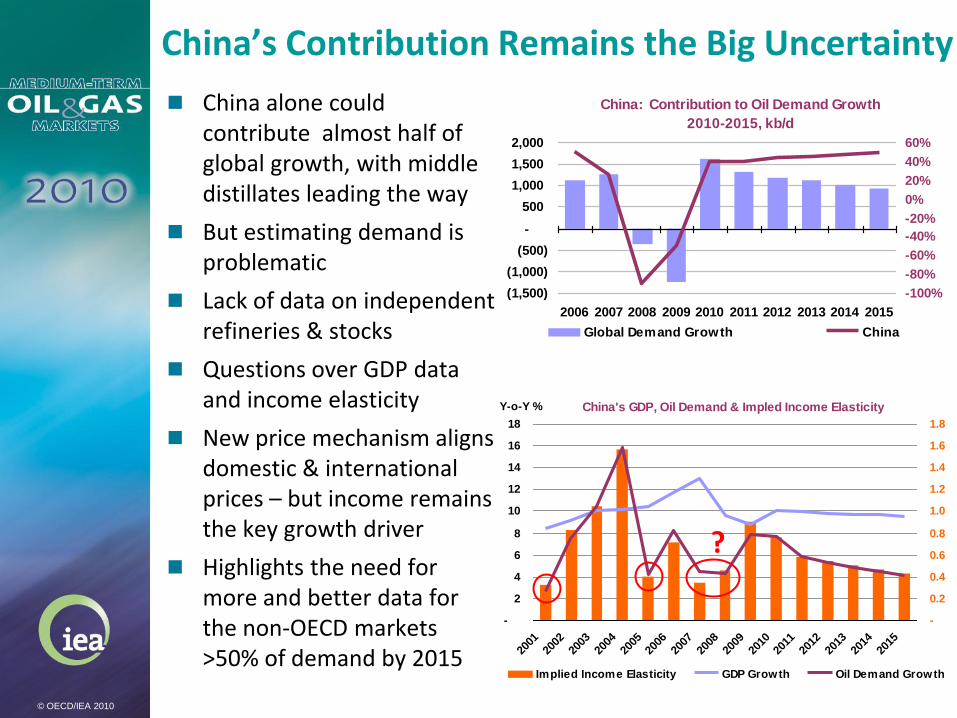

China’s Contribution Remains the Big Uncertainty

China alone could contribute almost half of global growth, with middle distillates leading the way

But estimating demand is problematic

Lack of data on independent refineries & stocks

Questions over GDP data and income elasticity

New price mechanism aligns domestic & international prices – but income remains the key growth driver

Highlights the need for more and better data for the non-OECD markets >50% of demand by 2015

China: Contribution to Oil Demand Growth

2010-2015, kb/d

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

Global Demand Growth China

China's GDP, Oil Demand & Impled Income Elasticity

-

2

4

6

8

10

12

14

16

18

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Y-o-Y %

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Implied Income Elasticity GDP Growth Oil Demand Growth

?

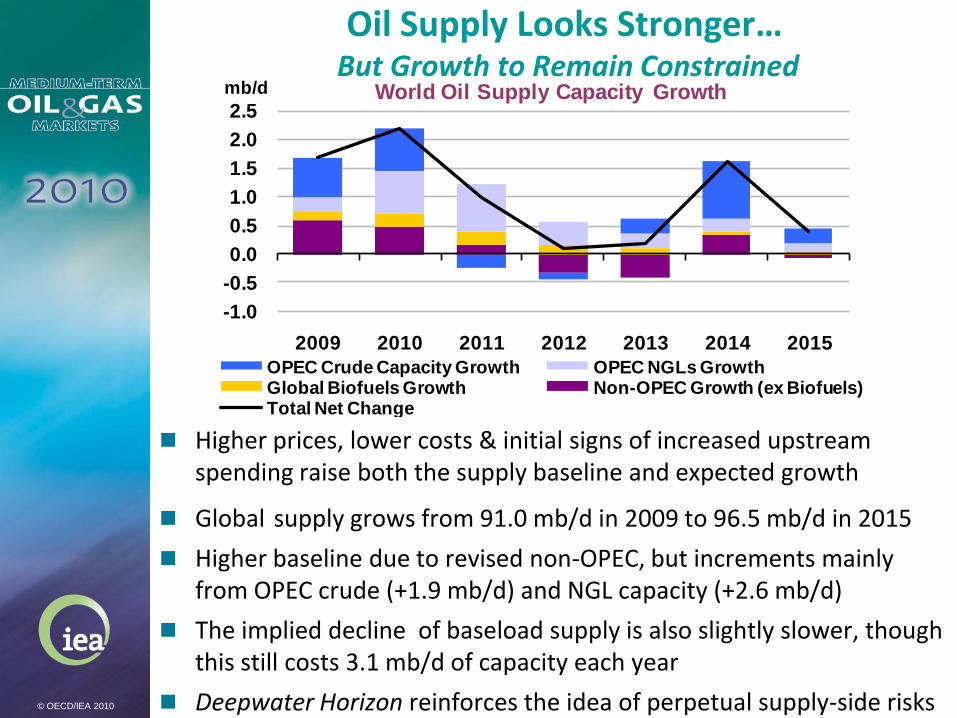

Oil Supply Looks Stronger…But Growth to Remain Constrained

Higher prices, lower costs & initial signs of increased upstream spending raise both the supply baseline and expected growth

Global supply grows from 91.0 mb/d in 2009 to 96.5 mb/d in 2015

Higher baseline due to revised non-OPEC, but increments mainly from OPEC crude (+1.9 mb/d) and NGL capacity (+2.6 mb/d)

The implied decline of baseload supply is also slightly slower, though this still costs 3.1 mb/d of capacity each year

Deepwater Horizon reinforces the idea of perpetual supply-side risks

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2009 2010 2011 2012 2013 2014 2015

mb/d World Oil Supply Capacity Growth

OPEC Crude Capacity Growth OPEC NGLs GrowthGlobal Biofuels Growth Non-OPEC Growth (ex Biofuels)Total Net Change

© OECD/IEA 2010

-0.40

0.00

0.40

0.80

1.20

1.60

2.00

2009 2010 2011 2012 2013 2014 2015

mb/dExpected Incremental Change

in OPEC Capacity

Iran IraqSaudi Arabia UAEAngola OtherTotal OPEC -1.00 -0.50 0.00 0.50 1.00

Iran

Nigeria

Ecuador

Kuwait

Algeria

Qatar

Venezuela

Libya

UAE

Angola

S. Arabia

Iraq

mb/d

Incremental Change in Crude Production Capacity 2009-15

© OECD/IEA 2010

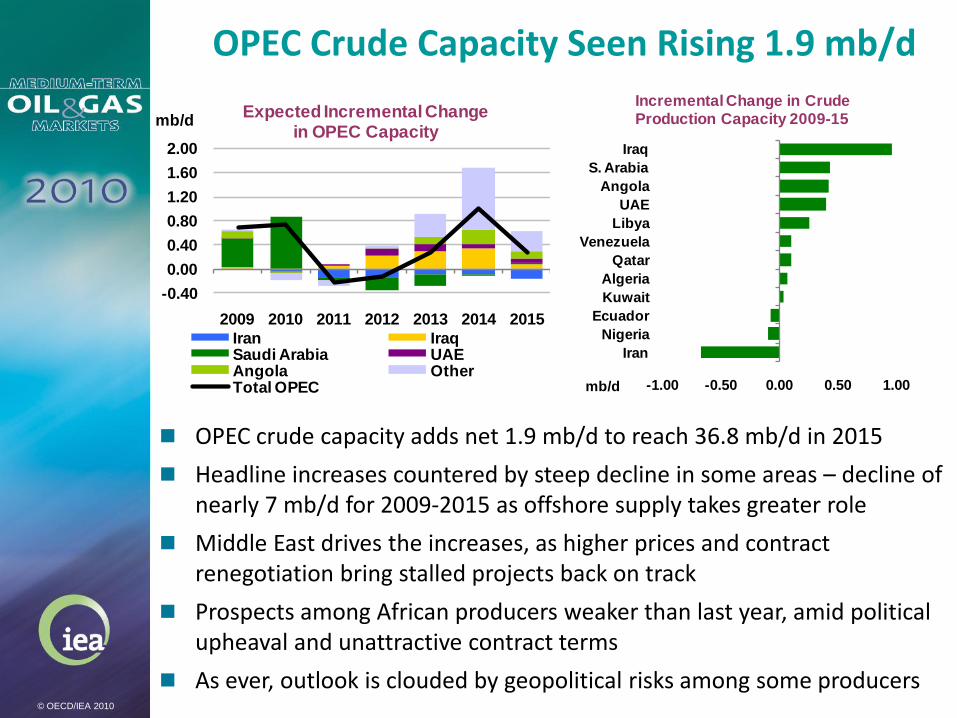

OPEC crude capacity adds net 1.9 mb/d to reach 36.8 mb/d in 2015

Headline increases countered by steep decline in some areas – decline of nearly 7 mb/d for 2009-2015 as offshore supply takes greater role

Middle East drives the increases, as higher prices and contract renegotiation bring stalled projects back on track

Prospects among African producers weaker than last year, amid political upheaval and unattractive contract terms

As ever, outlook is clouded by geopolitical risks among some producers

OPEC Crude Capacity Seen Rising 1.9 mb/d

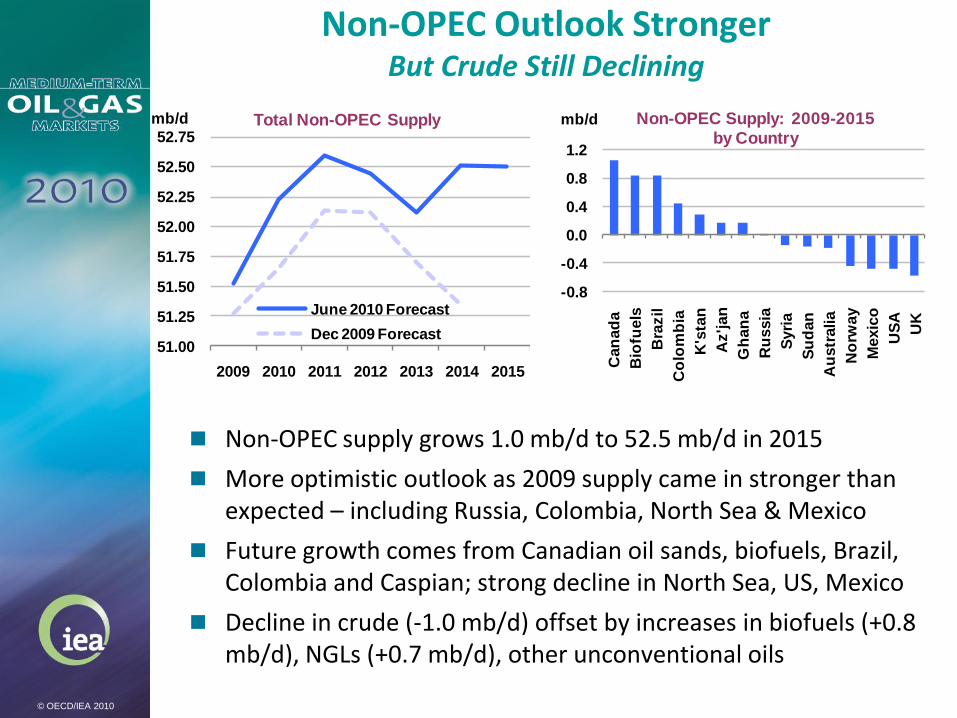

Non-OPEC Outlook StrongerBut Crude Still Declining

Non-OPEC supply grows 1.0 mb/d to 52.5 mb/d in 2015

More optimistic outlook as 2009 supply came in stronger than expected – including Russia, Colombia, North Sea & Mexico

Future growth comes from Canadian oil sands, biofuels, Brazil, Colombia and Caspian; strong decline in North Sea, US, Mexico

Decline in crude (-1.0 mb/d) offset by increases in biofuels (+0.8 mb/d), NGLs (+0.7 mb/d), other unconventional oils

51.00

51.25

51.50

51.75

52.00

52.25

52.50

52.75

2009 2010 2011 2012 2013 2014 2015

mb/d Total Non-OPEC Supply

June 2010 Forecast

Dec 2009 Forecast

-0.8

-0.4

0.0

0.4

0.8

1.2

Can

ad

a

Bio

fuels

Bra

zil

Co

lom

bia

K's

tan

Az'jan

Gh

an

a

Ru

ssia

Syri

a

Su

dan

Au

str

alia

No

rway

Mexic

o

US

A

UK

mb/d Non-OPEC Supply: 2009-2015 by Country

© OECD/IEA 2010

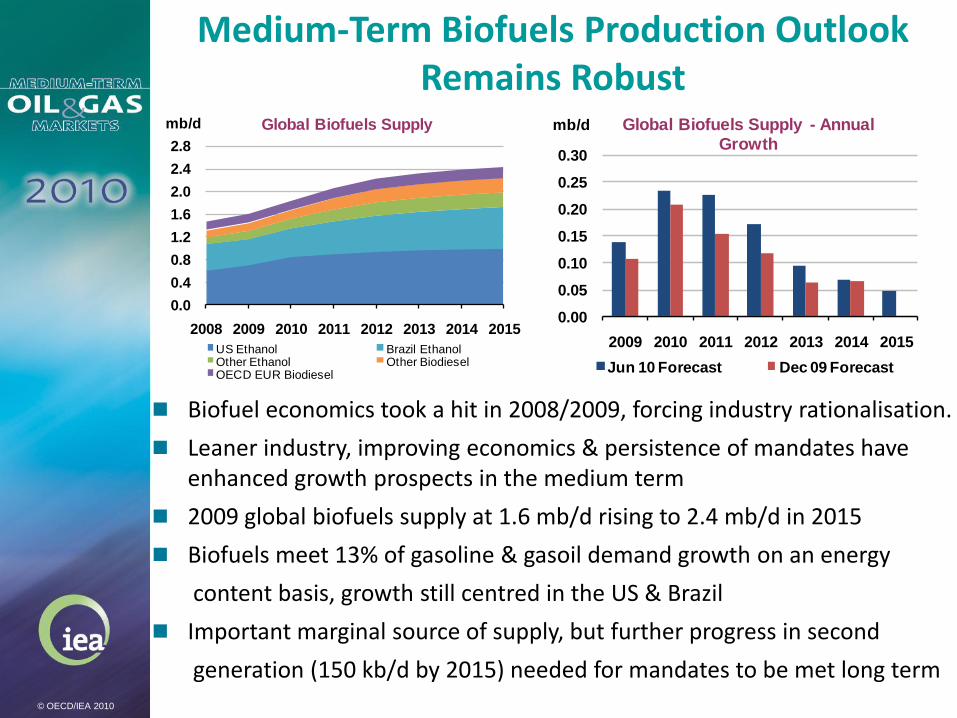

Medium-Term Biofuels Production Outlook Remains Robust

Biofuel economics took a hit in 2008/2009, forcing industry rationalisation.

Leaner industry, improving economics & persistence of mandates have enhanced growth prospects in the medium term

2009 global biofuels supply at 1.6 mb/d rising to 2.4 mb/d in 2015

Biofuels meet 13% of gasoline & gasoil demand growth on an energy

content basis, growth still centred in the US & Brazil

Important marginal source of supply, but further progress in second

generation (150 kb/d by 2015) needed for mandates to be met long term

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

2008 2009 2010 2011 2012 2013 2014 2015

mb/d Global Biofuels Supply

US Ethanol Brazil EthanolOther Ethanol Other BiodieselOECD EUR Biodiesel

0.00

0.05

0.10

0.15

0.20

0.25

0.30

2009 2010 2011 2012 2013 2014 2015

mb/d Global Biofuels Supply - Annual Growth

Jun 10 Forecast Dec 09 Forecast

© OECD/IEA 2010

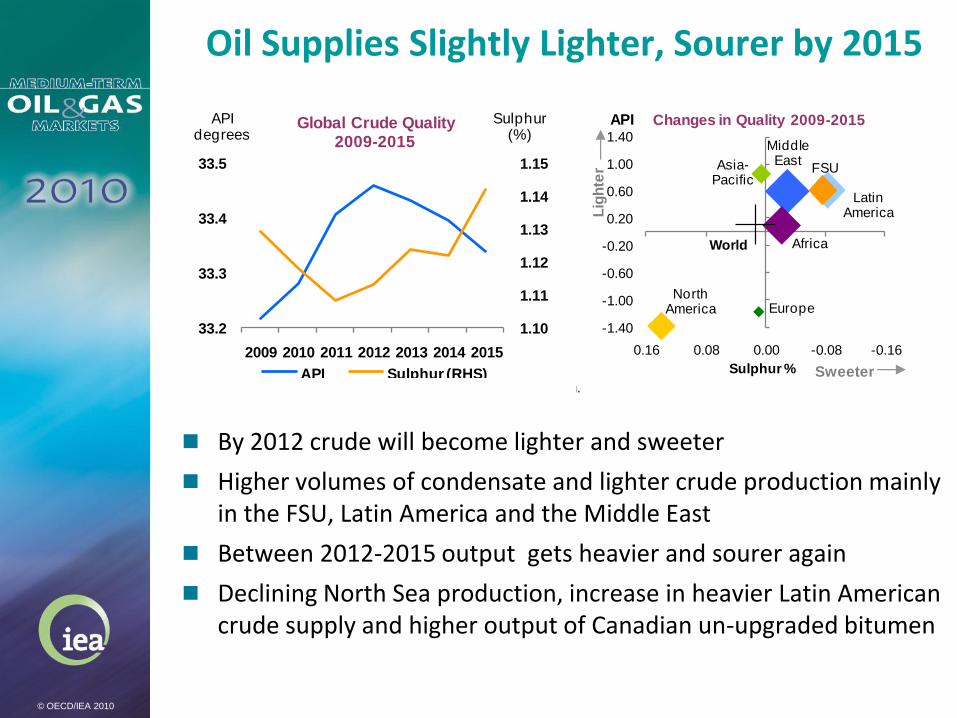

Oil Supplies Slightly Lighter, Sourer by 2015

By 2012 crude will become lighter and sweeter

Higher volumes of condensate and lighter crude production mainly in the FSU, Latin America and the Middle East

Between 2012-2015 output gets heavier and sourer again

Declining North Sea production, increase in heavier Latin American crude supply and higher output of Canadian un-upgraded bitumen

1.10

1.11

1.12

1.13

1.14

1.15

33.2

33.3

33.4

33.5

2009 2010 2011 2012 2013 2014 2015

Sulphur (%)

API degrees

Global Crude Quality2009-2015

API Sulphur (RHS)

Middle East

Africa

Latin America

FSU

North America Europe

Asia-Pacific

World

-1.40

-1.00

-0.60

-0.20

0.20

0.60

1.00

1.40

-0.16-0.080.000.080.16

API

Sulphur %

Changes in Quality 2009-2015

Sweeter

Lig

hte

r

FSU

Latin America

North America

Asia-Pacific

Middle East

Europe

Africa

World

25.0

30.0

35.0

40.0

0.00.51.01.52.0

API

Sulphur %

Current Gravity & Sulphur1

Sour Sweet

Lig

ht

He

av

y

1 Symbols proportionate in size to regional production.

© OECD/IEA 2010

© OECD/IEA 2010

0.0

2.5

5.0

7.5

10.0

2010 2011 2012 2013 2014 2015

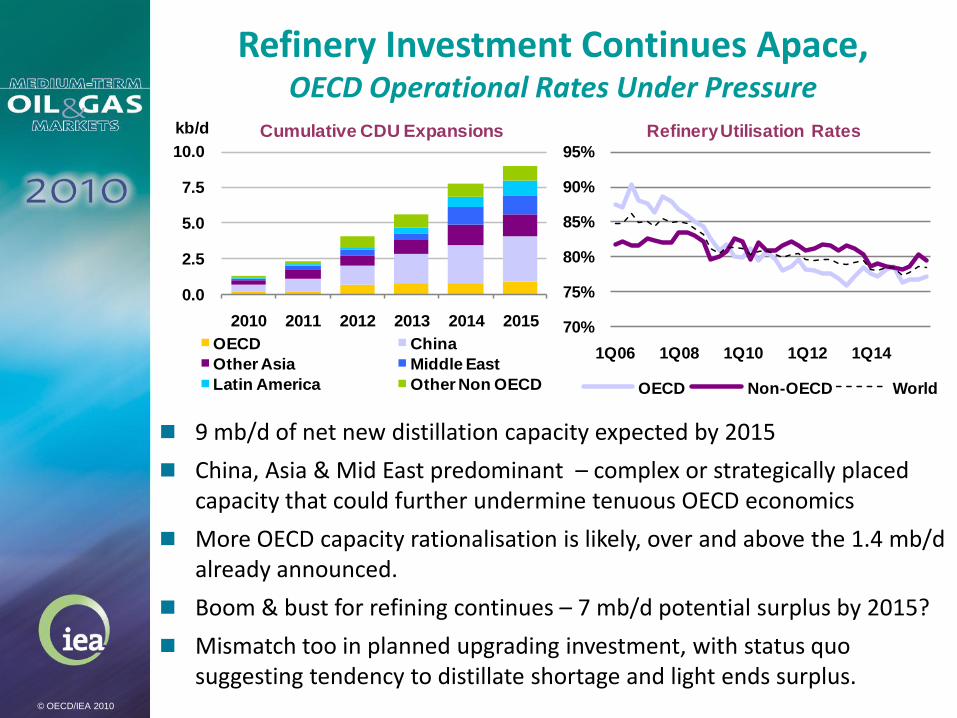

kb/d Cumulative CDU Expansions

OECD China

Other Asia Middle East

Latin America Other Non OECD

70%

75%

80%

85%

90%

95%

1Q06 1Q08 1Q10 1Q12 1Q14

Refinery Utilisation Rates

OECD Non-OECD World

Refinery Investment Continues Apace,OECD Operational Rates Under Pressure

9 mb/d of net new distillation capacity expected by 2015

China, Asia & Mid East predominant – complex or strategically placed capacity that could further undermine tenuous OECD economics

More OECD capacity rationalisation is likely, over and above the 1.4 mb/d already announced.

Boom & bust for refining continues – 7 mb/d potential surplus by 2015?

Mismatch too in planned upgrading investment, with status quo suggesting tendency to distillate shortage and light ends surplus.

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

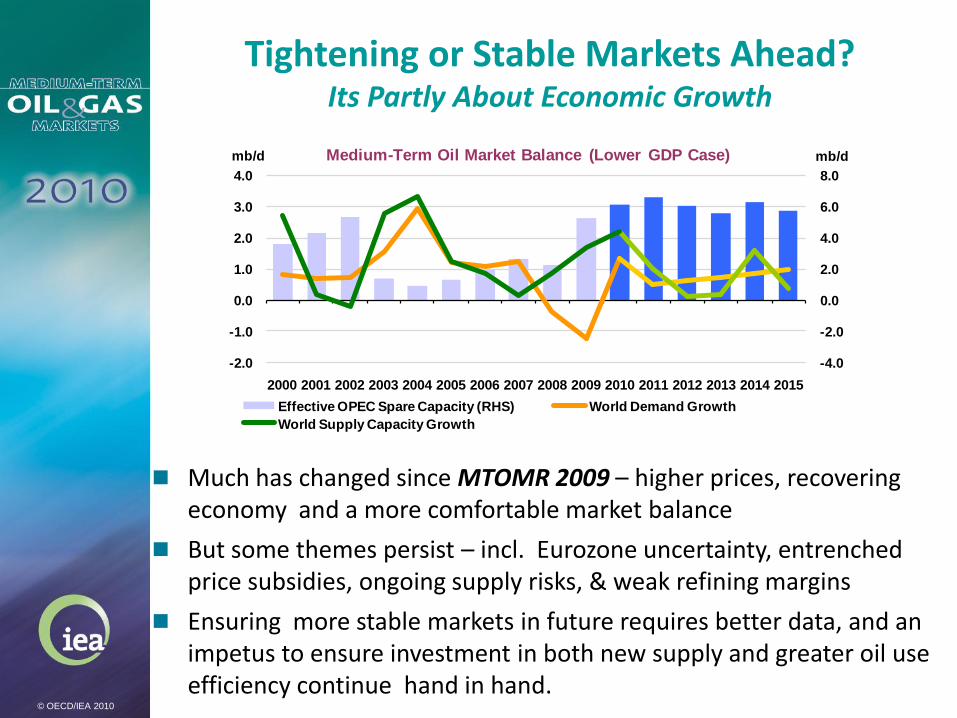

mb/dmb/d Medium-Term Oil Market Balance (Base Case)

Effective OPEC Spare Capacity (RHS) World Demand Growth

World Supply Capacity Growth

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

mb/dmb/d Medium-Term Oil Market Balance (Lower GDP Case)

Effective OPEC Spare Capacity (RHS) World Demand Growth

World Supply Capacity Growth

Tightening or Stable Markets Ahead?Its Partly About Economic Growth

© OECD/IEA 2010

Much has changed since MTOMR 2009 – higher prices, recovering economy and a more comfortable market balance

But some themes persist – incl. Eurozone uncertainty, entrenched price subsidies, ongoing supply risks, & weak refining margins

Ensuring more stable markets in future requires better data, and an impetus to ensure investment in both new supply and greater oil use efficiency continue hand in hand.

© OECD/IEA 2010